Prices of Mexican Wholesale Electricity Market: An Application of Alpha-Stable Regression

Abstract

1. Introduction

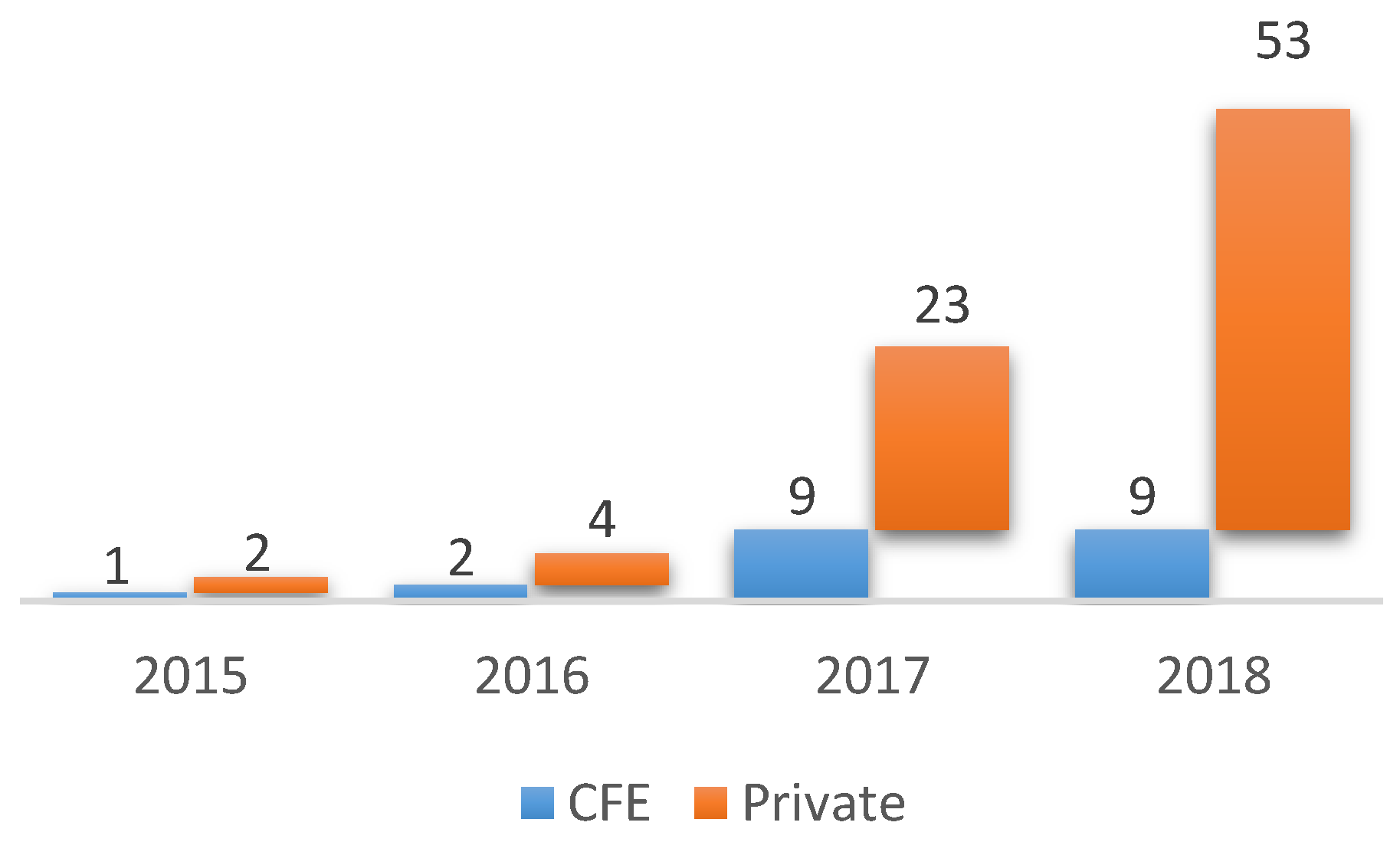

2. The Mexican Electric Sector

2.1. Mexican Wholesale Electricity Market

- Short-term Energy Market

- Power Balance

- Clean Energy Certificates Market

- Financial Transmission Rights Market

- Medium and long-term auctions

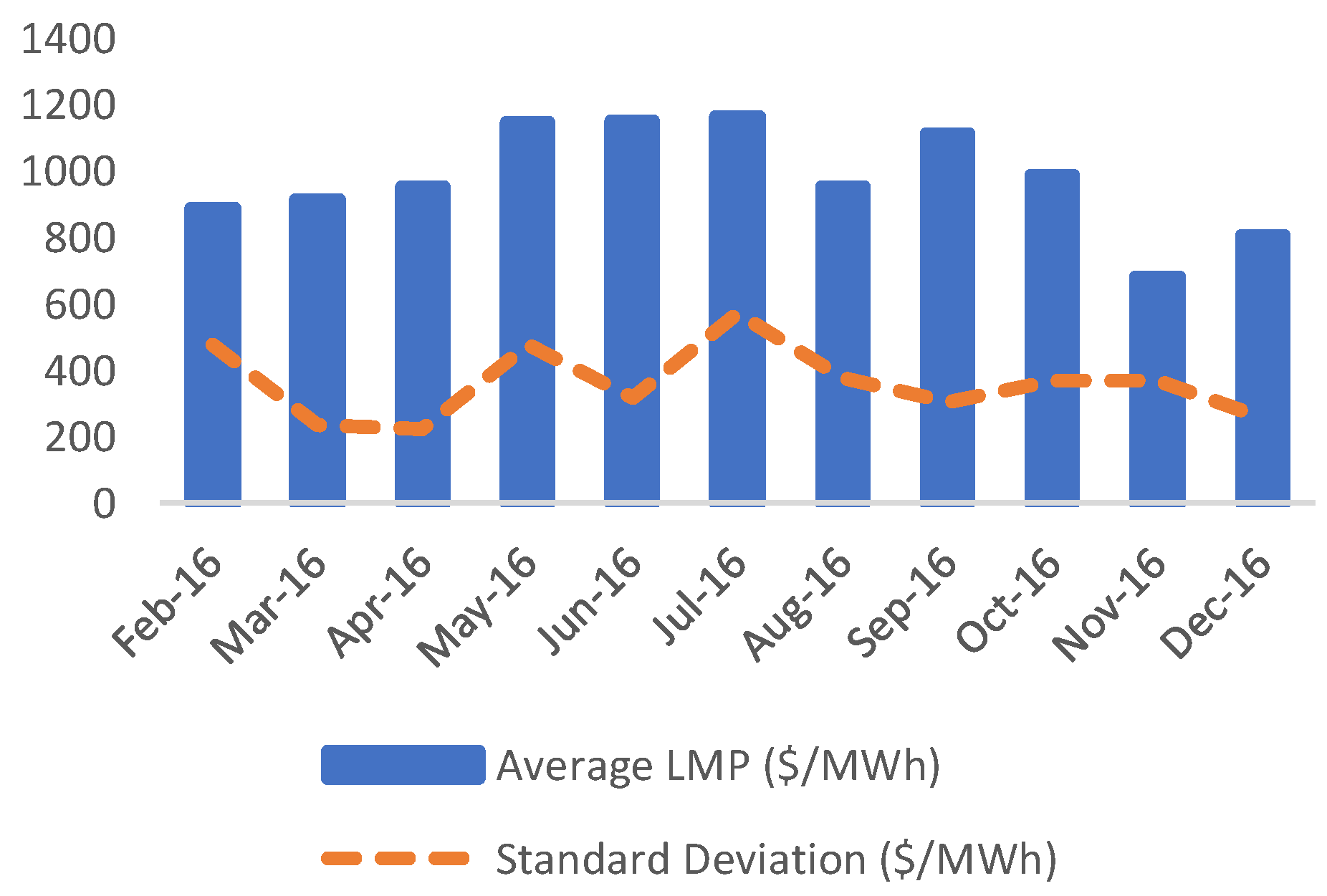

2.2. The Locational Marginal Prices

- corresponds to the energy component of node

- corresponds to the loss component of node

- corresponds to the congestion component of node

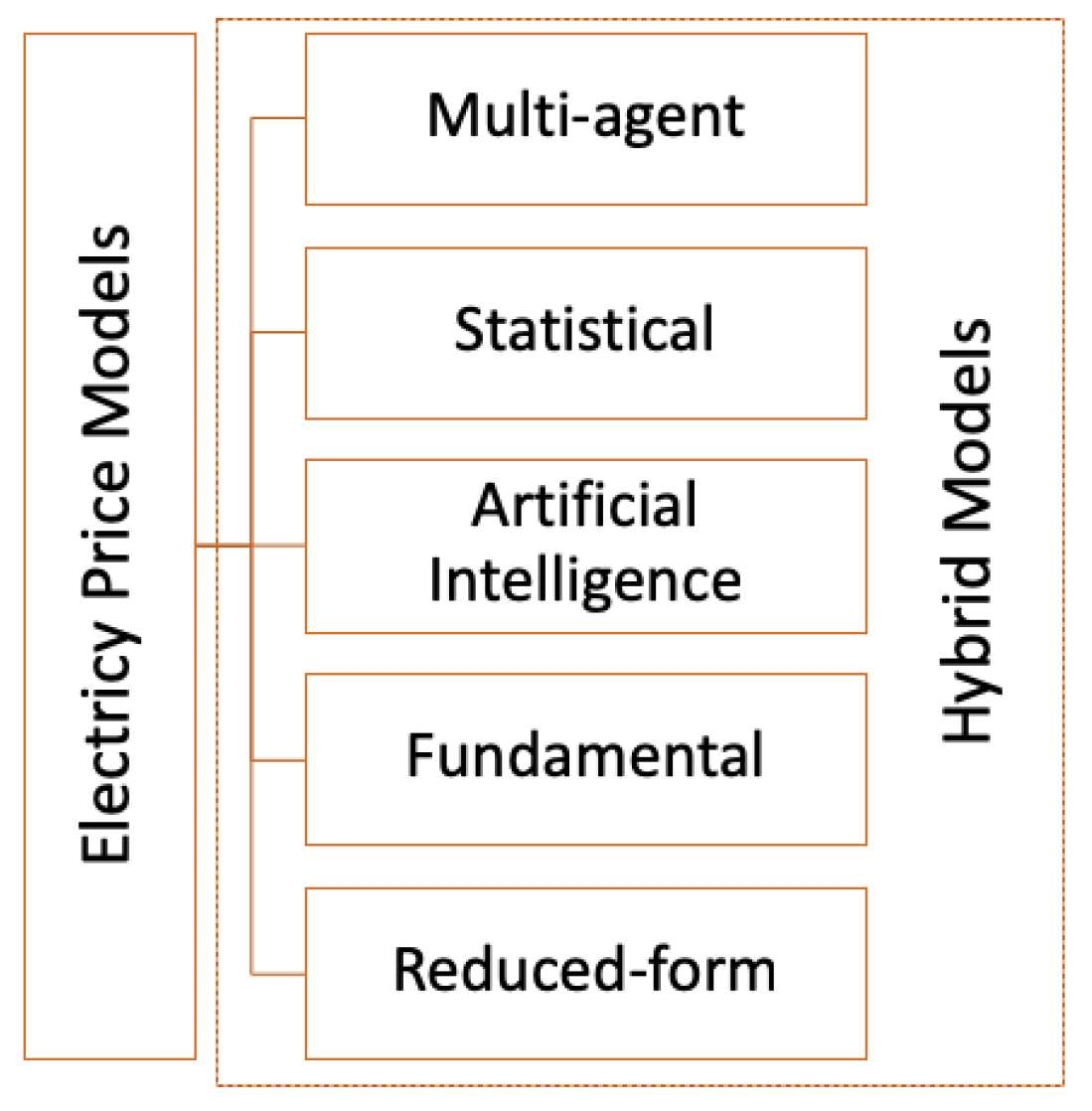

3. Alpha-Stable Distributions and Stable Regressions

3.1. α-Stable Distributions

3.2. Alpha-Stable Regression

- The tails of the distribution function are normal-like at .

- The density has infinite singularities at for and , when the distribution has peaks at .

- As , the density tends to normal and the peaks vanish

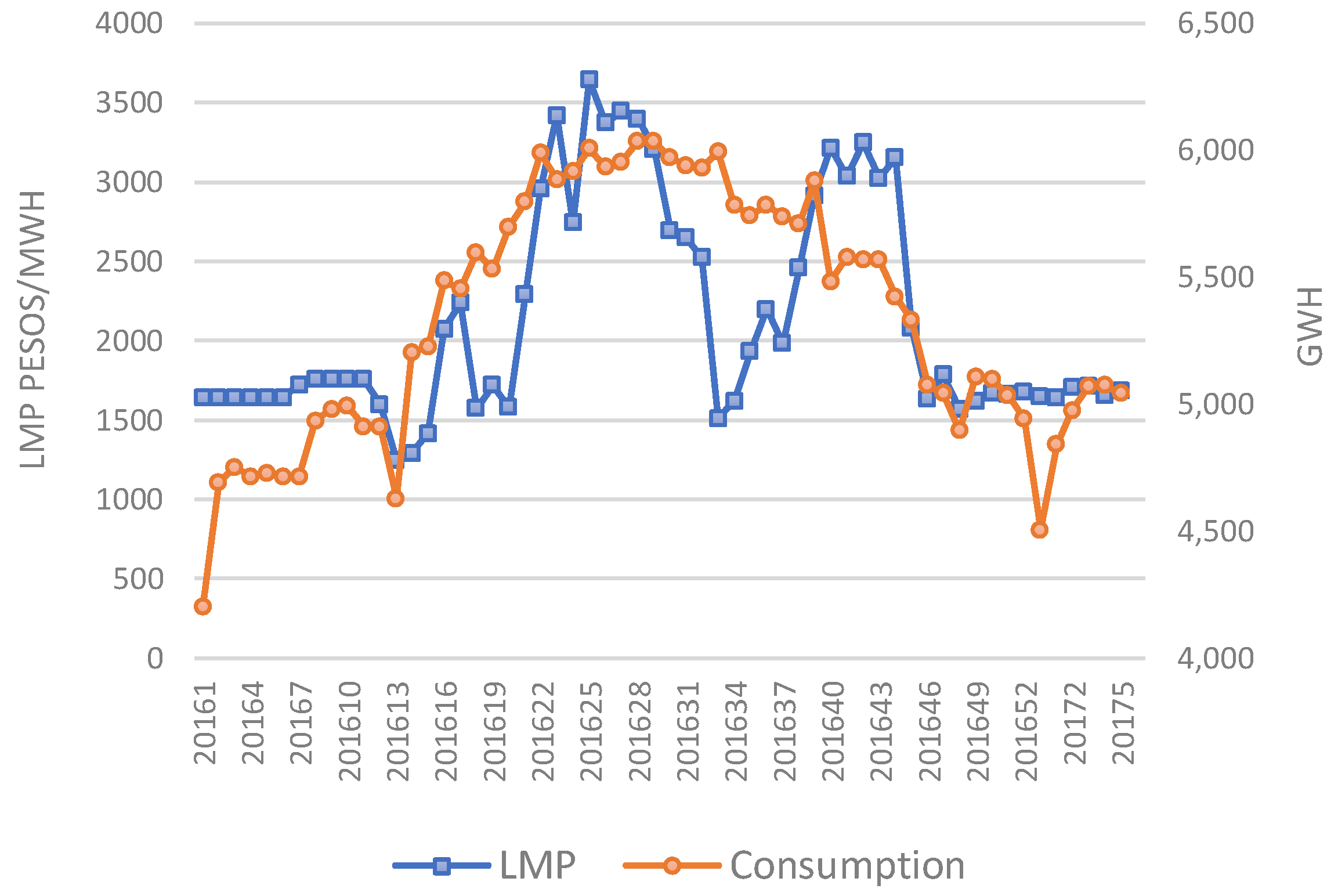

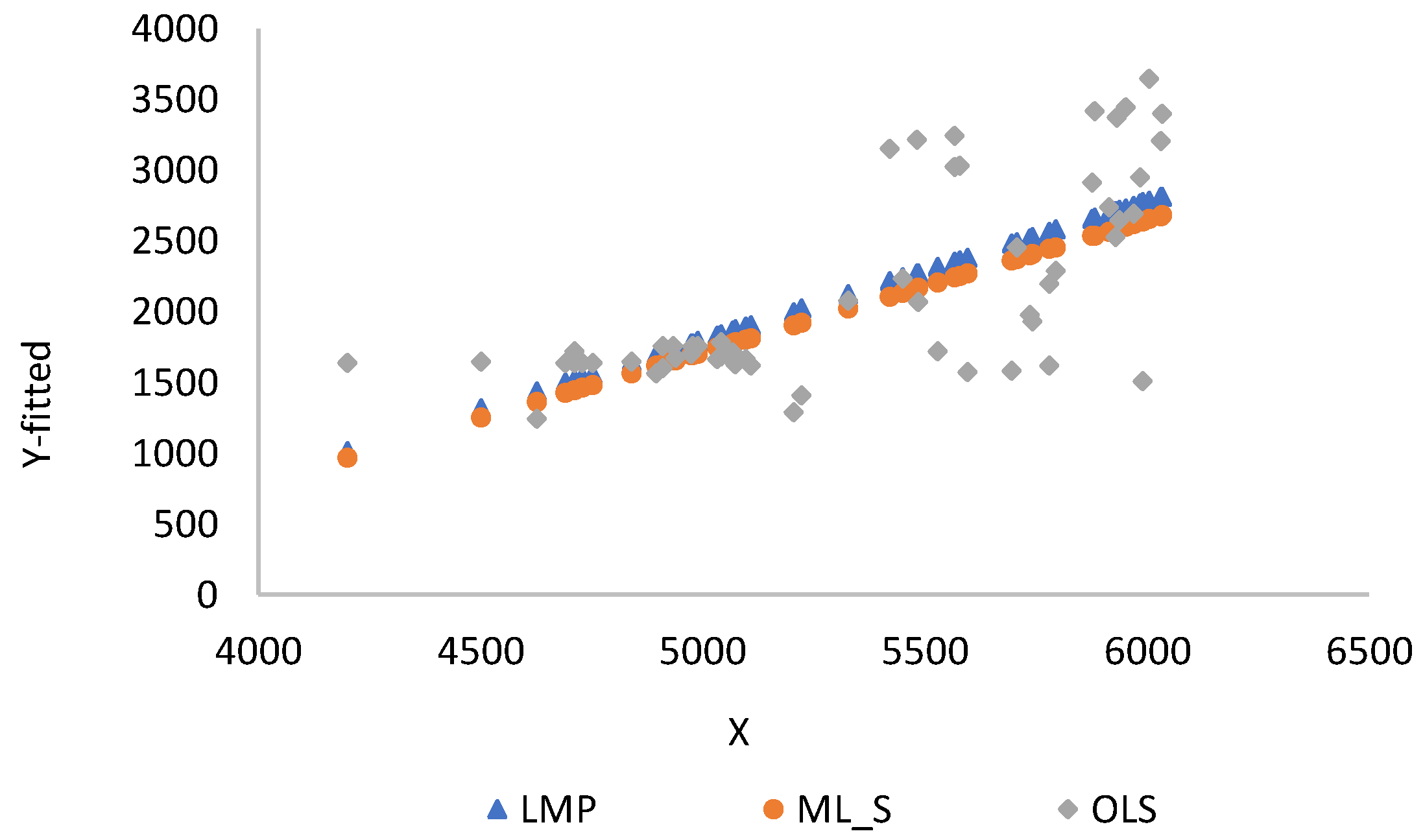

4. Estimation of Locational Marginal Prices in National Interconnected System Using Alpha-Stable Regressions

Estimation of Electricity Price in Mexico

5. Conclusions and Future Work

Author Contributions

Funding

Conflicts of Interest

References

- OECD; International Energy Agency. Mexico Energy Outlook—World Energy Outlook Special Report; International Energy Agency: Paris, France, 2016; Available online: https://www.iea.org/publications/freepublications/publication/MexicoEnergyOutlook.pdf (accessed on 30 June 2018).

- OECD; International Energy Agency. Energy Policies Beyond Countries; International Energy Agency: Paris, France, 2017; Available online: https://www.iea.org/publications/freepublications/publication/EnergyPoliciesBeyondIEACountriesMexico2017.pdf (accessed on 1 May 2018).

- Fundación Colosio. Reforma Energética: Motor de Crecimiento Económico y Bienestar; Fundación Colosio: Mexico City, Mexico, 2014; Available online: http://fundacioncolosio.mx/content/media/2015/02/1%20Reforma%20energ%C3%A9tica.pdf (accessed on 15 April 2018).

- JATA. Practical Handbook and Introduction to Mexico’s Energy Sector; JATA: San Pedro Garza Garcia, Mexico, 2016; Available online: http://jatabogados.com/publications/articles/JATA-Introduction_to_Mexicos_Energy_Sector.pdf (accessed on 14 Jun 2018).

- Frain, J.C. Maximum Likelihood Estimates of Regression Coefficients with α-Stable Residuals and Day of Week Effects in Total Returns on Equity Indices; Working Paper; Department of Economics, Trinity College Dublin: Dublin, Ireland, 2006; Available online: https://www.tcd.ie/Economics/staff/frainj/Stable_Distribution/weekday.pdf (accessed on 20 October 2018).

- Bassiou, N.; Kotropoulos, C.; Koliopoulou, E. Symmetric α-stable sparse linear regression for musical audio denoising. In Proceedings of the 8th International Symposium on Image and Signal Processing and Analysis (ISPA), Trieste, Italy, 4–6 September 2013; Available online: http://poseidon.csd.auth.gr/papers/PUBLISHED/CONFERENCE/pdf/2013/Bassiou13.pdf (accessed on 5 November 2018).

- Koutrouvelis, I.A. Regression-type estimation of the parameters of stable laws. JASA 1980, 75, 918–928. [Google Scholar] [CrossRef]

- Marmolejo-Saucedo, J.A.; Rodríguez-Aguilar, R.; Cedillo-Campos, M.G.; Salazar-Martínez, M.S. Technical efficiency of thermal power units through a stochastic frontier. Dyna 2015, 82, 63–68. [Google Scholar] [CrossRef]

- Secretaría de Energía. Prospectiva del Sector Eléctrico 2013–2027; Mexican Ministry of Energy: Mexico City, Mexico, 2013. Available online: http://sener.gob.mx/res/PE_y_DT/pub/2013/Prospectiva_del_Sector_Electrico_2013-2027.pdf (accessed on 18 July 2018).

- Secretaría de Energía. Bases del Mercado Eléctrico; Mexican Ministry of Energy: Mexico City, Mexico, 2018. Available online: https://www.cenace.gob.mx/Docs/MarcoRegulatorio/BasesMercado/Bases%20del%20Mercado%20El%C3%A9ctrico%20Acdo%20Sener%20DOF%202015%2009%2008.pdf (accessed on 22 August 2018).

- Abirami, A.; Manikanda, T. Locational Marginal Pricing approach for a deregulated electricity market. Int. Res. J. Eng. Technol. 2015, 2, 348–354. [Google Scholar]

- CENACE. Mathematical Formulation of the Model of Assignment of Units with Security Restrictions and Calculation of Locational Marginal Prices and of Related Services in the Market of a Day in Advance; Mexican Mnistry of Energy: Mexico City, Mexico, 2016. Available online: https://www.cenace.gob.mx/Docs/MercadoOperacion/Formulaci%C3%B3n%20Matem%C3%A1tica%20Modelo%20AU-MDA%20y%20PML%20v2016%20Enero.pdf (accessed on 5 May 2019).

- Nolan, J.P. Modeling Financial Data with Stable Distributions; Department of Mathematics and Statistics, American University: Washington, DC, USA, 2005; Available online: http://academic2.american.edu/~jpnolan/ (accessed on 3 April 2018).

- Andrews, B.; Calder, M.; Davis, R. Maximum Likelihood Estimation for α-Stable Autoregressive Processes. Ann. Stat. 2009, 37, 1946–1982. [Google Scholar] [CrossRef]

- Logan, B.F.; Mallows, C.L.; Rice, S.; Shepp, L.A. Limit distributions of self-normalized sums. Ann. Probab. 1973, 1, 788–809. [Google Scholar] [CrossRef]

- DuMouchel, W.H. On the asymptotic normality of the maximum likelihood estimate when sampling from a stable distribution. Ann. Stattistics 1973, 1, 948–957. [Google Scholar] [CrossRef]

- McCulloch, J.H. Linear regression with stable distributions. In A Practical Guide to Heavy Tails: Statistical Techniques and Applications; Adler, R.J., Feldman, R.E., Taqqu, M.S., Eds.; Birkhauser: Basel, Switzerland, 1998. [Google Scholar]

- Fama, E.F.; Roll, R. Some properties of symmetric stable distributions. J. Am. Stat. Assoc. 1968, 63, 817–836. [Google Scholar]

- Weron, R. Electricity price forecasting: A review of the state of the art with a look into the future. Int. J. Forecast. 2014, 30, 1030–1081. [Google Scholar] [CrossRef]

- Shahidehpour, M.; Yamin, H.; Li, Z. Market Operations in Electric Power Systems: Forecasting, Scheduling, and Risk Management; John Wiley & Sons, Inc.: New York, NY, USA, 2002. [Google Scholar]

- Weron, R. Modeling and Forecasting Electricity Loads and Prices: A Statistical Approach; John Wiley & Sons Ltd.: Chichester, UK, 2006. [Google Scholar]

- Zareipour, H. Price-Based Energy Management in Competitive Electricity Markets; VDM Verlag Dr. Müller: Saarbrücken, Germany, 2008. [Google Scholar]

- Bunn, D.W. Modeling Prices in Competitive Electricity Markets; John Wiley & Sons Ltd.: Chichester, UK, 2004. [Google Scholar]

- Burger, M.; Graeber, B.; Schindlmayr, G. Managing Energy Risk: An Integrated View on Power and Other Energy Markets; John Wiley & Sons, Inc.: New York, NY, USA, 2007. [Google Scholar]

- Huisman, R. An Introduction to Models for the Energy Markets; Risk Books: London, UK, 2009. [Google Scholar]

- Weber, R. Uncertainty in the Electric Power Industry; Springer: Berlin, Germany, 2006. [Google Scholar]

- Batlle, C.; Barquín, J. A strategic production-costing model for electricity market price analysis. IEEE Trans. Power Syst. 2005, 20, 67–74. [Google Scholar] [CrossRef]

- Koritarov, V.S. Real-world market representation with agents. IEEE Power Energy Mag. 2004, 2, 39–46. [Google Scholar] [CrossRef]

- Ventosa, M.; Baíllo, Á.; Ramos, A.; Rivier, M. Electricity market modeling trends. Energy Policy 2005, 33, 897–913. [Google Scholar] [CrossRef]

- Bunn, D.W. Forecasting loads and prices in competitive power markets. Proc. IEEE 2000, 88, 163–169. [Google Scholar] [CrossRef]

- Garcia-Martos, C.; Rodriguez, J.; Sanchez, M.J. Forecasting electricity prices by extracting dynamic common factors: Application to the Iberian market. IET Gener. Transm. Distrib. 2012, 6, 11–20. [Google Scholar] [CrossRef]

- Amjady, N.; Hemmati, M. Day-ahead price forecasting of electricity markets by a hybrid intelligent system. Eur. Trans. Electr. Power 2009, 19, 89–102. [Google Scholar] [CrossRef]

- Abedinia, O.; Amjady, N.; Shayanfar, H.A. A hybrid artificial neural network and VEPSO based on day-ahead price forecasting of electricity markets. In Proceedings of the International Conference on Artificial Intelligence (ICAI), Las Vegas, CA, USA, 21–24 July 2014. [Google Scholar]

- Amjady, N. Day-ahead price forecasting of electricity markets by a new fuzzy neural network. IEEE Trans. Power Syst. 2006, 21, 887–996. [Google Scholar] [CrossRef]

- Aggarwal, S.K.; Saini, L.M.; Kumar, A. Electricity price forecasting in Ontario electricity market using wavelet transform in artificial neural network-based model. Int. J. Contr. Autom. Syst. 2008, 6, 639–650. [Google Scholar]

- Chan, S.C.; Tsui, K.M.; Wu, H.C.; Hou, Y.; Wu, Y.-C.; Wu, F. Load/price forecasting and managing demand response for smart grids. IEEE Signal Process. Mag. 2012, 29, 68–85. [Google Scholar] [CrossRef]

- Chan, K.F.; Gray, P.; van Campen, B. A new approach to characterizing and forecasting electricity price volatility. Int. J. Forecast. 2008, 24, 728–743. [Google Scholar] [CrossRef]

- Garcia-Martos, C.; Conejo, A.J. Price forecasting techniques in power systems. In Wiley Encyclopedia of Electrical and Electronics Engineering; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2013; pp. 1–23. [Google Scholar]

- Hyndman, R.; Koehler, A.B. Another look at measures of forecast accuracy. Int. J. Forecast. 2006, 22, 679–688. [Google Scholar] [CrossRef]

- Garcia-Ascanio, C.; Mate, C. Electric power demand forecasting using interval time series: A comparison between VAR and iMLP. Energy Policy 2010, 38, 715–725. [Google Scholar] [CrossRef]

- Jonsson, T.; Pinson, P.; Nielsen, H.A.; Madsen, H.; Nielsen, T.S. Forecasting electricity spot prices accounting for wind power predictions. IEEE Trans. Sust. Energy 2013, 4, 210–218. [Google Scholar] [CrossRef]

- Misiorek, A.; Trück, S.; Weron, R. Point and interval forecasting of spot electricity prices: Linear vs. non-linear time series models. Stud. Nonlinear Dyn. E. 2006, 10, 1–36. [Google Scholar] [CrossRef]

- Nogales, F.J.; Conejo, A.J. Electricity price forecasting through transfer function models. J. Oper. Res. Soc. 2006, 57, 350–356. [Google Scholar] [CrossRef]

- Weron, R.; Misiorek, A. Forecasting spot electricity prices: A comparison of parametric and semiparametric time series models. Int. J. Forecast. 2008, 24, 744–763. [Google Scholar] [CrossRef]

- Nolan, J.P.; Ojeda-Revah, D. Linear and nonlinear regression with stable errors. J. Econ. 2013, 172, 186–194. [Google Scholar] [CrossRef]

- Nolan, J.P. Multivariate elliptically countered stable distributions: Theory and estimation. Comput. Stat. 2013, 23, 2067–2089. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| LMP | Consumption | |

|---|---|---|

| (Mexican Pesos/MWh) | (GW/h) | |

| Mean | 2132.784 | 5340.727 |

| St. dev | 680.7264 | 486.5223 |

| Skewness | 0.8344004 | −0.1500883 |

| Kurtosis | 2.218459 | 1.861669 |

| Goodness-of-Fit Test for Normal Distribution (p < 0.05) | ||

| KS test | 0.0176 | 0.0071 |

| SW test | 0.00000 | 0.00416 |

| LMP | Consumption | |

|---|---|---|

| (Mexican pesos/MWh) | (GW/h) | |

| 1.5340 | 1.7851 | |

| 0.4121 | 0.2579 | |

| 477.179 | 341.044 | |

| 2132.70 | 5340.73 | |

| Goodness-of-Fit Test for alpha-stable distribution (p < 0.05) | ||

| K-S test | 0.82939 | 0.65749 |

| Ordinary Least Squares | −3098.9843 | 0.9795 |

| Maximum Likelihood Stable | −2604.1885 | 0.9510 |

| Stable parameters of stable residuals | ||

| (Asymptotic 95% confidence intervals) | ||

| 1.34575 (1.19434, 2.49726) | ||

| 0.09980 (−0.14193, 0.34152) | ||

| 9.56450 (8.68237, 10.44663) | ||

| 182.4849 | −4.2016 | −8.7818 | −1.0338 | −2201.844 |

| −4.20169 | 79.6711 | −0.5106 | 6.2927 | 13401.96 |

| −8.7818 | −0.5106 | 5.3781 | −0.1778 | −378.819 |

| −1.0338 | 6.2927 | −0.1778 | 2.8481 | 6065.802 |

| −2201.844 | 13401.96 | −378.819 | 6065.802 | 1.46E + 07 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rodriguez-Aguilar, R.; Marmolejo-Saucedo, J.A.; Retana-Blanco, B. Prices of Mexican Wholesale Electricity Market: An Application of Alpha-Stable Regression. Sustainability 2019, 11, 3185. https://doi.org/10.3390/su11113185

Rodriguez-Aguilar R, Marmolejo-Saucedo JA, Retana-Blanco B. Prices of Mexican Wholesale Electricity Market: An Application of Alpha-Stable Regression. Sustainability. 2019; 11(11):3185. https://doi.org/10.3390/su11113185

Chicago/Turabian StyleRodriguez-Aguilar, Roman, Jose Antonio Marmolejo-Saucedo, and Brenda Retana-Blanco. 2019. "Prices of Mexican Wholesale Electricity Market: An Application of Alpha-Stable Regression" Sustainability 11, no. 11: 3185. https://doi.org/10.3390/su11113185

APA StyleRodriguez-Aguilar, R., Marmolejo-Saucedo, J. A., & Retana-Blanco, B. (2019). Prices of Mexican Wholesale Electricity Market: An Application of Alpha-Stable Regression. Sustainability, 11(11), 3185. https://doi.org/10.3390/su11113185