1. Introduction

Cooperatives play a key role in worldwide food production and distribution systems, from seed to plate, with farmers and their cooperative businesses playing a central role to ensure farm produce reaches consumers. The rising trend towards consolidating certain phases in the agricultural system (e.g., retail distribution, seed suppliers, phytosanitary products, and biotechnology) and greater internationalization results in the need to establish organizational strategies for small farmers. Consequently, small-scale farmers tend to band together through the creation of companies with cooperative structures for marketing, financing, processing, and other collective services. Such organizations have shown that they play a crucial role in ensuring the sustainability of family-oriented agriculture and small farms [

1,

2,

3].

As justified from the new institutionalism perspective, agricultural producer cooperatives emerged to address market failures or imperfections, overcoming monopsistic power held both upstream and downstream in the food industry. Farmers created cooperatives to have more direct control over and access to the market and a more efficient integration in the supply chain due to increased negotiating power, pooling resources to manage risk, and reducing transaction costs [

4,

5,

6]. Contemporary theories of the firm, through which cooperatives have often been studied, have relied on either the firm as hierarchy or the firm as a nexus of contracts, or both [

7,

8,

9], where in addition to market forces, cooperative governance gained significant importance. As well, the concept of hybrids [

10] depicts the cooperative as operating between markets and hierarchy.

However, by resorting to explanatory theories of the firm which rely predominantly on the characteristics and logic of investor-owned firms, dominated as they are by market exchanges and hierarchical control [

11], new institutionalism offers only a limited explanatory theory on the possible reasons for success and longevity of cooperatives. Given the significant differences between cooperatives and investor owned firms with respect to founding justification, internal cooperative governance and ownership structures [

12,

13,

14], cooperatives may very well continue to survive, overcoming the commonly referred to “market failures”, whilst in addition, or at the same time, creating value through diverse mechanisms (as opposed to simply creating profits) in a very different manner.

Relying on the insights of Elinor Ostrom [

15] that collective action based on cooperation can be as effective as markets or hierarchies, and the work of various scholars who are exploring cooperation as a coordination mechanism with an “associative nature that is based on the mutual benefit of participating actors” [

11,

16], we look to an example in the agricultural cooperatives of Almería in South East Spain to demonstrate the continuing longevity of the cooperatives of such region, due to a diversity of value created by virtue of cooperation as a coordination mechanism. Prior studies relying on a dynamic lifecycle approach have shown Almería cooperatives to be dynamic entities, capable of renewal, redeployment, regeneration, and recombination in order to meet new challenges [

17]. In this study, we take another complementary approach, specifically focusing on cooperation as the coordination mechanism of economic, social, and environmental activity, wherein value maximisation and not simply profit maximisation is emphasized, which in turn contributes to cooperative longevity.

The objectives of the present paper are twofold: (a) to review the role of cooperatives as a coordination mechanism in the horticultural sector of Almería; (b) to illustrate the balancing of diverse logics for Almeria cooperative justifications and objectives, particularly considering socio-economic and eco-social goals.

The rest of the paper is structured as follows: In the second section we describe the cooperative nature of Almería’s agricultural sector. In the third section we describe how cooperatives have functioned as a coordination mechanism, while the fourth section explores the relationship between sustainability and longevity of the cooperative agricultural system, relying on market, and eco-socio indicators. Finally, our conclusions point to the important role of agricultural cooperatives in mediating economic, social, and environmental sustainability needs and providing both private and collective goods, hence, their contribution to cooperative longevity. The cooperatives in Almería have increasingly relied on collective collaboration in order to meet social-economic and social-ecological challenges, transforming their role from a market dominant logic to that of cooperation as a coordination mechanism based on the mutual benefit of the community and environment.

2. Background Discussion of Almería Agricultural Cooperatives

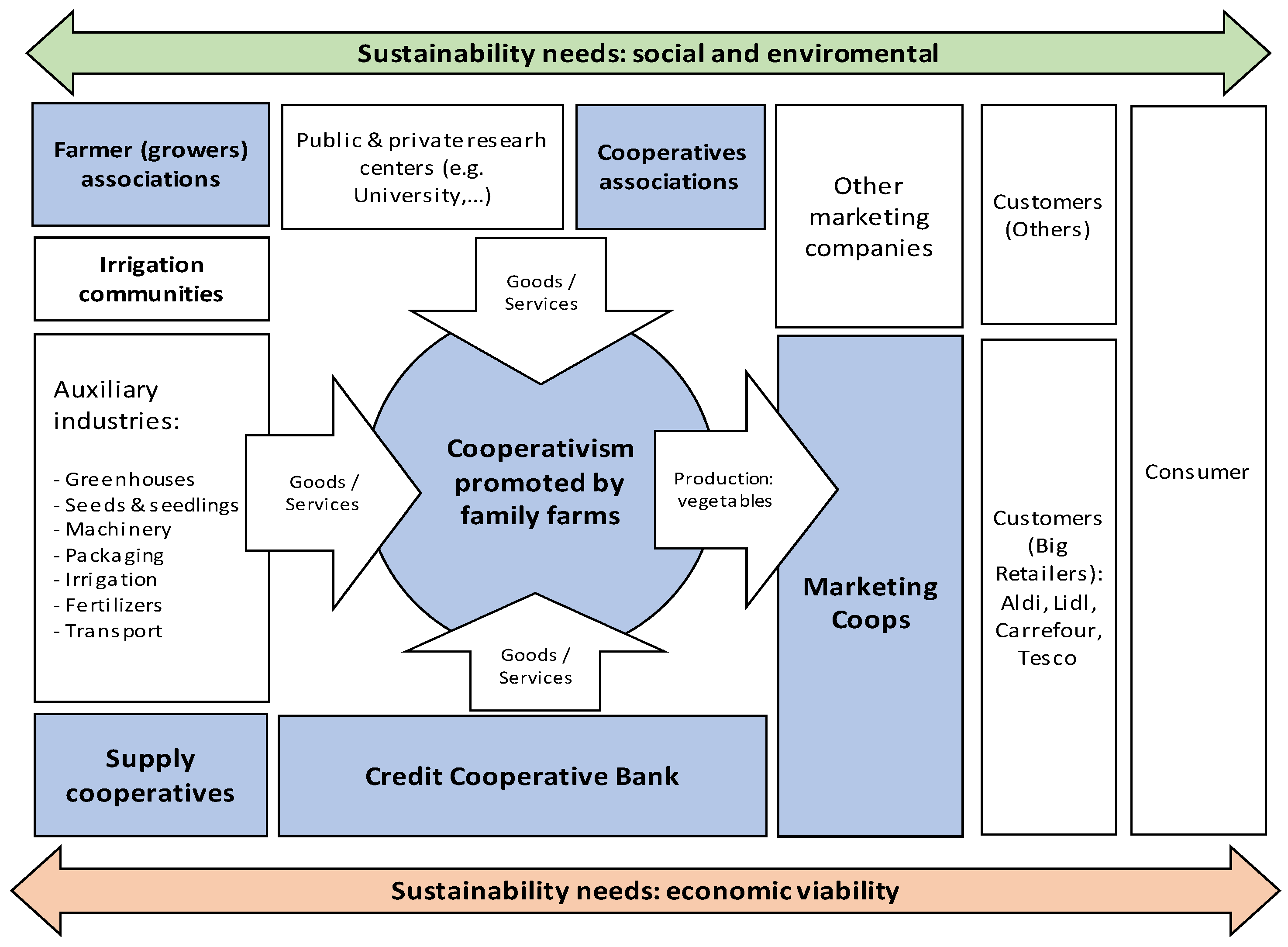

Almería represents a particular development model: in the last five decades, from the beginnings of subsistence farming in near desert conditions, Almería has fostered an economic base of family farmers that has created an innovative cooperative community based on greenhouse specialised in fruit and vegetables (F&V) production [

18,

19,

20]. The farmland, which occupies only 4% of the area of the province, is divided into small side-by-side parcels amongst 15,000 small-scale family farmers, each cultivating an average of approximately 2 hectares. The small production units are organised into cooperatives. Over 65% of sales are handled by marketing cooperatives, with an annual turnover of 1900 million Euros and annual production of 3 million tons. More than 90 farmer-owned cooperatives are currently operating in the area providing either specialized or general services. Most of the farmers are members of one or more cooperatives (marketing, supply or financing cooperatives). There are also cooperative associations (e.g., the Association of Growers and Exporters of Fruit and Vegetables of Almería, COEXPHAL, and the Federation of Agrarian Cooperative Entities of Andalusia, CAA) which represent their members in dealings with local institutions and play an important role in coordinating collective objectives. Despite fierce global competition, narrowing profit margins and increasing technological and regulatory demands, the cooperative sector endures. Currently, the agrarian cooperatives of Almeria represent 21% of all F&V cooperative turnover in Spain. The international commercialisation of this sector is also relevant, and cooperatives represent about 75% of Almeria’s exports, accounting for 25% of the total Spanish F&V exports. The cooperatives have evolved locally, generating networks among the farms and a greater degree of interrelationship with the other stakeholders in the sector and territory. An auxiliary industry almost equal in value has grown up around the sector and the Almería agriculture has often been characterized as an industrial district or cluster [

21]. Currently, this farming system maintains significant cooperative weight, as can be seen in

Figure 1 below.

Almería cooperatives, made up in large part by small holding, family farming members, occupy a central position in the cluster and receive advice and support from different business associations and public entities (the university), as well as finance from Cajamar, the leading Spanish cooperative bank with its origins in Almeria. Farm inputs are supplied for the most part by multinationals located in the area (e.g., seeds), although other local firms exist which are dedicated to greenhouse construction, integrated pest management, fertilisers, and phytosanitary products, constituting the above mentioned auxiliary industry. As well, the marketing companies have created supply cooperatives to reduce the price of inputs. Alongside cooperatives, other companies exist, which sell product by auction systems. For both these auctions and the marketing cooperatives, the main clients are large supermarkets such as Lidl, Aldi, Tesco, Carrefour, and Edeka. These international supply chains have implied an important extension of quality certifications and stricter controls to guarantee social and environmental sustainability.

The original thrust in the development of agricultural cooperatives stemmed from those who would later become the founders of the cooperative credit bank [

19]. Noting the lack of a market in which family farmers could sell their product, a classic market failure, several cooperative promotors encouraged the organisation of producer and supply cooperatives. Reflecting a virtuous cycle, it was in the cooperative bank’s interest that the farmers and agricultural cooperatives were successful. The family farms, able to survive due to collective action, gave rise to the parallel development of cooperative entities that specialized in different services: the marketing of produce, financing, the supply of resources, and agronomy assessment services [

22]. Consequently, the founding of the Almería cooperatives, both credit and agricultural, could be seen to fall neatly within market failure justifications.

With respect to cooperative longevity, it is important to consider that the Almería cooperative sector is only 50 years old, and the concept of longevity is relative. Nevertheless, the persistence of this small-scale family farming model is determined by cooperative development, which has been adapted to respond to different challenges of this specific farming system.

Nevertheless, the changing nature of both European and global agricultural markets, combined with the fact that sustainability has become a crucial issue, gaining more urgency with climate change and scarcity of natural resources, requires a reflection on the current situation of cooperative longevity and success in Almería. In other words, these entities have to rethink both their management and organizations to achieve adequate efficiency in supply chains while at the same time promoting social and environmental outcomes. Simply put, why do small family farmers and their many cooperatives still exist in Almería? They exist in a close geographical proximity of the 30,000 ha under greenhouse cultivation, and most marketing cooperatives carry out identical activities and export to the same small handful of large multi-national customers. If we look to theories of market and hierarchy, one could conclude that greater efficiencies and market power might be gained through the non-cooperative business model, not to mention simplified governance [

7,

9]. We consider that the organizational and structural Almería system is due to the role of the cooperative in the sustainability of family farms, which are the drivers for adaptation and for achieving a relative balance among economic, social, and environmental goals.

3. The Role of Cooperatives as a Coordination Mechanism

As mentioned above, enterprise can be considered as a coordination of economic activity, organizing production and the exchange of goods and services. But if we consider that entrepreneurial activity cannot be reduced only to markets (nexus or contracts) or hierarchy, both motivated by maximization of profits, the type of collective action represented by cooperatives, and in this case family farms, may be more fully analyzed. Both productive structures act as main agents of interrelationships among economic, social, and environmental dimensions [

3].

In this manner, production activities organized through cooperatives, especially those that include family farms, involve a great deal of interaction between social and economic components [

23], representing “socioeconomic” factors, as well as social and environmental components, forming “eco-social” factors [

24]. Social elements can act as drivers and controllers of economic activity, simultaneously promoting eco-social objectives such as organic agriculture, eco-efficiency in the use of agricultural resources, and environmental protection.

For example, from a socio-economic perspective, in a production sector with a broad base mainly consisting of cooperatives, cooperatives have been shown to be indispensable for maintaining employment and economic viability within local communities in rural areas [

23] and promoting entrepreneurship. Moreover, they develop social capital and promote welfare equity, participation and social cohesion [

20,

25].

From the eco-social perspective, as family farmers and their local cooperatives are in direct contact with the natural landscape and rely on basic natural resources, they are acutely aware of the limitations of land and water [

1,

26]. As Ostrom [

15] indicates, the “tragedy of the commons” is not always a necessary outcome, given the shared sense of place and interest in the shared common goods of natural resources, in addition to the shared economic interests. Moreover, for these cooperatives the goal of improving quality of life is more associated with the sense of belonging to a place and to the natural environment than it is for those in other production sectors [

25]. As a result, the sustainable management of resources and the environment has been found to be intrinsic components of family farms and their communities, who, in turn, transmit this awareness to other farming organizations and other rural economic activities [

27,

28].

In light of this, we set out in

Table 1 below, a scheme which represents the cooperative coordination or interrelationship mechanism between sustainability dimensions. Cooperative coordination mediates between market, socio-economic, and eco-social needs and justification. However, while there is some sense of progression from one logic to another, it should be kept in mind that all three logics may operate at the same time, with one logic being more or less dominant than another.

4. Sustainability and Longevity of Cooperative Agricultural System

4.1. Methodology

Following the case study method [

29], an in-depth analysis was performed on a particular development process, presenting a global vision of the phenomenon while striving to avoid generalisation. This practical case contributes to the debate on the cooperatives’ persistence and their role in the sustainability of the family farm model. In this context, the research design consists of linking the data to be compiled with the theoretical issues that were discussed in the previous sections. The initial premise of the present work is that cooperatives, in which family farms constitute the basic element in the intensive agrarian model in Almería, play a fundamental role in fostering sustainable development. In turn, their ability to meet a wide range of needs and challenges of members and the community leads to their longevity. Cooperatives are able to act as both a market and non-market coordination mechanism, balancing the economic, social, and environmental dimensions, such that neither market nor non-market logics are dominant or exclusive [

11]. With this in mind, our analysis identifies the socio-economic and eco-social components according to several studies focused on this cooperative farming system, as well as additional indicators contained in this paper. These studies are of an inter-disciplinary nature, because many aspects have been analyzed from the perspective of development and agricultural economics (e.g., Galdeano-Gómez et al., 2013) [

20], agronomy (e.g., Medina 2009) [

30], sociology (e.g., García Lorca 2010) [

31], geography (e.g., Tout 1990) [

32], ecology (e.g., Godoy-Durán et al., 2017) [

33], organizational studies (Giagnocavo, et al., 2013) [

19], or history (e.g., Aznar-Sánchez et al., 2011) [

22]. The data and information that are drawn from these studies outline several indicators that demonstrate the influence of the multiple/diverse factors in cooperatives’ longevity in an integrated way.

Based on these components described above (

Table 1), we have included the following indicators in our analysis:

- -

Market and socio-economic indicators: organization to gain market power (via collaboration and/or co-opetition), maintain stable employment and equitable income, and promote innovation and knowledge systems.

- -

Eco-social indicators: responsible use and management of natural resources, on the scale of individual farms and cooperatives (collective) as a whole.

4.2. Market and Socio-Economic Indicators

4.2.1. Organization to Gain Market Power

Cooperatives have played a key role in organising the small scale producers of Almería. Since the entrance into the European Union, and the designation of Producer Organisations (PO) of fruits and vegetables, cooperatives have been the predominant organisational form. These PO are the general organisational form established by the Common Agricultural Policy in several sectors, and this case according to the Common Market Organisation of fruit and vegetable sector (c.f. European Commission, 2016) [

34].As

Table 2 indicates, 86% of the value of horticultural production in Almería province is marketed by cooperatives (designed as PO), a much higher percentage than the Spanish national total of 36%, and higher than France and Italy. While Spanish cooperatives still lag behind some European countries as to size,

Table 3 shows that Almería vegetable cooperatives are larger with respect to Spanish vegetable cooperatives. Out of the top five such cooperatives in Spain, four are located in Almería [

35]. Amongst these, are cooperatives UNICA-Fresh and Murgiverde, which have created second level (or tier-two) cooperatives, or the case of Vicasol and Agroiris, which have attracted new members through increased international marketing efforts.

Currently, several big marketing cooperatives (as above mentioned) coexist with other smaller cooperatives (approximately 20). This fact represents a relative elevated number of entities, taking into account the actual configuration of international supply chains. Nevertheless, this situation is due to the characteristics of a sector largely composed of small scale family farms that have traditionally sought to have more direct contact with cooperative managers and a closer knowledge and relationship with cooperative members. However, new generations of farmers, with more formal education and with a broader vision of their markets, are observed to be in favour of larger cooperatives.

While we have shown that cooperatives have fulfilled the function of consolidating supply in comparison to other companies in the commercial sector (auctions) which market local product and the data shows that Almería cooperatives have managed to surpass the turnover of other competitors by capturing local production, it is important to analyze their financial situation in order to determine viability. We note that the assets and funds of cooperatives are inferior to those of purely commercial companies. This situation combined with high debt and low liquidity may raise doubts about the potential resilience of these organizations during prolonged periods of crisis. However, within the fruit and vegetable sector it is quite common for revenues to fall, a fact which constantly exerts stress on companies’ results while also increasing competition [

36]. This panorama could change as cooperatives start uniting or consolidating more, which has been taking place in recent years, as several second-tier cooperatives now exist which are currently market leaders [

37,

38].

Naturally, it follows that cooperatives display inferior financial results compared to other investor companies, as their objectives go beyond merely maximizing profits. A great deal of profits is passed on through the prices paid to cooperative members. As well, it is important to highlight the impact of cooperatives as generators of local employment. As

Table 4 indicates, cooperatives employ more people, although the cost of each employee is lower than non-cooperative companies, albeit with lower productivity. Cooperatives have shown great concern for incorporating workers in order to foster internal development, despite highly heterogeneous results.

4.2.2. Co-Opetition Relationships among Companies

Within the marketing system of Almería there are relationships of competition and cooperation among companies [

39]. These co-opetition relationships [

40] exist between cooperatives, and between cooperatives and non-cooperative companies, which are mainly auctions. All companies compete for growers, who are the suppliers of product, although cooperative members enjoy more stable relationships with their cooperatives. Cooperatives and non-cooperatives also compete for clients, which are commonly large retailers. At the same time there is cooperation, which takes the form of sector associations, whose main aim is the provision of services that result in mutual benefit, e.g., occupational risk prevention, training, laboratories for analysis, management of grants and subsidies, certification, traceability, food safety, healthy eating programs, lobby, R&D focused on the needs of the farmers and cooperatives, etc., as well as initiatives to form supply cooperatives in order to reduce the cost of inputs: seeds, fertilizers, phytosanitary products or fuel. In Almería alone supply cooperatives have an annual turnover of 300 million Euros. Simplification of logistics operations and transport management can also be seen, although in such case, the impetus comes from large distribution customers, who manage 70% of transits.

4.2.3. Contributions to Knowledge Systems and Employment

Cooperatives have been an important element in the continuing education, training, and work integration of farmers and contracted workers, both in production and auxiliary activities, allowing meaningful participation by growers and workers in the management at all levels of agricultural production. In the last two decades 35% to 40% of contracted workers have been foreign workers, representing a workforce composed of more than 100 nationalities. The cooperatives have been proactive, along with public administrations to promote and manage the contracting of workers in their countries of origin, guaranteeing them collective agreement contract wages and rights to basic living and working conditions, thus addressing the serious issue of exploitation of farm labour. A growing number of foreigners, currently between 8-10%, have become owners of farms and members of cooperatives [

31,

41]. Cooperatives have also proven to be a source of employment for women in the agricultural sector, as 70% of workers are women, with 30% of cooperative agricultural advisors (usually implying a degree in agricultural engineering) also being women [

42]. Work integration programmes for disadvantaged groups is also increasingly common and promoted by the association of cooperatives. In addition, the training of cooperative boards and CEOs and the focus on the governance of cooperatives has taken on increased urgency, with both the cooperative association, COEXPHAL, and the cooperative bank offering specialised cooperative governance and management courses. This is of particular relevance in Spanish and Almería cooperatives, as board members and presidents are active farmers, often lacking any formal management training, and where there is almost non-existent board supervisory entities [

37].

4.2.4. Promotion of Equitable Income

As a result of the Almería family farms and cooperative system involved in the development of employment and entrepreneurship, there has been a relatively equitable distribution of income and the creation of productive agricultural sector, which moved Almería from the last position of per capita income in Spain in the 1950s, to currently approximating the national average. 40% of the provincial GDP is directly or indirectly derived from the agricultural sector [

43]. The economic growth has also resulted in population growth, a trend that is contrary to rural depopulation across Europe. The maintenance of stable and specialized employment and the economic sustainability of many family farms, explained previously, also imply a contribution to the equitable distribution of income by cooperatives in this sector [

41]. In

Figure 2, the distribution of income in the Almería municipalities with horticultural activity, is compared with the national average. (The Gini index is a measure of the income or wealth distribution of a given territory’s residents and is the most commonly used measurement of inequality. A value of zero indicates perfect equality). While the Gini values have risen post crisis in Spain, with the introduction of severe austerity measures (2008), one can still note that the more equal distribution of income in Almería has endured.

4.3. Eco-Social Indicators

The impact of climate change on agriculture and farming systems have been found to be “alarming” by the FAO, which also noted the importance of the urgent need to support small holder farmers in adapting to climate change and the related pressure on scarce resources, such as water, land and energy [

44]. The Almería agricultural sector, already located in an arid climate, with severely stressed aquifers and pollution of aquifers by nitrates and other environmental problems that are commonly associated with vegetable farms for excessive application of irrigation and of nitrogen fertilizers, is acutely aware of the need to address environmental issues and the scarcity of resources. While the climatic conditions of sun and wind allow greenhouse systems without the necessity of heating or cooling, pressure on water and land resources and reliance on petroleum related products is a reality. In addition, through the years, the use of pesticides has proved to be less and less effective in controlling pests and disease. Collective responses to these challenges have been led predominantly by the cooperative sector as now discussed.

4.3.1. Water Management

Almería cooperatives have traditionally shown concern for the shortage of basic resources, such as land and water, and have been instrumental in encouraging efficient usage of these resources. Indeed, in 2009 [

30], greater awareness in this region was observed compared to those from other agricultural areas of Spain. This understanding of the limited available resources has led to a degree of stability in the size of the holdings, and investment efforts have focused on technologies and ecologically sound agricultural practices in order to improve efficiency in the use of resources [

22].

Regarding the judicious usage of water, significant statistical evidence is available. Irrigation communities are the traditional form of organization of family farms for water management, usually in several specific areas of the province. Currently, there exists an increasing collaboration between cooperatives and these communities to introduce innovations and achieve a better efficiency in water use [

45]. The networks of cooperatives-irrigation communities have given rise to what might be termed a culture of correct water usage [

46]. Recent analyses of the water usage and water footprint in Spain (see

Table 5) have revealed efficient use of hydrological resources in Almería [

46].

With respect to other environmental and social sustainability considerations, initial pressure was imposed by the cooperatives’ customers (large European distribution chains), who, in turn, were receiving pressure from consumers that were increasingly concerned about these aspects. Within the supply chain, cooperatives have served to translate and implement these requirements and were the pioneers in the introduction of quality standards. In Almería, the cooperative association initiated a certification company (AgroColor) and also participated in raising awareness and aiding farmers through the complicated certifications, regulations, requirements, and processes. At present, 91% of cooperative members follow certification systems or regulations of good farming practices, mainly GlobalGAP [

47], a protocol required by major customers: Aldi, Edeka, Asda, Lidl, Spar, Tesco, and Sainsbury’s. The demands of these quality regulations are superior to the Maximum Residue Levels (MRL) permitted in Europe. This practice led to a significant reduction in the detection of MRL above legal limits. According to EFSA [

48], Spain, with only 1.09% of samples above MRL, obtained one of the best results in the European Union, registering a rate similar to that of Holland (0.74%), and it significantly lower than those of neighboring Portugal (3.80%) and France (3.04%) or direct competitors like Morocco (3.39%), Italy (1.50%), Israel (4.27%), and Turkey (2.52%).

4.3.2. Decreasing Pesticides

With regard to the use of integrated pest management (IPM), which utilizes auxiliary fauna to control and manage pests, this practice has been in a state of constant evolution. While IPM comprises a competitive tool for sustainable production systems that positively influence the quality of produce and respond to consumer demands, it also has shown to be more effective and less costly for farmers. Almeria became the leader in the successful use of IPM, both in the Mediterranean and worldwide [

49]. Today, 55% of hectares of greenhouses use IPM. In the cases of crops like pepper, this system is used on 100% of farms [

43], surpassing application in competing countries such as Holland and Israel.

Achieving such a status could not have been made possible without the guidance and assistance of cooperatives [

50]. The technical support offered to this sector is quite substantial, directly affecting production levels and crop quality. Cooperatives employ agricultural technicians, who form a knowledge network, meeting twice monthly to share information, flag dangers, and seek solutions together. The cooperative coordination mechanism, as opposed to the market coordination, has had a profound impact on sustainable farming practices and techniques. Given that the cooperative’s goal is to maximise benefits for its members, it is in the cooperatives’ interest to invest in training and research in good agricultural practices and production techniques so as to avoid the need for application of and expenditure on phytosanitary products. A market logic would be more focused on developing an innovative product, rather than an innovative technique.

An example of this market vs. collective logic is demonstrated by the fact that in recent years, the use of IPM has decreased across Europe [

51] largely as a consequence of the research-innovation divide and the lack of research into the use of new insects adapted to emerging disease. Five years ago in Almería, the use of IPM was at 70%, thus the current figure of 55% represents a dramatic descent. This area of research requires a collective response, and could perhaps be considered a “market failure” in terms of R&D: because large firms made less profit as IPM was extended, they are now investing in biological products or “solutions” to be marketed, rather than in researching which cultivation techniques and best practices are most effective. In order to confront these issues, the close relationship between the association of cooperatives, the cooperative bank and the local University of Almería has been leveraged to find collective and specific solutions adapted to the needs of the sector, including jointly starting up and investing in a integrated pest control company, BioColor, specifically suited to local needs.

Turning to the topic of increased demand for organic produce in Europe, the cooperatives responded by converting and expanding the farmland dedicated to these crops. Almeria is the leading province in Andalusia in organic vegetables (37.8%), with a total land area of 3291 ha. (of which 80% use greenhouses, with 2678 ha.), to which neighboring Granada adds an additional 1330 ha. [

52]. Currently, the cultivated area of organic crop represents 10% of the total, with the percentage growing at a rate of over 25% (it should be noted that the conversion period from conventional to organic crop involves a process lasting three years.) The development of ecological practices is not only a response to consumer demand; rather, it is also due to the growing awareness of family farms and their corresponding cooperatives. For example, one of the most successful organic producers in the area, BioSabor, began after a group of related family farmers felt that their cooperative was not adequately supporting organic production. By establishing their own cooperative, they have now become market leaders in organic produce and the nutritional and health value of their products. The transgenerational character of cooperatives and the efforts to maintain environmental sustainability in the family farms, who produce for local markets as well, has led to more environmentally sustainable production.

4.3.3. Waste Management

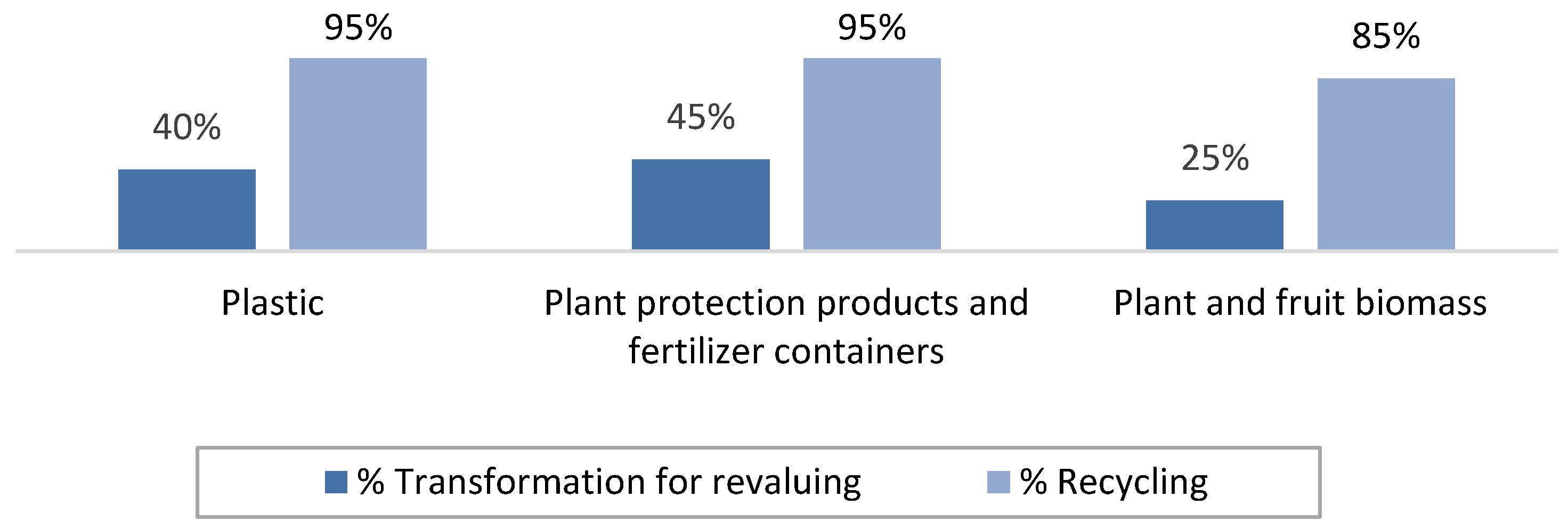

Evidence of the sector’s decreasing ecological footprint is also found in the Rural Hygiene Plans for the treatment of residues as implanted by the family farms and cooperatives with the support of local institutions. Plant waste generated in Almeria has great potential to be reutilized following the principles of circular economy [

53]. Cooperatives are taking the initiative in this regard, assuming the role of proactive entities and even co-participants in business initiatives aimed at recycling and/or harnessing renewable energy. Growers deposit different types of residues in containers that are placed conveniently close to their greenhouses for subsequent collection and treatment. Certain auxiliary enterprises have also been established to manage and reutilize the waste that is generated by horticultural activity (in some cases with public participation and private participation from cooperative associations). Currently, about 90% of the sector’s waste is recycled (see

Figure 3), that mainly includes plastics, vegetable residues, and packaging [

41,

54]. Over 95% of the plastics are collected from the farms of cooperative members, which are transformed for either reuse or revaluing (40%).

4.3.4. Energy

One of the major concerns of the current generation of growers resides in improving the use of resources and infrastructures, and in particular, exploiting renewable energy. Several R&D projects are being carried out in collaboration with local research centers along these lines, including the cogeneration of CO

2 and solar energy in greenhouses [

55], solar desalinization plants connected to greenhouses with precision irrigation [

56], and multi-actor projects such as the Internet of Food and Farm (IoF2020) European large scale pilot, FERTINNOWA thematic network on fertirrigation, etc. Multi-actor R&D driven by the cooperative association and the cooperative bank, with collaborations with public and private research centers, and the involvement of the public administration has been seen as a strategic necessity.

5. Conclusions

In this paper, we have taken the Almería cooperatives as a demonstrative case of cooperative longevity and survival, in order to observe the evolution and processes of adaptation to the distinct economic, social, and environmental demands of a broad range of member-owners.

Cooperativism has shown to be an effective organisational coordination mechanism for small-scale farmers in Almería. In spite of the important changes that have occurred in the agrifood sector in the last decades, the cooperatives have demonstrated their capacity to adapt and pivot and meet the changing needs of both members and the community and challenges of production and distribution. Global market changes have been very influential in marking the necessity for change, but as well, the demands of the farming community, members, and society in general have resulted in social and environmental factors being as much a priority as economic aspects.

Regarding socio-economic aspects, cooperatives have become the drivers of a business sector that has allowed family-based growers to access the market. From a local point of view, these organizations have managed to consolidate the supply thanks to the economic and social benefits growers derive from belonging to these associations. Cooperatives show greater concern for keeping and satisfying the growers, via market prices, allowing their economic sustainability and maintaining an equity income.

As far as eco-social aspects are concerned, cooperatives have made substantial efforts as a driver of innovation in the production and commercial sector and the improvements to production and adaptation to demand could not have been implemented so swiftly without the presence of these organizations. At the same time, they play a role in the transmission of social responsibility and awareness for efficient use of natural resources to the various generations.

The longevity and survival of the cooperatives are linked to their constant and rapid adaptation to crises in which the sector finds itself or to the challenges it faces. For example, if the cooperatives had not implemented Integrate Pest Management swiftly and not had the ability to affect change so rapidly through its network, the export opportunities to major markets, which represent 70% of sales, would have been closed. Other examples include facilitating demands of certification and mediating the exponential demand for ecological production. Without the mediation and facilitation of cooperatives to manage such transformations, small farmers would not be able to survive and compete, and conversely, without small farmers adopting sustainable practices, marketing cooperatives would not survive in Almería.

In conclusion, the persistence or longevity of cooperatives could be a response to a multitude of diverse factors, which need to be approached and analysed in the context of agricultural systems. This study is limited to the description of the context and identification of different factors which have determined the development and longevity of cooperative in the referenced sector as a whole. Accordingly, future research should be conducted in quantitative and/or qualitative analysis (e.g., taking a representative sample of cooperatives) to determine the more in-depth influence of these socio-economic and eco-social factors on this cooperative persistence. The Almería case may be considered unique in many of its features, but it also serves to underline the many different sustainability components that may be considered relevant in future cooperative studies on resilience and longevity.

{kind=link}

{kind=link}

{kind=link}