Sustainability and Ethics in the Process of Price Determination in Financial Markets: A Conceptual Analysis

Abstract

:1. Introduction

2. Literature Revision

2.1. Ethics and Finance

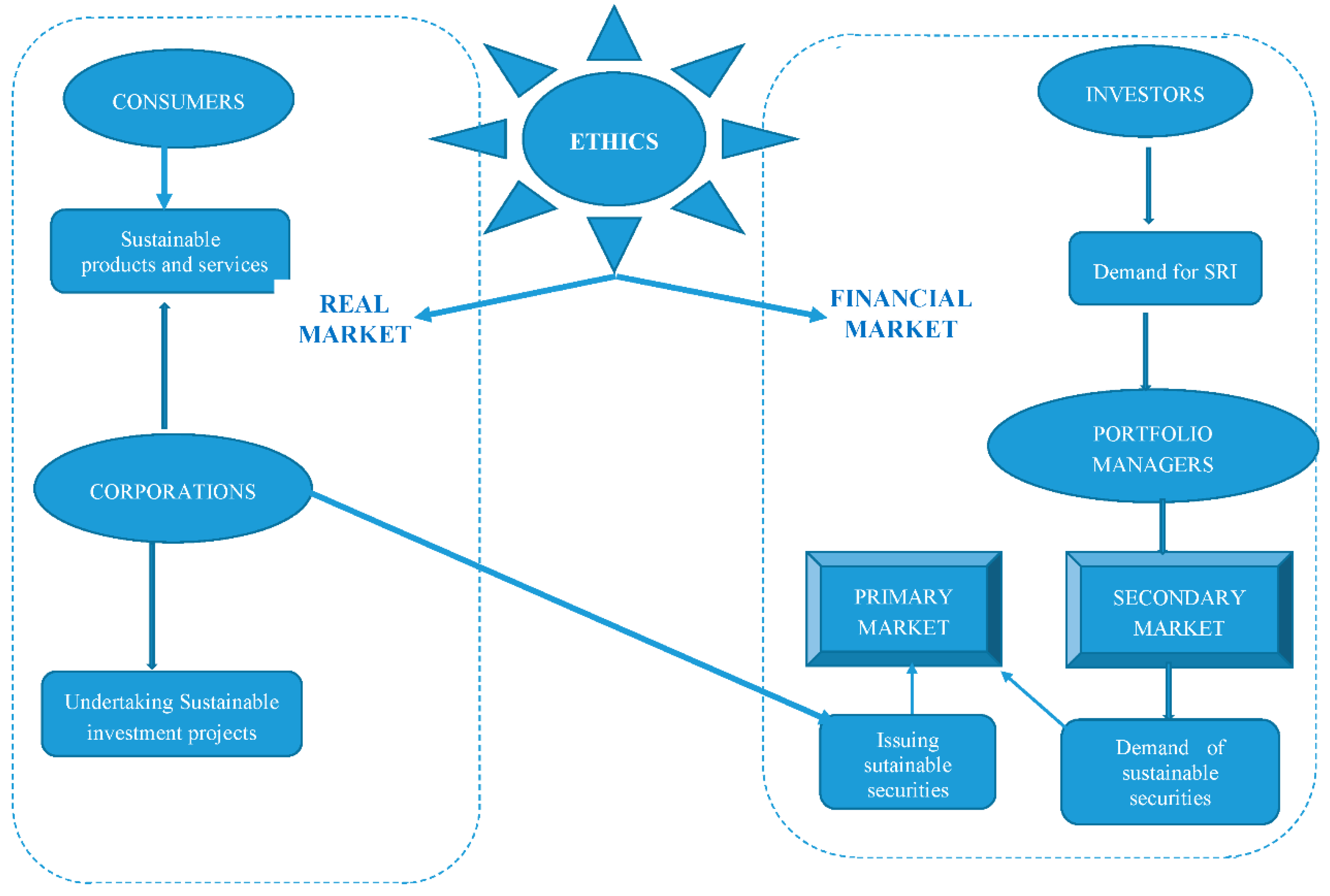

2.2. Corporate Social Responsibility and Socially Responsible Investment: Links with Capital Markets

2.3. Ethics vs. Speculation in Corporate Social Responsibility and Socially Responsible Investing

3. Creating Sustainable Value in the Light of SDGs

3.1. Sustainability and Value Creation

3.2. The SDGs and the Pillars of Sustainability

4. Financial Markets as a Support for Sustainability

4.1. The Capacity of Financial Markets to Contribute to the SDGs

4.2. Irrational Behavior and Short-Termism as Threats for Sustainable Efficiency

4.2.1. Irrational Behavior

4.2.2. Short-Termism

- (a)

- It exists a relevant parallelism between SDGs and long-term value creation. They reinforce each other.

- (b)

- SDGs cannot be achieved if short-term strategies pervade the corporate world and capital markets.

- (c)

- This parallelism remarks the relevance of the SDG 17, “strengthen the means of implementation and revitalise the global partnership for sustainable development” because it shows that corporations can be and should be an active part in the achievement of SDGs, together with the sustainable investment strategies in capital markets that must support them.

4.3. The Institutional Support to Sustainable Efficient Markets

5. Ethics and Sustainability in the Process of Price Determination

5.1. The Pluralist Ethics of Economics and Finance

5.2. Ethics and Sustainability in the Financial System

- (a)

- Macro or systemic: the nature and performance of total political economics.

- (b)

- Intermediate: the conduct of collective business actors.

- (c)

- Organizational: policies and actions of specific firms.

- (d)

- Individual: behavior of identifiable human actors.

5.3. Reputation and performance measurement

6. Discussion and Conclusions

Author Contributions

Acknowledgments

Conflicts of Interest

References

- Margolis, E.; Laurence, S. Concepts. The Stanford Encyclopedia of Philosophy. Edward, N.Z., Ed.; 2014. Available online: https://plato.stanford.edu/archives/spr2014/entries/concepts/ (accessed on 20 April 2018).

- Yehezkel, G. A Model of Conceptual Analysis. Metaphilosophy 2005, 36, 668–687. [Google Scholar] [CrossRef]

- Jackson, F. From Metaphysics to Ethics: A Defence of Conceptual Analysis; Oxford University Press: Oxford, UK, 2000. [Google Scholar] [CrossRef]

- Malkiel, B.G. The Efficient Market Hypothesis and Its Critics. J. Econ. Perspect. 2003, 17, 59–82. [Google Scholar] [CrossRef]

- Shiller, R.J. From Efficient Markets Theory to Behavioral Finance. J. Econ. Perspect. 2003, 17, 83–104. [Google Scholar] [CrossRef]

- Simon, H.A. Rationality as process and as product of thought. Am. Econ. Rev. 1978, 68, 1–16. [Google Scholar]

- Global Sustainable Investment Alliance. Available online: http://www.gsi-alliance.org/ (accessed on 2 April 2018).

- Boulding, K.E. Economics as a moral science. Am. Econ. Rev. 1969, 59, 1–12. [Google Scholar]

- Arrow, K.J. Some Failures of the Economy. In Performance & Progress; Rangan, S., Ed.; Oxford University Press: Oxford, UK, 2015; pp. 38–48. ISBN 978-0-19-879957-3. [Google Scholar]

- Sen, A. Progress and Public Reasoning. In Performance & Progress; Rangan, S., Ed.; Oxford University Press: Oxford, UK, 2015; pp. 151–173. ISBN 978-0-19-879957-3. [Google Scholar]

- Burbidge, D. Space for virtue in the economics of Kenneth J. Arrow, Amartya Sen and Elinor Ostrom. J. Econ. Methodol. 2016, 23, 396–412. [Google Scholar] [CrossRef]

- Sandel, M.J. What Money Can’t Buy: The Moral Limits of the Market; Farrar, Strauss and Giroux: New York, NY, USA, 2012; ISBN 0374533652. [Google Scholar]

- Sandel, M.J. Market Reasoning as Moral Reasoning: Why Economists Should Re-engage with Political Philosophy. J. Econ. Perspect. 2013, 27, 121–140. [Google Scholar] [CrossRef]

- Benatar, S.R.; Daar, A.S.; Singer, P.A. Global health ethics: the rationale for mutual caring. International Affairs 2003, 79, 107–138. [Google Scholar] [CrossRef]

- Okrent, D.; Pidgeon, N. Dilemmas in Intergenerational versus Intragenerational Equity and Risk Policy. Risk Analysis 2000, 20, 759–762. [Google Scholar] [CrossRef] [PubMed]

- Kermisch, C.; Taebi, B. Sustainability, Ethics and Nuclear Energy: Escaping the Dichotomy. Sustainability 2017, 9, 446. [Google Scholar] [CrossRef]

- Wight, J.B. Economics within a Pluralist Ethical Tradition. Rev. Soc. Economy 2014, 72, 417–435. [Google Scholar] [CrossRef]

- Wight, J.B. Ethics in Economics: An Introduction to Moral Frameworks; Stanford University Press: Stanford, CA, USA, 2015; ISBN 978-0-8047-9453-4. [Google Scholar]

- Dembinski, P.H. Ethics and Responsibility in Finance; Routledge: Abingdon, UK, 2017; ISBN 978-1-138-63790-0. [Google Scholar]

- Shiller, R.J. Finance and the Good Society; Princeton University Press: Princeton, CA, USA, 2012; ISBN 978-0-691-15488-6. [Google Scholar]

- Gatewood, R.D.; Carroll, A.B. Assessment of Ethical Performance of Organization Members: A Conceptual Framework. Acad. Manag. Rev. 1991, 16, 667–690. [Google Scholar] [CrossRef]

- Hellsten, S.; Mallin, C. Are “Ethical” or “Socially Responsible” Investments Socially Responsible? J. Bus. Ethics 2006, 66, 393–406. [Google Scholar] [CrossRef]

- Dam, L.; Scholtens, B. Toward a theory of responsible investing: On the economic foundations of corporate social responsibility. Resour. Energy Econ. 2015, 41, 103–121. [Google Scholar] [CrossRef]

- Mackey, A.; Mackey, T.B.; Barney, J.B. Corporate Social Responsibility and firm performance: Investor preferences and corporate strategies. Acad. Manag. Rev. 2007, 32, 817–835. [Google Scholar] [CrossRef]

- Heinkel, R.; Kraus, A.; Zechner, J. The Effect of Green Investment on Corporate Behavior. J. Financ. Quant. Anal. 2001, 36, 431–449. [Google Scholar] [CrossRef]

- Merton, R.C. A Simple Model of Capital Market Equilibrium with Incomplete Information. J. Financ. 1987, 42, 483–510. [Google Scholar] [CrossRef]

- Ballestero, E.; Bravo, M.; Pérez-Gladish, B.; Arenas-Parra, M.; Plà-Santamaria, D. Socially Responsible Investment: A multicriteria approach to portfolio selection combining ethical and financial objectives. Eur. J. Oper. Res. 2012, 216, 487–494. [Google Scholar] [CrossRef]

- Bilbao-Terol, A.; Arenas-Parra, M.; Canal-Fernandez, V.; Bilbao-Terol, C. Selection of Socially Responsible Portfolios Using Hedonic Prices. Oper. Res. Proc. 2012, 28, 51–56. [Google Scholar] [CrossRef]

- Xiao, Y.; Faff, R.; Gharghori, P.; Min, B.-K. The Financial Performance of Socially Responsible Investments: Insights from the Intertemporal CAPM. J. Bus. Ethics 2015, 146, 353–364. [Google Scholar] [CrossRef]

- Lee, D.D.; Faff, R.W. Corporate Sustainability Performance and Idiosyncratic Risk: A Global Perspective. Financ. Rev. 2009, 44, 213–237. [Google Scholar] [CrossRef]

- El Ghoul, S.; Guedhami, O.; Kwok, C.C.Y.; Mishra, D.R. Does corporate social responsibility affect the cost of capital? J. Bank. Financ. 2011, 35, 2388–2406. [Google Scholar] [CrossRef]

- Michaels, A.; Grüning, M. Relationship of corporate social responsibility disclosure on information asymmetry and the cost of capital. J. Manag. 2017, 28, 251–274. [Google Scholar] [CrossRef]

- Goss, A.; Roberts, G.S. The impact of corporate social responsibility on the cost of bank loans. J. Bank. Financ. 2011, 35, 1794–1810. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-Analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Von Wallis, M.; Klein, C. Ethical requirement and financial interest: A literature review on socially responsible investing. Bus. Res. 2014, 8, 61–98. [Google Scholar] [CrossRef]

- Junkus, J.; Berry, T.D. Socially responsible investing: A review of the critical issues. Manag. Financ. 2015, 41, 1176–1201. [Google Scholar] [CrossRef]

- Revelli, C.; Viviani, J.-L. Financial performance of socially responsible investing (SRI): What have we learned? A meta-analysis. Bus. Ethics 2014, 24, 158–185. [Google Scholar] [CrossRef]

- Derwall, J.; Koedijk, K.; Ter Horst, J. A tale of values-driven and profit-seeking social investors. J. Bank. Financ. 2011, 35, 2137–2147. [Google Scholar] [CrossRef]

- Døskeland, T.; Pedersen, L.J.T. Investing with Brain or Heart? A Field Experiment on Responsible Investment. Manag. Sci. 2016, 62, 1632–1644. [Google Scholar] [CrossRef]

- Riedl, A.; Smeets, P. Why Do Investors Hold Socially Responsible Mutual Funds? J. Financ. 2017, 72, 2505–2550. [Google Scholar] [CrossRef]

- Griskevicius, V.; Tybur, J.M.; Van den Bergh, B. Going green to be seen: Status, reputation, and conspicuous conservation. J. Personal. Soc. Psychol. 2010, 98, 392–404. [Google Scholar] [CrossRef] [PubMed]

- Barnea, A.; Heinkel, R.; Kraus, A. Green investors and corporate investment. Struct. Chang. Econ. Dyn. 2005, 16, 332–346. [Google Scholar] [CrossRef]

- Mackenzie, C.; Rees, W.; Rodionova, T. Do responsible investment indices improve corporate social responsibility? FTSE4Good’s impact on environmental management. Corp. Gov. 2013, 21, 495–512. [Google Scholar] [CrossRef]

- Gond, J.-P.; Piani, V. Enabling Institutional Investors’ Collective Action. Bus. Soc. 2012, 52, 64–104. [Google Scholar] [CrossRef]

- Generation Foundation. Available online: https://www.genfound.org/ (accessed on 2 April 2018).

- Adler, T.; Kritzman, M. The Cost of Socially Responsible Investing. J. Portf. Manag. 2008, 35, 52–56. [Google Scholar] [CrossRef]

- Revelli, C. Socially responsible investing (SRI): From mainstream to margin? Res. Int. Bus. Financ. 2017, 39, 711–717. [Google Scholar] [CrossRef]

- Revelli, C. Re-embedding financial stakes within ethical and social values in socially responsible investing (SRI). Res. Int. Bus. Financ. 2016, 38, 1–5. [Google Scholar] [CrossRef]

- Bosch-Badia, M.-T.; Montllor-Serrats, J.; Tarrazon-Rodon, M.-A. Corporate Social Responsibility: A Real Options Approach to the Challenge of Financial Sustainability. PLoS ONE 2015, 10, e0125972. [Google Scholar] [CrossRef] [PubMed]

- Stern, N. The Economics of Climate Change. American Economic Review 2008, 98, 1–37. [Google Scholar] [CrossRef]

- Singer, P. Ethics and Climate Change: A Commentary on MacCracken, Toman and Gardiner. Environ.Values 2006, 15, 415–422. [Google Scholar] [CrossRef]

- Singer, P. One World Now: The Ethics of Globalization; Yale University Press: New Haven, CT, USA, 2016; ISBN 978-0-300-19605-4. [Google Scholar]

- Harris, J.M.; Rauch, B. Environmental and Natural Resource Economics, 4th ed.; Routledge: Abingdon, UK, 2018; ISBN 978-1-138-65947-6. [Google Scholar]

- Black, F. Noise. J. Financ. 1986, 41, 528–543. [Google Scholar] [CrossRef]

- De Bondt, F.M.; Thaler, R.H. Financial Decision-Making in Markets and Firms: A Behavioral Perspective. In Handbooks in Operations Research and Management Science; Elsevier: Amsterdam, The Netherlands, 1995; pp. 385–410. ISBN 978-0-444-89084-9. [Google Scholar]

- Shleifer, A. Inefficient Markets; Oxford University Press: Oxford, UK, 2000; ISBN 9780198292272. [Google Scholar] [CrossRef]

- Hirshleifer, D. Behavioral Finance. Ann. Rev. Financ. Econ. 2015, 7, 133–159. [Google Scholar] [CrossRef]

- Barberis, N.; Thaler, R.H. A Survey of Behavioral Finance. In Advances in Behavioral Finance, Volume II; Thaler, R.H., Ed.; Princeton University Press: Princenton, NJ, USA, 2005; pp. 1–76. ISBN 9781400829125. [Google Scholar]

- Malkiel, B. A Random Wak Down Wall Street; W.W. Norton: New York, NY, USA, 2015; ISBN 978-0-393-24611-7. [Google Scholar]

- Charness, G.; Gneezy, U. Portfolio Choice and Risk Attitudes: An Experiment. Econ. Inq. 2010, 48, 133–146. [Google Scholar] [CrossRef]

- Dunlap, R.E.; Jacques, P.J. Climate Change Denial Books and Conservative Think Tanks. Am. Behav. Sci. 2013, 57, 699–731. [Google Scholar] [CrossRef] [PubMed]

- Janis, I. Groupthink. IEEE Eng. Manag. Rev. 2008, 5, 36. [Google Scholar] [CrossRef]

- Fielding, K.S.; Hornsey, M.J.; Swim, J.K. Developing a social psychology of climate change. Eur. J. Soc. Psychol. 2014, 44, 413–420. [Google Scholar] [CrossRef]

- Kahneman, D.; Tversky, A. Prospect Theory: An Analysis of Decision under Risk. Econometrica 1979, 47, 263–291. [Google Scholar] [CrossRef]

- Thaler, R.H. Misbehaving: The Making of Behavioral Economics; W.W. Norton: New York, NY, USA, 2016; ISBN 039335279X. [Google Scholar]

- Haldane, A.G. The Costs of Short-termism. Politic. Q. 2015, 86, 66–76. [Google Scholar] [CrossRef]

- Rappaport, A. Saving Capitalism from Short-Termism; McGraw-Hill: New York, NY, USA, 2012; ISBN 978-0-07-173636-7. [Google Scholar]

- Goldin, I.; Lamy, P. Overcoming Short-Termism: A Pathway for Global Progress. Wash. Q. 2014, 37, 7–24. [Google Scholar] [CrossRef]

- Oxford Martin Commission. Now for the Long Term; The Report of the Oxford Martin Commission for Future Generations; University of Oxford: Oxford, UK, 2013; ISBN 978-0-9927411-1-2. [Google Scholar]

- Maimbo, S.M.; Zadek, S. Roadmap for a Sustainable Financial System; United Nations Environment Programme: Nairobi, Kenya; The World Bank Group: Washington, DC, USA, 2017; Available online: http://wedocs.unep.org/bitstream/handle/20.500.11822/22282/Roadmap_Sustainable_Financial_System_ES.pdf?sequence=1&isAllowed=y (accessed on 10 May 2018).

- Bosch-Badia, M.-T.; Montllor-Serrats, J.; Tarrazon-Rodon, M.-A. Efficiency and Sustainability of CSR Projects. Sustainability 2017, 9, 1714. [Google Scholar] [CrossRef]

- UNEP Finance Initiative, UN Global Compact. Principles for Responsible Investment. 2017. Available online: https://www.unpri.org/download?ac=1534 (accessed on 2 April 2018).

- Principle for Responsible Investment. Sustainable Financial System: Nine Priorities to Address. 2017. Available online: https://www.unpri.org/Uploads/k/f/q/sustainable-financial-system-nine-priority-conditions-to-address.pdf (accessed on 5 May 2018).

- Collomb, B. Trust and Power; Performance & Progress; Rangan, S., Ed.; Oxford University Press: Oxford, UK, 2015; pp. 462–475. ISBN 978-0-19-879957-3. [Google Scholar]

- Shafer-Landau, R. Ethical Theory: An Anthology; Wiley-Blackwell: Chichester, UK, 2013. [Google Scholar]

- Blaug, M. Is competition such a good thing? Static efficiency versus dynamic efficiency. Rev. Ind. Organ. 2001, 19, 37–48. [Google Scholar] [CrossRef]

- Arrow, K.J.; Dasgupta, P.; Goulder, L.H.; Mumford, K.J.; Oleson, K. Sustainability and the measurement of wealth. Environ. Dev. Econ. 2012, 17, 317–353. [Google Scholar] [CrossRef]

- Barry, B. Sustainability and Intergenerational Justice. In Fairness and Futurity; Oxford University Press: Oxford, UK, 1999; pp. 3–117. [Google Scholar]

- Kermisch, C. Can today’s decisions really be future-proofed? Nature 2016, 530, 383. [Google Scholar] [CrossRef] [PubMed]

- Epstein, E.M. Business ethics, Corporate Good Citizenship and the Corporate Social Policy Process: A view from the United States. J. Bus. Ethics 1989, 8, 583–595. [Google Scholar] [CrossRef]

- Jacquet, J.; Jamieson, D. Soft but significant power in the Paris Agreement. Nature Climate Change 2016, 6, 643–646. [Google Scholar] [CrossRef]

- Taebi, B.; Safari, A. On Effectiveness and Legitimacy of “Shaming” as a Strategy for Combatting Climate Change. Sci. Eng. Ethics 2017, 23, 1289–1306. [Google Scholar] [CrossRef] [PubMed]

- Principles for Responsible Investment. Shifting Perceptions: ESG, Credit Risk, and Ratings. Part 1. 2017. Available online: https://www.unpri.org/fixed-income/shifting-perceptions-esg-credit-risk-and-ratings-part-1-the-state-of-play/78.article (accessed on 5 May 2018).

- Anand, S.; Sen, A. Human Development and Economic Sustainability. World Dev. 2000, 28, 2029–2049. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Creating Shared Value. Harv. Bus. Rev. 2011, 89, 2–17. [Google Scholar]

- Bowles, S.; Polanía-Reyes, S. Economic Incentives and Social Preferences: Substitutes or Complements? J. Econ. Lit. 2012, 50, 368–425. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Goal/Financial Sustainability | Environmental Sustainability | Social Sustainability | Financial Sustainability | Value Creation |

|---|---|---|---|---|

| No poverty (1) | ✓ | ✓ | ✓ | |

| Zero hunger (2) | ✓ | ✓ | ✓ | |

| Good health and well-being (3) | ✓ | ✓ | ||

| Quality education (4) | ✓ | ✓ | ||

| Gender equality (5) | ✓ | ✓ | ||

| Clean water and sanitation (6) | ✓ | ✓ | ||

| Affordable and clean energy (7) | ✓ | ✓ | ✓ | |

| Decent work and economic growth (8) | ✓ | ✓ | ✓ | |

| Industry, innovation, and infrastructure (9) | ✓ | ✓ | ||

| Reduced inequalities (10) | ✓ | ✓ | ||

| Sustainable cities and communities (11) | ✓ | ✓ | ||

| Responsible consumption and production (12) | ✓ | ✓ | ✓ | |

| Climate action (13) | ✓ | ✓ | ||

| Life below water (14) | ✓ | ✓ | ||

| Life on land (15) | ✓ | ✓ | ||

| Peace, justice, and strong institutions (16) | ✓ | ✓ |

| RLTP | SDGs |

|---|---|

| Do not manage earnings or provide earnings guidance (i.e., do not manipulate earnings and their expectations). | SDGs cannot be reached without fair information. |

| Select strategies that maximize long-term value, even at the expense of lowering near-term earnings. | SDG 9: Industry, innovation, and infrastructure. |

| Instill a customer-equity mindset through the processes of planning, decision making, and performance evaluation (i.e., value customers long-term revenues). | SDG 12: Responsible consumption and production. For the energy industry: SDG 7: Affordable and clean energy |

| Manage all business-existing, emerging, and embryonic, without regard to their stage of maturity with a single-minded focus on creating long-term value. | Manage all business with sustainability in mind. SDG 8: Decent work and economic growth. SDG 5: Gender equality. |

| Retain only assets that maximize value | SDG 8: Decent work and economic growth. SDG 12 |

| Reward CEOs and other senior executives for delivering superior long-term value. | Reward CEOs and other senior executives for implementing the SDGs as a way of preparing the corporation for long-term challenges. Control sustainability risks. SDG 12 SDG 16: Strong institutions (peace, justice, and strong institutions). |

| Require CEOs and other senior executives to hold a meaningful and continuing stake in the company’s equity. | Force CEOs to have a long-term commitment with the corporation. SDG 12 |

| Reward operating-unit executives for delivering superior multiyear value. | SDG 8 |

| Reward operating-unit employees for delivering superior performance on the key drivers of long-term value that they influence directly. | SDG 4: Quality education. (have a well-prepared staff and provide facilities for continuous training). SDG 12 |

| Make acquisitions that maximize expected long-term value. | SDG 9 |

| Return cash to shareholders when there are no value-creating opportunities to invest in the business. | SDG 12 |

| Provide investors with value-relevant information. | Including information on sustainability |

| Possible additional social contributions through long-term value creation and CSR initiatives: SDG 1: No poverty SDG 2: Zero hunger SDG 3: Good health and well-being SDG 4: Quality education SDG 6: Clean water and sanitation | |

| Possible additional environmental contributions through value creation and CSR initiatives: SDG 6: Clean water and sanitation SDG 13: Climate action SDG 14: Life below water SDG 15: Life on land | |

| SDGs beyond corporations: SDG 10: Reduced inequalities SDG 11: Sustainable cities and communities SDG 16: Peace justice and strong institutions | |

| Principle | Field | |

|---|---|---|

| 1 | We will incorporate ESG issues into investment analysis and decision-making processes. | Investment management |

| 2 | We will be active owners and incorporate ESG issues into our ownership policies and practices. | Control ESG performance through shareholders’ activism |

| 3 | We will seek appropriate disclosure on ESG issues by the entities in which we invest. | Information requirement |

| 4 | We will promote acceptance and implementation of the Principles within the investment industry. | Marketing/promotion |

| 5 | We will work together to enhance our effectiveness in implementing the Principles | Self-performance measurement |

| 6 | We will each report on our activities and progress towards implementing the Principles | Information on performance |

| Priority Conditions to Address | Investors | Portfolio Managers | Regulators | Gatekeepers | Companies | |

|---|---|---|---|---|---|---|

| 1 | Short-term investment objectives | x | ||||

| 2 | Attention to beneficiary interests (focus on financial returns) | x | x | |||

| 3 | Policy markets influence on markets | x | ||||

| 4 | Capture of government policy by vested interests | x | x | |||

| 5 | Influence of brokers, rating agencies, advisors and consultants | |||||

| 6 | Principal-agent relationships in the investment chain | x | x | x | ||

| 7 | Cultures of financialization and rent-seeking in market actors | x | x | x | x | |

| 8 | Investment objectives misaligned with sustainable economic development | x | x | |||

| 9 | Investor processes, practices, capacities and competencies | x |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bosch-Badia, M.-T.; Montllor-Serrats, J.; Tarrazon-Rodon, M.-A. Sustainability and Ethics in the Process of Price Determination in Financial Markets: A Conceptual Analysis. Sustainability 2018, 10, 1638. https://doi.org/10.3390/su10051638

Bosch-Badia M-T, Montllor-Serrats J, Tarrazon-Rodon M-A. Sustainability and Ethics in the Process of Price Determination in Financial Markets: A Conceptual Analysis. Sustainability. 2018; 10(5):1638. https://doi.org/10.3390/su10051638

Chicago/Turabian StyleBosch-Badia, Maria-Teresa, Joan Montllor-Serrats, and Maria-Antonia Tarrazon-Rodon. 2018. "Sustainability and Ethics in the Process of Price Determination in Financial Markets: A Conceptual Analysis" Sustainability 10, no. 5: 1638. https://doi.org/10.3390/su10051638

APA StyleBosch-Badia, M.-T., Montllor-Serrats, J., & Tarrazon-Rodon, M.-A. (2018). Sustainability and Ethics in the Process of Price Determination in Financial Markets: A Conceptual Analysis. Sustainability, 10(5), 1638. https://doi.org/10.3390/su10051638