How Do Venture Capitals Build Up Syndication Ecosystems for Sustainable Development?

Abstract

1. Introduction

2. Theory

2.1. Networks, Ecosystem and Sustainable Development

2.2. Sustainable Project Investments and Ecosystems

3. Method

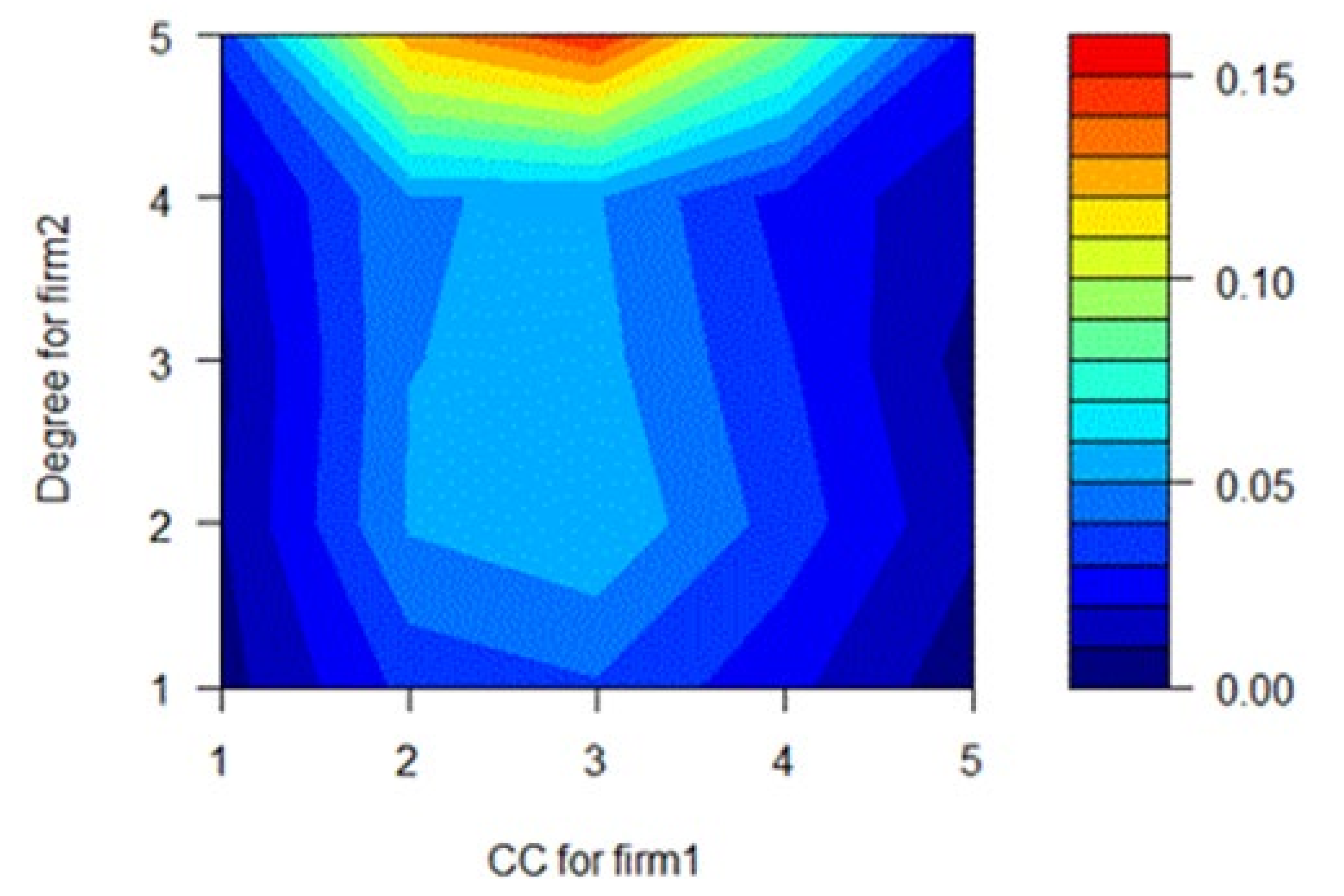

3.1. Modeling

3.2. Data Collection and Measures

- The previous syndication number is a variable to measure the number of joint investments between two nodes during the period 2000–2010.

- The relationship distance is measured by the Euclidean distance between two nodes in the industrial network formed from 2000 to 2010.

- The common neighbor is a measurement of the number of common neighbors between two VCs before 2010.

- The centrality–structural hole effect indicates the effect size, in the network during 2000–2010, of a selected VC who has syndication ties, during 2011–2013, with a leader ranking in the top 20% for degree centrality.

- The centrality–cluster coefficient effect indicates the clustering coefficient, in the network during 2000–2010, of a selected VC who has syndication ties, during 2011–2013, with a leader ranking in the top 20% for degree centrality.

4. Data Analyses and Results

5. Discussion and Future Directions

5.1. Syndication Circle: An Investment Ecosystem for Sustainable Development

- 1st level: frequent cooperation partners (core circle);

- 2nd level: occasional cooperation partners (peripheral circle).

- 3rd level: indirect ties with VCs that have high brokerage benefits (H2) or medium CC value (H3); (outer-circle partners for the future).

5.2. Nurturing an Investment Ecosystem

- Frequent cooperation partners help generate stable revenue. We call this strategy relational embeddedness.

- VCs can quickly build up mutual trust with weak-tie partners who can help reach many other VCs who otherwise have no common neighbors with the focal VC. Firms will use this strategy to quickly expand their current business landscape by finding some new partners through their strong- or weak-tie partners.

- Focal firms have to think about partners that are not in their current circle for future business growth, to hunt for business opportunities throughout the broader network, not just within their immediate network [5,55]. Bigger VCs tend to search for small players in bridging positions or those that represent a clique, as these firms possess a significant amount of resources that are beneficial to the focal firm. Focal firms need to maintain indirect connections with these “outsider” VCs and explore opportunities for future growth.

5.3. Contributions and Practical Implications for the Investment Ecosystem

5.4. Limitations and Future Directions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Davis, J.P. The group dynamics of inter-organizational relationships collaborating with multiple partners in innovation ecosystems. Admin. Sci. Q. 2016, 61, 621–661. [Google Scholar] [CrossRef]

- Umit, C.; Bilal, A. Big social network data and sustainable economic development. Sustainability 2019, 11, 2027. [Google Scholar]

- Chen, Y.S.; Lei, H.S.; Hsu, W.C. A Study on the sustainable development strategy of firms: Niche and social network theory. Sustainability 2019, 11, 2593. [Google Scholar] [CrossRef]

- Gomes, L.A.D.V.; Facin, A.L.F.; Salerno, M.S.; Ikenami, R.K. Unpacking the innovation ecosystem construct: Evolution, gaps, and trends. Technol. Soc. 2016, 136, 30–48. [Google Scholar] [CrossRef]

- Cumming, D.; Henriques, I.; Sadorsky, P. ‘Cleantech’ venture capital around the world. Int. Rev. Financ. Anal. 2016, 44, 86–97. [Google Scholar] [CrossRef]

- Buerer, M.J.; Wuestenhagen, R. Which renewable energy policy is a venture capitalist’s best friend? Empirical evidence from a survey of international cleantech investors. Energy Policy 2009, 37, 4997–5006. [Google Scholar] [CrossRef]

- Brander, J.A.; Amit, R.; Antweiler, W. Venture capital syndication: Improved venture selection vs. the value-added hypothesis. J. Econ. Manag. Strat. 2002, 11, 422–452. [Google Scholar] [CrossRef]

- Bygrave, W.D. Syndicated investments by venture capital firms: A networking perspective. J. Bus. Ventur. 1987, 2, 139–154. [Google Scholar] [CrossRef]

- Gu, W.; Luo, J.; Liu, J. Exploring Small-World Network with an Elite-Clique: Bringing Embeddedness Theory into the Dynamic Evolution of a Venture Capital Network. Soc. Netw. 2018, 57, 70–81. [Google Scholar] [CrossRef]

- Burt, R.S.; Burzynska, K. Chinese entrepreneurs, social networks, and guanxi. Manag. Organ. Rev. 2017, 13, 221–260. [Google Scholar] [CrossRef]

- Chen, X.P.; Chen, C.C. On the intricacies of the Chinese guanxi: A process model of guanxi development. Asia Pac. J. Manag. 2004, 21, 305–324. [Google Scholar] [CrossRef]

- Burt, R.S. People you know. In Neighbor Networks—Competitive Advantage Local and Personal; Oxford University Press: New York, NY, USA, 2010; pp. 1–18. [Google Scholar]

- Bruton, G.D.; Ahlstrom, D. An institutional view of China’s venture capital industry: Explaining differences between China and the west. J. Bus. Ventur. 2003, 18, 233–259. [Google Scholar] [CrossRef]

- Gulati, R. Network location and learning: The influence of network resources and firm capabilities on alliance formation. Strateg. Manag. J. 1999, 20, 397–420. [Google Scholar] [CrossRef]

- Ter Wal, A.L.J.; Alexy, O.; Block, J.; Sandner, P.G. The best of both worlds: The benefits of open-specialized and closed-diverse syndication networks for new ventures’ success. Admin. Sci. Q. 2016, 61, 393–432. [Google Scholar] [CrossRef] [PubMed]

- Zhang, L.; Gupta, A.K.; Hallen, B.L. The conditional importance of prior tie: A group-level analysis of venture capital syndication. Acad. Manag. J. 2017, 60, 1360–1386. [Google Scholar] [CrossRef]

- Luo, J. Guanxi Revisited: An Exploratory Study of Familiar Ties in a Chinese Workplace. Manag. Organ. Rev. 2011, 7, 329–351. [Google Scholar] [CrossRef]

- Rossi, M.; Martini, E. Venture capitalists and value creation: The role of informal investors in the growth of smaller European firms. Int. J. Glob. Small Bus. 2019, 3, 233–247. [Google Scholar] [CrossRef]

- Rossi, M.; Festa, G.; Fiano, F.; Giacobbe, R. To invest or to harvest? Corporate venture capital ambidexterity for exploiting/exploring innovation in technological business. Bus. Process Manag. J. 2019. [Google Scholar] [CrossRef]

- Powell, W.D.; White, D.R.; Koput, K.W.; Owen-Smith, J. Network dynamics, and field evolution: The growth of inter-organizational collaboration in the life sciences. Am. J. Sociol. 2005, 110, 1132–1205. [Google Scholar] [CrossRef]

- Granovetter, M. Introduction: Problems of explanation in economic sociology. In Society and Economy—Framework and Principles; Harvard University Press: Cambridge, MA, USA, 2017; pp. 1–26. [Google Scholar]

- Holmstrom, B. Moral hazard in teams. Bell J. Econ. 1982, 13, 324–340. [Google Scholar]

- Tykvov’a, T. Who chooses whom? Syndication, skills, and reputation. Annu. Rev. Financ. Econ. 2007, 16, 5–28. [Google Scholar] [CrossRef]

- Marcela, P. Management control systems in joint ventures: Literature review and description of three cases. Int. J. Manag. Financ. Acc. 2013, 5, 45–63. [Google Scholar]

- Jamel, C.; Habib, A.; Younes, B. Characteristics of the board of directors and involvement in innovation activities: A cognitive perspective. Int. J. Manag. Financ. Acc. 2010, 2, 240–255. [Google Scholar]

- Sorenson, O.T.; Stuart, E. Syndication networks and the spatial distribution of venture capital investments. Am. J. Sociol. 2001, 106, 1546–1588. [Google Scholar] [CrossRef]

- Hochberg, Y.V.; Ljungqvist, A.; Lu, Y. Whom you know matters: Venture capital networks and investment performance. J. Financ. 2007, 62, 251–301. [Google Scholar] [CrossRef]

- Stacey, R.D.; Griffin, D.; Shaw, P. Complexity and human action. In Complexity and Management; Routledge: New York, NY, USA, 2000; pp. 157–181. [Google Scholar]

- Padgett, J.F.; Powell, W.W. Introduction: The problem of emergence. In The Emergence of organizations and markets. Princeton University Press: Princeton, NJ, USA, 2012; pp. 4–30. [Google Scholar]

- Rong, K.; Hu, G.; Lin, Y.; Shi, Y.; Guo, L. Understanding business ecosystem using a 6C framework in Internet-of-Things-based sectors. Int. J. Prod. Econ. 2015, 159, 41–55. [Google Scholar] [CrossRef]

- Ahuja, G.; Soda, G.; Zaheer, A. The genesis and dynamics of organizational networks. Organ. Sci. 2012, 23. [Google Scholar] [CrossRef]

- Beckman, C.M.; Haunschild, P.R.; Phillips, D.J. Friends or strangers? Firm-specific uncertainty, market uncertainty, and network partner selection. Organ. Sci. 2004, 15, 259–275. [Google Scholar] [CrossRef]

- Polidoro, F.; Ahuja, G.; Mitchell, W. When the social structure overshadows competitive incentives: The effects of network embeddedness on joint venture dissolution. Acad. Manag. J. 2011, 54, 203–223. [Google Scholar] [CrossRef]

- Rowley, T.J.; Greve, H.R.; Rao, H.; Baum, J.A.C.; Shipilov, A.V. Time to break up: Social and instrumental antecedents of firm exits from exchange cliques. Acad. Manag. J. 2005, 48, 499–520. [Google Scholar] [CrossRef]

- Hochberg, Y.V.; Ljungqvist, A.; Lu, Y. Networking as a barrier to entry and the competitive supply of venture capital. J. Financ. 2010, 65, 829–859. [Google Scholar] [CrossRef]

- Kogut, B.; Urso, P.; Walker, G. Emergent properties of a new financial market: American venture capital syndication, 1960–2005. Manag. Sci. 2007, 53, 1181–1198. [Google Scholar] [CrossRef]

- Lerner, J. The syndication of venture capital investments. Financ. Manag. 1994, 23, 16–27. [Google Scholar] [CrossRef]

- Bruton, G.D.; Fried, V.; Manigart, S. Institutional influences on the worldwide expansion of venture capital. Entrep. Theory Pract. 2005, 29, 737–760. [Google Scholar] [CrossRef]

- Eisenhardt, K.M. Building theories from case study research. Acad. Manag. Rev. 1989, 14, 532–550. [Google Scholar] [CrossRef]

- Dean, T.; McMullen, J. Toward a theory of sustainable entrepreneurship: Reducing environmental degradation through entrepreneurial action. J. Bus. Ventur. 2007, 22, 50–76. [Google Scholar] [CrossRef]

- Granovetter, M.; Ferrary, M. The role of venture capital firms in Silicon Valley’s complex innovation network. Econ. Soc. 2009, 38, 326–359. [Google Scholar]

- Burt, R.; Knes, M. The Gossip of the Third Party in Trust in Organizations; Kramer, R.M., Tyler, T.R., Eds.; Sage Publications, Inc.: London, UK, 2001; pp. 68–89. [Google Scholar]

- Barabasi, A.; Albert, R. Emergence of scaling in random networks. Science 1999, 286, 509–513. [Google Scholar] [CrossRef]

- Powell, W.W. Neither market nor hierarchy: Network forms of organization. Organ. Behav. 1990, 12, 295–336. [Google Scholar]

- Nambisan, S.; Baron, R.A. Entrepreneurship in innovation ecosystems: Entrepreneurs’ self-regulatory processes and their implications for new venture success. Entrep. Theory Pract. 2013, 37, 1071–1097. [Google Scholar] [CrossRef]

- Pitelis, C. Clusters, entrepreneurial ecosystem co-creation, and appropriability: A conceptual framework. Ind. Corp. Chang. 2012, 21, 1359–1388. [Google Scholar] [CrossRef]

- Wüstenhagen, R.; Teppo, T. Do Venture capitalists really invest in good industries? Risk-return perceptions and path dependence in the emerging European energy VC market. Int. J. Technol. Manag. 2006, 34, 63. [Google Scholar] [CrossRef]

- Tsujimoto, M.; Kajikawa, Y.; Tomita, J.; Matsumoto, Y. A review of the ecosystem concept — Towards coherent ecosystem design. Tech. Forecast. Soc. 2018, 136, 49–58. [Google Scholar] [CrossRef]

- Krackardt, D. QAP partialling as a test of spuriousness. Soc. Netw. 1987, 9, 171–186. [Google Scholar] [CrossRef]

- Luo, J.; Cheng, M.; Zhang, T. Guanxi circle and organizational citizenship behavior—Taking a Chinese workplace as an example. Asia Pacif. J. Manag. 2016, 33, 649–671. [Google Scholar] [CrossRef]

- Hwang, K.K. Face and favor: The Chinese power game. Am. J. Sociol. 1987, 92, 944–974. [Google Scholar] [CrossRef]

- Chowdhry, B.; Nanda, V. Stabilization, syndication, and pricing of I.P.O.s. J. Financ. Q. Anal. 1996, 31, 25–42. [Google Scholar] [CrossRef]

- Chiplin, B.; Robbie, K.; Wright, M. The syndication of venture capital deals: Buy-outs and buy-ins. Entrep. Theory Pract. 1997, 21, 9–28. [Google Scholar]

- Burt, R. The social structure of competition. In Structural Holes: The Social Structure of Competition; Harvard University Press: Cambridge, MA, USA, 1992; pp. 8–45. [Google Scholar]

- Wareham, J.; Fox, P.B.; Cano Giner, J.L. Technology ecosystem governance. Organ. Sci. 2014, 25, 1195–1215. [Google Scholar] [CrossRef]

- Podolny, J.M. A Status-based model of market competition. Am. J. Sociol. 1993, 98, 829–872. [Google Scholar] [CrossRef]

- Inchauspe, J.; Ripple, R.D.; Trueck, S. The dynamics of returns on renewable energy companies: A state-space approach. Energy Econ. 2015, 48, 325–335. [Google Scholar] [CrossRef]

- Marcus, A.A.; Ellis, S.; Malen, J. Conferring Legitimacy: Takeoff in Clean Energy Venture Capital Investment. Acad. Manag. Annu. Meet. 2012, 2012, 16439. [Google Scholar] [CrossRef]

- Wüstenhagen, R.; Wolsink, M.; Bürer, J.M. Social acceptance of renewable energy innovation: An introduction to the concept. Energy Policy 2007, 35, 2683–2691. [Google Scholar] [CrossRef]

- Cox, P.E.; Katila, R.; Eisenhardt, K.M. Who takes you to the dance? How partners’ institutional logics influence innovation in young firms. Adm. Sci. Q. 2015, 60, 266–276. [Google Scholar]

{kind=link}

{kind=link}

| Year | Number of Active Investors | Number of Investment Events | Number of New Entrants | Total Number of Investors |

|---|---|---|---|---|

| 2000 | 128 | 277 | 82 | 192 |

| 2001 | 131 | 226 | 63 | 255 |

| 2002 | 120 | 213 | 40 | 295 |

| 2003 | 143 | 283 | 50 | 345 |

| 2004 | 179 | 420 | 60 | 405 |

| 2005 | 223 | 533 | 86 | 491 |

| 2006 | 345 | 990 | 150 | 641 |

| 2007 | 511 | 1476 | 232 | 873 |

| 2008 | 557 | 1471 | 212 | 1085 |

| 2009 | 551 | 1490 | 193 | 1278 |

| 2010 | 753 | 2687 | 316 | 1594 |

| 2011 | 882 | 3636 | 376 | 1970 |

| 2012 | 681 | 2639 | 229 | 2199 |

| 2013 | 462 | 2021 | 125 | 2324 |

| Variable Name | Measurement |

|---|---|

| Syndication Number | The number of joint investments between two nodes during the period 2011 to 2013. |

| Previous Syndication Number | The number of joint investments between two nodes during the period 2000 to 2010. |

| Distance | Relational distance between two nodes in the industrial network formed from 2000 to 2010. |

| Common Neighbor | The number of common neighbors in the industrial network from 2000 to 2010. |

| Centrality–SH | The effect size, in the industrial network, during 2000–2010, of a selected VC who has syndication ties, during 2011–2013, with a leader ranking in the top 20% for degree centrality. |

| Centrality–CC | The clustering coefficient in the industrial network during 2000–2010, of a selected VC who has syndication ties, during 2011–2013, with a leader ranking in the top 20% for degree centrality. |

| Industry Similarity | Was there any previous partner of a surveyed VC in the same industry of the end node of the syndication tie? If yes, this variable is 1; otherwise, 0. |

| Long Trend | The proportion of the industries jointly investing in two nodes, which belong to the top ten popular targets of investment. |

| Variable | 2000–2010 Frequency | Common Neighbor | Distance | Centrality–SH | Centrality–CC | Square of Cluster Coefficient | Industry Similarity | Long Trend | 2011–2013 Frequency |

|---|---|---|---|---|---|---|---|---|---|

| 2000–2010 Frequency | 1 | 0.539 *** | −0.308 *** | 0.195 *** | 0.095 *** | −0.006 | 0.120 *** | −0.034 ** | 0.247 *** |

| Common Neighbor | 1 | −0.531 *** | 0.400 *** | 0.269 ** | 0.002 | 0.209 *** | −0.052 * | 0.234 *** | |

| Distance | 1 | −0.362 *** | −0.278 ** | −0.021 | −0.228 *** | −0.023 | −0.150 *** | ||

| Centrality–SH | 1 | 0.539 *** | −0.041 | 0.092 *** | −0.038 | 0.117 *** | |||

| Centrality–CC | 1 | −0.004 | 0.059 *** | −0.039 | 0.053 *** | ||||

| CC square | 1 | −0.002 | 0.015 | −0.008 * | |||||

| Industry Similarity | 1 | 0.413 *** | 0.117 *** | ||||||

| Long Trend | 1 | −0.025 ** | |||||||

| 2011–2013 Frequency | 0.134 *** | ||||||||

| 1 |

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | |

|---|---|---|---|---|---|---|

| 2000–2010 Frequency | 0.216 *** | 0.171 *** | 0.209 *** | 0.170 *** | ||

| Common Neighbor | 0.100 *** | 0.101 *** | ||||

| Distance | −0.031 *** | −0.003 * | ||||

| Centrality–SH | 0.040 *** | 0.017 *** | ||||

| Centrality–CC | 0.003 | −0.021 ** | ||||

| CC square | −0.004 | −0.005 | ||||

| Industry Similarity | 0.108 *** | 0.092 *** | 0.104 *** | 0.136 *** | 0.137 *** | 0.092 *** |

| Long Trend | −0.059 *** | −0.050 *** | −0.059 *** | −0.076 *** | −0.077 *** | −0.050 *** |

| Intercept | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| AdjR2 | 0.078 | 0.084 | 0.079 | 0.035 | 0.034 | 0.084 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ren, J.; Luo, J.-D.; Rong, K. How Do Venture Capitals Build Up Syndication Ecosystems for Sustainable Development? Sustainability 2020, 12, 4385. https://doi.org/10.3390/su12114385

Ren J, Luo J-D, Rong K. How Do Venture Capitals Build Up Syndication Ecosystems for Sustainable Development? Sustainability. 2020; 12(11):4385. https://doi.org/10.3390/su12114385

Chicago/Turabian StyleRen, Jie, Jar-Der Luo, and Ke Rong. 2020. "How Do Venture Capitals Build Up Syndication Ecosystems for Sustainable Development?" Sustainability 12, no. 11: 4385. https://doi.org/10.3390/su12114385

APA StyleRen, J., Luo, J.-D., & Rong, K. (2020). How Do Venture Capitals Build Up Syndication Ecosystems for Sustainable Development? Sustainability, 12(11), 4385. https://doi.org/10.3390/su12114385