1. Introduction

The “Belt and Road” Initiative (BRI) was launched in 2013 as a consensus-based multinational cooperative framework that relies on existing Chinese dual multilateral mechanisms and existing regional cooperative platforms in particular countries. Borrowing from the ancient Silk Road, the BRI aims to actively develop economic cooperation with the countries along the nominated sea and land routes through the development of political mutual trust, economic integration, and cultural inclusion. In line with these BRI developments, Chinese firms have been progressively investing in countries along the route. OBOR (One Belt One Road) has become an important destination for China’s foreign direct investment. According to MOFCOM (Ministry of Commerce of People’s Republic of China) Statistics, in 2016 among the 196.2 billion US dollars of Chinese OFDI, there are 14.5 billion US dollars flowing into OBOR region which accounted for 8.5% of the total and increased by 72.49% compared with China’s OFDI stocks along OBOR by 2006. The proportion of Chinese OFDI along OBOR also increased from 6.81% in 2006 to 9.53% in 2016. Moreover, there is an obvious phenomenon of investment aggregation along the route. Within the OBOR region, 10 ASEAN countries attract the most investment from China and accounted for 55.29% of the total stock. Looking on the country-level, Singapore attracted nearly a quarter of Chinese OFDI along OBOR. Russia, Indonesia, Kazakhstan, etc. are also main destinations of Chinese OFDI (see

Appendix A Table A1,

Table A2 and

Table A3 for details). Looking on the firm-level, 56 cooperation zones have been established, and 107 state-owned enterprises (SOEs) had invested in BRI construction projects such as roads, ports, energy, engineering contracting, industrial parks, and other infrastructure facilities. Listed firms are actively participating in OBOR projects encouraged by all levels of governments.

Although BRI provided a package of stimulus such as financing facilities, registration conveniences, etc. which boost investments, OBOR countries’ political, economic, cultural, legal environmental differences, and instabilities are still obstacles for Chinese firms’ OFDI. Due to the uncertainties in the host countries’ market, and the inability to reverse the investment, Chinese firms often adopt a follow-up mode when making OFDI location decisions. Research has found that when Chinese firms are making location choices, their investment motives and investment layouts are often influenced by peers or trends, resulting in different levels of investment agglomeration [

1].

In recent years there has also been significant research into Chinese firm’ s OFDI locations and industry concentration, with many studies noting that Chinese OFDI firms tend to cluster in high-risk host countries [

2,

3,

4] and a stable and continuous agglomeration effect in Chinese OFDI has been discovered [

1,

5]. Although previous research has reached a certain degree of consensus on the foreign investment decision-making behavior of Chinese firms, these studies has been mostly limited to country-level data. However, for comprehensive BRI analysis, there needs to be a more detailed examination of firm-level location policies to provide concrete evidence for the institutional factors associated with the agglomeration effect. To do this, a Probit model is employed to estimate the effects of Chinese OFDI agglomeration and non-Chinese FDI agglomeration in host economies on investment location choices from 2004 to 2015. Using a large dataset constructed from detailed individual firm OFDI events information, it was possible to measure the effects of the country of origin and the industry on a firm’s location choice. It is also examined whether firms tend to invest more in OBOR countries after the BRI. Finally, firm investments are linked with firm characteristics such as size, profitability, and productivity. Somewhat different from Head et al. [

6], this study found that Chinese investors preferred to locate near other Chinese firms in a host country rather than near non-Chinese firms. As the Probit estimation results revealed that more Chinese firms tended to locate in OBOR countries after 2013, an FGLS model was used to determine the types of firms that had clustered in OBOR countries when making OFDI location choices.

This research contributes to existing literature on agglomeration economies, international firm location choices, foreign direct investment, and institutional interventions from home countries. To the best of our knowledge, this is the first study of agglomeration effects on Chinese investment location choices under the BRI. The empirical results are particularly important for Chinese firms as well as authorities when seeking to design policies aimed at promoting OFDI.

The remainder of this paper is organized as follows. Following the literature review on localization and the presentation of the hypotheses in

Section 2, in

Section 3, the dataset and variables are described, and in

Section 4, the methodology and empirical results are presented.

Section 5 gives the final conclusions from the analyses.

2. Literature Review

Industry localization is defined as “the geographic concentration of particular industries” [

6]. One of the mechanisms motivating this type of concentration is the existence of agglomeration economies, which are positive externalities that stem from the geographic clustering of certain industries. In this context, the investing firms contribute to and benefit from the externalities [

7]. The theory of agglomeration economies was first introduced by Marshall [

8], who outlined three reasons for the clustering of similar firms from the same industries; a pooled market for workers with specialized skills, easier development of specialized inputs and services, and benefits from technological spillovers. Krugman [

9] and Saxenian [

10] later constructed formal models to analyze and extend the agglomeration economies concepts. Research has found that multinational corporations tend to take a networked production coordination approach with associated companies in specific agglomeration areas to achieve optimal economies of scale, which often means that foreign investment location choices are highly aggregated. Consequently, the agglomeration effect has become a factor when determining a firm’s OFDI behavior, not only in their investment location choice, but also in the industries in which the firms belong; that is, firms from the same industry sector tend to follow each other’s investment choices [

11,

12,

13,

14,

15,

16].

Firms are able to enhance their performance by the positive externalities generated through agglomeration. Marshall [

8] identified three externalities that stemmed from industry localization: technological spillovers, a pooled market of workers with specialized skills, and a pool of specialized intermediate inputs for the industry. Generally, it has been found that firms can benefit from geographical localization in agglomeration economies. To date, there have been two types of studies on agglomeration benefits. The first have been qualitative studies that identify industry clusters and documented agglomeration externality mechanisms [

9,

10], and the second have been empirical studies that sought to determine the accruing benefits when a firm located near to other firms in the same industry or from the same country of origin. For example, the empirical research of Head et al. [

6], Head and Ries [

17], Head, Ries and Swenson [

18], Crozet et al. [

19], Guimaraes et al. [

13], and Coughlin and Segev [

20] all found that firms in the same industries and from the same countries of origin tended to locate near to each other. However, Shaver and Flyer [

7] found that in many agglomeration economies, many firms performed better if they did not cluster as firms are able to gain benefits from agglomeration economies as well as contribute. Therefore, large firms with better technologies, human capital, training programs, suppliers, and distributors often attempt to locate away from their competitors because the benefits they gain from locating near their competitors are less than the benefits the competitors gain from them.

In this study, based on the OFDI patterns in China, six hypotheses aimed at verifying the existence of agglomeration economies are tested.

Head et al. [

18] argued that the agglomeration effects between Japanese firms may have appeared because of their different characteristics from the firms of other countries. For example, the preference for higher skilled workers because of a stronger desire for quality control or the greater use of complex machinery could motivate a new Japanese firm to locate near earlier arrivals so as to hire employees who had already been trained in Japanese methods. Chinese OFDI research into investment locations and industry concentrations has suggested that Chinese OFDI firms have tended to focus on high-risk host countries [

2,

3,

4]. So, firm’s OFDI location decision tends to follow their Chinese peers for safety reasons. Qi and Liu [

21] studied the influence of past experience on Chinese OFDI location choices and found that OFDI firms conducted sequential market selection based on the investment experience of other firms, which they described as a “herd effect”. Therefore, it is possible to expect that there is an empirical relationship between the location choice or industry choice by new Chinese firms and prior Chinese firm investments in a particular host country. Based on the location patterns of Chinese multinationals, it is proposed that Chinese investors tend to concentrate in a particular region or industry. Based on existing findings, therefore, we developed the following Hypothesis 1:

Hypothesis 1. New Chinese investors tend to invest in host countries that already have large Chinese origin FDI stock.

Empirical research on different countries—Boudier-Bensabaa [

22] on Hungary, Meyer and Nguyen [

23] on Vietnam, Head and Ries [

18] and Cheng and Ruan [

24] on China, Crozet et al. [

19] on France, and Guimaraes et al. [

13] on Portugal—all found that new foreign firms were likely to locate near to other foreign investors so as to use the experience and performance of the earlier investors as indicators of the underlying business climate at the specific location. Therefore, it is possible that there is an empirical relationship between the location choice of a new foreign firm and prior investment by other foreign firms in a particular destination. The lagged volume of FDI to the same host countries is used as a proxy for country-specific agglomeration; therefore, we developed the following Hypothesis 2:

Hypothesis 2. New Chinese investors tend to invest in a host country that has already attracted a large volume of foreign FDI.

Head, Ries, and Swenson [

18], Crozet et al. [

19], Guimaraes et al. [

13], and Coughlin and Segev [

20] also found that firms in the same industry tended to invest near to each other and that the types of industry played an important role when choosing which home country firms to invest in. Because of obvious information asymmetry, firms pay more attention to the behavior of firms in similar industries when making their investment decisions [

25]. As international mutual investment inevitably affects the competitive environment in the investing countries and the international market, firms pay attention to their counterparts’ investment decisions, and therefore, to reduce competition and avoid uncertainties from the industry side, firms tend to follow the investment decisions of pioneer firms [

26]. Lin [

27] had suggested that there was a “surge phenomenon”, whereby firms from a developing country are likely to reach a consensus when selecting new and promising industries due to information asymmetry, which then resulted in clustered investment in the identified industry. Therefore, compared to other industries in the home country, firms from the same industry in the same country affect the investment decision-making of later firms. Hence, we propose Hypothesis 3:

Hypothesis 3. New Chinese investors tend to invest in an industry that has already attracted large Chinese OFDI.

Multinational investors and especially investors from developing countries have a strong demand for local knowledge in the host country [

28,

29]. Usually, if a firm wants to acquire local knowledge, it can choose to invest in the industrial agglomeration areas of the host country, interact with the local firms, and conduct horizontal and vertical learning [

30,

31]. Therefore, the industrial agglomeration areas in the host country have a strong attraction to international firms, especially in the manufacturing sector. The higher the level of local industrial agglomeration, the more the knowledge spillover. Regions with relatively high industrial agglomeration levels, therefore, attract upstream and downstream firm agglomeration and related services [

32], all of which enables firms to improve their production efficiencies [

9,

33]. Therefore, Hypothesis 4 was developed to assess Chinese firms’ response to host-country industrial agglomeration when conducting OFDI.

Hypothesis 4. Larger shares of certain industries in host countries attract a greater number of new Chinese investors in the same industry.

The BRI aims to connect China more closely to Central Asia, Southeast Asia, South Asia, Russia, and the Baltics. The BRI has proven effective as the Chinese government strongly promotes investment in OBOR countries. Before 2013, OBOR related countries had not been the main destinations for Chinese OFDI, only accounting for 10.8% of total Chinese OFDI. After 2013, however, the OBOR related countries became a preferred destination for construction project investment. In 2015, Chinese OFDI investment projects tended to be infrastructure facilities such as railways, airports, power grids, water conservancies, and port engineering, at over 70% of all Chinese OFDI. New foreign construction project contracts signed between China and OBOR related countries reached a record high of 92.6 billion USD and accounted for 44% of the total newly signed foreign construction projects (MinSheng Securities Research Institute, “Belt and Road” Report 2015.). Researches show the labor force, natural resources endowment, and bilateral investment agreements in OBOR areas have a significant role in promoting investment [

34]. Some scholars empirically analyze the industrial comparative advantages and complementarity between China and the countries (regions) along the route, and point out that the optimal choice of the countries and industries along the route can speed up the international industrial chain layout of domestic industries, accelerate the transfer of excess capacity and boost manufacturing upgrade [

35,

36]. Bilateral investment agreements (BIT) signed between China and OBOR countries play a particularly significant role in promoting and protecting Chinese firms’ foreign direct investment and encouraging investment activities in these areas [

35]. As this paper is assessing the links between the BRI and Chinese OFDI agglomeration and the effect of BRI on firm location choices, Hypothesis 5 was developed:

Hypothesis 5. The BRI encourages new Chinese investors to locate in countries along the OBOR route.

This paper further analyzes the characteristics of firms investing in OBOR countries. Firms that are actively investing in OBOR countries are generally those that are facing fierce domestic competition and eagerly seeking outlets for their excess productivity [

4]. One motivation behind the BRI was the urgent need for industrial structural upgrading especially for industries that had surplus capacity in China such as infrastructure construction. When Chinese domestic markets reached saturation, many firms began to experience profitability and productivity decreases. Based on existing literature, the relationship between FDI and firm labor productivity is found to be highly connected. Generally, OFDI promotes parent firm’s labor productivity and total factor productivity through reverse technology spillover effect. In addition, scholars also explained that firms with higher productivity will take more FDI actions [

37,

38,

39].

Relating to Chinese OFDI, one strand of researches agrees that OFDI firms have productivity advantages, and the higher the productivity of the firm, the greater the possibility of OFDI [

40,

41]. Another strand of researches argues firms with bigger total asset and revenue but lower productivity tend to invest more in host countries and Chinese OFDI has poor performance financially [

42,

43,

44], and firms with low efficiency can hardly generate a synergy effect when they conduct direct investment internationally [

40,

41], especially in a very uncertain overseas investment environment. Tang Xiaojun and Zhang Jinming [

41] found that compared with the heterogeneous factor of productivity, the nature of firm ownership plays a more important role in Chinese manufacturing firms’ FDI, and state-owned firms have more advantages in OFDI but lower productivity compared to private firms. Consequently, under the “OBOR” initiative, the government emphasizes that large state-owned enterprises should become the main body and support of the construction, and play a more active role in participating in international competition and international capacity cooperation [

35,

45,

46]. Large state-owned firm began playing a dominant OFDI role in the BRI countries; with this in mind, we developed Hypothesis 6:

Hypothesis 6. Chinese firms investing more in OBOR countries are larger but have lower productivity and profitability.

5. Conclusions and Implications

This paper developed four agglomeration variables for Chinese OFDI at both the industry and country level, based on which, the following conclusions were made.

(1) There was an obvious agglomeration effect on host country selection for Chinese OFDI. Firms were found to follow other Chinese firms and invest in host countries where previous Chinese investment was concentrated, and were found to avoid countries that had large non-Chinese FDI in general. By breaking full sample countries to four continents, differences are revealed due to OFDI motivations and heterogeneity of continents. In Asia and Europe, firms tend to invest in countries that has less Chinese investment agglomeration. In Arica and America, the results show positive tendency for Chinese firms’ investment decision related to previous Chinese investment agglomeration.

(2) There was also an obvious agglomeration effect in terms of Chinese OFDI industry selection. Firms were found to prefer to invest in industries for which there was already a large Chinese OFDI agglomeration or high host-country related industry agglomeration.

(3) The BRI was found to be influential in encouraging OFDI location decisions, with many firms choosing to tend to invest along the “Belt and Road” route.

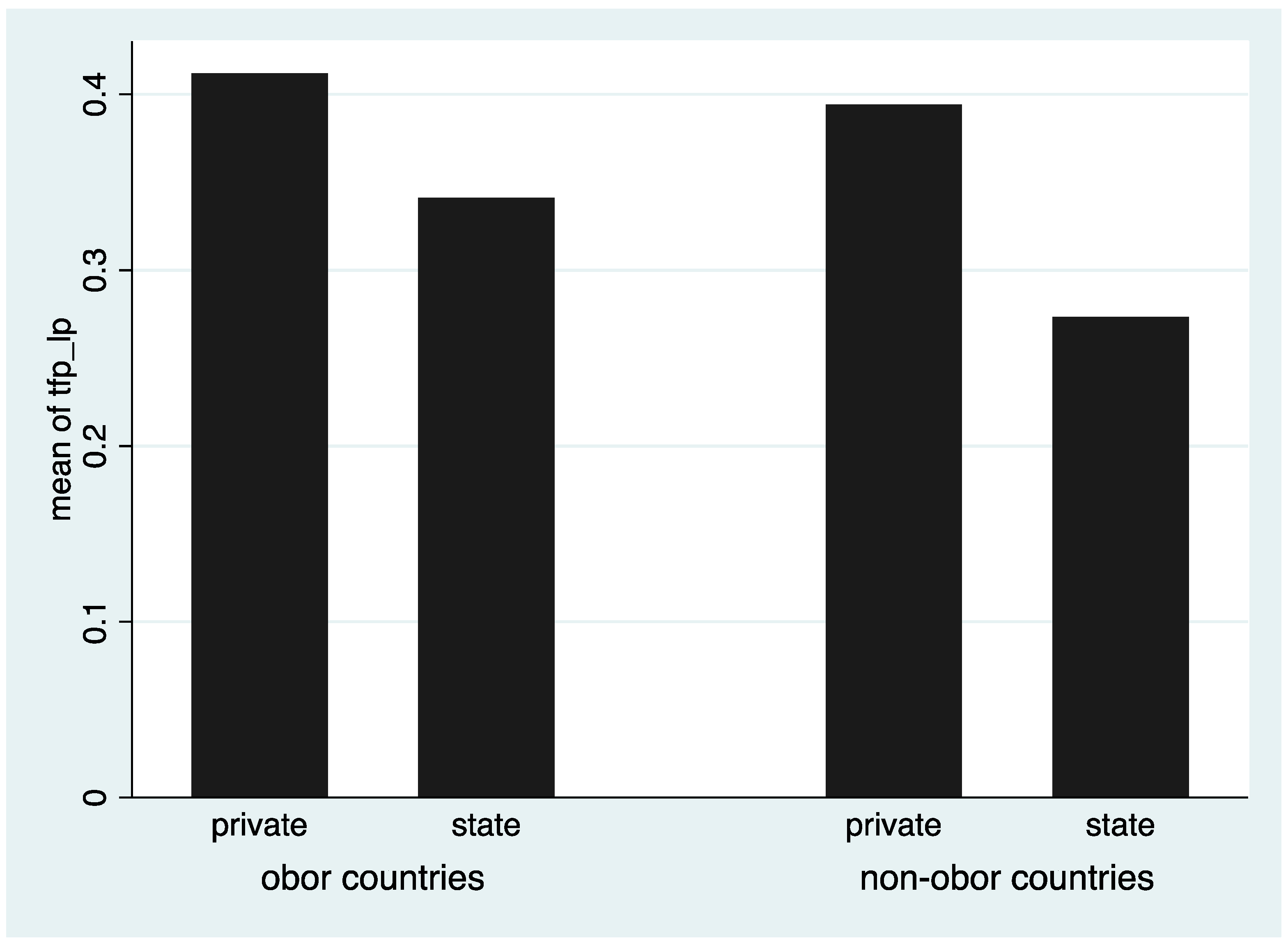

(4) Listed larger firms with higher leverage and lower productivity (Tfp_lp or lproductiviey_add) and profitability were more likely to invest along the “Belt and Road”, with state-owned firms being more active investors in large projects in the OBOR countries.

From this analysis of Chinese OFDI, it was concluded that the agglomeration effect should be seen as an important index when evaluating host country location or industry selections. OFDI policies should be carefully designed to have a guiding effect on Chinese firm location choices. Medium-sized firms and private firms should be encouraged to be more responsive to OFDI as they are generally more productive, efficient, and adaptable to competition. To assist firms avoid any irrational follow-up behavior caused by information asymmetry, the relevant authorities need to establish effective information dissemination channels to further promote the smooth flow of investment information between firms and reduce the risk and investment cost in foreign countries, and especially in those with poor political and financial environments.

{kind=link}

{kind=link}

{kind=link}