Factors Shaping Cow’s Milk Production in the EU

Abstract

:1. Introduction

- Elaboration of the impact of changes in milk production for particular countries of the EU during the period from 2018 to 2020;

- Identification of factors having an impact on milk production in the EU countries;

- Evaluation of the impact of various characteristics on milk production in the EU.

2. Impact of Common Agricultural Policy and Environmental Regulations on Milk Production

3. Materials and Methods

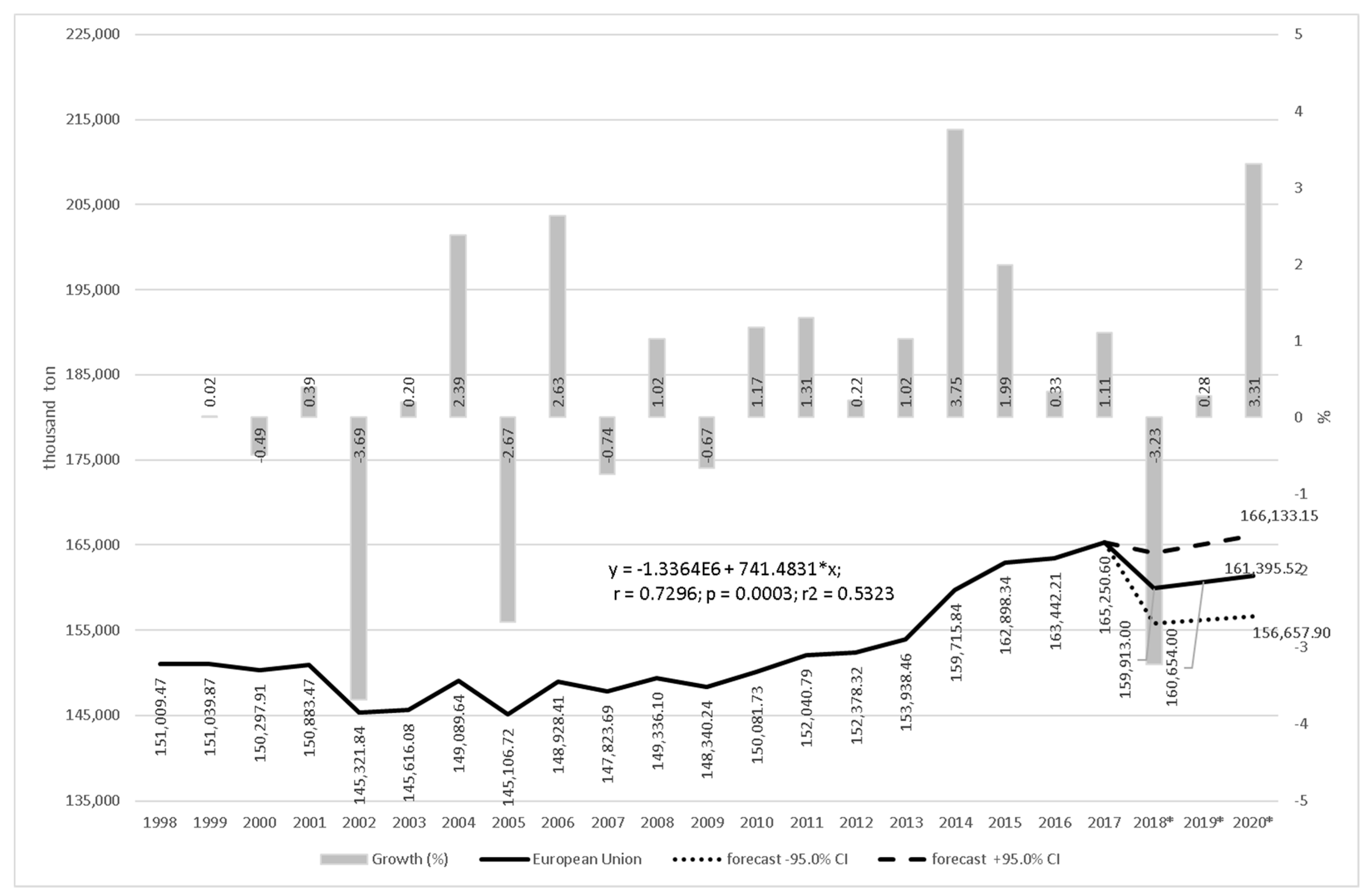

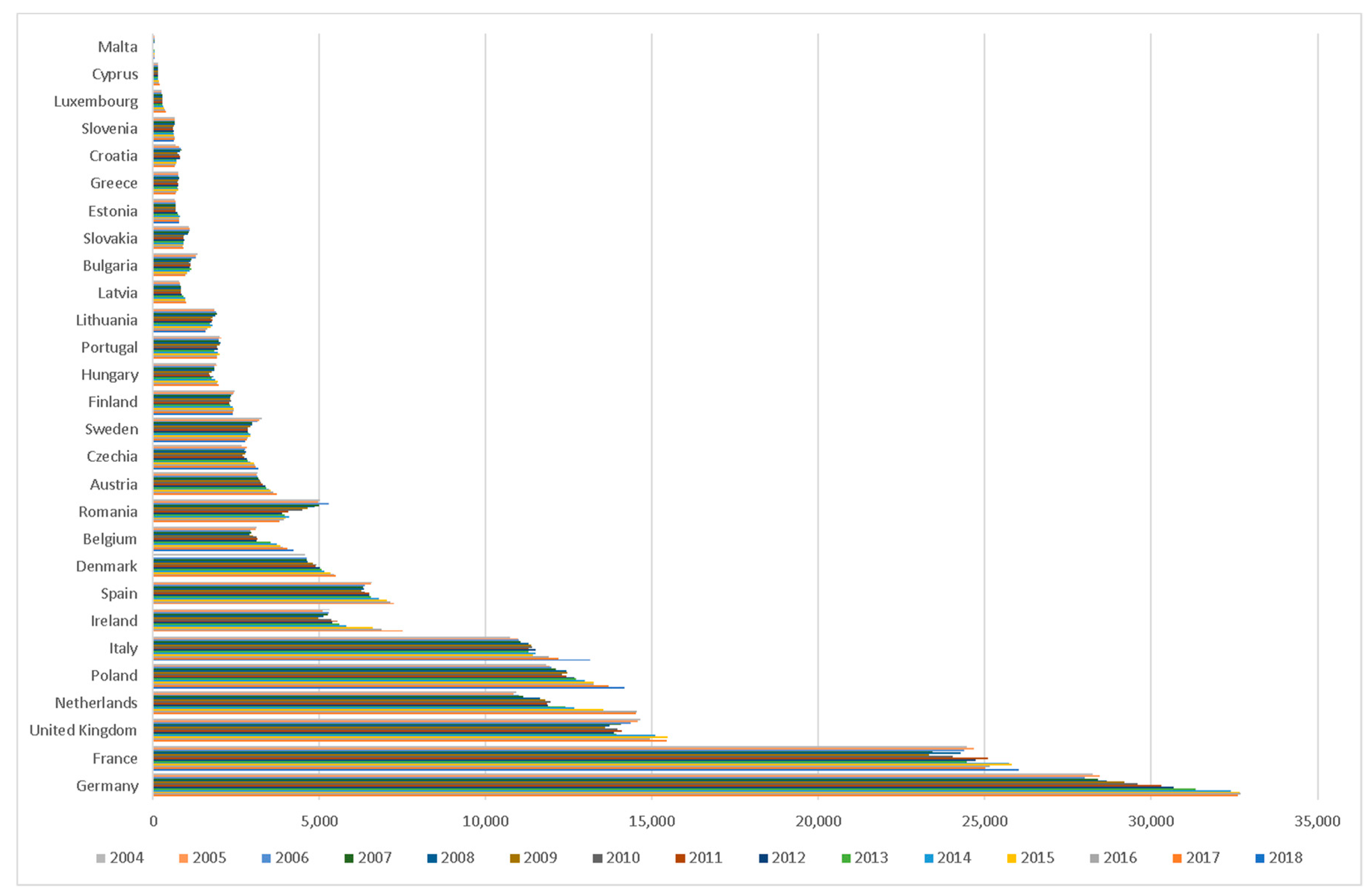

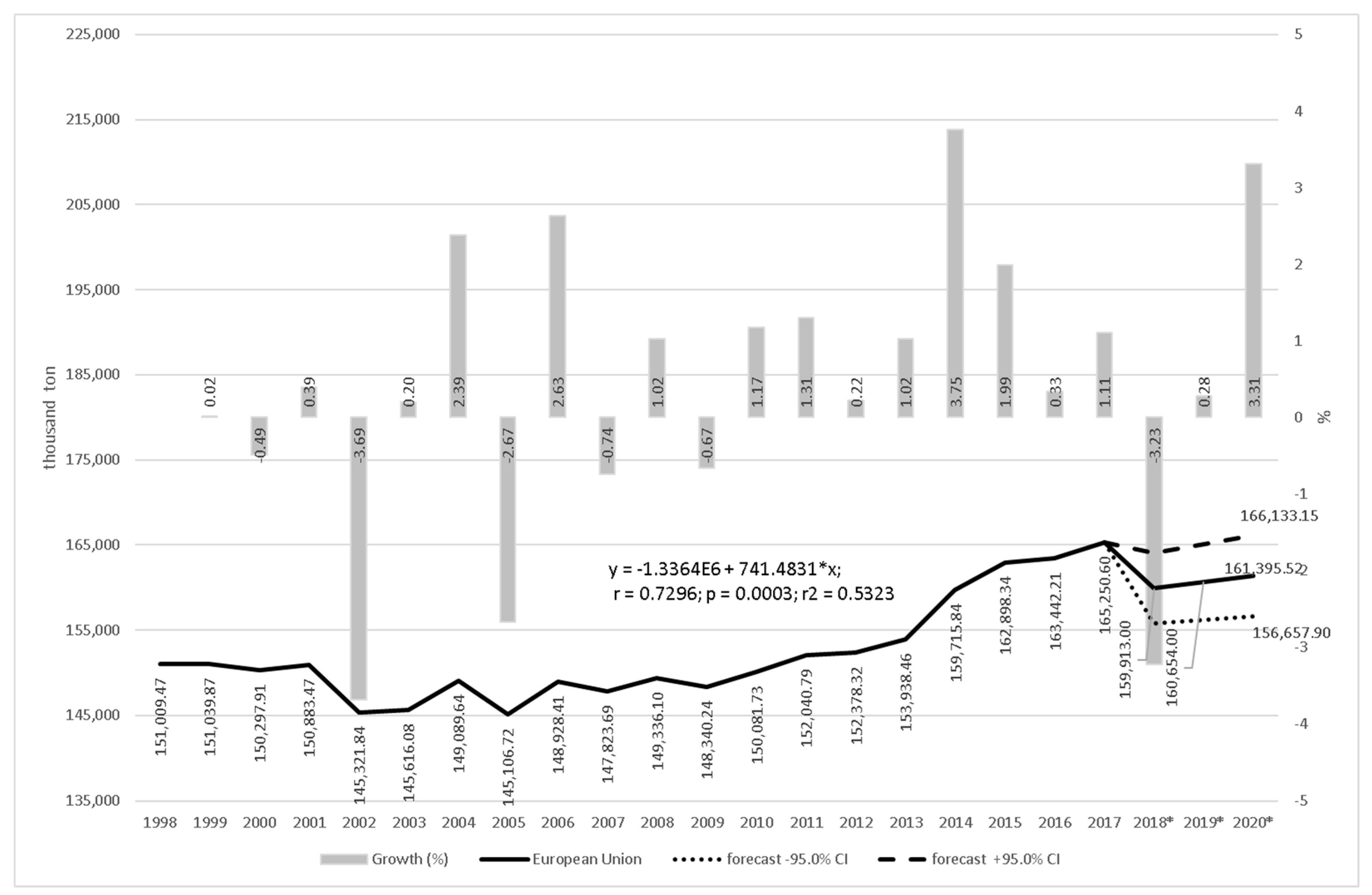

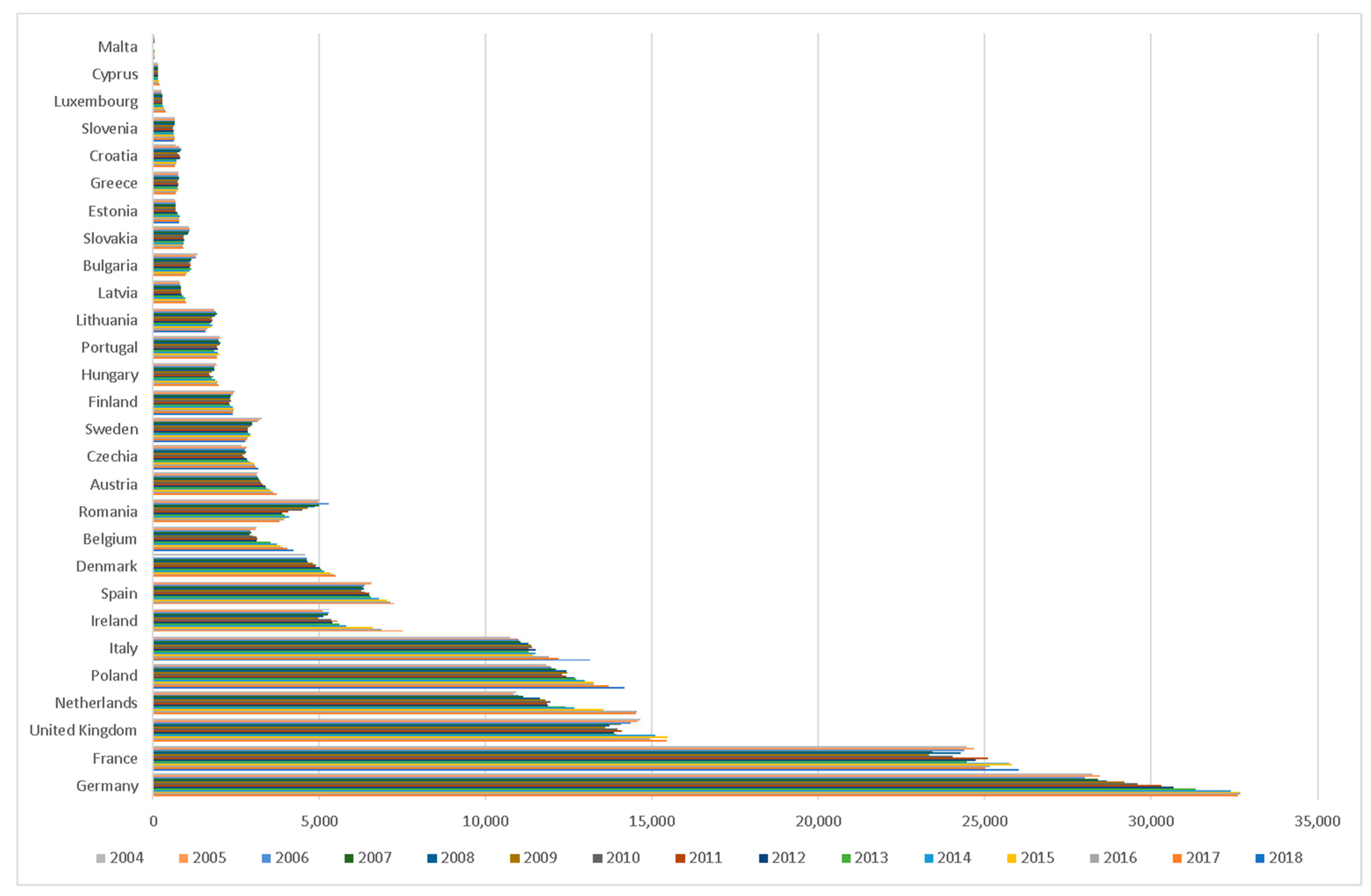

4. Results and Discussion

5. Implications for Common Agricultural Policy in Milk Market

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Simo, D.; Mura, L.; Buleca, J. Assessment of milk production competitiveness of the Slovak Republic within the EU-27 countries. Agric. Econ. Czech Repub. 2016, 62, 482–492. [Google Scholar] [CrossRef] [Green Version]

- Gulseven, O.; Wohlgenant, M. What are the factors affecting the consumers’ milk choices? Agric. Econ. Czech Repub. 2017, 63, 271–282. [Google Scholar] [CrossRef] [Green Version]

- Tukker, A.; Huppes, G.; Guinée, J.B.; Heijungs, R.; de Koning, A.; van Oers, L.; Suh, S.; Geerken, T.; van Holderbeke, M.; Jansen, B.; et al. Environmental Impact of Products (EIPRO)—Analysis of the Life Cycle Environmental Impacts Related to the Final Consumption of the EU-25; Main Report, IPTS/ESTO Project; European Commission, Directorate-General, Joint Research Centre: Brussels, Belgium, 2006; p. 139. Available online: http://ec.europa.eu/environment/ipp/pdf/eipro_report.pdf (accessed on 1 August 2018).

- Hillerton, J.E.; Berry, E.A. Quality of the Milk Supply: European Regulations Versus Practice. In Proceedings of the NMC 43rd Annual Meeting, 1–4 February 2004. [Google Scholar]

- Cabrera, V.E.; Solis, D.; Del Corral, J. Determinants of technical efficiency among dairy farms in Wisconsin. J. Dairy Sci. 2010, 93, 387–393. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Schick, M.; Hartmann, W. Arbeitszeitbedarfswerte in der Milchviehhaltung. Landtechnik 2005, 60, 226–227. [Google Scholar] [CrossRef]

- Pouch, T.; Trouvé, A. Deregulation and the crisis of dairy markets in Europe: facts for economic interpretation. Stud. Political Econ. 2018, 99, 194–212. [Google Scholar] [CrossRef]

- Pietola, K.; Heikkilä, A.M. Switching toward capital-intensive technologies in Finnish dairy farms. Agric. Econ. 2005, 33, 381–387. [Google Scholar] [CrossRef]

- Kramer, B.; Schorr, A.; Doluschitz, R.; Lips, M. Short and medium-term impact of dairy barn investment on profitability and herd size in Switzerland. Agric. Econ. Czech Repub. 2019, 65, 270–277. [Google Scholar] [CrossRef] [Green Version]

- Bewley, J. Precision dairy farming: Advanced analysis solutions for future profitability. In Proceedings of the First North American Conference on Precision Dairy Management, Toronto, ON, Canada, 2–5 March 2010. [Google Scholar]

- Wijnands, J.H.M.; van der Meulen, B.M.J.; Poppe, K.J. Competitiveness of the European Food Industry: An Economic and Legal Assessment 2007; Office for Official Publications of the European Communities: Luxemburg, 2007. [Google Scholar]

- Tacken, G.M.L.; Banse, M.A.H.; Batowska, A.; Gardebroek, C.; Turi, K.N.; Wijnands, J.H.M.; Poppe, K. Competitiveness of the EU Dairy Industry; LEI Wageningen UR: The Hague, The Netherlands, 2009. [Google Scholar]

- Naglova, Z.; Boberova, B.; Horakova, T.; Smutka, L. Statistical analysis of factors influencing the results of enterprises in dairy industry. Agric. Econ. Czech Repub. 2017, 63, 259–270. [Google Scholar] [CrossRef] [Green Version]

- FoodDrinkEurope. European Food and Drink Industry 2014–2015. 2014. Available online: https://www.fooddrinkeurope.eu/publication/data-trends-of-the-european-food-and-drink-industry-2013-2014/ (accessed on 27 July 2019).

- Gołębiewski, J. Economic performance of sectors along the food supply chain–comparative study of the European Union countries. Acta Sci. Pol. Oecon. 2018, 17, 69–78. [Google Scholar] [CrossRef]

- Pietrzak, M.; Roman, M. The problem of geographical delimitation of agri-food markets: Evidence from the butter market in European Union. Acta Sci. Pol. Oecon. 2018, 17, 85–95. [Google Scholar] [CrossRef]

- Zimmermann, A.; Heckelei, T. Structural change of European dairy farms-a case regional analysis. J. Agric. Econ. 2012, 63, 576–603. [Google Scholar] [CrossRef] [Green Version]

- Huettel, S.; Jongeneel, R. How has the EU milk quota affected patterns of herd-size change? Eur. Rev. Agric. Econ. 2011, 38, 497–527. [Google Scholar] [CrossRef]

- Dries, L.; Swinnen, J.F.M. The impact of interfirm relationship on investment: Evidence from the Polish dairy sector. Food Policy 2010, 35, 121–129. [Google Scholar] [CrossRef]

- Bórawski, P.; Pawlewicz, A.; Harper, J.K.; Dunn, J.W. The Intra-European Union Trade of Milk and Dairy Products. Acta Sci. Pol. Oecon. 2019, 18, 13–23. [Google Scholar] [CrossRef]

- Zuba-Ciszewska, M. The Role of Dairy Cooperatives in Reducing Waste of Dairy Products in the Lubelskie Voivodeship. J. Agribus. Rural Dev. 2018, 1, 97–105. [Google Scholar] [CrossRef]

- Von Keyserlingk, M.A.G.; Martin, N.P.; Kebreab, E.; Knowlton, K.F.; Grant, R.J.; Stephenson, M.W.; Sniffen, C.J.; Harner, J.P., III; Wright, A.D.; Smith, S.I. Invited review: Sustainability of the US dairy industry. J. Dairy Sci. 2013, 96, 5405–5425. [Google Scholar] [CrossRef] [Green Version]

- Krpalkova, L.; Cabrera, V.E.; Kvapilik, J.; Burdych, J. Dairy farm profit according to the herd size, milk yield, and number of cows per worker. Agric. Econ. Czech Repub. 2016, 62, 225–234. [Google Scholar] [CrossRef] [Green Version]

- Stelwagen, K.; Phyn, C.V.C.; Davis, S.R.; Guinard-Flament, J.; Pomies, D.; Roche, J.R.; Kay, J.K. Invited review: Reduced milking frequency: Milk production and management implications. J. Dairy Sci. 2013, 96, 3401–3413. [Google Scholar] [CrossRef] [PubMed]

- Zakova Kroupova, Z. Profitability development of Czech dairy farms. Agric. Econ. Czech Repub. 2016, 62, 269–279. [Google Scholar] [CrossRef] [Green Version]

- Folmer, C.; Keyzer, M.A.; Merbis, M.D.; Stolwijk, H.J.J.; Veenendaal, P.J.J. The Common Agricultural Policy Beyond the MacSharry Reform; Tinbergen, J., Ed.; Elsevier: Amsterdam, The Netherlands, 2013. [Google Scholar]

- Zhu, X.; Demeter, R.M.; Oude Lansink, A.G.J.M. Competitiveness of Dairy Farms in Three Countries: The Role of CAP Subsidies. In Proceedings of the 12th Congress of the European Association of Agricultural Economists—EAAE, Ghent, Belgium, 26–29 August 2008. [Google Scholar]

- Groeneveld, A.; Peerlings, J.; Bakker, M.; Heijman, W. The effect of milk quota abolishment on farm intensity: Shifts and stability. NJAS-Wagening. J. Life Sci. 2016, 77, 25–37. [Google Scholar] [CrossRef]

- Réquillart, V.; Bouamra-Mechemache, Z.; Jongeneel, R.; Penel, C. Economic Analysis of the Effects of the Expiry of the EU Milk Quota System. 2008. Available online: https://ec.europa.eu/agriculture/external-studies/milk_en (accessed on 19 September 2019).

- Bouamra-Mechemache, Z.; Jogeneel, R.; Réquillart, V. Removing EU Milk Quotas, Soft Landing Versus Hard Landing. In Proceedings of the 12th Congress of the European Association of Agricultural Economists, Ghent, Belgium, 26–29 August 2008. [Google Scholar]

- Boulanger, P.; Philippidis, G. The EU budget battle: Assessing the trade and welfare impacts of CAP budgetary reform. Food Policy 2015, 51, 119–130. [Google Scholar] [CrossRef] [Green Version]

- Lobley, M.; Butler, A. The impact of CAP reform on farmers’ plans for the future: Some evidence from South West England. Food Policy 2010, 35, 341–348. [Google Scholar] [CrossRef]

- EUROSTAT. Archive: Milk and Milk Products—30 Years of Quotas. 2015. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php/Archive:Milk_and_milk_products_-_30_years_of_quotas (accessed on 27 July 2019).

- Van Kampen, A.; Versepu, S. Zo gaat de afschaffing van het melkquotum de markt veranderen [This is How the Milk Quota Abolishment Will Change the Market]. 2014. Available online: https://www.nrc.nl/nieuws/2014/11/12/zo-gaat-de-afschaffing-van-het-melkquotum-de-markt-veranderen-a1499052 (accessed on 12 October 2019).

- Szajner, P. Price transmission on milk market in Poland between 2004 and 2017. Probl. Agric. Econ. 2017, 4, 3–23. [Google Scholar] [CrossRef] [Green Version]

- Alpmann, J.; Bitsch, V. Dynamics of asymmetric conflict: The case of the German Milk Conflict. Food Policy 2017, 66, 62–72. [Google Scholar] [CrossRef]

- BMEL. Ein Paradigmenwechsel am Milchmarkt—von der Milchquotenregelung zu mehr Verantwortung der Marktakteure [A Paradigm Shift in the Milk Market—From the Milk Quota Regime to Greater Responsibility of the Market Players]. 2015. Available online: https://www.bmel.de/DE/Landwirtschaft/Agrarpolitik/1_EU-Marktregelungen/_Texte/Auswirkungen-Ende-Milchquote.html (accessed on 12 October 2019).

- RegulationEU. No 261/2012 of the European Parliament and of the Council of 14 March 2012 amending Council Regulation (EC) No 1234/2007 as Regards Contractual Relations in the Milk and Milk Products Sector. Available online: https://eur-lex.europa.eu/legal-content/PL/TXT/?uri=uriserv%3AOJ.L_.2012.094.01.0038.01.ENG&toc=OJ%3AL%3A2012%3A094%3ATOC (accessed on 7 September 2019).

- Parzonko, A. The role of subsidies for cows and other cattle in the polish system direct payments in the development of the dairy sector. Ann. Pol. Assoc. Agric. Agribus. Econ. 2017, 19, 144–150. [Google Scholar] [CrossRef]

- Wąs, A.; Malak-Rawlikowska, A.; Majewski, E. The new delivery model of the Common Agricultural Policy after 2020-challenges for Poland. Probl. Agric. Econ./Zag. Ekon. Rolnej 2018, 4, 33–59. [Google Scholar] [CrossRef]

- Yarwood, R.; Evans, N. Livestock, locality and landscape: EU regulations and the new geography of Welsh farm animals. Appl. Geogr. 2003, 23, 137–157. [Google Scholar] [CrossRef] [Green Version]

- Shum, L.W.C.; McConnel, C.S.; Gunn, A.A.; House, J.K. Environmental mastitis in intensive high-producing dairy herds in New South Wales. Aust. Vet. J. 2009, 87, 469–475. [Google Scholar] [CrossRef]

- Stafford, K.J.; Gregory, N.G. Implications of intensification of pastoral animal production on animal welfare. N. Z. Vet. J. 2008, 56, 274–280. [Google Scholar] [CrossRef]

- Lagane, J. When students run AMAPs: Towards a French model of CSA. Agric. Hum. Values 2015, 32, 133–141. [Google Scholar] [CrossRef]

- Soltanali, H.; Emadi, B.; Rohani, A.; Khojastehpour, M.; Nikkhah, A. Life cycle assessment modeling of milk production in Iran. Inf. Process. Agric. 2015, 2, 101–108. [Google Scholar] [CrossRef] [Green Version]

- Olipra, J. Cycles in the Global Milk Market. J. Agribus. Rural Dev. 2019, 52, 165–172. [Google Scholar] [CrossRef]

- Repar, N.; Pierrick, J.; Nemecek, T.; Dunja Dux, D.; Reiner Doluschitz, R. Factors Affecting Global versus Local Environmental and Economic Performance of Dairying: A Case Study of Swiss Mountain Farms. Sustainability 2018, 10, 2940. [Google Scholar] [CrossRef] [Green Version]

- Hunt, T.; Kern, M. The End of the Old US Dairy Price Cycle. 2012. Available online: https://www.progressivedairy.com/topics/management/the-end-of-the-old-us-dairy-price-cycle (accessed on 12 October 2019).

- Tauer, L.W. Efficiency and competitiveness of the small New York dairy farm. J. Dairy Sci. 2001, 84, 2573–2576. [Google Scholar] [CrossRef]

- Parzonko, A. Global and region al conditions for milk production development. Rozprawy Naukowe i Monografie. Szkoła Główna Gospodarstwa Wiejskiego w Warszawie 2013, 426, 210. [Google Scholar]

- Chatellier, V. International, European and French Trade in Dairy Products: Trends and Competitive Dynamics. In Working Paper SMART—LERECO; INRA UMR SMART-LERECO: Rennes, France, 2017; Volume 17, p. 49. [Google Scholar]

- Bórawski, P.; Bełdycka-Bórawska, A. Polish international trade of agri food productsand its prognosis. Probl. World Agric./Probl. Rol. Świat. 2016, 16, 48–59. [Google Scholar]

- Pawlak, K. Changes in Polish foreign trade in agri-food products after accession to the European Union. Probl. World Agric. 2014, 14, 170–184. [Google Scholar]

- Windig, J.J.; Calus, M.P.L.; Beerda, B.; Veerkamp, R.F. Genetic correlations between milk production and health and fertility depending on herd environment. J. Dairy Sci. 2006, 89, 1765–1775. [Google Scholar] [CrossRef]

- EC. EU Agricultural Outlook for Markets and Income, 2018–2030. 2018. Available online: https://euagenda.eu/publications/eu-agricultural-outlook-for-markets-and-income-2018-2030 (accessed on 27 July 2019).

- Dries, L.; Germenji, E.; Noev, N.; Swinnen, J.F.M. Farmers, vertical coordination, and the restructuring of Polish supply chains in Central and Eastern Europe. World Dev. 2009, 37, 1742–1758. [Google Scholar] [CrossRef]

- Rabinowitz, A.N.; Liu, Y. The impact of regulations change on retail pricing: The New York state milk price gouging law. Agric. Resour. Econ. 2014, 43, 178–192. [Google Scholar] [CrossRef]

- Bernard, J.; LeGal, P.Y.; Triophe, B.; Hoostiou, N.; Moulin, C.H. Involvement of small-scale dairy farms in an industrial supply chain: When production standards meet farm diversity. Animal 2011, 5, 961–971. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Moreira, A.; Bravo-Ureta, B. Technical efficiency and meta technology ratios for dairy farms in three southern cone countries: A stochastic meta-frontier model. J. Prod. Anal. 2010, 33, 33–45. [Google Scholar] [CrossRef]

- Blayney, D.P.; Gehlhar, M.J. U.S. dairy at a new crossroads in a global setting. Amber Waves 2005, 3, 1–6. [Google Scholar]

- Van Asseldonk, M.A.P.M.; Huirne, R.B.M.; Dijkhuizeb, A.A.; Beulens, A.J.M. Dynamic programming to determine optimum investments in information technology on dairy farms. Agric. Syst. 1999, 62, 17–28. [Google Scholar] [CrossRef]

- Thijssen, G. Farmers’ Investment Behavior: An Empirical Assessment of Two Specifications of Expectations. Am. J. Agric. Econ. 1996, 78, 166–174. [Google Scholar] [CrossRef]

- Gallerani, V.; Gomez y Paloma, S.; Raggi, M.; Viaggi, D. Investment Behaviour in Conventional and Emerging Farming Systems under Different Policy Scenarios; JRC Scientific and Technical Report Institute for Prospective Technological Studies; European Commission: Brussels, Belgium, 2008; p. 170. [Google Scholar]

- Kataria, K.; Curtiss, J.; Balmann, A. Drivers of Agricultural Physical Capital Development, Theoretical Framework and Hypotheses; Working Papers 122842; Factor Markets, Centre for European Policy Studies: Brussels, Belgium, 2012. [Google Scholar]

- Waldman, K.B.; Kerr, J.M. Is Food and Drug Administration policy governing artisan cheese consistent with consumers’ preferences? Food Policy 2015, 55, 71–80. [Google Scholar] [CrossRef]

- Hafla, A.N.; MacAdam, J.W.; Soder, K.J. Sustainability of US organic beef and dairy production sustems: Soil, plant and cattle interactions. Sustainability 2013, 5, 3009–3034. [Google Scholar] [CrossRef] [Green Version]

- Morais, T.G.; Teixeira, R.M.; Rodrigues, N.R.; Domingos, T. Carbon footprint of milk from pastyre-based dairy farms in Azores, Portugal. Sustainability 2018, 10, 3658. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

| Years | N | Average | Median | Minimum | Maximum | SD | CV |

|---|---|---|---|---|---|---|---|

| Number | Thousand Tons | Thousand Tons | Thousand Tons | Thousand Tons | Thousand Tons | % | |

| 2004 | 28 | 5324.63 | 2561.95 | 41.99 | 28,244.73 | 6988.74 | 131.25 |

| 2005 | 28 | 5374.32 | 2433.20 | 41.47 | 28,452.95 | 7163.35 | 133.29 |

| 2006 | 28 | 5318.87 | 2590.07 | 41.02 | 27,994.97 | 6950.36 | 130.67 |

| 2007 | 28 | 5279.42 | 2555.80 | 40.59 | 28,402.77 | 6909.23 | 130.87 |

| 2008 | 28 | 5333.43 | 2556.11 | 39.91 | 28,656.26 | 7039.72 | 131.99 |

| 2009 | 27 * | 5492.60 | 2780.66 | 152.10 | 29,198.68 | 7084.71 | 128.97 |

| 2010 | 27 * | 5557.10 | 2682.52 | 151.02 | 29,593.88 | 7218.02 | 129.89 |

| 2011 | 27 * | 5629.66 | 2735.93 | 156.02 | 30,301.36 | 7410.42 | 131.63 |

| 2012 | 27 * | 5642.16 | 2814.68 | 153.74 | 30,672.15 | 7422.50 | 131.55 |

| 2013 | 28 | 5497.80 | 2588.62 | 40.92 | 31,324.24 | 7432.63 | 135.19 |

| 2014 | 28 | 5704.14 | 2665.83 | 42.77 | 32,381.06 | 7737.39 | 135.65 |

| 2015 | 28 | 5817.80 | 2684.96 | 41.57 | 32,670.88 | 7976.87 | 137.11 |

| 2016 | 28 | 5837.22 | 2645.91 | 43.13 | 32,672.34 | 7949.36 | 136.18 |

| 2017 | 28 | 5901.81 | 2611.21 | 41.03 | 32,598.20 | 7979.57 | 135.21 |

| Variable | Average | S D. | Raw Cows’ Milk from Farm (1000 t) |

|---|---|---|---|

| Raw cows’ milk from farm (1000 t) | 6119 | 8047 | 1 |

| Gross domestic product at market prices (Current prices, million euro) | 568,508 | 845,857 | 0.922137 * |

| Final consumption expenditure of households (Current prices, million euro) | 306,163 | 467,620 | 0.885822 * |

| Exports of goods (Current prices, million euro) | 185,587 | 261,299 | 0.929326 * |

| Imports of goods (Current prices, million euro) | 175,888 | 227,895 | 0.944257 * |

| Subsidies (Current prices, million euro) | 9300 | 14,317 | 0.817275 * |

| Gross domestic product at market prices (Current prices, euro per capita) | 29,378 | 19,225 | 0.183248 |

| Final consumption expenditure of households (Current prices, euro per capita) | 14,211 | 6461 | 0.346923 |

| Population (no) | 18,922,703 | 23,886,027 | 0.892247 * |

| Permanent grassland (ha) | 2,190,073 | 2,788,274 | 0.660394 * |

| Share of permanent grassland in Utilised Agricultural Area (%) | 33 | 19 | 0.067514 |

| Specification | Valid N | r | r2 | p | SE | Regression Equation | ↑⁄↓ |

|---|---|---|---|---|---|---|---|

| European Union (28) | 79 | 0.6729 | 0.4528 | 0.0000 | 761.03 | y = 8201.0273 + 14.375 *x | ↑ |

| European Union 15 (1995–2004) | 211 | 0.6783 | 0.4601 | 0.0000 | 701.59 | y = 8655.6546 + 6.8003 *x | ↑ |

| Germany | 355 | 0.7710 | 0.5945 | 0.0000 | 152.6 | y = 2013.3107 + 1.7979 *x | ↑ |

| Poland | 183 | 0.8177 | 0.6686 | 0.0000 | 66.923 | y = 356.5388 + 1.7894 *x | ↑ |

| The Netherlands | 355 | 0.7359 | 0.5415 | 0.0000 | 75.906 | y = 805.9958 + 0.8027 *x | ↑ |

| Ireland | 355 | 0.1998 | 0.0399 | 0.0002 | 229.73 | y = 385.1576 + 0.4558 *x | ↑ |

| Spain | 354 | 0.7532 | 0.5673 | 0.0000 | 39.622 | y = 411.0429 + 0.4427 *x | ↑ |

| France | 354 | 0.2182 | 0.0476 | 0.0000 | 182.97 | y = 1900.0505 + 0.3992 *x | ↑ |

| Italy | 354 | 0.5594 | 0.3129 | 0.0000 | 59.769 | y = 789.2863 + 0.3936 *x | ↑ |

| Denmark | 355 | 0.7217 | 0.5208 | 0.0000 | 25.079 | y = 347.6452 + 0.2544 *x | ↑ |

| Belgium | 355 | 0.6185 | 0.3825 | 0.0000 | 32.782 | y = 227.682 + 0.2511 *x | ↑ |

| Austria | 294 | 0.7959 | 0.6335 | 0.0000 | 16.025 | y = 178.1701 + 0.2474 *x | ↑ |

| Czechia | 187 | 0.5714 | 0.3265 | 0.0000 | 18.331 | y = 151.1571 + 0.2352 *x | ↑ |

| Lithuania | 235 | 0.4652 | 0.2164 | 0.0000 | 22.729 | y = 63.3998 + 0.1753 *x | ↑ |

| Latvia | 199 | 0.7496 | 0.5620 | 0.0000 | 8.6849 | y = 12.0155 + 0.1704 *x | ↑ |

| Estonia | 234 | 0.8934 | 0.7982 | 0.0000 | 4.1717 | y = 22.1291 + 0.1215 *x | ↑ |

| United Kingdom | 355 | 0.1284 | 0.0165 | 0.0155 | 87.525 | y = 1163.8126 + 0.1103 *x | ↑ |

| Portugal | 355 | 0.5466 | 0.2987 | 0.0000 | 15.191 | y = 129.8008 + 0.0965 *x | ↑ |

| Slovenia | 234 | 0.7289 | 0.5314 | 0.0000 | 2.3518 | y = 34.8294 + 0.0369 *x | ↑ |

| Greece | 354 | 0.4810 | 0.2314 | 0.0000 | 5.7533 | y = 45.5566 + 0.0308 *x | ↑ |

| Cyprus | 235 | 0.7924 | 0.6280 | 0.0000 | 1.5237 | y = 6.4896 + 0.0291 *x | ↑ |

| Luxembourg | 355 | 0.6698 | 0.4487 | 0.0000 | 2.9187 | y = 18.8402 + 0.0256 *x | ↑ |

| Malta | 116 | 0.1749 | 0.0306 | 0.0603 | 0.19849 | y = 3.3357 + 0.0005 *x | ↑ |

| Hungary | 199 | −0.0523 | 0.0027 | 0.4630* | 10.628 | y = 125.4752 − 0.0096 *x | ↓ |

| Romania | 187 | −0.0417 | 0.0017 | 0.5713* | 14.776 | y = 86.2107 − 0.0114 *x | ↓ |

| Croatia | 234 | −0.1307 | 0.0171 | 0.0457 | 7.2021 | y = 49.4579 − 0.014 *x | ↓ |

| Finland | 295 | −0.1722 | 0.0297 | 0.0030 | 9.9303 | y = 200.176 − 0.0203 *x | ↓ |

| Bulgaria | 163 | 0.3470 | 0.1204 | 0.0000 | 9.5838 | y = 69.7304 − 0.0749 *x | ↓ |

| Slovakia | 211 | −0.6821 | 0.4653 | 0.0000 | 5.2388 | y = 93.7112 − 0.0799 *x | ↓ |

| Sweden | 294 | −0.7501 | 0.5627 | 0.0000 | 12.945 | y = 290.3685 − 0.1724 *x | ↓ |

| N = 27 | R = 0.96567124 R^2 = 0.93252094 Corrected. R2 = 0.92371932 F (3, 23) = 105.95 p < 0.00000 std. Error: 2222.5 | |||||

|---|---|---|---|---|---|---|

| B * | SE with b * | b | SE with b | T (23) | p | |

| Intersept | 179.991 | 586.9733 | 0.30664 | 0.761874 | ||

| Gross domestic product at market prices (Current prices, million euro) | 2.96181 | 0.448553 | 0.0282 | 0.0043 | 6.60304 | 0.000001 |

| Final consumption expenditure of households (Current prices, million euro) | −2.61334 | 0.496457 | −0.045 | 0.0085 | −5.26399 | 0.000024 |

| Population (no) | 0.57863 | 0.20998 | 0.0002 | 0.0001 | 2.75565 | 0.011258 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bórawski, P.; Pawlewicz, A.; Parzonko, A.; Harper, J.K.; Holden, L. Factors Shaping Cow’s Milk Production in the EU. Sustainability 2020, 12, 420. https://doi.org/10.3390/su12010420

Bórawski P, Pawlewicz A, Parzonko A, Harper JK, Holden L. Factors Shaping Cow’s Milk Production in the EU. Sustainability. 2020; 12(1):420. https://doi.org/10.3390/su12010420

Chicago/Turabian StyleBórawski, Piotr, Adam Pawlewicz, Andrzej Parzonko, Jayson, K. Harper, and Lisa Holden. 2020. "Factors Shaping Cow’s Milk Production in the EU" Sustainability 12, no. 1: 420. https://doi.org/10.3390/su12010420

APA StyleBórawski, P., Pawlewicz, A., Parzonko, A., Harper, J. K., & Holden, L. (2020). Factors Shaping Cow’s Milk Production in the EU. Sustainability, 12(1), 420. https://doi.org/10.3390/su12010420