The Concept of Risk Capital and Its Application in Non-Financial Companies: A Sustainable Dimension

Abstract

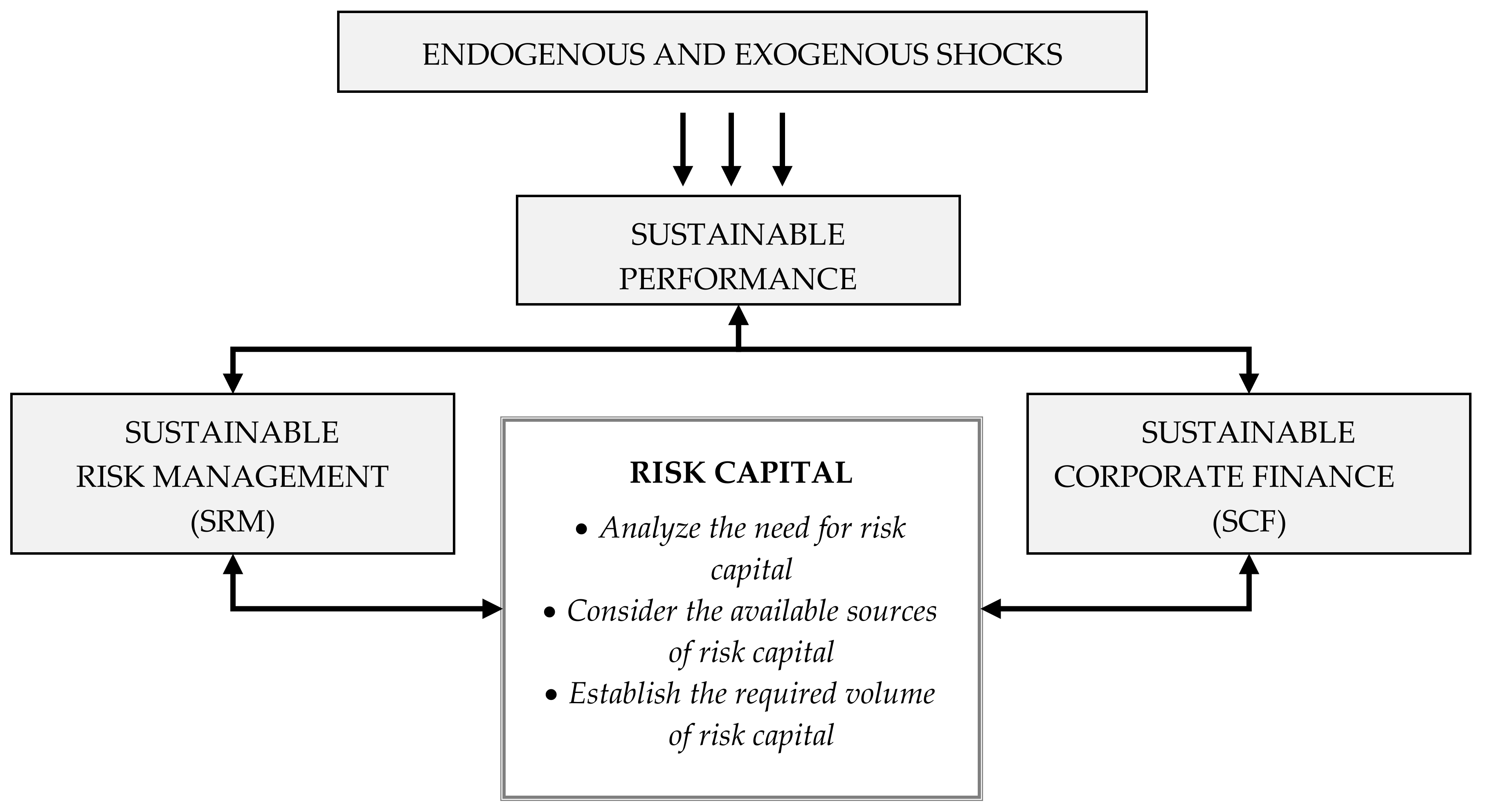

1. Introduction

2. The Concept of Risk Capital in A Non-Financial Company

2.1. The Origins of the Concept

2.2. The Need of Risk Capital: Risk Management Perspective

2.3. Sustainable Dimension of Risk Capital

3. Applicative Dimension: Sources of Risk Capital

3.1. General Considerations

3.2. Traditional Sources of Risk Capital

3.3. Alternative Sources of Risk Capital Available for Corporate End-Users—Brief Overview

- Insurance derivatives—the pay-off depends on the changes of a predefined risk index (that reflects the occurrence of risk); companies may implement the catastrophic derivatives (indices related to the cumulation of losses in the aftermath of a catastrophic event) or weather derivatives (indices capture extreme weather conditions);

- Catastrophic bonds—the coupon payment of the catastrophic bonds is determined by the changes of a defined catastrophic risk index; the issuer (a company) is allowed to reduce or release the payment of the coupon in the aftermath of the catastrophic risk (a detailed mechanism of the issuance of catastrophic bonds is presented in [83,89]) (The information on the issuance of corporate bonds by non-financial companies is obtainable in the ARTEMIS database [90]);

4. Conclusions and Final Remarks

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Traditional approach (derived from Modigliani-Miller substitution theory) [97,98] | where: —weighted average cost of capital, equity, —debt, —cost of equity, —after-tax cost of debt |

(P. Shimpi 2002; [12]) | where: T—total average cost of capital, equity,—debt,risk capital,—cost of equity, —after-tax cost of debt, —cost of risk capital |

(N.A. Doherty 2005; [13]) | and where: —weighted average cost of capital,equity, —debt,—operating capital, —risk capital,—cost of equity, —after-tax cost of debt |

(O’Brien 2006; [14]) | where: —weighted average cost of capital in terms of risk management, —operating capital, —risk capital, —cost of operating capital, —risk free rate (as the equivalent of the cost of risk capital) |

References

- Norman, W.; Mac Donald, C. Getting to the bottom line. Bus. Ethics Q. 2004, 14, 234–262. [Google Scholar] [CrossRef]

- Baker, H.K.; Nofsinger, J.R. Socially Responsible Finance and Investing: Financial Institutions, Corporations, Investors and Actions; Wiley: Hoboken, NJ, USA, 2012. [Google Scholar]

- Salzmann, A.J. The integration of sustainability into the theory and practice of finance: an overview of state of the art and the outline of future developments. J. Bus. Econ. 2013, 83, 555–576. [Google Scholar] [CrossRef]

- Lessen, J.; Dentchev, N.A.; Roger, L. Sustainability, risk management and governance: Towards an integrative approach. Corp. Gov. 2014, 14, 670–684. [Google Scholar] [CrossRef]

- Spedding, L.; Rose, A. Business Risk Management Handbook. A Sustainable Approach; CIMA Publishing/Elsevier: Burlington, UK, 2008; pp. 17–28. [Google Scholar]

- Basel Committee on Banking Supervision. Basel III: A global regulatory framework for more resilient banks and banking systems. Bank for International Settlements, Basel, Switzerland. Available online: https://www.bis.org/publ/bcbs189.pdf (accessed on 15 December 2018).

- Bar, A.; Liao, C.; Strassner, M. What Do You Know About Solvency II? High-Level Introduction for Interested Parties from Non-EU regions; Swiss Reinsurance Company: Zurich, Switzerland, 2013. [Google Scholar]

- Liebwein, P. Risk Models for Capital Adequacy: Applications in the Context of Solvency II and Beyond. Geneva Pap. Risk Insur. Issues Pract. 2006, 31, 528–550. [Google Scholar] [CrossRef]

- Elderfield, M. Solvency II: Setting the Pace for Regulatory Change. Geneva Pap. Risk Insur. Issues Pract. 2009, 34, 35–41. [Google Scholar] [CrossRef]

- Eling, M.; Schmeiser, H.; Schmit, J.T. The Solvency II Process: Overview and Critical Analysis. Risk Manag. Insur. Rev. 2007, 10, 69–85. [Google Scholar] [CrossRef]

- Culp, C. Structured Finance and Insurance. The ART of Managing Capital and Risk; John Wiley & Sons: Hoboken, NJ, USA, 2006. [Google Scholar]

- Shimpi, P. Integrating Risk Management and Capital Management. J. Appl. Corp. Finan. 2002, 14, 27–40. [Google Scholar] [CrossRef]

- Doherty, N.A. Risk Management, Risk Capital, and the Cost of Capital. J. Appl. Corp. Finan. 2005, 17, 119–123. [Google Scholar] [CrossRef]

- O’Brien, T.J. Risk Management and the Cost of Capital for Operating Assets. J. Appl. Corp. Finan. 2006, 18, 105–109. [Google Scholar] [CrossRef]

- Dickinson, G. Enterprise Risk Management: Its Origins and Conceptual Foundation. Geneva Pap. Risk Insur. 2001, 26, 360–366. [Google Scholar] [CrossRef]

- Hoyt, R.E.; Liebenberg, A.P. The value of enterprise risk management. J. Risk Insur. 2011, 78, 795–822. [Google Scholar] [CrossRef]

- Zhou, C. Are Banks Too Big to Fail? Measuring Systemic Importance of Financial Institutions. Int. J. Cent. Bank. 2010, 6, 205–250. [Google Scholar] [CrossRef]

- Diacon, S.R.; Carter, R.L. Success in Insurance, 3rd ed.; John Murray: London, UK, 1992. [Google Scholar]

- Dowd, K. The case for financial Laissez-Faire. Econ. J. 1996, 106, 679–687. [Google Scholar] [CrossRef]

- Sorkin, A.R. Too Big to Fail. The Inside Story of How Wall Street and Washington Fought to Save the Financial System—and Themselves; Penguin Books: New York, NY, USA, 2018. [Google Scholar]

- Acharya, V.; Philippon, T.; Richardson, M.; Roubini, N. The Financial Crisis of 2007–2009: Causes and Remedies. In Restoring Financial Stability. How to Repair a Failed System; Acharya, V., Richardson, M., Eds.; John Wiley & Sons: Hoboken, NJ, USA, 2009; pp. 1–56. [Google Scholar]

- Merton, R.C.; Perold, A.F. Theory of Risk Capital in Financial Firms. J. Appl. Corp. Finan. 1993, 6, 16–32. [Google Scholar] [CrossRef]

- Saunders, A.; Allen, L. Credit Risk Measurement. New Approaches to Value and Risk and Other Paradigms; John Wiley & Sons: New York, NY, USA, 2002. [Google Scholar]

- Klaassen, P.; Van Eeghen, I. Economic Capital; Elsevier: Burlington, NJ, USA, 2010. [Google Scholar]

- Bessis, J. Risk Management in Banking, 3rd ed.; John Wiley & Sons: Chichester, NH, USA, 2010. [Google Scholar]

- RiskMetricsTM—Technical Document. Morgan Guaranty Trust Company of New York. 1996. Available online: http://pascal.iseg.utl.pt/~aafonso/eif/rm/TD4ePt_2.pdf (accessed on 15 December 2018).

- Lam, J. Enterprise Risk Management. From Incentives to Controls; John Wiley & Sons: Hoboken, NJ, USA, 2003. [Google Scholar]

- Belmont, D.P. Value Added Risk Management in Financial Institutions. Leveraging Basel II and Risk Adjusted Performance Measurement; John Wiley & Sons: Singapore, 2004. [Google Scholar]

- Shimpi, P. Integrating Risk Management. In Financial Intermediation in the 21st Century; Mikdashi, Z., Ed.; Palgrave McMillan: London, UK, 2001; pp. 33–57. [Google Scholar]

- Shimpi, P. Leverage and the Cost of Capital in the Insurative Model. 2004. Available online: http://www.actuaries.org/AFIR/Colloquia/Boston/Shimpi.pdf (accessed on 15 June 2017).

- Ross, S.A. The Determination of Financial Structure: The Incentive-Signaling Approach. Bell J. Econ. 1977, 8, 23–40. [Google Scholar] [CrossRef]

- Culp, C.L. Contingent Capital: Integrating Corporate Financing and Risk Management Decisions. J. Appl. Corp. Finan. 2002, 15, 46–56. [Google Scholar] [CrossRef]

- Culp, C.L. The Art of Risk Management. Alternative Risk Transfer, Capital Structure and the Convergence of Insurance and Capital Markets; John Wiley & Sons: New York, YN, USA, 2002. [Google Scholar]

- Kloman, F.H. A Brief History of Risk Management. In Enterprise Risk Management. Today’s Leading Research and Best Practices for Tomorrow’s Executives; Fraser, J., Simkins, B.J., Eds.; John Wiley & Sons: Hoboken, NJ, USA, 2010. [Google Scholar]

- Dionne, G. Risk Management: History, Definition and Critique. Risk Manag. Insur. Rev. 2013, 16, 147–166. [Google Scholar] [CrossRef]

- Crockford, G.N. The Bibliography and History of Risk Management: Some Preliminary Observations. Geneva Pap. Risk Insur. 1982, 7, 169–179. [Google Scholar] [CrossRef]

- Bromiley, P.; McShane, M.; Nair, A.; Rustambekov, E. Enterpirse Risk Management. Review, Critique and Research Directions. Long Range Plan. 2015, 48, 265–276. [Google Scholar] [CrossRef]

- Purdy, G. ISO31000:2009—Setting a New Standard for Risk Management. Risk Anal. 2010, 30, 881–886. [Google Scholar] [CrossRef]

- Falkner, E.M.; Hiebl, M.R. Risk management in SMEs: A systematic review of the available evidence. J. Risk Finan. 2015, 2015 16, 122–144. [Google Scholar] [CrossRef]

- Bromiley, P.; Rau, D. A better way of managing major risks: Strategic risks management. IESE Insight 2016, 28, 15–22. [Google Scholar] [CrossRef]

- Hopkin, P. Fundamentals of Risk Management: Understanding, Evaluating and Implementing Effective Risk Management, 3rd ed.; Kogan Page: London, UK, 2015. [Google Scholar]

- Vaughan, E.; Vaughan, T. Fundamentals of Risk and Insurance; John Wiley & Sons: Hoboken, NJ, USA, 2003. [Google Scholar]

- Rejda, G.E. Principles of Risk Management and Insurance; Addison Wesley Longman: London, UK, 2001. [Google Scholar]

- Dorfman, M. Introduction to Risk Management and Insurance; Pearson-Prentice Hall: Upper Saddle River, NJ, USA, 2005. [Google Scholar]

- Mayers, D.; Smith, C.W. On the Corporate Demand for Insurance. J. Bus. 1982, 55, 281–296. [Google Scholar] [CrossRef]

- Smith, C.W.; Stulz, R.M. The determinants of Firm’s hedging policies. J. Finan. Quant. Anal. 1985, 20, 391–405. [Google Scholar] [CrossRef]

- MacMinn, R.D. Insurance and Corporate Risk Management. J. Risk Insur. 1987, 54, 658–677. [Google Scholar] [CrossRef]

- Smithson, C.; Simkins, B.J. Does Risk Management Add Value? A Survey of the Evidence. J. Appl. Corp. Finan. 2005, 17, 8–17. [Google Scholar] [CrossRef]

- Mikes, A.; Kaplan, R.S. When One Size Doesn’t Fit All: Evolving Directions in the Research and Practice of Enterprise Risk Management. J. Appl. Corp. Finan. 2015, 27, 37–40. [Google Scholar] [CrossRef]

- Gordon, L.A.; Loeb, M.P.; Tseng, C. Enterprise risk management and firm performance: A contingency perspective. J. Account. Public Policy 2009, 28, 301–327. [Google Scholar] [CrossRef]

- McShane, M.K.; Nair, A.; Rustambekov, E. Does enterprise risk management increase firm value? J. Account. Audit. Finan. 2011, 24, 641–658. [Google Scholar] [CrossRef]

- Whited, T.M. Debt, liquidity constraints, and corporate investment: Evidence from panel data. J. Finan. 1992, 47, 1425–1460. [Google Scholar] [CrossRef]

- Fraser, J.R.; Simkins, B.J. The challenges of and solutions for implementing enterprise risk management. Bus. Horiz. 2016, 59, 689–698. [Google Scholar] [CrossRef]

- Soppe, A. Sustainable Corporate Finance. J. Bus. Ethics 2004, 53, 213–224. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Donaldson, T.; Preston, L.E. The stakeholder theory of the corporation: Concepts, evidence, and implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Starik, M.; Marcus, A. Introduction to the Special Research Forum on the Management of Organizations in the Natural Environment: A Field Emerging From Multiple Paths, With Many Challenges Ahead. Acad. Manag. J. 2000, 43, 539–546. [Google Scholar]

- Wong, A. Corporate sustainability through non-financial risk management. Corp. Govern. 2014, 14, 575–586. [Google Scholar] [CrossRef]

- Anderson, D. The Critical Importance of Sustainability Risk Management. Risk Manag. 2006, 53, 66–74. [Google Scholar]

- Anderson, D.; Anderson, K. Sustainability Risk Management. Risk Manag. Insur. Rev. 2009, 12, 25–38. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: rethinking social initiatives by business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef]

- Pescaroli, G.; Alexander, D. A definition of cascading disasters and cascading effects: Going beyond the “toppling dominos” metaphor. Davos 2015, 2, 58–67. [Google Scholar]

- Houdet, J.; Germaneau, C. The Financial Impacts of BP’s Response to the Deepwater Horizon oil Spill. Synergis, Case Study 01–2011. Available online: http://synergiz.fr/wp-content/uploads/2011/04/Case-study-BP-gulf-oil.pdf (accessed on 15 December 2018).

- Amadeo, K. BP Gulf Oil Spill Economic Impact. The Balance. 2018. Available online: https://www.thebalance.com/bp-gulf-oil-spill-facts-economic-impact-3306212 (accessed on 15 December 2018).

- Flowler, J.T. Deepwater Horizon: A Lesson in Risk Analysis, Emergency and Disaster Management Digest. 2017. Available online: https://edmdigest.com/news/deepwater-horizon-lesson-risk-analysis/ (accessed on 15 December 2018).

- Norse, E.A.; Amos, J. Impacts, Perception, and Policy Implications of the Deepwater Horizon Oil and Gas. Disaster; Environmental Law Reporter, Environmental Law Institute: Washington, DC, USA, 2010; Available online: http://www.ourenergypolicy.org/wp-content/uploads/2013/08/Norse-and-Amos-2010.pdf (accessed on 15 December 2018).

- Technical analysis: Deepwater Horizon Accident Investigaton Report, 2010, Executive Summary. Available online: https://www.bp.com/content/dam/bp/pdf/sustainability/issue-reports/Deepwater_Horizon_Accident_Investigation_Report_Executive_summary.pdf (accessed on 15 December 2018).

- Lipscy, P.; Kushida, K.; Incerti, T. The Fukushima Disaster and Japan’s Nuclear Plant Vulnerability in Comparative Perspective. Environ. Sci. Technol. 2013, 47, 6082–6088. [Google Scholar] [CrossRef]

- Hatamura, Y.; Abe, S.; Fuchigami, M.; Kasahara, N.; Lino, K. Fukushima—A complex study The 2011 Fukushima Nuclear Power Plant Accident. How and Why It Happened; Woodhead Publishing: Cambridge, UK, 2015. [Google Scholar]

- Hollangel, E.; Fujita, Y. The Fukushima disaster—Systemic failures and the lack of resilience. Nucl. Eng. Technol. 2011, 45, 13–20. [Google Scholar] [CrossRef]

- Srinivasan, T.N.; Gopi Rethirnaaj, T.S. Fukushima and thereafter: Reassessment of risks of nuclear power. Energy Policy 2013, 52, 726–736. [Google Scholar] [CrossRef]

- Holzheu, T.; Karl, K.; Raturi, M. The Picture of Art; Sigma No. 1/2003; Swiss Re: Zurich, Switzerland, 2003. [Google Scholar]

- Hartwig, R.P.; Wilkinson, C. An Overview of Alternative Risk Transfer Market. In Handbook of International Insurance. Between Global Dynamics and Local Contingencies; Cummins, J.D., Vernard, B., Eds.; Springer: New York, NY, USA, 2007. [Google Scholar]

- Cummins, D.; Weiss, M.A. Convergence of insurance and financial markets: Hybrid and securitized risk transfer solutions. J. Risk Insur. 2009, 76, 493–545. [Google Scholar] [CrossRef]

- Outreville, J.F. Theory and Practice of Insurance; Kluwer Academic Publishers: London, UK, 1998. [Google Scholar]

- Williams, C.A.; Heins, R.M. Risk Management and Insurance; McGraw-Hill: New York, NY, USA, 1989. [Google Scholar]

- Weber, E.J. A short history of Derivative Security Markets. The University of Western Australia Discussion Paper 08.10. 2008. Available online: http://www.law.uwa.edu.au/__data/assets/pdf_file/0003/94260/08_10_Weber.pdf (accessed on 15 December 2018).

- Watson, D.; Head, A. Corporate Finance. Principles and Practice; Pearson Education: Harlow, UK, 2001. [Google Scholar]

- Bennett, D. Managing Foreign Exchange Risk; Ptitman Publishing: London, UK, 1997. [Google Scholar]

- Strauss, J. The Definitive Guide to Captive Insurance Companies. What Every Small Business Owner Needs to Know About Creating and Implementing a Captive; Author House: Bloomington, UK, 2011. [Google Scholar]

- Adkisson, J.D. Adkisson’s Captive Insurance Companies. An. Introduction to Captives, Closely-Held Insurance Companies and Risk Retention Groups; iUniverse: New York, NY, USA, 2006. [Google Scholar]

- Kloman, H.F.; Rosenbaum, D.H. The Captive Insurance Phenomenon: A Cautionary Tale? Geneva Pap. Risk Insur. 1982, 7, 129–151. [Google Scholar] [CrossRef]

- Banks, E. Alternative Risk Transfer. Integrated Risk Management through Insurance, Reinsurance and the Capital Markets; John Wiley & Sons: Chichester, NH, USA, 2004. [Google Scholar]

- Culp, C.; Heaton, B. Uses and Abuses of Finite Risk Reinsurance. J. Appl. Corp. Finan. 2005, 17, 18–31. [Google Scholar] [CrossRef]

- Carter, R.; Lucas, L.; Ralph, N. Reinsurance; Reactions Publishing Group in association with Guy Carpenter & Company: London, UK, 2000. [Google Scholar]

- Baur, E.; Schanz, K. Alternative Risk Transfer (ART) for Corporations: A Passing Fashion or Risk Management for the 21st Century? Sigma 2/1999; Swiss Re: Zurich, Switzerland, 1999. [Google Scholar]

- Harrington, S.E.; Niechaus, G.; Risko, K.J. Enterprise Risk Management: The Case of United Grain Growers. J. Appl. Corp. Finan. 2002, 14, 71–81. [Google Scholar] [CrossRef]

- Hagedorn, D.; Heigl, C.; Muller, A.; Seidler, G. Choice of Triggers. In The Handbook of Insurance-Linked Securities; Barrieu, P., Albertini, L., Eds.; John Wiley & Sons: Chichester, NH, USA, 2009; pp. 37–48. [Google Scholar]

- Frey, A.; Kirova, M.; Shmidt, C. The Role of Indices in Transferring Risks to the Capital Markets; Sigma 4/2009; Swiss Re: Zurich, Switzerland, 2009. [Google Scholar]

- ARTEMIS database. Available online: http://www.artemis.bm/deal_directory/ (accessed on 15 December 2018).

- Bourgeois, L.J. III. On the Measurement of Organizational Slack. Acad. Manag. Rev. 1981, 6, 29–39. [Google Scholar] [CrossRef]

- Kim, H.; Kim, H.; Lee, P.M. Ownership structure and the relationship between financial slack and R&D investments: Evidence from Korean Firms. Organ. Sci. 2008, 19, 404–418. [Google Scholar]

- Zhong, H. The Relationship between Slack Resources and Performance: An Empirical Study from China. Int. J. Mod. Educ. Comput. Sci. 2011, 1, 1–8. [Google Scholar] [CrossRef]

- Opler, T.; Pinkowitz, L.; Stulz, R.; Williamson, R. The determinants and implications of corporate cash holdings. J. Finan. Econ. 1999, 52, 3–46. [Google Scholar] [CrossRef]

- Almeida, H.; Campello, M.; Weisbach, M.S. Corporate demand for liquidity. 2002. Available online: https://www.nber.org/papers/w9253 (accessed on 15 December 2018).

- Laffranchini, G.; Braun, M. Slack in family firms: Evidence from Italy (2006–2010). J. Fam. Bus. Manag. 2004, 4, 171–193. [Google Scholar] [CrossRef]

- Modigliani, F.; Miller, M.H. The Cost of Capital, Corporate Finance and the Theory of Investment. Am. Econ. Rev. 1958, 48, 261–297. [Google Scholar]

- Ehrhardt, M.C.; Brigham, E.F. Corporate Finance. A Focused Approach; South Western CENGAGE Learning: Mason, OH, USA, 2009. [Google Scholar]

| Feature | Types of the Sources of Risk Capital | Characteristics |

|---|---|---|

| Balance sheet consideration | Balance-sheet captured ( and ) | Traditional debt and equity sources |

| Off-balance sheet () | Contingency funding (option on capital; the pay-off of the option dependent on the occurrence of a risky event) | |

| Moment of capital allocation | Pre-loss funding | Funds injected before the risk occurrence |

| Post-loss funding | Funds injected in the aftermath of risk occurrence | |

| Ongoing loss funding | Loss continuously incurred in profit and loss account (as operating cost) | |

| Ultimate bearers of the financial risk outcomes | Pure retention | Risk ultimately born by company’s stockholders (owners) |

| Pure transfer | Risk ultimately born by company’s stakeholders (third parties) | |

| Combination of retention and transfer | Risk dispersed between stockholders (owners) and shareholders (third parties) | |

| Innovativeness of risk financing mechanism | Traditional | Risk financing mechanisms traditionally implemented in companies |

| Alternative | Risk financing mechanisms adapted from insurance/reinsurance sector and capital markets |

| Source | Feature | ||

|---|---|---|---|

| Balance Sheet Consideration | Moment of Capital Injection | Ultimate Risk Bearers | |

| Insurance | Off-balance sheet | Post-loss funding | Transfer |

| Derivatives | Off-balance sheet | Post-loss funding | Transfer |

| Earmarked capital reserves | Balance sheet captured | Pre-loss funding | Retention |

| Credit lines | Off-balance sheet | Post-loss funding | Retention |

| Compensation | Balance sheet captured (through the net profit) | Ongoing loss funding | Retention |

| Source | Feature | ||

|---|---|---|---|

| Balance Sheet Consideration | Moment of Capital Injection | Ultimate Risk Bearers | |

| Captives | Partially balance sheet captured (the equity contribution of the parent company) | Post-loss funding | Combined |

| Finite risk programs | Off-balance sheet | Pre-loss funding or post-loss funding (depending on the type of the program shape) | Combined |

| Multi-risk products (MMPs and MTPs) | Off-balance sheet in transfer part, balance sheet captured in retention level | Post-loss funding | Combined |

| Insurance derivatives | Off-balance sheet | Post-loss funding | Transfer |

| Catastrophic bonds | Off-balance sheet | Post-loss funding | Transfer |

| Contingent capital structures | Off-balance sheet | Post-loss funding | Retention |

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wieczorek-Kosmala, M. The Concept of Risk Capital and Its Application in Non-Financial Companies: A Sustainable Dimension. Sustainability 2019, 11, 894. https://doi.org/10.3390/su11030894

Wieczorek-Kosmala M. The Concept of Risk Capital and Its Application in Non-Financial Companies: A Sustainable Dimension. Sustainability. 2019; 11(3):894. https://doi.org/10.3390/su11030894

Chicago/Turabian StyleWieczorek-Kosmala, Monika. 2019. "The Concept of Risk Capital and Its Application in Non-Financial Companies: A Sustainable Dimension" Sustainability 11, no. 3: 894. https://doi.org/10.3390/su11030894

APA StyleWieczorek-Kosmala, M. (2019). The Concept of Risk Capital and Its Application in Non-Financial Companies: A Sustainable Dimension. Sustainability, 11(3), 894. https://doi.org/10.3390/su11030894