Measuring Technical Efficiency and Returns to Scale in Taiwan’s Baking Industry―A Case Study of the 85 °C Company

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

3.1. Study Enterprise: 85 °C

- (1)

- The signboard was the same, but the product and price were not, causing confusion among consumers.

- (2)

- Consumers were willing to accept the newer decor and comfortable seating area, but not at a higher price.

- (3)

- Consumers stayed longer at the store, but the number of customers dropped significantly. The original take-away model disappeared greatly because the internal consumption model in addition to the increase in product unit price not only caused consumers more burden but also caused inconvenience to consumers.

- (4)

- The baking pattern was drastically changed: The cake production mode was changed from frozen to refrigerated, significantly increasing freshness and taste, but at the same time causing high loss. Afterwards, 85 °C reduced the display of items in order to avoid depletion, negatively affecting purchases and thus creating a dilemma.

- Since consumers liked the new decor but did not like the new price, they changed the new decor and sold old products and at the original price in order to retain old consumers and attract new consumers.

- Due to poor operation in the metropolitan market, 85 °C decided to focus on the township market, opening up large township stores and entering other small- and medium-sized towns. Low rents were characteristic of these new stores.

- The old products had a high preserving life, operation was convenient, attrition rate was low, and consumers were habitually willing to purchase. Therefore, product items and prices were restored, so that consumers could become more selective.

- In 2014, 85 °C had 51 direct-owned stores in Taiwan, compared with 39 in 2013 and 37 in 2012. There had been a significant increase in new stores, and it is also true that the II-generation stores incurred substantial losses, resulting in more than 5 million NTD losses in a single month in September 2014 alone. After adjusting the price model of the II-generation store, the number of customers and the turnover could not be increased. It was better to close such stores to reduce losses while focusing on the more promising stores.

3.2. The DEA Model

3.3. Data

3.4. Input–Output

- Total revenue of bread (y1), measured in units of thousand New Taiwan dollars (NT$).

- Total revenue of beverage (y2), measured in units of thousand New Taiwan dollars (NT$).

- Total revenue of pastry (y3), including incomes other than the two items mentioned above. They include cake sales, souvenir sales, snacking sales, and others, measured in units of thousand NT$.

- Total staff salaries (x1), including full-time employee salaries, pensions, labor premiums, healthcare expenses, and year-end bonuses, measured in units of New Taiwan dollars (NT$).

- Total dispatch employee salaries (x2), including part-time employee salaries, pensions, meals, labor premiums, healthcare expenses, and year-end bonuses, measured in units of New Taiwan dollars (NT$).

- Other expenses (x3), including rent expenses and others, measured in units of NT$.

3.5. Descriptive Statistics

4. Empirical Results

4.1. Efficiency Results

4.2. Efficiency of Different Operation Styles

4.3. Further Analysis

- Return on assets (ROA) is a widely used measure for profitability and is frequently used as a measure for corporate performance [34]. ROA represents the short-term financial performance of a firm by measuring how a firm efficiently creates profits by using its assets during a fiscal year. It reflects the ability of the company’s management to produce profit from the company’s assets [35].

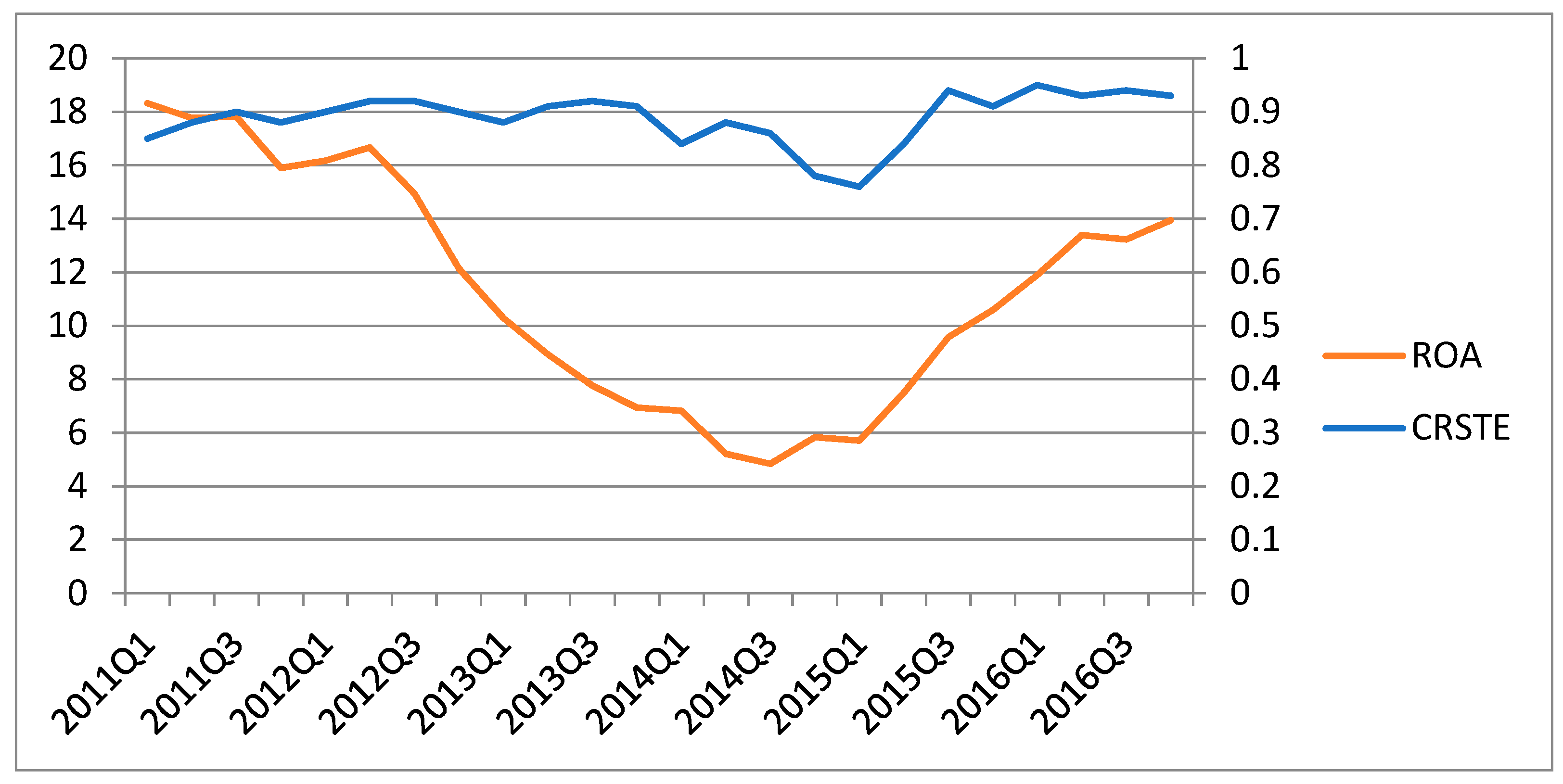

- Figure 2 below shows the trend of ROA and technical efficiency over the study period. The figure illustrates that ROA decreased from 2011 Q1 to 2014 Q3 and subsequently increased from 2014 Q4 to 2016 Q4. It also shows that, after 2013 Q4, there was a clear downward trend in technical efficiency, although there was a recent recovery in technical efficiency from 2015 Q2 onwards.

5. Conclusions, Limitations, and Future Research

Author Contributions

Funding

Conflicts of Interest

References

- ITIS Project of the Ministry of Economic Affairs. Food Industry. 2018. Available online: http://www.itis.org.tw/ (accessed on 30 September 2018).

- Mordor Intelligence Online. Bakery Products Market Analysis, Size—Segmented by Product Type (Cake, Biscuits, Bread, Pastries, Morning Goods), by Distribution Channel (Specialist Retailers, Retail Channel, Foodservice)—Growth, Trends and Forecasts (2018–2023). Available online: https://www.mordorintelligence.com/industry-reports/bakery-products-market (accessed on 12 October 2018).

- Directorate-General of Budget, Accounting and Statistics. 2018. Available online: https://www.dgbas.gov.tw/ct.asp?xItem=33338&ctNode=3099&mp=1 (accessed on 5 October 2018).

- Business Monitor Online (BMO). Available online: https://bmo.bmiresearch.com/search/results?all_words_kw=taiwan&kw=1 (accessed on 4 July 2018).

- Huang, S.W.; Kuo, H.F.; Hsieh, H.I.; Chen, T.H. Environmental efficiency evaluation of coastal tourism development in Taiwan. Int. J. Environ. Sci. Dev. 2016, 7, 145–150. [Google Scholar] [CrossRef]

- Su, C.S. An importance-performance analysis of dining attributes: A comparison of individual and packaged tourists in Taiwan. Asia Pac. J. Tour. Res. 2013, 18, 573–597. [Google Scholar] [CrossRef]

- Yin, P.; Tsai, H.; Wu, J. A hotel life cycle model based on bootstrap DEA efficiency: The case of international tourist hotels in Taipei. Int. J. Contemp. Hosp. Manag. 2015, 27, 918–937. [Google Scholar] [CrossRef]

- Chen, H.S.; Tsai, B.K.; Liou, G.B.; Hsieh, C.M. Efficiency assessment of inbound tourist service using data envelopment analysis. Sustainability 2018, 10, 1866. [Google Scholar] [CrossRef]

- Yang, X.L.; Zhang, Y.J.; Wang, L. An Empirical analysis of total factor productivity of the food processing industry in Jilin Province. J. Agrotech. Econ. 2012, 12, 61–67. [Google Scholar]

- Zhang, Z. Analysis of regional differences in the growth of TFP of China’s food industry. Spec. Zone Econ. 2014, 8, 102–104. [Google Scholar]

- Zhang, Z.; Wang, K. Scale competitiveness of food enterprises and TFP growth. Sci. Technol. Ind. 2014, 14, 83–88. [Google Scholar]

- Qiang, F.U.; Fang, J.I. Total factor productivity of food manufacturing industry in China: A DEA-Malmquist index measurement. Revista Facultad Ingeniería U.C.V. 2017, 32, 1–8. [Google Scholar]

- Dimara, E.; Skuras, D.; Tsekouras, K.; Tzelepis, D. Productive efficiency and firm exit in the food sector. Food Policy 2008, 33, 185–196. [Google Scholar] [CrossRef]

- Giokas, D.; Eriotis, N.; Dokas, I. Efficiency and productivity of the food and beverage listed firms in the pre-recession and recessionary periods in Greece. Appl. Econ. 2015, 47, 1927–1941. [Google Scholar] [CrossRef]

- Rezitis, A.N.; Kalantz, M.A. Investigating technical efficiency and its determinants by data envelopment analysis: An application in the Greek food and beverages manufacturing industry. Agribusiness 2016, 32, 254–271. [Google Scholar] [CrossRef]

- Kumar, M.; Basu, P. Perspectives of productivity growth in Indian food industry: A data envelopment analysis. Int. J. Product. Perform. Manag. 2008, 57, 503–522. [Google Scholar] [CrossRef]

- Ali, J.; Singh, S.P.; Ekanem, E. Efficiency and productivity changes in the Indian food processing industry: Determinants and policy implications. Int. Food Agribus. Manag. 2009, 12, 43–66. [Google Scholar]

- Kaur, N.; Kaur, K. Efficiency, productivity and profitability changes in the Indian food processing industry: A firm level analysis. Pac. Bus. Rev. Int. 2016, 1, 264–272. [Google Scholar]

- Mathur, R.; RAJU RAMNATH, S. Efficiency in food grains production in India using DEA and SFA. Cent. Eur. Rev. Econ. Manag. 2018, 2, 79–101. [Google Scholar] [CrossRef]

- Gregg, D.; Rolfe, J. Identifying sources and trends for productivity growth in a sample of Queensland broad-acre beef enterprises. Anim. Prod. Sci. 2011, 51, 443–453. [Google Scholar] [CrossRef]

- Setiawan, M.; Oude Lansink, A.G.J.M. Dynamic technical inefficiency and industrial concentration in the Indonesian food and beverages industry. Brit. Food J. 2018, 120, 108–119. [Google Scholar] [CrossRef]

- Holyk, S. Measuring technical efficiency and returns to scale in Finnish food processing industry. Int. J. Sci. Basic Appl. Res. 2016, 27, 226–238. [Google Scholar]

- Geylani, P.C.; Stefanou, S.E. Productivity growth patterns in U.S. dairy products manufacturing. Appl. Econ. 2011, 43, 3415–3432. [Google Scholar] [CrossRef]

- Rodmanee, S.; Huang, W. Efficiency evaluation of food and beverage companies in Thailand: An application of relational two-stage data envelopment analysis. Int. J. Soc. Sci. Humanit. 2013, 3, 202–205. [Google Scholar] [CrossRef]

- Kapelko, M.; Oude Lansink, A.; Stefanou, S.E. Analyzing the impact of investment spikes on dynamic productivity growth. Omega 2015, 54, 116–124. [Google Scholar] [CrossRef]

- Kapelko, M.; Oude Lansink, A.; Stefanou, S.E. Investment age and dynamic productivity growth in the Spanish food processing industry. Am. J. Agric. Econ. 2016, 98, 946–961. [Google Scholar] [CrossRef]

- Kapelko, M.; Oude Lansink, A.; Stefanou, S.E. The impact of 2008 financial crisis on dynamic productivity growth of the Spanish food manufacturing industry. Agric. Econ. 2017, 48, 561–571. [Google Scholar] [CrossRef]

- Kapelko, M. Measuring Productivity Change Accounting for Adjustment Costs: Evidence from the Food Industry in the European Union. 2018. Available online: https://link.springer.com/content/pdf/10.1007%2Fs10479-017-2497-0.pdf (accessed on 10 October 2018).

- Kapelko, M.; Oude Lansink, A.; Stefanou, S.E. Assessing the impact of changing economic environment on productivity growth: The case of the Spanish dairy processing industry. J. Food Prod. Mark. 2017, 23, 384–397. [Google Scholar] [CrossRef]

- Charnes, A.; Cooper, W.W.; Rhodes, E. Measuring the efficiency of decision making units. Eur. J. Oper. Res. 1978, 2, 429–444. [Google Scholar] [CrossRef]

- Banker, R.D.; Charnes, R.F.; Cooper, W.W. Some models for estimating technical and scale inefficiencies in data envelopment analysis. Manag. Sci. 1984, 30, 1078–1092. [Google Scholar] [CrossRef]

- Lin, W.B.; Chen, M.J.; Chen, I.C.; Lee, M.S. Applications of Multiple Criteria Decision Making to Sport Industry in Taiwan. 2007. Available online: http://www.shl.tpcu.edu.tw/ezfiles/24/1024/img/326/TSINT_J0109.pdf (accessed on 25 July 2018).

- Hu, J.L.; Shieh, H.S.; Huang, C.H.; Chiu, C.N. Cost efficiency of international tourist hotels in Taiwan: A data envelopment analysis application. Asia Pac. J. Tour. Res. 2009, 371–384. [Google Scholar] [CrossRef]

- Gonzalez-Hermosillo, B.; Pazarbasioglu, C.; Billings, R. Determinants of banking system fragility: A case study of Mexico. Int. Fund Staff Papers 1997, 44, 295–314. [Google Scholar] [CrossRef]

- Athanasoglou, P.P.; Brissimis, S.N.; Delis, M.D. Bank-specific, industry specific and macroeconomic determinants of bank profitability. J. Int. Financ. Mark. I. 2008, 18, 121–136. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Operations Style | Variables | Maximum | Minimum | Mean | S.D. |

|---|---|---|---|---|---|

| I | Output variables—revenue | ||||

| Bread (y1) | 9,806,532 | 0 | 2,829,384.735 | 2,201,254.160 | |

| Beverage (y2) | 3,365,941 | 0 | 1,899,884.379 | 736,262.707 | |

| Pastry (y3) | 3,176,996 | 96,116 | 1,580,692.555 | 643,703.704 | |

| Input variables—expense | |||||

| Staff salaries (x1) | 2,012,653 | 27,498 | 871,838.460 | 393,104.394 | |

| Dispatch worker salaries (x2) | 1,157,097 | 38,689 | 510,256.900 | 212,175.683 | |

| Other (x3) | 2,112,191 | 107,800 | 622,851.179 | 297,344.485 | |

| II | Output variables—revenue | ||||

| Bread (y1) | 8,618,333 | 0 | 2,226,680.339 | 2,026,621.835 | |

| Beverage (y2) | 4,007,737 | 0 | 1,964,168.175 | 905,142.190 | |

| Pastry (y3) | 3,389,182 | 11,447 | 1,483,051.802 | 643,151.385 | |

| Input variables—expense | |||||

| Staff salaries (x1) | 1,139,929 | 0 | 429,153.530 | 236,176.381 | |

| Dispatch worker salaries (x2) | 1,579,306 | 236,080 | 648,520.262 | 287,154.476 | |

| Other (x3) | 8,618,333 | 0 | 2,226,680.339 | 2,026,621.835 | |

| III | Output variables—revenue | ||||

| Bread (y1) | 8,2362,550 | 0 | 2,681,863.928 | 2,029,316.981 | |

| Beverage (y2) | 47,649,690 | 101,350 | 2,584,906.344 | 953,350.434 | |

| Pastry (y3) | 51,179,870 | 2,792,470 | 1,762,731.636 | 739,134.595 | |

| Input variables—expense | |||||

| Staff salaries (x1) | 14,011,570 | 0 | 516,816.980 | 274,308.442 | |

| Dispatch worker salaries (x2) | 15,532,060 | 1,609,560 | 693,131.949 | 329,249.647 | |

| Other (x3) | 82,362,550 | 0 | 2,681,863.928 | 2,029,316.981 | |

| All | Output variables—revenue | ||||

| Bread (y1) | 36,006,569 | 0 | 11,106,338.10 | 8,421,408.766 | |

| Beverage (y2) | 18,142,279 | 0 | 8,522,733.43 | 3,473,095.698 | |

| Pastry (y3) | 13,032,914 | 229,506 | 6,555,242.44 | 2,504,370.179 | |

| Input variables—expense | |||||

| Staff salaries (x1) | 6,960,295 | 812,928 | 3,496,687.97 | 1,293,128.429 | |

| Dispatch worker salaries (x2) | 4,279,343 | 0 | 2,013,625.28 | 826,985.607 | |

| Other (x3) | 6,489,285 | 466,391 | 2,609,337.45 | 1,188,422.361 | |

| y1 | y2 | y3 | x1 | x2 | x3 | |

| y1, total bread revenue | 0.151 * | 0.501 ** | 0.565 ** | 0.697 ** | 0.760 ** | |

| y2, total beverage revenue | 0.473 ** | 0.644 ** | 0.337 ** | 0.428 ** | 0.381 ** | |

| y3, total others revenue | 0.622 ** | 0.182 ** | 0.461 ** | 0.665 ** | 0.680 ** | |

| x1, total staff salary | 0.628 ** | 0.698 ** | 0.357 ** | 0.407 ** | 0.478 ** | |

| x2, total dispatch worker salary | 0.480 ** | 0.608 ** | 0.387 ** | 0.512 ** | 0.636 ** | |

| x3, total other expenses | 0.629 ** | 0.701 ** | 0.392 ** | 0.643 ** | 0.407 ** |

| Year | Operations Style | Technical Efficiency (CCR index) | Pure Technical Efficiency (BCC index) | Scale Efficiency |

|---|---|---|---|---|

| 2011Q1 | I | 0.854 | 0.939 | 0.910 |

| 2011Q2 | I | 0.884 | 0.936 | 0.944 |

| 2011Q3 | I | 0.895 | 0.928 | 0.964 |

| 2011Q4 | I | 0.882 | 0.934 | 0.945 |

| 2012Q1 | I | 0.900 | 0.938 | 0.959 |

| 2012Q2 | I | 0.917 | 0.944 | 0.972 |

| 2012Q3 | I | 0.920 | 0.954 | 0.964 |

| 2012Q4 | I | 0.902 | 0.943 | 0.956 |

| 2013Q1 | I | 0.877 | 0.929 | 0.943 |

| 2013Q2 | I | 0.906 | 0.937 | 0.967 |

| 2013Q3 | I | 0.916 | 0.939 | 0.976 |

| 2013Q4 | II | 0.906 | 0.935 | 0.969 |

| 2014Q1 | II | 0.837 | 0.918 | 0.915 |

| 2014Q2 | II | 0.883 | 0.907 | 0.973 |

| 2014Q3 | II | 0.862 | 0.886 | 0.973 |

| 2014Q4 | II | 0.778 | 0.842 | 0.918 |

| 2015Q1 | II | 0.760 | 0.845 | 0.892 |

| 2015Q2 | II | 0.839 | 0.905 | 0.926 |

| 2015Q3 | III | 0.938 | 0.959 | 0.978 |

| 2015Q4 | III | 0.910 | 0.944 | 0.964 |

| 2016Q1 | III | 0.947 | 0.962 | 0.983 |

| 2016Q2 | III | 0.928 | 0.950 | 0.977 |

| 2016Q3 | III | 0.941 | 0.959 | 0.981 |

| 2016Q4 | III | 0.930 | 0.954 | 0.974 |

| All period Mean | 0.888 | 0.929 | 0.955 | |

| Standard deviation | 0.047 | 0.032 | 0.026 | |

| Operations Style | Technical Efficiency (TE) | Pure Technical Efficiency (PE) | Scale Efficiency (SE) | Sample Number | |||

|---|---|---|---|---|---|---|---|

| Average | R-mean | Average | R-mean | Average | R-mean | ||

| I | 0.896 | 12.23 | 0.938 | 13 | 0.955 | 10.55 | 11 |

| II | 0.838 | 5.64 | 0.891 | 4.43 | 0.938 | 9. | 7 |

| III | 0.932 | 21 | 0.955 | 21 | 0.976 | 20.17 | 6 |

| Kruskal–Wallis test (Z) | 15.276 | 17.877 | 9.630 | ||||

| Prob. > Z | < 0.001 | < 0.001 | 0.008 | ||||

| Dunn post-hoc test (Q) | III > I, II | II < I, III | III > I, II | ||||

| 2011 | 2012 | 2013 | ||||

| Count | Percent | Count | Percent | Count | Percent | |

| Efficient | 15 | 37.5 | 16 | 44.4 | 14 | 42.4 |

| Inefficient | 25 | 62.5 | 20 | 55.6 | 19 | 57.6 |

| CRS | 15 | 37.5 | 16 | 44.4 | 14 | 42.4 |

| IRS | 8 | 20.0 | 10 | 27.8 | 6 | 18.2 |

| DRS | 17 | 42.5 | 10 | 27.8 | 13 | 39.4 |

| 2014 | 2015 | 2016 | ||||

| Count | Percent | Count | Percent | Count | Percent | |

| Efficient | 17 | 48.6 | 15 | 48.4 | 18 | 56.25 |

| Inefficient | 18 | 51.4 | 16 | 51.6 | 14 | 43.75 |

| CRS | 17 | 48.6 | 15 | 48.4 | 18 | 56.25 |

| IRS | 9 | 25.7 | 6 | 19.4 | 6 | 18.75 |

| DRS | 9 | 25.7 | 10 | 32.2 | 8 | 25.00 |

| Years | CRS | IRS | DRS | Total of Self-Owned Stores | |||

|---|---|---|---|---|---|---|---|

| Count | Percent | Count | Percent | Count | Percent | ||

| Panel A: by year | |||||||

| 2011Q1 | 12 | 30.0 | 6 | 15.0 | 22 | 55.0 | 40 |

| 2011Q2 | 17 | 41.5 | 9 | 22.0 | 15 | 36.5 | 41 |

| 2011Q3 | 18 | 42.9 | 9 | 21.4 | 15 | 35.7 | 42 |

| 2011Q4 | 18 | 42.9 | 3 | 7.1 | 21 | 50.0 | 42 |

| 2012Q1 | 17 | 42.5 | 5 | 12.5 | 18 | 45.0 | 40 |

| 2012Q2 | 19 | 51.4 | 8 | 21.6 | 10 | 27.0 | 37 |

| 2012Q3 | 18 | 48.6 | 12 | 32.5 | 7 | 18.9 | 37 |

| 2012Q4 | 16 | 41.0 | 11 | 28.2 | 12 | 30.8 | 39 |

| 2013Q1 | 15 | 39.5 | 6 | 15.8 | 17 | 44.7 | 38 |

| 2013Q2 | 17 | 44.7 | 9 | 23.7 | 12 | 31.6 | 38 |

| 2013Q3 | 22 | 61.1 | 5 | 13.9 | 9 | 25.0 | 36 |

| 2013Q4 | 20 | 55.6 | 5 | 13.9 | 11 | 30.4 | 36 |

| 2014Q1 | 9 | 24.3 | 1 | 2.7 | 27 | 73.0 | 37 |

| 2014Q2 | 22 | 56.4 | 8 | 20.5 | 9 | 23.1 | 39 |

| 2014Q3 | 22 | 48.9 | 15 | 33.3 | 8 | 17.8 | 45 |

| 2014Q4 | 13 | 26.5 | 11 | 22.5 | 25 | 51.0 | 49 |

| 2015Q1 | 12 | 23.5 | 9 | 17.7 | 30 | 58.8 | 51 |

| 2015Q2 | 11 | 26.8 | 4 | 9.8 | 26 | 63.4 | 41 |

| 2015Q3 | 18 | 56.2 | 4 | 15.6 | 10 | 31.2 | 32 |

| 2015Q4 | 15 | 46.9 | 5 | 15.6 | 12 | 37.5 | 32 |

| 2016Q1 | 16 | 48.5 | 13 | 39.4 | 4 | 12.1 | 33 |

| 2016Q2 | 19 | 57.6 | 8 | 24.2 | 6 | 18.2 | 33 |

| 2016Q3 | 17 | 51.5 | 7 | 21.2 | 9 | 27.3 | 33 |

| 2016Q4 | 15 | 46.9 | 5 | 15.6 | 12 | 37.5 | 32 |

| Total | 398 | 43.1 | 178 | 19.3 | 347 | 37.6 | 923 |

| Panel B: by operations style | |||||||

| I | 189 | 44.0 | 83 | 19.3 | 158 | 36.7 | 430 |

| II | 109 | 36.6 | 53 | 17.8 | 136 | 45.6 | 298 |

| III | 100 | 51.3 | 42 | 21.5 | 53 | 27.2 | 195 |

| ROA | Technical Efficiency | |

|---|---|---|

| ROA | 1 | 9.423 * |

| Technical efficiency | 9.423 * | 1 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chang, C.-W.; Wu, K.-S.; Chang, B.-G.; Lou, K.-R. Measuring Technical Efficiency and Returns to Scale in Taiwan’s Baking Industry―A Case Study of the 85 °C Company. Sustainability 2019, 11, 1268. https://doi.org/10.3390/su11051268

Chang C-W, Wu K-S, Chang B-G, Lou K-R. Measuring Technical Efficiency and Returns to Scale in Taiwan’s Baking Industry―A Case Study of the 85 °C Company. Sustainability. 2019; 11(5):1268. https://doi.org/10.3390/su11051268

Chicago/Turabian StyleChang, Chieh-Wen, Kun-Shan Wu, Bao-Guang Chang, and Kuo-Ren Lou. 2019. "Measuring Technical Efficiency and Returns to Scale in Taiwan’s Baking Industry―A Case Study of the 85 °C Company" Sustainability 11, no. 5: 1268. https://doi.org/10.3390/su11051268

APA StyleChang, C.-W., Wu, K.-S., Chang, B.-G., & Lou, K.-R. (2019). Measuring Technical Efficiency and Returns to Scale in Taiwan’s Baking Industry―A Case Study of the 85 °C Company. Sustainability, 11(5), 1268. https://doi.org/10.3390/su11051268