Quantification of Expected Return of Investment in Wood Processing Sectors in Slovakia

Abstract

1. Introduction

- RQ 1: What are the values of the expected return on investment in the investigated sectors?

- RQ 2: Are there significant differences in the expected return on investment in the studied industries?

- RQ 3: What are the fundamental causes of the differences in the expected return on investment?

2. Literature Review

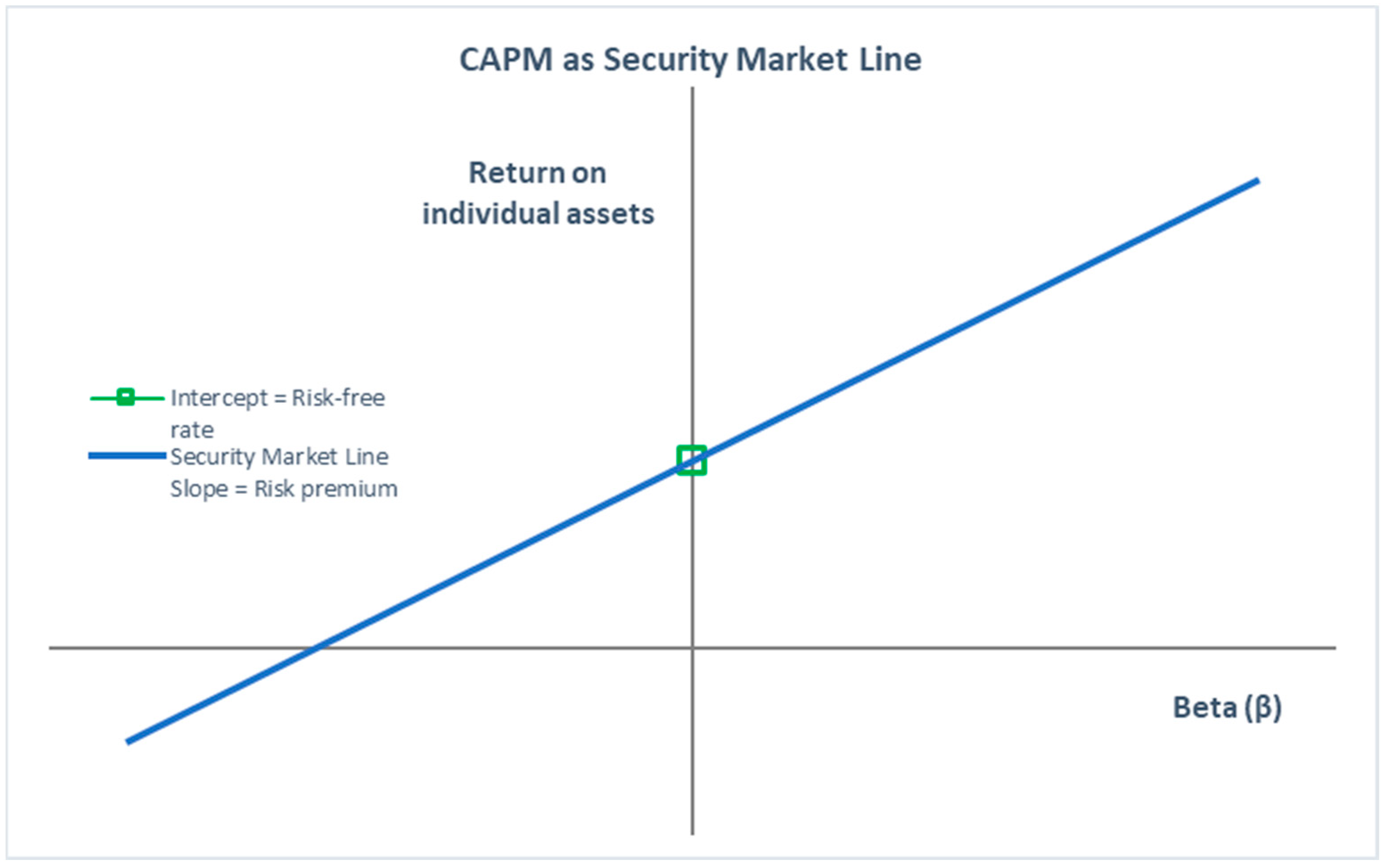

3. Materials and Methods

- The cost of debt capital rd means the interest rate that can be determined as a weighted average of the concluded loan and debt agreements;

- The cost of equity re was also determined based on the Modigliani–Miller theory (1958) [16], which is given by the formula:

- For the risk-free premium rf is usually used as the risk-free interest rate, which is determined, for example, from the US 10-year government bonds;

- Beta coefficient β determination is based on the fact that the debt of the company operates in the value of β;

- Risk premium (rm − rf) is determined for the concrete country of the region according to the rating credit of the rating agency (Standard and Poors’s or Moodys).

- Levered Beta → Inclusive of Capital Structure Effects (D/E Ratio);

- Unlevered Beta → Removed Capital Structure Effects (D/E Ratio).

- Beta = 1: Shares are just as risky as the market (no market sensitivity);

- Beta > 1: Shares are riskier than the market (high market sensitivity);

- Beta < 1: Shares are less risky than the market (low market sensitivity);

- Beta = 0: Shares have no correlation to the market (no market sensitivity).

4. Results and Discussion

5. Conclusions

- Lack of knowledge about methods of determining the required/expected rate of return on investments in wood-processing sectors in Slovakia;

- Absence/insufficient visibility of data on the necessary values for determining the required/expected rate of return on investments in forest-based sectors in Slovakia (value of risk premium, unlevered and levered beta, and the debt level of the sector).

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Feibel, B.J. Calculating investment returns. In Handbook of Finance; Wiley Online Library: New York, NY, USA, 2008. [Google Scholar] [CrossRef]

- Levy, H.; Sarnat, M. Capital Investment and Financial Decisions; Prentice-Hall: Hoboken, NJ, USA, 1986. [Google Scholar]

- Ward, J.; Taylor, P.; Bond, P. Evaluation and realisation of IS/IT benefits: An empirical study of current practice. Eur. J. Inf. Syst. 1996, 4, 214–225. [Google Scholar] [CrossRef]

- Renkema, T.J.; Berghout, E.W. Methodologies for information systems investment evaluation at the proposal stage: A comparative review. Inf. Softw. Technol. 1997, 39, 1–13. [Google Scholar] [CrossRef][Green Version]

- Brealey, M.A.; Myers, S.C. Principles of Corporate Finance; Mc Braw Hill: New York, NY, USA, 2003. [Google Scholar]

- Baum, A.E.; Hartzell, D. Global Property Investment: Strategies, Structures, Decisions; Wiley-Blackwell, Ltd.: West Sussex, UK, 2012. [Google Scholar]

- Damodaran, A. Investment Valuation, Tools and Techniques for Determining the Value of Any Asset, 3rd ed.; John Wiley and Sons: Hoboken, NJ, USA, 2012. [Google Scholar]

- Brealey, R.A.; Myers, S.C.; Allen, F. Principles of Corporate Finance, 2nd ed.; BizBooks: Brno, Czech Republic, 2014; ISBN 978-80-265-0028-5. [Google Scholar]

- Scholleová, H. Investiční Controlling; Grada: Praha, Czech Republic, 2009; ISBN 978-80-247-2952-7. [Google Scholar]

- Forest Europe. State of Europe’s Forests 2020. In Proceedings of the 8th Ministerial Conference on the Protection of Forests in Europe, Bratislava, Slovakia, 14–15 April 2021. [Google Scholar]

- Report on Forestry in the Slovak Republic for 2020—Green Report (2020); National Forestry Center; Ministry of Agriculture and Rural Development of the Slovak Republic: Bratislava, Slovak Republic, 2020.

- Report on Forestry in the Slovak Republic for 2021—Green Report (2021); National Forestry Center; Ministry of Agriculture and Rural Development of the Slovak Republic: Bratislava, Slovak Republic, 2021.

- Merková, M.; Drábek, J.; Jelačić, D. Evaluation of investment management and business performance in wood processing industry in Slovakia. Drv. Ind. 2015, 66, 241–249. [Google Scholar] [CrossRef]

- Merková, M.; Rajnoha, R.; Novák, P. Quantitative and qualitative diagnostic methods for measuring the effects of foreign direct investment in terms of the wood-processing industry in the Slovak Republic. Drewno 2012, 55, 187. [Google Scholar]

- Kara, G.; Özmen, A.; Weber, G.W. Stability advances in robust portfolio optimization under parallelepiped uncertainty. Cent. Eur. J. Oper. Res. 2019, 27, 241–261. [Google Scholar] [CrossRef]

- Modigliani, F.; Miller, M.H. The cost of capital, corporation finance and the theory of investment. Am. Econ. Rev. 1958, 48, 261–297. [Google Scholar]

- Özmen, A.; Kropat, E.; Weber, G.W. Robust optimization in spline regression models for multi-model regulatory networks under polyhedral uncertainty. Optimization 2017, 66, 2135–2155. [Google Scholar] [CrossRef]

- Savku, E.; Weber, G.W. A stochastic maximum principle for a markov regime-switching jump-diffusion model with delay and an application to finance. J. Optim. Theory Appl. 2018, 179, 696–721. [Google Scholar] [CrossRef]

- Fotr, J.; Souček, I. Investiční Rozhodování a Řízení Projektů: Jak Připravovat, Financovat a Hodnotiť Projekty, Řídit Jejich Riziko a Vytvářet Portfolio Projektů [Investment Decision-Making and Project Management: How to Prepare, Finance and Evaluate Projects, Manage Their Risk and Create a Portfolio of Projects]; Praha Grada Publishing: Prague, Czech Republic, 2011; ISBN 978-80-247-3293-0. [Google Scholar]

- Markowitz, H. Portfolio Selection. J. Financ. 1952, 7, 77–99. [Google Scholar]

- Markowitz, H. Portfolio Selection: Efficient Diversification of Investments. Cowles Foundation Monograph No. 16; John Wiley and Sons, Inc.: New York, NY, USA, 1959; pp. 1541–1578. [Google Scholar]

- Treynor, J.L. Market Value, Time, and Risk. Financ. Educ. Courses 1961, 95–209. [Google Scholar] [CrossRef]

- Treynor, J.L. Toward a Theory of Market Value of Risky Assets; Wiley Online Library: New York, NY, USA, 1962. [Google Scholar]

- Sharpe, W.F. Capital asset prices: A theory of market equilibrium under conditions of risk. J. Financ. 1964, 19, 425–442. [Google Scholar]

- Lintner, J. The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets. Rev. Econ. Stat. 1965, 47, 13–37. [Google Scholar] [CrossRef]

- Mossin, J. Equilibrium in a Capital Asset Market. Econometrica 1966, 34, 768–783. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. The capital asset pricing model: Theory and evidence. J. Econ. Perspect. 2004, 18, 25–46. [Google Scholar] [CrossRef]

- Wang, C.P.; Huang, H.H.; Hu, J.S. Reverse-Engineering and Real Options–Adjusted CAPM in the Taiwan Stock Market. Emerg. Mark. Financ. Trade 2017, 53, 670–687. [Google Scholar] [CrossRef]

- Anjum, N.; Rajput, S.K.O. Forecasting Islamic equity indices alpha. Int. J. Islam. Middle East. Financ. Manag. 2021, 14, 183–203. [Google Scholar] [CrossRef]

- Taussig, R.D. New evidence on practical implications of the CAPM: In memory of Simon Benninga. J. Corp. Account. Financ. 2022, 33, 72–77. [Google Scholar] [CrossRef]

- Anuno, F.; Madaleno, M.; Vieira, E. Using the Capital Asset Pricing Model and the Fama–French Three-Factor and Five-Factor Models to Manage Stock and Bond Portfolios: Evidence from Timor-Leste. J. Risk Financ. Manag. 2023, 16, 480. [Google Scholar] [CrossRef]

- Yamaka, W.; Phadkantha, R. A convex combination approach for Markov switching CAPM of interval data. Soft Comput. 2021, 25, 7839–7851. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. The value premium and the CAPM. J. Finance 2006, 61, 2163–2185. [Google Scholar] [CrossRef]

- Klieštik, T. Investment Management—Financial Investments; University of Žilina: Žilina, Slovakia, 2008; 138p. [Google Scholar]

- Fama, E.F.; French, K.R. A five-factor asset pricing model. J. Financ. Econ. 2015, 116, 1–22. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. International tests of a five-factor asset pricing model. J. Financ. Econ. 2017, 123, 441–463. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. Choosing factors. J. Financ. Econ. 2018, 128, 234–252. [Google Scholar] [CrossRef]

- Fama, E.F.; Macbeth, J.D. Risk, Return, and Equilibrium: Empirical Tests. J. Polit. Econ. 1973, 81, 607–636. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. Comparing Cross-Section and Time-Series Factor Models. Rev. Financial Stud. 2020, 33, 1891–1926. [Google Scholar] [CrossRef]

- Wang, J.; Chen, Z. Exploring Low-Risk Anomalies: A Dynamic CAPM Utilizing a Machine Learning Approach. Mathematics 2023, 11, 3220. [Google Scholar] [CrossRef]

- Merková, M.; Drábek, J.; Jelačić, D. Application of Risk Analysis in Business Investment Decision-Making. Drv. Ind. 2013, 64, 313–322. [Google Scholar] [CrossRef]

- Truong, G.; Partington, G.; Peat, M. Cost-of-Capital Estimation and Capital-Budgeting Practice in Australia. Aust. J. Manag. 2008, 33, 95–121. [Google Scholar] [CrossRef]

- Babusiaux, D.; Pierru, A. Capital budgeting, investment project valuation and financing mix: Methodological proposals. Eur. J. Oper. Res. 2001, 135, 326–337. [Google Scholar] [CrossRef]

- Zhang, L. The investment CAPM. Eur. Financ. Manag. 2017, 23, 545–603. [Google Scholar] [CrossRef]

- Vendrame, V.; Guermat, C.; Tucker, J. A conditional regime switching CAPM. Int. Rev. Financ. Anal. 2018, 56, 1–11. [Google Scholar] [CrossRef]

- Barberis, N.; Greenwood, R.; Jin, L.; Shleifer, A. X-CAPM: An extrapolative capital asset pricing model. J. Financ. Econ. 2015, 115, 1–24. [Google Scholar] [CrossRef]

- Hung, C. Return Predictability of Higher-Moment CAPM Market Models. J. Bus. Finance Account. 2008, 35, 998–1022. [Google Scholar] [CrossRef]

- Da, Z.; Guo, R.-J.; Jagannathan, R. CAPM for estimating the cost of equity capital: Interpreting the empirical evidence. J. Financ. Econ. 2012, 103, 204–220. [Google Scholar] [CrossRef]

- Chen, J.M. The capital asset pricing model. Encyclopedia 2021, 1, 915–933. [Google Scholar] [CrossRef]

- de Andrade Alves, C.R.; Laurini, M. Estimating the Capital Asset Pricing Model with Many Instruments: A Bayesian Shrinkage Approach. Mathematics 2023, 11, 3776. [Google Scholar] [CrossRef]

- Damodaran, A. Regional Breakdown. Last Update: 5 January 2022. 2022. Available online: http://people.stern.nyu.edu/adamodar/New_Home_Page/databreakdown.html#region (accessed on 11 April 2022).

- National Bank of Slovakia. Long-Term Interest Rates Statistics. Monthly Survey on Yield to Maturity of the 10 Years Government Bond—Benchmark. 2022. Available online: https://nbs.sk/statisticke-udaje/financne-trhy/urokove-sadzby/dlhodobe-urokove-sadzby/ (accessed on 24 May 2022).

- National Bank of Slovakia. Estimated Yield Curve. 2022. Available online: https://nbs.sk/en/statistics/financial-markets/interest-rates/estimated-yield-curve/ (accessed on 24 May 2022).

- Hamada, R.S. The effect of the firm’s capital structure on the systematic risk of common stocks. J. Financ. 1972, 27, 435–452. [Google Scholar] [CrossRef]

- Damodaran, A. Damodaran on Valuation; John Wiley and Sons: New York, NY, USA, 1994. [Google Scholar]

- Dybvig, P.H.; Ross, S.A. Differential information and performance measurement using a security market line. J. Financ. 1985, 40, 383–399. [Google Scholar] [CrossRef]

- Damodaran, A. Beta, Unlevered Beta and Other Risk Measures. Last Update: 5 January 2022. 2022. Available online: https://pages.stern.nyu.edu/~adamodar/pc/datasets/betaemerg.xls (accessed on 11 April 2022).

- National Bank of Slovakia. Average Lending Rates of Commercial Banks. 2022. Available online: https://nbs.sk/en/statistics/financial-markets/interest-rates/average-lending-rates-of-commercial-banks/ (accessed on 17 October 2022).

- Arouri, M.E.H.; Nguyen, D.K.; Pukthuanthong, K. An international CAPM for partially integrated markets: Theory and empirical evidence. J. Bank. Financ. 2012, 36, 2473–2493. [Google Scholar] [CrossRef]

- Blitz, D.; Falkenstein, E.; Van Vliet, P. Explanations for the volatility effect: An overview based on the CAPM assumptions. J. Portf. Manag. 2014, 40, 61–76. [Google Scholar] [CrossRef]

- Dempsey, M. The capital asset pricing model (CAPM): The history of a failed revolutionary idea in finance? Abacus 2013, 49, 7–23. [Google Scholar] [CrossRef]

- Chatterjee, S.; Lubatkin, M.H.; Lyon, E.M.; Schulze, W.S. Toward a Strategic Theory of Risk Premium: Moving beyond Capm. Acad. Manag. Rev. 1999, 24, 556. [Google Scholar] [CrossRef][Green Version]

- Kumar, S.; Kumar, A.; Singh, K.U.; Patra, S.K. The Six Decades of the Capital Asset Pricing Model: A Research Agenda. J. Risk Financial Manag. 2023, 16, 356. [Google Scholar] [CrossRef]

- OECD. Addressing Data Gaps in Long-Term Investment: An Agenda for Research. 2015. Available online: https://www.oecd.org/finance/private-pensions/Addressing-Data-Gaps-in-Long-Term-Investment-Research-Agenda.pdf (accessed on 20 September 2023).

- IMF. G-20 Data Gaps Initiative II: Meeting the Policy Challenge. 2016. Available online: https://www.imf.org/external/pubs/ft/wp/2016/wp1643.pdf (accessed on 14 August 2023).

{kind=link}

| Region | Includes | Included Countries |

|---|---|---|

| United States | Just US | |

| Europe | Western Europe and the UK (EU, UK, Switzerland, and Scandinavia) | Czech Republic, Croatia |

| Japan | Just Japan | |

| Emerging Markets | All of Asia, other than Japan, Latin America, Africa, the Middle East, Eastern Europe, and Russia, with a further breakdown for India and China | Slovakia, Slovenia |

| Australia, New Zealand, and Canada | Australia, New Zealand, and Canada | |

| Global | All firms |

| Industry Sector | Number of Firms | Levered Beta | D/E Ratio | Tax Rate | Unlevered Beta |

|---|---|---|---|---|---|

| Furn/Home Furnishings | 250 | 1.16 | 15.23% | 15.23% | 1.05 |

| Paper/Forest Products | 187 | 1.17 | 65.83% | 12.93% | 0.79 |

| Total Market | 24,435 | 1.11 | 55.19% | 13.47% | 0.79 |

| Total Market (without financials) | 21,977 | 1.13 | 33.31% | 13.33% | 0.91 |

| Geometric Average Historical Return | S&P 500 | 10-Year US T. Bond | Risk Premium (US) | CDS (SVK) | Risk Premium (SVK) |

|---|---|---|---|---|---|

| (rm) | (rf) | (rm − rf) | (rm − rf) | ||

| 1928–2021 | 9.98% | 4.84% | 5.13% | 1.03% | 6.16% |

| Indicator/Sector | Furniture/Home Furnishings | Paper/ Forest Products | |

|---|---|---|---|

| βu | Unlevered beta | 1.05 | 0.79 |

| D/E | D/E Ratio | 15% | 65% |

| t | Corporate tax rate | 21% | 21% |

| βl | Levered beta | 1.17 | 1.20 |

| Indicator/Sector | Furniture/Home Furnishings | Paper/ Forest Products | |

|---|---|---|---|

| rf (SVK) | Risk-free rate (SVK) | 1.529% | 1.529% |

| βl | Beta coefficient | 1.17 | 1.20 |

| (rm − rf) SVK | Risk premium (SVK) | 6.16% | 6.16% |

| re | Rate of Equity | 8.76% | 8.91% |

| Indicator/Sector | Furniture/Home Furnishings | Paper/ Forest Products | |

|---|---|---|---|

| rd | Rate of dept | 2.07% | 2.07% |

| t | Corporate tax rate | 21% | 21% |

| rd × (1 − t) | Rate of dept after tax | 1.64% | 1.64% |

| D/C | Dept share | 0.13 | 0.395 |

| re | Rate of equity | 8.76% | 8.91% |

| E/C | Equity share | 0.87 | 0.605 |

| WACC | Expected rate of return | 7.84% | 6.04% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kánová, M.; Drábek, J.; Ćurić, P.; Pirc Barčić, A. Quantification of Expected Return of Investment in Wood Processing Sectors in Slovakia. Forests 2024, 15, 75. https://doi.org/10.3390/f15010075

Kánová M, Drábek J, Ćurić P, Pirc Barčić A. Quantification of Expected Return of Investment in Wood Processing Sectors in Slovakia. Forests. 2024; 15(1):75. https://doi.org/10.3390/f15010075

Chicago/Turabian StyleKánová, Martina, Josef Drábek, Petar Ćurić, and Andreja Pirc Barčić. 2024. "Quantification of Expected Return of Investment in Wood Processing Sectors in Slovakia" Forests 15, no. 1: 75. https://doi.org/10.3390/f15010075

APA StyleKánová, M., Drábek, J., Ćurić, P., & Pirc Barčić, A. (2024). Quantification of Expected Return of Investment in Wood Processing Sectors in Slovakia. Forests, 15(1), 75. https://doi.org/10.3390/f15010075