Through these subclasses, it was possible to group the buildings located in the considered area into five clusters: n°1 including the mini tower type building units, n°2 grouping those of the tower type, n°3 concerning those of the “in line 2 stairs” type, n°4 consisting of those of the “In Line 3 Stairs” type, and n°5 involving those of the inclined 2 stairs type.

The searched website does not allow users to filter one energy rate in particular, but the query mask groups energy efficiency classes into three different categories: “high”, “medium”, or “low”, clustering together A, A+, A1, A2, A3, A4 classes; B, C, D classes; and also E, F, G classes respectively. Therefore, three separate searches were carried out (according to the elected energy rated) and the obtained results were analyzed to trace back the prevailing energy rating of the properties for sale in the selected area. Specifically, twenty-five matches were identified, of which nine did not specify their energy rating, fourteen fell into the “low” class, and two into the “medium” class, so it was considered correct to assume the reference energy rating of the properties in the Fiat Village was the “F”.

2.1. Description of the Intervention to Be Carried Out

The Fiat Village in Settimo Torinese is a typical example of postwar European residential district. By now, it consists of buildings that are over half a century old and thus at the end of their (supposed) service life, battling with outdated performances, vulnerability, lexical poverty, living discomfort, and decreasing value.

Among several European renovation-based experiences on postwar neighborhoods, a particular systemic and multibenefit approach (that is to say functional-, performance-, and look-based, etc.) on buildings’ envelope retrofitting has been consolidated, because it can better convey adaptive and subject-oriented works as well. This kind of approach suits particularly the Fiat Village district where the large-scale intervention not only updates each building’s energy performance, but also enhances the whole environmental sustainability in addition to an added value to environmental quality.

The original envelope of Fiat Village buildings consists of a traditional cavity masonry wall with brick texture veneer. The backup wall (inner layer) and veneer (outer layer) are almost independent of each other and separated by a cavity generally used to host the central heating piping and the plumbing system. Partial recladding of these existing fronts can keep the building usage ongoing during retrofit intervention and it can be considered an optimal strategy for these kinds of facades. The recladding works are targeted to the outer layer (brick veneer) only and to a general revamping of the HVAC and plumbing systems—the opportunity to install new water piping connected to sustainable systems (e.g., solar hot water, nondrinkable water to flush water closets vs. drinkable water, etc.) could go together with the general rebuilding of the media networks (fiber link, satellite TV, cable TV, and so on), thus getting a higher value for each apartment. Thanks to the updated performance of the newly built cladding, the thermal transmittance will decrease from about 2 W/m2K (original façade) to a value approximately equal or less than 0.2 W/m2K. As mentioned before, the back wall is kept in place with some adjustments to fit new high-performance windows and facilities—floorings, plasters, and inhabitants’ space are almost fully preserved.

The renovation proposed for the Fiat Village buildings is not only limited to technological works, but more articulated in order to create new services and improve the inhabitants’ living comfort: therefore, it can be defined more broadly as a “district-scale” intervention.

In fact, an “energy community” will be established to reduce condominium areas’ electricity bills through the installation of photovoltaic panels connected to storage batteries. In addition, the existing lighting system will be LED upgraded, replacing the existing condominium lights and installing new lightings in the outdoor areas for security reasons, as well the fact that access to each condominium will be controlled by way of new car access bars and a new video entry system.

The services for residents will be strongly enhanced by new spaces dedicated to personal services in which each family will be able to receive medical advice at any time of the day, a new condominium car sharing service, a new e-commerce point (Amazon, Ebay, etc.) to facilitate the delivery of users’ orders, a new Wi-Fi ultra-speed network for each building, and a single contract with an Italian energy marketing company to properly sell the energy overproduced by photovoltaic panels.

2.2. Summary of the Research

The price of each estate depends directly on its reference market (RM), which in turn is conditioned by supply/demand circumstances for similar goods in that specific area.

The graph reported in

Figure 5 represents the trend of the deflated house price index (HPI) about residential properties purchased by households, both newly built and existing ones. The reported values show the real increase or decrease in the values of these goods because they were stripped out by the consumer price inflation. As it is possible to see, between 2008 and 2014, the real estate bubble that originated in the United States caused a decreasing trend; then, in 2015 the house prices began to increase more than the inflation, and this trend is still ongoing. However, this graph shows an average trend of the residential market in all the states in the Eurozone; in some countries the situation can be quite different—in 2018, for example, Hungary recorded an increase of 10.9%, whereas Italy suffered a decrease of 1.5% in the same period (

Figure 6).

As far as the town of Turin is concerned, we processed the data provided by various sources (Estate Consultant, Real Estate Market Observatory, etc.) and we calculated their constant value, i.e., inflation-purged, referring to the year 2000 (year after the entry into force of the new Euro currency in financial markets). In this way, it was possible to reconstruct the trend of the reference market for new or renovated houses.

Figure 7 shows this price has been subject to significant fluctuations over the years, the most recent of them from 2007 up until today. On that date (2007), the price of new or renovated homes was about €2450.00 per sqm of sale area, but, due to the crisis that began in the USA with the real estate bubble deflation, this price fell down in 2017 to a minimum of about €1600.00 per square meter (euro at year 2000). Since then, a slow lost value recovery phase has begun; perhaps, from a slightly optimistic point of view, it is possible to estimate that in 2021 the price of houses will be around 1700.00 €/sqm (expressed still in euro at year 2000).

The Fiat Village is located in a municipality in the first metropolitan belt of Turin, and therefore, the specific trend of the real estate market in this area has been traced. To do this, data collected in the Quotation Database of the Real Estate Market Observatory (QD REMO, that in Italy is known as “Data Base OMI”) were used, because in Italy these data are managed by the Inland Revenue (IR), that is a public body (known as “Agenzia delle Entrate” [

17]) directly connected with the Ministry of Economy and Finance, so they have a good level of reliability.

Before going deeper into values and trends, it is useful to explain some general information on how this database gets updated.

The basis to set-up and update the QD REMO are the survey forms collecting information on the real estate market. They are divided into territorial or market areas according to the data recorded. Indeed, in the former, municipality and zone features influencing the market are reported, while in the latter, economic data of the real estate units are collected [

18].

In particular, the municipality form reports the town’s population, the territorial position, the level of connecting facilities, and transportations besides its attractiveness according to the town’s historical, tourist, and naturalistic interests, as well as agricultural, commercial, or industrial importance. The zone form, on the other hand, reports the main aspects and peculiarities that influence the market values of sales and rentals in a specific homogeneous area of that municipality. Instead, the market form on the real estate unit reports an aggregation of information about both the whole building and the unit [

18]. The surveyor must fill all these forms during the direct surveys he has carried out periodically, following the indications of the appropriate operational guide. In this way, a detailed survey of sales and rentals in a homogeneous zone is obtained, providing also the description of the building units’ features that are necessary for this study [

18]. The set of survey forms acquired in each homogeneous market zone constitutes and feeds up continuously the database of the QD REMO.

Table 1 shows the mandatory fields in the survey forms according to the type of building units to be reviewed. Indeed, there are four categories of data that must be studied in any survey: the general data, in which the surveyor and the survey object are clearly identified; the data about the building, in which there are data overviewing the surrounding area and all the amenities that are or are not present near the building; the data on the real estate unit, describing its main features like the number of rooms or the floor level, etc.; the economic data reporting the total area of the building unit and its sales price or its estimated value or how much money the owner is requiring.

The annex of QD REMO contains the standardized survey forms for building units in the various building types. In particular, this annex reports the features to be evaluated in order to define the overall maintenance level of the building and the real estate unit, respectively. The building maintenance status is defined observing the state of the following items: façade, windows and doors, cladding and plaster in the common areas, atrium floors, stairs and common areas, lifts, intercoms and video intercom systems, electrical system, centralized HVAC system, sewerage and plumbing system. The real estate maintenance level must be assessed on the condition of floors, ceilings and wall claddings, internal and external windows and doors, electric installation, waterworks, heating and air conditioning systems, sanitary fittings, and alarm systems. Both as far as the maintenance state of the buildings and the real estate units are concerned, a synthetic evaluation must be given according to the number of features that are judged to be in good condition—“excellent” if there are at least eight, “normal” if there are at least five, “poor” when there are up to four [

18].

The information acquiring activity in the surveys is carried out in collaboration with primary information sources, but the collection, use, and validation of all the data are the exclusive responsibility of the IR. According to the provisions of the manual, REMO’s surveyor must accurately know the object of the survey and, therefore, the features of the building and its territorial surroundings must be recognized and verified through ICT tools. Moreover, the surveyor cannot run an inspection in a virtual mode exclusively, reviewing the building through the use of existing databases such as Google Maps, Bing, and others [

18].

The REMO half-yearly quotations (freely available online from the first half of 2006) derive from the processing of the above-mentioned data. The quotations identify in each specific homogeneous territorial zone (REMO’s zone) of each municipality, a minimum and maximum range of sales and rental unit prices, through the building type and state of conservation. This range of values refers to ordinary buildings. Therefore, the properties of particular value or deterioration or which in any case do not have ordinary characteristics compared to the buildings in the same area are excluded. For the same type of building more than one state of conservation can be detected; in this case, the prevailing one shall be in any case specified. It should also be noted that for shops and shopping centers, the ratings “excellent”, “normal”, and “poor” rely upon the commercial position and not on the conservation state of the building unit, because their market does not show any significant difference in appreciation of the different states of conservation.

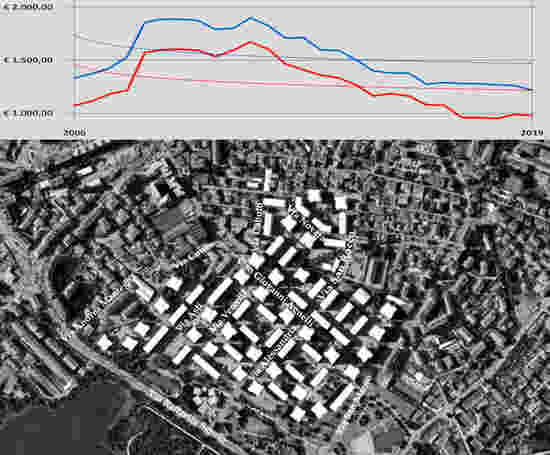

The buildings under analysis are situated in a “semi-central” area (as defined by REMO) of Settimo Torinese and they are intended for residential use with generally good condition of maintenance—their reference market value was identified on this basis. Indeed, entering these data and questioning into the QD REMO, we obtained the parametric market values range for both civil dwelling (CD) and low-cost dwelling (LCD) in each half-year starting from 2006. The typical CD unit is a private flat that is part of a building with good general construction and layout characteristics. A CD is part of a residential building with a significant value of the finishing works (floorings, coverings, fixtures, and plants) and it generally has rational layout characteristics with a good architectural level. Instead, the typical LCD is a private housing unit that is part of a residential complex with coarse external finishes without valuable elements [

19,

20].

In order to trace back to 2006 using the historical data series published in the QD REMO, we turned them from current values to constant values, i.e., stripping out the inflation. Therefore, the values have been restored to the first half of 2006 using the consumer price indexes for blue-collar and white-collar households (in Italy: FOI) provided by the Central Institute of Statistics (ISTAT). The market trends of the CD and of the LCD for the case-study area are shown in

Figure 8.

The information made available by a locally operating real estate brokerage company was processed through a direct estimation method for each type of estate to determine the preintervention average selling price per square meter of commercial area (PI-ASP). This brokerage company provided data about Fiat Village properties’ sales, which occurred between 1999 and 2018: the final global sale price; the location of the estate (address, floor number), and its state of conservation (original, partially renovated, completely renovated); the number of rooms; the commercial surface area; the year of selling; and the final sale price per square meter of commercial surface area (

Figure 9,

Figure 10,

Figure 11,

Figure 12,

Figure 13,

Figure 14 and

Figure 15).

In this case too, sale prices per square meter of commercial area were stripped out of inflation and referred to the year 2006 using FOI indices provided by the NSO. Looking at the graph in

Figure 16, it is easy to understand the obtained trend is similar LCD’s one, which was derived from data provided by REMO (

Figure 9). Moreover, since dwellings in the area in question mostly belong to a low-cost housing category according to Land Registry classification (A/3 in the Italian Land Registry), it was deemed correct to take LCDs as the reference market.

As mentioned before, the first research goal is to define the most likely market value for Settimo Torinese Fiat Village dwellings. At the beginning, it was supposed to estimate the PI-ASP for each cluster by means of 2018 trade-only prices mediation. However, analyzing the available data, it was noticed they were numerically too little to be significant (3 sales only); therefore, it was decided to group together all the sales data from the oldest (1999) until the most recent (2018). All these data must take into account both the average price growth owing to the inflation and the effect of the real estate market developments, in order to obtain correct values for PI-ASP. Thus, all sale prices were first stripped-out of inflation and restored to 2018 using NSO’s indices (FOI), then, they were tuned using a coefficient derived from reference market direct observation, and finally the average prices of each cluster were extrapolated. The graph in

Figure 16 shows a decreasing trend from 2006 to 2018 due to the sharp drop of dwelling sale prices.

Once this operation was carried out, the PI-ASP of each cluster was available and updatable to 2018. These values became the starting point to determine the new average sale price for each cluster, i.e., after the district energy revamping and the other planned works. In particular, it was believed real estate units’ value would increase because of both energy performance improvement (and the consequent energy cost savings) and the overall building improvement in its look and maintenance.

The multiple regression line, which is a direct multiparameter procedure to define asset market value, was used to assess the economic impact of the energy rating jump.

The regression has been widely used for a long time in real estate appraisal literature [

21,

22]. It describes the functional relationship between a dependent variable (Y, unknown) and a series of independent variables (X

i, measurable in a specific reference sample). Due to its versatility, this algorithm finds application in many fields of applied sciences, from chemistry to medicine, economic sciences, and even psychology. The generic function between Y and X

i is summarized by the following formula:

In the case of a real estate appraisal, the variable “Y” represents the price (i.e., the most probable market value), while Xi-k are the independent k-variables (the so-called intrinsic and extrinsic real estate features) and βi-K are the coefficients of regression, which represent the incidence of each single feature on the value of the asset.

Referring both to some recent literature on energy performance and housing prices in Europe and Italy [

23,

24,

25] and to the authors’ previous research (aimed at estimating energy rating incidence on property market value in very similar real estate markets to the one of this survey), it was possible to approximate each energy rating upgrade increase of about 2% the estate value (R

2 = 0.734542312; adjusted R

2 = 0.687970788, both significant in real estate applications).

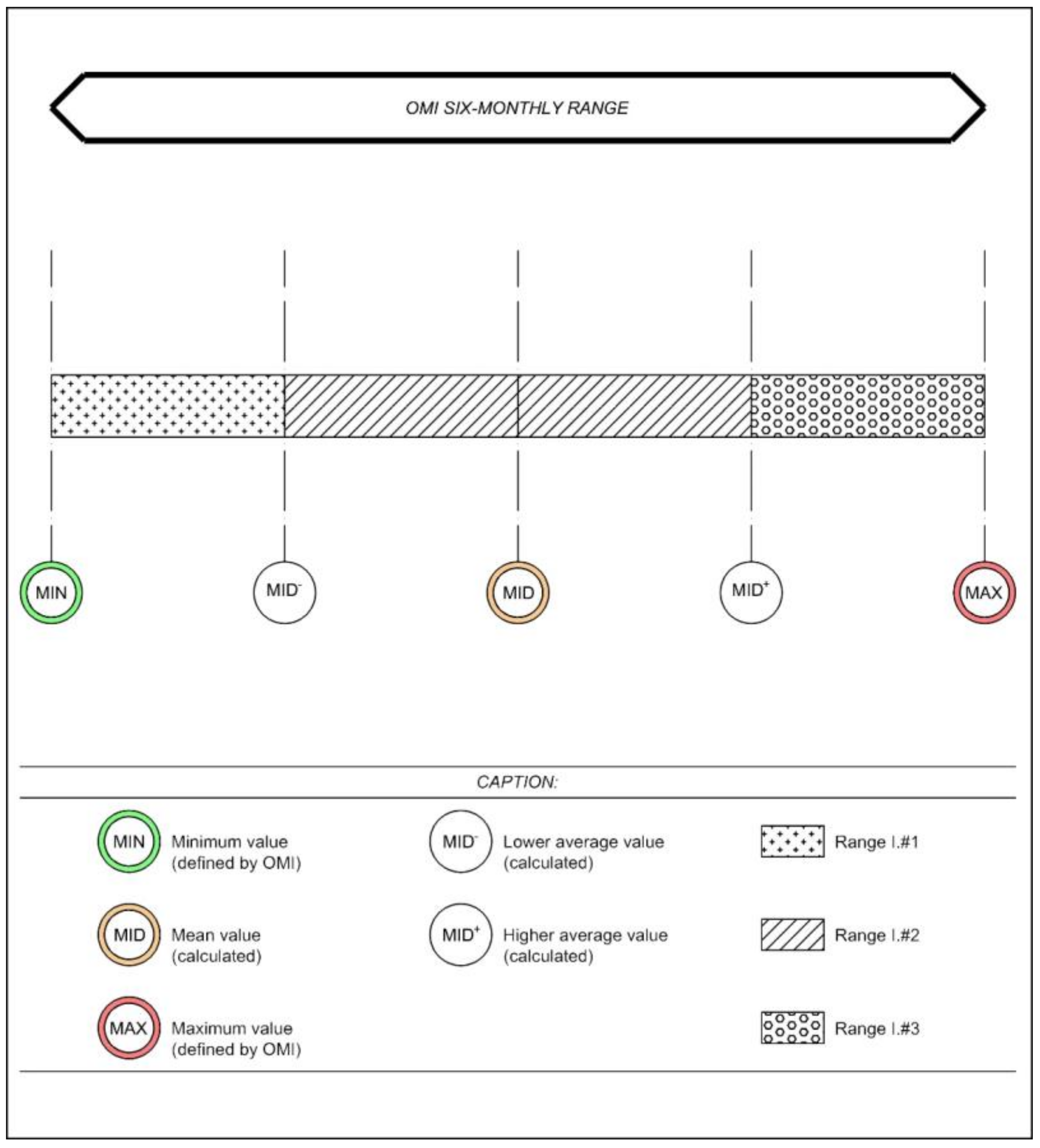

Moreover, as mentioned before, it is expected that planned works will also lead buildings to a preservation and maintenance improvement, which will increase the dwellings’ value. However, since no works inside the flats were planned in this district intervention, it is believed there won’t be any upgrade in land registry category (that generally changes every time there is substantial intervention on internal finishes and facilities) and therefore REMO’s reference class will remain the same (LCD). This class range has been split into three subranges to better estimate the appreciation in value of general conditions of improvement in terms of preservation and maintenance. The first subrange (I#1) has got the same lower limit as the minimum value of REMO’s, while the upper limit corresponds to the average value between the minimum and the average value of the REMO’s range itself. The second subrange (I#2) is the wider one: it has got a central value corresponding to the average of REMO’s range, a lower limit resulting from the average between the minimum value and the average value of REMO’s range itself, while the upper limit is the average between the maximum and the average value of REMO’s range itself. Lastly, the third subrange (I#3) has got an upper limit corresponding to the maximum value of REMO’s range and a lower limit resulting from the average between the average value and the maximum value of REMO’s range (

Figure 17).

The survey on buildings’ states of maintenance and preservation was carried out through a virtual inspection via Google Street View tool and two physical inspections in the months of September–October 2019. No relevant signs of significant degradation pathologies on preintervention buildings facades were noticed. Therefore, the right reference subrange (as above defined) would be the second one (I#2). This statement was also validated by the fact the PI-ASP value above calculated remains within this range and is very close to its average value.

As described before, the works will concern mainly façades, doors, and windows in the common parts; the heating systems; and the intercom/video systems. For each flat it can be therefore considered reasonable that there would be an appreciation in value due to an improvement on buildings state and “outer” maintenance. This will at least lead them to have as a reference price the average value of the I#3 subrange. This value increase was added to the one we got from energy rating upgrade to calculate the cluster postintervention average selling price (POI-ASP) per square meter of commercial area.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}