The Triple Bottom Line on Sustainable Product Innovation Performance in SMEs: A Mixed Methods Approach

Abstract

:1. Introduction

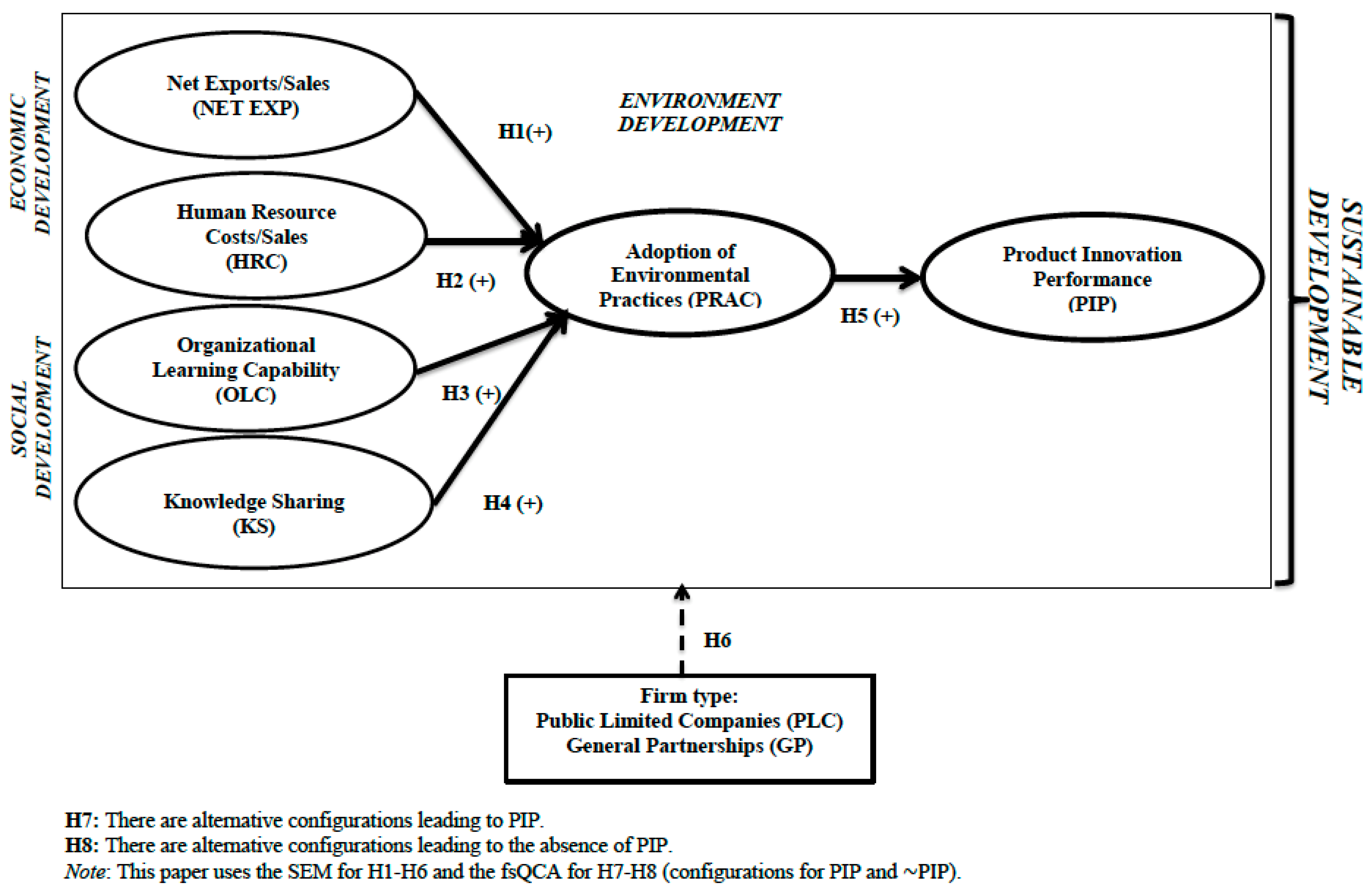

2. Literature Review and Hypotheses

2.1. Triple Bottom Line Approach

- ○

- How are economic, social, and environmental aspects balanced in innovation activities?

- ○

- What is needed to make the triple bottom line approach more effective (e.g., new communications, new human resources practices, and knowledge sharing management methods)?

- ○

- Does a firm’s legal form (e.g., public limited companies versus general partnerships) affect its commitment toward sustainable innovation?

2.2. Economic Development

2.2.1. Internationalization

2.2.2. Human Resource Cost

2.3. Social Development

2.3.1. Organizational Learning Capability

2.3.2. Knowledge Sharing

2.4. Environment Development

Adoption of Environmental Practices

2.5. Product Innovation Performance for Sustainable Development

2.6. Firm Type

2.6.1. Public Limited Companies

2.6.2. General Partnerships

2.7. Alternative Configurations

3. Methods

3.1. Mixed Methods Approach

- (1)

- Combines the strengths provided by the two approaches.

- (2)

- Attenuates the weaknesses of their separate application.

- (3)

- Allows for a better understanding of PRAC and PIP.

3.2. Sample

3.3. Variables

3.4. Calibration

4. Results

4.1. Structural Equation Modeling

4.2. Fuzzy-Set Qualitative Comparative Analysis

5. Discussion and Conclusions

5.1. Theoretical and Practical Implications

- International business for sustainable innovation:

- The willingness of experts to help with new international activities.

- Presence in congresses and international fairs.

- Continuous vigilance to detect new investment and export opportunities.

- Joint innovation projects with foreign partners.

- Investment in and development of new human resource practices for sustainable innovation:

- Courses and training in sustainable development.

- Encouragement of employee trust and motivation.

- Creation of a culture that encourages sustainable development.

- The build-up of norms that encourage sustainable development.

- Fast Organizational Learning Capability for sustainable innovation:

- Climate for learning and experimentation.

- Encouragement to take risks in the design of new sustainable products.

- Implementation of environmental information collection systems to determine the needs of consumers.

- Teamwork and effective communication.

- Involvement of employees in important decisions.

- Knowledge Sharing for sustainable innovation:

- Reinforcement of information sharing with new alliances and business partners.

- Creation of a culture that encourages knowledge sharing.

- Encouragement of employees to share their knowledge and ideas with those outside partners.

- Support for business networking (e.g., LinkedIn).

- Use of performance management systems to promote voice and knowledge sharing.

- Creation of incentives (e.g., promotion, bonus, higher salary) to facilitate knowledge sharing.

- Adoption of Environmental practices for sustainable innovation:

- Design of a code of environmental ethics for all members of the company and its business partners.

- Implementation of energy saving practices.

- Implementation of reverse logistics practices.

- Development of productive activity with ecological products.

- Advanced training in eco-innovation and social and environmental needs.

5.2. Limitations and Future Research

Author Contributions

Funding

Conflicts of Interest

References

- Dahlsrud, A. How Corporate Social Responsibility is defined: An Analysis of 37 definitions. Corp. Soc. Responsib. Environ. Manag. 2008, 15, 1–13. [Google Scholar] [CrossRef]

- Hart, S.L.; Milstein, M.B. Creating Sustainable Value. Acad. Manag. Exec. 2003, 17, 56–67. [Google Scholar] [CrossRef]

- Longoni, A.; Cagliano, R. Sustainable Innovativeness and the Triple Bottom Line: The Role of Organizational Time Perspective. J. Bus. Ethics 2018, 151, 1097–1120. [Google Scholar] [CrossRef]

- Ayyagari, M.; Demirgü-Kunt, A.; Maksimovic, V. Small vs. Young Firms across the World—Contribution to Employment, Job Creation, and Growth; Policy Research Working Paper 5631; World Bank: Washington, DC, USA, 2011. [Google Scholar]

- Testa, F.; Gusmerottia, N.M.; Corsini, F.; Passetti, E.; Iraldo, F. Factors Affecting Environmental Management by Small and Micro Firms: The Importance of Entrepreneurs’ Attitudes and Environmental Investment. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 373–385. [Google Scholar] [CrossRef]

- Schramm, C. All Entrepreneurship is Social. Stanf. Soc. Innov. Rev. 2010, 7, 20–22. [Google Scholar]

- Cohen, B.; Smith, B.; Mitchell, R. Toward a Sustainable Conceptualization of Dependent Variables in Entrepreneurship Research. Bus. Strategy Environ. 2008, 17, 107–119. [Google Scholar] [CrossRef]

- Glavas, A.; Mish, J. Resources and Capabilities of Triple Bottom Line Firms: Going over Old or Breaking New Ground? J. Bus. Ethics 2015, 127, 623–642. [Google Scholar] [CrossRef]

- Dibrell, C.; Craig, J.B.; Kim, J.; Johnson, A.J. Establishing How Natural Environmental Competency, Organizational Social Consciousness, and Innovativeness Relate. J. Bus. Ethics 2015, 127, 591–605. [Google Scholar] [CrossRef]

- Kennedy, E.B.; Marting, T.A. Biomimicry Streamlining the Front End of Innovation for Environmentally Sustainable Products. Res.-Technol. Manag. 2016, 59, 40–47. [Google Scholar] [CrossRef]

- Wagner, M. Innovation and Competitive Advantages from the Integration of Strategic Aspects with Social and Environmental Management in European Firms. Bus. Strategy Environ. 2009, 18, 291–306. [Google Scholar] [CrossRef]

- Hall, J.; Wagner, M. Integrating Sustainability into Firms’ Processes: Performance Effects and the Moderating Role of Business Models and Innovation. Bus. Strategy Environ. 2012, 21, 183–196. [Google Scholar] [CrossRef]

- Schaltegger, S.; Hansen, E.G.; Lüdeke-Freund, F. Business Models for Sustainability: Origins, Present Research, and Future Avenues. Organ. Environ. 2016, 29, 3–10. [Google Scholar] [CrossRef]

- Gasbarro, F.; Annunziata, E.; Rizzi, F.; Frey, M. The Interplay between Sustainable Entrepreneurs and Public Authorities: Evidence from Sustainable Energy Transitions. Organ. Environ. 2017, 30, 226–252. [Google Scholar] [CrossRef]

- Vollenbroek, F.A. Sustainable Development and the Challenge of Innovation. J. Clean. Prod. 2002, 10, 215–223. [Google Scholar] [CrossRef]

- Wu, G.C. Effects of Socially Responsible Supplier Development and Sustainability-Oriented Innovation on Sustainable Development: Empirical Evidence from SMEs. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 661–675. [Google Scholar] [CrossRef]

- Hitt, M.A.; Ireland, R.D.; Hoskisson, R.E. Strategic Management: Competitiveness and Globalization, 7th ed.; Thomson South-Western: Mason, OH, USA, 2007. [Google Scholar]

- Attig, N.; Boubakri, N.; El Ghoul, S.; Guedhami, O. Firm Internationalization and Corporate Social Responsibility. J. Bus. Ethics 2016, 134, 171–197. [Google Scholar] [CrossRef]

- Ayuso, S.; Roca, M.; Arevalo, J.A.; Aravind, D. What Determines Principle-Based Standards Implementation? Reporting on Global Compact adoption in Spanish Firms. J. Bus. Ethics 2016, 133, 553–565. [Google Scholar] [CrossRef]

- Bansal, P. Evolving Sustainability: A Longitudinal Study of Corporate Sustainable Development. Strateg. Manag. J. 2005, 26, 197–218. [Google Scholar] [CrossRef]

- Strike, V.M.; Gao, J.; Bansal, P. Being Good while Being Bad: Social Responsibility and International Diversification of US Firms. J. Int. Bus. Stud. 2006, 37, 850–862. [Google Scholar] [CrossRef]

- Hoppmann, J. The Role of Interfirm Knowledge Spillovers for Innovation in Mass-Produced Environmental Technologies: Evidence from the Solar Photovoltaic Industry. Organ. Environ. 2018, 31, 3–24. [Google Scholar] [CrossRef]

- Celma, D.; Martínez-Garcia, E.; Coenders, G. Corporate Social Responsibility in Human Resource Management: An Analysis of Common Practices and their Determinants in Spain. Corp. Soc. Responsib. Environ. Manag. 2014, 21, 82–99. [Google Scholar] [CrossRef]

- Gratton, L.; Ghoshal, S. Managing Personal Human Capital: New Ethos for the ‘Volunteer’employee. Eur. Manag. J. 2003, 21, 1–10. [Google Scholar] [CrossRef]

- Muñoz-Pascual, L.; Galende, J. The Impact of Knowledge and Motivation Management on Creativity: Employees of Innovative Spanish Companies. Empl. Relat. 2017, 39, 732–752. [Google Scholar] [CrossRef]

- Barney, J.B. Looking Inside for Competitive Advantage. Acad. Manag. Exec. 1995, 9, 49–61. [Google Scholar] [CrossRef]

- Jérez-Gómez, P.; Cespedes-Lorente, J.; Valle-Cabrera, R. Organizational Learning and Compensation Strategies: Evidence from the Spanish Chemical Industry. Hum. Resour. Manag. 2005, 44, 279–299. [Google Scholar] [CrossRef]

- Jaw, B.S.; Liu, W. Promoting Organizational Learning and Self-Renewal in Taiwanese Companies: The Role of HRM. Hum. Resour. Manag. 2003, 42, 223–241. [Google Scholar] [CrossRef]

- Argote, L. Organizational Learning: Creating, Retaining and Transferring Knowledge, 2nd ed.; Springer: Media, PA, USA, 2013. [Google Scholar]

- Lichtenthaler, U. Absorptive Capacity, Environmental Turbulence, and the Complementarity of Organizational Learning Processes. Acad. Manag. J. 2009, 52, 822–846. [Google Scholar] [CrossRef]

- Chiva, R.; Alegre, J.; Lapiedra, R. Measuring Organizational Learning Capability Among the Workforce. Int. J. Manpow. 2007, 28, 224–242. [Google Scholar] [CrossRef]

- Valaei, N.; Rezaei, S.; Wan-Ismail, W.K. Examining Learning Strategies, Creativity, and Innovation at SMEs using fuzzy set Qualitative Comparative Analysis and PLS Path Modeling. J. Bus. Res. 2017, 70, 224–233. [Google Scholar] [CrossRef]

- Shih, S.C.; Hsu, S.H.Y.; Zhu, Z.; Balasubramanian, S.K. Knowledge Sharing, a Key Role in the Downstream Supply Chain. Inf. Manag. 2012, 49, 70–80. [Google Scholar] [CrossRef]

- Bhatti, W.A.; Larimo, J.; Carrasco, I. Strategy’s Effect on Knowledge Sharing in Host Country Networks. J. Bus. Res. 2016, 69, 4769–4774. [Google Scholar] [CrossRef]

- Boer, N.I.; Berends, H.; Van Baalen, P. Relational Models for Knowledge Sharing Behavior. Eur. Manag. J. 2011, 29, 85–97. [Google Scholar] [CrossRef]

- Cheng, J.H. Inter-Organizational Relationships and Information Sharing in Supply Chains. Int. J. Inf. Manag. 2011, 31, 374–384. [Google Scholar] [CrossRef]

- Liu, Y.; Li, Y.; Shi, L.H.; Liu, T. Knowledge Transfer in Buyer-Supplier Relationships: The role of transactional and relational governance mechanisms. J. Bus. Res. 2017, 78, 285–293. [Google Scholar] [CrossRef]

- Kianto, A.; Sáenz, J.; Aramburu, N. Knowledge-Based Human Resource Management Practices, Intelectual Capital and Innovation. J. Bus. Res. 2017, 81, 11–20. [Google Scholar] [CrossRef]

- Xie, X.; Fang, L.; Zeng, S.; Huo, J. How does knowledge inertia affect firms’ product innovation? J. Bus. Res. 2016, 69, 1615–1620. [Google Scholar] [CrossRef]

- Gavronski, I.; Ferrer, G.; Paiva, E.L. ISO 14001 Certification in Brazil: Motivations and Benefits. J. Clean. Prod. 2008, 16, 87–94. [Google Scholar] [CrossRef]

- Fernández-Viñé, M.B.; Gómez-Navarro, T.; Capuz-Rizo, S.F. Eco-efficiency in the SMEs of Venezuela. Current Status and Future Perspectives. J. Clean. Prod. 2010, 18, 736–746. [Google Scholar] [CrossRef]

- Ramanathan, R.; Black, A.; Nath, P.; Muyldermans, L. Impact of Environmental Regulations on Innovation and Performance in the UK Industrial Sector. Manag. Decis. 2010, 48, 1493–1513. [Google Scholar] [CrossRef]

- Aragón-Correa, J.A.; Hurtado-Torres, N.; Sharma, S.; García-Morales, V.J. Environmental Strategy and Performance in Small Firms: A Resource-Based Perspective. J. Environ. Manag. 2008, 86, 88–103. [Google Scholar] [CrossRef]

- Chan, E.S.W.; Hawkins, R. Attitude Towards EMSs in an International Hotel: An Exploratory Case Study. Int. J. Hosp. Manag. 2010, 29, 641–651. [Google Scholar] [CrossRef]

- Mohamed, S.T. The Impact of ISO 14,000 on developing World Businesses. Renew. Energy 2001, 23, 579–584. [Google Scholar] [CrossRef]

- Fresner, J.; Engelhardt, G. Experiences with Integrated Management Systems for Two Small Companies in Austria. J. Clean. Prod. 2004, 12, 623–631. [Google Scholar] [CrossRef]

- Amabile, T.M.; Conti, R.; Coon, H.; Lazenby, J.; Herron, M. Assessing the Work Environment for Creativity. Acad. Manag. J. 1996, 39, 1154–1184. [Google Scholar]

- Ngo, L.V.; O’Cass, A. Innovation and Business Success: The Mediating Role of Customer Participation. J. Bus. Res. 2013, 66, 1134–1142. [Google Scholar] [CrossRef]

- Chang, C.H. The Determinants of Green Product Innovation Performance. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 65–76. [Google Scholar] [CrossRef]

- Alegre, J.; Lapiedra, R.; Chiva, R. A Measurement Scale for Product Innovation Performance. Eur. J. Innov. Manag. 2006, 9, 333–346. [Google Scholar] [CrossRef]

- Kyffin, S.; Gardien, P. Navigating the Innovation Matrix: An Approach to Designled Innovation. Int. J. Des. 2009, 3, 57–69. [Google Scholar]

- Gupta, S.; Malhotra, N. Marketing Innovation: A Resource-Based View of International and Local Firms. Mark. Intell. Plan. 2013, 31, 111–126. [Google Scholar] [CrossRef]

- Curado, C.; Muñoz-Pascual, L.; Galende, J. Antecedent to Innovation Performance in SMEs: A Mixed Methods Approach. J. Bus. Res. 2018, 89, 206–215. [Google Scholar] [CrossRef]

- Fiss, P.C. Building Better Causal Theories: A Fuzzy Set Approach to Typologies in Organization Research. Acad. Manag. J. 2011, 54, 393–420. [Google Scholar] [CrossRef]

- Osabutey, E.L.C.; Jin, Z. Factors Influencing Technology and Knowledge Transfer: Configurational Recipes for Sub-Saharan Africa. J. Bus. Res. 2016, 69, 5390–5395. [Google Scholar] [CrossRef]

- Ozkan-Canbolat, E.; Beraha, A. Evolutionary Knowledge Games in Social Networks. J. Bus. Res. 2016, 69, 1807–1811. [Google Scholar] [CrossRef]

- Cragun, D.; Pal, T.; Vadaparampil, S.; Baldwin, J.; Hampel, H.; DeBate, R. Qualitative Comparative Analysis: A Hybrid Method for Identifying Factors Associated with Program Effectiveness. J. Mix. Methods Res. 2016, 10, 251–272. [Google Scholar] [CrossRef]

- Oyemomi, O.; Liu, S.; Neaga, I.; Alkhuraiji, A. How Knowledge Sharing and Business Process Contribute to Organizational Performance: Using the fsQCA Approach. J. Bus. Res. 2016, 69, 4725–5546. [Google Scholar] [CrossRef]

- Berkovich, I. Beyond Qualitative/Quantitative Structuralism: The Positivist Qualitative Research and the Paradigmatic Disclaimer. Qual. Quant. 2018, 52, 2063–2077. [Google Scholar] [CrossRef]

- Creswell, J.; Plano, V. Designing and Conducting Mixed Methods Research; Sage Publications, Inc.: Thousand Oaks, CA, USA, 2007. [Google Scholar]

- Kraus, S.; Ribeiro-Soriano, D.; Schüssler, M. Fuzzy-set Qualitative Comparative Analysis (fsQCA) in Entrepreneurship and Innovation Research—The Rise of a Method. Int. Entrep. Manag. J. 2018, 14, 15–33. [Google Scholar] [CrossRef]

- Hair, J.; Anderson, R.; Tatham, R.; Black, W. Multivariate Data Analysis; Prentice-Hall: Upper Saddle River, PA, USA, 2005. [Google Scholar]

- Armstrong, J.S.; Overton, T.S. Estimating Nonresponse Bias in Mail Surveys. J. Mark. Res. 1977, 14, 396–402. [Google Scholar] [CrossRef]

- Westland, J.C. Data Collection, Control, and Sample Size. In Structural Equation Models: From Paths to Networks; Westland, J.C., Ed.; Springer International Publishing: Cham, Switzerland, 2015; Volume 22, pp. 83–115. [Google Scholar]

- Alegre, J.; Chiva, R. Assessing the Impact of Organizational Learning Capability on Product Innovation Performance: An Empirical Test. Technovation 2008, 28, 315–326. [Google Scholar] [CrossRef]

- Chen, Y.H.; Lin, T.P.; Yen, D.C. How to facilitate Inter-Organizational Knowledge Sharing: The Impact of Trust. Inf. Manag. 2014, 51, 568–578. [Google Scholar] [CrossRef]

- Molina-Azorín, J.F.; Claver-Cortes, E.; Pereira-Moliner, J.; Tarí, J.J. Environmental Practices and Firm Performance: An Empirical Analysis in the Spanish Hotel Industry. J. Clean. Prod. 2009, 17, 516–524. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, Y.; Podsakoff, N.P. Common Method Biases in Behavioral Research: A Critical Review of the Literature and Recommended Remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef] [PubMed]

- Rennings, K.; Ziegler, A.; Ankele, K.; Hoffmann, E. The Influence of Different Characteristics of the EU Environmental Management and Auditing Scheme on Technical Environmental Innovations and Economic Performance. Ecol. Econ. 2006, 57, 45–59. [Google Scholar] [CrossRef]

- Ziegler, A.; Nogareda, J.S. Environmental Management Systems and Technological Environmental Innovations: Exploring the Causal Relationship. Res. Policy 2009, 38, 885–893. [Google Scholar] [CrossRef]

- Ragin, C.C. Redesigning Social Inquiry: Fuzzy Sets and Beyond; University of Chicago Press: Chicago, IL, USA, 2008. [Google Scholar]

- Woodside, A.; Hsu, S.Y.; Marshall, R. General Theory of Cultures Consequences on International Tourism Behavior. J. Bus. Res. 2011, 64, 785–799. [Google Scholar] [CrossRef]

- Woodside, A.G.; Prentice, C.; Larsen, A. Revisiting Problem Gamblers’ Harsh Gaze on Casino Services: Applying Complexity Theory to Identify Exceptional Customers. Psychol. Mark. 2015, 32, 65–77. [Google Scholar] [CrossRef]

- Fiss, P.C.; Sharapov, D.; Conqvist, L. Opposites Attract? Opportunities and Challenges for Integrating Large-N QCA and Econometric Analysis. Political Res. Q. 2013, 66, 191–235. [Google Scholar]

- Ragin, C.C. Fuzzy-Set Social Science; Chicago University Press: Chicago, IL, USA, 2000. [Google Scholar]

- Ragin, C.C. From Fuzzy Sets to Crisp Truth Tables; Working paper; University of Arizona: Tucson, AZ, USA, 2005. [Google Scholar]

- Ragin, C.C. Qualitative Comparative Analysis using Fuzzy Sets (fsQCA). In Configurational Comparative Methods: Qualitative Comparative Analysis (QCA) and Related Techniques; Rihoux, B., Ragin, C.C., Eds.; Sage Publications: Thousand Oaks, CA, USA, 2009; pp. 87–121. [Google Scholar]

- Woodside, A.; Zhang, M. Cultural Diversity and Marketing Transactions: Are Market Integration, Large Community Size, and World Religions Necessary for Fairness in Ephemeral Exchanges? Psychol. Mark. 2013, 30, 263–276. [Google Scholar] [CrossRef]

- Molina-Azorín, J.F.; López-Gamero, M.D. Mixed Methods Studies in Environmental Management Research: Prevalence, Purposes and Designs. Bus. Strategy Environ. 2016, 25, 134–148. [Google Scholar] [CrossRef]

- White, C.L.; Nielsen, A.E.; Valentini, C. CSR Research in the Apparel Industry: A Quantitative and Qualitative Review of Existing Literature. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 382–394. [Google Scholar] [CrossRef]

- Song, W.; Yu, H. Green Innovation Strategy and Green Innovation: The Roles of Green Creativity and Green Organizational Identity. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 135–150. [Google Scholar] [CrossRef]

- Kraus, S.; Burtscher, J.; Niemand, T.; Roig-Tierno, N.; Syrjä, P. Configurational Paths to Social Performance in SMEs: The Interplay of Innovation, Sustainability, Resources and Achievement Motivation. Sustainability 2017, 9, 1828. [Google Scholar] [CrossRef]

- Musa, M.H.; Mohamad, M.N. Importance of Green Innovation in Malaysian SMEs: Advantages and Future Research. Int. Acad. J. Bus. Manag. 2018, 5, 64–73. [Google Scholar]

{kind=link}

| Constructs | Mean | SD | Loading Factor |

|---|---|---|---|

| *Organizational Learning Capability (OLC) (V.E = 70.09%); (α = 0.95) | |||

| Experimentation (OLC-E) | |||

| OLC-E1. In my organization, people receive support and encouragement when presenting new ideas | 4.91 | 1.65 | 0.86 |

| OLC-E2. In my organization, initiative receives a favorable response, so people feel encouraged to generate new ideas | 4.85 | 1.58 | 0.86 |

| Risk Taking (OLC-R) | |||

| OLC-R3. In my organization, people are encouraged to take risk | 4.54 | 1.62 | 0.85 |

| OLC-R4. In my organization, people often venture into unknown territory | 3.79 | 1.58 | 0.84 |

| Interaction with the external environment (OLC-I) | |||

| OLC-I5. In my organization, it is part of the work of all staff to collect, bring back, and report information about what is going on outside the company | 4.21 | 1.78 | 0.83 |

| OLC-I6. In my organization, there are systems and procedures for receiving, collating and sharing information from outside the company | 3.90 | 1.73 | 0.83 |

| OLC-I7. In my organization, people are encouraged to interact with the environment: competitors, customers, technological institutes, universities, suppliers, etc. | 4.48 | 1.69 | 0.82 |

| Dialogue (OLC-D) | |||

| OLC-D8. In my organization, employees are encouraged to communicate | 5.07 | 1.59 | 0.80 |

| OLC-D9. In my organization, there is a free and open communication within my work group | 5.38 | 1.47 | 0.77 |

| OLC-D10. In my organization, managers facilitate communication | 5.26 | 1.60 | 0.77 |

| OLC-D11. In my organization, cross-functional teamwork is a common practice | 4.84 | 1.70 | 0.73 |

| Participative decision making (OLC-P) | |||

| OLC-P12. Managers in my organization frequently involve employees in important decisions | 4.64 | 1.76 | 0.67 |

| OLC-P13. In my organization polices are significantly influenced by the employees’views | 4.33 | 1.67 | 0.63 |

| OLC-P14. In my organization, people feel involved in main company decisions | 4.28 | 1.72 | 0.58 |

| *Knowledge Sharing (KS) (V.E = 75.53%); (α = 0.92) | |||

| KS1. My organization provides relevant knowledge to our business partners | 4.57 | 1.58 | 0.92 |

| KS2. My organization teams up with business partners to enhance interfirm learning | 4.52 | 1.71 | 0.90 |

| KS3. My organization and other business partners jointly organize job training to enhance each other´s knowledge | 3.91 | 1.72 | 0.88 |

| KS4. My organization and other business partners share successful experiences with each other | 4.12 | 1.70 | 0.86 |

| KS5. My organization and other business partners share new knowledge and viewpoints with each other | 4.13 | 1.64 | 0.77 |

| *Adoption of Environmental Practices (PRAC) (V.E = 66.89%); (α = 0.87) | |||

| PRAC1. My organization buys ecological products | 4.27 | 1.69 | 0.86 |

| PRAC2. My organization has reduced the use of cleaning products that are harmful to the environment | 4.76 | 1.71 | 0.88 |

| PRAC3. My organization implements energy-saving practices | 5.39 | 1.44 | 0.82 |

| PRAC4. My organization implements water-saving practices | 5.21 | 1.48 | 0.77 |

| PRAC5. My organization implements the selective collection of solid residues | 5.79 | 1.45 | 0.72 |

| *Product Innovation Performance (PIP) (V.E = 63,49%); (α = 0.89) | |||

| Product innovation efficacy (PIP-EFFICA) | |||

| PIP-EFFICA1. Replacement of products being phased out | 4.81 | 1.56 | 0.84 |

| PIP-EFFICA2. Extension of product range within main product field through new products | 5.28 | 1.50 | 0.83 |

| PIP-EFFICA3. Extension of product range outside main product field | 4.63 | 1.64 | 0.83 |

| PIP-EFFICA4. Development of environment-friendly products | 4.37 | 1.77 | 0.81 |

| PIP-EFFICA5. Market share evolution | 5.17 | 1.54 | 0.73 |

| PIP-EFFICA6. Opening of new markets abroad | 5.07 | 1.83 | 0.68 |

| PIP-EFFICA7. Opening of new domestic target groups | 4.59 | 1.78 | 0.64 |

| Product innovation efficiency (PIP-EFFICI) | |||

| PIP-EFFICI8. Average innovation project development time | 4.29 | 1.64 | 0.58 |

| PIP-EFFICI9. Average number of working hours on innovation projects | 4.08 | 1.64 | 0.56 |

| PIP-EFFICI10. Average cost per innovation project | 4.15 | 1.69 | 0.63 |

| PIP-EFFICI11. Global degree of satisfaction with innovation project efficiency | 4.53 | 1.73 | 0.57 |

| Conditions and Outcome | Descriptive Statistics | Calibration (0.95; 0.50; 0.05) |

|---|---|---|

| Knowledge Sharing (KS) | μ = 4.26, σ = 1.45, min = 1.00, max = 7.00 | (6.2, 4.4, 1.6) |

| Adoption of environmental practices (PRAC) | μ = 5.08, σ = 1.28, min = 1.00, max = 7.00 | (6.8, 5.3, 2.6) |

| Firm type (FIRM TYPE) | Binary condition: 1=PLC; 0=GP | No need |

| Net exports (NET_EXP)(€) | μ = 6880761.39, σ = 7315699.7, min = -36678892.8, max = 30949844.5 | (19500000, 6450000, 4000000) |

| Human resources costs (HRC) | μ = 0.15, σ = 0.10, min = 0.00, max = 0.72 | (0.31, 0.13, 0.025) |

| Organizational learning capability (OLC) | Generated by the function of “fuzzy and” (stands for the mathematical logic operation in Boolean algebra “conjunction”) (E_OLC, R_OLC, I_OLC, D_OLC, P_OLC) - no descriptives available for uncalibrated values | (0.95; 0.50; 0.05) |

| Sustainable product innovation performance (PIP) | Generated by the function of “fuzzy or” (stands for the mathematical logic operation in Boolean algebra “disjunction”) (PIP_EFFICI, PIP_EFFICA) - no descriptives available for uncalibrated values | (0.95; 0.50; 0.05) |

| Paths | Estimate | SE | CR | P | Results | ||

|---|---|---|---|---|---|---|---|

| Model 1: | |||||||

| H1 (+) | PRAC ← NET EXP | 0.074 | 0.030 | 2.419 | 0.016 | Supported | |

| H2 (+) | PRAC ← HRC | 0.446 | 0.538 | 0.829 | 0.407 | Not Supported | |

| H3 (+) | PRAC ← OLC | 0.423 | 0.064 | 6.584 | *** | Supported | |

| H4 (+) | PRAC ← KS | 0.258 | 0.056 | 4.629 | *** | Supported | |

| H5 (+) | PIP ← PRAC | 0.769 | 0.096 | 8.013 | *** | Supported | |

| Model 2: Firm type (H6) Model 2A: PLC | |||||||

| H1 (+) | PRAC ← NET EXP | 0.094 | 0.046 | 2.027 | 0.043 | Supported | |

| H2 (+) | PRAC ← HRC | 0.029 | 0.742 | 0.039 | 0.969 | Not Supported | |

| H3 (+) | PRAC ← OLC | 0.410 | 0.088 | 4.682 | *** | Supported | |

| H4 (+) | PRAC ← KS | 0.284 | 0.073 | 3.916 | *** | Supported | |

| H5 (+) | PIP ← PRAC | 0.647 | 0.105 | 6.136 | *** | Supported | |

| Model 2B: GP | |||||||

| H1 (+) | PRAC ← NET EXP | 0.050 | 0.031 | 1.612 | 0.107 | Supported | |

| H2 (+) | PRAC ← HRC | 0.977 | 0.608 | 1.608 | 0.108 | Supported | |

| H3 (+) | PRAC ← OLC | 0.368 | 0.084 | 4.367 | *** | Supported | |

| H4 (+) | PRAC ← KS | 0.220 | 0.072 | 3.056 | 0.002 | Supported | |

| H5 (+) | PIP ← PRAC | 1.113 | 0.234 | 4.762 | *** | Supported | |

| X2 | Df | p-value | X2 /df | CFI | TLI | RMESA | |

| Measurement Model Summary: First Order: KS & PRAC | 281.727 | 34 | 0.000 | 8.286 | 0.905 | 0.874 | 0.042 |

| Measurement Model Summary: Second Order: OLC | 357.042 | 72 | 0.000 | 4.959 | 0.934 | 0.917 | 0.041 |

| Second Order: PIP | 262.569 | 43 | 0.000 | 6.106 | 0.903 | 0.876 | 0.040 |

| Structural Model 1 Summary | 953.304 | 575 | 0.000 | 1.658 | 0.961 | 0.955 | 0.043 |

| Structural Models 2A/2B Summary | 1769.018 | 1150 | 0.000 | 1.538 | 0.939 | 0.929 | 0.039 |

| Intermediate Solution (PIP) | |||||||||

| Model: PIP = f (FIRM TYPE, NET EXP, HRC, OLC, KS, PRAC) | |||||||||

| Configurations | FIRM TYPE | NET EXP | HRC | OLC | KS | PRAC | Coverage | Consistency | |

| Raw | Unique | ||||||||

| 1 | ● | 0.728123 | 0.351214 | 0.795770 | |||||

| 2 | ○ | ● | 0.200603 | 0.011803 | 0.896009 | ||||

| 3 | • | ● | 0.328973 | 0.019606 | 0.921915 | ||||

| 4 | ○ | ○ | ○ | 0.170574 | 0.018461 | 0.811225 | |||

| Overall solution coverage: 0.795650 | Overall solution consistency: 0.785965 | ||||||||

| IntermediateSolution(~PIP) | |||||||||

| Model:~PIP = f(FIRMTYPE,NETEXP,HRC,OLC,KS,PRAC) | |||||||||

| Configurations | FIRM TYPE | NET EXP | HRC | OLC | KS | PRAC | Coverage | Consistency | |

| Raw | Unique | ||||||||

| 1 | ○ | ● | ○ | ○ | 0.172478 | 0.023613 | 0.811683 | ||

| 2 | ○ | ● | ○ | ○ | 0.432359 | 0.283494 | 0.818233 | ||

| Overallsolutioncoverage:0.455971 | Overallsolutionconsistency:0.816442 | ||||||||

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Muñoz-Pascual, L.; Curado, C.; Galende, J. The Triple Bottom Line on Sustainable Product Innovation Performance in SMEs: A Mixed Methods Approach. Sustainability 2019, 11, 1689. https://doi.org/10.3390/su11061689

Muñoz-Pascual L, Curado C, Galende J. The Triple Bottom Line on Sustainable Product Innovation Performance in SMEs: A Mixed Methods Approach. Sustainability. 2019; 11(6):1689. https://doi.org/10.3390/su11061689

Chicago/Turabian StyleMuñoz-Pascual, Lucía, Carla Curado, and Jesús Galende. 2019. "The Triple Bottom Line on Sustainable Product Innovation Performance in SMEs: A Mixed Methods Approach" Sustainability 11, no. 6: 1689. https://doi.org/10.3390/su11061689

APA StyleMuñoz-Pascual, L., Curado, C., & Galende, J. (2019). The Triple Bottom Line on Sustainable Product Innovation Performance in SMEs: A Mixed Methods Approach. Sustainability, 11(6), 1689. https://doi.org/10.3390/su11061689