A Hybrid Multi-Criteria Decision-Making Model for Evaluating Companies’ Green Credit Rating

Abstract

1. Introduction

2. Literature Review

2.1. Previous Studies on the Company’s Credit Evaluation

2.2. The Application of Hybrid MCDM Methods

3. Methodology

3.1. Sample Selection

3.2. The Evaluation Criteria for Green Credit Policy

3.2.1. Credit Risk Evaluation Criteria

3.2.2. Economic Performance Indicators

3.2.3. Social Performance Indicators

3.2.4. Environmental Performance Indicators

3.3. Data Source

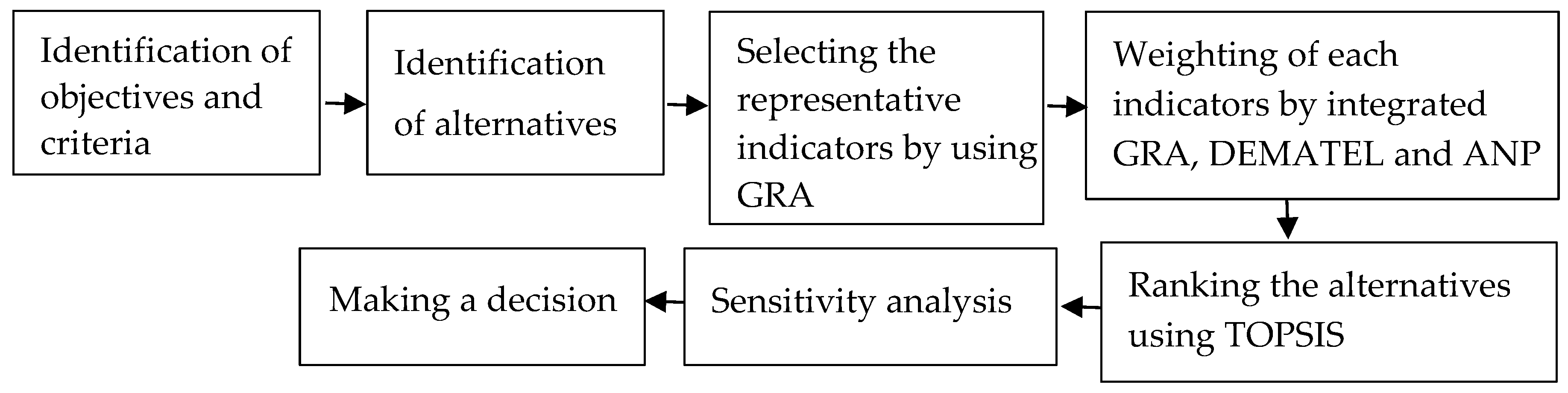

3.4. The Proposed Hybrid MCDM Model

- Establish the original sequence , where .

- Before attempting grey relational analysis, the original experimental data must be normalized. Normalization can be done according to whether the indicators are the larger-the-better, the smaller-the-better or the nominal-the-better criterion. In this step, all the representative financial ratios are normalized in the range between zero and one. There are methods of data normalization [61]:

- (1)

- Larger-the-better: Upper-bound effectiveness measuring.where is the maximum value of , is the minimum value of and is the value after grey relational generation.

- (2)

- Smaller-the-better: Lower-bound effectiveness measuring

- (3)

- Nominal-the-better: Moderate effectiveness measuringwhere is the objective value of xi(k).After the normalization of the data, we can obtain the normalized data matrix .

- Calculation of the grey relational coefficientFor a sequence comparison, when any one sequence can be used as a reference sequence, another sequence acts as a comparative sequence.Then, the globalized grey relational coefficient is defined aswhere , , , , , , is the distinguishing coefficient and . In general, the distinguishing coefficient is set as 0.5 [27].

- Calculation of the grey relational grade

- Calculation of the grey relational matrix.Based on the grey relational grade, a grey relational matrix can be obtained,where represents the degree of correlation between and sequences.

3.5. Sensitivity Analysis

4. Empirical Results

4.1. The Results of Banks’ Green Credit Decision-Making

4.1.1. The Selection of Representative Financial Indicators

4.1.2. Integrating Globalized GRA and DEMATEL to Calculate the Degree of the Relationship between Two Indicators

4.1.3. Integrating Globalized GRA-DEMATEL and ANP to Calculate the Weights of Evaluation Indicators

4.1.4. Using the TOPSIS Method to Evaluate and Rank High-Tech Industry Listed Companies

4.2. The Results of Sensitivity Analysis

5. Conclusions and Future Work

Author Contributions

Funding

Conflicts of Interest

Appendix A. List of Equator Principles

| Principle | Statement of Principles | Main Contents |

|---|---|---|

| Principle 1 | Review and Categorisation | When a project is proposed for financing, it is reviewed and classified according to the magnitude of its potential environmental and social risks and impacts. |

| Principle 2 | Environmental and Social Assessment | For all projects, the relevant environmental and social risks and impacts of the proposed project |

| Principle 3 | Applicable Environmental and Social Standards | The assessment process should address compliance with the relevant host country laws, regulations and permits that pertain to environmental and social issues. |

| Principle 4 | Environmental and Social Management System and Equator Principles Action Plan | An Environmental and Social Management System (ESMS) must be developed or maintained by the client. |

| Principle 5 | Stakeholder Engagement | The client requires a demonstration of effective stakeholder engagement as an ongoing process in a structured and culturally appropriate manner with affected communities. |

| Principle 6 | Grievance Mechanism | The client requires the establishment of a grievance mechanism designed to receive and facilitate the resolution of concerns and grievances. |

| Principle 7 | Independent Review | For all projects, an independent consultant, not directly associated with the client, will carry out an Independent Review of the assessment documentation. |

| Principle 8 | Covenants | For all projects, the client will covenant in the financing documentation a compliance with all relevant host country environmental and social laws, regulations and permits in all material respects. |

| Principle 9 | Independent Monitoring and Reporting | To assess the project compliance with the Equator Principles and to ensure ongoing monitoring and reporting after Financial Closure and over the life of the loan. |

| Principle 10 | Reporting and Transparency | The Equator Principles Financial Institutions (EPFI) will report publicly on transactions that have reached financial closure and on its Equator Principles implementation processes and experience, taking into account appropriate confidentiality considerations. |

Appendix B. Results in Detail

- As mentioned in Section 4, we collected 21 financial indicators by using a globalized GRA to obtain the grey relational matrix, as shown in Table A2. According to Reference [34], we selected 9 indicators (see Section 4.1).Table A2. The grey relational matrix.

Profitability 1 0.6261 0.6432 0.8573 0.8492 0.7821 0.6931 1 0.5954 0.6618 0.6559 0.6644 0.7083 0.5954 1 0.7511 0.7574 0.7391 0.8624 0.6020 0.7010 1 0.9384 0.7997 0.8578 0.6029 0.7136 0.9399 1 0.7981 0.8099 0.6403 0.7192 0.8208 0.8154 1 Operating ability 1 0.732 0.7762 0.7786 0.8659 0.5703 0.4863 0.7266 1 0.7598 0.7021 0.726 0.5679 0.4805 0.7782 0.7668 1 0.7652 0.8038 0.5371 0.4568 0.7807 0.7102 0.7652 1 0.8239 0.4937 0.4237 0.8656 0.7308 0.8016 0.8218 1 0.534 0.4596 0.5635 0.5679 0.5267 0.4831 0.5276 1 0.7176 0.4894 0.4911 0.4568 0.4237 0.4635 0.7254 1 Solvency 1 0.7126 0.7149 0.7078 0.6316 0.5089 0.7504 0.7536 0.7223 1 0.6679 0.6687 0.5829 0.5275 0.7842 0.7785 0.7196 0.6626 1 0.9375 0.7672 0.4232 0.7052 0.7087 0.7147 0.6659 0.9382 1 0.7664 0.4229 0.7056 0.7090 0.6426 0.5829 0.7712 0.7685 1 0.4043 0.6248 0.6259 0.5116 0.5176 0.4198 0.4167 0.395 1 0.4934 0.4898 0.7253 0.7526 0.6714 0.6697 0.5785 0.4553 1 0.9745 0.7287 0.7461 0.675 0.6734 0.5794 0.4516 0.9745 1 - To integrate a globalized GRA and DEMATEL, use the selection indicators in Table 2 to establish a direct-relation matrix . Then, the total-relation matrix can be obtained.

- To integrate a globalized GRA, DEMATEL and ANP, the weighted supermatrix () was obtained by using “Super Decision 2.2”. Then, the limit supermatrix can be obtained by the ANP method. A relative weight for each indicator can be obtained by limit supermatrix, as shown in Table A3.Table A3. The weights of the indicators using a globalized GRA-DEMATEL-ANP.

Indicators Weights 0.05798 0.05902 0.05726 0.0576 0.0565 0.05175 0.05811 0.05707 0.05243 Indicators ECO CSRD EID EE DOL DFL RAROC RDE TCRI Weights 0.05625 0.05872 0.05848 0.05363 0.0515 0.05887 0.0545 0.05538 0.04495 Note: : return on assets, : return on equity, : net profit margin : current ratio, : long-term capital ratio, : times interest earned, : oper. income/capital, : turnover of net worth, : days-inventory turnover, ECO: eco-efficiency indicator, CSRD: CSR disclosures, EID: environment information disclosures, EE: environment expenditure, DOL: degree of operating leverage, DFL: degree of financial leverage, RAROC: risk-adjusted rate of return on capital, RDE: R&D expenditure, TCRI: Taiwan corporate credit risk index. - Establish the normalized decision matrix for the TOPSIS analysis. Then, the weighted normalized decision matrix for each indicator can be calculated.

- Identify the positive idea solution and the negative idea solution . Then, calculate the positive and negative ideal solutions ( and ) for each company, respectively.

- 6. Calculate the relative closeness coefficient for each alternative. Then, rank the 55 companies according to the relative closeness coefficients. The results are shown in Table 3.

{kind=link}

{kind=link}

{kind=link}

Appendix C. The Ranking Results of the Sensitivity Analysis

| Indicators | |||||||||

| Weights | 0.06407 | 0.07082 | 0.06299 | 0.06336 | 0.05368 | 0.04140 | 0.06973 | 0.06278 | 0.04981 |

| Indicators | ECO | CSRD | EID | EE | DOL | DFL | RAROC | RDE | TCRI |

| Weights | 0.05344 | 0.07046 | 0.07018 | 0.05095 | 0.04120 | 0.07064 | 0.05178 | 0.05261 | 0.03596 |

| Companies | F1 | F2 | F3 | F4 | F5 | F6 | F7 | F8 | F9 | F10 | F11 | F12 | F13 | F14 |

| Rank | 51 | 42 | 5 | 3 | 14 | 38 | 24 | 16 | 11 | 7 | 13 | 39 | 52 | 1 |

| Companies | F15 | F16 | F17 | F18 | F19 | F20 | F21 | F22 | F23 | F24 | F25 | F26 | F27 | F28 |

| Rank | 21 | 6 | 46 | 34 | 32 | 23 | 9 | 15 | 35 | 29 | 2 | 4 | 20 | 30 |

| Companies | F29 | F30 | F31 | F32 | F33 | F34 | F35 | F36 | F37 | F38 | F39 | F40 | F41 | F42 |

| Rank | 17 | 26 | 18 | 19 | 47 | 53 | 36 | 22 | 27 | 8 | 28 | 40 | 10 | 44 |

| Companies | F43 | F44 | F45 | F46 | F47 | F48 | F49 | F50 | F51 | F52 | F53 | F54 | F55 | |

| Rank | 50 | 45 | 37 | 43 | 12 | 55 | 33 | 41 | 49 | 25 | 54 | 31 | 48 |

References

- Eccles, R.G.; Pyburn, P.F. Creating a comprehensive system to measure performance. Manag. Acc. 1992, 74, 41–44. [Google Scholar]

- Weber, O.; Scholz, R.W.; Michalik, G. Incorporating sustainability criteria into credit risk management. Bus. Strateg. Environ. 2010, 19, 39–50. [Google Scholar] [CrossRef]

- Aruldoss, M.; Lakshmi, T.M.; Venkatesan, V.P. A survey on multi criteria decision making methods and its applications. Am. J. Inf. Syst. 2013, 1, 31–43. [Google Scholar]

- Büyüközkan, G.; Arsenyan, J.; Ertek, G. Evaluation of e-learning web sites using fuzzy axiomatic design based approach. Int. J. Comput. Int. Syst. 2010, 3, 28–42. [Google Scholar] [CrossRef]

- Kou, G.; Peng, Y.; Lu, C. MCDM approach to evaluating bank loan default models. Technol. Econ. Dev. 2014, 20, 292–311. [Google Scholar] [CrossRef]

- Rostamzadeh, R.; Ismail, K.; Bodaghi Khajeh Noubar, H. An application of a hybrid MCDM method for the evaluation of entrepreneurial intensity among the SMEs: A case study. Sci. World J. 2014, 2014, 703650. [Google Scholar] [CrossRef] [PubMed]

- Alam-Tabriz, A.; Rajabani, N.; Farrokh, M. An integrated fuzzy DEMATEL-ANP-TOPSIS methodology for supplier selection problem. Glob. J. Manag. Stud. Res. 2014, 1, 85–99. [Google Scholar]

- Alimardani, M.; Rabbani, M.; Rafiei, H. A novel hybrid model based on DEMATEL, ANP and TOPSIS for supplier selection in agile supply chains. Int. J. Serv. Oper. Manag. 2014, 18, 179–211. [Google Scholar] [CrossRef]

- Kuan, M.; Chen, Y. A hybrid MCDM framework combined with DEMATEL-based ANP to evaluate enterprise technological innovation capabilities assessment. Decis. Sci. Lett. 2014, 3, 491–502. [Google Scholar] [CrossRef]

- Shen, K.Y.; Yan, M.R.; Tzeng, G.H. Combining VIKOR-DANP model for glamor stock selection and stock performance improvement. Knowl. Based Syst. 2014, 58, 86–97. [Google Scholar] [CrossRef]

- Hsu, L.C. Investment decision making using a combined factor analysis and entropy-based TOPSIS model. J. Bus. Econ. Manag. 2013, 14, 448–466. [Google Scholar] [CrossRef]

- Bulgurcu, B. Financial performance ranking of automotive industry firms in Turkey: Evidence from entropy weighted technique. Int. J. Econ. Financ. 2013, 3, 844–851. [Google Scholar]

- Ghadikolaei, A.S.; Esbouei, S.K. Integrating fuzzy AHP and fuzzy ARAS for evaluating financial performance. Bol. Soc. Parana. Mat. 2013, 32, 163–174. [Google Scholar] [CrossRef]

- Ghadikolaei, A.S.; Esbouei, S.K.; Antucheviciene, J. Applying fuzzy MCDM for financial performance evaluation of Iranian companies. Technol. Econ. Dev. 2014, 20, 274–291. [Google Scholar] [CrossRef]

- Moghimi, R.; Anvari, A. An integrated fuzzy MCDM approach and analysis to evaluate the financial performance of Iranian cement companies. Int. J. Adv. Manuf. Technol. 2014, 71, 685–698. [Google Scholar] [CrossRef]

- Wang, Y.J. The evaluation of financial performance for Taiwan container shipping companies by fuzzy TOPSIS. Appl. Soft Comput. 2014, 22, 28–35. [Google Scholar] [CrossRef]

- Sun, Y.F.; Wu, C.H. Green credit loan as environmental policy. Environ. Econ. 2010, 1, 68–75. [Google Scholar]

- Li, J.L. Enterprises’ environmental credit assessment-from the perspective of financial institutions’ green credit. Adv. Mater. Res. 2012, 361, 1868–1873. [Google Scholar] [CrossRef]

- Xu, L. On the evaluation of performance system incorporating “green credit” policies in China’s financial industry. J. Financ. Risk Manag. 2013, 2, 33–37. [Google Scholar] [CrossRef]

- Toloie-Eshlaghy, A.; Homayonfar, M. MCDM methodologies and applications: A literature review from 1999 to 2009. Res. J. Int. Stud. 2011, 21, 86–137. [Google Scholar]

- Büyüközkan, G.; Çifçi, G. A novel hybrid MCDM approach based on fuzzy DEMATEL, fuzzy ANP and fuzzy TOPSIS to evaluate green suppliers. Expert Syst. Appl. 2012, 39, 3000–3011. [Google Scholar] [CrossRef]

- Ou Yang, Y.P.; Shieh, H.M.; Tzeng, G.H. A VIKOR technique based on DEMATEL and ANP for information security risk control assessment. Inf. Sci. 2013, 232, 482–500. [Google Scholar] [CrossRef]

- Ding, S.H.; Kamaruddin, S. Assessment of distance-based multi-attribute group decision-making methods from a maintenance strategy perspective. J. Ind. Eng. Int. 2014, 11, 73–85. [Google Scholar] [CrossRef]

- Hassan, M.; Kamran, N.; Mohsen, M.C.; Vahidreza, M. Design of a combined fuzzy model in codifying and ranking strategies. Afr. J. Bus. Manag. 2012, 6, 11797–11808. [Google Scholar] [CrossRef]

- Stanujkic, D.; Djordjevic, B.; Djordjevic, M. Comparative analysis of some prominent MCDM methods: A case of ranking Serbian banks. Serb. J. Manag. 2013, 8, 213–241. [Google Scholar] [CrossRef]

- Ou, Y.C. Using a hybrid decision-making model to evaluate the sustainable development performance of high-tech listed companies. J. Bus. Econ. Manag. 2016, 17, 331–346. [Google Scholar] [CrossRef]

- Hsu, L.C.; Ou, S.L.; Ou, Y.C. A comprehensive performance evaluation and ranking methodology under a sustainable development perspective. J. Bus. Econ. Manag. 2015, 16, 74–92. [Google Scholar] [CrossRef]

- Hwang, R.C.; Chung, H.; Siao, J.S.; Lin, C.L. Does the local rating agency provide reliable credit ratings? An empirical analysis from an emerging market. J. Fixed Income 2012, 22, 41–51. [Google Scholar] [CrossRef]

- Lu, S.L. Assessing the credit risk of bank loans using an extended Markov chain model. J. Appl. Financ. Bank. 2012, 2, 197–223. [Google Scholar]

- Norman, W.; MacDonald, C. Getting to the bottom of “triple bottom line”. Bus. Ethics Q. 2004, 14, 243–262. [Google Scholar] [CrossRef]

- Fujii, H.; Iwata, K.; Kaneko, S.; Managi, S. Corporate environmental and economic performances of Japanese manufacturing firms: Empirical study for sustainable development. Bus. Strateg. Environ. 2013, 22, 187–201. [Google Scholar] [CrossRef]

- Grigoroudis, E.; Orfanoudaki, E.; Zopounidis, C. Strategic performance measurement in a healthcare organization: A multiple criteria approach based on balanced score. Omega 2012, 40, 104–119. [Google Scholar] [CrossRef]

- Ittner, C.D.; Larcker, D.F. Coming up short on non-financial performance measurement. Harv. Bus. Rev. 2003, 81, 88–95. [Google Scholar] [PubMed]

- Hsu, L.C. A hybrid multiple criteria decision-making model for investment decision making. J. Bus. Econ. Manag. 2014, 15, 509–529. [Google Scholar] [CrossRef]

- Hsu, L.C. Using a decision-making process to evaluate efficiency and operating performance for listed semiconductor companies. Technol. Econ. Dev. 2015, 21, 301–331. [Google Scholar] [CrossRef]

- Fu, G.; Wang, J.; Jia, M. The relationship between corporate social performance and financial performance: Modified models and their application: Evidence from listed companies in China. J. Contemp. Manag. 2013, 2, 17–37. [Google Scholar]

- Karagiorgos, T. Corporate social responsibility and financial performance: An empirical analysis on Greek companies. Eur. Res. Stud. 2010, 13, 85–108. [Google Scholar]

- Rundle-Thiele, S.; Ball, K.; Gillespie, M. Raising the bar: From corporate social responsibility to corporate social performance. J. Consum. Mark. 2008, 25, 245–253. [Google Scholar] [CrossRef]

- Fauzi, H.; Svensson, G.; Rahman, A.A. “Triple bottom line” as “sustainable corporate performance”: A proposition for the future. Sustainability 2010, 2, 1345–1360. [Google Scholar] [CrossRef]

- Elsakit, O.; Worthington, A. The attitudes of managers and stakeholders towards corporate social and environmental disclosure. Int. J. Econ. Financ. 2012, 4, 240–251. [Google Scholar] [CrossRef]

- Yılmaz, İ. Social performance vs. financial performance: CSR disclosures as an indicator of social performance. Int. J. Financ. Bank Stud. 2013, 2, 53–65. [Google Scholar] [CrossRef]

- Porter, M.E. The competitive advantage of the inner city. Harv. Bus. Rev. 1995, 73, 55–71. [Google Scholar]

- Maxwell, J.; Rothenberg, S.; Briscoe, F.; Marcus, A. Green schemes: Corporate environmental strategies and their implementation. Calif. Manag. Rev. 1997, 39, 118–120. [Google Scholar] [CrossRef]

- Chen, Y.S.; Lai, S.B.; Wen, C.T. The influence of green innovation performance on corporate advantage in Taiwan. J. Bus. Ethics 2006, 67, 331–339. [Google Scholar] [CrossRef]

- King, A.A.; Lenox, M.J. Does it really pay to be green? An empirical study of firm environmental and financial performance: An empirical study of firm environmental and financial performance. J. Ind. Ecol. 2001, 5, 105–116. [Google Scholar] [CrossRef]

- López-Gamero, M.D.; Molina-Azorín, J.F.; Claver-Cortés, E. The whole relationship between environmental variables and firm performance: Competitive advantage and firm resources as mediator variables. J. Environ. Manag. 2009, 90, 3110–3121. [Google Scholar] [CrossRef] [PubMed]

- Wang, W.K.; Lu, W.M.; Wang, S.W. The impact of environmental expenditures on performance in the U.S. chemical industry. J. Clean. Prod. 2013, 64, 447–456. [Google Scholar] [CrossRef]

- Aerts, W.; Cormier, D.; Magnan, M. Corporate environmental disclosure, financial markets and the media: An international perspective. Ecol. Econ. 2008, 64, 643–659. [Google Scholar] [CrossRef]

- Charles, H.C.; Martin, F.; Dennis, M.P. Corporate disclosure of environmental capital expenditures: A test of alternative theories. Account. Audit. Account. J. 2012, 25, 486–507. [Google Scholar]

- Leiter, A.M.; Parolini, A.; Winner, H. Environmental regulation and investment: Evidence from European industry data. Ecol. Econ. 2011, 70, 759–770. [Google Scholar] [CrossRef]

- Patten, D.M. The relation between environmental performance and environmental disclosure: A research note. Account. Org. Soc. 2002, 27, 763–773. [Google Scholar] [CrossRef]

- Verrecchia, R.E. Discretionary disclosure. J. Acc. Econ. 1983, 5, 179–194. [Google Scholar] [CrossRef]

- Christmann, P.; Taylor, G. Globalization and the environment: Determinants of firm self-regulation in China. J. Int. Bus. Stud. 2001, 32, 439–458. [Google Scholar] [CrossRef]

- Dean, T.J.; Brown, R.L. Pollution regulation as a barrier to new firm entry: Initial evidence and implications for future research. Acad. Manag. J. 1995, 38, 288–303. [Google Scholar]

- Yoon, K.P.; Hwang, C.L. Multiple Attribute Decision Making: An Introduction; Sage Publications: Thousand Oaks, CA, USA, 1995. [Google Scholar]

- Kung, C.Y.; Wen, K.L. Applying grey relational analysis and grey decision-making to evaluate the relationship between company attributes and its financial performance—A case study of venture capital enterprises in Taiwan. Decis. Support Syst. 2007, 43, 842–852. [Google Scholar] [CrossRef]

- Özdağoğlu, A.; Gümüş, Y.; Özdağoğlu, G.; Gümüş, G.K. Evaluating financial performance with grey relational analysis: An application of manufacturing companies listed on Borsa İstanbul. Muhasebe ve Finansman Dergisi 2017, 73, 289–312. [Google Scholar] [CrossRef]

- Malek, A.; Ebrahimnejad, S.; Tavakkoli-Moghaddam, R. An improved hybrid grey relational analysis approach for green resilient supply chain network assessment. Sustainability 2017, 9, 1433. [Google Scholar] [CrossRef]

- Kuo, T. A review of some modified grey relational analysis models. J. Grey Syst. 2017, 29, 70–77. [Google Scholar]

- Wang, Y.J. Combining grey relation analysis with FMCGDM to evaluate financial performance of Taiwan container lines. Expert Syst. Appl. 2009, 36, 2424–2432. [Google Scholar] [CrossRef]

- Sa, B.; Mb, S.; Pasupathy, S.A.; Karthick Kumar, K.; Ge, S. Multi objective optimization of anaerobic digestion of poultry litter using Taguchi grey relational analysis. Int. J. Appl. Eng. Res. 2018, 13, 5216–5222. [Google Scholar]

- Deng, J.L. Control problems of grey systems. Syst. Control Lett. 1982, 1, 288–294. [Google Scholar]

- Shao, Q.G.; Liou, J.J.; Weng, S.S.; Chuang, Y.C. Improving the green building evaluation system in China based on the DANP method. Sustainability 2018, 10, 1173. [Google Scholar] [CrossRef]

- Moghassem, A.R.; Fallahpour, A.R. Selecting doffing tube components for rotor-spun yarn for weft knitted fabrics using multi-criteria decision-making approach with interval data. J. Eng. Fiber Fabr. 2011, 6, 44–53. [Google Scholar] [CrossRef]

- Moghassem, A.R. Comparison among two analytical methods of multi-criteria decision making for appropriate spinning condition selection. World Appl. Sci. J. 2013, 21, 784–794. [Google Scholar]

- Yu, V.F.; Hu, K.J. An integrated fuzzy multi-criteria approach for the performance evaluation of multiple manufacturing plants. Comput. Ind. Eng. 2010, 58, 269–277. [Google Scholar] [CrossRef]

- Feng, C.M.; Wang, R.T. Performance evaluation for airlines including the consideration of financial ratios. J. Air Transp. Manag. 2000, 6, 133–142. [Google Scholar] [CrossRef]

- Ballı, S.; Korukoğlu, S. Development of a fuzzy decision support framework for complex multi-attribute decision problems: A case study for the selection of skilful basketball players. Expert Syst. 2014, 31, 56–69. [Google Scholar] [CrossRef]

- Chakraborty, R.; Ray, A.; Dan, P. Multi criteria decision making methods for location selection of distribution centers. Int. J. Ind. Eng. Comput. 2013, 4, 491–504. [Google Scholar] [CrossRef]

| Category | Code | Financial ratios | Definition |

|---|---|---|---|

| Solvency | Cash flow adequacy ratio | Net cash flow operation over the last five years/(Capital spending + Addition to inventory + Cash dividend) over the five years | |

| Cash reinvestment ratio | (Net cash flow from operating activities − Cash dividend)/(Total fixed assets + Long-term investments + Other assets + Working capital) | ||

| Current ratio | Current assets/Current liabilities | ||

| Quick ratio | (Current assets − Inventories)/Current liabilities | ||

| Long-term capital ratio | (Net shareholder’s equity + Long-term Liabilities)/Net fixed assets | ||

| Times interest earned | (Net income + Interest expense)/Interest expense | ||

| Operation income/Capital | Operation income/Capital | ||

| Pre tax income/Capital | Pretax income/Capital | ||

| Operating ability | Total assets turnover | Net operating revenue/Total assets | |

| Accounts receivable turnover | Net sales/Average balance of account receivable | ||

| Inventory turnover | Cost of sales/Average inventory | ||

| Fixed assets turnover | Net operating revenue/Total fixed assets | ||

| Turnover of net worth | Net Sales/Net worth (Stockholders’ equity) | ||

| Days-A/R turnover | (Total A/R Outstanding/Total Sales) * Days | ||

| Days-inventory turnover | (Average inventory/Cost of goods sold) * days | ||

| Profitability | Returns on assets | (Earning + Interest expenses (1 − Tax rate))/Average total assets | |

| Returns on equity | Current term net profit/Shareholder equity | ||

| Profit margin | (Total sales –Total expenses)/Total sales | ||

| Operating margin | Operating profit/Net sales | ||

| Net profit margin | Net Profit/Total Revenue | ||

| Earnings per share | Net income/Average outstanding common shares |

| Criteria | Indicators |

|---|---|

| Credit risk | Taiwan Corporate Credit Risk Index (TCRI) |

| Economic performance | Return on assets (), Return of equity () and Net profit margin (), Turnover of net worth (), Days-inventory turnover (), Current ratio (), Long-term capital ratio (), Times interest earned (), Oper. income/capital (), R&D expenditure (RDE), Risk-adjusted rate of return on capital (RAROC), Degree of operating leverage (DOL) and Degree of financial leverage (DFL) |

| Social performance | Corporate social responsibility disclosure (CSRD) |

| Environmental performance | Eco-efficiency indicators (ECO), Environmental expenditure (EE) and Environmental information disclosure (EID) |

| Companies | Rank | Companies | Rank | ||||||

|---|---|---|---|---|---|---|---|---|---|

| F1 | 0.16577 | 0.10763 | 0.39367 | 52 | F29 | 0.14519 | 0.13226 | 0.47671 | 15 |

| F2 | 0.15567 | 0.11922 | 0.43370 | 34 | F30 | 0.15546 | 0.12591 | 0.44749 | 26 |

| F3 | 0.14356 | 0.13242 | 0.47982 | 10 | F31 | 0.15034 | 0.13523 | 0.47355 | 17 |

| F4 | 0.13650 | 0.14453 | 0.51429 | 3 | F32 | 0.15342 | 0.12923 | 0.45720 | 21 |

| F5 | 0.14406 | 0.13166 | 0.47753 | 14 | F33 | 0.16088 | 0.10984 | 0.40573 | 48 |

| F6 | 0.16029 | 0.11685 | 0.42163 | 43 | F34 | 0.17682 | 0.10615 | 0.37513 | 55 |

| F7 | 0.15130 | 0.12547 | 0.45333 | 23 | F35 | 0.15611 | 0.11558 | 0.42542 | 42 |

| F8 | 0.14240 | 0.12854 | 0.47441 | 16 | F36 | 0.14905 | 0.13079 | 0.46737 | 19 |

| F9 | 0.14303 | 0.13288 | 0.48162 | 9 | F37 | 0.15046 | 0.12175 | 0.44727 | 27 |

| F10 | 0.14431 | 0.13589 | 0.48498 | 7 | F38 | 0.14867 | 0.13627 | 0.47824 | 13 |

| F11 | 0.14409 | 0.13211 | 0.47830 | 12 | F39 | 0.15173 | 0.12381 | 0.44934 | 25 |

| F12 | 0.15667 | 0.11915 | 0.43199 | 36 | F40 | 0.15878 | 0.11763 | 0.42556 | 41 |

| F13 | 0.16713 | 0.10893 | 0.39458 | 51 | F41 | 0.14057 | 0.13590 | 0.49155 | 5 |

| F14 | 0.14394 | 0.15773 | 0.52285 | 1 | F42 | 0.17360 | 0.11934 | 0.40738 | 46 |

| F15 | 0.15411 | 0.13074 | 0.45897 | 20 | F43 | 0.16653 | 0.10978 | 0.39732 | 50 |

| F16 | 0.14373 | 0.13678 | 0.48763 | 6 | F44 | 0.16157 | 0.11690 | 0.41978 | 44 |

| F17 | 0.15881 | 0.11244 | 0.41452 | 45 | F45 | 0.15488 | 0.11921 | 0.43493 | 33 |

| F18 | 0.15127 | 0.11791 | 0.43802 | 31 | F46 | 0.15779 | 0.11713 | 0.42605 | 40 |

| F19 | 0.16577 | 0.10763 | 0.39367 | 35 | F47 | 0.14519 | 0.13598 | 0.48361 | 8 |

| F20 | 0.15567 | 0.11922 | 0.43370 | 22 | F48 | 0.17064 | 0.10381 | 0.37825 | 54 |

| F21 | 0.14356 | 0.13242 | 0.47982 | 11 | F49 | 0.16161 | 0.12268 | 0.43153 | 37 |

| F22 | 0.13650 | 0.14453 | 0.51429 | 18 | F50 | 0.16004 | 0.11966 | 0.42782 | 38 |

| F23 | 0.14406 | 0.13166 | 0.47753 | 32 | F51 | 0.16281 | 0.11144 | 0.40635 | 47 |

| F24 | 0.16029 | 0.11685 | 0.42163 | 28 | F52 | 0.15049 | 0.12294 | 0.44963 | 24 |

| F25 | 0.15130 | 0.12547 | 0.45333 | 2 | F53 | 0.16963 | 0.10966 | 0.39265 | 53 |

| F26 | 0.14240 | 0.12854 | 0.47441 | 4 | F54 | 0.16421 | 0.12275 | 0.42776 | 39 |

| F27 | 0.14303 | 0.13288 | 0.48162 | 29 | F55 | 0.17838 | 0.12123 | 0.40464 | 49 |

| F28 | 0.14431 | 0.13589 | 0.48498 | 30 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yang, C.-C.; Ou, S.-L.; Hsu, L.-C. A Hybrid Multi-Criteria Decision-Making Model for Evaluating Companies’ Green Credit Rating. Sustainability 2019, 11, 1506. https://doi.org/10.3390/su11061506

Yang C-C, Ou S-L, Hsu L-C. A Hybrid Multi-Criteria Decision-Making Model for Evaluating Companies’ Green Credit Rating. Sustainability. 2019; 11(6):1506. https://doi.org/10.3390/su11061506

Chicago/Turabian StyleYang, Chia-Chen, Shang-Ling Ou, and Li-Chang Hsu. 2019. "A Hybrid Multi-Criteria Decision-Making Model for Evaluating Companies’ Green Credit Rating" Sustainability 11, no. 6: 1506. https://doi.org/10.3390/su11061506

APA StyleYang, C.-C., Ou, S.-L., & Hsu, L.-C. (2019). A Hybrid Multi-Criteria Decision-Making Model for Evaluating Companies’ Green Credit Rating. Sustainability, 11(6), 1506. https://doi.org/10.3390/su11061506