Decomposing Dynamics in the Farm Profitability: An Application of Index Decomposition Analysis to Lithuanian FADN Sample

,

,

,

,  and

and

Abstract

1. Introduction

2. Lithuanian Farming in the EU Context

3. Methods and Data

3.1. IDA

3.2. Data Used

4. Results

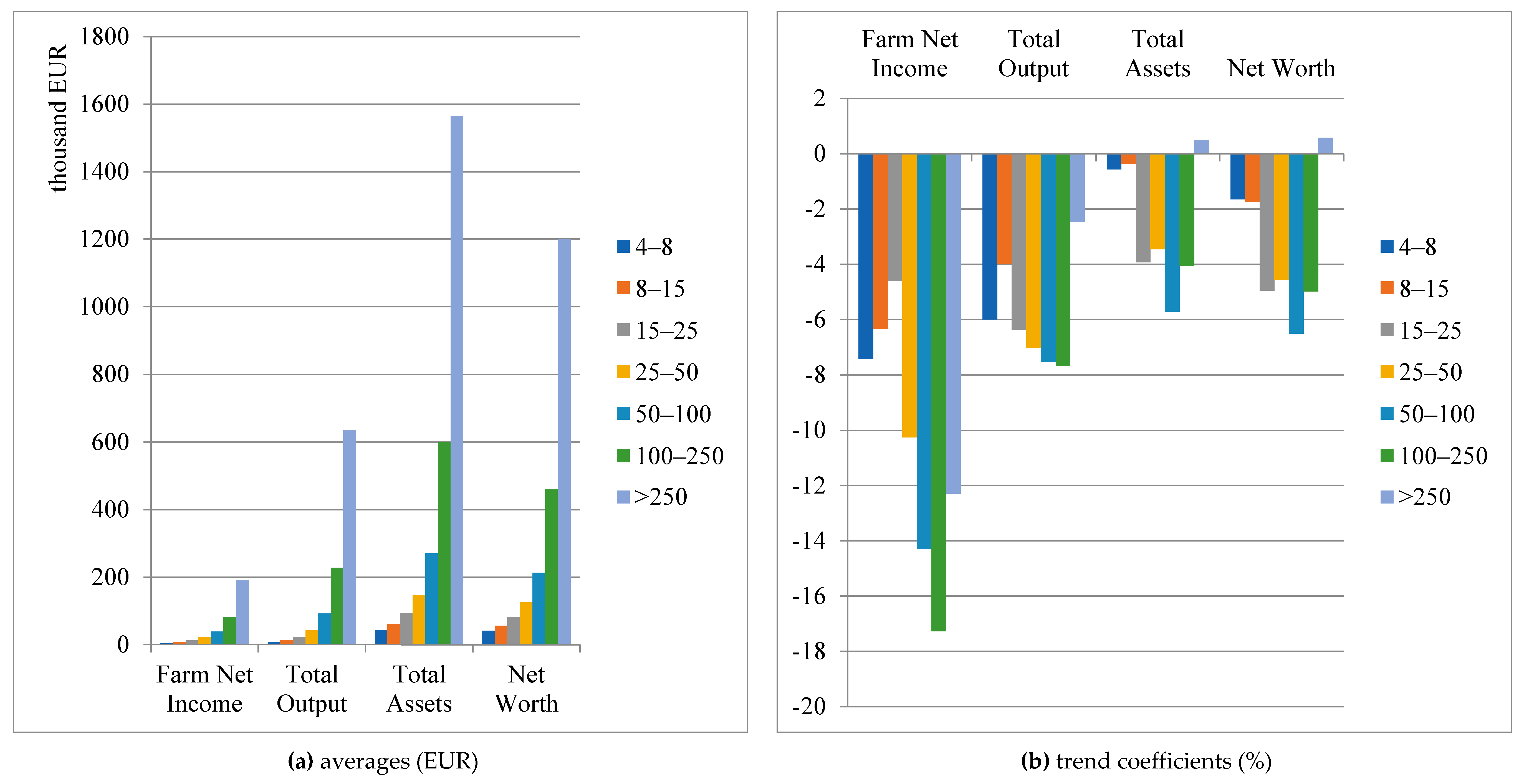

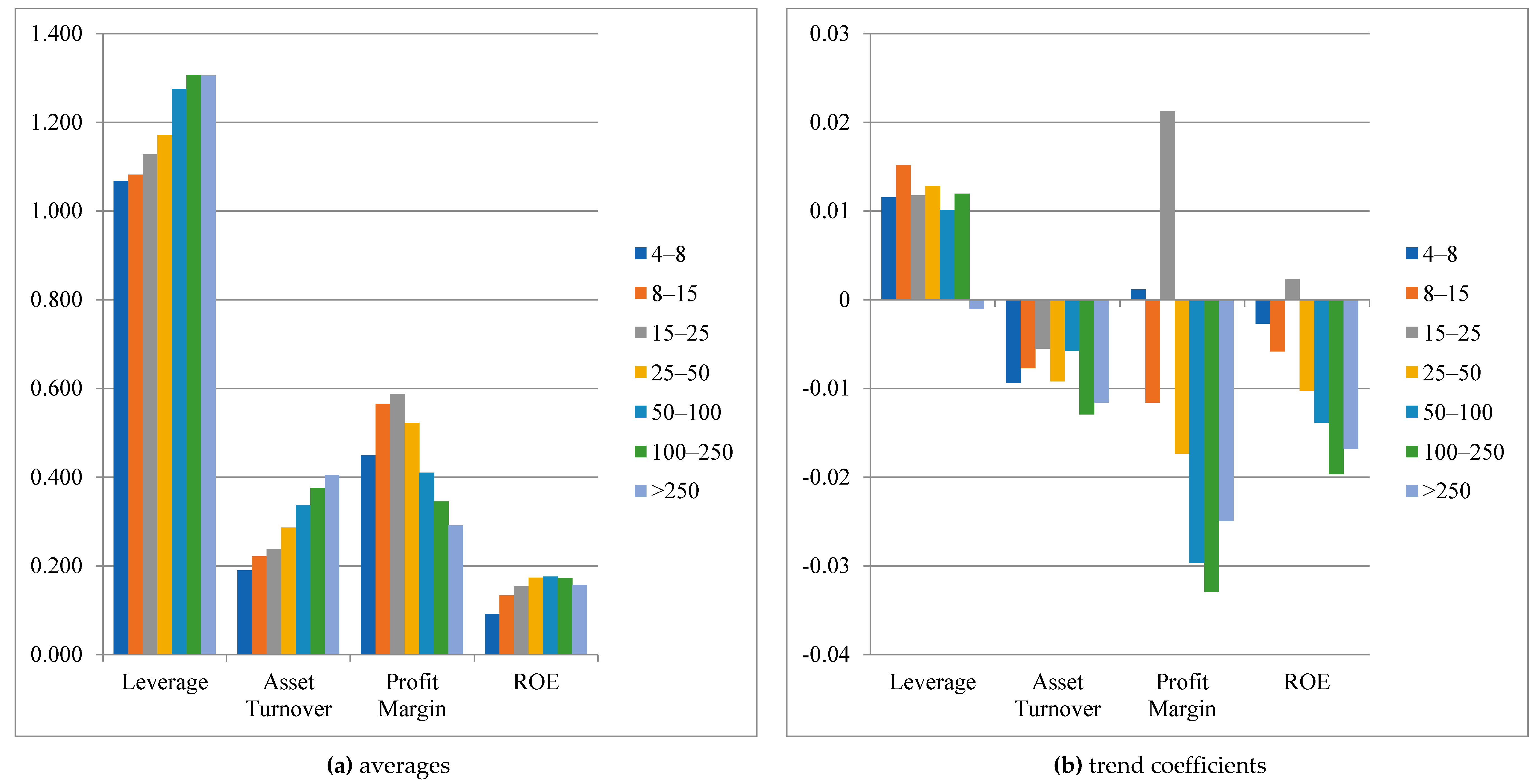

4.1. Financial Indicators

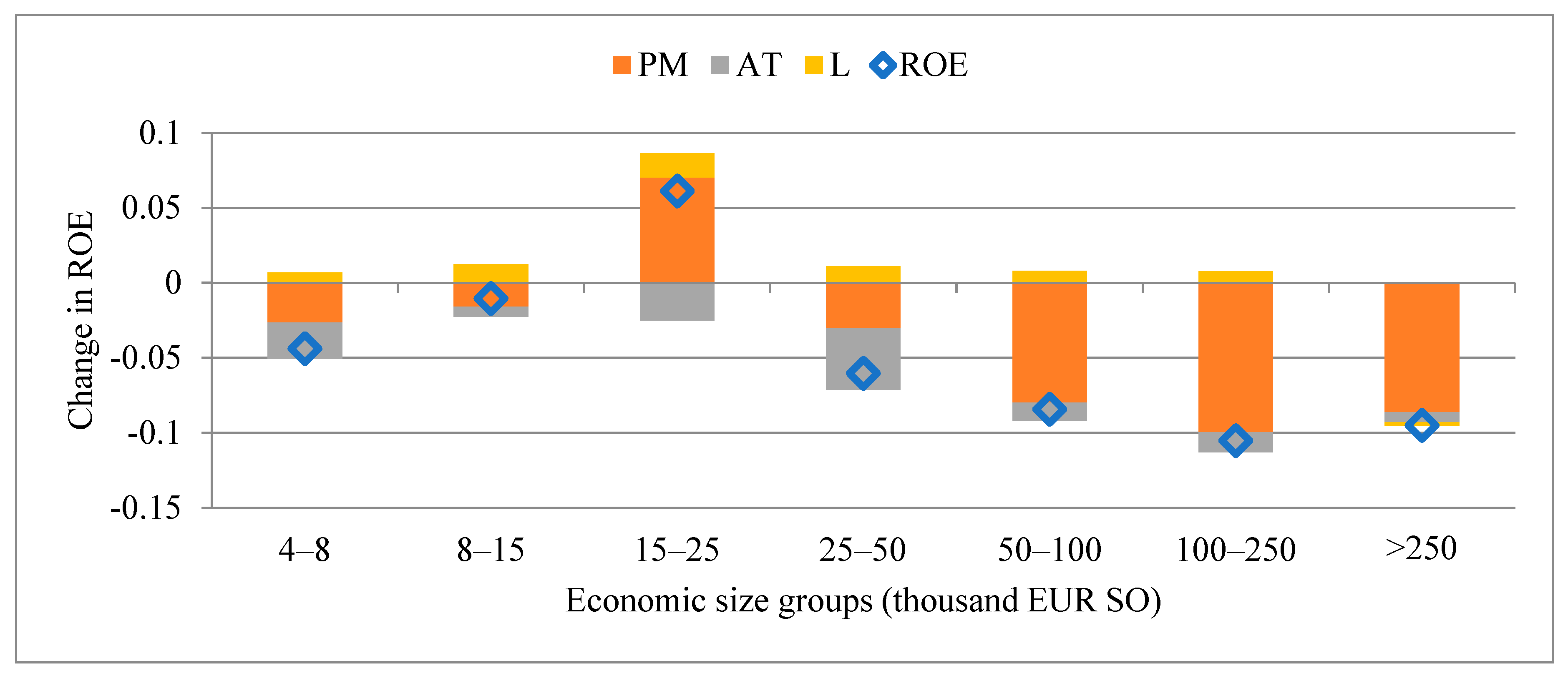

4.2. IDA

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Meul, M.; Van Passel, S.; Nevens, F.; Dessein, J.; Rogge, E.; Mulier, A.; Van Hauwermeiren, A. MOTIFS: A monitoring tool for integrated farm sustainability. Agron. Sustain. Dev. 2008, 28, 321–332. [Google Scholar] [CrossRef]

- Zahm, F.; Viaux, P.; Vilain, L.; Girardin, P.; Mouchet, C. Assessing farm sustainability with the IDEA method–from the concept of agriculture sustainability to case studies on farms. Sustain. Dev. 2008, 16, 271–281. [Google Scholar] [CrossRef]

- Kelly, E.; Latruffe, L.; Desjeux, Y.; Ryan, M.; Uthes, S.; Diazabakana, A.; Dillon, E.; Finn, J. Sustainability indicators for improved assessment of the effects of agricultural policy across the EU: Is FADN the answer? Ecol. Indic. 2018, 89, 903–911. [Google Scholar] [CrossRef]

- Repar, N.; Jan, P.; Nemecek, T.; Dux, D.; Doluschitz, R. Factors affecting global versus local environmental and economic performance of dairying: A case study of Swiss mountain farms. Sustainability 2018, 10, 2940. [Google Scholar] [CrossRef]

- Lien, G.; Hardaker, J.B.; Flaten, O. Risk and economic sustainability of crop farming systems. Agric. Syst. 2007, 94, 541–552. [Google Scholar] [CrossRef]

- Zorn, A.; Esteves, M.; Baur, I.; Lips, M. Financial Ratios as Indicators of Economic Sustainability: A Quantitative Analysis for Swiss Dairy Farms. Sustainability 2018, 10, 2942. [Google Scholar] [CrossRef]

- Czyżewski, B.; Matuszczak, A.; Miśkiewicz, R. Public goods versus the farm price-cost squeeze: shaping the sustainability of the EU’s common agricultural policy. Technol. Econ. Dev. Econ. 2019, 25, 82–102. [Google Scholar] [CrossRef]

- Balezentis, T.; Novickyte, L. Are Lithuanian Family Farms Profitable and Financially Sustainable? Evidence Using DuPont Model, Sustainable Growth Paradigm and Index Decomposition Analysis. Transform. Bus. Econ. 2018, 17, 237–254. [Google Scholar]

- Gorton, M.; Davidova, S. Farm productivity and efficiency in the CEE applicant countries: A synthesis of results. Agric. Econ. 2004, 30, 1–16. [Google Scholar] [CrossRef]

- Henningsen, A. Why is the Polish farm sector still so underdeveloped? Post-Communist Econ. 2009, 21, 47–64. [Google Scholar] [CrossRef]

- Swinnen, J.; Burkitbayeva, S.; Schierhorn, F.; Prishchepov, A.V.; Müller, D. Production potential in the “bread baskets” of Eastern Europe and Central Asia. Glob. Food Secur. 2017, 14, 38–53. [Google Scholar] [CrossRef]

- Janovska, V.; Simova, P.; Vlasak, J.; Sklenicka, P. Factors affecting farm size on the European level and the national level of the Czech Republic. Agric. Econ. (Zemědělská Ekonomika) 2017, 63, 1–12. [Google Scholar]

- Popescu, A.; Alecu, I.N.; Dinu, T.A.; Stoian, E.; Condei, R.; Ciocan, H. Farm Structure and Land Concentration in Romania and the European Union’s Agriculture. Agric. Agric. Sci. Procedia 2016, 10, 566–577. [Google Scholar] [CrossRef]

- Zdanovskis, K.; Pilvere, I. Agricultural development in Latvia after joining the European Union. Res. Rural Dev. 2015, 2, 161–168. [Google Scholar]

- Lorber, L.; Žiberna, I. European Agricultural Policy and Structural Changes in Agricultural Holdings in Podravje between 2002–2012. Podrav. Čas. za Multidiscip. Istraživanja 2014, 13, 19–44. [Google Scholar]

- Dannenberg, P.; Kuemmerle, T. Farm size and land use pattern changes in postsocialist Poland. Prof. Geogr. 2010, 62, 197–210. [Google Scholar] [CrossRef]

- Latruffe, L.; Davidova, S.; Douarin, E.; Gorton, M. Farm expansion in Lithuania after accession to the EU: The role of CAP payments in alleviating potential credit constraints. Eur.-Asia Stud. 2010, 62, 351–365. [Google Scholar] [CrossRef]

- Savickienė, J.; Miceikienė, A. Sustainable economic development assessment model for family farms. Agric. Econ. Czech 2018, 64, 527–535. [Google Scholar] [CrossRef]

- Krpalkova, L.; Cabrera, V.E.; Kvapilik, J.; Burdych, J. Dairy farm profit according to the herd size, milk yield, and number of cows per worker. Agric. Econ. (Zemědělská Ekonomika) 2016, 62, 225–234. [Google Scholar] [CrossRef]

- Naglova, Z.; Gurtler, M. Consequences of supports to the economic situation of farms with respect to their size. Agric. Econ. (Zemědělská Ekonomika) 2016, 62, 311–323. [Google Scholar]

- Poczta, W.; Średzińska, J. Wyniki produkcyjno-ekonomiczne i finansowe indywidualnych gospodarstw rolnych według ich wielkości ekonomicznej (na przykładzie regionu FADN Wielkopolska i Śląsk). Probl. World Agric. 2007, 2, 433–443. [Google Scholar]

- Vasiliev, N.; Astover, A.; Roostalu, H.; Matvejev, E. An agro-economic analysis of grain production in Estonia after its transition to market economy. Agron. Res. 2006, 4, 99–110. [Google Scholar]

- Wolf, C.A.; Stephenson, M.W.; Knoblauch, W.A.; Novakovic, A.M. Dairy farm financial performance: Firm, year, and size effects. Agric. Financ. Rev. 2016, 76, 532–543. [Google Scholar] [CrossRef]

- Bojnec, Š.; Latruffe, L. Farm size, agricultural subsidies and farm performance in Slovenia. Land Use Policy 2013, 32, 207–217. [Google Scholar] [CrossRef]

- Zimmermann, A.; Heckelei, T. Structural change of European dairy farms—A cross-regional analysis. J. Agric. Econ. 2012, 63, 576–603. [Google Scholar] [CrossRef]

- Breustedt, G.; Glauben, T. Driving forces behind exiting from farming in Western Europe. J. Agric. Econ. 2007, 58, 115–127. [Google Scholar] [CrossRef]

- Zimmermann, A.; Heckelei, T.; Domínguez, I.P. Modelling farm structural change for integrated ex-ante assessment: Review of methods and determinants. Environ. Sci. Policy 2009, 12, 601–618. [Google Scholar] [CrossRef]

- European Commission. FADN Public Database. Available online: http://ec.europa.eu/agriculture/rica/database/database_en.cfm (accessed on 1 April 2019).

- Soliman, M.T. The use of DuPont analysis by market participants. Account. Rev. 2008, 83, 823–853. [Google Scholar] [CrossRef]

- Ang, B.W.; Huang, H.C.; Mu, A.R. Properties and linkages of some index decomposition analysis methods. Energy Policy 2009, 37, 4624–4632. [Google Scholar] [CrossRef]

- Aristondo, O.; Onaindia, E. On measuring the sources of changes in poverty using the Shapley method. An application to Europe. Fuzzy Sets Syst. 2018. [Google Scholar] [CrossRef]

- Stalgiene, A.; Jedik, A.; Viira, A.H.; Krievina, A. Market Power in Lithuanian, Latvian and Estonian Dairy Sectors: The Case of Raw Milk Market. Transform. Bus. Econ. 2017, 16, 89–105. [Google Scholar]

- Ciaian, P.; Fałkowski, J.; Kancs, D.A. Access to credit, factor allocation and farm productivity: Evidence from the CEE transition economies. Agric. Financ. Rev. 2012, 72, 22–47. [Google Scholar] [CrossRef]

- Pandey, B.; Bandyopadhyay, P.; Kadam, S.; Singh, M. Bibliometric study on relationship of agricultural credit with farmer distress. Manag. Environ. Qual. 2018, 29, 278–288. [Google Scholar] [CrossRef]

- Petrick, M. Farm investment, credit rationing, and governmentally promoted credit access in Poland: A cross-sectional analysis. Food Policy 2004, 29, 275–294. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Country | Economic Size, 1000 EUR | Total Utilised Agricultural Area, ha | Total Output, EUR | Farm Net Income, EUR | Total Assets, EUR | Net Worth, EUR |

|---|---|---|---|---|---|---|

| Average | ||||||

| Netherlands | 372.4 | 35.3 | 422,167 | 51,384 | 2,065,995 | 1,335,299 |

| Denmark | 295.9 | 93.3 | 371,053 | 12,028 | 2,354,637 | 1,026,715 |

| Germany | 216.2 | 84.0 | 219,573 | 36,877 | 813,050 | 651,501 |

| Estonia | 73.2 | 121.6 | 88,892 | 14,549 | 223,024 | 152,735 |

| Lithuania | 23.4 | 43.7 | 31,600 | 12,743 | 99,404 | 84,683 |

| Latvia | 33.9 | 66.4 | 47,672 | 11,801 | 119,345 | 80,992 |

| Poland | 24.2 | 18.4 | 26,727 | 8646 | 132,633 | 123,326 |

| Annual Rate of Growth (%) | ||||||

| Netherlands | 4.0 | 1.3 | 5.0 | 6.2 | 4.8 | 5.1 |

| Denmark | 5.3 | 1.7 | 4.8 | 6.8 | 3.6 | 2.1 |

| Germany | 1.9 | 1.5 | 4.4 | 2.7 | 2.9 | 2.2 |

| Estonia | 6.7 | 2.4 | 7.0 | -3.9 | 7.8 | 6.7 |

| Lithuania | 7.0 | 3.6 | 7.1 | 1.6 | 7.0 | 6.3 |

| Latvia | 4.6 | 0.7 | 4.6 | 0.6 | 6.3 | 6.2 |

| Poland | 4.1 | 0.5 | 2.4 | 1.8 | 8.5 | 9.1 |

| Country | Land Productivity, EUR/ha | Asset Intensity, EUR/ha | ROA, % | ROE, % |

|---|---|---|---|---|

| Averages | ||||

| Netherlands | 11,883 | 58,183 | 2.5 | 3.8 |

| Denmark | 3951 | 25,108 | 0.6 | 1.4 |

| Germany | 2600 | 9656 | 4.5 | 5.6 |

| Estonia | 722 | 1809 | 7.4 | 10.4 |

| Lithuania | 710 | 2241 | 13.2 | 15.3 |

| Latvia | 718 | 1794 | 10.4 | 15.3 |

| Poland | 1447 | 7167 | 7.0 | 7.6 |

| Annual Rates of Growth (%) | Annual Rates of Change (p.p.) | |||

| Netherlands | 3.7 | 3.5 | 0.0 | 0.0 |

| Denmark | 3.1 | 1.8 | 0.1 | 0.2 |

| Germany | 2.9 | 1.4 | 0.0 | 0.0 |

| Estonia | 4.6 | 5.4 | −0.9 | −1.3 |

| Lithuania | 3.5 | 3.3 | −0.7 | −0.7 |

| Latvia | 3.9 | 5.6 | −0.6 | −0.9 |

| Poland | 1.9 | 8.0 | −0.5 | −0.6 |

| Economic Size | Netherlands | Denmark | Germany | Estonia | Lithuania | Latvia | Poland |

|---|---|---|---|---|---|---|---|

| (03) 4000–8000 EUR | 21.8 | 16.2 | 24.0 | 7.8 | |||

| (04) 8000–15,000 EUR | 34.2 | 26.8 | 33.7 | 11.6 | |||

| (05) 15,000–25,000 EUR | 20.7 | 52.6 | 46.0 | 50.6 | 17.2 | ||

| (06) 25,000–50,000 EUR | 15.5 | 35.0 | 28.8 | 94.0 | 76.3 | 83.2 | 26.6 |

| (07) 50,000–100,000 EUR | 21.7 | 61.5 | 39.6 | 172.3 | 142.2 | 159.2 | 45.0 |

| (08) 100,000–250,000 EUR | 32.5 | 99.6 | 67.5 | 335.6 | 286.8 | 324.0 | 79.7 |

| (09) 250,000–500,000 EUR | 46.9 | 137.5 | 109.8 | 626.1 | 586.4 | 673.4 | 204.0 |

| (10) 500,000–750,000 EUR | 45.8 | 176.9 | 168.8 | 751.0 | 854.1 | 1072.9 | 334.8 |

| (11) 750,000–1,000,000 EUR | 46.5 | 209.5 | 250.1 | 933.2 | 1154.3 | 491.6 | |

| (12) 1,000,000–1,500,000 EUR | 40.0 | 249.8 | 423.0 | 1185.1 | 695.5 | ||

| (13) 1,500,000–3,000,000 EUR | 33.7 | 333.5 | 1010.5 | 1682.7 | 1539.4 | 1460.0 | |

| (14) ≥3,000,000 EUR | 29.6 | 345.6 | 1729.4 | ||||

| Average | 35.3 | 93.3 | 84.0 | 121.6 | 43.7 | 66.4 | 18.4 |

| Ratio (10)/(6), % | 295 | 506 | 586 | 799 | 1120 | 1290 | 1260 |

| Total Output Per ha, Eur/ha | Netherlands | Denmark | Germany | Estonia | Lithuania | Latvia | Poland |

|---|---|---|---|---|---|---|---|

| (03) 4000–8000 EUR | 519 | 375 | 831 | ||||

| (04) 8000–15,000 EUR | 379 | 504 | 394 | 902 | |||

| (05) 15,000–25,000 EUR | 3498 | 355 | 501 | 556 | 1042 | ||

| (06) 25,000–50,000 EUR | 6037 | 2833 | 1694 | 399 | 578 | 523 | 1321 |

| (07) 50,000–100,000 EUR | 6033 | 2803 | 2081 | 510 | 658 | 573 | 1594 |

| (08) 100,000–250,000 EUR | 6484 | 2450 | 2588 | 546 | 797 | 700 | 2046 |

| (09) 250,000–500,000 EUR | 8457 | 3315 | 3154 | 722 | 881 | 1019 | 2294 |

| (10) 500,000–750,000 EUR | 14,004 | 4099 | 3235 | 1127 | 3209 | ||

| (11) 750,000–1,000,000 EUR | 20,135 | 4647 | 3093 | 1193 | 1810 | ||

| (12) 1,000,000–1,500,000 EUR | 35,880 | 5314 | 2584 | 2504 | |||

| (13) 1,500,000–3,000,000 EUR | 70,429 | 6191 | 2026 | 1993 | 1925 | ||

| (14) ≥3,000,000 EUR | 238,168 | 2651 | |||||

| Average | 11,883 | 3951 | 2600 | 722 | 710 | 718 | 1398 |

| Ratio (10)/(6) | 232 | 145 | 191 | 181 | 195 | 195 | 243 |

| Indicator | FADN Variable |

|---|---|

| Financial Indicators | |

| Farm Net Income, EUR | SE420 |

| Total output, EUR | SE131 |

| Total assets, EUR | SE436 |

| Net worth, EUR | SE501 |

| Relative Indicators | |

| Profit margin (P) | SE420/SE131 |

| Asset turnover (N) | SE131/SE436 |

| Leverage (L) | SE436/SE501 |

| Return on Equity (ROE) | SE420/SE501 |

| Farm Size Indicators | |

| Economic size, EUR | SE005 |

| Total Utilised Agricultural Area, ha | SE025 |

| Year | Input Price Index | Output Price Index | Price Scissors | ||||

|---|---|---|---|---|---|---|---|

| Crop | Livestock | Combined | Crop | Livestock | Combined | ||

| 2010 | 100 | 100 | 100 | 100 | 100 | 100 | 100 |

| 2011 | 119 | 137.5 | 113.3 | 123.8 | 115.5 | 95.2 | 104.0 |

| 2012 | 126.3 | 133.6 | 115.2 | 123.1 | 105.8 | 91.2 | 97.5 |

| 2013 | 119.3 | 129.7 | 123.5 | 126.2 | 108.7 | 103.5 | 105.8 |

| 2014 | 115.6 | 110.3 | 111.4 | 110.9 | 95.4 | 96.4 | 95.9 |

| 2015 | 117.9 | 109.7 | 95 | 101.3 | 93.0 | 80.6 | 85.9 |

| 2016 | 102.8 | 101.7 | 93.9 | 97.3 | 98.9 | 91.3 | 94.6 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Baležentis, T.; Galnaitytė, A.; Kriščiukaitienė, I.; Namiotko, V.; Novickytė, L.; Streimikiene, D.; Melnikiene, R. Decomposing Dynamics in the Farm Profitability: An Application of Index Decomposition Analysis to Lithuanian FADN Sample. Sustainability 2019, 11, 2861. https://doi.org/10.3390/su11102861

Baležentis T, Galnaitytė A, Kriščiukaitienė I, Namiotko V, Novickytė L, Streimikiene D, Melnikiene R. Decomposing Dynamics in the Farm Profitability: An Application of Index Decomposition Analysis to Lithuanian FADN Sample. Sustainability. 2019; 11(10):2861. https://doi.org/10.3390/su11102861

Chicago/Turabian StyleBaležentis, Tomas, Aistė Galnaitytė, Irena Kriščiukaitienė, Virginia Namiotko, Lina Novickytė, Dalia Streimikiene, and Rasa Melnikiene. 2019. "Decomposing Dynamics in the Farm Profitability: An Application of Index Decomposition Analysis to Lithuanian FADN Sample" Sustainability 11, no. 10: 2861. https://doi.org/10.3390/su11102861

APA StyleBaležentis, T., Galnaitytė, A., Kriščiukaitienė, I., Namiotko, V., Novickytė, L., Streimikiene, D., & Melnikiene, R. (2019). Decomposing Dynamics in the Farm Profitability: An Application of Index Decomposition Analysis to Lithuanian FADN Sample. Sustainability, 11(10), 2861. https://doi.org/10.3390/su11102861