1. Introduction

The area of capital structure has received widespread attention in the literature of corporate finance. There has been some consensus in the literature that both measures of debt levels; namely the book and market leverage are inter-related, and thus, are of concern to managers [

1]. However, given that equity values tend to change due to fluctuations in share prices and returns, there would be a gap between both measures. The literature documents that firms do not necessarily respond to shocks in equity prices by changing the book values of their debt as it would lead to an observable deviation during differing periods of rises and falls in share prices [

2].

The current study proposes to offer a distinctive perspective on the relationship between market and book leverage ratios by examining the impact of Shari’ah compliance on the divergence between both values. The notion is based on the differing styles of the managers of both categories of firms, as well as the potential for differing preferences for debt policy [

3].

The notion of Shari’ah compliance can be considered as a subset of socially responsible investments (SRI) [

4] which have grown immensely in the post 2007/08 crisis, since which time investors have been taking into consideration non-financial aspects of their investment portfolios such as ethical and governance issues, environmental concerns as well as social impacts. These considerations are also part and parcel of the screening process of Shari’ah compliance [

5]. Shari’ah screening methodologies go further to exclude firms which are highly levered, involved in businesses with elements of uncertainty as well as gambling [

3]. The screening methodologies employed are in order to ensure the sustainability of investors’ portfolios which allows solid investments paired with the aim of minimising risks [

6,

7]. Thus, the current study provides a unique insight into financing behaviour based on the nature of compliance and classifications which arise from social pressures rather than pure financial objective of wealth maximisation. To evaluate specific responses brought about by the impact of changes in equity values, this study examines the differing conditions in market prices which lead to changes in book debt. The model of the study differentiates potential conditions which drive firms to balance the deviation between the two measures. Also, the study further documents the resulting changes and their impact on the speed of adjustment.

In order to analyse the adjustment of book debt to changes in equity prices, this study utilises a set of unbalanced panel data of Malaysian firms from the period of 2003 to 2018. The rationale for selecting Malaysian firms as the sample is based on the lack of studies examining target adjustment behaviour for book debt in response to changes in equity values for developing markets. Moreover, our empirical priors indicate that there remains contention in the capital structure policies of developing markets [

8]. This study provides the opportunity to analyse the relative adjustment for a developing market where transaction costs are known to be high [

8]. Furthermore, as of the end of 2018, more than 70% of the listed companies in Malaysia were classified as Shari’ah compliant (as defined by the Securities Commission of Malaysia), Malaysia provides a unique institutional setting for this study where book debt adjustments by compliant versus non-compliant firms can be compared. Also, Malaysian capital market remains one of the most advanced Shari’ah compliant markets in the world given that Malaysia is at the forefront of Islamic finance [

9]. In addition, the literature documents that Shari’ah compliant firms are able to raise debt financing at cheaper costs given the captive markets observed in Malaysian capital markets [

10,

11]. Further contention can also be found in a recent study where the nature of compliance restricts firms’ ability to borrow, which in turn acts as an impediment to adjusting to target levels [

12].

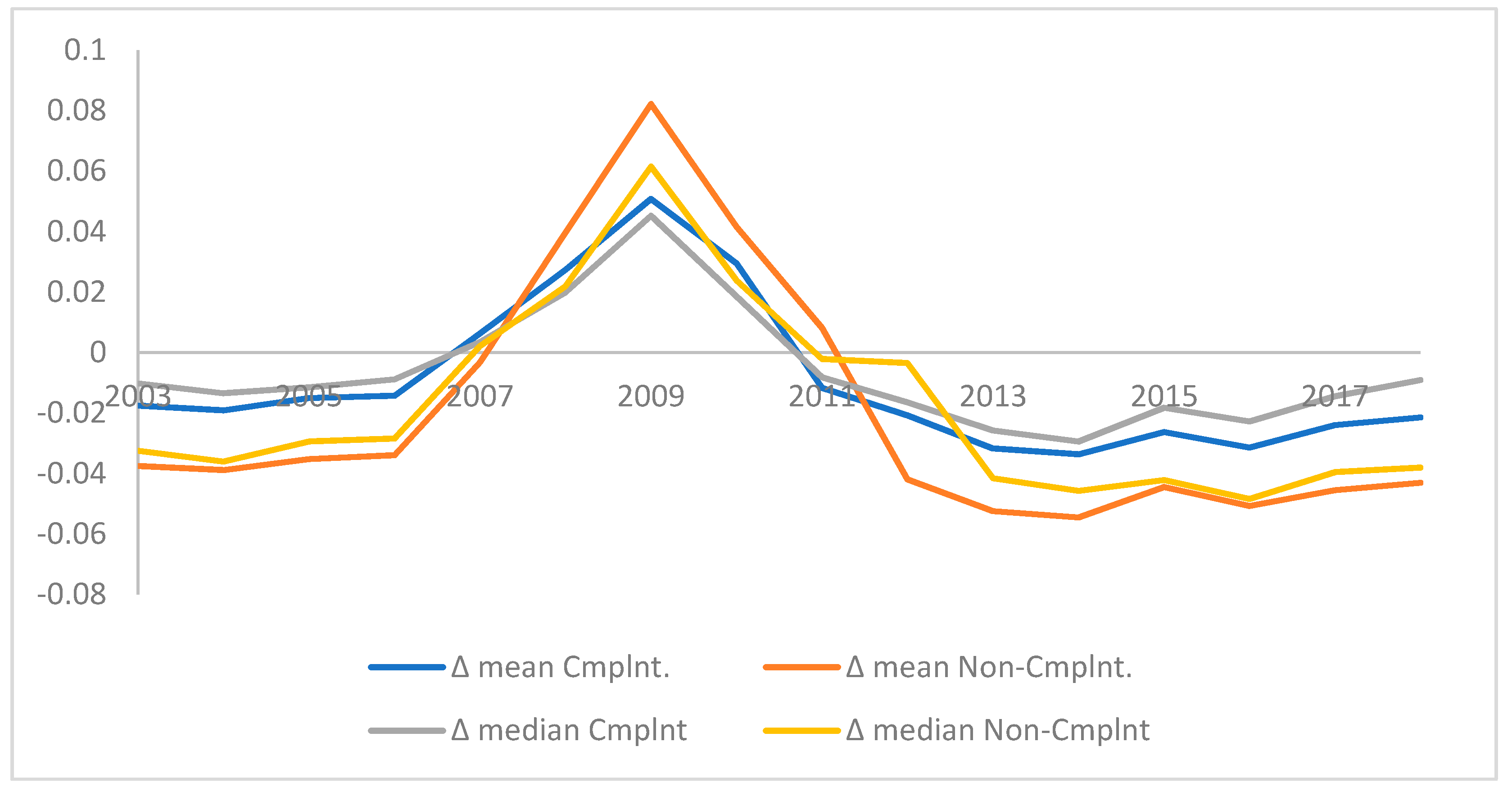

The results of the current study indicate both compliant and non-compliant firms adjust book debt ratios in response to changes in equity values. Increases in equity prices result in a lower market leverage ratio relative to book ratios. The results show that firms’ adjustment of book debt to market ratios to be at 10% on average so that non-compliant firms tend to adjust at more rapid rates (14%) relative to their counterparts (8%) indicating differences in dynamics of transaction costs for both set of firms.

In contrast, the results indicate that firms do not significantly adjust book leverage levels in response to reductions in equity prices which leads to drops in market leverage levels. The findings are consistent with the literature where firms reduce target leverage levels in-line with preserving debt capacity to fund future growth opportunities [

13]. Further analysis reveals an interesting observation where such behaviour is prevalent amongst Shari’ah compliant firms, whilst non-compliant firms tend to adjust book leverage levels in line with declining equity values.

Our asymmetric findings confirm that the results are not spurious or arising from mechanical mean reversion in methodological limitations, as suggested in the literature [

14]. Also, as an additional measure of robustness, we implement random simulation tests to validate the findings and show that the results are not spurious [

15,

16].

To further understand the approach utilised by compliant versus non-compliant firms in order to reduce the deviation from book to market leverage levels, we evaluate financing choices based on the segregation proposed by Chang and Dasgupta (2009) [

17]. The sample firms are classified based on the relative extent of deviation and then subsequent security issues are evaluated. Our findings indicate that both categories of firms tend to opt for equity issues if book values are higher than market values. However, compliant firms are less likely to retire debt in such situations. On the other hand, when market leverage is greater than book leverage, compliant firms are more likely to make significant changes to book debt ratio. Both categories of firms are equally likely to reduce reliance on equities during these periods.

This study makes several contributions to the literature which have important implications. Our findings suggest that firms in a developing market such as Malaysia tend to adjust book leverage ratios in response to increases in equity values. The effect is more profound for non-compliant firms than compliant firms. Thus, increases in market valuations tend to flow to book values to a greater extent in non-compliant firms relative to their compliant counterparts. Decreases in equity prices induce in a similar response for compliant firms but less likely for non-compliant firms. The findings indicate differing managerial views on leverage policies for both categories of firms, and thus support the findings iterated by Naz et al. 2017 [

7]. In addition, compliant firms’ motives for debt issues and the respective market interpretation are different relative to their non-compliant counterparts suggesting that these firms tend to be more sustainable i.e., less susceptible to fluctuations in equity markets [

18]. Thus, such firms are in-line with the objectives of SRI funds [

19] and provide opportunities for diversification for fund managers and investors guided by SRI principles [

20,

21]. The asymmetric response observed partially supports the findings of past studies in developed markets [

2]. However, the nature of compliance tends to moderate the responses by managers. The findings further indicate that both measures are partially interdependent.

The rest of the paper is organised in the following manner.

Section 2 provides a discussion on the literature linking changes in market values to equity and its implication on changes in book debt ratios. Moreover, this section discusses the distinction of Shari’ah compliance and non-compliance and its commonalities with SRI classifications. Furthermore, the screening based on the criteria set by the Securities Commission of Malaysia and its implications on financing decisions are discussed.

Section 3 describes the methodology applied, data and sample selection process.

Section 4 reports the results of the analysis which captures how firms respond to changes in equity prices via adjustments in book ratios. The analysis is also further subjected to a set of randomised tests to validate the findings as a measure of robustness. Results from this section are also subjected to additional tests to account for shocks in the economy as well as to account for firm cyclicality in order to test validity of the findings. Finally,

Section 5 concludes the study with a discussion of the main contributions and implications, which improves our understanding of dynamic financing choices in responses to shocks in equity prices as well as the sustainability of debt financing across firms in a developing capital market.

3. Methodology

The main objective of the current study is to evaluate the link between market and book leverage ratios for compliant and non-compliant firms. This is accomplished by examining whether firms alter their book leverage levels in line with the changes in market leverage. Thus, the deviation of these two ratios are affected by changes in the market value of a firm’s equity. Changes in equity values lead to immediate changes in market ratios whilst book ratios are expected to change gradually via the issuance of new securities.

In order to estimate the difference between the market and book leverage ratios and the speed of the adjustment for firms, the current study adopts a single stage model. The approach is based on the reformulation of the partial adjustment model which is intended to measure the rate at which managers change book values of leverage in-line with market prices of equity which determines firm value [

27]. Based on the reformulation of the partial adjustment model proposed, the difference between the market and book ratios is modelled as follows [

27]:

where

measures the change in book leverage in year

t to

t−1 for firm

i, whilst

captures the deviation of market measures relative to book measures at year

t−1 for firm

i, as a consequence of changes in equity values.

is the coefficient of interest which measures the speed of adjustment for firms after taking into account changes in market valuation of equities.

is a vector of control variables identified in

Table 1 below. The approach allows us to counter the potential for mechanical mean reversion as well as potential bias in overestimating the speed of adjustment as highlighted in the literature [

14]. The model is further expanded to control for shocks to the economy where GDP growth is negative (shocks) and cyclical firms (cyclical) and is expressed as follows:

Cyclical firms are classified based on the top 30th percentile of earnings volatility as it is a common measure of firms’ pro-cyclicality behavior evidenced in the literature [

36]. Given that the objective of this study is to estimate the difference in response to changes in market leverage ratios, the study examines the adjustment behavior depending on whether the difference between market and book ratios are positive or negative. Thus, the difference is calculated for each firm. A negative difference would indicate that market value of the firms is higher than its book value (i.e., market leverage is lower than book leverage). Divergently, firms with a market value lower than book value would have a positive difference. In order to account for these differences, the base model from Equation (1) is thus modified as follows:

where

is a dummy that captures the contrasting negative difference when market leverage is lower than book leverage. The dummy is measured at time

t−1. In order to address the potential for endogeneity issues, our estimations utilise a 2-step system GMM dynamic model [

37].

Sample Selection and Definition of Variables

The selection of the sample for this study includes all firms available in the Datastream Thomson Reuters database for the period of 2003 to 2018. The pre-2003 period is excluded as the list of compliant companies compiled by the Securities Commission of Malaysia is only available since 2003. The current study utilizes unbalanced panel data to maximize number of observations and generalization of the results [

38]. Moreover, using dynamic panel data methods this study only includes firms that are listed for a minimum of 3 years continuously. Also, financial firms due to their unique capital requirements are excluded from the sample [

39]. Furthermore, firm-years with missing variables are dropped from the analysis. The final sample comprises of 863 firms with a total of 10,408 firm-year observations. The selection and definition of regressors as control variables is further guided by the literature. Definition of variables are reported in

Table 1.

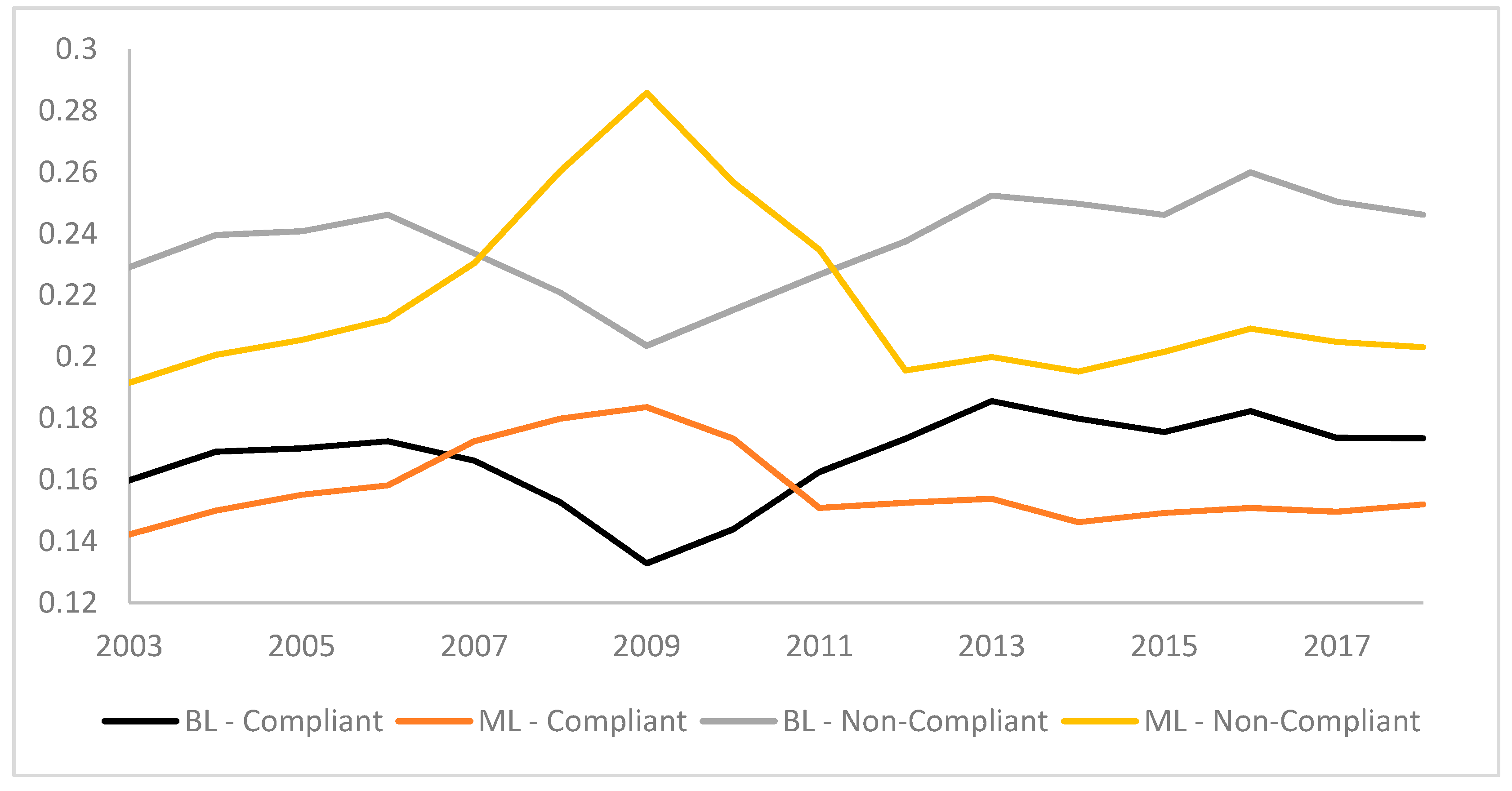

Table 2 shows the descriptive statistics of the sample. The results show that compliant firms tend to hold lower levels of debt relative to their non-compliant counterparts based on both measures. This could be attributed to the limitation placed on borrowing from conventional sources of financing [

34]. A similar situation is observed in the industry figures. Compliant firms tend to be less profitable which could plausibly be attributed to the restriction on certain business activities which are deemed immoral such as weapons and defense sectors, gambling, as well as non-halal and alcohol related activities. These firms also show to have higher levels of tangible assets yet are relatively smaller which provides an indication on the requirement to have ‘underlying assets’ for financial transactions as promoted by compliance requirements [

40].

5. Conclusions and Implications

The current study utilizes a sample of Malaysian firms from the period of 2003 to 2018 to evaluate whether firms’ adjustment of book leverage ratios in response to shocks in equity prices which leads to changes in market leverage based on the distinction of compliance to a set of rules defined as ‘Shari’ah Compliant’ by the Securities Commission of Malaysia. The nature of compliance is derived from societal pressures of providing a means for channeling savings into a more productive use in Malaysian capital market given the rising income levels, as well as high levels of savings. Moreover, institutional players (domestic and foreign) have an appetite for investment in Shari’ah compliant equities, as evidenced by the literature [

35]. Compliance to Shari’ah requirements tends to require firms to resort to more sustainable levels of financing, hence leading to differing responses to changes in share prices.

The empirical results show that adjustments in book leverage ratios are asymmetric for compliant to non-compliant firms. It is evident from the results that non-compliant firms tend to reduce book leverage ratios. This is because market leverage ratios are reduced due to increases in share prices. Non-compliant firms are also more exposed to shocks in the economy, as well as the potential for financial distress. Furthermore, our results point towards compliant firms having a higher degree of earnings quality. The bulk of reduction for non-compliant firms tend to be via the redemption of debt whereas compliant firms tend to issue equity during increases in share prices despite their limited adjustment which increases wealth for existing shareholders. This further validates the notion of compliant firms resorting to sustainable sources of financing.

During periods of depreciation in share valuations, market leverages mechanically increase, which would trigger managers to increase book leverage ratios. Compliant firms make some adjustments to increase book leverage ratios whilst non-compliant firms do not adjust during periods of decreasing share prices. Similar to the above findings, the observations point towards a more sustainable source of financing where debt levels for compliant firms tend to be less influenced by changes in equity prices. The nature of compliance requires firms to issue debt which is backed by real-assets rather than issuing debt based on changes in market valuations. The notion is robust to firms’ adjustments to target leverage levels.

The findings have important implications and provide an alternative explanation for capital structure decisions which is influenced by societal pressures rather than purely by the shareholders’ wealth maximization objective. Share price movements tend to influence non-compliant firms and have a limited influence on the book leverage ratio of compliant firms. Thus, our findings provide further insight as well as an alternative explanation which indicates that whilst the results of our empirical priors challenge the notion of leverage adjustment behavior being explained purely by movements in equity prices, our study tends to provide an explanation that includes aspects often ignored in past studies of capital markets. Therefore, our arguments point towards managers reacting with differing managerial styles depending on the investors’ expectations, as well as society, when it is institutionalized via a set of filters instituted by regulatory bodies.

,

,

{kind=link}

{kind=link}