Could Gwadar Port in Pakistan Be a New Gateway? A Network Simulation Approach in the Context of the Belt and Road Initiative

Abstract

1. Introduction

2. Literature Review

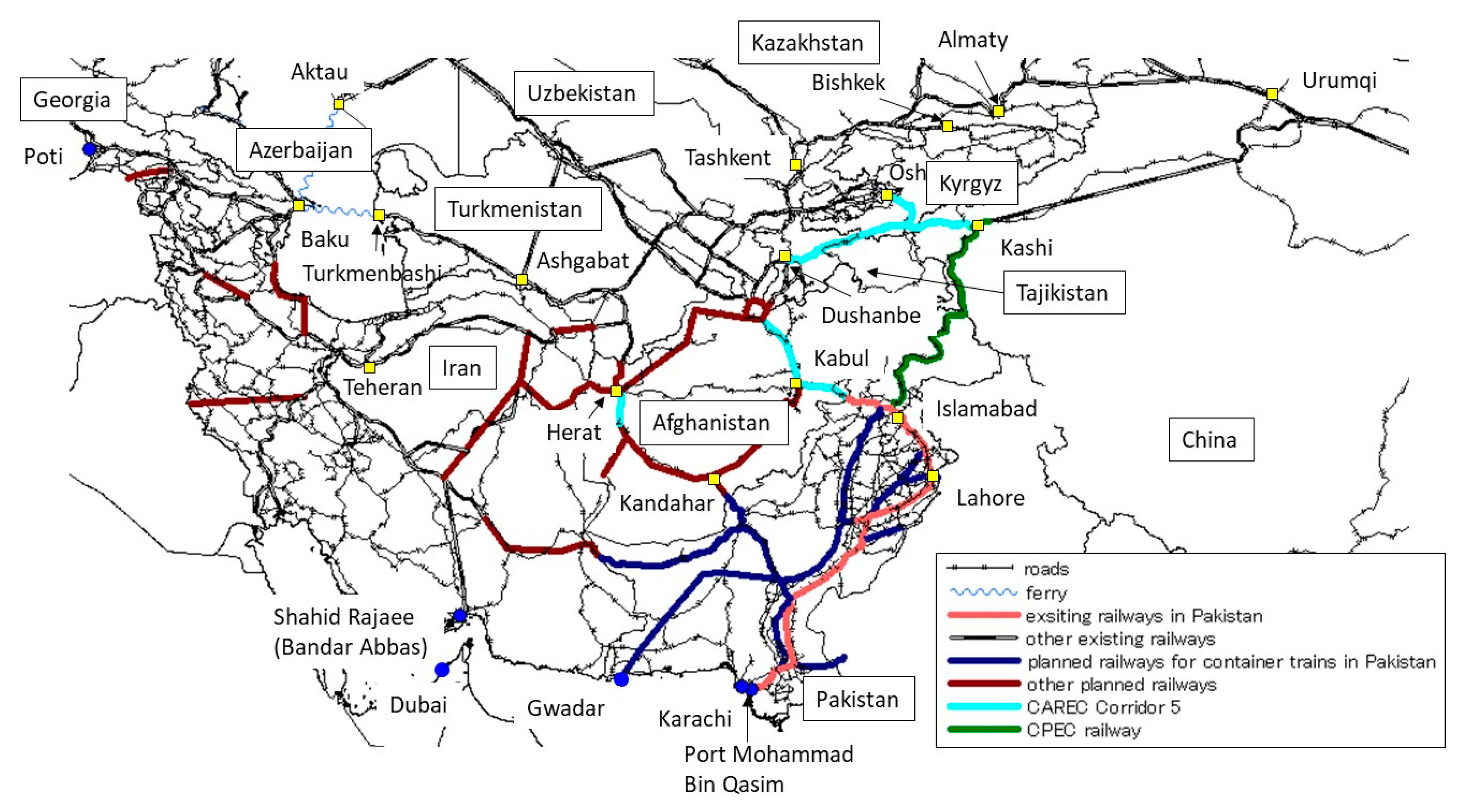

3. Pakistani Seaports as a Gateway of Central Asia

4. Model

4.1. Model Structure

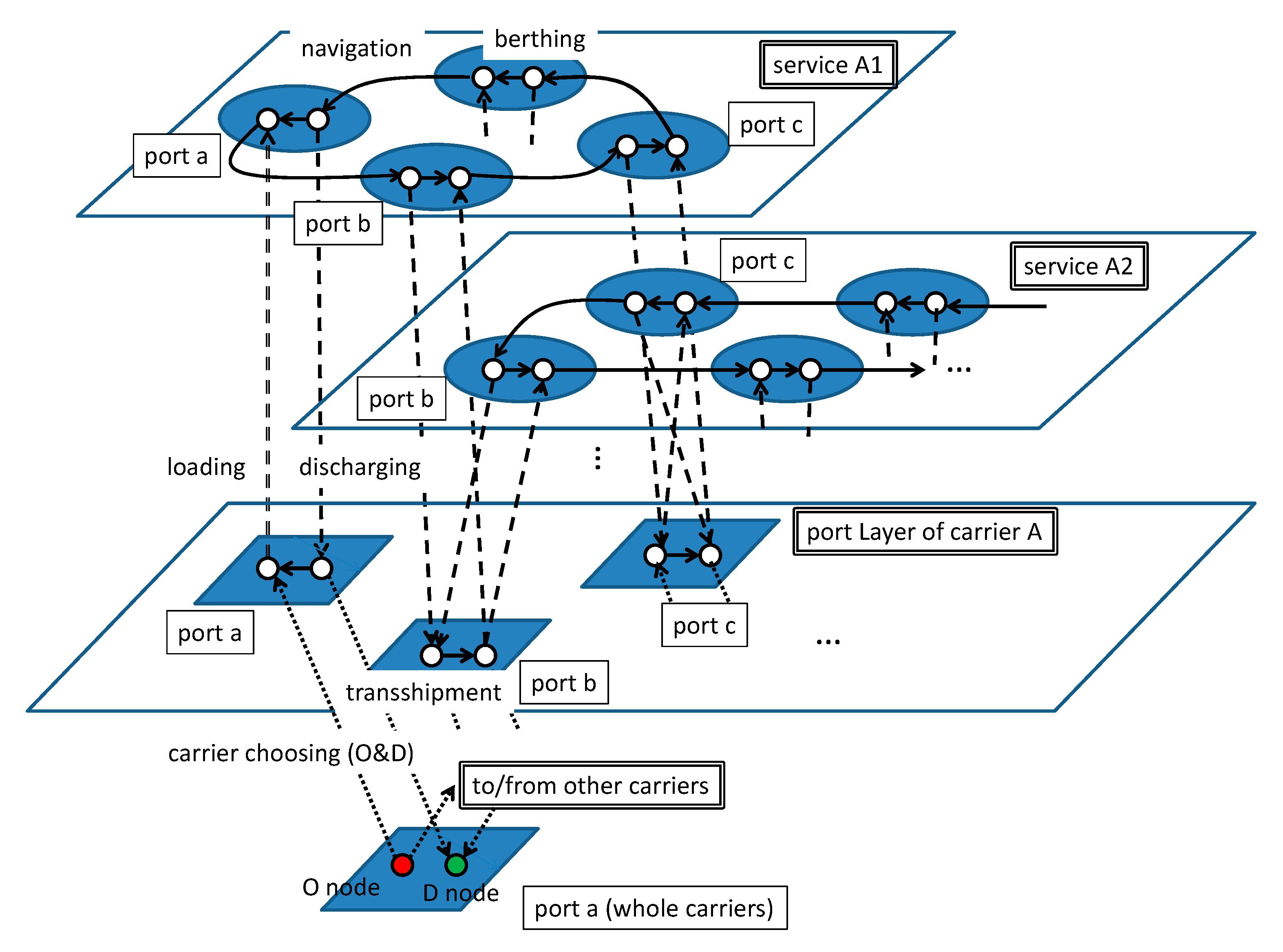

4.1.1. Super-Network Model

4.1.2. Global MS Submodel

4.1.3. Regional HT Submodel

4.2. Data

4.2.1. Ports

4.2.2. Global MS Network

4.2.3. Eurasian HT Network

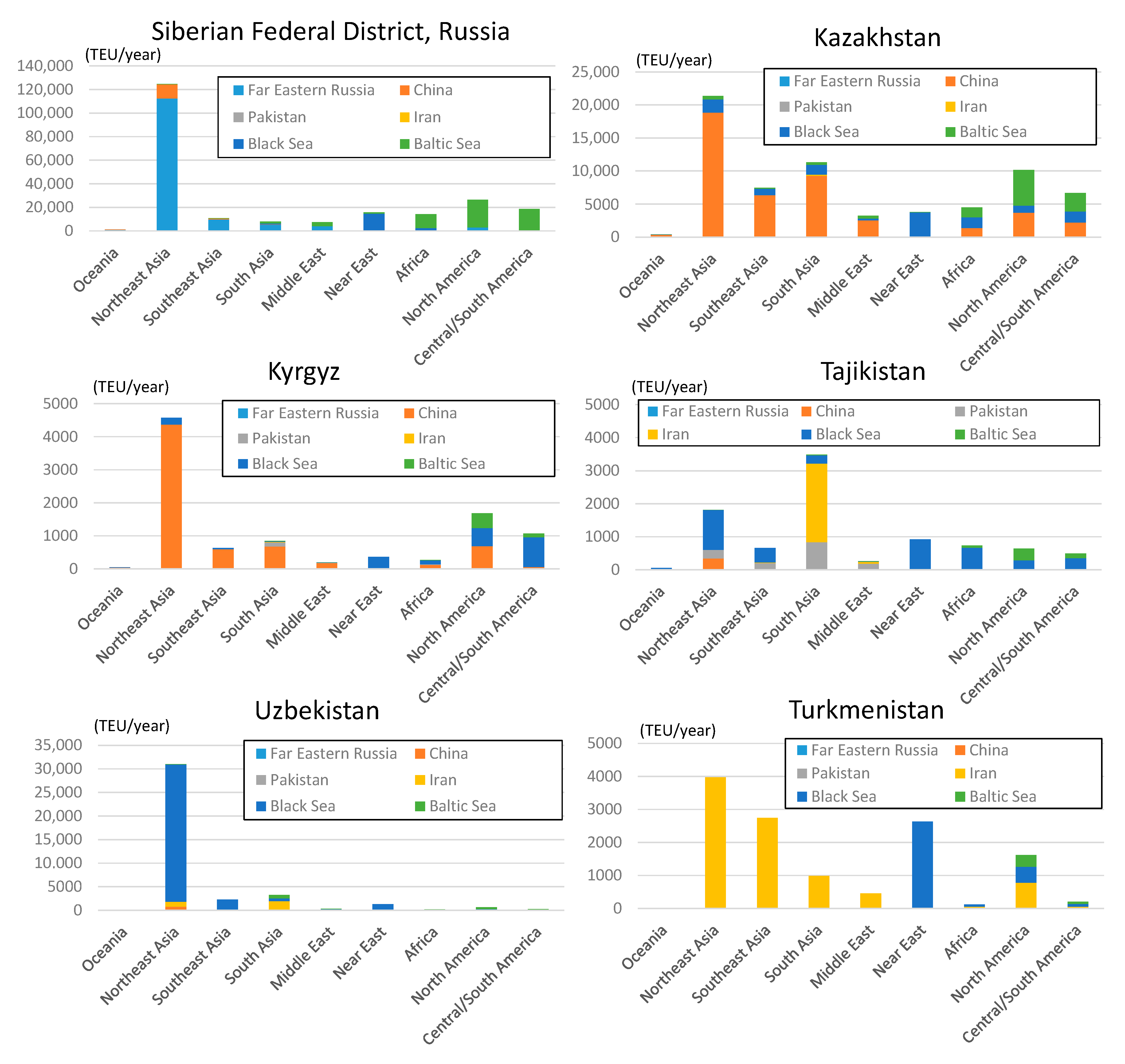

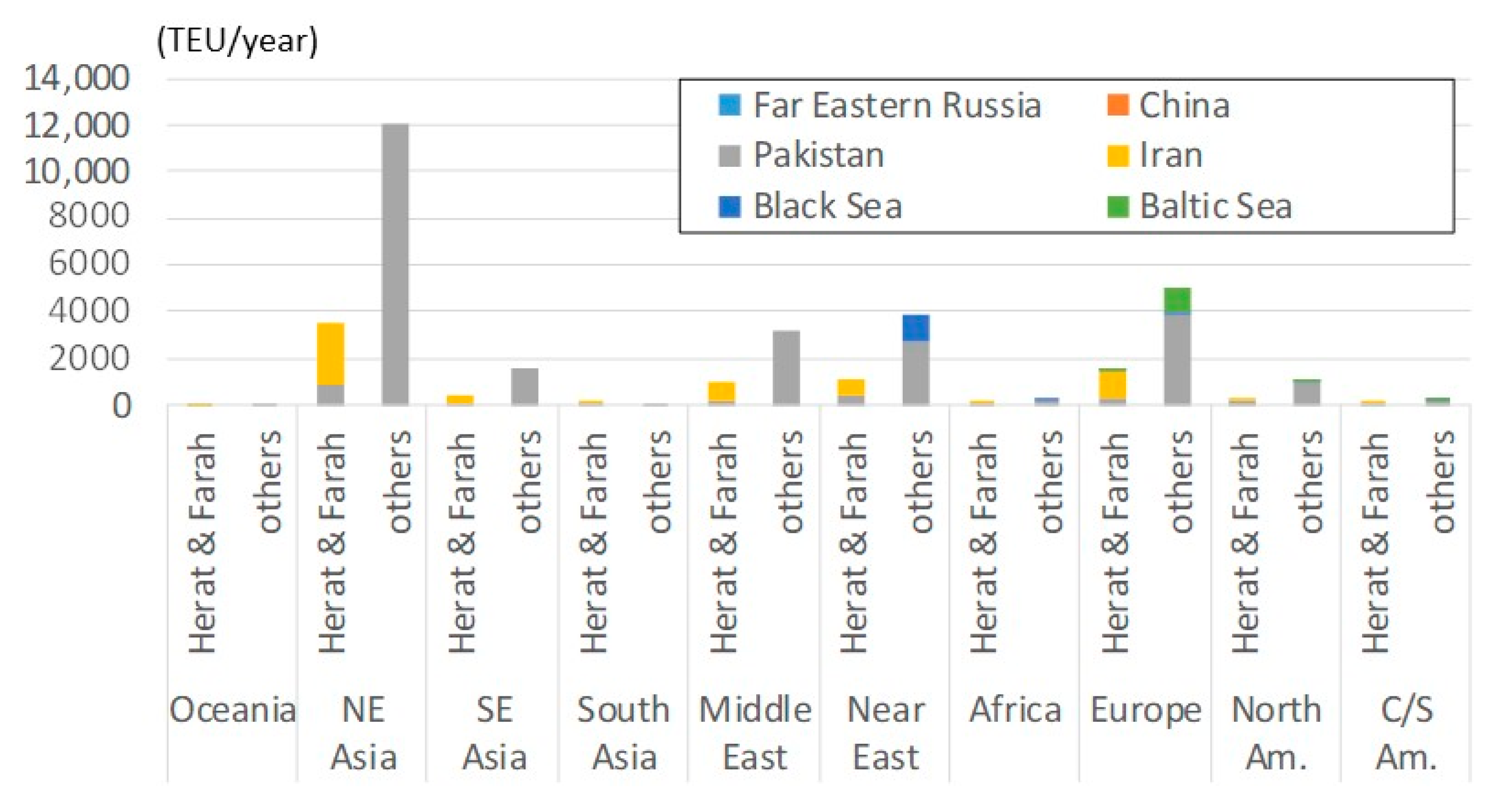

4.2.4. Container Shipping Demand between Regions (Container OD Cargo)

4.3. Model Performance

4.3.1. Port Throughput

4.3.2. Choice of Gateway Seaport

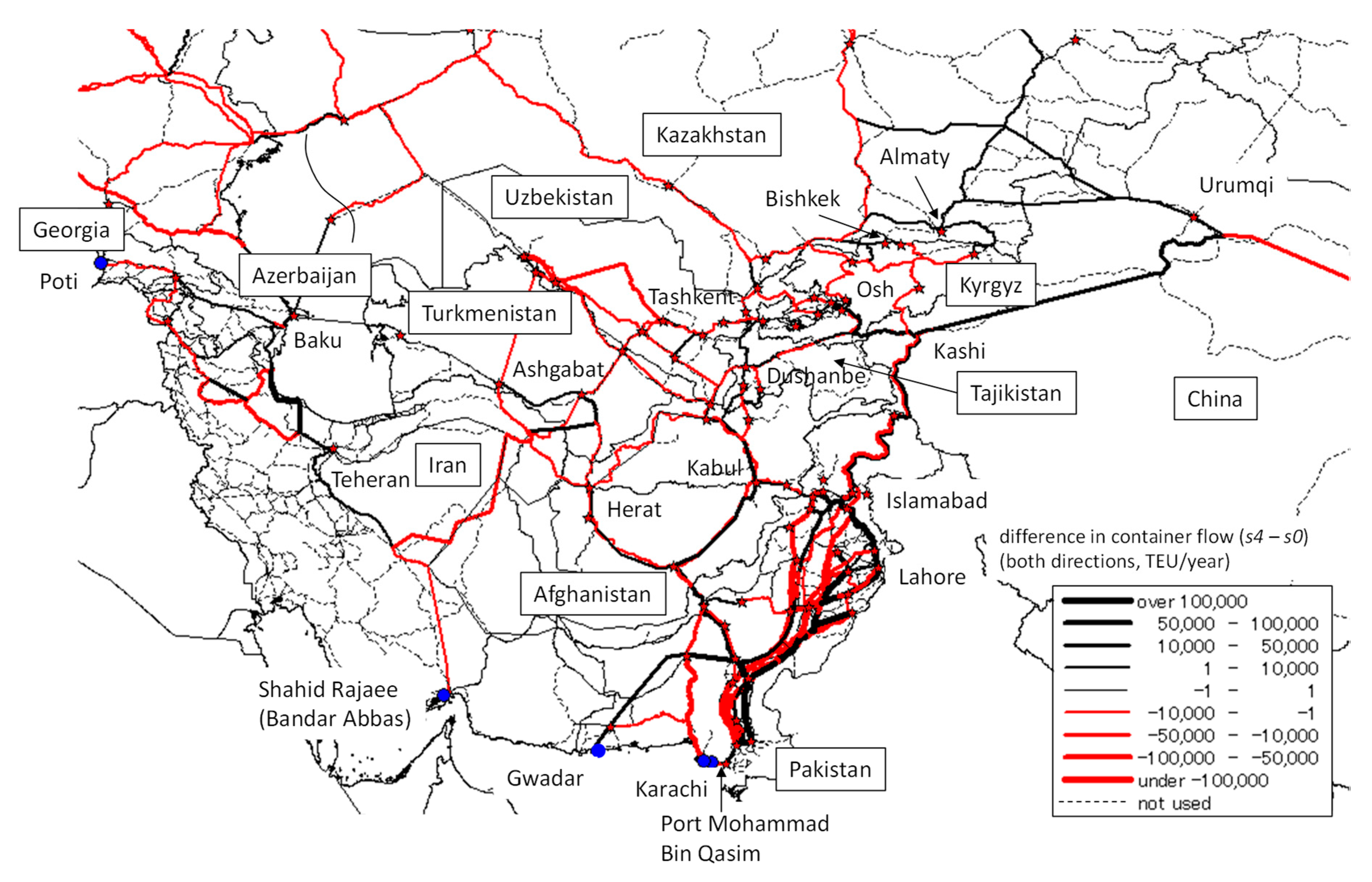

5. Scenario Analysis for the Pakistani Intermodal Network

5.1. Scenarios Prepared

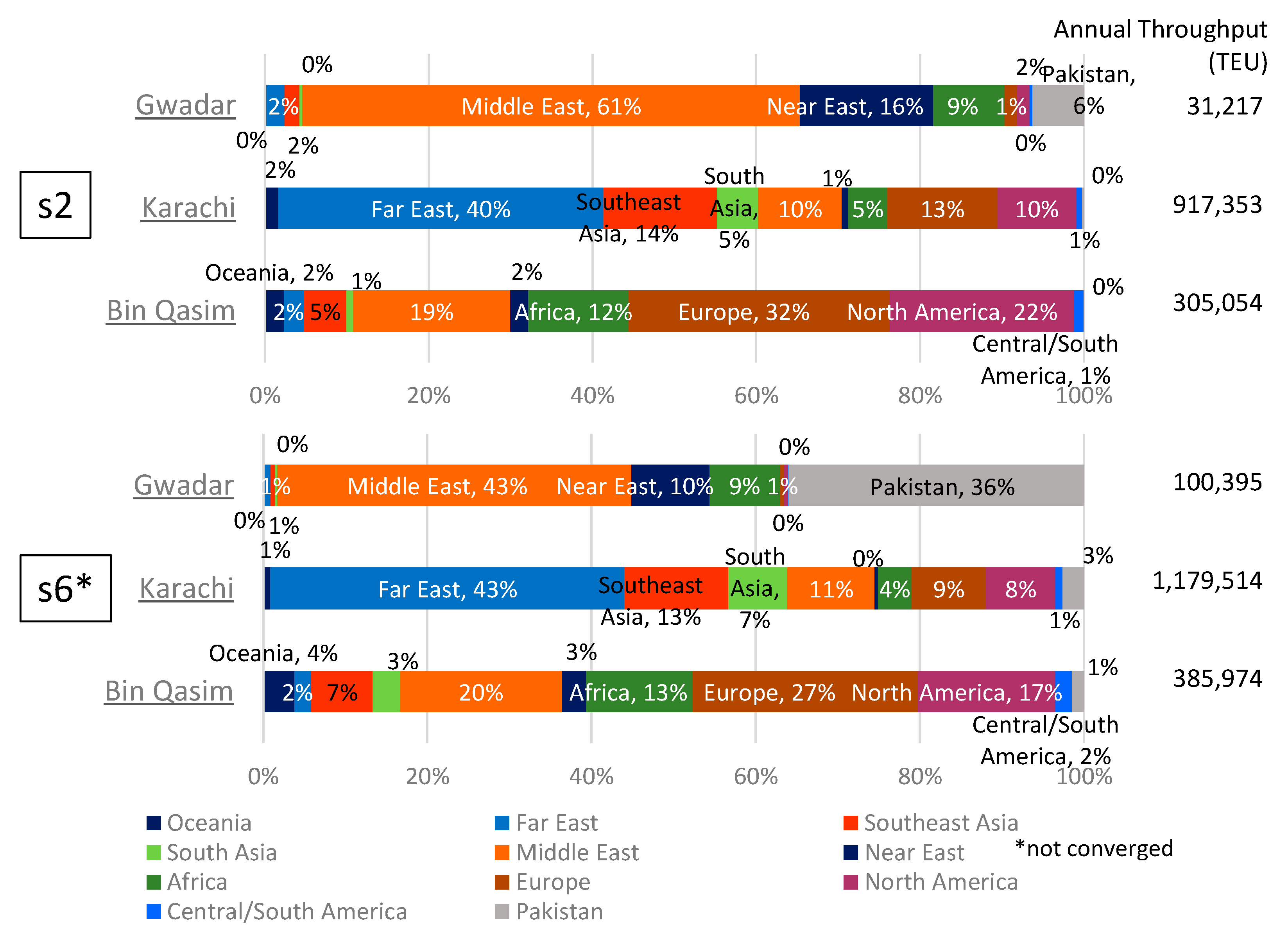

5.2. Port Throughputs and HT Flows Estimated

5.3. Estimated MS Flows

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A. Summary of the Interview Survey and Field Trip

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | Place | Date | Interviewee | Interviewee’s Organization |

|---|---|---|---|---|

| Pakistan | Karachi | July, 2015 | Ministry of Ports and Shipping | Government |

| Karachi Port Trust (KPT) | Port administrator | |||

| Karachi International Container Terminal (KICT) | Terminal operator | |||

| Pakistan International Container Terminal (PICT) | Terminal operator | |||

| DP World Karachi | Terminal operator | |||

| Sojitz Corporation, Sumitomo Corporation | Cargo owners and Investors | |||

| P.S.S Container, PAKLINK Shipping Services | Forwarders to Afghanistan | |||

| Bin Qasim | Qasim Port Authority (QPA) | Port administrator | ||

| National Industrial Park (NIP) | Special Economic Zone (SEZ) | |||

| Kazakhstan | Astana | August, 2017 | Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) | International organization (Germany) |

| Ministry of Investment and Development | Government | |||

| Kazakhstan Temir Zholy (KTZ) Express | Railway company (Container train operator) | |||

| Marubeni Corporation | Cargo owner and Investor | |||

| August, 2018 | Kazakhstan Railway | Railway company | ||

| Continental Logistics | Distribution Centre/ICD | |||

| Embassy of Japan | Diplomatic organization | |||

| Almaty | August, 2017 | Association of National Forwarders | Forwarder (railway) | |

| Globalink, Senko, Azuma Shipping, Nisshin | Logistics companies | |||

| Mitsubishi Corporation | Cargo owner and Investor | |||

| August, 2018 | European Bank for Reconstruction and Development (EBRD) Almaty Branch Office | International organization | ||

| Unico | Logistics companies | |||

| Damu Logistics | Distribution Centre | |||

| Khorgos | August, 2017 | International Center for Boundary Cooperation (ICBC) | Free Trade Zone (FTZ) | |

| Khorgos SEZ | SEZ, Dry port | |||

| Aktau | August, 2018 | Aktau Port | Terminal operator | |

| Aktau North Port | Terminal operator | |||

| Uzbekistan | Tashkent | September, 2009 | State Customs Committee | Government |

| Uzbek Agency of Road and River Transportation | Government | |||

| State-Joint-Stock Railway Company (SJSRC) | Railway company | |||

| Association of International Road Carriers | Logistics companies | |||

| Association of International Forwarders of Uzbekistan | Forwarders | |||

| Inland Container Depot | Dry Port (railway) | |||

| November, 2013 | Tashkent office, Japan External Trade Organization (JETRO) | Public organization | ||

| Itochu Corporation | Cargo owner and Investor | |||

| Turkmenistan | Ashkhabad | November, 2013 | Embassy of Japan | Diplomatic organization |

| Sojitz Corporation | Cargo owner and Investor | |||

| Kyrgyz | Bishkek | November, 2013 | Freight Operators Association of the Kyrgyzstan (KGZ FOA) | Logistics companies |

| Tajikistan | Dushanbe | August, 2017 | JICA Tajikistan office | International organization |

| Ministry of Transport | Government | |||

| Azerbaijan | Baku | November, 2013 | Transport Corridor Europe/Caucasus/Asia (TRACECA) | International organization (EU) |

| Azerbaijan International Road Carriers Association (ABADA) | Logistics companies | |||

| Itochu Corporation | Cargo owner and Investor | |||

| Georgia | Tbilisi | August, 2018 | JICA Georgia office | International organization |

| Anaklia Development Consortium | Terminal developer | |||

| Association of Freight Forwarders of Georgia | Forwarders | |||

| Poti | APM Terminals Poti | Terminal operator | ||

| China | Liangyungang | December, 2006 | Lianyungang Port Company | Port administrator/Terminal operator |

| Urumqi | November, 2013 | Xinjiang Logistics Association | Logistics association/University | |

| Xinjiang Huacheng International Transportation service CO., LTD. | Logistics company | |||

| DB Schenker Urumuch branch | Logistics company | |||

| Russia | Vladivostok | December, 2012 | Primorsky Krai Government | Local government |

| Pacific Strategy Development Center, Regional Fund, Administration of Primorsky Territory | Governmental research institute | |||

| Commercial Port of Vladivostok | Terminal operator | |||

| Far Eastern Marine Research, Design and Technology Institute (FEMRI) | Research institute | |||

| Vostochny | Vostochnaya Stevedoring Company (VSC) | Terminal operator | ||

| Vostochny Port | Terminal operator | |||

| Rosmorport Vostochny Branch | Port administrator (landlord) | |||

| Japan | Tokyo | November, 2013 | ITS Nippon | Logistics company, Consultant |

| June, 2017 | Toyota Tsusho Co | Cargo owner and Investor | ||

| July, 2017 | Senko Co. | Logistics company |

| Visiting Point | Date | Visiting Route | Used Transport |

|---|---|---|---|

| Ala Shankou (China)—Dostik (Kazakhstan) | 17 August 2008 | crossed from China to Kazakh | rail |

| Chorgos (China)—Khorgos (Kazakhstan) | 5 August 2017 | crossed from Kazakh to China | car |

| Irkeshtam (China)—Irkeshtam (Kyrgyz) | 7 August 2017 | crossed from China to Kyrgyz | car |

| Korday (Kazakhstan)—Akjol (Kyrgyz) | 18 August 2008 | crossed from Kazakh to Kyrgyz | car |

| 6 November 2013 | accessed from the Kyrgyz side | car | |

| Karasu (Kazakhstan)—Aktilek (Kyrgyz) | 6 November 2013 | accessed from the Kyrgyz side | car |

| Konsybaeva (Kazakhstan)—Yallama (Uzbekistan) | 2 October 2009 | accessed from the Uzbek side | car |

| 6 November 2013 | accessed from the Uzbek side | car | |

| Dustlik (Uzbekistan)—Osh (Kyrgyz) | 8 August 2017 | crossed from Kyrgyz to Uzbek | car |

| Jartepa (Uzbekistan)—Sarazm (Tajikistan) | 2 October 2009 | accessed from the Uzbek side | car |

| Andarkhon (Uzbekistan)—Patar (Tajikistan) | 8 August 2017 | crossed from Uzbek to Tajik | car |

| Alat (Uzbekistan)—Farab (Turkmenistan) | 30 September 2009 | accessed from the Uzbek side | car |

| 5 November 2013 | crossed from Turkmen to Uzbek | car | |

| Artyk (Turkmenistan)—Lotfabad (Iran) | 4 November 2013 | accessed from the Turkmen side | car |

References

- Shepherd, B.; Wilson, J.S. Road Infrastructure in Europe and Central Asia: Does Network Quality Affect Trade? World Bank Policy Research Working Paper (No. 4104); World Bank: Washington, DC, USA, 2006; Available online: http://documents.worldbank.org/curated/en/685631468034174351/Road-infrastructure-in-Europe-and-Central-Asia-does-network-quality-affect-trade (accessed on 29 April 2018).

- World Bank. World Development Report 2009: Reshaping Economic Geography; World Bank: Washington, DC, USA, 2009. [Google Scholar]

- Gallup, J.L.; Sachs, J.D.; Mellinger, A.D. Geography and economic development. Int. Reginal Sci. Rev. 1999, 22, 179–232. [Google Scholar] [CrossRef]

- Hall, P.; McCalla, R.J.; Comtois, C.; Slack, B. (Eds.) Integrating Seaports and Trade Corridors; Routledge: New York, NY, USA, 2010. [Google Scholar]

- Asian Development Bank (ADB). CAREC Transport and Trade Facilitation Strategy 2020. Available online: https://www.adb.org/sites/default/files/institutional-document/34107/files/carec-ttfs-2020.pdf (accessed on 29 April 2018).

- Shibasaki, R.; Iijima, T.; Kawakami, T.; Kadono, T.; Shishido, T. Network assignment model of integrating maritime and hinterland container shipping: Application to Central America. Marit. Econ. Logist. 2017, 19, 234–273. [Google Scholar] [CrossRef]

- Shibasaki, R.; Kawasaki, T. International intermodal container shipping network in South Asia: Modelling and policy simulations. Int. J. Shipp. Transp. Logist. Accepted.

- Limao, N.; Venables, A.J. Infrastructure, geographical disadvantage, transport costs, and trade. World Bank Econ. Rev. 2001, 15, 451–479. [Google Scholar] [CrossRef]

- Arvis, J.; Raballand, G.; Marteau, J. The Cost of Being Landlocked: Logistics Costs and Supply Chain Reliability; World Bank: Washington, DC, USA, 2010; Available online: https://openknowledge.worldbank.org/bitstream/handle/10986/2489/558370PUB0cost1C0disclosed071221101.pdf?sequence=1 (accessed on 29 April 2018).

- Anukoonwattaka, W.; Saggu, A. Trade performance of Asian landlocked developing economies: State of play and the way forward. Trade, Investment and Innovation, Working Paper Series No.1, United Nations Economic and Social Commission for Asia and the Pacific (UN-ESCAP). 2016. Available online: http://www.unescap.org/sites/default/files/Trade-performance-of-Asian-LLDCs.pdf (accessed on 29 April 2018).

- Kashiha, M.; Thill, J.C.; Depken, C.A. Shipping route choice across geographies: Coastal vs. landlocked countries. Transp. Res. 2016, 91E, 1–14. [Google Scholar] [CrossRef]

- Lim, S.-W.; Suthiwartnarueput, K.; Abareshi, A.; Lee, P.T.-W.; Duval, Y. Key factors in developing transit trade corridors in Northeast Asia. J. Korea Trade 2017, 21, 191–207. [Google Scholar] [CrossRef]

- Faye, M.L.; McArthur, J.W.; Sachs, J.D.; Snow, T. The challenges facing landlocked developing countries. J. Hum. Dev. 2004, 5, 31–68. [Google Scholar] [CrossRef]

- Carrere, C.; Grigoriou, C. Landlockedness, infrastructure and trade: New estimates for Central Asian countries. Centre d’Etude et de Recherches sur le Développement International (CERDI) Working Paper, No 2008.01. Available online: http://publi.cerdi.org/ed/2008/2008.01.pdf (accessed on 29 April 2018).

- Lahiri, B.; Masjidi, F.K. Landlocked countries: A way to integrate with coastal economies. J. Econ. Integr. 2012, 27, 504–519. [Google Scholar] [CrossRef]

- de Langen, P.W. Port competition and selection in contestable hinterlands, the case of Austria. Eur. J. Transp. Infrastruct. Res. 2007, 7, 1–14. [Google Scholar]

- Lihoussou, M.; Limbourg, S. Network design model for intermodal transport: The case of the hinterland of the Port of Cotonou. In Proceedings of the 4th International Conference on Information Systems, Logistics and Supply Chain. (ILS) 2012, Quebec, QC, Canada, 26–29 August 2012. [Google Scholar]

- Iwata, T.; Kato, H.; Shibasaki, R. Influence of transportation infrastructure development on freight traffic flow patterns in GMS. In Gender, Roads and Mobility in Asia; Kusakabe, K., Ed.; Practical Action Publishing: Rugby, Warwickshire, UK, 2012; pp. 25–32. [Google Scholar]

- Kawasaki, T.; Hanaoka, S.; Nguyen, L.X. Inland cargo flow modelling considering shipment time variability on cross-border transport. Transp. Plan. Technol. 2015, 38, 664–683. [Google Scholar] [CrossRef]

- Munim, Z.H.; Haralambides, H. Competition and cooperation for intermodal container transhipment: A network optimization approach. Res. Transp. Bus. Manag. 2018, 26, 87–99. [Google Scholar] [CrossRef]

- World Bank. The Impact of China on Europe and Central Asia; World Bank: Washington, DC, USA, 2009; Available online: http://www.worldbank.org/en/region/eca/publication/europe-and-central-asia-economic-update-april-2016 (accessed on 29 April 2018).

- Kurmanalieva, E.; Parpiev, Z. Geography and Trade in Central Asia. Available online: http://dx.doi.org/10.2139/ssrn.1824933 (accessed on 29 April 2018).

- Peyrouse, S.; Raballand, G. Central Asia: The New Silk Road Initiative’s questionable economic rationality. Eurasian Geogr. Econ. 2015, 56, 405–420. [Google Scholar] [CrossRef]

- Vinokurov, E.; Dzhadraliyev, M.; Shcherbanin, Y. The EurAsEC Transport Corridors; Eurasian Development Bank. 2009. Available online: http://eabr.org/general/upload/docs/EurAsEC_Trans_Cor.pdf (accessed on 29 April 2018).

- Kulipanova, E. International Transport in Central Asia: Understanding the Patterns of (Non-) Cooperation. University of Central Asia, Institute of Public Policy and Administration Working Paper. 2012, Volume 2. Available online: http://www.ucentralasia.org/Content/downloads/UCA-IPPA-WP2-International%20Transport%20in%20Central%20Asia.pdf (accessed on 29 April 2018).

- Rodemann, H.; Templar, S. The enablers and inhibitors of intermodal rail freight between Asia and Europe. J. Rail Transp. Plan. Manag. 2014, 4, 70–86. [Google Scholar] [CrossRef]

- Islam, D.M.Z.; Zunder, T.H.; Jackson, R.; Nesterova, N.; Burgess, A. The potential of alternative rail freight transport corridors between Central Europe and China. Transp. Probl. 2013, 8, 45–57. [Google Scholar]

- Rastogi, C.; Arvis, J. The Eurasian Connection Supply-Chain Efficiency along the Modern Silk Route through Central Asia; International Bank for Reconstruction and Development, World Bank: Washington, DC, USA, 2014; Available online: https://openknowledge.worldbank.org/bitstream/handle/10986/18779/888910PUB0Box300EPI199120June122014.pdf?sequence=1 (accessed on 29 April 2018).

- Bulis, A.; Skapars, R. Development of “New Silk Road” Northern branch through seaport of Riga in Latvia. Procedia-Soc. Behav. Sci. 2014, 150, 1222–1229. [Google Scholar] [CrossRef][Green Version]

- Regmi, M.B.; Hanakoka, S. Assessment of intermodal transport corridors: Cases from North-East and Central Asia. Res. Transp. Bus. Manag. 2012, 5, 27–37. [Google Scholar] [CrossRef]

- Wang, Y.; Yeo, G.-T. A Study on International Multimodal Transport Networks from Korea to Central Asia: Focus on Secondhand Vehicles. Asian J. Shipp. Logist. 2016, 32, 41–47. [Google Scholar] [CrossRef]

- Wang, Y.; Yeo, G.-T. Intermodal route selection for cargo transportation from Korea to Central Asia by adopting Fuzzy Delphi and Fuzzy ELECTRE I methods. Marit. Policy Manag. 2018, 45, 3–18. [Google Scholar] [CrossRef]

- Yousefi, H. Strategic Planning for Port Development: Improvement of Container Transit from the Iranian Southern Ports Terminals. TransNav, Int. J. Mar. Navig. Saf. Sea Transp. 2013, 7, 433–440. [Google Scholar] [CrossRef][Green Version]

- Sayareh, J. Chabahar port vs. Gwadar port: A logistics performance comparison. In Proceedings of the International Association of Maritime Economists (IAME) 2016 Conference, Hamburg, Germany, 23–26 August 2016. paper ID: 112. [Google Scholar]

- Anwar, Z. Development of infrastructural linkages between Pakistan and Central Asia. South Asian Stud. 2011, 26, 103–115. [Google Scholar]

- Masood, M.T.; Farooq, M.; Hussain, S.B. Pakistan’s potential as a transit trade corridor and transportation challenges. Pak. Bus. Rev. 2016, 18, 267–289. [Google Scholar] [CrossRef]

- Khan, S.A. Geo-economic imperatives of Gwadar Sea Port and Kashgar Economic Zone for Pakistan and China. IPRI J. 2013, 13, 87–100. [Google Scholar]

- Li, K.X.; Jin, M.; Qi, G.; Shi, W.; Ng, A.K.Y. Logistics as a driving force for development under the Belt and Road Initiative—the Chinese model for developing countries. Transp. Rev. 2017, 38, 457–478. [Google Scholar] [CrossRef]

- Lee, P.T.-W.; Hu, Z.-H.; Lee, S.-J.; Choi, K.-S.; Shin, S.-H. Research trends and agenda on the Belt and Road (B&R) initiative with a focus on maritime transport. Marit. Policy Manag. 2018, 45, 282–300. [Google Scholar] [CrossRef]

- Wang, J.J.; Yau, S. Case studies on transport infrastructure projects in belt and road initiative: An actor network theory perspective. J. Transp. Geogr. 2018, 71, 213–223. [Google Scholar] [CrossRef]

- Sheu, J.B.; Kundu, T. Forecasting time-varying logistics distribution flows in the One Belt–One Road strategic context. Transp. Res. 2018, 117E, 5–22. [Google Scholar] [CrossRef]

- Wang, S.; Yang, D.; Lu, J. A connectivity reliability-cost approach for path selection in the maritime transportation of China’s crude oil imports. Marit. Policy Manag. 2018, 45, 567–584. [Google Scholar] [CrossRef]

- Shao, Z.-Z.; Ma, Z.-J.; Sheu, J.-B.; Gao, H.O. Evaluation of large-scale transnational high-speed railway construction priority in the belt and road region. Transp. Res. 2018, 117E, 40–57. [Google Scholar] [CrossRef]

- Yang, D.; Pan, K.; Wang, S. On service network improvement for shipping lines under the one belt one road initiative of China. Transp. Res. 2018, 117E, 82–95. [Google Scholar] [CrossRef]

- Yang, D.; Jiang, L.; Ng, A.K.Y. One Belt one Road, but several routes: A case study of new emerging trade corridors connecting the Far East to Europe. Transp. Res. 2018, 117A, 190–204. [Google Scholar] [CrossRef]

- Japan External Trade Organization (JETRO). Rail and Air Transport to the Moscow and Siberia Region via Russian Far Eastern Customs. 2010. Available online: https://www.jetro.go.jp/ext_images/jfile/report/07000390/russia_foodexport.pdf (accessed on 29 April 2018). (In Japanese)

- Pleis, L.; Lliteras, R.; David, W.; Bain, M.; Hendrickson, S. The Afghanistan National Railway A Plan of Opportunity. 2014. Available online: http://ndupress.ndu.edu/Portals/68/Documents/jfq/jfq-75/jfq-75_19-27_Pleis-et-al.pdf (accessed on 31 December 2016).

- Pakistan Bureau of Statistics, Government of Pakistan. Pakistan Statistical Year Book 2016. Available online: http://www.pbs.gov.pk/sites/default/files//PAKISTAN%20STATISTICAL%20YEAR%20BOOK%2C%202016.pdf (accessed on 17 July2019).

- Neelum, N. CPEC: Gwadar Port Becomes Operational for Container Vessels. Issue Brief, Institute of Strategic Studies Islamabad. 27 March 2018. Available online: http://issi.org.pk/wp-content/uploads/2018/03/IB_Neelum_March_27_2018.pdf (accessed on 19 August 2019).

- Ministry of Railways, Government of Pakistan. Pakistan Railways Year Book 2014–15. Available online: https://www.docdroid.net/t84Dro5/pak-railways.pdf.html (accessed on 29 April 2018).

- China Pakistan Economic Corridor (CPEC). CPEC Infrastructure Projects Website. Available online: http://cpec.gov.pk/infrastructure (accessed on 29 April 2018).

- Shibasaki, R.; Usami, T.; Furuichi, M.; Teranishi, H.; Kato, H. How do the new shipping routes affect Asian LNG markets and economy?—Case of the Northern Sea Route and Panama Canal Expansion. Marit. Policy Manag. 2018, 45, 543–566. [Google Scholar] [CrossRef]

- Dial, R. A probabilistic multipath traffic assignment algorithm which obviates path enumeration. Transp. Res. 1971, 5, 83–111. [Google Scholar] [CrossRef]

- MDS Transmodal Inc. MDS Containership Databank; MDS Transmodal Inc.: Chester, UK, 2013. [Google Scholar]

- Sheffi, Y. Urban Transportation Networks: Equilibrium Analysis with Mathematical Programming Methods; Prentice-Hall, Inc.: Englewood Cliffs, NJ, USA, 1985. [Google Scholar]

- World Bank Group, Doing Business Website “Trading Across Borders” 2015 Rank. Available online: http://www.doingbusiness.org/data/exploretopics/trading-across-borders (accessed on 15 September 2015).

- American Digital Cartography Inc. (ADC). ADC World Map Version 4.0; ADC: Appleton, WI, USA, 2005. [Google Scholar]

- IHS, Inc. World Trade Service (WTS) Database. Available online: https://ihsmarkit.com/products/world-trade-service.html (accessed on 21 May 2015).

- United Nations. UN Comtrade Database. Available online: https://comtrade.un.org/ (accessed on 21 May 2015).

- Ministry of National Economy of the Republic of Kazakhstan Committee on Statistics. The Official Statistical Information, Operational Data. 2015. Available online: http://stat.gov.kz/faces/publicationsPage/publicationsOper?_adf.ctrl-state=bm75ob63i_17&_afrLoop=16789316187516983 (accessed on 29 April 2018).

- National Statistics Committee of the Kyrgyz Republic. Kyrgyzstan in Figures 2013. Available online: http://www.stat.kg/media/publicationarchive/6a89fb49-cc30-4ead-8c47-d53810976f17.pdf (accessed on 29 April 2018). (In Russian)

- Agency on Statistics under President of the Republic of Tajikistan. Socio-Economic Situation in Tajikistan January–December 2013. Available online: http://www.stat.tj/ru/img/a6069090cb7edbe5efb67aec241e9816_1359030405.pdf (accessed on 29 April 2018). (In Russian)

- State Committee of the Republic of Uzbekistan on Statistics. Uzbekistan in Figures: Statistical Yearbook 2013; State Committee of the Republic of Uzbekistan on Statistics: Tashkent, Uzbekistan, 2013.

- National Institute of State Statistics and Information of Turkmenistan. Social-Economic Situation of Turkmenistan in 2001; State Committee of the Republic of Uzbekistan on StatisticsNational Institute of State Statistics and Information of Turkmenistan: Ashgabat, Turkmenistan, 2001. (In Russian)

- Central Statistics Organization, Government of Afghanistan. Statistical Yearbook 2014–2015. Available online: http://www.mrrd.gov.af/nabdp/Provincial%20Development%20Plan.htm (accessed on 26 September 2015).

- Bengali, K.; Sadaqat, M. Regional Accounts of Pakistan: Methodology and Estimates, 1973–2000; Social Policy and Development Centre: Karachi, Pakistan, 2005; Available online: http://www.spdc.org.pk/Data/Publication/PDF/WP5.pdf (accessed on 29 April 2018).

- Pakistan Bureau of Statistics. Area and Population of Administrative units by rural/urban: 1951–1998 Censuses. Available online: http://www.pbs.gov.pk/sites/default/files/population_census/Administrative%20Units.pdf (accessed on 31 December 2016).

- Federal State Statistics Service, Russian Federation. The Gross Regional Product of the Subjects of the Russian. Available online: http://mrd.gks.ru/wps/wcm/connect/rosstat_ts/mrd/ru/statistics/grp/ (accessed on 29 April 2016).

- National Bureau of Statistics of China. China Statistical Yearbook 2015. Available online: http://www.stats.gov.cn/tjsj/ndsj/2015/indexeh.htm (accessed on 29 April 2018).

- Shibasaki, R.; Kawasaki, T. A transhipment hub in South Asia and its competition: Application of network equilibrium assignment model for global maritime container shipping. Asian Transp. Stud. 2019, 5, 546–569. [Google Scholar] [CrossRef]

| Port | Cargo Type | Draft | Import | Export | Total | Annual Capacity |

|---|---|---|---|---|---|---|

| Unit (Cargo: Million Tonnes, Container: Million TEUs) | ||||||

| Karachi | Cargo | 10–13 m | 40.3 * | 9.78 * | 50.0 * | N/A |

| Container | 13 m | 1.01 | 0.897 | 1.90 | 1.78 | |

| Port Qasim | Cargo | 10–13 m | 25.7 * | 7.44 * | 33.2 * | 63 |

| Container | 12, 13 m | 0.556 | 0.568 | 1.12 | 2.03 | |

| Gwadar | Cargo | 12.5 m | N/A | N/A | 0.00360 ** | N/A |

| Container | 12.5 m | N/A | N/A | 0.000145 ** | N/A | |

| Country | Number of Sub-countries (zones) | Zone Level | Representative of Zonal Economy | Source |

|---|---|---|---|---|

| Kazakhstan | 14 | Oblast level | Import: zonal value of imports (2013) | [60] |

| Export: zonal value of manufacturing production (2013) | ||||

| Kyrgyz | 8 | Oblast level | Gross Regional Product (2012) | [61] |

| Tajikistan | 5 | Province level | Gross Regional Product (2012) | [62] |

| Uzbekistan | 13 | Province level | Gross Regional Product (2012) | [63] |

| Turkmenistan | 6 | Province level | Population (2001) | [64] |

| Afghanistan | 7 | United Nation region level | Population (2014–2015 estimates) | [65] |

| Pakistan | 31 | Division level | Gross Regional Product (2000) at the province level and population (1998) at the division level | [66,67] |

| Russia | 8 | Federal district level | Gross Regional Product (2009) | [68] |

| China | 31 | Province level | regional value of exports and imports (2014) | [69] |

| Armenia, Azerbaijan, Belarus, Estonia, Georgia, Iran, Latvia, Lithuania, Moldova, Mongolia and Ukraine | 1 | Country level | - | - |

| Scenario Code | Scenario Condition | Description |

|---|---|---|

| s0 | Base scenario | In addition to the original settings prepared in this model, the changes in the border barriers since 2013 are considered |

| s1 | Gwadar Port opening | In addition to s0, the opening of Gwadar Port (12 services calling), with hinterland connection by road, is considered |

| s2 | Rail construction within Pakistan | In addition to s1, the increase in the service frequency of the existing rail network (from 5 to 50 trains/week) and new rail construction (10 trains/week) in the whole of Pakistan, except for the CPEC, are considered |

| s3 | International rail connection with neighbouring countries | In addition to s2, the opening of the planned railway along the CAREC corridor 5, outside Pakistan, except for the CPEC (10 trains/week), and other planned railways in Afghanistan, Iran and the South Caucasus (at the same level of frequency as the existing rail service in each country) are considered |

| s4 | The CPEC railway opening | In addition to s3, the opening of the CPEC railway (10 trains/week) is considered |

| s5 | CAREC border reduction | In addition to s4, the CAREC border barriers decline to half of the current level is considered |

| s6 | CAREC border removal | In addition to s4, the CAREC border barriers decline to zero is considered |

| Export | Import | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| s1 | s2 | s3 | s4 | s5 | s6 * | s1 | s2 | s3 | s4 | s5 | s6 * | |

| Russia | 0 | 0 | 0 | 254 | 928 | 5431 | 0 | 0 | 0 | 1157 | 1246 | 16,697 |

| China | 0 | 0 | 0 | 917 | 4210 | 6479 | 0 | 0 | 0 | 2094 | 2749 | 2963 |

| CA countries (except Afghanistan) | 0 | 39 | 63 | 207 | 369 | 565 | 0 | 1689 | 2937 | 8030 | 8929 | 10,917 |

| Afghanistan | 0 | 389 | 483 | 798 | 631 | 484 | 0 | 2568 | 3015 | 3082 | 3106 | 3769 |

| South Caucasus Countries | 0 | 0 | 0 | 0 | 0 | 1068 | 0 | 0 | 0 | 0 | 0 | 2554 |

| Pakistan | 2130 | 17,562 | 17,115 | 21,500 | 20,695 | 22,074 | 2410 | 8099 | 8171 | 9595 | 9886 | 18,687 |

| Total | 2130 | 17,990 | 17,661 | 23,676 | 26,832 | 36,101 | 2410 | 12,356 | 14,123 | 23,957 | 25,916 | 55,587 |

| Export | Import | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| s1 | s2 | s3 | s4 | s5 | s6 * | s1 | s2 | s3 | s4 | s5 | s6 * | |

| Far Eastern Russian Ports | −201 | −22 | −233 | −2141 | −19,646 | −23,954 | −357 | −134 | −275 | −4320 | −8963 | −94,906 |

| Chinese Ports | 341 | 120 | 7 | −10,395 | −4309 | −5021 | 171 | −1089 | 41 | −16,387 | −23,438 | 105,850 |

| Pakistani Ports | −207 | 1,126 | 5728 | 18,317 | 37,513 | 120,739 | 402 | 6361 | 16,694 | 43,680 | 86,489 | 292,128 |

| Iranian Port | −1651 | −2127 | −2935 | −2977 | −3398 | −14,699 | 2103 | −3805 | −1709 | −2508 | −10,206 | −67,781 |

| Black Sea Ports | 2218 | 103 | −709 | −2654 | −4183 | −24,910 | 3012 | −6035 | −14,424 | −19,624 | −41,613 | −28,549 |

| Baltic Sea Ports | −500 | 800 | −1858 | −151 | −5977 | −52,155 | −5331 | 4702 | −328 | −840 | −2267 | −206,742 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shibasaki, R.; Tanabe, S.; Kato, H.; Lee, P.T.-W. Could Gwadar Port in Pakistan Be a New Gateway? A Network Simulation Approach in the Context of the Belt and Road Initiative. Sustainability 2019, 11, 5757. https://doi.org/10.3390/su11205757

Shibasaki R, Tanabe S, Kato H, Lee PT-W. Could Gwadar Port in Pakistan Be a New Gateway? A Network Simulation Approach in the Context of the Belt and Road Initiative. Sustainability. 2019; 11(20):5757. https://doi.org/10.3390/su11205757

Chicago/Turabian StyleShibasaki, Ryuichi, Satoshi Tanabe, Hironori Kato, and Paul Tae-Woo Lee. 2019. "Could Gwadar Port in Pakistan Be a New Gateway? A Network Simulation Approach in the Context of the Belt and Road Initiative" Sustainability 11, no. 20: 5757. https://doi.org/10.3390/su11205757

APA StyleShibasaki, R., Tanabe, S., Kato, H., & Lee, P. T.-W. (2019). Could Gwadar Port in Pakistan Be a New Gateway? A Network Simulation Approach in the Context of the Belt and Road Initiative. Sustainability, 11(20), 5757. https://doi.org/10.3390/su11205757