1. Introduction

Non-performing loans (NPLs) are a threat to sustainable development for developing countries. NPLs are considered as the major indicator of the financial stability of the banking sector. In developing economies, banks usually take greater risks to increase their market shares. With the chance of higher profit, risk increases, which ultimately results in non-performing loans [

1]. NPLs have become a matter of concern for all countries in the world, and as a prerequisite to reinstate the functionality of financial markets, NPLs and its determinants should be addressed carefully [

2]. Ex-post credit risk as an element of non-performing loans is one of the key features of the banking system and economic downturn [

3,

4]. Banks at risk of failing have significant proportions of NPLs in their portfolios of loans before collapse or financial distress [

5].

Banks are intertwined and operate with other banks in a competitive industry. Hence, the bad performance of a bank can affect the entire sector and cause performance variability and create fear. Degraded loan quality creates threats of systemic risk, fear and causes drainage of deposits, a hindrance to financial intermediation, and finally, slows down the pace of economic growth and development. Non-performing loans play a crucial part in creating a poor performance of banks [

6,

7]. Banks are restrained from an intermediation role to the real economy and economic growth by NPLs [

8,

9]. NPLs have been termed “financial pollution” for their negative impacts on the economy [

10,

11]. If regulatory authorities implement any policy, the underlying determinants of NPLs should be taken care of first. As per Basel II, a loan unpaid for more than 90 days is considered as uncollectible.

After the global financial crunch of 2007 and 2008 followed by the share market scam in 2010 and 2011 in Bangladesh, the country faced financial turbulence in the economy, and the banking sector went through a transition time. Fifteen new banks have received licenses to operate in the economy in the last 10 years, and 11 banks in the last 5 years. At present, a total of 59 banks are operating in the economy. Hence, there is acute competitiveness in the industry.

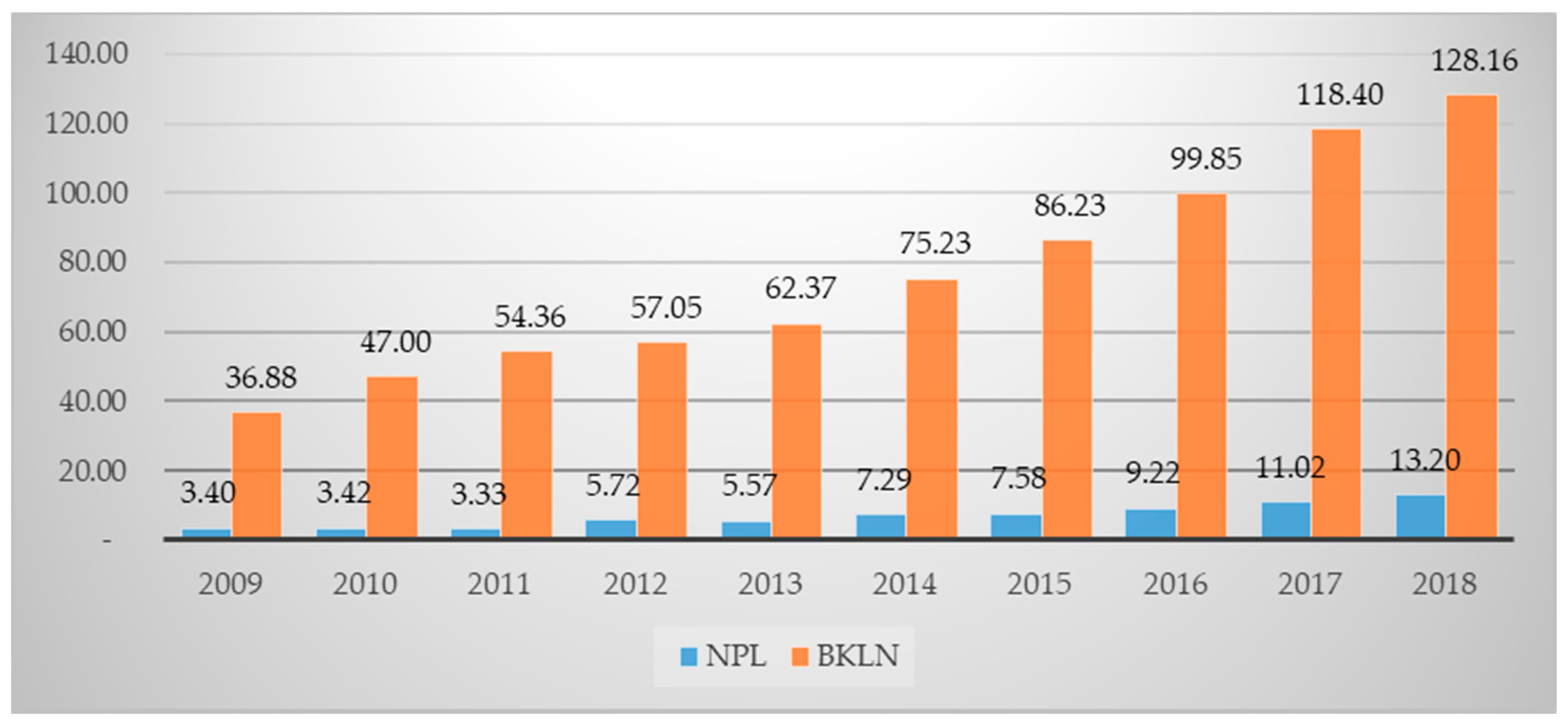

After 2010, non-performing loans started to increase rapidly (

Figure 1). In 2011, they were 2.70 billion US dollars; in 2012, they were 5.09 billion US dollars, and in 2018, breaking all records, they soared up to 13.20 billion US dollars. For a developing country like Bangladesh, it is a matter of concern and a threat to sustainable development.

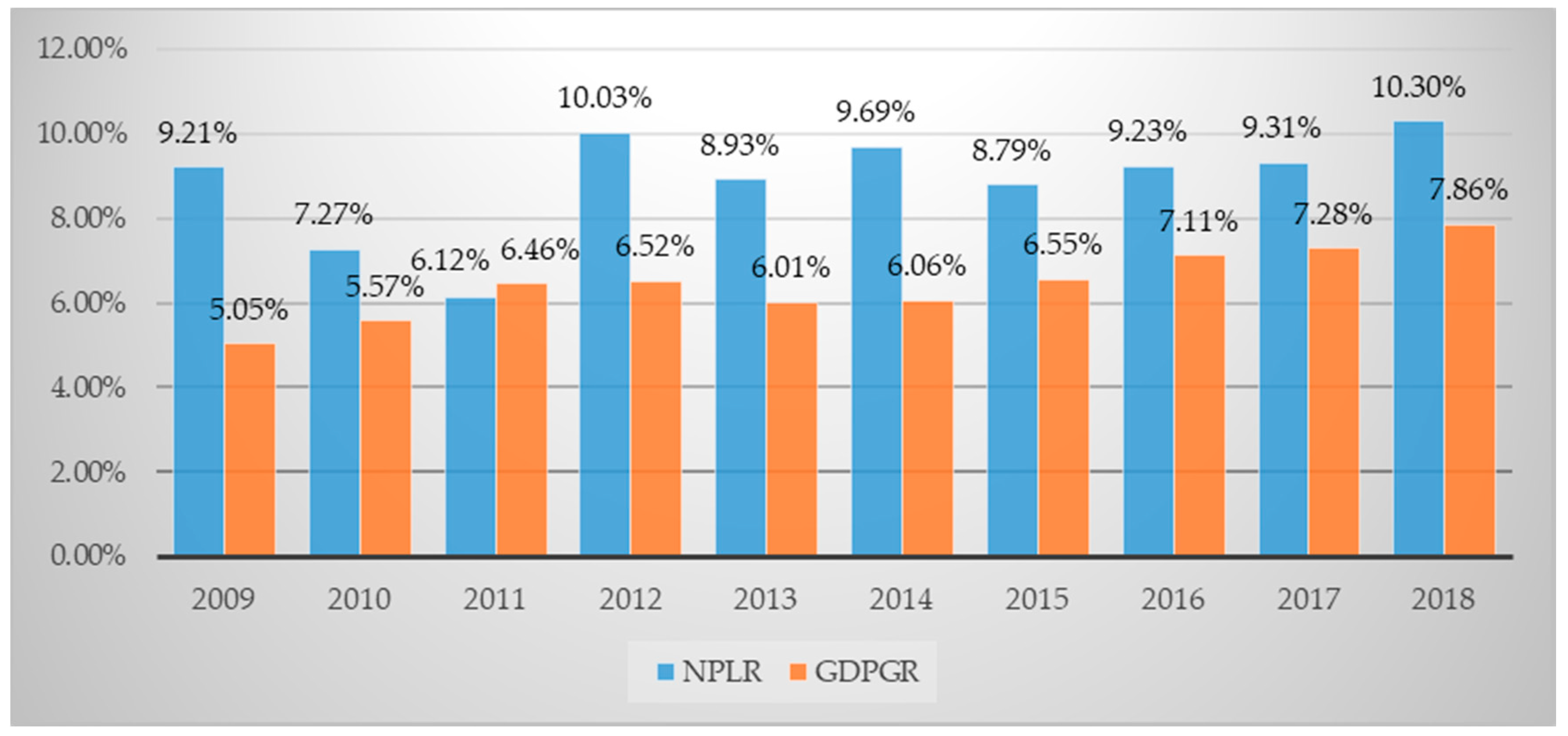

The Non-Performing Loan Ratio (NPLR) reached 40.65% in 1998, which is the highest ever in the history of Bangladesh. Although it gradually came down, this was not enough as it had been 10.30% in 2018 (

Figure 2). Total banking sector NPLs were around 4% of the total GDP in 2018. This current research examines both industry-specific and macroeconomic components of NPLs of all 59 banks in the economy for the period from 1979 to 2018. In our study, we used data from the whole banking sector using a time series dataset with an annual frequency. This study can be considered as a reference to understand and measure the determinants of NPLs in Bangladesh and for developing countries like Bangladesh. To analyze our dataset, we first used the ARDL model and then by finding co-integration with the variables through the Johansen test of co-integration, we conducted a VEC model. Results found in both the models are analogous, indicating the robustness of the study. To know the stability of the models used in the study, we performed some diagnostic tests.

2. Theoretical Background

During our study, we went through many literary works to know the variables, models, and backgrounds on which research was conducted already. We found that factors of NPLs are broadly categorized into two major sources. The macroeconomic sources are GDP and inflation [

2,

12], unemployment [

8], and real interest rates [

13,

14] and the industry-specific factors are management efficacy [

4,

15] and bank size [

3,

5], which may impact the ability to repay loans.

Researchers have found an affiliation between macroeconomic determinants and loan quality, which is a crucial yardstick of the banking sector’s health. Previous findings suggest that bad loans decrease with the expansion of the economy. Borrowers have enough income to repay on time. During economic growth, loans are likely to be approved irrespective of the creditworthiness of the customers while during the economic downturn, NPLs tend to increase (Messai and Jouini 2013). Keeton and Morris (1987) studied 2470 commercial banks in the US from 1979 to 1985, which suggested the regional economy and inferior performance of industries had been the key factors for in loan losses. Espinoza and Prasad [

16] found relationships of NPLs with economic advancement, risk aversion, and interest rates. NPL used to increase when there is a decreasing trend in economic growth and an increase in risk aversion and interest rates. Louzis, Vouldis et al. [

3] looked into types of loans, i.e., consumer, business, mortgage, etc., to find determinants impelling NPLs. They found that macroeconomic variables, such as gross domestic product, interest rates, unemployment, and public debts, can impact the growth of NPLs.

Skarica [

17] found that prime sources of NPLs are the economic (GDP) downturn, lack of employment, and the rate of inflation. In a study in France and Germany, it was found that macroeconomic variables influence NPLs [

18]. Researchers also found the French economy to be vulnerable to bank-specific factors compared to Germany. Economic expansion and unemployment is positively associated with the reduction of NPLs. Macroeconomic variables, including unemployment and economic development, significantly influence NPLs while industry-specific variables, such as management skill and risk preferences, have consequences on future NPLs [

19].

As our quest for literature went on, we found a good number of industry-specific determinants impacting NPLs, i.e., profitability expressed as return on asset (ROA) or return on equity (ROE), capital size expressed as the capital adequacy ratio (CAR), and performance as managerial efficiency. Of these aspects, ROE and ROA have been used as variables to explain managerial efficiency. Weak credit monitoring and poor control over operating expenses led to decreased cost efficiency, which supports the bad management theorem [

5]. The bad management theory is also found by [

20] while applying NPL as technical efficiency. Shreds of evidence were found on the “too big to fail” syndrome in the US banking sector and it was also argued that an increase in income negatively impacts NPLs [

21]. Cost efficiency also impacts NPLs. Poor management and moral hazards have been positively associated with variations in NPLs. Managerial efficiency as a proxy to ROA has negative connections with NPLs [

22]. Podpiera and Weill [

4] used cost efficiency to describe management quality to find an underlying relationship with NPLs. They performed Granger causality tests to show the unconditional connection of inefficiency to NPLs. Louzis, Vouldis et al. [

3] using dynamic panel data found management quality along with GDP, unemployment, interest rate, and public debt are the determinants of NPLs. In a very recent study (2019) on the banking system structure of Bangladesh, Barun Kumar Dey [

23] found that poor follow-up of loans after disbursement and lack of willingness to write off bad loans are the root causes that cause NPLs to increase. He also argued that NPLs limit lending capacity, the trickle-down effect of which slows down economic growth in the long run. Also, a high level of NPLs leads to higher requirements of loan loss provisioning, which in turn affects ROA and ROE and creates a threat for solvency and liquidity. Finally, NPLs change the nature risk preferences of the managers that leads to a higher cost of funds and less efficiency.

Vardar and Özgüler [

24] found the presence of a steady and long-run affiliation between non-performing loans, macroeconomic variables, and bank-specific factors. Inflation and unemployment were found to be positively and significantly associated with NPLs. Bardhan and Mukherjee [

25] found results supporting the ‘bad management hypothesis’ predicting negative future relationships with NPAs (non-performing assets). They used performance as a proxy for managerial efficiency. They also found capital adequacy ratio (CAR) requirements had an impact on the NPAs of banks. According to their research, large banks have more default rates compared to smaller ones.

Rajan, Bardhan, and Mukherjee [

25,

26] identified that future NPLs are related to past earnings and increases in profit can reduce NPLs. They also explained that managers could manipulate their power to alter credit policies to inflate current earnings, change the terms of the loan, and relax the conditions, which may lead to bad loans. Using the data of 129 Spanish banks from 1993 to 2003 García-Marco and Robles-Fernández [

27] found that higher ROEs had been the key reason to boost risk and higher default rates. ROE has positive associations with elevated NPLs [

28].

Changes in credit management policy, loan interest rates, fees, and commissions are also other determinants of NPLs. GDP and ROA have a negative impact while unemployment and interest rates have a positive impact on NPLs [

14]. In a study in the United States, it was found that elevated interest rates and superfluous lending as internal aspects and economic conditions as external aspects have a significant positive connection to NPLs [

29]. Structural differences between countries can create differences in the efficiency of banks as well [

30].

Kjosevski [

31] conducted sector-wise research and found NPLs of both the enterprise and household were negatively sensitive to profitability, loan growth, and better economic conditions while banks’ solvency and unemployment were positively correlated. The authors of [

19] examined NPLs determinants in the Eurozone and, like past examinations, found bank-specific and macroeconomic elements had a remarkable impact clarifying variations in NPLs [

32,

33].

We found researches on Bangladesh covering a research period of 5 to 20 years. A synopsis is given in

Table 1.

4. Results and Discussion

4.1. Unit Root Test

Unit root tests (

Table 3) for macroeconomic variables with ADF found two macroeconomic variables of lnGDPGR and lnEXR found to be stationary at the level I (0) while lnCPI, indoor, and lnUNEM became stationary at first differentiation as indicated by I (1) at the 5% level of confidence. On the other hand, in PP, only lnGDPGR was stationary at the level I (0); all other variables became stationary, except lnCPI, after first differentiation I (1) at a 5% confidence level. lnCPI became stationary at first differentiation I (1) with 10% at the confidence level. Unit root tests (

Table 3) for industry-specific variables with ADF found two macroeconomic variables, lnNOP (at 10% confidence level) and lnDPR, to be stationary at the level I (0) while lnBNLN, lnLIQ, and lnLDR became stationary at first differentiation as indicated by I (1) at the 5% level of confidence. On the other hand, in PP, all the variables became stationary after first differentiation I (0).

4.2. ARDL Model

We constructed two different models to reduce the multi-collinearity problem among the variables. The co-integration relationship was examined among the determinants (i.e., analyzing the zero hypotheses (

H0:

λ = 1,

λ = 2 …

λn = 0). From the ARDL bounds test, it is apparent that (

Table 4) the F statistics are 30.609 and 15.34 for the first and second models. The F values are significant, and in both models, the F statistics are greater than the upper limit. So, we reject the null hypothesis and agree that there are co-integrations among the determinants. Then, we used Akaike’s information criterion (AIC) criterion to choose optimal lag lengths for each model (

Table 5). For macroeconomic variables, the AIC selects the ARDL (4,3,4,3,2,1) specification and for industry-specific variables (3,3,4,1,4,2). The reason for using AIC is that AIC provides a smaller standard deviation than the Schwarz information criterion (SIC) when running in a model (Pesaran & Pesraran, 1997). We tested both long-run associations and short-run dynamics (error correction model) in the ARDL model (

Table 6 and

Table 7). The coefficients were found to have multiple connotations between NPLs and macroeconomic and industry-specific variables.

4.2.1. ARDL Long-Run Results

Among the macroeconomic variables, the results identified that lnGDPGR has a significant negative effect on the lnNPLR, meaning that as the economy becomes stronger, bad lending decreases. If there is an increase of 1% in economic growth, non-performing loans will decrease by 1.40% in the long run in Bangladesh.

lnCPI also has a negative relationship with lnNPLR, but in this case, the relationship is insignificant in the long run. Domestic credit growth (lnDOCR) and exchange rates (lnEXR) both have significant positive relationships with the bad loan ratio (lnNPLR) while unemployment (lnUNEM) in the country has a significant negative relation with increasing bad loans. With every 1% increase in both the domestic credit and exchange rates, there is a 1.07% and 3.76% increase in non-performing loans, respectively. Surprisingly, with the decrease of non-performing loans by 7.64%, there is a 1% increase in unemployment.

The long-run results of industry-specific variables show that bank loan growth (lnBKLN) has a negative association with the non-performing loan ratio (lnNPLR). Net operating profit (lnNOP) and deposit rates (lnDPR) also have the same impact over non-performing loans with significant p values, which means that with the growth of bank lending by 0.52%, there will be a decrease of 1% bad loan, which indicates healthy behavior by the banking sector. NPL reduces bank profitability by 0.02% when it increases by 1%, and also a 1% increase in lnNPLR reduces the capacity of the banks to provide depositors good returns, which is 0.76%. Finally, a 1% increase in lending rates (lnLDR) and liquidity (lnLIQ) increase non-performing loans by 3.79% and 2.67%, respectively.

In both models, the R2, and the adjusted R2 were remarkably good. The R2 and the adjusted R2 for macroeconomic variables are 0.9618 and 0.8971, respectively, while for industry-specific variables, it is 0.9338 and 0.8219, respectively, meaning the models fit quite well, which means that the models can explain 96.18% and 93.38% of the changes in non-performing loans.

4.2.2. ARDL Short-Run Results

The short-run outcomes suggest the growth of GDP has a significant positive influence on lnNPLR. Meaning that if there is a growth of 1% in GDP in Bangladesh, the non-performing loans of banks will rise by 0.36%. Then, only lnUNEM has a significant positive relation with NPLR. A 1% increase in unemployment will cause a 2.45% decrease in bad loans in the short run. The other three variables, lnCPI, lnDOCR, and lnEXR, affect lnNPLR negatively, with lnDOCR being the only insignificant variable. To be specific, a 1% increase in all these variables can cause a 5.01%, 0.27%, and 0.88% decrease consecutively in lnNPLR.

The short-run results of industry-specific variables show that bank loan growth (lnBKLN) has an insignificant positive relationship with non-performing loans (lnNPLR). Net operating profit (lnNOP) and deposit rates (lnDPR) also have the same impact over non-performing loans, which is statistically significant, while liquidity (lnLIQ) and lending rates (lnLDR) were found to have a statistically significant negative connection with non-performing loans.

4.3. Co-Integration Test

We found four co-integration relationships in the first model and for the second model, we found two co-integrating connections. We considered trace statistics to figure out the co-integrating equations at a the 5% level of significance. The existence of more than one co-integrating equation indicates a long-run convergence of the two models (

Table 8).

4.4. Vector Error Correction (Vec) Model Results

The VECM was applied to assess the long-run and short-run coefficients (

Table 9). We found two lag periods for macroeconomic variables and four lag periods for industry-specific variables using the Schwarz information criterion. We selected the lag length of SIC criterions as it gives better results than AIC criterions. We then calculated the long and short-run coefficients, putting lag length outcomes in the VECM.

The first model states that lnNPLR converges to long-run equilibrium with a 25.58% speed of adjustment every year by the influence of the variables, lnGDPGR, lnCPI, lnDOCR, lnUNEM, and lnEXR. The second model suggests an 18.85% speed of adjustment in lnNPLR by the influence of lnBKLN, lnLIQ, lnNOP, lnLDR, and lnDPR. The results from both the models recommend that long-run adjustment in the independent variables has substantial influence compared to short-run variables on NPLR. The long-run equations are explained in the following manner:

Model 1: In the case of macroeconomic variables, when lnGDPGR has a negative movement by 1%, non-performing loans lnNPLR will rise by 0.4780902%. lnCPI and lnUNEM have the same negative relationship as lnGDPGR, with 0.1832198% and 6.997589%, respectively. Meanwhile, domestic credit lnDOCR and exchange rates lnEXR, if appreciated by 1%, will cause an escalation in non-performing loans (lnNPLR) by 0.5250594% and 3.293177% respectively.

Model 2: Among industry-specific variables, when bank lending (lnBKLN) is decreased by 1%, non-performing loans (lnNPLR) will increase by 0.3681242%. Net operating profit (lnNOP) and deposit rates (lnDPR) also have an inverse relationship with lnNPLR. When lnNOP and lnDPR decrease by 1%, lnNPLR increases by 0.0602165%, and 2.718319% respectively. On the contrary, at a 1% increase in banks’ liquidity (lnLIQ) and lending rates (lnLDR), bad loan (lnNPLR) is hyped by 0.424397% and 4.923853%, respectively.

To check if there is any autocorrelation, we performed the Lagrange-multiplier test (

Table 10). Both models are free from the autocorrelation problem.

4.5. Robustness of the Study

The overall stability of the models was examined through a few diagnostic tests of the ARDL model (

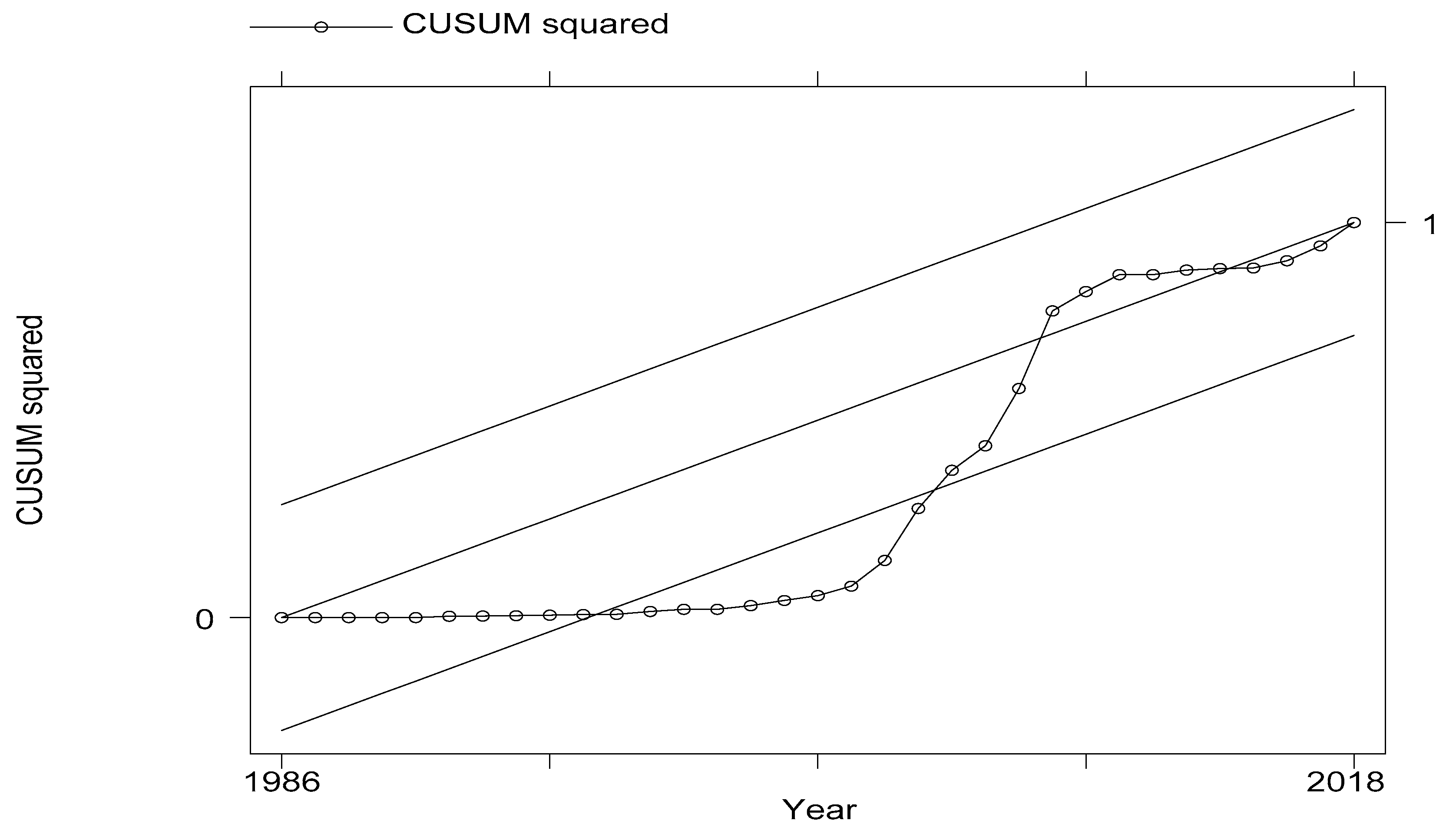

Table 11). The Durbin–Watson tests (for autocorrelation) suggest that neither the macroeconomic nor the industry-specific variables have autocorrelations among them. Again, for the Jarque–Bera, Breusch–Godfrey (serial correlation test), and White’s tests (homoscedasticity test), we cannot reject the zero hypothesis as all the coefficients are not significant, and hence, the models are normal; there is no serial correlation among the variables and the models are free from the heteroscedasticity problem. We checked autocorrelation for VECM and found no autocorrelation problem through the Lagrange-multiplier test. The CUSUM (cumulative sum) was tested to check the model stability (

Figure 3 and

Figure 4). The model with macroeconomic variables seems okay, with a slight deviation in the middle. Again, the results of VECM are consistent with ARDL estimates as the signs of the coefficients are similar (

Table 12).

5. Conclusions

Throughout the study, we found significant shreds of evidence that our hypothesis of industry-specific and macroeconomic determinants influencing non-performing loans in Bangladesh is being established. To the best of our information, this research is the first to discover the impact of both industry-specific and macroeconomic determinants of NPLs in Bangladesh at a time horizon of 40 years. Also, very few studies, we found, had been conducted comparing the results in ARDL and VECM. Hence, it can be considered a robust study.

Long-run convergences of ARDL show that non-performing loans negatively impact economic growth. That means as the economy advances to good shape, entrepreneurs are more capable of repaying loans. The movement of exchange rates is another important factor, the consequence of which has a positive impact on NPLs. Results show as the exchange rate increases, entrepreneurs have to pay more on their imports causing a reduction in the capacity to repay. Again, with the increase in NPLs, unemployment rises in the short run, which can create instability in the economy as well.

Loan growth in the long run decreases non-performing loans. As the lending horizon has been increasing during the last decade in small and medium enterprises (SMEs) and micro-finances, non-performing loans have decreased proportionately. We may look into this fact in our future research as this is not the focal point of this study. In the short run, NPLs increase with loan growth. Banks’ profitability decreases with higher NPLs as banks need to increase the base of loan loss provisions for future losses. This has a spillover effect on the lending interest rates and the deposit rates as well. Lending interest rates increase and deposit rates decrease with the growth of NPLs. Finally, the liquidity of banks needs to be handled carefully so that banks do not become too ambitious and make bad lending. There is a high chance of excess liquidity being wrongly managed by the bankers, as our research found a positive correlation between bad loans and liquidity. Central banks and policymakers can step into this to act as a guide in this regard. Banks may be controlled by implementing contractionary lending policies during an economic downturn and expansionary lending policies during economic growth to ensure their sustainability in the long run. Regulatory bodies may carefully monitor the growth of domestic credit and exchange rate fluctuation to scale down the impact of bad loans in the economy.

The results obtained piloting econometric examination can be used to project fundamental grounds of NPLs in the economy of Bangladesh. It will help policymakers of developing countries like Bangladesh to take enough measures to control NPLs or take precautions against it. The contribution of the current study puts light on future research. For example, future research can be conducted in the developing and emerging economies like Bangladesh.

{kind=link}

{kind=link}

{kind=link}

{kind=link}