1. Introduction

One of the keys to achieving prosperity in urban agglomerations is sustainable urban and territorial development. A desired sustainable development implies relations between human communities in the environment to occur not by physical environment quantitative or uncontrolled growth but through qualitative improvements favoring development over growth. Here lays the difference between growth and development: there can be no undefined and continuous urban growth, but development can be continuous, and this would be a territorial and sustainable urban development [

1]. In a development with minimal physical growth, it is possible to avoid compromising resources of future generations. The Sustainable Urban and Territorial Development (SUTD) implies abandoning the idea of unlimited urban growth in favor of a concept of urban regeneration, in such a way that new urban developments will be well justified. Nevertheless, to achieve SUTD, its inspiring principles need to be embodied in the instruments of territorial and urban planning with a strong commitment by all the involved actors [

2,

3,

4].

Also, the concept of the Circular Green Economy is gaining attention in the field of sustainable planning. The main goal of a circular green economy is to achieve environmental sustainability, which, at a local level, is performed through the transition to more sustainable cities. Therefore, the SUTD model should involve sustainable urban planning and limit the effects and impacts that urban planning can represent over the environment. This would be the contribution that can achieve urban circular economy towards sustainability [

5]. In this sense, one of the essential requirements to achieve more sustainable, inclusive, and equitable cities would have to go through a proper allocation of land use and adopting innovative and flexible approaches leading to adequate services to the inhabitants [

6].

Thus, one of the principles of the SUTD is to present public policies related to the established legislation of land use regulation [

7] (

Figure 1). Sustainability, as a global concept, will depend on the sustainability of cities and other factors [

8]. In this regard, it is widely accepted that the incorporation into the city of newly urbanized lands will have an impact in the economic sustainability of municipalities and their local finances, in terms of both expenses incurred since the start of the new developments, and expected taxation that local councils may apply on increasing local property. Contextually, to achieve economic sustainability in the long term, there must be a balance between expenditures that should consider the effect of councils and incomes. These will be based on the value that the administration grants to specific land, so it is critical to set a fair contribution system according to its real value [

9], particularly in times of economic crisis and/or recession periods.

The development of municipal planning must ensure the economic sustainability of municipalities, and therefore be referred and considered in the documents that comprise it. The costs of infrastructure and non-residential equipment required by a sustainable city must be identified and considered in new urban developments; determining the long-term economic sustainability for municipal treasuries and public services is pivotal to meet a guaranteed urban growth [

10,

11,

12].

Soil is a scarce, limited, and non-renewable natural resource [

13,

14], and is central to territorial and urban planning instruments to manage land use, which should be developed according to sustainable principles to reach integrated planning. Within the process of urban planning, the establishment of land values both by assigning its applications and building intensities, implies the attribution of economic value to land through planning objects, and therefore providing those lands with certain capital gains.

Consequentially, the generation of capital gains is carried out in a reciprocal manner, since when administrations promote infrastructure and community facilities, there is also an increase in value of surrounding lands [

15]. However, in some exceptions (e.g., the core of the economic crisis of 2008), such land valuation did not occur until the area and their surroundings developed considerably. Such a scenario is due to the land value being deeply connected to the final real estate product value. In those cases, the scarcity of sales, along with low real estate values, can have a direct influence on the value of undeveloped land.

On the other hand, there is also public participation in generated capital incomes, the necessary support for effective financing instruments, strengthening municipal finance and local tax systems through fair taxes over the capital gains [

16,

17] aimed at returning the land value to the benefit of the community, and allowing economic development of the environment through the improvement of facilities and infrastructures. For the determination of these gains, it is essential to perform a correct economic valuation of land with urban development features. Actual assessment that is made over a piece of land is carried out based on the economic benefit coming from the adoption of sustainable land use management and compared with the costs that will be generated [

18].

In fact, there are models that value the land through sustainability indicators [

19], on explanatory theories of the space formation of land valuation, and depending on accessibility, space qualification or space social hierarchy [

20,

21]. However, the fact remains that to determine land valuation with urban development, it must be performed using models that quantify economically its real and reasonable value, which will depend on the realization of land use rights [

22,

23,

24,

25,

26,

27].

The methods for land valuation must be rigorous and prudent, preventing its results from causing tensions in the market, i.e., a new housing crisis affecting banks, in the long run, and eventually extending into the economy [

28]. Therefore, it would be desirable that bullish cycles in the real estate market are contained and balanced [

29]. Therefore, the criteria applied in valuation methods must be guided to prevent results rising to speculative practices. The value of soil has an influence in central elements of municipal funding [

30], either through obtaining part of the generated capital gains [

15], or through real estate taxes, or even through tax figures on vacant ground [

31]. Therefore, valuation methods should be vested with transparency and objectivity that make them easily understood by the taxpayer [

32].

In this regard, there are studies on the change which occurs in land value with urbanizing features, unfolding from the land without urban developing power until it is fully built, with repercussions that land value has on the final real estate product [

7,

33,

34]. However, these changes in land values only occur once it has finished construction, independent of urban development, ending when the land is already urbanized; in fact, they are actually linked to the evolution of the real estate market.

The novelty of this work consists in the presentation of the analysis of impact that different stages of urban planning development [

35] have on the gradual increase in land value, depending on the different states of urbanization that are acquired as land develops. In this regard, the impact of already developed land is not considered, once the changes in value that may occur in it are produced by the change in the value of the complete real estate product, due to market fluctuations, but not due to a change in urban planning, which would be fully developed in the stage of urbanized land. The study has been carried out on the change in value of specific land based on data collected by urban planning tools. To calculate the land value at each state of urbanization, the free cash flow discount model has been used, which is one of the most widely used methods (across different countries) to value investment projects [

36,

37].

The land value in the initial state corresponds to the delimited developable land, without any detailed planning. The following state corresponds to the land on which a detailed arrangement is established; the third is related to an action unit with approved re-parceling, and lastly, the value is calculated in the final state, corresponding to fully urbanized land. With these results, the calculated values are compared, in the different states, to the value corresponding to the land in the final state.

The relevance of this study lies in establishing changes in relative value that are produced at each stage (state) of urban development, comparing them with value acquired by the land when fully developed, and enabling the extrapolation of value to any land in the nearby environment, where the urban features and conditions are manifestly similar. The present study hopes to be a useful tool to perform massive assessments, in which it might be necessary to provide valuation to land that is not urbanized or in which it is necessary to carry out urbanization actions—when they are not yet fully urbanized or are developing or unconsolidated—based on the value impact of urbanized land.

2. Materials and Methods

2.1. Study Area

The proposed methodology has been applied in the valuation of a specific land endowed with urban use. The area is in a region of southern Europe—the EUROACE is a Euro-Region located in the Iberian Peninsula that comprises the Portuguese regions of

Alentejo and Centro and the Spanish region of Extremadura—and inserted in a Euro-City, the Euro-City Elvas-Badajoz-Campo-Maior (

Figure 2) [

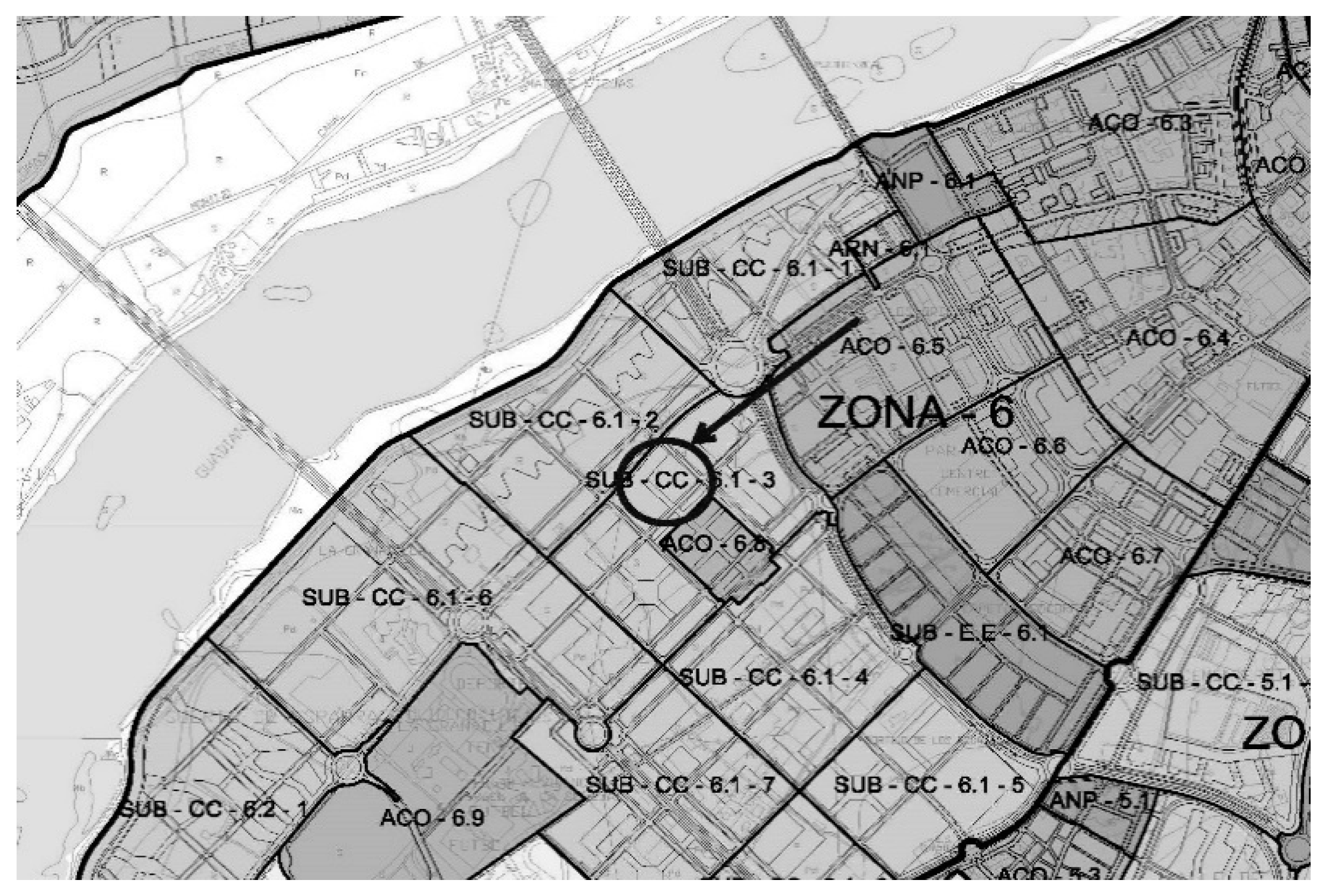

38]. The chosen area for the study is in the municipality of Badajoz (Spain), within Zone 6, Sector SUB-CC-6.1-3, according to the Municipal General Plan (PGM) (

Figure 3). Badajoz is a city located in the southwest Spain and is also the capital of its province, the Autonomous Community of Extremadura. It has 150,000 inhabitants, and is the most populated city of Extremadura. Badajoz is crossed by one of the most relevant water resources of the Iberian Peninsula, the Guadiana river. The proximity of Badajoz to the border with Portugal is relevant. Badajoz is inserted in a Cross-Border Cooperation project with the Portuguese cities of Elvas and Campo-Maior, the Euro-city Elvas-Badajoz-Campo-Maior.

At the time of this research, Badajoz has urban developable land classification, but is, however, located in a sector without development. It has not established its detailed ordering or drafted the corresponding partial plan. Its global use is residential [

39].

The planning development that affects the study area has been divided into four urban states: the first level is the current state—state E1—which corresponds to the classified land and delimited in sectors in the general plan, with no management detailed; the second level—state E2—corresponds to the land of the sector developed through a partial plan and in which its detailed arrangement is already reflected; the third level—state E3—corresponds to the action units with approved re-parceled project, its goal being the distribution among the owners of the urban development granted by the planning, proportional to the area of land that each one has, with a distribution equitable of charges and benefits. In fact, at this level, the city blocks and plots are already reflected with their respective parameters of detailed uses, buildings and building typologies, but the land is not yet urbanized. The fourth level—state E4—corresponds to the final urbanized land, ready to be built.

2.2. Methodology Fundamentals

The selected methodology for land valuation in the different urban states was the discount model of the Free Cash Flow (FCF). This methodology is based on the economic analysis of a virtual real estate investment project, to be developed on the land subject to valuation, following the greater-and-better-use principle. This process does not take place at a specific time or in a single moment; however, the collections flow and the consequent payments occur over a time horizon, a circumstance that is decisive for the final result [

40,

41].

One of the main principles of corporate finance establishes that the value of an investment project can be expressed as the updated value of the FCF expected by that asset. The FCF discount model is one of the most widely used internationally to value investment projects [

42,

43,

44,

45,

46,

47]. FCF represents the excess liquidity or the money that remains available to attend, on the one hand, the sharing of profits among the investors and on the other, the payment of the debt to the creditors. The FCF is the flow of funds generated by the operations, without taking into account the indebtedness, after taxes. In fact, it is the money that would be available in the investment project assuming there is no debt. In short, it is the flow generated by the project regardless of how it is financed [

48,

49].

As these flows are expected over a certain time horizon, to update them, they will have to be discounted at a specific discount rate. The general formulation of the model to determine the Net Present Value (NPV) of the investment, using the FCF will be:

where:

A = initial disbursement of the project, equivalent to the land value; FCFj = the expected free cash flow of each considered period; j = each period of the time horizon in which the flows occur; k = discount rate; and n = number of considered periods for the project's time horizon.

To determine the total value of the investment project, the appropriate flows considered are the FCF and the appropriate discount tax is the weighted average capital cost (WACC) [

50,

51]; therefore,

k = WACC.

If we consider NPV = 0, thus, would be at the threshold of minimum profitability required by the project, and therefore this discount rate (WACC) is equivalent to the Internal Return Rate (IRR) of the project. The initial outlay, “A”, would be the land value (A = VS), which represents the maximum amount that could be paid for it to make the project profitable. If NPV = 0, the discount rate, WACC = IRR. The expression to obtain the value of the soil would be:

2.3. Stablishing of Free Cash Flow (FCF)

The general formulation for the calculation of the

FCF is given by the following expression [

44,

45,

52,

53]:

where:

EBIT = Earnings before interest and taxes; T = Tax rate; Dep = Depreciations; FCInv = Fixed Capital Investment (capital expenditure); WCInv = Working Capital Investment.

In the analyzed case study, it has been considered that the project will be developed through a real estate development—where the initial capitals contribute—without investments in amortizable assets or cash investments or fixed assets. Therefore, the FCF of the real estate investment project will be given by the following expression:

The FCF of each period is a parameter that will depend on many variables [

54,

55], thus, they will influence, both in the sales collection of the real estate units and in the payments made for the expenses that are generated along the time horizon.

The inflows include all incomes obtained from the sales of real estate units. To calculate the inflows, the valuation criterion has been followed by use units (u.u.), with the corresponding application of the homogenization coefficients by uses, established in the initially collected data in the granted conditions by the planning [

39]. Therefore, it has been considered that this criterion is acceptable and prudent since these data are supported in the initial documentary information, and calculated according to the legal possibilities that the land has, relating to uses and building intensities [

56].

The outflows comprise the following elements: Management and Urban Development expenses (MUD); Urbanization Costs (CU); Construction Costs (CC); Necessary Promotion Expenses (NPE); and Marketing Expenses (ME).

The estimated time horizon to develop the investment project, until finalizing the sales for the real estate units, considering each one of the states’ (S) are as follows: S1 14 years; S2 11 years; S3 8 years; and S4 4 years. The outflows dispersion in the time horizon, of each one of the urbanistic states, have been estimated as follows: for S1 and S2, where the lands are undeveloped, have been considering payment typologies as MUD, CU, CC, NPE and ME; for S3, where the land is already in (re)parceling have been considered CU, CC, NPE and ME; and for S4, where the land is urbanized, have been considered CC, NPE and ME.

The MDU includes the following expenses: expenses associated with land sales; creation of the compensation board; urban interest group; topographic survey and demarcation; professional fees for drafting the execution program; development planning; re-parceling the project; notary fees and registration of the resulting parcels; environment effect investigation; technical fees for urbanization works (project, facultative direction, security and health); real estate property tax; municipal taxes for urbanization works; and other management and urban development expenses. The CU include the costs of contract execution of the urbanization works and topographic surveys. The CCs include contract execution costs of the construction works of the real estate units; construction waste management costs according to current legislation; geotechnical study; and quality control standards. The NPE includes the following expenses: technical-facultative fees (projects, work management, security); municipal taxes levied on urbanization and construction; compulsory insurance of the promoter; management expenses of the promotion (salaries, social security, labor management, fiscal); notary, registration, and taxes not recoverable by the deeds of new work and horizontal division; property tax of real estate units until sale; and other necessary expenses. The CCs include the following expenses: commissions for sales of real estate agents; and advertising and marketing expenses. It should be highlighted that, in the calculation of the FCF, the financial expenses generated by the financing of the investment project with foreign capital are not considered, once the FCF is the operating cash flow; that is, the cash flow generated by the operations of the project activity, without taking into account the indebtedness, after taxes. The debt is not considered to prevent the indebtedness chosen by the project managers (degree of financial leverage) from conditioning the value of such project. Therefore, this analysis is performed without considering the debt taken to develop the project [

42,

44].

2.4. Defining the Discount Rate: The WACC Model

2.4.1. Formulation

A major issue that must be noted, before defining the discount rate, is that there is no discount rate that is objective and indisputable, because it is a value that is calculated based on the risk perceived by the assessor (who provides valuation) in the investment project, depending on whether there is a greater or lesser risk in the production of project flows [

57].

In the valuation of investment projects for the discount of free cash flow, the appropriate discount rate to consider is the WACC model [

58,

59,

60]. The WACC is the cost of financing the project as a whole and, therefore, given that the capital costs differ from each financial source, depending on whether it is equity capital or debt, we will have to calculate the weighted average cost according to the different funding sources from which the virtual project feeds. The weightings reflect individual weights that each of the sources has in the whole project, and in short, they reflect the proportion of the capital structure of the investment project. Conceptually, WACC provides an estimate of the average opportunity cost of capital providers to an investment project. The WACC model is based on the theory that capital costs are different depending on the financing source on which the company feeds, i.e. if a company is financed on the one hand through its own capital and on the other through debt, each of these two sources of financing will have a determined cost of capital that will be different from one another. As each resource (debt and equity capital-equity) represents a certain weight in the total capital of the project, we will have to weigh each type of resource according to the weight that each of them has in the total capital [

44,

45].

According to the WACC definition, it is obtained by the following formulation [

61]:

where:

ke, the cost of the project’s own capital (equity); kd, the cost of project debt; E, the total value of the project equity; D, the total value of the project debt; T, the legal tax rate at the time of valuation.

Thus, to calculate the WACC, the following steps (3) must be followed:

2.4.2. The Equity Cost, ke

The equity costs of an investment project represent the opportunity cost of the project, reflecting the return that an investor requires to their own resources, when investing in said project, including a premium for the risk assumed when making the investment. It is equivalent to the minimum profitability demanded by the investors of the project because of them investing in it. Of all the financing costs, that of the own capital is the one with the highest risk associated [

62]. The expected return of a physical asset, i.e., land with urban development or financial assets, is obtained by adding a risk premium to the profitability offered by an asset without risk. The investor will demand his own capital invested in a project, an opportunity cost that will be determined by the addition of a differential or compensation for risk to an asset free of any risk [

63,

64]. The cost of equity will be given by the following expression:

i =

io + differential (compensation) for risk, where

io is the free rate of all risks. This differential will be the project's risk premium. Therefore, the mathematical expression for the equity costs of an investment project will be given by the following formula:

where:

ke, the equity capital costs of an investment project; rf, the risk-free rate; PR, the risk premium of the investment project

The risk-free rate (

rf) is the rate of return of an asset whose profitability is always known and equal to that expected within its investment horizon and known with complete accuracy and certainty the maturity at a certain moment [

65]. For the case study, the Debt of the Spanish State has been estimated as a risk-free asset, with a single payment at maturity and the most recent issuance possible for the valuation of the investment. Given that it is an investment project in Spanish territory, the choice of the Spanish State Debt is justifiable since it is considered to have sufficient liquidity. In this regard, it is not necessary to add the country risk premium to a risk-free rate of the debt issued by another country with lower risk than Spain, such as that of Germany or the United States. Therefore, the calculation of this parameter has been obtained through the arithmetic mean of the marginal interest rates of the 10-year Obligations auctions issued by the Spanish Government.

Therefore, the risk-free rate is an element that is possible to obtain through the publications put forward by the government’s economic departments; nevertheless, the risk premium is a feature that depends on the market or the investment project and is, thus, is not sustainable in historical data to calculate the risk premium [

37,

42] once it is an element with direct dependent on the project risk [

36,

41]. There is, thus, difficulty in obtaining the data related to the risk premiums of another project. This is due to the reluctance that originates in the promoters themselves to provide this information, and also the existing reservation from data protection policies. Such circumstances arise that the assessor does not have enough data to calculate the risk premium with a minimum of scientific rigor [

24,

26,

28]. The calculation of the project risk premium (RP) was made based on the factors that influence the risk of the project, considering the following variables: the type of real estate asset to be built, the location of the real estate project, the liquidity of the investment, the time horizon of the project, the volume of investment necessary to perform it, access to the credit of the potential buyers of the real estate units, the level of indebtedness of the project, and the interest rates offered by banks in the market of mortgage loans and inflation [

66]. The methodology for determining the risk premium of the project was based on the Analytical Hierarchical Process (AHP). AHP is an alternative selection method that considers variables that influences the final outcomes. It consists in the weighting of the criteria and alternatives through the so-called paired comparison matrix, which is a judgments matrix that is released by previously selected experts [

67,

68,

69]. This method is widely used for the evaluation of all types of projects in numerous fields and disciplines [

70,

71,

72].

Thus, it should be taken into account that the same discount rate cannot be used in the four land development states once the assessment of each state has been evaluated as different investment projects with different time horizons; in short, they have different levels of risk [

73]. The time horizon is an explanatory variable for the determination of the risk premium of the project and is different for each state of urbanization; therefore, there will also be a different risk premium for each state. In the same way, different risk-free rates could have been used according to the different debt issuance state periods, but still, given the low variation and the low interest rates offered by Spanish public debt, it has finally been estimated according to the state obligations with a 10-year maturity (Table 4). Furthermore, those issues are the most representative of the auctions carried out by the Spanish government and as used as a reference to establish the differential of the risk premium regarding a German bond.

2.4.3. The Debt Costs, kd

Debt costs, kd, is another component of WACC. It will be estimated from the information on the existing interest rates in the mortgage market. The cost of the debt is the profitability required to meet the payment of this. Therefore, to obtain it, an analysis of the current economic situation has been carried out [

74,

75]. Once the data was collected, a prudent estimate was made of the non-preferential interest rates offered by the financial entities that operate in the sector.

2.4.4. The Level of Financial Leverage: Determination of E and D

It is usual for companies in the real estate sector, both in Spain and abroad, to have high levels of leverage, although in recent years this level has been in decline [

76]. The level of leverage is a factor that must be estimated prudently since a high level of indebtedness for the project directly influences an increase in the investment risk [

77]. The capital structure of the project is determined by the contribution of own capital (equity) and third parties (debt). The term E is the percentage that represents the equity in the total investment, and the term D is the percentage that represents the debt in the total investment, in such a way that: E + D = 100 [

78].

Contextually, to calculate these parameters, other information must be inserted into the data regarding the financial leverage ratio of companies in the real estate development sector [

79,

80]. From this ratio it has been possible to obtain the leverage degree that transport it directly to the WACC formula; the degree of financial leverage is given by the expression: NAF = D/(E + D), therefore: E/(E + D) + NAF = 1.

2.5. The Time Horizon for the Evaluation of the Investment Project

In the valuation model of investment projects by discounting flows, the time horizon is the period during which the different flows, positive and negative, will occur. It is one of the factors that most influence the value of the project [

81] since it is necessary to estimate the specific moments in which both the inflow and the outflow will occur. The time horizon is a parameter that also influences the determination of the discount rate of the project, increasing it as that parameter increases [

82]. In the case of the valuation of land by the flow discount model, this horizon is related to the global term of management, development, and completion of the virtual real estate development that is considered to be developed on land. It will cover the global timeframe, considering the totality of flows that may occur during the development of the real estate investment project, from the creation of the company to carry out the virtual project until its dissolution. It is a parameter that requires good coordination among principles of management, development, urbanization, construction process and marketing promotion, especially when the land is in the phase of urban development, as there are deadlines that do not depend on the direction of the project but do depend on the time that the administration delays in approving definitively the different instruments of planning and urban development [

83]. On the other hand, there are authors establishing that the maximum time horizon to apply the discount model of flows can be simply considered to be fifteen years [

52,

84].

2.6. Data Collection

The inflows have been calculated based on the urban development conditions established by the Badajoz’ City Master Plan for the specific sector where the land is located (

Table 1). The criteria for evaluating the subjective average use of the distribution area—where the study land lies—has been followed, based on the units of use, coefficients of homogenization and use features established by the municipal planning [

39]. The conversion of the use of monetary flows has been made based on an analysis of previous publications on the sale price of the residential characteristic use established for the sector [

85].

The outflows corresponding to the costs of urbanization and construction have been calculated from the data provided by specialized publications [

86,

87]. An inter-annual inflation rate of 1.5% has been considered.

The risk-free rate was obtained from the data published by the treasury for the marginal interest rates of the 10-year obligations issued by the Government of Spain [

88]. A risk-free rate of 1.70% has been estimated.

The risk premium of the investment project has been calculated by applying the AHP multi-criteria model [

67]. The expert panel was made up of academics and professionals with considerable experience in urban planning and real estate valuation processes. It was composed of a total of 10 experts: a Ph.D. expert in environmental sciences, 2 environmental engineers, 2 architects, 2 civil engineers and 3 real estate appraisers. Thus, the following criteria and variables have been selected: V1, the type of real estate asset; V2, the location; V3, the liquidity of the investment; V4, the time horizon; V5, the volume of investment; V6, access to the credit of the potential buyers of the real estate units; V7, the financial leverage level; V8, the interest rates; and V9, the inflation rate. The set of experts has also selected the following alternatives or risk levels: level 1, very low; level 2, low; level 3, medium; level 4, high; and level 5, very high. Thus, the consistency and the own vector (OV) of the comparison matrix, as well as the variable paired comparison (VPC), with a size of 9 × 9 was calculated. The OV enable us to define the weight or importance of each variable with respect to the rest. On the other hand, the different paired comparison matrix of risk levels was obtained, for each variable (size 5x5), obtaining the OV of each one, once the consistency of each one was verified. Therefore, 9 OV were obtained. With these vectors it has been possible to obtain the matrix (OVM) (size 5x9). The result of the multiplication of the OVM by the column matrix OV offers us the weights of each risk level [

66]. The overall result of the risk premium in each state of urbanization is shown in Table 4.

A different risk premium was calculated for each state, once, among the explanatory variables considered in the AHP model, considering the time horizon and the volume of investment needed, and parameters that are determined by the urban development of the land. The following values were obtained (

Table 2).

The level of financial leverage has been obtained from the data published by the Bank of Spain on sectorial ratios of non-financial corporations [

89]. A level of financial leverage of 30% was estimated.

The cost of the debt has been estimated at 4.75% and was acquired from surveys conducted on local banks on the interest rates of loans for real estate developments. The general rate of corporate income tax has been estimated at 25%, the current rate in Spain.

2.7. Formulating Land Values in Each Urban State

The main components of the formulation are: the annual free cash-flow updated (FCF), the discount rate (WACC) and the considered time horizon of the investment project, finalizing with the sales of the real estate units (HT). The FCF obtained over the years will be shown in Table 5. The WACC is presented in Table 4.

Contextually, the time horizons of the investment project, used for the calculation, to the end of the sales of real estate units were: for S1-14 years; for S2-11 years; for S3-8 years; and for S4-4 years (

Table 3). Below are the applied formulas to obtain the land value for each urban state:

The

WACC is presented in

Table 4. The

FCF obtained over the years will be shown in

Table 5. To develop the inflows, the authors started from the collected data regarding the sales of real estate units carried out by real estate companies in the sector; thus, the time horizon, necessary to consider for the investment project analysis, goes from the considered state until the completion of the sales of the real estate units.

The S1 (state 1) corresponds to the current moment, therefore the obtained land value for this state does not need to be corrected; however, the land values in S2, S3 and S4 have been extrapolated under the current state hypothesis and must be corrected through capitalization at a future moment in which it is estimated that these states are achieved. The used time periods for the calculation are shown in

Table 3. Through

Figure 4 is possible to analyze the time sequence of the different urban states.

2.8. Capitalization of the Value at the Time of Each Urban State

Through the parameters described, it is possible to obtain the land value for each urban state—E1, E2, E3, and E4—on the current period. Therefore, only the value obtained for the state E1 will be real, since the states E2, E3, and E4 will be acquired in the future, throughout the development of the urban planning inherent processes. Thus, the values obtained for the states E2, E3 and E4 must be capitalized to obtain the value in future periods, when those urban states are acquired. For this, studies on the evolution of the real estate market have been considered [

90,

91]. The estimated time to obtain the corresponding urban states is presented in

Table 3.

3. Results

Four urban states have been considered: E1, developable land without detailed planning; E2, developable land with detail arrangement; E3, action unit with approved re-parceled, without urbanization; and E4, final urbanized land.

In

Table 4, it is possible to analyze the actualized FCF of the investment project, through the time horizon until the end of the real estate units’ sales. For the calculation, a unit of 100,000 m

2 has been used, with urban development potential of 50,820 m

2t.

Through the starting data presented, a discount rate was obtained for each state, which is shown in

Table 5.

With the data, the proposed methodology and the starting assumptions, the land value has been calculated in each state of urbanization, compared to the results with the land value in the E4 state completely urbanized. The results obtained are shown in the following (

Table 6,

Figure 5).

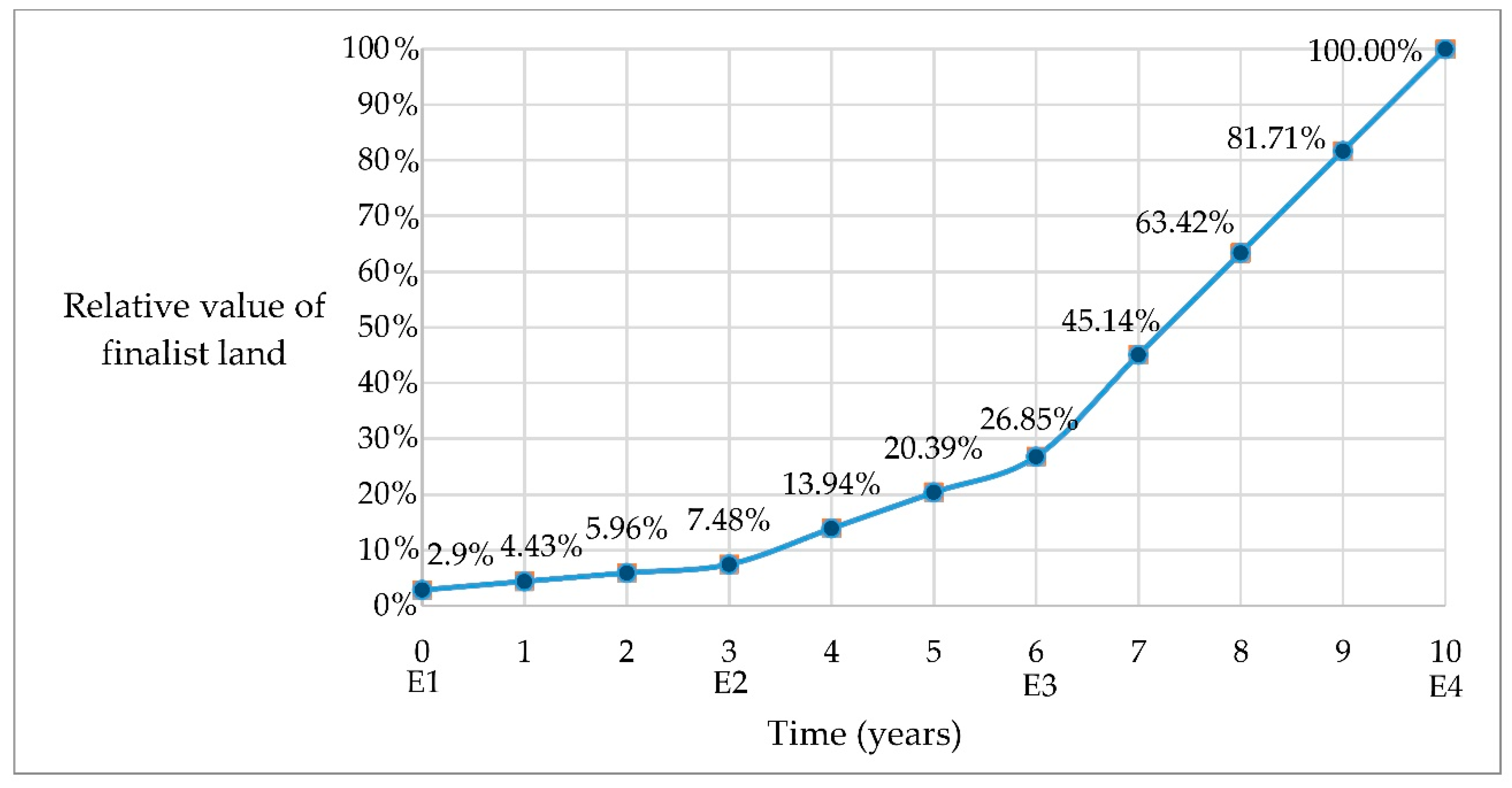

Through the analysis of the graphic above, the land valuation in state E1 represents a low percentage of the completely urbanized land. Such percentage goes up steadily until state E3, which corresponds to the floor of the action unit with re-parceling. The transition from this state to the urbanized land is when the greatest jump in the land value takes place, until obtaining the value that the completely urbanized land has. With this figure, it is shown that the exposed valuation model does indeed work and is also compatible with a sustainable valuation of the land.

4. Discussion and Conclusions

Through the study, the evolution of land valuation has been determined, along with the planning processes developed, applying the principle of prudential value in the estimation of the fundamental parameters, flows, time horizon and risk premium, obtaining results far from all considerations of unattainable expectations and speculation, fundamental aspects in the sustainable valuation of the land use, and catalysts for future land values approaches in a more sustainable and realistic manner.

The main goal of a sustainable land valuation should be able to eliminate most speculative elements, strengthening the initial stages of the planning development process with adequate criteria, in a way that can be used to provide more accurate results in those initial states, which do not cause artificial growth in the final urbanized land value.

The establishment of classification and urban qualification of land in planning processes implies the allocation of uses and building intensities, determining their urban development and therefore its real value. However, this real value is not attributed to the land at the time of its expression in the planning documents. However, it increases as it develops and is managed until it reaches its maximum value when it is already completely urbanized land.

Also, through the literature review, several models have been identified, explaining the changes in the value of real estate property as urban planning is developed, from the drafting of municipal planning in which the land is classified, to the final real estate product, with the construction of buildings [

7,

33,

34]. In these models, the obtained land value is represented according to the prices of the finalized or already existing building. Such models admit an increase in the land value after urbanization (when built). Nevertheless, the authors believe that such increase is not due to the development of urban planning itself, but instead it incorporates a certain post-value that would be motivated by the increase in the real estate prices and not by the development of urban planning. On the other hand, through the literature review, we have not found specific valuation methodology to obtain land valuation. In this regard, the present study summarizes two main differences related to it: (i) the impact of urban planning development is analyzed in the evolution of the increase of land value, motivated solely by its development over time, until it is fully urbanized, which does not consider the subsequent increase when the land is built on, produced by the movements that occur in the real estate market; (ii) a specific method of land valuation is established and specified, which is the discount model of the FCF, considering the virtual real estate investment project to be developed on the land to be valued. Effectively, this method is one of the most widely used internationally for the evaluation of investment projects [

42,

43,

44,

45,

46,

47]. The discount rate considered was the WACC (after taxes). For proper application, a different risk premium has been estimated depending on the urban development state of the land, resulting in different discount rates for each one of them.

The obtained results show that at the end of each state, different capital gains will be generated. Four levels of surplus value are obtained: (i) by delimitation; (ii) by ordination; (iii) by re-parceling; and (iv) by urbanization. These capital gains increase as the state moves closer to fully urbanized land, with the highest surplus value obtained with the passage from state E3 to E4—from re-parceled land to fully urbanized. The function of creating land value throughout the development of urban planning increases, as is the case of its slope as it approaches urbanized land.

To determine the gradual evolution of the land value as planning progresses, unitary values on gross soil surface should not be used, since the land surface in the initial stages—when there is no management—will not match the surface or with the geometry plots resulting from the re-parceling; but what will not vary are the units of subjective use established in the planning. Therefore, it is necessary to consider this parameter.

In the land value obtained, for each state, we have presented of major relevance not only the consideration of different time horizons, but also the application of different discount rates, considering a discount rate for each state, depending on the estimated risk for the investment project. By introducing the time horizon as an explanatory variable for the risk premium calculation of the project, discount rates are obtained that increase as the variable does too. In the general model formulation, the discount rate and the time horizon represent an exponential function, the base being the discount rate and the exponent the time horizon (Formula 2); This function causes the resulting values to decrease sharply as these two parameters also increase, especially for the time horizon variable.

In the present study, it is obvious that land values in the initial stages of urban development represent a fraction of the value in the final urbanized state, producing a steep rise when the land is urbanized and ready to be built. The highest rise occurs between the final states, E3 and E4. The unit values resulting from the application of the method by flow discount for the case study are valid for the time of writing; if absolute value is needed to be assessed, it must have updated in order to use the model for future scenarios and time periods; however, this has no significance in the study results, which represent the evolution of the land once we are given in relative values, as a percentage of the value of the final urbanized land. The low values obtained in the urban planning states of land without planning are very close to the initial value—which encompass their agricultural use—confirm that they have not considered expectations of difficult realization and therefore are far from any speculative practice. The maximum capital gains are obtained in the passage of re-parceled land to urbanized land, which promotes a sustainable land valuation, avoiding the creation of unrealized capital gains.

A major achievement of this methodology is its practical functionality to calculate the land value of the different urbanization states from the value of the fully urbanized land. Calculating only the value of this urbanized land, we have the value of the land in prior states to urbanization, by applying the different coefficient results for each state.

For final remarks, this research contributes directly to both making individualized land valuations and in making massive valuations, carried out by the administration for the liquidation of taxes on the land. Following this methodology, the land values without development or urbanization can be calculated, starting from the establishment of the hypothetical value of the fully urbanized land for the land that belongs to the same sector, always considering the same features of urban development established by the available planning tools.

Thus, the study has considered an estimate of the time horizons in the analysis of the investment project that involves land valuation in each urban state. Nevertheless, future research and study may be able to introduce variables of uncertainty and even consider other time horizons.

and

and

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}