What Dimension of CSR Matters to Organizational Resilience? Evidence from China

Abstract

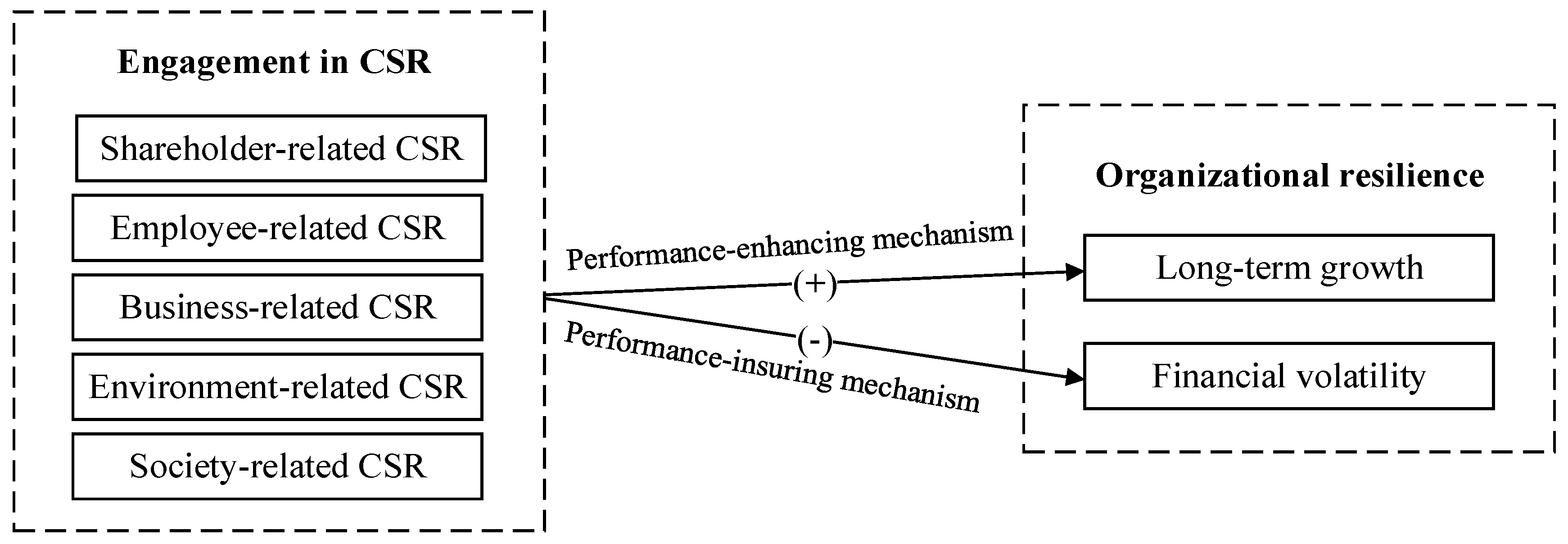

1. Introduction

2. Theory and Hypotheses

2.1. The Conceptualization and Operationalization of Organizational Resilience

2.2. CSR and Organizational Resilience

2.3. Shareholder-Related CSR and Organizational Resilience

2.4. Employee-Related CSR and Organizational Resilience

2.5. Business-Related CSR and Organizational Resilience

2.6. Environment-Related CSR and Organizational Resilience

2.7. Society-Related CSR and Organizational Resilience

3. Methodology

3.1. Data and Sample

3.2. Variables

3.3. Results

3.4. Robustness Test Analysis

4. Discussion and Conclusions

4.1. Theoretical Contributions

4.2. Managerial Implications

4.3. Limitations and Future Research

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

| First-Order | Second-Order | Third-Order |

|---|---|---|

| Shareholder (30%) | Earnings (10%) | Return on equity (2%) |

| Return on total assets (2%) | ||

| Profit margin of main business (2%) | ||

| Profit margin on cost (1%) | ||

| Earnings per share (2%) | ||

| Undistributed profit per share (1%) | ||

| Solvency (3%) | Quick ratio (0.5%) | |

| Current ratio (0.5%) | ||

| Cash ratio (0.5%) | ||

| Shareholder equity ratio (0.5%) | ||

| Asset-liability ratio (1%) | ||

| Returns (8%) | Dividend-financing ratio (2%) | |

| Dividend yield (3%) | ||

| Dividends-distributable profits ratio (3%) | ||

| Information disclosure (5%) | Number of penalties imposed by the stock exchange on the company and relevant individuals in charge (5%) | |

| Innovation (4%) | Expenditure on product development (1%) | |

| Innovative ideas of technologies (1%) | ||

| Number of technological innovation projects (2%) | ||

| Employee (15%) (10% for consumer industries) | Performance (5%) | Per capita income of employees (4%) (3%) |

| Staff training (1%) (1%) | ||

| Safety (5%) | Safety inspection (2%) (1%) | |

| Safety training (3%) (2%) | ||

| Care (5%) | Awareness of condolences (1%) (1%) | |

| Condolences to employees (2%) (1%) | ||

| Condolence payments (2%) (1%) | ||

| Business (including suppliers, customer, and consumer interests) (15%) (20% for consumer industries) | Product quality (7%) | Awareness of quality management (3%) (5%) |

| Certificate of quality management system (4%) (4%) | ||

| After-sale services (3%) | Customer satisfaction survey (3%) (4%) | |

| Integrity and reciprocity (5%) | Fair competition among suppliers (3%) (4%) | |

| Anti-bribery training (2%) (3%) | ||

| Environment (20%) (30%, 10% for manufacturing and service industries respectively) | Environmental governance (20%) | Environmental awareness (2%) (4%) (2%) |

| Certificate of environmental management system (3%) (5%) (2%) | ||

| Investment in environmental protection (5%) (7%) (2%) | ||

| Types of pollution discharge (5%) (7%) (2%) | ||

| Types of energy savings (5%) (7%) (2%) | ||

| Society (20%) (10%, 30% for manufacturing and service industries respectively) | Value contribution (20%) | Ratio of income tax to total profit (10%) (5%) (15%) |

| Charitable donations (10%) (5%) (15%) |

Appendix B

| Independent Variables | Dependent Variable: Long-term Growth | Dependent Variable: Financial Volatility | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | Model 7 | Model 8 | Model 9 | Model 10 | Model 11 | Model 12 | |

| Total CSR | 0.00894 ** | −0.000296 *** | ||||||||||

| (0.00423) | (0.000454) | |||||||||||

| Shareholder | −0.0195 | −0.000708 *** | ||||||||||

| (0.0137) | (0.000147) | |||||||||||

| Employee | 0.0539 ** | −0.000927 *** | ||||||||||

| (0.0227) | (0.000243) | |||||||||||

| Business | 0.0285 ** | −0.000846 *** | ||||||||||

| (0.0138) | (0.000149) | |||||||||||

| Environment | 0.0466 *** | −0.000676 *** | ||||||||||

| (0.0123) | (0.000135) | |||||||||||

| Society | 0.00938 | −0.000559 *** | ||||||||||

| (0.0150) | (0.000168) | |||||||||||

| S&A | −1.267 | −1.359 | −1.390 | −1.312 | −1.325 | −1.267 | −0.0461 *** | −0.0478 *** | −0.0435 *** | −0.0445 *** | −0.0444 *** | −0.0465 *** |

| (1.123) | (1.125) | (1.124) | (1.124) | (1.123) | (1.124) | (0.0132) | (0.0132) | (0.0132) | (0.0132) | (0.0132) | (0.0132) | |

| HHI | 2.703 | 2.577 | 2.624 | 2.619 | 2.402 | 2.753 | −0.264 *** | −0.271 *** | −0.266 *** | −0.263 *** | −0.262 *** | −0.268 *** |

| (4.591) | (4.593) | (4.591) | (4.591) | (4.589) | (4.592) | (0.0496) | (0.0496) | (0.0497) | (0.0496) | (0.0496) | (0.0497) | |

| SOE | 0.110 | 0.109 | 0.108 | 0.104 | 0.0937 | 0.116 | −0.0116 *** | −0.0120 *** | −0.0116 *** | −0.0114 *** | −0.0114 *** | −0.0117 *** |

| (0.289) | (0.289) | (0.289) | (0.289) | (0.289) | (0.289) | (0.00331) | (0.00332) | (0.00332) | (0.00332) | (0.00332) | (0.00332) | |

| MB | 2.902 *** | 2.513 *** | 2.786 *** | 2.786 *** | 2.845 *** | 2.755 *** | 0.0369 *** | 0.0343 *** | 0.0413 *** | 0.0407 *** | 0.0407 *** | 0.0404 *** |

| (0.637) | (0.650) | (0.632) | (0.632) | (0.632) | (0.633) | (0.00650) | (0.00665) | (0.00647) | (0.00646) | (0.00647) | (0.00648) | |

| LEV | −1.874 *** | −1.845 *** | −1.877 *** | −1.876 *** | −1.898 *** | −1.850 *** | −0.0315 *** | −0.0322 *** | −0.0320 *** | −0.0316 *** | −0.0317 *** | −0.0321 *** |

| (0.121) | (0.120) | (0.121) | (0.121) | (0.121) | (0.120) | (0.00132) | (0.00131) | (0.00132) | (0.00132) | (0.00132) | (0.00132) | |

| ACF | 0.130 | 0.172 | 0.141 | 0.147 | 0.145 | 0.142 | 0.000173 | 0.000748 | −0.000338 | −0.000458 | −0.000383 | −0.000274 |

| (0.185) | (0.186) | (0.185) | (0.185) | (0.185) | (0.185) | (0.00210) | (0.00211) | (0.00210) | (0.00210) | (0.00210) | (0.00210) | |

| YFE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| FFE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | 2.952 *** | 3.628 *** | 3.085 *** | 3.183 *** | 3.127 *** | 3.195 *** | 0.106 *** | 0.109 *** | 0.0989 *** | 0.0979 *** | 0.0977 *** | 0.0995 *** |

| (0.385) | (0.444) | (0.364) | (0.359) | (0.358) | (0.369) | (0.00399) | (0.00462) | (0.00379) | (0.00374) | (0.00374) | (0.00386) | |

| N | 9936 | 9936 | 9936 | 9936 | 9936 | 9936 | 12,214 | 12,214 | 12,214 | 12,214 | 12,214 | 12,214 |

| No. of firms | 2328 | 2328 | 2328 | 2328 | 2328 | 2328 | 2444 | 2444 | 2444 | 2444 | 2444 | 2444 |

| Adj. R2 | 0.266 | 0.266 | 0.266 | 0.266 | 0.264 | 0.266 | 0.169 | 0.171 | 0.172 | 0.170 | 0.171 | 0.172 |

References

- Hamel, G.; Valikangas, L. The quest for resilience. Harv. Bus. Rev. 2003, 81, 52–63. [Google Scholar] [PubMed]

- Teixeira, E.D.; Werther, W.B. Resilience: Continuous renewal of competitive advantages. Bus. Horiz. 2013, 56, 333–342. [Google Scholar] [CrossRef]

- Gao, C.; Zuzul, T.; Jones, G.; Khanna, T. Overcoming institutional voids: A reputation-based view of long-run survival. Strateg. Manag. J. 2017, 38, 2147–2167. [Google Scholar] [CrossRef]

- Pal, R.; Torstensson, H.; Mattila, H. Antecedents of organizational resilience in economic crises-an empirical study of swedish textile and clothing SMEs. Int. J. Prod. Econ. 2014, 147, 410–428. [Google Scholar] [CrossRef]

- Cho, S.; Mathiassen, L.; Robey, D. Dialectics of resilience: A multi-level analysis of a telehealth innovation. J. Inf. Technol. 2007, 22, 24–35. [Google Scholar] [CrossRef]

- Ortiz-de-Mandojana, N.; Bansal, P. The long-term benefits of organizational resilience through sustainable business practices. Strateg. Manag. J. 2016, 37, 1615–1631. [Google Scholar] [CrossRef]

- Markman, G.M.; Venzin, M. Resilience: Lessons from banks that have braved the economic crisis-and from those that have not. Int. Bus. Rev. 2014, 23, 1096–1107. [Google Scholar] [CrossRef]

- Reinmoeller, P.; van Baardwijk, N. The link between diversity and resilience. MIT Sloan Manag. Rev. 2005, 46, 61–65. [Google Scholar]

- Pal, R. Organizational resilience and health of business systems. Int. J. Bus. Contin. Risk Manag. 2011, 2, 372–398. [Google Scholar] [CrossRef]

- Blanco, J.M.M.; Montes-Botella, J.L. Exploring nurtured company resilience through human capital and human resource development findings from spanish manufacturing companies. Int. J. Manpow. 2017, 38, 661–674. [Google Scholar] [CrossRef]

- Bode, C.; Singh, J.; Rogan, M. Corporate social initiatives and employee retention. Organ. Sci. 2015, 26, 1702–1720. [Google Scholar] [CrossRef]

- Wei, Y.C.; Egri, C.P.; Lin, C.Y.Y. Do corporate social responsibility practices yield different business benefits in eastern and western contexts? Chin. Manag. Stud. 2014, 8, 556–576. [Google Scholar] [CrossRef]

- Wisse, B.; van Eijbergen, R.; Rietzschel, E.F.; Scheibe, S. Catering to the needs of an aging workforce: The role of employee age in the relationship between corporate social responsibility and employee satisfaction. J. Bus. Ethics 2018, 147, 875–888. [Google Scholar] [CrossRef]

- Barakat, S.R.; Isabella, G.; Boaventura, J.M.G.; Mazzon, J.A. The influence of corporate social responsibility on employee satisfaction. Manag. Decis. 2016, 54, 2325–2339. [Google Scholar] [CrossRef]

- Abdelmotaleb, M.; Metwally, A.; Saha, S.K. Exploring the impact of being perceived as a socially responsible organization on employee creativity. Manag. Decis. 2018, 56, 2325–2340. [Google Scholar] [CrossRef]

- Bocquet, R.; Le Bas, C.; Mothe, C.; Poussing, N. CSR, innovation, and firm performance in sluggish growth contexts: A firm-level empirical analysis. J. Bus. Ethics 2017, 146, 241–254. [Google Scholar] [CrossRef]

- Chang, C.H. Proactive and reactive corporate social responsibility: Antecedent and consequence. Manag. Decis. 2015, 53, 451–468. [Google Scholar] [CrossRef]

- Singh, J. The influence of csr and ethical self-identity in consumer evaluation of cobrands. J. Bus. Ethics 2016, 138, 311–326. [Google Scholar] [CrossRef]

- Zou, P.; Li, G.F. How emerging market investors’ value competitors’ customer equity: Brand crisis spillover in China. J. Bus. Res. 2016, 69, 3765–3771. [Google Scholar] [CrossRef]

- Wang, D.H.M.; Chen, P.H.; Yu, T.H.K.; Hsiao, C.Y. The effects of corporate social responsibility on brand equity and firm performance. J. Bus. Res. 2015, 68, 2232–2236. [Google Scholar] [CrossRef]

- Benlemlih, M.; Bitar, M. Corporate social responsibility and investment efficiency. J. Bus. Ethics 2018, 148, 647–671. [Google Scholar] [CrossRef]

- Shiu, Y.M.; Yang, S.L. Does engagement in corporate social responsibility provide strategic insurance-like effects? Strateg. Manag. J. 2017, 38, 455–470. [Google Scholar] [CrossRef]

- Godfrey, P.C.; Merrill, C.B.; Hansen, J.M. The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management hypothesis. Strateg. Manag. J. 2009, 30, 425–445. [Google Scholar] [CrossRef]

- Freeman, R. Strategic Management: A Stakeholder Perspective; HarperCollins College Div: New York, NY, USA, 1984. [Google Scholar]

- Mattingly, J.E.; Berman, S.L. Measurement of corporate social action: Discovering taxonomy in the kinder lydenburg domini ratings data. Bus. Soc. 2006, 45, 20–46. [Google Scholar] [CrossRef]

- Su, W.C.; Tsang, E.W.K. Product diversification and financial performance: The moderating role of secondary stakeholders. Acad. Manag. J. 2015, 58, 1128–1148. [Google Scholar] [CrossRef]

- Freeman, R.; Harrison, J.; Wicks, A.; Parmar, B.; De Colle, S. Stakeholder Theory: The State of the Art; Cambridge University Press: Cambridge, UK, 2010. [Google Scholar]

- Eesley, C.; Lenox, M.J. Firm responses to secondary stakeholder action. Strateg. Manag. J. 2006, 27, 765–781. [Google Scholar] [CrossRef]

- Hawn, O.; Ioannou, I. Mind the gap: The interplay between external and internal actions in the case of corporate social responsibility. Strateg. Manag. J. 2016, 37, 2569–2588. [Google Scholar] [CrossRef]

- Folke, C. Resilience: The emergence of a perspective for social-ecological systems analyses. Glob. Environ. Chang. 2006, 16, 253–267. [Google Scholar] [CrossRef]

- Holling, C.S. Resilience and stability of ecological systems. Annu. Rev. Ecol. Syst. 1973, 4, 1–23. [Google Scholar] [CrossRef]

- Walker, B.; Holling, C.S.; Carpenter, S.R.; Kinzig, A.P. Resilience, adaptability and transformability in social-ecological systems. Ecol. Soc. 2004, 9, 3438–3447. [Google Scholar] [CrossRef]

- Weick, K.; Sutcliffe, K. Managing the Unexpected: Resilient Performance in an Age of Uncertainty; John Wiley & Sons: Hoboken, NJ, USA, 2001. [Google Scholar]

- Sheffi, Y.; Rice, J.B. A supply chain view of the resilient enterprise. MIT Sloan Manag. Rev. 2005, 47, 41–48. [Google Scholar]

- Gittell, J.H. Relationships and resilience care provider responses to pressures from managed care. J. Appl. Behav. Sci. 2008, 44, 25–47. [Google Scholar] [CrossRef]

- Van der Vegt, G.S.; Essens, P.; Wahlstrom, M.; George, G. Managing risk and resilience. Acad. Manag. J. 2015, 58, 971–980. [Google Scholar] [CrossRef]

- Fiksel, J.; Polyviou, M.; Croxton, K.L.; Pettit, T.J. From risk to resilience: Learning to deal with disruption. MIT Sloan Manag. Rev. 2015, 56, 79–86. [Google Scholar]

- Luthans, F. The need for and meaning of positive organizational behavior. J. Organ. Behav. 2002, 23, 695–706. [Google Scholar] [CrossRef]

- Coutu, D.L. How resilience works. Harv. Bus. Rev. 2002, 80, 46–54. [Google Scholar]

- Acquaah, M.; Amoako-Gyampah, K.; Jayaram, J. Resilience in family and nonfamily firms: An examination of the relationships between manufacturing strategy, competitive strategy and firm performance. Int. J. Prod. Res. 2011, 49, 5527–5544. [Google Scholar] [CrossRef]

- Reeves, M.; Levin, S.; Ueda, D. The biology of corporate survival. Harv. Bus. Rev. 2016, 94, 47–55. [Google Scholar]

- Sutcliffe, K.M.; Vogus, T.J. Organizing for resilience. In Positive Organizational Scholarship: Foundations of a New Discipline, 1st ed.; Cameron, K.S., Dutton, J.E., Quinn, R.E., Eds.; Berrett-Koehler Publishers: Oakland, CA, USA, 2003; pp. 94–110. [Google Scholar]

- Smallbone, D.; Deakins, D.; Battisti, M.; Kitching, J. Small business responses to a major economic downturn: Empirical perspectives from new zealand and the United Kingdom. Int. Small Bus. J. 2012, 30, 754–777. [Google Scholar] [CrossRef]

- Lampel, J.; Bhalla, A.; Jha, P.P. Does governance confer organisational resilience? Evidence from UK employee owned businesses. Eur. Manag. J. 2014, 32, 66–72. [Google Scholar]

- Mackey, A.; Mackey, T.B.; Barney, J.B. Corporate social responsibility and firm performance: Investor preferences and corporate strategies. Acad. Manag. Rev. 2007, 32, 817–835. [Google Scholar] [CrossRef]

- Ortas, E.; Moneva, J.M.; Burritt, R.; Tingey-Holyoak, J. Does sustainability investment provide adaptive resilience to ethical investors? Evidence from Spain. J. Bus. Ethics 2014, 124, 297–309. [Google Scholar] [CrossRef]

- Lengnick-Hall, C.A.; Beck, T.E. Adaptive fit versus robust transformation: How organizations respond to environmental change. J. Manag. 2005, 31, 738–757. [Google Scholar] [CrossRef]

- Gunasekaran, A.; Rai, B.K.; Griffin, M. Resilience and competitiveness of small and medium size enterprises: An empirical research. Int. J. Prod. Res. 2011, 49, 5489–5509. [Google Scholar] [CrossRef]

- Chan, M.C.; Watson, J.; Woodliff, D. Corporate governance quality and CSR disclosures. J. Bus. Ethics 2014, 125, 59–73. [Google Scholar] [CrossRef]

- Cui, J.; Jo, H.; Na, H. Does corporate social responsibility affect information asymmetry? J. Bus. Ethics 2018, 148, 549–572. [Google Scholar] [CrossRef]

- Cheung, Y.L.; Tan, W.Q.; Wang, W.M. National stakeholder orientation, corporate social responsibility, and bank loan cost. J. Bus. Ethics 2018, 150, 505–524. [Google Scholar] [CrossRef]

- Cheng, B.T.; Ioannou, I.; Serafeim, G. Corporate social responsibility and access to finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Attig, N.; Cleary, S.W.; El Ghoul, S.; Guedhami, O. Corporate legitimacy and investment-cash flow sensitivity. J. Bus. Ethics 2014, 121, 297–314. [Google Scholar]

- Werner, T. Gaining access by doing good: The effect of sociopolitical reputation on firm participation in public policy making. Manag. Sci. 2015, 61, 1989–2011. [Google Scholar] [CrossRef]

- McDonnell, M.-H.; King, B. Keeping up appearances: Reputational threat and impression management after social movement boycotts. Adm. Sci. Q. 2013, 58, 387–419. [Google Scholar] [CrossRef]

- Zavyalova, A.; Pfarrer, M.D.; Reger, R.K.; Hubbard, T.D. Reputation as a benefit and a burden? How stakeholders’ organizational identification affects the role of reputation following a negative event. Acad. Manag. J. 2016, 59, 253–276. [Google Scholar] [CrossRef]

- Bromiley, P. Testing a causal model of corporate risk taking and performance. Acad. Manag. J. 1991, 34, 37–59. [Google Scholar]

- Nickel, M.N.; Rodriguez, M.C. A review of research on the negative accounting relationship between risk and return: Bowman’s paradox. Omega 2002, 30, 1–18. [Google Scholar] [CrossRef]

- Shi, G.F.; Sun, J.F. Corporate bond covenants and social responsibility investment. J. Bus. Ethics 2015, 131, 285–303. [Google Scholar] [CrossRef]

- Wang, X.; Cao, F.; Ye, K.T. Mandatory corporate social responsibility (CSR) reporting and financial reporting quality: Evidence from a quasi-natural experiment. J. Bus. Ethics 2018, 152, 253–274. [Google Scholar] [CrossRef]

- Peric, M.; Vitezic, V. Impact of global economic crisis on firm growth. Small Bus. Econ. 2016, 46, 1–12. [Google Scholar] [CrossRef]

- Tognazzo, A.; Gubitta, P.; Favaron, S.D. Does slack always affect resilience? A study of quasi-medium-sized italian firms. Entrep. Reg. Dev. 2016, 28, 768–790. [Google Scholar] [CrossRef]

- Kachaner, N.; Stalk, G.; Bloch, A. What you can learn from family business. Harv. Bus. Rev. 2012, 90, 102–106. [Google Scholar]

- Govindarajan, V.; Srivastava, A. The scary truth about corporate survival. Harv. Bus. Rev. 2016, 94, 24–25. [Google Scholar]

- Wastell, D.G.; McMaster, T.; Kawalek, P. The rise of the phoenix: Methodological innovation as a discourse of renewal. J. Inf. Technol. 2007, 22, 59–68. [Google Scholar] [CrossRef]

- Ates, A.; Bititci, U. Change process: A key enabler for building resilient SMEs. Int. J. Prod. Res. 2011, 49, 5601–5618. [Google Scholar] [CrossRef]

- Jaaron, A.A.M.; Backhouse, C.J. Service organisations resilience through the application of the vanguard method of systems thinking: A case study approach. Int. J. Prod. Res. 2014, 52, 2026–2041. [Google Scholar] [CrossRef]

- Sabatino, M. Economic crisis and resilience: Resilient capacity and competitiveness of the enterprises. J. Bus. Res. 2016, 69, 1924–1927. [Google Scholar] [CrossRef]

- Shen, J.; Benson, J. When CSR is a social norm: How socially responsible human resource management affects employee work behavior. J. Manag. 2016, 42, 1723–1746. [Google Scholar] [CrossRef]

- Demmer, W.A.; Vickery, S.K.; Calantone, R. Engendering resilience in small- and medium-sized enterprises (SMEs): A case study of demmer corporation. Int. J. Prod. Res. 2011, 49, 5395–5413. [Google Scholar] [CrossRef]

- Lengnick-Hall, C.A.; Beck, T.E.; Lengnick-Hall, M.L. Developing a capacity for organizational resilience through strategic human resource management. Hum. Resour. Manag. Rev. 2011, 21, 243–255. [Google Scholar] [CrossRef]

- Yacob, S. Trans-generational renewal as managerial succession: The behn meyer story (1840–2000). Bus. Hist. 2012, 54, 1166–1185. [Google Scholar] [CrossRef]

- Shan, L.; Fu, S.; Zheng, L. Corporate sexual equality and firm performance. Strateg. Manag. J. 2017, 38, 1812–1826. [Google Scholar] [CrossRef]

- Stoian, C.; Gilman, M. Corporate social responsibility that “pays”: A strategic approach to CSR for smes. J. Small Bus. Manag. 2017, 55, 5–31. [Google Scholar] [CrossRef]

- Gittell, J.H.; Cameron, K.; Lim, S.; Rivas, V. Relationships, layoffs, and organizational resilience airline industry responses to September 11. J. Appl. Behav. Sci. 2006, 42, 300–329. [Google Scholar] [CrossRef]

- Van Essen, M.; Strike, V.M.; Carney, M.; Sapp, S. The resilient family firm: Stakeholder outcomes and institutional effects. Corp. Gov. Int. Rev. 2015, 23, 167–183. [Google Scholar] [CrossRef]

- Moore, J.F. The Death of Competition: Leadership and Strategy in the Age of Business Ecosystems; HarperBusiness: New York, NY, USA, 1996. [Google Scholar]

- Erol, O.; Sauser, B.J.; Mansouri, M. A framework for investigation into extended enterprise resilience. Enterp. Inf. Syst. 2010, 4, 111–136. [Google Scholar] [CrossRef]

- Marwa, S.; Zairi, M. An exploratory study of the reasons for the collapse of contemporary companies and their link with the concept of quality. Manag. Decis. 2008, 46, 1342–1370. [Google Scholar] [CrossRef]

- Zhang, M.; Jin, B.Y.; Wang, G.A.; Goh, T.N.; He, Z. A study of key success factors of service enterprises in china. J. Bus. Ethics 2016, 134, 1–14. [Google Scholar] [CrossRef]

- Day, G.S. Closing the marketing capabilities gap. J. Mark. 2011, 75, 183–195. [Google Scholar] [CrossRef]

- Leguizamon, F.; Selva, G.; Santos, M. Small farmer suppliers from local to global. J. Bus. Res. 2016, 69, 4520–4525. [Google Scholar] [CrossRef]

- Asgary, N.; Li, G. Corporate social responsibility: Its economic impact and link to the bullwhip effect. J. Bus. Ethics 2016, 135, 665–681. [Google Scholar] [CrossRef]

- Winston, A. Resilience in a hotter world. Harv. Bus. Rev. 2014, 92, 56–64. [Google Scholar]

- Zhang, M.; Ma, L.J.; Su, J.; Zhang, W. Do suppliers applaud corporate social performance? J. Bus. Ethics 2014, 121, 543–557. [Google Scholar] [CrossRef]

- Sharfman, M.P.; Fernando, C.S. Environmental risk management and the cost of capital. Strateg. Manag. J. 2008, 29, 569–592. [Google Scholar] [CrossRef]

- Cordeiro, J.J.; Tewari, M. Firm characteristics, industry context, and investor reactions to environmental CSR: A stakeholder theory approach. J. Bus. Ethics 2015, 130, 833–849. [Google Scholar] [CrossRef]

- Russo, M.V.; Harrison, N.S. Organizational design and environmental performance: Clues from the electronics industry. Acad. Manag. J. 2005, 48, 582–593. [Google Scholar] [CrossRef]

- Cho, S.Y.; Lee, C.; Pfeiffer, R.J. Corporate social responsibility performance and information asymmetry. J. Account. Public Policy 2013, 32, 71–83. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Verbeeten, F.H.M.; Gamerschlag, R.; Moller, K. Are CSR disclosures relevant for investors? Empirical evidence from Germany. Manag. Decis. 2016, 54, 1359–1382. [Google Scholar] [CrossRef]

- Gautier, A.; Pache, A.C. Research on corporate philanthropy: A review and assessment. J. Bus. Ethics 2015, 126, 343–369. [Google Scholar] [CrossRef]

- File, K.M.; Prince, R.A. Cause related marketing and corporate philanthropy in the privately held enterprise. J. Bus. Ethics 1998, 17, 1529–1539. [Google Scholar] [CrossRef]

- Zhao, M. CSR-based political legitimacy strategy: Managing the state by doing good in China and Russia. J. Bus. Ethics 2012, 111, 439–460. [Google Scholar] [CrossRef]

- Xavier, W.G.; Bandeira-de-Mello, R.; Marcon, R. Institutional environment and business groups’ resilience in Brazil. J. Bus. Res. 2014, 67, 900–907. [Google Scholar] [CrossRef]

- Su, W.; Peng, M.W.; Tan, W.Q.; Cheung, Y.L. The signaling effect of corporate social responsibility in emerging economies. J. Bus. Ethics 2016, 134, 479–491. [Google Scholar] [CrossRef]

- Wang, H.L.; Qian, C.L. Corporate philanthropy and corporate financial performance: The roles of stakeholder response and political access. Acad. Manag. J. 2011, 54, 1159–1181. [Google Scholar] [CrossRef]

- Godfrey, P.C. The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. Acad. Manag. Rev. 2005, 30, 777–798. [Google Scholar] [CrossRef]

- Thomas, A.; Byard, P.; Francis, M.; Fisher, R.; White, G.R.T. Profiling the resiliency and sustainability of UK manufacturing companies. J. Manuf. Technol. Manag. 2016, 27, 82–99. [Google Scholar] [CrossRef]

- Schwert, G.W. Stock market volatility. Financ. Anal. J. 1990, 46, 23–34. [Google Scholar] [CrossRef]

- Hu, Y.; Chen, S.; Shao, Y.; Gao, S. CSR and firm value: Evidence from China. Sustainability 2018, 10, 4597. [Google Scholar] [CrossRef]

- Song, M.-L.; Fisher, R.; Wang, J.-L.; Cui, L.-B. Environmental performance evaluation with big data: Theories and methods. Ann. Oper. Res. 2018, 270, 459–472. [Google Scholar] [CrossRef]

- Feltham, G.A.; Ohlson, J.A. Valuation and clean surplus accounting for operating and financial activities. Contemp. Account. Res. 1995, 11, 689–731. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. Value versus growth: The international evidence. J. Financ. 1998, 53, 1975–1999. [Google Scholar] [CrossRef]

- Ahmed, M.U.; Kristal, M.M.; Pagell, M. Impact of operational and marketing capabilities on firm performance: Evidence from economic growth and downturns. Int. J. Prod. Econ. 2014, 154, 59–71. [Google Scholar] [CrossRef]

- Andersen, T.J. Multinational risk and performance outcomes: Effects of knowledge intensity and industry context. Int. Bus. Rev. 2012, 21, 239–252. [Google Scholar] [CrossRef]

- Chen, C.J.; Guo, R.S.; Hsiao, Y.C.; Chen, K.L. How business strategy in non-financial firms moderates the curvilinear effects of corporate social responsibility and irresponsibility on corporate financial performance. J. Bus. Res. 2018, 92, 154–167. [Google Scholar] [CrossRef]

- Chen, R.C.Y.; Lee, C.H. Assessing whether corporate social responsibility influence corporate valuee. Appl. Econ. 2017, 49, 5547–5557. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate social responsibility and financial performance: Correlation or misspecification? Strateg. Manag. J. 2000, 21, 603–609. [Google Scholar] [CrossRef]

- Ahn, S.Y.; Park, D.J. Corporate social responsibility and corporate longevity: The mediating role of social capital and moral legitimacy in Korea. J. Bus. Ethics 2018, 150, 117–134. [Google Scholar] [CrossRef]

- Peloza, J. Using corporate social responsibility as insurance for financial performance. Calif. Manag. Rev. 2006, 48, 52–72. [Google Scholar] [CrossRef]

- Vidaver-Cohen, D.; Bronn, P.S. Reputation, responsibility, and stakeholder support in scandinavian firms: A comparative analysis. J. Bus. Ethics 2015, 127, 49–64. [Google Scholar] [CrossRef]

| Variable | Measurement |

|---|---|

| Dependent variables | |

| Growth | The accumulation of net sales growth in three years (Unit: billion). |

| Volatility | The standard deviations of monthly stock returns in each year. |

| Independent variables | |

| Total CSR | The comprehensive score of Hexun CSR index. |

| Shareholder | The shareholder score of Hexun CSR index. |

| Employee | The employee score of Hexun CSR index. |

| Business | The supplier, client and consumer score of Hexun CSR index. |

| Environment | The environment score of Hexun CSR index. |

| Society | The society score of Hexun CSR index. |

| Control variables | |

| MB | The ratio of book value of equity to the market value of equity. |

| HHI | Industry concentration measured by the Herfindahl–Hirschman Index. |

| S&A | Selling and administrative divided by the total assets at the end of fiscal year. |

| LEV | The ratio of total debt to the total assets at the end of fiscal year. |

| ACF | The ratio of cash flow to the total assets at the end of fiscal year. |

| SOE | SOE = 1 if the firm is a state-owned enterprise (SOE); SOE = 0 otherwise. |

| Variables | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Growth | 1 | |||||||||||||

| 2. Volatility | −0.00800 | 1 | ||||||||||||

| 3. CSR score | 0.206 *** | −0.141 *** | 1 | |||||||||||

| 4. Shareholder | 0.110 *** | −0.098 *** | 0.582 *** | 1 | ||||||||||

| 5. Employee | 0.197 *** | −0.094 *** | 0.839 *** | 0.242 *** | 1 | |||||||||

| 6. Business | 0.167 *** | −0.117 *** | 0.876 *** | 0.248 *** | 0.826 *** | 1 | ||||||||

| 7. Environment | 0.180 *** | −0.114 *** | 0.841 *** | 0.210 *** | 0.865 *** | 0.866 *** | 1 | |||||||

| 8. Society | 0.099 *** | −0.078 *** | 0.485 *** | 0.278 *** | 0.183 *** | 0.255 *** | 0.114 *** | 1 | ||||||

| 9. S&A | −0.020 ** | −0.00100 | −0.0140 | 0.080 *** | −0.076 *** | −0.0130 | −0.060 *** | −0.00800 | 1 | |||||

| 10. HHI | −0.023 ** | −0.00300 | −0.024 *** | −0.055 *** | −0.00700 | −0.00700 | 0.00300 | −0.0130 | −0.025 *** | 1 | ||||

| 11. SOE | 0.084 *** | −0.051 *** | 0.103 *** | −0.053 *** | 0.155 *** | 0.138 *** | 0.144 *** | 0.0130 | −0.060 *** | 0.023 ** | 1 | |||

| 12. MB | 0.216 *** | −0.204 *** | 0.175 *** | −0.079 *** | 0.225 *** | 0.171 *** | 0.198 *** | 0.172 *** | −0.276 *** | −0.037 *** | 0.140 *** | 1 | ||

| 13. LEV | 0.202 *** | −0.035 *** | −0.00500 | −0.331 *** | 0.127 *** | 0.082 *** | 0.095 *** | 0.095 *** | −0.157 *** | 0.0110 | 0.166 *** | 0.562 *** | 1 | |

| 14. ACF | −0.047 *** | −0.023 ** | 0.132 *** | 0.341 *** | 0.0120 | 0.035 *** | 0.023 ** | 0.00500 | 0.109 *** | 0.027 *** | −0.036 *** | −0.190 *** | −0.405 *** | 1 |

| Mean | 2.03 | 0.15 | 27.69 | 13.78 | 3.36 | 2.67 | 2.83 | 5.06 | 0.09 | 0.03 | 0.19 | 0.93 | 0.45 | 0.2 |

| Median | 0.43 | 0.12 | 22.52 | 14.29 | 1.91 | 0 | 0 | 4.5 | 0.07 | 0.02 | 0 | 0.63 | 0.45 | 0.12 |

| Std. Dev | 6.31 | 0.1 | 19.09 | 6.21 | 3.69 | 5.58 | 6.18 | 4.74 | 0.08 | 0.07 | 0.4 | 0.88 | 0.22 | 0.4 |

| Minimum | −9.10 | 0.02 | −16.99 | −11.69 | −0.17 | 0 | 0 | −15 | 0 | 0 | 0 | 0.08 | 0.05 | −0.65 |

| Maximum | 42.81 | 4.66 | 90.87 | 28.19 | 15 | 20 | 30 | 30 | 2.92 | 1 | 1 | 4.68 | 1.02 | 2.11 |

| Independent Variables | Dependent Variable: Long-Term Growth | Dependent Variable: Financial Volatility | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | Model 7 | Model 8 | Model 9 | Model 10 | Model 11 | Model 12 | |

| Total CSR | 0.0235 *** | −0.000537 *** | ||||||||||

| (0.00339) | (7.39 × 10−5) | |||||||||||

| Shareholder | 0.0169 | −0.00176 *** | ||||||||||

| (0.0110) | (0.000239) | |||||||||||

| Employee | 0.123 *** | −0.00138 *** | ||||||||||

| (0.0182) | (0.000397) | |||||||||||

| Business | 0.0644 *** | −0.00135 *** | ||||||||||

| (0.0112) | (0.000243) | |||||||||||

| Environment | 0.0836 *** | −0.00102 *** | ||||||||||

| (0.0101) | (0.000220) | |||||||||||

| Society | 0.141 | −0.00110 *** | ||||||||||

| (0.0857) | (0.000273) | |||||||||||

| S&A | −1.800 * | −1.822 * | −2.081 ** | −1.931 * | −1.959 ** | −2.587 | −0.0548 ** | −0.0599 *** | −0.0506 ** | −0.0519 ** | −0.0519 ** | −0.0558 *** |

| (0.986) | (0.989) | (0.986) | (0.987) | (0.985) | (6.759) | (0.0215) | (0.0215) | (0.0215) | (0.0215) | (0.0215) | (0.0215) | |

| HHI | 0.304 | 0.733 | 0.349 | 0.266 | −0.118 | −32.94 | −0.601 *** | −0.616 *** | −0.606 *** | −0.601 *** | −0.600 *** | −0.609 *** |

| (3.708) | (3.717) | (3.709) | (3.712) | (3.705) | (25.40) | (0.0808) | (0.0807) | (0.0809) | (0.0809) | (0.0809) | (0.0809) | |

| SOE | 0.0733 | 0.0886 | 0.0681 | 0.0597 | 0.0490 | −0.327 | −0.0174 *** | −0.0184 *** | −0.0174 *** | −0.0171 *** | −0.0172 *** | −0.0176 *** |

| (0.248) | (0.248) | (0.248) | (0.248) | (0.247) | (1.696) | (0.00539) | (0.00539) | (0.00540) | (0.00540) | (0.00540) | (0.00540) | |

| MB | 3.045 *** | 2.834 *** | 2.719 *** | 2.738 *** | 2.799 *** | 2.745 | 0.0909 *** | 0.0813 *** | 0.0991 *** | 0.0981 *** | 0.0980 *** | 0.0970 *** |

| (0.486) | (0.498) | (0.483) | (0.484) | (0.483) | (3.316) | (0.0106) | (0.0108) | (0.0105) | (0.0105) | (0.0105) | (0.0106) | |

| LEV | −1.638 *** | −1.571 *** | −1.623 *** | −1.626 *** | −1.646 *** | −3.238 *** | −0.0599 *** | −0.0611 *** | −0.0609 *** | −0.0603 *** | −0.0606 *** | −0.0610 *** |

| (0.0987) | (0.0984) | (0.0985) | (0.0988) | (0.0985) | (0.673) | (0.00215) | (0.00214) | (0.00215) | (0.00215) | (0.00215) | (0.00214) | |

| ACF | −0.0669 | −0.0466 | −0.0302 | −0.0173 | −0.0245 | 0.713 | 0.000700 | 0.00250 | −0.000271 | −0.000432 | −0.000329 | −0.000107 |

| (0.157) | (0.158) | (0.157) | (0.157) | (0.157) | (1.074) | (0.00342) | (0.00344) | (0.00342) | (0.00342) | (0.00342) | (0.00342) | |

| YFE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| FFE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Constant | 1.684 *** | 2.115 *** | 2.071 *** | 2.295 *** | 2.241 *** | 4.905 ** | 0.203 *** | 0.219 *** | 0.190 *** | 0.189 *** | 0.188 *** | 0.193 *** |

| (0.298) | (0.346) | (0.283) | (0.280) | (0.279) | (1.974) | (0.00650) | (0.00751) | (0.00618) | (0.00609) | (0.00609) | (0.00629) | |

| N | 12,215 | 12,215 | 12,215 | 12,215 | 12,215 | 12,215 | 12,215 | 12,215 | 12,215 | 12,215 | 12,215 | 12,215 |

| No. of firms | 2444 | 2444 | 2444 | 2444 | 2444 | 2444 | 2444 | 2444 | 2444 | 2444 | 2444 | 2444 |

| Adj. R2 | 0.212 | 0.218 | 0.213 | 0.214 | 0.210 | 0.247 | 0.140 | 0.140 | 0.144 | 0.142 | 0.143 | 0.144 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lv, W.; Wei, Y.; Li, X.; Lin, L. What Dimension of CSR Matters to Organizational Resilience? Evidence from China. Sustainability 2019, 11, 1561. https://doi.org/10.3390/su11061561

Lv W, Wei Y, Li X, Lin L. What Dimension of CSR Matters to Organizational Resilience? Evidence from China. Sustainability. 2019; 11(6):1561. https://doi.org/10.3390/su11061561

Chicago/Turabian StyleLv, Wendong, Yuan Wei, Xiaoyun Li, and Lin Lin. 2019. "What Dimension of CSR Matters to Organizational Resilience? Evidence from China" Sustainability 11, no. 6: 1561. https://doi.org/10.3390/su11061561

APA StyleLv, W., Wei, Y., Li, X., & Lin, L. (2019). What Dimension of CSR Matters to Organizational Resilience? Evidence from China. Sustainability, 11(6), 1561. https://doi.org/10.3390/su11061561