Abstract

Given their intermediary role and resulting influence on other industries, banks are pivotal in achieving the sustainable development goals (SDGs), for which they approach ecological and social challenges in numerous ways. This study aims at creating a typology of the sustainability strategies that banks implement. To this end, 26 in-depth interviews were conducted within the German banking industry to detect patterns in the sustainable practices of these financial institutions. The strategy types identified are narrow, peripheral, balanced, and integrative, which are similar in structure but substantially different with respect to the kind of practices. Specifically, three main features distinguish these strategies. First, banks focus on either their core businesses or the peripheries of their business. Second, banks can concentrate on social or environmental issues. Third, within the peripheries of their businesses, banks can support external sustainability projects in terms of finances or content. It is also found that the choice of strategy is driven by varying combinations of business, social, and environmental motives. I thus explore the ways by which financial institutions contribute to the realization of the SDGs. The typology established in this work improves understanding with regards to the implementation of sustainability strategies and serves as inspiration to sustainability managers of banks. It also adds to sustainability research in the service context, which, unlike the manufacturing industry, is a widely under-researched setting.

Keywords:

sustainability; SDGs; banking industry; case study; typology; CSR; financial services; sustainable banking 1. Introduction

Banks are widely acknowledged as playing a crucial role in achieving the sustainable development goals (SDGs) [1,2,3]. Given their major impact on society and the environment, these financial institutions increasingly address social and environmental challenges and engage in numerous sustainable practices. To name a few examples, banks may offer green credit funds, use energy-efficient systems, encourage employees to use public transport, provide access to people with disabilities, and choose suppliers who abide by environmental and social principles [4]. Such practices enhance corporate social and environmental performance, which in turn, can positively affect the reputation [5] and financial performance of banks [6,7,8] as well as the affective and behavioral responses of customers [9,10].

The literature provides several guidelines that outline how banks can pursue sustainable development [11,12,13]. Previous studies have also inquired into the extent of effort that financial service providers have devoted in this regard [14,15,16] or specific practices, such as environmental credit risk management [17,18], sustainable project finance [19], and impact investing [20,21]. However, no research has been conducted on what practices banks implement to realize sustainability. Thus, a gap exists with regard to the content of banks’ sustainability strategies, i.e., the patterns that underlie the sustainable practices of banks. Compounding this deficiency is the absence of an explanation on how different types of sustainability strategies and motives that drive sustainable practices are related, despite claims in previous research that different strategies are stimulated by varying motives [22]. I address this shortcoming by creating a typology of the sustainability strategies of banks to enable the identification of motives that prompt the adoption of such strategies. I, therefore, ask the following research questions:

- (1)

- What types of sustainability strategies do banks implement?

- (2)

- What prevailing motives stimulate these different types of strategies?

To illuminate these questions, I conducted 26 in-depth interviews with 26 executives working in the banking industry and carried out analysis that enabled me to uncover four kinds of strategies. These are a narrow, peripheral, balanced, and integrative strategy type, each of which can be understood as a specific pattern of sustainable practices. Although these types are similar in structure, they substantially differ with regards to related practices that are implemented. The typology developed in this work encompasses three main distinctive features, amongst which the most striking is whether banks focus on their core businesses or on the peripheries of their business. The second feature revolves around the directing of focus towards social or environmental issues, and the third indicates that within the peripheries of their businesses, banks can support external sustainability projects in terms of financial or content-related backing. I, likewise, found three principal categories of corporate motives for sustainability, namely, social, environmental, and business rationales. The analysis reveals that decisions regarding the choice of strategy type result from different combinations of motives.

These findings are relevant because knowledge about banks’ sustainability strategies allows for the identification of potential for improvement. In particular, a thorough comprehension of such strategies can benefit stakeholders concerned with environmental and social issues, including sustainability managers, policymakers, and environmental organizations. Such knowledge makes clear where strategic action can be taken to move banks towards contributing to sustainable development goals (SDGs). Such knowledge can also clarify where strategic action can be taken to move banks towards advancing the SDGs. Adding to this advantage is the awareness of motives, which is a particularly valuable source of insights because an extensive understanding of the reasons that underlie banks’ engagement in sustainable practices equally sheds light on why they disregard certain practices. Considering that the banking sector is lagging behind other industries as regards sustainability outcomes [14], the cognition of motives is crucial to the development of tools that effectively encourage banks to implement substantive strategies and thus contribute to the achievement of the SDGs. This study accordingly explores the ways and means by which organizations advance the SDGs.

The research contributes to theory and practice in three ways. First, it presents a typology of sustainability strategies implemented in the banking industry, thereby providing a basis for future studies on unraveling both the antecedents and consequences of different sustainability strategies. Second, the typology shows that despite similarities in structure amongst strategies, they vary considerably, thus concretizing our knowledge about dissimilarities in types of practice as opposed to variances in degrees of practice. Third, the findings indicate that there is a more complex relationship between sustainability motives and a specific strategy than expected. This research, therefore, offers a more fine-tuned understanding of why different sustainability strategies are implemented. It also adds to sustainability research in the service context, which, unlike the manufacturing industry, is a widely under-researched setting [23,24,25].

The rest of the paper is structured as follows. I begin by outlining what is meant by the term ‘sustainability strategy’. I then provide background information on corporate motives for sustainability and the social and environmental practices implemented by the banking sector. I subsequently describe the methods adopted in this work and present the findings, after which I discuss the results further and end with the conclusions drawn from the research.

2. Theoretical Background

2.1. Sustainability Strategies

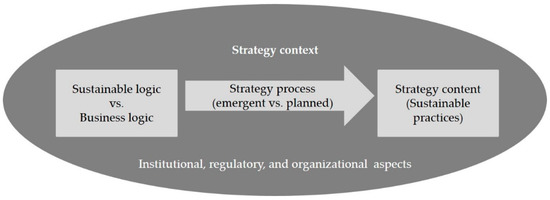

A firm’s sustainability strategy is defined as a strategy aimed at achieving present and future economic prosperity, environmental integrity, and social equity for both the company itself and its stakeholders [26,27,28]. Drawing on the strategy literature, Baumgartner and Rauter [29] propose a framework for sustainability strategies that consists of four elements (see Figure 1): In this framework, a specific strategy content is implemented on the basis of an underlying logic and as the outcome of a strategy process. Logic, process, and content are embedded in the strategy context.

Figure 1.

Elements of a sustainability strategy.

The underlying logic is closely linked to organizational purpose, and represents the phenomenon that predefines “order, direction, and coherence” [30] (p. 139). Strategic decisions are thus supposed to be derived from the organizational purpose. Previous research described a dualism between two logics—a business case logic and a sustainable logic—as to why companies implement sustainable practices. Objectives that correspond to the business case logic are cost and risk reduction, efficiency gain, brand building, and new market creation [31,32,33]. In contrast, the sustainable logic implies that economic goals are instruments of sustainable development, as revenue can be used to fulfil social and ecological needs. Objectives that correspond to the sustainable logic include environmental protection, social justice and equality, or the fight against poverty [21,34,35,36]. The strategy process is the manner by which a strategy is formulated and constructed to achieve an intended purpose [37]. This process is described through two approaches. The first assumes that strategy creation is a fully conscious and rational planning process. The second approach opposes the notion that strategies are planned in a linear fashion and instead projects them as emerging from practice in a bottom–up or undirected way [38].

The course of action constitutes the strategy content; that is, the pattern of sustainable practices that are implemented to achieve an outcome [29]. A wide range of social and environmental practices are available to companies for them to advance sustainable development. These practices may refer to those carried out for a firm’s employees (e.g., work–life balance or diversity activities) or those implemented in its supply chain (e.g., supplier selection with consideration for social and ecological aspects) or production and operational processes (e.g., energy saving, resource preservation). Practices that address issues in the external environment that surrounds a company, such as donation to and sponsorship of social, cultural, or environmental organizations, can also contribute to sustainable development. Strategy content should not be confused with the communication of a strategy or intended strategy, as such communication pertains to possible patterns of practices, whereas strategy content refers to realized strategies, which reflect actual patterns of practices [39,40].

Finally, the strategy content and process are embedded in the strategy context, which comprises institutional, regulatory, and organizational elements. It is understood as the conglomerate of surrounding conditions under which the strategy process and content are determined. It refers to the environment where a business operates and therefore differs across companies [41]. The strategy context both opens and limits possibilities for sustainable practices [42].

2.2. Corporate Motives for Sustainability

Extensive research has been conducted on the motives of firms for social and/or environmental behaviors [43,44,45,46,47,48,49,50]. Such motives are often labeled differently, but two main categories can be identified. Intrinsic motives are value-driven, moral, altruistic, or ethical motivations that stem from concern for social/environmental issues. In contrast, extrinsic, self-driven, or instrumental motives represent the potential improvement of legitimacy, competitiveness, efficiency gains, and innovativeness that a firm aims to realize through a specific sustainable behavior.

Most studies on motives implicitly assumed that different motivations are connected to varying degrees of sustainable practice [44,47,51,52,53]. Extrinsic motives, for example, are associated with reactive strategies, whereas intrinsic motives are related to ambiguous proactive strategies [48]. In addition, classifications of sustainability strategies are frequently underlain by the assumption that only one motive drives sustainable practices in each company [42,54,55,56,57,58]. This idea was challenged by Santana [22], who argued that different motives co-exist within each company and that each motivation can prevail to different extents. Likewise, the salience of motivations might vary depending on organization [59] and practice, from which company- and practice-specific “motivation positions” [22] (p. 765) result. This supposition was supported by a study wherein corporate motives were confirmed to differ with respect to the kinds of sustainable practices in which a company engages [60].

With the exception of analyses directed solely to particular social [22] or environmental [43,61] practices or studies conducted in the manufacturing industry [45], research that explicitly refers to a connection between kinds of practices and different motives is largely inadequate. A necessary requirement, therefore, is to empirically unravel the tie between different types of sustainability strategy content and corporate motives.

2.3. Sustainability in the Banking Industry

Given their intermediary position, financial services can foster or hamper the (non-)sustainable behaviors of states, companies, and individuals and can even trigger structural change in society [1]. These offerings are therefore considered transformative services [62], which influence society and the environment in a very particular manner. As briefly described above, companies can generally implement environmental practices (e.g., energy saving), social practices (e.g., corporate volunteering, health management), and external practices (e.g., donation).

The same is true for banks, but practices that are anchored in these institutions’ core businesses have considerably more extensive effects. They can, for instance, consider sustainability aspects as they make decisions regarding investments. Such initiatives are described as socially responsible investments (SRIs), and these date back to the 16th century when Italian banks used religious ethics as guidance in the decision process [11]. Nowadays, an SRI is an investment form that integrates non-financial concerns, such as ethical, social, or environmental issues, into decision making [21,63,64,65,66]. For example, financial institutions can apply negative criteria (e.g., excluding the nuclear sector as a client) and positive criteria (e.g., fostering growth in the renewable energy sector) in decision making and thereby “directly influence the functioning, priorities, and values of businesses” [1] (p. 4). In the same vein, sustainable criteria can be employed in decision making on lending [3,17,18,34], as is the case when banks sign the Equator Principles (EPs), which are environmental and social risk management standards that are voluntarily adopted by the project finance sector [67,68]. Banks can also engage in active ownership [69] by, say, voting on shares and engaging in dialogue with investee companies or borrowers to improve environmental and social outcomes. Active ownership [69] can likewise take the form of writing (open) letters, proposing shareholder resolutions, collaborating with other organizations, or even divesting from a company under scrutiny [70,71].

Previous studies have devoted much attention to the extent of effort that financial service providers expend towards sustainable development [14,15,16] or the manner by which specific practices are implemented [17,21,34,70] and the effects of these practices on economic and marketing outcomes [7,10,72,73,74]. However, no knowledge has been acquired as to what kinds of sustainable practices banks typically implement in combination. This deficiency translates to a research gap with regard to the content of banks’ sustainability strategies and a corresponding lack of explanation on how different types of such content are motivated. Given that the banking sector lags behind other industries in terms of sustainability outcomes [14], an understanding of motivations is crucial to the development of tools that effectively encourage financial institutions to implement substantive strategies and thus contribute to the achievement of the sustainable development goals (SDGs) established by the United Nations [75]. In response to this challenge, the current work qualitatively examined sustainability practices in the banking industry. The succeeding section details the methods used for this purpose.

3. Methods

A qualitative research design was chosen given the explorative nature of my research aim. I conducted semi-structured interviews, which are considered “the heart” of qualitative studies [76] (p. 19), with executives of 26 banks. I spoke with sustainability managers, where this post is existing. In banks without such a position, the individual responsible for sustainability-related practices was interviewed (i.e., CEO, product manager, or marketing manager). The interview questionnaire was supplemented by multiple other data sources, such as corporate publications (e.g., websites and annual or sustainability reports), which I expected to improve the validity of the data [77]. The 26 cases were analyzed iteratively; that is, I repeatedly revisited the data collection, data analysis, and reflection on the literature [78].

Maximum variation sampling was adopted [79,80], with a purposeful selection of banks that differ as much as possible in terms of strategy content and corporate motives. Variance in the two concepts of interest and the comparison of cases are precisely the components that pave the way for an in-depth understanding of the link between types of sustainability strategy content and motives [81]. To achieve such variance, I included different banking structures (public, private, and cooperative) in the sample and stopped adding cases when saturation was reached (i.e., when no additional sustainable practices or motives could be identified). I initially used information available on the websites of the banks as an indicator of strategy content. If a bank matched the purposes of the study, I contacted its employees and determined their willingness to participate in the research. The participants were assured of anonymity, and then data collection was conducted between June 2017 and September 2018.

The questionnaire encompasses different variations of the questions ‘What are you doing with respect to corporate sustainability?’ and ‘Why are you implementing these initiatives?’ (Appendix A). Although the questionnaire was developed carefully by five service researchers, it was used as a rough guide rather than a strictly followed survey instrument. I allowed for flexibility in adjusting the questionnaire throughout the study should the analysis have suggested necessary adaptation. For instance, the first cases implied that motives underlying diverse sustainable practices vary. Correspondingly, I adapted the instrument and inquired into the motivation behind each activity instead of the overall justification for a sustainability strategy. I conducted all the interviews, either by telephone or onsite (i.e., at a bank). The recorded sessions lasted between 45 and 88 min and were transcribed afterwards to ensure systematic analysis.

The data analysis was guided by the principles put forward by Gioia et al. [76] and Kluge [82]. Gioia et al. [76] presented a systematic approach to qualitative studies, with the authors emphasizing independence from existing knowledge. This approach offers a reasonable way for researchers to dissociate themselves from assumptions that have thus far been made about strategy types. Kluge [82] provided useful recommendations on how to construct typologies in qualitative research. Both these researchers underlined the significance of an inductive and iterative procedure, which is why their methods are consistent and complementary. The analysis in the current work was performed in MaxQDA and involved two major steps: The construction of the typology and the assignment of motives to each strategy type.

The analysis of the first cases yielded a list of the sustainable practices that the participating banks implement. When no additional sustainable practices could be found, I grouped similar activities. For instance, I grouped membership in a sustainability-related network or association, cooperation with research institutions, and communication on sustainability-related issues under content-related involvement. Drawing on Yuan et al. [83], I distinguished between sustainable practices for core businesses and those for business peripheries, as well as sustainable practices that focus on external projects and initiatives. Practices were also differentiated according to whether they center on social or environmental issues.

Simultaneously, the identified groups of sustainable practices were used to “dimensionalize” the typology [82] (p. 3). On the basis of the concept of attribute space [84], the groups of practices were used to identify all possible combinations of practices. In an ongoing process, data were analyzed to ascertain similarities and differences [76] so that the attribute space could be reduced to typology dimensions that distinguish between emerging types; that is, the attributes by which strategy types could be most clearly differentiated. Conflating the attributes yielded a preliminary classification of sustainability strategy content. Revisiting the data collection and analysis and increasingly considering the literature, I further refined the typology dimensions. Finally, following the logic of comparison [85], I analyzed each bank once more and checked whether it was correctly assigned in accordance with the constructed typology. It is important to consider that the constructed typology covers ideal types of strategies, from which actual cases may somewhat differ. These ideal forms provide the most appropriate descriptions, indicating whether each case best corresponds to a given type of sustainability strategy. Each empirical case is equally classifiable so that no instance is left unassigned to any of the identified ideal strategy types. The basic rules of classification, exhaustiveness, and mutually exclusiveness of types, were thus followed [86].

Parallel to the procedure for sustainable practices, the categorization of motives was developed inductively using informant-centric category labels [76], which closely adhere to the terms used by the interviewees. For instance, the statement “Slipped disks are a serious problem. People are absent for a longer period of time. So we had to find ways to reduce it.” (B15) was coded as reducing employee absenteeism. As the data analysis proceeded, second-order constructs were established by clustering first-order constructs and taking into account the literature. Similarly, second-order constructs were aggregated and thus grouped under an even more abstract category (see Appendix B). Each case was then assigned to a single motive or a combination of motives. On the basis of this within-case analysis, the grouped banks were compared in the matter of the link between motives and types of strategy content. This final step was thus deductive, consistent with Spiggle [78], who described the continuous transition of an iterative study from inductive to deductive analysis.

4. Results

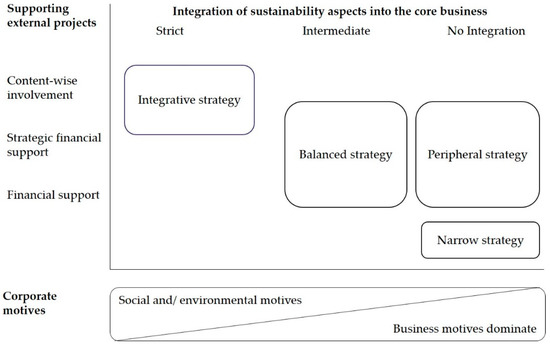

Throughout the analysis of the 26 cases, I identified five types of strategy content, each understood as a specific pattern of sustainable practices. The typology is constituted by three key distinctive features, amongst which the most striking is whether banks focus on the core or on the peripheries of their business. The second feature points to the laying of focus on social or environmental issues, and the third revolves around the fact that within the business periphery, banks can support external sustainability projects in terms of finances or content (see Figure 2).

Figure 2.

Typology of the sustainability strategy content in the banking industry.

I also found three principal categories of corporate motives for sustainability; namely, social, environmental, and business motives.

The social motive category implies that a bank aims to create a viable society by contributing to public welfare, social justice, and social cohesion. The environmental motive category suggests that banks endeavor to build a viable natural environment by reducing their climate footprint and promoting environmental consciousness. Both categories implicate banks and their employees, as well as society in general. The business motive category implies that banks strive for a viable business by improving financial performance and pursuing marketing- and employee-related objectives.

The analysis reveals that the strategy type result from a different combination of motives. The following section describes the strategy content types and underlying motives in detail.

4.1. Type 1: Narrow Strategy Content

As reflected in the label, a narrow strategy involves the implementation of sustainable practices in a limited manner; accordingly, banks do not plan to carry out additional activities because they do not perceive sustainability as a relevant matter. When asked about what sustainable practices the banks have implemented, one of the respondents provided “None. None at all.” (B10) as a response. Amongst banks that implement this strategy type, therefore, sustainability is not concentrated in core businesses; no official guidelines on investments and lending decisions that require sustainability components are taken into account. The lack of sustainability in the core business originates from what banks perceive as the absence of economic relevance; that is, there is neither noticeable demand from customers nor pressure from secondary stakeholders (e.g., non-government organizations) to espouse sustainability initiatives. Some of these banks offer sustainable funds, but customers are compelled to explicitly ask for such financial products.

Banks belonging to this group also donate to social organizations, such as youth associations, sports clubs, or kindergartens, in their region but do not support ecological organizations. The allocation of donations is not grounded in any pre-defined criteria. Certain practices are pursued to save energy (e.g., the insulation of building facade, the use of low-energy bulbs, and automatic timers for heating) and other resources, such as water and paper. Employee-related practices are adopted to an equally low degree, with the respondents lamenting the deficiency in addressing issues regarding work–life balance. This strategy type is driven primarily by business motives. Although image, reputation, and differentiation are key issues, particularly in relation to donations and sponsoring, the potential to reduce costs is the chief driver of resource efficiency measures. This strategy has been implemented by six of the participating banks, and they are in most cases, small cooperatives where no employee position is dedicated to sustainability.

4.2. Type 2: Peripheral Strategy Content

The peripheral strategy content is substantially similar to the first type of strategy, with banks imposing no sustainable exclusion criteria on investments or lending decisions. However, the sampled institutions have recently launched a few sustainable investment products, such as funds that reflect a consideration for environmental and social matters. Within the margins of their businesses, peripherally oriented banks strategically allocate considerable funds to charitable projects or organizations, including sports clubs, cultural associations, and social welfare organizations in the same region. Donations are administrated by a foundation, which ensures criteria-led decisions. Part of the strategy, as well, is support for volunteerism amongst employees, for whom association membership fees are paid and rewards for special commitments are awarded. Unlike the narrow strategy, the periphery scheme involves adherence to systematic environmental practices. Banks apply various energy efficiency measures and directives regarding business trips, and activities revolving around health management and work–life balance are well established.

Similar to the narrow strategy, however, the periphery scheme is dominated by business motives, with customer demand and potential cost savings accorded particular priority. Banks that operate in accordance with a periphery-oriented scheme embrace social and environmental responsibilities, albeit to a minor extent. The pursuit of philanthropy is mostly motivated by the desire to contribute to public welfare. This type of strategy has been implemented by four of the sampled banks, and these are either public institutions or cooperatives of different sizes. The personnel responsible for social practices is usually a member of the marketing department.

4.3. Type 3: Balanced Strategy Content

The balanced strategy is characterized by the advanced integration of sustainable criteria into core businesses, as reflected in the availability of a wide range of sustainable products. In addition, customers may benefit from interest rebates if they meet positive criteria, such as when they buy an electric car instead of a conventional automobile. Banks that pursue this course of action abide by sustainable standards for investments and lending decisions. For instance, they forego the infusion of capital into certain forms of coal production and verify their clients’ compliance with human rights regulations. Banks also actively engage with these clients if socially or environmentally critical issues arise.

With regard to practices within their business peripheries, banks employing this strategy type are very similar to those that implement the second strategy. They have well-established and systematic philanthropic practices with a social focus, employee-related activities, and environmental management projects. Employee-related occupations include endeavors towards gender diversity. Banks also occasionally involve themselves in content-intensive ventures, such as collaborations with universities on research and participation in round-table discussions on different aspects of sustainability.

Because an economic line of argumentation remains relevant to this strategy type, business motives are still definitive components of decisions. This means that sustainable practices are not implemented without consideration for financial benefits or the potential reduction of risk. In particular, exclusion criteria that are integrated into lending decisions originate from a risk perspective. Likewise, a steadily growing demand, particularly from institutional investors, drives the broader proportion of the entire portfolio of sustainable products. Nevertheless, social and environmental motives are attached more weight than they are in the first two strategy types. Again, philanthropic practices are stimulated primarily by social motives. At the same time, social and environmental motivations also figure in practices related to core businesses or environmental management.

Out of the 26 banks, seven have implemented this type of strategy, and these institutions are public, private, or cooperative banks of different sizes. In the large banks, one or more employees are explicitly in charge of sustainability issues and report to strategy departments. In their smaller counterparts, the task of sustainability is performed by a marketing department employee, who tends to this responsibility on a part-time basis.

4.4. Type 4: Integrated Strategy Content with a Social Focus

Banks that enforce the fourth strategy emphasize social issues in their core businesses. A social added value is thus a prerequisite to lending. Accordingly, most institutional customers are social organizations (e.g., charitable institutions), and banking products are designed in consideration of manifold strict social, and some environmental, exclusion criteria. For instance, nuclear power and fossil fuel industries, the arms industry, companies that use child labor, firms with human rights abuses or corruption, and companies whose businesses are related to alcohol, tobacco, and pornography are denied inclusion as investment beneficiaries. This means that criteria are also applied to the proprietary investments of banks. Furthermore, microcredits are granted, and investments are infused into microfinance bonds. Finally, banks exercise their voting rights as institutional investors to achieve environmental and social improvements.

Banks that abide by this strategy donate to a considerable degree, mostly to charities, via foundations, but financial support is not paramount as involvement can also take the form of content support. These banks aid and promote employee volunteerism in charities through paid extra holidays, affiliate themselves with sustainability-related associations, and engage in forms of lobbying, such as campaigns that advocate tax justice. They execute advanced environmental management that covers reductions in energy, water, paper, and other resources, as well as decreases in travel. They enact purchasing policies that are typified by consideration for both social and environmental aspects. For instance, material orders are assigned to charities, and activities connected to work–life balance and health management are well established. In particular, employees receive assistance if they need to take care of either their children or the elderly members of their families. Finally, part of this strategy is the pursuit of gender diversity.

All in all, banks whose sustainability initiatives are governed by this strategy are driven chiefly by the aim to advance social justice and social cohesion. Environmental benefits are also weighed more importantly than they are under the balanced strategy, but integration is not exclusively linked to social and environmental motives. The interviewees acknowledged that their institutions are also motivated by business factors. For example, they value the risk mitigation effects of the strategy. This strategy has been carried out by five of the participating banks, most of which are small or medium cooperatives with less than 500 employees. One or two employees are responsible exclusively for sustainability management and report directly to the executive board.

4.5. Type 5: Integrated Strategy Content with an Environmental Focus

The fifth strategy is similar to the fourth but has an environmental focus. Under this scheme, banks exclusively finance projects and corporations that positively contribute to an environmentally healthy world. A vast array of stringent positive and negative criteria is applied to every investment decision, be it proprietary in nature, falling within a security business, or involving credit grants. The main criteria are biodiversity in forestry and agriculture, resource efficiency, the use of renewable energy, support for a circular economy, and pollutant reduction. When these standards are violated, deals can be rejected. A case in point is the denial of financing for a photovoltaic system in a conventional farm when the farmer refuses to switch to sustainable agriculture. In developing countries, microcredits are granted to small conventional farms that are transformed into sustainable agricultural businesses.

In this strategy, philanthropic practices are accorded a minor role, with banks instead focusing on content-related involvement. They can, for example, provide professional input for sustainable projects, help build networks, deliver presentations, write articles, conduct research, and actively involve themselves in sustainability-related networks and associations. Internal environmental practices extend beyond the endeavors implemented in the previous strategies. Banks use renewable energy, buy highly resource-efficient hardware, up-cycle technical devices instead of buying new ones, and adhere to a strict regional purchasing policy. Remaining carbon dioxide emissions are compensated, and employee-related practices are largely similar to those in the fourth strategy. Banks also underscore internal communication about sustainability-related issues, with newsletters or events launched to inform employees about matters related to sustainable finance.

Banks that implement the fifth approach are largely driven by the aim to have a hand in creating a viable natural environment. They seek to reduce their climate footprint and strengthen environmental consciousness in society. They are also inspired by social and business motives, but these are considered subordinate drivers. Consequently, the core business itself is transformed into a means of achieving environmental objectives. Four of the 26 banks have implemented this type of strategy, and these institutions are either private banks or differently sized cooperatives. No explicitly designed position exists for sustainability management, but social and ecological issues are directly incorporated into the dealings of every department.

5. Discussion

As previously stated, this research was intended to illuminate what specific types of sustainability strategy content are implemented by banks and how these schemes are motivated. The analysis of the sustainable practices carried out by the participating banks uncovered five types of strategy content. As with every typology, that developed in this work features ideal strategy types, from which real cases may differ in respect of certain details. They nonetheless provide the most appropriate descriptions of sustainability schemes. In line with the literature [4], the findings delineated two crucial distinguishing characteristics amongst the cases: The manner in which sustainable practices are integrated into core businesses (strict, intermediate, or non-existent) and the means through which banks support external projects and initiatives (content support, strategic financial backing, or non-strategic financial aid). The participating banks have also carried out internal practices, such as resource efficiency and health management, but an important issue for consideration is that such practices were found across all the cases and types, which is why they were disregarded as distinguishing characteristics.

The typology indicated that although the identified strategy types are similar in structure, they substantially vary with respect to involved practices. A major difference, in particular, is the focus on core businesses (integrative strategy) versus the concentration on business peripheries (peripheral strategy). One strategy contributes to sustainable development through a conscious shaping of financial flows, whereas the other makes such contribution via support for social projects in the form of donations and sponsorships. In addition, differences in practices within business peripheries exist. The integrative strategy, for instance, features content-related involvement with organizations or projects wherein a social or environmental purpose is pursued. Such practices ultimately represent a form of institutional entrepreneurship as they are “[aimed] at influencing market conditions” [87] (p. 224).

When the types of strategy content are related to the SDGs, the differences become even more apparent. In particular, the integrative strategy (types 4 and 5) reflect a contribution to SDG 1 (no poverty), SDG 7 (affordable and clean energy), and SDG 15 (life on land). An example is when the banks provide the financial resources needed to achieve an increased share of renewable energy and organic agriculture or reduced poverty rates as they use their businesses as a means towards sustainable ends. With reference to the negative criteria applied to lending and investment decisions, further connections to the SDGs can be identified. Excluding the arms industry as an avenue for investment supports SDG 16 (peace, justice, and strong institutions), and denying assistance to companies that abuse human rights contributes to SDG 10 (reduced inequalities). The strategies which do not entail the integration of sustainable practices into core businesses remain facilitative, albeit indirectly, of the SDGs. A connection can be seen, for example, between the banks’ philanthropic practices and SDG 4 (quality and education). Given that the banks mostly support social organizations and often concentrate on projects for children and youth, such assistance can be argued as fairly reductive of social inequality.

Although research results may be sensitive to how company size is measured [88], extensive empirical evidence has been derived as to the positive relationship between the size and sustainability performance of a company [89,90,91,92]. In this regard, the high resource slack of large companies is employed as an explanatory dimension [93]. Such firms are also more visible than their smaller counterparts and thus often face more pressure from secondary stakeholders, which is why they exhibit higher levels of social and environmental responsiveness [89,94]. This relationship, however, was not as conclusively supported by the findings of the present study. With the exception of the group of banks that has implemented the narrow strategy (mostly small institutions), the banks belonging to the other groups are diverse in terms of firm size. To put it in Bowen’s words, “size does not always matter” [95] (p. 123). It can be assumed that the size of a company only has an impact on the sustainability strategy of the banks in conjunction with other factors.

A more fruitful explanatory approach is to look into the different motives of banks. I found that, contrary to previous assumptions, banks are not necessarily driven by only one motive. They can, for example, be spurred by both business and environmental reasons, and different sustainable practices can be underlain by varying motivations. These results support the propositions of Santana [22], who established the construct of a motivation-mix and maintained that motives differ across practices, thereby engendering a specific “motivation position for a company as a whole” [22] (p. 765). To explain further, different motives may co-exist, but one is typically regarded as superior to others. It is precisely this superiority that is crucial in the choice of a strategy content, as demonstrated in the present work. Although business motives factor in all the cases, their sphere of influence on sustainable practices change with increasing or decreasing strength. Such “motivational antecedents” [96] (p. 141) provide a fruitful explanation for the different types of sustainability strategy content espoused by banks. In particular, I argue that considering the identified motive categories as configurations might clear the way for an enhanced elucidation of sustainability strategies. An essential issue for examination, therefore, is how different motives are combined and intertwined. As long as business motives are used on their own, a narrow strategy content ensues, but when they are employed in concert with other motivations, other strategy types arise. Their combination with social motives, for instance, is commensurate to the application of a peripheral strategy, and adopting them in conjunction with environmental grounds results in a balanced strategy. In all these combinations, business motives remain the strongest drivers, but when they are dominated by ecological or social motives, then the course of action becomes integrative in nature.

Given the relevance of motives to ascertaining the kinds of sustainability strategy content employed by organizations, a question that arises is from where motive categories originate. A potential explanation lies in the institutional logics perspective [97,98], which posits that logics are taken-for-granted assumptions that place principles of action in the hands of organizations and individuals given their provision of vocabularies of motive [99]. In doing so, they shape the reasoning schemas for the behaviors of organizations [98]. With this theoretical approach as grounding, I contend that logics are instrumental in molding banks’ motivations for sustainable practices and, ultimately, in shaping their sustainability strategies. In line with this argumentation, the strategy context, which covers the institutional environment amongst other domains, is the component that exerts a decisive influence on the relevance of various motive categories and, consequently, on sustainability strategy content. Recent studies on the environmental and social practices of financial service providers have equally illustrated how the sustainable logic can affect sustainable behavior if it prevails against market logic [21,34].

With a more general reference to the business and society literature, another potential explanation for differences amongst banks is the varying governance structures that they put into effect [100,101,102,103,104]. Previous studies suggested that board attributes [104,105], shareholder activism and concentration, and environmental committees affect corporate environmental performance [100]. Similarly, companies with a mechanistic organizational structure are likely to achieve high levels of environmental performance [103]. Empirical evidence has been obtained as to the positive effects of integrating social performance outcomes into the compensation of executives [101] and CEO proficiency [102] on social outcomes.

Considering the relationship between bank type and the type of sustainability strategy content implemented by such institutions, however, this study does not provide a solid conclusion on the link between the structure of governance and the type of sustainability strategy in a bank. This resonates with research pointing out that the association between governance structure and social and/or environmental outcomes is not always consistent [5,106]. Such inconsistencies might, in turn, be rooted in other attributes that affect overall governance; these attributes include the gender diversity of a company’s board of directors [107,108,109], the characteristics of top management [110], and the organizational design for bank sustainability [106,111]. Along with each type of sustainability strategy content comes a different organizational structure for social and environmental practices. I submit that as a result of this heterogeneity, banks are encouraged to consider other aspects of sustainability (e.g., core business or business periphery, social vs. ecological) to be particularly relevant and align their strategies accordingly.

Finally, the findings make room for theorizing on the mechanisms that can bring about a change in strategy. I reason that such alteration is possible when a logic gains strength and a shift in the weighting of motives occurs. Corbett et al. [35] argued that depending on the interplay of multiple logics and organizational identity, a window of opportunity emerges and allows different decisions for or against sustainable practices. On this basis, I posit that different motivations are facilitated by this window of opportunity, after which the specific constellation of various sustainable practices is affected. The results led me to assume that the shift from the narrow to the peripheral strategy is relatively likely as only a slight change in the motive situation would be necessary. The move towards the balanced strategy, in contrast, entails a more substantial change in the motive mix and would thus have to be accompanied by a change in values. This change in strategy can thus be expected to cause disturbance. This situation is even more applicable to the integrative strategy. Because such strategy is mostly induced by social and/or environmental motives, its implementation is unlikely as long as business motivations continue to dominate.

The findings also implied that a change in strategy is realized when sustainable practices satisfy not only environmental and social motives but also business rationales. This phenomenon reflects, for example, that growing demand for sustainable investments on the part of customers [112] or growing pressure to impose social and environmental criteria on lending decisions (e.g., as advocated by the fossil fuel divestment movement) [113] indicate the underlying business motives of banks. Reducing risks and meeting customer expectations then function as mediators of practices that have thus far been predominantly socially or environmentally motivated. In other words, if business motives come to the fore when implementing sustainable practices, banks might recognize them as a potential for increasing profits, reducing risks, maintaining legitimacy, and ultimately ensuring their financial viability.

6. Conclusions

This research expands extant literature in three ways. The first contribution lies in its development of a typology of sustainability strategy content in the banking industry. Typologies present numerous benefits; they reduce complexity, enable the identification of similarities and differences amongst cases, offer utility in recognizing relationships between concepts, and provide criteria for measurement [86]. This study thus serves as basis for future research that is intended to pinpoint both the antecedents and consequences of different types of sustainability strategy content.

Second, the typology showed that, despite similarities in structure, substantial differences typify the types of strategy content. This finding aligns with the literature on sustainability strategies in which companies respond in various ways to environmental and social challenges. The current work adds to previous research in that it revealed the tendency of banks to pursue different patterns of practices; that is, it concretized assumptions about differences in the kinds of practices—as opposed to differences in the degree of practice—and provided empirical evidence for an industry that plays a crucial role in achieving the SDGs [1,2,3].

Third, the findings indicated that there is a more complex relationship between motives and strategy content than expected. Whereas previous research principally assumed the existence of a single motivation behind each type of sustainability strategy content [44,47,51], the present work empirically showed that the situation corresponds to a motive mix [22], which determines which sustainable practices are carried out. This study thus finetunes our understanding of why different sustainability strategies are adopted by various organizations.

The results present managerial implications for stakeholders concerned with environmental and social issues, such as sustainability managers, policymakers, and environmental organizations. The findings enable an enhanced identification of gaps in strategy and their resolution with appropriate measures. The insights presented here equip practitioners with the means to evaluate and adopt an existing sustainability strategy or develop a new one, as well as to reflect on current situations and discover opportunities for improvement. The typology thus eases the selection of practices that meet a bank’s sustainability goals. Identifying the type of strategy content that is presently practiced may also advance more efficient communication about the sustainability strategy, enabling a bank to better achieve its communication goals and, for example, differentiate itself from the competition.

This study likewise indicated that banks have thus far neglected a clear-cut delineation of the work to be devoted to the SDGs even though these goals provide an effective framework for recognizing potential domains where a bank might contribute to sustainable development. For example, none of the 26 cases referred to SDG 3 (good health and wellbeing) and SDG 6 (water and sanitation) despite the major relevance of the two goals. Banks can use the SDGs as a stimulus to create special financial products. If social or environmental benefits are easily discernible, then the number of customers willing to invest in such sustainable products might increase as well.

Finally, in line with Müller and Pfleger, I recommend that banks take their core activities as “starting points for transformations towards sustainability” [114] (p. 321) and begin with the integration of sustainability into their core businesses. Three reasons drive this suggestion. First, using a provided service as a practice may contribute positively and substantially to the achievement of the SDGs. Second, treating a given service as such can prevent suspicions of greenwashing. For instance, if a bank supports external climate projects but also invests in environmentally dubious endeavors, then skepticism from stakeholders may arise. However, taking into account environmental aspects in investment decisions might raise the trustworthiness of a sustainability strategy. Third, by integrating sustainability into core businesses, banks leverage their resources [115] and ensure the strategic fit [116,117] that research has so often called for.

Similar to any other study, this research is encumbered by a number of limitations. First, data were collected in Germany, thereby rendering generalizability to other contexts difficult. Further studies should examine whether identified strategy types identified in the current work can also be found in different countries. Second, the data do not contain information on how the strategies evolve over time. Future research can delve into changes in patterns. Third, this study is not representative with regard to the distribution of strategy types among German banks because of its grounding in qualitative data and thus limited number of cases. Thus, an interesting issue for researchers to cast light on is how the strategy types are distributed in Germany or other nations in Europe. Such knowledge would enable an analysis of the discussed determinants of corporate motives, size, and governance and a testing of assumed relationships. In particular, an organization’s design for sustainability, board characteristics, and the manner by which executives are compensated [101] might play a crucial role for sustainable outcomes [104,106,108,109].

Additional directions for research include the lack of strategic orientation in the banks that apply the narrow strategy. Scholars could analyze the reason these institutions do not see the relevance of social and environmental aspects in sustainable development and thus forgo the implementation of sustainable practices. Moreover, the typology of sustainability strategy content helps improve measurements of the effects of specific sustainability practices on customer attitudes and behaviors. Such effects are assumed to strongly depend on the context surrounding a specific practice because customers tend to perceive and evaluate a practice with reference to setting; that is, as a part of an entire strategy. The exploration of this relationship between corporate sustainability and customer response also opens possibilities for further inquiries.

Funding

This publication is sponsored by FernUniversität in Hagen.

Conflicts of Interest

The author declares no conflict of interest.

Appendix A

Interview questionnaire

Introductory questions

- Please first describe the position you hold within the company: What are your tasks? Which department are you assigned to?

Questions on sustainable practices and motives

- 2.

- Is your company committed to social/environmental issues? How did it come about? When did it happen? Why (not)? What’s the main motive?

- 3.

- What do you do when it comes to sustainability? How and when did this come about? Why (not)? Why (not)? What’s the main motive?

- 4.

- Are there any internal measures in the area of environmental protection? How did this happen? When? Why (not)? Why (not)? What’s the main motive?

- 5.

- Are there any internal social measures, e.g., any employee-related practices? How did this happen? When? Why (not)? Why (not)? What’s the main motive?

- 6.

- Are there any external social projects that support you? How did this happen? When? Why (not)? Why (not)? What’s the main motive?

- 7.

- Are there any external environmental projects that support you? How did this happen? When? Why (not)? What’s the main motive? Why (not)? What’s the main motive?

- 8.

- What role do environmental aspects play in your core business, e.g., in lending and investment decisions? How did this happen? When? Why (not)? Why (not)? What’s the main motive?

- 9.

- What role do social aspects play in your core business, e.g., in lending and investment decisions? How did this happen? When? Why (not)? Why (not)? What’s the main motive?

Closing questions

- 10.

- Are you planning to expand or limit your sustainable practices in the future? In what way? Why?

- 11.

- Do you pursue a certain strategy with your sustainable practice? What’s the overall aim?

- 12.

- To what extent does your sustainability strategy differ from the strategy of other banks? What do you do differently from other banks? Do you do more or less?

Appendix B

First-order concepts, second-order concepts, and aggregate dimension of corporate motives for sustainable practices

| First-Order Concepts | Second-Order Concepts | Aggregate Motive Categories |

| Stand up for the community Give back something to the community Promote the region | Contribution to public welfare | Social motives |

| Enable social participation Promote human rights Create equal opportunities | Contribution to social justice | |

| Enable voluntary work Support social commitment Promote social organizations | Contribution to social cohesion | |

| Do something for the environment Preserving resources Reduce emissions | Contribution to the climate footprint | Environmental motives |

| Make the green thought mainstream Function as a role mode | Contribution to environmental consciousness | |

| Reduce costs Stimulate additional business Reach the return on investment Reduce financial risks | Contribution to the financial performance | Business motives |

| Bind customers Meet customer expectations Attract new customers Exploit publicity purposes Differentiate against customers Improve image Become more known | Contribution to marketing-related motives | |

| Employee satisfaction Bind employees Motivate employees Finding adequate staff Reducing employees absence | Contribution to the employee-related motives |

References

- Louche, C.; Busch, T.; Crifo, P.; Marcus, A. Financial Markets and the Transition to a Low-Carbon Economy: Challenging the Dominant Logics. Organ. Environ. 2019, 32, 3–17. [Google Scholar] [CrossRef]

- Shrivastava, P.; Zsolnai, L.; Wasieleski, D.; Stafford-Smith, M.; Walker, T.; Weber, O.; Krosinsky, C.; Oram, D. Finance and Management for the Anthropocene. Organ. Environ. 2019, 32, 26–40. [Google Scholar] [CrossRef]

- Busch, T.; Bauer, R.; Orlitzky, M. Sustainable Development and Financial Markets: Old Paths and New Avenues. Bus. Soc. 2016, 55, 303–329. [Google Scholar] [CrossRef]

- Weber, O. Sustainability benchmarking of European banks and financial service organizations. Corp. Soc. Responsib. Environ. Manag. 2005, 12, 73–87. [Google Scholar] [CrossRef]

- Dell’Atti, S.; Trotta, A.; Iannuzzi, A.P.; Demaria, F. Corporate Social Responsibility Engagement as a Determinant of Bank Reputation: An Empirical Analysis. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 589–605. [Google Scholar] [CrossRef]

- Wu, M.-W.; Shen, C.-H. Corporate social responsibility in the banking industry: Motives and financial performance. J. Bank. Financ. 2013, 37, 3529–3547. [Google Scholar] [CrossRef]

- Gangi, F.; Meles, A.; D’Angelo, E.; Daniele, L.M. Sustainable development and corporate governance in the financial system: Are environmentally friendly banks less risky? Corp. Soc. Responsib. Environ. Manag. 2018, 27, 17. [Google Scholar] [CrossRef]

- Esteban-Sanchez, P.; de la Cuesta-Gonzalez, M.; Paredes-Gazquez, J.D. Corporate social performance and its relation with corporate financial performance: International evidence in the banking industry. J. Clean. Prod. 2017, 162, 1102–1110. [Google Scholar] [CrossRef]

- Fatma, M.; Rahman, Z. The CSR’s influence on customer responses in Indian banking sector. J. Retail. Consum. Serv. 2016, 29, 49–57. [Google Scholar] [CrossRef]

- Pérez, A.; Rodríguez del Bosque, I. The Formation of Customer CSR Perceptions in the Banking Sector: The Role of Coherence, Altruism, Expertise and Trustworthiness. Int. J. Bus. Soc. 2015, 16, 75–94. [Google Scholar] [CrossRef]

- Weber, O.; Feltmate, B. Sustainable Banking. Managing the Social and Environmental Impact of Financial Institutions; University of Toronto Press: Toronto, ON, Canada, 2016. [Google Scholar]

- Ramiah, V.; Gregoriou, G.N. (Eds.) Handbook of Environmental and Sustainable Finance; Elsevier: Amsterdam, The Netherlands, 2015. [Google Scholar]

- Jeucken, M. Sustainable Finance and Banking: The Financial Sector and the Future of the Planet; Earthscan Publicatoin: London, UK, 2001. [Google Scholar]

- Thien, G.T.K. CSR for Clients’ Social/Environmental Impacts? Corp. Soc. Responsib. Environ. Manag. 2015, 22, 83–94. [Google Scholar] [CrossRef]

- Weber, O.; Diaz, M.; Schwegler, R. Corporate Social Responsibility of the Financial Sector—Strengths, Weaknesses and the Impact on Sustainable Development. Sustain. Dev. 2014, 22, 321–335. [Google Scholar] [CrossRef]

- Johannsdottir, L. The Geneva Association framework for climate change actions of insurers: A case study of Nordic insurers. J. Clean. Prod. 2014, 75, 20–30. [Google Scholar] [CrossRef]

- Weber, O. Environmental Credit Risk Management in Banks and Financial Service Institutions. Bus. Strat. Environ. 2012, 21, 248–263. [Google Scholar] [CrossRef]

- Weber, O.; Scholz, R.W.; Michalik, G. Incorporating sustainability criteria into credit risk management. Bus. Strat. Environ. 2010, 19, 39–50. [Google Scholar] [CrossRef]

- Eisenbach, S.; Schiereck, D.; Trillig, J.; von Flotow, P. Sustainable Project Finance, the Adoption of the Equator Principles and Shareholder Value Effects. Bus. Strat. Environ. 2014, 23, 375–394. [Google Scholar] [CrossRef]

- Nikolakis, W.; Nelson, H.W.; Cohen, D.H. Who Pays Attention to Indigenous Peoples in Sustainable Development and Why?: Evidence From Socially Responsible Investment Mutual Funds in North America. Organ. Environ. 2014, 27, 368–382. [Google Scholar] [CrossRef]

- Risi, D. Time and Business Sustainability: Socially Responsible Investing in Swiss Banks and Insurance Companies. Bus. Soc. 2018, 49. [Google Scholar] [CrossRef]

- Santana, A. Disentangling the Knot: Variable Mixing of Four Motivations for Firms’ Use of Social Practices. Bus. Soc. 2015, 54, 763–793. [Google Scholar] [CrossRef]

- Goyal, P.; Rahman, Z.; Kazmi, A.A. Corporate sustainability performance and firm performance research. Manag. Decis. 2013, 51, 361–379. [Google Scholar] [CrossRef]

- Zimmermann, S.; Fließ, S. Nachhaltigkeit als Gegenstand der Dienstleistungsforschung—Ergebnisse einer Zitationsanalyse. In Beiträge zur Dienstleistungsforschung 2016; Büttgen, M., Ed.; Springer Gabler: Wiesbaden, Germany, 2017; pp. 139–163. [Google Scholar]

- Leonidou, C.N.; Leonidou, L.C. Research into environmental marketing/management: A bibliographic analysis. Eur. J. Mark. 2011, 45, 68–103. [Google Scholar] [CrossRef]

- Engert, S.; Baumgartner, R.J. Corporate sustainability strategy-bridging the gap between formulation and implementation. J. Clean. Prod. 2016, 113, 822–834. [Google Scholar] [CrossRef]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strat. Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Strand, R. Strategic Leadership of Corporate Sustainability. J. Bus. Ethics 2014, 123, 687–706. [Google Scholar] [CrossRef]

- Baumgartner, R.J.; Rauter, R. Strategic perspectives of corporate sustainability management to develop a sustainable organization. J. Clean. Prod. 2017, 140, 81–92. [Google Scholar] [CrossRef]

- Warriner, C.K. The Problem of Organizational Purpose. Sociol. Q. 1965, 6, 139–146. [Google Scholar] [CrossRef]

- Almandoz, J. Arriving at the Starting Line: The Impact of Community and Financial Logics on New Banking Ventures. Acad. Manag. J. 2012, 55, 1381–1406. [Google Scholar] [CrossRef]

- Almandoz, J. Founding Teams as Carriers of Competing Logics. Adm. Sci. Q. 2014, 59, 442–473. [Google Scholar] [CrossRef]

- Hockerts, K. A Cognitive Perspective on the Business Case for Corporate Sustainability. Bus. Strat. Environ. 2015, 24, 102–122. [Google Scholar] [CrossRef]

- Kok, A.M.; de Bakker, F.G.A.; Groenewegen, P. Sustainability Struggles: Conflicting Cultures and Incompatible Logics. Bus. Soc. 2017, 21, 1–37. [Google Scholar] [CrossRef]

- Corbett, J.; Webster, J.; Jenkin, T.A. Unmasking Corporate Sustainability at the Project Level: Exploring the Influence of Institutional Logics and Individual Agency. J. Bus. Ethics 2018, 147, 261–286. [Google Scholar] [CrossRef]

- Dyllick, T.; Muff, K. Clarifying the Meaning of Sustainable Business: Introducing a Typology from Business-as-Usual to True Business Sustainability. Organ. Environ. 2016, 29, 156–174. [Google Scholar] [CrossRef]

- Baumgartner, R.J.; Korhonen, J. Strategic thinking for sustainable development. Sustain. Dev. 2010, 18, 71–75. [Google Scholar] [CrossRef]

- Neugebauer, F.; Figge, F.; Hahn, T. Planned or Emergent Strategy Making?: Exploring the Formation of Corporate Sustainability Strategies. Bus. Strat. Environ. 2015, 25, 323–336. [Google Scholar] [CrossRef]

- Steensen, E.F. Five types of organizational strategy. Scand. J. Manag. 2014, 30, 266–281. [Google Scholar] [CrossRef]

- Pistoni, A.; Songini, L.; Perrone, O. The how and why of a firm’s approach to CSR and sustainability: A case study of a large European company. J. Manag. Gov. 2016, 20, 655–685. [Google Scholar] [CrossRef]

- De Wit, B.; Meyer, R. Strategy. Process, Content, Context: An International Perspective, 5th ed.; Cengage Learning: Singapore, 2010. [Google Scholar]

- Baumgartner, R.J. Managing Corporate Sustainability and CSR: A Conceptual Framework Combining Values, Strategies and Instruments Contributing to Sustainable Development. Corp. Soc. Responsib. Environ. Manag. 2014, 21, 258–271. [Google Scholar] [CrossRef]

- Bansal, P.; Roth, K. Why companies go green: A model of ecological responsiveness. Acad. Manag. J. 2000, 43, 717–736. [Google Scholar] [CrossRef]

- Baumgartner, R.J.; Ebner, D. Corporate sustainability strategies: Sustainability profiles and maturity levels. Sustain. Dev. 2010, 18, 76–89. [Google Scholar] [CrossRef]

- Brockhaus, S.; Fawcett, S.E.; Knemeyer, M.A.; Fawcett, A.M. Motivations for environmental and social consciousness—Reevaluating the sustainability-based view. J. Clean. Prod. 2017, 143, 933–947. [Google Scholar] [CrossRef]

- Brønn, P.S.; Vidaver-Cohen, D. Corporate Motives for Social Initiative: Legitimacy, Sustainability, or the Bottom Line? J. Bus. Ethics 2009, 87, 91–109. [Google Scholar] [CrossRef]

- Font, X.; Garay, L.; Jones, S. Sustainability motivations and practices in small tourism enterprises in European protected areas. J. Clean. Prod. 2016, 137. [Google Scholar] [CrossRef]

- Paulraj, A. Environmental motivations: A classification scheme and its impact on environmental strategies and practices. Bus. Strat. Environ. 2009, 18, 453–468. [Google Scholar] [CrossRef]

- Shnayder, L.; van Rijnsoever, F.J.; Hekkert, M. Motivations for Corporate Social Responsibility in the packaged food industry: An institutional and stakeholder management perspective. J. Clean. Prod. 2016, 122, 212–227. [Google Scholar] [CrossRef]

- Wright, C.; Nyberg, D. An Inconvenient Truth: How Organizations Translate Climate Change into Business as Usual. Acad. Manag. J. 2017, 60, 1633–1661. [Google Scholar] [CrossRef]

- Den Hond, F.; de Bakker, F.G.A.; Doh, J. What Prompts Companies to Collaboration With NGOs?: Recent Evidence From the Netherlands. Bus. Soc. 2012, 54, 187–228. [Google Scholar] [CrossRef]

- Van Marrewijk, M.; Werre, M. Multiple levels of sustainability. J. Bus. Ethics 2003, 44, 107–119. [Google Scholar] [CrossRef]

- Sangle, S. Empirical analysis of determinants of adoption of proactive environmental strategies in India. Bus. Strat. Environ. 2009, 15, 51–63. [Google Scholar] [CrossRef]

- Gabaldon, P.; Gröschl, S. A Few Good Companies: Rethinking Firms’ Responsibilities Toward Common Pool Resources. J. Bus. Ethics 2015, 132, 579–588. [Google Scholar] [CrossRef]

- Hahn, T.; Scheermesser, M. Approaches to corporate sustainability among German companies. Corp. Soc. Responsib. Environ. Manag. 2006, 13, 150–165. [Google Scholar] [CrossRef]

- Sauser, W.I. Ethics in Business: Answering the Call. J. Bus. Ethics 2005, 58, 345–357. [Google Scholar] [CrossRef]

- Schaltegger, S.; Burritt, R. Business Cases and Corporate Engagement with Sustainability: Differentiating Ethical Motivations. J. Bus. Ethics 2015, 1–19. [Google Scholar] [CrossRef]

- Sebastiani, R.; Corsaro, D.; Montagnini, F.; Caruana, A. Corporate sustainability in action. Serv. Ind. J. 2014, 34, 584–603. [Google Scholar] [CrossRef]

- Aguilera, R.V.; Rupp, D.E.; Williams, C.A.; Ganapathi, J. Putting the S Back in Corporate Social Responsibility: A Multilevel Theory of Social Change in Organizations. Acad. Manag. Rev. 2007, 32, 836–863. [Google Scholar] [CrossRef]

- Graafland, J.; Mazereeuw-Van der Duijn Schouten, C. Motives for Corporate Social Responsibility. Economist 2012, 160, 377–396. [Google Scholar] [CrossRef]

- Babiak, K.; Trendafilova, S. CSR and environmental responsibility: Motives and pressures to adopt green management practices. Corp. Soc. Responsib. Environ. Manag. 2011, 18, 11–24. [Google Scholar] [CrossRef]

- Anderson, L.; Ostrom, A.L.; Corus, C.; Fisk, R.P.; Gallan, A.S.; Giraldo, M.; Mende, M.; Mulder, M.; Rayburn, S.W.; Rosenbaum, M.S.; et al. Transformative service research: An agenda for the future. J. Bus. Res. 2013, 66, 1203–1210. [Google Scholar] [CrossRef]

- Von Wallis, M.; Klein, C. Ethical requirement and financial interest: A literature review on socially responsible investing. Bus. Res. 2015, 8, 61–98. [Google Scholar] [CrossRef]

- Humphrey, J.E.; Warren, G.J.; Boon, J. What is Different about Socially Responsible Funds? A Holdings-Based Analysis. J. Bus. Ethics 2016, 138, 263–277. [Google Scholar] [CrossRef]

- Arjaliès, D.-L. A Social Movement Perspective on Finance: How Socially Responsible Investment Mattered. J. Bus. Ethics 2010, 92. [Google Scholar] [CrossRef]

- Crifo, P.; Mottis, N. Socially Responsible Investment in France. Bus. Soc. 2016, 55, 576–593. [Google Scholar] [CrossRef]

- Haack, P.; Schoeneborn, D.; Wickert, C. Talking the Talk, Moral Entrapment, Creeping Commitment? Exploring Narrative Dynamics in Corporate Responsibility Standardization. Organ. Stud. 2012, 33, 815–845. [Google Scholar] [CrossRef]

- Wörsdorfer, M. Equator Principles: Bridging the Gap between Economics and Ethics? Bus. Soc. Rev. 2015, 120, 205–243. [Google Scholar] [CrossRef]

- Gifford, E.J.M. Effective Shareholder Engagement: The Factors that Contribute to Shareholder Salience. J. Bus. Ethics 2010, 92, 79–97. [Google Scholar] [CrossRef]

- Goodman, J.; Arenas, D. Engaging Ethically: A Discourse Ethics Perspective on Social Shareholder Engagement. Bus. Ethics Q. 2015, 25, 163–189. [Google Scholar] [CrossRef]

- Goodman, J.; Louche, C.; van Cranenburgh, K.C.; Arenas, D. Social Shareholder Engagement: The Dynamics of Voice and Exit. J. Bus. Ethics 2014, 125, 193–210. [Google Scholar] [CrossRef]

- Soana, M.-G. The Relationship Between Corporate Social Performance and Corporate Financial Performance in the Banking Sector. J. Bus. Ethics 2011, 104, 133–148. [Google Scholar] [CrossRef]

- Jo, H.; Kim, H.; Park, K. Corporate Environmental Responsibility and Firm Performance in the Financial Services Sector. J. Bus. Ethics 2014. [Google Scholar] [CrossRef]

- Pérez, A.; Rodríguez del Bosque, I. Corporate social responsibility and customer loyalty: Exploring the role of identification, satisfaction and type of company. J. Serv. Mark. 2015, 29, 15–25. [Google Scholar] [CrossRef]

- United Nations. Sustainable Development Goals; 2015; Available online: https://sustainabledevelopment.un.org/sdgs (accessed on 2 February 2019).

- Gioia, D.A.; Corley, K.G.; Hamilton, A.L. Seeking Qualitative Rigor in Inductive Research: Notes on the Gioia Methodology. Organ. Res. Methods 2012, 16, 15–31. [Google Scholar] [CrossRef]

- Golafshani, N. Understanding Reliability and Validity in Qualitative Research. Qual. Rep. 2003, 8, 597–606. [Google Scholar]

- Spiggle, S. Analysis and Interpretation of Qualitative Data in Consumer Research. J. Consum. Res. 1994, 21, 491. [Google Scholar] [CrossRef]

- Patton, M.Q. Qualitative Research and Evaluation Methods, 3rd ed.; Sage Publications: Thousand Oaks, CA, USA, 2002. [Google Scholar]

- Palinkas, L.A.; Horwitz, S.M.; Green, C.A.; Wisdom, J.P.; Duan, N.; Hoagwood, K. Purposeful Sampling for Qualitative Data Collection and Analysis in Mixed Method Implementation Research. Adm. Policy Mental Health 2015, 42, 533–544. [Google Scholar] [CrossRef]

- Creswell, J.W. Qualitative Inquiry & Research Design: Choosing among Five Approaches; Sage Publications: Thousand Oaks, CA, USA, 2013. [Google Scholar]

- Kluge, S. Empirically Grounded Construction of Types and Typologies in Qualitative Social Research. Forum Qual. Sozialforschung 2000, 1. [Google Scholar] [CrossRef]

- Yuan, W.; Bao, Y.; Verbeke, A. Integrating CSR Initiatives in Business: An Organizing Framework. J. Bus. Ethics 2011, 101, 75–92. [Google Scholar] [CrossRef]

- Lazarsfeld, P. Some remarks on typological procedures in social research. Zeitschrift für Sozialforschung 1939, 6, 119–139. [Google Scholar] [CrossRef]

- George, A.L.; Bennett, A. Case Studies and Theory Development in the Social Sciences; MIT Press: Cambridge, UK, 2005. [Google Scholar]

- Bailey, K.H. Typologies and Taxonomies: An Introduction to Classification Techniques; Sage Publications: Thousand Oaks, CA, USA, 1994. [Google Scholar]

- Schaltegger, S.; Wagner, M. Sustainable entrepreneurship and sustainability innovation: Categories and interactions. Bus. Strat. Environ. 2011, 20, 222–237. [Google Scholar] [CrossRef]

- Dang, C.; Li, Z.; Yang, C. Measuring firm size in empirical corporate finance. J. Bank. Financ. 2018, 86, 159–176. [Google Scholar] [CrossRef]

- Yu, J.; Lo, C.W.-H.; Li, P.H.Y. Organizational Visibility, Stakeholder Environmental Pressure and Corporate Environmental Responsiveness in China. Bus. Strat. Environ. 2017, 26, 371–384. [Google Scholar] [CrossRef]

- Schreck, P.; Raithel, S. Corporate Social Performance, Firm Size, and Organizational Visibility: Distinct and Joint Effects on Voluntary Sustainability Reporting. Bus. Soc. 2018, 57, 742–778. [Google Scholar] [CrossRef]

- Eilert, M.; Walker, K.; Dogan, J. Can Ivory Towers be Green? The Impact of Organization Size on Organizational Social Performance. J. Bus. Ethics 2017, 140, 537–549. [Google Scholar] [CrossRef]

- Pantouvakis, A.; Vlachos, I.; Zervopoulos, P.D. Market orientation for sustainable performance and the inverted-U moderation of firm size: Evidence from the Greek shipping industry. J. Clean. Prod. 2017, 165, 705–720. [Google Scholar] [CrossRef]

- Zhang, Y.; Li, J.; Jiang, W.; Zhang, H.; Hu, Y.; Liu, M. Organizational structure, slack resources and sustainable corporate socially responsible performance. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 1099–1107. [Google Scholar] [CrossRef]

- Elsayed, K. Reexamining the Expected Effect of Available Resources and Firm Size on Firm Environmental Orientation: An Empirical Study of UK Firms. J. Bus. Ethics 2006, 65, 297–308. [Google Scholar] [CrossRef]

- Bowen, F.E. Does Size Matter?: Organizational Slack and Visibility as Alternative Explanations for Environmental Responsiveness. Bus. Soc. 2002, 41, 118–124. [Google Scholar] [CrossRef]

- Martinez, F. A Three-Dimensional Conceptual Framework of Corporate Water Responsibility. Organ. Environ. 2015, 28, 137–159. [Google Scholar] [CrossRef]

- Friedland, R.; Alford, R. Bringing society back in: Symbols, practices and institutional contradictions. In The New Institutionalism in Organizational Analysis; Powell, W.W., DiMaggio, P.J., Eds.; University of Chicago Press: Chicago, IL, USA, 1991; pp. 232–263. [Google Scholar]

- Thornton, P.H.; Ocasio, W.; Lounsbury, M. The Institutional Logics Perspective: A New Approach to Culture, Structure, and Process; Oxford University Press: Oxford, UK, 2012. [Google Scholar]

- Ocasio, W.; Loewenstein, J.; Nigam, A. How Streams of Communication Reproduce and Change Institutional Logics: The Role of Categories. Acad. Manag. Rev. 2015, 40, 28–48. [Google Scholar] [CrossRef]

- Walls, J.L.; Berrone, P.; Phan, P.H. Corporate governance and environmental performance: Is there really a link? Strat. Manag. J. 2012, 33, 885–913. [Google Scholar] [CrossRef]

- Hong, B.; Li, Z.; Minor, D. Corporate Governance and Executive Compensation for Corporate Social Responsibility. J. Bus. Ethics 2016, 136, 199–213. [Google Scholar] [CrossRef]

- García-Sánchez, I.-M.; Hussain, N.; Martínez-Ferrero, J. An empirical analysis of the complementarities and substitutions between effects of ceo ability and corporate governance on socially responsible performance. J. Clean. Prod. 2019, 215, 1288–1300. [Google Scholar] [CrossRef]

- Walker, K.; Ni, N.; Dyck, B. Recipes for Successful Sustainability: Empirical Organizational Configurations for Strong Corporate Environmental Performance. Bus. Strat. Environ. 2015, 24, 40–57. [Google Scholar] [CrossRef]

- Shaukat, A.; Qiu, Y.; Trojanowski, G. Board Attributes, Corporate Social Responsibility Strategy, and Corporate Environmental and Social Performance. J. Bus. Ethics 2016, 135, 569–585. [Google Scholar] [CrossRef]

- Bachiller, P.; Garcia-Lacalle, J. Corporate governance in Spanish savings banks and its relationship with financial and social performance. Manag. Decis. 2018, 56, 828–848. [Google Scholar] [CrossRef]

- Burke, J.J.; Hoitash, R.; Hoitash, U. The Heterogeneity of Board-Level Sustainability Committees and Corporate Social Performance. J. Bus. Ethics 2019, 154, 1161–1186. [Google Scholar] [CrossRef]