Factors Affecting Local Governments’ Public–Private Partnership Adoption in Urban China

Abstract

1. Introduction

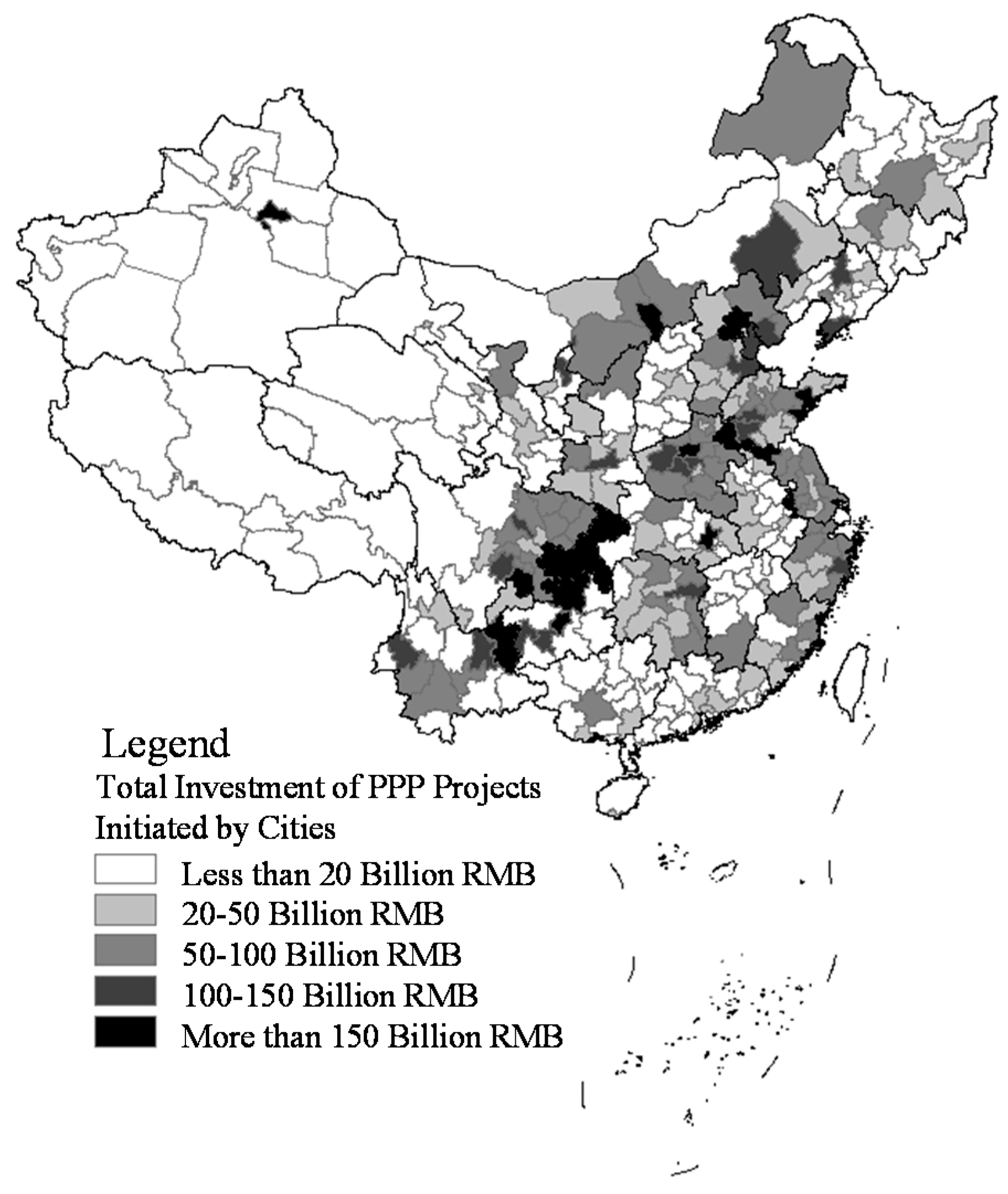

2. PPP Development in China

3. Theoretical Analysis and Hypothesis

3.1. Theoretical Analysis

3.2. Hypotheses

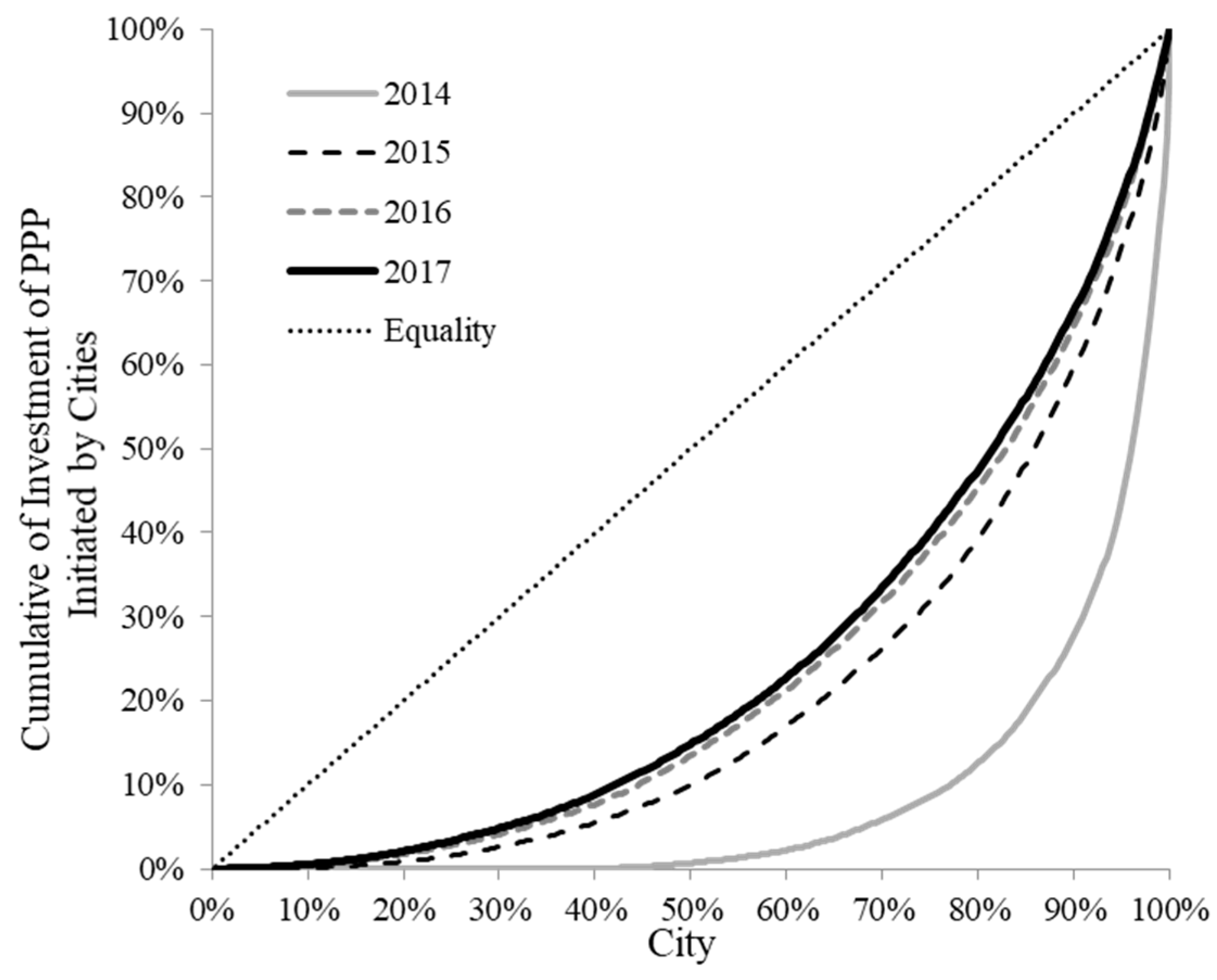

4. Data and Method

4.1. Data and Variables

4.2. Empirical Method

5. Empirical Results

5.1. Impact of Factors on PPP Projects Initiated by Local Governments

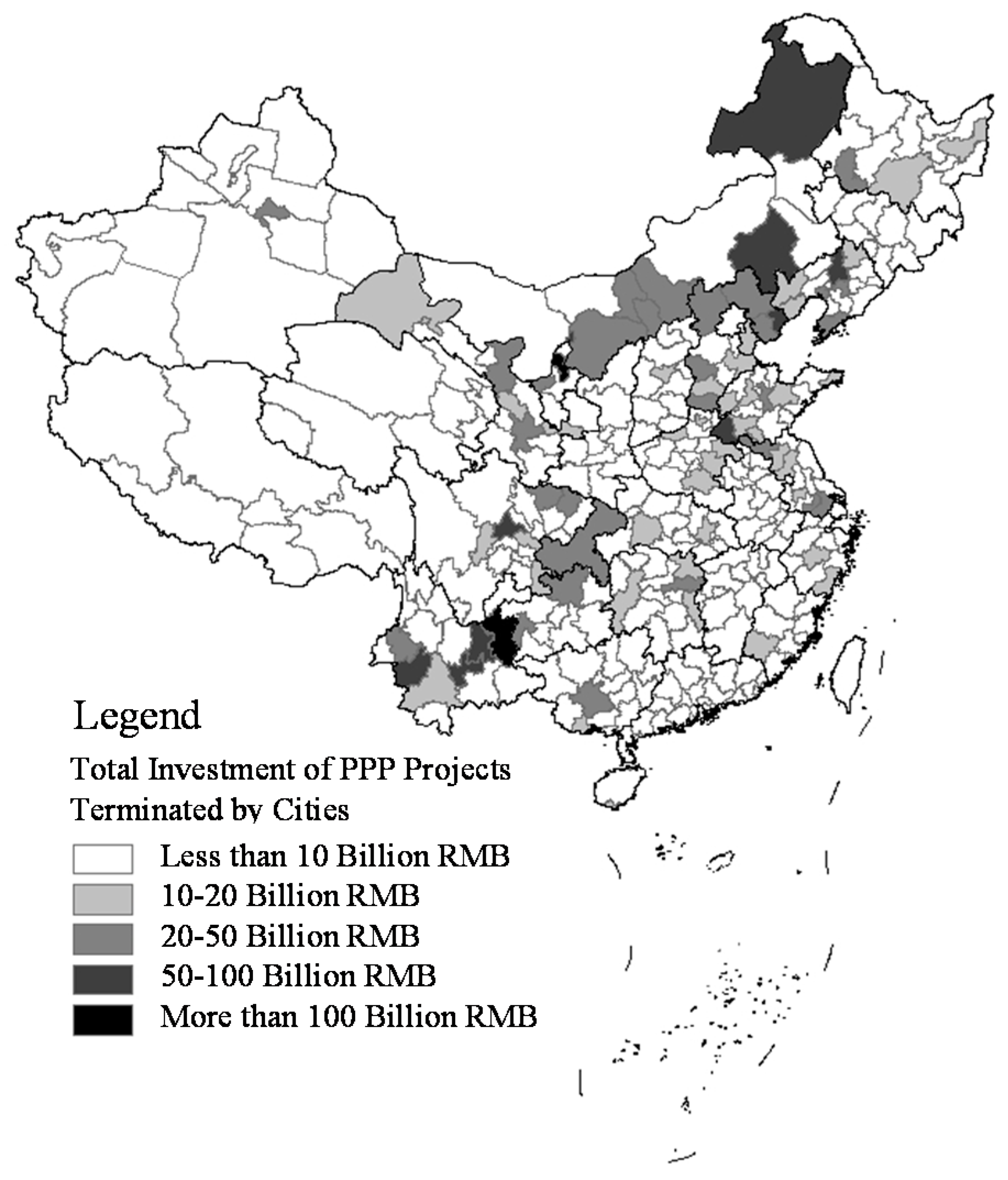

5.2. Factors Impacting the Withdrawal of PPP Projects

6. Conclusions and Policy Implications

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Hodge, G.A.; Greve, C. Public–private partnerships: An international performance review. Public Admin. Rev. 2007, 67, 545–558. [Google Scholar] [CrossRef]

- Ke, Y.; Wang, S.; Chan, A.; Lam, P.T. Preferred risk allocation in China’s public–private partnership (PPP) projects. Int. J. Proj. Manag. 2010, 28, 482–492. [Google Scholar] [CrossRef]

- Cheng, Z.; Ke, Y.; Lin, J.; Yang, Z.; Cai, J. Spatio-temporal dynamics of public private partnership projects in China. Int. J. Proj. Manag. 2016, 34, 1242–1251. [Google Scholar] [CrossRef]

- Chen, C.; Li, D.; Man, C. Toward Sustainable Development? A Bibliometric Analysis of PPP-Related Policies in China between 1980 and 2017. Sustainability 2019, 11, 142. [Google Scholar] [CrossRef]

- Tan, J.; Zhao, J.Z. The Rise of Public–Private Partnerships in China: An Effective Financing Approach for Infrastructure Investment? Public Admin. Rev. 2019. [Google Scholar] [CrossRef]

- Wang, H.M.; Xiong, W.; Wu, G.D.; Zhu, D.J. Public-private partnership in Public Administration discipline: A literature review. Public Manag. Rev. 2018, 20, 293–316. [Google Scholar] [CrossRef]

- Zheng, S.; Xu, K.; He, Q.; Fang, S.; Zhang, L. Investigating the sustainability performance of ppp-type infrastructure projects: A case of China. Sustainability 2018, 10, 4162. [Google Scholar] [CrossRef]

- Ross, T.W.; Yan, J. Comparing Public–Private Partnerships and Traditional Public Procurement: Efficiency vs. Flexibility. J. Comp. Policy Anal. Res. Pract. 2015, 17, 448–466. [Google Scholar] [CrossRef]

- Fernandes, C.; Ferreira, M.; Moura, F. PPPs—True Financial Costs and Hidden Returns. Transp. Rev. 2016, 36, 207–227. [Google Scholar] [CrossRef]

- Slavov, S.N. Public Versus Private Provision of Public Goods. J. Public Econ. 2014, 16, 222–258. [Google Scholar] [CrossRef]

- Biondi, Y. Cost of capital, discounting and relational contracting: Endogenous optimal return and duration for joint investment projects. Appl. Econ. 2011, 43, 4847–4864. [Google Scholar] [CrossRef]

- Wang, G.; Xue, Y.; Skibniewski, M.; Song, J.; Lu, H. Analysis of Private Investors Conduct Strategies by Governments Supervising Public-Private Partnership Projects in the New Media Era. Sustainability 2018, 10, 4723. [Google Scholar] [CrossRef]

- Chou, J.S.; Pramudawardhani, D. Cross-country comparisons of key drivers, critical success factors and risk allocation for public-private partnership projects. Int. J. Proj. Manag. 2015, 33, 1136–1150. [Google Scholar] [CrossRef]

- Heald, D. Value for money tests and accounting treatment in PFI schemes. Account. Audit. Account. J. 2003, 16, 342–371. [Google Scholar] [CrossRef]

- Odoemena, A.T.; Horita, M.A. Strategic analysis of contract termination in public–private partnerships: Implications from cases in sub-Saharan Africa. Constr. Manag. Econ. 2018, 36, 96–108. [Google Scholar] [CrossRef]

- Yehoue, M.E.B.; Hammami, M.; Ruhashyankiko, J.F. Determinants of Public-Private Partnerships in Infrastructure; International Monetary Fund: Washington, DC, USA, 2006. [Google Scholar]

- Albalate, D.; Bel, G.; Geddes, R.R. Recovery risk and labor costs in public–private partnerships: Contractual choice in the US water industry. Local Gov. Stud. 2013, 39, 332–351. [Google Scholar] [CrossRef]

- Girth, A.M. What Drives the Partnership Decision? Examining Structural Factors Influencing Public-Private Partnerships for Municipal Wireless Broadband. Int. Public Manag. J. 2014, 17, 344–364. [Google Scholar] [CrossRef]

- Wang, Y.; Zhao, Z.J. Motivations, obstacles, and resources: Determinants of public-private partnership in state toll road financing. Public Perform. Manag. Rev. 2014, 37, 679–704. [Google Scholar] [CrossRef]

- Yang, Y.; Hou, Y.; Wang, Y. On the Development of Public–Private Partnerships in Transitional Economies: An Explanatory Framework. Public Admin. Rev. 2013, 73, 301–310. [Google Scholar] [CrossRef]

- Scott, W.R. Organizations and Organizing: Rational, Natural and Open Systems Perspectives; Routledge: Abingdon upon Thames, UK, 2015. [Google Scholar]

- Shen, L.; Tam, V.W.; Gan, L.; Ye, K.; Zhao, Z. Improving sustainability performance for public-private-partnership (PPP) projects. Sustainability 2016, 8, 289. [Google Scholar] [CrossRef]

- Démurger, S. Infrastructure development and economic growth: An explanation for regional disparities in China? J. Comp. Econ. 2001, 29, 95–117. [Google Scholar] [CrossRef]

- Cong, X.; Ma, L. Performance evaluation of public-private partnership projects from the perspective of efficiency, economic, effectiveness, and equity: A study of residential renovation projects in China. Sustainability 2018, 10, 1951. [Google Scholar] [CrossRef]

- Cui, C.; Liu, Y.; Hope, A.; Wang, J. Review of studies on the public–private partnerships (PPP) for infrastructure projects. Int. J. Proj. Manag. 2018, 36, 773–794. [Google Scholar] [CrossRef]

- Berry, F.S.; Berry, W.D. State lottery adoptions as policy innovations: An event history analysis. Am. Polit. Sci. Rev. 1990, 84, 395–415. [Google Scholar] [CrossRef]

- English, L.M.; Guthrie, J. Driving privately financed projects in Australia: What makes them tick? Account. Audit. Account. J. 2003, 16, 493–511. [Google Scholar] [CrossRef]

- Glasser, B.L. Economic Development and Political Reform: The Impact of External Capital on the Middle East; Edward Elgar Publishing: Trotterham, UK, 2001. [Google Scholar]

- Liang, Y.; Shi, K.; Wang, L.; Xu, J. Local Government Debt and Firm Leverage: Evidence from China. Asian Econ. Policy R. 2017, 12, 210–232. [Google Scholar] [CrossRef]

- Panayides, P.M.; Parola, F.; Lam, J.S.L. The effect of institutional factors on public–private partnership success in ports. Transp. Res. Part A Policy Pract. 2015, 71, 110–127. [Google Scholar] [CrossRef]

- Zhang, S.; Gao, Y.; Feng, Z.; Sun, W. PPP Application in Infrastructure Development in China: Institutional Analysis and Implications. Int. J. Proj. Manag. 2015, 33, 497–509. [Google Scholar] [CrossRef]

- Henisz, W.J. The institutional environment for economic growth. Econ. Polit. 2000, 12, 1–31. [Google Scholar] [CrossRef]

- Van Ham, H.; Koppenjan, J. Building public-private partnerships: Assessing and managing risks in port development. Public Manag. Rev. 2001, 3, 593–616. [Google Scholar] [CrossRef]

- Brewer, B.; Hayllar, M.R. CAPAM Symposium on Networked Government: Building public trust through public–private partnerships. Int. Rev. Adm. Sci. 2005, 71, 475–492. [Google Scholar] [CrossRef]

- Sanghi, A.; Sundakov, A.; Hankinson, D. Designing and Using Public-Private Partnership Units in Infrastructure: Lessons from Case Studies around the World; PPIAF—GRIDLINES; World Bank: Washington, DC, USA, 2007; pp. 1–5. [Google Scholar]

- Xu, C. The Fundamental Institutions of China’s Reforms and Development. J. Econ. Lit. 2011, 49, 1076–1151. [Google Scholar] [CrossRef]

- Bucovetsky, S. Public input competition. J. Public Econ. 2005, 89, 1763–1787. [Google Scholar] [CrossRef]

- Cai, H.; Treisman, D. Does competition for capital discipline governments? Decentralization, globalization, and public policy. Am. Econ. Rev. 2005, 95, 817–830. [Google Scholar] [CrossRef]

- Keen, M.; Marchand, M. Fiscal competition and the pattern of public spending. J Public. Econ. 1997, 66, 33–53. [Google Scholar] [CrossRef]

- Bo, L.; Mear, F.C.; Huang, J. New Development: China’s Debt Transparency and the Case of Urban Construction Investment Bonds. Public Money Manag. 2017, 37, 225–230. [Google Scholar] [CrossRef]

- Bai, C.; Hsieh, C.; Zheng, M. The Long Shadow of a Fiscal Expansion; National Bureau of Economic Research: Cambridge, MA, USA, 2016. [Google Scholar]

- Jin, H.; Qian, Y.; Weingast, B.R. Regional decentralization and fiscal incentives: Federalism, Chinese style. J. Public Econ. 2005, 89, 1719–1742. [Google Scholar] [CrossRef]

- Tao, R.; Su, F.; Liu, M.; Cao, G. Land leasing and local public finance in China’s regional development: Evidence from prefecture-level cities. Urban Stud. 2010, 47, 2217–2236. [Google Scholar]

- Wu, Q.; Li, Y.; Yan, S. The incentives of China’s urban land finance. Land Use Policy 2015, 42, 432–442. [Google Scholar] [CrossRef]

- Azuma, Y.; Kurihara, J. Examining China’s Local Government Fiscal Dynamics: With a Special Emphasis on Local Investment Companies (LICs)’. Politico-Econ. Comment. 2011, 5, 121–140. [Google Scholar]

- Fan, J.P.; Rui, O.M.; Zhao, M. Public governance and corporate finance: Evidence from corruption cases. J. Comp. Econ. 2008, 36, 343–364. [Google Scholar] [CrossRef]

- Li, K.; Yue, H.; Zhao, L. Ownership, institutions, and capital structure: Evidence from China. J. Comp. Econ. 2009, 37, 471–490. [Google Scholar] [CrossRef]

- Fan, G.; Wang, X.; Zhu, H. NERI Index of Marketization of China’s Provinces; National Economic Research Institute: Beijing, China, 2003. [Google Scholar]

- McDonald, J.F.; Moffitt, R.A. The Uses of Tobit Analysis. Rev. Econ. Stat. 1980, 62, 318–321. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Variable | Definition | N | Mean | SD | Min | Max |

|---|---|---|---|---|---|---|

| Dependent Variables | ||||||

| INVEST_PPP | Per capita investment in PPP initiated by local governments; in 104 RMB | 1144 | 0.308 | 0.609 | 0 | 9.296 |

| INVEST_ECO | Per capita investment in PPP for economic infrastructure initiated by local governments; in 104 RMB | 1144 | 0.268 | 0.548 | 0 | 7.456 |

| INVEST_SOC | Per capita investment in PPP for social infrastructure initiated by local governments; in 104 RMB | 1144 | 0.040 | 0.100 | 0 | 1.839 |

| WITHDRAW | Per capita investment in PPP for those projects that are withdrawn by their initiator; in 104 RMB | 1144 | 0.130 | 0.464 | 0 | 8.986 |

| NWITHDRAW | Per capita investment in PPP for those projects that are not withdrawn by their initiator; in 104 RMB | 1144 | 0.178 | 0.296 | 0 | 2.902 |

| WITHDRAW_ECO | Per capita investment in PPP for those economic projects that are withdrawn by their initiator; in 104 RMB | 1144 | 0.115 | 0.420 | 0 | 7.388 |

| WITHDRAW_SOC | Per capita investment in PPP for those economic projects that are withdrawn by their initiator; in 104 RMB | 1144 | 0.152 | 0.269 | 0 | 2.885 |

| Infrastructure Shortage (IS) | ||||||

| GDPPC | Per capita gross domestic product (GDP); in 104 RMB | 1144 | 6.175 | 3.608 | 0.413 | 43.932 |

| D_GDPPC | Growth rate in annual per capita GDP | 1144 | 0.073 | 0.449 | −0.903 | 9.511 |

| INFRA_STOCK | The ratio of fiscal expenditure for construction, maintenance, and management of public services to GDP | 1144 | 0.046 | 0.078 | 0.000 | 1.305 |

| Financial Pressure (FP) | ||||||

| BUDGET_DEFICIT | Gap between fiscal revenue and fiscal expenditure accounts for the proportion of fiscal expenditure | 1144 | 0.514 | 0.231 | −1.107 | 0.925 |

| LAND_REVENUE | Ratio of land grant premiums to fiscal revenue | 1144 | 0.538 | 0.388 | 0.009 | 3.495 |

| DEBT | Ratio of total local government financial vehicle (LGFV) debts to GDP | 1144 | 0.177 | 0.218 | 0 | 1.521 |

| Institution Environment (IE) | ||||||

| MARKETIZATION | Index of marketization for China’s provinces calculated by Fan and Wang (2014) to capture regional disparity | 1144 | 6.946 | 1.555 | 0.620 | 9.780 |

| PRIVATERATIO | Ratio of private sectors’ employees to the total working population | 1144 | 0.916 | 0.408 | 0.056 | 3.135 |

| INTEGRITY | The government integrity index compiled by the Renmin University of China based on the data of 2016, including two main aspects: the fiscal transparency and the level of anti-corruption | 1144 | 0.216 | 0.197 | 0.003 | 1.000 |

| Control variable | ||||||

| lnPOP_UR | Logarithmic form of the permanent urban population at end of the year; in 104 RMB | 1144 | 5.260 | 0.781 | 3.213 | 7.838 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Variable | INVEST_PPP | INVEST_ECO | INVEST_SOC |

| GDPPC | −0.002 | −0.002 | 0.000 |

| (−0.261) | (−0.367) | (0.431) | |

| D_GDPPC | 0.028 | 0.026 | 0.002 |

| (0.708) | (0.716) | (0.330) | |

| INFRA_STOCK | −0.278 | −0.270 | −0.008 |

| (−1.151) | (−1.227) | (−0.201) | |

| BUDGET_DEFICIT | −0.512 *** | −0.462 *** | −0.050 ** |

| (−4.080) | (−4.043) | (−2.360) | |

| LAND_REVENUE | 0.025 | 0.021 | 0.004 |

| (0.477) | (0.431) | (0.503) | |

| DEBT | 0.277 *** | 0.273 *** | 0.004 |

| (2.762) | (2.985) | (0.260) | |

| MARKETIZATION | −0.022 | −0.028 | 0.006 |

| (–0.272) | (–0.382) | (0.446) | |

| PRIVATERATIO | 0.102 ** | 0.088 ** | 0.014 * |

| (2.263) | (2.154) | (1.791) | |

| INTEGRITY | −0.004 | −0.004 | 0.000 |

| (−0.985) | (−1.083) | (0.009) | |

| lnPOP_UR | −0.144 *** | −0.122 *** | −0.023 *** |

| (−4.897) | (−4.531) | (−4.570) | |

| Constant | 1.219 ** | 1.124 ** | 0.095 |

| (2.233) | (2.261) | (1.028) | |

| 0.520 *** | 0.474 *** | 0.088 *** | |

| (47.833) | (47.833) | (47.833) | |

| PRO FE | Yes | Yes | Yes |

| YEAR FE | Yes | Yes | Yes |

| Observations (N) | 1144 | 1144 | 1144 |

| Log-likelihood | −875.416 | −768.361 | 1160.349 |

| χ2 | 424.947 | 384.642 | 335.123 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variable | NWITHDRAW | WITHDRAW | WITHDRAW_ECO | WITHDRAW_SOC |

| GDPPC | −0.003 | 0.001 | 0.002 | −0.001 |

| (−0.748) | (0.255) | (0.397) | (−0.844) | |

| D_GDPPC | 0.035 | −0.007 | −0.008 | 0.001 |

| (1.597) | (−0.243) | (−0.303) | (0.209) | |

| INFRA_STOCK | −0.048 | −0.222 | −0.213 | −0.011 |

| (−0.349) | (−1.154) | (−1.232) | (−0.416) | |

| BUDGET_DEFICIT | −0.209 *** | −0.297 *** | −0.268 *** | −0.030 ** |

| (−2.945) | (−2.966) | (−2.973) | (−2.204) | |

| LAND_REVENUE | −0.018 | 0.042 | 0.040 | 0.003 |

| (−0.587) | (1.008) | (1.050) | (0.463) | |

| DEBT | 0.055 | 0.221 *** | 0.198 *** | 0.023 ** |

| (0.969) | (2.713) | (2.711) | (2.085) | |

| MARKETIZATION | −0.012 | −0.010 | −0.010 | 0.001 |

| (−0.261) | (−0.145) | (−0.178) | (0.092) | |

| PRIVATERATIO | 0.060 ** | 0.041 | 0.034 | 0.008 |

| (2.341) | (1.114) | (1.025) | (1.524) | |

| INTEGRITY | −0.002 | −0.002 | −0.002 | −0.000 |

| (−0.804) | (−0.648) | (−0.712) | (−0.080) | |

| lnPOP_UR | −0.055 *** | −0.089 *** | −0.080 *** | −0.010 *** |

| (−3.284) | (−3.717) | (−3.707) | (−2.928) | |

| Constant | 0.520 * | 0.691 | 0.638 | 0.055 |

| (1.680) | (1.552) | (1.600) | (0.913) | |

| 0.295 *** | 0.396 *** | 0.361 *** | 0.056 *** | |

| (47.833) | (41.404) | (41.402) | (41.410) | |

| PRO FE | Yes | Yes | Yes | Yes |

| YEAR FE | Yes | Yes | Yes | Yes |

| Observations (N) | 1144 | 1144 | 1144 | 1144 |

| Log-likelihood | −225.475 | −584.461 | −473.505 | 1670.281 |

| χ2 | 515.654 | 184.915 | 184.956 | 142.667 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, B.; Zhang, L.; Wu, J.; Wang, S. Factors Affecting Local Governments’ Public–Private Partnership Adoption in Urban China. Sustainability 2019, 11, 6831. https://doi.org/10.3390/su11236831

Zhang B, Zhang L, Wu J, Wang S. Factors Affecting Local Governments’ Public–Private Partnership Adoption in Urban China. Sustainability. 2019; 11(23):6831. https://doi.org/10.3390/su11236831

Chicago/Turabian StyleZhang, Bo, Li Zhang, Jing Wu, and Shouqing Wang. 2019. "Factors Affecting Local Governments’ Public–Private Partnership Adoption in Urban China" Sustainability 11, no. 23: 6831. https://doi.org/10.3390/su11236831

APA StyleZhang, B., Zhang, L., Wu, J., & Wang, S. (2019). Factors Affecting Local Governments’ Public–Private Partnership Adoption in Urban China. Sustainability, 11(23), 6831. https://doi.org/10.3390/su11236831