The Effects of Geopolitical Uncertainty in Forecasting Financial Markets: A Machine Learning Approach

Abstract

1. Introduction

2. Methodology and Data

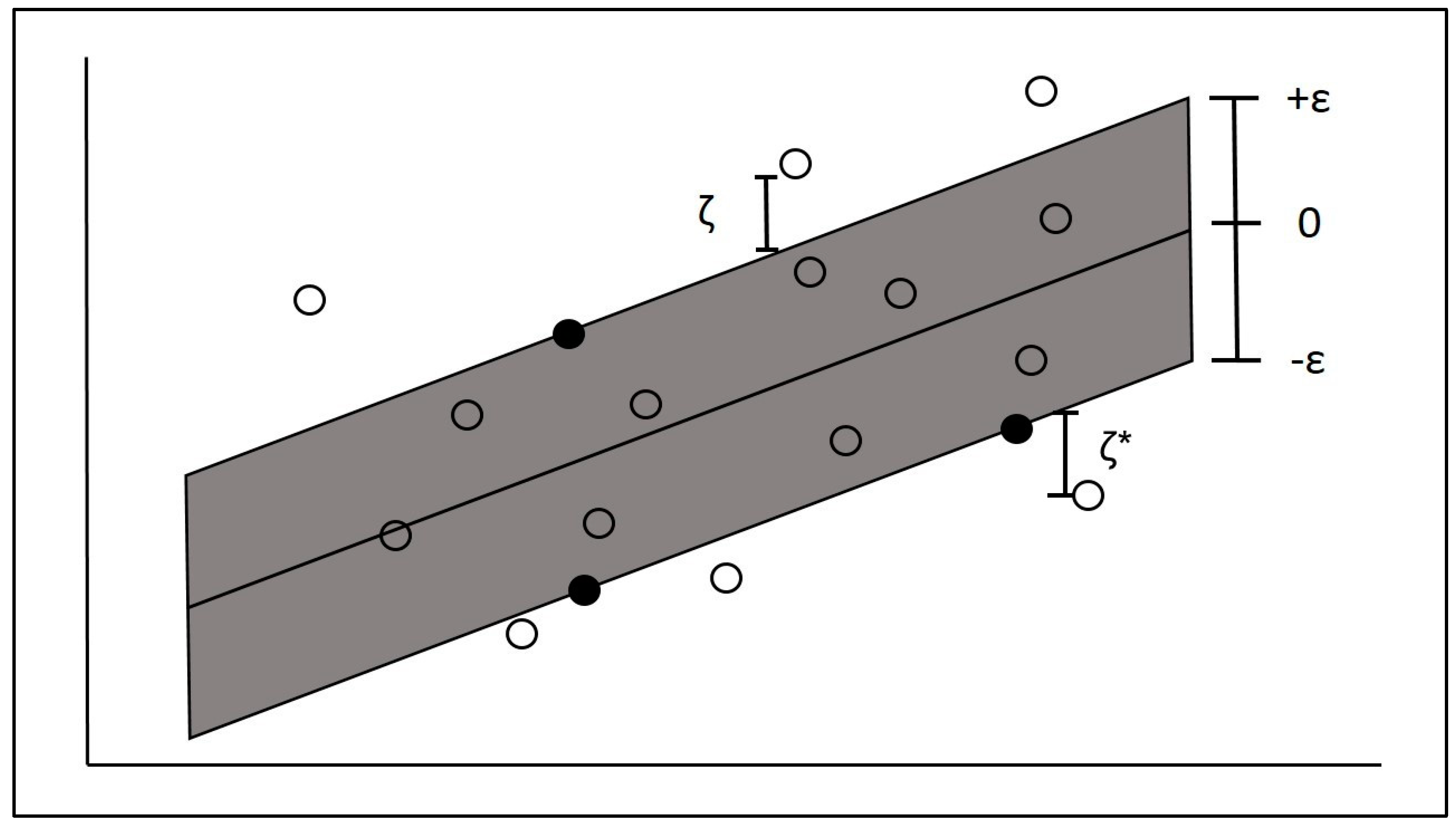

2.1. Support Vector Regression

2.2. The Data

3. Empirical Results

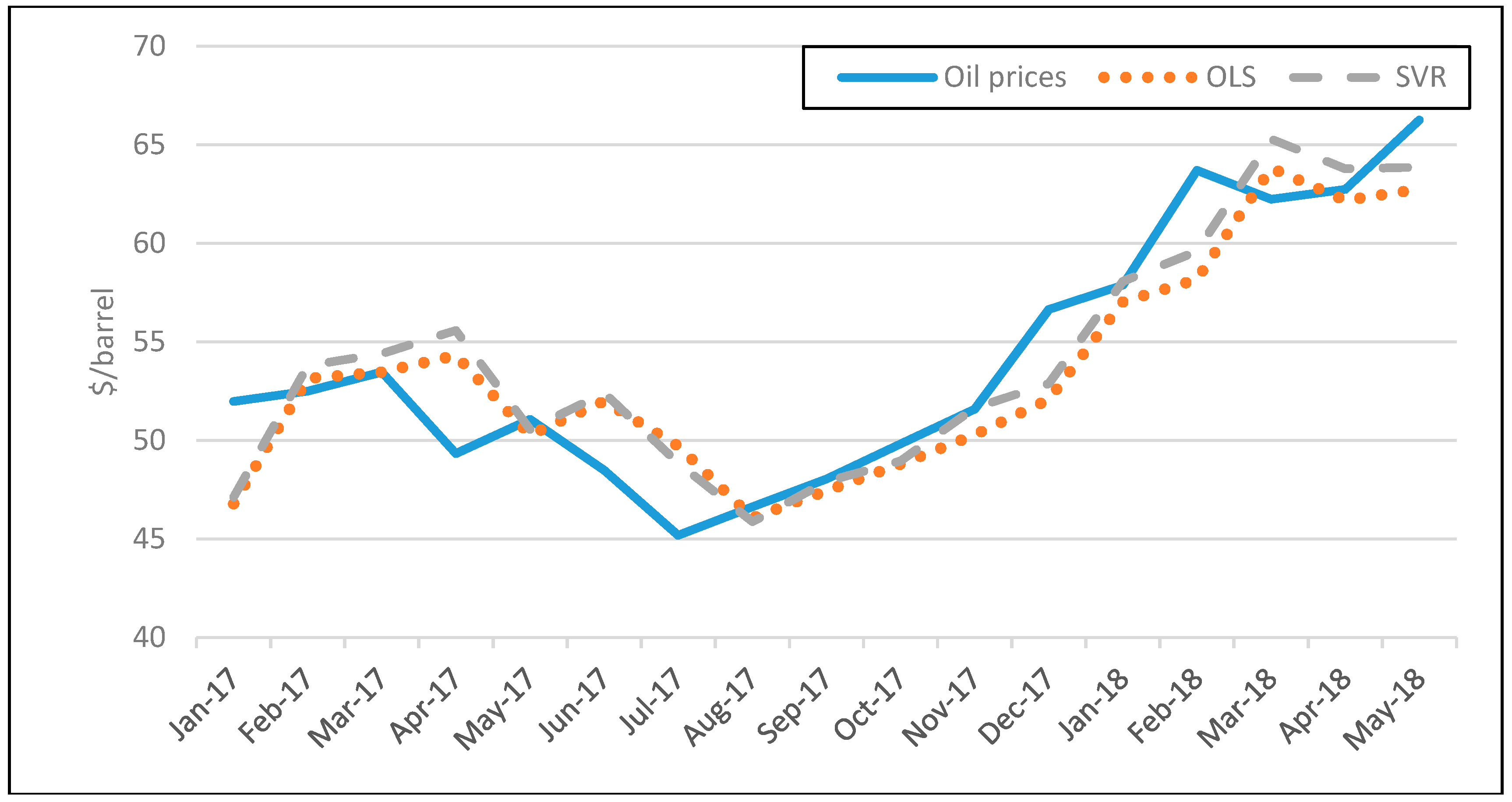

3.1. Oil prices

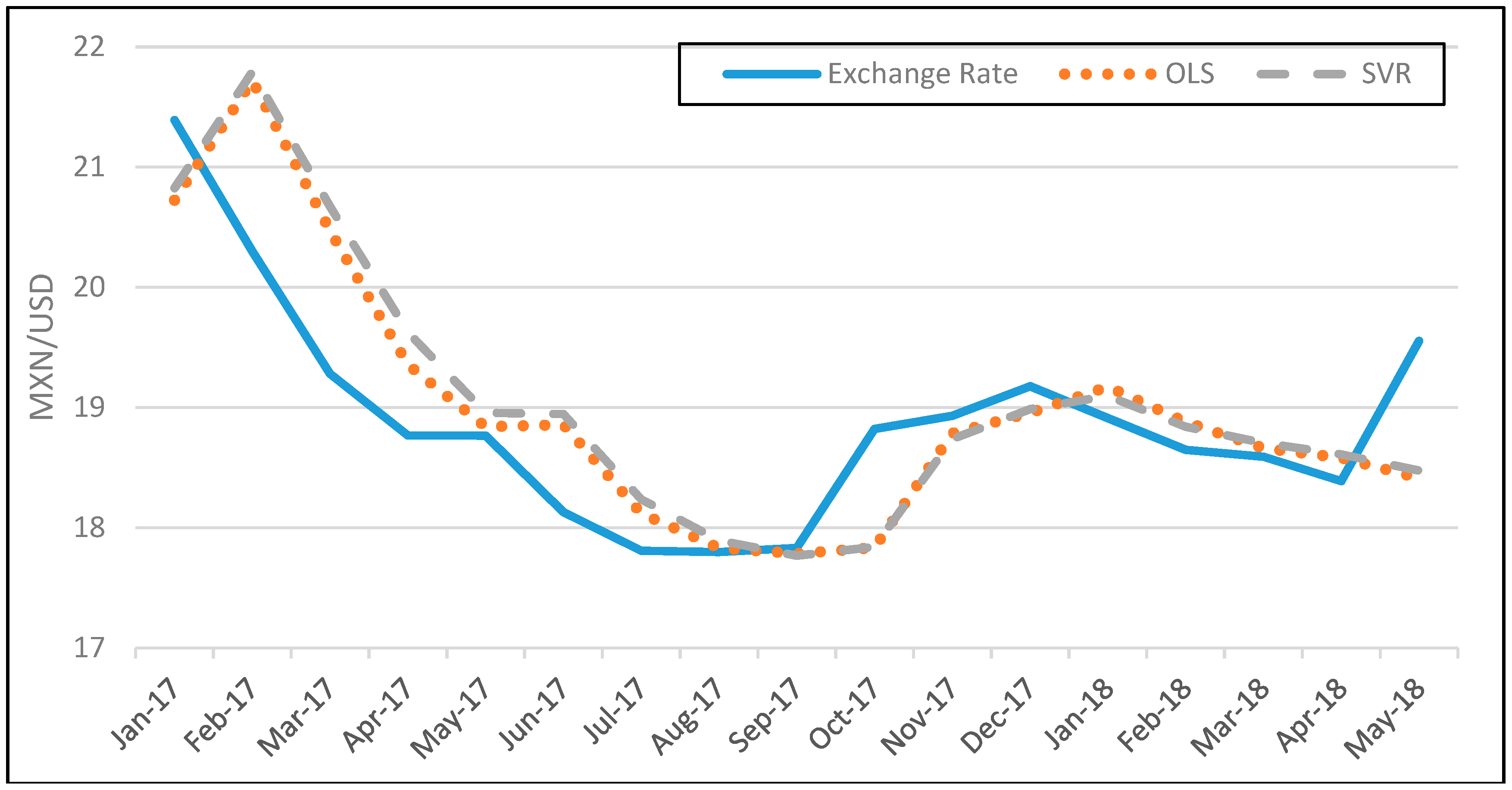

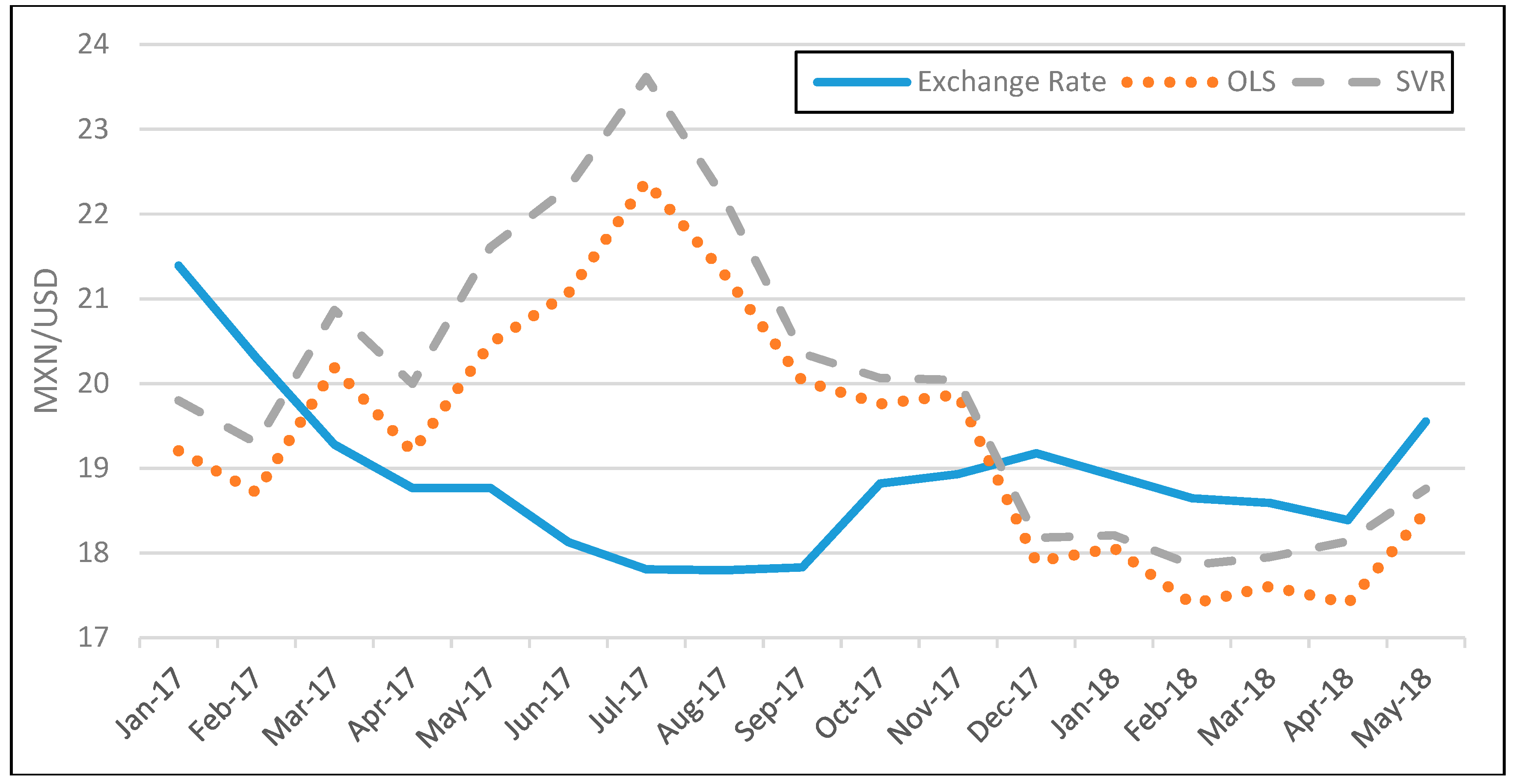

3.2. Exchange Rates

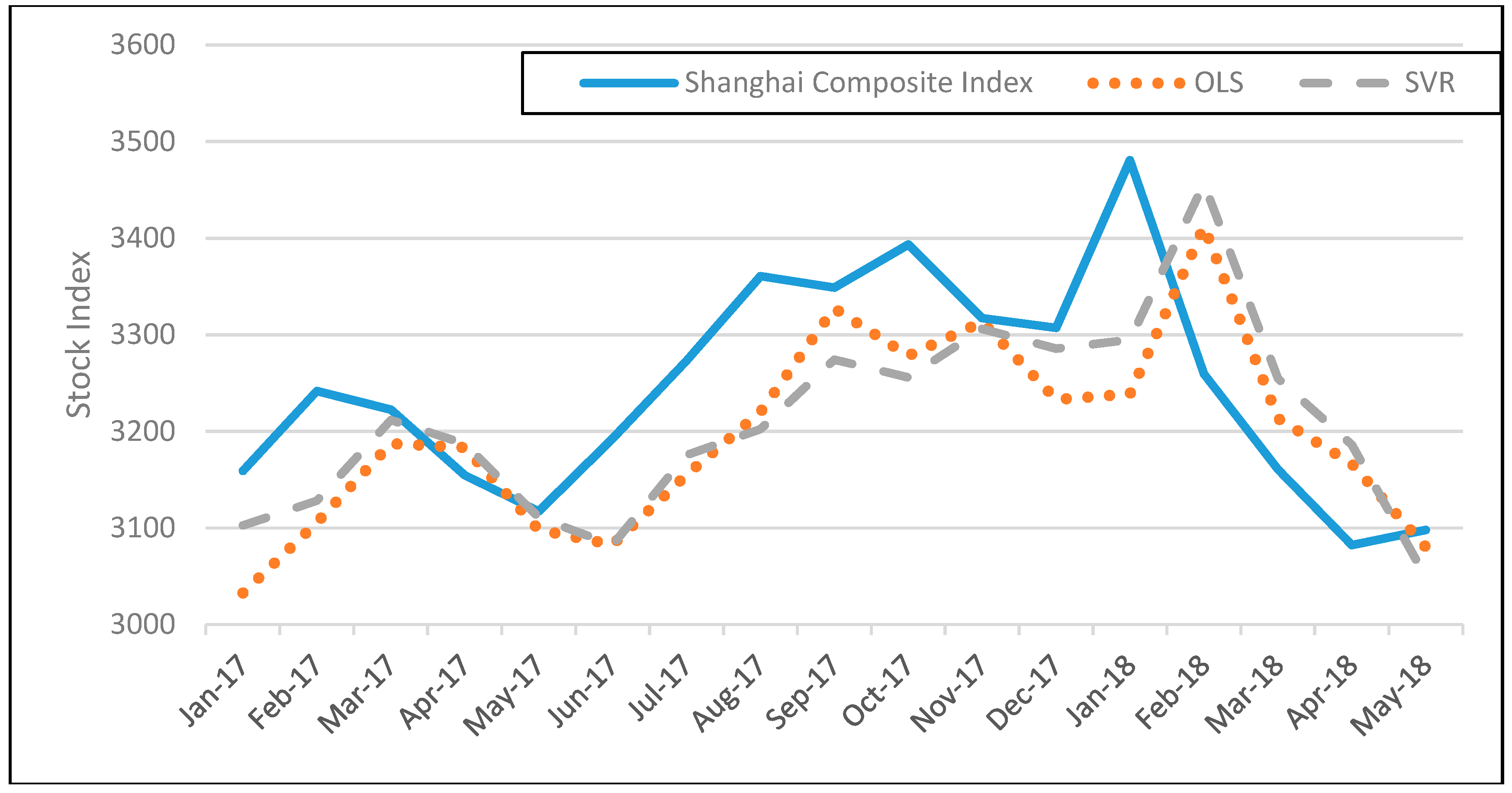

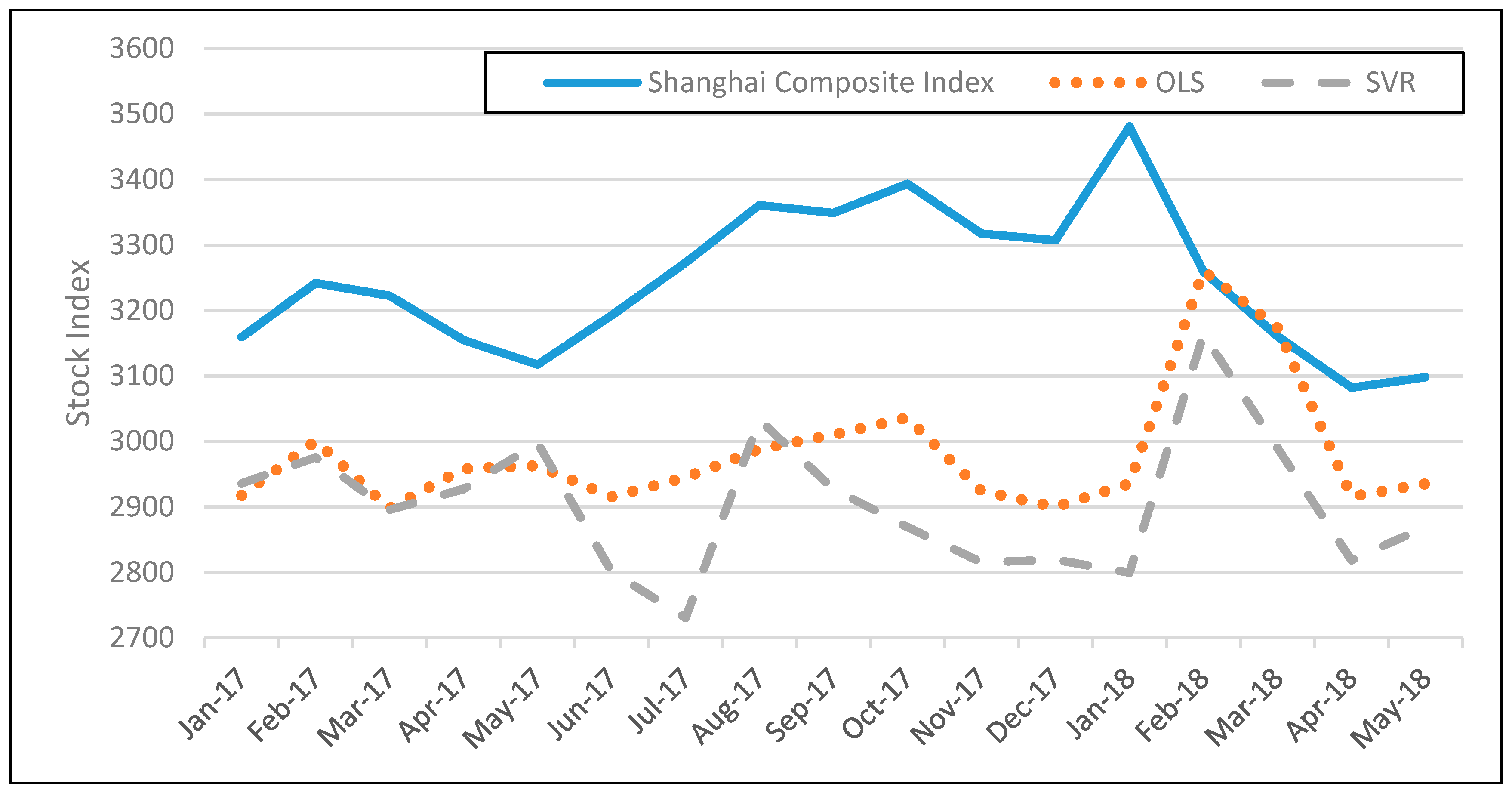

3.3. Stock Indices

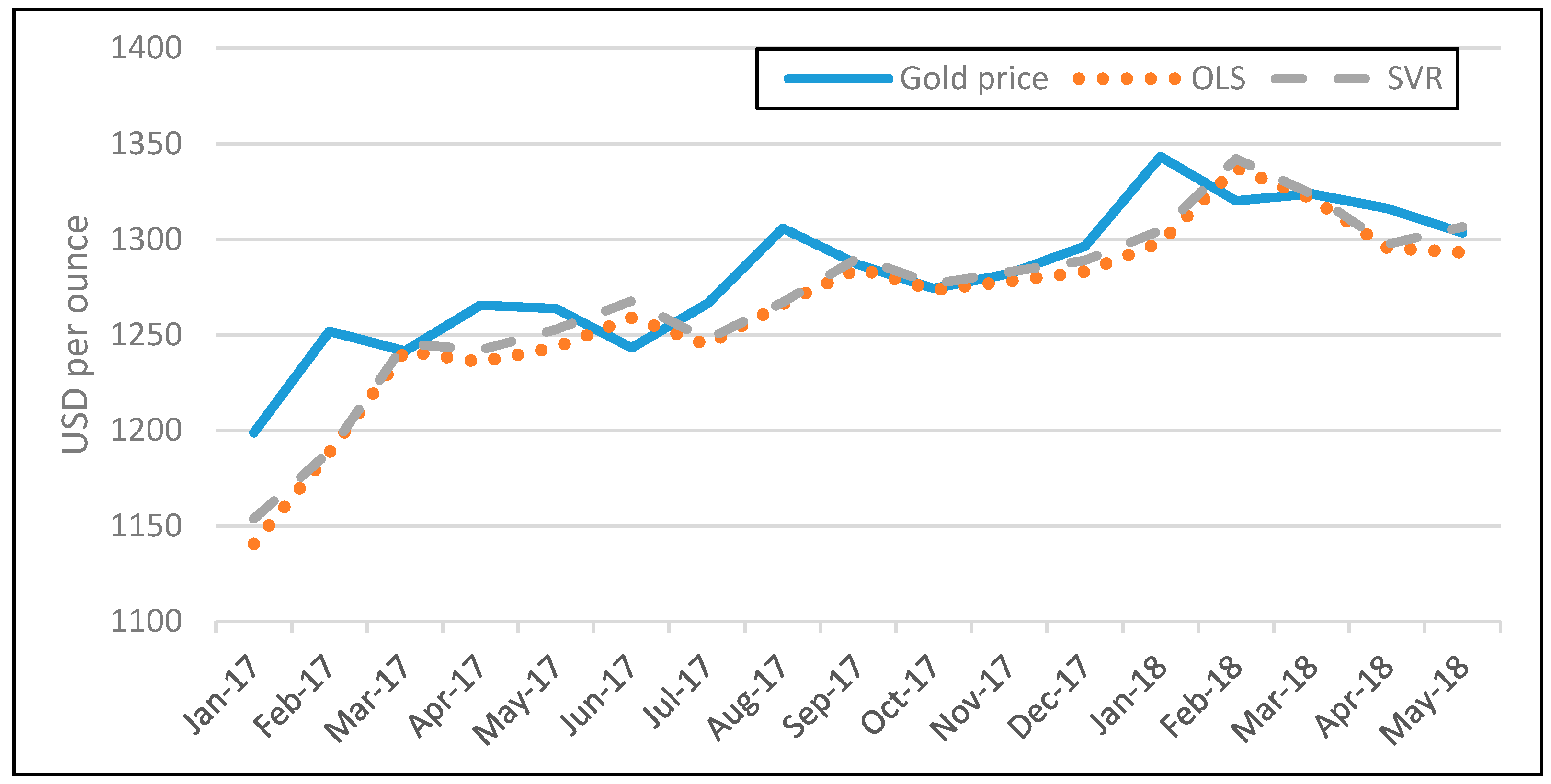

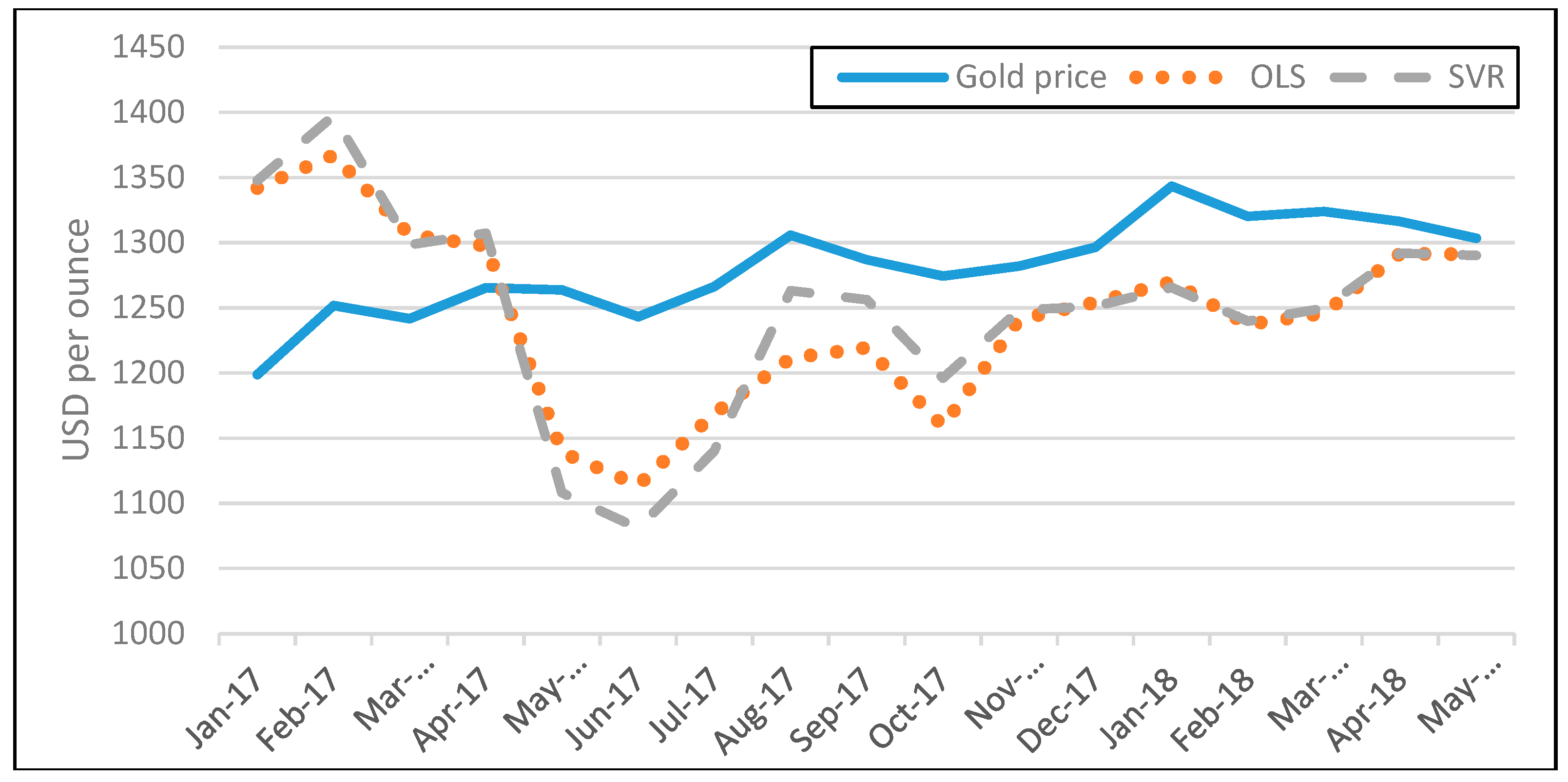

3.4. Gold Prices

4. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Carney, M. Uncertainty, the Economy and Policy; Bank of England: London, UK, 2016. [Google Scholar]

- European Central Bank. Economic Bulletin, Frankfurt, 2017, 3. Available online: https://www.ecb.europa.eu/pub/economic-bulletin/html/eb201703.en.html (accessed on 20 December 2018).

- International Monetary Fund. Seeking Sustainable Growth: Short-Term Recovery, Long-Term Challenges. Washington, DC, USA, October 2017. Available online: https://www.imf.org/~/media/Files/Publications/WEO/2017/October/pdf/main-chapter/text.ashx (accessed on 20 December 2018).

- Alesina, A.; Ozler, S.; Roubini, N.; Swagel, P. Political instability and economic growth. J. Econ. Growth 1996, 1, 189–211. [Google Scholar] [CrossRef]

- Asteriou, D.; Siriopoulos, C. The role of political instability in stock market development and economic growth: The case of Greece. Econ. Notes 2000, 29, 355–374. [Google Scholar] [CrossRef]

- Kollias, C.; Papadamou, S.; Siriopoulos, C. Terrorism Induced Cross-Market Transmission of Shocks: A Case Study Using Intraday Data; Economics of Security Working Paper, No. 66; Deutsches Institut für Wirtschaftsforschung (DIW): Berlin, Germany, 2012. [Google Scholar]

- Blomberg, B.; Hess, G.; Jackson, H. Terrorism and the returns to oil. Econ. Politics 2009, 21, 409–432. [Google Scholar] [CrossRef]

- Antonakakis, N.; Gupta, R.; Kollias, C.; Papadamou, S. Geopolitical risks and the oil-stock nexus over 1899–2016. Financ. Res. Lett. 2017, 23, 165–173. [Google Scholar] [CrossRef]

- Kollias, C.; Kyrtsou, C.; Papadamou, S. The Effects of Terrorism and War on the Oil Price–stock Index Relationship. Energy Econ. 2013, 40, 743–752. [Google Scholar] [CrossRef]

- Drakos, K. Terrorism activity, investor sentiment and stock returns. Rev. Financ. Econ. 2010, 19, 128–135. [Google Scholar] [CrossRef]

- Kollias, C.; Papadamou, S.; Stagiannis, A. Stock markets and terrorist attacks: Comparative evidence from a large and a small capitalization market. Eur. J. Political Econ. 2011, 27 (Suppl. 1), S64–S77. [Google Scholar] [CrossRef]

- Nikkinen, J.; Omran, M.; Sahlstrom, P.; Aijo, J. Stock returns and volatility following the September 11 attacks: Evidence from 53 equity markets. Int. Rev. Financ. Anal. 2008, 17, 27–46. [Google Scholar] [CrossRef]

- Gupta, R.; Majumdar, A.; Pierdzioch, C.; Wohar, M.E. Do Terror Attacks Predict Gold Returns? Evidence from a Quantile-Predictive-Regression Approach. Q. Rev. Econ. Financ. 2017, 65, 276–284. [Google Scholar] [CrossRef]

- International Monetary Fund. How has September 11 influenced the global economy. In World Economic Outlook; International Monetary Fund: Washington, DC, USA, 2001; Chapter 2; pp. 14–33. [Google Scholar]

- Balcilar, M.; Gupta, R.; Pierdzioch, C.; Wohar, M. Do terror attacks affect the dollar-pound exchange rate? A nonparametric causality-in-quantiles analysis. N. Am. J. Econ. Financ. 2017, 41, 44–56. [Google Scholar] [CrossRef]

- Filippou, I.; Gozluklu, A.; Taylor, M. Global Political Risk and Currency Momentum. J. Financ. Quant. Anal. 2018, 53, 2227–2259. [Google Scholar] [CrossRef]

- Suleman, M.T. Political Uncertainty, Exchange Rate Return and Volatility. 2015. Available online: https://ssrn.com/abstract=2598866 (accessed on 1 October 2018).

- Cosset, J.C.; Doutriaux De La Rianderie, B. Political Risk and Foreign Exchange Rates: An Efficient-Market Approach. Int. J. Bus. Stud. 1985, 16, 21–55. [Google Scholar] [CrossRef]

- Caldara, D.; Iacovello, M. Measuring Geopolitical Risk. Board of Governors of the Federal Reserve System; International Finance Discussion Paper; Federal Reserve: Washington, DC, USA, 2018; No. 1222. [Google Scholar]

- Davis, S. Policy Uncertainty vs. the VIX: Streets and Horizons. In Proceedings of the Federal Reserve Board Workshop on Global Risk, Uncertainty, and Volatility, Washington, DC, USA, 25 September 2017. [Google Scholar]

- Mensi, W.; Beljid, M.; Boubaker, A.; Managi, S. Correlations and Volatility Spillovers across Commodity and Stock Markets: Linking Energies, Food, and Gold. Econ. Model. 2013, 32, 15–22. [Google Scholar] [CrossRef]

- Mullainathan, S.; Spiess, J. Machine Learning: An Applied Econometric Approach. J. Econ. Perspect. 2017, 31, 87–106. [Google Scholar] [CrossRef]

- Campbell, J.Y. Viewpoint: Estimating the equity premium. Can. J. Econ. 2008, 41, 1–21. [Google Scholar] [CrossRef]

- Khandani, A.E.; Kim, A.J.; Lo, A.W. Consumer credit-risk models via machine-learning algorithms. J. Bank. Financ. 2010, 34, 2767–2787. [Google Scholar] [CrossRef]

- Öğüt, H.; Doğanay, M.M.; Ceylan, N.B.; Aktaş, R. Prediction of bank financial strength ratings: The case of Turkey. Econ. Model. 2012, 29, 632–640. [Google Scholar] [CrossRef]

- Plakandaras, V.; Gupta, R.; Gogas, P.; Papadimitriou, T. Forecasting the U.S., Real House Price Index. Econ. Model. 2015, 45, 259–267. [Google Scholar] [CrossRef]

- Rubio, G.; Pomares, H.; Rojas, I.; Herrera, L.J. A heuristic method for parameter selection in LS-SVM: Application to time series prediction. Int. J. Forecast. 2011, 27, 725–739. [Google Scholar] [CrossRef]

- Cortes, C.; Vapnik, V. Support-Vector Networks. Mach. Learn. 1995, 20, 273–297. [Google Scholar] [CrossRef]

- U.S. Geological Survey. Mineral Commodity Summaries 2018; U.S. Geological Survey: Reston, VA, USA, 2018.

- Jones, A.; Sackley, W. An uncertain suggestion for gold-pricing models: The effect of economic policy uncertainty on gold prices. J. Econ. Financ. 2106, 40, 367–379. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Countries | Mean | Standard Deviation | Skewness | Kurtosis | Start Date | End Date |

|---|---|---|---|---|---|---|

| Panel A: Exchange rates | ||||||

| Turkey | −1.79 | 2.95 | −0.76 | 2.00 | Dec-84 | Apr-18 |

| Mexico | 2.37 | 0.36 | −1.19 | 5.69 | Dec-92 | Jun-17 |

| Korea | 6.89 | 0.20 | −0.17 | 2.00 | Dec-84 | May-18 |

| Russia | 2.89 | 1.21 | −1.68 | 5.49 | May-92 | Mar-18 |

| India | 3.58 | 0.50 | −0.96 | 2.78 | Dec-84 | May-18 |

| Brazil | 0.71 | 0.38 | −0.46 | 2.52 | Dec-94 | May-18 |

| China | 1.86 | 0.30 | −1.13 | 3.29 | Dec-84 | May-18 |

| Indonesia | 8.55 | 0.84 | −0.48 | 1.50 | Dec-84 | Mar-18 |

| Saudi Arabia | 1.32 | 0.00 | −3.69 | 50.75 | Oct-95 | May-18 |

| Argentina | 1.20 | 0.87 | 0.17 | 2.37 | Jul-96 | May-18 |

| Thailand | 3.46 | 0.19 | 0.25 | 1.78 | Dec-84 | May-18 |

| Israel | 1.15 | 0.37 | −1.32 | 4.19 | Dec-84 | Mar-18 |

| Malaysia | 1.16 | 0.18 | −0.03 | 1.53 | Dec-84 | May-18 |

| Philippines | 3.80 | 0.19 | −1.53 | 5.21 | Oct-95 | May-18 |

| Panel B: Stock indices | ||||||

| Turkey | 8.88 | 2.61 | −0.91 | 2.44 | Dec-89 | May-18 |

| Mexico | 9.37 | 1.15 | −0.25 | 1.61 | Oct-91 | May-18 |

| Korea | 6.83 | 0.66 | −0.72 | 3.50 | Dec-84 | May-18 |

| Russia | 6.56 | 1.12 | −1.10 | 3.19 | Aug-97 | May-18 |

| India | 8.49 | 1.29 | −0.33 | 2.12 | Dec-84 | May-18 |

| Brazil | 8.61 | 3.94 | −2.16 | 6.54 | Nov-89 | May-18 |

| China | 7.35 | 0.73 | −1.27 | 5.22 | Nov-90 | May-18 |

| Indonesia | 6.69 | 1.30 | −0.11 | 2.20 | Dec-84 | May-18 |

| Saudi Arabia | 8.37 | 0.76 | −0.30 | 1.71 | Dec-93 | May-18 |

| Argentina | 6.66 | 2.39 | −2.09 | 9.16 | Dec-87 | May-18 |

| Thailand | 6.87 | 0.40 | −0.18 | 1.91 | Apr-03 | May-18 |

| Israel | 6.38 | 0.69 | −0.39 | 1.73 | Aug-92 | May-18 |

| Malaysia | 7.15 | 0.33 | −0.57 | 1.97 | Jun-02 | May-18 |

| Philippines | 7.76 | 0.71 | 0.14 | 2.12 | Nov-86 | May-18 |

| Panel C: Other variables | ||||||

| WTI oil | 3.54 | 0.65 | 0.36 | 1.78 | Dec-84 | May-18 |

| Gold price | 6.30 | 0.60 | 0.64 | 1.82 | Dec-84 | May-18 |

| Forecasting Horizons | 1 Month | 3 Months | 6 Months | 12 Months | 24 Months | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Country | OLS | SVR | RW | OLS | SVR | RW | OLS | SVR | RW | OLS | SVR | RW | OLS | SVR | RW |

| Turkey | 6.86 | 6.86 | 6.69 | 15.74 | 15.63 | 13.98 | 28.27 | 27.34 | 21.06 | 42.76 | 43.64 | 27.58 | 50.70 | 48.98 | 36.74 |

| Mexico | 7.02 | 7.02 | 6.68 | 16.27 | 16.30 | 14.68 | 29.47 | 28.28 | 22.65 | 43.25 | 42.27 | 30.05 | 49.12 | 47.58 | 39.64 |

| Korea | 6.73 | 6.68 | 6.55 | 15.13 | 15.49 | 13.33 | 25.96 | 25.79 | 20.16 | 36.70 | 36.32 | 27.59 | 44.59 | 42.95 | 36.56 |

| Russia | 7.21 | 7.26 | 6.98 | 17.77 | 17.84 | 16.27 | 31.68 | 29.24 | 25.10 | 45.89 | 42.39 | 32.44 | 49.35 | 46.98 | 43.24 |

| India | 6.88 | 6.77 | 6.55 | 15.39 | 15.12 | 13.33 | 25.85 | 25.15 | 20.16 | 35.83 | 36.56 | 27.59 | 42.98 | 46.78 | 36.56 |

| Brazil | 6.88 | 6.85 | 6.77 | 16.44 | 16.53 | 14.97 | 30.75 | 29.41 | 23.05 | 43.30 | 44.36 | 29.97 | 47.43 | 51.48 | 39.16 |

| China | 6.82 | 6.85 | 6.66 | 15.55 | 15.78 | 14.23 | 27.95 | 26.48 | 21.53 | 39.65 | 40.02 | 28.45 | 51.47 | 55.24 | 37.54 |

| Indonesia | 6.71 | 6.82 | 6.57 | 15.31 | 15.66 | 13.41 | 26.23 | 25.80 | 20.24 | 35.51 | 36.63 | 27.79 | 41.83 | 45.70 | 36.64 |

| Saudi Arabia | 6.89 | 6.98 | 6.71 | 17.37 | 16.96 | 15.25 | 33.22 | 30.54 | 23.70 | 48.40 | 48.72 | 30.54 | 47.01 | 49.21 | 40.81 |

| Argentina | 6.91 | 7.02 | 6.82 | 17.75 | 17.81 | 15.70 | 34.02 | 32.23 | 24.51 | 47.70 | 46.60 | 32.15 | 49.75 | 52.64 | 41.60 |

| Thailand | 7.02 | 7.15 | 6.56 | 18.83 | 18.41 | 14.64 | 37.63 | 35.45 | 21.86 | 62.67 | 66.68 | 35.20 | 85.87 | 89.41 | 77.78 |

| Israel | 6.87 | 6.83 | 6.73 | 15.73 | 15.63 | 14.43 | 29.08 | 27.73 | 21.73 | 43.46 | 43.92 | 28.90 | 51.54 | 55.64 | 39.69 |

| Malaysia | 6.44 | 6.53 | 6.46 | 14.61 | 15.15 | 13.95 | 27.38 | 25.30 | 19.71 | 54.06 | 53.62 | 31.25 | 78.61 | 78.91 | 64.72 |

| Philippines | 6.84 | 6.84 | 6.71 | 16.25 | 16.58 | 15.25 | 31.92 | 30.11 | 23.70 | 45.95 | 45.07 | 30.54 | 50.95 | 56.62 | 40.81 |

| Forecasting Horizons | 1 Month | 3 Months | 6 Months | 12 Months | 24 Months | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Country | OLS | SVR | RW | OLS | SVR | RW | OLS | SVR | RW | OLS | SVR | RW | OLS | SVR | RW |

| Turkey | 2.97 | 2.90 | 2.82 | 6.67 | 6.30 | 5.92 | 11.05 | 10.56 | 8.97 | 19.04 | 18.61 | 13.73 | 40.65 | 32.29 | 18.72 |

| Mexico | 1.82 | 1.84 | 1.83 | 3.78 | 3.88 | 3.84 | 5.59 | 5.68 | 5.33 | 8.74 | 9.41 | 7.97 | 13.06 | 14.68 | 11.41 |

| Korea | 1.96 | 1.93 | 1.80 | 4.98 | 4.22 | 3.72 | 8.25 | 6.44 | 5.78 | 13.87 | 10.72 | 9.17 | 15.04 | 12.75 | 13.77 |

| Russia | 3.23 | 3.25 | 3.15 | 7.29 | 7.09 | 6.61 | 9.19 | 9.83 | 8.96 | 17.12 | 16.86 | 13.04 | 25.84 | 23.08 | 19.85 |

| India | 1.16 | 1.14 | 1.08 | 2.53 | 2.51 | 2.35 | 4.05 | 4.17 | 3.64 | 6.92 | 7.42 | 6.19 | 9.71 | 10.64 | 9.35 |

| Brazil | 2.99 | 3.11 | 2.69 | 6.87 | 6.54 | 5.66 | 12.26 | 11.09 | 9.22 | 19.61 | 17.86 | 14.33 | 32.38 | 31.82 | 19.57 |

| China | 0.38 | 0.36 | 0.34 | 0.94 | 0.93 | 0.88 | 1.76 | 1.74 | 1.56 | 3.65 | 4.08 | 2.78 | 10.61 | 11.72 | 5.07 |

| Indonesia | 3.68 | 3.39 | 3.21 | 7.60 | 6.73 | 6.13 | 14.53 | 9.63 | 8.53 | 30.34 | 14.93 | 12.70 | 61.78 | 22.22 | 18.19 |

| Saudi Arabia | 0.05 | 0.05 | 0.06 | 0.05 | 0.05 | 0.06 | 0.05 | 0.05 | 0.07 | 0.05 | 0.05 | 0.07 | 0.05 | 0.05 | 0.07 |

| Argentina | 1.85 | 1.68 | 1.82 | 5.12 | 4.28 | 4.63 | 9.76 | 7.25 | 7.85 | 17.16 | 16.32 | 14.26 | 22.20 | 24.52 | 27.12 |

| Thailand | 1.02 | 1.01 | 1.01 | 2.22 | 2.10 | 2.12 | 3.79 | 3.85 | 3.39 | 5.94 | 6.32 | 5.23 | 7.62 | 7.84 | 8.66 |

| Israel | 1.78 | 1.81 | 1.72 | 3.39 | 3.47 | 3.15 | 5.23 | 5.38 | 4.73 | 7.15 | 7.39 | 6.72 | 10.75 | 9.91 | 8.06 |

| Malaysia | 1.65 | 1.63 | 1.59 | 3.67 | 3.63 | 3.41 | 6.19 | 6.42 | 4.68 | 10.11 | 10.83 | 7.85 | 19.01 | 19.00 | 13.57 |

| Philippines | 1.18 | 1.15 | 1.12 | 2.68 | 2.78 | 2.42 | 4.57 | 4.69 | 5.94 | 7.53 | 7.89 | 5.87 | 11.40 | 12.09 | 8.21 |

| Forecasting Horizons | 1 Month | 3 Months | 6 Months | 12 Months | 24 Months | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Country | OLS | SVR | RW | OLS | SVR | RW | OLS | SVR | RW | OLS | SVR | RW | OLS | SVR | RW |

| Turkey | 7.84 | 7.70 | 7.63 | 13.33 | 12.85 | 12.10 | 22.26 | 21.80 | 17.35 | 35.86 | 35.07 | 24.18 | 66.99 | 47.70 | 27.88 |

| Mexico | 3.64 | 3.62 | 3.68 | 6.90 | 7.09 | 6.63 | 11.31 | 11.69 | 10.16 | 21.18 | 22.32 | 15.76 | 40.06 | 39.75 | 21.64 |

| Korea | 5.55 | 5.54 | 5.47 | 10.53 | 10.52 | 10.25 | 16.25 | 16.55 | 14.85 | 24.19 | 24.72 | 22.12 | 26.46 | 26.28 | 26.23 |

| Russia | 5.62 | 5.54 | 5.30 | 12.04 | 11.60 | 10.63 | 20.33 | 19.55 | 17.09 | 33.08 | 32.08 | 23.65 | 40.08 | 19.85 | 19.90 |

| India | 5.41 | 5.48 | 5.39 | 9.86 | 10.04 | 9.58 | 15.30 | 15.41 | 13.87 | 24.83 | 24.22 | 20.36 | 35.30 | 35.86 | 25.75 |

| Brazil | 5.20 | 5.21 | 5.09 | 10.00 | 10.05 | 9.63 | 15.57 | 16.03 | 14.40 | 22.03 | 23.28 | 19.68 | 32.90 | 31.02 | 21.09 |

| China | 5.83 | 6.00 | 5.80 | 11.95 | 12.02 | 11.44 | 19.25 | 18.44 | 17.76 | 24.57 | 23.50 | 25.73 | 41.07 | 33.80 | 30.19 |

| Indonesia | 5.54 | 5.56 | 5.52 | 11.15 | 11.24 | 10.83 | 17.05 | 17.22 | 16.22 | 27.46 | 29.24 | 23.62 | 33.54 | 34.33 | 28.08 |

| Saudi Arabia | 6.00 | 6.45 | 5.83 | 11.54 | 12.50 | 11.18 | 20.02 | 21.40 | 16.98 | 38.68 | 40.42 | 26.67 | 75.58 | 70.66 | 30.84 |

| Argentina | 7.63 | 7.49 | 7.39 | 13.86 | 13.86 | 13.81 | 21.97 | 22.00 | 21.68 | 37.13 | 36.42 | 34.51 | 46.62 | 50.09 | 42.79 |

| Thailand | 2.80 | 2.83 | 2.72 | 5.54 | 5.83 | 5.08 | 8.41 | 8.50 | 7.61 | 10.50 | 10.80 | 11.10 | 12.47 | 18.90 | 7.69 |

| Israel | 3.74 | 3.75 | 3.71 | 7.41 | 7.78 | 7.18 | 12.45 | 12.58 | 11.04 | 21.73 | 21.71 | 16.98 | 29.11 | 30.16 | 21.04 |

| Malaysia | 1.77 | 1.75 | 1.76 | 2.93 | 2.96 | 2.85 | 4.02 | 3.96 | 3.72 | 8.18 | 7.00 | 6.30 | 7.93 | 9.06 | 8.64 |

| Philippines | 4.22 | 4.13 | 4.13 | 8.57 | 8.46 | 8.02 | 14.76 | 14.60 | 13.02 | 23.26 | 22.83 | 19.49 | 27.43 | 31.67 | 25.17 |

| Forecasting Horizons | 1 Month | 3 Months | 6 Months | 12 Months | 24 Months | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Country | OLS | SVR | RW | OLS | SVR | RW | OLS | SVR | RW | OLS | SVR | RW | OLS | SVR | RW |

| Turkey | 3.83 | 3.90 | 7.63 | 6.11 | 6.16 | 12.10 | 8.70 | 8.71 | 17.35 | 15.33 | 15.65 | 24.18 | 31.74 | 32.55 | 27.88 |

| Mexico | 4.20 | 4.20 | 3.68 | 6.75 | 6.85 | 6.63 | 9.51 | 9.51 | 10.16 | 16.08 | 16.32 | 15.76 | 35.24 | 36.08 | 21.64 |

| Korea | 3.56 | 3.58 | 5.47 | 6.04 | 5.93 | 10.25 | 8.55 | 8.58 | 14.85 | 14.58 | 15.06 | 22.12 | 30.78 | 31.50 | 26.23 |

| Russia | 4.16 | 4.27 | 5.30 | 6.79 | 6.83 | 10.63 | 8.80 | 9.22 | 17.09 | 15.25 | 15.59 | 23.65 | 33.40 | 34.53 | 19.90 |

| India | 3.56 | 3.55 | 5.39 | 5.99 | 5.95 | 9.58 | 8.47 | 8.53 | 13.87 | 14.31 | 14.88 | 20.36 | 31.15 | 32.50 | 25.75 |

| Brazil | 4.06 | 4.08 | 5.09 | 6.68 | 6.70 | 9.63 | 9.31 | 9.42 | 14.40 | 15.75 | 16.21 | 19.68 | 32.67 | 33.65 | 21.09 |

| China | 3.86 | 3.89 | 5.80 | 6.49 | 6.51 | 11.44 | 8.94 | 9.03 | 17.76 | 15.28 | 15.90 | 25.73 | 31.44 | 32.98 | 30.19 |

| Indonesia | 3.60 | 3.61 | 5.52 | 5.95 | 5.83 | 10.83 | 8.51 | 8.42 | 16.22 | 14.46 | 14.89 | 23.62 | 31.41 | 32.76 | 28.08 |

| Saudi Arabia | 4.07 | 4.14 | 5.83 | 6.74 | 6.75 | 11.18 | 9.05 | 9.10 | 16.98 | 14.20 | 14.77 | 26.67 | 30.31 | 31.96 | 30.84 |

| Argentina | 4.01 | 4.05 | 7.39 | 6.61 | 6.65 | 13.81 | 8.72 | 8.82 | 21.68 | 14.51 | 14.97 | 34.51 | 30.51 | 31.61 | 42.79 |

| Thailand | 3.45 | 3.39 | 2.72 | 5.72 | 5.74 | 5.08 | 6.80 | 6.74 | 7.61 | 9.69 | 9.70 | 11.10 | 19.25 | 20.99 | 7.69 |

| Israel | 4.05 | 4.03 | 3.71 | 6.44 | 6.55 | 7.18 | 8.97 | 8.90 | 11.04 | 14.87 | 15.05 | 16.98 | 31.46 | 32.81 | 21.04 |

| Malaysia | 3.36 | 3.35 | 1.76 | 5.95 | 6.51 | 2.85 | 8.47 | 8.65 | 3.72 | 15.58 | 15.90 | 6.30 | 33.97 | 35.89 | 8.64 |

| Philippines | 4.11 | 4.15 | 4.13 | 6.78 | 6.78 | 8.02 | 9.20 | 9.07 | 13.02 | 14.74 | 15.53 | 19.49 | 30.86 | 32.11 | 25.17 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Plakandaras, V.; Gogas, P.; Papadimitriou, T. The Effects of Geopolitical Uncertainty in Forecasting Financial Markets: A Machine Learning Approach. Algorithms 2019, 12, 1. https://doi.org/10.3390/a12010001

Plakandaras V, Gogas P, Papadimitriou T. The Effects of Geopolitical Uncertainty in Forecasting Financial Markets: A Machine Learning Approach. Algorithms. 2019; 12(1):1. https://doi.org/10.3390/a12010001

Chicago/Turabian StylePlakandaras, Vasilios, Periklis Gogas, and Theophilos Papadimitriou. 2019. "The Effects of Geopolitical Uncertainty in Forecasting Financial Markets: A Machine Learning Approach" Algorithms 12, no. 1: 1. https://doi.org/10.3390/a12010001

APA StylePlakandaras, V., Gogas, P., & Papadimitriou, T. (2019). The Effects of Geopolitical Uncertainty in Forecasting Financial Markets: A Machine Learning Approach. Algorithms, 12(1), 1. https://doi.org/10.3390/a12010001