A Critical Study of Stationary Energy Storage Policies in Australia in an International Context: The Role of Hydrogen and Battery Technologies

Abstract

:1. Introduction

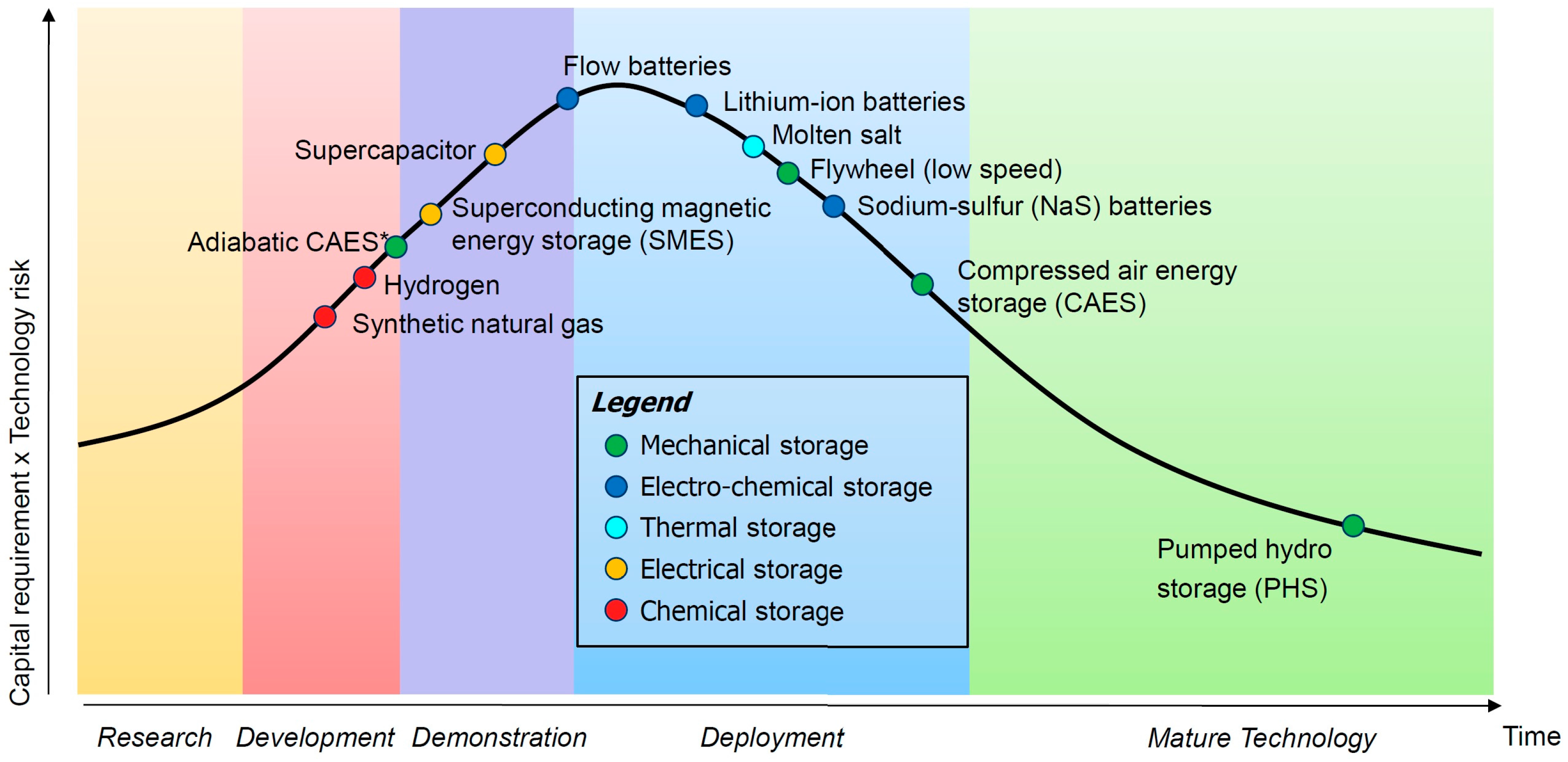

2. Energy Storage: A Global Overview

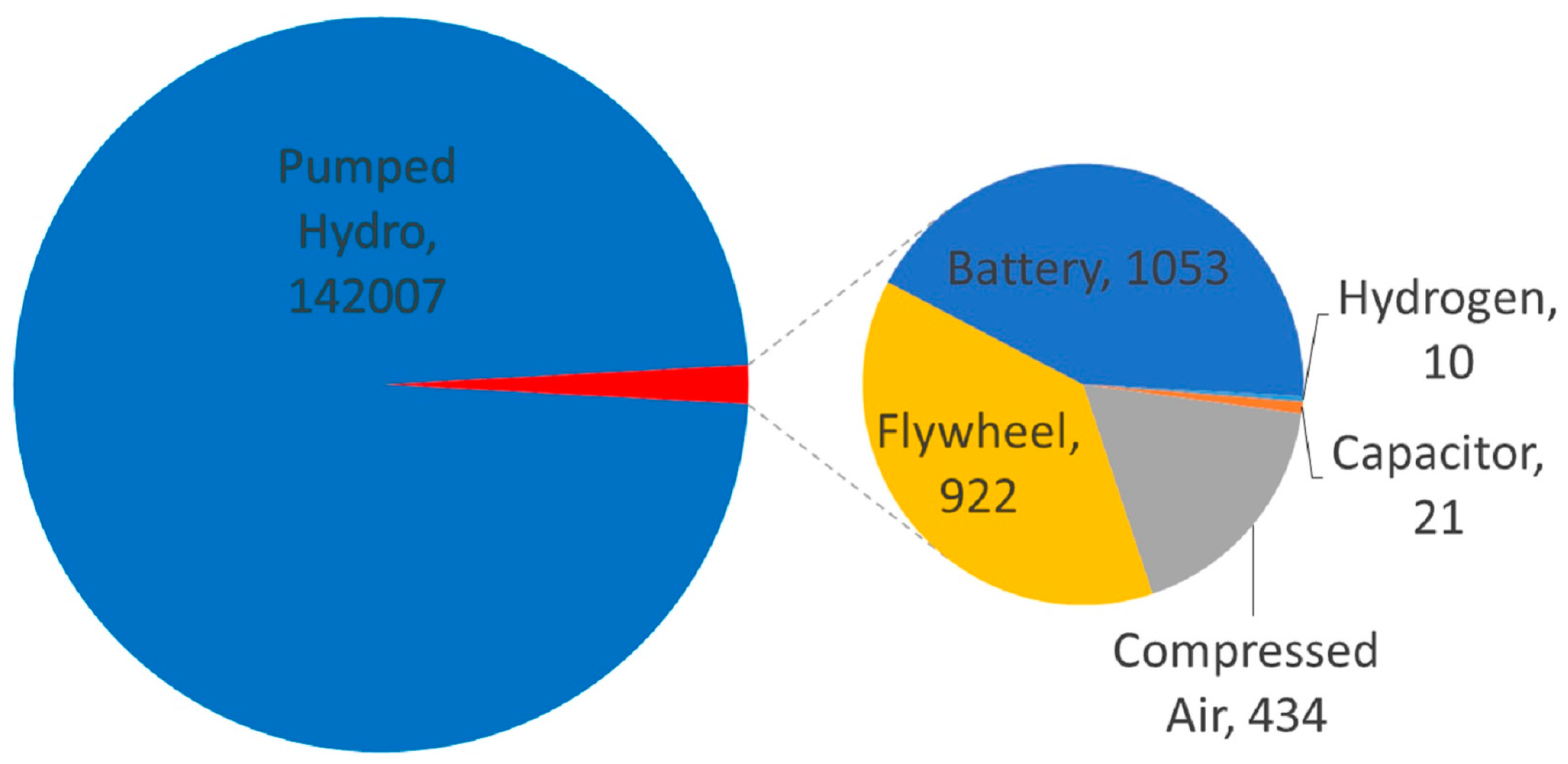

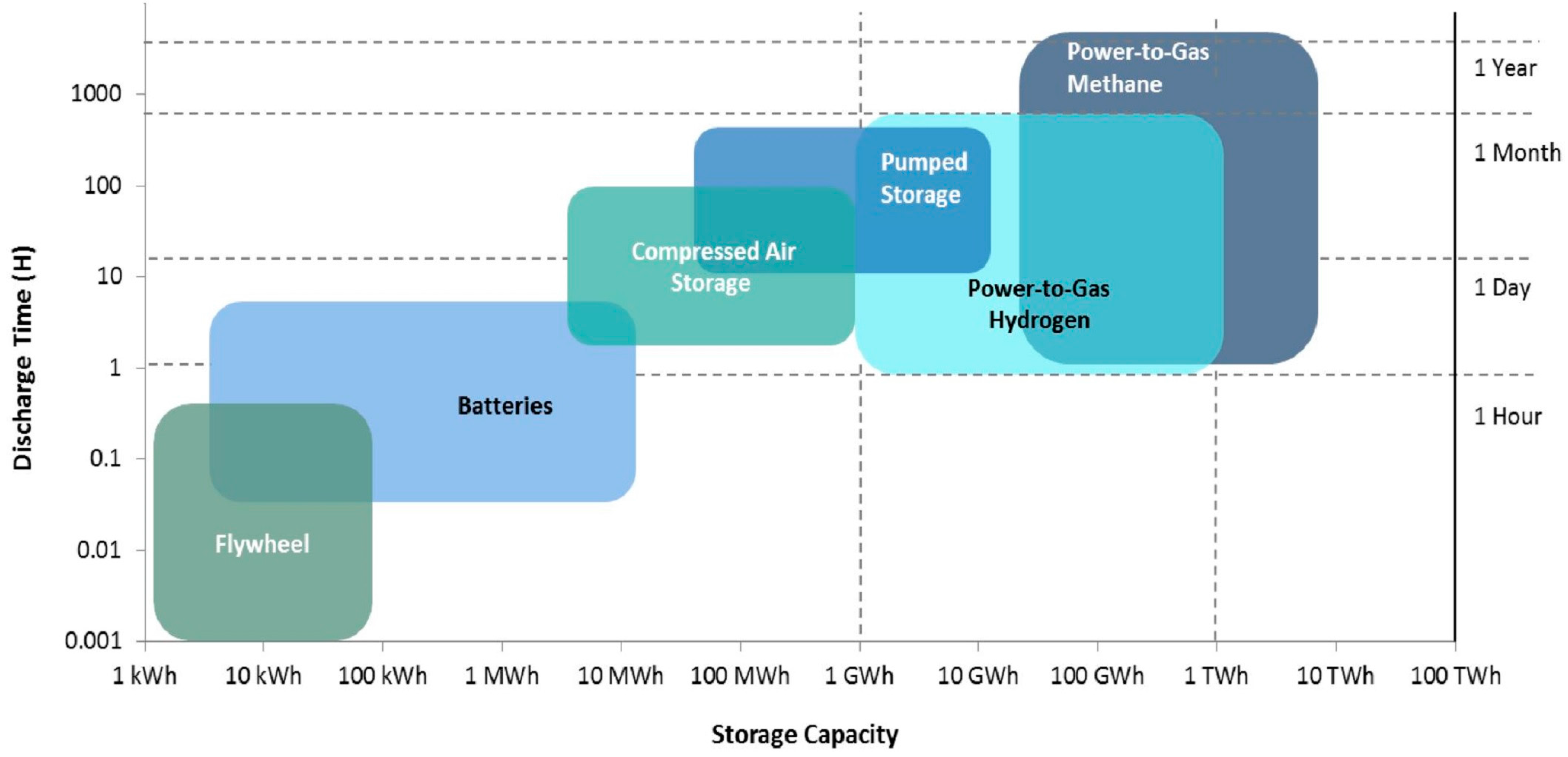

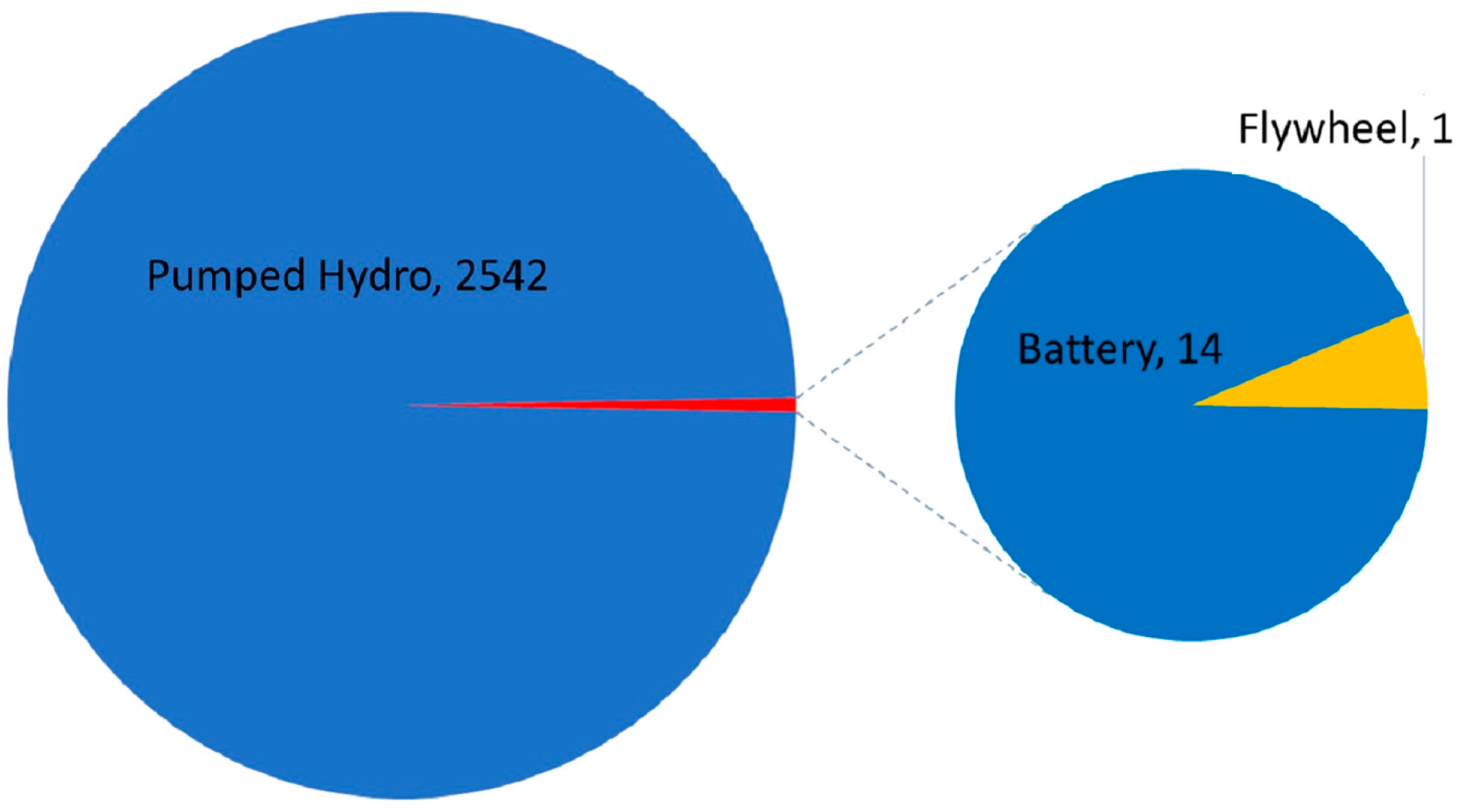

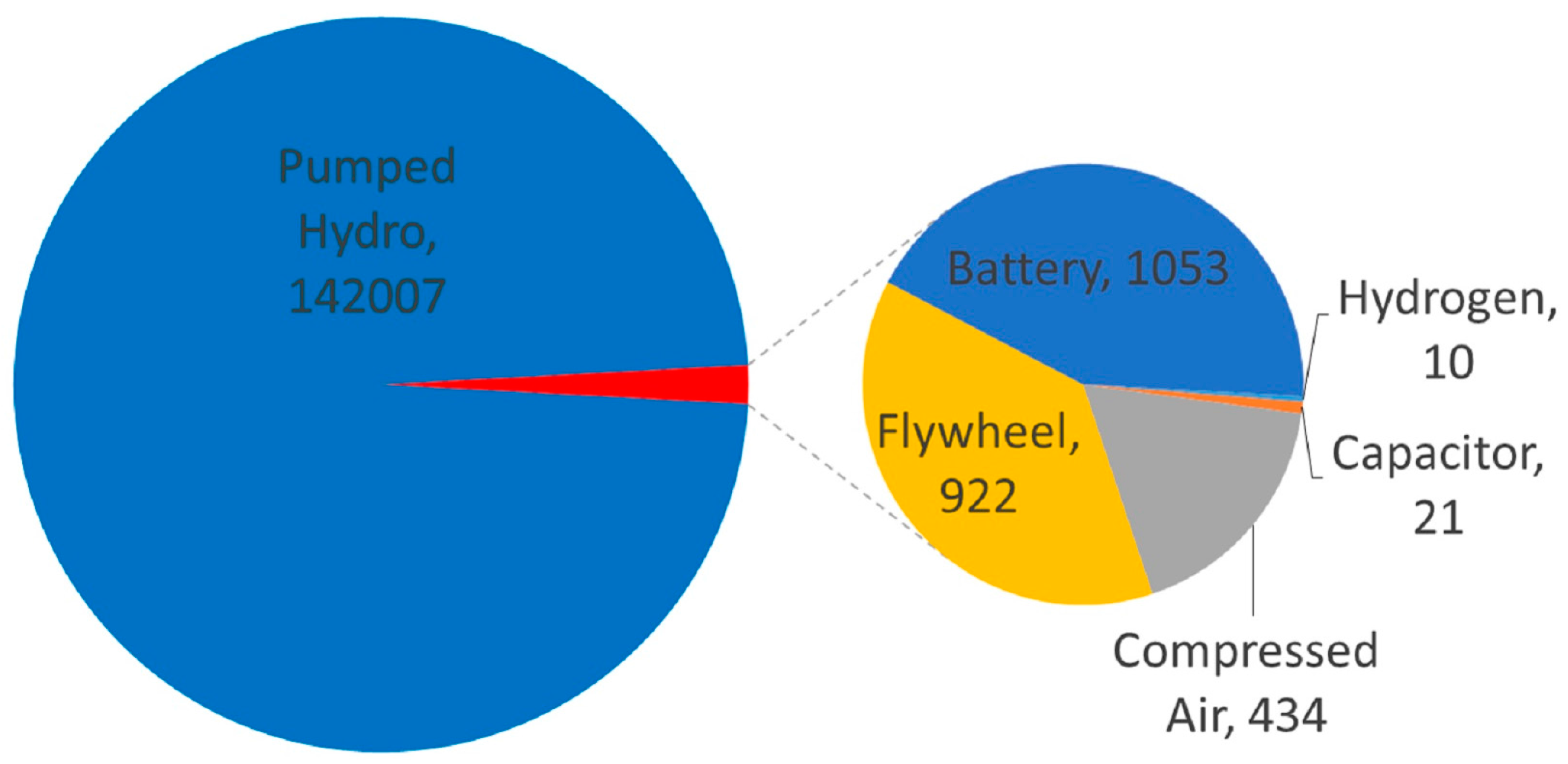

2.1. Technologies and Current Global Capacity

2.2. Energy Market Segments

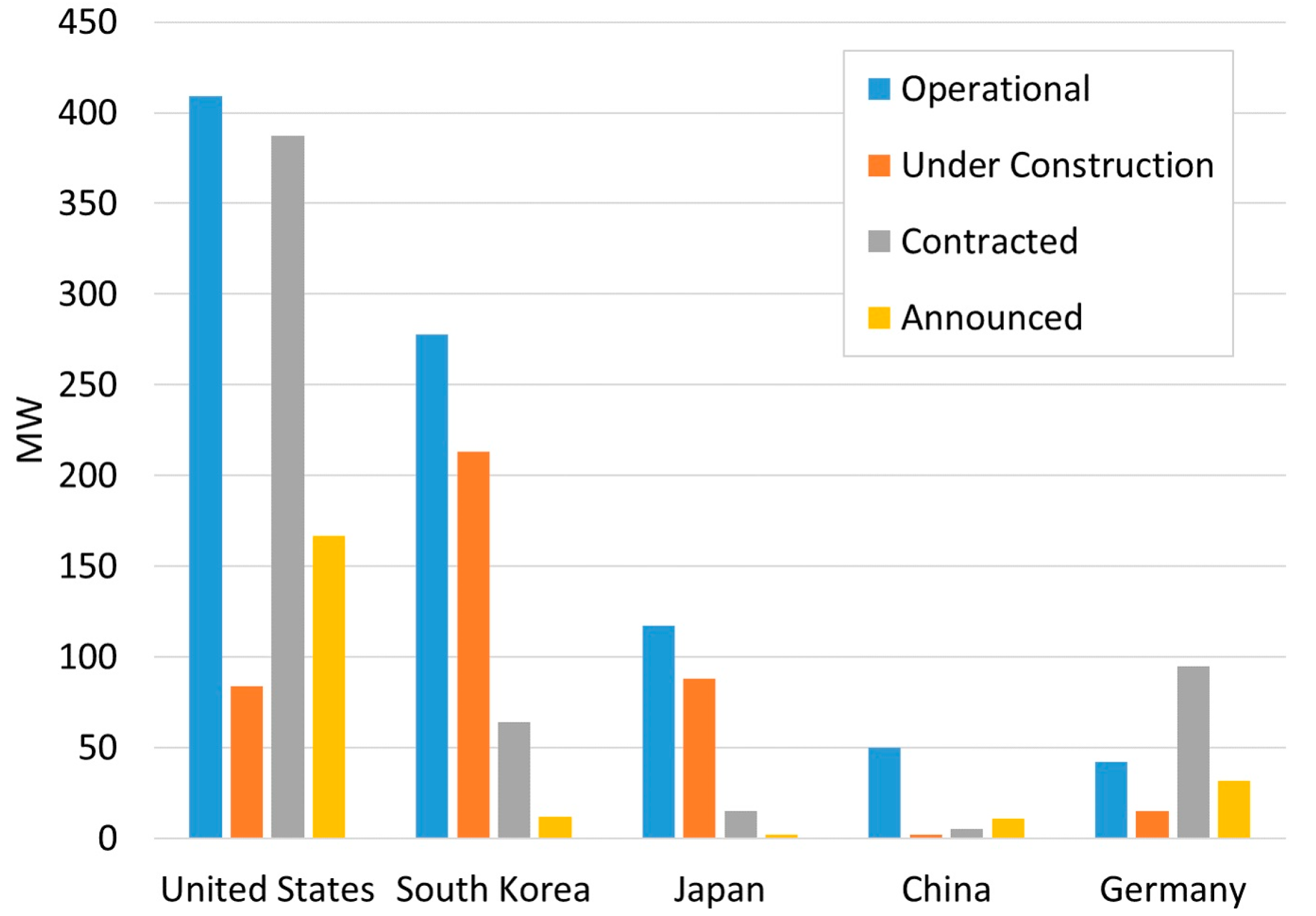

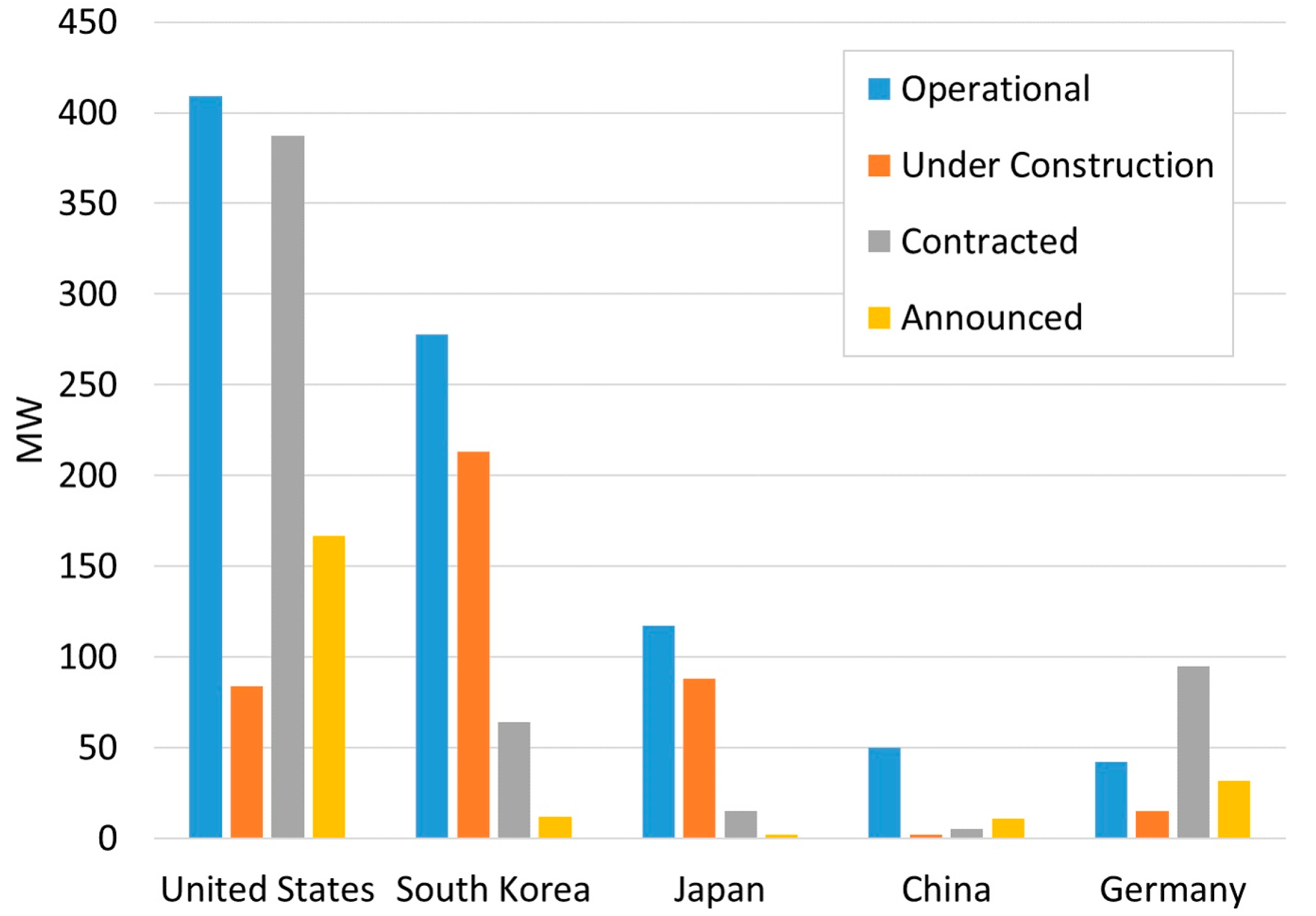

2.2.1. International Policies and Plans

2.2.2. Wholesale Market

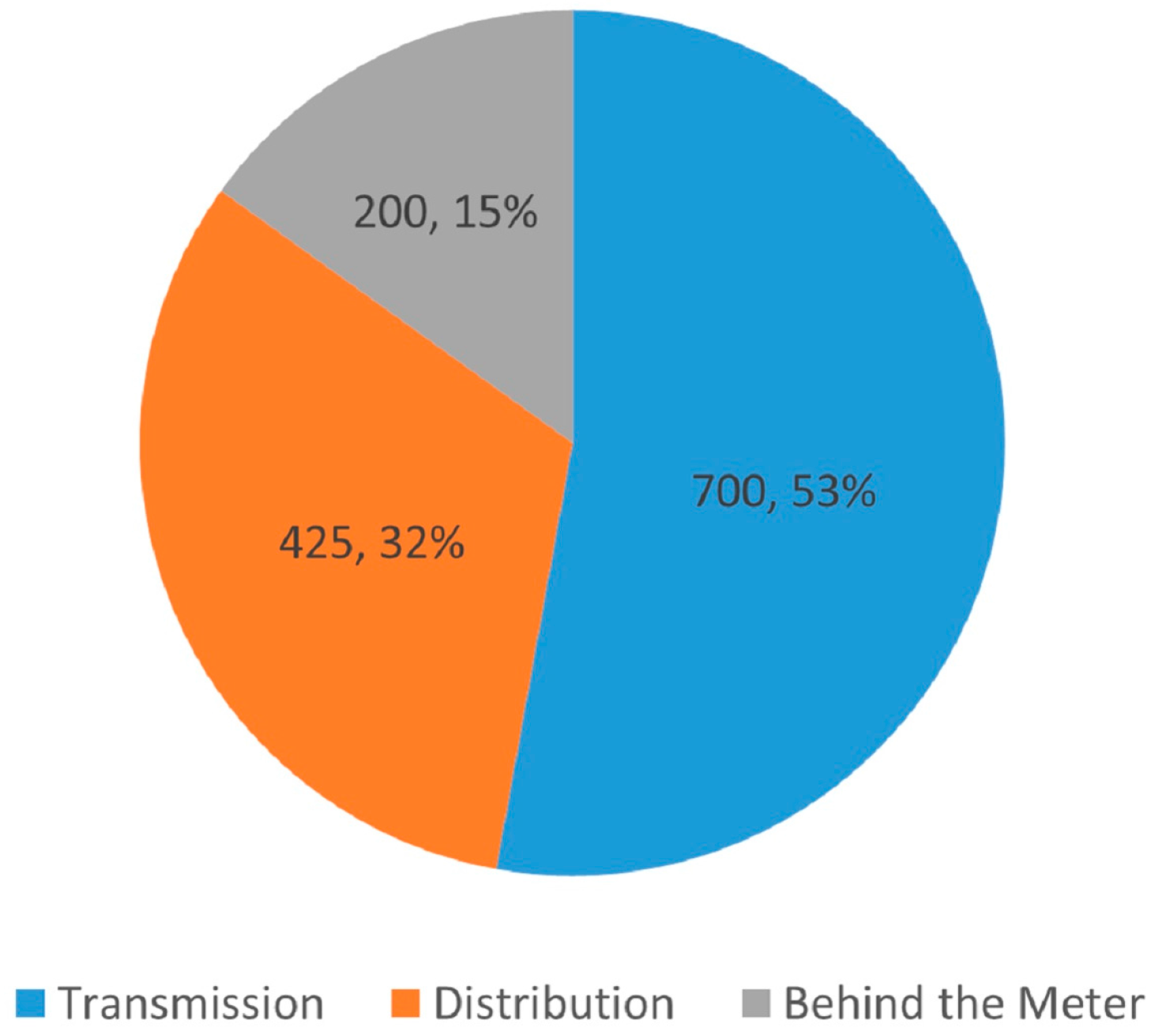

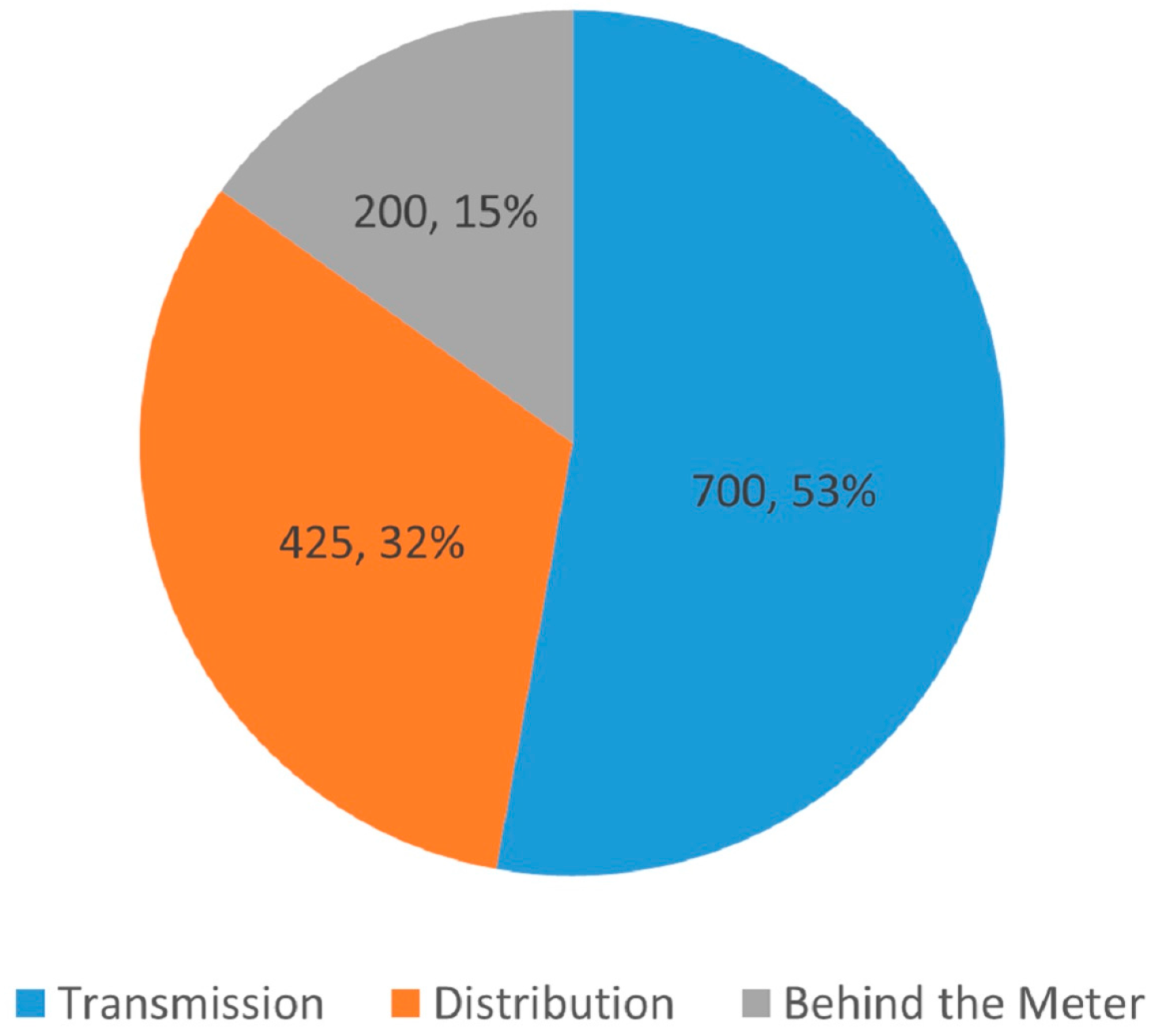

2.2.3. Transmission and Distribution Market

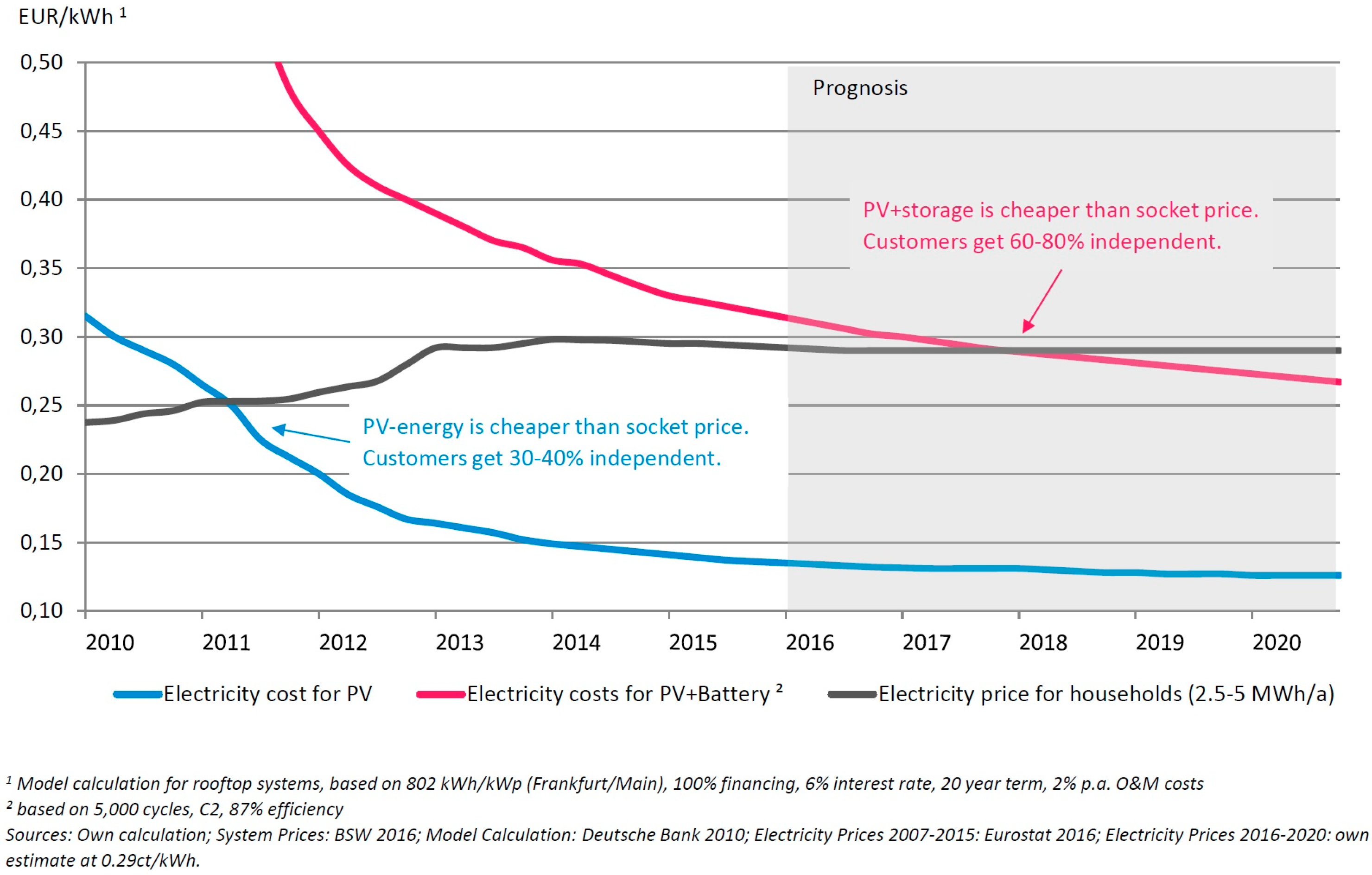

2.2.4. End User Market (Behind the Meter)

2.2.5. Off Grid Market

3. Australian Policies and Plans

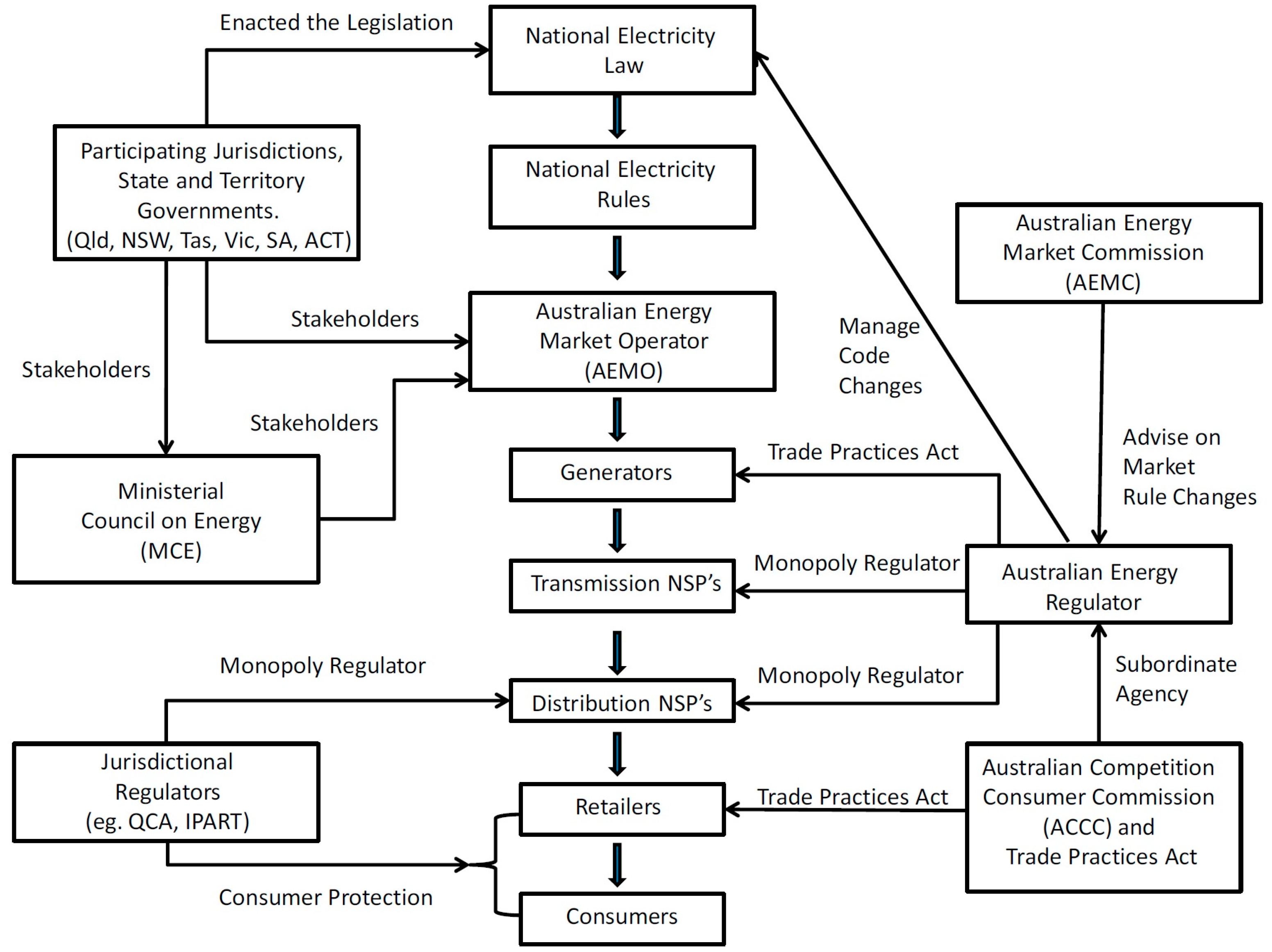

3.1. Government System

3.2. Federal Government Energy Storage Policies and Plans

- A 2 MW/2 MWh battery installed in 2016 in Buninyong, Victoria which is the largest grid connected battery in Australia. It is equivalent to 20% of the current powerlines’ capacity and will run automatically to reduce peak demand and provide emergency backup (Powercor, 2016).

- Ergon Energy’s Grid Utility Storage Solution, which is being deployed in constrained fringe-of-grid regions in Queensland to improve power quality and regulate demand. The network expects to deploy hundreds of these 25 kW/100 kWh units in the coming years and estimates it will reduce network infrastructure investment by over 35% [87].

3.3. State and Territory Government Energy Storage Policies and Plans

4. Discussion

4.1. Australian Policy in an International Context

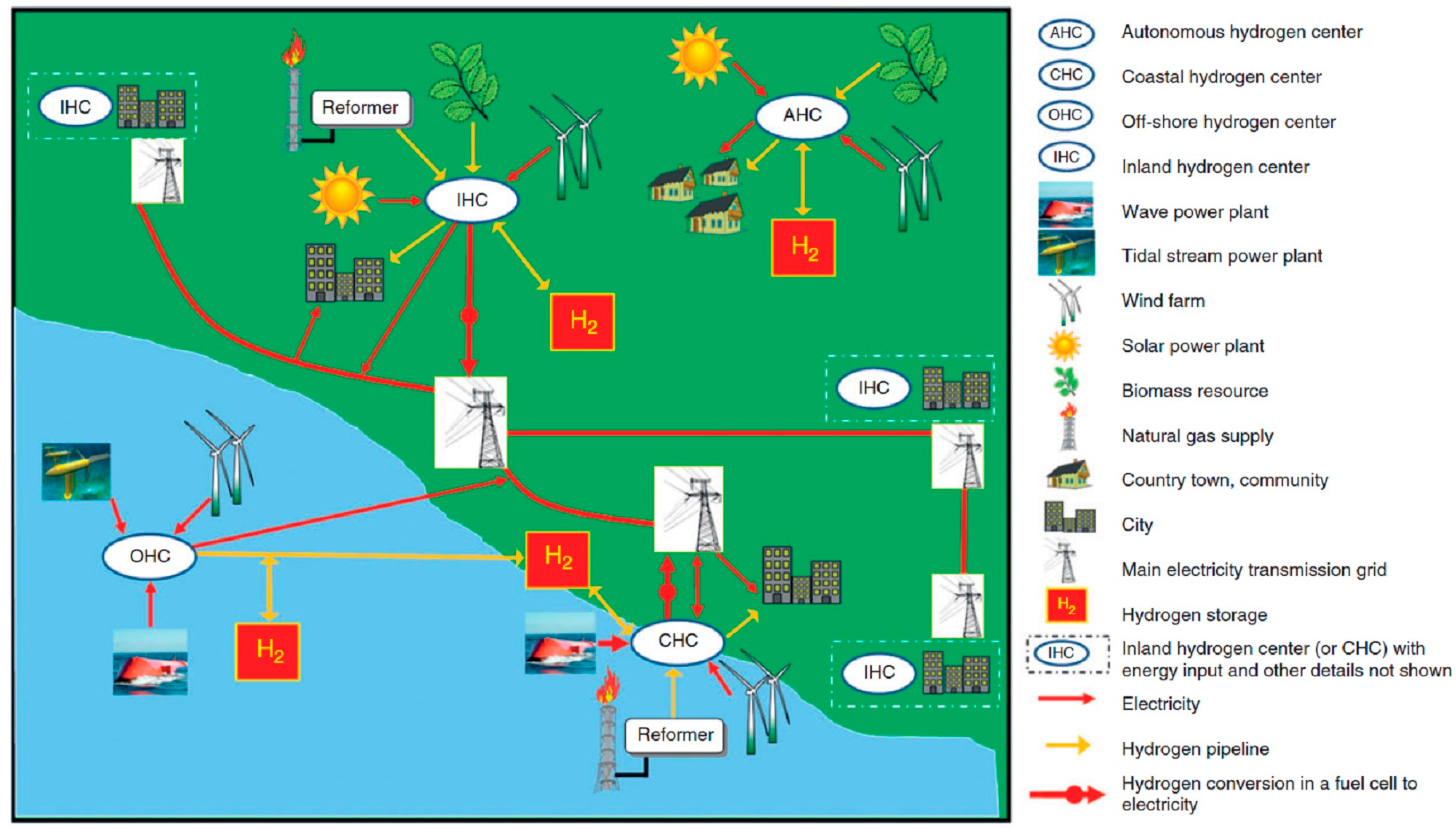

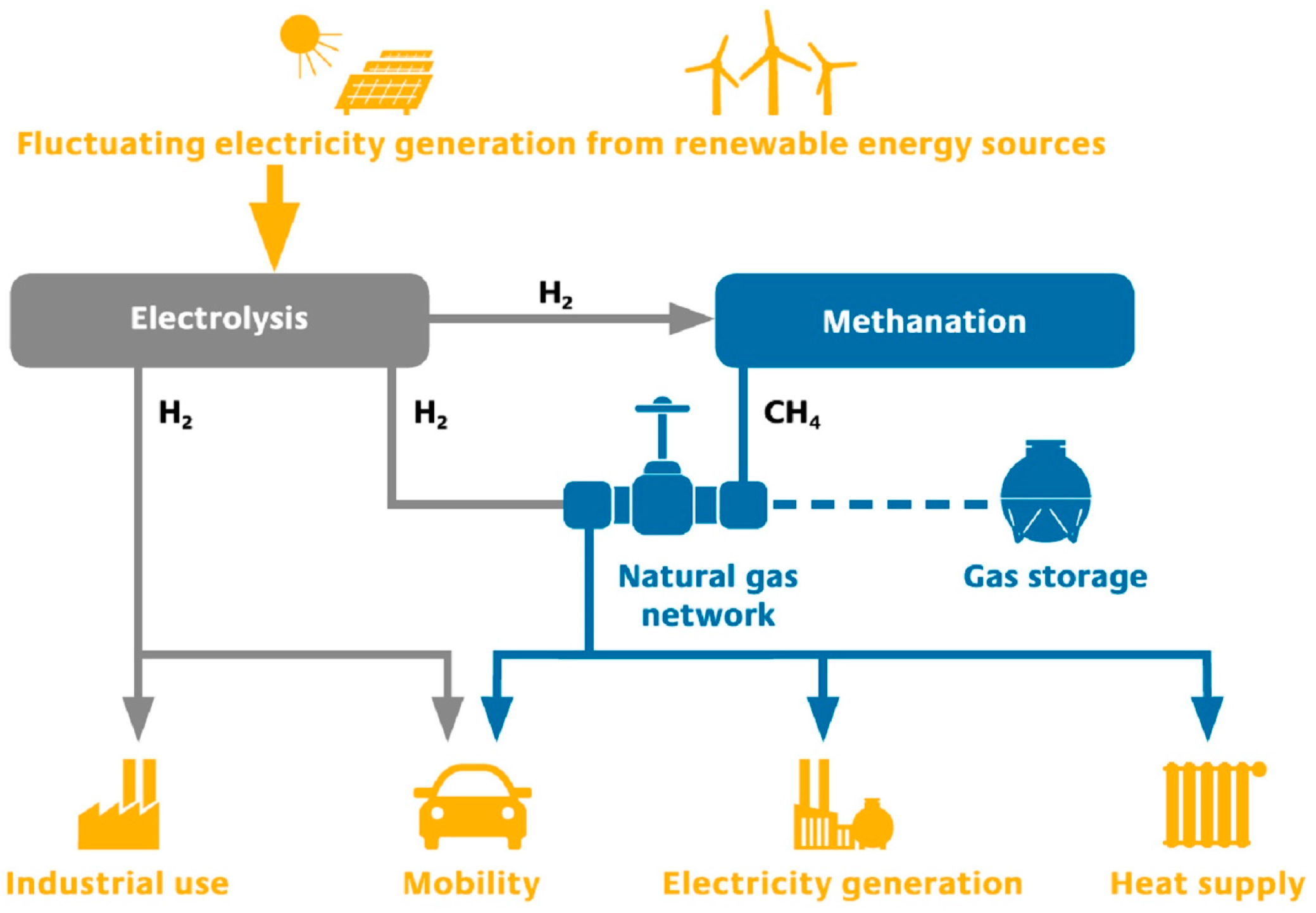

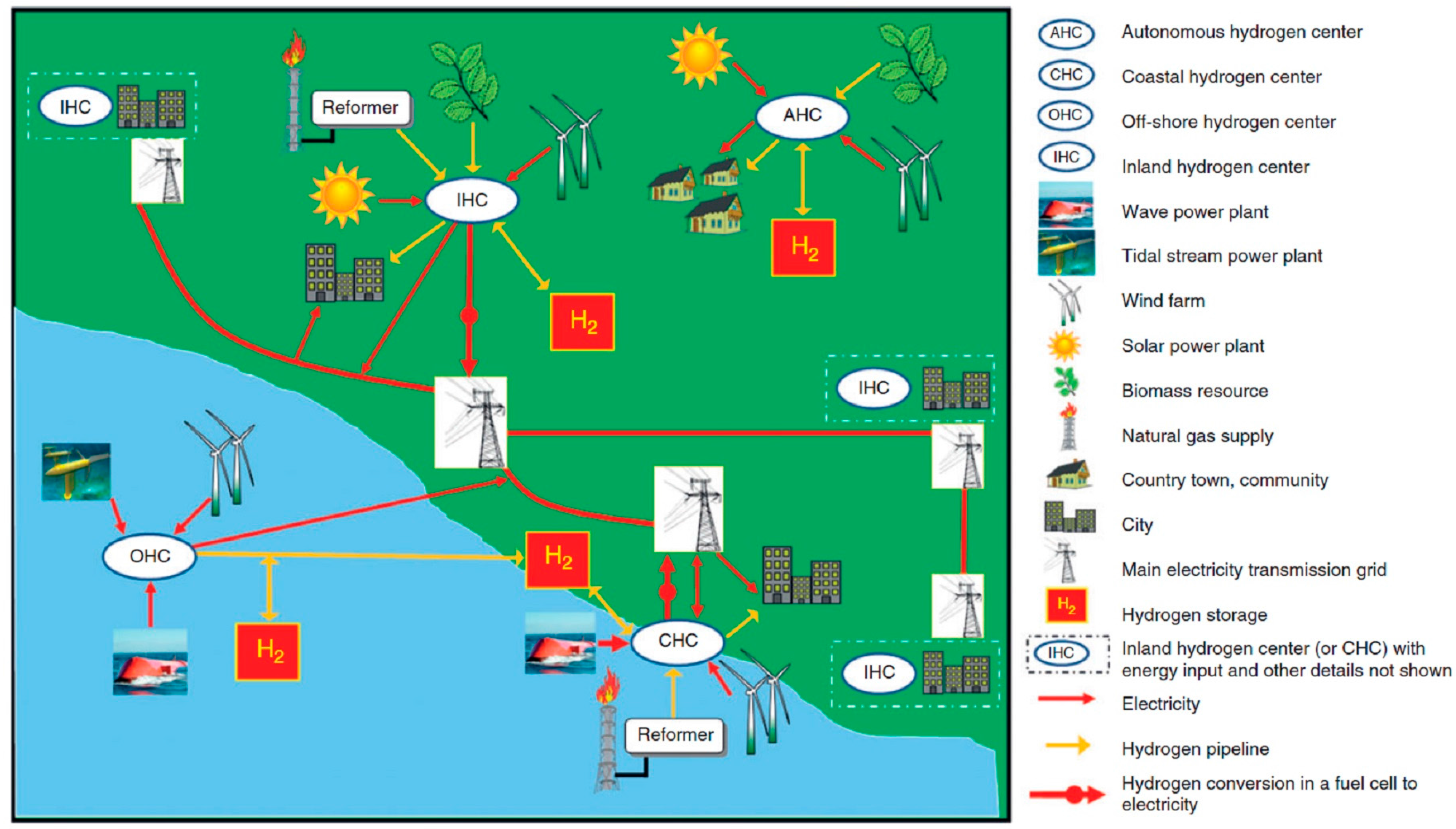

4.2. Hydrogen as an Alternative Energy Storage Solution

5. Conclusions

Author Contributions

Conflicts of Interest

References

- Andrews, J.; Shabani, B. The role of hydrogen in a global sustainable energy strategy. Wiley Interdiscip. Rev. Energy Environ. 2014, 3, 474–489. [Google Scholar] [CrossRef]

- By, P. The role of energy storage with renewable electricity generation. Natl. Renew. Energy Lab. 2010, 48, 563–575. [Google Scholar]

- Lott, M.; Tam, C.; Elzinga, D. Technology Roadmap: Energy Storage; International Energy Agency: Paris, France, 2014. [Google Scholar]

- Ibrahim, H.; Ilinca, A.; Perron, J. Energy storage systems—characteristics and comparisons. Renew. Sustain. Energy Rev. 2008, 12, 1221–1250. [Google Scholar] [CrossRef]

- Papaefthymiou, G.; Dragoon, K. Towards 100% renewable energy systems: Uncapping power system flexibility. Energy Policy 2016, 92, 69–82. [Google Scholar] [CrossRef]

- Beaudin, M.; Zareipour, H.; Schellenberglabe, A.; Rosehart, W. Energy storage for mitigating the variability of renewable electricity sources: An updated review. Energy Sustain. Dev. 2010, 14, 302–314. [Google Scholar] [CrossRef]

- Doe global energy storage database. Available online: http://www.energystorageexchange.org/projects (accessed on 1 March 2016).

- Renewable capacity statistics 2016. Available online: http://indiaenvironmentportal.org.in/content/427222/renewable-capacity-statistics-2016/ (accessed on 25 May 2016).

- Installed wind capacity. Available online: http://apps2.eere.energy.gov/wind/windexchange/wind_installed_capacity.asp (accessed on 26 May 2016).

- Energiewende in Germany: From Generation to Integration; Germany Trade and Invest: Berlin, Germany, 2014.

- California’s Energy Storage Mandate; California Public Utilities Commission (CPUC): San Francisco, CA, USA, 2014.

- The Texas Renewable Energy Industry; Government of Texas: Austin, TX, USA, 2014.

- New York State. Reforming the energy vision. Available online: http://www3.dps.ny.gov/W/PSCWeb.nsf/All/CC4F2EFA3A23551585257DEA007DCFE2?OpenDocument (accessed on 17 April 2016).

- Leading the Energy Transition Factbook—Electricity Storage; SBC Energy Institute: Gravenhage, TX, USA, 2013.

- Electrical Energy Storage White Paper; International Electrotechnical Commission: Geneva, Switzerland, 2011.

- Andrews, J.; Shabani, B. Re-envisioning the role of hydrogen in a sustainable energy economy. Fuel Energy Abstr. 2012, 37, 1184–1203. [Google Scholar] [CrossRef]

- Australian Energy Resource Assessment; Commonwealth of Australia: Canberra, Australia, 2010.

- Renewable Energy in Australia—How Do We Really Compare? Energy Supply Association of Australia: Canberra, Australia, 2014.

- Opportunities for Pumped Hydro Energy Storage in Australia; University of Melbourne, Melbourne Energy Institute: Melbourne, Australia, 2014.

- Kidston pumped storage project. Available online: http://arena.gov.au/project/kidston-pumped-storage-project/ (accessed on 7 July 2016).

- South Australian Electricity Report; Australian Energy Market Operator (AEMO): Melbourne, Australia, 2015.

- Battery Storage for Renewables: Market Status and Technology Outlook; International Renewable Energy Agency (IRENA): Abu Dhabi, UAE, 2015.

- Andrews, J.; Shabani, B. Where does hydrogen fit in a sustainable energy economy? Procedia Eng. 2012, 49, 15–25. [Google Scholar] [CrossRef]

- Power to Gas: The Case for Hydrogen White Paper; California Hydrogen Business Council: Los Angeles, CA, USA, 2015.

- Energy Storage Study—Funding and Knowledge Sharing Priorities; AECOM Australia Pty Ltd.: Brisbane, Australia, 2015.

- Overview of Korea’s electric power industry. Available online: https://home.kepco.co.kr/kepco/EN/B/htmlView/ENBAHP001.do?menuCd=EN020101 (accessed on 25 April 2016).

- California Public Utilities Commission (CPUC). Clean energy and pollution reduction act of 2015 (sb 350). Available online: http://www.cpuc.ca.gov/sb350/ (accessed on 29 March 2016).

- Advancing and Maximizing the Value of Energy Storage Technology—A California Roadmap; California Independent System Operator (ISO): Folsom, CA, USA, 2014.

- Pierpoint, L.M. Harnessing electricity storage for systems with intermittent sources of power: Policy and R&D needs. Energy Policy 2016, 96, 751–757. [Google Scholar]

- Duke energy to upgrade its Notrees energy storage system. Available online: https://www.duke-energy.com/news/releases/2015063001.asp (accessed on 13 April 2016).

- 2009 American Recovery and Reinvestment Act. Available online: http://energy.gov/oe/information-center/recovery-act (accessed on 13 April 2016).

- The Energy Storage Market in Germany; Germany Trade and Invest: Berlin, Germany, 2015.

- METI. Establishment of storage battery strategy project team. Available online: http://www.meti.go.jp/english/press/2012/0106_02.html (accessed on 16 April 2016).

- METI selected successful applicants that will introduce large-scale storage batteries into electricity grid substations and commit to expanding the introduction of renewable energy. Available online: http://www.meti.go.jp/english/press/2013/0731_03.html (accessed on 16 April 2016).

- Frequency Regulation Compensation in the Organized Wholesale Power Markets; Federal Energy Regulatory Commission (FERC): Washington, DC, USA, 2011.

- Third-Party Provision of Ancillary Services; Accounting and Financial Reporting for New Electric Storage Technologies; Federal Energy Regulatory Commission (FERC): Washington, DC, USA, 2013.

- State of the Market Report; Monitoring Analytics: Eagleville, PA, USA, 2015.

- U.S. Energy Storage Monitor: 2015 Year in Review; GTM Research: Boston, MA, USA, 2016.

- Pay for Performance Regulation Year 1 Design Changes; California Emergency Services Association (CESA): Berkeley, CA, USA, 2014.

- New York State Energy Plan; New York State: New York, NY, USA, 2015.

- Energy Storage Roadmap for New York’s Electric Grid; New York Battery & Energy Storage Technology Consortium (NY-BEST): New York, NY, USA, 2015.

- Con Edison. Demand management incentives. Available online: http://www.coned.com/energyefficiency/demand_management_incentives.asp (accessed on 19 April 2016).

- ESS Market Trend & Korea ESS Project Case Study; Kokam: Suwon, Korea, 2015.

- PG&E presents innovative energy storage agreements. Available online: https://www.pge.com/en/about/newsroom/newsdetails/index.page?title=20151202_pge_presents_innovative_energy_storage_agreements_ (accessed on 17 April 2016).

- Low carbon networks fund. Available online: https://www.ofgem.gov.uk/electricity/distribution-networks/network-innovation/low-carbon-networks-fund (accessed on 10 April 2016).

- Younicos. S&C Electric, Samsung SDI, UK Power Networks and Younicos collaborate to launch the smarter network storage project. Available online: http://www.younicos.com/en/media_library/press_area/press_releases/024_2014_12_15_Opening_Battery_Park_Leighton_Buzzard.html (accessed on 22 April 2016).

- Enhanced Frequency Response; National Grid: London, UK, 2016.

- Energy Storage Update. UK’s 200 mw grid storage tender flooded by battery bid interest. Available online: http://analysis.energystorageupdate.com/uks-200-mw-grid-storage-tender-flooded-battery-bid-interest (accessed on 23 April 2016).

- Southern California Edison—Local capacity requirements (“LCR”) RFO. Available online: https://www.sce.com/wps/portal/home/procurement/solicitation/lcr (accessed on 31 March 2016).

- Issue Brief: A Survey of State Policies to Support Utility-Scale and Distributed-Energy Storage; National Renewable Energy Laboratory (NREL): Golden, CO, USA, 2014.

- PG&E. Self-generation incentive program (sgip). Available online: http://www.pge.com/en/mybusiness/save/solar/sgip.page (accessed on 19 April 2016).

- Self-Generation Incentive Program—Program statistics. Available online: https://energycenter.org/programs/self-generation-incentive-program/program-statistics (accessed on 19 April 2016).

- RWTH Aachen University. Support program for battery storage systems. Available online: http://www.rwth-aachen.de/cms/root/Die-RWTH/Aktuell/Pressemitteilungen/Januar/~kbqx/Foerderprogramm-fuer-Batteriespeichersys/lidx/1/ (accessed on 21 April 2016).

- Energy Storage—Power to the People; HSBC: London, UK, 2014.

- The German Energy Transition–Status Quo and what Lies Ahead; Germany Trade & Invest (GTAI): Berlin, Germany, 2016.

- Hawaiian electric close to selecting energy storage providers to support more renewable energy for Oahu. Available online: https://www.hawaiianelectric.com/hawaiian-electric-close-to-selecting-energy-storage-providers-to-support-more-renewable-energy-for-oahu (accessed on 10 April 2016).

- HCEI. How Hawaii has empowered energy storage and forever changed the U.S. Solar industry. Available online: http://www.hawaiicleanenergyinitiative.org/how-hawaii-has-empowered-energy-storage-and-forever-changed-the-u-s-solar-industry/ (accessed on 10 April 2016).

- Community Energy Scotland. Community energy Scotland. Available online: http://www.communityenergyscotland.org.uk/index.asp (accessed on 10 April 2016).

- Eigg electric. Available online: http://www.isleofeigg.net/eigg_electric.html (accessed on 10 April 2016).

- Byron Shire Council. Byron shire aims to become Australia’s first zero emissions community. Available online: http://www.byron.nsw.gov.au/byron-shire-aims-to-become-australias-first-zero-emissions-community (accessed on 28 April 2016).

- Indigo Shire Council. Council, chamber throw weight behind energy blueprint. Available online: http://www.indigoshire.vic.gov.au/Your_Council/Media_Releases/Council_Chamber_throw_weight_behind_energy_blueprint (accessed on 28 April 2016).

- Commonwealth of Australia. How government works. Available online: http://www.australia.gov.au/about-government/how-government-works (accessed on 24 April 2016).

- Nelson, T.; Nelson, J.; Ariyaratnam, J.; Camroux, S. An analysis of Australia’s large scale renewable energy target: Restoring market confidence. Energy Policy 2013, 62, 386–400. [Google Scholar] [CrossRef]

- Australian Government. Repealing the carbon tax. Available online: http://www.environment.gov.au/climate-change/repealing-carbon-tax (accessed on 28 February 2016).

- Australian Government. Renewable energy (electricity) amendment bill 2015. Available online: http://www.aph.gov.au/Parliamentary_Business/Bills_Legislation/bd/bd1415a/15bd119 (accessed on 28 February 2016).

- Securing a Clean Energy Future: The Australian Government’s Climate Change Plan; Commonwealth of Australia: Canberra, Australia, 2011.

- Energy White Paper 2012—Australia’s Energy Transformation; Commonwealth of Australia: Canberra, Australia, 2012.

- Renew Economy. Turnbull’s sleight of hand on clean energy investment. Available online: http://reneweconomy.com.au/2016/turnbulls-sleight-of-hand-on-clean-energy-investment-63202 (accessed on 30 April 2016).

- Australian large-scale investment plunges 88% in 2014. Available online: http://about.bnef.com/landing-pages/australian-large-scale-investment-plunges-88-2014/ (accessed on 28 February 2016).

- Australia and Global Outlook for Energy Storage Development; Bloomberg New Energy Finance: Sydney, Australia, 2015.

- Energy storage. Available online: http://arena.gov.au/projects/energy-storage/ (accessed on 1 March 2016).

- About ARENA. Available online: http://arena.gov.au/about-arena/ (accessed on 1 March 2016).

- Investment Plan—July 2015; Australian Renewable Energy Agency (ARENA): Canberra, Australia, 2015.

- Australia’s Off-Grid Clean Energy Market Research Paper; AECOM Australia Pty Ltd: Sydney, Australia, 2014.

- Hydro Tasmania. Project information. Available online: http://www.kingislandrenewableenergy.com.au/project-information/overview (accessed on 2 March 2016).

- Hydrexia. Hydrexia products. Available online: http://hydrexia.com/hydrexia-hydrogen-storage-technology/ (accessed on 5 March 2016).

- Hydrogen Technology Road Map; Australian Government: Canberra, Australia, 2008.

- Clean Energy Finance Corporation Act 2012; Australian Government: Canberra, Australia, 2012.

- Sandfire Resources NL. Solar power project. Available online: http://www.sandfire.com.au/operations/degrussa/solar-power-project.html (accessed on 6 March 2016).

- CEFC Annual Report 2014–2015; Clean Energy Finance Corporation (CEFC): Brisbane, Australia, 2015.

- Delivering a Competitive Australian Power System—Part 1: Australia’s Global Position; Global Change Institute, University of Queensland: Brisbane, Australia, 2011.

- AEMC. National electricity market. Available online: http://www.aemc.gov.au/Australias-Energy-Market/Markets-Overview/National-electricity-market (accessed on 30 April 2016).

- AEMC. Demand response mechanism and ancillary services unbundling. Available online: http://aemc.gov.au/Rule-Changes/Demand-Response-Mechanism# (accessed on 8 March 2016).

- National Electricity Amendment (Local Generation Network Credits) Rule 2015; Australian Energy Market Commission (AEMC): Sydney, Australia, 2015.

- New Rules for a Demand Management Incentive Scheme; Australian Energy Market Commission (AEMC): Sydney, Australia, 2015.

- Australian Energy Regulator (AER). Electricity ring-fencing guideline 2016. Available online: https://www.aer.gov.au/networks-pipelines/guidelines-schemes-models-reviews/electricity-ring-fencing-guideline-2016 (accessed on 11 March 2016).

- Ergon Energy. Battery technology on electricity network an Australian first. Available online: https://www.ergon.com.au/about-us/news-hub/media-releases/regions/general/battery-technology-on-electricity-network-and-australian-first (accessed on 12 March 2016).

- Renewable Energy (Electricity) Act 2000—Compilation No.23; Australian Government: Canberra, Australia, 2015.

- Government of South Australia. RenewablesSA. Available online: http://www.renewablessa.sa.gov.au/ (accessed on 13 March 2016).

- Act Sustainable Energy Policy; Australian Capital Territory (ACT) Government: Canberra, Australia, 2011.

- A Renewable Energy Plan for South Australia; Government of South Australia: Adelaide, Australia, 2011.

- The Australian Renewable Energy Race: Which States Are Winning or Losing; Climate Council: Sydney, Australia, 2014.

- Parkinson, G. South Australia hits 100% renewables—for a whole working day. Available online: http://reneweconomy.com.au/2014/south-australia-hits-100-renewables-for-a-whole-working-day-86069 (accessed on 14 March 2016).

- Low Carbon Investment Plan for South Australia; Government of South Australia: Adelaide, Australia, 2015.

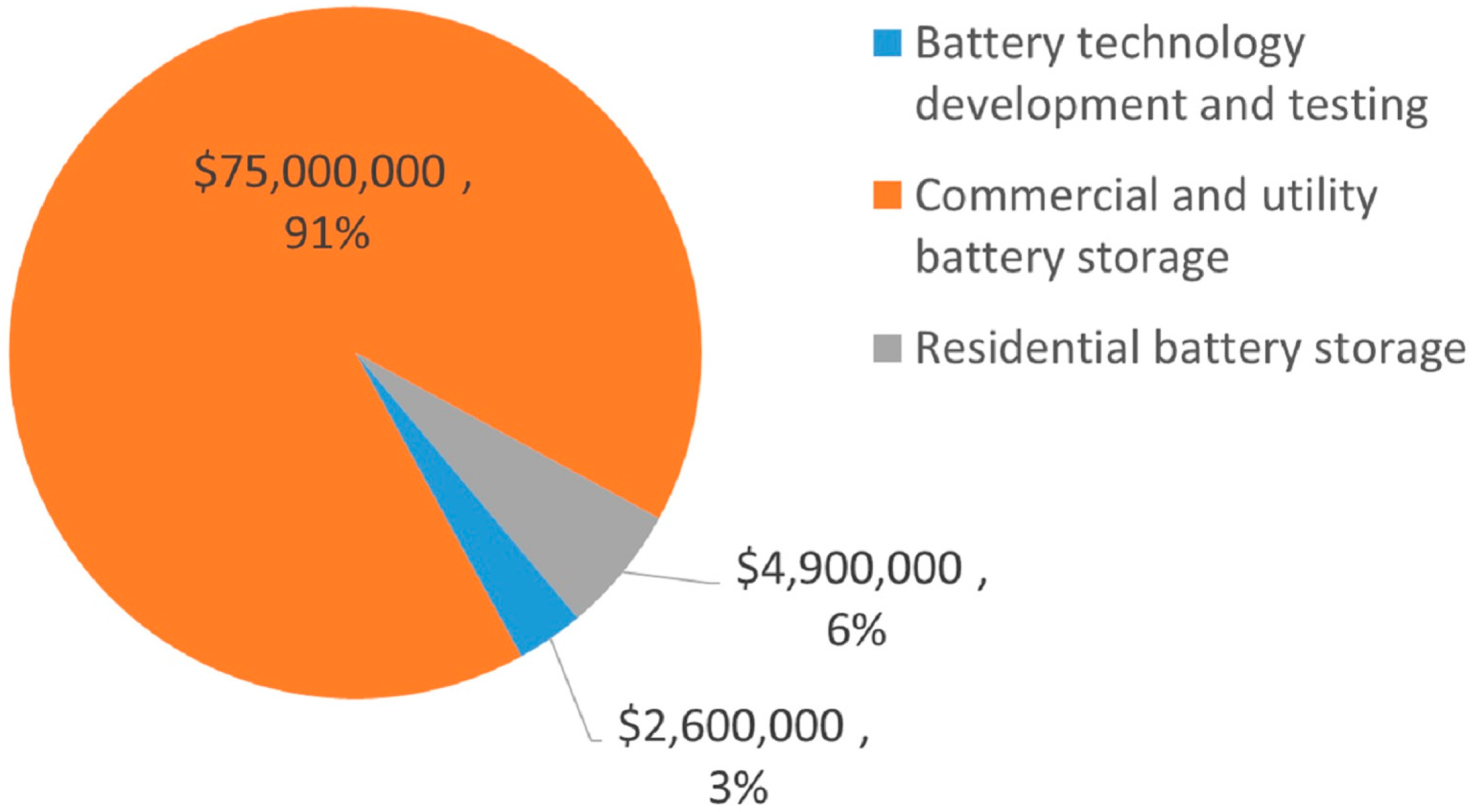

- Energy Storage for Commercial Renewable Integration; Australian Renewable Energy Agency (ARENA): Adelaide, Australia, 2015.

- Sustainable city incentives scheme. Available online: http://www.adelaidecitycouncil.com/your-council/funding/sustainable-city-incentives-scheme/ (accessed on 14 March 2016).

- Next generation renewables. Available online: http://www.environment.act.gov.au/energy/cleaner-energy/next-generation-renewables (accessed on 14 March 2016).

- Growth in the clean economy. Available online: http://www.environment.act.gov.au/energy/growth-in-the-clean-economy (accessed on 14 March 2016).

- Factsheet—Renewables from Germany; Berlin Energy Transition Dialogue: Berlin, Germany, 2016.

- Detailed Summary of 2015 Electricity Forecasts; Australian Energy Market Operator (AEMO): Melbourne, Australia, 2015.

- Future Energy Storage Trends; Commonwealth Scientific and Industrial Research Organisation (CSIRO): Newcastle, Australia, 2015.

- Emerging Technologies Information Paper; Australian Energy Market Operator (AEMO): Melbourne, Australia, 2015.

- Powerwall payback. Available online: https://www.choice.com.au/home-improvement/energy-saving/solar/articles/tesla-powerwall-payback-time (accessed on 4 June 2016).

- Colmenar-Santos, A.; de Palacio, C.; Enríquez-García, L.; López-Rey, Á. A Methodology for Assessing Islanding of Microgrids: Between Utility Dependence and Off-Grid Systems. Energies 2015, 8, 4436–4454. [Google Scholar] [CrossRef]

- Jacobson, M.Z.; Delucchi, M.A. Providing all global energy with wind, water, and solar power, Part I: Technologies, energy resources, quantities and areas of infrastructure, and materials. Energy Policy 2011, 39, 1154–1169. [Google Scholar] [CrossRef]

- Renewable Energy Sources and Climate Change Mitigation; Intergovernmental Panel on Climate Change (IPCC): Geneva, Switzerland, 2012.

- Balta-Ozkan, N.; Baldwin, E. Spatial development of hydrogen economy in a low-carbon UK energy system. Int. J. Hydrog. Energy 2013, 38, 1209–1224. [Google Scholar] [CrossRef]

- Lechtenböhmer, S.; Schneider, C.; Roche, M.; Höller, S. Re-industrialisation and low-carbon economy—Can they go together? Results from stakeholder-based scenarios for energy-intensive industries in the german state of north rhine westphalia. Energies 2015, 8, 11404–11429. [Google Scholar] [CrossRef]

- Power to Gas System Solution; Deutsche Energie-Agentur GmbH (dena): Berlin, Germany, 2015.

- European Parliament. Energy Storage: Which Market Designs and Regulatory Incentives Are Needed? European Union: Brussels, Belgium, 2015. [Google Scholar]

- European Power to Gas. Available online: http://www.europeanpowertogas.com/ (accessed on 1 June 2016).

- Bloomberg. Ene-farms use hydrogen to power homes but don’t come cheap. Available online: http://www.bloomberg.com/news/articles/2015-01-15/fuel-cells-for-homes-japanese-companies-pitch-clean-energy (accessed on 4 June 2016).

- Doe Hydrogen and Fuel Cells Program—Annual Progress Report; United States Department of Energy (USDOE): Washington, DC, USA, 2015.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Market | Application | Definition | Benefits of Energy Storage | Australian Context |

|---|---|---|---|---|

| Wholesale | Utility scale storage | Electricity generators which supply and sell electricity into the market, ancillary services for grid stability | Support higher penetration of intermittent renewable energy, price arbitrage, ancillary services | High state based renewable energy targets (50%–100%) |

| Transmission and Distribution (T&D) | Network management | Regulated monopolies that distribute electricity from generators to end users, ancillary services | Demand management, alleviate network constraints and power quality issues, ancillary services | Network constraints, power quality issues due to concentrations of renewable energy |

| End User | Behind the meter | Electricity consumers across the residential, commercial and industrial sectors | Support larger solar photovoltaics (PV) installations, increase solar PV utilisation, reduce network demand | High penetration of residential solar PV |

| Off Grid | Renewable energy hybridisation | Electricity systems not connected to main grid (e.g., islands, remote communities) | Support higher concentration of intermittent renewable energy to offset fossil fuels | Large off grid market |

| Country/State | Wholesale | Transmission and Distribution | End User | Off-Grid | |

|---|---|---|---|---|---|

| U.S. | California | Very High | Very High | High | Low |

| Hawaii | High | Medium | Low | High | |

| New York | Medium | Medium | Medium | Low | |

| Texas | Med- High | Low | Low | Low | |

| Germany | Medium | Medium | High | N/A | |

| UK | Medium | Medium | Low | Medium | |

| Japan | Medium | Medium | Medium | Medium | |

| Korea | Low | High | Medium | N/A | |

| Capacity | Type | Year | Operator | Application |

|---|---|---|---|---|

| 5 MW/5 MWh | Li-ion | 2014 | E.ON | Grid stability in a region with 80% renewable energy, ancillary services |

| 5 MW/5 MWh | Modular (Li-ion, high-temp, lead-acid) | 2015 | WEMAG AG | Renewable energy integration, grid stability, wholesale price arbitrage, ancillary services |

| 10 MW/10 MWh | Li-ion | 2015 | 50 Hertz | Grid stability, load balancing wind energy, ancillary services |

| Capacity | Type | Year | Operator | Application |

|---|---|---|---|---|

| 15 MW/60 MWh | Redox Flow | 2016 | Hokkaido Electric | Renewable energy integration, grid stability |

| 40 MW/20 MWh | Li-ion | 2016 | Tohoku Electric | Renewable energy integration, grid stability |

| Capacity | Type | Supplier | Application |

|---|---|---|---|

| 85 MW | Li-ion | Stem | Multiple locations to provide demand reduction and grid support |

| 50 MW | Li-ion | Advanced Microgrid Solutions | Multiple commercial and industrial buildings to provide demand reduction and grid support |

| Title | Description | Benefits for Energy Storage |

|---|---|---|

| Demand Response Mechanism rule change [83] | Establish a new class of market participant, a demand response aggregator (DRA), to allow consumers to participate in the wholesale market | Aggregation of small-scale battery storage units to act as one generator |

| Local Generation Network Credits (LGNCs) rule change [84] | Incentivise networks to recognise the benefits of local generation by requiring them to implement a LGNC | Financial incentive |

| Demand Management Incentive Scheme (DMIS) rule change [85] | Reward networks to deliver non-network options that deliver cost savings to customers through demand management | Financial incentive |

| Demand Management Innovation Allowance (DMIA) rule change [85] | Provide funding for research and development projects that have the potential to reduce long term network costs via demand reduction | Financial incentive |

| Electricity ring-fencing guideline [86] | Enable networks to provide behind the meter services through third party contractors or ring fenced businesses | Competitive market development |

| Key Strategy | Relevance to Energy Storage | Specific Project/Funding |

|---|---|---|

| Clear policy and efficient regulatory environment | Creation of an Investment Attraction Agency to attract new businesses | AUD $200,000 grant for ZEN Energy Systems to support the further development of its battery storage system |

| Information to inform investment | Improve information to assess project viability | Update existing directory of diesel generation to assess opportunities for hybrid renewable energy and storage projects |

| Sponsoring uptake and government procurement | Financial incentives and market development support | - AUD $1.1 million to demonstrate battery storage on government buildings - AUD $3 million for a mobile energy storage testing facility for battery technology and grid integration |

| Facilitating projects to leverage funding and support | Financial incentives | - Subsidise Coober Pedy Council PPA for electricity produced by a hybrid renewable energy and battery storage project - Funding to assess feasibility of medium-large scale battery storage (5 MW–30 MW/25 MW–300 MWh) to integrate intermittent renewable energy |

| Capacity | Year | Utility | Technology Provider | Electrolyser Type |

|---|---|---|---|---|

| 6 MW | 2015 | Stadtwerke Mainz AG | Siemens | PEM |

| 1 MW | 2015 | E.ON | Hydrogenics | PEM |

| 150 kW | 2015 | RWE | ITM Power | PEM |

| 300 kW | 2014 | Mainova AG | ITM Power | PEM |

| 2 MW | 2013 | E.ON | Hydrogenics | PEM |

| 1 MW | 2013 | UNK | Hydrogenics | PEM |

| 400 kW | 2013 | EnBW | Hydrogenics | PEM |

| Capacity | Year | Country | Project Name | Application |

|---|---|---|---|---|

| 1 MW | 2016 | Denmark | Bio Cat | Combined heat and power (CHP) |

| 1.2 MW | 2016 | Italy | INGRID | supply-demand balancing |

| 48 kW | 2004 | Norway | Utsira | Micro-grid (island) |

| 1 MW | 2012 | France (Corsica) | Jupiter 1000 | Island grid stability |

| 70 kW | 2010 | Spain | ITHER | Mobility |

| 400 kW | 2006 | Spain | HyFLEET:CUTE | Mobility |

| 400 kW | 2003 | Netherlands | HyFLEET:CUTE | Mobility |

| 12 MW | 2016 | Netherlands | Delfzijl | Chemical processing |

© 2016 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Moore, J.; Shabani, B. A Critical Study of Stationary Energy Storage Policies in Australia in an International Context: The Role of Hydrogen and Battery Technologies. Energies 2016, 9, 674. https://doi.org/10.3390/en9090674

Moore J, Shabani B. A Critical Study of Stationary Energy Storage Policies in Australia in an International Context: The Role of Hydrogen and Battery Technologies. Energies. 2016; 9(9):674. https://doi.org/10.3390/en9090674

Chicago/Turabian StyleMoore, Jason, and Bahman Shabani. 2016. "A Critical Study of Stationary Energy Storage Policies in Australia in an International Context: The Role of Hydrogen and Battery Technologies" Energies 9, no. 9: 674. https://doi.org/10.3390/en9090674

APA StyleMoore, J., & Shabani, B. (2016). A Critical Study of Stationary Energy Storage Policies in Australia in an International Context: The Role of Hydrogen and Battery Technologies. Energies, 9(9), 674. https://doi.org/10.3390/en9090674