4.1. Australian Policy in an International Context

Australia currently has a renewable energy target of 20% by 2020 but no target beyond this date, a significant point of difference compared to global leaders such as Germany, which has a 2050 target of 80% renewable energy. As mentioned earlier, the significant changes to federal policy including the repeal of the Carbon Tax and reduction in the LRET resulted in an 80% decrease in large scale renewable energy investment in 2014 compared to 2005 [

70], whereas in Germany investment increased by 58% over the same period [

99]. Such uncertainty in Australia, coupled with a lack of a long-term target, means that there is less of an incentive to drive investment in renewable energy and consequently energy storage.

As such, there is also a disparity between Australia and the leading countries supporting energy storage, who view these technologies as being critical in facilitating a significant increase in intermittent renewable energy penetration. Again, this is reflected in increased levels of investment with Bloomberg Finance forecasting that 11.3 GW of energy storage will be deployed by 2020 which is a 900% increase compared to 2013 [

70]. Approximately 77% of this will be deployed in only four countries, U.S.A, Germany, Japan and Korea which are all countries strongly supporting energy storage through effective policy and regulation as outlined earlier. In contrast, Australia is predicted to remain a minor player with 104 MW of capacity installed by 2020 [

70].

However, should Australian policy makers decide to increase support for energy storage it would be advisable for them to study and learn from the leading states and countries supporting energy storage such as California and Germany. This is because that whilst Australia has its own unique energy market, there are aspects that are similar to these global leaders including areas of high concentrations of intermittent renewable energy (Texas and California) and high penetration of residential solar PV (Germany).

Furthermore, with SA and the ACT pursuing very high renewable energy targets [

90,

94] and continued growth in residential solar PV [

100], these aspects are only going to become more of an issue in the future in terms of electricity grid management. Therefore, it is imperative that steps are taken to address these through the implementation of technologies such as energy storage.

As has been demonstrated in this paper, there are a number of mechanisms available to policy makers to support energy storage, including, but not limited to, mandatory targets, financial subsidies or grants and energy market regulatory reform. The following section will briefly outline how each of these may play a role in Australia.

California’s energy storage target is particularly relevant to SA given that they have similar renewable energy targets. Subject to NEM rules, Australia could implement a similar policy mechanism although more emphasis would need to be placed on behind the meter storage due to the higher proportion of small-scale residential solar PV in SA compared to California. There is no doubt that significant amounts of energy storage will be required in SA given that is it estimated that by 2024 the installed capacity of small-scale solar PV will be in the range of 1.5 GW–2.3 GW, sufficient to meet 100% of the state’s electricity demand at certain times. This combined with a forecast wind capacity of 4.4 GW would mean that at times electricity supply will greatly exceed demand and without energy storage would result in significant curtailment as the interconnector with the neighbouring state, Victoria, does not have the capacity to transmit that amount of electricity [

21].

Based on this forecast and an estimated storage capacity 10%–20% of the intermittent renewable energy capacity [

6], a 2024 target in the range of 150 MW–230 MW for end user storage and approximately 450 MW–900 MW for wholesale/(T&D) storage would be required. This is not unachievable as shown by the progress made to date toward meeting California’s 1.3 GW energy storage target. Furthermore, such a possible future scenario could present a good case for hydrogen storage as will be discussed shortly. Currently, the only such target or goal that exists in Australia is in the ACT which aims to install 36 MW of small-scale battery storage by 2020 [

97]. This is a commendable first step and one in which the Federal Government should replicate and build upon.

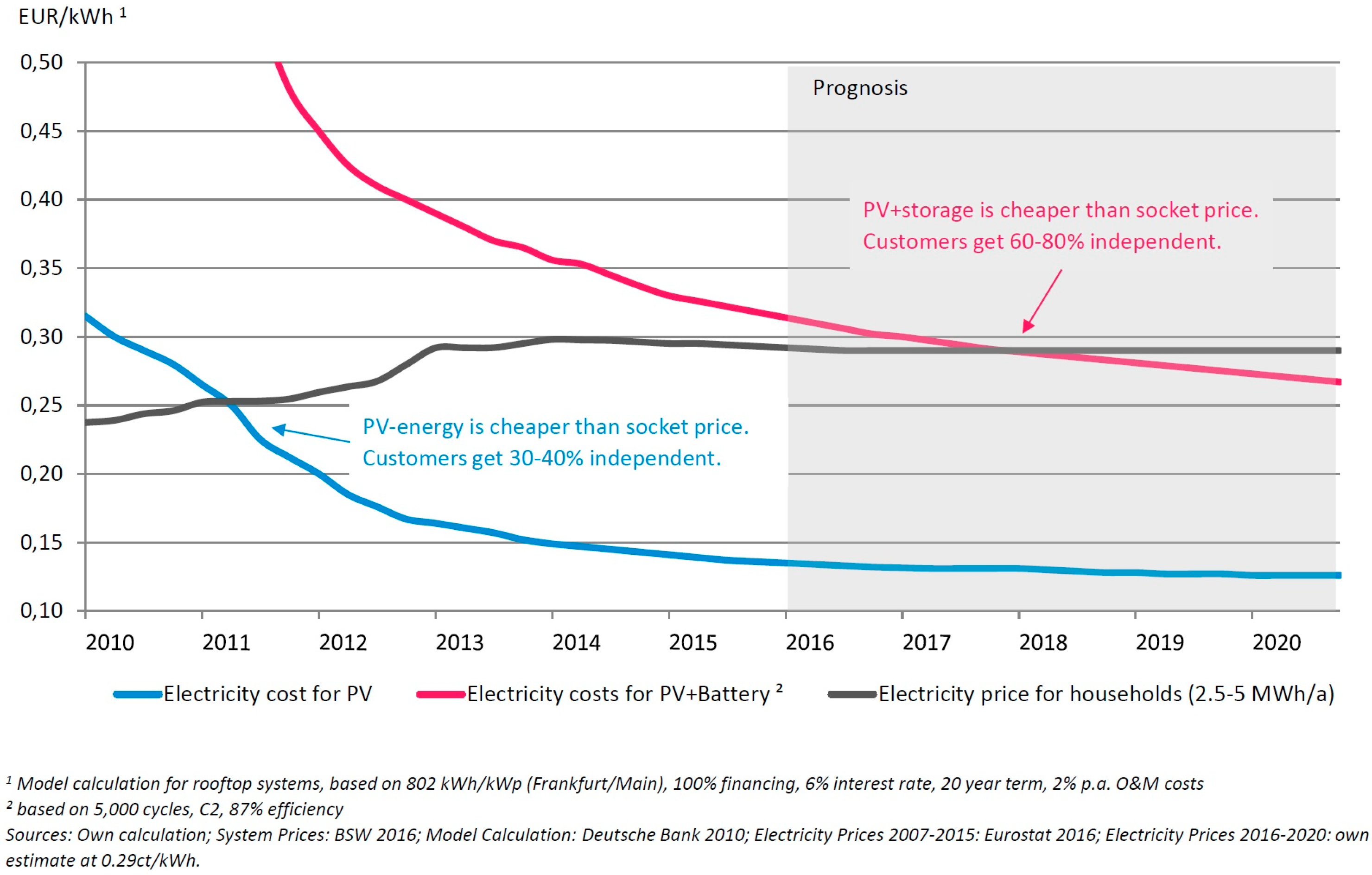

In Australia, it is likely that one of the earliest markets for battery storage systems will be the residential sector as has occurred with solar PV due to excellent solar resources and high electricity prices. Current financial analysis of payback periods for a typical residential battery storage system in Australia varies widely from 6 to 35 years [

70,

101,

102]. However, it should be noted that the lower range was calculated based on an assumed installed cost of AUD $4000–5000 for the 7 kWh Tesla Powerwall but the actual cost ended up being around AUD $12,000 [

103]. Based on this, the current payback periods for a residential battery storage system in Australia are greater that its lifespan of 10 years and are therefore uneconomical. Therefore, Australia should look to leaders such as California and Germany and offer a financial rebate until such time that battery storage costs decrease and become economically viable without subsidy. In California, the SGIP funding has resulted in the installation of 88 MW of battery storage.

Currently, the only rebate on offer in Australia is Adelaide’s Sustainable City Incentives Scheme which provides 50% of the system cost up to AUD $5,000 [

96]. Using the 7 kWh Tesla Powerwall as an example, this would reduce the cost by AUD $3,500 almost 30% but not quite enough to reduce the payback period below 10 years. It is interesting to note that the level of rebate is identical to that which would be offered in California (AUD $3,500) and Germany (AUD $3,600) for the same product when using the Australian price for the Tesla unit. However, the rebate in Germany brings the payback period to 5 years due to higher electricity prices and a lower installed cost [

54] and so to be more effective a higher initial rebate would need to be offered in Australia before being scaled back as battery costs decreased as per the German policy [

55].

One area where Australia is making progress to support energy storage is through regulatory reform with the AEMC currently reviewing a number of rule changes and guidelines [

83,

84,

85]. These are designed to recognise the benefits of energy storage for the electricity grid as a whole and for all stakeholders (consumers, transmission operators, DNSPs, etc.). Such reforms are crucial in ensuring that these micro grids, in which the energy storage systems are situated, remain connected to the grid and do not opt to become permanently islanded. The consequences of increasing numbers of defections from the grid is significant and includes the possibility of shutting down grid power generation and increasingly underused grid assets. As a result, the entire system could become unsustainable to maintain financially by the remaining connected consumers [

104].

4.2. Hydrogen as an Alternative Energy Storage Solution

As mentioned earlier in this paper, hydrogen storage can play an integral role alongside various other storage technologies in a future where renewable energy provides up to 100% of the world’s electricity needs. This may be difficult to envisage at present since this technology is still in the development phase and is less advanced and more expensive than other storage technologies such as PHS. However, as this section will show, recent pioneering studies and technological advancements have meant that hydrogen storage is beginning to be perceived as a viable solution to integrate the significant amounts of intermittent renewable energy required for a sustainable energy future. Whilst much of this research is focused on the use of hydrogen for the transport sector, it is worth discussing briefly as the required infrastructure is very similar to that which would be required for stationary energy use.

Jacobson and Delucchi conducted a comprehensive study in 2011, which demonstrated that renewable energy (wind, water and solar), from a technology and economic perspective, is capable of providing the global primary energy requirements in 2030. In this future, a significant percentage of the transportation sector would use hydrogen, created from renewable energy, as a fuel [

105].

The Intergovernmental Panel on Climate Change (IPCC) published a report in 2012 entitled Renewable Energy Sources and Climate Change Mitigation which analysed the role of renewable energy in providing the majority of global primary energy supply in order to limit carbon dioxide emissions. Within this report, the IPCC identified that hydrogen, created from renewable energy, could play a significant role as a fuel in the transport sector of the future alongside battery electric vehicles [

106].

More recently, Balta-Ozkan and Baldwin modelled a hydrogen network within the UK MARKAL Energy System model to investigate whether this technology could contribute towards the UK’s CO

2 emissions reduction target of 80% by 2050. They demonstrated that hydrogen appears to be a competitive fuel for the transportation sector and could lead to a 74% reduction in emissions by 2050 [

107].

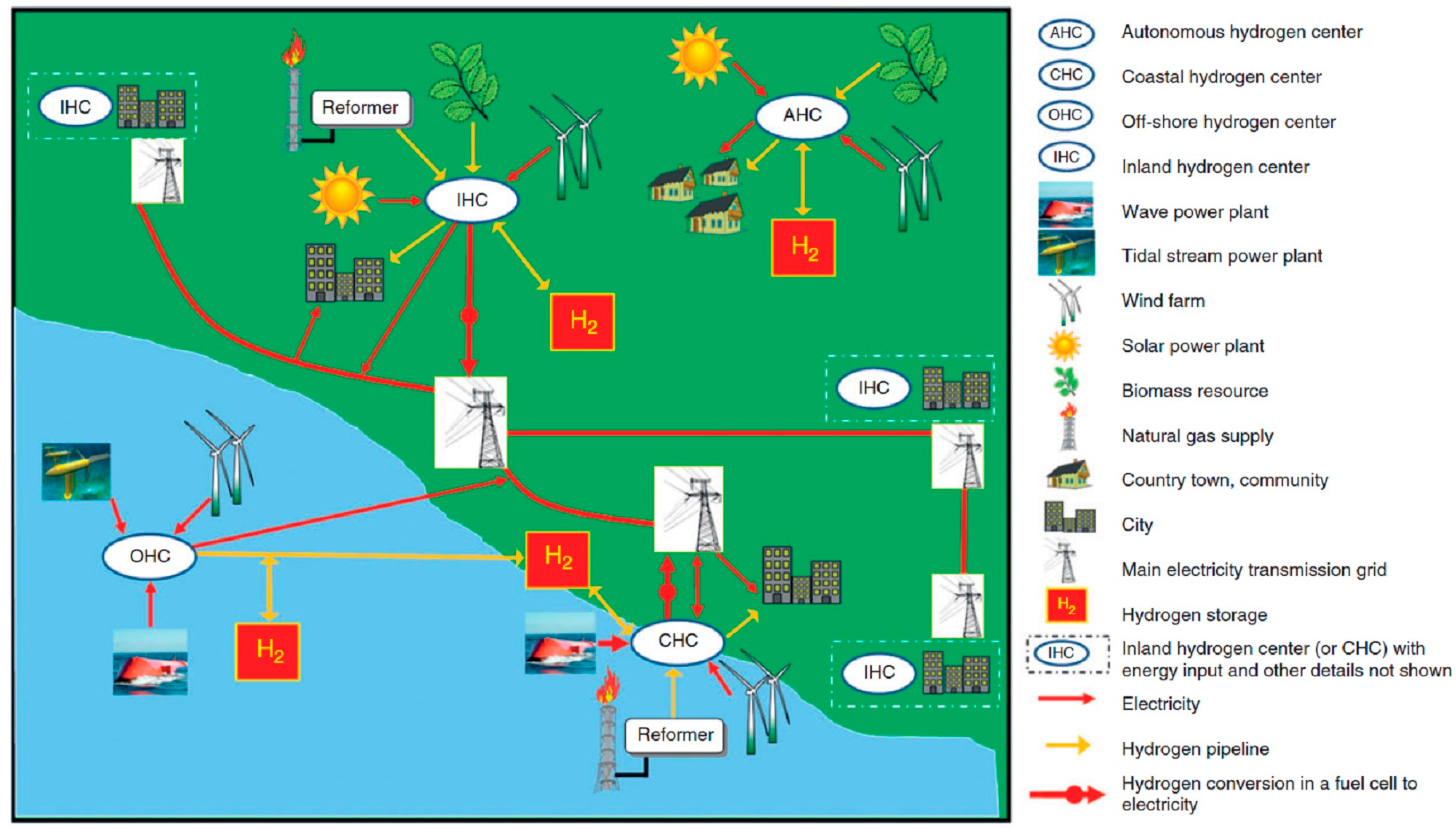

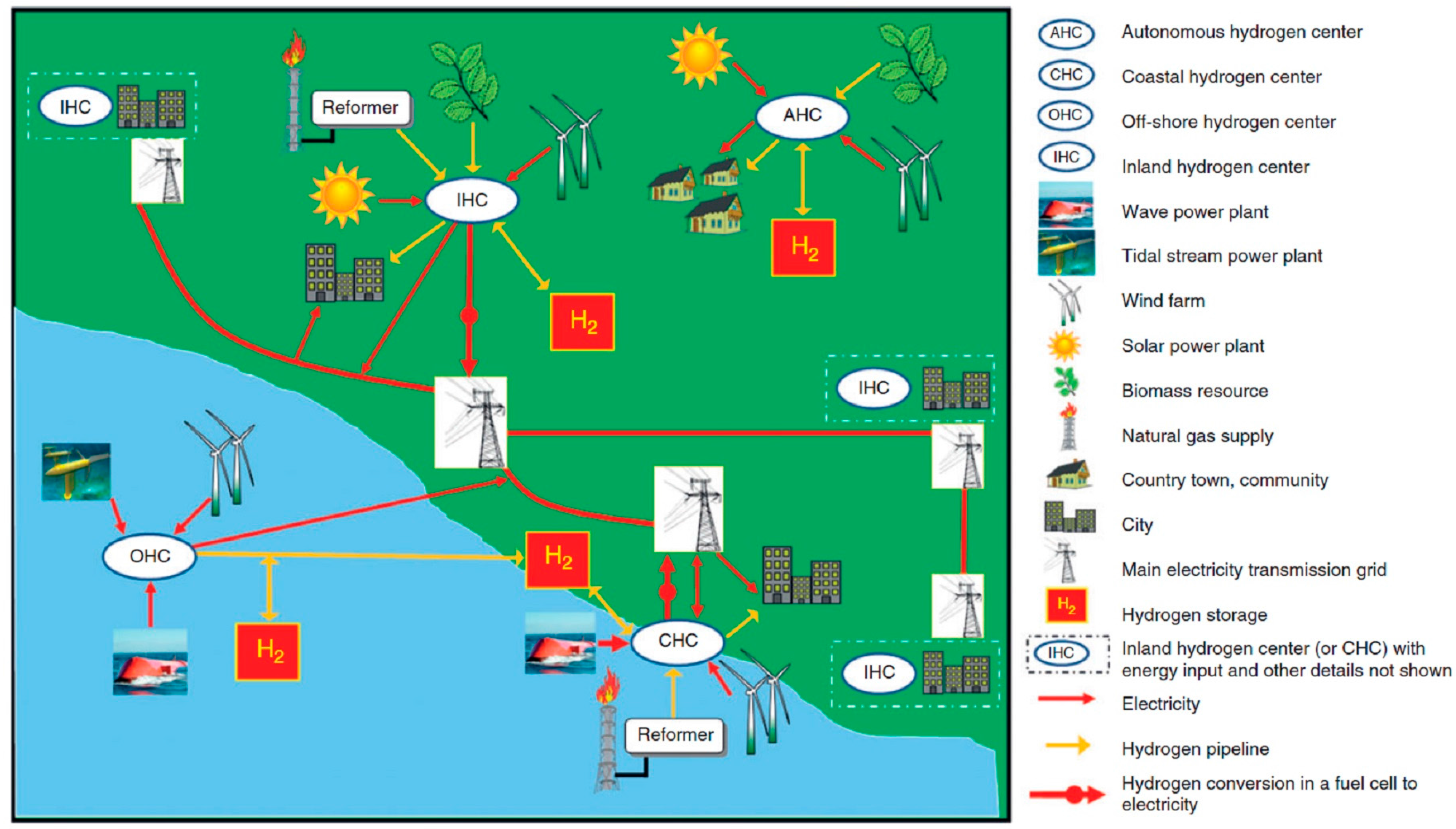

Research into addressing the knowledge gap around the role of hydrogen for stationary energy has been recently conducted by Andrews and Shabani who have proposed a strategy for a re-envisioned hydrogen economy. This Hydrogen in a Sustainable Energy (HISE) strategy outlines the crucial role hydrogen can play in the transportation sector and also in longer-term seasonal storage for electricity grids. Additionally, this bulk hydrogen storage would replace fossil fuels as a strategic energy reserve to ensure national and global energy security [

16]. Crucial to the strategy is that the hydrogen would be produced exclusively by a variety of renewable energy sources, making it a truly sustainable energy carrier. Due to the wide distribution of these renewable energy sources, a hierarchy of production, storage and distribution centres would be established in order to produce the hydrogen as close as possible to where it will be consumed as shown in

Figure 10. The benefit of this is that it would minimise the necessity of an expensive long-distance hydrogen pipeline network. Importantly, the strategy recognises that hydrogen energy is not the best solution for all applications and as such it will work alongside other energy storage technologies such as batteries, in a symbiotic role to meet the needs of a sustainable energy future [

16].

However, in order for hydrogen to fulfil this crucial role, there are a number of barriers that must be overcome including technology-lock in or entrenchment, political and economic resistance, lack of a strong industry body and community support, poor understanding about the role of hydrogen and limited funding for research and development [

1]. Efforts to address these barriers are currently being undertaken and a few countries have emerged as the global leaders in advancing hydrogen technology.

In terms of large-scale hydrogen storage, Germany is at the forefront of research and development as it is looking to this technology for a number of key reasons. This includes as an alternative to pumped hydro, which is limited in terms of future growth in the country due to a lack of suitable sites and to support the decarbonisation of its industrial sector.

The latter is critical for Germany to achieve its 2050 target of an 80% reduction in CO

2 emissions [

10] whilst maintaining the capability of its industrial sector. This is particularly the case for the state of North Rhine-Westphalia (NRW), which is home to one of the most important industrial regions in Europe. Lechtenböhmer et al., in consultation with industry stakeholders, developed three long-term technology scenarios to determine the ability to meet this target. One of these, the low carbon technology scenario, has the potential to achieve a 50% reduction in CO

2 emissions by 2050. The backbone of this scenario is the establishment of a hydrogen infrastructure with electrolysers and storage located close to areas of consumption and excess renewable energy supplied via high voltage direct current (DC) lines, already under construction, from northern Germany. Hydrogen would also be used directly in the steel industry and for various processes in the chemical industry. Although considered an ambitious scenario by industrial firm stakeholders, it is nonetheless an important study into the role that hydrogen can play in a low carbon economy [

108].

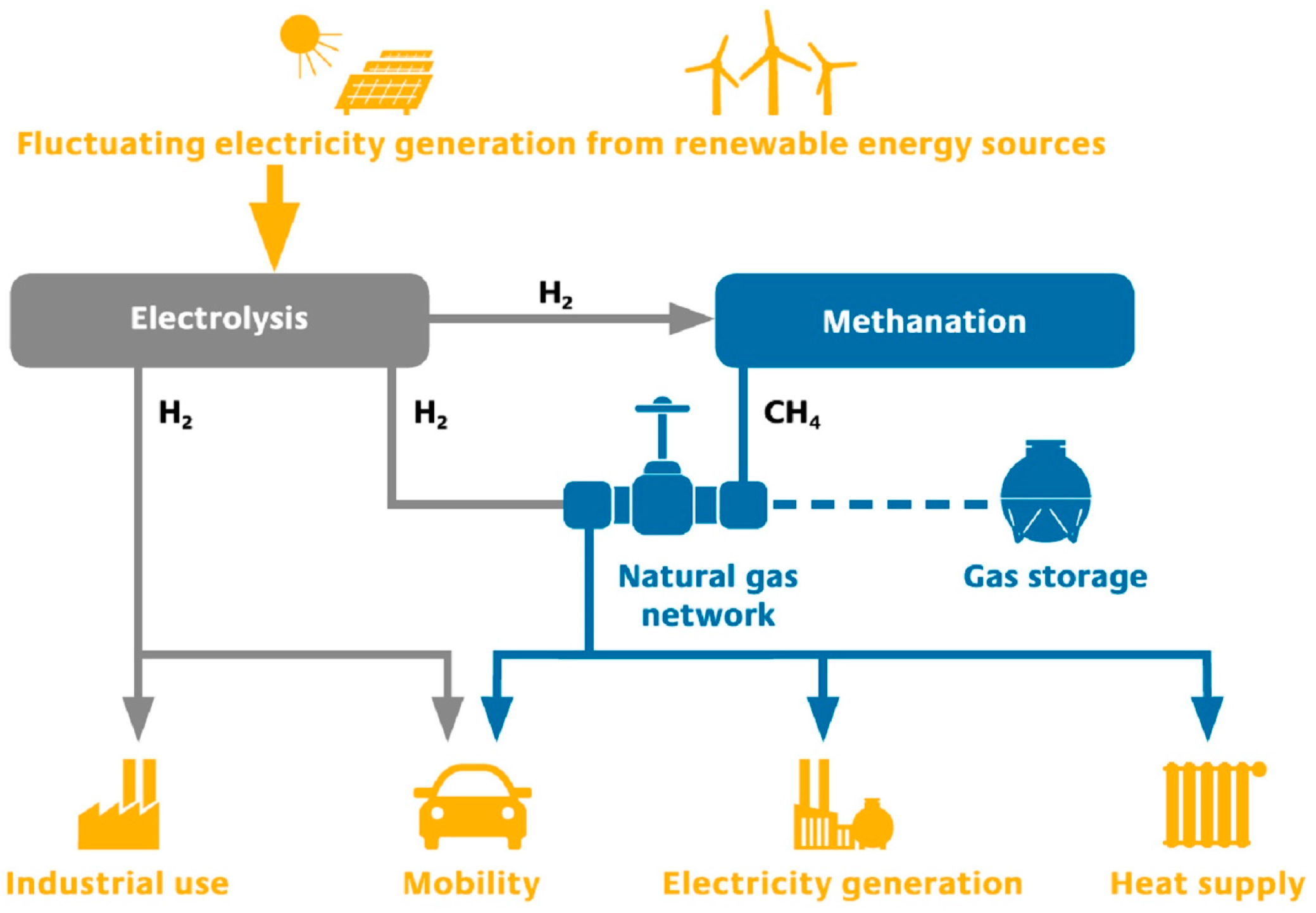

Germany is focusing on Power-to-Gas (P2G) technology, which has a variety of applications including electricity and heat generation and transport as shown in

Figure 11 [

109]. The process firstly involves using excess renewable electricity to electrolyse water into oxygen and hydrogen [

5]. The hydrogen is then either stored directly before being converted back into electricity via a fuel cell or alternatively converted into methane (methanisation) and stored in the existing natural gas infrastructure for later use in a variety of applications including electricity, heat generation and transportation [

109]. The supporting argument about the advantage of P2G technology is that the gas transmission grids have a huge storage capacity, approximately 200 TWh in Germany [

15]; this is while the parasitic losses of using the natural gas pipelines in large scales as well as the conversion to methane and back to hydrogen must be taken into consideration. Overall, the electricity-gas-electricity process has a round trip efficiency of approximately 40% and so increasing this is one of the main research and development objectives [

109].

Despite the yet-to-be-addressed low round-trip energy of this approach, P2G is being supported through the Germany Energy Agency (Deutsche Energie-Agentur GmbH-DENA), which established the Power to Gas Strategy Platform in 2012 in partnership with industry and research stakeholders. Key to this is the Roadmap Power to Gas which sets out the pathway to achieve large-scale, economically viable use of this technology, including a very ambitious goal of 1 GW of installed capacity by 2022 [

109]. Project funding is being provided through the €200 million Energy Storage Funding initiative which aims to support research projects to develop a broad range of storage technologies for electricity, heat and other forms of energy [

32]. Additionally, the German Federal Energy Industry Act contains a provision for hydrogen and hydrogen-based gas facilities to be exempted from network access charges [

110].

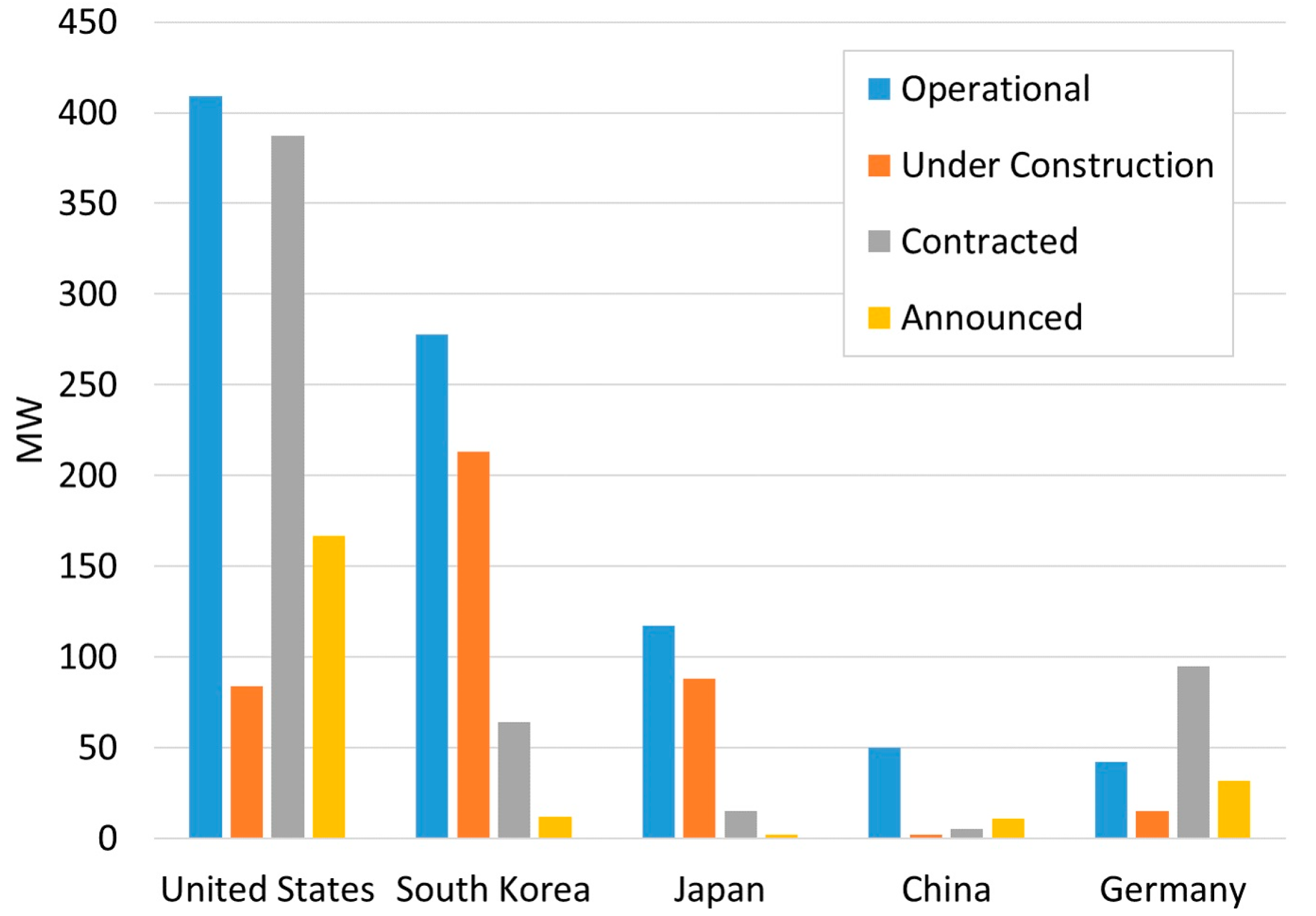

Currently in Germany there are 14 operational P2G demonstration projects with an installed capacity of just over 10 MW (key projects listed in

Table 8) and more than 17 facilities under construction [

109]. This represents over 95% of the global installed capacity of P2G.

Some other European countries are also looking to P2G technology and this is being facilitated through the European Power to Gas Platform, which is a joint body, based on an integrated network of industry and government stakeholders [

111]. At present, a number of demonstration projects have been completed throughout Europe with key examples listed in

Table 9.

As shown in

Table 9, there are some P2G projects being installed to fuel vehicles with hydrogen fuel cells and this is another technology that will play an important role in the future alongside hydrogen storage. For stationary energy applications, the current global leaders are Japan for micro fuel cells (less than 5 kW) and Korea, USA and Germany for larger units (greater than 100 kW).

In Japan, over 100,000 micro fuel cells have been installed since 2009, which is impressive but well short of the government target of 5.3 million units by 2030. This target is being supported through the Ene-Farm program, which was launched in 2009 and provides a subsidy on each unit sold. This was initially set at ¥1.7 million (~USD $15,000) but has been progressively reduced over time as unit prices decreased and is currently ¥350,000 (~USD $3,000) compared to a cost of about USD $167,000 [

112].

The emerging market for large fuel cell units has similarly been supported through government subsidies. For example, in the U.S., there is a federal tax credit of up to 30% or $3000/kW (whichever is less) with an additional 10% for Combined Heat and Power (CHP) applications. In California, the SGIP provides $4,500/kW for fuel cells fuelled by biogas, nearly double the rebate for those using natural gas as a fuel source [

113].

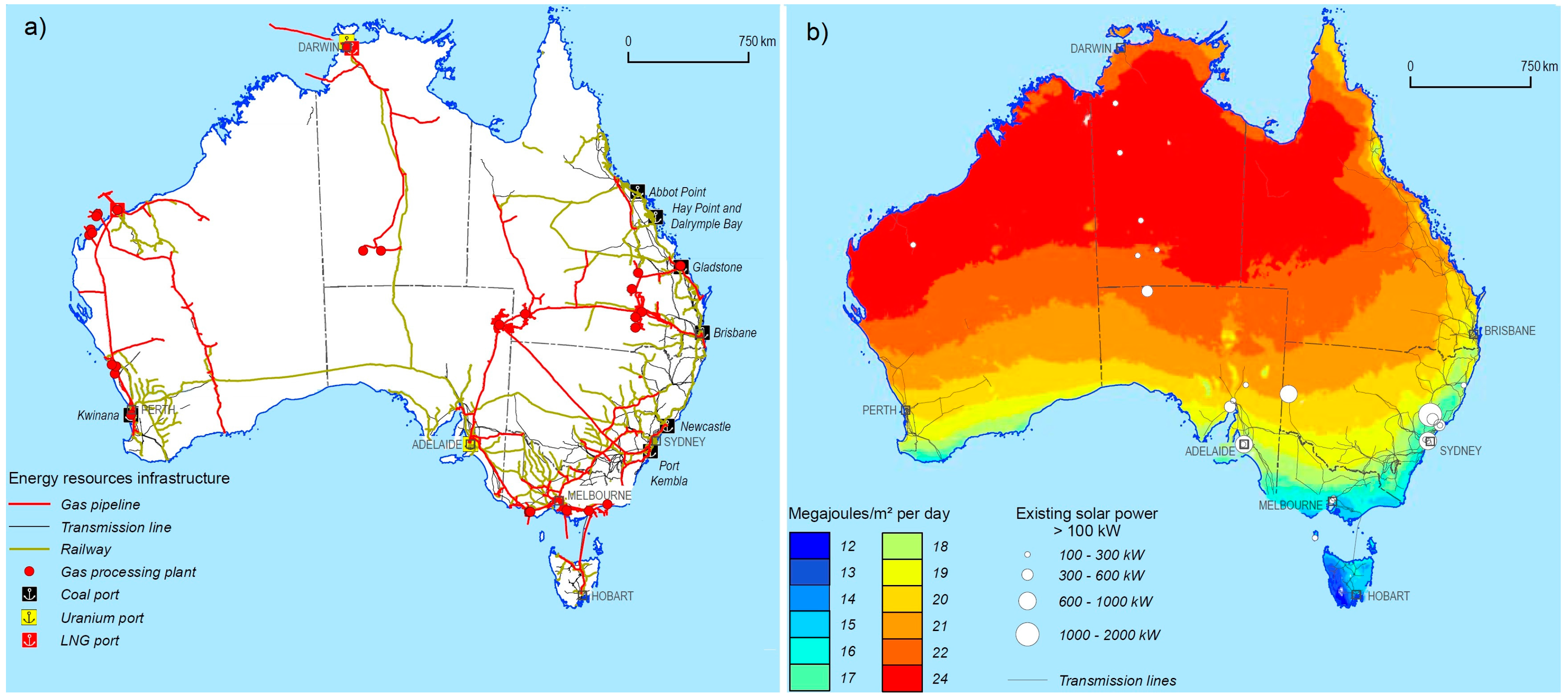

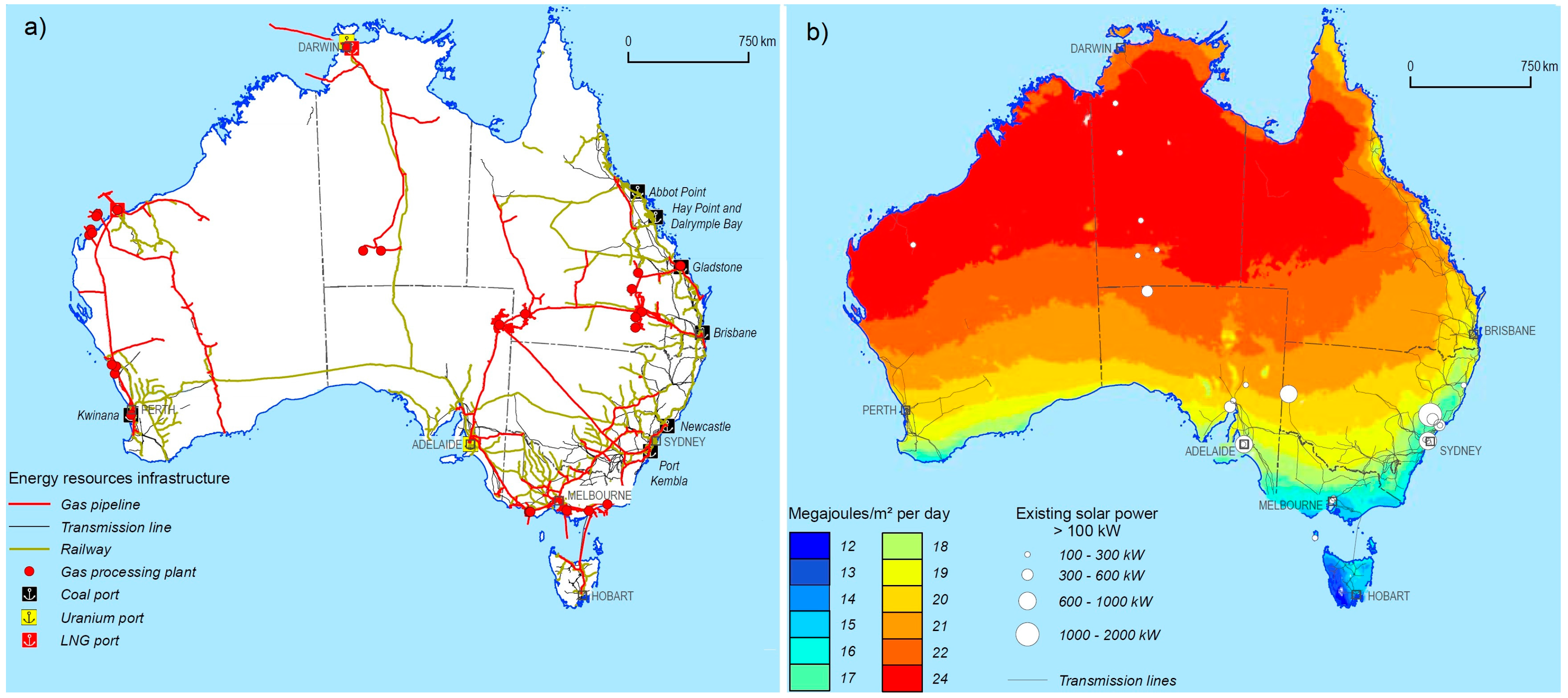

Ideally, the long-term goal is to move away from using natural gas as a fuel source for hydrogen fuel cells and use hydrogen P2G technology. Australia has an extensive natural gas pipeline distribution network (

Figure 12) and, importantly, this covers the majority of the populated areas of the country where the hydrogen would be consumed. Therefore, potentially an interim step on the road to a sustainable hydrogen future is, at a local level, to use the gas pipeline infrastructure to store and distribute the natural gas created from hydrogen close to where it will be consumed. This would be in place until such a time that a localised hydrogen pipeline infrastructure is constructed which would eliminate the necessity to convert the hydrogen into natural gas, which has inefficiencies.

An alternative approach is to use the national gas grid to distribute the natural gas created from hydrogen over long distances instead of using the electricity grid. However, the merits of hydrogen distribution at a national level was studied by Andrews and Shabani who concluded that limiting hydrogen distribution to local pipelines was the preferred option [

16]. To ascertain the advantages and disadvantages of each solution specifically for Australia, it is recommended that a detailed quantitative study be conducted.

Hydrogen storage would also be well suited to regions of the country where the intermittent renewable energy capacity is forecast to greatly exceed electricity demand such as in SA as discussed earlier [

21]. The excess energy can be stored locally in the form of hydrogen and used when required, thus flattening out the variation in renewable energy supply, particularly at the seasonal level.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}