External Costs of Agriculture Derived from Payments for Agri-Environment Measures: Framework and Application to Switzerland

Abstract

1. Introduction

2. Literature Review

3. Conceptual Framework

3.1. External Costs and Benefits

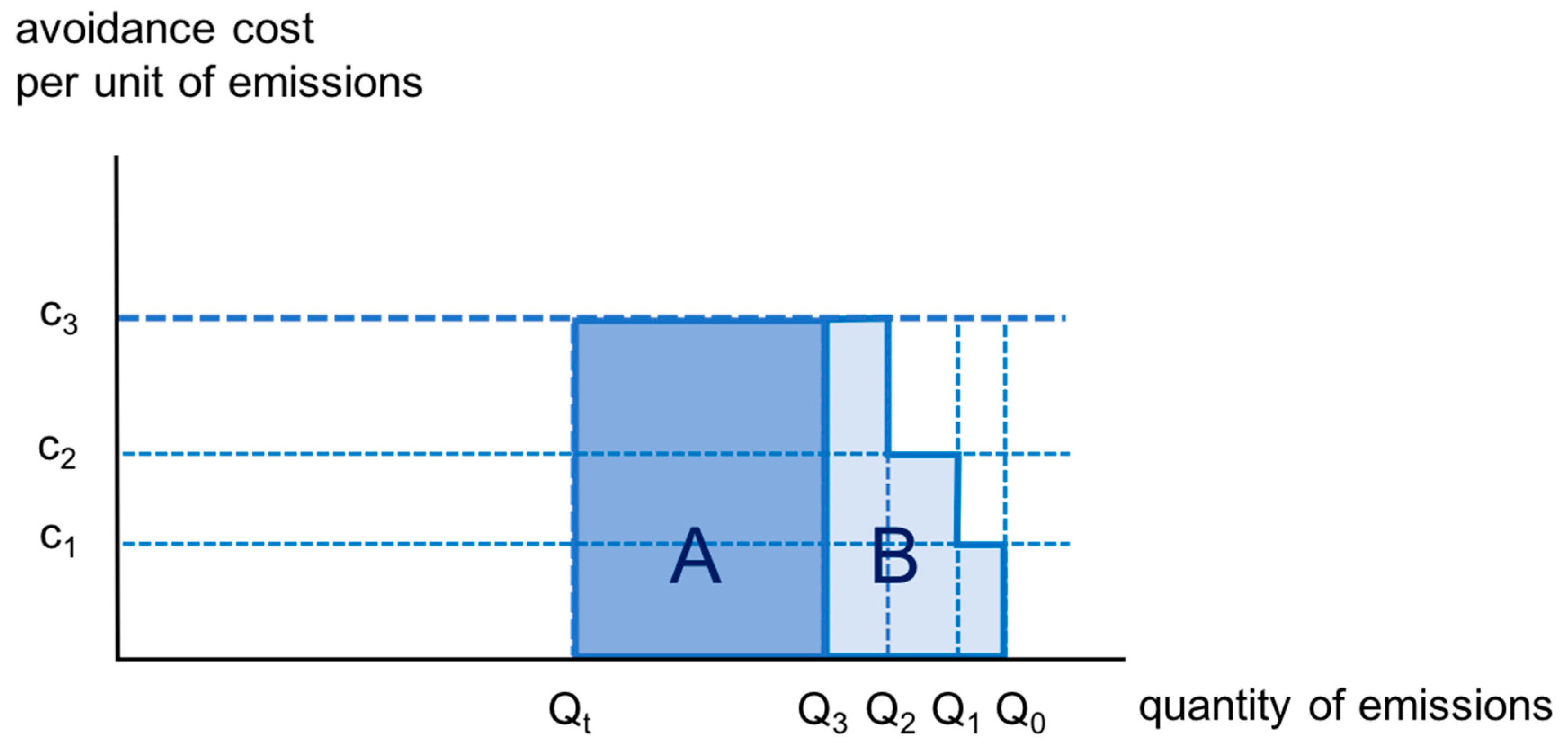

3.2. Avoidance Cost Approach

- (1)

- Identifying the agri-environmental measures that compensate farmers for avoiding or reducing greenhouse gas emissions and other relevant externalities;

- (2)

- Assessing the effectiveness of these measures;

- (3)

- Computing the costs per unit of avoided externality (c in Figure 1);

- (4)

- Identifying the quantities of harmful externalities;

- (5)

- (6)

- Computing the estimate of total external costs of agriculture by summing across all examined externalities.

3.3. Concept of Value

4. Methods

4.1. Identification of Avoidance Measures

4.2. Effectiveness of the Avoidance Measures

4.2.1. Direct Seeding

4.2.2. Nitrogen-Reduced Feeding of Pigs

4.2.3. Reduced-Emissions Application of Manure (3 Measures)

4.2.4. Extensive Livestock on Grassland

4.2.5. No application of Synthetic Herbicides (Measures for Different Crops)

4.2.6. No application of Synthetic Fungicides or Insecticides (Measures for Different Crops)

4.2.7. Biodiversity Measures Securing Minimal Habitat Requirements

4.2.8. Animal Welfare—Outdoor Space and Housing Conditions

4.2.9. CO2 Tax on Fuels

4.3. Calculation of Costs per Unit of Avoided Externality

4.4. Quantity of Harmful Emissions

4.5. Calculation External Costs for Each Externality

4.6. Calculation of Total External Costs

4.7. Data

5. Results

5.1. Avoidance Costs per Unit of Externality

5.2. Total External Costs

6. Discussion

7. Conclusions

Supplementary Materials

Funding

Acknowledgments

Conflicts of Interest

References

- Kim, K.; Kabir, E.; Jahan, S.A. Exposure to pesticides and the associated human health effects. Sci. Total Environ. 2017, 575, 525–535. [Google Scholar] [CrossRef] [PubMed]

- Poore, J.; Nemecek, T. Reducing food’s environmental impacts through producers and consumers. Science 2018, 360, 987–992. [Google Scholar] [CrossRef] [PubMed]

- Cooper, T.; Hart, K.; Baldock, D. The Provision of Public Goods through Agriculture in the European Union; Report Prepared for DG Agriculture and Rural Development, Contract No. 30-CE-0233091/00-28; Institute for European Environmental Policy: London, UK, 2009. [Google Scholar]

- Pretty, J.; Benton, T.G.; Bharucha, Z.P.; Dicks, L.V.; Flora, C.B.; Godfray, C.J.; Goulson, D.; Hartley, S.; Lampkin, N.; Morris, C.; et al. Global assessment of agricultural system redesign for sustainable intensification. Nat. Sustain. 2018, 1, 441–446. [Google Scholar] [CrossRef]

- Sutton, M.; Howard, C.; Erisman, J.W.; Billen, A.; Gerennfelt, P.; Van Grinsven, H.; Grizzetti, B. (Eds.) The European Nitrogen Assessment: Sources, Effects and Policy Perspectives; Cambridge University Press: Cambridge, UK, 2011. [Google Scholar]

- Giannadaki, D.; Giannakis, E.; Pozzer, A.; Lelieveld, J. Estimating health and economic benefits of reductions in air pollution from agriculture. Sci. Total Environ. 2018, 622, 1304–1316. [Google Scholar] [CrossRef]

- Bobbink, R.; Hicks, K.; Galloway, J.; Spranger, T.; Alkemade, R.; Ashmore, M.; Bustamante, M.; Cinderby, S.; Davidson, E.; Dentener, F.; et al. Global Assessment of nitrogen deposition effects on terrestrial plant diversity: A synthesis. Ecol. Appl. 2010, 20, 30–59. [Google Scholar] [CrossRef]

- Hanley, N.J.; Shogren, J.; White, B. Environmental Economics in Theory and Practice; Palgrave: London, UK, 2007. [Google Scholar]

- FAO. Natural Capital Impacts in Agriculture. Supporting Better Business Decision-Making; Food and Agriculture Organization of the United Nations: Rome, Italy, 2015. [Google Scholar]

- Pretty, J.N.; Brett, C.; Gee, D.; Hine, R.E.; Mason, C.F.; Morison, J.I.L.; Raven, H.; Rayment, M.D.; Van der Bijl, G. An assessment of the total external costs of UK agriculture. Agric. Syst. 2000, 65, 113–136. [Google Scholar] [CrossRef]

- Pretty, J.; Brett, C.; Gee, D.; Hine, R.; Mason, C.; Morison, J.; Rayment, M.; Van Der Bijl, G.; Dobbs, T. Policy challenges and priorities for internalizing the externalities of modern agriculture. J. Environ. Plan. Manag. 2001, 44, 263–283. [Google Scholar] [CrossRef]

- Pretty, J.N.; Ball, A.S.; Lang, T.; Morison, J.I.L. Farm costs and food miles: An assessment of the full cost of the UK weekly food basket. Food Policy 2005, 30, 1–19. [Google Scholar] [CrossRef]

- Tegtmeier, E.M.; Duffy, M.D. External costs of agricultural production in the United States. Int. J. Agric. Sustain. 2004, 2, 1–20. [Google Scholar] [CrossRef]

- Jongeneel, R.; Polman, N.; Van Kooten, G.C. How Important are Agricultural Externalities? A Framework for Analysis and Application to Dutch Agriculture; Working Paper 2016-04, Resource Economic; Policy Analysis Research Group, Department of Economic, University of Victoria: Victoria, BC, Canada, 2016. [Google Scholar]

- Stiglitz, J.; Rosengaard, J.K. Economics of the Public Sector; W. W. Norton: New York, NY, USA, 2015. [Google Scholar]

- Batáry, P.; Lynn, V.; Dicks, L.V.; Kleijn, D.; Sutherland, W.J. The role of agri-environment schemes in conservation and environmental management. Conserv. Biol. 2015, 29, 1006–1016. [Google Scholar] [CrossRef]

- Buchanan, J.; Stubblebine, C. Externality. Economica 1962, 29, 371–384. [Google Scholar] [CrossRef]

- European Commission. Eurobarometer 80.2; European Commission: Brussels, Belgium, 2013. [Google Scholar]

- Schläpfer, F.; Baur, I. Does CAP spending reflect taxpayer preferences? An analysis of expenditures for public goods and income redistribution in relation to preference indicators. In Proceedings of the 15th Congress of the European Association of Agricultural Economists, Parma, Italy, 28 August 2017. [Google Scholar]

- Obst, C.; Hein, L.; Edens, B. National accounting and the valuation of ecosystem assets and their services. Environ. Res. Econ. 2015, 64, 1–23. [Google Scholar] [CrossRef]

- Hein, L.; Bagstad, K.; Edens, B.; Obst, C.; de Jong, R.; Lesschen, J.P. Defining ecosystem assets for natural capital accounting. PLoS ONE 2016, 11, e0164460. [Google Scholar] [CrossRef] [PubMed]

- Badura, T.; Ferrini, S.; Agarwala, M.; Turner, K. Valuation for Natural Capital and Ecosystem Accounting. Synthesis Report for the European Commission; Centre for Social and Economic Research on the Global Environment, University of East Anglia: Norwich, UK, 2017. [Google Scholar]

- Kling, L.K.; Phaneuf, D.J.; Zhao, J. From Exxon to BP: Has some number become better than no number? J. Econ. Perspect. 2012, 26, 3–26. [Google Scholar] [CrossRef]

- Mack, G.; Heitkämper, K.; Käufeler, B.; Möbius, S. Evaluation der Beiträge für Graslandbasierte Milch- und Fleischproduktion (GMF). Agroscope Sci. 2017, 54, 1–106. [Google Scholar]

- Möhring, A.; Mack, G.; Zimmermann, A.; Mann, S.; Ferjani, A. Evaluation Versorgungssicherheitsbeiträge. Schlussbericht. Agroscope Science 66; Agroscope: Tänikon, Ettenhausen, Switzerland, 2018. [Google Scholar]

- Baur, I.; Schläpfer, F. Expert estimates of the share of agricultural support that compensates European farmers for providing public goods and services. Ecol. Econ. 2018, 147, 264–275. [Google Scholar] [CrossRef]

- FOA. Agricultural Report 2018; Federal Office of Agriculture: Bern, Switzerland, 2019. [Google Scholar]

- Prechsl, U.E.; Wittwer, R.; Van der Heijden, M.; Lüscher, G.; Jeanneret, P.; Nemecek, T. Assessing the environmental impacts of cropping systems and cover crops: Life cycle assessment of FAST, a long-term arable farming field experiment. Agric. Syst. 2017, 157, 39–50. [Google Scholar] [CrossRef]

- Schaller, B.; Nemecek, T.; Streit, B.; Zihlmann, U.; Chervet, A.; Sturny, G. Vergleichsökobilanz Direktsaat und Pflug. Agrarforschung 2006, 13, 482–487. [Google Scholar]

- Agridea. Ressourceneffizienzbeiträge REB. Beitragsdauer 2014–2021. Schonende Bodenbearbeitung; Agridea: Lindau, Switzerland, 2019. [Google Scholar]

- Bracher, A.; Spring, P. Möglichkeiten zur Reduktion der Ammoniakemissionen durch Fütterungsmassnahmen bei Schweinen; Schweizerische Hochschule für Landwirtschaft (SHL), Zollikofen, and Agroscope: Liebefeld-Posieux, Switzerland, 2010. [Google Scholar]

- Kupper, T.; Bonjour, C.; Menzi, H.; Bretscher, D.; Zaucker, F. Ammoniakemissionen der schweizerischen Landwirtschaft 1990–2015. In Auftrag des Bundesamts für Umwelt. Hochschule für Agrar-, Forst- und Lebensmittelwissenschaften, Bonjour Engineering GmbH und Oetiker+Partner AG; Hochschule für Agrar-, Forst- und Lebensmittelwissenschaften (HAFL): Zollikofen, Switzerland, 2018. [Google Scholar]

- Heldstab, J.; Leippert, F.; Biedermann, R.; Schwank, O. Stickstoffflüsse in der Schweiz 2020. Stoffflussanalyse und Entwicklungen; Bundesamt für Umwelt: Bern, Switzerland, 2013. [Google Scholar]

- Agridea. Ressourceneffizienzbeiträge REB. Beitragsdauer 2018–2021. Stickstoffreduzierte Phasenfütterung bei Schweinen; Agridea: Lindau, Switzerland, 2018. [Google Scholar]

- Frick, R.; Menzi, H.; Katz, P. Ammoniakemissionen Nach der Hofdüngerausbringung; FAT-Berichte Nr. 486. Eidg; Forschungsanstalt für Agrarwirtschaft und Landtechnik (FAT): Tänikon, Switzerland, 1996. [Google Scholar]

- Richner, W.; Oberholzer, H.R.; Freiermuth, R.; Knuchel, R.; Huguenin, O.; Ott, S.; Nemecek, T.; Walther, U. Modell zur Beurteilung der Nitrat-auswaschung in Ökobilanzen—SALCA-NO3. Agroscope Sci. 2014, 5, 1–28. [Google Scholar]

- Agridea. Ressourceneffizienzbeiträge REB. Beitragsdauer 2014–2019. Emissionsmindernde Ausbringverfahren; Agridea: Lindau, Switzerland, 2017. [Google Scholar]

- UNECE. Draft Guidance Document for Preventing and Abating Ammonia Emissions from Agricultural Sources; Paper ECE/EB.AIR/2012/L.9; UNECE: Geneva, Switzerland, 2012. [Google Scholar]

- Econcept; Agridea; L’Azure; Agroscope. Evaluation der Biodiversitätsbeiträge. Schlussbericht. Im Auftrag des Bundesamts für Landwirtschaft; Agroscope: Bern, Switzerland, 2019. [Google Scholar]

- FOEN; FOA. Umweltziele Landwirtschaft; Federal Office for the Environment and Federal Office of Agriculture: Bern, Switzerland, 2008. [Google Scholar]

- FOEN; FOA. Umweltziele Landwirtschaft. Statusbericht; Federal Office for the Environment and Federal Office of Agriculture: Bern, Switzerland, 2016. [Google Scholar]

- FOEN. Boden in der Schweiz. Zustand und Entwicklung; Stand 2017; Federal Office for the Environment: Bern, Switzerland, 2017. [Google Scholar]

- Doppler, T.; Mangold, S.; Wittmer, I.; Spycher, S.; Stamm, C.; Singer, H.; Junghans, M.; Kunz, M. Hohe Pflanzenschutzmittelbelastung in Schweizer Bächen. Aqua Gas 2017, 4, 46–56. [Google Scholar]

- FOEN. Zustand und Entwicklung Grundwasser Schweiz. Ergebnisse der Nationalen Grundwasserbeobachtung NAQUA, Stand 2016; Federal Office for the Environment: Bern, Switzerland, 2019. [Google Scholar]

- De Baan, L.; Spycher, S.; Daniel, O. Einsatz von Pflanzenschutzmitteln in der Schweiz von 2009 bis 2012. Agrarforschung Schweiz 2015, 6, 48–55. [Google Scholar]

- FOA. Überblick: Direktzahlungen an Schweizer Ganzjahresbetriebe; Federal Office of Agriculture: Bern, Switzerland, 2018. [Google Scholar]

- OECD. OECD Review of Agricultural Policies: Switzerland; OECD: Paris, France, 2015. [Google Scholar]

- OECD. Agricultural Policy Monitoring and Evaluation 2019; OECD: Paris, France, 2019. [Google Scholar]

- OECD. Producer Support Estimates (PSE) Database; OECD: Paris, France, 2020. [Google Scholar]

- FOS. Produktionswert von Biologischer und Konventioneller Landwirtschaft; Federal Office of Statistics: Neuchatel, Switzerland, 2019. [Google Scholar]

- Huber, R.; Finger, R. Popular initiatives increasingly stimulate agricultural policy in Switzerland. EuroChoices 2019, 18, 38–39. [Google Scholar] [CrossRef]

- Vonplon, D. Wie die Milliarden für die Landwirtschaft verpuffen. Neue Zürcher Zeitung, 7 March 2019; 15. [Google Scholar]

- Federal Council. Botschaft zur Weiterentwicklung der Agrarpolitik ab 2022 (AP22+). Federal Bulletin 2020; Federal Council: Bern, Switzerland, 2020; pp. 3955–4212. [Google Scholar]

- FOSD. Fair and Efficient. The Distance-Related Heavy Vehicle Fee (HVF) in Switzerland; Federal Office for Spatial Development: Bern, Switzerland, 2015. [Google Scholar]

- Fitzpatrick, I.; Young, R.; Perry, M.; Rose, E. The Hidden Cost of UK Food; Sustainable Food Trust: Bristol, UK, 2017. [Google Scholar]

- FSVO. Eating Well and Staying Healthy. Swiss Nutrition Policy 2017–2024; Federal Food Safety and Veterinary Office: Bern, Switzerland, 2017. [Google Scholar]

- Finger, R.; Möhring, N.; Dalhaus, T.; Böcker, T. Revisiting pesticide taxation schemes. Ecol. Econ. 2017, 134, 263–266. [Google Scholar] [CrossRef]

- Schläpfer, F. An incentive tax on nitrogen loss in Swiss agriculture? Agrarforschung Schweiz 2016, 7, 496–503. [Google Scholar]

- Hein, L.; Bagstad, K.J.; Obst, C.; Edens, B.; Schenau, S.; Castillo, G.; Soulard, F.; Brown, C.; Driver, A.; Bordt, M.; et al. Progress in natural capital accounting for ecosystems. Science 2020, 367, 514–515. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

| Study | Country | Assessed Cost Categories | Greenhouse Gases | Ammonia | Nitrate | Phosphate | Soil Erosion | Pesticides | Biodiversity | Pathogens | Other | Assessed Quantity | Assessed Financial Costs per Hectare | Valuation of Greenhouse Gases, per t of CO2 | Total External Costs per Hectare |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Pretty et al. 2000 | UK | Financial a | - | - | t, m | t, r | t, m | t, m, a | r, m | r, m | r, m | Various e | £102 | £63 (1996) | £208 |

| Other b | IH | IH | - | - | - | - | - | - | SA | ||||||

| Pretty et al. 2001 | UK; US; GER | Financial a | - | - | t, m | t, m | t, m | t, m | r, m | t, r | r, m | Various e | £102; £24; £6 | £63 (1996) | £208; £49; £71 |

| Other b | IH | IH | - | - | - | - | - | - | SA | ||||||

| Tegtmeier & Duffy 2004 | US | Financial a | - | - | t, m | t, m | t, r, m | t, m | r, m | t, r | - | Various e | $2.65 | $0.98 (2002) | $29–96 |

| Other b | MA + | - | - | - | - | - | - | - | - | ||||||

| FAO 2015 | 40 countries c | Financial a | - | - | - | - | - | - | - | - | Total quantity | NA | $115 (2013) | $475 d | |

| Other b | IH | IH | IH | IH | IH | IH | - | IH | |||||||

| Jongeneel et al. 2016 | NL | Financial a | - | - | t | t | t, m | t, m | r, m | t, r | m, a | Various e | €193 | €16 (2012) | €988 |

| Other b | MA + | IH | MA | - | - | - | - | - | var. | ||||||

| (this study) | CH | Financial a | a | a | a | a | a | a | a | - | a | Harmful units | CHF 636 | CHF 96 (2018) | CHF 3494 |

| Other b | SA | SA | SA | SA | SA | SA | - | - | SA |

| Type of Payment a | Direct Payment Expenditures | |

|---|---|---|

| mio. CHF | % of Total | |

| Payments for services | 1210 | 41.9 |

| Subsidies for damage avoidance | 636 | 22.1 |

| Other subsidies | 1309 | 36.0 |

| Total | 2884 | 100.0 |

| No. | Environmental Measure a | Unit of Measure | Total Expenditures (mio. CHF) | Payment per Unit of Measure (CHF) | Targeted Externality | Weight b | Payment per Unit of Measure for Targeted Externality (CHF) |

|---|---|---|---|---|---|---|---|

| 1 | CO2 tax on fuels (not limited to agriculture) | t CO2 | 1200 | 96 | greenhouse gas e. | 1 | 96 |

| 2 | Direct seeding (3 targeted externalities) | ha | 16.7 c | 250 | (a) nitrate e. | 0.333 | 83.33 |

| (b) soil erosion | 0.333 | 83.33 | |||||

| (c) greenhouse gas e. | 0.167 | 41.67 | |||||

| 3 | Nitrogen-reduced feeding of pigs (2 targeted ext.) | LSU | 2.4 | 35 | (a) ammonia e. | 0.75 | 26.25 |

| (b) greenhouse gas e. | 0.25 | 8.75 | |||||

| 4 | Reduced emissions appl. of manure, trailing hose | ha × appl. | 13.1 d | 30 | ammonia e. | 1 | 30 |

| 5 | Reduced emissions appl. of manure, trailing shoe | ha × appl. | 30 | ammonia e. | 1 | 30 | |

| 6 | Reduced emissions appl. of manure, injection | ha × appl. | 30 | ammonia e. | 1 | 30 | |

| 7 | Extensive livestock on grassland | ha | 110.8 | 200 | ammonia e. | 1 | 200 |

| 8 | No herbicide in FR, VI | ha | 1.8 e | 600 | herbicide e. | 1 | 600 |

| 9 | No herbicide in SB | ha | 800 | herbicide e. | 1 | 800 | |

| 10 | No herbicide in soil cons. measures | ha | 200 | herbicide e. | 1 | 200 | |

| 11 | No fungicide in FR | ha | 200 | fungicide e. | 1 | 200 | |

| 12 | No fungicide in VI | ha | 300 | fungicide e. | 1 | 300 | |

| 13 | No fungicide, insecticide in SB | ha | 400 | fungi-/insecticide e. | 1 | 400 | |

| 14 | No fungi-, insecticide in GR, RS, SF, LF | ha | 35.2 | 400 | fungi-/insecticide e. | 1 | 400 |

| 15 | Biodiversity—extensive grassland, Q1 (4 zones) | ha | 67.0 | 1080/860/500/450 | habitat deficits | 1 | 1080/860/500/450 |

| 16 | Biodiversity—low-intensity meadow, Q1 | ha | 7.2 | 450 | habitat deficits | 1 | 450 |

| 17 | Biodiversity—extensive pasture, Q1 | ha | 21.6 | 450 | habitat deficits | 1 | 450 |

| 18 | Biodiversity—pollinator strips | ha | 0.3 | 2500 | habitat deficits | 1 | 2500 |

| 15 | Animals, outdoor space (3 LS categories) | LSU | 191.6 | 90/155/280 | animal suffering | 1 | 90/155/280 |

| 16 | Animals, housing (4 LS categories) | LSU | 83.9 | 165/190/290/370 | animal suffering | 1 | 165/190/290/370 |

| No. | Targeted Externality a | Measure | Unit of Measure | Payment per Unit of Measure for Single Externality (from Table 3) (CHF) | Unit of Externality | Quantity of Externality Avoided by One Unit of Measure b | Cost per Unit of Targeted Externality (CHF) |

|---|---|---|---|---|---|---|---|

| 1a | Greenhouse gas e. | CO2 tax on fuels | t | 96 | t CO2 | 1 | 96 |

| 1b | Greenhouse gas e. | nitrogen-reduced feeding of pigs | LSU | 8.75 | t CO2-eq. | 0.064 | 137 |

| 1c | Greenhouse gas e. | direct seeding | ha | 41.67 | t CO2-eq. | 150 | 278 |

| 2a | Ammonia e. | nitrogen-reduced feeding of pigs | LSU | 26.25 | kg N | 2.34 | 11.22 |

| 2b | Ammonia e. | extensive livestock on grassland | ha | 200 | kg N | 2 | 100 |

| 2c | Ammonia e. | reduced emissions appl. of manure, trailing hose | ha × appl. | 30 | kg N | 4.875 | 6.15 |

| 2d | Ammonia e. | reduced emissions appl. of manure, trailing shoe | ha × appl. | 30 | kg N | 6.75 | 4.44 |

| 2e | Ammonia e. | reduced emissions appl. of manure, injection | ha × appl. | 30 | kg N | 10.5 | 2.86 |

| 3 | Nitrate emissions | direct seeding | ha | 83.33 | kg N | 3 | 27.8 |

| 4 | Soil erosion | direct seeding | ha | 83.33 | ha | 1 | 83.33 |

| 5a | Herbicide e. | no herbicide in FR, VI | ha | 600 | ha | 1 | 600 |

| 5b | Herbicide e. | no herbicide in SB | ha | 800 | ha | 1 | 800 |

| 5c | Herbicide e. | no herbicide in soil conservation | ha | 200 | ha | 1 | 200 |

| 6a | Fungicide e. | no fungicide in FR | ha | 200 | ha | 1 | 200 |

| 6b | Fungicide e | no fungicide in VI | ha | 300 | ha | 1 | 300 |

| 6c | Fungi- & insecticide e. | no fungi-, insecticide in GR/RS/SF/LF | ha | 400 | ha | 1 | 400 |

| 6d | Fungi- & insecticide e. | no fungicide, insecticide in SB | ha | 400 | ha | 1 | 400 |

| 7a | Habitat deficits | biodiversity—extensive grassland, Q1 (4 zones) | ha | 1080/860/500/450 | ha | 1 | 1080/860/500/450 |

| 7b | Habitat deficits | biodiversity—low-intensity meadow, Q1 | ha | 450 | ha | 1 | 450 |

| 7c | Habitat deficits | biodiversity—extensive pasture, Q1 | ha | 450 | ha | 1 | 450 |

| 7d | Habitat deficits | biodiversity—pollinator strips | ha | 2500 | ha | 1 | 2500 |

| 8 | Animal suffering | animals, outdoor space (3 livestock categories) | LSU | 90/155/280 | LSU | 1 | 90/155/280 |

| 9 | Animal suffering | animals, housing conditions (4 livestock cat.) | LSU | 165/190/290/370 | LSU | 1 | 165/190/290/370 |

| Externality | Relevant Emissions a | Unit | Quantity | Avoidance Cost per Unit of Externality (CHF) | |

|---|---|---|---|---|---|

| Average | Highest | ||||

| Greenhouse gases | All emissions | t CO2eq | 8390 | 96 | 278 |

| Ammonia | Units above legal target | kg N | 17 × 106 | 89 | 100 |

| Nitrate | Units above legal target | kg N | 12 × 106 | 27 | 27 |

| Soil erosion | Surface threatened by erosion | ha | 28,000 | 83 | 83 |

| Herbicide | Area with application | ha | 245,000 | 700 | 800 |

| Fungicide, insecticide | Area with application | ha | 156,000 | 400 | 400 |

| Habitat deficits b | Area below quantitative target | ha | 0 | 701 | 2500 |

| Animal outdoor space | LSU without high standard | LSU | 295,000 | 197 | 280 |

| Animal housing conditions | LSU without high standard | LSU | 480,000 | 108 | 370 |

| Externality | Financial Costs of Avoidance (Burden on Taxpayers; mio. CHF) | Costs of Unavoided Externalities (Burden on Society at Large; Million CHF) | Total External Costs (Burden on Society and Taxpayers; Million CHF) | ||

|---|---|---|---|---|---|

| Based on Average Avoidance Costs | Based on Highest Avoidance Costs | Based on Average Avoidance Costs | Based on Highest Avoidance Costs | ||

| Environment (total) | 284 | 2905 | 4664 | 3189 | 4948 |

| Greenhouse gases | 3 a | 809 | 2349 | 812 | 2352 |

| Ammonia | 124 | 1527 | 1720 | 1651 | 1844 |

| Nitrate | 4 | 334 | 334 | 338 | 338 |

| Soil erosion | 4 | 2 | 2 | 7 | 6 |

| Herbicide | 2 | 172 | 196 | 174 | 198 |

| Fungi-/insecticide | 35 | 62 | 62 | 97 | 97 |

| Habitat deficits | 111 | 0 | 0 | 111 | 111 |

| Animal suffering (total) | 269 | 110 | 260 | 379 | 529 |

| Outdoor space | 192 | 58 | 83 | 250 | 275 |

| Housing conditions | 77 | 52 | 178 | 129 | 255 |

| Multiple externalitiesb | 83 | 83 | 83 | ||

| Total | 636 | 3015 | 4924 | 3651 | 5560 |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Schläpfer, F. External Costs of Agriculture Derived from Payments for Agri-Environment Measures: Framework and Application to Switzerland. Sustainability 2020, 12, 6126. https://doi.org/10.3390/su12156126

Schläpfer F. External Costs of Agriculture Derived from Payments for Agri-Environment Measures: Framework and Application to Switzerland. Sustainability. 2020; 12(15):6126. https://doi.org/10.3390/su12156126

Chicago/Turabian StyleSchläpfer, Felix. 2020. "External Costs of Agriculture Derived from Payments for Agri-Environment Measures: Framework and Application to Switzerland" Sustainability 12, no. 15: 6126. https://doi.org/10.3390/su12156126

APA StyleSchläpfer, F. (2020). External Costs of Agriculture Derived from Payments for Agri-Environment Measures: Framework and Application to Switzerland. Sustainability, 12(15), 6126. https://doi.org/10.3390/su12156126