Trends of Business-to-Business Transactions to Develop Innovative Cancer Drugs

Abstract

1. Introduction

- Much more inter-firm partnerships are performed for biologics in their product life cycle than for small molecules.

- Inter-firm transactions positively impact drug values, or specifically, the number of drug approvals.

2. Materials and Methods

2.1. Samples and Data Sources

2.2. Variables and Data Sources

2.3. Statistical Analysis

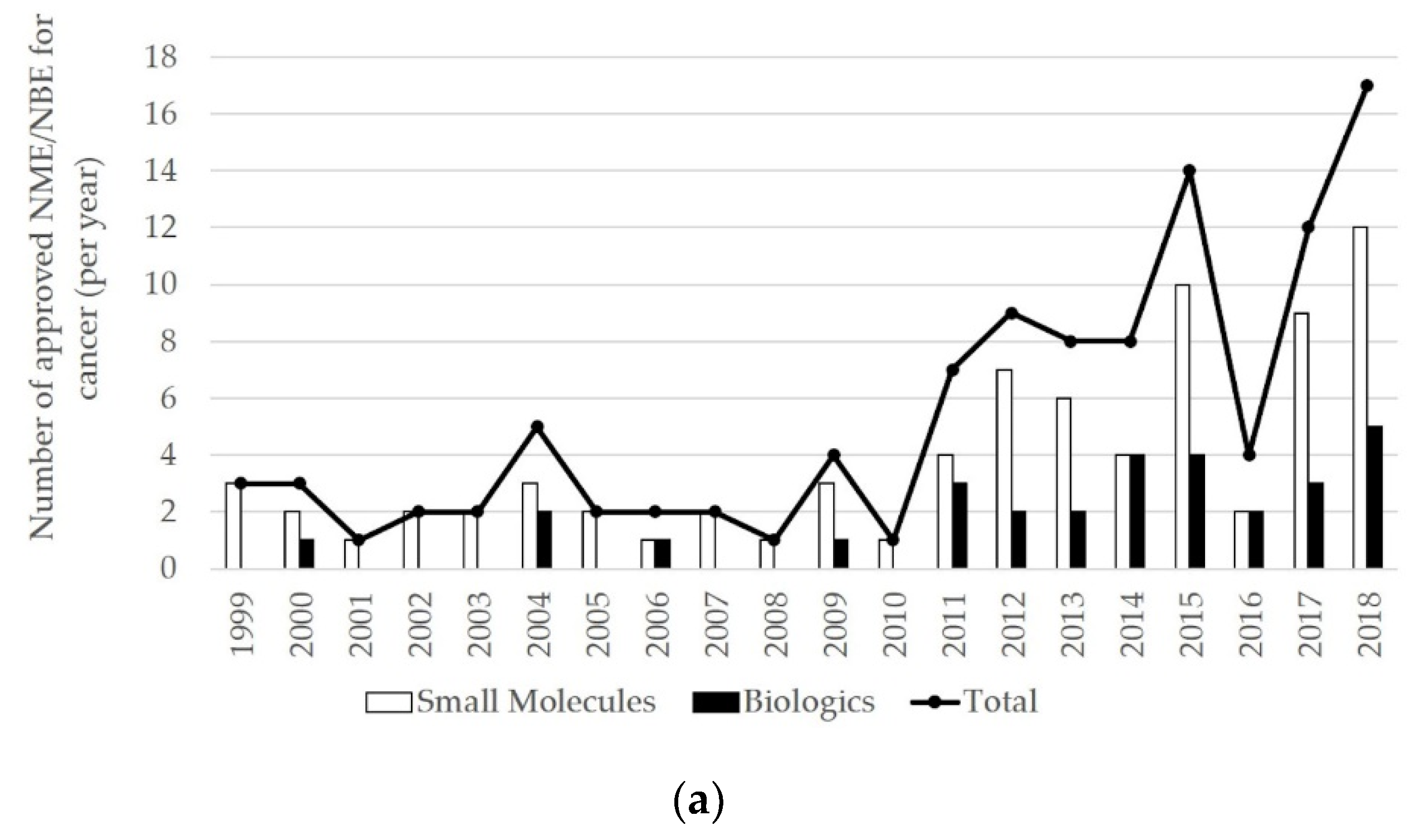

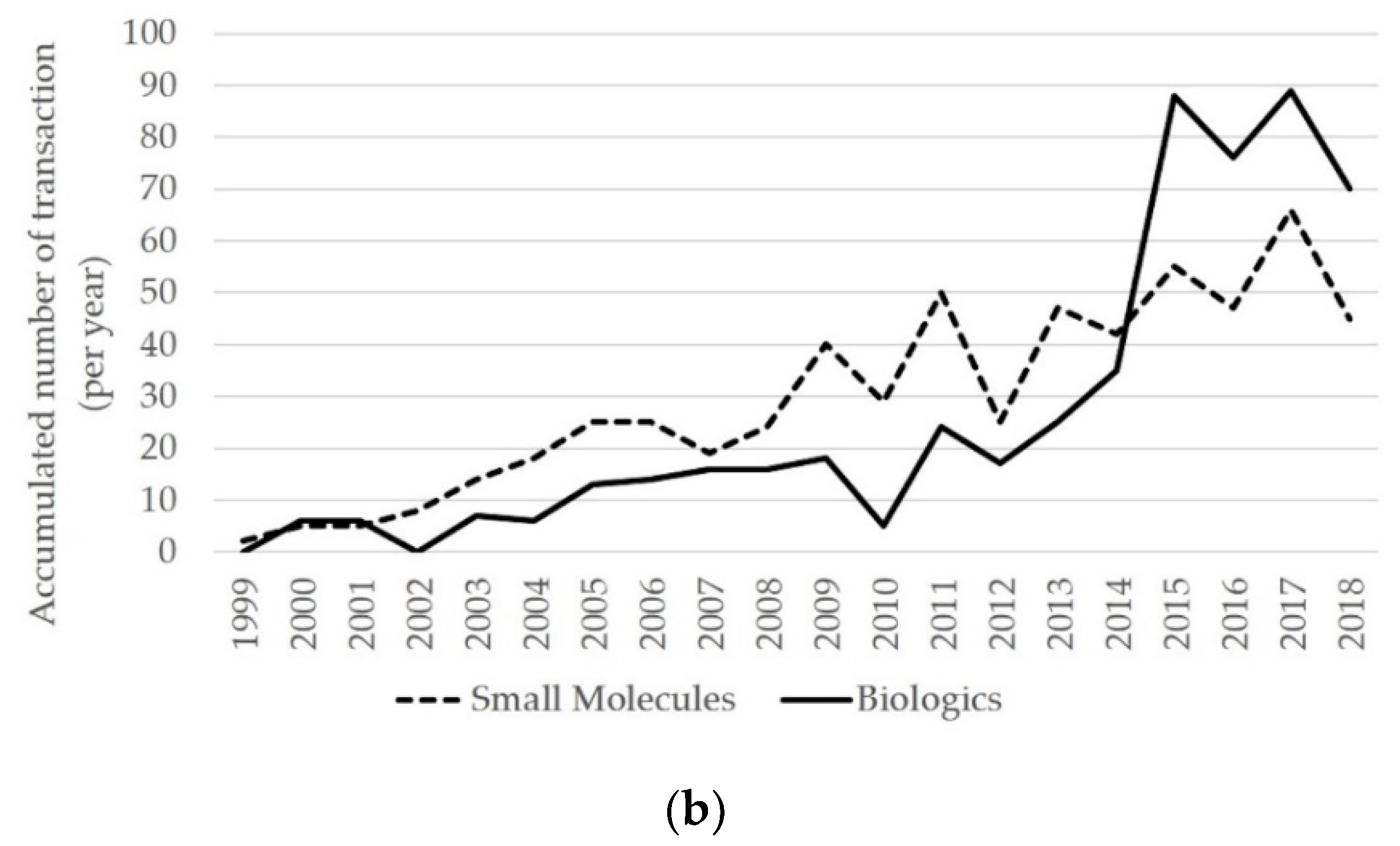

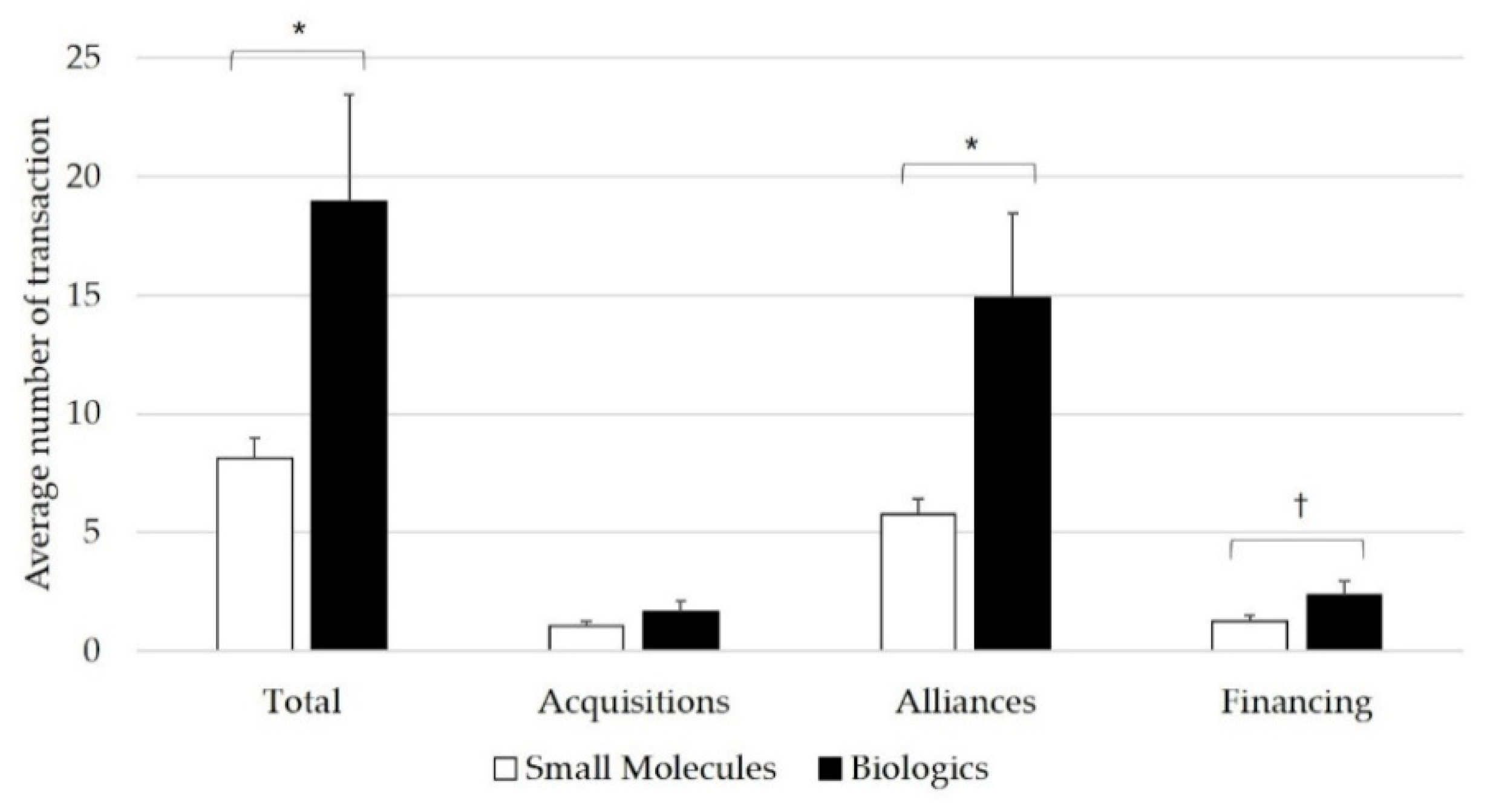

3. Results

3.1. Inter-Firm Partnerships for Biologics and Small Molecules

3.2. Key Driver of Inter-Firm Transactions for Biologics in 2015

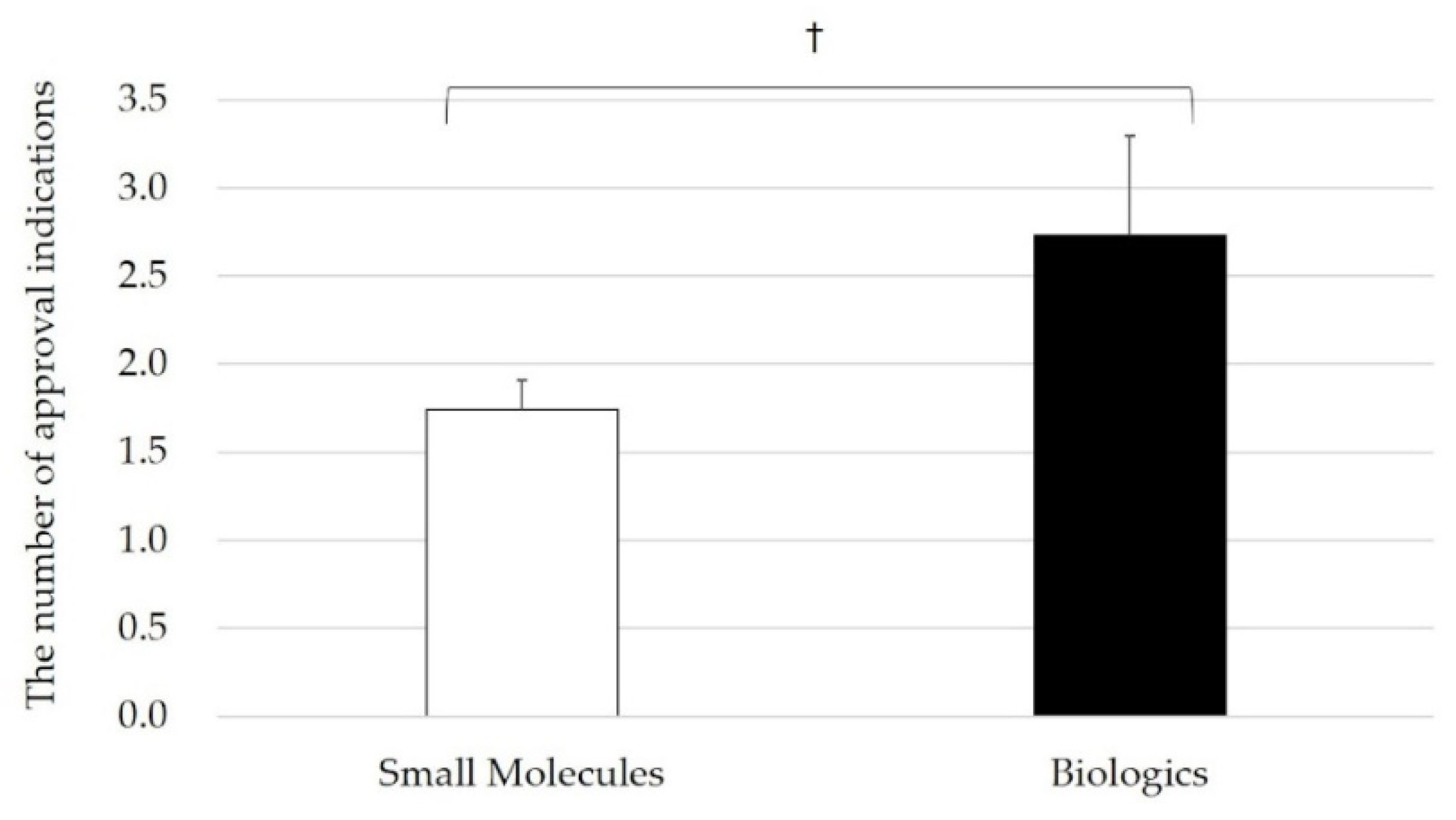

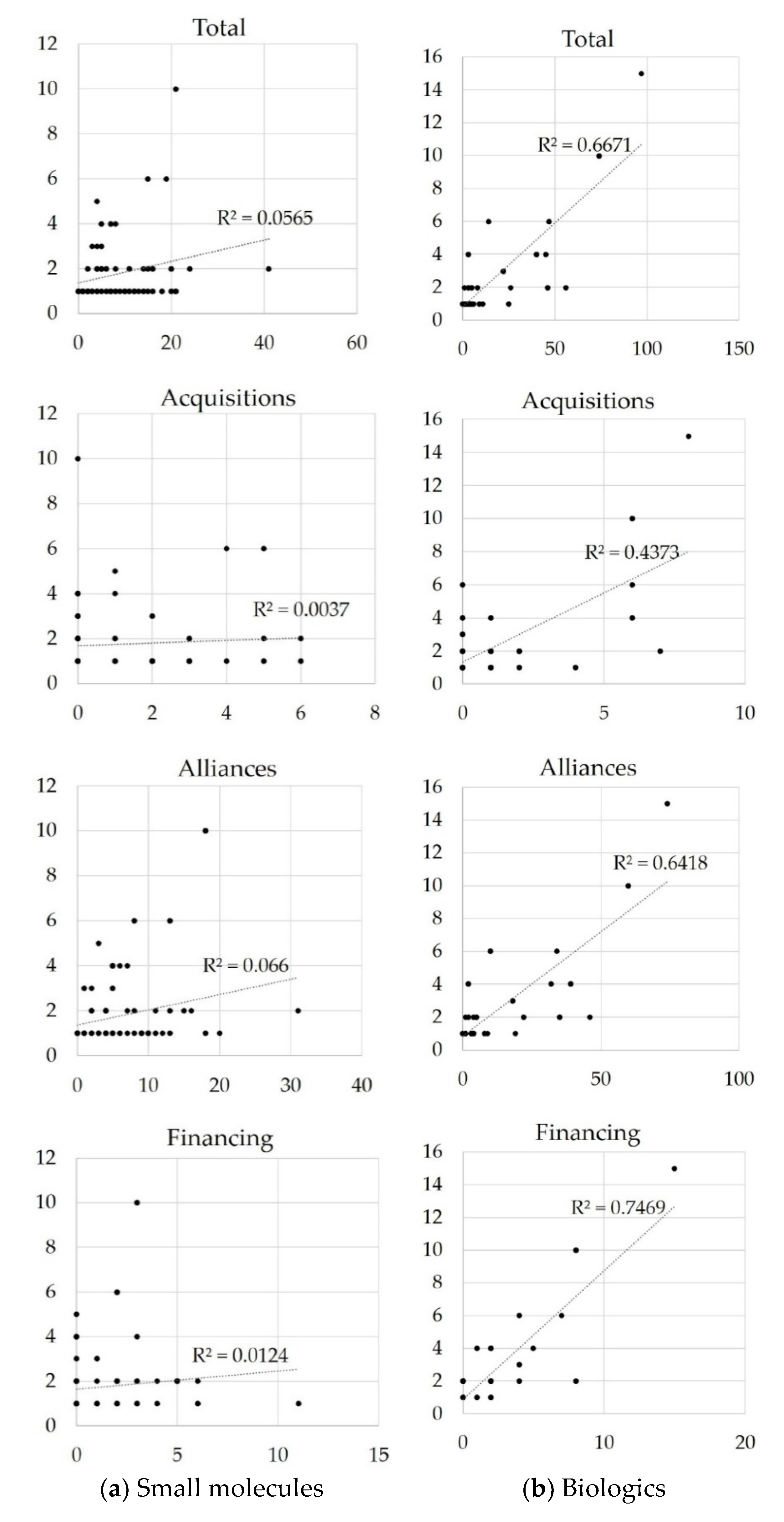

3.3. Relationship between Inter-Firm Transactions and Approved Indications

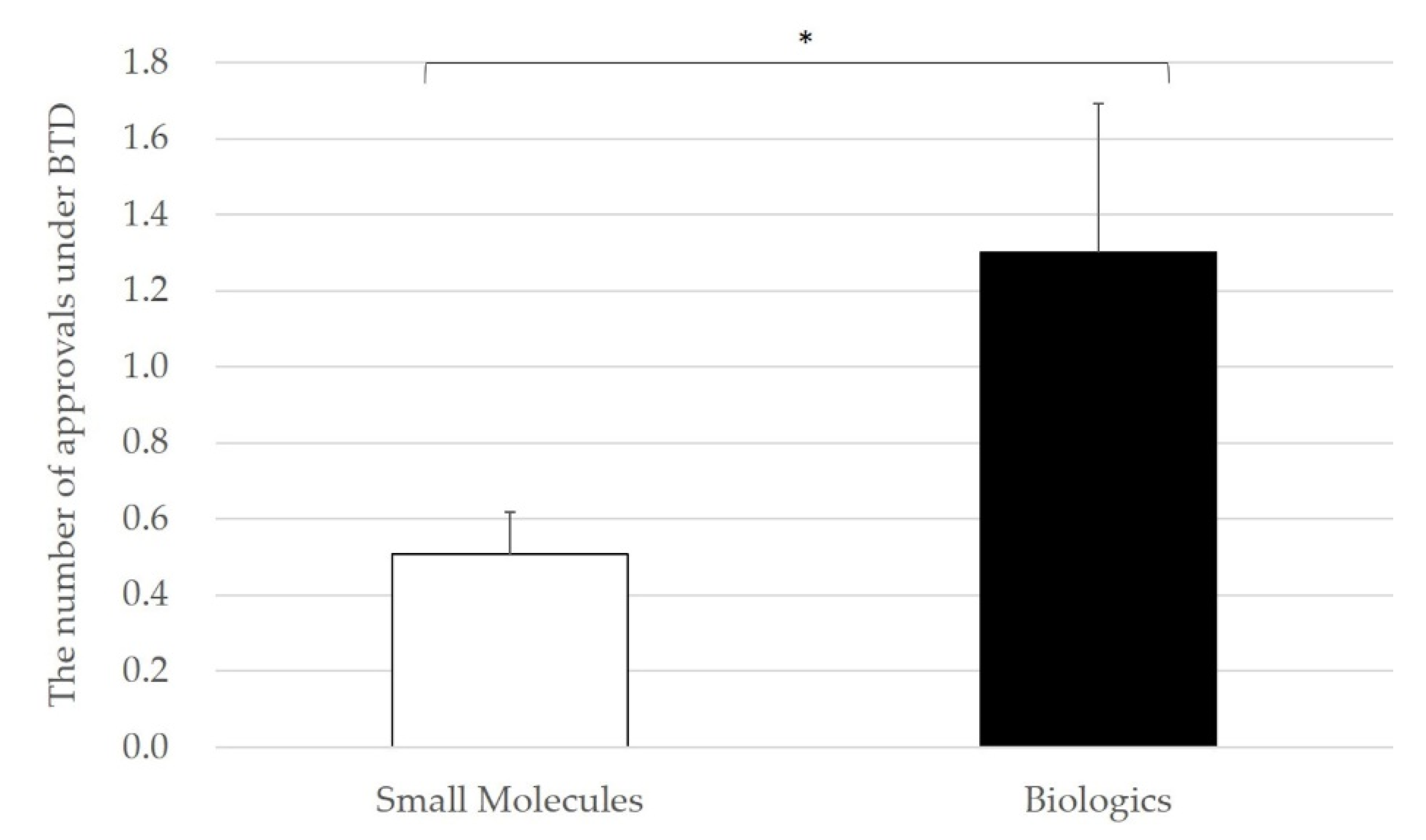

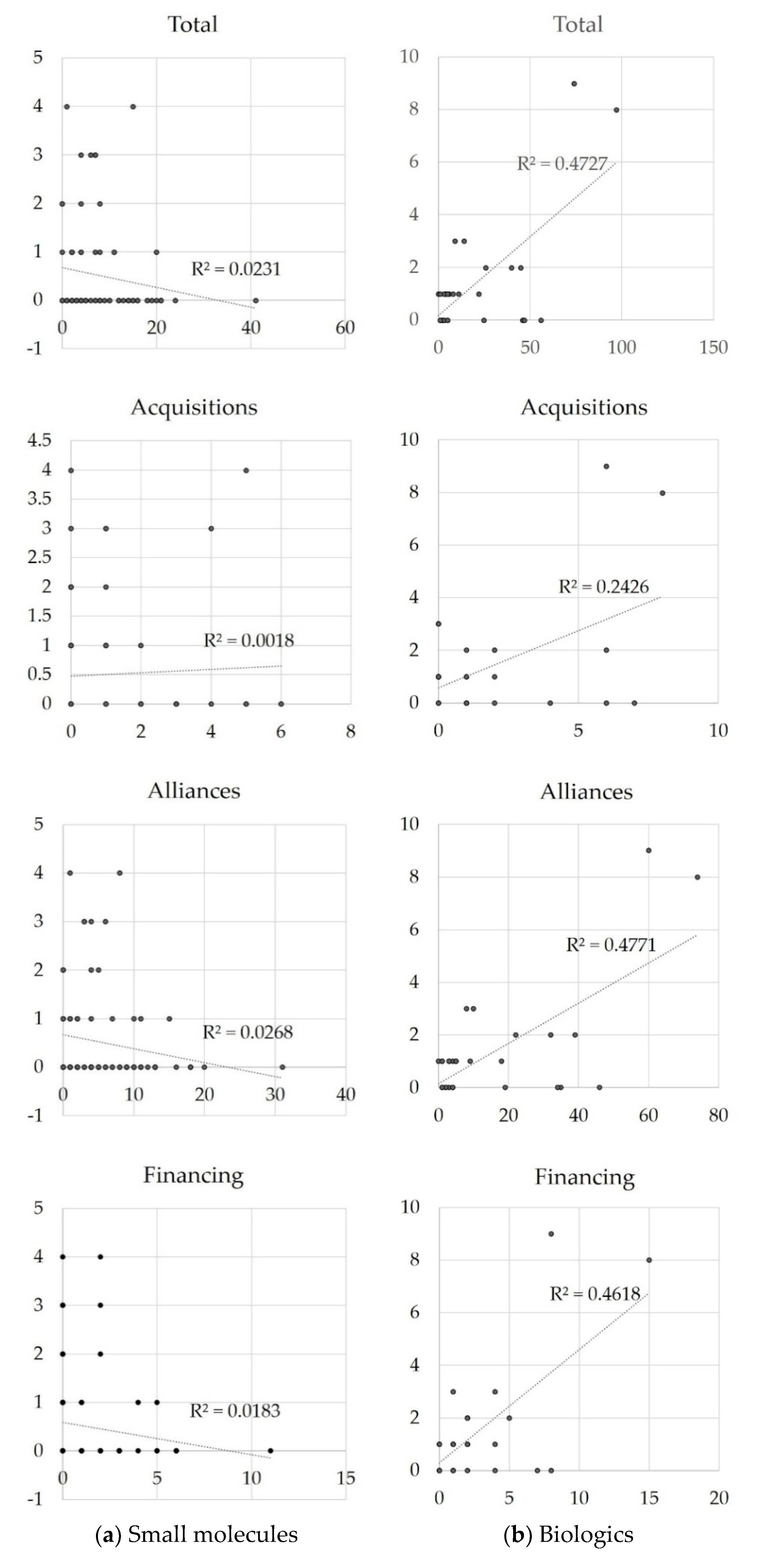

3.4. Relationship between Inter-Firm Transactions and Approved Indication under BTD

4. Discussion

5. Conclusions and Implications

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Kola, I.; Landis, J. Can the pharmaceutical industry reduce attrition rates? Nat. Rev. Drug Discov. 2004, 3, 711–715. [Google Scholar] [CrossRef]

- DiMasi, J.A.; Hansen, R.W.; Grabowski, H.G. The price of innovation: New estimates of drug development costs. J. Health Econ. 2003, 22, 151–185. [Google Scholar] [CrossRef]

- Adams, C.P.; Van Brantner, V. Market watch: Estimating the cost of new drug development: Is it really $802 million? Health Aff. 2006, 25, 420–428. [Google Scholar] [CrossRef] [PubMed]

- Kondo, H.; Hata, T.; Ito, K.; Koike, H.; Kono, N. The Current Status of Sakigake Designation in Japan, PRIME in the European Union and Breakthrough Therapy Designation in the United States. Ther. Innov. Regul. Sci. 2017, 51, 51–54. [Google Scholar] [CrossRef] [PubMed]

- Muensterman, E.T.; Luo, Y.; Parker, J.M. Breakthrough Therapy, PRIME and Sakigake: A Comparison Between Neuroscience and Oncology in Obtaining Preferred Regulatory Status. Ther. Innov. Regul. Sci. 2020, 54, 658–666. [Google Scholar] [CrossRef]

- Carroll, G.P.; Srivastava, S.; Volini, A.S.; Piñeiro-Núñez, M.M.; Vetman, T. Measuring the effectiveness and impact of an open innovation platform. Drug Discov. Today 2017, 22, 776–785. [Google Scholar] [CrossRef] [PubMed]

- Chesbrough, H.W. Open Innovation for Creating and Profiting from Technology; Harvard Business Review Press: Cambridgde, MA, USA, 2003. [Google Scholar]

- Gassmann, O.; Ellen, E.; Chesbrough, H. The future of open innovation. R D Manag. 2010, 40, 213–221. [Google Scholar] [CrossRef]

- Dries, L.; Pascucci, S.; Török, Á.; Tóth, J. Keeping your secrets public? Open versus closed innovation processes in the hungarian wine sector. Int. Food Agribus. Manag. Rev. 2014, 17, 147–162. [Google Scholar]

- Chiang, Y.H.; Hung, K.P. Exploring open search strategies and perceived innovation performance from the perspective of inter-organizational knowledge flows. R D Manag. 2010, 40, 292–299. [Google Scholar] [CrossRef]

- Mazzola, E.; Bruccoleri, M.; Perrone, G. The effect of inbound, outbound and coupled innovation on performance. Int. J. Innov. Manag. 2012, 16. [Google Scholar] [CrossRef]

- Mazzola, E.; Bruccoleri, M.; Perrone, G. Open innovation and firms’ performance: State of the art and empirical evidences from the bio-pharmaceutical industry. Int. J. Technol. Manag. 2016, 70, 109–134. [Google Scholar] [CrossRef]

- Demirbag, M.; Ng, C.-K.; Tatoglu, E. Performance of Mergers and Acquisitions in the Pharmaceutical Industry: A Comparative Perspective. Multinatl. Bus. Rev. 2007, 15, 41–62. [Google Scholar] [CrossRef]

- Munos, B. Lessons from 60 years of pharmaceutical innovation. Nat. Rev. Drug Discov. 2009, 8, 959–968. [Google Scholar] [CrossRef]

- Lamattina, J.L. The impact of mergers on pharmaceutical R&D. Nat. Rev. Drug Discov. 2011, 10, 559–560. [Google Scholar] [CrossRef] [PubMed]

- Schuhmacher, A.; Germann, P.-G.; Trill, H.; Gassmann, O. Models for open innovation in the pharmaceutical industry. Drug Discov. Today 2013, 18, 1133–1137. [Google Scholar] [CrossRef]

- Dahlander, L.; Gann, D.M. How open is innovation? Res. Policy 2010, 39, 699–709. [Google Scholar] [CrossRef]

- Lazonick, W.; Tulum, Ö. US biopharmaceutical finance and the sustainability of the biotech business model. Res. Policy 2011, 40, 1170–1187. [Google Scholar] [CrossRef]

- Wang, L.; Plump, A.; Ringel, M. Racing to define pharmaceutical R&D external innovation models. Drug Discov. Today 2015, 20, 361–370. [Google Scholar] [CrossRef]

- DiMasi, J.A.; Feldman, L.; Seckler, A.; Wilson, A. Trends in risks associated with new drug development: Success rates for investigational drugs. Clin. Pharmacol. Ther. 2010, 87, 272–277. [Google Scholar] [CrossRef] [PubMed]

- Bianchi, M.; Cavaliere, A.; Chiaroni, D.; Frattini, F.; Chiesa, V. Organisational modes for Open Innovation in the bio-pharmaceutical industry: An exploratory analysis. Technovation 2011, 31, 22–33. [Google Scholar] [CrossRef]

- Kinch, M.S.; Griesenauer, R.H. 2018 in review: FDA approvals of new molecular entities. Drug Discov. Today 2019, 24, 1710–1714. [Google Scholar] [CrossRef]

- Chen, L.; Han, X. Anti-PD-1/PD-L1 therapy of human cancer: Past, present, and future Find the latest version. J. Clin. Investig. 2015, 125, 3384–3391. [Google Scholar] [CrossRef] [PubMed]

- Nishijima, T.F.; Shachar, S.S.; Nyrop, K.A.; Muss, H.B. Safety and Tolerability of PD-1/PD-L1 Inhibitors Compared with Chemotherapy in Patients with Advanced Cancer: A Meta-Analysis. Oncologist 2017, 22, 470–479. [Google Scholar] [CrossRef] [PubMed]

- Drugs@FDA: FDA-Approved Drugs. Available online: https://www.accessdata.fda.gov/scripts/cder/daf/ (accessed on 20 July 2019).

- Merrifield, R.B. Solid Phase Peptide Synthesis. I. The Synthesis of a Tetrapeptide. J. Am. Chem. Soc. 1963, 85, 2149–2154. [Google Scholar] [CrossRef]

- Schreiber, S.L. Target-oriented and diversity-oriented organic synthesis in drug discovery. Science 2000, 287, 1964–1969. [Google Scholar] [CrossRef]

- Bleicher, K.H.; Böhm, H.J.; Müller, K.; Alanine, A.I. Hit and lead generation: Beyond high-throughput screening. Nat. Rev. Drug Discov. 2003, 2, 369–378. [Google Scholar] [CrossRef]

- DiMasi, J.A.; Grabowski, H.G. The cost of biopharmaceutical R&D: Is biotech different? Manag. Decis. Econ. 2007, 28, 469–479. [Google Scholar] [CrossRef]

- Carter, P.J. Potent antibody therapeutics by design. Nat. Rev. Immunol. 2006, 6, 343–357. [Google Scholar] [CrossRef]

- Huang, S.; Armstrong, E.A.; Benavente, S.; Chinnaiyan, P.; Harari, P.M. Dual-agent molecular targeting of the epidermal growth factor receptor (EGFR): Combining anti-EGFR antibody with tyrosine kinase inhibitor. Cancer Res. 2004, 64, 5355–5362. [Google Scholar] [CrossRef]

- Hay, M.; Thomas, D.W.; Craighead, J.L.; Economides, C.; Rosenthal, J. Clinical development siccess rates for investigational drugs. Nat. Biotechnol. 2014, 32, 40–51. [Google Scholar] [CrossRef]

- Schuhmacher, A.; Gassmann, O.; Hinder, M. Changing R&D models in research-based pharmaceutical companies. J. Transl. Med. 2016, 14, 1–11. [Google Scholar] [CrossRef]

- Imai, K.; Takaoka, A. Comparing antibody and small-molecule therapies for cancer. Nat. Rev. Cancer 2006, 6, 714–727. [Google Scholar] [CrossRef]

- DiMasi, J.A.; Grabowski, H.G.; Hansen, R.W. Innovation in the pharmaceutical industry: New estimates of R&D costs. J. Health Econ. 2016, 47, 20–33. [Google Scholar] [CrossRef] [PubMed]

- Calfee, J.E.; DuPré, E. The emerging market dynamics of targeted therapeutics. Health Aff. 2006, 25, 1302–1308. [Google Scholar] [CrossRef] [PubMed]

- CenterWatch. Available online: https://www.centerwatch.com/directories/1067-fda-approved-drugs (accessed on 20 July 2019).

- Breakthrough Therapy Approvals. Available online: https:https://www.fda.gov/drugs/nda-and-bla-approvals/breakthrough-therapy-approvals (accessed on 20 September 2019).

- Strategic Transactions. Available online: https://www.pharmamedtechbi.com/search (accessed on 26 July 2019).

- ClinicalTrials. Available online: https://clinicaltrials.gov/ (accessed on 1 November 2019).

- Pisano, G. Science Business: The Promise, the Reality and the Future of Biotech; Harvard Business School Press: Cambridge, MA, USA, 2006. [Google Scholar]

- Makino, T.; Lim, Y.; Kodama, K. Strategic R&D transactions in personalized drug development. Drug Discov. Today 2018, 23, 1334–1339. [Google Scholar] [CrossRef] [PubMed]

- Makino, T.; Sengoku, S.; Ishida, S.; Kodama, K. Trends in interorganizational transactions in personalized medicine development. Drug Discov. Today 2019, 24, 364–370. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Original Approval Year | Brand Name | Generic Name | +5y | +4y | +3y | +2y | +1y | App | −1y | −2y | −3y | −4y | −5y |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Small Molecules | |||||||||||||

| 2018 | VITRAKVI | LAROTRECTINIB | NA | NA | NA | NA | NA | 0 | 6 | 0 | 0 | 0 | 1 |

| 2018 | COPIKTRA | DUVELISIB | NA | NA | NA | NA | NA | 6 | 2 | 1 | 0 | 1 | 0 |

| 2017 | ZEJULA | NIRAPARIB | NA | NA | NA | NA | 4 | 6 | 5 | 1 | 1 | 1 | 1 |

| 2012 | XTANDI | ENZALUTAMIDE | 0 | 6 | 3 | 3 | 2 | 0 | 0 | 0 | 1 | 0 | 0 |

| 2012 | ICLUSIG | PONATINIB | 3 | 5 | 3 | 6 | 1 | 0 | 1 | 1 | 0 | 0 | 0 |

| 2004 | TARCEVA | ERLOTINIB HYDROCHLORIDE | 4 | 5 | 5 | 2 | 2 | 1 | 2 | 1 | 1 | 0 | 0 |

| Biologics | |||||||||||||

| 2017 | BAVENCIO | AVELUMAB | NA | NA | NA | NA | 7 | 5 | 6 | 3 | 1 | 0 | 0 |

| 2017 | IMFINZI | DURVALUMAB | NA | NA | NA | NA | 8 | 4 | 1 | 10 | 2 | 0 | 0 |

| 2016 | TECENTRIQ | ATEZOLIZUMAB | NA | NA | NA | 10 | 10 | 12 | 5 | 1 | 1 | 0 | 0 |

| 2014 | KEYTRUDA | PEMBROLIZUMAB | NA | 20 | 28 | 15 | 19 | 3 | 0 | 1 | 0 | 0 | 0 |

| 2014 | OPDIVO | NIVOLUMAB | NA | 11 | 23 | 15 | 12 | 6 | 0 | 0 | 1 | 0 | 0 |

| 2013 | KADCYLA | TRASTUZUMAB EMTANSINE | 5 | 5 | 6 | 7 | 2 | 7 | 3 | 2 | 1 | 5 | 0 |

| 2011 | YERVOY | IPILIMUMAB | 7 | 7 | 5 | 1 | 1 | 4 | 0 | 1 | 0 | 0 | 2 |

| 2004 | ERBITUX | CETUXIMAB | 1 | 1 | 5 | 6 | 5 | 6 | 2 | 2 | 0 | 2 | 1 |

| 2004 | AVASTIN | BEVACIZUMAB | 1 | 2 | 2 | 8 | 2 | 2 | 1 | 2 | 0 | 0 | 0 |

| Acquisition | Alliance | Financing | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Acquisition of Private Biotech | Full Acquisition | Includes Contract | Includes Earn-outs | Intra-Biotech Deal | Payment Includes Cash | Payment Includes Stock | Reverse Acquisition | Co-Promotion | Includes Contract | Includes Equity | Includes Royalty or Profit Split Information | Intra-Biotech Deal | Marketing-Licensing | Product or Technology Swap | R&D and Marketing-Licensing | Trial Collaborations | Follow-On Public Offering | Initial Public Offering | Nonconvertible Debt | Private Investment in Public Equity | Private Placement | |

| Keytruda | 3 | 8 | 4 | 4 | 0 | 8 | 1 | 0 | 7 | 1 | 3 | 11 | 6 | 4 | 0 | 16 | 56 | 5 | 3 | 0 | 3 | 7 |

| Opdivo | 4 | 6 | 3 | 4 | 1 | 5 | 2 | 1 | 3 | 2 | 6 | 18 | 2 | 1 | 1 | 27 | 40 | 2 | 4 | 1 | 0 | 2 |

| Tecentriq | 1 | 1 | 0 | 1 | 0 | 1 | 0 | 0 | 5 | 1 | 2 | 12 | 18 | 0 | 0 | 12 | 30 | 0 | 4 | 0 | 0 | 1 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Djurian, A.; Makino, T.; Lim, Y.; Sengoku, S.; Kodama, K. Trends of Business-to-Business Transactions to Develop Innovative Cancer Drugs. Sustainability 2020, 12, 5535. https://doi.org/10.3390/su12145535

Djurian A, Makino T, Lim Y, Sengoku S, Kodama K. Trends of Business-to-Business Transactions to Develop Innovative Cancer Drugs. Sustainability. 2020; 12(14):5535. https://doi.org/10.3390/su12145535

Chicago/Turabian StyleDjurian, Arisa, Tomohiro Makino, Yeongjoo Lim, Shintaro Sengoku, and Kota Kodama. 2020. "Trends of Business-to-Business Transactions to Develop Innovative Cancer Drugs" Sustainability 12, no. 14: 5535. https://doi.org/10.3390/su12145535

APA StyleDjurian, A., Makino, T., Lim, Y., Sengoku, S., & Kodama, K. (2020). Trends of Business-to-Business Transactions to Develop Innovative Cancer Drugs. Sustainability, 12(14), 5535. https://doi.org/10.3390/su12145535