M-PESA and Financial Inclusion in Kenya: Of Paying Comes Saving?

Abstract

1. Introduction

2. M-PESA Identikit

3. State of the Literature on M-PESA

3.1. Adoption

3.2. Use

3.3. Economic Impact

4. Data

5. Methodology

5.1. Dependent Variables

5.2. Independent Variables

6. Results

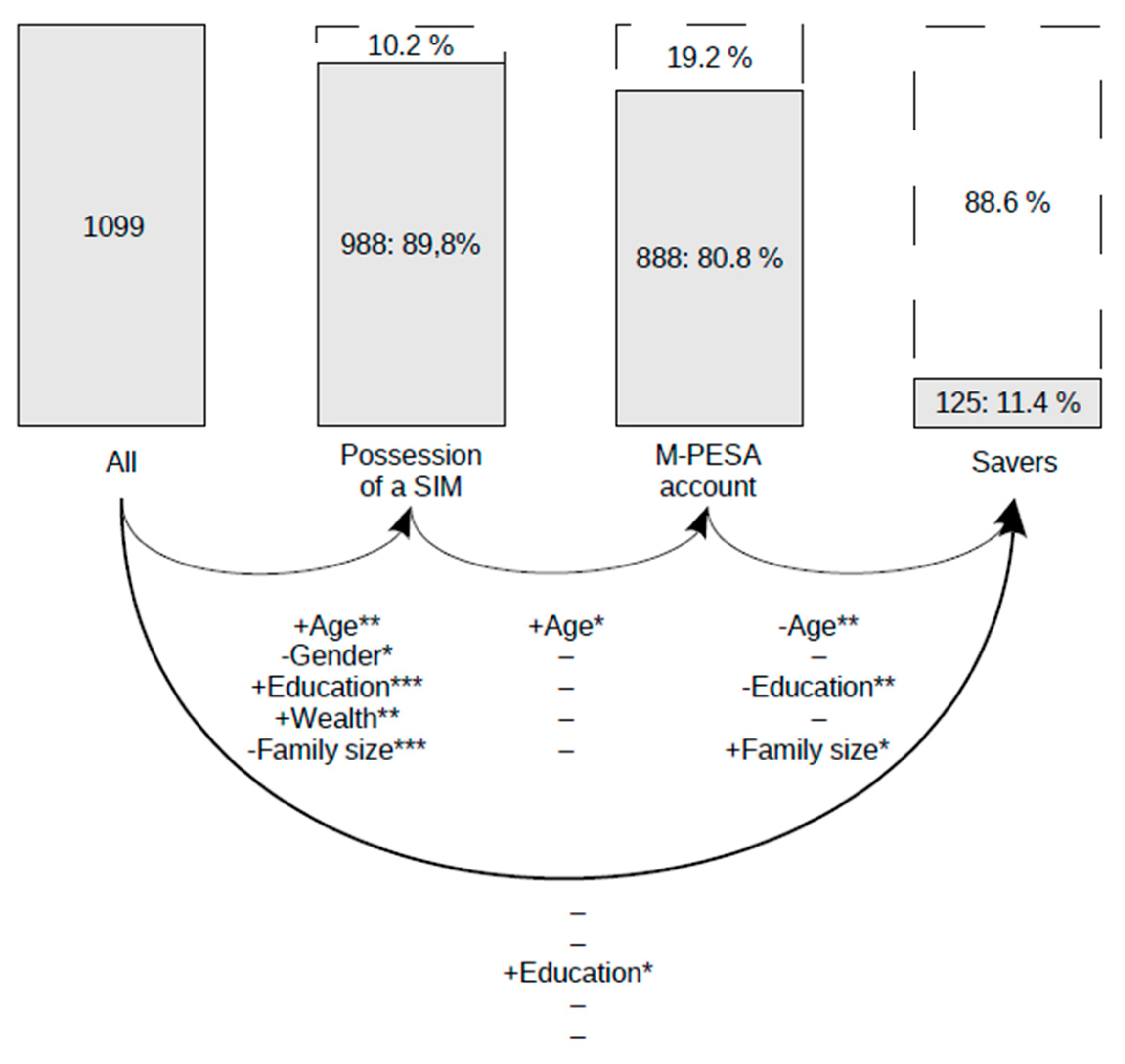

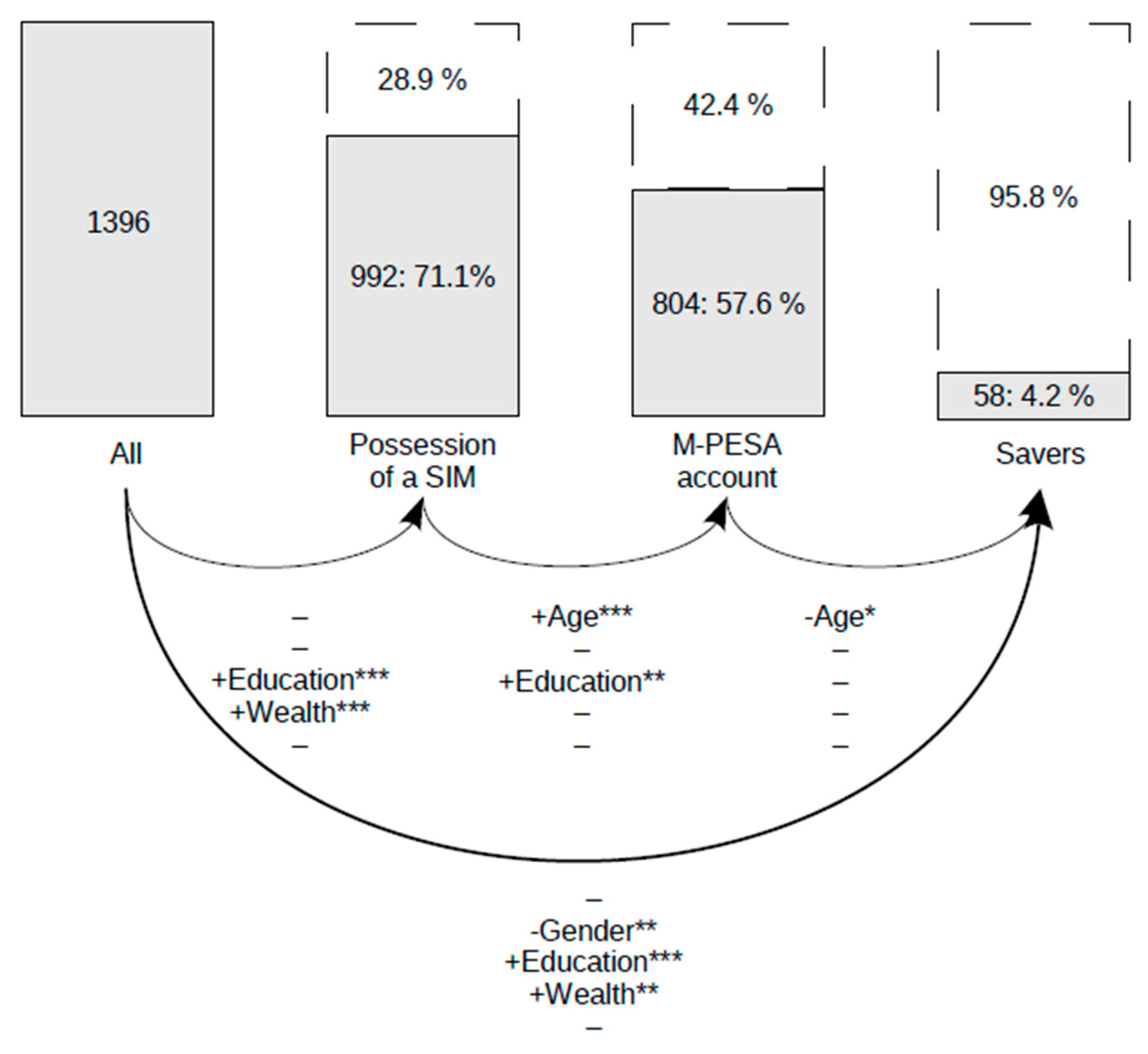

6.1. Precondition: SIM Ownership

6.2. M-PESA Adoption

6.3. Saving

6.4. A View Across the Three Steps

7. Conclusions and Policy Implications

Supplementary Materials

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| FII | FinAccess | |

|---|---|---|

| M-PESA users | 72.7 | 58.7 |

| Bank account owners | 28.2 | 27.1 |

| Age | ||

| 15–25 | 22.3 | 25.9 |

| 26–30 | 17.2 | 17.3 |

| 31–35 | 13.1 | 12.1 |

| 36–40 | 12.2 | 10.4 |

| 41–55 | 20.8 | 16.8 |

| Over 55 | 14.4 | 17.5 |

| Gender | ||

| Female | 62 | 59.1 |

| Male | 38 | 40.9 |

| Education | ||

| No education | 33.3 | 39.0 |

| Primary | 39.1 | 36.1 |

| Secondary | 25.6 | 22.8 |

| College | 2.0 | 2.1 |

| Urbanity (Urban = 1) | 36.7 | 35.9 |

| Employed | 70.4 | 79.8 |

| Wealth | 14.1 | 11.6 |

| N | 3000 | 6449 |

| Saving on MFS | Saving on a Bank Account | ||||||

|---|---|---|---|---|---|---|---|

| Urban + Rural | Urban | Rural | Rural, Vulnerable | Urban + Rural | Urban | Rural | |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

| Outcome equation | |||||||

| Age | n.s. | n.s. | n.s. | n.s. | n.s. | * | n.s. |

| 15–25 | – | – | – | – | – | – | – |

| 26–30 | 0.0982 | 0.0623 | 0.181 | 0.429 * | 0.437 ** | 0.604 *** | 0.0935 |

| (0.92) | (0.45) | (1.05) | (2.06) | (3.19) | (3.62) | (0.35) | |

| 31–35 | 0.0236 | −0.306 | 0.335 | 0.419 | 0.368 * | 0.285 | 0.552 * |

| (0.20) | (−1.66) | (1.92) | (1.92) | (2.43) | (1.37) | (2.29) | |

| 36–40 | 0.134 | 0.215 | 0.177 | 0.234 | 0.308 | 0.315 | 0.419 |

| (1.11) | (1.22) | (1.00) | (1.00) | (1.94) | (1.38) | (1.71) | |

| 41–55 | 0.00117 | 0.0726 | 0.0433 | 0.214 | 0.293 * | 0.323 | 0.373 |

| (0.01) | (0.46) | (0.26) | (1.00) | (2.06) | (1.61) | (1.64) | |

| Over 55 | −0.318 * | −0.137 | −0.292 | −0.271 | 0.366 * | 0.751 ** | 0.322 |

| (−2.12) | (−0.58) | (−1.38) | (−0.83) | (2.28) | (3.21) | (1.27) | |

| Gender (Female = 1) | −0.205 ** | −0.185 | −0.272 ** | −0.362 ** | −0.301 *** | −0.415 *** | −0.231 |

| (−2.80) | (−1.71) | (−2.62) | (−2.65) | (−3.46) | (−3.40) | (−1.77) | |

| Education | *** | * | *** | *** | *** | *** | *** |

| Non-educated | – | – | – | – | – | – | – |

| Primary | 0.475 *** | 0.371 * | 0.460 ** | 0.396 * | 0.322 * | 0.339 | 0.213 |

| (4.36) | (2.03) | (3.21) | (2.27) | (2.43) | (1.48) | (1.20) | |

| Secondary | 0.766 *** | 0.594 ** | 0.801 *** | 0.915 *** | 0.790 *** | 0.685 ** | 0.782 *** |

| (6.68) | (3.15) | (5.27) | (4.66) | (5.84) | (2.98) | (4.31) | |

| College | 0.271 | −0.118 | 0.588 | no variation | 1.316 *** | 1.131 *** | 1.304 *** |

| (1.00) | (−0.31) | (1.44) | (6.05) | (3.64) | (3.68) | ||

| Wealth | 0.0232 ** | 0.0104 | 0.0333 ** | 0.0403 ** | 0.0135 | 0.0183 | 0.0119 |

| (3.26) | (1.00) | (3.26) | (3.02) | (1.61) | (1.47) | (0.98) | |

| Family size | −0.0180 | −0.00335 | −0.00408 | 0.00393 | −0.0207 | −0.0342 | 0.0193 |

| (−1.18) | (−0.13) | (−0.20) | (0.15) | (−1.14) | (−1.15) | (0.86) | |

| Constant | −2.05 *** | −1.64 *** | −2.44 *** | −2.701 *** | −2.382 *** | −2.194 *** | −2.726 *** |

| (−12.55) | (−6.64) | (−10.08) | (−8.83) | (−11.79) | (−7.01) | (−8.74) | |

| Pseudo R2 | 0.0768 | 0.0387 | 0.1102 | 0.1416 | 0.1053 | 0.1037 | 0.1073 |

| AIC | 1512.554 | 772.5237 | 736.0625 | 436.1237 | 1030.454 | 564.7305 | 455.7456 |

| BIC | 1584.607 | 832.5496 | 802.6262 | 493.7709 | 1102.506 | 624.7564 | 522.3093 |

| Log likelihood | −744.277 | −374.261 | −356.031 | −207.06187 | −503.2270 | −270.3652 | −215.8728 |

| Observations | 2994 | 1099 | 1895 | 1395 | 2994 | 1099 | 1895 |

References

- Klapper, L.; Singer, D. The Opportunities of Digitizing Payments; Working Paper; The World Bank: Washington, DC, USA, 2014. [Google Scholar]

- Johnson, S.; Nino-Zarazua, M. Financial Access and Exclusion in Kenya and Uganda. J. Dev. Stud. 2011, 47, 475–496. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, A.; Klapper, L.; Singer, D.; Ansar, S.; Hess, J. The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution; The World Bank: Washington, DC, USA, 2017. [Google Scholar]

- Johnson, S. Competing Visions of Financial Inclusion in Kenya: The Rift Revealed by Mobile Money Transfer. Revue Canadienne D’études du Développement 2016, 37, 83–100. [Google Scholar] [CrossRef]

- Morduch, J. Poverty and Vulnerability. Am. Econ. Rev. 1994, 84, 221–225. [Google Scholar]

- Binswanger, H.P.; Khandker, S.R. The Impact of Formal Finance on the Rural Economy of India. J. Dev. Stud. 1995, 32, 234–262. [Google Scholar] [CrossRef]

- Beck, T.; Demirgüç-Kunt, A.; Levine, R. SMEs, Growth, and Poverty: Cross-Country Evidence. J. Econ. Growth 2005, 10, 199–229. [Google Scholar] [CrossRef]

- Gulyani, S.; Talukdar, D.; Bassett, E.M. A Sharing Economy? Unpacking Demand and Living Conditions in the Urban Housing Market in Kenya. World Dev. 2018, 109, 57–72. [Google Scholar] [CrossRef]

- United Nations. Sustainable Development Goals. Available online: https://sustainabledevelopment.un.org/?menu=1300 (accessed on 12 December 2018).

- Committee on Payments and Market Infrastructures and World Bank Group. Payment Aspects of Financial Inclusion; Bank for International Settlements: Basle, Switzerland, 2016. [Google Scholar]

- World Bank. World Development Indicators. Available online: https://data.worldbank.org/indicator/SI.POV.NAHC?locations=KE (accessed on 9 December 2018).

- Food and Agriculture Organization (FAO). Kenya at a Glance. Available online: http://www.fao.org/kenya/fao-in-kenya/kenya-at-a-glance/en/ (accessed on 9 December 2018).

- Kaminska, I. Mpesa: The Costs of Evolving an Independent Central Bank. FT.com. 15 July 2015. Available online: http://ftalphaville.ft.com/2015/07/15/2134081/the-collateral-velocity-and-sovereign-costs-of-mobile-money/ (accessed on 12 December 2018).

- Burns, S. M-PESA and the ‘Market-led’ Approach to Financial Inclusion. Econ. Aff. 2018, 38, 406–421. [Google Scholar] [CrossRef]

- InterMedia. The Financial Inclusion Insight Program; Intermedia: Washington, DC, USA, 2013. [Google Scholar]

- FSD Kenya; Central Bank of Kenya. FinAccess National Survey 2013: Profiling Developments in Financial Access and Usage in Kenya; FSD Kenya and Central Bank of Kenya: Nairobi, Kenya, 2013. [Google Scholar]

- Suri, T.; Jack, W. The Long-Run Poverty and Gender Impacts of Mobile Money. Science 2016, 354, 1288–1292. [Google Scholar] [CrossRef]

- Di Castri, S.; Gidvani, L. The Kenyan Journey to Digital Financial Inclusion; Working Paper No. 15; GSMA: London, UK, 2013. [Google Scholar]

- Muthiora, B. Enabling Mobile Money Policies in Kenya: Fostering a Digital Financial Revolution; GSMA: London, UK, 2015. [Google Scholar]

- InterMedia. Kenya Quicksights Report, Fourth Annual FII Tracker Survey; Intermedia: Washington, DC, USA, 2016. [Google Scholar]

- Johnson, S. Competing Visions of Financial Inclusion in Kenya: The Rift Revealed by Mobile Money Transfer; Working Paper No. 30; Bath Papers in International Development and Wellbeing, University of Bath: Bath, UK, 2014. [Google Scholar]

- Demombynes, G.; Thegeya, A. Kenya’s Mobile Revolution and the Promise of Mobile Savings; Working Paper No. 5988; The World Bank: Washington, DC, USA, 2012. [Google Scholar]

- Aron, J. Mobile Money and the Economy: A Review of the Evidence. World Bank Res. Obs. 2018, 33, 135–188. [Google Scholar] [CrossRef]

- Donner, J.; Tellez, C.A. Mobile Banking and Economic Development: Linking Adoption, Impact, and Use. Asian J. Commun. 2008, 18, 318–332. [Google Scholar] [CrossRef]

- Suri, T. Mobile Money. Annu. Rev. Econ. 2017, 9, 497–520. [Google Scholar] [CrossRef]

- Porteous, D. Just How Transformational is M-Banking? FinMark Trust: Johannesburg, South Africa, 2007. [Google Scholar]

- Aker, J.C.; Mbiti, I.M. Mobile Phones and Economic Development in Africa. J. Econ. Perspect. 2010, 24, 207–232. [Google Scholar] [CrossRef]

- Johnson, S.; Arnold, S. Inclusive Financial Markets: Is Transformation Under Way in Kenya? Dev. Policy Rev. 2012, 30, 719–748. [Google Scholar] [CrossRef]

- Jack, W.; Suri, T. Risk Sharing and Transactions Costs: Evidence from Kenya’s Mobile Money Revolution. Am. Econ. Rev. 2014, 104, 183–223. [Google Scholar] [CrossRef]

- Morawczynski, O. Surviving in the ‘Dual System’: How M-PESA is Fostering Urban to Rural Remittances in a Kenyan Slum; Working Paper; Social Studies Unit, University of Edinburgh: Edinburgh, UK, 2008. [Google Scholar]

- Morawczynski, O.; Pickens, M. Poor People Using Mobile Financial Services: Observations on Customer Usage and Impact from M-PESA; CGAP: Washington, DC, USA, 2009. [Google Scholar]

- Mbiti, I.; Weil, D.N. Mobile Banking: The Impact of M-PESA in Kenya; Working Paper No. 17129; National Bureau of Economic Research: Cambridge, MA, USA, 2014. [Google Scholar]

- Kikulwe, E.M.; Fischer, E.; Qaim, M. Mobile Money, Smallholder Farmers, and Household Welfare in Kenya. PLoS ONE 2014, 9. [Google Scholar] [CrossRef] [PubMed]

- Plyler, M.G.; Haas, S.; Nagarajan, G. Community-Level Economic Effects of M-PESA in Kenya; Financial Services Assessment: College Park, MD, USA, 2010; pp. 1–8. [Google Scholar]

- Jack, W.; Suri, T. Mobile Money: The Economics of M-PESA; Working Paper No. W16721; National Bureau of Economic Research: Cambridge, MA, USA, 2011. [Google Scholar]

- Morawczynski, O. Exploring the Usage and Impact of ‘Transformational’ Mobile Financial Services: The Case of M-PESA in Kenya. J. East. Afr. Stud. 2009, 3, 509–525. [Google Scholar] [CrossRef]

- Arestoff, F.; Venet, B. Learning to Walk Before You Run: Financial Behavior and Mobile Banking in Madagascar; Working Paper No. DT/2013/09; Université Paris-Dauphine: Paris, France, 2013. [Google Scholar]

- Ouma, S.A.; Odongo, T.M.; Were, M. Mobile Financial Services and Financial Inclusion: Is it a Boon for Savings Mobilization? Rev. Dev. Econ. 2017, 7, 29–35. [Google Scholar] [CrossRef]

- InterMedia. Digital Pathways to Financial Inclusion. Findings from the First FII Tracker Survey in Kenya. 2014. Available online: http://finclusion.org/uploads/file/reports/FII-Kenya-Wave-One-Wave-Report.pdf (accessed on 12 November 2018).

- The World Factbook. Available online: https://www.cia.gov/library/publications/the-world-factbook/geos/ke.html (accessed on 12 November 2018).

- Munyegera, G.K.; Matsumoto, T. Mobile Money, Remittances, and Household Welfare: Panel Evidence from Rural Uganda. World Dev. 2016, 79, 127–137. [Google Scholar] [CrossRef]

- Murendo, C.; Wollni, M.; de Brauw, A.; Mugabi, N. Social Network Effects on Mobile Money Adoption in Uganda. J. Dev. Stud. 2018, 54, 327–342. [Google Scholar] [CrossRef]

- Munyegera, G.K.; Matsumoto, T. ICT for Financial Access: Mobile Money and the Financial Behavior of Rural Households in Uganda. Rev. Dev. Econ. 2018, 22, 45–66. [Google Scholar] [CrossRef]

- Apiors, E.K.; Suzuki, A. Mobile Money, Individuals’ Payments, Remittances, and Investments: Evidence from the Ashanti Region, Ghana. Sustainability 2018, 10, 1409. [Google Scholar] [CrossRef]

- Van Hove, L. Comment on Apiors, E.K.; Suzuki, A. Mobile Money, Individuals’ Payments, Remittances, and Investments: Evidence from the Ashanti Region, Ghana, Sustainability 2018, Vol. 10, 1409. Sustainability 2018, 10, 2784. [Google Scholar] [CrossRef]

- Wyche, S.; Olson, J. Kenyan Women’s Rural Realities, Mobile Internet Access, and “Africa Rising”. Inf. Technol. Int. Dev. 2018, 14, 33–47. [Google Scholar]

- Kusimba, S.B.; Yang, Y.; Chawla, N.V. Family Networks of Mobile Money in Kenya. Inf. Technol. Int. Dev. 2015, 11, 1–21. [Google Scholar]

- Johnson, S.; Brown, G.K.; Fouillet, C. The Search for Inclusion in Kenya’s Financial Landscape: The Rift Revealed; Financial Sector Deepening (FSD) Kenya: Nairobi, Kenya, 2012. [Google Scholar]

- Johnson, S.; Krijtenburg, F. Upliftment, Friends and Finance: Everyday Concepts and Practices of Resource Exchange Underpinning Mobile Money Adoption in Kenya; Working Paper No. 41; Bath Papers in International Development and Wellbeing, University of Bath: Bath, UK, 2015. [Google Scholar]

- Desiere, S.; Vellema, W.; D’Haese, M.A. Validity Assessment of the Progress out of Poverty Index (PPI). Eval. Program Plan. 2015, 49, 10–18. [Google Scholar] [CrossRef] [PubMed]

- Kenya. Available online: https://www.povertyindex.org/country/kenya (accessed on 13 November 2018).

- Murphy, L.; Priebe, A.E. My Co-wife can Borrow my Mobile Phone! Gendered Geographies of Cell Phone Usage and Significance for Rural Kenyans. Gend. Technol. Dev. 2011, 15, 1–23. [Google Scholar] [CrossRef]

- Blumenstock, J.E.; Eagle, N. Divided We Call: Disparities in Access and Use of Mobile Phones in Rwanda. Inf. Technol. Int. Dev. 2012, 8, 1–16. [Google Scholar]

- Jonker, N. Payment Instruments as Perceived by Consumers: Results from a Household Survey. Economist (Leiden) 2007, 155, 271–303. [Google Scholar] [CrossRef]

- Dupas, P.; Robinson, J. Savings Constraints and Microenterprise Development: Evidence from a Field Experiment in Kenya. AEJ Appl. Econ. 2013, 5, 163–192. [Google Scholar] [CrossRef]

- Johnson, S.; Brown, G.K.; Fouillet, C. The Search for Inclusion in Kenya’s Financial Landscape: The Rift Revealed—Annex 2: Demand-Side Survey; Financial Sector Deepening (FSD) Kenya: Nairobi, Kenya, 2012. [Google Scholar]

- Communications Authority of Kenya. Second Quarter Sector Statistics Report for the Financial Year 2017/2018; Authority of Kenya: Nairobi, Kenya, 2017. [Google Scholar]

- Roessler, P.; Myamba, F.; Carroll, P.; Jahari, C.; Kilama, B.; Nielson, D.L. Mobile-Phone Ownership Increases Poor Women’s Household Consumption: A Field Experiment in Tanzania. In Proceedings of the Evidence in Governance and Politics Meeting, Nairobi, Kenya, 8–9 June 2018. [Google Scholar]

- Kiconco, R.I.; Rooks, G.; Solana, G.; Matzat, U. A Skills Perspective on the Adoption and Use of Mobile Money Services in Uganda. Inf. Dev. 2018. [Google Scholar] [CrossRef]

- Wyche, S.; Simiyu, N.; Otheno, M.E. Mobile Phones as Amplifiers of Social Inequality among Rural Kenyan Women. ACM Trans. Comput. Hum. Interact. 2016, 23, 14. [Google Scholar] [CrossRef]

- Batista, C.; Vicente, P.C. Improving Access to Savings through Mobile Money: Experimental Evidence from Smallholder Farmers in Mozambique; Working Paper No. 1705; NOVAFRICA: Carcavelos, Portugal, 2017. [Google Scholar]

- Karlan, D.; Latan, A.L.; Zinman, J. Savings by and for the Poor: A Research Review and Agenda. Rev. Income Wealth 2014, 60, 36–78. [Google Scholar] [CrossRef] [PubMed]

- Habyarimana, J.; Jack, W. High Hopes: Experimental Evidence on Saving and the Transition to High School in Kenya; Working Paper No. 4; Georgetown University Initiative on Innovation, Development and Evaluation: Washington, DC, USA, 2018. [Google Scholar]

- Johnson, S.; Krijtenburg, F. ‘Upliftment’, Friends and Finance: Everyday Exchange Repertoires and Mobile Money Transfer in Kenya. J. Mod. Afr. Stud. 2018, 56, 569–594. [Google Scholar] [CrossRef]

- Kusimba, S.B.; Yang, Y.; Chawla, N.V. Hearthholds of Mobile Money in Western Kenya. Econ. Anthrop. 2016, 3, 266–279. [Google Scholar] [CrossRef]

- Tech Innovation Puts Workers on Firmer Financial Footing. Available online: https://www.ft.com/content/4da30abe-a2b0-11e7-8d56-98a09be71849 (accessed on 12 November 2018).

- Long, S. Exclusive Access, Special Report on Financial Inclusion. Available online: https://www.economist.com/special-report/2018/05/03/financial-inclusion-is-making-great-strides (accessed on 12 November 2018).

| M-PESA Uses | Number | Percentage |

|---|---|---|

| Own a SIM card | 2454 | 82.0 |

| Own or have access to a SIM card | 2832 | 94.6 |

| Use M-PESA | 2171 | 72.5 |

| Use M-KESHO | 34 | 1.1 |

| Use M-SHWARI | 283 | 9.4 |

| Mobile money transfers | ||

| Withdraw money a | 2303 | 76.9 |

| Deposit money | 1868 | 62.4 |

| Pay for goods at a store | 54 | 1.8 |

| Receive money for regular support | 1235 | 41.2 |

| Send money for regular support | 1118 | 37.3 |

| Receive money for emergency | 761 | 25.4 |

| Send money for emergency | 764 | 25.5 |

| Mobile banking | ||

| Save money for future purchase/payment | 205 | 6.8 |

| Receive a salary | 59 | 2.0 |

| Take a loan | 37 | 1.2 |

| Receive state aid or pension | 18 | 0.6 |

| Buy insurance | 5 | 0.2 |

| Urban + Rural (1) | Urban (2) | Rural (3) | Rural (4) | Rural, Vulnerable (5) | |

|---|---|---|---|---|---|

| Age | ** | ** | ** | n.s. | n.s. |

| 15–25 | – | – | – | – | – |

| 26–30 | 0.454 *** | 0.595 *** | 0.392 ** | 0.394 ** | 0.381 ** |

| (4.63) | (3.55) | (3.15) | (3.24) | (2.91) | |

| 31–35 | 0.480 *** | 0.489 ** | 0.497 *** | 0.419 *** | 0.485 *** |

| (4.57) | (2.69) | (3.80) | (3.33) | (3.54) | |

| 36–40 | 0.597 *** | 0.638 ** | 0.599 *** | 0.503 *** | 0.526 *** |

| (5.43) | (2.95) | (4.57) | (4.00) | (3.74) | |

| 41–55 | 0.521 *** | 0.640 *** | 0.534 *** | 0.427 *** | 0.457 *** |

| (5.77) | (3.51) | (4.91) | (4.09) | (3.91) | |

| Over 55 | 0.203 * | 0.350 | 0.226 * | −0.00383 | 0.166 |

| (2.13) | (1.68) | (2.01) | (−0.04) | (1.33) | |

| Gender (Female = 1) | −0.165 ** | −0.326 * | −0.116 | −0.201 ** | −0.103 |

| (−2.62) | (−2.44) | (−1.59) | (−2.84) | (−1.28) | |

| Education | *** | *** | *** | *** | |

| Non-educated | – | – | – | – | |

| Primary | 0.587 *** | 0.453 ** | 0.568 *** | 0.546 *** | |

| (8.59) | (3.22) | (7.02) | (6.15) | ||

| Secondary | 1.049 *** | 0.916 *** | 1.011 *** | 0.865 *** | |

| (10.77) | (5.36) | (7.94) | (5.87) | ||

| College | no variation | no variation | no variation | no variation | |

| Wealth | 0.0542 *** | 0.0292 ** | 0.0633 *** | 0.0833 *** | 0.0609 *** |

| (9.83) | (2.73) | (9.62) | (13.54) | (8.43) | |

| Family size | −0.0316 ** | −0.0881 *** | −0.00953 | −0.0244 * | −0.00922 |

| (−3.11) | (−3.57) | (−0.82) | (−2.18) | (−0.74) | |

| Constant | −0.295 * | 0.593 *** | −0.606 *** | −0.299 * | −0.637 *** |

| (−2.57) | (2.59) | (−4.38) | (−2.29) | (−4.30) | |

| Pseudo R2 | 0.1685 | 0.1273 | 0.1708 | 0.1268 | 0.1376 |

| AIC | 2351.6 | 642.4 | 1694.0 | 1788.1 | 1469.9 |

| BIC | 2417.4 | 697.0 | 1754.9 | 1838.0 | 1527.6 |

| Log likelihood | −1164.8 | −310.2 | −836.0 | −855.0 | −723.9 |

| Observations | 2994 | 1099 | 1895 | 1895 | 1396 |

| Urban + Rural | Urban | Rural | Rural, Vulnerable | ||

|---|---|---|---|---|---|

| M-PESA | Bank Account | M-PESA | M-PESA | M-PESA | |

| (1) | (2) | (3) | (4) | (5) | |

| Outcome Equation | |||||

| Age | *** | *** | * | *** | *** |

| 15–25 | – | – | – | – | – |

| 26–30 | 0.202 * | 0.424 *** | 0.334 * | 0.122 | 0.105 |

| (2.10) | (4.50) | (2.17) | (0.95) | (0.74) | |

| 31–35 | 0.319 ** | 0.440 *** | 0.454 * | 0.256 | 0.283 |

| (2.92) | (4.36) | (2.37) | (1.80) | (1.68) | |

| 36–40 | 0.415 *** | 0.618 *** | 0.796 ** | 0.320 * | 0.354 * |

| (3.58) | (5.90) | (2.95) | (2.27) | (2.08) | |

| 41–55 | 0.428 *** | 0.748 *** | 0.287 | 0.483 *** | 0.512 ** |

| (4.21) | (7.58) | (1.54) | (3.59) | (3.09) | |

| Over 55 | 0.441 *** | 0.737 *** | 0.222 | 0.510 *** | 0.607 ** |

| (3.73) | (6.43) | (0.92) | (3.41) | (3.09) | |

| Gender (Female = 1) | −0.0527 | −0.422 *** | −0.109 | −0.0496 | 0.0123 |

| (−0.78) | (−6.77) | (−0.84) | (−0.60) | (0.13) | |

| Education | *** | *** | n.s. | *** | ** |

| Non-educated | – | – | – | – | |

| Primary | 0.156 | 0.134 | 0.0521 | 0.159 | 0.189 |

| (1.94) | (1.35) | (0.27) | (1.64) | (1.56) | |

| Secondary | 0.456 *** | 0.764 *** | 0.354 | 0.456 *** | 0.607 ** |

| (4.50) | (5.55) | (1.46) | (3.48) | (3.18) | |

| College | 0.728 * | 1.951 *** | 0.334 | 4.096 | no variation |

| (2.25) | (7.31) | (0.82) | (0.03) | ||

| Wealth | 0.0131 * | 0.0191 * | 0.0141 | 0.0135 | 0.00820 |

| (2.05) | (2.57) | (1.13) | (1.64) | (0.78) | |

| Family size | −0.0108 | −0.0160 | −0.0251 | −0.00431 | 0.000427 |

| (−0.89) | (−1.35) | (−0.82) | (−0.33) | (0.03) | |

| Selection Equation (SIM ownership) | |||||

| Age | 0.0390 * | 0.0388 * | 0.0936 ** | 0.0366 | 0.0212 |

| (2.28) | (2.26) | (2.69) | (1.80) | (0.95) | |

| Gender | −0.102 | −0.108 | −0.286* | −0.0530 | −0.0574 |

| (−1.63) | (−1.72) | (−2.12) | (−0.73) | (−0.72) | |

| Education | 0.548 *** | 0.548 *** | 0.461 *** | 0.535 *** | 0.475 *** |

| (12.13) | (12.06) | (5.60) | (9.53) | (7.36) | |

| Wealth | 0.0539 *** | 0.0528 *** | 0.0305 ** | 0.0619 *** | 0.0598 *** |

| (9.96) | (9.70) | (2.87) | (9.52) | (8.34) | |

| Family size | −0.0272 ** | −0.0245 * | −0.0810 ** | −0.00792 | −0.00841 |

| (−2.73) | (−2.42) | (−3.27) | (−0.68) | (−0.66) | |

| Employed | 0.236 *** | 0.255 *** | 0.210 | 0.232 ** | 0.237 ** |

| (3.81) | (4.03) | (1.82) | (3.07) | (2.97) | |

| athrho | −1.038 | −0.622 ** | −0.395 | −1.070 | −1.028 |

| (−1.83) | (−2.59) | (−0.39) | (−1.77) | (−1.35) | |

| Chi2 | 5.66 | 4.13 | 0.15 | 4.96 | 2.96 |

| p | 0.0173 | 0.0422 | 0.69 | 0.02 | 0.08 |

| Log likelihood | −2069.6 | −2484.2 | −623.6467 | −1416.378 | −1176.13 |

| Censored | 540 | 540 | 111 | 429 | 404 |

| Uncensored | 2454 | 2454 | 988 | 1466 | 992 |

| Urban + Rural | Urban | Rural | Rural, Vulnerable | |

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| Outcome equation | ||||

| Age | *** | ** | *** | * |

| 15–25 | – | – | – | – |

| 26–30 | −0.0484 | −0.0835 | −0.0360 | 0.216 |

| (−0.54) | (−0.85) | (−0.30) | (0.89) | |

| 31–35 | −0.186 | −0.394 ** | −0.0563 | 0.0753 |

| (−1.82) | (−2.72) | (−0.41) | (0.28) | |

| 36–40 | −0.121 | −0.0886 | −0.185 | −0.100 |

| (−1.13) | (−0.61) | (−1.42) | (−0.38) | |

| 41–55 | −0.265 ** | −0.232 | −0.332 ** | −0.147 |

| (−2.59) | (−1.62) | (−2.66) | (−0.54) | |

| Over 55 | −0.529 *** | −0.400 * | −0.576 *** | −0.580 * |

| (−4.20) | (−2.14) | (−3.89) | (−2.03) | |

| Gender (Female = 1) | −0.0783 | 0.0182 | −0.108 | −0.278 |

| (−0.98) | (0.16) | (−1.15) | (−1.69) | |

| Education | n.s. | ** | n.s. | n.s. |

| Non-educated | – | – | – | |

| Primary | −0.0327 | −0.0362 | −0.214 | −0.0829 |

| (−0.18) | (−0.19) | (−1.25) | (−0.22) | |

| Secondary | −0.0678 | −0.123 | −0.301 | 0.102 |

| (−0.24) | (−0.43) | (−1.15) | (0.16) | |

| College | −0.666 | −0.826 * | −0.697 | no variation |

| (−1.84) | (−2.37) | (−1.61) | (−0.00) | |

| Wealth | −0.0122 | −0.0118 | −0.0214 | −0.00102 |

| (−1.05) | (−1.15) | (−1.53) | (−0.03) | |

| Family size | 0.00785 | 0.0460 * | 0.00487 | 0.00681 |

| (0.53) | (1.97) | (0.32) | (0.28) | |

| Selection equation | ||||

| Age | 0.0828 *** | 0.102 *** | 0.0965 *** | 0.0954 *** |

| (5.25) | (3.47) | (5.05) | (4.41) | |

| Gender | −0.104 | −0.189 | −0.0926 | −0.0492 |

| (−1.88) | (−1.82) | (−1.40) | (−0.64) | |

| Education | 0.520 *** | 0.385 *** | 0.542 *** | 0.548 *** |

| (13.48) | (5.80) | (11.08) | (9.23) | |

| Wealth | 0.0489 *** | 0.0270 ** | 0.0576 *** | 0.0557 *** |

| (10.10) | (3.01) | (9.75) | (8.34) | |

| Family size | −0.0318 ** | −0.0681 ** | −0.00572 | −0.00590 |

| (−3.18) | (−3.29) | (−0.51) | (−0.46) | |

| Employed | 0.245 *** | 0.188 | 0.238 ** | 0.261 ** |

| (4.16) | (1.86) | (3.10) | (3.04) | |

| athrho | −1.114 * | −1.608 | −1.594 ** | −0.923 |

| (−2.30) | (−1.55) | (−2.66) | (−1.06) | |

| Chi2 | 4.47 | 2.44 | 5.64 | 0.81 |

| p | 0.0345 | 0.1179 | 0.0175 | 0.3680 |

| Log likelihood | −2218.225 | −838.3561 | −1345.318 | −1005.425 |

| Censored | 861 | 211 | 650 | 592 |

| Uncensored | 2133 | 888 | 1245 | 804 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Van Hove, L.; Dubus, A. M-PESA and Financial Inclusion in Kenya: Of Paying Comes Saving? Sustainability 2019, 11, 568. https://doi.org/10.3390/su11030568

Van Hove L, Dubus A. M-PESA and Financial Inclusion in Kenya: Of Paying Comes Saving? Sustainability. 2019; 11(3):568. https://doi.org/10.3390/su11030568

Chicago/Turabian StyleVan Hove, Leo, and Antoine Dubus. 2019. "M-PESA and Financial Inclusion in Kenya: Of Paying Comes Saving?" Sustainability 11, no. 3: 568. https://doi.org/10.3390/su11030568

APA StyleVan Hove, L., & Dubus, A. (2019). M-PESA and Financial Inclusion in Kenya: Of Paying Comes Saving? Sustainability, 11(3), 568. https://doi.org/10.3390/su11030568