Exploring Twitter for CSR Disclosure: Influence of CEO and Firm Characteristics in Latin American Companies

Abstract

1. Introduction

2. Literature Review and Exposition of Hypotheses

2.1. Legitimacy Theory

2.2. Upper Echelons Theory

2.3. Twitter as an Innovatory Medium of Communication

3. Study Design

3.1. Sample

3.2. Study Method

3.3. The Disclosure Index

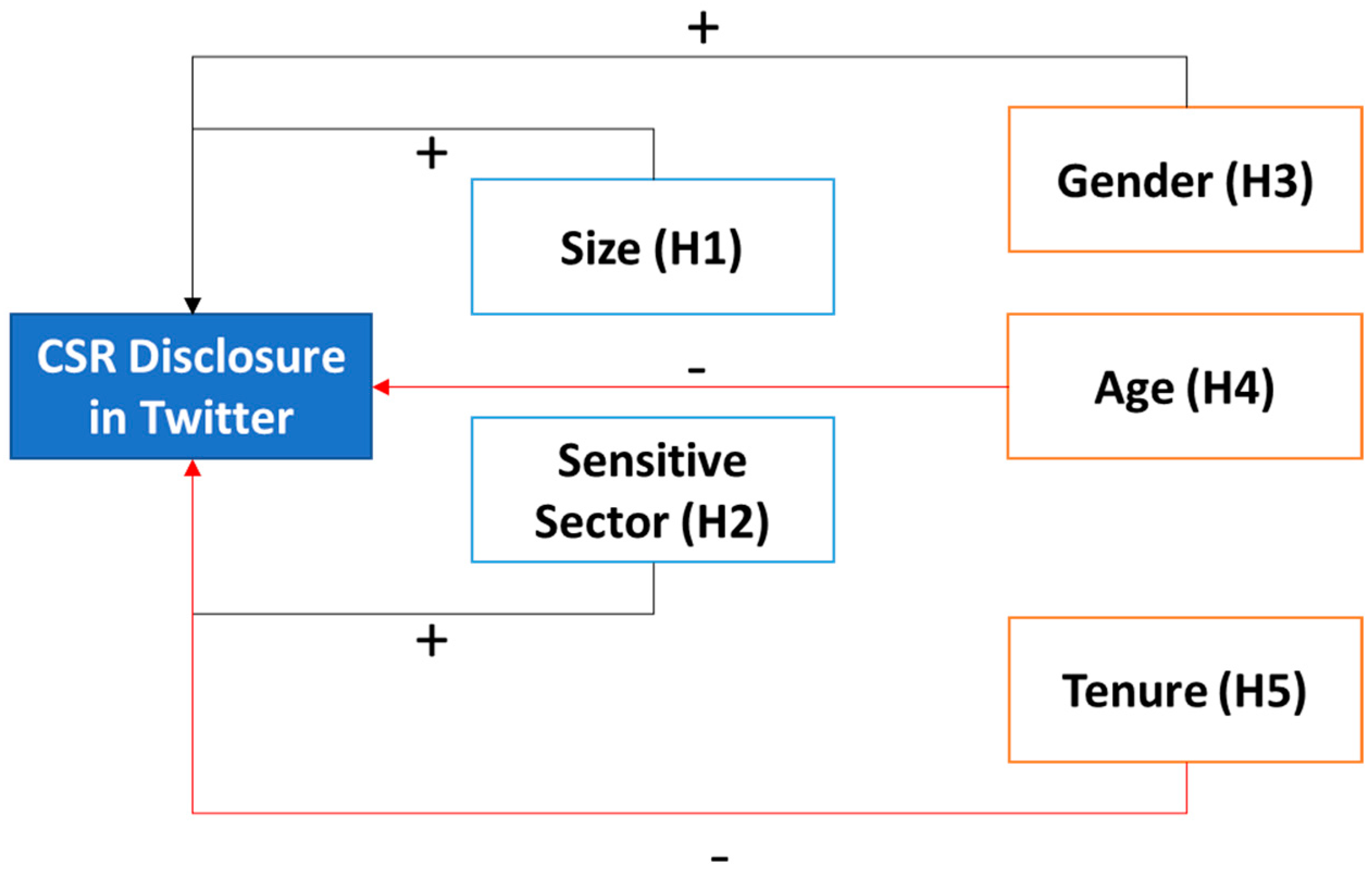

3.4. Regression Model

- Size

- = Company size, measured as the natural log of its assets in 2016

- Sens

- = Sensitivity, scored 1 if the company operates in an environmentally sensitive business sector (Mining, Oil, Industrial, Cements and Energy, Gas and Water) and 0 otherwise.

- Gen

- = Gender, scored 1 if the CEO is female and 0 otherwise.

- Age

- = Age of the CEO (years).

- Tenure

- = Number of years the CEO has held the position.

- CEODuality

- = Scored 1 if the CEO is also chair of the board, and 0 otherwise

- CSRComm

- = Scored 1 if there is a CSR committee within the board

- Adherence

- = Level of adherence of the 2016 CSR report to the GRI standards (1 if Undeclared, 2 if Core and 3 if Comprehensive)

- ε

- = Error term

4. Results

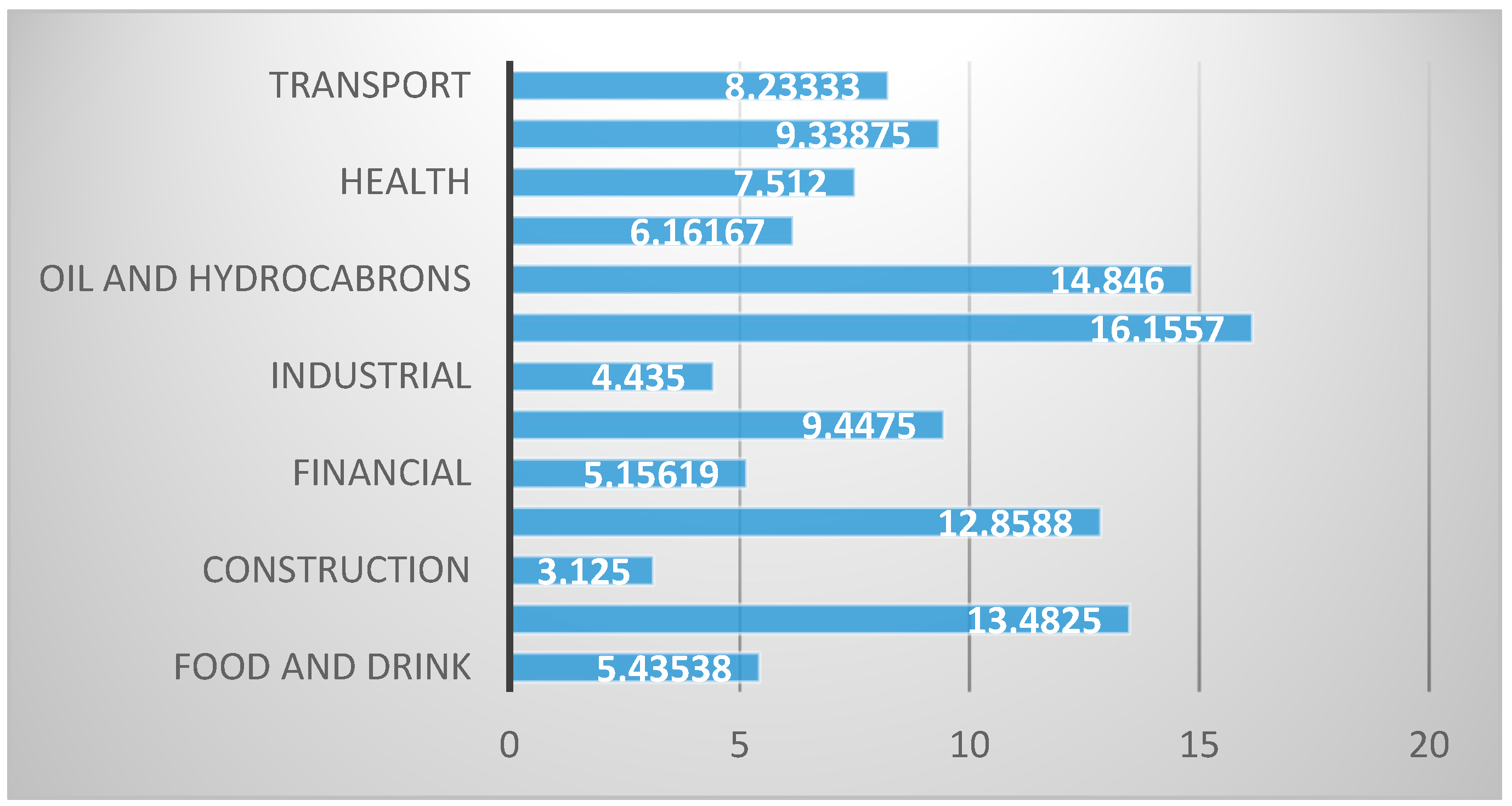

4.1. Descriptive Results

4.2. Results of the Regression Analysis

5. Discussion

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A. Coding Criteria

| Sub-Index | Category | Classification Criteria |

| General disclosure | Organisational profile | Information on organisational characteristics: brands, products, location of operations, types of customers, quantity of products offered. |

| Strategy and analysis | Information about the relevance of sustainability for the organization; trends that may affect it; and the main events, achievements, and failures in the period. | |

| Ethics and integrity | Explains the principles, values, norms, and ethical standards of the organisation, together with complaints mechanisms. | |

| Government and governance practices | Issues related to the organisation’s governance structure and the role of the board in risk management and in preparing the sustainability report. | |

| Relations with stakeholders | Explains how stakeholders may participate and the identification of the organisation’s stakeholders. | |

| Reporting practices | The report, its content and verification, and the reporting period or cycle. | |

| Economic issues | Economic performance | Aspects of the direct economic value generated and distributed to capital suppliers, employees, and government, and the financial implications, risks, and opportunities arising from climate change. |

| Presence in the market | Information about the proportion of senior managers hired from the local community. | |

| Indirect economic impact | How the economic development of poorer areas has been promoted and what improvements have been achieved in the social conditions. | |

| Acquisition practices | How the company supports suppliers that are local or owned by women or vulnerable groups. The forms of dialogue used to relate with suppliers and policies for the inclusion of new suppliers. | |

| Anticorruption practices | Issues related with policies, procedures, and/or legal actions related to the prevention of corruption. | |

| Unfair trade | The company’s position on monopolistic practices and free competition; related legal actions and the results obtained from them. | |

| Environmental issues | Materials | The inputs, renewable or non-renewable, used to manufacture or package the company’s products; the type of materials used the company’s operations and the supplies that are recycled, reused, and recovered. |

| Energy | The organization’s policies on energy consumption and their impact on climate change. | |

| Water | Aspects of the company’s operations related to the impact on water, through extraction or consumption, by type of source or by volume, and whether water is recycled or reused. | |

| Biodiversity | The prevention, management, or repair of damage to natural habitats in proximity to the company’s operations. The positive or negative impact made on biodiversity of flora and fauna. | |

| Emissions | Information about the release of substances into the atmosphere, such as greenhouse gases, their current intensity, and policies to reduce such emissions. | |

| Effluents and waste | Water spills, and the generation, treatment, and elimination of waste. Product spills. | |

| Environmental evaluation of suppliers | The environmental filters applied in the evaluation and selection of new suppliers, with respect to possible negative environmental impacts. | |

| Employment issues | Employment | The company’s approach to job creation, hiring, retention, and related practices. |

| Worker-company relations | On timely and satisfactory consultations with employees and their representatives, and the communication of significant operational changes. | |

| Health and safety in the workplace | Organisational practices to ensure health and safety in the workplace, and measures to analyse and control potential risks in this respect. Current measures to promote and protect health and well-being. | |

| Training and education | Policies and programmes for training and improvement of employee skills, and evaluations of performance and professional development. Annual training provided (hours), financial support, and time allocated to training. | |

| Diversity and equal opportunities | Opportunities for equality, and/or obstacles in this respect. The gender balance of workers, salary levels, women’s participation in governance, basic salaries for women and men and for minority or vulnerable groups. | |

| Non discrimination | Cases of discrimination and corrective actions taken. Measures adopted to prevent discrimination. | |

| Freedom of association and collective bargaining | The measures taken to allow and guarantee freedom of association, and operative conditions within the organisation or among its suppliers that may endanger this right. | |

| Social issues | Child labour | The measures taken to contribute to the abolition of child labour, and the organisation’s operations, or those of its suppliers, presenting significant risk in this respect. |

| Forced labour | The measures taken to contribute to the abolition of forced labour, and the organisation’s operations, or those of its suppliers, presenting significant risk in this respect. | |

| Safety practices | The conduct of the organisation’s security personnel towards third parties, effective training in human rights and respect for indigenous peoples. | |

| Rights of indigenous peoples | How the organisation prevents the rights of indigenous peoples from being infringed and how respect and consultation with indigenous peoples is fostered in matters that affect them. | |

| Evaluation of human rights | The organisation’s approach to preventing and mitigating negative impacts on human rights, and to creating and upholding agreements and contracts with human rights clauses. | |

| Local communities | How the community’s needs and vulnerabilities are addressed, how negative impacts are prevented and/or alleviated, how the organisation relates directly to each group, what community development programmes are supported, and how consultation processes are carried out. | |

| Social evaluation of suppliers | The social evaluation of suppliers and their selection, noting any negative social impacts in this respect and the measures taken to correct them. | |

| Public policy | The organisation’s participation in public policies and in lobbying. | |

| Product liability issues | Consumers’ health and safety | The health impacts of the organisation’s products and services. Improvements in product development, R&D, certification, manufacturing, production/service, distribution and/or elimination. |

| Marketing and product labelling | The organisation’s policies concerning responsible marketing, and its reporting of the origin of its services or product components. | |

| Consumer privacy | How the privacy of the clients’ personal data is protected. Acknowledgment of identified cases of leaks, thefts or loss of data. | |

| Socioeconomic compliance | The organisation’s compliance with laws and regulations in social and economic matters. |

References

- Baue, B.; Murninghan, M. The Accountability Web. Weaving Corporate Accountability and Interactive Technology. J. Corp. Citizsh. 2011, 41, 27–49. [Google Scholar]

- Sundstrom, B.; Levenshus, A.B. The art of engagement: Dialogic strategies on Twitter. J. Commun. Manag. 2017, 21, 17–33. [Google Scholar] [CrossRef]

- Abitbol, A.; Lee, S.Y. Messages on CSR-dedicated Facebook pages: What works and what doesn’t. Public Relat. Rev. 2017, 43, 796–808. [Google Scholar] [CrossRef]

- Etter, M. Reasons for low levels of interactivity: (Non-) interactive CSR communication in twitter. Public Relat. Rev. 2013, 39, 606–608. [Google Scholar] [CrossRef]

- Etter, M. Broadcasting, reacting, engaging—Three strategies for CSR communication in Twitter. J. Commun. Manag. 2014, 18, 322–342. [Google Scholar] [CrossRef]

- Merkl-Davies, D.M.; Brennan, N.M. A theoretical framework of external accounting communication: Research perspectives, traditions, and theories. Account. Audit. Account. J. 2017, 30, 433–469. [Google Scholar] [CrossRef]

- Dutot, V.; Lacalle Galvez, E.; Versailles, D.W. CSR communications strategies through social media and influence on e-reputation An exploratory study. Manag. Decis. 2016, 54, 363–389. [Google Scholar] [CrossRef]

- Chae, B.; Park, E. Corporate Social Responsibility (CSR): A Survey of Topics and Trends Using Twitter Data and Topic Modeling. Sustainability 2018, 10, 2231. [Google Scholar] [CrossRef]

- Mazzei, M.J.; Noble, D. Big data dreams: A framework for corporate strategy. Bus. Horiz. 2017, 60, 405–414. [Google Scholar] [CrossRef]

- U Mass-Darmouth. The 2017 Fortune 500 Go Visual and Increase Use of Instagram, Snapchat, and YouTube. Available online: https://www.umassd.edu/cmr/socialmediaresearch/2017fortune500/#d.en.963986 (accessed on 3 April 2018).

- Painter-Morland, M.; Deslandes, G. Reconceptualizing CSR in the Media Industry as Relational Accountability. J. Bus. Ethics 2017, 143, 665–679. [Google Scholar] [CrossRef]

- Hossain, M.; Reaz, M. The determinants and characteristics of voluntary disclosure by Indian banking companies. Corp. Soc. Responsib. Environ. Manag. 2007, 14, 274–288. [Google Scholar] [CrossRef]

- Tan, A.; Benni, D.; Liani, W. Determinants of Corporate Social Responsibility Disclosure and Investor Reaction. Int. J. Econ. Financ. Issues 2016, 6, 11–17. [Google Scholar]

- Thijssens, T.; Bollen, L.; Hassink, H. Secondary Stakeholder Influence on CSR Disclosure: An Application of Stakeholder Salience Theory. J. Bus. Ethics 2015, 132, 873–891. [Google Scholar] [CrossRef]

- Patten, D.M. Exposure, legitimacy, and social disclosure. J. Account. Public Policy 1991, 10, 297–308. [Google Scholar] [CrossRef]

- Bakhtina, K.; Goudriaan, J.W. CSR reporting in multinational energy companies. Transf. Eur. Rev. Labour Res. 2011, 17, 95–99. [Google Scholar] [CrossRef]

- Castelló, I.; Etter, M.; Årup Nielsen, F. Strategies of Legitimacy Through Social Media: The Networked Strategy. J. Manag. Stud. 2016, 53, 402–432. [Google Scholar] [CrossRef]

- Bonsón, E.; Ratkai, M. A set of metrics to assess stakeholder engagement and social legitimacy on a corporate Facebook. Online Inf. Rev. 2013, 37, 787–803. [Google Scholar] [CrossRef]

- Cho, M.; Furey, L.D.; Mohr, T. Communicating Corporate Social Responsibility on Social Media: Strategies, Stakeholders, and Public Engagement on Corporate Facebook. Bus. Prof. Commun. Q. 2017, 80, 52–69. [Google Scholar] [CrossRef]

- Li, Q.; Wei, W.; Xiong, N.; Feng, D.; Ye, X.; Jiang, Y. Social Media Research, Human Behavior, and Sustainable Society. Sustainability 2017, 9, 384. [Google Scholar] [CrossRef]

- OECD. Government at a Glance: Latin America and the Caribbean 2017; OECD: París, France, 2016; ISBN 9789264266391. [Google Scholar]

- Evans, M. 3 Things You Need To Know about Latin American Digital Consumers. Available online: https://www.forbes.com/sites/michelleevans1/2017/08/10/3-things-you-need-to-know-about-latin-american-digital-consumers/2/#6379015f226f (accessed on 12 June 2018).

- Tench, R.; Jones, B. Social media: The Wild West of CSR communications. Soc. Responsib. J. 2015, 11, 290–305. [Google Scholar] [CrossRef]

- Kaplan, A.M.; Haenlein, M. Users of the world, unite! The challenges and opportunities of Social Media. Bus. Horiz. 2010, 53, 59–68. [Google Scholar] [CrossRef]

- Jansen, B.J.; Zhang, M.; Sobel, K.; Chowdury, A. Twitter power: Tweets as electronic word of mouth. J. Am. Soc. Inf. Sci. Technol. 2009, 60, 2169–2188. [Google Scholar] [CrossRef]

- Colleoni, E. CSR communication strategies for organizational legitimacy in social media. Corp. Commun. Int. J. 2013, 18, 228–248. [Google Scholar] [CrossRef]

- Bachmann, P.; Ingenhoff, D. Legitimacy through CSR disclosures? The advantage outweighs the disadvantages. Public Relat. Rev. 2016, 42, 386–394. [Google Scholar] [CrossRef]

- Benites-Lazaro, L.L.; Mello-Théry, N.A. CSR as a legitimatizing tool in carbon market: Evidence from Latin America’s Clean Development Mechanism. J. Clean. Prod. 2017, 149, 218–226. [Google Scholar] [CrossRef]

- Suchman, M. Managing Legitimacy: Strategic and Institutional Approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman: Mashfield, UK, 1984; Volume 1, ISBN 0631218602. [Google Scholar]

- Zimmerman, M.A.; Zeitz, G.J. Beyond Survival: Achieving New Venture Growth by Building Legitimacy. Acad. Manag. Rev. 2002, 27, 414–431. [Google Scholar] [CrossRef]

- Dowling, J.; Pfeffer, J. Organizational Legitimacy: Social Values and Organizational Behavior between the Organizations seek to establish congruence. Pac. Sociol. Rev. 1975, 18, 122–136. [Google Scholar] [CrossRef]

- Cowen, S.S.; Ferreri, L.B.; Parker, L.D. The impact of corporate characteristics on social responsibility disclosure: A typology and frequency-based analysis. Account. Organ. Soc. 1987, 12, 111–122. [Google Scholar] [CrossRef]

- Branco, M.; Rodrigues, L. Factors Influencing Social Responsibility Disclosure by Portuguese Companies. J. Bus. Ethics 2008, 83, 685–701. [Google Scholar] [CrossRef]

- Bayoud, N.S.; Kavanagh, M. Factors Influencing levels of Corporate Social Responsibility Disclosure by Libyan Firms: A Mixed Study. Int. J. Econ. Financ. 2012, 4, 13–29. [Google Scholar] [CrossRef]

- Gamerschlag, R.; Möller, K.; Verbeeten, F. Determinants of voluntary CSR disclosure: Empirical evidence from Germany. Rev. Manag. Sci. 2011, 5, 233–262. [Google Scholar] [CrossRef]

- Du, S.; Vieira, E.T. Striving for Legitimacy Through Corporate Social Responsibility: Insights from Oil Companies. J. Bus. Ethics 2012, 110, 413–427. [Google Scholar] [CrossRef]

- Hackston, D.; Milne, M.J. Some determinants of social and environmental disclosures in New Zealand companies. Account. Audit. Account. J. 1996, 9, 77–108. [Google Scholar] [CrossRef]

- Wang, J.; Yao, S. The Determinants of Corporate Social Responsibility Disclosure: Evidence From China. J. Appl. Bus. Res. 2013, 29, 1833. [Google Scholar] [CrossRef]

- Astley, W.; Van de Ven, A. Central Perspectives and Debates in Organization Theory. Adm. Sci. Q. 1983, 28, 245–273. [Google Scholar] [CrossRef]

- Carpenter, M.A.; Geletkanycz, M.A.; Sanders, W.G. Upper Echelons Research Revisited: Antecedents, Elements, and Consequences of Top Management Team Composition. J. Manag. 2004, 30, 749–778. [Google Scholar] [CrossRef]

- Hambrick, D.C.; Mason, P.A. Upper Echelons: The Organization as a Reflection of Its Top Managers. Source Acad. Manag. Rev. 1984, 9, 193–206. [Google Scholar] [CrossRef]

- Ng, E.S.; Sears, G.J. CEO Leadership Styles and the Implementation of Organizational Diversity Practices: Moderating Effects of Social Values and Age. J. Bus. Ethics 2012, 105, 41–52. [Google Scholar] [CrossRef]

- Hambrick, D.C. Upper Echelons Theory: An Update. Acad. Manag. Rev. 2007, 32, 334–343. [Google Scholar] [CrossRef]

- Petrenko, O.; Aime, F.; Ridge, J.; Hill, A. Corporate Social Responibility or CEO narcissism? CSR motivations and organizational performance. Strateg. Manag. J. 2016, 37, 262–279. [Google Scholar] [CrossRef]

- Lewis, B.; Walls, J.; Dowell, G. Difference in Degrees: CEO characteristics and firm environmental disclosure. Strateg. Manag. J. 2014, 35, 712–722. [Google Scholar] [CrossRef]

- Marais, M. CEO rhetorical strategies for corporate social responsibility (CSR). Soc. Bus. Rev. 2012, 7, 223–243. [Google Scholar] [CrossRef]

- Oh, W.-Y.; Chang, Y.K.; Cheng, Z. When CEO Career Horizon Problems Matter for Corporate Social Responsibility: The Moderating Roles of Industry-Level Discretion and Blockholder Ownership. J. Bus. Ethics 2016, 133, 279–291. [Google Scholar] [CrossRef]

- Manner, M. The impact of CEO characteristics on Corporate Social Performance. Corp. Soc. Responsib. Environ. Manag. 2010, 93, 53–72. [Google Scholar] [CrossRef]

- Khlif, H.; Achek, I. Gender in accounting research: A review. Manag. Audit. J. 2017, 32, 627–655. [Google Scholar] [CrossRef]

- Huang, S.K. The Impact of CEO Characteristics on Corporate Sustainable Development. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 234–244. [Google Scholar] [CrossRef]

- Zhang, H.; Ou, A.Y.; Tsui, A.S.; Wang, H. CEO humility, narcissism and firm innovation: A paradox perspective on CEO traits. Leadersh. Q. 2017, 28, 585–604. [Google Scholar] [CrossRef]

- Damanpour, F.; Schneider, M. Characteristics of innovation and innovation adoption in public organizations: Assessing the role of managers. J. Public Adm. Res. Theory 2009, 19, 495–522. [Google Scholar] [CrossRef]

- Barker, V.L.; Mueller, G.C. CEO Characteristics and Firm R&D Spending. Manag. Sci. 2002, 48, 782–801. [Google Scholar] [CrossRef]

- Kitchell, S. CEO characteristics and technological innovativeness: A Canadian perspective. Can. J. Adm. Sci. 1997, 14, 111–121. [Google Scholar] [CrossRef]

- Musteen, M.; Barker, V.L.; Baeten, V.L. The influence of CEO tenure and attitude toward change on organizational approaches to innovation. J. Appl. Behav. Sci. 2010, 46, 360–387. [Google Scholar] [CrossRef]

- Finkelstein, S.; Hambrick, D.; Canella, A. Strategic Leadership: Theory and Research on Executives, Top Management Teams, and Boards; Oxford University Press: Oxford, UK, 2009; ISBN 978-0-19-516207-3. [Google Scholar]

- Fuchs, C.; Hofkirchner, W.; Schafranek, M.; Raffl, C.; Sandoval, M.; Bichler, R. Theoretical Foundations of the Web: Cognition, Communication, and Co-Operation. Towards an Understanding of Web 1.0, 2.0, 3.0. Future Internet 2010, 2, 41–59. [Google Scholar] [CrossRef]

- Lin, K.-Y.; Lu, H.-P. Why people use social networking sites: An empirical study integrating network externalities and motivation theory. Comput. Hum. Behav. 2011, 27, 1152–1161. [Google Scholar] [CrossRef]

- Millham, M.H.; Atkin, D. Managing the virtual boundaries: Online social networks, disclosure, and privacy behaviors. New Media Soc. 2016, 20, 50–67. [Google Scholar] [CrossRef]

- Telefónica Redes Sociales en el Mundo Corporativo. Experiencias y Aprendizajes. Available online: https://www.fundacioncarolina.es/wp-content/uploads/2015/07/Redes-sociales-mundo-corporativo-Douglas-Ochoa.pdf (accessed on 12 April 2018).

- Internet Live Stats Twitter Usage Statistics. Available online: http://www.internetlivestats.com/twitter-statistics/ (accessed on 4 April 2018).

- Statista.com. Number of Monthly Active Twitter Users Worldwide from 1st Quarter 2010 to 4th Quarter 2017 (in Millions). Available online: https://www.statista.com/statistics/282087/number-of-monthly-active-twitter-users/ (accessed on 4 April 2018).

- Busch, T.; Shepherd, T. Doing well by doing good? Normative tensions underlying Twitter’s corporate social responsibility ethos. Converg. Int. J. Res. New Media Technol. 2014, 20, 293–315. [Google Scholar] [CrossRef]

- Van Dijck, J. Tracing Twitter: The Rise of a Microblogging platform. Int. J. Media Cult. Polit. 2012, 7, 333–348. [Google Scholar] [CrossRef]

- Khalil, S.; O’sullivan, P. Corporate social responsibility: Internet social and environmental reporting by banks. Meditari Account. Res. 2017, 25, 414–446. [Google Scholar] [CrossRef]

- Lyon, T.P.; Montgomery, A.W. Tweetjacked: The Impact of Social Media on Corporate Greenwash. J. Bus. Ethics 2013, 118, 747–757. [Google Scholar] [CrossRef]

- Saxton, G.D.; Waters, R.D. What do Stakeholders Like on Facebook? Examining Public Reactions to Nonprofit Organizations’ Informational, Promotional, and Community-Building Messages. J. Public Relat. Res. 2014, 26, 280–299. [Google Scholar] [CrossRef]

- Araujo, T.; Kollat, J. Communicating effectively about CSR on Twitter: The power of engaging strategies and storytelling elements For Authors Communicating effectively about CSR on Twitter The power of engaging strategies and storytelling elements. Internet Res. 2018, 28, 419–431. [Google Scholar] [CrossRef]

- MERCO. Qué es Merco-Monitor Empresarial de Reputación Corporativa. Available online: http://www.merco.info/co/que-es-merco (accessed on 11 July 2018).

- Cegarra-Navarro, J.; Martínez-Martínez, A. Linking orporate social responsibility with admiration through organizational outcomes. Soc. Responsib. J. 2009, 5, 499–511. [Google Scholar] [CrossRef]

- Ros-Diego, V.-J.; Castelló-Martínez, A.; Martínez-Arcos, C.-A. CSR communication through online social media. Rev. Lat. Comun. Soc. 2012, 67, 47–67. [Google Scholar] [CrossRef]

- Odriozola, M.D.; Baraibar-Diez, E. Is Corporate Reputation Associated with Quality of CSR Reporting? Evidence from Spain. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 121–132. [Google Scholar] [CrossRef]

- Global Reporting Initiative. GRI Sustainability Reporting Standards. Available online: https://www.globalreporting.org/standards/ (accessed on 12 February 2018).

- Krippendorff, K. Content Analysis: An Introduction to Its Methodology; SAGE Publications: Thousand Oaks, CA, USA, 2012. [Google Scholar]

- Conde, M.D.F.T. Diseño de Índices de Divulgación de la Información de Responsabilidad Social Empresarial y Gobierno Corporativo: Un Análisis en las Mayores Empresas de la Península Ibérica. 2014. Available online: http://dehesa.unex.es/bitstream/handle/10662/2467/TDUEX_2014_Conde_MF.pdf?sequence=1 (accessed on 12 February 2018).

- Correa, T.; Hinsley, A.W.; Gil De Zúñiga, H. Who interacts on the Web? The intersection of users’ personality and social media use. Comput. Hum. Behav. 2010, 26, 247–253. [Google Scholar] [CrossRef]

- Wamba, F.; Carter, L.S. Twitter adoption and use by SMEs: An empirical study. In Proceedings of the 46 Hawaii International Conferences on System Sciences (HICSS), Maui, HI, USA, 7–10 January 2013. [Google Scholar]

- Brammer, S.; Millington, A.I. Firm size, organizational visibility and corporate philanthropy: An empirical analysis. J. Bus. Ethics 2006, 15, 6–19. [Google Scholar] [CrossRef]

- El Mercurio April 2016. Available online: http://www.emol.com/noticias/Nacional/2016/04/23/799468/Girardi-anuncia-acciones-penales-contra-Codelco-por-grave-contaminacion-en-Chacabuco.html (accessed on 13 July 2018).

- Cooperativa August 2016. Available online: https://www.cooperativa.cl/noticias/pais/medioambiente/contaminacion/codelco-provoco-nuevo-derrame-de-concentrado-de-cobre-en-los-andes/2016-08-24/163051.html (accessed on 13 July 2018).

- Pozas, M.D.C.S.; Lindsay, N.M.; du Monceau, M.I. Corporate social responsibility and extractives industries in Latin America and the Caribbean: Perspectives from the ground. Extr. Ind. Soc. 2015, 2, 93–103. [Google Scholar] [CrossRef]

- Weng, D.H.; Lin, Z.; Amason, A.; Croson, R.; Dess, G.; Jargowsky, P.; Lim, E.; Peng, M. Beyond CEO Tenure: The Effect of CEO Newness on Strategic Changes. J. Manag. 2014, 40, 2009–2032. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Panel A: Distribution by Country | |||

| Country | Freq. | Percent | Cum. |

| Chile | 28 | 30.10 | 30.10 |

| Colombia | 34 | 36.55 | 66.66 |

| Mexico | 20 | 21.50 | 88.17 |

| Peru | 11 | 11.82 | 100 |

| Total | 93 | 100 | |

| Panel B: Distribution by Sector | |||

| Sector | Freq. | Percent | Cum. |

| Food and drink | 13 | 13.98 | 14.44 |

| Cement | 4 | 4.30 | 18.28 |

| Construction | 2 | 2.15 | 20.43 |

| Energy, gas & water | 8 | 8.60 | 29.03 |

| Financial | 21 | 22.58 | 51.61 |

| Business holding | 4 | 4.30 | 55.91 |

| Industrial | 7 | 7.53 | 63.44 |

| Mining | 7 | 7.53 | 70.97 |

| Oil and hydrocarbons | 5 | 5.38 | 76.34 |

| Retail | 6 | 6.45 | 82.80 |

| Health | 5 | 5.38 | 88.17 |

| Telecommunications | 8 | 8.60 | 96.77 |

| Transport | 3 | 3.23 | 100 |

| Total | 93 | 100 | |

| Sector | CSR Tweets | Percentage | Acc. |

|---|---|---|---|

| Food and drink | 244 | 14.57% | 14.57% |

| Cement | 113 | 6.75% | 21.31% |

| Construction | 5 | 0.30% | 21.61% |

| Energy, gas & water | 289 | 17.25% | 38.87% |

| Financial | 167 | 9.97% | 48.84% |

| Business holding | 51 | 3.04% | 51.88% |

| Industrial | 52 | 3.10% | 54.99% |

| Mining | 297 | 17.73% | 72.72% |

| Oil and hydrocarbons | 165 | 9.85% | 82.57% |

| Retail | 82 | 4.90% | 87.46% |

| Health | 81 | 4.84% | 92.30% |

| Telecommunications | 82 | 4.90% | 97.19% |

| Transport | 47 | 2.81% | 100.00% |

| Total | 1675 | 100 |

| Country | N | Mean | Median | sd | Min | Max |

|---|---|---|---|---|---|---|

| Overall | 93 | 8.305 | 6.25 | 6.612 | 0 | 29.7 |

| Chile | 28 | 8.923 | 6.31 | 7.79 | 0 | 29.7 |

| Colombia | 34 | 9.055 | 6.34 | 6.591 | 1.25 | 24.05 |

| Mexico | 20 | 7.146 | 6.55 | 5.614 | 0 | 20.12 |

| Peru | 11 | 6.521 | 4.58 | 5.098 | 1.25 | 15 |

| Variable | N | Mean | Median | sd | Min | Max |

|---|---|---|---|---|---|---|

| Size | 93 | 15.17 | 15.01 | 1.70 | 9.66 | 18.01 |

| Sens | 93 | 0.24 | 0 | 0.43 | 0 | 1 |

| Gen | 93 | 0.07 | 0 | 0.25 | 0 | 1 |

| Age | 93 | 52.58 | 51 | 7.13 | 38 | 75 |

| Tenure | 93 | 6.02 | 4 | 7.60 | 0 | 36 |

| CEODuality | 93 | 0.38 | 0 | 0.49 | 0 | 1 |

| CSRComm | 93 | 0.26 | 0 | 0.44 | 0 | 1 |

| Adherence | 93 | 2.02 | 2 | 0.61 | 1 | 3 |

| TDI | Coef. | Std. Err. | t | p > t | Significance |

|---|---|---|---|---|---|

| Size | −0.31 | 0.35 | −0.89 | 0.375 | |

| Sens | 3.69 | 1.82 | 2.02 | 0.047 | ** |

| Gen | −0.58 | 3.31 | −0.17 | 0.862 | |

| Age | 0.14 | 0.09 | 1.46 | 0.147 | |

| Tenure | −0.21 | 0.07 | −2.8 | 0.006 | *** |

| CEODuality | 0.08 | 1.19 | 0.07 | 0.948 | |

| CSRcommitee | 1.23 | 1.65 | 0.75 | 0.456 | |

| Adherence | 2.93 | 0.97 | 3.02 | 0.003 | *** |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Suárez-Rico, Y.M.; Gómez-Villegas, M.; García-Benau, M.A. Exploring Twitter for CSR Disclosure: Influence of CEO and Firm Characteristics in Latin American Companies. Sustainability 2018, 10, 2617. https://doi.org/10.3390/su10082617

Suárez-Rico YM, Gómez-Villegas M, García-Benau MA. Exploring Twitter for CSR Disclosure: Influence of CEO and Firm Characteristics in Latin American Companies. Sustainability. 2018; 10(8):2617. https://doi.org/10.3390/su10082617

Chicago/Turabian StyleSuárez-Rico, Yuli Marcela, Mauricio Gómez-Villegas, and María Antonia García-Benau. 2018. "Exploring Twitter for CSR Disclosure: Influence of CEO and Firm Characteristics in Latin American Companies" Sustainability 10, no. 8: 2617. https://doi.org/10.3390/su10082617

APA StyleSuárez-Rico, Y. M., Gómez-Villegas, M., & García-Benau, M. A. (2018). Exploring Twitter for CSR Disclosure: Influence of CEO and Firm Characteristics in Latin American Companies. Sustainability, 10(8), 2617. https://doi.org/10.3390/su10082617