Evaluating the Greenhouse Gas Emissions in the Craft Beer Industry: An Assessment of Challenges and Benefits of Greenhouse Gas Accounting

Abstract

1. Introduction

- RQ1: What are the challenges of GHG accounting in craft breweries in Ontario?

- RQ2: What are the benefits of GHG accounting in craft breweries in Ontario?

2. Background

2.1. GHG Accounting in the Craft Brewery Industry

2.2. GHG Reduction Efforts and Craft Brewing in Ontario, Canada

2.3. Theory

2.3.1. Institutional Theory

2.3.2. Image Theory

3. Materials and Methods

3.1. Ontario Craft Brewer Interviews

3.2. Ontario Craft Brewer Case Study

4. Results

4.1. Ontario Craft Brewer Interviews

4.1.1. Interviewee Background

4.1.2. Interview Results

4.1.3. Interview Challenges in GHG Measurement and Reduction

“We’re still coming out of like trying to pay off a lot of expenses, the money is like super, super tight right now and we’re still not operating like in the positive yet … our business model has to … have some sort of cost savings associated with it and to me that’s a challenge …”.(Company P06)

“… if we had a better cash flow we’d be willing to make some sacrifices to change the way that we do things, even if it was more costly but it’s certainly an industry that has razor thin margins especially when you’re starting”.(Company P13)

“We have no time to collect data … we continue to be a small staff but we’re really focused on making and selling beer, that is our business … I don’t want my people involved. I’ll do what I can, you know, but to me, like right now, knock on wood we’re doing very well, but I need all hands on deck, you know, making beer … as we get bigger and we have more roles to play, there might be an opportunity to have an … environmental lead person in a brewery, may be in charge of our wastewater and in charge of our emissions and in charge of all environmental stuff, but we’re a long way away from that right now”.(Company P04)

“… maybe having groups or agencies that can sort of give a helping hand and educate on ways to reduce carbon emission and other sort of environmentally unfriendly things that happen at [brewery name], we are probably one of the bigger craft breweries, but there are many, many people that are smaller than us that would have even less resources than we do and honestly it’s likely not a priority for a lot of businesses it’s based on priorities and a lot of financial perspectives and the craft beer industry is struggling right now in general”.(Company P10)

[In reference to OCB member meetings]: “I don’t recall us actually talking about greenhouse gas emissions at the sessions, I mean there’s lots on wastewater management and you know, quality assurance and those things, but not as much on greenhouse emissions …”.(Company P12)

“… we don’t necessarily see a lot of what initiatives are going on from what companies aren’t publicly traded, like you know, there’s not a lot of small brewers that are publishing their annual sustainability reports and so it’s very hard for us to gauge and I think that you know, our industry is actually really good with sharing best practices around a lot of other things and it’s still very collegial and I sense that that will also extend to sustainability and carbon management, but the fact that we haven’t really heard about it to me indicates that our industry isn’t there and so there’s not much to share otherwise they would be more collaborative around that, in my mind.”.(Company P13)

“I’m assuming that we have to pay something for it in future and this will be like, it won’t cripple us but it is a worry, an ongoing worry … [at different point in interview] I feel that … cap and trade or whatever it is, [is] payment to the government. They already take so much from us. At the end of the day there will be a tipping point that we have to hold off, not because we’re not making money, is that we’re to make enough to survive because the government takes a big cut”.(Company P04)

“I suspect on the industry there’s probably going to be some rude awakening, but I think for [brewery name] … I think for the most part it won’t have a tremendous impact on us personally”.(Company P07)

4.1.4. Interview Benefits to GHG Measurement and Reduction

“I understand that aspect of a business [i.e., increasing sales] and you have to run it but it’s like, this transcends things like selling your product. It gets to the point of you know, just being like I said, good stewards of what we have here on earth …”.(Company P06)

4.2. Case Study Results

4.2.1. Case Study Process Mapping

4.2.2. Case Study GHG Calculations

4.2.3. Case Study Scenario Analysis

- Simplified Formula:CO2eY2028 = [CO2e from bottles produced for packaging in year 2028 − CO2e saved from recycled bottles used to produce bottles in year 2028] + [CO2e from cans produced for packaging in year 2028 − CO2e saved from recycled cans used to produce cans in year 2028]

- Complete Formula:CO2eY2028 = (2016 hL packaged in bottles * 100(L/hL)/.341(L/bottle) * (10 year compound/2)‡ * % growth) * (1-decrease in bottle packaging) * weight bottle(g)/1000(g/kg) * (% returned bottles * EF for bottle recycled + (99% returned bottles) * EF for new bottles)+(2016 hL packaged in cans * 100(L/hL)/(0.473 + 0.355)/2 (L/can) * (10 year compound/2)‡ * % growth) * (1 + increase in can packaging) * weight can (g)/1000(g/kg) * (% returned cans * EF for can recycling + (94% returned cans) * EF for new cans)‡ the time horizon for this calculation is 10 years (2018–2028). Since the growth in beer sales value drawn from OCB (2018) reflected their growth over two years (2015–2017), the formula reflects five compounding periods (one every two years) instead of 10 (one per year).Other notes: two sizes of aluminum cans are reflected in the (0.473 + 0.355)/2 section of the formula to calculate the average volume of cans because the case company’s primary data did not specify litres packaged in the two sizes of cans. The return rates of aluminum cans were 94%, with all other recycled material having a return rate of 99% (Teotonio, 2013).

4.2.4. Case Study Challenges and Benefits of GHG Reduction

5. Discussion

6. Conclusions

Author Contributions

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Interview Question Number | Interview Questions |

|---|---|

| 1 | A. Does your company measure its electricity usage? B. If so, does your company have plans in place to minimize electricity use? C. Are you aware of your company’s electricity composition (i.e., percentage sourced from renewable vs. non-renewable energy)? |

| 2 | A. Does your company measure its greenhouse gas (GHG) emissions? B. If so, does your company have any GHG reduction programs in place? C. What is your company’s process and considerations for developing GHG reduction targets? D. Do you measure direct and indirect GHG emissions? |

| 3 | Do you see managing electricity use and reducing GHG emissions as priorities in your business model? Why or why not? |

| 4 | Regardless of whether you collect baseline GHG emissions data, what do you see as the main A. challenges and B. benefits of collecting baseline GHG emissions data? Prompt: for example, do you see a marketing opportunity for promoting your beer as environmentally sustainable for reducing its carbon footprint? Is cost a consideration? |

| 5 | A. Does your company have any sustainability initiatives? B. What are the main challenges in implementing/maintaining these programs? C. If you do not have a program in place, what are your reasons for opting not to? D. Do you foresee development of a program(s) in the future? |

| 6 | A. Have you heard of Ontario’s cap and trade program? B. If so, what do you know of it? C. How do you think this carbon pricing scheme will impact your company? |

| 7 | Do you have any ideas on an effective carbon pricing mechanism that should be applied in Ontario aside from cap and trade? |

| 8 | A. Do you think the beer industry is doing enough to reduce its GHG emissions? B. How do you think your company compares to others in this industry? |

Appendix B

| Keyword Category | Keywords Included in the Category | Frequency (# Keywords Included in Category) |

|---|---|---|

| Environmental sustainability | Accountability, B-Corps, carbon neutral, eco-friendly, environmental impact, environmental performance, environmental sustainability, environmentally conscious, environmentally responsible, green, sustainable, sustainable environmental best practices | 16 |

| Supply chain management | Biodiesel, closed loop, green electricity, grown on site, ink reduction, local, locally sourced, low-emission heating and cooling, renewable energy, renewable power, responsibly sourced, sustainably sourced energy | 13 |

| Input efficiency | Paper reduction, reduce energy usage, remove chemical usage, water conservation | 4 |

| Waste reduction | Compost, nothing goes to waste, organic waste, waste diversion | 4 |

| Responsible packaging | Reusable bottles, sustainable packaging | 2 |

| Environmental behaviour | Clean commute, employee education, re-use, recyclable, recycle, transparency | 7 |

| Total keywords | 46 |

Appendix C

| Product/Process | Emission Factor | Emission Factor Unit | Source/Standard | Table/Figure/Page |

|---|---|---|---|---|

| Steel production | 0.07 | tonnes CO2/tonne steel | 2017 Canadian National Inventory Submission to the United Nations Framework Convention on Climate Change (using 2015 inventory) | Table 2(I).A-Hs2 |

| Steam production | 67.800 | kgCO2e/1000lbs steam | Rolff, D. (2011). LCA of deep lake water cooling in Toronto. (Unpublished master’s paper). University of Toronto, Toronto, Canada. | Page 18 |

| Refrigeration and cooling | 0.040 | kgCO2e/tonne hour | Rolff, D. (2011). LCA of deep lake water cooling in Toronto. (Unpublished master’s paper). University of Toronto, Toronto, Canada. | Page 22 |

| Fuel consumption for Class 7 and 8 vehicles | 0.39 | L/km | 2017 Canadian National Inventory Submission to the United Nations Framework Convention on Climate Change (using 2015 inventory) | Table 1.A(a)s3 |

| Road diesel | 10.131 | kg CO2/US gallon | WRI Emission Factors from Cross Sector Tools, 2017 | CO2 for road diesel fuel: Table 12 |

| Road diesel | 2.676327 | kg CO2/L diesel | (conversion) WRI Emission Factors from Cross Sector Tools, 2017 | CO2 for road diesel fuel: Table 12 |

| Gasoline/petrol | 8.59873 | kg CO2/US gallon | WRI Emission Factors from Cross Sector Tools 2017 | CO2 for gasoline/petrol: Table 12 |

| Gasoline/petrol | 2.271544 | kg CO2/L gasoline | (conversion) WRI Emission Factors from Cross Sector Tools, 2017 | CO2 for gasoline/petrol: Table 12 |

| Jet fuel | 9.428 | kg CO2/US gallon | WRI Emission Factors from Cross Sector Tools 2017 | CO2 for jetfuel: Table 12 |

| Jet fuel emissions | 0.61324 | kg CO2/tonne km | WRI Emission Factors from Cross Sector Tools 2017 | Table 16 |

| Rail transportation | 0.0252 | kg CO2/short tonne mile | WRI Emission Factors from Cross Sector Tools 2017 | CO2 for rail transportation: Table 16 |

| Rail transportation | 2.77782 × 10−5 | kg CO2/kg mile | WRI Emission Factors from Cross Sector Tools 2017 | CO2 for rail transportation: Table 16 |

| Ocean container transportation | 0.048 | kg CO2/short tonne mile | WRI Emission Factors from Cross Sector Tools 2017 | Table 16 |

| Ocean container transportation | 3.286 × 10−5 | kg CO2/kg km | (converted) WRI Emission Factors from Cross Sector Tools 2017 | Table 16 |

| Biofuel | 8.10442 | kg/US gallon biodiesel | WRI Emission Factors from Cross Sector Tools 2017 | CO2 for biofuel: Table 12 |

| Biofuel | 2.140961 | kg/L biodiesel | (Converted) WRI Emission Factors from Cross Sector Tools 2017 | CO2 for biofuel: Table 12 |

| Waste to landfill | 0.05 | tonnes CH4/tonne waste | 2017 Canadian National Inventory Submission to the United Nations Framework Convention on Climate Change (using 2015 inventory) | Table 5.a |

| Waste to landfill | 1.40 | tonnes CO2e/tonne waste | (conversion) 2017 Canadian National Inventory Submission to the United Nations Framework Convention on Climate Change (using 2015 inventory) | |

| Waste incinerated | 413.57 | kt CO2/kt waste | 2017 Canadian National Inventory Submission to the United Nations Framework Convention on Climate Change (using 2015 inventory) | Table 5.a |

| Waste incinerated | 0.26 | kt CH4/kt waste | 2017 Canadian National Inventory Submission to the United Nations Framework Convention on Climate Change (using 2015 inventory) | Table 5 |

| Waste incinerated | 0.44 | kt N2O/kt waste | 2017 Canadian National Inventory Submission to the United Nations Framework Convention on Climate Change (using 2015 inventory) | Table 5 |

| Organic compost | 21.89 | kt CH4/kt waste | 2017 Canadian National Inventory Submission to the United Nations Framework Convention on Climate Change (using 2015 inventory) | Table 5 |

| Organic compost | 1.31 | kt N2O/kt waste | 2017 Canadian National Inventory Submission to the United Nations Framework Convention on Climate Change (using 2015 inventory) | Table 5 |

| Freight truck fuel efficiency | 2.676326532 | kg CO2/L diesel | WRI Emission Factors from Cross Sector Tools 2017 | GHG Protocol emission factors from cross sector tools March 2017 |

| Max load Class 7/8 vehicle | 13,381.50 | kg/truck load | https://en.wikipedia.org/wiki/Truck_classification | US GVWR truck classifications |

| CH4 (GWP) | 28 | g CO2e/g CH4 | 2014 IPCC GWP (AR5) found in IPCC 2014 Climate Change report and GHG Protocol "Global Warming Potential Values" | Box 3.2, Page 87 |

| CO2 (GWP) | 1 | g CO2e/g CO2 | 2014 IPCC GWP (AR5) found in IPCC 2014 Climate Change report and GHG Protocol "Global Warming Potential Values" | Box 3.2, Page 88 |

| N2O (GWP) | 265 | g CO2e/g N2O | 2014 IPCC GWP (AR5) found in IPCC 2014 Climate Change report and GHG Protocol "Global Warming Potential Values" | Box 3.2, Page 89 |

| Paper packaging waste | 1.34 | kg CO2e/kg waste | BUWAL 250; Ecoinvent | Table 1, Cimini & Moresi, 2016 |

| Cardboard packaging waste | 1.73 | kg CO2e/kg waste | BUWAL 250; Ecoinvent | Table 1, Cimini & Moresi, 2016 |

| Paper recycling | −0.0635 | kg CO2e/kg recycled | BUWAL 250; Ecoinvent | Table 1, Cimini & Moresi, 2016 |

| Plastic recycling (includes PE, not PVC) | −0.332 | kg CO2e/kg recycled | BUWAL 250; Ecoinvent | Table 1, Cimini & Moresi, 2016 |

| Glass recycling | −0.376 | kg CO2e/kg recycled | BUWAL 250 | Table 1, Cimini & Moresi, 2016 |

| Aluminum recycling | −10.6 | kg CO2e/kg recycled | BUWAL 250 | Table 1, Cimini & Moresi, 2016 |

| Steel recycling | −1.69 | kg CO2e/kg recycled | BUWAL 250 | Table 1, Cimini & Moresi, 2016 |

| Aluminum can production | 1.75 | tonnes CO2/tonne aluminum | 2017 Canadian National Inventory Submission to the United Nations Framework Convention on Climate Change (using 2015 inventory) | Table 2(I).A |

| Aluminum can (50% recycled) production | 8.96 | kg CO2e/kg can produced | International Aluminum Institute, 2013 | Table 1, Cimini & Moresi, 2016 |

| Aluminum can (99% purity) production | 11.5 | kg CO2e/kg can produced | Idemat 2001 | Table 1, Cimini & Moresi, 2016 |

| Green glass (net) | 0.314 | kg CO2e/kg glass | Turner, Williams & Kemp, 2015 | Table 6, calculated from study LCA (and in same Table, literature values listed) |

| Green glass (gross) | 0.395 | kg CO2e/kg green glass | Turner, Williams & Kemp, 2015 | Table 6, calculated from study LCA (and in same Table, literature values listed) |

| Brown glass (net) | 0.314 | kg CO2e/kg glass | Turner, Williams & Kemp, 2015 | Table 6, calculated from study LCA (and in same Table, literature values listed) |

| Brown glass (gross) | 0.395 | kg CO2e/kg glass | Turner, Williams & Kemp, 2015 | Table 6, calculated from study LCA (and in same Table, literature values listed) |

| Aluminum cans (net) | 8.143 | kg CO2e/kg | Turner, Williams & Kemp, 2015 | Table 6, calculated from study LCA (and in same Table, literature values listed) |

| Aluminum cans (gross) | 1.113 | kg CO2e/kg | Turner, Williams & Kemp, 2015 | Table 6, calculated from study LCA (and in same Table, literature values listed) |

| Mixed plastics (net) | 1.024 | kg CO2e/kg | Turner, Williams & Kemp, 2015 | Table 6, calculated from study LCA (and in same Table, literature values listed) |

| Mixed plastics (gross) | 0.339 | kg CO2e/kg | Turner, Williams & Kemp, 2015 | Table 6, calculated from study LCA (and in same Table, literature values listed) |

| Barley (produced Europe or USA) | 0.26 | kg CO2e/kg | BIER (2012) | Table 1, Cimini & Moresi, 2016 |

| Barley Malting | 0.292 (±) 0.084 | kg CO2e/kg | Chicago Manufacturing Centre (2009) | Table 1, Cimini & Moresi, 2016 |

| Barley malting | 0.000256277 | kWh/g malt | The Climate Conservancy (2008) | The Carbon Footprint of Fat Tire Amber Ale (report) |

| Fermentation | 15 | g CO2/473.176 mL | https://www.theguardian.com/environment/green-living-blog/2010/jun/04/carbon-footprint-beer | Value taken from book "How Bad are Bananas?: The Carbon Footprint of Everything" by Mark Berners-Lee (2010) |

| Hops emissions | 11.492766 | g CO2e/L beer | The Climate Conservancy (2008) | The Carbon Footprint of Fat Tire Amber Ale (report) |

| Max number of containers on ocean freighter | 10,000 | TEU/freighter ship | https://en.wikipedia.org/wiki/Container_ship | (TEU = Twenty-foot equivalent container units) |

| Max weight of one container on ocean freighter | 16,727,256 | g/container | https://en.wikipedia.org/wiki/Container_ship | (TEU = Twenty-foot equivalent container units) |

| bottle cap weights | 2.2 | g steel/bottle cap | ||

| 355 mL can weight | 14.9 | g aluminum/aluminum can | ||

| 473 mL can weight | 18.79 | g aluminum/aluminum can | ||

| Nuclear power generation | 0.15 | g CO2e/kWh | Intrinsik Corporation (2016) | Table E-1, page ii |

| Natural gas power generation | 525.00 | g CO2e/kWh | Intrinsik Corporation (2016) | Table E-1, page ii |

| Hydro power generation | 0.00 | g CO2e/kWh | Intrinsik Corporation (2016) | Table E-1, page ii |

| Wind power generation | 0.74 | g CO2e/kWh | Intrinsik Corporation (2016) | Table E-1, page ii |

| Biofuel power generation | 0.17 | kg CO2e/kWh | Intrinsik Corporation (2016) | Table E-1, page ii |

| Solar power generation | 6.15 | g CO2e/kWh | Intrinsik Corporation (2016) | Table E-1, page ii |

Appendix D

| Data Name | Data Type and/or Scope | Source |

|---|---|---|

| Electricity purchased | Primary data, Scope 2 | Case company primary contact, 2016 and 2017 |

| Fuel purchased | Primary data, Scope 1 | |

| Hops purchased | Primary data, Scope 3 | |

| Spring water purchased | Primary data, Scope 3 | |

| Municipal water used | Primary data, Scope 3 | |

| Waste generated | Primary data, Scope 1 | |

| Steam purchased | Primary data, Scope 2 | |

| Carbon dioxide purchased | Primary data, Scope 1 | |

| Glass bottles purchased | Primary data, Scope 3 | |

| Aluminum cans purchased | Primary data, Scope 3 | |

| Kegs purchased | Primary data, Scope 3 | |

| Secondary packaging purchased | Primary data, Scope 3 | |

| Return percentage of kegs and bottles | Primary data, Scope 2 and 3 | |

| Supplier information (location, number of shipments per year) | Primary data, Scope 3 | |

| Shipment method for each supplier | Primary data, Scope 3 |

References

- Olajire, A.A. The brewing industry and environmental challenges. J. Clean. Prod. 2012. [Google Scholar] [CrossRef]

- Statista. Beer Industry-Statistics & Facts. Available online: https://www.statista.com/topics/1654/beerproduction-and-distribution/ (accessed on 22 October 2018).

- Gómez-Corona, C.; Escalona-Buendía, H.B.; García, M.; Chollet, S.; Valentin, D. Craft vs. industrial: Habits, attitudes and motivations towards beer consumption in Mexico. Appetite 2016, 96, 358–367. [Google Scholar] [CrossRef] [PubMed]

- Institute for Prospective Technological Studies (IPTS). Environmental Impact of Products (EIPRO): Analysis of the Life Cycle Environmental Impacts Related to the Final Consumption of the EU-25. 2005. Available online: ec.europa.eu/environment/ipp/pdf/eipro_report.pdf (accessed on 22 October 2018).

- Cimini, A.; Moresi, M. Carbon footprint of a pale lager packed in different formats: Assessment and sensitivity analysis based on transparent data. J. Clean. Prod. 2016, 112, 4196–4213. [Google Scholar] [CrossRef]

- Cordella, M.; Tugnoli, A.; Spadoni, G.; Santarelli, F.; Zangrando, T. LCA of an Italian lager beer. Int. J. Life Cycle Assess. 2008, 13, 133–139. [Google Scholar] [CrossRef]

- Sturm, B.; Hugenschmidt, S.; Joyce, S.; Hofacker, W.; Roskilly, A.P. Opportunities and barriers for efficient energy use in a medium-sized brewery. Appl. Therm. Eng. 2013, 53, 397–404. [Google Scholar] [CrossRef]

- Rajaniemi, M.; Mikkola, H.; Ahokas, J. Greenhouse gas emissions from oats, barley, wheat and rye production. Agron. Res. 2011, 1, 189–195. [Google Scholar]

- Koroneos, C.; Roumbas, G.; Gabari, Z.; Papagiannidou, E.; Moussiopoulos, N. Life cycle assessment of beer production in Greece. J. Clean. Prod. 2005, 13, 433–439. [Google Scholar] [CrossRef]

- Mozny, M.; Tolasz, R.; Nekovar, J.; Sparks, T.; Trnka, M.; Zalud, Z. The impact of climate change on the yield and quality of Saaz hops in the Czech Republic. Agric. For. Meteorol. 2009, 149, 913–919. [Google Scholar] [CrossRef]

- Crowell, C. Bad News about This Year’s Barley Crop. 2014. Available online: https://www.craftbrewingbusiness.com/ingredients-supplies/bad-news-years-barley-crop/ (accessed on 22 October 2018).

- Beverage Industry Environmental Roundtable (BIER). Beverage Industry Continues to Drive Improvement in Water and Energy Use: 2016 Trends and Observations. 2016. Available online: http://www.bieroundtable.com/blank-c1gkm (accessed on 22 October 2018).

- Beverage Industry Environmental Roundtable (BIER). Joint Commitment on Climate Change. 2015. Available online: https://www.bieroundtable.com/single-post/2015/05/20/BIER-Releases-Joint-Commitment-on-Climate-Change (accessed on 22 October 2018).

- Ontario Craft Brewers Association (OCB). Ontario Craft Brewer’s Strategic Plan, 2018–2027. 2018. Available online: http://www.ontariocraftbrewers.com/About.html (accessed on 22 October 2018).

- Rice, J. Professional purity: Revolutionary writing in the craft beer industry. J. Bus. Tech. Commun. 2016, 30, 236–261. [Google Scholar] [CrossRef]

- Aquilani, B.; Laureti, T.; Poponi, S.; Secondi, L. Beer choice and consumption determinants when craft beers are tasted: An exploratory study of consumer preferences. Food Qual. Preference 2015, 41, 214–224. [Google Scholar] [CrossRef]

- Beverage Industry Environmental Roundtable (BIER). Research on the Carbon Footprint of Beer. 2012. Available online: http://www.bieroundtable.com/energy--climate (accessed on 22 October 2018).

- Cimini, A.; Moresi, M. Effect of brewery size on the main process parameters and cradle-to-grave carbon footprint of lager beer. J. Ind. Ecol. 2018, 22, 1139–1154. [Google Scholar] [CrossRef]

- Williams, A.G.; Mekonen, S. Environmental performance of traditional beer production in a micro-brewery. In Proceedings of the 9th International Conference on Life Cycle Assessment in the Agri-Food Sector, San Francisco, CA, USA, 8–10 October 2014; Schenck, R., Huizenga, D., Eds.; American Center for Life Cycle Assessment: Vashon, DC, USA, 2014; pp. 1535–1540. [Google Scholar]

- Lalonde, S.; Nicholson, A.; Schenck, R. Life Cycle Assessment of Beer in Support of an Environmental Product Declaration. Institute for Environmental Research and Education (IERE), 2013. Available online: http://iere.org/wp-content/uploads/2013/10/IERE_ Beer_LCA_Final.pdf (accessed on 10 December 2017).

- Amienyo, D.; Azapagic, A. Life cycle environmental impacts and costs of beer production and consumption in the UK. Int. J. Life Cycle Assess. 2016, 21, 492–509. [Google Scholar] [CrossRef]

- Tan, D.; Benni, D.; Liani, W. Determinants of corporate social responsibility disclosure and investor reaction. Int. J. Econ. Financ. Issues 2016, 6, 11–17. [Google Scholar]

- World Business Council for Sustainable Development and World Resources Institute (WBCSD & WRI). The Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard. 2004. Available online: http://ghgprotocol.org/corporate-standard (accessed on 22 October 2018).

- Food and Agriculture Organization of the United Nations (FAO). FAO Agribusiness Handbook: Barley, Malt and Beer. 2009. Available online: http://www.fao.org/fileadmin/user_upload/tci/docs/AH3_BarleyMaltBeer.pdf (accessed on 22 October 2018).

- Fish, H. Effects of the craft beer boom in Virginia: How breweries, regulators, and the public can collaborate to mitigate environmental impacts. William Mary Environ. Law Policy Rev. 2015, 40, 273–304. [Google Scholar] [CrossRef]

- Hoalst-Pullen, N.; Patterson, M.W.; Mattord, R.A.; Vest, M.D. Sustainability trends in the regional craft beer industry. In The Geography of Beer; Springer Science and Business Media: Dordrecht, The Netherlands, 2014; pp. 109–116. [Google Scholar]

- Molson Coors. Environmental, Social and Governance Report. 2017. Available online: http://www.molsoncoors.com/-/media/molson-coors-corporate/sustainability/esg-report-en.ashx (accessed on 22 October 2018).

- New Belgium Brewing. Carbon Emissions. 2017. Available online: http://www.newbelgium.com/Sustainability/Environmental-Metrics/GHG (accessed on 22 October 2018).

- Muster-Slawitsch, B.; Hubmann, M.; Murkovic, M.; Brunner, C. Process modelling and technology evaluation in brewing. Chem. Eng. Process. 2014, 84, 98–108. [Google Scholar] [CrossRef]

- Beverage Industry Environmental Roundtable (BIER). BIER: About. Available online: http://www.bieroundtable.com/about1 (accessed on 22 October 2018).

- Beverage Industry Environmental Roundtable (BIER). Beverage Industry Sector Guidance for Greenhouse Gas Emissions Reporting (Version 3.0). 2013. Available online: http://www.bieroundtable.com/energy--climate (accessed on 22 October 2018).

- The Climate Conservancy. The Carbon Footprint of Fat Tire® Amber Ale. 2008. Available online: http://www.ess.uci.edu/~sjdavis/pubs/Fat_Tire_2008.pdf (accessed on 22 October 2018).

- Baldwin, R. Regulation lite: The rise of emissions trading. Regul. Gov. 2008, 2, 193–215. [Google Scholar] [CrossRef]

- Harrison, K. A tale of two taxes: The fate of environmental tax reform in Canada. Rev. Policy Res. 2012, 29, 383–407. [Google Scholar] [CrossRef]

- Ontario Ministry of the Environment and Climate Change. Chapter 4: Cap and Trade. 2016. Available online: https://media.assets.eco.on.ca/web/2016/11/2016-Annual-GHG-Report_Chapter-4.pdf (accessed on 22 October 2018).

- Ontario Regulation 144/16: The Cap and Trade Program. Filed under the Climate Change Mitigation and Low Carbon Economy Act. Government of Ontario, 2016. Available online: https://www.ontario.ca/laws/regulation/r16144 (accessed on 22 October 2018).

- Syed, F. Here’s What You Need to Know about Ontario’s Termination of Cap and Trade. Canada’s National Observer, 2018. Available online: https://www.nationalobserver.com/2018/11/01/news/ontario-cancelled-its-cap-and-trade-program-amid-contradictions-and-inaccuracies-now (accessed on 22 October 2018).

- Ontario Craft Brewers Association (OCB). OCB Breweries List. 2018. Available online: http://www.ontariocraftbrewers.com/breweriesList.php (accessed on 1 February 2018).

- Ontario Craft Brewers Association (OCB). Ontario Craft Brewers-Industry Fact Sheet. 2018. Available online: www.ontariocraftbrewers.com/pdf/media_IndustryFactSheet.pdf (accessed on 15 January 2018).

- Comyns, B. Climate change reporting and multinational companies: Insights from institutional theory and international business. Account. Forum 2018, 42, 65–77. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W.W. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef]

- Miles, J.A. Management and Organization Theory; John Wiley & Sons, Inc.: San Francisco, CA, USA, 2012. [Google Scholar]

- Pishdad, A.; Haider, A.; Koronios, A. Technology and organizational evolution: An institutionalisation perspective. J. Innov. Bus. Best Pract. 2012, 1–12. [Google Scholar] [CrossRef]

- Beach, L.R.; Mitchell, T.R. Part one: An introduction to Image Theory. In Image Theory: Theoretical and Empirical Foundations; Ebook; Routledge: Abingdon-on-Thames, UK, 1998; pp. 9–20. [Google Scholar]

- Jayawardhena, C.; Morrell, K.; Stride, C. Ethical consumption behaviours in supermarket shoppers: Determinants and marketing implications. J. Purch. Supply Manag. 2016, 32, 777–805. [Google Scholar] [CrossRef]

- Thomas, D.R. A general inductive approach for analyzing qualitative evaluation data. Am. J. Eval. 2006, 27, 237–246. [Google Scholar] [CrossRef]

- Krippendorff, K. Content analysis: An Introduction to Its Methodology, 2nd ed.; Sage Publications, Inc.: Thousand Oaks, CA, USA, 2004. [Google Scholar]

- World Business Council for Sustainable Development and World Resources Institute (WBCSD & WRI). Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard. 2011. Available online: https://ghgprotocol.org/standards/scope-3-standard (accessed on 22 October 2018).

- World Business Council for Sustainable Development and World Resources Institute (WBCSD & WRI). Supplier Engagement Guidance. 2011. Available online: http://www.ghgprotocol.org/standards/scope-3-standard (accessed on 22 October 2018).

- World Business Council for Sustainable Development and World Resources Institute (WBCSD & WRI). Emission Factors from Cross-Sector Tools. 2017. Available online: http://www.ghgprotocol.org/calculationtools (accessed on 22 October 2018).

- Government of Canada. Canadian National Inventory Submission to the United Nations Framework Convention on Climate Change in National Inventory Submissions. 2017. Available online: http://unfccc.int/national_reports/annex_i_ghg_inventories/national_inventories_submissions/items/10116.php (accessed on 22 October 2018).

- Cook, C.; Inayatullah, S.; Burgman, M.; Sutherland, W.; Wintle, B. Strategic foresight: How planning for the unpredictable can improve environmental decision-making. Trends Ecol. Evol. 2014, 29, 531–541. [Google Scholar] [CrossRef] [PubMed]

- International Panel on Climate Change (IPCC). Climate Change 2014: Synthesis Report; Contribution of Working Groups I, II and III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Pachauri, R.K., Meyer, L.A., Eds.; IPCC: Geneva, Switzerland, 2014; Available online: http://www.ipcc.ch/report/ar5/syr/ (accessed on 22 October 2018).

- Schoemaker, P. Scenario planning: A tool for strategic thinking. Sloan Manag. Rev. 1995, 36, 25–40. [Google Scholar]

- Beer Canada. Industry Trends. 2017. Available online: http://industry.beercanada.com/statistics (accessed on 22 October 2018).

- Damelio, R. The Basics of Process Mapping, 2nd ed.; Productivity Press: New York, NY, USA, 2011. [Google Scholar]

- Patterson, R.E.; Pierce, B.J.; Bell, H.H.; Klein, G. Implicit learning, tacit knowledge, expertise development, and naturalistic decision making. J. Cogn. Eng. Decis. Mak. 2010, 4, 289–303. [Google Scholar] [CrossRef]

- Sloane, T.R. Green beer: Incentivizing sustainability in California’s brewing industry. Gold. Gate Univ. Environ. Law J. 2012, 5, 481–508. [Google Scholar]

- Barzagli, F.; Giorgi, C.; Mani, F.; Peruzzini, M. CO2 capture by aqueous Na2CO3 integrated with high-quality CaCO3 formation and pure CO2 release at room conditions. J. CO2 Util. 2017, 22, 346–354. [Google Scholar] [CrossRef]

- Marchi, M.; Neri, E.; Pulselli, F.; Bastianoni, S. CO2 recovery from wine production: Possible implications on the carbon balance at territorial level. J. CO2 Util. 2018, 28, 137–144. [Google Scholar] [CrossRef]

| Step Description | Standards and Supplementary Materials Referenced |

|---|---|

| Greenhouse gas accounting | |

| Meet with Company A to determine why they are interested in calculating their carbon footprint; what are their goals and intended use of this information. | Chapter 2 GHG Protocol ARS [23] |

| Set organizational and operational boundaries. Since Company A is independently owned and operated, its direct and indirect processes are included in the analysis. Operational boundaries determine whether direct (scope 1 and 2) or indirect emissions (scope 3) are to be included in calculations. Under the GHG Protocol, it is mandatory to account for scope 1 and 2 emissions, while scope 3 emissions are voluntary. Scope 3 emissions are recommended for inclusion when they are significant in magnitude, have future risk associated, and/or face sociopolitical instability (source i. and ii.). | i. Chapter 3 and 4 GHG Protocol ARS [23] |

| Since Company A is independently owned, the control approach as outlined in the GHG Protocol ARS3 is used, so all calculated GHGs are applied to Company A. For companies that have split ownership, use the equity approach to greenhouse gas accounting, where emissions are calculated and reported relative to ownership structure (source ii.). | ii. Chapter 3 GHG Protocol ARS3, [48] |

| Set a baseline from which to calculate greenhouse gas emissions. The greenhouse gas emissions in the baseline year will be used to inform reduction goals for the future. Data from 2016 is used for Company A. | Chapter 5 GHG Protocol ARS [23] |

| Collect primary data (provided by Company A) and identify as scope 1, 2 or 3. Use a centralized approach (primary data collected from Company A’s corporate office). Collect secondary data as required (i.e., emission factors) from external sources. Scope 3 emission data collection should be prioritized by its magnitude relative to other scope 3 emission sources (source i.). | i. Chapter 6 GHG Protocol ARS [23] |

| Calculation approaches should be documented and consistent; purchase records (i.e., fuel, electricity, other raw materials) and activity records (i.e., kilometers travelled) are appropriate sources of Company A data (source ii.). | ii. Chapter 7 GHG Protocol ARS3 [48] |

| Carbon dioxide, methane, nitrous oxide, hydrofluorocarbons, perfluorocarbons, and sulfur hexafluoride are the six GHGs included in calculations of scope 1, 2, and 3 emissions (source iii.). | iii. Glossary GHG Protocol ARS [23] |

| Work with the primary contact at Company A to identify and collect missing data appropriate for the GHG calculations. | Supplier Engagement Guidance [49] |

| Calculate greenhouse gas emissions from primary and secondary data. This is in line with the calculation method, with the alternative being the direct measurement method. Decisions as to whether to use primary or secondary data should be based on data availability and goals of the GHG accounting (source i.). | i. Emission-factors from cross sector tools [50] |

| Formula for calculation method (source ii): | ii. Chapter 6, 7 & 9 GHG Protocol ARS [23] |

| GHG = activity data x emission factor x greenhouse warming potential (GWP100) | iii. Chapter 7 GHG Protocol ARS3 [48] |

| Use sector-specific or cross-sector tools for GHG calculations. The most recent greenhouse warming potentials (GWPs) produced by the International Panel on Climate Change (IPCC) should be used with a 100-year horizon (expressed as GWP100) for conversion of all GHGs to carbon dioxide equivalents (CO2e) (source iii.). | iv. United Nations Framework Convention on Climate Change (UNFCCC) Canadian 2017 submission [51] |

| Maintain a clear record of data sources, assumptions, and calculations used. These records can be used to verify GHG calculations in an internal and/or external audit (source iv.). | |

| Design the GHG database to allow Company A to add, modify, and track emissions over time. | Chapter 3 GHG Protocol ARS [23] |

| Greenhouse gas reporting | |

| When publicly reporting GHG emissions, absolute values must be reported. Ratios can also be useful to report to compare performance over time. Common ratios to report include efficiency (unit GHG produced per volume of beer), productivity (GHG produced per dollar revenue), and percentage ratios to compare performance over years. | Chapter 9 GHG Protocol ARS [23] |

| Scenario analysis | |

| After reviewing the GHG calculations with Company A, recommendations for scenario analysis will be made to see how GHG amounts change due to internal and external changes. | [52,53,54] |

| Scenario 1: 10-Year Horizon CO2e with Beer Production Estimates x Bottle Versus Can Production Ratio | ||||

|---|---|---|---|---|

| Case Company Beer Production (hL) | ||||

| Primary Scenario | Intermediate Scenario | Advanced Scenario | ||

| Change (in hL) in beer packaged in bottles vs. cans | Primary Scenario | CO2e emissions estimate #1 | CO2e emissions estimate #2 | CO2e emissions estimate #3 |

| Intermediate Scenario | CO2e emissions estimate #4 | CO2e emissions estimate #5 | CO2e emissions estimate #6 | |

| Advanced Scenario | CO2e emissions estimate #7 | CO2e emissions estimate #8 | CO2e emissions estimate #9 | |

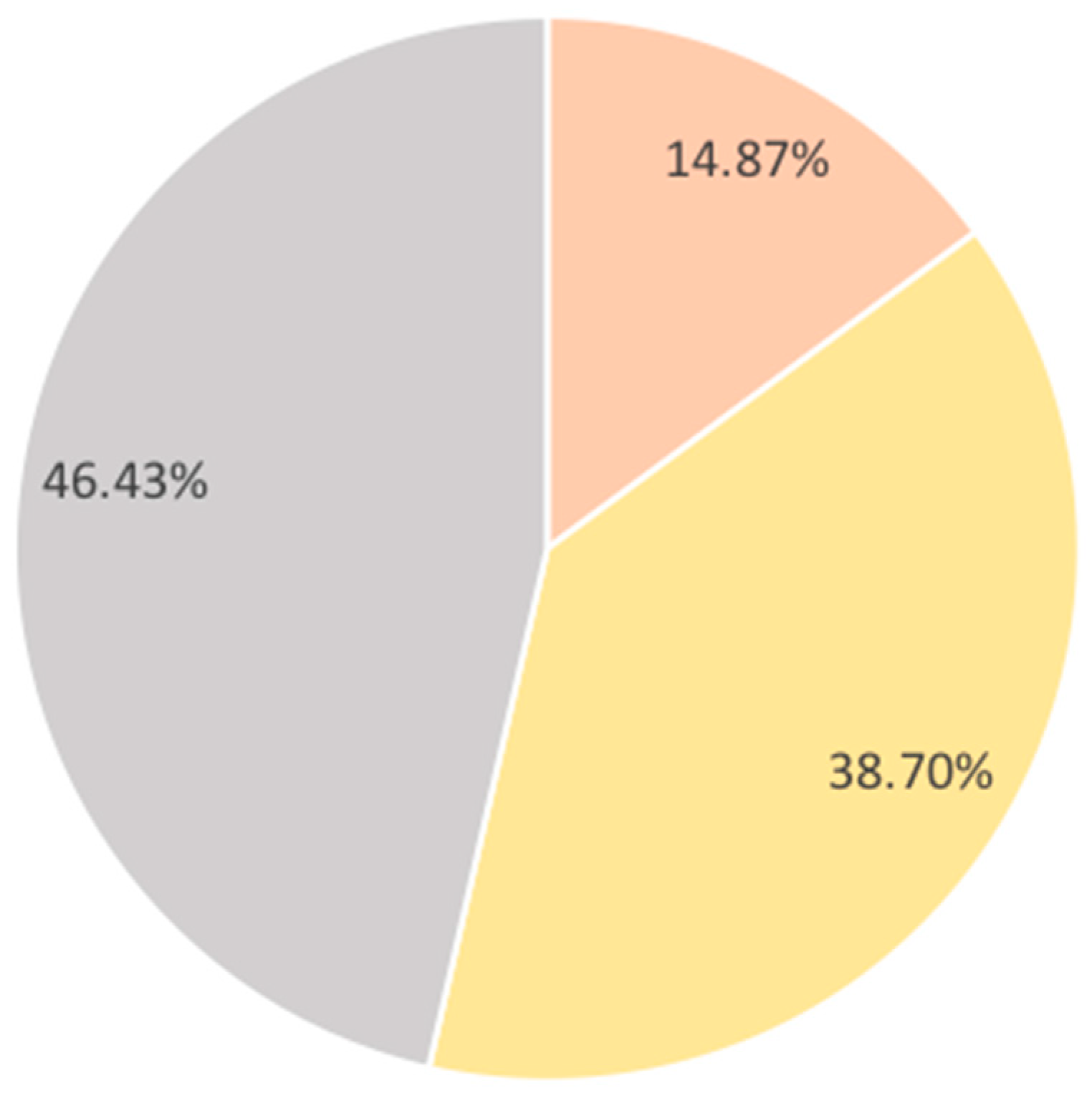

| Source | Scope | Category | Tonnes CO2e/Year | Percent (%) of Overall GHG Emissions |

|---|---|---|---|---|

| Diesel | Scope 1 | Mobile emissions | 178.98 | 4.20% |

| Gasoline | Scope 1 | Mobile emissions | 228.43 | 5.36% |

| B20 Biofuel | Scope 1 | Mobile emissions | 188.79 | 4.43% |

| Steam | Scope 2 | Purchased steam | 897.61 | 21.05% |

| Electricity | Scope 2 | Purchased electricity | 406.39 | 9.53% |

| CO2 bulk liquid | Scope 2 | Beverage production and warehousing | 337.14 | 7.91% |

| Barley agriculture | Scope 3 | Raw material processing | 457.56 | 10.37% |

| Malted barley transportation | Scope 3 | Transportation and distribution | 332.44 | 7.80% |

| Malting | Scope 3 | Raw material processing | 317.15 | 7.44% |

| Percent GHGs from top three sources from each scope | 78.09% | |||

| Scenario 1: 10-Year Horizon (2028): Tonnes CO2e/Year in Year 2028 with Beer Production Estimates x Bottle Versus Can Production Ratio | ||||

|---|---|---|---|---|

| Case Company Beer Production (hL) | ||||

| Primary Scenario (+18%) | Intermediate Scenario (+24%) | Advanced Scenario (+30%) | ||

| Change (in hL) in beer packaged in bottles vs. cans | Primary Scenario (no change) | 7959.86 | 8364.59 | 8769.34 |

| Intermediate Scenario (+10% cans, −10% bottles) | 7463.05 | 7842.53 | 8222.01 | |

| Advanced Scenario (+20% cans, −20% bottles) | 6966.25 | 7320.46 | 7674.68 | |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shin, R.; Searcy, C. Evaluating the Greenhouse Gas Emissions in the Craft Beer Industry: An Assessment of Challenges and Benefits of Greenhouse Gas Accounting. Sustainability 2018, 10, 4191. https://doi.org/10.3390/su10114191

Shin R, Searcy C. Evaluating the Greenhouse Gas Emissions in the Craft Beer Industry: An Assessment of Challenges and Benefits of Greenhouse Gas Accounting. Sustainability. 2018; 10(11):4191. https://doi.org/10.3390/su10114191

Chicago/Turabian StyleShin, Rachel, and Cory Searcy. 2018. "Evaluating the Greenhouse Gas Emissions in the Craft Beer Industry: An Assessment of Challenges and Benefits of Greenhouse Gas Accounting" Sustainability 10, no. 11: 4191. https://doi.org/10.3390/su10114191

APA StyleShin, R., & Searcy, C. (2018). Evaluating the Greenhouse Gas Emissions in the Craft Beer Industry: An Assessment of Challenges and Benefits of Greenhouse Gas Accounting. Sustainability, 10(11), 4191. https://doi.org/10.3390/su10114191