Abstract

The automobile industry is shifting from internal combustion engine vehicles (ICEVs) to hybrid electric vehicles (HEVs) or electric vehicles (EVs) extremely fast. Our calculation regarding the most popular private car brand in Bangladesh, Toyota, shows that the life cycle cost (LCC) of a Toyota BZ3 (EV), USD 43,409, is more expensive than a Toyota Aqua (HEV) and Toyota Prius (HEV), but cheaper than a Toyota Axio (ICEV) and Toyota Allion (ICEV). It has been found that about a 25% reduction in the acquisition cost of a Toyota BZ3 would lower its LCC to below others. EVs can be a good choice for those who travel a lot. Changes in electricity prices have little effect upon the LCC of EVs. With the expected decline in the annual price for batteries, which is between 6 and 9%, and the improvement of their capacities, EVs will be more competitive with other vehicles by 2030 or even earlier. EVs will dominate the market since demand for alternative fuel-powered vehicles is growing due to their environmental and economic advantages.

1. Introduction

Renewable and alternative energy technologies are becoming more and more crucial for future energy generation and storage [1]. The environmental, economic, and health impacts resulting from the greenhouse effect is a primary concern all over the world. The transportation sector is one of the main contributors to greenhouse gas (GHG) emissions worldwide. The transportation sector is responsible for over 20% of energy-related CO2 emissions and about 15% of worldwide GHG emissions [2,3]. One of the potential solutions aimed towards lowering GHG emissions is the adoption of electric vehicles and alternative fuels such as hydrogen [4,5]. Mainly three types of vehicles are available in the world, i.e., internal combustion engine vehicles (ICEV), Hybrid electric vehicles (HEVs), and electric vehicles (EV). The global automobile industry, which is dominated by ICEVs, is gradually shifting towards EVs from conventional vehicles. Among the three types, EVs require no fossil fuels and provide less emissions than HEVs and ICEVs [6]. The present EVs are mainly powered by rechargeable batteries [7], but fuel cell-based EVs are also getting popular due to their advantages [8]. The thermal management of battery stacks is one of the major concerns related to maximizing EVs’ efficiency [9]. Moreover, EVs will reduce dependence on fossil fuels, which are not only expensive but also scarce in nature. The automobile industry is one of the fastest-growing sectors in developing countries like Bangladesh. In Bangladesh, the average growth rate of the automobile industry is about 5.6% per year, and it has become an industry worth USD 1 billion (BDT 110,000 million). The nation’s middle and higher middle classes’ growing purchasing power and socioeconomic development have contributed to the industry’s steady growth. The Bangladesh Road Transport Authority (BRTA)’s data indicate that between 2011 and 2020, the number of passenger cars grew at a compound annual growth rate of 5.43%. However, Bangladesh still has a relatively low passenger car penetration rate—just 0.5 cars per 1000 people—when compared to other Asian nations. By the end of 2018, 30 out of 1000 persons in India were automobile owners. Twelve out of every thousand persons in Myanmar possess an automobile. The decreasing number of cars on the road can be attributed to various factors, such as high acquisition costs, higher car taxes, limited and inadequate national roadways, high traffic density, high fuel prices, higher interest rates on private car loans, and insufficient parking spaces. As of May 2021, 4,729,393 vehicles were registered in Bangladesh, according to the BRTA’s data. Of all the vehicles registered, 544,616 are passenger automobiles, or roughly 11.52% of the total. The market for automobiles is once again dominated by sedans, which account for about 68% of the passenger car market. Sports utility vehicles (SUVs) and microbuses cover 12.40% and 19.27% of the total.

By types of fuels, more than 95% of cars in the country are ICEVs, and the rest are HEVs. However, hybrid electric vehicle imports are steadily increasing in the country. Hybrid car imports in Bangladesh increased by 154% from 3296 units in the 2017–2018 financial year to 8.366 units in the 2020–2021 financial year. Hybrid cars in Bangladesh include the Toyota Axio, Honda Grace, and Nissan X-trail. Hybrid vehicles are becoming more and more popular among buyers due to the fact that hybrid vehicles have lower tax rates than gasoline-fueled vehicles. All car brands are going to introduce EV cars in the future. A standard 1500 cc car can go up to 7 to 10 km/L, while a hybrid car of the same cc can go up to 15 to 25 km/L. Apart from engines, hybrid cars have motors that give extra brake horsepower to the car. So, compared to a gasoline-fueled version of a similar cc car, hybrid models give extra power to the car. Due to this, hybrid cars can benefit from lower cc import duty rates but provide power like higher cc cars. Electric vehicles are making their way into the country following the introduction of hybrid vehicles. The import tax rates for EVs in Bangladesh are currently very low. Gasoline-fueled CBU vehicles face import duties ranging from 128% to 827%. In contrast, the Total Tax Incidence (TTI) for electric vehicles stands at 59%, which is nearly half of the tax burden on the least taxed imported gasoline-fueled vehicles. Some models, like the ‘Tesla’ and ‘Porsche Taycan’ models, have already been brought into Bangladesh. However, challenges such as the lack of charging infrastructure, insufficient power supply, the scarcity of spare parts, limited technical know-how, and poor road conditions hinder the widespread adoption of EVs in the market.

The government of Bangladesh has made a firm commitment to reducing carbon emissions to 21.85% by 2030, reflecting their concern for the environment. Despite the country’s contribution of only 0.21% to global carbon dioxide emissions, there is a worrisome average annual growth rate of 7.52%. Local manufacturers are taking steps to address the challenges associated with electric vehicles (EVs), with there being a significant increase in the number of electric three-wheelers in recent years. However, the adoption of electric cars still faces obstacles due to consumers’ limited purchasing capacity and lack of motivation. Dandan Chen, the Acting World Bank Country Director for Bangladesh and Bhutan, highlighted that air pollution is a significant economic burden on Bangladesh, leading to premature death and worsened health. In 2019, air pollution ranked as the second leading cause of deaths and disability in Bangladesh, costing approximately 3.9 to 4.4 percent of the country’s GDP. The 2020 automotive industry development policy, released by the Ministry of Industries, offers opportunities for both domestic and international investors to establish local assembly plants. This policy includes financial benefits for constructing assembly plants and tax breaks for importing semi-knocked down (SKD) and completely knocked down (CKD) parts to support local assembly processes. The presence of hybrid cars on the roads of Bangladesh is steadily increasing, and importer–dealers are optimistic that their popularity will continue to rise over the next five to ten years, potentially leading to a significant reduction in the use of fossil fuel vehicles.

Life cycle cost analysis (LCCA) is a crucial tool that can be utilized to assess the viability of a product during its initial production phase [10]. The aim of this study is to evaluate the feasibility of upcoming EVs in the Bangladeshi automobile market by conducting an LCC analysis and comparing them with existing ICEVs and HEVs. While the data parameters are tailored for the Bangladeshi market, the methodology employed in this research can be easily applied for evaluating the competitiveness of EVs in other economies as well.

2. Literature Review

A small number of studies have been conducted so far on the LCC analysis of EVs in the contexts of different countries. Abas et al. [11] performed a comprehensive feasibility study of EVs in the Bruneian market through an LCC analysis and compared the LCCs of EVs, ICEVs, and HEVs. This study indicates that electric vehicles (EVs) remain costly in comparison to internal combustion engine vehicles (ICEVs) and hybrid electric vehicles (HEVs) in Brunei, primarily due to their high acquisition cost, which significantly impacts their life cycle cost (LCC). To encourage the adoption of EVs and discourage other vehicle types, it is suggested that a direct government subsidy be implemented alongside an increase in the current gasoline price. A different study was conducted to examine the cost competitiveness of EVs in relation to hybrid electric vehicles (HEVs) and an Internal Combustion Vehicle (ICV) [12]. The researchers performed a life cost analysis (LCC) on two EVs and compared them to HEVs and ICVs. The findings indicate that the Nissan Leaf and BMW i3s EVs, with LCC values of USD 1.75 and USD 2.5 per km, are not cost-competitive when compared to HEVs and ICVs. The sensitivity analysis revealed that the operating costs have a significant impact on the overall cost of owning an EV, while the cost of owning HEVs and ICVs did not experience any significant influence. Despite the lower emission costs and vehicle use costs of electric vehicles, they are still unable to offset the difference in initial purchase costs. A similar conclusion was drawn from a study conducted on the Australian automobile market which revealed that the 2011 Nissan Leaf, an electric vehicle, has a higher total life cycle cost compared to its ICEV counterpart (the Toyota Corolla). The authors of [13,14] achieved remarkable findings in their studies. Research indicates that the life cycle cost (LCC) of an electric vehicle (EV) is approximately 9% higher than that of an internal combustion engine vehicle (ICEV) based on the driving cycle in Beijing in 2020. Moreover, the life cycle greenhouse gas (GHG) emissions of an EV are around 29% lower compared to those of an ICEV. If the lifetime mileage falls short of expectations, the difference in LCC would widen, while the variance in GHG emissions would decrease. Ayodele and Mustapa [10] revealed a discrepancy in life cycle cost (LCC) among the various EVs they examined, which can be attributed to several factors. The findings indicate that, considering the LCC, EVs are still not on par with conventional internal combustion engine cars due to the expensive nature of batteries [15]. Furch et al. [16] have emphasized the development of a mathematical model for the calculation of the life cycle costs of passenger vehicles. Their analysis indicates that the most favorable choice in terms of life cycle cost (LCC) within the passenger car category is the combination of petrol and CNG propulsion. Despite the current restrictions on emissions, diesel-fueled cars are also highly regarded. Additionally, this model highlights one drawback of electric vehicles, namely their limited battery lifespan or reduced capacity below a predetermined threshold. Consequently, electric vehicles fail to meet the minimum range criteria. Mixed results have been documented in Europe regarding this matter. According to Yan S. [17], the life cycle cost (LCC) of electric vehicles (EVs) is lower than that of internal combustion engine vehicles (ICEVs) in France, Norway, and the UK. However, in Italy, Austria, Hungary, Portugal, and Germany, the LCC of EVs is higher. Another study by Fuentes and González [18] found that the LCC of EVs surpassed that of ICVs, with acquisition costs being the primary contributor to the overall LCC, followed by maintenance costs. In order to encourage the adoption of EVs, it is crucial to reduce either the acquisition costs or the battery costs. In the context of Bangladesh, a Strengths, Weaknesses, Opportunities, and Threats (SWOT) analysis together with Analytic Hierarchy Process (AHP), a multicriteria decision-making technique, was applied to conduct a SWOT-AHP analysis on the nation’s automobile industry. The electric vehicle SWOT-AHP analysis shows that the strengths and opportunities are looking brighter [19]. Additionally, the analysis identified some threats, such as energy crises, undeveloped infrastructure, political instability, etc.

The majority of studies have reached the consensus that EVs are not economically competitive with HEVs and ICEVs in various countries due to a range of factors. However, the attractiveness of EVs increases in comparison to ICEVs and HEVs as the distance traveled by the vehicle increases [20]. Several crucial factors, such as tax structure [17], acquisition costs [11], the costs of gasoline and electricity, maintenance costs, and the costs of electricity and battery replacement, play a significant role in determining the competitiveness of EVs in the market [13].

From the literature review, it was found that an LCC analysis of EVs in Bangladesh has not yet been carried out. This paper aims to fill this knowledge gap so that both potential customers and policy makers can utilize the results for better decision making.

3. Methodology

3.1. Vehicle Selection

This study assesses the feasibility of electric vehicles (EVs) in Bangladesh by comparing their life cycle cost (LCC) with the prevalent hybrid electric vehicles (HEVs) and internal combustion engine vehicles (ICEVs) in the market. Toyota, renowned for the cost efficiency, durability, and ease of maintenance of their vehicles, has emerged as the dominant brand in Bangladesh. Although a specific electric model from Toyota, the BZ3, has not yet been introduced to the Bangladeshi market, its potential attractiveness lies in its affordability, a key consideration for Bangladeshi consumers. This hypothetical scenario offers an insight into the possible market dynamics should the Toyota BZ3 be launched. Figure 1 shows an image of a Toyota VZ3 electric car.

Figure 1.

Toyota VZ3 electric vehicle (meaning of Chinese letters in the plate is: Car Home).

In this study, we sought to represent both the hybrid electric vehicle (HEV) and internal combustion engine vehicle (ICEV) categories by selecting two models from each category based on their popularity and affordability. For the ICEV category, the Toyota Axio and Toyota Allion were chosen, providing valuable insights into options commonly accessible to the average consumer in Bangladesh [21]. In contrast, the HEV category features the Toyota Prius and Toyota Aqua, two prominent choices available in the Bangladeshi market. These models are renowned for their ability to strike a harmonious balance between performance and fuel efficiency, making them highly appealing to consumers who prioritize both environmental friendliness and cost-effectiveness. Luxury cars are excluded from the analysis. The decision-making factors for luxury car buyers, which are primarily not cost-driven and characterized by a wide price range, diverge significantly from the general consumer market. Including luxury cars would introduce a disparity in comparison, detracting from the realistic assessment of vehicle options available to most of the consumers in Bangladesh. Table 1 lists the major specifications of the selected vehicles (BZ3, Aqua, Prius, Axio and Allion).

Table 1.

Major specifications of the selected vehicles.

The selection of these specific models allows for a comprehensive comparison across different vehicle types, providing valuable insights into the potential shift towards more sustainable automotive options in Bangladesh.

3.2. Life Cycle Cost Calculation

The life cycle cost (LCC) encompasses the sum of all costs associated with an object over its lifespan, discounted to their present values [22]. This approach, integral for economic evaluations, encompasses acquisition costs, operating costs, maintenance expenses, and the salvage value of vehicles. Present value (PV) calculations are pivotal in determining LCCs [23], with the relationship between current and future values commonly given as follows:

Here, PV = present value, FV = future value, i = number of periods, and r = discount rate (or cost of capital). Using Equation (1), the LCC, encompassing all vehicle-related costs, may be calculated:

where AC is the initial acquisition cost of the vehicle. and are the operating and maintenance costs of the vehicle incurred in year i, whilst is the salvage value of the vehicle or its components, particularly the battery, in year i. Acquisition cost is the only cost not affected by the interest rate, as it is incurred at the beginning of the period.

3.2.1. Acquisition Cost

The acquisition cost is the amount of money spent to obtain title of ownership to a property. This includes the purchase price plus the registration fess for a new car, including its initial registration, the fitness certificate, the route permit, etc. Without these payments, a person cannot claim the title of ownership of a car in Bangladesh. The acquisition cost (AC) includes the manufacturer’s suggested retail price (MSRP) and the registration fees for new cars. The MSRP, the price recommended by a manufacturer at the point of sale, is a significant component of the high acquisition cost of EVs, primarily due to the high cost of its battery. A decline in the costs of batteries due to technological advancement and economies of scale is expected to reduce the acquisition costs of EVs, making EVs more affordable to the general public. The MSRP also depends largely on import taxes, which are very high in comparison to other countries. Typically, the import value-added tax (VAT) stands at 15%. For a 1500 cc engine, there is a 45% import duty, while engines up to 2000 cc incur a 100% import duty fee. Beyond 2000cc, the import duty fee increases to 200% based on the engine size. In addition to these charges, there are supplementary duty (SD) and regulatory duty (RD), which are calculated as 100% of the cost, insurance and freight (CIFD) value and 4% of the CIFD plus the supplementary duty (SD) value, respectively. Advance Income Tax (AIT) is also applicable at a rate of 5% of the CIFD value. Importers should also consider expenses related to transportation, insurance, and other miscellaneous costs. Although EVs’ engine displacement is not measured in cc units, the Bangladesh Road Transport Authority (BRTA) assumes that 1 kWh is equivalent to a 20 cc engine to impose tax or supplementary duty. The MSRP includes the aforementioned fees. Table 2 shows the import taxes as a percentage of the import prices.

where AC = acquisition cost, MSRP = manufacturer’s suggested retail price, and RFnew = registration fees of new cars.

AC = MSRP + RFnew

Table 2.

Import taxes on a percentage of the import prices on private cars.

The registration fee for a new car is a one-time payment which includes initial its registration, fitness certificate, tax token, and route permit. The BRTA has fixed the fees for EVs (such as the Toyota BZ3) at BDT 37,500 (USD 341), whereas for other cars, it is BDT 145,400 (USD 1322).

3.2.2. Operating Costs

Operating costs (OCs) cover expenses related to energy consumption, including fuel costs for ICEVs and average electricity recharging costs for EVs. Additional costs encompass service fees like holding taxes and roadworthiness fees.

Car insurance is not mandatory in Bangladesh and is thus excluded from this calculation. The total operating cost is given as:

where and are fuel costs and service fees incurred in year i. Fuel costs are dependent on distance traveled and vehicle efficiency. Both ICEVs and HEVs consume gasoline only, whilst EVs consume electricity. Fuel costs for ICEVs and HEVs are represented as and , respectively, and can be determined as follows:

FCICEV,i = ηICEV × Di × Cgas,i

FCHEV,i = ηHEV × Di × Cgas,i

Here, ηICEV is ICEV vehicle efficiency, ηHEV is HEV vehicle efficiency, Di is the annual distance traveled, and Cgas,i is the cost of gasoline per kilometer. It is assumed that EVs are charged from domestic electric sockets with a charging efficiency of ηch. The fuel cost for EVs (FCEV,i) is given by the following:

where ηEV, Di, and Celec,i are vehicle efficiency, distance traveled, and electricity cost per kilometer, respectively. The fuel cost is expected to increase every year at an average inflation rate (6.8%). The current inflation rate is 9.48% (2023), and it was 7.70% in 2022 and 5.55%, 5.69%, 5.59%, 5.54%, 5.70%, 5.51%, 6.19%, and 6.99% in the previous years [24], with the average being 6.80%.

FCEV,i = ηEV × Di × Celec,i/ηch

3.2.3. Maintenance Cost

Maintenance cost (MC) includes servicing and periodic maintenance fees (MFi), battery replacement costs (BRi), and tire replacement costs (TRi). Regular maintenance fees are expected to increase at the average inflation rate of 6.8%. The unscheduled maintenance cost is excluded due to the inaccuracy and unreliability in obtaining its estimated value. The expenses for battery and tire replacements are typically incurred within the year as specified by the manufacturers of the vehicle and tires. A tire has a certain life span in terms of distance traveled. The average distance traveled will determine the frequency of tire replacement. On the other hand, battery life usually depends on the number of years for which the battery has been used, and it has different values for EVs, HEVs, and ICEVs. The prices of batteries also differ significantly, with the highest cost being for EVs followed by HEVs and ICEVs. According to current industry expectations, EV batteries are projected to last between 100,000 and 200,000 miles, or about 15 to 20 years. EVs are estimated to lose an average of 2.3 percent of their battery capacity per year. Even after driving for 12 years, it will have more than 70% capacity to store power, and battery replacement for EVs will not be applicable. On the other hand, HEVs and ICEVs will incur battery replacement costs. Maintenance cost can then be expressed as:

Since battery prices are likely to decline, Bri can be re-written as:

where BR0 = current battery price and rb = annual battery price reduction rate.

BRi = BR0 (1 − rb)i

3.2.4. Salvage Value

The total salvage value (SV) comprises the scrap values of batteries upon replacement and the vehicle at the conclusion of its lifespan. This value is expected to be compensated in the year when the vehicle or battery is discarded.

where and are the scrap value of the battery at year i and scrap value of the vehicle at the end of its lifetime, respectively.

3.2.5. Final Equation of LCC

The life cycle cost (LCC) of a vehicle encompasses the sum of present value assessments for acquisition, operating, and maintenance expenses while deducting the salvage value [25]. A lower LCC signifies a vehicle that is more economically feasible, whereas a higher LCC implies the opposite. Incorporating all components, the LCC is expressed as:

3.3. Sensitivity Analysis of LCC

The life cycle cost (LCC) for vehicles in this study has been determined using the best estimate values for key parameters. However, the future states of nature are inherently unpredictable, and fluctuations in any of these parameters are expected, which could result in changes to the LCC. Consequently, a sensitivity analysis is essential to assess the impact of varying factors on the LCC. This analysis considers several critical elements, including acquisition and battery costs, electricity and fuel costs, and the annual distance traveled.

The acquisition cost for all vehicle types is influenced by the manufacturer’s suggested retail price (MSRP), import taxes, and registration costs of new cars. These costs are subject to variation due to market dynamics, technological advancements, and other factors, potentially altering the LCC for EVs, ICEVs, or HEVs. Notably, the acquisition cost remains unaffected by interest rate fluctuations, making it the only component of the life cycle cost (LCC) that remains constant. Consequently, any alterations in this cost will directly influence the overall LCC. Furthermore, the impact of import taxes or subsidies can be examined by adjusting the acquisition cost, where subsidies for purchases are often required to encourage the adoption of innovative technologies such as electric vehicles (EVs). On the other hand, all other expenses considered in the LCC calculations are subject to the discount rate. Generally, a higher discount rate results in lower LCC values, while a lower discount rate leads to higher LCC values.

The calculation of LCC is determined by a fixed assumption regarding the annual distance covered, yet variations are expected based on differing driving patterns across regions and individuals. These variations can significantly affect maintenance and operating costs. Therefore, analyzing the changes in annual distance traveled can illuminate the impact of driving habits on the feasibility of EVs.

Fuel costs are a major component of operating costs. Variations in both electricity and gasoline prices are crucial to this analysis. The cost of gasoline is not subsidized, but electricity is subsidized in the country, and this subsidy is decreasing gradually, with the aim being to eliminate it completely within a few years. An increase in gasoline prices would increase the LCCs of ICEVs and HEVs, potentially making EVs more attractive. Conversely, electricity costs, despite being subsidized in Bangladesh, are also subject to increases over time, which could make EVs less cost-effective. Additionally, taxing gasoline purchases and subsidizing electricity costs have also been used to promote EV adoption, making sensitivity analyses on electricity and gasoline more important.

Lastly, changes in battery prices are likely to influence both the battery replacement cost and the acquisition cost of vehicles. This is particularly relevant for EVs, where battery costs significantly impact production expenses. Several studies [26,27] have identified battery cost as a critical factor affecting the LCC of electric vehicles. Future projections indicate that there is a possibility of cost reduction ranging from 6 to 9%, with a cumulative doubling of production [28].

4. Results and Discussions

The LCCs of three fuel-type vehicles have been calculated in the context of the Bangladesh Market. Data specific to each country have been acquired from research papers, technical notes, and reports provided by manufacturers and subject-matter experts. Additionally, the latest market prices have been gathered from various sources.

4.1. Required Data

The cost data are represented in both Bangladeshi Taka (BDT) and US Dollars (USD). The conversion rate as of 4 January 2024—1 USD = BDT 110.00—has been used. Regarding the interest rate, r = 0.1093, as the present interest rate of most of the scheduled banks (lending rate) is 10.93% [29]. Hence, the tax-adjusted cost of capital would be 7.92%. Different vehicle lifetimes have been used in different studies, for example, a lifetime of 8 years was used in [18], 12 years was used in [11], and 20 years was used in [24,30]. In our study, the vehicle lifetime is assumed to be 12 years. Table 3 shows a summary of the important parameters used.

Table 3.

Important parameters for LCC calculations.

Although the Toyota BZ3 has not yet been commercially launched, some importers have brought this model into the country to introduce its features and prices to potential customers. Including taxes, the price is assumed to be BDT 3,465,000 or USD 31,500. Another model is the Toyota BZ4, an SUV, which is likely to have a lower demand, as SUVs are not popular in the country. According to sources at CG-Runner Bangladesh Ltd., Dhaka, Bangladesh, a distributor of BYD, a prominent electric vehicle (EV) company headquartered in Shenzhen, the company is preparing to introduce its inaugural car in Bangladesh by March of next year. Presently, the importation of EVs incurs a tariff and tax burden ranging from 85 to 96 percent, whereas conventional cars face duties ranging from 100% to 300% of the vehicle’s price. For instance, importing a car with a gasoline engine capacity of up to 1600 cc attracts a total tax and duty of over 125%, while the corresponding figure for an electric car is 89%.

In urban areas, car owners typically travel an average distance of 22.57 km per trip, with an average frequency of trips made per week of 9.15 times a week [31]. In addition to these regular journeys, car owners also undertake longer trips, roughly 400 km each, around 8 to 10 times annually. Taking into account both the regular and long-distance travel, it is estimated that the average annual travel distance for a car owner in urban settings amounts to approximately 14,740 km.

The Toyota Axio and Toyota Allion have been reported to have fuel consumption rates of 8.0 and 8.1 km/L, respectively [21]. The Toyota Prius consumes 3.4 L per 100 km with a fuel tank capacity of 43 L, while the Aqua has a fuel tank capacity of 36 L and an average fuel consumption of 3.9 L per 100 km (SBT, Global Car exporter). These figures are crucial for calculating the operating costs of ICEVs.

With a full charge, the Toyota BZ3 (with a battery capacity of 71.4 kWh) can run about 252 miles (about 405.5 km). The theoretical energy consumption rate is about 17.62 kWh/100 km or about 5.67 km/kWh. It should be borne in mind that this is the rate for the theoretical total battery energy consumed, and in reality, the useable capacity is lower. Recently, the Ministry of Energy, Power and Mineral resources published a gazette wherein a flat rate was set for EV charging stations, effective from March 2024. The rate is BDT 9.62/kWh plus BDT 90 demand rate/charge (Bangladesh Gazette, MOPEMR, 2024). Assuming a Toyota BZ3, which requires 3132 kWh to drive 14,740 km per year at an 83% charging efficiency, 44 times the demand charge will be paid per year. The electricity bill will be BDT 34,090 in total. An additional 20% payment will be charged (VAT + surcharge) by the government. Thus, a yearly EV charging cost of BDT 40,908 is assumed, resulting in a cost of BDT 2.78 or USD 0.0253 per kilometer.

Lithium Ferro Phosphate (LFP) battery cells are commonly used in EVs. Contemporary Amperex Technology Co., Limited (CATL), the world’s largest EV battery maker, now offers batteries at USD 56/kWh. For the Toyota BZ3’s battery (71.4 kWh), this translates to a cost of around USD 4000 (BDT 440,000). On the other hand, batteries for the Toyota Aqua are available in automobile repair shops for a price of BDT 175,000 (USD 1591), and those for the Toyota Prius are available for BDT 225,000 or USD 2045 (Car Care BD). Due to the high costs of new cars in Bangladesh, there is a significant market for used cars. It is observed that after 12 years of usage, a well-maintained car can retain at least one-fourth of its original purchase price, regardless of the vehicle type.

Registration costs for new cars have been calculated using the online Bangladesh Road Transport Authority (BRTA) calculator. Annual registration fees are fixed over a number of years. The BRTA revises the fee every 4/5 years, with an increment of about 50% or more. We have assumed that the annual fees will be reviewed every 5 years with a 50% increment. Predicting maintenance costs is challenging due to variability across brands, vehicle age, and other factors. However, it is noted that the owner of a five-year-old 1500 cc car may spend an average of BDT 18,000 or USD 164 annually on servicing. Hybrids have both electric and internal combustion engines, meaning that they have all the maintenance costs of both types of cars. The owner will still need regular oil changes and need to replace parts like spark plugs, batteries, and brake pads on roughly the same maintenance schedule. However, because there are two engines in a hybrid, some of the parts are hard to get to when replacing them, which can lead to higher labor costs. A study has shown that the maintenance cost of an HEV is 58% higher than that of an ICEV [32]. Electric vehicles necessitate less maintenance compared to gas-powered vehicles as they eliminate the need for oil changes or air filter replacements. By adhering to the automakers’ guidelines for maintenance, electric vehicles result in a cost reduction of USD 330 annually in comparison to gasoline-powered cars, totaling USD 949 per year (aaa.com), or 26% lower than ICEVs. Considering these issues, we have assumed that the regular maintenance cost of HEVs will be BDT 28,000 (USD 255), and that of EVs will be BDT 12,700 (USD 115).

4.2. Life Cycle Cost Analysis

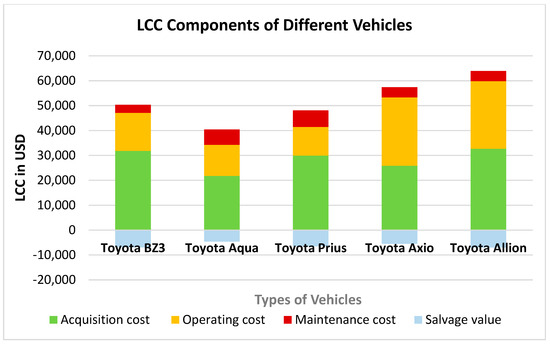

Table 3 presents a detailed summary of the life cycle cost (LCC) analysis for the selected vehicle types. The analysis indicates that the LCC of the Toyota BZ3, USD 43,409, is higher than those of hybrid electric vehicles (HEVs) but lower than those of internal combustion engine vehicles (ICEVs). Among these categories, HEVs are identified as having the lowest LCCs, with the Aqua and Prius having LCCs of USD 35,789 and USD 41,569, respectively, lower than the Toyota BZ3 by USD 7620 and USD 1840, respectively. The main reasons behind the lowest cost belonging to HEVs is the lower acquisition costs. On the other hand, the LCCs of the Axio and Allion are USD 51,907 and USD 56,932, which are approximately USD 8498 and USD 13,523 more expensive than that of the BZ3, respectively. The possible reasons of this higher cost are the higher acquisition costs and very high operating costs that result from the high price of gasoline. Our LCC results contrast with those of an analysis in which it was found that EVs are currently still expensive compared to the ICEVs and HEVs in Brunei, with the acquisition costs contributing much to the life cycle cost (LCC) [11]. On the other hand, our EV acquisition cost is competitive with ICEVs, but the operating cost of ICEVs is much higher, as the electricity cost is very low in Bangladesh, whereas the gasoline cost is very high. The majority of other studies also show that EVs are not cost-competitive compared to HEVs and ICEVs [13,28,30]. On the other hand, the LCC of EVs is lower than that of ICEVs in France, Norway, and the UK [17,25], which agrees with our study’s results. Table 4 shows the comparison of LCC, acquisition cost, operating cost, maintenance cost, and salvage value of the different types of vehicles.

Table 4.

Comparisons of results for the different vehicles.

In terms of acquisition costs, the Toyota BZ3 and the Toyota Allion, a conventional ICEV, are nearly on par. However, these costs are found to be lowest for HEVs. A significant aspect of the cost analysis is that the acquisition cost makes up a comparatively larger portion of the total LCC for the Toyota BZ3 (73%), while for HEVs, it ranges from 61% to 72%, and for ICEVs, it lies between 50% and 57%. These data highlight the importance of considering both initial purchase costs and ongoing expenses in vehicle evaluation.

Operating costs are the second most dominant contributor to the LCCs of the vehicles. Within our calculated annual distance, the operating costs of EVs and HEVs are almost similar. But HEVs occupy the most advantageous position according to operational cost percentage to LCC, which is only 28 to 35%. EVs incur 35% of their LCCs as operating costs, whereas ICEVs incur 48% to 53% of their LCCs as operating costs because of the high gasoline price in the country. For this reason, when the annual distance traveled is very high, obviously, EVs will be the most feasible vehicles.

Under maintenance costs, the tire replacement cost will not vary among the three types of vehicles, but battery replacement costs have wide variations. The price of a battery for a Toyota BZ3 is USD 4000, while the price is USD 1136 for a battery for a Toyota Aqua, and the price is USD 1590 for that for a Toyota Prius. Battery replacement will not be applicable for EVs, as explained earlier. For that reason, the maintenance costs for both EVs and ICEVs are lower (7% to 8%) than those for HEVs (16–17%). In contrast, the maintenance cost is higher (14% to 21%) than the operating cost (9% to 15%) in Brunei [11].

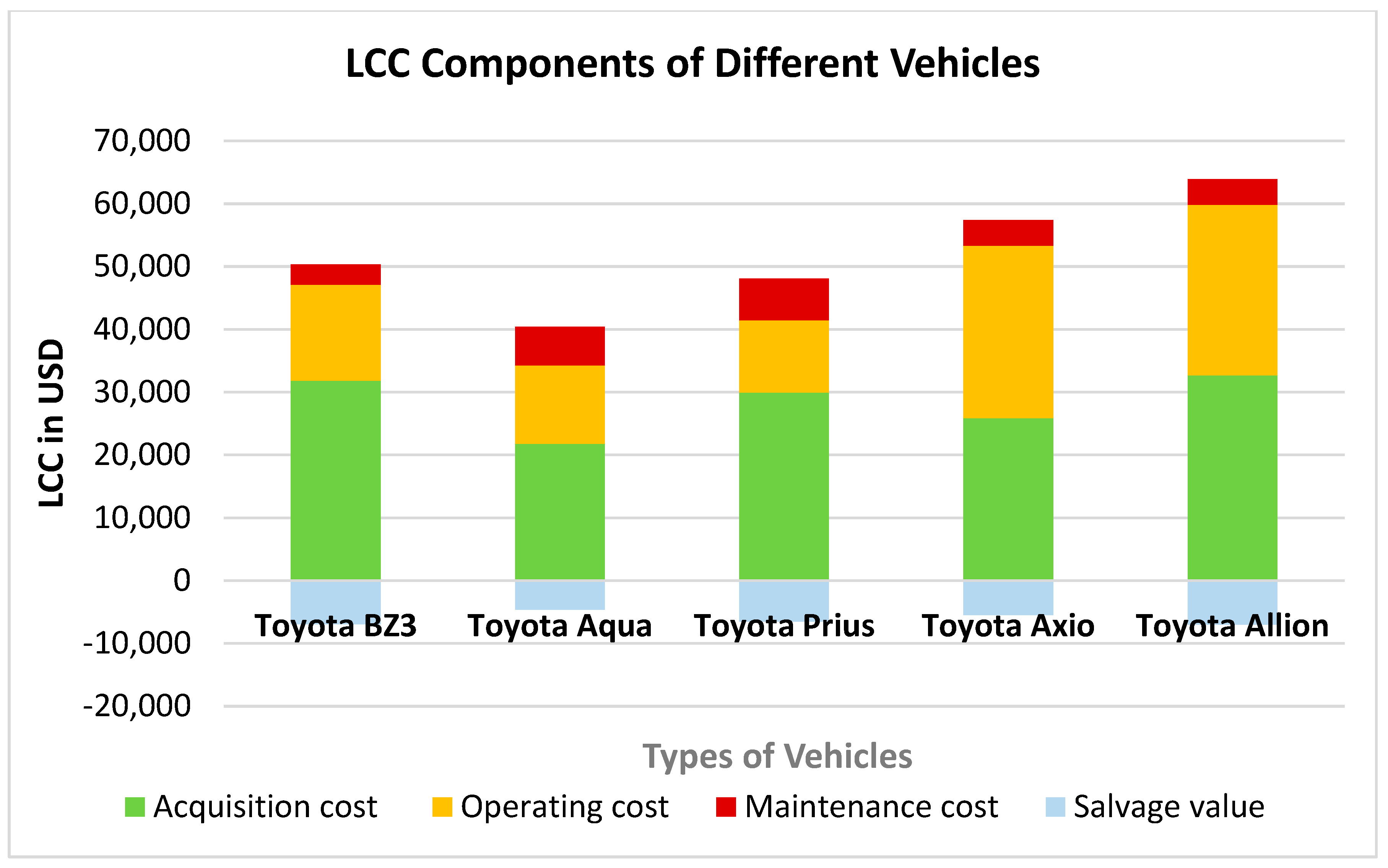

Lastly, the salvage values of different vehicles vary within a narrow range of 11% to 16%. This variation also occurs due to the salvage values of batteries. The salvage value of an HEV battery is higher than that of ICEV batteries. EV batteries have no role in salvage value, as they are expected to last longer than 12 years. The following figure clearly depicts that the LCCs of ICEVs are higher than those of most other vehicles. It also shows that EVs’ acquisition cost is higher than those of other vehicles, whereas ICEVs’ operating costs are higher than those of other vehicles. HEVs have the lowest LCCs, with the lowest acquisition costs, moderate operating costs, and highest maintenance cost. In general, for all types of vehicles, acquisition costs cover the majority of the LCC, followed by operating costs and maintenance costs. Figure 2 shows the graphical representation of LCC of the different vehicles differentiating their acquisition, operating, maintenance and salvage cost.

Figure 2.

LCCs of the different vehicles, differentiating their acquisition, operating, maintenance and salvage costs.

4.3. Sensitivity Analysis

The acquisition cost (AC) for a Toyota BZ3 is higher than that for a Toyota Aqua, Toyota Prius, and Toyota Axio and lower than that for a Toyota Allion. A reduction in the cost of acquiring a product may arise from a decrease in the manufacturer’s suggested retail price (MSRP), reductions in taxes [17], or the provision of subsidies by the government to promote the adoption of electric vehicles in the market [20]. The Electric Motor Vehicle Registration and Operation Guidelines 2023, along with the tax rate for electric vehicles, have been officially approved by the BRTA. All electric vehicles will now fall under the E or EV categories for registration purposes. Similar to traditional combustion engine vehicles, electric cars will need to obtain registration, fitness certificates, tax tokens, and route permits in order to legally operate on roads.

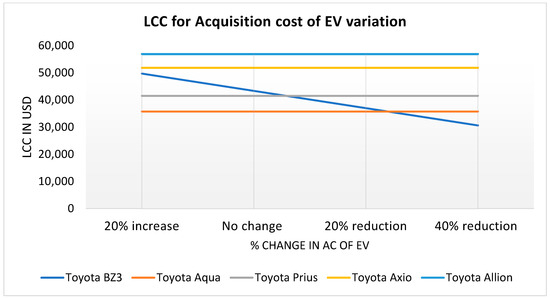

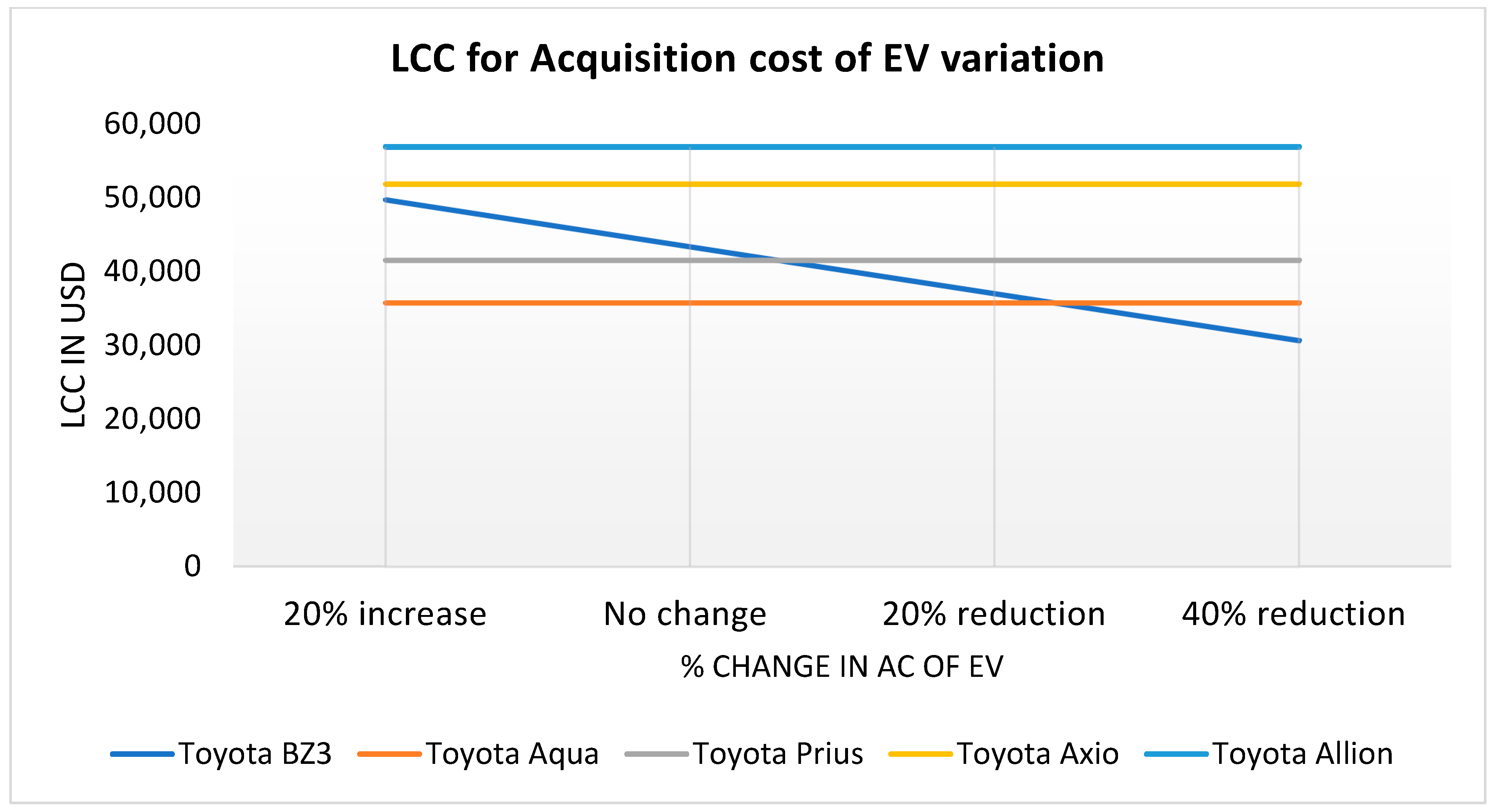

We have conducted a sensitivity analysis of LCC to percentage change of acquisition costs with a range from −40% to +20%. Figure 3 illustrates that a decrease of approximately 5% in AC will lead to the LCC of Toyota BZ3 being lower than that of Toyota Prius. Furthermore, a reduction of around 25% in the AC of EVs could potentially result in the most cost-effective LCC for EVs compared to other vehicle types. If the AC of EVs increases by 20%, it can still compete with that of the Toyota Axio (an ICEV).

Figure 3.

Sensitivity of acquisition cost percentage variation.

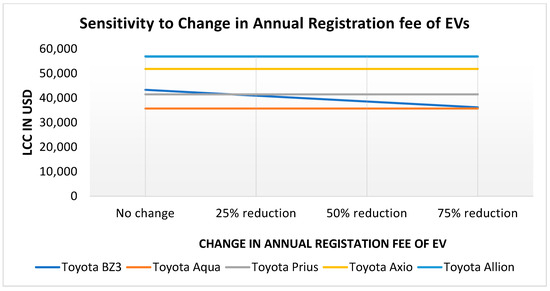

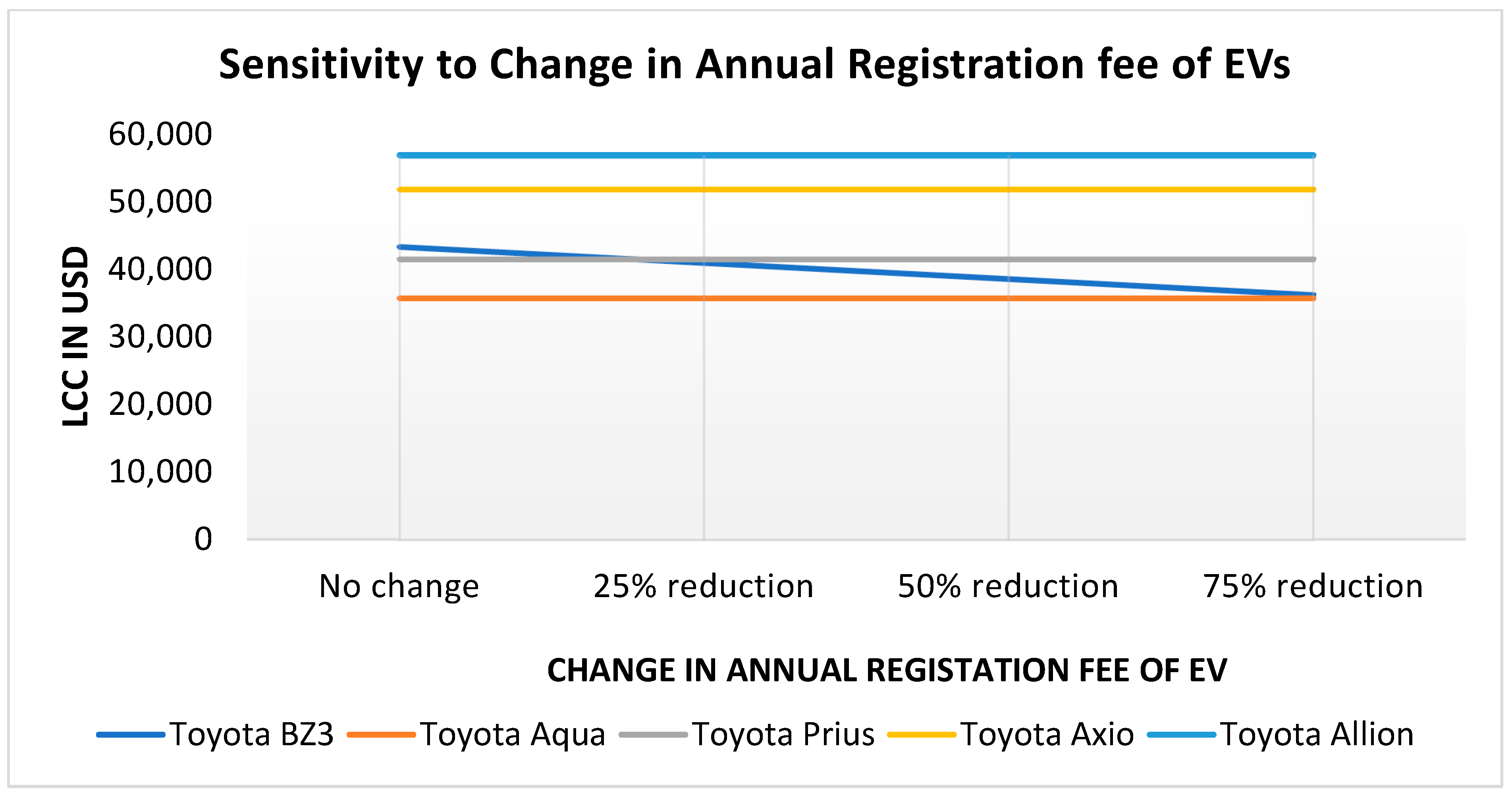

The annual registration fee will depend on the motor capacity (kW) of the vehicle. The proposed annual registration fee for an EV with 125–150 kW engine capacity is BDT 125,000 (USD 1136), whereas HEVs and ICEVs’ registration fee is BDT 60,000 (USD 545) per year. So, the registration fee of EVs should be reduced by at least 50% to make it competitive with HEVs. Figure 4 shows that with about a 20% reduction in the registration fees of EVs will make the Toyota BZ3 car competitive with the Toyota Prius. A 75% reduction in annual registration fee will make the Toyota VZ3 the least costly vehicle among all.

Figure 4.

Life cycle costs of the vehicles against annual registration fees of EVs.

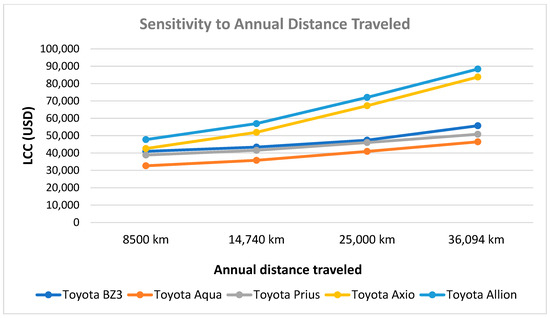

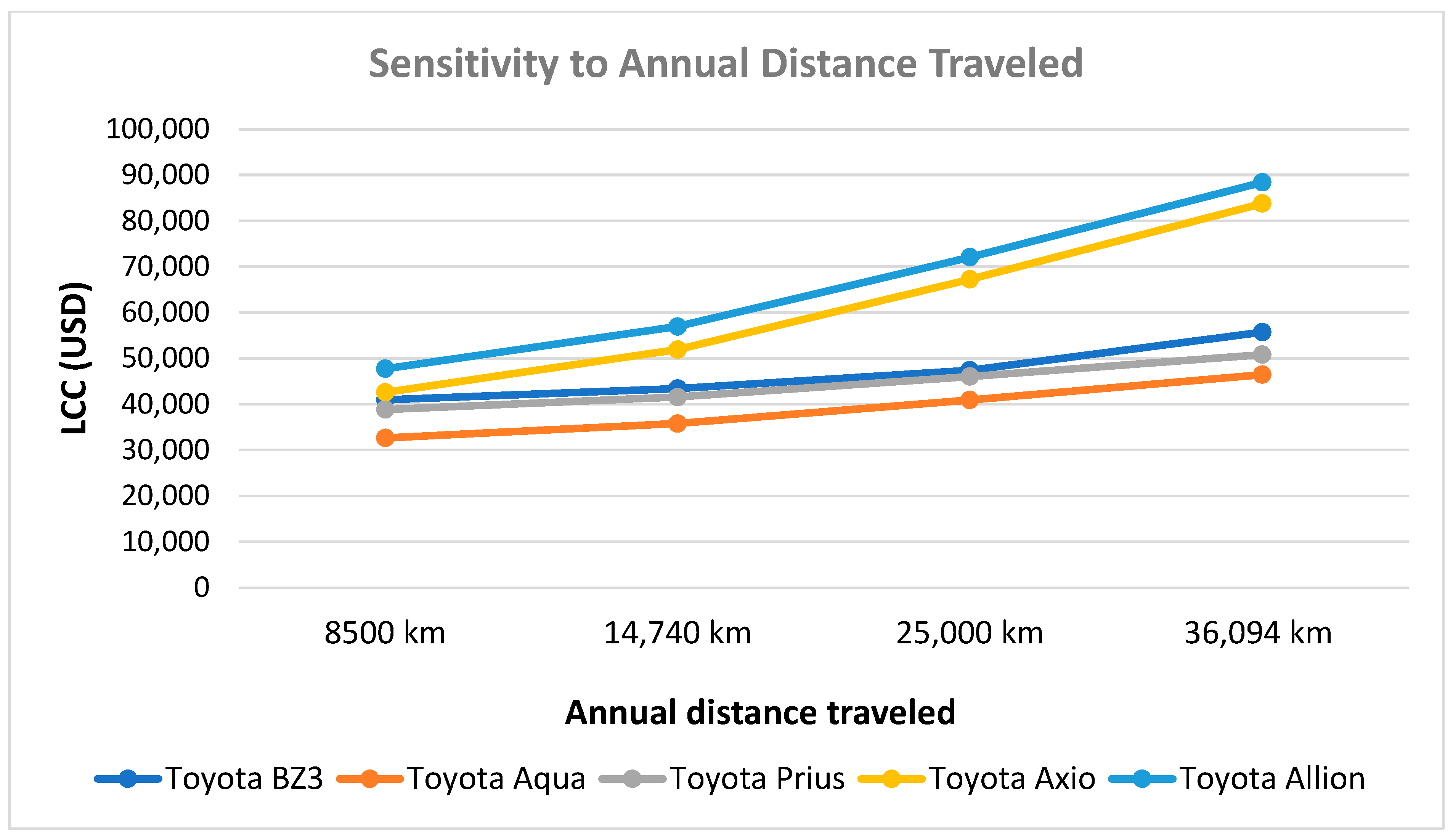

To cover longer distances, more fuel will be consumed and maintenance costs will rise. Additionally, tires and batteries will need to be replaced more often, leading to higher maintenance expenses. These additional costs contribute to an overall increase in the life cycle costs (LCCs) of vehicles, as illustrated in Figure 4. Most private vehicles are possessed by people from big cities in Bangladesh. They usually travel inside the city area. So, their range of annual travel is very limited because of high traffic and time constraints. The minimum travel range is 8500 km [31], and the maximum range is 36,094 km per year (Bangladesh Road Research Laboratory, 2017) in the country. Figure 5 shows that the LCCs of EVs are the least sensitive to distance, as they use electricity with a low cost. HEVs are more sensitive, and ICEVs are very highly sensitive, as they use gasoline, which is very costly. If the vehicles travel 36,094 km per year, the LCCs of ICEVs will differ from other vehicles’ LCCs at a very significant amount, and the LCCs of HEVs will become much closer to those of EVs, making EVs more feasible to the consumers.

Figure 5.

Sensitivity of LCC to annual distance traveled.

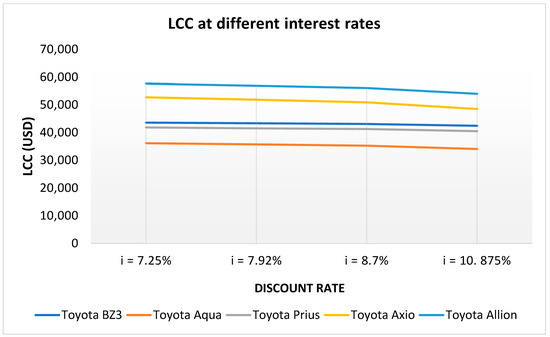

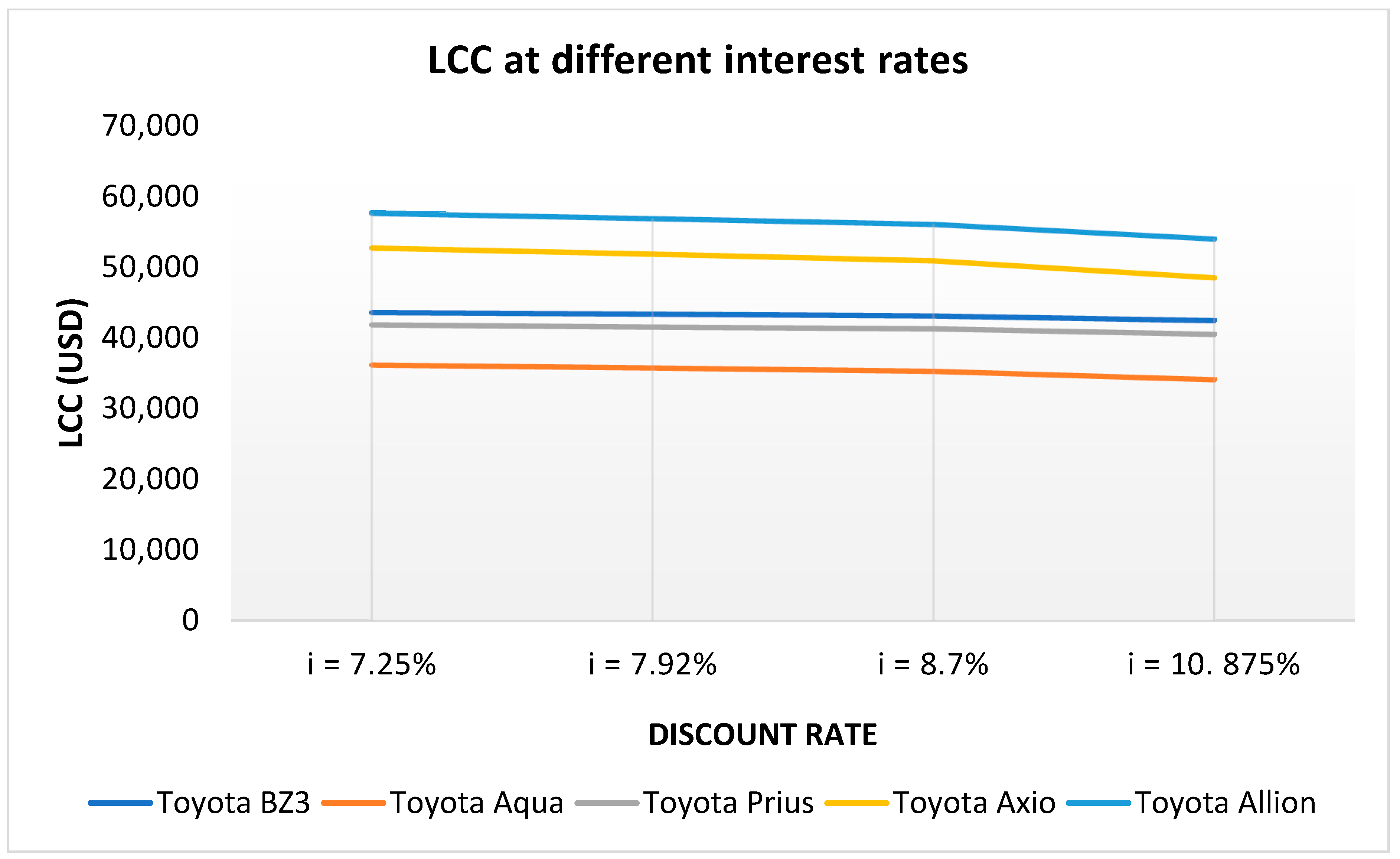

The interest rate changes from year to year depending on many economic factors. In Bangladesh, the lending interest rate has rarely been a single digit number. Sometimes, it has become as high as 14 or 15%. Depending on the variations in interest rates, the minimum cost of capital would be 7.25%, and the maximum cost would be 10.875%. The LCC always declines with higher interest rates. Figure 6 shows that higher interest rates reduce the LCCs but do not change the order of feasibility of the vehicles. Among all costs, the acquisition cost is not affected by discount rates. ICEVs are dominant among other costs, which are highly sensitive to discount rates. As the discount rate increases, the LCCs of ICEVs are reduced more than the LCCs of other vehicles. That is why the LCCs of ICEVs are more downward sloping than other vehicles’ LCC curves.

Figure 6.

Sensitivity of interest rates to LCC.

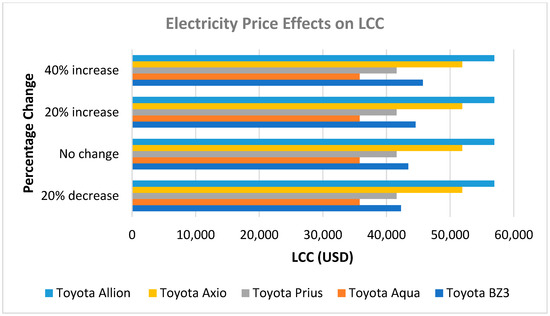

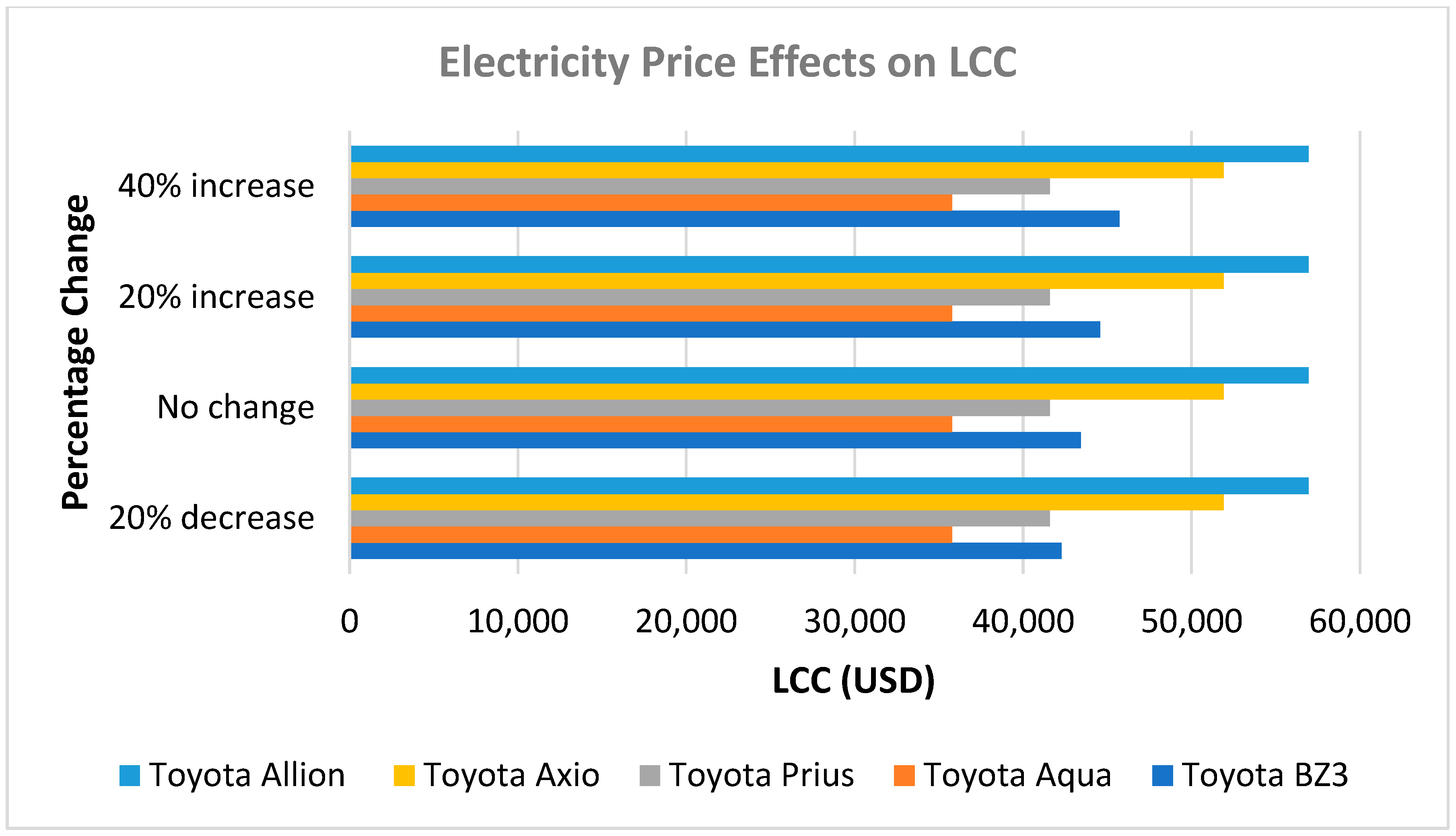

The electricity price will affect the LCC of EVs only. The government has increased the power price at consumer level thrice in the last five years, and the government has stated its aim to completely eliminate subsidies on power within the next few years. So, there is little possibility that the electricity price will decrease in future. Even though the govt. can subsidize electricity to encourage EV adoption. We assume that the electricity price may decrease by 20% or increase by 20% to 40%. Figure 7 shows that, with an increased electricity price and all other variables remaining constant, the LCC of EVs increases further, making them more infeasible to consumers.

Figure 7.

Sensitivity of electricity price to LCC.

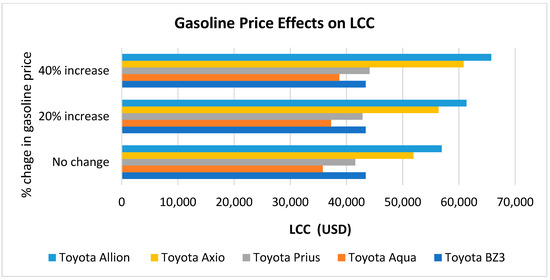

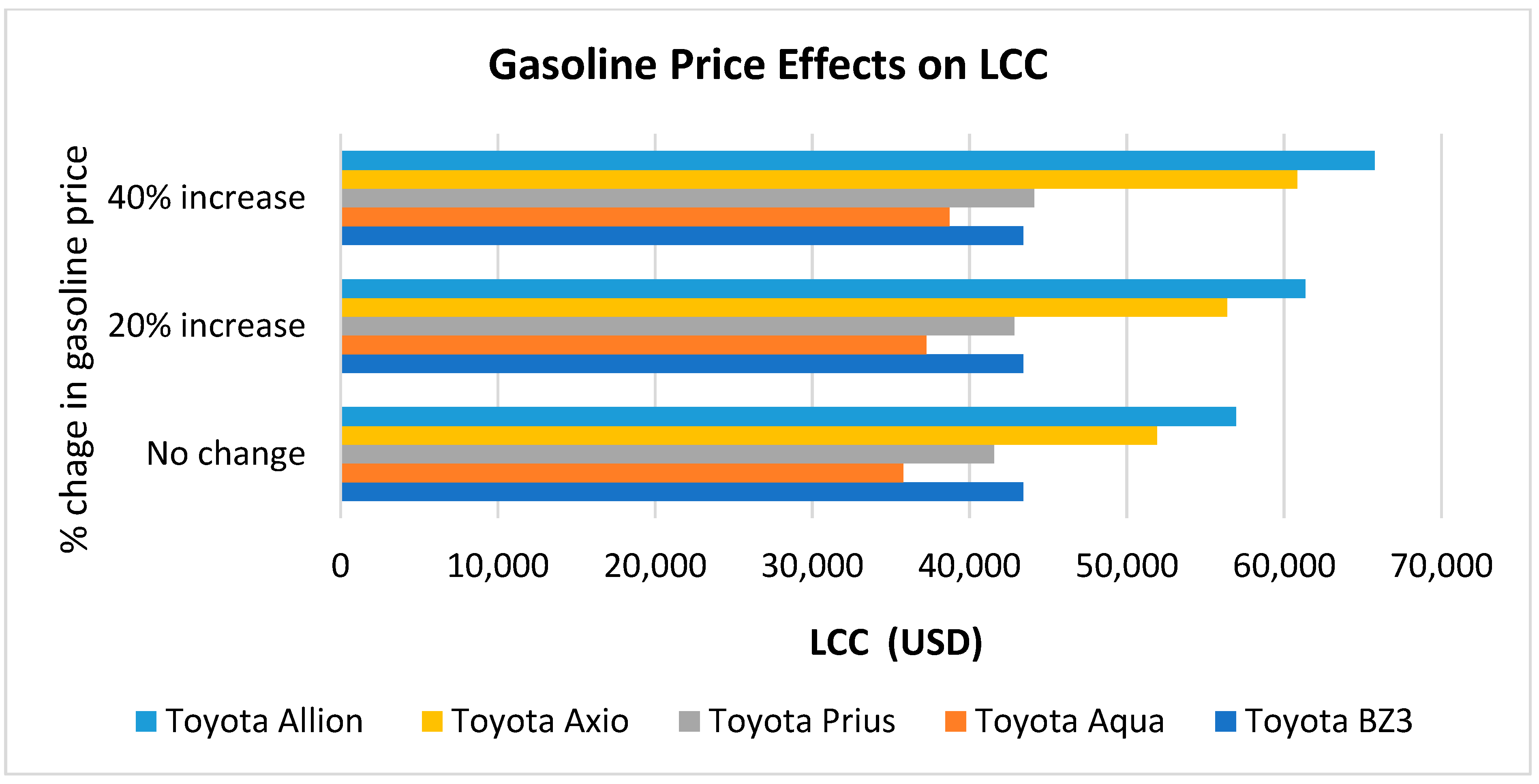

The gasoline price may change with higher amounts of import duty being imposed or price hikes in international markets. Figure 8 shows the life cycle costs of the vehicles against the cost of gasoline with the cost of electricity fixed. Figure 9 depicts that with an increased gasoline price, the LCC of HEVs will increase at a lower rate, but the LCC of ICEVs will increase at a very high scale. With a 40% increase in gasoline price, the LCC of HEVs would be almost equal to the LCC of EVs.

Figure 8.

Life cycle costs of the vehicles against cost of gasoline with the cost of electricity fixed.

Figure 9.

Life cycle costs of the vehicles against increased cost of gasoline and decreased cost of electricity at the same time.

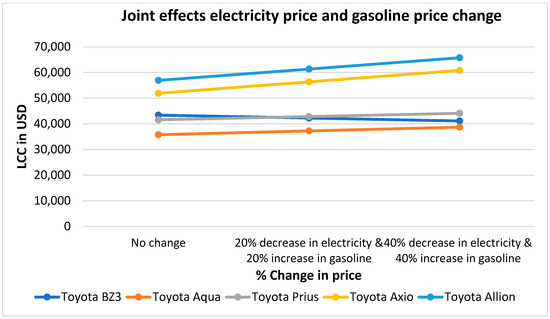

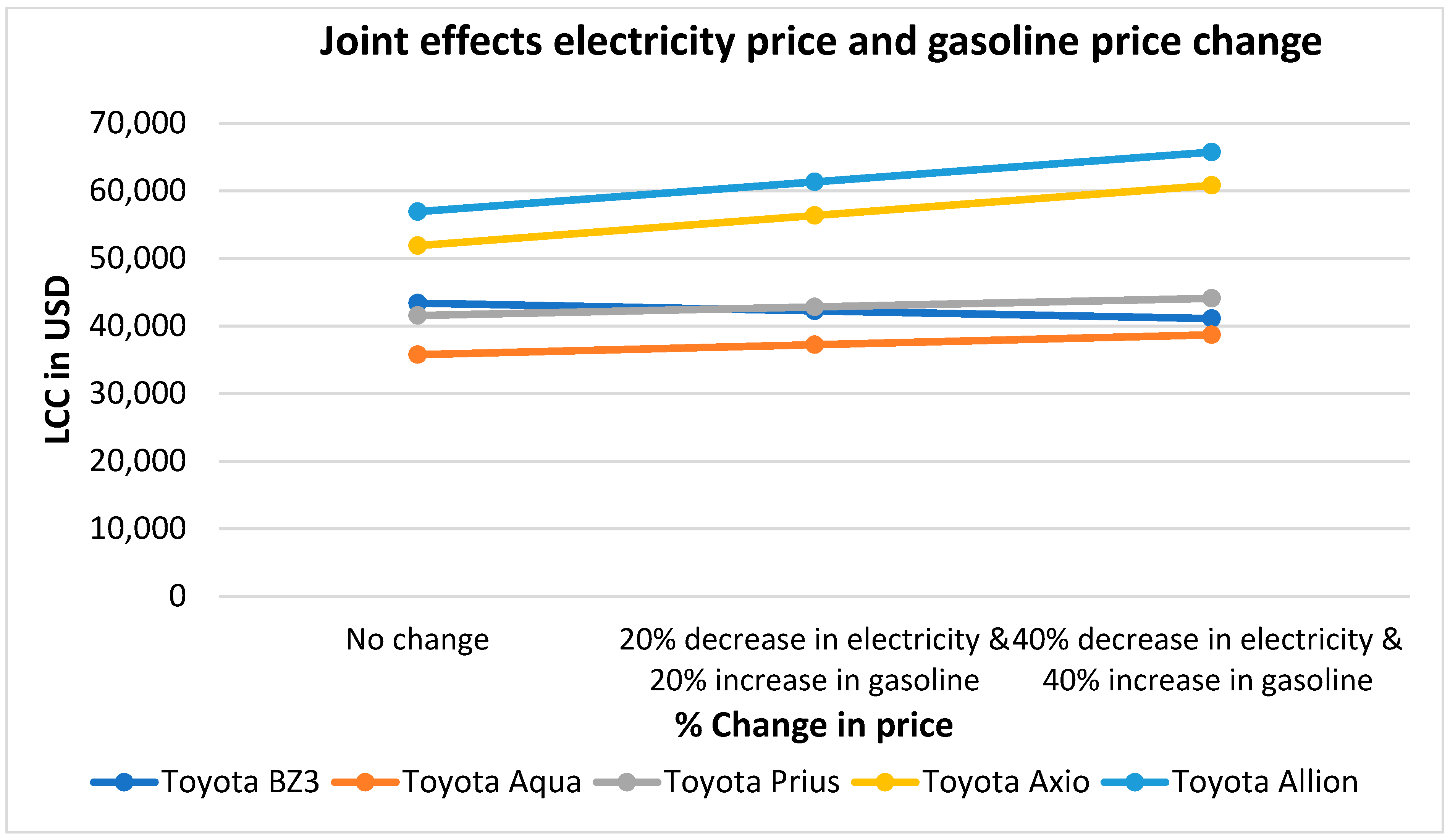

Figure 10 depicts the joint effects of electricity price and gasoline price on the LCC. If the electricity price reduces by 20% and, at the same time, the gasoline price increases by 20%, the gaps between the LCC of EVs and ICEVs will increase by a lot, and the LCC of the Toyota BZ3 will go below that of the LCC of the Toyota Prius. If the electricity price reduces by 40% and, at the same time, the gasoline price increases by 40%, the gaps between the LCC of EVs and ICEVs will increase at a significant level, and the LCCs of the Toyota BZ3 and Toyota Aqua will become closer.

Figure 10.

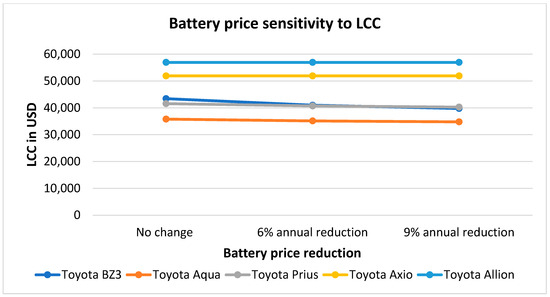

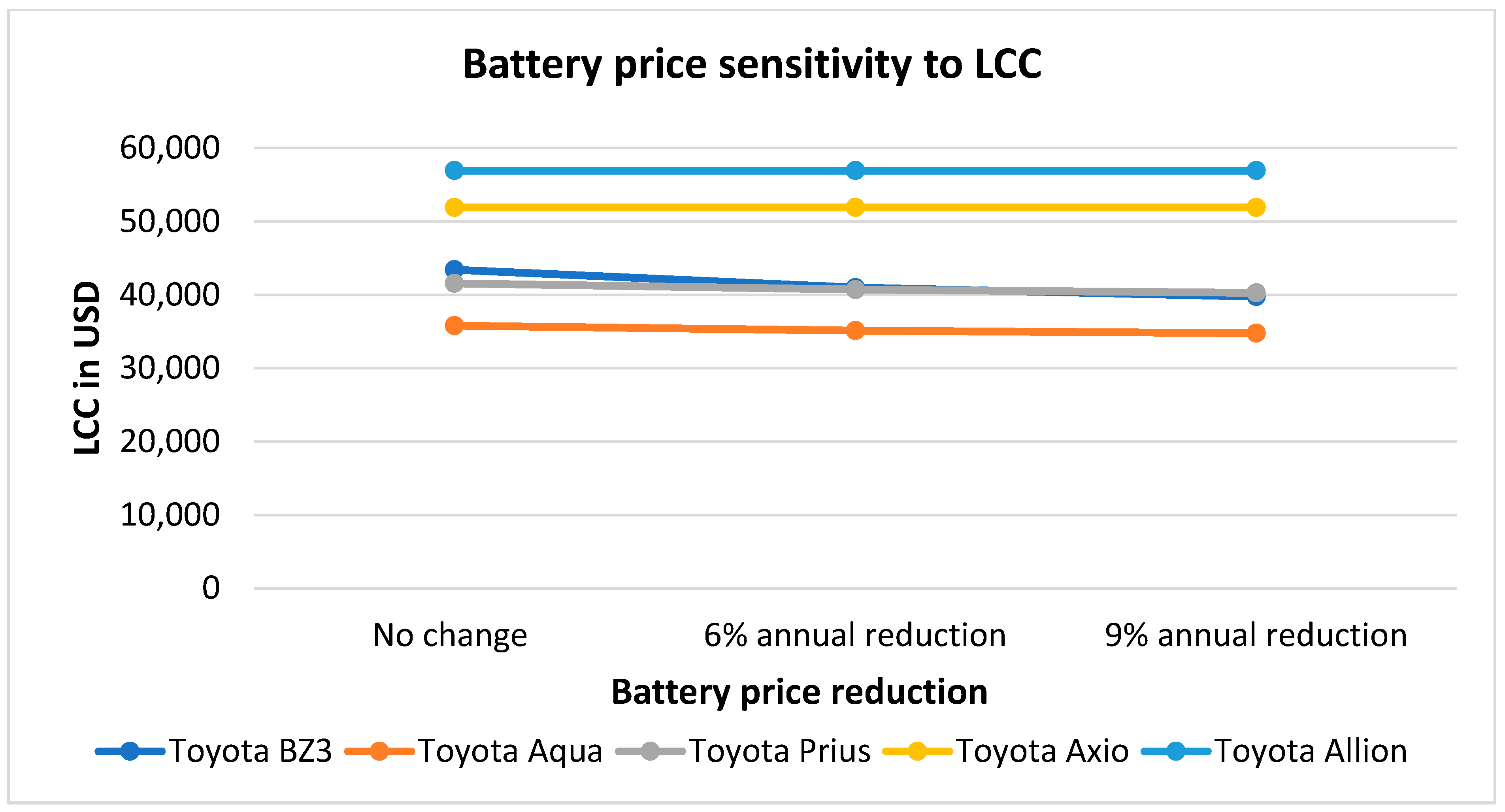

Life cycle costs of the vehicles against reduced battery replacement costs for EVs and HEVs.

The costs of batteries are very high both for EVs and HEVs. It is predicted that battery price shall decline between 6 and 9% annually until 2030 [11]. Battery cost will affect both the acquisition and maintenance costs of vehicles. Figure 10 shows that with a 6 to 9% decline in battery replacement costs, the LCC of EVs decreases more than the LCC of HEVs, and EVs’ LCC becomes lower than that of the Toyota Prius.

5. Recommendations

While the initial registration cost for electric vehicles (EVs) is lower compared to that of internal combustion engine vehicles (ICEVs), the annual tax rates for EVs in Bangladesh are significantly higher. This disparity in tax rates may pose a challenge to the growth of the EV market in the country. For the EV model we have chosen for our analysis, the Toyota BZ3, one will have to pay BDT 125,000 (or USD 1136) annual tax per year, which is more than two times higher than tax rate for HEVs and ICEVs, which is BDT 60,000 (or USD 545). The annual tax rates of EVs should be reduced by at least 50% of the proposed rates. There have also been maintenance issues. These will need to be resolved if the country is going to move towards an electrified vehicle fleet. Batteries for EVs are imported from other countries, and the price of which is very high (USD 4000). If the government encourages the establishment of production plants for batteries and other spare parts for EVs, the market for EVs will grow faster. Unfortunately, the government is increasing the electricity price every year, with its ultimate aim being to eliminate the subsidy given to the power sector. This may restrict the adoption of EVs in the market. So, the govt. should carry on the subsidy on power and impose additional taxes on oil and CNG to encourage the adoption of EVs and discourage the use of ICEVs.

To bolster consumer inclination towards electric vehicles (EVs), the Chinese government has implemented a range of policies. These include initial subsidies and subsequent tax advantages, along with the development of infrastructure. In line with China’s approach, the Government of Bangladesh should prioritize augmenting power generation and establishing a comprehensive high-voltage electric grid nationwide to facilitate EV charging. Before the commercial use of electric vehicles (EVs) in Bangladesh, it is anticipated that numerous charging stations and a multitude of charging piles (small charging facilities specifically designed for EVs and typically found in parking lots) will be established in developed regions like Dhaka, Chittagong, Sylhet, Khulna, and Rajshahi. Over the next few years, the charging piles in these major cities are likely to be predominantly located in residential parking lots, office parking lots, market parking lots, school parking lots, and hospital parking lots. After the adoption of EVs, the country is expected to produce huge amounts of battery waste, which means that the batteries could pollute the environment if they are not recycled and reused. The government should enact a policy guideline to handle battery waste and recycling in order to protect the environment and public health.

6. Conclusions

Among the three types of vehicles, ICEVs are the most expensive, and HEVs are the cheapest, while EVs lie in between them, according to life cycle cost (LCC). The LCC of the Toyota BZ3 (EV) has been calculated to be USD 43,409, more expensive than that of the Toyota Aqua (HEV), with a cost of USD 35,789, and Toyota Prius (HEV), with a cost of USD 41,569. On the other hand, a Toyota BZ3 (EV) is cheaper than a Toyota Axio (ICEV), with a cost of USD 51,907, and a Toyota Allion (ICEV), with a cost of USD 56,932. The acquisition cost (73.35%) dominates the LCC of the Toyota BZ3 (EV), followed by operating costs (35.13%) and then maintenance cost (7.53). It has been found that a reduction of around 25% in the acquisition cost of EVs could potentially result in EVs having the most cost-effective LCC compared to the other vehicle types. The annual registration fee for an EV has been set at USD 1591, which is very high in comparison to other vehicles’ fee (USD 545). A 20% reduction in the registration fee for EVs would make the Toyota BZ3 car competitive with the Toyota Prius, and a 75% reduction would make the Toyota VZ3 the least costly vehicle among all. EVs can be a good choice for those who travel a long distance, as their LCC is significantly lower in comparison to that of ICEVs. A change in the electricity price would have little effect upon the LCC of EVs, but a change in the gasoline price would have a high impact upon the LCC of ICEVs, resulting in EVs becoming the better choice. Battery cost affects both the acquisition costs and maintenance costs of vehicles. With a 9% decline in battery replacement costs, the LCC of EVs becomes lower than that of a Toyota Prius (HEV).

It has been suggested that in order to encourage the adoption of electric vehicles (EVs), the government should consider implementing subsidies, raising current gasoline prices, and reducing annual registration fees for EVs. Additionally, with the projected annual decrease of 6–9% in battery prices until 2030, EVs are expected to become more competitive with traditional vehicles by 2030 or even earlier. EV manufacturers should also focus on the manufacturer’s suggested retail price (MSRP) of EVs, as it plays a significant role in determining the affordability of EVs in the local market. Despite this, improving the fuel efficiency of EVs would have a minimal impact on the life cycle cost (LCC) of EVs, mainly due to the low cost of electricity in Bangladesh.

Despite Bangladesh making preparations to transition towards electric vehicles (EVs), sales are not expected to pick up momentum due to factors such as a limited understanding and awareness about EVs, expensive prices exacerbated by high import duties, and the costly annual registration fees, as reported by industry insiders. Nevertheless, it is anticipated that EVs will eventually become prevalent in the domestic market, given the growing interest in vehicles powered by alternative fuels, driven by the rising global consciousness regarding their environmental and economic advantages. At present, about 1.5 million battery-driven three-wheeler easy-bikes are running on the roads of Bangladesh, which produce huge amounts of electronic waste, and this amount is expected to accelerate after the adoption of EVs. Unfortunately, the majority of the country’s LIB waste is currently being disposed of in landfills, leading to adverse consequences for both the environment and public health. However, this waste contains valuable resources such as cobalt, lithium, base metals, graphite, and others, which have the potential to be locally recovered and utilized in the production of new products. In light of the pressing issue of climate change, it is imperative to adopt interdisciplinary solutions to effectively address the management of end-of-life lithium-ion batteries (LIBs) used in electric vehicles (EVs) and prevent potential waste problems in the future. Several research studies have highlighted that the recycling costs of USD 9/kWh are relatively minor compared to the manufacturing costs of USD 56/kWh. Additionally, recycling LIBs can significantly reduce the normalized and weighted environmental impact of these cells by an impressive rate of 75%.

Author Contributions

Conceptualization, M.S.K., J.T. and A.K.A.; methodology, M.S.K., A.M.A. and P.E.A.; software, M.S.K., P.E.A. and M.S.R.; validation, M.S.K. and P.E.A., formal analysis, M.S.K.; investigation, M.S.K., resources, M.S.K. and J.T., data curation, M.S.K., J.T. and M.S.R.; writing-original draft preparation, M.S.K. and A.K.A.; writing-review and editing, J.T., A.M.A., P.E.A., M.S.R. and A.K.A.; visualization, M.S.K.; supervision, J.T. and A.K.A.; project administration, J.T.; fund acquisition, J.T. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

The raw data supporting the conclusions of this article will be made available by the authors on request.

Acknowledgments

One of the authors, M.S.K., was supported by the Energy Technology Program, Department of Mechanical and Mechatronics Engineering, Faculty of Engineering, Prince of Songkla University, Hat Yai, Thailand, through his PhD scholarship.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Abdalla, A.M.; Hossain, S.; Nisfindy, O.B.; Azad, A.T.; Dawood, M.; Azad, A.K. Hydrogen production, storage, transportation and key challenges with applications: A review. Energy Convers. Manag. 2018, 165, 602–627. [Google Scholar] [CrossRef]

- Alhindawi, R.; Nahleh, Y.A.; Kumar, A.; Shiwakoti, N. Projection of greenhouse gas emissions for the road transport sector based on multivariate regression and the double exponential smoothing model. Sustainability 2020, 12, 9152. [Google Scholar] [CrossRef]

- Reiter, A.J.; Kong, S.C. Demonstration of compression-ignition engine combustion using ammonia in reducing greenhouse gas emissions. Energy Fuels 2008, 22, 2963–2971. [Google Scholar] [CrossRef]

- Saifuddin, M.R.M.; Diana, W.R.W.A.; Karim, M.R. Addressing GHG emissions from land transport in a developing country. IOP Conf. Ser. Earth Environ. Sci. 2019, 373, 012024. [Google Scholar] [CrossRef]

- Yang, F.; Xie, Y.; Deng, Y.; Yuan, C. Predictive modeling of battery degradation and greenhouse gas emissions from U.S. state-level electric vehicle operation. Nat. Commun. 2018, 9, 2429. [Google Scholar] [CrossRef] [PubMed]

- Li, W.; Long, R.; Chen, H.; Geng, J. A review of factors influencing consumer intentions to adopt battery electric vehicles. Renew. Sustain. Energy Rev. 2017, 78, 318–328. [Google Scholar] [CrossRef]

- Jones, N. The new car batteries that could power the electric vehicle revolution. Nature 2024, 626, 248–251. [Google Scholar] [CrossRef] [PubMed]

- Cano, Z.P.; Banham, D.; Ye, S.; Hintennach, A.; Lu, J.; Fowler, M.; Chen, Z. Batteries and fuel cells for emerging electric vehicle markets. Nat. Energy 2018, 3, 279–289. [Google Scholar] [CrossRef]

- Azad, A.K.; Abdalla, A.M.; Kumarasinghe, P.I.I.; Nourean, S.; Azad, A.T.; Ma, J.; Jiang, C.; Dawood, M.M.K.; Wei, B.; Patabendige, C.N.K. Developments and key challenges in micro/nanostructured binary transition metal oxides for lithium-ion battery anodes. J. Energy Storage 2024, 84, 110850. [Google Scholar] [CrossRef]

- Ayodele, B.V.; Mustapa, S.I. Life Cycle Cost Assessment of Electric Vehicles: A Review and Bibliometric Analysis. Sustainability 2020, 12, 2387. [Google Scholar] [CrossRef]

- Abas, A.E.P.; Yong, J.; Mahlia, T.M.I.; Hannan, M.A. Techno-Economic Analysis and Environmental Impact of Electric Vehicle. IEEE Access 2019, 7, 98565–98578. [Google Scholar] [CrossRef]

- Petrauskienė, K.; Galinis, A.; Kliaugaitė, D.; Dvarionienė, J. Comparative Environmental Life Cycle and Cost Assessment of Electric, Hybrid, and Conventional Vehicles in Lithuania. Sustainability 2021, 13, 957. [Google Scholar] [CrossRef]

- Kara, S.; Li, W.; Sadjiva, N. Life Cycle Cost Analysis of Electrical Vehicles in Australia. Procedia CIRP 2017, 61, 767–772. Available online: https://api.semanticscholar.org/CorpusID:113475092 (accessed on 15 January 2024). [CrossRef]

- Verma, S.; Dwivedi, G.; Verma, P. Life cycle assessment of electric vehicles in comparison to combustion engine vehicles: A review. Mater. Today Proc. 2022, 49, 217–222. [Google Scholar] [CrossRef]

- Held, M.; Schücking, M. Utilization effects on battery electric vehicle life-cycle assessment: A case-driven analysis of two commercial mobility applications. Transp. Res. D Transp. Environ. 2019, 75, 87–105. [Google Scholar] [CrossRef]

- Furch, J.; Konečný, V.; Krobot, Z. Modelling of life cycle cost of conventional and alternative vehicles. Sci. Rep. 2022, 12, 10661. [Google Scholar] [CrossRef] [PubMed]

- Yan, S. The economic and environmental impacts of tax incentives for battery electric vehicles in Europe. Energy Policy 2018, 123, 53–63. [Google Scholar] [CrossRef]

- Fuentes, D.A.M.; González, E.G. Technoeconomic Analysis and Environmental Impact of Electric Vehicle Introduction in Taxis: A Case Study of Mexico City. World Electric. Veh. J. 2021, 12, 93. [Google Scholar] [CrossRef]

- Suman, M.N.H.; Chyon, F.A.; Ahmmed, M.S. Business strategy in Bangladesh—Electric vehicle SWOT-AHP analysis: Case study. Int. J. Eng. Bus. Manag. 2020, 12, 184797902094148. [Google Scholar] [CrossRef]

- Breetz, H.L.; Salon, D. Do electric vehicles need subsidies? Ownership costs for conventional, hybrid, and electric vehicles in 14 U.S. cities. Energy Policy 2018, 120, 238–249. [Google Scholar] [CrossRef]

- Hasan, M.M.; Haque, M.E.; Zahin, M.T.N.; Islam, M.M.; Habib, M.A.; Hasanuzzaman, M. A comparative analysis of energy consumption and GHG emission by the private vehicles of different fuel types in Dhaka, Bangladesh. Energy Nexus 2023, 11, 100222. [Google Scholar] [CrossRef]

- Gransberg, D. Life Cycle Costing for Engineers. Constr. Manag. Econ. 2010, 28, 1113–1114. [Google Scholar] [CrossRef]

- Spickova, M.; Myskova, R. Costs Efficiency Evaluation using Life Cycle Costing as Strategic Method. Procedia Econ. Financ. 2015, 34, 337–343. [Google Scholar] [CrossRef]

- Bangladesh Inflation Rate. Available online: https://tradingeconomics.com/bangladesh/inflation-cpi (accessed on 14 January 2024).

- Yan, M.; He, H.; Li, M.; Li, G.; Zhang, X.; Chen, Z. A comprehensive life cycle assessment on dual-source pure electric bus. J. Clean Prod. 2020, 276, 122702. [Google Scholar] [CrossRef]

- Berckmans, G.; Messagie, M.; Smekens, J.; Omar, N.; Vanhaverbeke, L.; Van Mierlo, J. Cost projection of state of the art lithium-ion batteries for electric vehicles up to 2030. Energies 2017, 10, 1314. [Google Scholar] [CrossRef]

- Elgowainy, A.; Wang, M.; Joseck, F.; Ward, J. Life-Cycle Analysis of Fuels and Vehicle Technologies. Encycl. Sustain. Technol. 2017, 317–327. [Google Scholar] [CrossRef]

- Guo, X.; Sun, Y.; Ren, D. Life cycle carbon emission and cost-effectiveness analysis of electric vehicles in China. Energy Sustain. Dev. 2023, 72, 1–10. [Google Scholar] [CrossRef]

- Bangladesh Bank. Available online: https://www.bb.org.bd/en/index.php (accessed on 15 January 2024).

- Mustapa, S.I.; Ayodele, B.V.; Ishak, W.W.M.; Ayodele, F.O. Evaluation of Cost Competitiveness of Electric Vehicles in Malaysia Using Life Cycle Cost Analysis Approach. Sustainability 2020, 12, 5303. [Google Scholar] [CrossRef]

- Rahman, M.L.; Baker, D.; Rahman, M.S.U. Modelling induced travel demand in a developing country: Evidence from Dhaka, Bangladesh. Transp. Res. Procedia 2020, 48, 3439–3456. [Google Scholar] [CrossRef]

- Salisa, A.R.; Walker, P.D.; Zhang, N.; Zhu, J.G. Comparative cost-based analysis of a novel plug-in hybrid electric vehicle with conventional and hybrid electric vehicles. Int. J. Automot. Mech. Eng. 2015, 11, 2262–2271. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).