Environmental Management Accounting and Performance Efficiency in the Vietnamese Construction Material Industry—A Managerial Implication for Sustainable Development

Abstract

1. Introduction

2. Research Literature and Hypotheses Development

2.1. Environmental Management Accounting (EMA)

2.2. Research Theories Applied in EMA

2.2.1. Contingency Theory

2.2.2. Institutional Theory

2.2.3. Legitimacy Theory

2.2.4. Stakeholder Theory

2.3. An Organization’s Environmental and Financial Efficiency

3. Research Methodology

3.1. Sampling

3.2. Questionnaire Design

3.3. Data Analysis

4. Research Results

4.1. Profile of Sample

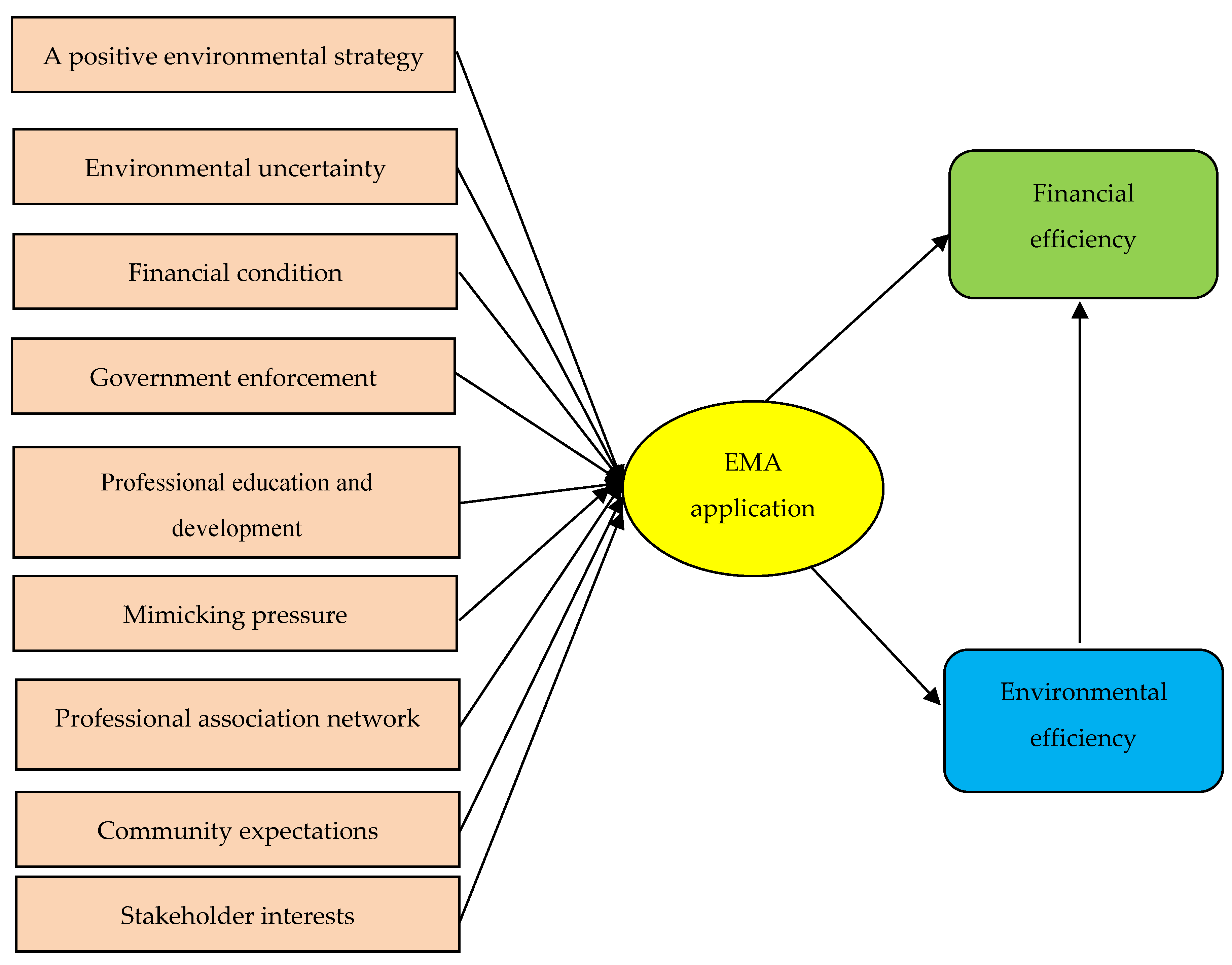

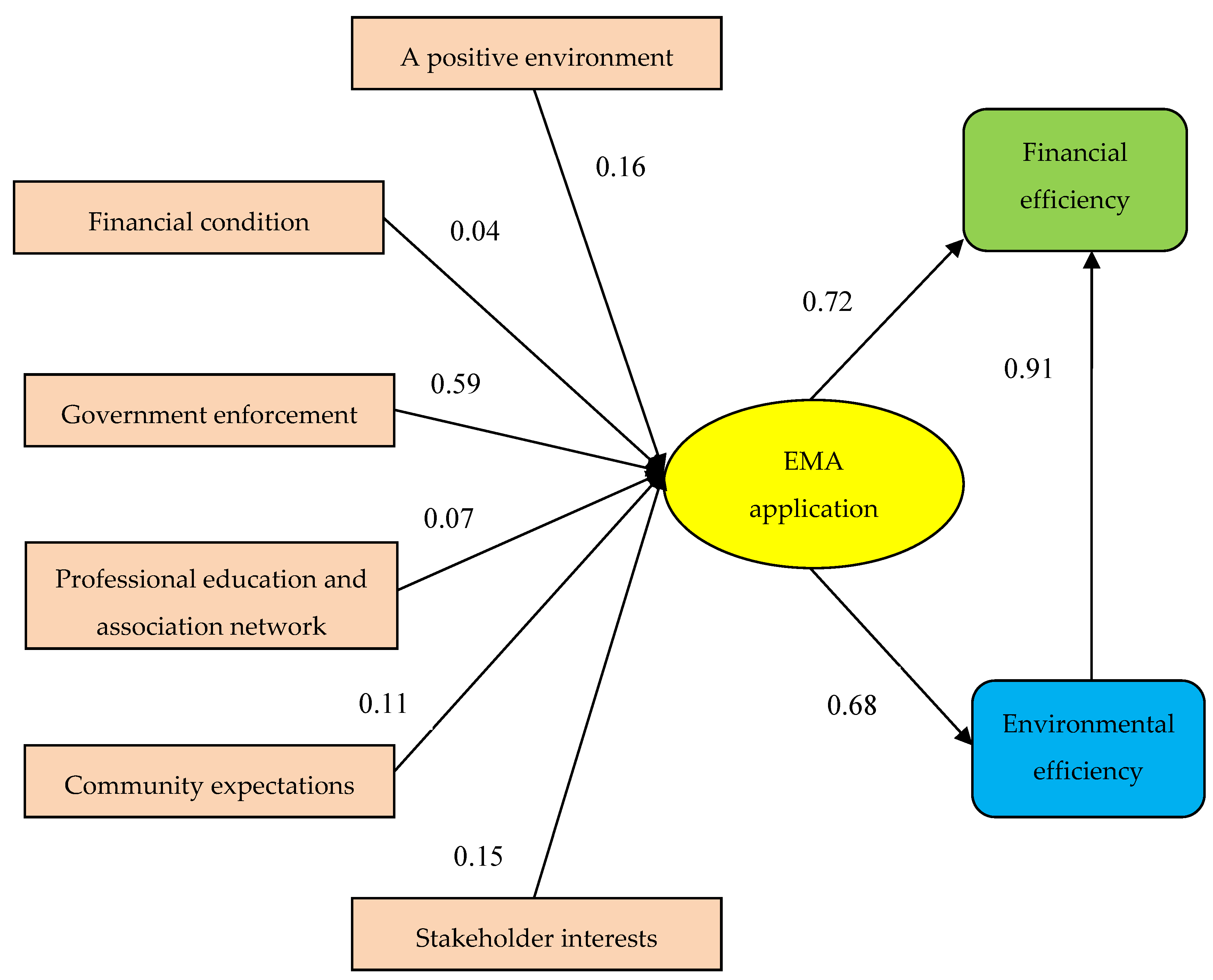

4.2. Factors Influencing EMA Application

4.3. The Relationship between EMA Application and Performance Efficiency

5. Discussion

6. Conclusions

7. Further Research

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Item | Description | Sources |

|---|---|---|

| Positive environmental Strategy (PES) | ||

| PES1 | Make plans to develop effective environmental management | [19,29] |

| PES2 | Establish strategies for sustainable development | |

| PES3 | Attain the goal of environmental impact reduction | |

| PES4 | Achieve leadership in sustainable environmental management | |

| Environmental Uncertainty (ENU) | ||

| ENU1 | Change environmental regulations | [34,53] |

| ENU2 | The scarcity of resources | |

| ENU3 | Change green competition | |

| ENU4 | Change environmental technology | |

| ENU5 | Changes in the stakeholders’ behavior toward the environment | |

| Financial Condition (FIC) | ||

| FIC1 | Enterprise with high financial efficiency has good environmental management | [53] |

| FIC2 | Enterprise spends much money on environmental management activities | |

| FIC3 | Enterprise easily accesses capital for environmental management activities | |

| Government Enforcement (GOE) | ||

| GOE1 | Regulations on waste management and efficient use of materials | [16,42,79] |

| GOE2 | Tighten environmental licensing | |

| GOE3 | Require government environmental reporting | |

| GOE4 | Regulations on environmental fines | |

| GOE5 | Environmental standards for products and processes | |

| Professional education and development (EDD) | ||

| EDD1 | The managers are trained about environmental management | [24,29,42] |

| EDD2 | Staff are trained about environmental management | |

| EDD3 | Departments in enterprise exchange environmental information together | |

| EDD4 | Using large funds to train and develop environmental management | |

| Mimic Pressure (MIP) | ||

| MIP1 | Enterprises in the same industry have good environmental management activities | [16,19,24,42,79] |

| MIP2 | Competitors have good environmental management activities | |

| MIP3 | Enterprises in other industries have good environmental management activities | |

| Profession association network (PANE) | ||

| PAN1 | As leader of associations | Authors |

| PAN2 | Bring many contributions to associations | |

| PAN3 | Interacts well with members of associations | |

| Community’s expectations (COEX) | ||

| COE1 | Community is interested in improving the organization’s environment | [16,19,79] |

| COE2 | Community expects to improve waste management | |

| COE3 | Community cares about budget for environmental management activities | |

| COE4 | Community attends to environmental report from the enterprise | |

| COE5 | Increase community’s awareness of environmental impacts | |

| Stakeholder’s interests (STI) | ||

| STI1 | Customers | [24,42,66,80] |

| STI2 | Investors and banks | |

| STI3 | Environmental organizations | |

| STI4 | Other stakeholders | |

| Environmental Management Accounting Application (EMAA) | ||

| EMA1 | Using monetary information | [15,17,19,24,42,48,56,71,81,82,83] |

| EMA2 | Using physical information | |

| EMA3 | Trace environmental information by detailed accounts | |

| EMA4 | Determine environmental costs by modern method | |

| EMA5 | Estimating environmental costs | |

| EMA6 | Estimating environmental cost report | |

| EMA7 | Developing environmental performance indicators | |

| EMA8 | Use software to track environmental information | |

| EMA9 | Integrate environmental information into short-term decisions | |

| EMA10 | Integrating environmental information into long-term decisions | |

| Financial Efficiency | ||

| FIE1 | ROA | [3,12,26,57,62,69,84] |

| FIE2 | ROS | |

| FIE3 | ROE | |

| Environmental Efficiency | ||

| ENE1 | Reduce amount of waste generated | [3,12,26,44,62,84,85] |

| ENE2 | Environmentally friendly products | |

| ENE3 | Improve enterprise’s image and reputation | |

Appendix B

| Items | Cronbach’s Alpha | Corrected Item-Total Correlation | Cronbach’s Alpha if Item Deleted | Mean | Std. Deviation | Skewness |

|---|---|---|---|---|---|---|

| Positive environmental strategy (PES) | ||||||

| PES1 | 0.903 | 0.825 | 0.860 | 3.38 | 0.943 | −0.210 |

| PES2 | 0.770 | 0.880 | 3.52 | 0.863 | 0.019 | |

| PES3 | 0.802 | 0.869 | 3.44 | 0.930 | −0.204 | |

| PES4 | 0.740 | 0.890 | 3.67 | 0.854 | −0.384 | |

| Environmental Uncertainty (ENU) | ||||||

| ENU1 | 0.923 | 0.850 | 0.896 | 3.38 | 1.047 | −0.273 |

| ENU2 | 0.677 | 0.913 | 3.59 | 0.863 | −0.549 | |

| ENU3 | 0.846 | 0.897 | 3.46 | 1.059 | −0.307 | |

| ENU4 | 0.836 | 0.898 | 3.49 | 1.032 | −0.270 | |

| ENU5 | 0.800 | 0.906 | 3.74 | 0.947 | −0.253 | |

| Financial Condition (FIC) | ||||||

| FIC1 | 0.855 | 0.670 | 0.841 | 3.45 | 0.716 | −0.490 |

| FIC2 | 0.673 | 0.753 | 3.27 | 0.928 | −0.568 | |

| FIC3 | 0.671 | 0.757 | 3.32 | 0.933 | −0.501 | |

| Government enforcement (GOE) | ||||||

| GOE1 | 0.890 | 0.701 | 0.875 | 3.78 | 0.706 | 0.505 |

| GOE2 | 0.767 | 0.858 | 3.29 | 0.877 | 0.254 | |

| GOE3 | 0.725 | 0.869 | 3.21 | 0.923 | 0.360 | |

| GOE4 | 0.750 | 0.863 | 3.25 | 0.929 | 0.340 | |

| GOE5 | 0.742 | 0.865 | 3.94 | 0.782 | 0.506 | |

| Professional education and development (EDD) | ||||||

| EDD1 | 0.831 | 0.511 | 0.825 | 3.45 | 0.783 | −0.134 |

| EDD2 | 0.669 | 0.730 | 2.89 | 0.983 | −0.113 | |

| EDD3 | 0.713 | 0.740 | 3.17 | 0.924 | −0.339 | |

| EDD4 | 0.646 | 0.726 | 3.19 | 1.005 | −0.268 | |

| Mimicking pressure (MIPR) | ||||||

| MIP1 | 0.801 | 0.624 | 0.781 | 3.82 | 0.717 | −0.502 |

| MIP2 | 0.620 | 0.758 | 3.64 | 0.765 | −0.322 | |

| MIP3 | 0.629 | 0.747 | 3.79 | 0.746 | −0.203 | |

| Professional association network (PAN) | ||||||

| PAN1 | 0.897 | 0.827 | 0.834 | 3.02 | 0.874 | −0.249 |

| PAN2 | 0.811 | 0.848 | 3.19 | 0.867 | 0.014 | |

| PAN3 | 0.790 | 0.883 | 2.84 | 1.109 | 0.014 | |

| Community’s expectations (COE) | ||||||

| COE1 | 0.847 | 0.623 | 0.827 | 4.03 | 0.722 | −0.050 |

| COE2 | 0.764 | 0.789 | 4.00 | 0.598 | −0.001 | |

| COE3 | 0.740 | 0.779 | 3.96 | 0.639 | 0.035 | |

| COE4 | 0.551 | 0.842 | 3.74 | 0.634 | 0.272 | |

| COE5 | 0.575 | 0.837 | 3.98 | 0.666 | 0.019 | |

| Stakeholder’s interests (STI) | ||||||

| STI1 | 0.868 | 0.600 | 0.758 | 3.80 | 0.799 | −0.200 |

| STI2 | 0.557 | 0.855 | 3.62 | 0.802 | −0.060 | |

| STI3 | 0.673 | 0.810 | 3.48 | 0.901 | −0.440 | |

| STI4 | 0.722 | 0.789 | 3.46 | 0.927 | −0.322 | |

| Environmental Management Accounting Application (EMA) | ||||||

| EMA1 | 0.919 | 0.727 | 0.909 | 2.56 | 0.935 | −0.049 |

| EMA2 | 0.620 | 0.915 | 2.06 | 0.834 | 0.331 | |

| EMA3 | 0.620 | 0.915 | 1.86 | 0.781 | 0.586 | |

| EMA4 | 0.383 | 0.906 | 1.64 | 0.649 | 0.563 | |

| EMA5 | 0.832 | 0.903 | 2.22 | 0.886 | 0.309 | |

| EMA6 | 0.717 | 0.911 | 2.08 | 0.887 | 0.478 | |

| EMA7 | 0.727 | 0.910 | 2.07 | 0.752 | 0.195 | |

| EMA8 | 0.832 | 0.903 | 2.23 | 0.902 | 0.388 | |

| EMA9 | 0.695 | 0.908 | 2.31 | 0.890 | 0.164 | |

| EMA10 | 0.783 | 0.906 | 2.15 | 0.949 | 0.427 | |

| Financial Efficiency (FIE) | ||||||

| FIE1 | 0.931 | 0.861 | 0.897 | 3.01 | 1.217 | 0.149 |

| FIE2 | 0.855 | 0.901 | 3.13 | 1.203 | 0.032 | |

| FIE3 | 0.857 | 0.900 | 3.15 | 1.161 | 0.068 | |

| Environmental Efficiency (ENE)0 | ||||||

| ENE1 | 0.911 | 0.843 | 0.856 | 3.37 | 1.045 | 0.175 |

| ENE2 | 0.817 | 0.845 | 3.49 | 0.982 | −0.044 | |

| ENE3 | 0.787 | 0.889 | 3.04 | 1.259 | −0.052 | |

Appendix C

| Component | ||||||||

|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | |

| PAN1 | 0.898 | |||||||

| EDD3 | 0.883 | |||||||

| PAN3 | 0.876 | |||||||

| EDD2 | 0.847 | |||||||

| PAN2 | 0.843 | |||||||

| EDD1 | 0.819 | |||||||

| EDD4 | ||||||||

| ENU5 | 0.844 | |||||||

| ENU3 | 0.821 | |||||||

| ENU1 | 0.816 | |||||||

| ENU4 | 0.807 | |||||||

| ENU2 | 0.795 | |||||||

| GOP5 | 0.752 | |||||||

| GOP3 | 0.726 | |||||||

| GOP4 | 0.724 | |||||||

| GOP2 | 0.699 | |||||||

| GOP1 | 0.666 | |||||||

| PES1 | 0.793 | |||||||

| PES4 | 0.776 | |||||||

| PES2 | 0.755 | |||||||

| PES3 | 0.747 | |||||||

| COE2 | 0.864 | |||||||

| COE3 | 0.845 | |||||||

| COE4 | 0.626 | |||||||

| COE5 | 0.605 | |||||||

| COE1 | ||||||||

| FIC2 | 0.887 | |||||||

| FIC3 | 0.867 | |||||||

| FIC1 | 0.747 | |||||||

| STI3 | 0.777 | |||||||

| STI4 | 0.753 | |||||||

| STI1 | 0.626 | |||||||

| STI2 | 0.515 | |||||||

| MIP3 | 0.756 | |||||||

| MIP1 | 0.698 | |||||||

| MIP2 | 0.691 | |||||||

Appendix D

| Correlations | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| EMA | PES | ENU | FIC | GOE | PEA | MIP | COE | STI | ||

| EMA | Pearson Correlation | 1 | 0.642 ** | 0.494 ** | 0.367 ** | 0.871 ** | 0.465 ** | 0.495 ** | 0.614 ** | 0.623 ** |

| Sig. (2-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| PES | Pearson Correlation | 1 | 0.481 ** | 0.448 ** | 0.565 ** | 0.247 ** | 0.476 ** | 0.422 ** | 0.338 ** | |

| Sig. (2-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||

| ENU | Pearson Correlation | 1 | 0.180 ** | 0.523 ** | 0.191 ** | 0.426 ** | 0.421 ** | 0.376 ** | ||

| Sig. (2-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | ||||

| FIC | Pearson Correlation | 1 | 0.304 ** | 0.066 | 0.400 ** | 0.220 ** | 0.227 ** | |||

| Sig. (2-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |||||

| GOE | Pearson Correlation | 1 | 0.381 ** | 0.465 ** | 0.550 ** | 0.513 ** | ||||

| Sig. (2-tailed) | 0.000 | 0.000 | 0.000 | 0.000 | ||||||

| PEA | Pearson Correlation | 1 | 0.244 ** | 0.257 ** | 0.583 ** | |||||

| Sig. (2-tailed) | 0.000 | 0.000 | 0.000 | |||||||

| MIP | Pearson Correlation | 1 | 0.489 ** | 0.423 ** | ||||||

| Sig. (2-tailed) | 0.000 | 0.000 | ||||||||

| COE | Pearson Correlation | 1 | 0.482 ** | |||||||

| Sig. (2-tailed) | 0.000 | |||||||||

| STI | Pearson Correlation | 1 | ||||||||

| Sig. (2-tailed) | ||||||||||

References

- Bennett, M.; Bouma, J.; Wolter, T. Environmental Management Accounting: Informational and Institutional Developments; Eco-Efficiency in Industry and Science 3; Springer: Dordrecht, The Netherlands, 2002. [Google Scholar] [CrossRef]

- Schaltegger, S.; Burritt, R. Contemporary Environmental Accounting: Issues, Concepts and Practice; Greenleaf: Austin, TX, USA, 2000. [Google Scholar] [CrossRef]

- IFAC. International Guidance Document: Environmental Management Accounting; International Federation of Accountants: New York, NY, USA, 2005. [Google Scholar]

- Epstein, M. Measuring Corporate Environmental Performance: Best Practices for Costing and Managing an Effective Environmental Strategy; Irwin Professional Publishing: Chicago, IL, USA, 1996. [Google Scholar] [CrossRef]

- Rikhardsson, P.; Bennett, M.; Bouma, J.; Schaltegger, S. Implementing Environmental Management Accounting: Status and Challenges; Springer: Dordrecht, The Netherlands, 2005; Volume 18. [Google Scholar] [CrossRef]

- Schaltegger, S.; Bennett, M.; Burritt, R.; Jasch, C. Environmental Management Accounting for Cleaner Production; Springer: Dordrecht, The Netherlands, 2008. [Google Scholar]

- UNDSD. Environmental Management Accounting: Procedures and Principles; United Nations Division for Sustainable Development: New York, NY, USA, 2001. [Google Scholar]

- USEPA. Improving Government Role in the Promotion of Environmental Managerial Accounting; United State Environmental Protection Agency: Washington, DC, USA, 2000.

- Ahmad, A. Environmental accounting & reporting practices: Significance and issues: A case from Bangladesh companies. Glob. J. Manag. Bus. Res. 2012, 12, 119–127. [Google Scholar]

- Bennett, M.; Jame, P. The Green Bottom Line: Environmental Accounting for Management: Current Practice and Future Trends; Greenleaf Publishing Limited: Austin, TX, USA, 2000. [Google Scholar] [CrossRef]

- Herzig, C. Environmental Management Accounting: Case Studies of South East Companies. Account. Forum 2012, 36, 310–312. [Google Scholar] [CrossRef]

- Le, T.T.; Nguyen, H. Factors affecting to ECMA application in Vietnamese brick manufacturing enterprises. Res. J. Financ. Account. 2018, 9, 136–145. [Google Scholar]

- Chang, H.H. Environmental Management Accounting Within Universities: Current State and Future Potential. Ph.D. Thesis, RMIT University, Melbourne, V, Australia, November 2007. [Google Scholar]

- Jalaludin, D.; Sulaiman, M.; Ahmad, N.N.N. Understanding Environmental Management Accounting (EMA) Adoption: A New Institutional Sociology Perspective. Soc. Responsib. J. 2011, 7, 540–557. [Google Scholar] [CrossRef]

- Jamil, C.Z.M.; Mohamed, R.; Muhammad, F.; Ali, A. Environmental Management Accounting Practices in Small Medium Manufacturing Firms. Procedia Soc. Behav. Sci. 2015, 172, 619–626. [Google Scholar] [CrossRef]

- Qian, W.; Burritt, R. The development of environmental management accounting: An institutional view. In Environmental Management Accounting for Cleaner Production; Schaltegger, S., Bennett, M., Burritt, R., Jasch, C., Eds.; Springer: Dordrecht, The Netherlands, 2008; Volume 24, pp. 233–247. [Google Scholar]

- Qian, W.; Burritt, R. Contingency perspectives on environmental accounting: An exploratory study of local government. Account. Account. Perform. J. 2009, 15, 39–70. [Google Scholar]

- Kokubu, K.; Nashioka, E. Environmental Management Accounting Practices in Japan. In Implementing Environmental Management Accounting: Status and Challenges; Rikhardsson, P., Bennett, M., Bouma, J., Schaltegger, S., Eds.; Springer: Dordrecht, The Netherlands, 2005; Volume 18, pp. 321–341. [Google Scholar] [CrossRef]

- Kumpulainen, A. Environmental Business Accounting in Four Finnish Case Companies: Follow up Study between 1996 and 2005. Master’s Thesis, Helsinki University of Technology, Espoo, Finland, 2005. [Google Scholar]

- Setthasakko, W. Barriers to the development of environmental management accounting: An exploratory study of pulp and paper companies in Thailand. EuroMed J. Bus. 2010, 5, 315–331. [Google Scholar] [CrossRef]

- Bansal, P.; Roth, K. Why Companies Go Green: A Model of Ecological Responsiveness. Acad. Manag. J. 2000, 43, 717–736. [Google Scholar] [CrossRef]

- Khalid, F.M.; Lord, B.R.; Dixon, D.K. Environmental Management Accounting Implementation in Environmentally Sensitive Industries in Malaysia. In Proceedings of the 6th NZ Management Accounting Conference, Palmerston North, New Zealand, 22–23 November 2012. [Google Scholar]

- Earnhart, D.; Lizal, L. The Effect of Corporate Environmental Performance on Financial Outcomes—Profits, Revenues and Costs: Evidence from the Czech Transition Economy; DRUID: Frederiksberg, Denmark, 2010; Volume 46, pp. 1–44. [Google Scholar]

- Iwata, H.; Okada, K. How does environmental performance affect FINANCIAL performance? Evidence from Japanese manufacturing firms. Ecol. Econ. 2011, 70, 1691–1700. [Google Scholar] [CrossRef]

- Ong, T.; Teh, B.; Ang, Y. The impact of Environmental Improvements on the Financial Performance of Leading Companies Listed in Bursa Malaysia. Int. J. Tradeecon. Financ. 2014, 5, 386–391. [Google Scholar] [CrossRef]

- Al-Tuwaijri, S.; Christensen, T.; Hughes, K. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Account.Org. Soc. 2014, 29, 447–471. [Google Scholar] [CrossRef]

- Konar, S.; Cohen, M.A. Does the market value environmental performance? Rev. Econ. Stat. 2001, 83, 281–289. [Google Scholar] [CrossRef]

- Filbeck, G.; Gorman, R. The relationship between the environmental and financial performance of public utilities. Environ. Res. Econ. 2004, 29, 137–154. [Google Scholar] [CrossRef]

- Qian, W. Revisiting the link between environmental performance and financial performance: Who cares about private companies? In Proceedings of the 11th ACSEAR Conference, Wollongong, Australia, 2–4 December 2012. [Google Scholar]

- Rassier, D.G.; Earnhart, D. Does the Porter hypothesis explain expected future financial performance? the effect of clean water regulation on chemical manufacturing firms. Environ. Resour. Econ. 2010, 45, 353–377. [Google Scholar] [CrossRef]

- Sarkis, J.; Cordeiro, J.J. An empirical evaluation of environmental efficiencies and firm performance: Pollution prevention versus end-of-pipe practice. Eur. J. Oper. Res. 2001, 135, 102–113. [Google Scholar] [CrossRef]

- Wagner, M.; Nguyen, V.P.; Azomahou, T.; Wehrmeyer, W. The relationship between the environmental and economic performance of firms: An empirical analysis of the European paper industry. Corp. Soc. Responsib. Environ. Manag. 2002, 9, 133–146. [Google Scholar] [CrossRef]

- Vietnam Institute for Building Materials. Overview of Construction Materials Industry in Vietnam; Vietnam Institute for Building Materials: Hanoi, Vietnam, 2018. [Google Scholar]

- Le, T.T.; Nguyen, T.M.A. Practice environmental cost management accounting: The case of Vietnamese brick production companies. Manag. Sci. Lett. 2018, 9, 105–120. [Google Scholar] [CrossRef]

- Niap, D.T.F. Environmental Management Accounting for an Australian Cogeneration Company. Master’s Thesis, RMIT University, Melbourne, Australia, 2006. [Google Scholar]

- Betianu, L.; Briciu, S. The impact of the economic crisis on environmental costs. Analele Stiintifice ale Universitatii. Alexandru Ioan Cuza” din Iasi-Stiinte Economice 2010, 2010SE, 3–14. [Google Scholar]

- Le, T.T. Applying environmental cost management accounting in brick production companies–Evidence from Vietnam. Res. J. Financ. Account. 2018, 9, 17–26. [Google Scholar]

- Deegan, C. Environmental Management Accounting: An Introduction and Case Studies for Australia; Institute of Chartered Accountants in Australia: Melbourne, Australia, 2003. [Google Scholar]

- Bennett, M.; Rikhardsson, P.; Schaltegger, S. Eco-efficiency in industry and science 12. In Environmental Management Accounting: Purpose and Progress; Springer: Berlin, Germany, 2003. [Google Scholar] [CrossRef]

- Bartolomeo, M.; Bennett, M.D.; Bouma, J.J.; Heydkamp, P.; James, P.; de Walle, F.B.; Wolters, T.J. Eco-Efficiency in Industry and Science 3. In Eco—Management Accounting; Springer: Amsterdam, The Netherlands, 1999. [Google Scholar] [CrossRef]

- Fernando, S.; Lawrence, S. A theoretical framework for CSR practices: Integrating legitimacy theory, stakeholder theory and institutional theory. J. Theor. Account. Res. 2014, 10, 149–179. [Google Scholar]

- Islam, J.; Hu, H. A review of literature on contingency theory in managerial accounting. Afr. J. Bus. Manag. 2012, 6, 5159–5161. [Google Scholar] [CrossRef]

- Covaleski, M.; Dirsmith, M.; Samuel, S. Managerial accounting research: The contributions of organizational and sociological theory. J. Manag. Account. Res. 1996, 8, 1–35. [Google Scholar]

- Muslichah, M. The Effect of Contingency Variables on Management Accounting System Characteristics and Managerial Performance. Int. J. Account. Bus. Soc. 2004, 12, 47–70. [Google Scholar]

- Bouma, J.J.; Van der Veen, M. Wanted: A Theory for Environmental Management Accounting. In Environmental Management Accounting: Informational and Institutional Development; Bennett, M., Bouma, J., Wolter, T., Eds.; Springer: Dordrecht, The Netherlands, 2002; Volume 9, pp. 279–290. [Google Scholar]

- Gordon, L.A.; Narayanan, V.K. Management Accounting Systems, Perceived Environmental Uncertainty and Organizational Structure: An Empirical Investigation. Account. Org. Soc. 1984, 9, 33–47. [Google Scholar] [CrossRef]

- Sharma, S. Managerial interpretations and organizational context and predictors of corporate choice of environmental strategy. Acad. Manag. J. 2000, 43, 681–697. [Google Scholar] [CrossRef]

- Guo, X. Failure of an Environmental Strategy: Lessons from an Explosion at Petrochina and Subsequent Water Pollution. In Environmental Management Accounting for Cleaner Production; Schaltegger, S., Bennett, M., Burritt, R., Jasch, C., Eds.; Springer: Dordrecht, The Netherlands, 2008; Volume 24, pp. 423–441. [Google Scholar] [CrossRef]

- Lewis, G.J.; Harvey, B. Perceived Environmental Uncertainty: The Extension of Miller’s Scale to the Natural Environment. J. Manag. Stud. 2001, 38, 201–233. [Google Scholar] [CrossRef]

- Hussain, M.M.; Gunasekaran, A. An Institutional Perspective of Non-Financial Management Accounting Measures: A Review of the Financial Service Industry. Manag. Audit. J. 2002, 17, 518–536. [Google Scholar] [CrossRef]

- Osborn, D. Process and Content: Visualizing the Policy Challenges of Environmental Management Accounting in PM. In Implementing Environmental Management Accounting: Status and Challenges; Rikhardsson, P.M., Bennett, M., Bouma, J.J., Schaltegger, S., Eds.; Springer: Dordrecht, The Netherlands, 2005; Volume 18, pp. 81–104. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W.W. The iron cage revisited: Institutional isomorphism and collective efficient in organizational fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef]

- Burritt, R. Environmental Management Accounting: Roadblocks on the Way to the Green and Pleasant Land. Bus. Strat. Environ. 2004, 13, 13–32. [Google Scholar] [CrossRef]

- Delmas, M.; Toffel, M. Stakeholders and environmental management practices: An institutional framework. Bus. Strat. Environ. 2004, 13, 209–222. [Google Scholar] [CrossRef]

- Granlund, M.; Lukka, K. It’s a Small World of Management Accounting Practices. J. Manag. Account. Res. 1998, 10, 153–179. [Google Scholar]

- Hoffman, A. Linking Organizational and Field—Level Analyses. Org. Environ. J. 2001, 14, 133–156. [Google Scholar] [CrossRef]

- Scott, W.R.; Meyer, J.W. Institutional Environments and Organizations: Structural Complexity and Individualism; SAGE Publications: Thousand Oaks, CA, USA, 1994. [Google Scholar]

- Jennings, P.; Zandbergen, P. Ecologically Sustainable Organizations: An Institutional Approach. Acad. Manag. Rev. 1995, 20, 1015–1052. [Google Scholar] [CrossRef]

- Wong, L.T.; Fryxell, G.E. Stakeholder influences on environmental management practices: A study of fleet operations in Hong Kong (SAR), China. Transp. J. 2004, 43, 22–35. [Google Scholar]

- Parker, L.D. Green Strategy Costing: Early Days. Australian Account. Rev. 2000, 10, 46–55. [Google Scholar] [CrossRef]

- UNIDO. Introducing Environmental Management Accounting (EMA) At Enterprise Level Methodology and Case Studies from Central and Eastern Europe; United Nations Industrial Development Organization: Vienna, Austria, 2003. [Google Scholar]

- Pfeffer, J.; Salacik, G. The External Control of Organizations: A Resource Dependent Perspective; Harper and Row: New York, NY, USA, 1978. [Google Scholar]

- Shocker, A.D.; Sethi, S.P. An approach to incorporating societal preferences in developing corporate action strategies. Calif. Manag. Rev. 1973, 15, 97–105. [Google Scholar] [CrossRef]

- Florida, R.; Davison, D. Gaining from green management: Environmental management Systems inside and outsite the factory. Calif. Manag. Rev. 2001, 43, 64–84. [Google Scholar] [CrossRef]

- Prakash, A. Why Do Firms Adopt ‘Beyond—Compliance’ Environmental Policies? Bus. Strat. Environ. J. 2001, 10, 286–299. [Google Scholar] [CrossRef]

- Freeman, R. Strategic Management: A Stakeholder Approach; Pitman Publishing: Lanham, MD, USA, 1984. [Google Scholar]

- Belal, A.; Owen, D. The views of corporate managers on the current state of, and future prospects for, social reporting in Bangladesh: An engagement-based study. Account. Audit. Account. J. 2007, 20, 472–494. [Google Scholar] [CrossRef]

- Deegan, C.; Blomquist, C. Stakeholder influence on corporate reporting: An exploration of the interaction between WWF-Australia and the Australian minerals industry. Account. Org. Soc. 2006, 31, 343–372. [Google Scholar] [CrossRef]

- Ten, E. Applying stakeholder theory to analyze corporate environmental performance: Evidence from Australian listed companies. Asian Rev. Account. 2005, 15, 164–184. [Google Scholar] [CrossRef]

- Deegan, C. The Legitimising Effect of Social and Environmental Disclosures - A Theoretical Foundation. Account. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- Kitzman, K.A. Evironmental Cost Accounting for Improved Environmental Decision Making. Pollut. Eng. J. 2001, 33, 20–23. [Google Scholar]

- Godschalk, S.K.B. Does Corporate Environmental Accounting Make Business Sense? In Environmental Management Accounting for Cleaner Production; Schaltegger, S., Bennett, M., Burritt, R., Jasch, C., Eds.; Springer: Dordrecht, The Netherlands, 2008; Volume 24, pp. 249–265. [Google Scholar]

- Schaltegger, S.; Herzig, C.; Kleiber, O.; Muller, J. Sustainability management in business enterprises—Concepts and instruments for sustainable organization development, 2nd ed.; Federal Ministry for the Environment, Nature Conservation and Nuclear Safety: Berlin, Germany, 2002. [Google Scholar]

- Sarker, T.P.; Burritt, R.L. An empirical examination of the role of environmental accounting information in environmental investment decision making. In Environmental Management Accounting for Cleaner Production; Sarker, T.P.; Burritt, R.L. Springer: Dordrecht, The Netherlands, 2008; Volume 24, pp. 457–475. [Google Scholar]

- Onishi, Y.; Kokubu, K.; Nakajama, M. Implementing Material Flow Cost Accounting in a Pharmaceutical Company. In Environmental Management Accounting For Cleaner Production; Schaltegger, S., Bennett, M., Burrit, R., Jasch, C., Eds.; Springer: Dordrecht, The Netherlands, 2008; Volume 24, pp. 395–409. [Google Scholar]

- Wagner, M. Environmental performance and the quality of corporate environmental reports: The role of environmental management accounting. In Implementing Environmental Management Accounting: Status and Challenges; Rikhardsson, P., Bennett, M., Bouma, J., Schaltegger, S., Eds.; Springer: Dordrecht, The Netherlands, 2005; Volume 18, pp. 105–122. [Google Scholar] [CrossRef]

- Hart, S.L.; Ahuja, G. Does it pay to be green? an empirical examination of the relationship between emission reduction and firm performance. Bus. Strat. Environ. 1996, 5, 30–37. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 7th ed.; Prentice Hall International, Inc.: Upper Saddle River, NJ, USA, 2009; p. 7. [Google Scholar]

- Qian, W.; Burritt, R.; Monroe, G. Environmental management accounting in local government: A case of waste management. Account. Audit. Account. J. 2011, 24, 93–128. [Google Scholar] [CrossRef]

- Abreu, M.C.S.; Castro, F.C.; Lazoro, J.C. Stakeholder influence on environmental proactivity of Brazilian companies. J. Account. Organ. 2013, 17, 20–32. [Google Scholar] [CrossRef][Green Version]

- Hyršlová, J.; Hájek, M. Environmental management accounting in the framework of EMAS II in the Czech republic. In Implementing Environmental Management Accounting: Status and Challenges; Rikhardsson, P., Bennett, M., Bouma, J., Schaltegger, S., Eds.; Springer: Dordrecht, The Netherlands, 2005; Volume 18, pp. 279–295. [Google Scholar] [CrossRef]

- Jinadu, O.; Agbeyangi, B.A.; Mamidu, I.A. Impact of Environmental Management Accounting on Current Practices and Future Sustainability in South-West Nigerian Polytechnics. Int. J. Econ. Commerce Manag. 2015, 3, 586–603. [Google Scholar]

- Ramli, A.; Ismail, M.S. Environmental management accounting practices: A Survey of ISO 14001 certified Malaysian organizations. J. Energy Technol. Policy 2013, 3, 415–432. [Google Scholar]

- Le, T.T. Performance measures and metrics in a supply chain environment. Uncertain Supply Chain Manag. 2019, 8. [Google Scholar] [CrossRef]

- Doorasamy, M. Using Environmental Management Accounting to Investigate Benefits of Cleaner Production at a Paper Manufacturing Company in Kwadakuza, Kwazulu Natal: A Case Study. Ph.D. Thesis, Durban University of Technology, Durban, South Africa, 2014. [Google Scholar]

| Collecting information |  | EMA practices |  | Decision making |

| - Environmental audit - Environmental impact assessment - Environmental risk appraisal - Product cycle analysis | - Calculate environmental issues (cost, revenue, asset, debt) - Analyze environmental efficiency | - Green market development - Activity based management - Synchronous quality management - Pollution prevention - Product management - Environmental report |

| Kaiser−Meyer−OlkinMeasure of Sampling Adequacy | 0.907 | |

| Bartlett’s Test of Sphericity | Approximate Chi-Square | 12335.894 |

| df | 630 | |

| Sig. | 0.000 | |

| Total | % of Variance | Cumulative % | Total | % of Variance | Cumulative % | Total | % of Variance | Cumulative % | |

|---|---|---|---|---|---|---|---|---|---|

| 1 | 12.432 | 34.533 | 34.533 | 12.432 | 34.533 | 34.533 | 5.418 | 15.050 | 15.050 |

| 2 | 4.703 | 13.063 | 47.597 | 4.703 | 13.063 | 47.597 | 4.179 | 11.607 | 26.657 |

| 3 | 2.620 | 7.277 | 54.874 | 2.620 | 7.277 | 54.874 | 3.650 | 10.138 | 36.795 |

| 4 | 2.035 | 5.652 | 60.526 | 2.035 | 5.652 | 60.526 | 3.508 | 9.746 | 46.540 |

| 5 | 1.764 | 4.899 | 65.426 | 1.764 | 4.899 | 65.426 | 3.308 | 9.189 | 55.729 |

| 6 | 1.355 | 3.763 | 69.189 | 1.355 | 3.763 | 69.189 | 2.644 | 7.344 | 63.073 |

| 7 | 1.248 | 3.468 | 72.657 | 1.248 | 3.468 | 72.657 | 2.469 | 6.858 | 69.931 |

| 8 | 1.083 | 3.007 | 75.664 | 1.083 | 3.007 | 75.664 | 2.064 | 5.733 | 75.664 |

| 9 | 0.749 | 2.080 | 77.744 | ||||||

| 10 | 0.673 | 1.869 | 79.613 | ||||||

| 11 | 0.650 | 1.804 | 81.417 | ||||||

| 12 | 0.549 | 1.526 | 82.943 | ||||||

| ….. |

| Component | ||||||||

|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | |

| PAN1 | 0.899 | |||||||

| EDD3 | 0.884 | |||||||

| PAN3 | 0.874 | |||||||

| EDD2 | 0.848 | |||||||

| PAN2 | 0.843 | |||||||

| EDD1 | 0.819 | |||||||

| ENU5 | 0.846 | |||||||

| ENU3 | 0.822 | |||||||

| ENU1 | 0.815 | |||||||

| ENU4 | 0.806 | |||||||

| ENU2 | 0.797 | |||||||

| GOE5 | 0.761 | |||||||

| GOE3 | 0.724 | |||||||

| GOE4 | 0.724 | |||||||

| GOE2 | 0.703 | |||||||

| GOE1 | 0.684 | |||||||

| PES1 | 0.796 | |||||||

| PES4 | 0.780 | |||||||

| PES2 | 0.755 | |||||||

| PES3 | 0.750 | |||||||

| COE2 | 0.864 | |||||||

| COE3 | 0.838 | |||||||

| COE4 | 0.637 | |||||||

| COE5 | 0.601 | |||||||

| FIC2 | 0.888 | |||||||

| FIC3 | 0.869 | |||||||

| FIC1 | 0.749 | |||||||

| STI3 | 0.780 | |||||||

| STI4 | 0.758 | |||||||

| STI1 | 0.632 | |||||||

| STI2 | 0.524 | |||||||

| MIP3 | 0.760 | |||||||

| MIP1 | 0.706 | |||||||

| MIP2 | 0.692 | |||||||

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | Change Statistics | Durbin−Watson | ||||

|---|---|---|---|---|---|---|---|---|---|---|

| R Square Change | F Change | df1 | df2 | Sig. F Change | ||||||

| 1 | 0.871 a | 0.759 | 0.759 | 0.31816 | 0.759 | 1310.925 | 1 | 416 | 0.000 | |

| 2 | 0.895 b | 0.801 | 0.800 | 0.28921 | 0.042 | 88.458 | 1 | 415 | 0.000 | |

| 3 | 0.911 c | 0.830 | 0.828 | 0.26814 | 0.028 | 68.795 | 1 | 414 | 0.000 | |

| 4 | 0.915 d | 0.837 | 0.835 | 0.26279 | 0.007 | 18.020 | 1 | 413 | 0.000 | |

| 5 | 0.916 e | 0.840 | 0.838 | 0.26058 | 0.003 | 8.046 | 1 | 412 | 0.005 | |

| 6 | 0.917 f | 0.842 | 0.839 | 0.25946 | 0.002 | 4.554 | 1 | 411 | 0.033 | 1.439 |

| Model | Sum of Squares | df | Mean Square | F | Sig. | |

|---|---|---|---|---|---|---|

| 6 | Regression | 147.143 | 6 | 24.524 | 364.293 | 0.000 f |

| Residual | 27.668 | 411 | 0.067 | |||

| Total | 174.811 | 417 | ||||

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | 95.0% Confidence Interval for B | Collinearity Statistics | ||||

|---|---|---|---|---|---|---|---|---|---|---|

| B | Std. Error | Beta | Lower Bound | Upper Bound | Tolerance | VIF | ||||

| 6 | Constant | −0.960 | 0.113 | −8.470 | 0.000 | −1.183 | −0.737 | |||

| GOE | 0.530 | 0.025 | 0.592 | 21.409 | 0.000 | 0.482 | 0.579 | 1.984 | 1.984 | |

| STI | 0.139 | 0.025 | 0.153 | 5.553 | 0.000 | 0.090 | 0.189 | 1.969 | 1.969 | |

| POE | 0.138 | 0.021 | 0.168 | 6.535 | 0.000 | 0.096 | 0.179 | 1.719 | 1.719 | |

| COE | 0.143 | 0.031 | 0.114 | 4.581 | 0.000 | 0.082 | 0.205 | 1.604 | 1.604 | |

| PEA | 0.064 | 0.021 | 0.076 | 3.096 | 0.002 | 0.023 | 0.104 | 1.576 | 1.576 | |

| FIC | 0.040 | 0.019 | 0.047 | 2.134 | 0.033 | 0.003 | 0.078 | 1.283 | 1.283 | |

| EMA | FIE | ENE | ||

|---|---|---|---|---|

| EMA (EMA application) | Pearson Correlation | 1 | 0.720 ** | 0.689 ** |

| Sig. (2-tailed) | 0.000 | 0.000 | ||

| FIE (Financial efficiency) | Pearson Correlation | 0.720 ** | 1 | 0.916 ** |

| Sig. (2-tailed) | 0.000 | 0.000 | ||

| ENE (Environmental efficiency) | Pearson Correlation | 0.689 ** | 0.916 ** | 1 |

| Sig. (2-tailed) | 0.000 | 0.000 | ||

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | 95.0% Confidence Interval for B | |||

|---|---|---|---|---|---|---|---|---|

| B | Std. Error | Beta | Lower Bound | Upper Bound | ||||

| 1 (Effect ofEMA to FIE) | Constant | 0.452 | 0.131 | 3.464 | 0.001 | 0.196 | 0.709 | |

| EMA | 1.245 | 0.059 | 0.720 | 21.181 | 0.000 | 1.129 | 1.360 | |

| Adjust R2 = 0.518 | ||||||||

| Durbin−Watson = 0.872 | ||||||||

| Sig. in ANOVA test = 0.000 | ||||||||

| 2 (Effect of EMA to ENE) | Constant | 1.002 | 0.124 | 8.092 | 0.000 | 0.758 | 1.245 | |

| EMA | 1.080 | 0.056 | 0.689 | 19.396 | 0.000 | 0.971 | 1.190 | |

| Adjust R2 = 0.474 | ||||||||

| Durbin−Watson = 0.735 | ||||||||

| Sig. in ANOVA test = 0.000 | ||||||||

| 3 (Effect of ENE to FIE) | Constant | −0.231 | 0.075 | −3.079 | 0.002 | −0.378 | −0.083 | |

| ENE | 1.009 | 0.022 | 0.916 | 46.491 | 0.000 | 0.967 | 1.052 | |

| Adjust R2 = 0.838 | ||||||||

| Durbin−Watson = 1.476 | ||||||||

| Sig. in ANOVA test = 0.000 | ||||||||

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Le, T.T.; Nguyen, T.M.A.; Phan, T.T.H. Environmental Management Accounting and Performance Efficiency in the Vietnamese Construction Material Industry—A Managerial Implication for Sustainable Development. Sustainability 2019, 11, 5152. https://doi.org/10.3390/su11195152

Le TT, Nguyen TMA, Phan TTH. Environmental Management Accounting and Performance Efficiency in the Vietnamese Construction Material Industry—A Managerial Implication for Sustainable Development. Sustainability. 2019; 11(19):5152. https://doi.org/10.3390/su11195152

Chicago/Turabian StyleLe, Thi Tam, Thi Mai Anh Nguyen, and Thi Thu Hien Phan. 2019. "Environmental Management Accounting and Performance Efficiency in the Vietnamese Construction Material Industry—A Managerial Implication for Sustainable Development" Sustainability 11, no. 19: 5152. https://doi.org/10.3390/su11195152

APA StyleLe, T. T., Nguyen, T. M. A., & Phan, T. T. H. (2019). Environmental Management Accounting and Performance Efficiency in the Vietnamese Construction Material Industry—A Managerial Implication for Sustainable Development. Sustainability, 11(19), 5152. https://doi.org/10.3390/su11195152