A Systematic Review of Smart Real Estate Technology: Drivers of, and Barriers to, the Use of Digital Disruptive Technologies and Online Platforms

Abstract

1. Introduction

1.1. Technological Disruption and Innovation in the Real Estate Industry

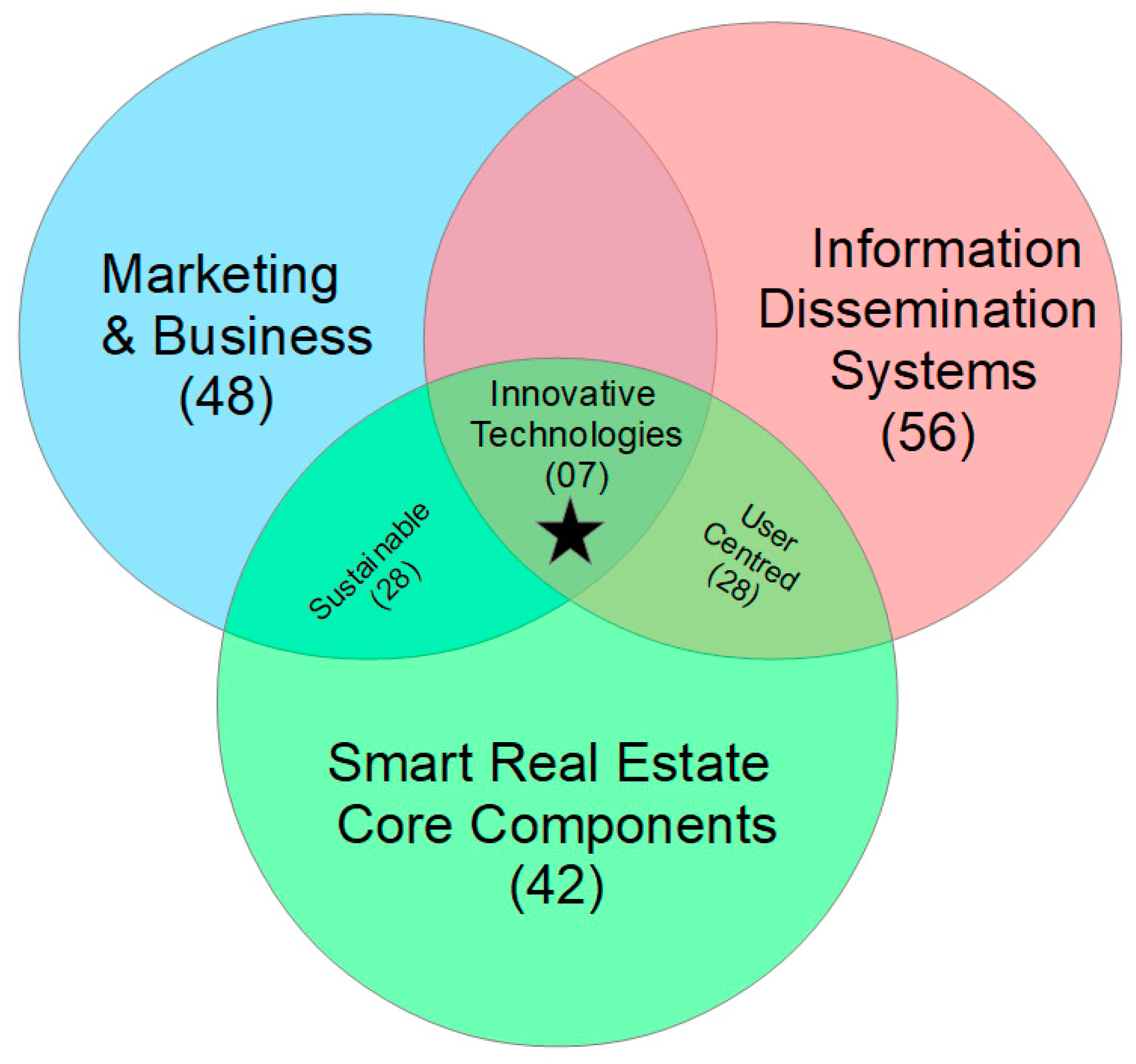

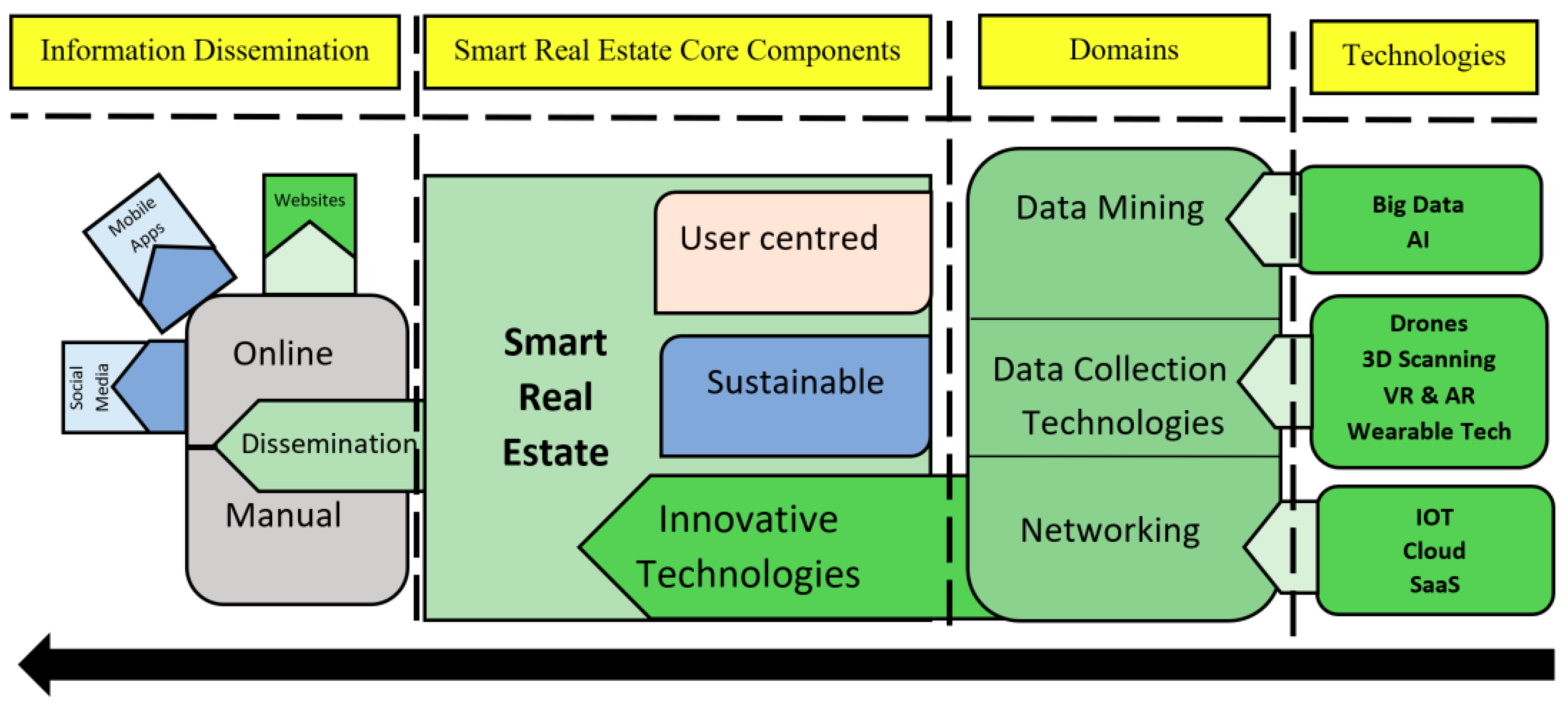

1.2. Smart Real Estate (SRE): Definition, Core Components, Technologies and Stakeholders

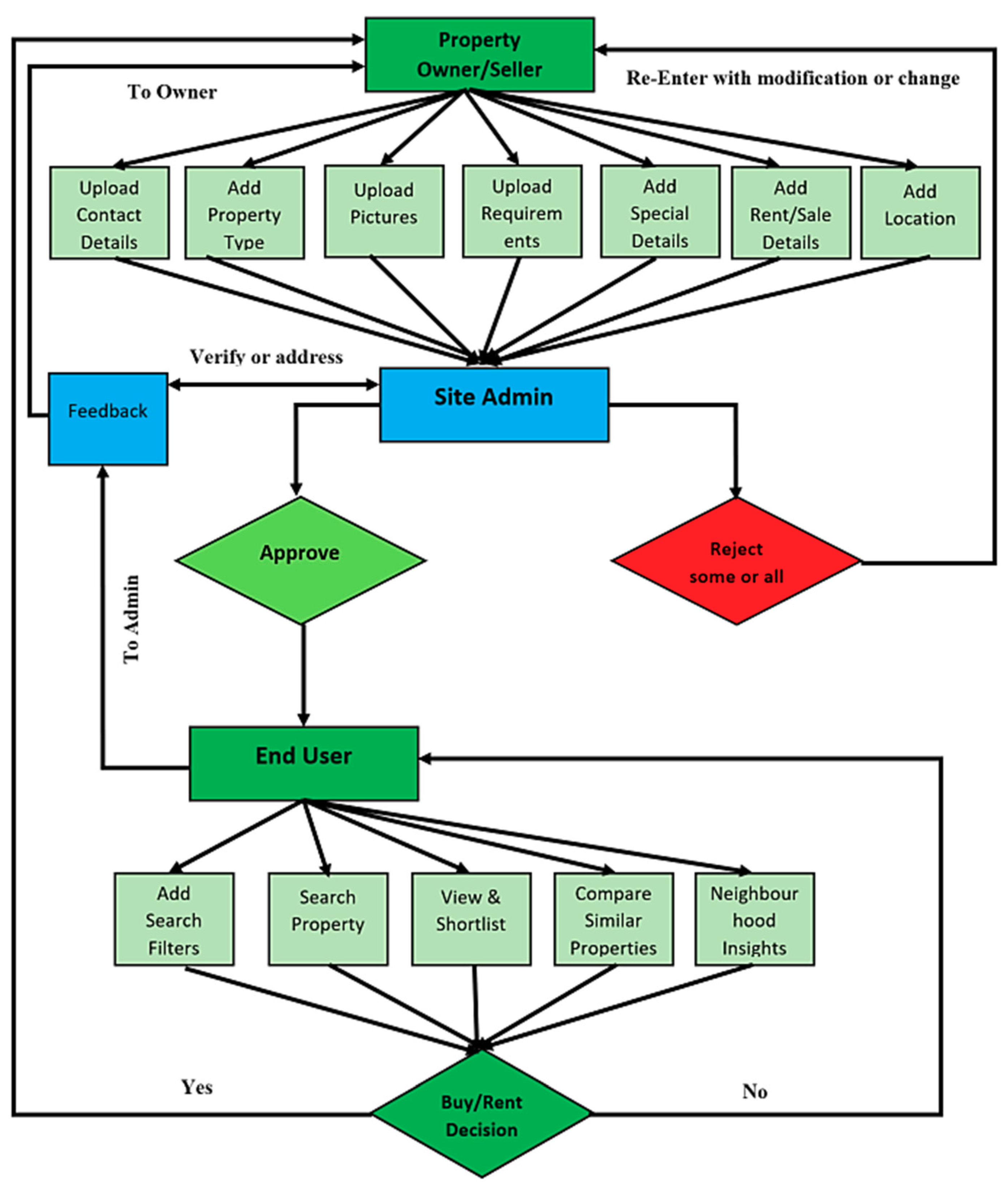

1.3. Online Rent or Buy Process

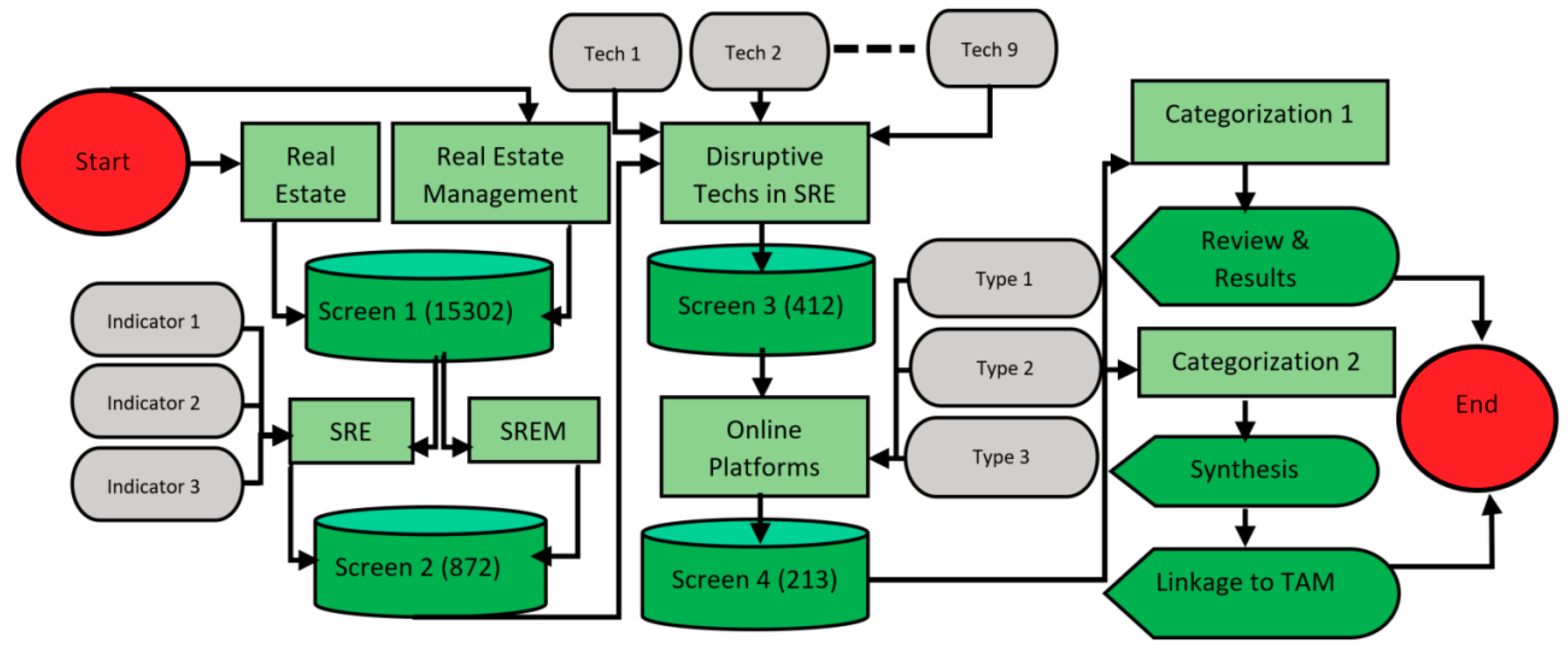

2. Materials and Methods

3. Search Results and Selected Publications

4. The SRE Conceptual Model and Definitions of its Key Components

4.1. User-Centredness

4.2. Sustainability

4.3. Innovative Technologies

5. A Review of State-of-the-Art Technology

5.1. Data-Mining Technologies

5.1.1. Big Data

5.1.2. Artificial Intelligence (AI) and Robotics

5.2. Networking Tools

5.2.1. Clouds

5.2.2. Software as a Service (SaaS)

5.2.3. Internet of Things (IoT)

5.3. Data Collection Technologies

5.3.1. Drones

5.3.2. 3D Scanning

5.3.3. Wearable Technology

5.3.4. Virtual Reality (VR) and Augmented Reality (AR)

6. Disseminating Information to Consumers in Smart Real Estate

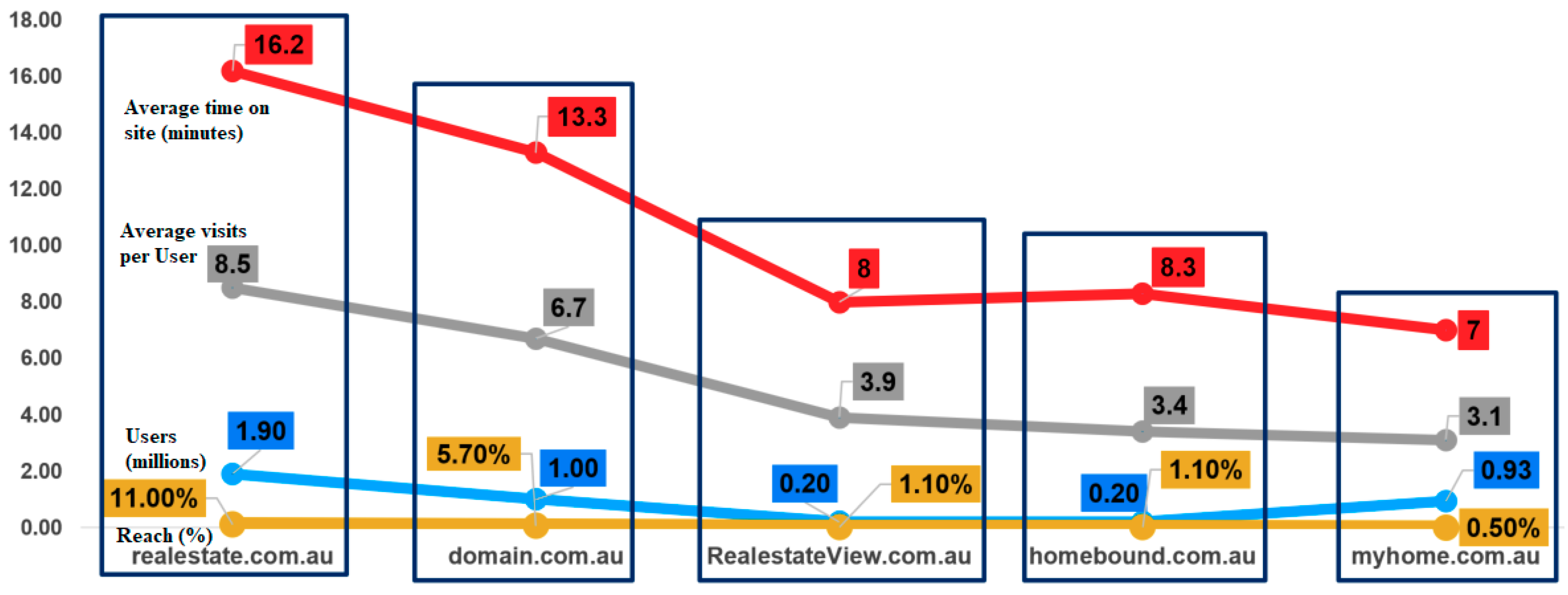

6.1. Information Dissemination on Real Estate Websites

6.2. Smartphone Applications for Disseminating Information to Real Estate Consumers

6.3. The Role of Social Media in Disseminating Information to Real Estate Consumers

7. Technology Adoption Models (TAM)

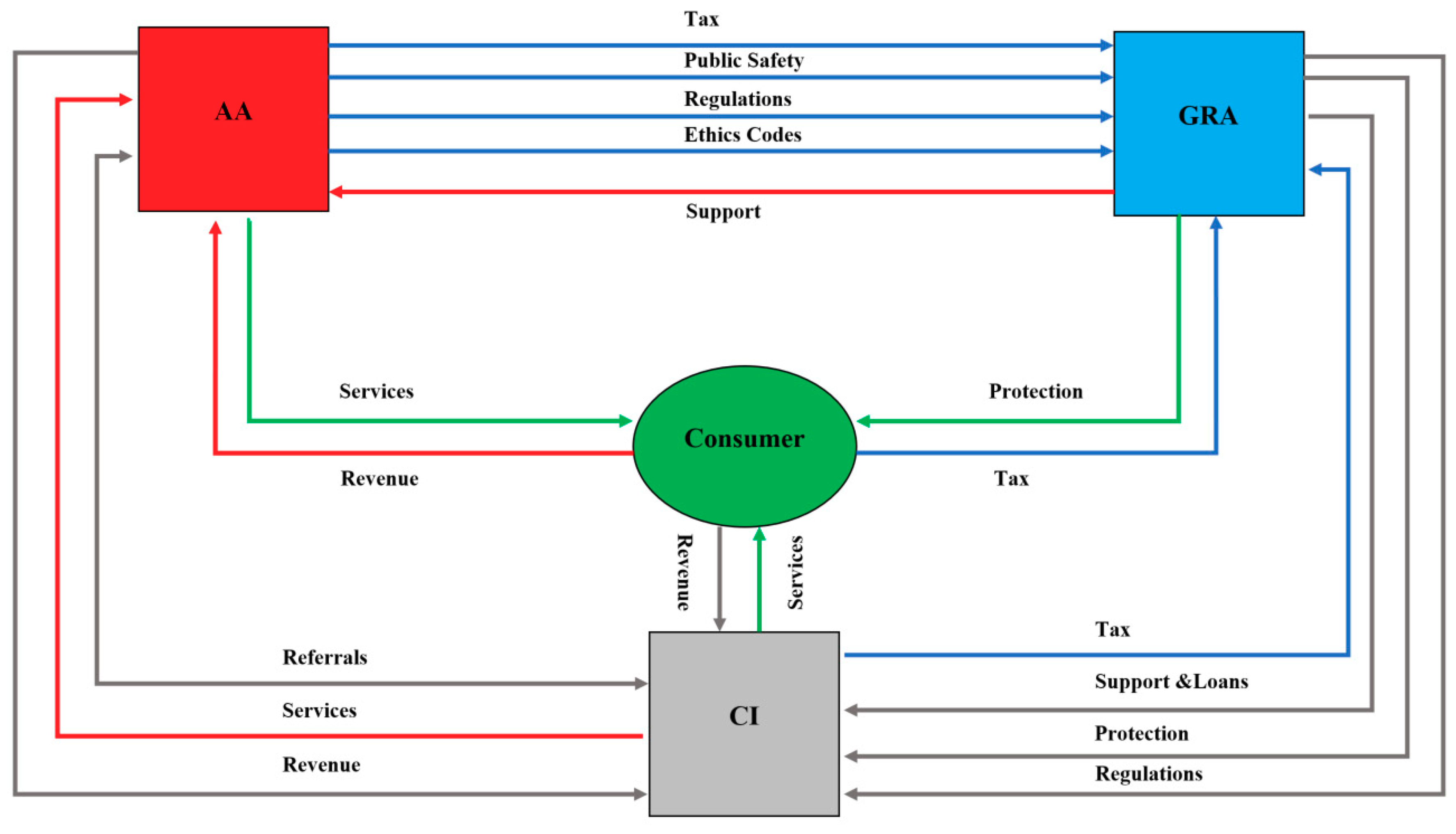

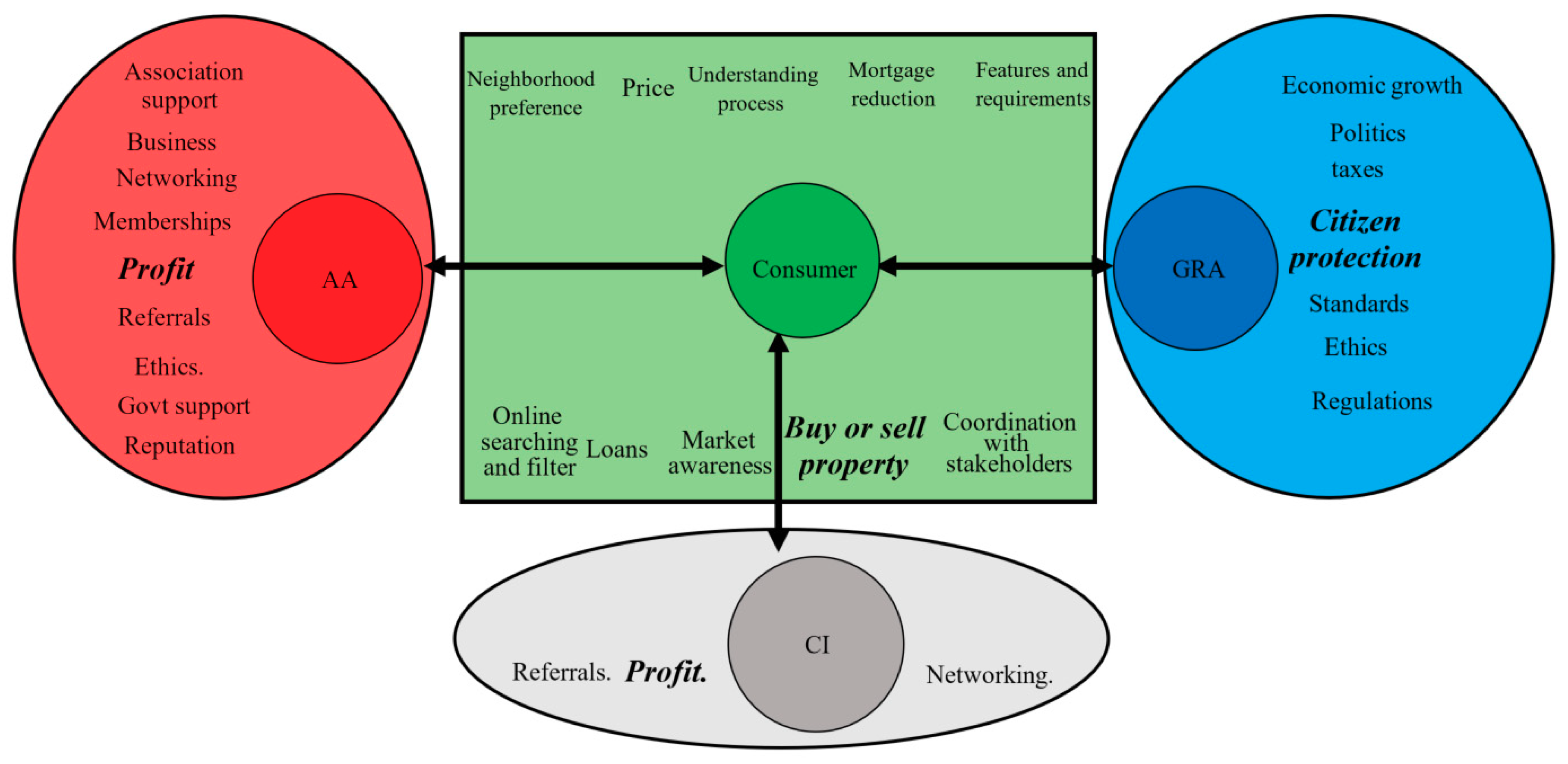

8. Stakeholder Analysis

9. Stakeholder Synthesis

10. Conclusions

Implications, Limitaions and Future Directions

Author Contributions

Funding

Conflicts of interest

References

- CB-Insights. Real Estate Tech Funding Reaches New Highs in 2016. Available online: https://www.cbinsights.com/research/real-estate-tech-startup-funding/ (accessed on 26 March 2018).

- CB-Insights. Funding to Real Estate Tech Startups Skyrockets in First Half of 2016. Available online: https://www.cbinsights.com/research/real-estate-tech-startup-funding-trends-q2-2016/ (accessed on 26 March 2018).

- Warburton, D. The Role of Technology in the Real Estate Industry. Ph.D. Thesis, University of Cape Town, Cape Town, South Africa, 2016. [Google Scholar]

- Ferren, B.; Entin, R.; Millsaps, K.; Cocosa, D.; Edwards, M.; Darragh, A. Proceedings of the 17th Annual Realcomm/IBcon Conference, Marriot Rivercenter, San Antonio, TX, USA, 9–10 June 2015; Available online: https://www.24-7pressrelease.com/press-release/406551/realcomm-ibcon-2015-announce-keynote-speakers-renowned-technologist-bran-ferren-to-headline (accessed on 3 September 2018).

- Sepasgozar, S.M.; Davis, S.R.; Li, H.; Luo, X. Modeling the Implementation Process for New Construction Technologies: Thematic Analysis Based on Australian and US Practices. J. Manag. Eng. 2018, 34, 05018005. [Google Scholar] [CrossRef]

- Danneels, E. Disruptive technology reconsidered: A critique and research agenda. J. Prod. Innov. Manag. 2004, 21, 246–258. [Google Scholar] [CrossRef]

- Sepasgozar, S.M.; Davis, S. Construction Technology Adoption Cube: An Investigation on Process, Factors, Barriers, Drivers and Decision Makers Using NVivo and AHP Analysis. Buildings 2018, 8, 74. [Google Scholar] [CrossRef]

- Conole, G.; De Laat, M.; Dillon, T.; Darby, J. ‘Disruptive technologies’, ‘pedagogical innovation’: What’s new? Findings from an in-depth study of students’ use and perception of technology. Comput. Educ. 2008, 50, 511–524. [Google Scholar] [CrossRef]

- Hall, J.K.; Martin, M.J. Disruptive technologies, stakeholders and the innovation value-added chain: A framework for evaluating radical technology development. R&D Manag. 2005, 35, 273–284. [Google Scholar]

- Conole, G. MOOCs as disruptive technologies: Strategies for enhancing the learner experience and quality of MOOCs. RED Rev. Educ. Distancia 2016, 50, 1–18. [Google Scholar] [CrossRef]

- Ganguly, A.; Chatterjee, D.; Rao, H. The Role of Resiliency in Managing Supply Chains Disruptions. In Supply Chain Risk Management; Springer: New York, NY, USA, 2018; pp. 237–251. [Google Scholar]

- Flavin, M. Disruptive technologies in higher education. Res. Learn. Technol. 2012, 20, 19184. [Google Scholar] [CrossRef]

- Dorsey, E.R.; Venuto, C.; Venkataraman, V.; Harris, D.A.; Kieburtz, K. Novel methods and technologies for 21st-century clinical trials: A review. JAMA Neurol. 2015, 72, 582–588. [Google Scholar] [CrossRef] [PubMed]

- Ba, S.; Yang, X. Zillow—Online Media Tycoon in US Real Estate Brokerage Industry. In “Internet Plus” Pathways to the Transformation of China’s Property Sector; Springer: New York, NY, USA, 2016; pp. 67–84. [Google Scholar]

- Trulia. Real Estate Regrets: Recovery Edition. Available online: https://www.trulia.com/blog/trends/regrets-2017/ (accessed on 25 April 2018).

- Chen, J.; Hui, E.C.; Wang, Z. Perceived risk, anticipated regret and post-purchase experience in the real estate market: The case of China. Hous. Stud. 2011, 26, 385–402. [Google Scholar] [CrossRef]

- Marte, J. The Biggest Regrets People Have after Buying a Home. Available online: https://www.washingtonpost.com/news/get-there/wp/2017/04/20/the-biggest-regrets-people-have-after-buying-a-home/?noredirect=on&utm_term=.79bc863bc842 (accessed on 8 June 2018).

- Zhang, Z.; Qiang, M.; Jiang, H. Finding Academic Concerns on Real Estate of US and China: A Topic Modeling Based Exploration. In Proceedings of the 21st International Symposium on Advancement of Construction Management and Real Estate; Springer: Singapore, 2018; pp. 807–817. [Google Scholar]

- Forum, W.E. Innovating in the Digital Economy. In The Global Information Technology Report 2016; Silja Baller, S.D., Lanvin, B., Eds.; Johnson Cornell University: Ithaca, NY, USA, 2016. [Google Scholar]

- Winson-Geideman, K.; Krause, A. Transformations in Real Estate Research: The Big Data Revolution. In Proceedings of the 22nd Annual Pacific-Rim Real Estate Society Conference, Queensland, Australia, 17–20 January 2016; pp. 17–20. [Google Scholar]

- Guttentag, D. Airbnb: Disruptive innovation and the rise of an informal tourism accommodation sector. Curr. Issues Tour. 2015, 18, 1192–1217. [Google Scholar] [CrossRef]

- Cheung, A. How Australia’s Cities of the Future Will Be Shaped by Real Estate Technology Startups. Available online: https://www.commercialrealestate.com.au/news/how-australias-cities-of-the-future-will-be-shaped-by-real-estate-technology-startups/ (accessed on 27 March 2018).

- Allameh, E.; Jozam, M.H.; de Vries, B.; Timmermans, H.; Beetz, J. Smart Home as a smart real estate: A state of the art review. In Proceedings of the 18th Annual European Real Estate Society Conference, Eindhoven, The Netherlands, 16–18 June 2011. [Google Scholar]

- Gabrys, J. Programming environments: Environmentality and citizen sensing in the smart city. Environ. Plan. D Soc. Space 2014, 32, 30–48. [Google Scholar] [CrossRef]

- Cocchia, A. Smart and digital city: A systematic literature review. In Smart City; Springer: Cham, Switzerland, 2014; pp. 13–43. [Google Scholar]

- Paroutis, S.; Bennett, M.; Heracleous, L. A strategic view on smart city technology: The case of IBM Smarter Cities during a recession. Technol. Forecast. Soc. Chang. 2014, 89, 262–272. [Google Scholar] [CrossRef]

- Nam, T.; Pardo, T.A. Conceptualizing smart city with dimensions of technology, people, and institutions. In Proceedings of the 12th Annual International Digital Government Research Conference: Digital Government Innovation in Challenging Times, College Park, MD, USA, 12–15 June 2011; ACM: New York, NY, USA, 2011; pp. 282–291. [Google Scholar]

- Allameh, E.; Heidari Jozam, M.; Vries, B.; de Timmermans, H.; Masoud, M. Smart Homes from vision to reality: Eliciting users’ preferences of Smart Homes by a virtual experimental method. In Proceedings of the First International Conference on Civil and Building Engineering Informatics, Tokyo, Japan, 7–8 November 2013; pp. 297–305. [Google Scholar]

- Miller, N.; Sayce, S.; Dixon, T.; Wilkinson, S. Sustainable real estate: A snapshot of where we are. In Routledge Handbook of Sustainable Real Estate; Routledge: Abingdon-on-Thames, UK, 2018; pp. 3–18. [Google Scholar]

- Miller, E. Trends and Innovations in the Real Estate Industry. Available online: http://www.innovationmanagement.se/2017/11/21/trends-and-innovations-in-the-real-estate-industry/ (accessed on 5 April 2018).

- Shulman, D. Technology vs. Commercial Real Estate: Retail, Office and Hotel Markets Face Major Disruptions. 2014. Available online: http://www.anderson.ucla.edu/lib/email/documents/econ_letter_june_2014.pdf (accessed on 27 March 2018).

- PWC. ‘Sustainability’ Transforms Design of Buildings and Developments; PWC Real Estate: Hon Kong, China, 2014. [Google Scholar]

- Richard. Table of Disruptive Technologies & Innovation. Available online: https://toptrends.nowandnext.com/2018/03/12/table-of-disruptive-technologies-innovation/ (accessed on 26 August 2018).

- Allameh, E.; Heidari Jozam, M.; de Vries, B.; Timmermans, H.; Beetz, J.; Mozaffar, F. The role of Smart Home in smart real estate. J. Eur. Real Estate Res. 2012, 5, 156–170. [Google Scholar] [CrossRef]

- Gharaibeh, A.; Salahuddin, M.A.; Hussini, S.J.; Khreishah, A.; Khalil, I.; Guizani, M.; Al-Fuqaha, A. Smart Cities: A Survey on Data Management, Security, and Enabling Technologies. IEEE Commun. Surv. Tutor. 2017, 19, 2456–2501. [Google Scholar] [CrossRef]

- Pan, S.; Jordan-Marsh, M. Internet use intention and adoption among Chinese older adults: From the expanded technology acceptance model perspective. Comput. Hum. Behav. 2010, 26, 1111–1119. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Q. 1989, 13, 319–340. [Google Scholar] [CrossRef]

- Li, Q.; Wang, Q.; Lin, Z. Effects of consumer visit to online community and product channel on local sales of large consumer goods: Evidence from real estate industry. J. Strat. Inf. Syst. 2017, 27, 191–204. [Google Scholar] [CrossRef]

- Yuan, X.; Lee, J.-H.; Kim, S.-J.; Kim, Y.-H. Toward a user-oriented recommendation system for real estate websites. Inf. Syst. 2013, 38, 231–243. [Google Scholar] [CrossRef]

- Cucchiarelli, P.; McGreal, S. Real Estate Agents; Elsevier: Amsterdam, The Netherlands, 2012. [Google Scholar]

- Gountas, S.; Gountas, J.; Mavondo, F.T. Exploring the associations between standards for service delivery (organisational culture), co-worker support, self-efficacy, job satisfaction and customer orientation in the real estate industry. Aust. J. Manag. 2014, 39, 107–126. [Google Scholar] [CrossRef]

- Pan, J.-N.; Huang, J.-T.; Chiang, T.-F. Empirical study of the local government deficit, land finance and real estate markets in China. China Econ. Rev. 2015, 32, 57–67. [Google Scholar] [CrossRef]

- Berger, A.N.; Bouwman, C.H.; Kick, T.; Schaeck, K. Bank liquidity creation following regulatory interventions and capital support. J. Financ. Intermediation 2016, 26, 115–141. [Google Scholar] [CrossRef]

- Robertson, S.; Rogers, D. Education, real estate, immigration: Brokerage assemblages and Asian mobilities. J. Ethn. Migr. Stud. 2017, 43, 2393–2407. [Google Scholar] [CrossRef]

- Chan, S.; Han, G.; Zhang, W. How strong are the linkages between real estate and other sectors in China? Res. Int. Bus. Finance 2016, 36, 52–72. [Google Scholar] [CrossRef]

- Grant, D.; Cherif, E. Using design science to improve web search innovation in real estate. J. Organ. Comput. Electron. Commer. 2016, 26, 267–284. [Google Scholar] [CrossRef]

- Rae, A.; Sener, E. How website users segment a city: The geography of housing search in London. Cities 2016, 52, 140–147. [Google Scholar] [CrossRef]

- Rae, A. Online housing search and the geography of submarkets. Hous. Stud. 2015, 30, 453–472. [Google Scholar] [CrossRef]

- Ullah, F.; Speasgozar, S.M.E.; Siddiqui, S.Q. An Investigation of Real Estate Technology Utilization in Technologically Advanced Marketplace. In Proceedings of the 9th International International Civil Engineering Congress (ICEC-2017) “Striving Towards Resilient Built Environment”, Karachi, Pakistan, 22–23 December 2017; Farrukh Arif, S.H.L., Sangi, A J., Eds.; Institute of Engineers Pakistan & NED University: Karachi, Pakistan, 2017; Volume 9, pp. 173–183. [Google Scholar]

- Kim, W.; Jeong, O.-R.; Lee, S.-W. On social Web sites. Inf. Syst. 2010, 35, 215–236. [Google Scholar] [CrossRef]

- Dalén, A.; Krämer, J. Towards a User-Centered Feedback Design for Smart Meter Interfaces to Support Efficient Energy-Use Choices. Bus. Inf. Syst. Eng. 2017, 59, 361–373. [Google Scholar] [CrossRef]

- Shin, J.; Park, Y.; Lee, D. Google TV or Apple TV?—The Reasons for Smart TV Failure and a User-Centered Strategy for the Success of Smart TV. Sustainability 2015, 7, 15955–15966. [Google Scholar] [CrossRef]

- Wang, Y.; Wang, L.; Rastegar-Mojarad, M.; Moon, S.; Shen, F.; Afzal, N.; Liu, S.; Zeng, Y.; Mehrabi, S.; Sohn, S. Clinical information extraction applications: A literature review. J. Biomed. Inform. 2017, 77, 34–39. [Google Scholar] [CrossRef] [PubMed]

- Papaioannou, D.; Sutton, A.; Carroll, C.; Booth, A.; Wong, R. Literature searching for social science systematic reviews: Consideration of a range of search techniques. Health Inf. Libr. J. 2010, 27, 114–122. [Google Scholar] [CrossRef] [PubMed]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G.; Group, P. Preferred reporting items for systematic reviews and meta-analyses: The PRISMA statement. PLoS Med. 2009, 6, e1000097. [Google Scholar] [CrossRef] [PubMed]

- Reinhardt, R.; Gurtner, S. Differences between early adopters of disruptive and sustaining innovations. J. Bus. Res. 2015, 68, 137–145. [Google Scholar] [CrossRef]

- Wise, N. Outlining triple bottom line contexts in urban tourism regeneration. Cities 2016, 53, 30–34. [Google Scholar] [CrossRef]

- Addae-Dapaah, K.; Hiang, L.K.; Sharon, N.Y.S. Sustainability of sustainable real property development. J. Sustain. Real Estate 2009, 1, 203–225. [Google Scholar]

- Robinson, S.; McAllister, P. Heterogeneous price premiums in sustainable real estate? An investigation of the relation between value and price premiums. J. Sustain. Real Estate 2015, 7, 1–20. [Google Scholar]

- Crosby, N. The Search for a Long Term/Sustainable Real Estate Appraisal/Valuation for Secured Lending. In Proceedings of the 24th Annual European Real Estate Society Conference, Delft, The Netherlands, 28 June–1 July 2017. [Google Scholar]

- Deloitte. Sustainable Real Estate: Responsible Property Investment. Available online: https://www2.deloitte.com/lu/en/pages/sustainable-development/solutions/sustainable-real-estate.html (accessed on 4 April 2018).

- Angelidou, M. Smart cities: A conjuncture of four forces. Cities 2015, 47, 95–106. [Google Scholar] [CrossRef]

- Tukiainen, T.; Leminen, S.; Westerlund, M. Cities as collaborative innovation platforms. Technol. Innov. Manag. Rev. 2015, 5, 16–23. [Google Scholar] [CrossRef]

- Kahkonen, K. Role and nature of systemic innovations in construction and real estate sector. Constr. Innov. 2015, 15, 130–133. [Google Scholar] [CrossRef]

- Tangkar, M.; Arditi, D. Innovation in the construction industry. Civ. Eng. Dimens. 2004, 2, 96–103. [Google Scholar]

- Thompson, B. Innovation in property management. J. Prop. Investig. Finance 2015, 33, 436–445. [Google Scholar] [CrossRef]

- Blayse, A.M.; Manley, K. Key influences on construction innovation. Constr. Innov. 2004, 4, 143–154. [Google Scholar] [CrossRef]

- Durão, D.; Sarmento, M.; Varela, V.; Maltez, L. Virtual and real-estate science and technology parks: A case study of Taguspark. Technovation 2005, 25, 237–244. [Google Scholar] [CrossRef]

- CB-Insights. How This Real Estate Tech Company Pioneered A New Home-Buying Model and Became A Unicorn in 3 Years. Available online: https://www.cbinsights.com/research/report/opendoor-real-estate-teardown-expert-intelligence/ (accessed on 27 March 2018).

- Gandomi, A.H.; Sajedi, S.; Kiani, B.; Huang, Q. Genetic programming for experimental big data mining: A case study on concrete creep formulation. Autom. Constr. 2016, 70, 89–97. [Google Scholar] [CrossRef]

- Huang, F.; Wang, F. A system for early-warning and forecasting of real estate development. Autom. Constr. 2005, 14, 333–342. [Google Scholar] [CrossRef]

- Cao, J.; Chan, J.Y.; Li, H.; Mahdjoubi, L.; Love, P.E. REALMEDIA: Providing multimedia-based real-estate services through the Internet. Autom. Constr. 2001, 10, 275–289. [Google Scholar] [CrossRef]

- Kim, S. Forecasting short-term air passenger demand using big data from search engine queries. Autom. Constr. 2016, 70, 98–108. [Google Scholar] [CrossRef]

- Cheng, M.-Y.; Hoang, N.-D.; Wu, Y.-W. Hybrid intelligence approach based on LS-SVM and Differential Evolution for construction cost index estimation: A Taiwan case study. Autom. Constr. 2013, 35, 306–313. [Google Scholar] [CrossRef]

- Sepasgozar, S.M.; Davis, S.R.; Loosemore, M. Dissemination Practices of Construction Sites’ Technology Vendors in Technology Exhibitions. J. Manag. Eng. 2018, 34, 04018038. [Google Scholar] [CrossRef]

- Winson-Geideman, K.; Krause, A.; Lipscomb, C.A.; Evangelopoulos, N. Real Estate Analysis in the Information Age: Techniques for Big Data and Statistical Modeling; Routledge: Abingdon-on-Thames, UK, 2017. [Google Scholar]

- Chen, X.; Lu, W. Scenarios for Applying Big Data in Boosting Construction: A Review. In Proceedings of the 21st International Symposium on Advancement of Construction Management and Real Estate; Springer: Singapore, 2018; pp. 1299–1306. [Google Scholar]

- Du, D.; Li, A.; Zhang, L. Survey on the applications of big data in Chinese real estate enterprise. Procedia Comput. Sci. 2014, 30, 24–33. [Google Scholar] [CrossRef]

- Zhou, L.; Shi, L.; Zhang, S. Database Construction of Real Estate Assessment Based on Big Data. In Proceedings of the 4th International Conference on Computer, Mechatronics, Control and Electronic Engineering, Hangzhou, China, 28–29 September 2015; Atlantis Press: Paris, France, 2015; pp. 92–96. [Google Scholar]

- Mathew, P.A.; Dunn, L.N.; Sohn, M.D.; Mercado, A.; Custudio, C.; Walter, T. Big-data for building energy performance: Lessons from assembling a very large national database of building energy use. Appl. Energy 2015, 140, 85–93. [Google Scholar] [CrossRef]

- Hoppe, G. 10 Surprising Big Data Statistics. Available online: https://blog.capterra.com/10-surprising-big-data-statistics/ (accessed on 10 April 2018).

- Phillimore, J. Housing, home and neighbourhood renewal in the era of superdiversity: Some lessons from the West Midlands. Hous. Stud. 2013, 28, 682–700. [Google Scholar] [CrossRef]

- Marr, B. Big Data: 20 Mind-Boggling Facts Everyone Must Read. Available online: https://www.forbes.com/sites/bernardmarr/2015/09/30/big-data-20-mind-boggling-facts-everyone-must-read/#25f3da8a17b1 (accessed on 10 April 2018).

- Elmqvist, N.; Irani, P. Ubiquitous analytics: Interacting with big data anywhere, anytime. Computer 2013, 46, 86–89. [Google Scholar] [CrossRef]

- Rossini, P. Using expert systems and artificial intelligence for real estate forecasting. In Proceedings of the Sixth Annual Pacific-Rim Real Estate Society Conference, Sydney, Australia, 23–27 January 2000. [Google Scholar]

- Kehoe, B.; Patil, S.; Abbeel, P.; Goldberg, K. A survey of research on cloud robotics and automation. IEEE Trans. Autom. Sci. Eng. 2015, 12, 398–409. [Google Scholar] [CrossRef]

- Ismail, N. How AI Will Drive Real Estate’s Evolution in 2018. Available online: http://www.information-age.com/ai-will-drive-real-estates-evolution-2018-123469422/ (accessed on 3 April 2018).

- Rolls, C. 5 Trends Impacting the Future of Real Estate. Available online: https://www.reinsw.com.au/web/Members/Real_Estate_Journals/201801/5_trends_impacting_the_future_of_real_estate.aspx (accessed on 10 April 2018).

- Abramovich, G. 15 Mind-Blowing Stats about Artificial Intelligence. Available online: http://www.cmo.com/features/articles/2017/8/24/15-mindblowing-stats-about-artificial-intelligence-dmexco.html#gs.IujuMlA (accessed on 10 April 2018).

- Omohundro, S. Cryptocurrencies, smart contracts, and artificial intelligence. AI Matters 2014, 1, 19–21. [Google Scholar] [CrossRef]

- Sileno, G.; Boer, A.; van Engers, T. Reading agendas between the lines, an exercise. Artif. Intell. Law 2017, 25, 89–106. [Google Scholar] [CrossRef]

- Bock, T. The future of construction automation: Technological disruption and the upcoming ubiquity of robotics. Autom. Constr. 2015, 59, 113–121. [Google Scholar] [CrossRef]

- Morano, P.; Tajani, F.; Torre, C.M. Artificial intelligence in property valuations an application of artificial neural networks to housing appraisal. Adv. Environ. Sci. Energy Plan. 2015, 2015, 23–29. [Google Scholar]

- Syam, N.; Sharma, A. Waiting for a sales renaissance in the fourth industrial revolution: Machine learning and artificial intelligence in sales research and practice. Ind. Mark. Manag. 2018, 69, 135–146. [Google Scholar] [CrossRef]

- Rafiei, M.H.; Adeli, H. A novel machine learning model for estimation of sale prices of real estate units. J. Constr. Eng. Manag. 2015, 142, 04015066. [Google Scholar] [CrossRef]

- White, R.; Banks, E. Computer Networking Problems and Solutions: An Innovative Approach to Building Resilient, Modern Networks; Addison-Wesley Professional: Boston, MA, USA, 2017. [Google Scholar]

- Petri, I.; Beach, T.; Rana, O.F.; Rezgui, Y. Coordinating multi-site construction projects using federated clouds. Autom. Constr. 2017, 83, 273–284. [Google Scholar] [CrossRef]

- Quintana, B.; Prieto, S.; Adán, A.; Bosché, F. Door detection in 3D coloured point clouds of indoor environments. Autom. Constr. 2018, 85, 146–166. [Google Scholar] [CrossRef]

- Patil, A.K.; Holi, P.; Lee, S.K.; Chai, Y.H. An adaptive approach for the reconstruction and modeling of as-built 3D pipelines from point clouds. Autom. Constr. 2017, 75, 65–78. [Google Scholar] [CrossRef]

- Schwartz, H. Majority of Professionals Use Multiple Devices at Work More Than 50% of the Time. Available online: https://businessfacilities.com/2015/06/majority-of-professionals-use-multiple-devices-at-work-more-than-50-of-the-time/ (accessed on 28 March 2018).

- Dawson, S. Technology: The power of the cloud. J. Real Estate Inst. New South Wales 2016, 67, 35. [Google Scholar]

- Mladenow, A.; Novak, N.M.; Strauss, C.; Gregu, M. Clouds and Interclouds in the Real Estate Sector. In Proceedings of the 2015 3rd International Conference on Future Internet of Things and Cloud (FiCloud), Rome, Italy, 24–26 August 2015; IEEE: Piscataway, NJ, USA, 2015; pp. 532–537. [Google Scholar]

- Carter, G. 5 Ways VR Is Making the Real Estate Business Better for Everyone. Available online: https://venturebeat.com/2017/08/17/5-ways-vr-is-making-the-real-estate-business-better-for-everyone/ (accessed on 3 April 2018).

- Olson, M. Cloud Computing Trends to Watch in 2018. Available online: https://apiumhub.com/tech-blog-barcelona/cloud-computing/ (accessed on 30 March 2018).

- Columbus, L. 2017 State of Cloud Adoption and Security. Available online: https://www.forbes.com/sites/louiscolumbus/2017/04/23/2017-state-of-cloud-adoption-and-security/#32dd5f661848 (accessed on 30 March 2018).

- Technologies, W. 2017 Cloud Facts and Statistics. Available online: https://www.waterfordtechnologies.com/cloud-computing-stats-2017/ (accessed on 30 March 2018).

- WMS, A. The State of the Cloud 2017: Here Come the Enterprises! Available online: https://www.irms360.com/blog_post/state_cloud_2017_here_come_enterprises (accessed on 30 March 2018).

- Dion Alley, T.A.; Androvich, J.; Archibald, S.; Baker, A.; Bullock, D.; Fultz, N.; Heusser, S.; Keahey, R.; Krogue, K.; Menon, R.; et al. The Cloud ComputingGuide for Construction. FOCUS, 2012. Available online: http://download.microsoft.com/download/0/0/4/0040A3AC-FC39-441C-B982-D3D8007BBB4D/The-Cloud-Computing-Guide-for-Construction.pdf (accessed on 27 March 2018).

- Columbus, L. Roundup of Cloud Computing Forecasts. 2017. Available online: https://www.forbes.com/sites/louiscolumbus/2017/04/29/roundup-of-cloud-computing-forecasts-2017/#4abdf07331e8 (accessed on 30 March 2018).

- Li, X.; Li, Y.; Liu, T.; Qiu, J.; Wang, F. The method and tool of cost analysis for cloud computing. In Proceedings of the IEEE International Conference on Cloud Computing, CLOUD’09, Bangalore, India, 21–25 September 2009; IEEE: Piscataway, NJ, USA, 2009; pp. 93–100. [Google Scholar]

- Hashem, I.A.T.; Yaqoob, I.; Anuar, N.B.; Mokhtar, S.; Gani, A.; Khan, S.U. The rise of “big data” on cloud computing: Review and open research issues. Inf. Syst. 2015, 47, 98–115. [Google Scholar] [CrossRef]

- Cheng, Y.; Chen, Y.; Wei, R.; Luo, H. Development of a Construction Quality Supervision Collaboration System based on a SaaS private cloud. J. Intell. Robot. Syst. 2015, 79, 613–627. [Google Scholar] [CrossRef]

- Rohner, P.; Uhl, M.W. The Compensation Portfolio. Finance Res. Lett. 2018, in press. [Google Scholar]

- Rentlytics. Available online: https://rentlytics.com/power-of-saas-real-estate-tech/ (accessed on 30 March 2018).

- Cusumano, M. Cloud computing and SaaS as new computing platforms. Commun. ACM 2010, 53, 27–29. [Google Scholar] [CrossRef]

- Limbasan, A.; Rusu, L. Implementing SaaS solution for CRM. Inform. Econ. 2011, 15, 175. [Google Scholar]

- Chan, V. 60 SAAS Statistics That Will Change the Way You Think. Available online: https://content.digitalmediastream.co.uk/blog/60-saas-statistics-that-will-change-the-way-you-think (accessed on 10 April 2018).

- Collingwood, N.J. SaaS Company Becomes Largest Provider of Mobile Real Estate Apps in Residential Housing Sector. Available online: https://www.prnewswire.com/news-releases/saas-company-becomes-largest-provider-of-mobile-real-estate-apps-in-residential-housing-sector-262565121.html (accessed on 10 April 2018).

- Advice, T. TechnologyAdvice Buyer’s Guide to Real Estate Software. Available online: https://technologyadvice.com/real-estate-software/ (accessed on 10 April 2018).

- Wortmann, F.; Flüchter, K. Internet of things. Bus. Inf. Syst. Eng. 2015, 57, 221–224. [Google Scholar] [CrossRef]

- Yang, S.-H. Internet of things. In Wireless Sensor Networks; Springer: New York, NY, USA, 2014; pp. 247–261. [Google Scholar]

- Symantec, N. 5 Predictions on the Future of the Internet of Things. Available online: https://us.norton.com/internetsecurity-iot-5-predictions-for-the-future-of-iot.html (accessed on 4 April 2018).

- Zhilong, T.; Bowen, T.; Yu, H. Applications and Business Models of the Internet of Things Technology in the Real Estate Field. China Real Estate 2015, 18, 006. [Google Scholar]

- Dijkstra, M. Blockchain: Towards Disruption in the Real Estate Sector: An Exploration on the Impact of Blockchain Technology in the Real Estate Management Process. Master’s Thesis, Delft University of Technology, Delft, The Netherlands, 2017. [Google Scholar]

- Li, C.Z.; Hong, J.; Xue, F.; Shen, G.Q.; Xu, X.; Luo, L. SWOT analysis and Internet of Things-enabled platform for prefabrication housing production in Hong Kong. Habitat Int. 2016, 57, 74–87. [Google Scholar] [CrossRef]

- Donovan, N.; Gray, A.; Shaw, R. The Internet of Things and the Real Estate Sector. Available online: https://www.dlapiper.com/en/australia/insights/publications/2018/03/the-internet-of-things-and-the-real-estate-sector/ (accessed on 4 April 2018).

- Qu, T.; Lei, S.; Wang, Z.; Nie, D.; Chen, X.; Huang, G.Q. IoT-based real-time production logistics synchronization system under smart cloud manufacturing. Int. J. Adv. Manuf. Technol. 2016, 84, 147–164. [Google Scholar] [CrossRef]

- Bonomi, F.; Milito, R.; Natarajan, P.; Zhu, J. Fog computing: A platform for internet of things and analytics. In Big Data and Internet of Things: A Roadmap for Smart Environments; Springer: Cham, Switzerland, 2014; pp. 169–186. [Google Scholar]

- NewGenApps. 13 IoT Statistics Defining the Future of Internet of Things. Available online: https://www.newgenapps.com/blog/iot-statistics-internet-of-things-future-research-data (accessed on 10 April 2018).

- PostScapes. IoT Market Forecasts. Available online: https://www.postscapes.com/internet-of-things-market-size/ (accessed on 30 March 2018).

- Laprie, J.-C.; Arlat, J.; Beounes, C.; Kanoun, K. Definition and analysis of hardware-and software-fault-tolerant architectures. Computer 1990, 23, 39–51. [Google Scholar] [CrossRef]

- Edith Burke, M.; O’Callaghan, S.; Quigley, M. The business of digital storytelling: Augmenting information systems with QR codes. J. Syst. Inf. Technol. 2013, 15, 347–367. [Google Scholar] [CrossRef]

- Du, J.; Zou, Z.; Shi, Y.; Zhao, D. Zero latency: Real-time synchronization of BIM data in virtual reality for collaborative decision-making. Autom. Constr. 2018, 85, 51–64. [Google Scholar] [CrossRef]

- Wu, W.; Yang, H.; Chew, D.A.; Yang, S.-H.; Gibb, A.G.; Li, Q. Towards an autonomous real-time tracking system of near-miss accidents on construction sites. Autom. Constr. 2010, 19, 134–141. [Google Scholar] [CrossRef]

- Takin, M.; Peng, J.; Sepasgozar, S.; Ebrahimi, H. A Framework for Using Advanced Visualization Tools for Residential Property Management. In Proceedings of the International Symposium on Automation and Robotics in Construction, ISARC, Taipei, Taiwan, 28 June–1 July 2017; Vilnius Gediminas Technical University, Department of Construction Economics & Property: Vilnius, Lithuania, 2017. [Google Scholar]

- Kuzma, J.; O’Sullivan, S.; Philippe, T.; Koehler, J.; Coronel, R. Commercialization Strategy in Managing Online Presence in the Unmanned Aerial Vehicle Industry. Int. J. Bus. Strategy 2017, 17, 59–68. [Google Scholar] [CrossRef]

- Luppicini, R.; So, A. A technoethical review of commercial drone use in the context of governance, ethics, and privacy. Technol. Soc. 2016, 46, 109–119. [Google Scholar] [CrossRef]

- Newell, C. The use of ‘drones’ in marketing a property for sale. REIQ J. 2017, 2017, 35–37. [Google Scholar]

- Sepasgozar, S.M.; Davis, S.; Loosemore, M.; Bernold, L. An investigation of modern building equipment technology adoption in the Australian construction industry. Eng. Constr. Arch. Manag. 2018. [Google Scholar] [CrossRef]

- Baker, A. Provocation: Unmanned Aerial Realtors. Cult. Mach. 2015, 16, 1–5. [Google Scholar]

- Rao, B.; Gopi, A.G.; Maione, R. The societal impact of commercial drones. Technol. Soc. 2016, 45, 83–90. [Google Scholar] [CrossRef]

- Kuzma, J.; Dobson, K.; Robinson, A.; Williams, N. Drones in Business: Can your Organisation Capitalise on this New Technology? Int. J. Bus. Strategy 2016, 17, 59–68. [Google Scholar] [CrossRef]

- McNeil, B.; Snow, C. The truth about drones in mapping and surveying. Skylogic Res. 2016, 200, 1–6. [Google Scholar]

- Mohan, H. Innovation is the key order in Start Ups–Recent Paradigms in Marketing Vertical. Innovation 2015, 2, 24–30. [Google Scholar]

- SoldbyAir. Real Estate Drone Statistics. Available online: https://www.soldbyair.com/real-estate-drone-study (accessed on 11 April 2018).

- Young, D. Drones for Real Estate Marketing: Are They Worth It? Available online: http://rismedia.com/2016/12/20/drones-real-estate-marketing/ (accessed on 11 April 2018).

- Grand View Research. Scanning Market Analysis by Product (Laser Scanner, Structured Light Scanner, Optical Scanner), by Range (Short Range, Medium Range, Long Range), by Application, and Segment Forecasts, 2014–2025; Grand View Research: San Francisco, CA, USA, 2015. [Google Scholar]

- Sepasgozar, S.; Forsythe, P.; Shirowzhan, S. Scanners and Photography: A combined framework. In Australian Universities Building Education Association Annual Conference; Central Queensland University: Brisbane, Australia, 2016. [Google Scholar]

- Sepasgozar, S.M.; Shirowzhan, S. Challenges and Opportunities for Implementation of Laser Scanners in Building Construction. In Proceedings of the International Symposium on Automation and Robotics in Construction, ISARC, Auburn, AL, USA, 18–21 July 2016; Vilnius Gediminas Technical University, Department of Construction Economics & Property: Vilnius, Lithuania, 2016; p. 1. [Google Scholar]

- Remondino, F. Heritage recording and 3D modeling with photogrammetry and 3D scanning. Remote. Sens. 2011, 3, 1104–1138. [Google Scholar] [CrossRef]

- Mahdjoubi, L.; Moobela, C.; Laing, R. Providing real-estate services through the integration of 3D laser scanning and building information modelling. Comput. Ind. 2013, 64, 1272–1281. [Google Scholar] [CrossRef]

- Fagandini, R.; Federici, B.; Ferrando, I.; Gagliolo, S.; Pagliari, D.; Passoni, D.; Pinto, L.; Rossi, L.; Sguerso, D. Evaluation of the Laser Response of Leica Nova MultiStation MS60 for 3D Modelling and Structural Monitoring. In Proceedings of the International Conference on Computational Science and Its Applications, Trieste, Italy, 3–6 July 2017; Springer: Cham, Switzerland, 2017; pp. 93–104. [Google Scholar]

- Sepasgozar, S.M.; Lim, S.; Shirowzhan, S. Implementation of Rapid As-built Building Information Modeling Using Mobile LiDAR. In Proceedings of the Construction Research Congress 2014: Construction in a Global Network, Atlanta, GA, USA, 19–21 May 2014; pp. 209–218. [Google Scholar]

- Arayici, Y. An approach for real world data modelling with the 3D terrestrial laser scanner for built environment. Autom. Constr. 2007, 16, 816–829. [Google Scholar] [CrossRef]

- Skibniewski, M.J. Information technology applications in construction safety assurance. J. Civ. Eng. Manag. 2014, 20, 778–794. [Google Scholar] [CrossRef]

- Shirowzhan, S.; Sepasgozar, S.; Zaini, I.; Wang, C. An Integrated GIS and Wi-Fi Based Locating System for Improving Construction Labor Communications. In Proceedings of the International Symposium on Automation and Robotics in Construction, ISARC, Taipei, Taiwan, 28 June–1 July 2017; Vilnius Gediminas Technical University, Department of Construction Economics & Property: Vilnius, Lithuania, 2017. [Google Scholar]

- Rosalinda, R. Wearable Tech for Real Estate Set to Reshape the Industry. Available online: http://www.jamesdearsley.co.uk/wearable-tech-for-real-estate/ (accessed on 3 April 2018).

- Wheatley, M. 4 Pieces of Wearable Tech for ‘Smart’ Real Estate Agents. Available online: http://realtybiznews.com/4-pieces-of-wearable-tech-for-smart-real-estate-agents/98727385/ (accessed on 3 April 2018).

- Sepasgozar, S.; Lim, S.; Shirowzhan, S.; Kim, Y. Implementation of as-built information modelling using mobile and terrestrial lidar systems. In Proceedings of the International Symposium on Automation and Robotics in Construction, ISARC, Sydney, Australia, 9–11 July 2014; Vilnius Gediminas Technical University, Department of Construction Economics & Property: Vilnius, Lithuania, 2014; p. 1. [Google Scholar]

- Li, R.Y.M.; Ng, D.P.L. Wearable Robotics, Industrial Robots and Construction Worker’s Safety and Health. In International Conference on Applied Human Factors and Ergonomics; Springer: Cham, Switzerland, 2017; pp. 31–36. [Google Scholar]

- Ju, A. Functionality in Wearable Tech: Device, as Jewelry, as Body Mediator. In Proceedings of the TEI’16: Tenth International Conference on Tangible, Embedded, and Embodied Interaction, Eindhoven, The Netherlands, 14–17 February 2016; ACM: New York, NY, USA, 2016; pp. 641–646. [Google Scholar]

- Smith, N. Wearable Tech: Smart Watches. Eng. Technol. 2015, 10, 20–21. [Google Scholar] [CrossRef]

- Kim, K.S.; Mansour, A.-M.; Lundell, J.W. Lessons learned from designing a displayless consumer wearable tech. In Proceedings of the 18th International Conference on Human-Computer Interaction with Mobile Devices and Services Adjunct, Florence, Italy, 6–9 September 2016; ACM: New York, NY, USA, 2016; pp. 585–590. [Google Scholar]

- Boga, S.R.C.; Kansagara, B.; Kannan, R. Integration of Augmented Reality and Virtual Reality in Building Information Modeling: The Next Frontier in Civil Engineering Education. In Mobile Technologies and Augmented Reality in Open Education; Kurubacak, G., Altinpulluk, H., Eds.; IGI Global: Hershey, PA, USA, 2018; pp. 1037–1066. Available online: https://www.igi-global.com/chapter/integration-of-augmented-reality-and-virtual-reality-in-building-information-modeling/178245 (accessed on 3 September 2018).

- NewsgenApps. 6 VR and AR Statistics: Shaping the Future of Augmented Reality with Data. Available online: https://www.newgenapps.com/blog/6-vr-and-ar-statistics-shaping-the-future-of-augmented-reality-with-data (accessed on 3 April 2018).

- Li, M.; Bao, Z.; Sellis, T.; Yan, S. Visualization-aided exploration of the real estate data. In Australasian Database Conference; Springer: Cham, Switzerland, 2016; pp. 435–439. [Google Scholar]

- Deacon, H. Smartwatches and Smart Bands Dominate Fast-Growing Wearables Market. Available online: https://www.ccsinsight.com/press/company-news/1944-smartwatches-and-smart-bands-dominate-fast-growing-wearables-market (accessed on 11 April 2018).

- Danova, T. The Wearables Report: Growth Trends, Consumer Attitudes, and Why Smartwatches Will Dominate. Available online: https://www.businessinsider.com.au/the-wearable-computing-market-report-bii-2015-7 (accessed on 11 April 2018).

- Montreal360. 7 Stats That Will Make You Rethink Virtual Home Tours. Available online: https://www.montreal360virtualtour.com/7-stats-will-make-rethink-virtual-home-tours/ (accessed on 11 April 2018).

- Council, F.R.E. Eight Ways Virtual and Augmented Reality Are Changing the Real Estate Industry. Available online: https://www.forbes.com/sites/forbesrealestatecouncil/2017/07/14/eight-ways-virtual-and-augmented-reality-are-changing-the-real-estate-industry/#5b066dc365a3 (accessed on 3 April 2018).

- Glebb, B. Five Innovative Ways You Can Use Virtual Reality in the Real Estate Business. Available online: https://rubygarage.org/blog/virtual-reality-in-real-estate (accessed on 3 April 2018).

- Brenner, A.J. Virtual Reality: The Game Changer for Residential Real Estate Staging through Increased Presence. CMC Senior Theses. 2017. Available online: https://scholarship.claremont.edu/cmc_theses/1471 (accessed on 27 March 2018).

- Sonje, R.D.; Lokhande, R.R.; Joshi, V.V.; Student, B. Virtual Reality for Real Estates. Int. J. Eng. Sci. 2018, 16197. [Google Scholar]

- Paredes, A.M. An Examination of Mobile Augmented Reality Apps for the Commercial Real Estate Industry in Mexico City. Master’s Thesis, London School of Business and Finance, London, UK, 2014. [Google Scholar]

- National Association of Realtors. Real Estate in a Digital Age2017 Report; National Association of Realtors: Chicago, IL, USA, 2017. [Google Scholar]

- Black, W. How Long Is the Average Home Buyer Search? Available online: https://www.zillow.com/advice-thread/How-long-is-the-average-home-buyer-search/455342/ (accessed on 22 October 2017).

- Davies, J. How Long Does It Take to Find A House To Buy? Available online: https://www.canstar.com.au/home-loans/how-long-does-it-take-to-find-a-house-to-buy/ (accessed on 22 October 2017).

- Batten, G. Real Estate Online Statistics & Demographics—Portals. Available online: https://www.business2.com.au/2010/09/real-estate-online-statistics-demographics-%E2%80%93-portals/ (accessed on 26 October 2017).

- Stewart, A. 28 Eye-Popping Real Estate Marketing Statistics. Available online: https://www.paveya.com/28-eye-popping-real-estate-marketing-statistics/ (accessed on 26 October 2016).

- Rogers, D. Becoming a super-rich foreign real estate investor: Globalising real estate data, publications and events. In Cities and the Super-Rich; Springer: New York, NY, USA, 2017; pp. 85–104. [Google Scholar]

- Consignado, M.L.L.S.; Velasco, M.L.A.; Sanvictores, A.P.A.; Jain, A.M.; Balahadia, F.F. Haybol: An Android-Based Apartment Locator Application. Int. J. Comput. Sci. Res. 2017, 1, 1–9. [Google Scholar] [CrossRef]

- Rastogi, U.; Tiwari, R.; Suman, S. StereoCam3D (An Android App. That Lets You Capture Realtime 3D Pics And Videos). Int. J. Sci. Res. Comput. Sci. Eng. Inf. Technol. 2017, 2, 837–840. [Google Scholar]

- Krotov, V.; Junglas, I.; Steel, D. The mobile agility framework: An exploratory study of mobile technology enhancing organizational agility. J. Theor. Appl. Electron. Commer. Res. 2015, 10, 1–7. [Google Scholar] [CrossRef]

- Thompson, B. Social Media in the Built Environment. In Sustainable Futures in the Built Environment to 2050: A Foresight Approach to Construction and Development; Wiley-Blackwell: Milton, QLD, Australia, 2018; p. 223. [Google Scholar]

- Lu, B.; Fan, W.; Zhou, M. Social presence, trust, and social commerce purchase intention: An empirical research. Comput. Hum. Behav. 2016, 56, 225–237. [Google Scholar] [CrossRef]

- Shelton, T.; Poorthuis, A.; Zook, M. Social media and the city: Rethinking urban socio-spatial inequality using user-generated geographic information. Landsc. Urban Plan. 2015, 142, 198–211. [Google Scholar] [CrossRef]

- Zamani, M.; Schwartz, H.A. Using Twitter Language to Predict the Real Estate Market. In Proceedings of the 15th Conference of the European Chapter of the Association for Computational Linguistics, Valencia, Spain, 3–7 April 2017; pp. 28–33. [Google Scholar]

- Rauniar, R.; Rawski, G.; Yang, J.; Johnson, B. Technology acceptance model (TAM) and social media usage: An empirical study on Facebook. J. Enterp. Inf. Manag. 2014, 27, 6–30. [Google Scholar] [CrossRef]

- Wang, S.; Feeney, M.K. Determinants of information and communication technology adoption in municipalities. Am. Rev. Public Adm. 2016, 46, 292–313. [Google Scholar] [CrossRef]

- Song, J.; Sawang, S.; Drennan, J.; Andrews, L. Same but different? Mobile technology adoption in China. Inf. Technol. People 2015, 28, 107–132. [Google Scholar] [CrossRef]

- Picot, S.H.A. Are Users All the Same?–A Comparative International Analysis of Digital Technology Adoption. In Homo Connectus: Einblicke in die Post-Solo-Ära des Kunden; Springer Gabler: Wiesbaden, Germany, 2018; p. 103. [Google Scholar]

- Zhang, C.; Dhaliwal, J. An investigation of resource-based and institutional theoretic factors in technology adoption for operations and supply chain management. Int. J. Prod. Econ. 2009, 120, 252–269. [Google Scholar] [CrossRef]

- Maertens, A.; Barrett, C.B. Measuring social networks’ effects on agricultural technology adoption. Am. J. Agric. Econ. 2012, 95, 353–359. [Google Scholar] [CrossRef]

- Nguyen, T.H.; Newby, M.; Macaulay, M.J. Information technology adoption in small business: Confirmation of a proposed framework. J. Small Bus. Manag. 2015, 53, 207–227. [Google Scholar] [CrossRef]

- Sepasgozar, S.M.; Loosemore, M.; Davis, S.R. Conceptualising information and equipment technology adoption in construction: A critical review of existing research. Eng. Constr. Arch. Manag. 2016, 23, 158–176. [Google Scholar] [CrossRef]

- Benbasat, I.; Barki, H. Quo vadis TAM? J. Assoc. Inf. Syst. 2007, 8, 7. [Google Scholar] [CrossRef]

- Jasperson, J.S.; Carter, P.E.; Zmud, R.W. A comprehensive conceptualization of post-adoptive behaviors associated with information technology enabled work systems. MIS Q. 2005, 29, 525–557. [Google Scholar] [CrossRef]

- Mun, Y.Y.; Hwang, Y. Predicting the use of web-based information systems: Self-efficacy, enjoyment, learning goal orientation, and the technology acceptance model. Int. J. Hum. Comput. Stud. 2003, 59, 431–449. [Google Scholar]

- Lu, J.; Yao, J.E.; Yu, C.-S. Personal innovativeness, social influences and adoption of wireless Internet services via mobile technology. J. Strat. Inf. Syst. 2005, 14, 245–268. [Google Scholar] [CrossRef]

- Ahn, T.; Ryu, S.; Han, I. The impact of Web quality and playfulness on user acceptance of online retailing. Inf. Manag. 2007, 44, 263–275. [Google Scholar] [CrossRef]

- Hornbæk, K.; Hertzum, M. Technology acceptance and user experience: A review of the experiential component in HCI. ACM Trans. Comput. Hum. Interact. 2017, 24, 33. [Google Scholar] [CrossRef]

- Venkatesh, V. Determinants of perceived ease of use: Integrating control, intrinsic motivation, and emotion into the technology acceptance model. Inf. Syst. Res. 2000, 11, 342–365. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Pillar | US | Britain | Australia | |||

|---|---|---|---|---|---|---|

| Rank | Value | Rank | Value | Rank | Value | |

| Network readiness | 5 | 5.8 | 8 | 5.7 | 18 | 5.5 |

| Availability of latest technologies | 2 | 6.5 | 5 | 6.5 | 24 | 5.9 |

| Individuals using the internet | 13 | 87.4% | 8 | 91.6% | 19 | 84.6% |

| Firm-level technology absorption | 3 | 6.1 | 14 | 5.7 | 22 | 5.6 |

| Capacity for innovation based on adoption capabilities | 2 | 5.9 | 10 | 5.4 | 25 | 4.8 |

| Business-to-consumer successful transfer over the internet use | 2 | 6.3 | 1 | 6.4 | 25 | 5.5 |

| Government success in internet and communication technologies (ICT) promotion | 25 | 4.8 | 15 | 4.9 | 55 | 4.2 |

| Key-Term | Explanation |

|---|---|

| Smart real estate (SRE) | This is an amalgam of user-centred, sustainable and innovative technologies for managing real estate resources efficiently in an urban area, whereby the key information is made available to consumers, managers and agents. The technologies and systems must be sustainable, user-centred and innovative, thereby disrupting traditional practices [28,34]. |

| Smart real estate management (SREM) | Just like its industrial doppelganger, the smart city, SREM is the management of the SRE process, including data collection and its processing and dissemination through computers and networked technologies to promote the overall life quality of consumers using real estate services. It has specific measures about privacy and data security [23,28,35]. |

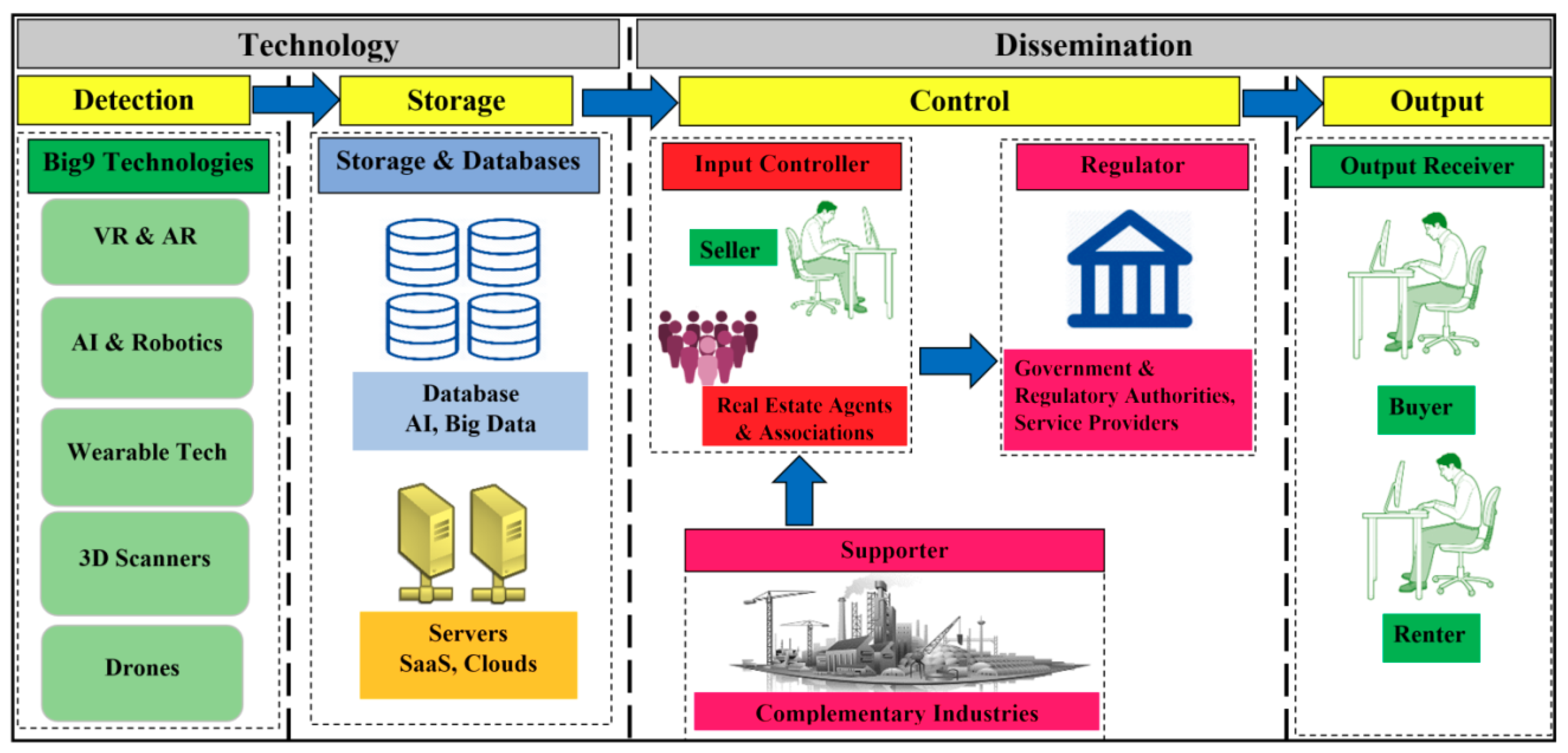

| Big9 technologies | These nine disruptive technologies are the focus of this study. They include big data, virtual and augmented realities (VR and AR), the internet of things (IoT), clouds, software as a service (SaaS), drones, 3D scanning, AI and wearable techs. |

| Technology adoption model (TAM) | This is an information systems theory used for modelling the use and acceptance of technologies by end users. It starts with the perceived ease of use and usefulness to a user of technology that might effect behavioural change as they start to use the technology, thus providing a holistic mechanism [36,37]. |

| Consumers | This refers to buyers, renters, end users or sellers of real estate. These are the primary beneficiaries of the transactions because at the end of the process they are the ones with the resources to keep the process alive. They are therefore at the centre of the system [38,39]. |

| Agents and associations (AA) | These stakeholders provide services to the consumer in exchange for revenue. This category includes the real estate managers, developers, private investors and other services providing bodies. Associations exist to guide agents and ensure their compliance with codes of ethics and local, state and federal laws [40,41]. |

| Government and regulatory authorities (GRA) | Governments aim to protect citizens in exchange for tax revenues. Regulatory authorities exist at local, state and/or federal levels to ensure compliance and to formulate laws for the real estate industry [42,43]. |

| Complementary industries (CI) | These industries aim to facilitate consumers, agents and associations in the buying or selling of property. They receive revenues in exchange for their services. They include banks, law firms, inspectors, contractors, lenders and others [44,45] |

| Search Engine | Strings and Filters | Articles Retrieved | Duplicates |

|---|---|---|---|

| Google Scholar, ASCE Library, Taylor & Francis, Emerald Insight, Science Direct. | TOPIC: Real Estate Tech OR Real Estate Technology OR Disruptive Technologies in Real Estate OR Smart Real Estate OR Real Estate Technology Acceptance OR Real Estate Technology Adoption Information dissemination OR Web based dissemination OR Apps for dissemination Information retrieval 1 and 2 not 3 English Language Only Limit 2010 and onwards Editorial or erratum or letter or note or comment Limit 6 not 7 Remove Duplicates | 6542 8760 1780 13522 11800 1840 560 1300 52 | 462 786 |

| Web of Science | TOPIC: Real Estate Tech OR Real Estate Technology OR Disruptive Technologies in Real Estate OR Smart Real Estate OR Real Estate Technology Acceptance OR Real Estate Technology Adoption TOPIC: Information dissemination OR Web based dissemination OR Apps for dissemination LANGUAGE: (English) DOCUMENT TYPES: Article OR Abstract OR Book OR Book Chapter OR Meeting Abstract OR Proceedings Paper Indexes = SCI-EXPANDED Timespan = 2010–2018 TS = “information retrieval” NOT 4 and 6 NOT Duplicates | 5896 7523 11853 1256 1634 2864 1120 47 | 378 695 |

| Scopus | TITLE-ABS-KEY (Real Estate Tech OR Real Estate Technology OR Disruptive Technologies in Real Estate OR Smart Real Estate OR Real Estate Technology Acceptance OR Real Estate Technology Adoption TITLE-ABS-KEY (Information dissemination OR Web based dissemination OR Apps for dissemination) TITLE-ABS-KEY (Information retrieval) PUBYEAR AFT 2010 AND LANGUAGE (English) 4 not 3 DOCTYPE Limit 5 and not 6 Not Duplicates | 5761 6894 1923 2514 591 184 407 40 | 171 196 |

| Grand Total | 139 | ||

| Type | Sub Type | Data Mining | Networking Tools | Data Collection | Dissemination | General | Multi Tech | Total | Share (%) | Portion (%) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Big Data | AI and Robotics | Cloud | SaaS | IoT | Drones | 3D Scanning | Wearable Tech | VR and AR | ||||||||

| Journal/Conference papers | Technology-based | 6 * | 5 | 5 | 2 | 3 * | 5 | 7 | 3 | 5 | 13 | 36 | 2 * | 90 | 42 | 65 |

| Case studies | 2 | 2 | 3 * | 1 | 2 | 1 | 2 | 1 | 1 | 11 | 11 | 1 * | 37 | 17 | ||

| Review papers | 2 | 1 | 1 | 1 * | 1 | 2 | 4 | 1 * | 12 | 5 | ||||||

| Online Sources | Reports | 1 | 1 | 3 | 12 | 17 | 7 | 29 | ||||||||

| Webpages | 2 | 2 | 5 | 4 | 4 | 2 | 2 | 8 | 5 | 2 | 9 | 45 | 21 | |||

| Others | Theses | 1 | 1 | 1 * | 3 | 1 * | 6 | 2 | 5 | |||||||

| Book chapters | 1 | 1 | 2 | 1 | 1 | 6 | 2 | |||||||||

| Total | 13 | 10 | 17 | 7 | 11 | 9 | 13 | 12 | 13 | 32 | 76 | 5 * | 213 | |||

| Opportunities | Potential Losses | Exploitation Level | Domain | Ref |

|---|---|---|---|---|

| By 2020, 50% of software queries will be over search features, natural language processing, or voice recognition. | Three out of 5 leaders fear that inability to adapt to big data will lead to obsolescence. | Six million job opportunities. Only 37% success so far. Wal-Mart customers’ transactions provide them with about 2.5 petabytes of data a day. | Business intelligence | [81] |

| The digital universe of data to 44 trillion gigabytes (2020). Fifty billion smart devices were connected globally in 5 years A 10% increase in data accessibility results in more than $65 million additional net income. | At present, less than 0.5% of all data is ever analysed. | In 2017, nearly 80% of photos were taken on smartphones. 73% of organisations had already invested in big data in 2016. | Big data revolution | [82] |

| Opportunities | Potential Losses | Exploitation Level | Domain | Ref |

|---|---|---|---|---|

| Buyer-seller customisations. Predictive analytics. 68% automation for agents and auctioneers. Link 83% people to properties. | PurpleBricks technology bringing commissions down. | Manage multiple properties: 200,000 in USA. Rex bot: answer queries and charges 2% commission only. ‘Rita’: AI digital assistant. | Future of Real Estate | [89] |

| Agenda for next year: 31% of enterprises. 72% business advantage. 61% innovation. Can manage 85% of customer interactions. Can manage 40% of mobile interactions. Can decrease labour productivity by 40%. | AI could jeopardise between 40–75 million jobs worldwide by 2025. | AI is being used by 15% of enterprises at present. 77% of consumers use an AI-powered service globally. Only half of the largest companies with at least 100,000 employees have an AI strategy. | AI as emerging technology | [90] |

| Opportunities | Potential Losses | Exploitation Level | Domain | Ref |

|---|---|---|---|---|

| 73% of companies plan to install software data centres in two years. Private cloud use shows 77% growth, hybrid 71% and enterprise as 31%. In future, about 28% of an organisation’s budget will be for clouds. | 49% of companies are delaying it due to a lack of skills. | Growth from 19% to 57% in the past three years. 46% of organisations are integrating cloud APIs for databases, messenger systems and storage systems. | Cloud adoption and security. | [104,105] |

| 25% annual adoption increase 10–30% company growth potential. 41% of businesses plan to invest in clouds. | 32% of companies accept they lack skills for it. 52% of companies lack adoption strategies. | 30% of Microsoft revenue expected from clouds in 2018. Amazon uses 31% clouds at present. | Clouds and information technology (IT). | [106] |

| Software-based service to grow by 20% to $46.3bn. 60–70% of all software will be cloud based by 2020. | 79% losses in competition by 2011. | 22% growth rate in 2017. Spending increase from 4.5 times in 2009 to 6 times through 2020. | Cloud forecasts for business applications. | [107,108,109] |

| Opportunities | Potential Losses | Exploitation Level | Domain | Ref |

|---|---|---|---|---|

| Offer 5 times higher returns. | 3.2% loss of revenue for fast-growing SaaS-equipped companies with $255 MRR. Median SaaS firms lose about 10% at rate of 0.83% per month. | 48% median revenue growth in 2016. 3.9% growth ratio for global SaaS companies. | SaaS oerformance. | [117] |

| Generate 33% per cent more home views per user session. | - | Smarter Agent Mobile registered more than 4,000,000 unique app downloads in 2014. More than 1 billion properties viewed. | Mobile real estate. | [118] |

| Faster follow-up and management abilities of more than 5000 contacts simultaneously. | - | 87% of agents with income over $100,000 use SaaS more. | Marketing. | [119] |

| Opportunities | Potential Losses | Exploitation Level | Domain | Ref |

|---|---|---|---|---|

| The number of IoT devices will increase by 31% to 82.5 million by 2020. By 2019, 1.9 billion smart home devices are expected to be shipped. 24.75 billion smart clothes are expected to be purchased by 2021. | 87% of consumers are unaware of the “IoT”. | 28.3 million units of IoT devices used in 2016. Samsung bought SmartThings® to launch itself into smart homes 968,000 smart clothes sold in 2015. | IoT potential | [129] |

| 32.4% growth is predicted between 2016 and 2022. $1.3 trillion to be invested in 2019 with a compound annual growth rate of 17%. | $591.7 billion invested in 2014. 20 billion connected devices counted in 2013. | IoT market forecasts | [130] |

| Opportunities | Potential Losses | Exploitation Level | Domain | Ref |

|---|---|---|---|---|

| 83% of home sellers prefer working with an agent who uses drones. Global real estate drone demands are expected to reach $20.5 billion over 2017–2025. | - | 3.5x greater customer attraction among agents using drones than their counterparts. | Drones future. | [145] |

| Homes with aerial images sell 68% faster than homes with standard images. | - | Only 9% of agents create listing videos using drones. 403% increase in traffic was noted for an Australian real estate firm with video-based listings. | Real estate marketing. | [146] |

| Structured light scanners are forecast to grow at a CAGR of over 10.4%. Architectural and engineering usage of 3D scanners will increase by 22% by 2025. | - | The 3D laser scanners valued at $3.32 billion generated revenue of about $US2.26 billion in 2015. Short-range 3D scanners had a market share of over 67.9% in 2015. | Scanners’ market size and trends. | [147] |

| Opportunities | Potential Losses | Exploitation Level | Domain | Ref |

|---|---|---|---|---|

| Production set to exceed 250 million smart wearables, or 14x more than in 2013. 14 times more sales in 2018 expected as compared with 2013. | - | 129% increase from 2013. 40% of all wearables are used in North America. | Smart watches and bands. | [167] |

| Expected growth of 35% by 2020. 70% of wearable shipments will be smart watches. | - | Apple Watch accounts for 40% count and 48% share of the smart watch market in 2017. | Wearables future. | [168] |

| Real estate listings with virtual home tours garner 87% more views. Virtual tours keep people looking at a website 5 to 10 times longer. | 54% of buyers will not look at a property unless it has a virtual tour. | 6 million people take virtual tours every day. | Virtual tours. | [169] |

| VR penetration will reach 25.5% of households by 2021. VR/AR software revenues to be $2.6 billion by 2025. | - | In 2016, 150,000 shipments of AR glasses were made. | VR/AR future and market. | [166] |

| Criteria | Definition | Factors |

|---|---|---|

| Information quality. | Reliable and consistent information that inclines a user to use the service [196]. | Familiar technology, information novelty, 3D models, accurate information, updated information. |

| Systems quality. | Efficient, ethical and smooth systems for delivering and disseminating information [197]. | Page location, loading speed, loading info structure, website evaluation, website design. |

| Self-efficacy. | The completeness of a platform in terms of more features, more options and filters [198]. | Content richness, search filters, sorting, maps. |

| Service quality. | Fast, efficient, reliable and responsive services made available to the end user [199]. | Hyperlinks, customisation, response time, consistent graphics |

| Playfulness and usability. | Offering more interactivity, immersion and gaming attributes to keep the user more involved and enhance use of the platform by attracting more customers [200]. | Easy return, navigation tools, finding information, learning website. |

| Perceived enjoyment. | The feeling of ease and services at finger tips including neighbourhood aspects for a better lifestyle [201]. | Data analytics, crime rates, neighbourhood insights, distances to parks, virtual tours. |

| What | Who | How | ||

|---|---|---|---|---|

| Tech | Stakeholders Affected Directly | Needs Addressed Directly | Primary Dissemination Mechanism | Resources Used |

| Big data | AA | Business, profit, networking | Websites, social media and gadgets to facilitate buy, rent or sell | Land resources, realties, buyer’s requirement, owner’s info, buyer’s demands, transaction records, page views |

| Consumers | Market awareness, Understanding process Features and requirements | |||

| GRA | Ethics, regulations | |||

| CI | Referrals | |||

| Cloud | AA | Business, profit, networking, referrals, reputation | Websites, apps, gadgets and social media to facilitate buy, rent or sell | Internet connected devices, shared storage, Recent searches, Stakeholder preferences, High-speed internet, Remote access servers |

| Consumer | Buy or sell, price, stakeholder co-ordination, online searching and filter | |||

| CI | Networking, profit, referrals | |||

| GRA | Ethics, regulations | |||

| SaaS | AA | Business, profit, networking, referrals, reputation | Websites, apps, gadgets and social media to facilitate buy, rent or sell | Computer software, High speed internet, remote access servers, shared storage |

| CI | Networking, profit, referrals | |||

| IoT | AA | Business, profit, networking | Websites and gadgets to facilitate sales | Telemetry, sensors, local networks, remote access servers, consumer habits |

| Consumer | Online searching and filters, Understanding process, market awareness | |||

| CI | Networking | |||

| GRA | Ethics, public safety, regulations | |||

| Drones | AA | Business, profit, ethics | Websites and gadgets to facilitate buy, rent or sell | UAVs, flight routes, wi-fi or bluetooth connectivity |

| Consumer | Neighborhood preference, features and requirements, buy/sell | |||

| CI | Profit | |||

| GRA | Ethics, public safety, regulations | |||

| 3D scanning | AA | Business | Gadgets to facilitate buy, rent or sell | Lasers, building drawings, training |

| CI | Profit | |||

| GRA | Ethics, public safety, regulations | |||

| Wearable tech | AA | Business | Gadgets and apps to facilitate buy, rent or sell | Human resources, Bluetooth/Wi-Fi connectivity, smart processors |

| CI | Profit, referrals | |||

| GRA | Public safety, regulations | |||

| VR & AR | AA | Business | Gadgets, websites and apps to facilitate buy, rent or sell | VR AR gadgets, Bluetooth or Wi-Fi connectivity, high speed internet, building drawings or plans |

| CI | Profit, referrals | |||

| Consumer | Neighborhood preference, features and requirements, Buy or sell, online searching and filters, price | |||

| GRA | Regulations | |||

| AI and robotics | AA | Business, profit | Websites, apps and gadgets to facilitate buy, rent or sell | Speech recognition, search history, page views, buyer’s demands and info, sensors |

| Consumer | Market awareness, features and requirements | |||

| GRA | Ethics, regulations | |||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ullah, F.; Sepasgozar, S.M.E.; Wang, C. A Systematic Review of Smart Real Estate Technology: Drivers of, and Barriers to, the Use of Digital Disruptive Technologies and Online Platforms. Sustainability 2018, 10, 3142. https://doi.org/10.3390/su10093142

Ullah F, Sepasgozar SME, Wang C. A Systematic Review of Smart Real Estate Technology: Drivers of, and Barriers to, the Use of Digital Disruptive Technologies and Online Platforms. Sustainability. 2018; 10(9):3142. https://doi.org/10.3390/su10093142

Chicago/Turabian StyleUllah, Fahim, Samad M. E. Sepasgozar, and Changxin Wang. 2018. "A Systematic Review of Smart Real Estate Technology: Drivers of, and Barriers to, the Use of Digital Disruptive Technologies and Online Platforms" Sustainability 10, no. 9: 3142. https://doi.org/10.3390/su10093142

APA StyleUllah, F., Sepasgozar, S. M. E., & Wang, C. (2018). A Systematic Review of Smart Real Estate Technology: Drivers of, and Barriers to, the Use of Digital Disruptive Technologies and Online Platforms. Sustainability, 10(9), 3142. https://doi.org/10.3390/su10093142