What Happens after the Rare Earth Crisis: A Systematic Literature Review

Abstract

:1. Introduction

2. Materials and Methods

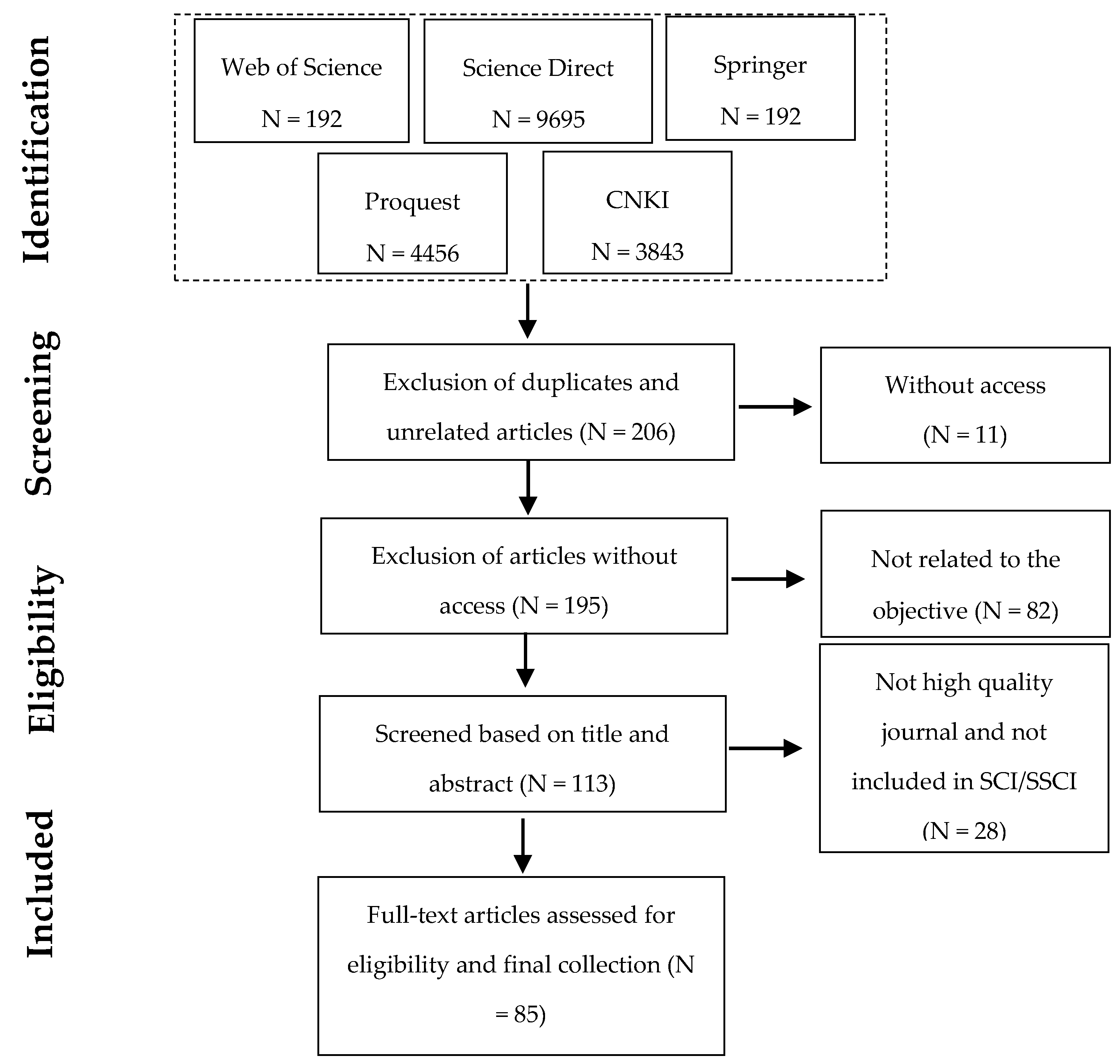

2.1. Literature Research

2.2. Quality Assessment

2.3. Eligibility and Inclusion Criteria

2.4. Studies Included in Qualitative Synthesis

3. Results

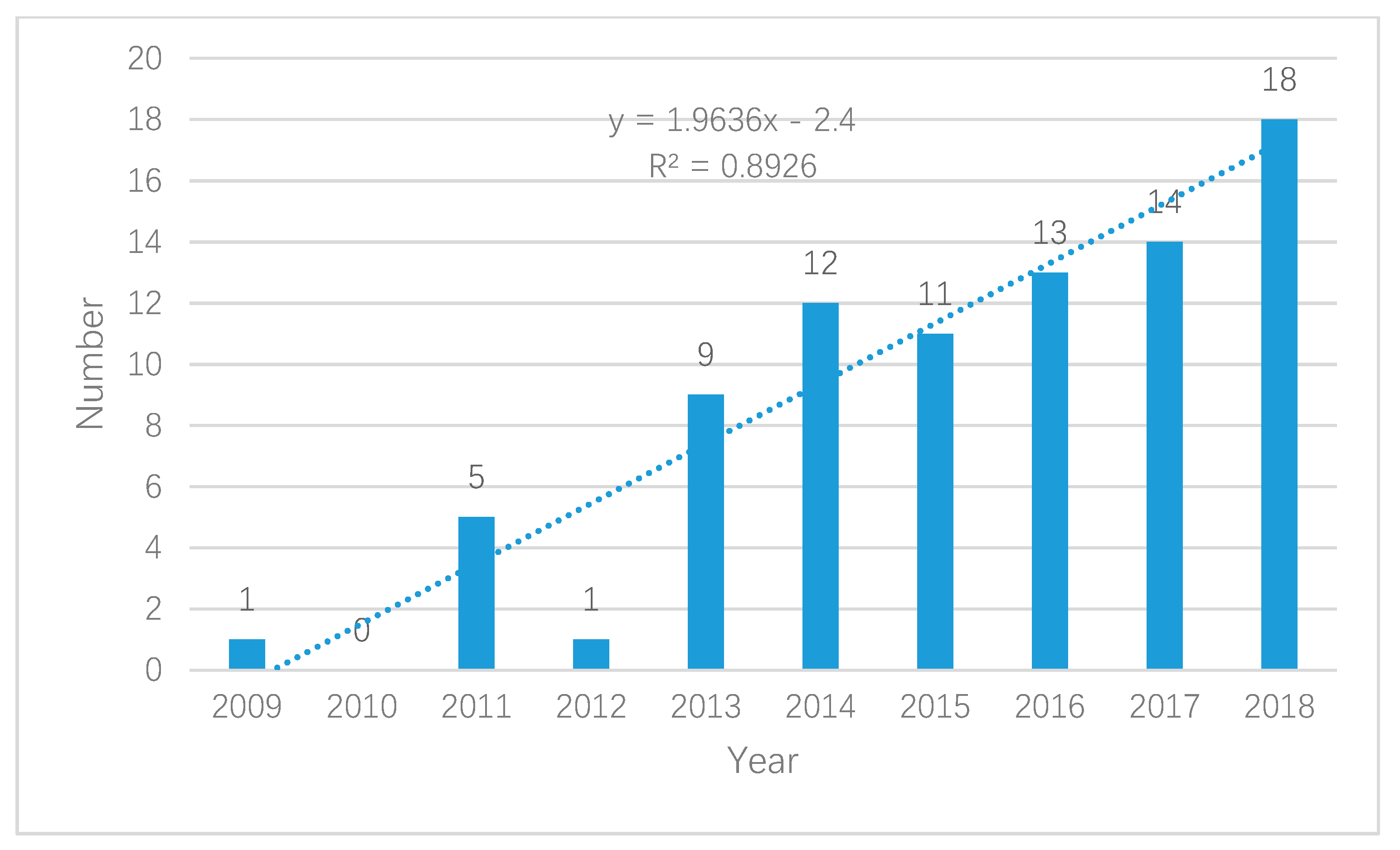

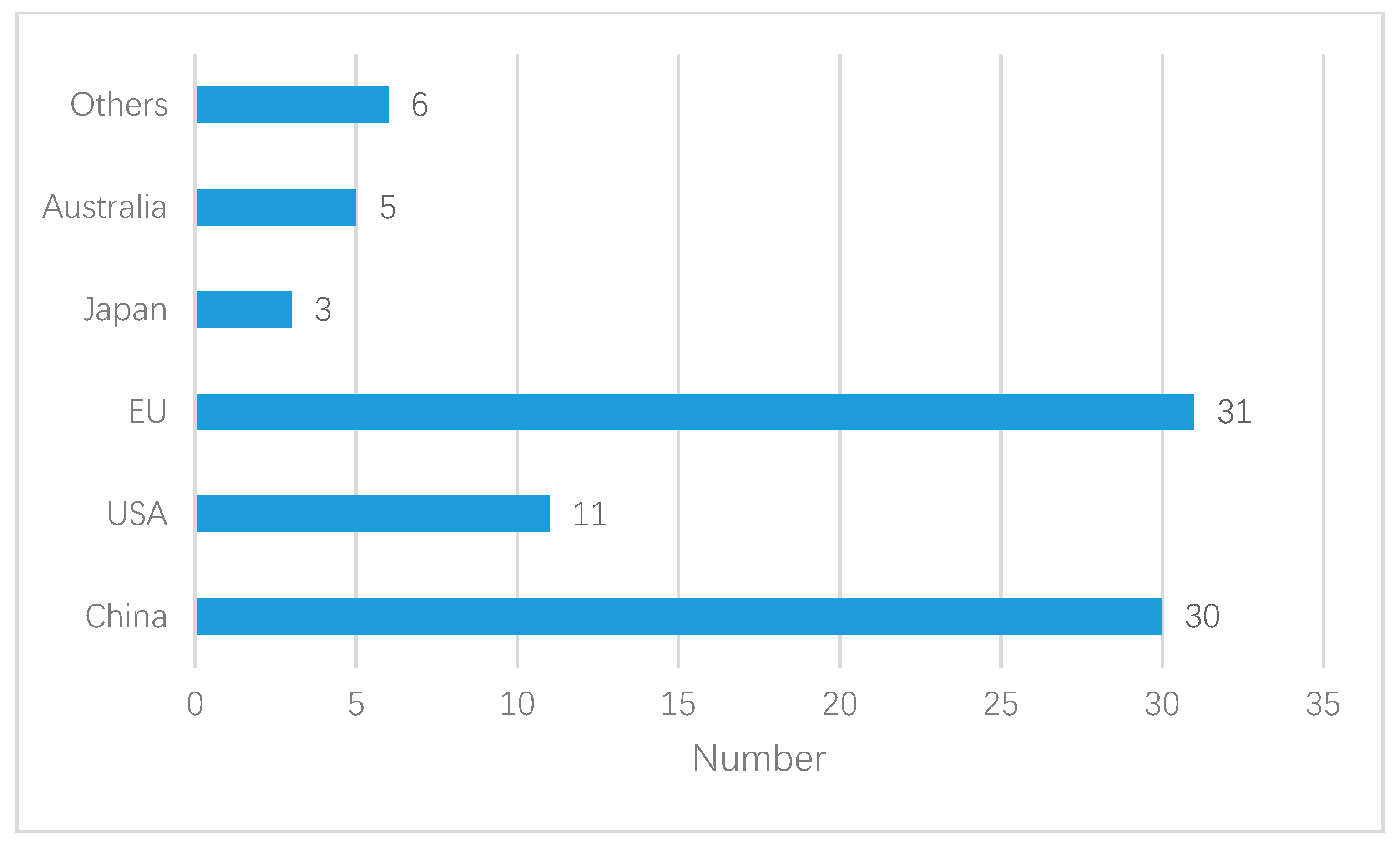

3.1. Descriptive Analysis

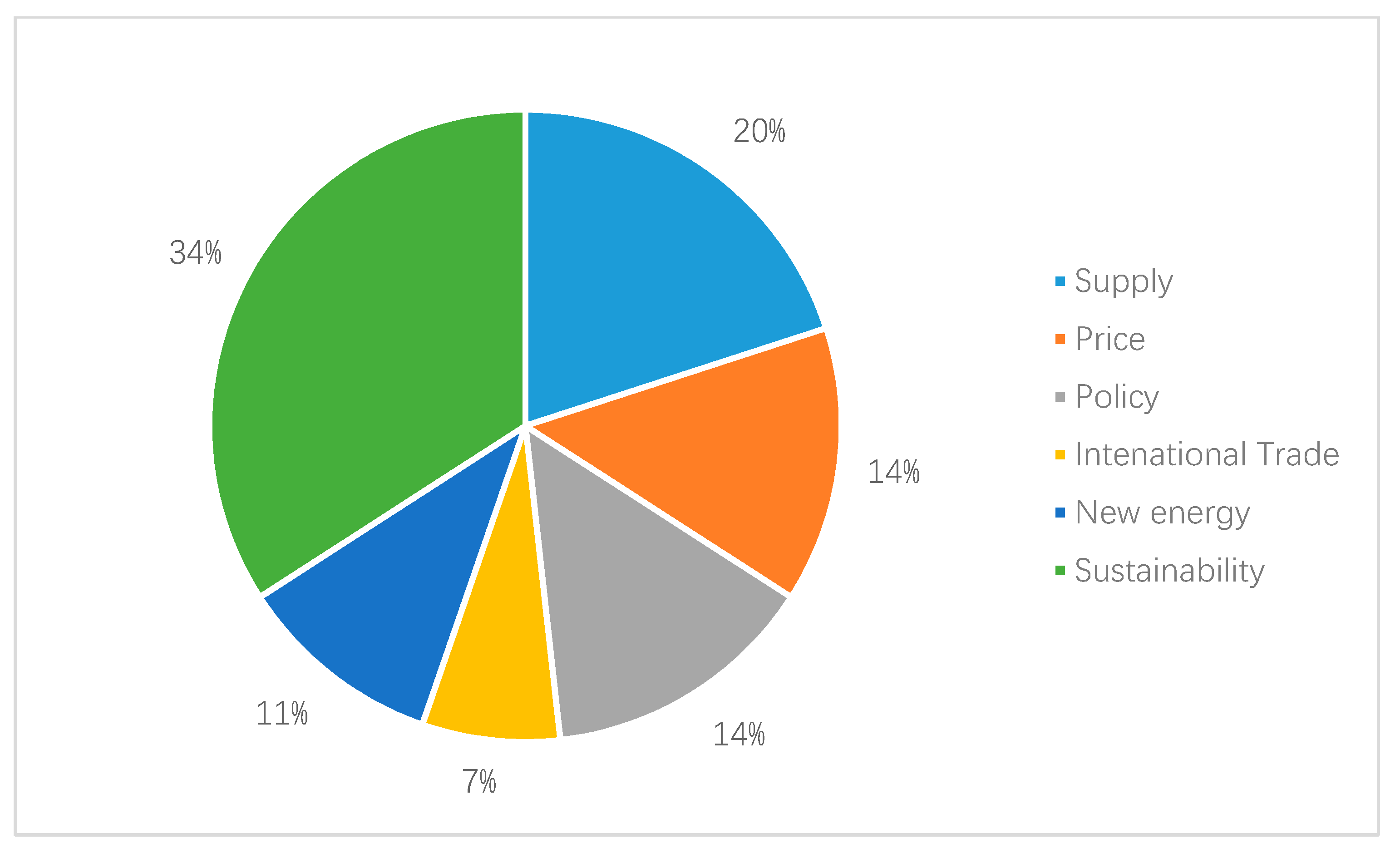

3.2. Content Analysis

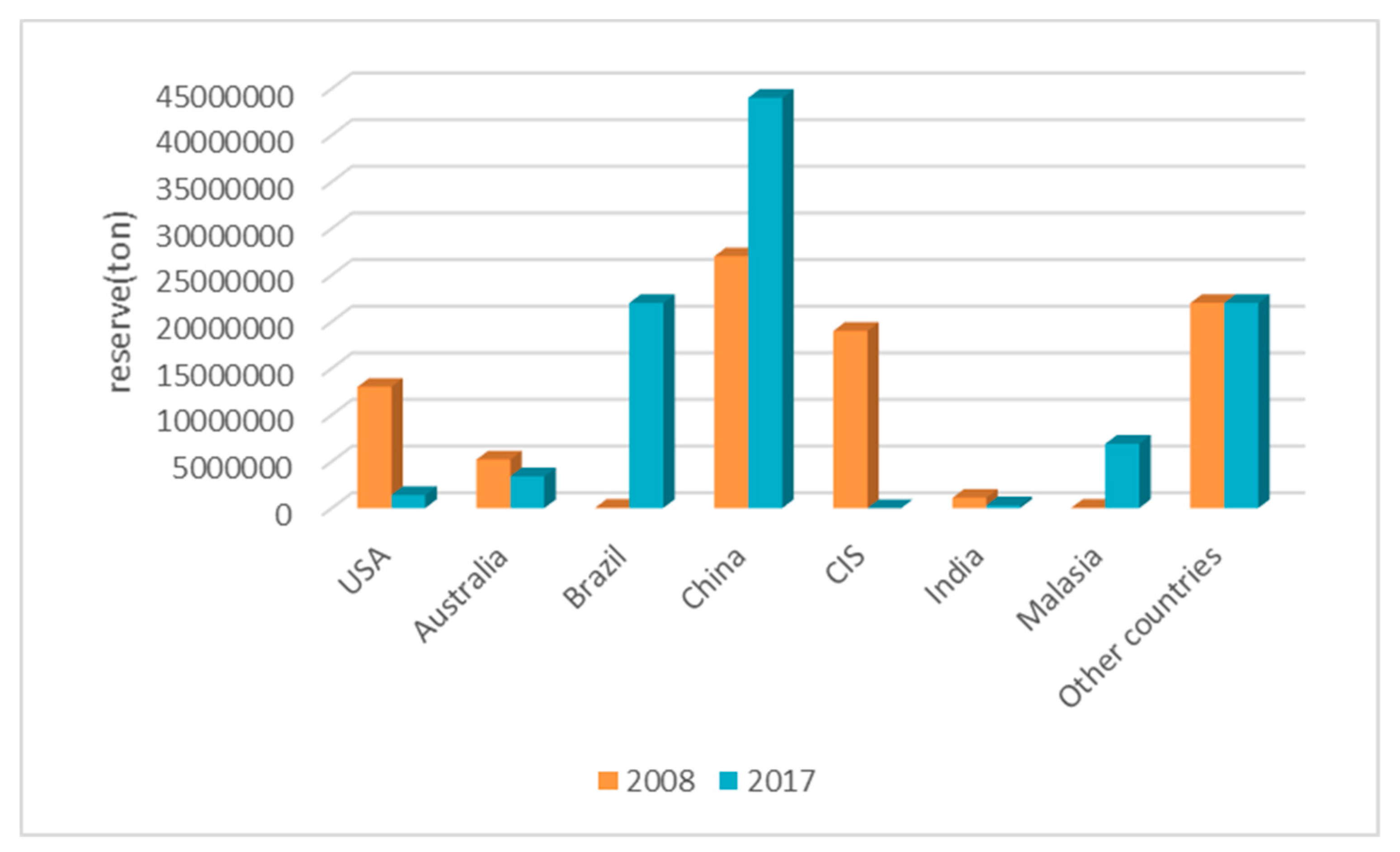

3.2.1. Issues about the Supply of REs

3.2.2. The Price of REs

3.2.3. The Export Policy of China

3.2.4. International Trade of REs

3.2.5. Research about the Relationship with Clean Energy

3.2.6. Sustainability

4. Discussion

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Gupta, C.K.; Krishnamurthy, N. Extractive metallurgy of rare earths. Int. Mater. Rev. 1992, 37, 197–248. [Google Scholar] [CrossRef]

- Moldoveanu, G.A.; Papangelakis, V.G. Recovery of rare earth elements adsorbed on clay minerals: I. Desorption mechanism. Hydrometallurgy 2012, 117–118, 71–78. [Google Scholar] [CrossRef]

- Jordens, A.; Cheng, Y.P.; Waters, K.E. A review of the beneficiation of rare earth element bearing minerals. Miner. Eng. 2013, 41, 97–114. [Google Scholar] [CrossRef]

- Xie, F.; Zhang, T.A.; Dreisinger, D.; Doyle, F. A critical review on solvent extraction of rare earths from aqueous solutions. Miner. Eng. 2014, 56, 10–28. [Google Scholar] [CrossRef]

- Hayes-Labruto, L.; Schillebeeckx, S.J.D.; Workman, M.; Shah, N. Contrasting perspectives on China’s rare earths policies: Reframing the debate through a stakeholder lens. Energy Policy 2013, 63, 55–68. [Google Scholar] [CrossRef]

- Han, A.; Ge, J.; Lei, Y. An adjustment in regulation policies and its effects on market supply: Game analysis for China’s rare earths. Resour. Policy 2015, 46, 30–42. [Google Scholar] [CrossRef]

- Hoenderdaal, S.; Tercero Espinoza, L.; Marscheider-Weidemann, F.; Graus, W. Can a dysprosium shortage threaten green energy technologies? Energy 2013, 49, 344–355. [Google Scholar] [CrossRef]

- Bristish Geological Survey. Risk List 2015; Bristish Geological Survey: Nottingham, UK, 2015. [Google Scholar]

- US Department of Energy. Critical Materials Strategy; US Department of Energy: Washington, DC, USA, 2011.

- Massari, S.; Ruberti, M. Rare earth elements as critical raw materials: Focus on international markets and future strategies. Resour. Policy 2013, 38, 36–43. [Google Scholar] [CrossRef]

- Ali, S.H. Social and Environmental Impact of the Rare Earth Industries. Resources 2014, 3, 123–134. [Google Scholar] [CrossRef]

- Anastopoulos, I.; Bhatnagar, A.; Lima, E.C. Adsorption of rare earth metals: A review of recent literature. J. Mol. Liq. 2016, 221, 954–962. [Google Scholar] [CrossRef]

- Cox, C.; Kynicky, J. The rapid evolution of speculative investment in the REE market before, during, and after the rare earth crisis of 2010–2012. Extr. Ind. Soc. 2018, 5, 8–17. [Google Scholar] [CrossRef]

- Klinger, J.M. Rare earth elements: Development, sustainability and policy issues. Extr. Ind. Soc. 2018, 5, 1–7. [Google Scholar] [CrossRef]

- Klinger, J.M. A historical geography of rare earth elements: From discovery to the atomic age. Extr. Ind. Soc. 2015, 2, 572–580. [Google Scholar] [CrossRef]

- Kiggins, R.D. The Political Economy of Rare Earth Elements: Rising Powers and Technological Change; Springer: Berlin, Germany, 2015. [Google Scholar]

- Klinger, J.M. Rare Earth Frontiers: From Terrestrial Subsoils to Lunar Landscapes; Cornell University Press: Ithaca, NY, USA, 2018. [Google Scholar]

- Wübbeke, J. China’s Rare Earth Industry and End-Use: Supply Security and Innovation; Palgrave Macmillan: London, UK, 2015. [Google Scholar]

- Chen, J.; Zhu, X.; Liu, G.; Chen, W.; Yang, D. China’s rare earth dominance: The myths and the truths from an industrial ecology perspective. Resour. Conserv. Recycl. 2018, 132, 139–140. [Google Scholar] [CrossRef]

- Jin, Y.; Kim, J.; Guillaume, B. Review of critical material studies. Resour. Conserv. Recycl. 2016, 113, 77–87. [Google Scholar] [CrossRef]

- Bailey, G.; Mancheri, N.; Acker, K.V. Sustainability of Permanent Rare Earth Magnet Motors in (H)EV Industry. J. Sustain. Metall. 2017, 3, 611–626. [Google Scholar] [CrossRef]

- Mancheri, N.; Sundaresan, L.; Chandrashekar, S. Dominating the World China and the Rare Earth Industry; National Institute of Advanced Studies: Bengaluru, India, 2013. [Google Scholar]

- Hurst, C. China’s Rare Earth Elements Industry: What Can the West Learn? Institute for the Analysis of Global Security: Washington, DC, USA, 2010. [Google Scholar]

- Humphries, M. Rare Earth Elements: The Global Supply Chain; Congressional Research Service: Washington, DC, USA, 2013.

- Mancheri, N.A.; Marukawa, T. Rare Earth Elements China and Japan in Industry, Trade and Value Chain; Institute of Social Science, University of Tokyo: Tokyo, Japan, 2016. [Google Scholar]

- Sahebalzamani, S.; Bertella, G. Business models and sustainability in nature tourism: A systematic review of the literature. Sustainability 2018, 10, 3226. [Google Scholar] [CrossRef]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G. PRISMA Group. Preferred reporting items for systematic reviews and meta-analyses: The PRISMA statement. PLoS Med. 2009, 6, e1000097. [Google Scholar] [CrossRef] [PubMed]

- Moher, D.; Shamseer, L.; Clarke, M.; Ghersi, D.; Liberati, A.; Petticrew, M.; Shekelle, P.; Stewart, L.A. Preferred reporting items for systematic review and metaanalysis protocols (PRISMA-P) 2015 statement. Syst. Rev. 2015, 4, 1. [Google Scholar] [CrossRef] [PubMed]

- Cook, D.J.; Mulrow, C.D.; Haynes, R.B. Systematic reviews: Synthesis of best evidence for clinical decisions. Ann. Intern. Med. 1997, 126, 376–380. [Google Scholar] [CrossRef] [PubMed]

- Gimenez, E.; Salinas, M.; Manzano-Agugliaro, F. Worldwide research on plant defense against biotic stresses as improvement for sustainable agriculture. Sustainability 2018, 10, 391. [Google Scholar] [CrossRef]

- Rodrigues, M.; Mendes, L. Mapping of the literature on social responsibility in the mining industry: A systematic literature review. J. Clean. Prod. 2018, 181, 88–101. [Google Scholar] [CrossRef]

- Hou, W.; Liu, H.; Wang, H.; Wu, F. Structure and patterns of the international rare earths trade: A complex network analysis. Resour. Policy 2018, 55, 133–142. [Google Scholar] [CrossRef]

- Nieto, A.; Guelly, K.; Kleit, A. Addressing criticality for rare earth elements in petroleum refining: The key supply factors approach. Resour. Policy 2013, 38, 496–503. [Google Scholar] [CrossRef]

- Vikström, H. The Extractive Industries and Society Is There a Supply Crisis? Sweden’s Critical Metals, 1917–2014. Extr. Ind. Soc. 2018, 5, 393–403. [Google Scholar]

- Jasiński, D.; Cinelli, M.; Dias, L.C.; Meredith, J.; Kirwan, K. Assessing supply risks for non-fossil mineral resources via multi-criteria decision analysis. Resour. Policy 2018, 58, 150–158. [Google Scholar] [CrossRef]

- Rabe, W.; Kostka, G.; Smith Stegen, K. China’s supply of critical raw materials: Risks for Europe’s solar and wind industries? Energy Policy 2017, 101, 692–699. [Google Scholar] [CrossRef]

- Valero, A.; Valero, A.; Calvo, G.; Ortego, A. Material bottlenecks in the future development of green technologies. Renew. Sustain. Energy Rev. 2018, 93, 178–200. [Google Scholar] [CrossRef]

- Golev, A.; Scott, M.; Erskine, P.D.; Ali, S.H.; Ballantyne, G.R. Rare earths supply chains: Current status, constraints and opportunities. Resour. Policy 2014, 41, 52–59. [Google Scholar] [CrossRef]

- Sprecher, B.; Daigo, I.; Murakami, S.; Kleijn, R.; Vos, M.; Kramer, G.J. Framework for Resilience in Material Supply Chains, With a Case Study from the 2010 Rare Earth Crisis. Environ. Sci. Technol. 2015, 49, 6740–6750. [Google Scholar] [CrossRef] [PubMed]

- Wang, X.; Lei, Y.; Ge, J.; Wu, S. Production forecast of China’s rare earths based on the generalized Weng model and policy recommendations. Resour. Policy 2015, 43, 11–18. [Google Scholar] [CrossRef]

- Ge, J.L.; Lei, Y.; Zhao, L. China’s Rare Earths Supply Forecast in 2025: A Dynamic Computable General Equilibrium Analysis. Minerals 2016, 6, 95. [Google Scholar] [CrossRef]

- He, C.; Lei, Y. Potential Impact of U.S. Re-Emerging Rare Earths Industry on Future Global Supply and Demand Trend. Int. Bus. Res. 2013, 6, 44–50. [Google Scholar] [CrossRef]

- Wang, X.; Ge, J.; Li, J.; Han, A. Market impacts of environmental regulations on the production of rare earths: A computable general equilibrium analysis for China. J. Clean. Prod. 2017, 154, 614–620. [Google Scholar] [CrossRef]

- Tiess, G. Minerals policy in Europe: Some recent developments. Resour. Policy 2010, 35, 190–198. [Google Scholar] [CrossRef]

- Seo, Y.; Morimoto, S. Comparison of dysprosium security strategies in Japan for 2010–2030. Resour. Policy 2014, 39, 15–20. [Google Scholar] [CrossRef]

- Machacek, E.; Kalvig, P. Assessing advanced rare earth element-bearing deposits for industrial demand in the EU. Resour. Policy 2016, 49, 186–203. [Google Scholar] [CrossRef]

- Jamaludin, H.; Lahiri-dutt, K. Could Lynas make a difference in the global political economy of Rare Earth Elements in future? Resour. Policy 2017, 53, 267–273. [Google Scholar] [CrossRef]

- Barteková, E.; Kemp, R. National strategies for securing a stable supply of rare earths in different world regions. Resour. Policy 2016, 49, 153–164. [Google Scholar] [CrossRef]

- Alonso, E.; Sherman, A.M.; Wallington, T.J.; Everson, M.P.; Field, F.R.; Roth, R.; Kirchain, R.E. Evaluating rare earth element availability: A case with revolutionary demand from clean technologies. Environ. Sci. Technol. 2012, 46, 3406–3414. [Google Scholar] [CrossRef] [PubMed]

- Goodenough, K.M.; Wall, F.; Merriman, D. The rare earth elements: Demand, global resources, and challenges for resourcing future generations. Nat. Resour. Res. 2018, 27, 201–216. [Google Scholar] [CrossRef]

- Dutta, T.; Kim, K.; Uchimiya, M.; Kwon, E.E.; Jeon, B.; Deep, A.; Yun, S. Global demand for rare earth resources and strategies for green mining. Environ. Res. 2016, 150, 182–190. [Google Scholar] [CrossRef] [PubMed]

- Chen, Z. Global rare earth resources and scenarios of future rare earth industry. J. Rare Earths 2011, 29, 1–6. [Google Scholar] [CrossRef]

- Yang, B.; Zhang, X. Forecast of price of rare earths neodymium oxide and dysprosium oxide based on ARIMA time series model. J. Chin. Rare. Earth Soc. 2017, 5, 680–686. (In Chinese) [Google Scholar]

- Riesgo, G.M.V.; Krzemień, A.; Manzanedo, D.C.M.Á.; Menéndez, Á.M.; Gent, M.R. Rare earth elements mining investment: It is not all about China. Resour. Policy 2017, 53, 66–76. [Google Scholar] [CrossRef]

- Riesgo, G.M.V.; Krzemie, A.; Ángel, M.; García-miranda, C.E.; Sánchez, F. Rare earth elements price forecasting by means of transgenic time series developed with ARIMA models. Resour. Policy 2018, 59, 95–102. [Google Scholar] [CrossRef]

- Yang, B.; Zhang, X. Periodic analysis of fluctuations in rare earth oxide prices—Based on X12 seasonal adjust method and H-P filter model. J. Chin. Rare Earth Soc. 2016, 3, 354–362. (In Chinese) [Google Scholar]

- Song, W.; Li, G.; Han, X. Missed pricing power over rare earth: Theoretical mechanism and system explanation. Chin. Ind. Econ. 2011, 10, 46–55. (In Chinese) [Google Scholar]

- Yu, Z.; Yi, F. Analysis on Formation on mechanism of lack of China’s pricing power on rare earth export. Financ. Trade Econ. 2013, 5, 97–104. (In Chinese) [Google Scholar]

- Liao, Z.; Liu, K. Analysis on international pricing role of Chinese rare earth. Int. Bus. 2011, 3, 59–66. (In Chinese) [Google Scholar]

- Fang, J.; Song, Y. Analysis on China’s market power in rare metal export markets: Case study on tungsten and rare earth. J. Int. Trade 2011, 1, 3–11. (In Chinese) [Google Scholar]

- Goldenberg, P.K.; Knetter, M.M. Measuring the Intensity of Competition in Export Markets. J. Int. Econ. 1999, 47, 27–60. [Google Scholar] [CrossRef]

- Sun, Z.; Jiang, S. Empirical study on the market power of China rare earth export. J. Int. Trade 2009, 4, 31–37. (In Chinese) [Google Scholar]

- Yu, W.; Wang, Z. An empirical analysis of China’s international pricing status in rare earth trade. Int. Econ. Trade Res. 2014, 5, 49–61. (In Chinese) [Google Scholar]

- Zhu, X.; Zhang, H.; Li, X. Measurement of the international market power of China’s rare earth and the effectiveness of policy. J. Int. Trade 2018, 1, 32–44. (In Chinese) [Google Scholar]

- Deng, W. International experiences in contending for commodity pricing power and their enlightenment to China rare earth. Int. Econ. Trade Res. 2011, 1, 30–34. (In Chinese) [Google Scholar]

- Zhang, L.; Guo, Q.; Zhang, J.; Huang, Y.; Xiong, T. Did China’s rare earth export policies work?—Empirical evidence. Resour. Policy 2015, 43, 82–90. [Google Scholar] [CrossRef]

- He, H.; Feng, M. An empirical study of the evaluation for China’s rare earth exporting. World Econ. Stud. 2017, 11, 88–99. (In Chinese) [Google Scholar]

- Packey, D.J.; Kingsnorth, D. The impact of unregulated ionic clay rare earth mining in China. Resour. Policy 2016, 48, 112–116. [Google Scholar] [CrossRef]

- Biedermann, R.P. China’s rare earth sector—Between domestic consolidation and global hegemony. Int. J. Emerg. Mark. 2014, 9, 276–293. [Google Scholar] [CrossRef]

- Brown, M.; Eggert, R. Simulating producer responses to selected Chinese rare earth policies. Resour. Policy 2018, 55, 31–48. [Google Scholar] [CrossRef]

- Wübbeke, J. Rare earth elements in China: Policies and narratives of reinventing an industry. Resour. Policy 2013, 38, 1–11. [Google Scholar] [CrossRef]

- Mancheri, N.A.; Sprecher, B.; Bailey, G.; Ge, J.; Tukker, A. Effect of Chinese policies on rare earth supply chain resilience. Resour. Conserv. Recycl. 2019, 142, 101–112. [Google Scholar] [CrossRef]

- Du, F.; Wang, Y.; Lu, B. Rare earth export regulation: Theoretical analysis and empirical evidence. Chin. Rare Earth 2014, 35, 112–118. [Google Scholar]

- Wan, R.; Wen, J.F. The Environmental Conundrum of Rare Earth Elements. Environ. Resour. Econ. 2017, 67, 157–180. [Google Scholar] [CrossRef]

- Ge, J.; Lei, Y. Resource tax on rare earths in China: Policy evolution and market responses. Resour. Policy 2018, 59, 291–297. [Google Scholar] [CrossRef]

- Yang, L.; Cai, L. Research on the influence of rare earth resource tax on rare earth price from system dynamic perspective. Chin. Rare Earths 2016, 5, 152–158. (In Chinese) [Google Scholar]

- Proelss, J.; Schweizer, D.; Seiler, V. Do announcements of WTO dispute resolution cases matter? Evidence from the rare earth elements market. Energy Econ. 2018, 73, 1–23. [Google Scholar] [CrossRef]

- Pan, A.; Wei, L. Effect of institutional distance on China’s export of rare earth: Data analysis of 18 countries and regions’ trade based on the gravity model. J. Int. Trad. 2013, 4, 96–104. (In Chinese) [Google Scholar]

- Wei, L.; Pan, A. Institutions, export potentials and rare earths trade friction: An empirical analysis based on the trade gravity model. World Econ. Stud. 2014, 10, 61–65. (In Chinese) [Google Scholar]

- Mancheri, N.A. World trade in rare earths, Chinese export restrictions, and implications. Resour. Policy 2015, 46, 262–271. [Google Scholar] [CrossRef]

- Ge, J.; Wang, X.; Guan, Q.; Li, W.; Zhu, H.; Yao, M. World rare earths trade network: Patterns, relations and role characteristics. Resour. Policy 2016, 50, 119–130. [Google Scholar] [CrossRef]

- Li, Z.; Zhou, B.; Zhao, Y. Analysis on the world’s future rare earths supply and demand situation and recommendations. Chin. Rare Earth 2016, 37, 153–158. [Google Scholar]

- Dutta, A.; Bouri, E.; Noor, M.H. Return and volatility linkages between CO2 emission and clean energy stock prices. Energy 2018, 164, 803–810. [Google Scholar] [CrossRef]

- Binnemans, K.; Jones, P.T.; Müller, T.; Yurramendi, L. Rare Earths and the Balance Problem: How to Deal with Changing Markets? J. Sustain. Metall. 2018, 4, 126–146. [Google Scholar] [CrossRef] [Green Version]

- Zhou, B.; Li, Z.; Zhao, Y.; Zhang, C.; Wei, Y. Rare Earth Elements supply vs. clean energy technologies: New problems to be solve. Gospod. Surowcami Miner. 2016, 32, 29–44. [Google Scholar] [CrossRef]

- Zhou, B.; Li, Z.; Chen, C. Global Potential of Rare Earth Resources and Rare Earth Demand from Clean Technologies. Minerals 2017, 7, 203. [Google Scholar] [CrossRef]

- Stegen, K.S. Heavy rare earths, permanent magnets, and renewable energies: An imminent crisis. Energy Policy 2015, 79, 1–8. [Google Scholar] [CrossRef]

- Habib, K.; Wenzel, H. Exploring rare earths supply constraints for the emerging clean energy technologies and the role of recycling. J. Clean. Prod. 2014, 84, 348–359. [Google Scholar] [CrossRef]

- Zhang, K.; Kleit, A.N.; Nieto, A. An economics strategy for criticality—Application to rare earth element Yttrium in new lighting technology and its sustainable availability. Renew. Sustain. Energy Rev. 2017, 77, 899–915. [Google Scholar] [CrossRef]

- Apergis, E.; Apergis, N. The role of rare earth prices in renewable energy consumption: The actual driver for a renewable energy world. Energy Econ. 2017, 62, 33–42. [Google Scholar] [CrossRef]

- Baldi, L.; Peri, M.; Vandone, D. Clean energy industries and rare earth materials: Economic and financial issues. Energy Policy 2014, 66, 53–61. [Google Scholar] [CrossRef] [Green Version]

- Tkaczyk, A.H.; Bartl, A.; Amato, A.; Lapkovskis, V.; Petranikova, M. Sustainability evaluation of essential critical raw materials: Cobalt, niobium, tungsten and rare earth elements. J. Phys. D Appl. Phys. 2018, 51, 203001. [Google Scholar] [CrossRef]

- Schlinkert, D.; Gerald, K.; Boogaart, V.D. The development of the market for rare earth elements: Insights from economic theory. Resour. Policy 2015, 46, 272–280. [Google Scholar] [CrossRef]

- Zhü, K.; Zhao, S.; Yang, S.; Liang, C.; Gu, D. Where is the way for rare earth industry of China: An analysis via ANP-SWOT approach. Resour. Policy 2016, 49, 349–357. [Google Scholar] [CrossRef]

- Charalampides, G.; Vatalis, K.I.; Apostoplos, B.; Ploutarch-Nikolas, B. Rare Earth Elements: Industrial Applications and Economic Dependency of Europe. Procedia Econ. Financ. 2015, 24, 126–135. [Google Scholar] [CrossRef] [Green Version]

- Rollat, A.; Guyonnet, D.; Planchon, M.; Tuduri, J. Prospective analysis of the flows of certain rare earths in Europe at the 2020 horizon. Waste Manag. 2016, 49, 427–436. [Google Scholar] [CrossRef] [PubMed]

- Machacek, E.; Fold, N. Alternative value chains for rare earths: The Anglo-deposit developers. Resour. Policy 2014, 42, 53–64. [Google Scholar] [CrossRef]

- Pavel, C.C.; Lacal-Arántegui, R.; Marmier, A.; Schüler, D.; Tzimas, E.; Buchert, M.; Jenseit, W.; Blagoeva, D. Substitution strategies for reducing the use of rare earths in wind turbines. Resour. Policy 2017, 52, 349–357. [Google Scholar] [CrossRef]

- Silva, G.A.; Petter, C.O.; Albuquerque, N.R. Factors and competitiveness analysis in rare earth mining, new methodology: Case study from Brazil. Heliyon 2018, 4, e00570. [Google Scholar] [CrossRef] [PubMed]

- Ali, S.H.; Giurco, D.; Arndt, N.; Nickless, E.; Brown, G.; Demetriades, A.; Durrheim, R.; Enriquez, M.A.; Kinnaird, J.; Littleboy, A.; et al. Mineral supply for sustainable development requires resource governance. Nature 2017, 543. [Google Scholar] [CrossRef] [PubMed]

- Henckens, M.L.C.M.; Driessen, P.P.J.; Worrell, E. Metal scarcity and sustainability, analyzing the necessity to reduce the extraction of scarce metals. Resour. Conserv. Recycl. 2014, 93, 1–8. [Google Scholar] [CrossRef]

- De Koning, A.; Kleijn, R.; Huppes, G.; Sprecher, B.; Engelen, G.V.; Tukker, A. Metal supply constraints for a low-carbon economy? Resour. Conserv. Recycl. 2018, 129, 202–208. [Google Scholar] [CrossRef]

- Fernandez, V. Rare-earth elements market: A historical and financial perspective. Resour. Policy 2017, 53, 26–45. [Google Scholar] [CrossRef]

- Klossek, P.; Kullik, J.; Boogaart, K.G. Van Den A systemic approach to the problems of the rare earth market. Resour. Policy 2016, 50, 131–140. [Google Scholar] [CrossRef]

- Lee, H.; Nunez, M.; Cruz, J. Competition for limited critical resources and the adoption of environmentally sustainable strategies. Eur. J. Oper. Res. 2018, 264, 1130–1143. [Google Scholar] [CrossRef]

- Jin, H.; Yih, Y.; Sutherland, J.W. Modeling operation and inventory for rare earth permanent magnet recovery under supply and demand uncertainties. J. Manuf. Syst. 2018, 46, 59–66. [Google Scholar] [CrossRef]

- McLellan, B.; Corder, G.; Ali, S. Sustainability of Rare Earths—An Overview of the State of Knowledge. Minerals 2013, 3, 304–317. [Google Scholar] [CrossRef] [Green Version]

- Brunner, P.; Rechberger, H. Practical Handbook of Material Flow Analysis; Lewis Publishers: Boca Raton, FL, USA, 2004. [Google Scholar]

- Guyonnet, D.; Planchon, M.; Rollat, A.; Escalon, V. Material flow analysis applied to rare earth elements in Europe. J. Clean. Prod. 2015, 107, 215–228. [Google Scholar] [CrossRef] [Green Version]

- Chen, W.; Nie, Z.; Wang, Z.; Gong, X.; Sun, B.; Gao, F.; Liu, Y. Substance flow analysis of neodymium based on the generalized entropy in China. Resour. Conserv. Recycl. 2018, 133, 438–443. [Google Scholar] [CrossRef]

- Wang, X.; Wei, W.; Ge, J.; Wu, B.; Bu, W.; Li, J.; Yao, M. Embodied rare earths flow between industrial sectors in China: A complex network approach. Resour. Conserv. Recycl. 2017, 125, 363–374. [Google Scholar] [CrossRef]

- Lee, I.S.; Kim, J.G. Industrial demand and integrated material flow of terbium in Korea. Int. J. Precis. Eng. Manuf. Green Technol. 2014, 1, 145–152. [Google Scholar] [CrossRef] [Green Version]

- Swain, B.; Kang, L.; Mishra, C.; Ahn, J.; Seon, H. Materials flow analysis of neodymium, status of rare earth metal in the Republic of Korea. Waste Manag. 2015, 45, 351–360. [Google Scholar] [CrossRef] [PubMed]

- Shigetomi, Y.; Nansai, K.; Kagawa, S.; Kondo, Y.; Tohno, S. Economic and social determinants of global physical flows of critical metals. Resour. Policy 2017, 52, 107–113. [Google Scholar] [CrossRef]

- Peiró, T.L.; Méndez, G.V.; Ayres, R.U. Material flow analysis of scarce metals: Sources, functions, end-uses and aspects for future supply. Environ. Sci. Technol. 2013, 47, 2939–2947. [Google Scholar] [CrossRef] [PubMed]

- Nansai, K.; Nakajima, K.; Kagawa, S.; Kondo, Y.; Shigetomi, Y.; Suh, S. Global mining risk footprint of critical metals necessary for low-carbon technologies: The case of neodymium, cobalt, and platinum in Japan. Environ. Sci. Technol. 2015, 49, 2022–2031. [Google Scholar] [CrossRef] [PubMed]

- Yu, F.; Wang, X.; Ma, G.; Wang, Z. Analysis of changes of production and emission of three wastes pollutants and evaluation of environment cost of rare earth refining in Baotou from 2000 to 2013. J. Chin. Rare. Earth Soc. 2017, 35, 537–545. [Google Scholar]

- Ma, G.; Zhu, W.; Wang, X.; Zhou, X.; Yu, F. Evaluation of ecological and environmental cost of rare earth resource exploitation in China from 2001 to 2013. J. Nat. Resour. 2016, 32, 1087–1099. [Google Scholar]

- Rau, H.; Goggins, G.; Fahy, F. From invisibility to impact: Recognizing the scientific and societal relevance of interdisciplinary sustainability research. Res. Policy 2018, 47, 266–276. [Google Scholar] [CrossRef]

- Tröster, R.; Hiete, M. Success of voluntary sustainability certification schemes—A comprehensive review. J. Clean. Prod. 2018, 196, 1034–1043. [Google Scholar] [CrossRef]

- Binnemans, K.; Jones, P.T. Rare Earths and the Balance Problem. J. Sustain. Metall. 2015, 1, 29–38. [Google Scholar] [CrossRef] [Green Version]

- Binnemans, K.; Jones, P.T.; Van Acker, K.; Blanpain, B.; Mishra, B.; Apelian, D. Rare-earth economics: The balance problem. JOM 2013, 65, 846–848. [Google Scholar] [CrossRef]

- Li, Z.; Lin, L.; Zhang, A. The progress in research on rare earth pricing. Chin. Rare Earths 2016, 37, 145–150. [Google Scholar]

- Tengku Ismail, T.H.; Juahir, H.; Aris, A.Z.; Zain, S.; Abu Samah, A. Local community acceptance of the rare earth industry: The case of the Lynas Advanced Materials Plant (LAMP) in Malaysia. Environ. Dev. Sustain. 2016, 18, 739–762. [Google Scholar] [CrossRef]

- Iyer, A.V.; Vedantam, A. A Market Model for Evaluating Technologies That Impact Critical-Material Intensity. JOM 2016, 68, 1957–1963. [Google Scholar] [CrossRef]

- Keilhacker, M.L.; Minner, S. Supply chain risk management for critical commodities: A system dynamics model for the case of the rare earth elements. Resour. Conserv. Recycl. 2017, 125, 349–362. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Field | Function | Main Productions | REEs | |

|---|---|---|---|---|

| Traditional applications | Metallurgy, Machinery | Alter chemical and physical properties, improve performance | Superalloys, steel aluminum magnets | La, Ce, Pr, Nd, Y |

| Petrochemical industry | Catalyst | Petroleum refining, catalytic converts | La, Ce, Pr, Nd | |

| Glass, Ceramic | Polishing, decoloration, additive, colorant | Capacitors, sensors, colorants, scintillators, refractories | La, Ce, Pr, Nd, Y, Eu, Gd, Lu, Dy | |

| New applications | Clean energy | Improve performance and property | Motors, wind Turbines, NiMH batteries | Nd, Pr, Tb, Dy |

| Nuclear | Improve performance | Water treatment | Eu, Gd, Ce, Y | |

| Journal | Number | Percentage |

|---|---|---|

| Resources Policy | 27 | 32% |

| Energy Policy | 3 | 3% |

| Resources, Conservation, & Recycling | 6 | 7% |

| The Journal of The Minerals, Metals, & Materials Society | 4 | 5% |

| Journal of Cleaner Production | 4 | 5% |

| Others | 39 | 48% |

| Model | Scope | Advantages | Limitations |

|---|---|---|---|

| ARIMA Model | Widely applied in bond, economics, medicine, the forecast of supply and demand of mineral resources | Suitable for non-stationary time series, stable, high accuracy of the forecast | Unable to respond immediately, with a certain lag |

| Logistic Model | Forecast of population, economics, energy supply | Widely application, high accuracy, suitable for fewer variables, fewer data and longer prediction cycle | Limited use for short forecast and the modification value is hard to verify |

| Hubbert Model | Mostly applied for the forecast of petroleum | Based on life cycle theory, fewer variables required, mature for the forecast of petroleum | Excessive reliance on historical data |

| BP Neural Network Model | Widely applied in various professions | High accuracy, strong robustness and fault tolerance, fast calculation | Base on Matlab software and experience |

| System Dynamics Model | Widely applied in economics, environment, military, and national defense | Suitable for complex time-varying systems with high order terms, non-linear and multiple feedback | Need large data, complex, large work |

| Generalized Weng Model | Mostly applied for the forecast of supply and demand of exhaustible resources petroleum | Based on life cycle theory, fewer variables, especially suitable for the field of petroleum forecast | Sensitive to the selection of data |

| 2009–2011 REE oxide (FOB price) | Average Price Increase | Price Increase Difference | |

|---|---|---|---|

| Rest of World | China | ||

| Lanthanum oxide | 2133.20% | 531.37% | 401.45% |

| Cerium oxide | 2628.87% | 919.25% | 285.98% |

| Neodymium oxide | 1225.94% | 1132.59% | 108.24% |

| Praseodymium oxide | 1094.29% | 919.16% | 119.05% |

| Samarium oxide | 3041.18% | 578.05% | 526.11% |

| Dysprosium oxide | 1253.39% | 1239.19% | 101.15% |

| Europium oxide | 576.75% | 575.69% | 100.18% |

| Terbium oxide | 645.39% | 629.66% | 102.50% |

| Year | China’s Rare Earth Policy |

|---|---|

| 1985 | Implemented the export tax rebate policy for rare earth products |

| 1998 | Implemented the export quota and license system for rare earth products; rare earth raw materials were included in the catalog of prohibited trade commodities |

| 2005 | Canceled tax rebates on exports of rare earth metals and rare earth oxides; the export quota was 65,609 tons |

| 2006 | Imposed 10% export tariff on rare earth metals and rare earth oxides; qualified exporters of rare earth products were cut from 47 to 39 |

| 2009 | Export quotas for general trade fell by 3% year on year, export quotas for foreign companies fell 21% year-on-year, the export quota was 50,145 tons |

| 2010 | Qualified exporters of rare earth products are 32, the export tariff on rare earth metallic ore retained 15%, the export tariff on Nd improved from 15% to 25%, the export tariff on other rare earth oxides retained 15% |

| 2015 | Canceled the export quota and export tariff and began to enforce the export license on rare earths |

| Country | Company | Mine | Planned Annual Production/Thousand Ton | TREO (Total Rare Earth Oxide) /Thousand Ton | Current Status |

|---|---|---|---|---|---|

| America | Molycorp | Mountain Pass | —— | 2072 | Filed for bankruptcy in 2015 |

| America | Rare Element Resources | Bear Lodge | 10 | 1553 | Put into production in 2018 |

| Australia | Lynas | Mount Weld | 22 | 1889 | Put into production in 2012 |

| Australia | Arafura Resources | Nolans | 20 | 1236 | Planned to be put into production in 2019 |

| Australia | Alkane Resources | Dubbo Zirconia Project | 4.9 | 651 | Put into production in 2017 |

| South Africa | Frontier Rare Earths | Zandkopsdrift | —— | 948 | The assessment was completed in 2015. The production capacity of the first stage was 8000 tons, and the fifth year was 16,000 tons |

| Korea Resources | —— | ||||

| Tanzania | Peak Resources | Ngualla | 10 | 1748 | The feasibility study was completed in 2014 |

| Brazil | MBAC Fertilizer | Araxá | —— | 1190 | The first stage was 8,750 tons, and the fifth year was 17,500 tons |

| Canada | Commerce Resources | Ashram | 27 | 4700 | Put into production in 2015 |

| Canada | Quest Rare Minerals | Strange Lake | 12 | 4406 | The preliminary evaluation was completed in 2014 |

| Kenya | Pacific Wildcat Resources | Mrima Hill | —— | 6145 | Completed economic evaluation in 2013 |

| Greenland | Greenland Mineralsand Energy | Kvanefjeld | 7 | 7369 | An environmental assessment was carried out in 2015 |

| Rare Ear th Element | Main CRITICALITY (Large Volume) Applications at Present | Level (2014) |

|---|---|---|

| Neodymium (Nd) | Nd–Fe–B permanent magnets | High |

| Europium (Eu) | Y2O3: Eu3+lamp phosphor | High |

| Terbium (Tb) | Green lamp phosphor LaPO4: Ce3+, Tb3+ (LAP)) | Very high |

| Dysprosium (Dy) | Additive in Nd–Fe–B permanent magnets | Highest |

| Yttrium (Y) | Red lamp phosphor Y2O3: Eu3+, yttria-stabilized zirconia (YSZ), and ceramics | High |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, Y.; Zheng, B. What Happens after the Rare Earth Crisis: A Systematic Literature Review. Sustainability 2019, 11, 1288. https://doi.org/10.3390/su11051288

Chen Y, Zheng B. What Happens after the Rare Earth Crisis: A Systematic Literature Review. Sustainability. 2019; 11(5):1288. https://doi.org/10.3390/su11051288

Chicago/Turabian StyleChen, Yufeng, and Biao Zheng. 2019. "What Happens after the Rare Earth Crisis: A Systematic Literature Review" Sustainability 11, no. 5: 1288. https://doi.org/10.3390/su11051288

APA StyleChen, Y., & Zheng, B. (2019). What Happens after the Rare Earth Crisis: A Systematic Literature Review. Sustainability, 11(5), 1288. https://doi.org/10.3390/su11051288