The Role of Sustainability in Brand Equity Value in the Financial Sector

Abstract

1. Introduction

2. Literature Review

2.1. Intangible Assets and Brand Value

2.2. Sustainability Brands and Financial Performance

2.3. Sustainability Brands and the Financial Sector

2.4. Sustainability Brands and Marketing Strategies

3. Model, Methodology and Data

3.1. Model

3.2. Method

3.3. Data

4. Empirical Results

5. Conclusions, Managerial Implications, limitations and Further Research

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

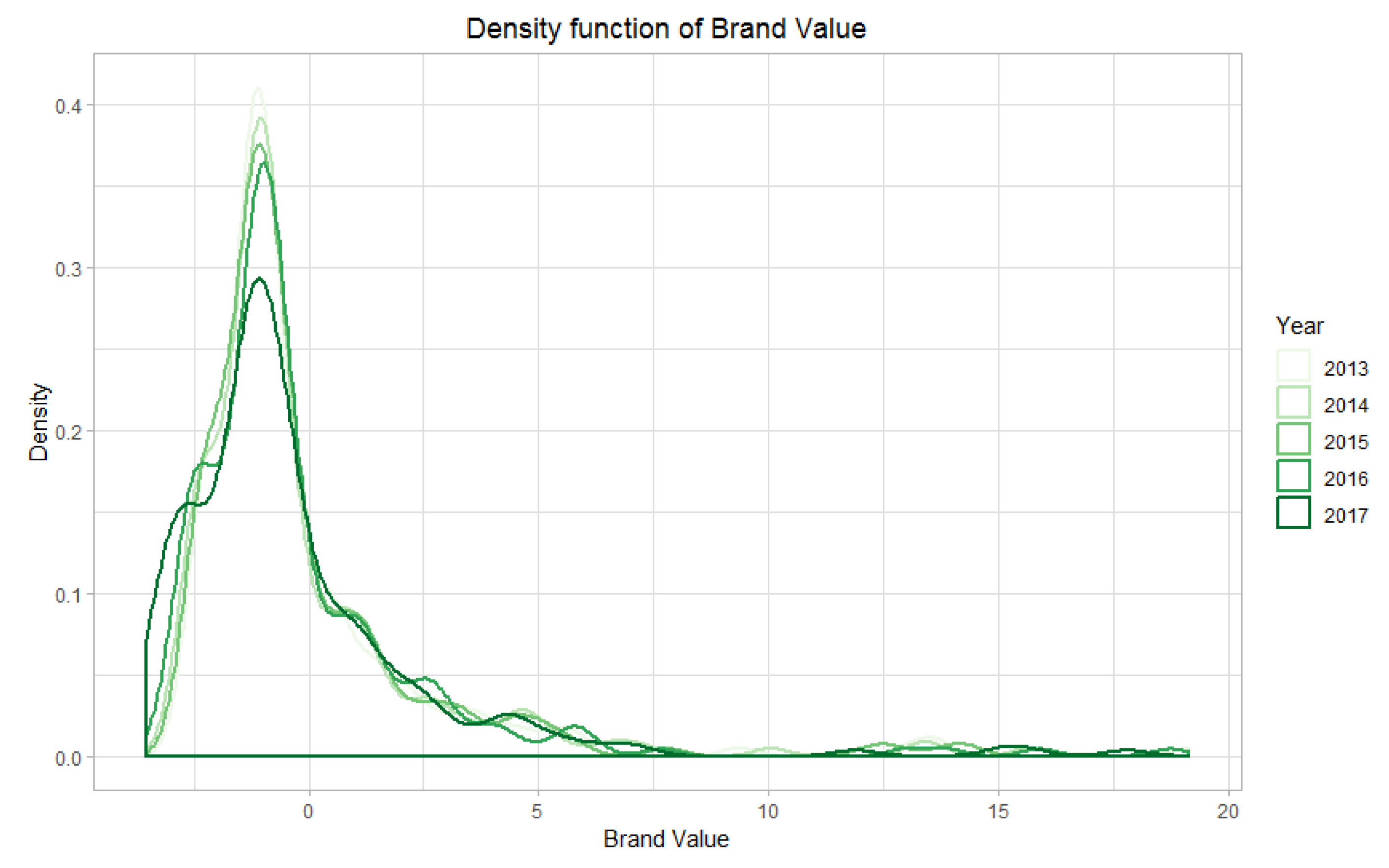

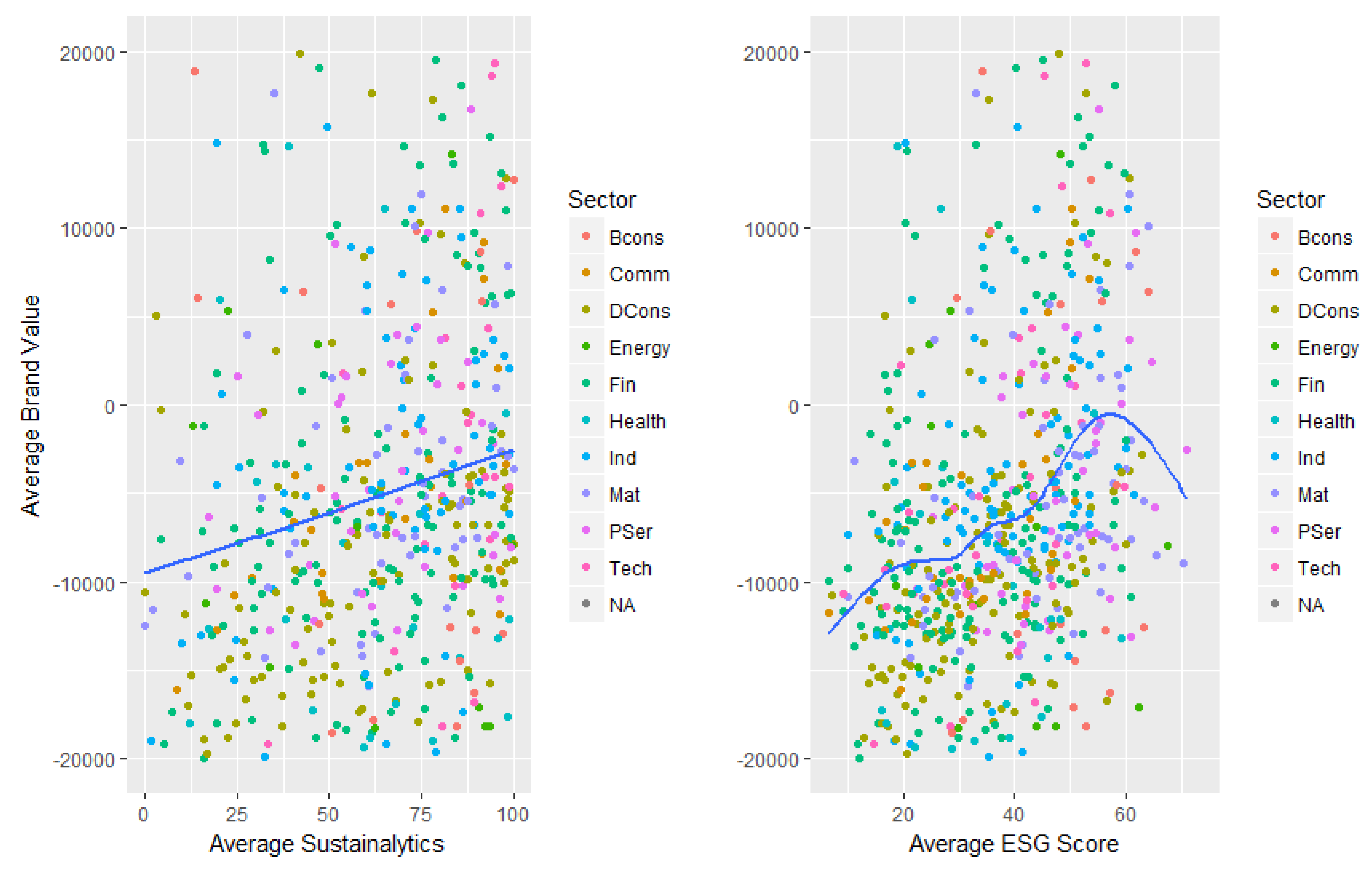

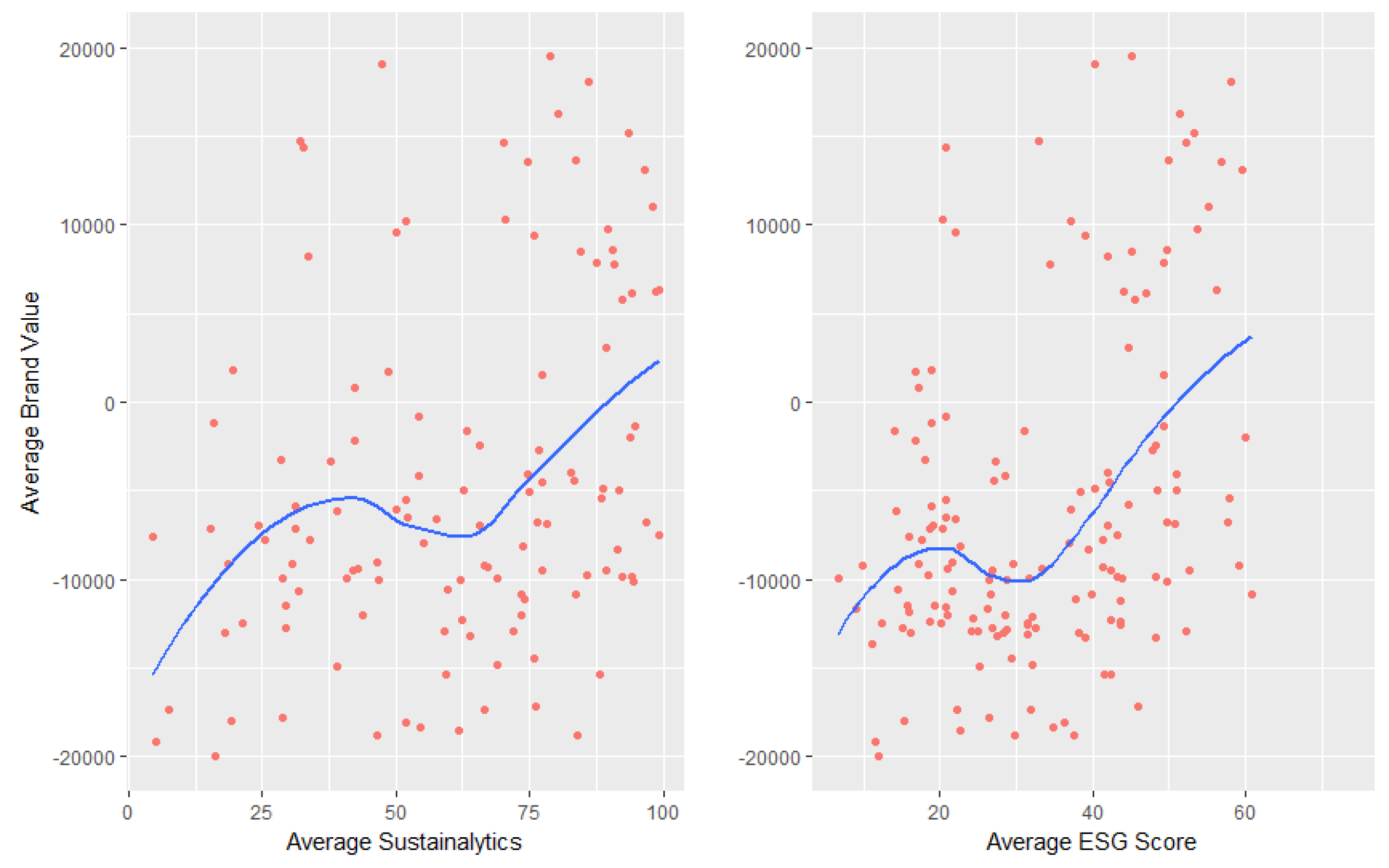

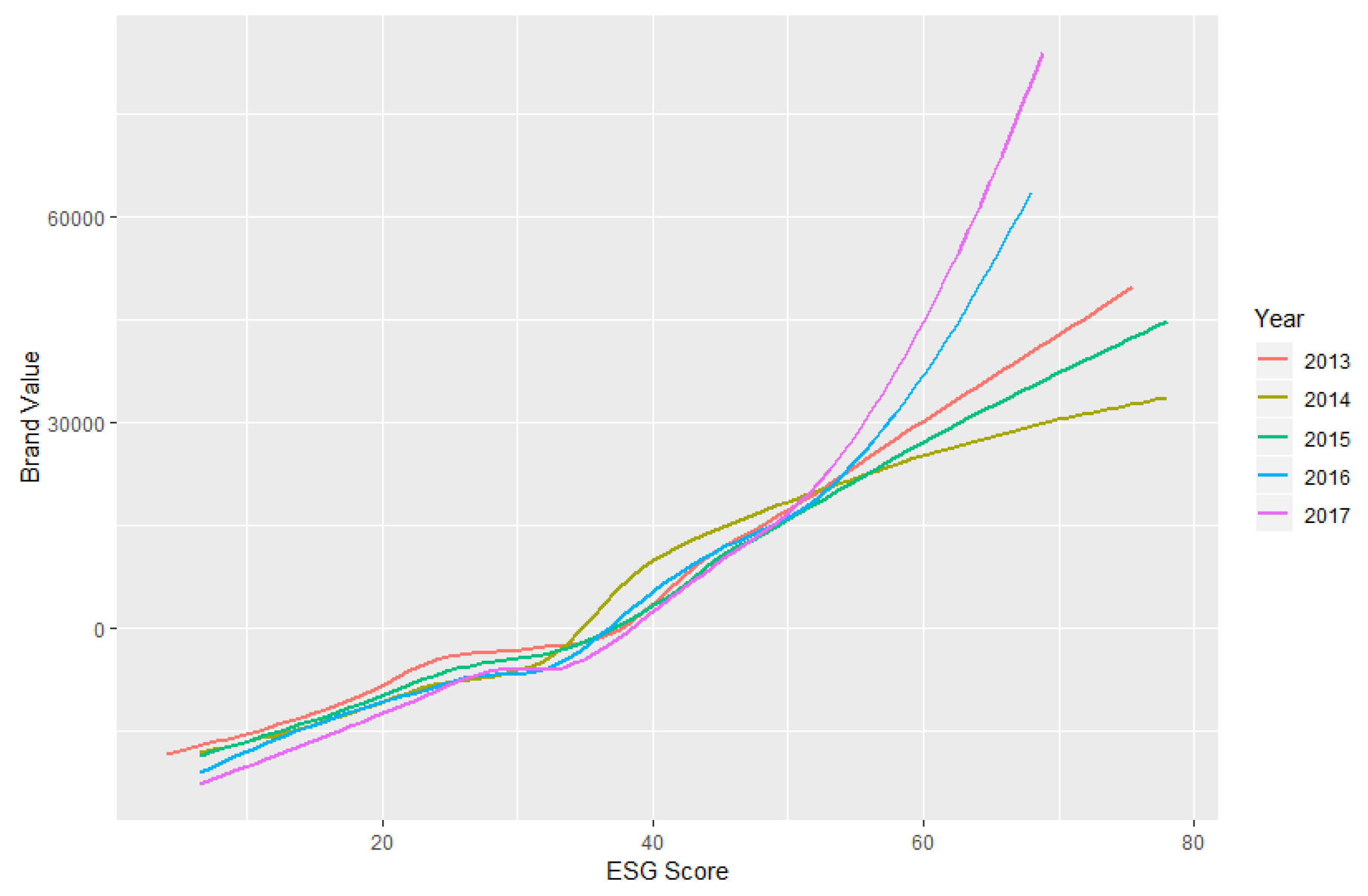

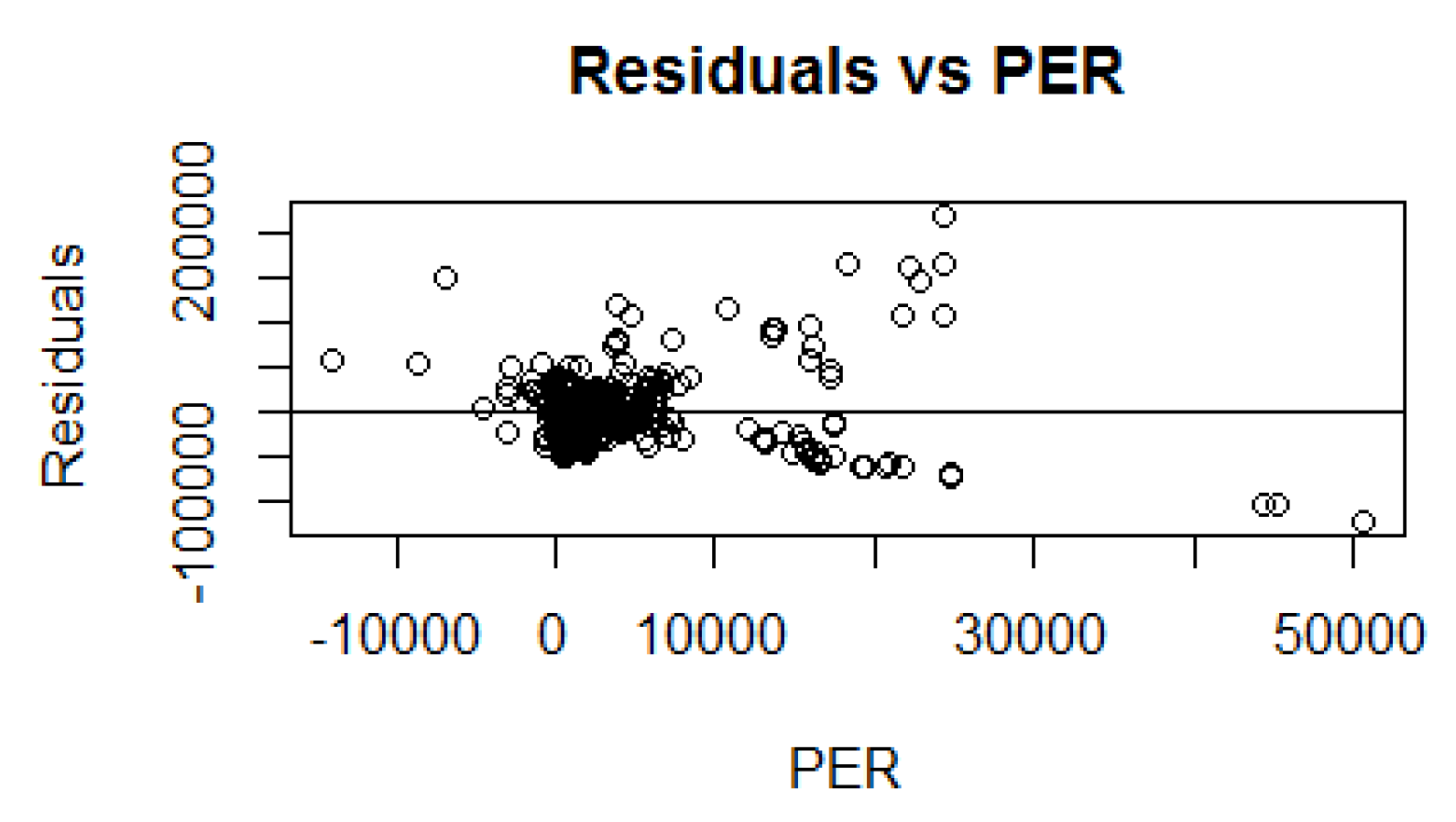

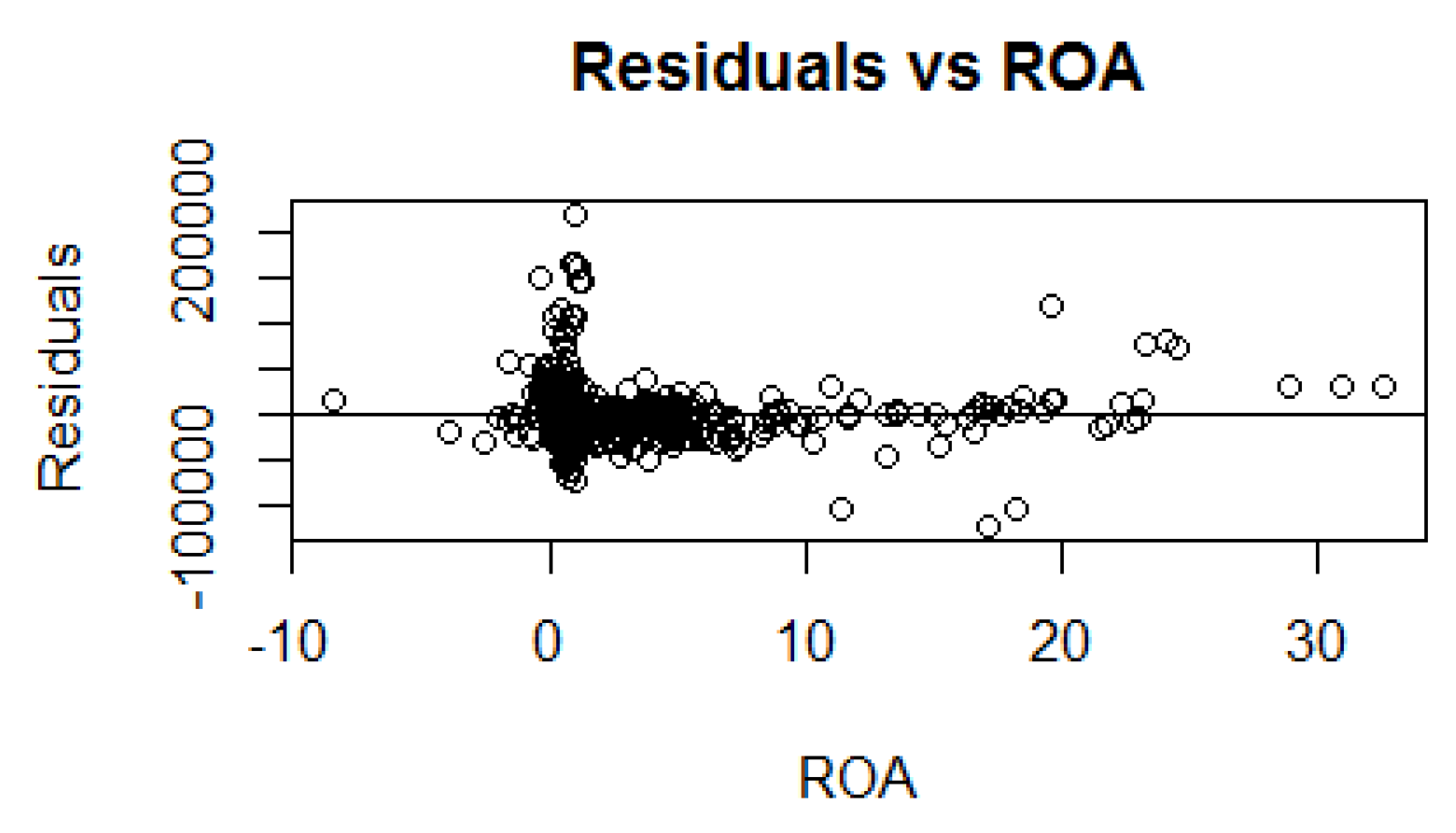

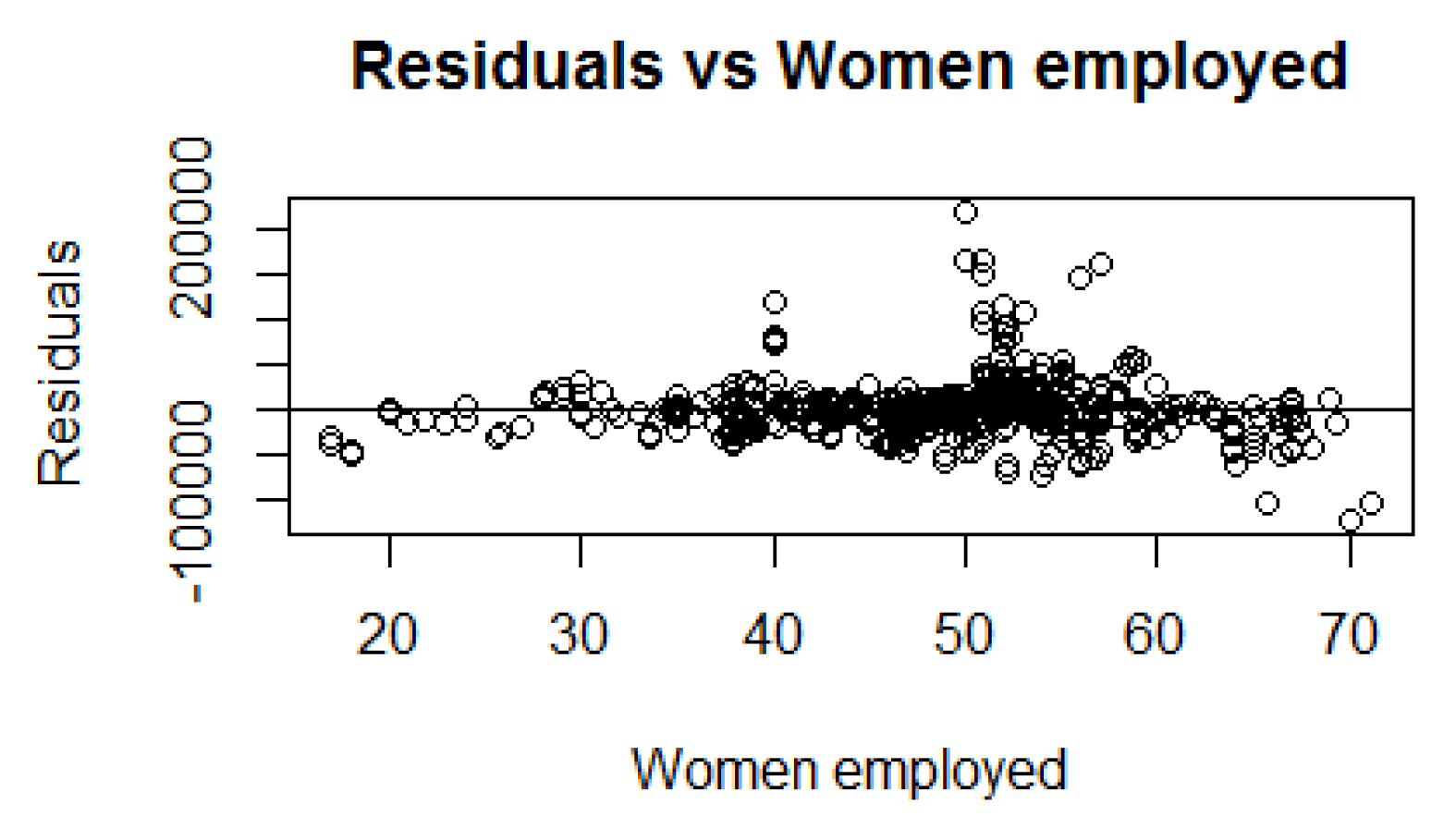

Appendix A. Model Validation Graphs

References

- Hale, J. Sustainable Funds U.S. Landscape Report; Morningstar Inc.: Chicago, IL, USA, 2018. [Google Scholar]

- Alliance, G.S.I. Global Sustainable Investment Review. 2018. Available online: http://www.gsi-alliance.org/wp-content/uploads/2019/03/GSIR_Review2018.3.28.pdf (accessed on 11 November 2019).

- Damodaran, A. Valuation approaches and metrics: a survey of the theory and evidence. Found. Trends Financ. 2007, 1, 693–784. [Google Scholar] [CrossRef]

- Dull, R.B.; Tegarden, D.P. Using control charts to monitor financial reporting of public companies. Int. J. Account. Inf. Syst. 2004, 5, 109–127. [Google Scholar] [CrossRef]

- Staudt, S.; Shao, C.Y.; Dubinsky, A.J.; Wilson, P.H. Corporate social responsibility, perceived customer value, and customer-based brand equity: A cross-national comparison. J. Strateg. Innov. Sustain. 2014, 10, 65. [Google Scholar]

- Sheth, J.N.; Sinha, M. B2B branding in emerging markets: A sustainability perspective. Ind. Mark. Manag. 2015, 51, 79–88. [Google Scholar] [CrossRef]

- Churchill, G.A., Jr. A paradigm for developing better measures of marketing constructs. J. Mark. Res. 1979, 16, 64–73. [Google Scholar] [CrossRef]

- Srinivasan, S.; Hanssens, D.M. Marketing and firm value: Metrics, methods, findings, and future directions. J. Mark. Res. 2009, 46, 293–312. [Google Scholar] [CrossRef]

- McInnis, J.M.; Monsen, B. The Operating Returns to Acquired Intangible Assets; SSRN 3279123; SSRN: Rochester, NY, USA, 2018. [Google Scholar]

- Anson, W.; Drews, D.C. The Intangible Assets Handbook: Maximizing Value from Intangible Assets; American Bar Association: Chicago, IL, USA, 2007. [Google Scholar]

- Smith, G.V.; Parr, R.L. Valuation of Intellectual Property and Intangible Assets; Wiley: Hoboken, NJ, USA, 2000; Volume 13. [Google Scholar]

- Osterwalder, A.; Pigneur, Y. Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers; John Wiley & Sons: Hoboken, NJ, USA, 2010. [Google Scholar]

- Wood, L. Brands and brand equity: Definition and management. Manag. Decis. 2000, 38, 662–669. [Google Scholar] [CrossRef]

- Feldwick, P. What is brand equity anyway, and how do you measure it? Mark. Res. Soc. J. 1996, 38, 1–17. [Google Scholar] [CrossRef]

- Motameni, R.; Shahrokhi, M. Brand equity valuation: A global perspective. J. Prod. Brand Manag. 1998, 7, 275–290. [Google Scholar] [CrossRef]

- Farris, P.; Shames, E.; Gregg, E. Perspectives on Brand Equity; Darden Case No. UVA-M-0668; SSRN: Rochester, NY, USA, 2018. [Google Scholar]

- Gidwani, B. The Link between Brand Value and Sustainability; The Conference Board: New York, NY, USA, 2013. [Google Scholar]

- Friedman, M. The social responsibility of business is to increase its profits. In Corporate Ethics and Corporate Governance; Springer: Berlin, Germany, 2007; pp. 173–178. [Google Scholar]

- Vance, S.C. Are socially responsible corporations good investment risks. Manag. Rev. 1975, 64, 19–24. [Google Scholar]

- Wang, Y.G. Corporate social responsibility and stock performance—Evidence from Taiwan. Mod. Econ. 2011, 2, 788. [Google Scholar] [CrossRef]

- Aupperle, K.E.; Carroll, A.B.; Hatfield, J.D. An empirical examination of the relationship between corporate social responsibility and profitability. Acad. Manag. J. 1985, 28, 446–463. [Google Scholar]

- Richardson, A.J.; Welker, M.; Hutchinson, I.R. Managing capital market reactions to corporate social resposibility. Int. J. Manag. Rev. 1999, 1, 17–43. [Google Scholar] [CrossRef]

- Høgevold, N.M.; Svensson, G.; Wagner, B.; Petzer, D.J.; Klopper, H.; Carlos Sosa Varela, J.; Padin, C.; Ferro, C. Sustainable business models: Corporate reasons, economic effects, social boundaries, environmental actions and organizational challenges in sustainable business practices. Balt. J. Manag. 2014, 9, 357–380. [Google Scholar]

- Barnett, M.L. Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Acad. Manag. Rev. 2007, 32, 794–816. [Google Scholar] [CrossRef]

- Turban, D.B.; Greening, D.W. Corporate social performance and organizational attractiveness to prospective employees. Acad. Manag. J. 1997, 40, 658–672. [Google Scholar]

- Griffin, J.J.; Mahon, J.F. The corporate social performance and corporate financial performance debate: Twenty-five years of incomparable research. Bus. Soc. 1997, 36, 5–31. [Google Scholar] [CrossRef]

- Wagner, M.; Schaltegger, S. The effect of corporate environmental strategy choice and environmental performance on competitiveness and economic performance:: an empirical study of EU manufacturing. Eur. Manag. J. 2004, 22, 557–572. [Google Scholar] [CrossRef]

- Fadul, J. Business Ethics, Corporate Social Responsibility, and Firm Value in the Oil and Gas Industry; Society of Petroleum Engineers: London, UK, 2004. [Google Scholar]

- Ameer, R.; Othman, R. Sustainability practices and corporate financial performance: A study based on the top global corporations. J. Bus. Ethics 2012, 108, 61–79. [Google Scholar] [CrossRef]

- Al-Tuwaijri, S.A.; Christensen, T.E.; Hughes Ii, K. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Account. Organ. Soc. 2004, 29, 447–471. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B. The corporate social performance–financial performance link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- McGuire, J.B.; Sundgren, A.; Schneeweis, T. Corporate social responsibility and firm financial performance. Acad. Manag. J. 1988, 31, 854–872. [Google Scholar]

- Brammer, S.; Brooks, C.; Pavelin, S. Corporate social performance and stock returns: UK evidence from disaggregate measures. Financ. Manag. 2006, 35, 97–116. [Google Scholar] [CrossRef]

- Farooq, O. Financial centers and the relationship between ESG disclosure and firm performance: Evidence from an emerging market. J. Appl. Bus. Res. (JABR) 2015, 31, 1239–1244. [Google Scholar] [CrossRef]

- Redclift, M. Sustainable development (1987–2005): An oxymoron comes of age. Sustain. Dev. 2005, 13, 212–227. [Google Scholar] [CrossRef]

- Kates, R.W.; Clark, W.C.; Corell, R.; Hall, J.M.; Jaeger, C.C.; Lowe, I.; McCarthy, J.J.; Schellnhuber, H.J.; Bolin, B.; Dickson, N.M.; et al. Sustainability science. Science 2001, 292, 641–642. [Google Scholar] [CrossRef]

- Boulouta, I.; Pitelis, C.N. Who needs CSR? The impact of corporate social responsibility on national competitiveness. J. Bus. Ethics 2014, 119, 349–364. [Google Scholar] [CrossRef]

- Bansal, P. The corporate challenges of sustainable development. Acad. Manag. Perspect. 2002, 16, 122–131. [Google Scholar] [CrossRef]

- Muff, K.; Dyllick, T.L. An Organizational Roadmap of Business Sustainability; SSRN 2442211; SSRN: Rochester, NY, USA, 2014. [Google Scholar]

- Han, H.; Hsu, L.T.J.; Lee, J.S.; Sheu, C. Are lodging customers ready to go green? An examination of attitudes, demographics, and eco-friendly intentions. Int. J. Hosp. Manag. 2011, 30, 345–355. [Google Scholar] [CrossRef]

- Lubin, D.A.; Esty, D.C. The sustainability imperative. Harv. Bus. Rev. 2010, 88, 42–50. [Google Scholar]

- Ireton, K.; Valido, V.; Ramirez, L. Sustainability Reporting in the Financial Sector: A Governmental Approach; United Nations Environment Programme: Nairobi, Kenya, 2017. [Google Scholar]

- European Commission. Financing a Sustainable Economy: Final Report by the High-Level Expert Group on Sustainable Finance; European Commission: Brussels, Belgium, 2018. [Google Scholar]

- Jeucken, M. Sustainable Finance and Banking: The Financial Sector and the Future of the Planet; Routledge: Abingdon, UK, 2010. [Google Scholar]

- Wiek, A.; Weber, O. Sustainability challenges and the ambivalent role of the financial sector. J. Sustain. Financ. Invest. 2014, 4, 9–20. [Google Scholar] [CrossRef]

- Kaufer, K. Social responsibility as a core business model in banking: A case study in the financial sector. J. Sustain. Financ. Invest. 2014, 4, 76–89. [Google Scholar] [CrossRef]

- Carolina Rezende de Carvalho Ferreira, M.; Amorim Sobreiro, V.; Kimura, H.; Luiz de Moraes Barboza, F. A systematic review of literature about finance and sustainability. J. Sustain. Financ. Invest. 2016, 6, 112–147. [Google Scholar] [CrossRef]

- Epstein, M.J.; Roy, M.J. Sustainability in action: Identifying and measuring the key performance drivers. Long Range Plan. 2001, 34, 585–604. [Google Scholar] [CrossRef]

- Piercy, N.F.; Lane, N. Corporate social responsibility: Impacts on strategic marketing and customer value. Mark. Rev. 2009, 9, 335–360. [Google Scholar] [CrossRef]

- Lai, C.S.; Chiu, C.J.; Yang, C.F.; Pai, D.C. The effects of corporate social responsibility on brand performance: The mediating effect of industrial brand equity and corporate reputation. J. Bus. Ethics 2010, 95, 457–469. [Google Scholar] [CrossRef]

- Hsu, K.T. The advertising effects of corporate social responsibility on corporate reputation and brand equity: Evidence from the life insurance industry in Taiwan. J. Bus. Ethics 2012, 109, 189–201. [Google Scholar] [CrossRef]

- Kang, S.; Hur, W.M. Investigating the antecedents of green brand equity: A sustainable development perspective. Corp. Soc. Responsib. Environ. Manag. 2012, 19, 306–316. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Kaplan, R.E.; Norton, D.P.; Norton, D.P.; Davenport, T.H. Strategy Maps: Converting Intangible Assets into Tangible Outcomes; Harvard Business Press: Cambridge, MA, USA, 2004. [Google Scholar]

- Bansal, P. Evolving sustainably: A longitudinal study of corporate sustainable development. Strateg. Manag. J. 2005, 26, 197–218. [Google Scholar] [CrossRef]

- Nidumolu, R.; Prahalad, C.K.; Rangaswami, M.R. Why sustainability is now the key driver of innovation. Harv. Bus. Rev. 2009, 87, 56–64. [Google Scholar]

- Kerr, J.E. Sustainability Meets Profitability: The Convenient Truth of How the Business Judgment Rule Protects a Board’s Decision to Engage in Social Entrepreneurship. Cardozo Law Rev. 2007, 29, 623. [Google Scholar] [CrossRef]

- Dyer, J.H.; Singh, H. The relational view: Cooperative strategy and sources of interorganizational competitive advantage. Acad. Manag. Rev. 1998, 23, 660–679. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Strategy and society: The link between corporate social responsibility and competitive advantage. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar] [PubMed]

- Giuntini, R. An introduction to reverse logistics for environmental management: A new system to support sustainability and profitability. Environ. Qual. Manag. 1996, 5, 81–87. [Google Scholar] [CrossRef]

- Hall, R. A framework linking intangible resources and capabiliites to sustainable competitive advantage. Strateg. Manag. J. 1993, 14, 607–618. [Google Scholar] [CrossRef]

- First, I.; Khetriwal, D.S. Exploring the relationship between environmental orientation and brand value: Is there fire or only smoke? Bus. Strategy Environ. 2010, 19, 90–103. [Google Scholar] [CrossRef]

- Konar, S.; Cohen, M.A. Does the market value environmental performance? Rev. Econ. Stat. 2001, 83, 281–289. [Google Scholar] [CrossRef]

- Balmer, J.M.; Gray, E.R. Corporate identity and corporate communications: Creating a competitive advantage. Corp. Commun. Int. J. 1999, 4, 171–177. [Google Scholar] [CrossRef]

- Fahy, J.; Farrelly, F.; Quester, P. Competitive advantage through sponsorship: A conceptual model and research propositions. Eur. J. Mark. 2004, 38, 1013–1030. [Google Scholar] [CrossRef]

- Aaker, D.A. Measuring brand equity across products and markets. Calif. Manag. Rev. 1996, 38. [Google Scholar] [CrossRef]

- Madden, T.J.; Fehle, F.; Fournier, S. Brands matter: An empirical demonstration of the creation of shareholder value through branding. J. Acad. Mark. Sci. 2006, 34, 224–235. [Google Scholar] [CrossRef]

- Fernández, F.L.; Fernandez, P.; Fernández, P.; López, P.F. Valuation Methods and Shareholder Value Creation; Academic Press: Cambridge, MA, USA, 2002. [Google Scholar]

- Treynor, J. The investment value of brand franchise. Financ. Anal. J. 1999, 55, 27–34. [Google Scholar] [CrossRef]

- Bloomberg, C. Classification Data. 2018. Available online: https://www.bloomberg.com/europe (accessed on 3 June 2018).

- Allison, P. Prediction vs. Causation in Regression Analysis; Statistical Horizons: Ardmore, PA, USA, 2014. [Google Scholar]

- Blackburn, V.B.; Iles, P.; Shrader, C. Women in management and firm financial performance: An exploratory study. J. Manag. Issues 1997, 9, 355–373. [Google Scholar]

- Crifo, P.; Forget, V.D. Think global, invest responsible: Why the private equity industry goes green. J. Bus. Ethics 2013, 116, 21–48. [Google Scholar] [CrossRef]

- Christofi, A.; Christofi, P.; Sisaye, S. Corporate sustainability: historical development and reporting practices. Manag. Res. Rev. 2012, 35, 157–172. [Google Scholar] [CrossRef]

- Fowler, S.J.; Hope, C. A critical review of sustainable business indices and their impact. J. Bus. Ethics 2007, 76, 243–252. [Google Scholar] [CrossRef]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Financ. Invest. 2015, 5, 210–233. [Google Scholar] [CrossRef]

- Fox, J. Applied Regression Analysis and Generalized Linear Models; Sage Publications: Thousand Oaks, CA, USA, 2015. [Google Scholar]

- Myers, C.A. Managing brand equity: A look at the impact of attributes. J. Prod. Brand Manag. 2003, 12, 39–51. [Google Scholar] [CrossRef]

- Daily, C.M.; Dalton, D.R. Women in the boardroom: A business imperative. J. Bus. Strategy 2003, 24. [Google Scholar] [CrossRef]

- Kochan, T.; Bezrukova, K.; Ely, R.; Jackson, S.; Joshi, A.; Jehn, K.; Leonard, J.; Levine, D.; Thomas, D. The effects of diversity on business performance: Report of the diversity research network. Hum. Resour. Manag. 2003, 42, 3–21. [Google Scholar] [CrossRef]

- Zoeteman, B.C. Sustainability rating as internal challenge for the financial sector. In CSR und Finanzratings; Springer: Berlin, Germany, 2016; pp. 151–171. [Google Scholar]

- Salinas, G.; Ambler, T. A taxonomy of brand valuation practice: Methodologies and purposes. J. Brand Manag. 2009, 17, 39–61. [Google Scholar] [CrossRef]

- Frost, J. Regression Analysis. An Intuitive Guide for Using and Interpreting Linear Models. ebook 2019. [Google Scholar]

- Flockhart, A. Is measuring Social Return on Investment (SROI) a tool that can be used to raise the profile of Social Enterprises and help attract Investment? 2004. [Google Scholar]

- Vomberg, A.; Homburg, C.; Bornemann, T. Talented people and strong brands: The contribution of human capital and brand equity to firm value. Strateg. Manag. J. 2015, 36, 2122–2131. [Google Scholar] [CrossRef]

- Abratt, R.; Bick, G. Valuing brands and brand equity: Methods and processes. J. Appl. Manag. Entrep. 2003, 8, 21–39. [Google Scholar]

- Bick Geoffrey, N.C. Increasing shareholder value through building customer and brand equity. J. Mark. Manag. 2009, 25, 117–141. [Google Scholar] [CrossRef]

- Robbin, A. The Potential Value of Brand Accounting, Unpublished MBA Research Report. 1991.

- Fernández, P. Valuation of Brands and Intellectual Capital; IESE Business School: Barcelona, Spain, 2001. [Google Scholar]

- Kanter, R.M. From spare change to real change: The social sector as beta site for business innovation. Harv. Bus. Rev. 1999, 77, 122–123. [Google Scholar] [PubMed]

- Nedungadi, P.; Hutchinson, J. The prototypicality of brands: Relationships with brand awareness, preference and usage. In ACR North American Advances; Advances in Consumer Research: Urbana, IL, USA, 1985. [Google Scholar]

- Herremans, I.M.; Reid, R.E. Developing awareness of the sustainability concept. J. Environ. Educ. 2002, 34, 16–20. [Google Scholar] [CrossRef]

- Yeshin, T. Integrated marketing communications. In The Marketing Book; Routledge: London, UK, 2008; pp. 365–389. [Google Scholar]

- Dolich, I.J. Congruence relationships between self images and product brands. J. Mark. Res. 1969, 6, 80–84. [Google Scholar] [CrossRef]

- Maison, D.; Greenwald, A.G.; Bruin, R.H. Predictive validity of the Implicit Association Test in studies of brands, consumer attitudes, and behavior. J. Consum. Psychol. 2004, 14, 405–415. [Google Scholar] [CrossRef]

- Iacobucci, D.; Ostrom, A.; Grayson, K. Distinguishing service quality and customer satisfaction: The voice of the consumer. J. Consum. Psychol. 1995, 4, 277–303. [Google Scholar] [CrossRef]

- Nguyen, N.; LeBlanc, G. The mediating role of corporate image on customers’ retention decisions: An investigation in financial services. Int. J. Bank Mark. 1998, 16, 52–65. [Google Scholar] [CrossRef]

- White, L.; Yanamandram, V. Why customers stay: Reasons and consequences of inertia in financial services. Manag. Serv. Qual. Int. J. 2004, 14, 183–194. [Google Scholar] [CrossRef]

- Ian Stuart, F.; Tax, S.S. Planning for service quality: an integrative approach. Int. J. Serv. Ind. Manag. 1996, 7, 58–77. [Google Scholar] [CrossRef]

- Randjelovic, J.; O’Rourke, A.R.; Orsato, R.J. The emergence of green venture capital. Bus. Strategy Environ. 2003, 12, 240–253. [Google Scholar] [CrossRef]

- Corfee-Morlot, J.; Marchal, V.; Kauffmann, C.; Kennedy, C.; Stewart, F.; Kaminker, C.; Ang, G. Towards a Green Investment Policy Framework; OECD: Paris, France, 2012. [Google Scholar]

- Vishwanath, T.; Kaufmann, D. Towards Transparency in Finance and Governance; SSRN 258978; SSRN: Rochester, NY, USA, 1999. [Google Scholar]

- Brand, U. Green economy–the next oxymoron? No lessons learned from failures of implementing sustainable development. GAIA-Ecol. Perspect. Sci. Soc. 2012, 21, 28–32. [Google Scholar] [CrossRef]

- Gray, R.; Collison, D.; Bebbington, J. Environmental and social accounting and reporting. In Financial Reporting Today; University of St Andrews: St Andrews, UK, 1998; pp. 179–214. [Google Scholar]

- Schultz, D.E. Understanding and measuring brand equity. Mark. Manag. 2000, 9, 8. [Google Scholar]

- Mori, K.; Christodoulou, A. Review of sustainability indices and indicators: Towards a new City Sustainability Index (CSI). Environ. Impact Assess. Rev. 2012, 32, 94–106. [Google Scholar] [CrossRef]

- Singh, R.K.; Murty, H.R.; Gupta, S.K.; Dikshit, A.K. An overview of sustainability assessment methodologies. Ecol. Indic. 2009, 9, 189–212. [Google Scholar] [CrossRef]

- Dumitriu, D.; Militaru, G.; Deselnicu, D.C.; Niculescu, A.; Popescu, M.A.M. A Perspective Over Modern SMEs: Managing Brand Equity, Growth and Sustainability through Digital Marketing Tools and Techniques. Sustainability 2019, 11, 2111. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Latent Variables | Observable Variables | |

|---|---|---|

| Financial situation | Intangibility | Measured intangible assets |

| ROA | Return on assets | |

| PER | Price–earnings ratio | |

| Index Growth | Average growth of relevant index | |

| Social factors | ESG score | Environmental and Social Governance index |

| Women Directors | Share of female directors | |

| Women Employed | Share of women employed | |

| Unobserved factors | Region | US/EUR |

| Time | Year variable |

| Mean | Median | Std. Dev | Max | Min | |

|---|---|---|---|---|---|

| Brand Value | 157.5 | 47,775.99 | 733,090.4 | −97,977.6 | |

| Intangibility | 0.077 | 0.037 | 0.001 | 0.799 | |

| ROA | 5.930 | 4.881 | 0.09 | 235.4 | |

| PER | 1631 | 535 | 46.8 | 141,828 | −35,206 |

| ESG | 36.861 | 37.191 | 0.151 | 78.512 | 3.509 |

| Women Directors | 74.81 | 80.00 | 0.179 | 100.00 | 0.00 |

| Women Employed | 36.94 | 35.00 | 0.160 | 84.7 | 6.0 |

| Dependent Variable: | |

|---|---|

| Brand Value | |

| Intangibility | 16,732.2 * |

| (8978.9) | |

| ROA | −205.64 * |

| (81.6) | |

| PER | 4.2 *** |

| (0.1) | |

| ESG score | 648.2 *** |

| (81.0) | |

| Women Directors | 103.1 * |

| (52.8) | |

| Women Employed | 8.1 |

| (56.9) | |

| Index growth | 38,296.8 |

| (3085.9) | |

| Region (U.S.) | 11,290.0 *** |

| (3085.9) | |

| Constant | −44,198.7 *** |

| (7497.0) | |

| Observations | 2467 |

| R | 0.281 |

| Adjusted R | 0.278 |

| F-Statistic | 80.101 *** (df = 12; 512) |

| Variable | Test Statistic |

|---|---|

| Intangibility | 1.012 |

| ROA | 1.069 |

| PER | 1.073 |

| ESG score | 1.086 |

| Women Directors | 1.349 |

| Women Employed | 1.047 |

| Index Growth | 3.732 |

| Region | 2.419 |

| Year | 3.396 |

| Variable | Model |

|---|---|

| Statistic | 689.72 |

| Degrees of freedom | 12 |

| p-value | 0 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ajour El Zein, S.; Consolacion-Segura, C.; Huertas-Garcia, R. The Role of Sustainability in Brand Equity Value in the Financial Sector. Sustainability 2020, 12, 254. https://doi.org/10.3390/su12010254

Ajour El Zein S, Consolacion-Segura C, Huertas-Garcia R. The Role of Sustainability in Brand Equity Value in the Financial Sector. Sustainability. 2020; 12(1):254. https://doi.org/10.3390/su12010254

Chicago/Turabian StyleAjour El Zein, Samer, Carolina Consolacion-Segura, and Ruben Huertas-Garcia. 2020. "The Role of Sustainability in Brand Equity Value in the Financial Sector" Sustainability 12, no. 1: 254. https://doi.org/10.3390/su12010254

APA StyleAjour El Zein, S., Consolacion-Segura, C., & Huertas-Garcia, R. (2020). The Role of Sustainability in Brand Equity Value in the Financial Sector. Sustainability, 12(1), 254. https://doi.org/10.3390/su12010254