Online Company Reputation—A Thorny Problem for Optimizing Corporate Sustainability

,

,

Abstract

1. Introduction

2. Literature Review

3. Materials and Methods

- CR—Company online reputation;

- k, a1, a2, …am—the estimation parameters of the online reputation characteristics that will be determined at the company level;

- RIN—Online visibility;

- GS—Employee satisfaction;

- CD—Increase sales to customers who improve the company’s image;

- ROA—Return on assets;

- NCSR—Level of corporate social responsibility disclosure.

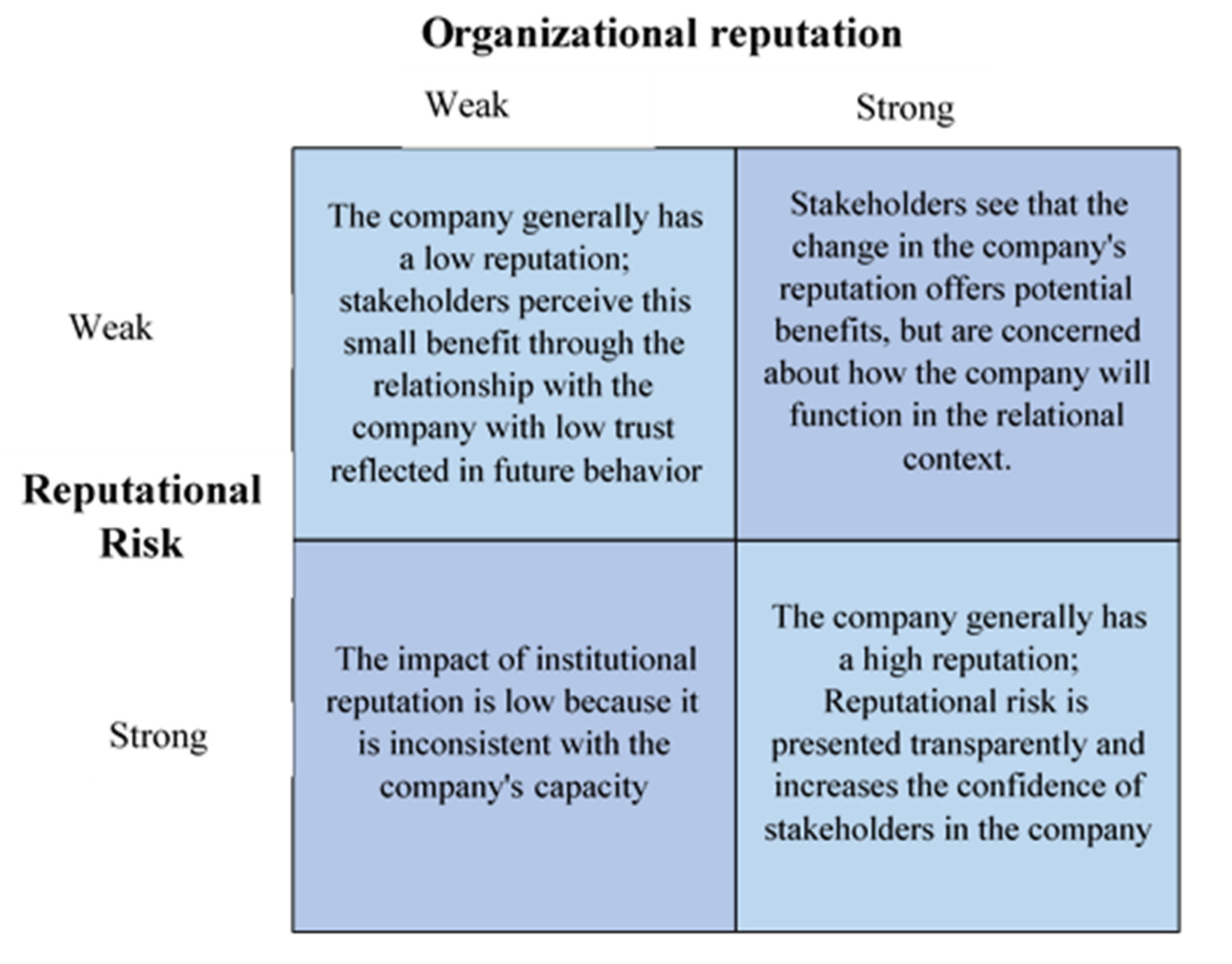

4. Results and Discussion

- Reputation in the online environment is dynamic, and the positions of different entries change from day to day and even from one search to another, depending on clicks, visits, different weights of sources, or search dynamics;

- The reputation in the online environment is built in competition with others, and the search experience reveals that there may be similarities in names that affect the online reputation of the company;

- Reputation in the online environment exists anyway, therefore its management is absolutely necessary because the lack of this management only creates a vulnerability.

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Rodríguez-Díaz, M.; Rodríguez-Voltes, C.I.; Rodríguez-Voltes, A.C. Gap Analysis of the online reputation. Sustainability 2018, 10, 1603. [Google Scholar] [CrossRef]

- Chen, Y.; Fay, S.; Wang, Q. The role of marketing in social media: How online consumer reviews evolve. J. Interact. Mark. 2011, 25, 85–94. [Google Scholar] [CrossRef]

- Lee, S.H.; Ro, H. The impact of online reviews on attitude changes: The deferential effects of review attributes and consumer knowledge. Int. J. Hosp. Manag. 2016, 56, 1–9. [Google Scholar] [CrossRef]

- Cismaru, D.M. Online reputation management in online social networks for governmental actors: Opportunities and threats. Rom. J. Commun. Public Relat. 2012, 14, 25–43. [Google Scholar]

- Means, G. The Modern Corporation and Private Property; Routledge: Abingdon, UK, 2017. [Google Scholar]

- Perakakis, E.; Mastorakis, G.; Kopanakis, I. Social media monitoring: An innovative intelligent approach. Designs 2019, 3, 24. [Google Scholar] [CrossRef]

- Kang, K.H.; Lee, S.; Huh, C. Impacts of positive and negative corporate social responsibility activities on company performance in the hospitality industry. Int. J. Hosp. Manag. 2010, 29, 72–82. [Google Scholar] [CrossRef]

- Sepasi, S.; Rahdari, A.; Rexhepi, G. Developing a sustainability reporting assessment tool for higher education institutions: The University of California. Sustain. Dev. 2018, 26, 672–682. [Google Scholar] [CrossRef]

- Radomir, L.; Plăiaş, I.; Nistor, V.C. Corporate online reputation, image and identity: Conceptual approaches. Mark. Inf. Decis. 2014, 7, 219–229. [Google Scholar]

- Walker, K.; Dyck, B. The primary importance of corporate social responsibility and ethicality in corporate online reputation: An empirical study. Bus. Soc. Rev. 2014, 119, 147–174. [Google Scholar] [CrossRef]

- Bennett, R.; Kottasz, R. Practitioner perceptions of corporate reputation: An empirical investigation. Corp. Commun. Int. J. 2000, 5, 224–235. [Google Scholar] [CrossRef]

- Déroche, G.; Penzenstadler, B. An analysis of best practice patterns for corporate social responsibility in top IT companies. Technologies 2018, 6, 76. [Google Scholar] [CrossRef]

- Grigorescu, A.; Maer-Matei, M.M.; Mocanu, C.; Zamfir, A.M. Key drivers and skills needed for innovative companies focused on sustainability. Sustainability 2020, 12, 102. [Google Scholar] [CrossRef]

- Li, S.; Niu, J.; Tsai, S.-B. Opportunism motivation of environmental protection activism and corporate governance: An empirical study from China. Sustainability 2018, 10, 1725. [Google Scholar] [CrossRef]

- Alcorn, S.; Alcorn, M. Benefit Corporations: A New Formula for Social Change; Associations Now: Washington, DC, USA, 2012. [Google Scholar]

- Cian, L.; Cervai, S. Under the online reputation umbrella: An integrative and multidisciplinary review for corporate image, projected image, construed image, organizational identity, and organizational culture. Corp. Commun. Int. J. 2014, 19, 182–199. [Google Scholar] [CrossRef]

- Garcia, S.; Cintra, Y.; de Torres, R.C.S.R.; Lima, F.G. Corporate sustainability management: A proposed multi-criteria model to support balanced decision-making. J. Clean. Prod. 2016, 136, 181–196. [Google Scholar] [CrossRef]

- Brammer, S.; Agarwal, V.; Taffler, R.; Brown, M. Corporate online reputation and financial performance: The interaction between capability and character. In Proceedings of the European Financial Management Association 2015 Annual Meeting, Amsterdam, The Netherlands, 24–27 June 2015; Available online: https://pdfs.semanticscholar.org/be37/c852180d142d8ea9ced7b19bf82d18db0735.pdf (accessed on 22 January 2020).

- Park, J.; Lee, H.; Kim, C. Corporate social responsibilities, consumer trust and corporate online reputation: South Korean consumers’ perspectives. J. Bus. Res. 2014, 67, 295–302. [Google Scholar] [CrossRef]

- Rodríguez-Díaz, M.; Rodríguez-Díaz, R.; Rodríguez-Voltes, A.C.; Rodríguez-Voltes, C.I. A model of market positioning of destinations based on online customer reviews of lodgings. Sustainability 2018, 10, 78. [Google Scholar] [CrossRef]

- Zaki Ahmed, A.; Rodríguez-Díaz, M. Analyzing the online reputation and positioning of airlines. Sustainability 2020, 12, 1184. [Google Scholar] [CrossRef]

- Van Marrewijk, M.; Werre, M. Multiple levels of corporate sustainability. J. Bus. Ethics 2003, 44, 107–119. [Google Scholar] [CrossRef]

- Pavláková Dočekalová, M.; Kocmanová, A. Comparison of sustainable environmental, social, and corporate governance value added models for investors decision making. Sustainability 2018, 10, 649. [Google Scholar] [CrossRef]

- Hu, N.; Liu, L.; Zhang, J.J. Do online reviews affect product sales? The role of reviewer characteristics and temporal effects. Inf. Technol. Manag. 2008, 9, 201–214. [Google Scholar] [CrossRef]

- Walker, K. A systematic review of the corporate online reputation literature: Definition, measurement, and theory. Corp. Online Reput. Rev. 2010, 12, 357–387. [Google Scholar] [CrossRef]

- Fischer, E.; Reuber, R. The good, the bad, and the unfamiliar: The challenges of online reputation formation facing new firms. Entrep. Theory Pract. 2007, 31, 53–75. [Google Scholar] [CrossRef]

- Fombrun, C.J.; Gardberg, N.A.; Sever, J.M. The online reputation quotient: A multiple stakeholder measure of corporate online reputation. J. Brand Manag. 2000, 7, 241–255. [Google Scholar] [CrossRef]

- Gray, E.R.; Balmer, J.M.T. Managing corporate image and corporate reputation. Long Range Plan. 1998, 31, 695–702. [Google Scholar] [CrossRef]

- Duca, I.; Gherghina, R. CSR Initiatives: An Opportunity for the Business Environment. In Ethics and Decision-Making for Sustainable Business Practices; Oncioiu, I., Ed.; IGI Global: Hershey, PA, USA, 2018; Volume 6, pp. 154–196. [Google Scholar]

- Luca, M. Reviews, Reputation, and Revenue: The Case of Yelp.com; Harvard Business School NOM Unit, Working Paper; Harvard Business School: Boston, MA, USA, 2011; pp. 12–16. [Google Scholar]

- Bae, S.M.; Masud, M.A.K.; Kim, J.D. A cross-country investigation of corporate governance and corporate sustainability disclosure: A signaling theory perspective. Sustainability 2018, 10, 2611. [Google Scholar] [CrossRef]

- Chevalier, J.A.; Mayzlin, D. The effect of word of mouth on sales: Online book reviews. J. Mark. Res. 2006, 43, 345–354. [Google Scholar] [CrossRef]

- Berens, G.; van Riel, C. Corporate associations in the academic literature: Three main streams of thought in the online reputation measurement literature. Corp. Online Reput. Rev. 2004, 7, 61–178. [Google Scholar] [CrossRef]

- Chun, R. Corporate reputation: Meaning and measurement. Int. J. Manag. Rev. 2005, 7, 91–109. [Google Scholar] [CrossRef]

- Winters, L.C. The effect of brand advertising on company image-implications for corporate advertising. J. Advert. Res. 1986, 26, 54–59. [Google Scholar]

- Lange, D.; Lee, P.M.; Dai, Y. Organizational online reputation: A review. J. Manag. 2011, 37, 153–183. [Google Scholar]

- Alshehhi, A.; Nobanee, H.; Khare, N. The impact of sustainability practices on corporate financial performance: Literature trends and future research potential. Sustainability 2018, 10, 494. [Google Scholar] [CrossRef]

- Chen, L.; Feldmann, A.; Tang, O. The relationship between disclosures of corporate social performance and financial performance: Evidences from GRI reports in manufacturing industry. Int. J. Prod. Econ. 2015, 170, 445–456. [Google Scholar] [CrossRef]

- Lin, W.L.; Ho, J.A.; Sambasivan, M. Impact of corporate political activity on the relationship between corporate social responsibility and financial performance: A dynamic panel data approach. Sustainability 2019, 11, 60. [Google Scholar] [CrossRef]

- Li, Z.F. Mutual monitoring and corporate governance. J. Bank. Financ. 2014, 45, 255–269. [Google Scholar]

- Banbhan, A.; Cheng, X.; Ud Din, N. Financially qualified members in an upper echelon and their relationship with corporate sustainability: Evidence from an emerging economy. Sustainability 2018, 10, 4697. [Google Scholar] [CrossRef]

- Rexhepi, G.; Kurtishi, S.; Bexheti, G. Corporate social responsibility (CSR) and innovation the drivers of business growth. Procedia Soc. Behav. Sci. 2013, 75, 532–541. [Google Scholar] [CrossRef]

- Socoliuc, M.; Grosu, V.; Hlaciuc, E.; Stanciu, S. Analysis of social responsibility and reporting methods of romanian companies in the countries of the European Union. Sustainability 2018, 10, 4662. [Google Scholar] [CrossRef]

- Lozano, R. A holistic perspective on corporate sustainability drivers. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 32–44. [Google Scholar] [CrossRef]

- Boyd, B.K.; Bergh, D.D.; Ketchen, D.J. Reconsidering the online reputation—Performance relationship: A resource-based view. J. Manag. 2010, 36, 588–609. [Google Scholar]

- Jeng, S.P. The effect of corporate online reputation s on customer perceptions and cross-buying intentions. Serv. Ind. J. 2011, 31, 851–862. [Google Scholar] [CrossRef]

- Rodríguez-Díaz, M.; Rodríguez-Díaz, R.; Rodríguez-Voltes, A.C.; Rodríguez-Voltes, C.I. Analysing the relationship between price and online reputation by lodging category. Sustainability 2018, 10, 4474. [Google Scholar] [CrossRef]

- Chi, G.G.; Gursoy, D. Employee satisfaction, customer satisfaction and financial performance: An empirical examination. Int. J. Hosp. Manag. 2009, 28, 245–253. [Google Scholar] [CrossRef]

- Kim, J.; Kim, J. Corporate sustainability management and its market benefits. Sustainability 2018, 10, 1455. [Google Scholar] [CrossRef]

- Yang, T.-K.; Yan, M.-R. The corporate shared value for sustainable development: An ecosystem perspective. Sustainability 2020, 12, 2348. [Google Scholar] [CrossRef]

- Callison, C. Media relations and the Internet: How Fortune 500 company web sites assist journalists in news gathering. Public Relat. Rev. 2003, 29, 29–41. [Google Scholar] [CrossRef]

- Love, G.E.; Kraatz, M. Character, conformity or the bottom line? How and why downsizing affected corporate online reputation. Acad. Manag. J. 2009, 52, 314–335. [Google Scholar] [CrossRef]

- Dahlsrud, A. How corporate social responsibility is defined: An analysis of 37 definitions. Corp. Soc. Responsib. Environ. Manag. 2008, 15, 1–13. [Google Scholar] [CrossRef]

- Davies, G.; Chun, R.; da Vinhas Silva, R.; Roper, S. Corporate Online Reputation and Competitiveness; Routledge: London, UK, 2003. [Google Scholar]

- Lee, Y.-M.; Hu, J.-L. Integrated approaches for business sustainability: The perspective of corporate social responsibility. Sustainability 2018, 10, 2318. [Google Scholar] [CrossRef]

- Köppl, P.; Neureiter, M. Corporate Social Responsibility—Guidelines and Concepts in the Management of Corporate Social Responsibility; Linde Verlag: Vienna, Austria, 2004; pp. 293–314. [Google Scholar]

- Barnett, M.L.; Jermier, J.M.; Lafferty, B.A. Corporate online reputation: The definitional landscape. Corp. Online Reput. Rev. 2006, 9, 26–38. [Google Scholar] [CrossRef]

- Fombrun, C.; Shanley, M. What’s in a name? Reputation building and corporate strategy. Acad. Manag. J. 1990, 33, 233–258. [Google Scholar]

- Mahmood, Z.; Kouser, R.; Ali, W.; Ahmad, Z.; Salman, T. Does corporate governance affect sustainability disclosure? A mixed methods study. Sustainability 2018, 10, 207. [Google Scholar] [CrossRef]

- Sweeney, L.; Coughlan, J. Do different industries report corporate social responsibility differently? An investigation through the lens of stakeholder theory. J. Mark. Commun. 2008, 14, 113–124. [Google Scholar] [CrossRef]

- Maden, C.; Arıkan, E.; Telci, E.E.; Kantur, D. Linking corporate social responsibility to corporate online reputation: A study on understanding behavioral consequences. Procedia Soc. Behav. Sci. 2012, 58, 655–664. [Google Scholar] [CrossRef]

- Hu, W.; Du, J.; Zhang, W. Corporate social responsibility information disclosure and innovation sustainability: Evidence from China. Sustainability 2020, 12, 409. [Google Scholar] [CrossRef]

- Okazaki, S.; Taylor, C.R. Social media and international advertising: Theoretical challenges and future directions. Int. Mark. Rev. 2013, 30, 56–71. [Google Scholar] [CrossRef]

- Elena Windolph, S.; Schaltegger, S.; Herzig, C. Implementing corporate sustainability: What drives the application of sustainability management tools in Germany? Sustain. Account. Manag. Policy J. 2014, 5, 378–404. [Google Scholar] [CrossRef]

- Dijkmas, C.; Kerkhof, P.; Beukeboom, C.J. A stage to engage: Social media use and corporate reputation. Tour. Manag. 2015, 47, 58–67. [Google Scholar] [CrossRef]

- Deephouse, D.L. How do reputations affect corporate performance? The effect of financial and media reputations on performance. Corp. Reput. Rev. 1997, 1, 68–72. [Google Scholar] [CrossRef]

- Deephouse, D.L. Media reputation as a strategic resource: An integration of mass communication and resource-based theories. J. Manag. 2000, 26, 1091–1112. [Google Scholar] [CrossRef]

- Wartick, S.L. Measuring corporate online reputation definition and data. Bus. Soc. 2002, 41, 371–392. [Google Scholar] [CrossRef]

- Myšková, R.; Hájek, P. Sustainability and corporate social responsibility in the text of annual reports—The case of the IT services industry. Sustainability 2018, 10, 4119. [Google Scholar] [CrossRef]

- Gatti, L.; Caruana, A.; Snehota, I. The role of corporate social responsibility, perceived quality and corporate online reputation on purchase intention: Implications for brand management. J. Brand Manag. 2012, 20, 65–76. [Google Scholar] [CrossRef]

- Timbate, L.; Park, C.K. CSR performance, financial reporting, and investors’ perception on financial reporting. Sustainability 2018, 10, 522. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Morioka, S.N.; de Carvalho, M.M. A systematic literature review towards a conceptual framework for integrating sustainability performance into business. J. Clean. Prod. 2016, 136, 134–146. [Google Scholar] [CrossRef]

- Perrini, F.; Tencati, A. Sustainability and stakeholder management: The need for new corporate performance evaluation and reporting systems. Bus. Strategy Environ. 2006, 15, 296–308. [Google Scholar] [CrossRef]

- De Castro, G.M.; López, J.E.N.; Sáez, P.L. Business and social online reputation: Exploring the concept and main dimensions of corporate online reputation. J. Bus. Ethics 2006, 63, 361–370. [Google Scholar] [CrossRef]

- Jiang, C.; Fu, Q.A. Win-win outcome between corporate environmental performance and corporate value: From the perspective of stakeholders. Sustainability 2019, 11, 921. [Google Scholar] [CrossRef]

- Lai, C.S.; Chiu, C.J.; Yang, C.F.; Pai, D.C. The effects of corporate social responsibility on brand performance: The mediating effect of industrial brand equity and corporate online reputation. J. Bus. Ethics 2010, 95, 457–469. [Google Scholar] [CrossRef]

- CSR Reports from the Corporate Register. Available online: http://www.corporateregister.com (accessed on 22 January 2020).

- Ministry of Public Finance. Available online: http://www.datoriepublica.gov.ro/agenticod.html?pagina=domenii (accessed on 22 January 2020).

- Caputo, F.; Veltri, S.; Venturelli, A. Sustainability strategy and management control systems in family firms. Evidence from a case study. Sustainability 2017, 9, 977. [Google Scholar] [CrossRef]

{kind=link}

| Variabile | Simbol | Definition |

|---|---|---|

| Online visibility | RIN | The proportion of entries displayed by the Google search engine as a result of the search with the name of the organization |

| Employee satisfaction | GS | where i—degree of satisfaction, i = 1,2,3,4,5 (5 is the highest degree of satisfaction) ni—number of people declaring a degree of satisfaction i |

| Increase sales to customers that improve the company’s image | CD | where PCDt—production sold to customers in t PCDt−1—production sold to customers in (t−1) |

| Return on assets | ROA | net profit/total assets |

| Level of corporate social responsibility disclosure | NCSR | Transparency regarding the reporting of information on corporate social responsibility (CSR); addresses the behavioral aspects of CSR and demonstrates consideration of CSR reporting tools |

| Alternative Hypothesis: Common AR coefs. (within-Dimension) | ||||

| Weighted | ||||

| Statistic | Prob. | Statistic | Prob. | |

| Panel V-Statistic | 0.887423 | 0.1611 | −2.25481 | 0.9916 |

| Panel rho-Statistic | 2.085566 | 0.9712 | 2.365137 | 0.9942 |

| Panel PP-Statistic | −30.0969 | 0.0000 | −4.47336 | 0.0000 |

| Panel ADF-Statistic | −7.27425 | 0.0000 | −4.31616 | 0.0000 |

| Alternative Hypothesis: Individual AR coefs. (between-Dimension) | ||||

| Statistic | Prob. | |||

| Group rho-Statistic | 4.157497 | 1.0000 | ||

| Group PP-Statistic | −9.38635 | 0.0000 | ||

| Group ADF-Statistic | −5.64525 | 0.0000 | ||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| Long Run Equation | ||||

| ROA | 2.812595 | 0.147727 | 16.67522 | 0.0000 |

| CD | −0.41821 | 0.154155 | −2.47684 | 0.0125 |

| NCSR | 1.277083 | 0.03905 | 21.1945 | 0.0000 |

| GS | 0.315095 | 0.179038 | 1.654249 | 0.0902 |

| RIN | −0.35355 | 0.029289 | −7.29914 | 0.0000 |

| Short Run Equation | ||||

| COINTEQ01 | −0.23107 | 0.057264 | −3.17061 | 0.0012 |

| D(ROA) | 0.547101 | 0.947611 | 0.56493 | 0.5315 |

| D(CD) | −0.75679 | 0.909813 | −0.81381 | 0.3809 |

| D(NCSR) | 0.176128 | 0.258459 | 0.684422 | 0.4584 |

| D(GS) | 0.329277 | 0.360372 | 0.896665 | 0.3296 |

| D(RIN) | 0.046815 | 0.018067 | 1.70081 | 0.0627 |

| Mean dependent var | 0.006101 | S.D. dependent var | 0.052002 | |

| S.E. of regression | 0.016484 | Akaike info criterion | −5.38566 | |

| Sum squared resid | 0.219562 | Schwartz criterion | −3.32031 | |

| Log likelihood | 1083.606 | Hanan-Quinn criter. | −4.52042 | |

| COINTEQ01 | D(ROA) | D(CD) | D(NCSR) | D(GS) | D(RIN) | |

|---|---|---|---|---|---|---|

| Ability to retain employees | −0.048 *** | 1.56 * | 0.26 *** | 0.54 *** | 1.12 ** | 0.14 *** |

| Innovation | −0.09 *** | −0.007 *** | 1.11 ** | 0.036 * | 0.01 ** | 0.22 *** |

| Online control | −0.21 *** | −0.23 | 0.29 ** | −0.06 *** | 0.32 * | 0.04 * |

| The value of long-term investments | −0.11 *** | 2.62 *** | 0.46 ** | 0.68 *** | 1.3 | 0.011 |

| Financial security | −0.02 *** | 4.29 *** | 0.22 ** | 1.06 *** | 0.65 | 0.25 *** |

| Ability to attract employees | −0.43 *** | 1.10 *** | 0.20 ** | 0.36 *** | 0.68 *** | 0.25 *** |

| Management quality | −0.24 *** | 2.25 *** | 0.32 *** | −0.69 *** | 0.88 *** | 0.02 *** |

| Quality of products and services | −0.16 *** | −0.15 *** | 0.57 *** | −0.45 *** | 2.21 *** | 0.33 *** |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Oncioiu, I.; Popescu, D.-M.; Anghel, E.; Petrescu, A.-G.; Bîlcan, F.-R.; Petrescu, M. Online Company Reputation—A Thorny Problem for Optimizing Corporate Sustainability. Sustainability 2020, 12, 5547. https://doi.org/10.3390/su12145547

Oncioiu I, Popescu D-M, Anghel E, Petrescu A-G, Bîlcan F-R, Petrescu M. Online Company Reputation—A Thorny Problem for Optimizing Corporate Sustainability. Sustainability. 2020; 12(14):5547. https://doi.org/10.3390/su12145547

Chicago/Turabian StyleOncioiu, Ionica, Delia-Mioara Popescu, Elena Anghel, Anca-Gabriela Petrescu, Florentina-Raluca Bîlcan, and Marius Petrescu. 2020. "Online Company Reputation—A Thorny Problem for Optimizing Corporate Sustainability" Sustainability 12, no. 14: 5547. https://doi.org/10.3390/su12145547

APA StyleOncioiu, I., Popescu, D.-M., Anghel, E., Petrescu, A.-G., Bîlcan, F.-R., & Petrescu, M. (2020). Online Company Reputation—A Thorny Problem for Optimizing Corporate Sustainability. Sustainability, 12(14), 5547. https://doi.org/10.3390/su12145547