1. Introduction

Although the demand for new nuclear power plants (NPPs) dropped significantly during the 1980s and 1990s, the number of potential customers of nuclear energy has since increased, especially in the 2000s, which led to the suggestion of a possible “nuclear renaissance” that was later deemed far-fetched after the Fukushima nuclear accident in 2011 and several years of low oil prices [

1]. Nevertheless, the shift of demand for NPPs from traditional customers in the West to emerging countries in the East, especially China, has been observed since the end of the Cold War [

2]. There have been concerns that such a nuclear spread to states having no prior experience can undermine the robustness of the nonproliferation regime [

3]. Addressing such concerns, this paper examines the evolution of the nuclear export market from both the demand and supply sides, with focus on the characteristics of stakeholders in the market in terms of governance capabilities and nonproliferation compliance.

Although the construction time of a nuclear power unit can vary from several to ten years or more, in general a functional NPP can be operated for decades, thus the stability and governance capability of the host country throughout such a long lifetime of the plant are crucial to the safety, security, and nonproliferation of these complex industrial projects [

4]. To assess the stability of a country and its governance capability, this paper uses the definition of governance quality proposed by Kaufmann et al. [

5] and measured by the World Bank [

6], which include “(a) the process by which governments are selected, monitored and replaced; (b) the capacity of the government to effectively formulate and implement sound policies; and (c) the respect of citizens and the state for the institutions that govern economic and social interactions among them”. For example, governments with low level of stability and governance capability have a high risk of losing control of their nuclear facilities to rogue factions in cases of coups d’état or a sudden take-over like the cases of South Vietnam, Iraq, Ukraine, or Syria. It is also significantly more difficult to maintain the safety of nuclear infrastructure when political disputes occur or low-intensity conflicts persist. On the exporting side, similarly the lack of good governance has been a matter of concern. For example, in the early 1990s the United States (U.S.) implemented numerous policies to reverse Russia’s nuclear export to Iran partly due to the concern that the lack of an effective export control system in Russia following the collapse of the Soviet Union might lead to the leakage of nuclear materials and sensitive technologies to potential proliferators. In addition, having a high level of corruption may expose a government to a greater risk of corrupted officials and scientists transferring knowledge, skills, and technologies to non-state actors like terrorist groups. This problem has been particularly highlighted since the proliferation activities of the A.Q. Khan network were uncovered in the early 2000s.

This paper also argues that membership to nonproliferation-related agreements and organizations also helps the evaluation of a country’s adherence to the nonproliferation and export control regime. This is due to the fact that in many situations, a country participates in such the international regime in order to either communicate their nonproliferation compliance to other treaty members, or call for support to strengthen such compliance. Besides, by admitting new members, international organizations provide a cooperative environment for them to improve their domestic nonproliferation infrastructure. The improvement of Brazil’s compliance to the nonproliferation and export control regimes after its participation in the Missile Technology Control Regime (MTCR), or the admission of former communist countries to the Wassenaar Arrangements that helped transform the export control practices of these countries are two examples for this argument about considering nonproliferation-related treaty membership as an indicator for treaty compliance. In another case, despite its robust export control system, Taiwan has been considered a target for illicit proliferation-related trades due to its isolation from international treaties and organizations related to the nonproliferation regime.

2. Overview of the Nuclear Export Market

The new landscape in the demand side of the market has also initiated the transformation of the supply side in all stages of the nuclear fuel cycle. Although the export of nuclear reactors is often considered synonymous with the nuclear export market [

7], there are other types of services and technology transactions related to different stages of the nuclear fuel cycle, from uranium mining and milling, to conversion, enrichment, fuel fabrication, and nuclear reprocessing. Despite the lower total estimated value of these transactions in one year in comparison with NPP export contracts [

8], the supply of nuclear fuel and other services is often in forms of long-term contracts with consistent revenues for nuclear companies. In fact, such sustainable profits have been considered as one of the reasons why nuclear suppliers are sometimes willing to export reactors at discounted prices [

9].

At the front-end, the market for natural uranium, which was mostly shared among Western countries and the Soviet Union in the 1980s, is now dominated by Kazakhstan, Canada, Australia, and several African producers [

8]. In terms of enrichment services, the dominance of the trio United States Enrichment Corporation (USEC), Tenex (Russia), and Areva (France) in the early 1990s has gradually transformed into a duopoly between Tenex and Areva, which was renamed Orano in January 2018, by the late 2000s [

10]. The consolidation of market shares has also been observed in fuel fabrication, with almost three-quarters of the market belonging to Orano and two U.S.-Japan joint ventures. Finally, the lack of orders for new NPPs in the West has led to a situation where Rosatom gained ground while Chinese suppliers are catching up, whereas traditional suppliers from the U.S., European Union, and Japan have encountered diminishing commercial prospects [

11]. As a result, the industry has observed the transfer of ownership of numerous American and European technology suppliers to conglomerates from East Asia [

12].

To measure the change in market share, and the level of concentration in different sections of the nuclear fuel cycle market [

10], the Herfindahl-Hirschman Index (

HHI) was calculated based on Equation (1) and market share data [

8,

13,

14,

15]. According to the U.S. Department of Justice, the market is considered highly concentrated when H ≥ 0.25, moderately concentrated when 0.15 ≤ H < 0.25, unconcentrated when 0.01 ≤ H < 0.15, and highly competitive when H < 0.01. Any merger that leads to such highly concentrated market would be considered a matter of concern, as it can disadvantage customers in due to the increasing market power [

16].

where with

si being the market share of producer

i among

N producers competing in the market; 0 ≤

si ≤ 1.

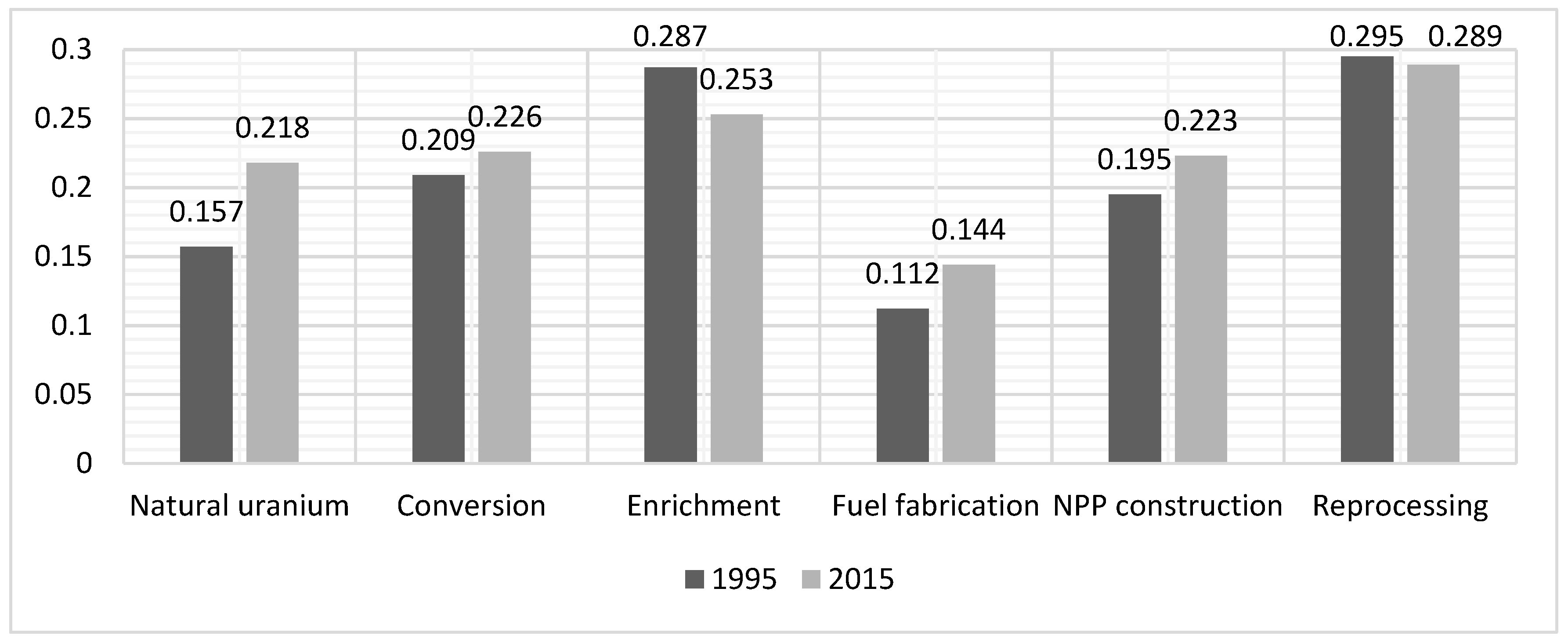

The comparison of estimated

HHI in 1995 and 2015 of the six major sections of the nuclear export market is presented in

Figure 1. Accordingly, the market has become more concentrated in almost all sectors, except for enrichment and reprocessing, which remain highly concentrated despite having lower

HHI after 20 years. This finding, which is similar to the results of a report by the Nuclear Energy Agency [

13], validates the longstanding concern of nuclear customers about the existence of a “nuclear cartel” that is a small group of powerful suppliers controlling the market [

17], especially in sections like natural uranium supply, reactor construction, and fuel cycle services. Even in the case of a less-concentrated enrichment sector, end-users still have reason to worry, as enriched uranium can only be used in reactors after the fuel fabrication process, of which the market concentration has increased noticeably since the early 1990s. Furthermore, when a customer wants to diversify the fuel supply from its original producer, a new supplier needs years to acquire the necessary safety license to be able to produce such alternative fuel [

18]. On the other hand, arguments have also been made that the supply surplus in natural uranium and nuclear fuel, and the uneventful history of uranium and fuel deliveries of the market can be considered reasons to assure nuclear customers about the long-term supply sustainability, and to render ideas like multinational reserves of fuel or enriched uranium like the Low-Enriched Uranium Bank owned and controlled by the International Atomic Energy Agency (IAEA) and hosted by Kazakhstan, impractical and uneconomical [

19]. Such arguments can be refuted, however, by historical evidence such as the decision by the U.S. halting uranium export to Brazil during the 1970s [

20].

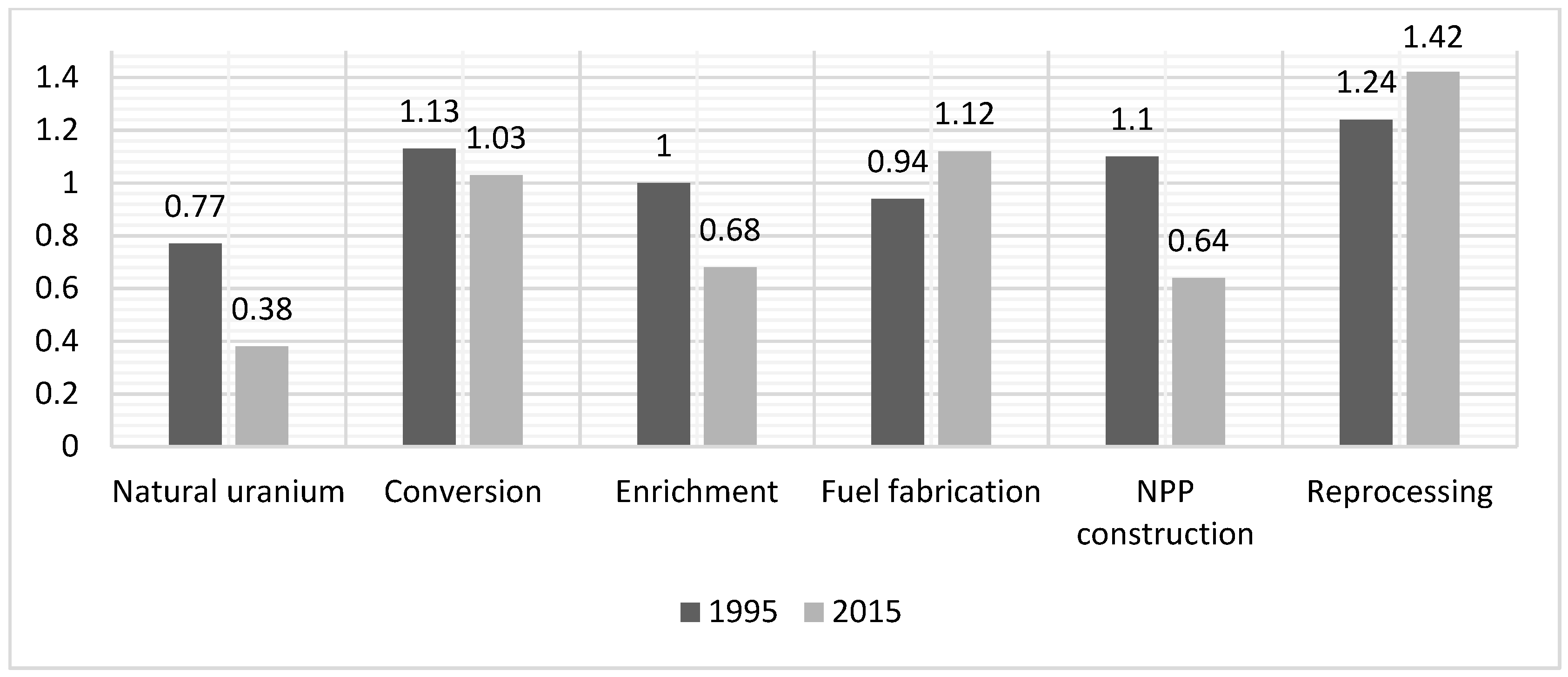

Given the reshuffle of suppliers in terms of market share, the total governance effectiveness of the market has also changed noticeably. Using the data provided by the World Bank, the overall governance effectiveness of the market (

Eff) was calculated using Equation (2) for 1995 and 2015 [

5,

6]. As is shown in

Figure 2, the estimated governance effectiveness of the nuclear market indicates a deterioration in almost all sections of the market, with the natural uranium supply and NPP construction having the biggest drops. Such lowered governance effectiveness can be explained by the shift of market shares in these sections from the well-developed Western countries to Eastern and African suppliers, which generally have lower governance capabilities. As new nuclear customers are also often developing countries with lesser governance capabilities, this deterioration may increase the risk of nuclear export to nuclear newcomers with lesser capabilities in safety (due to corruption in project management), security (due to sabotage and terrorism), and nonproliferation (due to domestic and regional instabilities).

where with

Effi being the governance effectiveness score of exporter

i; −2.5 (weakest effectiveness) ≤

Effi ≤ 2.5 (strongest).

After reviewing the nuclear market in a whole, the next sections will address the specific situations of the demand and supply sides of the market. In most of the onward discussions, the term “nuclear exporter” or “nuclear supplier”, unless specified otherwise, are used to refer to the supplying country of nuclear reactor technology, as this section of the nuclear fuel cycle market is the most visible in term of commercial, political, and social values, and reactor exporters are often selected as suppliers of nuclear fuels and other services for safety and economic reasons.

3. Status of Nuclear Exporters

As previously mentioned, Russia has been the dominating exporter in the global nuclear market since the 2000s. Despite some setbacks like Vietnam’s decision to indefinitely postpone the NPP contract under the agreement with Russia [

21], the Russian state-owned corporation Rosatom has been able to win contracts in numerous countries, ranging from existing nuclear users like Finland or Hungary, to newcomers like Jordan or Bangladesh. The repeated successes of Russia’s nuclear export have been attributed to the favorable financial clauses of Rosatom’s bids with direct support from the Russian government, the corporation’s ability to provide full fuel cycle services, or the flexible contractual structure that Rosatom can employ [

22]. Given the capital-intensive nature of NPP projects and Russia’s poor financial conditions due to the low oil price and sanctions by Western countries since 2014, experts have questioned Rosatom’s capabilities to deliver its signed contracts, and possibilities that the Russian government might use such projects as political leverage against its customers [

23]. Nevertheless, Rosatom has continued to put new VVER reactors into commercial operation domestic and abroad, whereas the Russian government has been actively looking for opportunities in new markets in Asia or Africa [

24].

Following Russia in expanding its portfolio in the nuclear market in recent years is China. Despite being a latecomer in the export market and being occupied with strong domestic demand, the Chinese nuclear industry has been able to gain a foothold abroad by taking over nuclear contracts of which suppliers and/or customers have struggled with financial issues, such as the NPP projects in Romania, Argentina, or the United Kingdom (UK) [

25]. Backed with financial advantages, strong political support from the government, and technological advantages, as China already possesses licenses for most of the advanced reactor technologies, Chinese nuclear corporations have emerged as strong contenders in the nuclear market [

26]. State ownership has also been cited as one of the advantages of the Republic of Korea (ROK) when they won contract to build four new reactors in the United Arab Emirates (UAE) over more experienced suppliers from the U.S. or France [

27]. However, the lack of full fuel cycle capabilities, and recent government’s nuclear phase-out policy might hinder ROK efforts to compete in the export market [

28].

Unlike the state-owned enterprises from Russia, China, and ROK, their private or partially state-owned counterparts from traditional nuclear suppliers like the U.S., France, Japan, and Canada have been struggling with completing delayed projects, or bidding in new markets with negligible financial supports from their governments. Furthermore, the lack of new orders back home has also greatly affected the manufacturing capabilities of these nuclear companies, and put them in an even more disadvantaged position [

29].

Surveying the involvement of the major nuclear exporters to the nonproliferation and export control regimes, it can be concluded that except for China, which has participated in only a half of the major relevant agreements and is the last among them joining the Nuclear Suppliers Group (NSG), all other exporters have comprehensive memberships to the ten international instruments related to nuclear nonproliferation and export control, namely the Nonproliferation Treaty (NPT); Comprehensive Safeguards Agreement (CSA); Additional Protocol (AP); Nuclear Suppliers Group (NSG); Zangger Committee (ZC); Missile Technology Control Regime (MTCR); Hague Code of Conduct (HCOC); Australian Group (AG); Wassenaar Arrangement (WASS); and Proliferation Security Initiative (PSI). China has not participated in the last five instruments from this list, whereas Russia was not an AG member but has partly incorporated the AG’s export control list in its domestic legislation [

30]. Even in the case of China’s non-participation, such absence has been partly due to legal disputes or the lack of consensus among existing participants about China’s bid for membership, while China has proven to be increasingly active in reinforcing its export control system [

31]. Still, the country has been criticized for its reactor exports to Pakistan, and for its complacency implementing international sanctions against North Korea [

32]. Here, it is necessary to mention that there have been other controversial export decisions made by suppliers with comprehensive nonproliferation membership, such as the nuclear cooperation agreement signed by the U.S. with India in 2005 despite the fact that India was not a member of the NPT and has not joined the regime since then. However, given the potential of China exporting technology to newcomer countries, China’s non-participation in international export control instruments might remain a matter of concern [

33].

5. Conclusions and Policy Recommendations

Based on the analysis in this paper, several conclusions can be made regarding the nuclear export market in general, and the situations of nuclear exporters and importers in particular, along with recommendations to improve the security and nonproliferation robustness of the market. Firstly, the nuclear export market has become more concentrated and uncertain. Such concentration and uncertainty will likely cause concerns among nuclear importers about the stable supply of technologies, materials, and services. Given the decline of traditional exporters and the emergence of new exporters with lesser governance capabilities, the average governance effectiveness of exporters has generally deteriorated, which could lead to the mismanagement of nuclear exports to newcomers.

Secondly, with respect to the evolution of nuclear suppliers, it is evident that Russia has been be dominating the market along with China, and will dominate the market in the future. Given Russia’s tendency to use energy supplies as a political leverage tool [

23], and China’s history of resorting to economic retaliation to address political disputes [

48], it would be desirable that traditional suppliers from the Western world retain certain shares in the market, especially in technology export related to the nuclear steam supply system, enrichment, and fuel fabrication in order to keep the market in healthy competition, and to maintain global standards. In particular, the foothold in uranium enrichment and fuel fabrication seems to be more feasible for the Western companies, as the markets for enrichment and fuel fabrication are less capital intensive while providing more long-term contracts, especially when customers need to diversify their fuel supply from Russian and Chinese suppliers. Such a foothold can be in the form of multilateral cooperation with new suppliers, in which technologies would be provided by traditional suppliers, whereas new suppliers are in charge of funding and financing [

49]. It should be noted, though, that safety regulations for alternative fuel fabrication will be a challenge, as was exemplified by the difficulties that Westinghouse faced in acquiring regulatory approval for their VVER-type fuel fabricated for Ukraine. Thus, state support in testing and licensing is essential.

Although regaining the technology market might be difficult for Western and Japanese suppliers due to their precarious domestic situations, a strategy to maintain their partial control in this sector still needs to be considered given the link between technology supply and fuel/services supply. When state-sponsored financial packages are unavailable, other incentives should be considered like state bilateral agreements on arms trade, direct investment, or technology transfer that are coupled with the bid for the nuclear contract. In this aspect, traditional nuclear exporters should also focus on the retransfer of Western-origin technologies to a third party through tightening the criteria for technological transfer/indigenization, as well as encouraging the NSG guideline implementation by its new Member States. The AP should also be made a prerequisite for any technology import in order to enhance the transparency by the importers in utilizing nuclear technology, to demonstrate the adherence of the exporters to export control regimes, and to supplement the ad-hoc nature of the control list. In fact, as there has not existed a full-scope framework for civil nuclear export control, in 2008 the Carnegie Endowment for International Peace has initiated the development and promotion of the Nuclear Power Plant Exporters’ Principles of Conduct [

50]. Despite containing innovative features such as the independence from state involvement, or the flexible adaptation of the safety requirements by the IAEA, this initiative has not been mentioned recently when its participants like Areva (now Orano) or KEPCO encountered safety-related issues with their supply chains. In addition, traditional suppliers should secure the market for spent fuel management, including dry storage and final disposal solutions, as back-end fuel cycle has become an issue to many nuclear users. To facilitate commercial opportunities in this part of the fuel cycle, geological disposal should be successfully implemented in Sweden, Finland, France, and the U.S., whereas disposal in a third and non-nuclear party like Mongolia or Australia should be explored.

Thirdly, most of the prospective nuclear customers have significantly lower governance capabilities than major nuclear exporters in term of nuclear safety, security, and project managements. Also, there is a discrepancy regarding the adherence of prospective importers to international nonproliferation norms. In contrast to their efforts to build up the scientific and technological capabilities to develop nuclear energy, new customers have not paid enough attention to reinforcing their export control and nonproliferation commitments. Such lack of governance capabilities in nuclear newcomers indicates not only the risk of mismanagement by state actors, but also the risk of the state system bypassed or exploited by non-state actors. As most newcomers are looking for full-scale reactors for the purpose of energy security, financing has been the most difficult barrier for nuclear newcomers [

51]. This creates enough incentive for the newcomer countries to seek active external support in building governance capabilities, especially in nuclear security and export control. In particular, these countries should be persuaded that a higher priority for nonproliferation and export control would facilitate the flow of nuclear trade in and out of their territories, and not affect the benefits from nuclear cooperation [

52]. Moreover, given the lack of economic viability and the diversity of suppliers, a stable and diverse supply of uranium should be maintained from Canada, Australia, and Africa. In addition, Western countries should retain the conversion, enrichment, and fuel fabrication capabilities to prevent the total control of these markets by Russia and China.

Finally, the zero-growth policy and reliance of safeguards funding on extra budgetary contributions should be replaced by demand-based budget planning and adequate regular funding. Safeguards contribution of a Member State to the IAEA should be commensurate with the size or potential of its nuclear program, and not based on the shielding program. In particular, emerging nuclear exporters like Russia, ROK, and China should financially support the safeguards system proportionally to the benefits they acquire from the market. Transparency and openness for areas such as the public distribution of reports related to IAEA safeguards funding, are also necessary in order to mobilize third-party support for such a reform of the funding mechanism for the Agency. In addition, newcomers looking for an acquisition of research reactor require equal attention to other constructing nuclear power plants, as the financial demands for safeguarding these two types of facilities are comparable. It is easier for states to provide legitimate rationales for these types of projects, which are also less demanding nature in terms of technology and funding, whereas a small reactor can still be directly used for proliferation purposes, or indirectly for increasing nuclear latent capabilities through manpower development. Therefore, the nonproliferation and security of the civil nuclear market can only be ensured if the export of research reactors, especially to developing countries with no prior nuclear experiences, is properly addressed with necessary scrutiny of the implication of such projects.

In terms of nuclear nonproliferation and security policies over the past two decades, the attention of the international community has mostly focused on a number of specific and prominent cases like the North Korea and Iran nuclear crises. However, as this paper illustrated, the evolution of the civil nuclear export market during the same period has fundamentally changed the market shares of, and the dynamics between nuclear exporters and their potential customers. These changes, which are exemplified by the rise of new nuclear suppliers and importers from the East, may lead to new nuclear risks into the future due to their lesser governance capabilities and lower priority for nonproliferation and export control policies. Therefore, a range of policies, as discussed above, should be carefully examined and systematically implemented in order to reinforce the nonproliferation and security characteristics of the global nuclear industry for the responsible use of nuclear energy.

Lastly, it is necessary to note the limitations of current compliance measurements like the UNSCR1540 matrices or the NTI Nuclear Security Index. For example, the NTI Index was partly developed through expert judgement, thus specific conditions of countries will create discrepancies in the assessment by reviewers from different countries, as was the case with China [

53]. Neither checklist-form of the UNSCR1540 matrices can assure that the final score of a state matrix would truly reflect its compliance to nonproliferation and export control. In addition, these metrics are not sufficient to address the synergy between nuclear safety, security, and safeguards, which have played an increasingly important role in the safe and secured development of nuclear power in any country [

54]. However, due to the lack of alternative metrics, these datasets were used in this paper as an attempt to provide a holistic picture of nonproliferation compliance worldwide. Although this approach may not be suitable to point out the different weaknesses and disadvantages of different newcomers that have distinctive socio-political conditions and nuclear energy ambitions, the comprehensive perspective it provided about the state of countries’ compliance to the nonproliferation and export control regime is a useful contribution to the nonproliferation literature, and may encourage reconsideration of the distribution of international resources for safeguards and export control, as well as general policies that can be applied to improve the market situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}