Environmental Innovation, Environmental Performance and Financial Performance: Evidence from Malaysian Environmental Proactive Firms

Abstract

1. Introduction

2. Literature Review

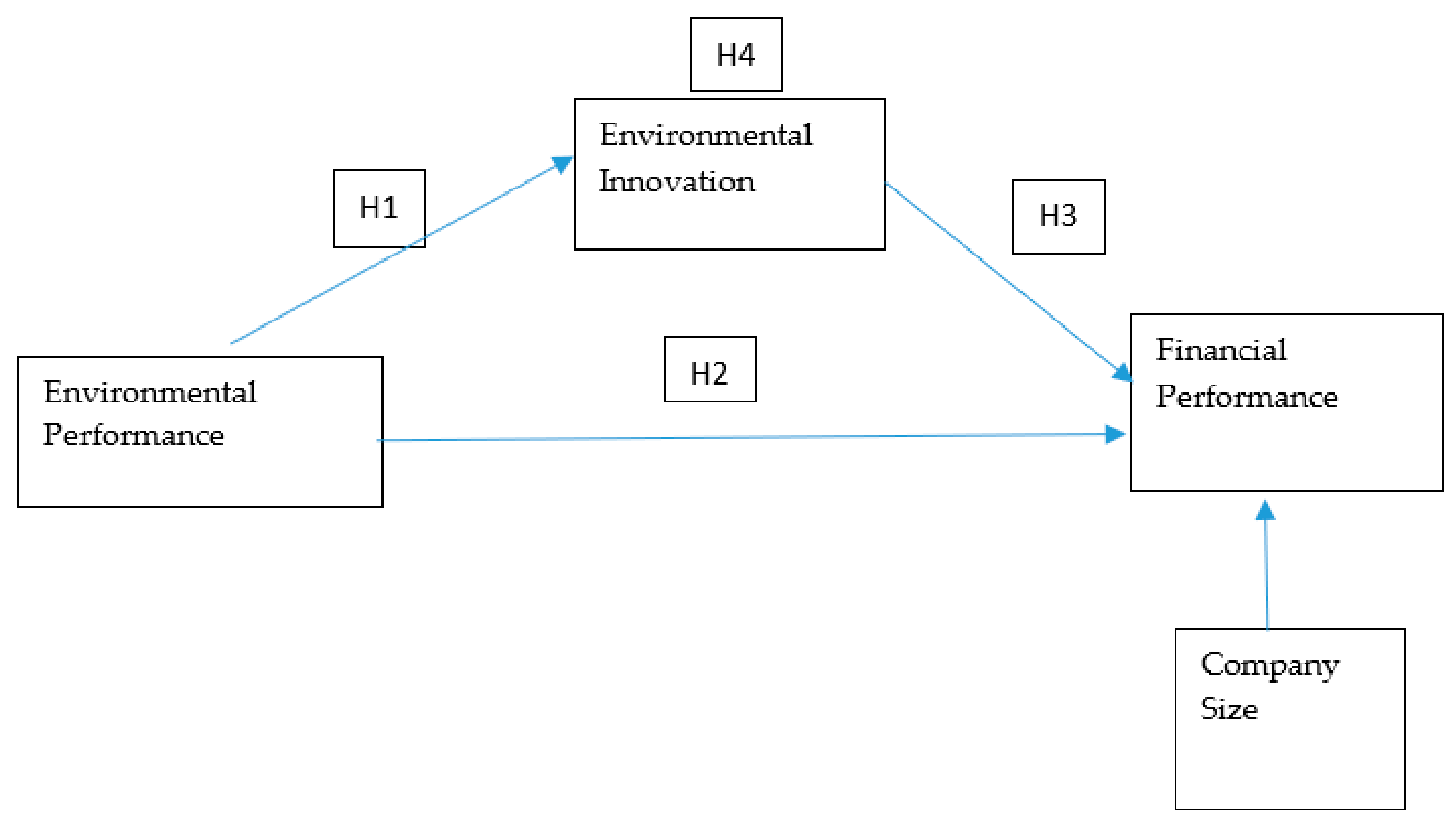

2.1. Effects of Environmental Performance on Environmental Innovation

2.2. Environmental Performance and Financial Performance

2.3. Environmental Innovation and Financial Performance

2.4. Environmental Innovation as a Mediator between Environmental Performance and Financial Performance

3. Methodology

3.1. Data Collection and Procedures

3.2. Common Method, Non-Response Bias and Endogeneity Problem

4. Results

4.1. Descriptive Statistics

4.2. Assessment of Model Using PLS-SEM

4.2.1. Measurement Model Assessment

4.2.2. Structural Model Assessment

4.2.3. Mediation Effect of Environmental Innovation between Environmental Performance and Financial Performance

5. Discussion

5.1. Environmental Performance and Environmental Innovation

5.2. Environmental Performance And Financial Performance

5.3. Environmental Innovation and Financial Performance

5.4. Environmental Innovation as a Mediator between Environmental Performance and Financial Performance

6. Conclusions and Implication

7. Limitations and Future Directions

Author Contributions

Funding

Conflicts of Interest

References

- Gabler, C.B.; Richey, R.G.; Rapp, A. Developing an econ-capability through competing in the age of capabilities. Calif. Manag. Rev. 2015, 42, 118–147. [Google Scholar]

- Christmann, P. Effects of “best practices” of environmental management on cost advantage: The role of complementary assets. Acad. Manag. J. 2000, 43, 663–680. [Google Scholar]

- Yang, M.G.; Hong, P.; Modi, S.B. Impact of lean manufacturing and environmental management on business performance: An empirical study of manufacturing firms. Int. J. Prod. Econ. 2011, 129, 251–261. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Does it really pay to be green? Determinants and consequences of proactive environmental strategies. J. Account. Public Policy 2011, 30, 122–144. [Google Scholar] [CrossRef]

- Chang, C.-H. The influence of corporate environmental ethics on competitive advantage: The mediation role of green innovation. J. Bus. Ethics 2011, 104, 361–370. [Google Scholar] [CrossRef]

- Chiou, T.-Y.; Chan, H.K.; Lettice, F.; Chung, S.H. The influence of greening the suppliers and green innovation on environmental performance and competitive advantage in Taiwan. Transp. Res. Part E Logist. Transp. Rev. 2011, 47, 822–836. [Google Scholar] [CrossRef]

- Forsman, H. Environmental innovations as a source of competitive advantage or vice versa? Bus. Strategy Environ. 2013, 22, 306–320. [Google Scholar] [CrossRef]

- Liao, Z. Temporal cognition, environmental innovation, and the competitive advantage of enterprises. J. Clean. Prod. 2016, 135, 1045–1053. [Google Scholar] [CrossRef]

- Dangelico, R.M.; Pujari, D. Mainstreaming green product innovation: Why and how companies integrate environmental sustainability. J. Bus. Ethics 2010, 95, 471–486. [Google Scholar] [CrossRef]

- Grekova, K.; Bremmers, H.J.; Trienekens, J.H.; Kemp, R.G.M.; Omta, S.W.F. The mediating role of environmental innovation in the relationship between environmental management and firm performance in a multi-stakeholder environment. J. Chain Netw. Sci. 2013, 13, 119–137. [Google Scholar] [CrossRef]

- Dowell, G.; Hart, S.L.; Yeung, B. Do corporate global environmental standards create or destroy market value? Manag. Sci. 2000, 46, 1059–1074. [Google Scholar] [CrossRef]

- Hart, S.L. A natural-resource-based view of the firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar] [CrossRef]

- Hart, S.L.; Dowell, G. A natural-resource-based view of the firm: Fifteen years after. J. Manag. 2011, 37, 1464–1479. [Google Scholar]

- Eisenhardt, K.M.; Martin, J.A. Dynamic capabilities: What are they? Strateg. Manag. J. 2000, 21, 1105–1121. [Google Scholar] [CrossRef]

- Helfat, C.E.; Peteraf, M.A. The dynamic resource-based view: Capability lifecycles. Strateg. Manag. J. 2003, 24, 997–1010. [Google Scholar] [CrossRef]

- Teece, D.J. Explicating dynamic capabilities: The nature and microfoundations of (sustainable) enterprise performance. Strateg. Manag. J. 2007, 28, 1319–1350. [Google Scholar] [CrossRef]

- Crossan, M.M.; Apaydin, M. A multi-dimensional framework of organizational innovation: A systematic review of the literature. J. Manag. Stud. 2010, 47, 1154–1191. [Google Scholar] [CrossRef]

- Cohen, W.M.; Levinthal, D.A. Absorptive capacity: A new perspective on learning and innovation. Adm. Sci. Q. 1990, 35, 128–152. [Google Scholar] [CrossRef]

- Delmas, M.A.; Burbano, V.C. The Drivers of Greenwashing. Calif. Manag. Rev. 2011, 54, 64–87. Available online: https://ssrn.com/abstract=1966721 (accessed on 25 May 2017). [CrossRef]

- Wagner, M. Innovation and competitive advantages from the integration of strategic aspects with social and environmental management in European firms. Bus. Strategy Environ. 2009, 18, 291–306. [Google Scholar] [CrossRef]

- Carrión-Flores, C.E.; Innes, R. Environmental innovation and environmental performance. J. Environ. Econ. Manag. 2010, 59, 27–42. [Google Scholar] [CrossRef]

- Chen, Y.S.; Lai, S.B.; Wen, C.T. The influence of green innovation performance on corporate advantage in Taiwan. J. Bus. Ethics 2006, 67, 331–339. [Google Scholar] [CrossRef]

- Sezen, B.; Çankaya, S.Y. Effects of green manufacturing and eco-innovation on sustainability performance. Procedia Soc. Behav. Sci. 2013, 99, 154–163. [Google Scholar] [CrossRef]

- Barney, J.B. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Eltayeb, T.K.; Zailani, S.; Ramayah, T. Green supply chain initiatives among certified companies in Malaysia and environmental sustainability: Investigating the outcomes. Resour. Conserv. Recycl. 2011, 55, 495–506. [Google Scholar] [CrossRef]

- Long, X.; Chen, Y.; Du, J.; Oh, K.; Han, I. Environmental innovation and its impact on economic and environmental performance: Evidence from Korean-owned firms in China. Energy Policy 2017, 107, 131–137. [Google Scholar] [CrossRef]

- Wagner, M.; Schaltegger, S. The effect of corporate environmental strategy choice and environmental performance on competitiveness and economic performance: An empirical study of EU manufacturing. Eur. Manag. J. 2004, 22, 557–572. [Google Scholar] [CrossRef]

- Delmas, M.; Lim, J.; Nairn-Birch, N. Corporate Environmental Performance and Lobbying. Acad. Manag. Discov. Forthcom. 2015, 2, 175–197. Available online: https://ssrn.com/abstract=2603359 (accessed on 17 September 2018). [CrossRef]

- Lee, V.-H.; Ooi, K.-B.; Chong, A.Y.-L.; Lin, B. A structural analysis of greening the supplier, environmental performance and competitive advantage. Prod. Plan. Control. Manag. Oper. 2013, 26, 116–130. [Google Scholar] [CrossRef]

- Rassier, D.G.; Earnhart, D. Does the porter hypothesis explain expected future financial performance? The effect of clean water regulation on chemical manufacturing firms. Environ. Resour. Econ. 2010, 45, 353–377. [Google Scholar] [CrossRef]

- Wagner, M.; Van Phu, N.; Azomahou, T.; Wehrmeyer, W. The relationship between the environmental and economic performance of firms: An empirical analysis of the European paper industry. Corp. Soc. Responsib. Environ. Manag. 2002, 9, 133–146. [Google Scholar] [CrossRef]

- Iwata, H.; Okada, K. How does environmental performance affect financial performance? Evidence from Japanese manufacturing firms. Ecol. Econ. 2011, 70, 1691–1700. [Google Scholar] [CrossRef]

- Cheng, C.C.; Yang, C.-L.; Sheu, C. The link between eco-innovation and business performance: A Taiwanese industry context. J. Clean. Prod. 2014, 64, 81–90. [Google Scholar] [CrossRef]

- Ambec, S.; Lanoie, P. Does it pay to be green? A systematic overview. Acad. Manag. Perspect. 2008, 22, 45–62. [Google Scholar]

- Porter, M.E.; Van der Linde, C. Green and competitive: Ending the stalemate. Harv. Bus. Rev. 1995, 73, 120–134. [Google Scholar]

- Rennings, K.; Ziegler, A.; Ankele, K.; Hoffmann, E. The influence of different characteristics of the EU environmental management and auditing scheme on technical environmental innovations and economic performance. Ecol. Econ. 2006, 57, 45–59. [Google Scholar] [CrossRef]

- Aguilera-Caracuel, J.; Ortiz-de-Mandojana, N. Green Innovation and Financial Performance: An Institutional Approach. Organ. Environ. 2013, 26, 365–385. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T. Is green and profitable sustainable? Assessing the trade-off between economic and environmental aspects environmental performance. Int. J. Prod. Econ. 2012, 140, 92–102. [Google Scholar] [CrossRef]

- Orsato, R.J. Competitive environmental strategies: When does it pay to be green? Calif. Manag. Rev. 2006, 48, 127–143. [Google Scholar] [CrossRef]

- Schaltegger, S.; Synnestvedt, T. The link between ‘green’ and economic success: Environmental management as the crucial trigger between environmental and economic performance. J. Environ. Manag. 2002, 65, 339–346. [Google Scholar]

- Figge, F. Value-based environmental management. From environmental shareholder value to environmental option value. Corp. Soc. Responsib. Environ. Manag. 2005, 12, 19–30. [Google Scholar] [CrossRef]

- Hart, S.L.; Milstein, M.B. Creating sustainable value. Acad. Manag. Exec. 2003, 17, 56–67. [Google Scholar] [CrossRef]

- Schaltegger, S.; Figge, F. Environmental shareholder value: Economic success with corporate environmental management. Eco Manag. Audit. 2000, 7, 29–42. [Google Scholar] [CrossRef]

- Guenther, M.; Hoppe, H. Merging Limited Perspectives A Synopsis of Measurement Approaches and Theories of the Relationship Between Corporate Environmental and Financial Performance. J. Ind. Ecol. 2014, 18, 689–707. [Google Scholar] [CrossRef]

- Karagozoglu, N.; Lindell, M. Environmental Management: Testing the Win-Win Model. J. Environ. Plan. Manag. 2000, 43, 817–829. [Google Scholar] [CrossRef]

- Rao, P.; Holt, D. Do green supply chains lead to competitiveness and economic performance? Int. J. Oper. Prod. Manag. 2005, 25, 898–916. [Google Scholar] [CrossRef]

- Rao, P. Greening the supply chain: A new initiative in South East Asia. Int. J. Oper. Prod. Manag. 2002, 22, 632–655. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J. Relationships between Operational Practices and Performance among Early Adopters of Green Supply Chain Management Practices in Chinese Manufacturing Enterprises. J. Oper. Manag. 2004, 22, 265–289. [Google Scholar] [CrossRef]

- Chen, Y.-S. The driver of green innovation and green image—Green core competence. J. Bus. Ethics 2008, 81, 531–543. [Google Scholar] [CrossRef]

- Lin, R.-J.; Tan, K.-H.; Geng, Y. Market demand, green product innovation, and firm performance: Evidence from Vietnam motorcycle industry. J. Clean. Prod. 2013, 40, 101–107. [Google Scholar] [CrossRef]

- González-Benito, J.; González-Benito, O. Environmental Proactivity and Business Performance: An Empirical Analysis. Omega 2005, 33, 1–15. [Google Scholar] [CrossRef]

- Rohani, M.; Marini, N.M.; Ramayah, T. Supply chain integration: Level of existence in green supply chain management practices among Malaysian ISO 14001 manufacturing firms. Int. J. Supply Chain Manag. 2017, 6, 243–249. [Google Scholar]

- Podsakoff, N.P. Common Method Biases in Behavioral Research: A Critical Review of the Literature and Recommended Remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; Organ, D.W. Self-reports in organisational research: Problems and prospects. J. Manag. 1986, 12, 531–544. [Google Scholar]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 7th ed.; Prentice Hall: Upper Saddle River, NY, USA, 2010. [Google Scholar]

- Hair, J.F.; Hult, G.T.M.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; Sage: Thousand Oaks, CA, USA, 2016. [Google Scholar]

- Ringle, C.M.; Wende, S.; Becker, J.M. SmartPLS 3. Boenningstedt: SmartPLS. 2015. Available online: http://www.smartpls.com (accessed on 8 November 2018).

- Magsi, B.H.; Ong, T.S.; Ho, J.A.; Sheikh Hassan, A.F. Organizational Culture and Environmental Performance. Sustainability 2018, 10, 2690. [Google Scholar] [CrossRef]

- Hair, J.F.; Hollingsworth, C.L.; Randolph, A.B.; Chong, A.Y.L. An updated and expanded assessment of PLS-SEM in information systems research. Ind. Manag. Data Syst. 2017, 117, 442–458. [Google Scholar] [CrossRef]

- Henseler, J. A new simple approach to multigroup analysis in partial least squares path modelling. In Proceedings of the 5th International Symposium on PLS and Related Methods (PLS’07), Oslo, Norway, 5–7 September 2007. [Google Scholar]

- Bradley, W.; Henseler, J. Modeling Reflective Higher-Order Constructs Using Three Approaches with PLS Path Modeling: A Monte Carlo Comparison; Conceptual Paper; University of Otago: Dunedin, New Zealand, 2007; pp. 791–800. [Google Scholar]

- Chua, K.B.; Quoquab, F.; Mohammad, J.; Basiruddin, R. The mediating role of new ecological paradigm between value orientations and pro-environmental personal norm in the agricultural context. Asia Pac. J. Mark. Logist. 2016, 28, 323–349. [Google Scholar] [CrossRef]

- Henseler, J.; Hubona, G.; Ray, P.A. Using PLS path modeling in new technology research: Updated guidelines. Ind. Manag. Data Syst. 2016, 116, 2–20. [Google Scholar] [CrossRef]

- Pujari, D.; Peattie, K.; Wright, G. Organizational antecedents of environmental responsiveness in industrial new product development. Ind. Mark. Manag. 2004, 33, 381–391. [Google Scholar] [CrossRef]

- Teece, D.J.; Pisano, G.; Shuen, A. Dynamic capabilities and strategic management. Strateg. Manag. J. 1997, 18, 509–533. [Google Scholar] [CrossRef]

- Reinhardt, F.L. Environmental product differentiation: Implicaitons for corporate strategy. Calif. Manag. Rev. 1998, 40, 43–73. [Google Scholar] [CrossRef]

- Cordeiro, J.J.; Sarkis, J. Environmental proactivism and firm performance: Evidence from security analyst earnings forecasts. Bus. Strategy Environ. 1997, 6, 101–114. [Google Scholar] [CrossRef]

- Hassel, L.; Nilsson, H.; Nyquist, S. The value relevance of environmental performance. Eur. Account. Rev. 2005, 14, 41–61. [Google Scholar] [CrossRef]

- Sarkis, J.; Cordeiro, J.J. An empirical evaluation of environmental efficiencies and firm performance: Pollution prevention versus end-of-pipe practice. Eur. J. Oper. Res. 2001, 135, 102–113. [Google Scholar] [CrossRef]

- Cortez, M.A.; Cudia, C.P. The impact of environmental innovations on financial performance: The case of Japanese automotive and electronics companies. J. Int. Bus. Res. 2010, 9, 33–47. [Google Scholar]

- Peteraf, M.A.; Barney, J.B. Unraveling the resource-based tangle. Manag. Decis. Econ. 2003, 24, 309–323. [Google Scholar] [CrossRef]

- Chow, W.S.; Chen, Y. Corporate sustainable development: Testing a new scale based on the mainland Chinese context. J. Bus. Ethics 2012, 105, 519–533. [Google Scholar] [CrossRef]

- Delmas, M.A.; Pekovic, S. Environmental standards and labor productivity: Understanding the mechanisms that sustain sustainability. J. Organ. Behav. 2013, 34, 230–252. [Google Scholar] [CrossRef]

- Sharma, S.; Vredenburg, H. Proactive corporate environmental strategy and the development of competitively valuable organizational capabilities. Strateg. Manag. J. 1998, 19, 729–753. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Construct | Operationalization | Source of References |

|---|---|---|

| Financial performance |

| adapted from scales of several authors [45,46,47] |

| Environmental performance |

| Adapted from the scale developed by [48] |

| Environmental Innovation | Environmental product innovation dimension:

| Adapted from scales of several authors: [6,22,46,47,49,50] |

| Control variable: Firm size | Number of employees of a firm | [25,51] |

| Description | Frequency | % |

|---|---|---|

| N = 124 | ||

| Sector | ||

| Electrical machinery, radio television & communication equipment, optical equipment | 29 | 23% |

| Basic metals and fabricated metal products, motor vehicles and transport equipment | 22 | 18% |

| Rubber and plastics products | 18 | 15% |

| Chemicals, chemical products and man-made fibres | 16 | 13% |

| Others | 39 | 31% |

| Employees size | ||

| Below 200 | 52 | 42% |

| Between 200 to 500 | 41 | 33% |

| Above 500 | 31 | 25% |

| Constructs | Item Code | Mean | SD | Kurtosis | Skewness |

|---|---|---|---|---|---|

| Financial performance (FP) | FP1 | 4.85 | 0.67 | 0.489 | 0.516 |

| FP2 | 4.89 | 0.74 | (0.360) | 0.425 | |

| FP3 | 5.07 | 0.97 | (0.789) | 0.507 | |

| FP4 | 4.95 | 0.91 | (0.319) | 0.690 | |

| FP5 | 5.11 | 0.87 | (0.546) | 0.391 | |

| Environmental performance (EP) | EP1 | 4.97 | 0.78 | (0.007) | 0.159 |

| EP2 | 4.96 | 0.78 | 0.362 | 0.280 | |

| EP3 | 4.85 | 0.87 | 0.440 | 0.750 | |

| EP4 | 4.94 | 0.90 | (0.077) | 0.537 | |

| EP5 | 4.92 | 0.85 | (0.214) | 0.236 | |

| Environmental product innovation (ENP) | ENP1 | 5.05 | 0.68 | (0.419) | 0.093 |

| ENP2 | 5.15 | 0.71 | 0.686 | 0.599 | |

| ENP3 | 5.02 | 0.83 | 0.255 | 0.733 | |

| ENP4 | 4.98 | 0.93 | (0.302) | 0.721 | |

| ENP5 | 5.03 | 0.88 | (0.620) | 0.441 | |

| ENP6 | 5.05 | 0.74 | 0.056 | 0.408 | |

| ENP7 | 5.07 | 0.73 | (0.155) | 0.283 | |

| Environmental process innovation (ENC) | ENC1 | 4.98 | 0.73 | (1.117) | 0.025 |

| ENC2 | 4.99 | 0.76 | (0.005) | 0.466 | |

| ENC3 | 4.95 | 0.74 | 0.318 | 0.563 | |

| ENC4 | 4.99 | 0.93 | (0.354) | 0.688 | |

| ENC5 | 4.84 | 0.79 | (0.989) | 0.397 | |

| ENC6 | 4.88 | 0.85 | (0.860) | 0.476 |

| Items | Loadings | Constructs | AVE | CR | CA |

|---|---|---|---|---|---|

| FP1 | 0.787 | Financial performance (FP) | 0.588 | 0.877 | 0.826 |

| FP2 | 0.732 | ||||

| FP3 | 0.763 | ||||

| FP4 | 0.794 | ||||

| FP5 | 0.755 | ||||

| EP1 | 0.897 | Environmental Performance (EP) | 0.616 | 0.888 | 0.841 |

| EP2 | 0.830 | ||||

| EP3 | 0.603 | ||||

| EP4 | 0.773 | ||||

| EP5 | 0.791 | ||||

| ENC1 | 0.855 | Environmental Process Innovation (ENC) | 0.699 | 0.920 | 0.892 |

| ENC2 | 0.806 | ||||

| ENC4 | 0.796 | ||||

| ENC5 | 0.868 | ||||

| ENC6 | 0.853 | ||||

| ENP1 | 0.820 | Environmental Product Innovation (ENP) | 0.561 | 0.836 | 0.738 |

| ENP2 | 0.705 | ||||

| ENP4 | 0.737 | ||||

| ENP7 | 0.731 |

| First-Order Constructs | Loadings | Second-Order Constructs | AVE | CR | CA |

|---|---|---|---|---|---|

| ENC | 0.928 | EN | 0.856 | 0.923 | 0.832 |

| ENP | 0.923 |

| FP | EP | ECS | ECC | ECM | |

|---|---|---|---|---|---|

| FP | 0.767 | ||||

| EP | 0.458 | 0.785 | |||

| EN | 0.495 | 0.558 | 0.813 |

| EN | EP | FP | |

|---|---|---|---|

| EN | 2.335 | ||

| EP | 2.218 | 1.885 |

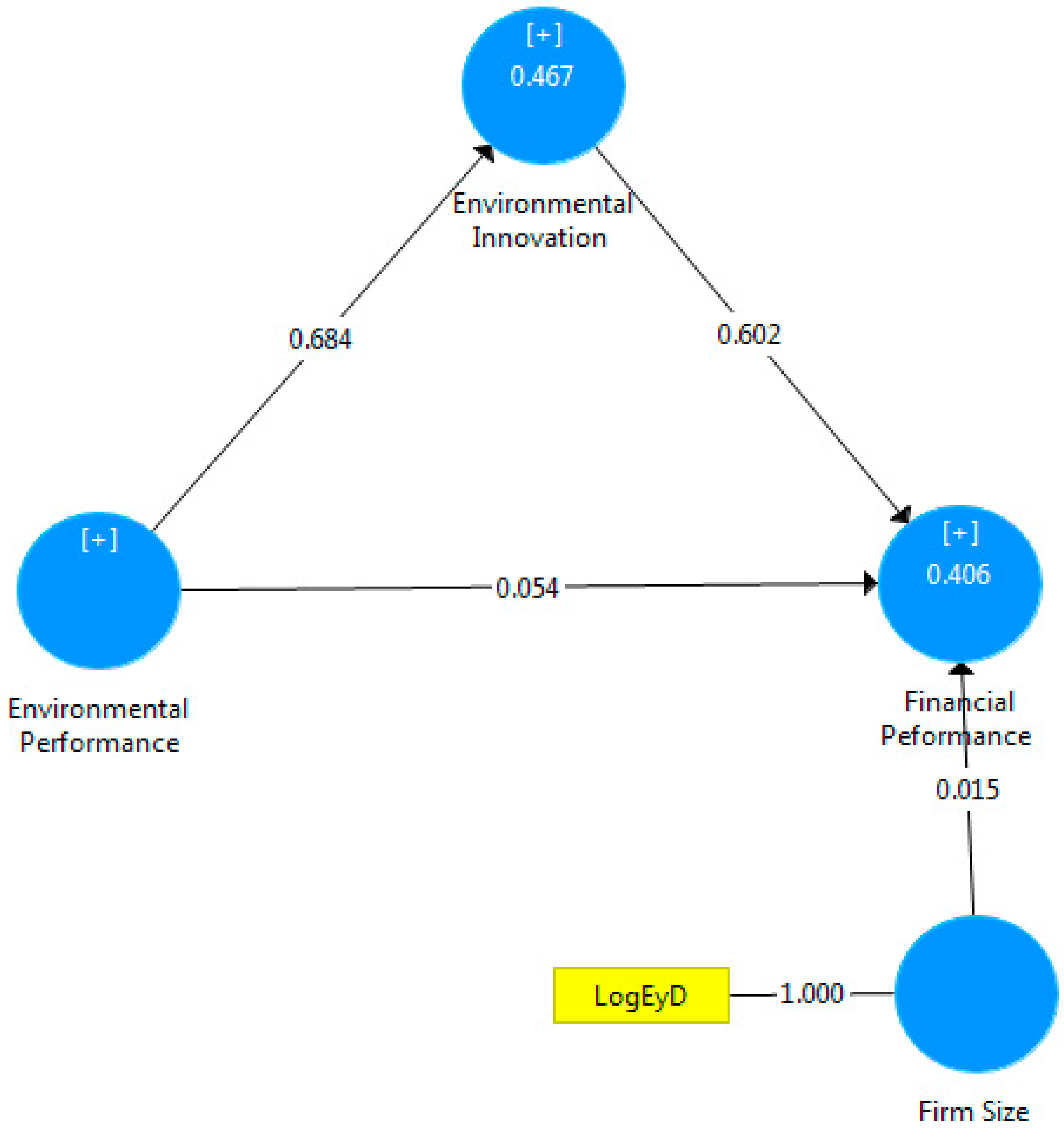

| Hypothesis | Path | Standard Beta | Standard Error | t Value | p Value | Results | f2 | R2 |

|---|---|---|---|---|---|---|---|---|

| H1 | EP>EN | 0.684 | 0.044 | 15.691 *** | 0.000 | Supported | 0.035 | 0.467 |

| H2 | EP>FP | 0.054 | 0.067 | 0.472 | 0.000 | Supported | 0.063 | 0.406 |

| H3 | EN>FP | 0.602 | 0.094 | 6.411 *** | 0.000 | Supported | 0.116 | |

| Control Variable | Log EY>FP | 0.015 | 0.071 | 0.217NS | 0.829 | Unsupported | 0.000 |

| Path | Hypothesis | Indirect Effects | Results | ||

|---|---|---|---|---|---|

| Beta | Standard Error | t-Value | |||

| EP to FP mediated by EN | H4 | 0.412 | 0.073 | 5.673 *** | Supported |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ong, T.S.; Lee, A.S.; Teh, B.H.; Magsi, H.B. Environmental Innovation, Environmental Performance and Financial Performance: Evidence from Malaysian Environmental Proactive Firms. Sustainability 2019, 11, 3494. https://doi.org/10.3390/su11123494

Ong TS, Lee AS, Teh BH, Magsi HB. Environmental Innovation, Environmental Performance and Financial Performance: Evidence from Malaysian Environmental Proactive Firms. Sustainability. 2019; 11(12):3494. https://doi.org/10.3390/su11123494

Chicago/Turabian StyleOng, Tze San, Ah Suat Lee, Boon Heng Teh, and Hussain Bakhsh Magsi. 2019. "Environmental Innovation, Environmental Performance and Financial Performance: Evidence from Malaysian Environmental Proactive Firms" Sustainability 11, no. 12: 3494. https://doi.org/10.3390/su11123494

APA StyleOng, T. S., Lee, A. S., Teh, B. H., & Magsi, H. B. (2019). Environmental Innovation, Environmental Performance and Financial Performance: Evidence from Malaysian Environmental Proactive Firms. Sustainability, 11(12), 3494. https://doi.org/10.3390/su11123494