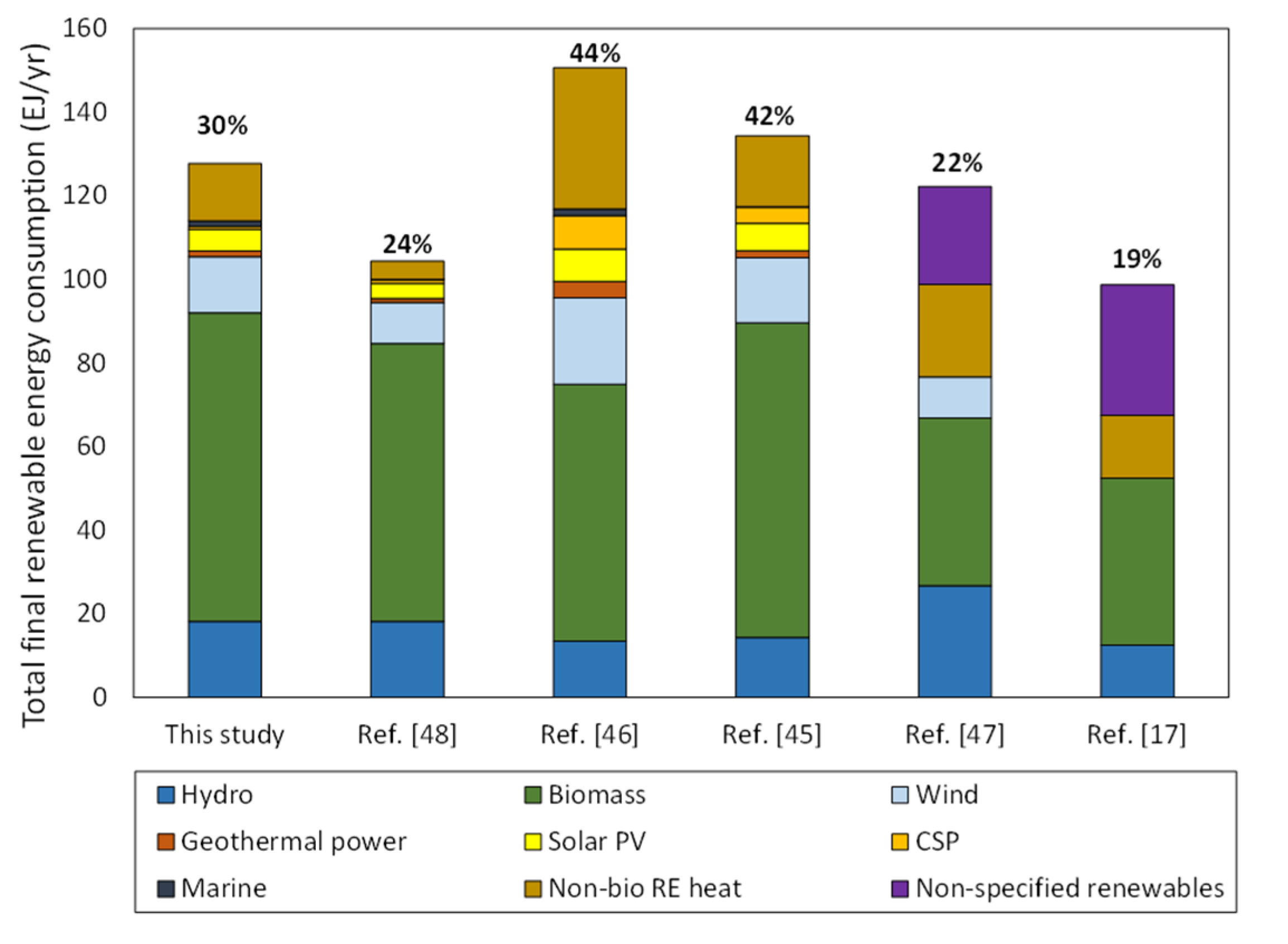

The Implications for Renewable Energy Innovation of Doubling the Share of Renewables in the Global Energy Mix between 2010 and 2030

Abstract

:1. Introduction

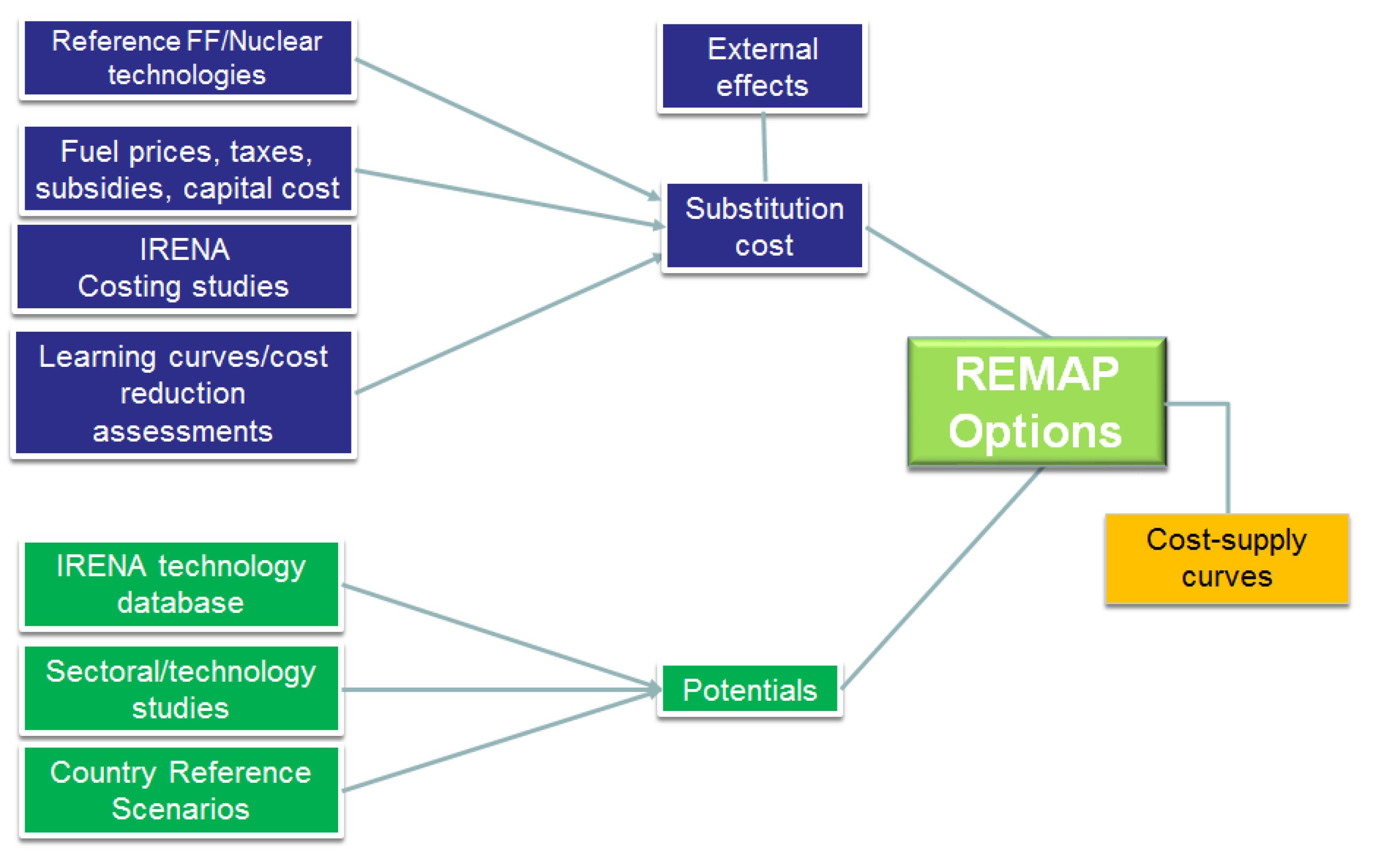

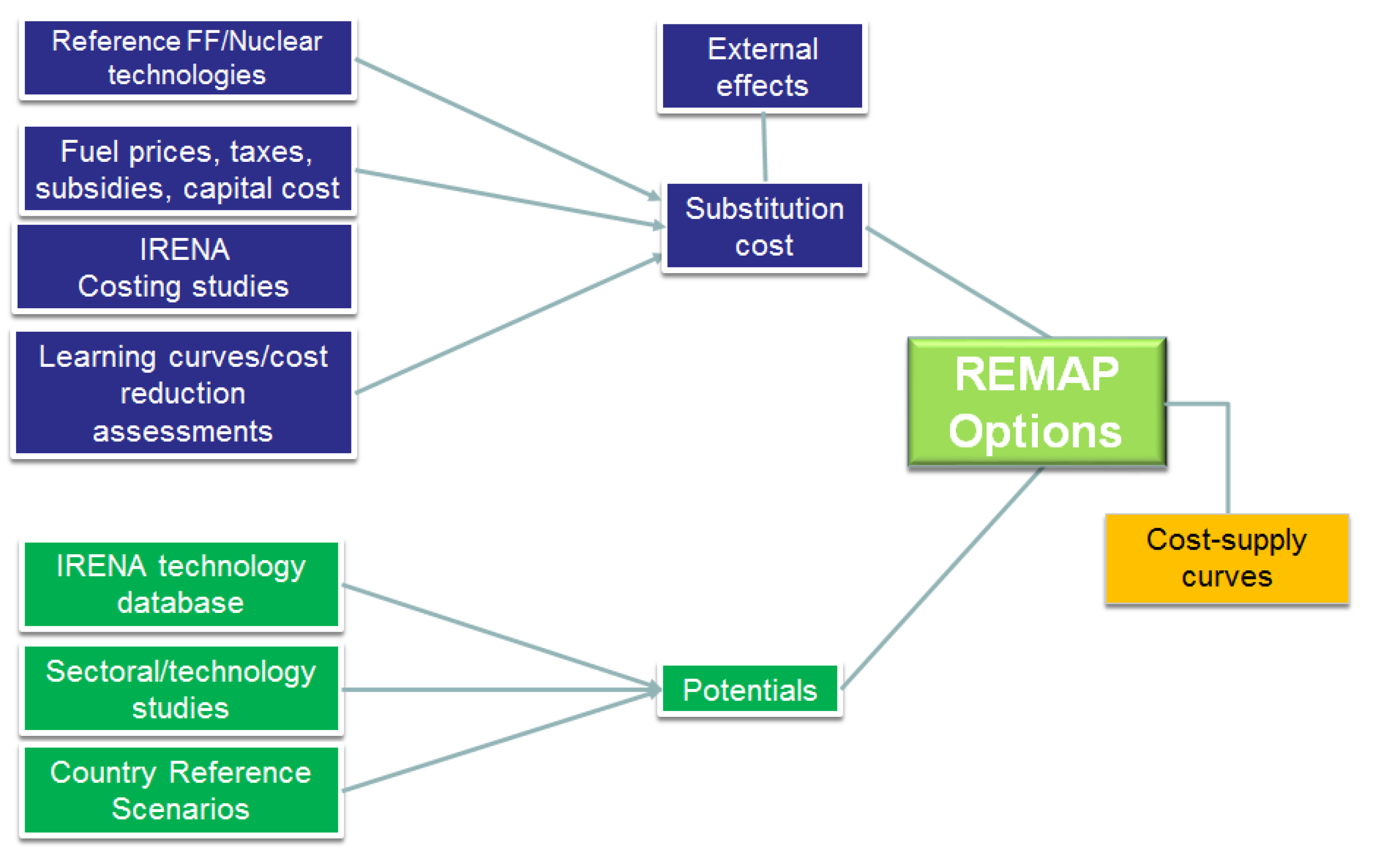

2. Methodology and Data Sources

- (i)

- As a starting point, we developed a Reference Case for each country, which represents policies in place or under consideration. The Reference Case also includes any expected developments in energy efficiency improvement. The analysis starts with a base year of 2010 and we collected the most up-to-date national plans of each country with a time horizon of 2030. These plans include a breakdown by energy carriers for the transformation (power and DH) and end-use sectors. However, the availability of country data varies, hence we filled data gaps. If no energy plan was available, IRENA worked with the REmap experts in developing a Reference Case (see Annex for an overview). We also completed any missing datasets, for instance for end-use sector demand, with information from literature and commercial databases. In collecting data from 26 countries, we harmonized the data in terms of the energy units expressed (final energy in petajoules (PJ) per year) and the system boundary of the end-use sectors.

- (ii)

- In a subsequent step, we investigated the REmap Options in each country together with the national experts. REmap Options are technology opportunities to replace conventional energy technologies (fossil fuel, nuclear and traditional biomass) present in 2030 with RE technologies (biomass, solar, wind, hydro, geothermal and ocean). The choice for the options approach is different than a scenario analysis since REmap is an exploratory study, and not a target-setting exercise. Each REmap Option is expressed in PJ final renewable energy per year and includes an associated substitution cost (in real 2010 US Dollars (USD) per gigajoule (GJ) final renewable energy). We collected our own data and combined this with the insights national experts provided about the technical, economic and political feasibility of different pathways to 2030. Once the REmap Options were estimated, a conventional technology that needs to be substituted is selected with additional input from national experts. This is based on the policy choices of the countries.

- (iii)

- After the data collection step was completed, we included the REmap Options in the Reference Case, which resulted in a “REmap 2030 Case” for each country. We shared results with the countries for final review and subsequently updated them if necessary. Once the REmap 2030 results were agreed on with the countries, we aggregated and extrapolated the 26 country findings to arrive at the global potential.

- (i)

- Growth in RE use in TFEC (PJ/year) and technology capacity (indicator 1): We estimate the total consumption of each resource (e.g., liquid biofuels, geothermal heat) or the total installed capacity (e.g., gigawatt (GW) wind power plant, or million square meters (m2) of solar thermal) for the years 2000, 2010, and 2030, and compare this to 2010 level. This indicator represents the scale of the deployment challenge for renewables, including potential barriers in scale-up of production, supply chains, and capacity for installation and maintenance. This indicator provides information about the policy required to overcome technological challenges, according to readiness of each technology, if the full deployment of the 2030 potential is targeted.

- (ii)

- RE share (in %) (indicator 2): We estimate the RE share separately for end-use (buildings, transport and industry) and generation sectors (in addition to the power sector, we also estimated the RE share for the DH sector. However, given the size of the sector relative to others, it is not discussed in further detail in the rest of this paper). For the end-use sectors, we add up the total RE use by all energy carriers and the share of electricity and DH consumption originating from RE to estimate each sector’s total RE use. We divide this total by that sector’s TFEC to arrive at the sector RE share. We also estimate this indicator by excluding all DH and electricity use, both from RE use and the TFEC (both RE share indicators, with and without electricity and DH, could also be estimated for the TFEC of the entire country by adding up the three end-use sectors). For the power sector, we compare the total power generation from renewables and divide this by the total power generation from all energy carriers in the sector in that country. We estimate all RE share indicators for 2010 and separately for Reference Case in 2030 and REmap 2030. This indicator represents the penetration level of renewables, and as such the level of change required in the energy system. Higher penetration levels will require different system adjustments to support renewables-based energy systems. This information indicates the innovation requirement and adjustments needed in current infrastructure and energy system (manufacturers, component suppliers, installers, and support services). These requirements have to accompany the increase in the RE share [28] estimated between 2010 and 2030.

- (iii)

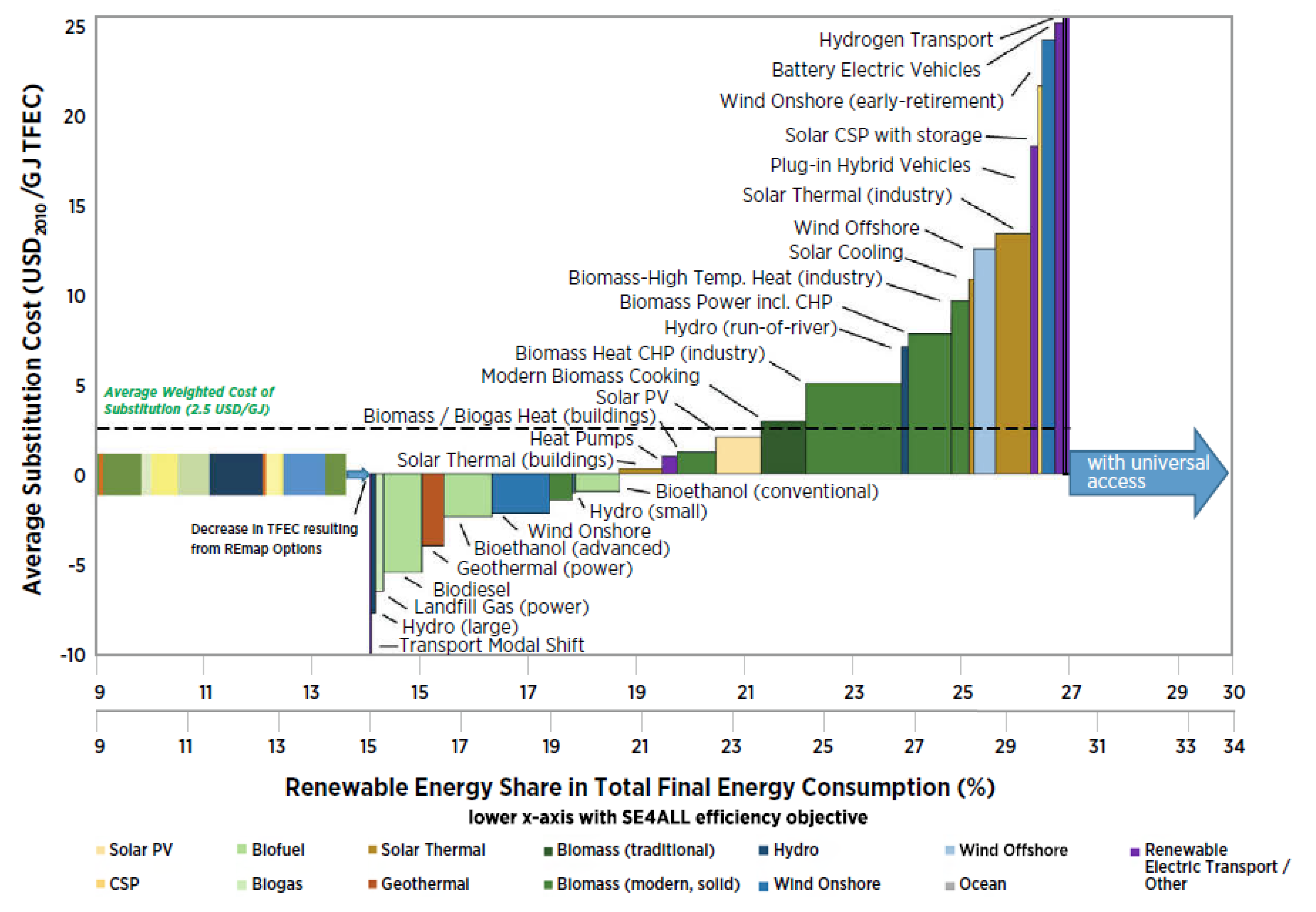

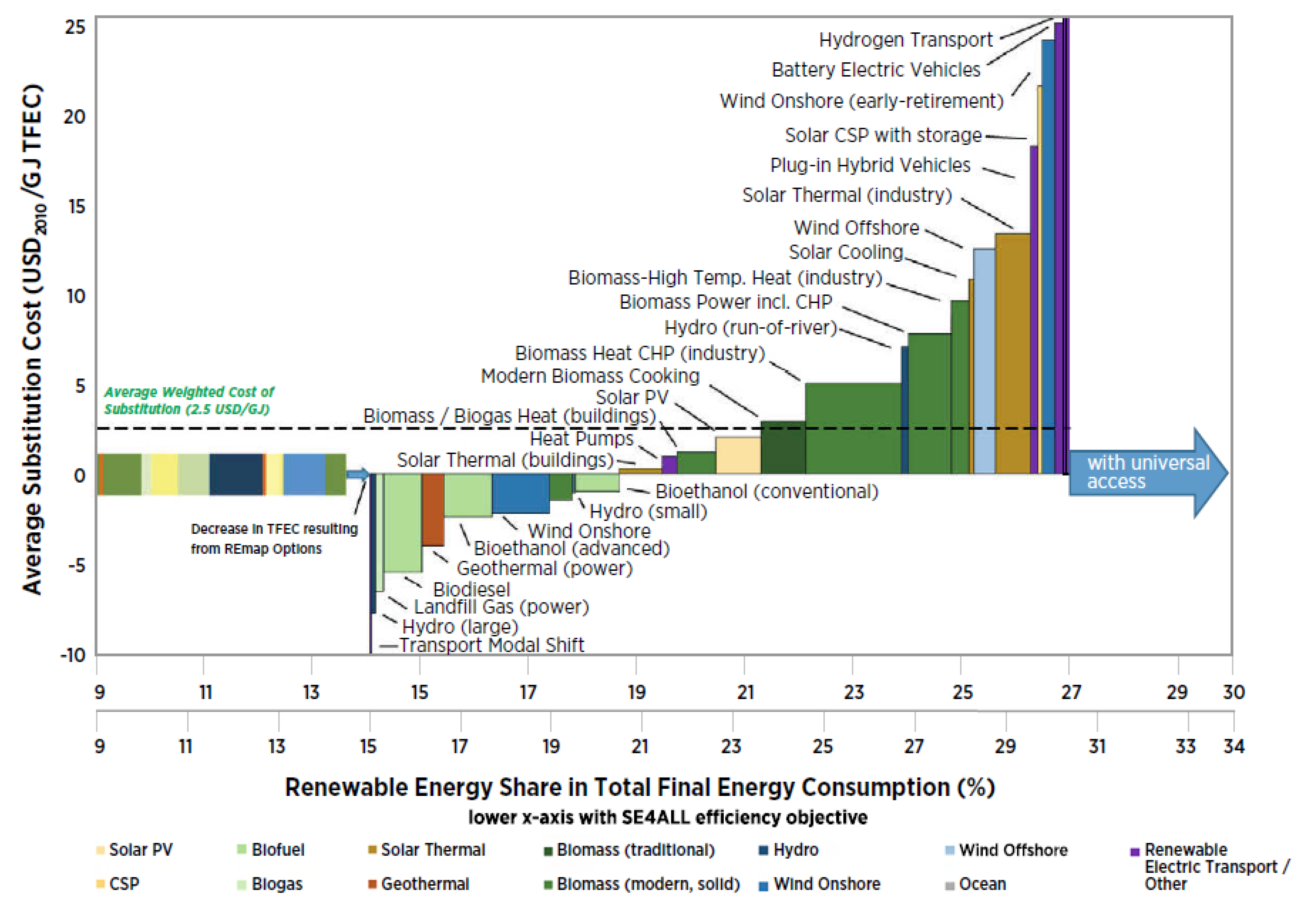

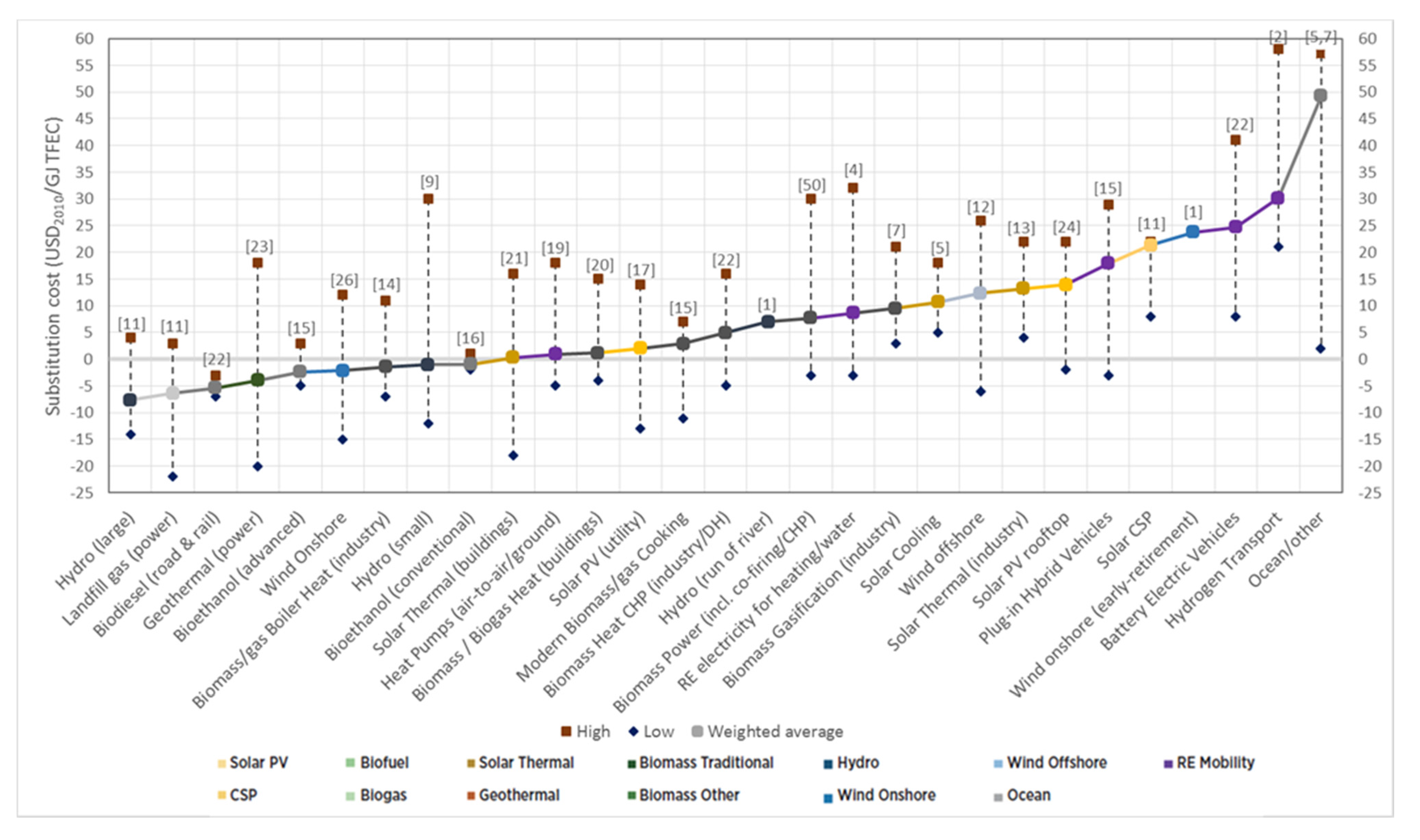

- Substitution cost (in USD/GJ) (indicator 3): This is the key indicator to estimate the cost-effectiveness of renewable energy technologies. It represents the difference between the annualized costs of the REmap Options and a conventional technology used to generate the same amount of useful energy output (e.g., cooking heat, electricity, mechanical work) divided by the total renewable energy use in final energy terms. Negative substitution costs suggest that there are opportunities to save money, whilst positive substitution costs suggest that additional efforts will be needed to attract the investments required to achieve the targeted deployment levels. This indicator represents the challenges associated with the need to attract innovation investments. A thorough consultation with experts complements the estimates of substitution costs and reduces the uncertainty in the estimates. By doing so, substitution costs can guide both investors and policy-makers on innovation investment opportunities arising in certain technology and sectors, as well as the efforts required to expand the funding portfolio within certain other innovative technological fields.

3. Results

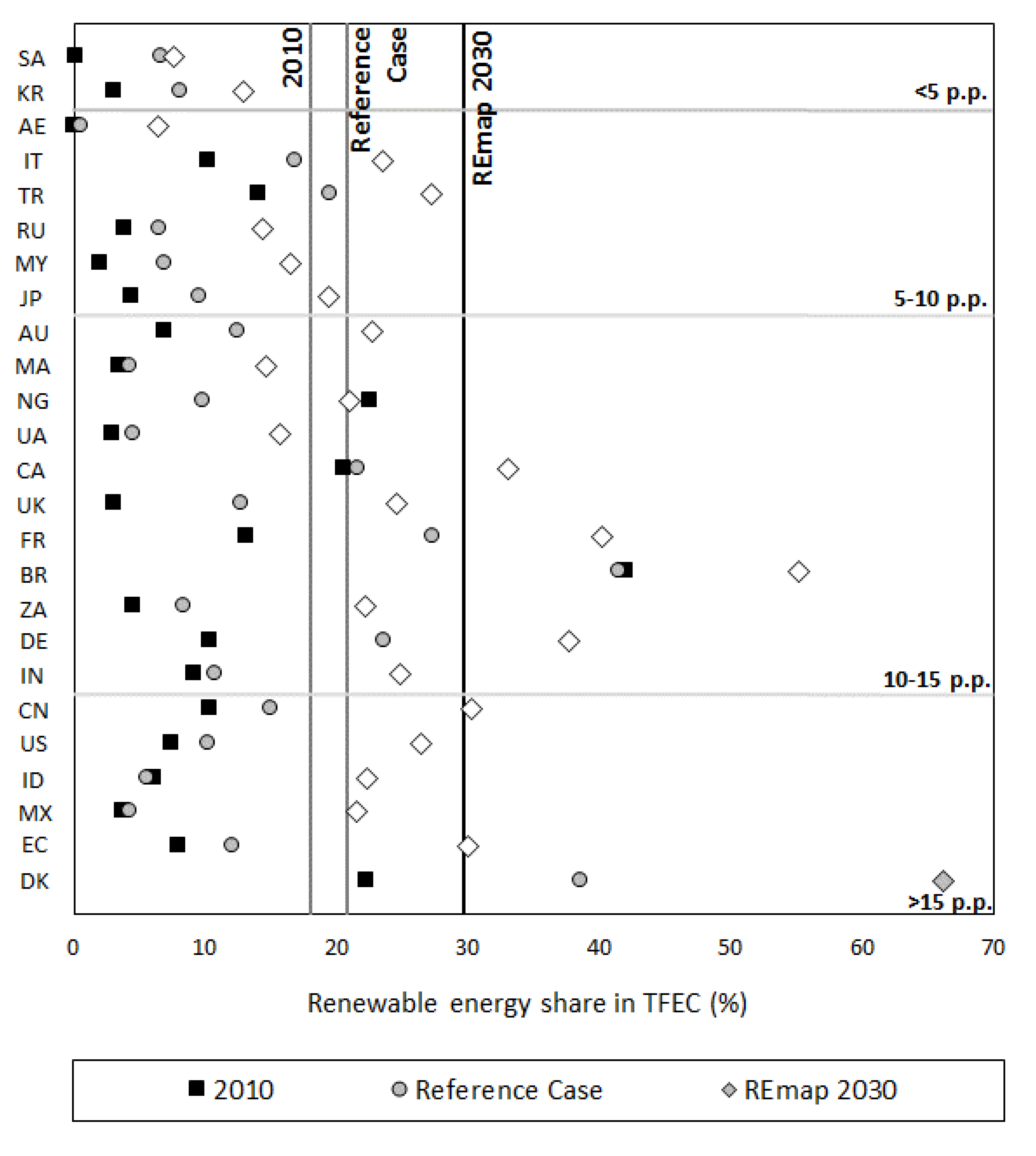

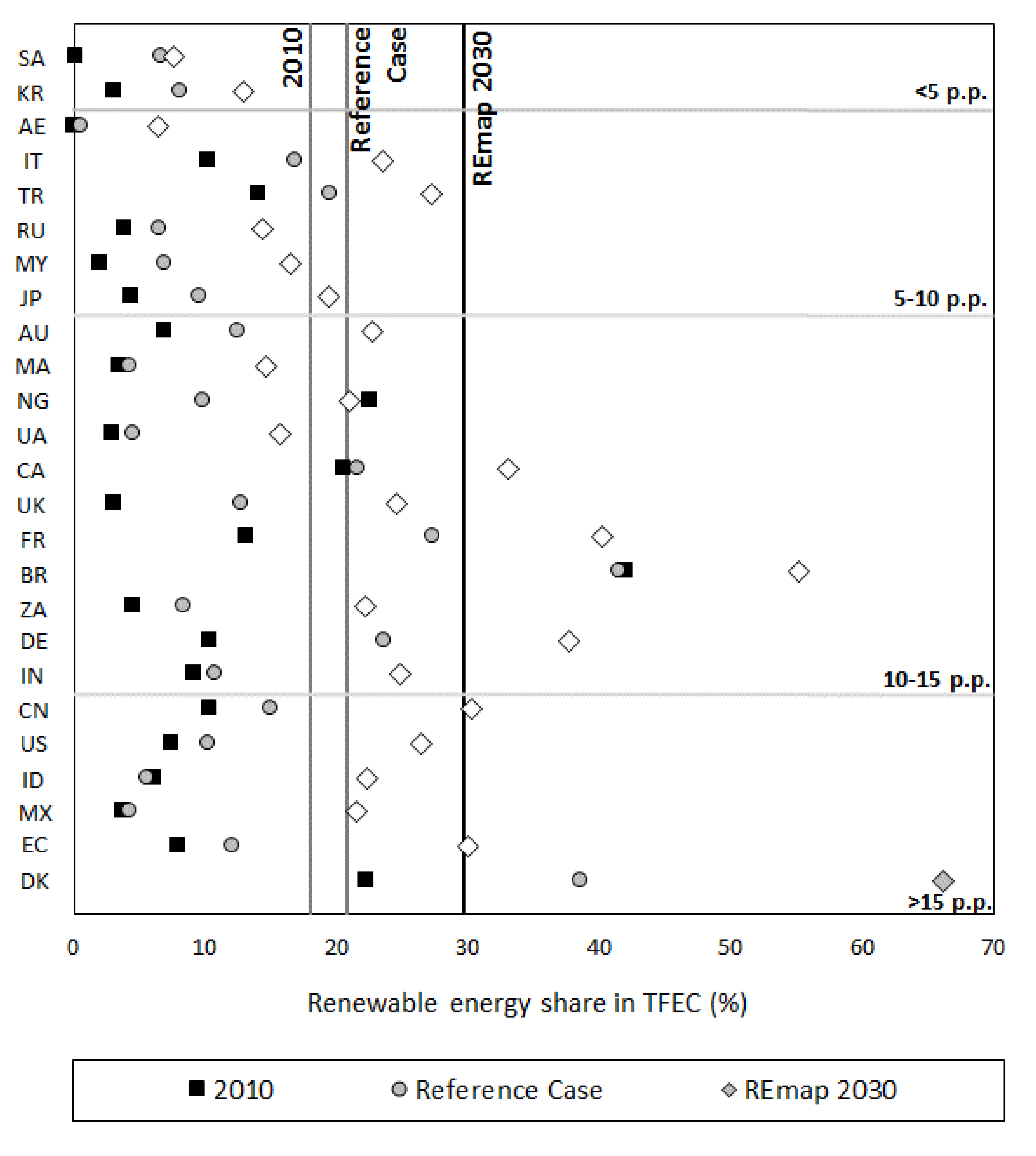

3.1. Findings at Country-Level

- Four countries of the European Union (EU) with high RE shares in 2010, namely Denmark, France, Germany and the UK, increase their shares the most by at least 10 percentage points between 2010 and the Reference Case. In 2030, these countries reach between 13% (UK) and 39% (Denmark) RE share. France and Germany more than double their shares, and the UK triples it (we assessed the RE shares for the Reference Case for France and the UK based on their 2020 RE commitments according to their national renewable energy action plans (NREAP) [33]. We included no further deployment of RE between 2020 and 2030; however, any improvements in energy efficiency were taken into account. Denmark and Germany have targets for 2030 which take their renewable energy share in the 2030 Reference Case higher than the 2020 targets according to their NREAPs).

- In 2010, 16 other countries have RE shares ranging from 0% to 10%. Given the very low starting points of some of them, the growth in Reference Case takes the RE shares to between 1% (UAE) and 13% (Australia) only. This is much lower than the global average of 18% today and efforts in national plans of these countries to 2030 are lower compared to EU countries. This is mainly an outcome of the differences in the existing policies and target setting approach between the EU countries and the rest of the world. In addition, the TFEC growth in the EU is low which helps achieving higher RE shares.

- We estimate a decrease in the RE shares between 2010 and Reference Case for Brazil (42%), Indonesia (6%), and Nigeria (23%). Brazil and Indonesia start at high RE share levels due to large amount of biomass use. The decrease in RE share is a result of the substitution of the traditional use of biomass with modern forms of renewables in the Reference Case. Traditional uses of biomass are characterized by inefficient combustion, therefore, more energy input is required than with a modern form of RE.

- Compared to the Reference Case, most countries have a potential to more than double their RE shares in REmap 2030. For example China, Ecuador, India, Indonesia, Mexico and the US increase their RE shares by at least 15 percentage points between the Reference Case and REmap 2030 (see the bottom category in Figure 2). In other countries, we estimate potential to increase the RE shares by between 10 and 27 percentage points. The large increase in RE share beyond Reference Case indicates that the potential of renewables may not be fully considered by countries. The increase in RE shares in the UAE, Malaysia, Russia, South Korea or Saudi Arabia is among the lowest, but this is also explained by their very low starting points today.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | 2010 | Reference Case | REmap 2030 | Contribution to global RE use 2030 | RE share in REmap 2030 |

|---|---|---|---|---|---|

| (PJ/year) | (PJ/year) | (PJ/year) | (%) | (%) | |

| China | 12.2 | 14.0 | 26.7 | 20.2 | 30.2 |

| US | 4.9 | 6.9 | 17.6 | 13.3 | 26.4 |

| Brazil | 4.1 | 7.2 | 9.4 | 7.2 | 55.1 |

| India | 7.6 | 3.3 | 7.3 | 5.6 | 24.8 |

| Indonesia | 1.6 | 0.9 | 3.6 | 2.7 | 22.3 |

| Canada | 1.8 | 2.2 | 3.4 | 2.5 | 33.0 |

| Russia | 0.8 | 1.3 | 2.9 | 2.2 | 14.4 |

| Germany | 1.0 | 1.5 | 2.4 | 1.8 | 37.7 |

| Japan | 0.6 | 1.1 | 2.2 | 1.7 | 19.4 |

| France | 0.8 | 1.4 | 2.0 | 1.5 | 40.2 |

| Mexico | 0.5 | 0.3 | 1.7 | 1.3 | 21.5 |

| Turkey | 0.4 | 1.2 | 1.7 | 1.3 | 27.2 |

| Nigeria | 3.8 | 0.7 | 1.4 | 1.0 | 21.0 |

| United Kingdom | 0.2 | 0.7 | 1.2 | 0.9 | 24.5 |

| Italy | 0.5 | 0.8 | 1.2 | 0.9 | 23.5 |

| Australia | 0.3 | 0.6 | 1.0 | 0.8 | 22.7 |

| South Korea | 0.2 | 0.6 | 0.9 | 0.7 | 12.9 |

| South Africa | 0.3 | 0.3 | 0.8 | 0.6 | 22.2 |

| Ukraine | 0.1 | 0.2 | 0.6 | 0.5 | 15.7 |

| Malaysia | 0.1 | 0.2 | 0.4 | 0.3 | 16.5 |

| Denmark | 0.1 | 0.2 | 0.4 | 0.3 | 66.1 |

| Saudi Arabia | 0.0 | 0.3 | 0.4 | 0.3 | 7.7 |

| UAE | 0.0 | 0.0 | 0.3 | 0.2 | 6.4 |

| Morocco | 0.1 | 0.0 | 0.2 | 0.1 | 14.6 |

| Ecuador | 0.1 | 0.1 | 0.1 | 0.1 | 29.9 |

| Other | 21.0 | 46.8 | 41.9 | 32.1 | 30.0 |

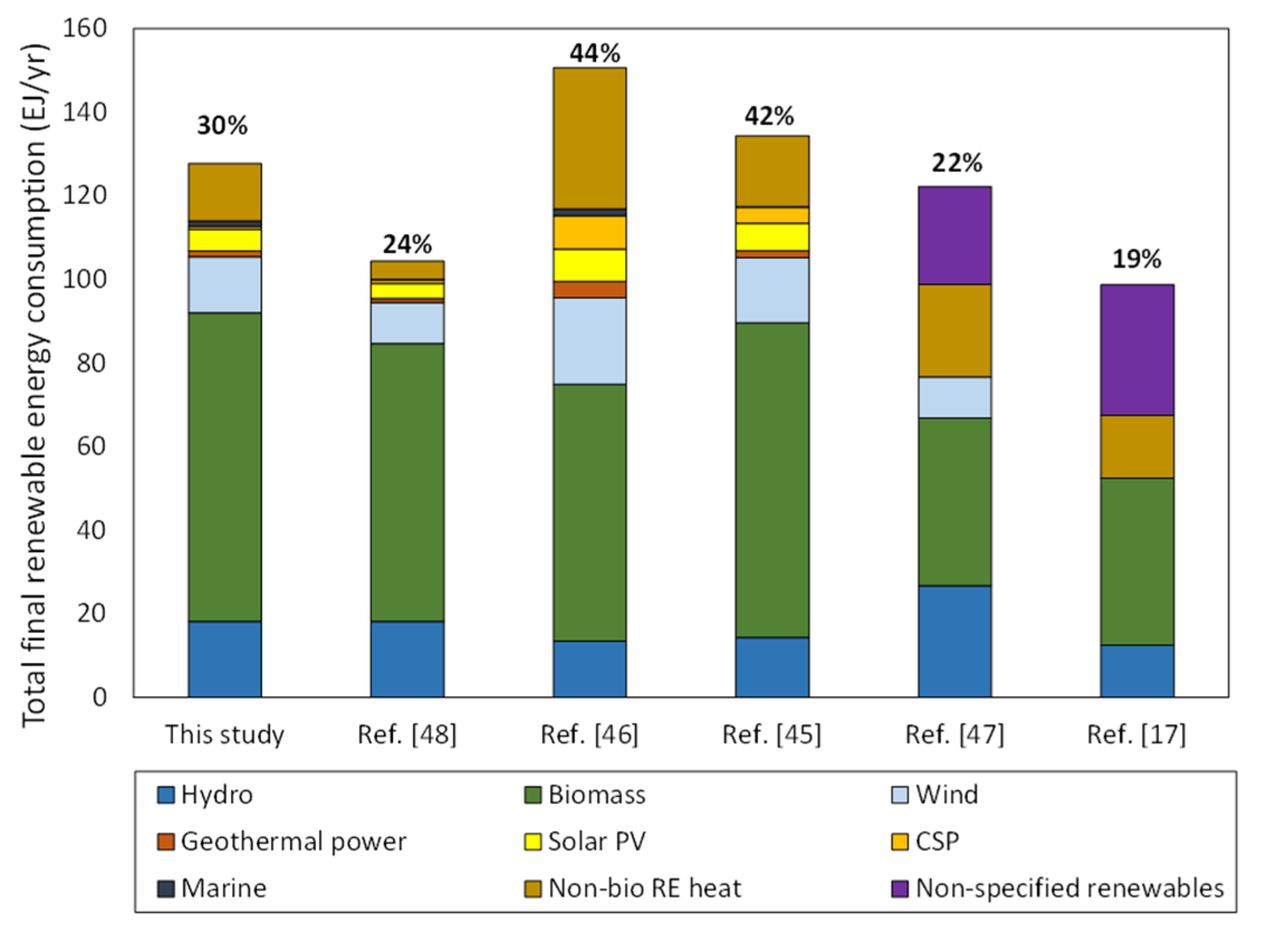

| World | 62.9 | 93.0 | 131.5 | 100 | 29.9 |

3.2. Findings for Technologies

| 2010 | Reference Case 2030 | REmap 2030 | RE share in TFEC | |||

|---|---|---|---|---|---|---|

| 2010 | Reference Case 2030 | REmap 2030 | ||||

| (PJ/year) | (PJ/year) | (PJ/year) | (%) | (%) | (%) | |

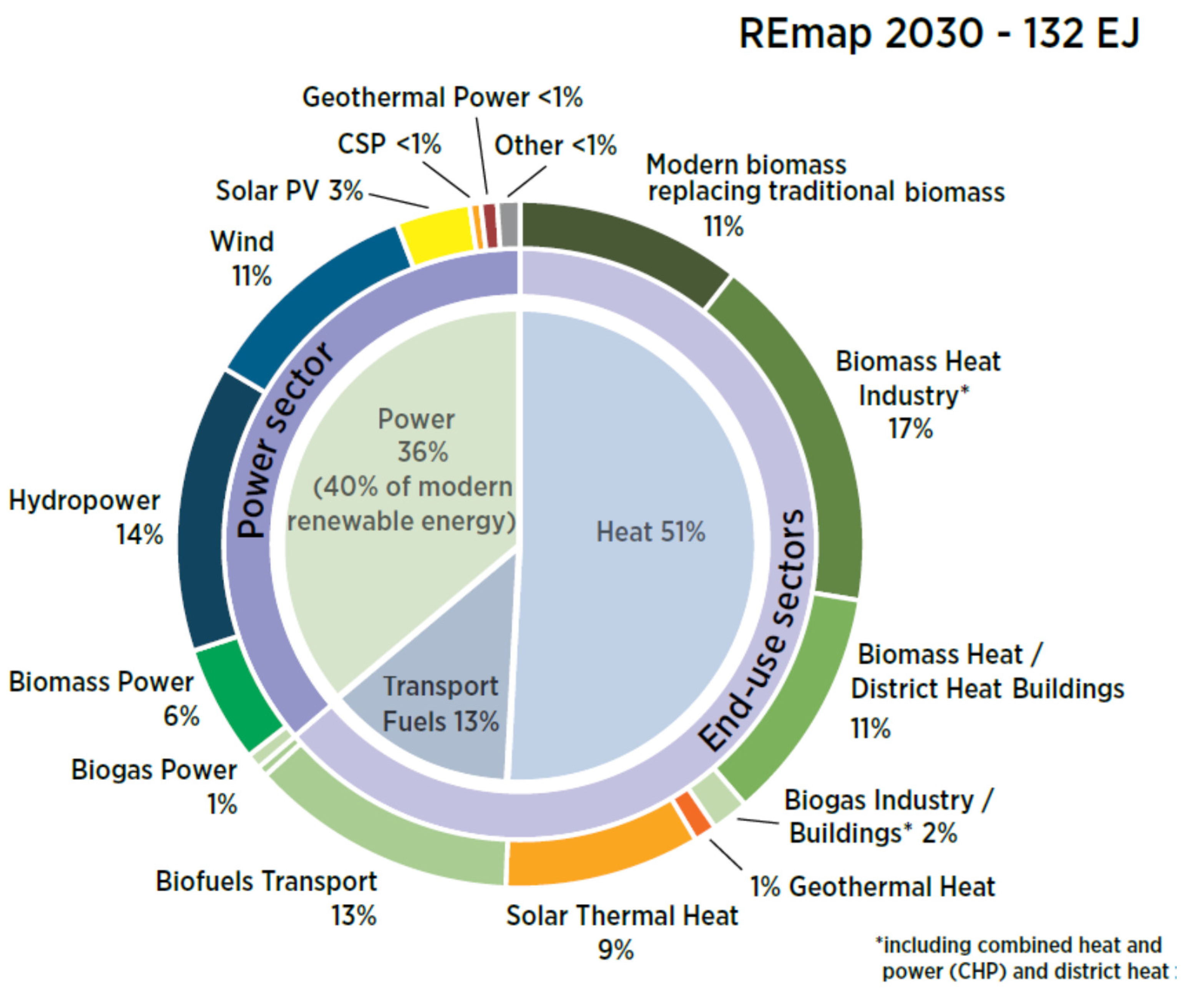

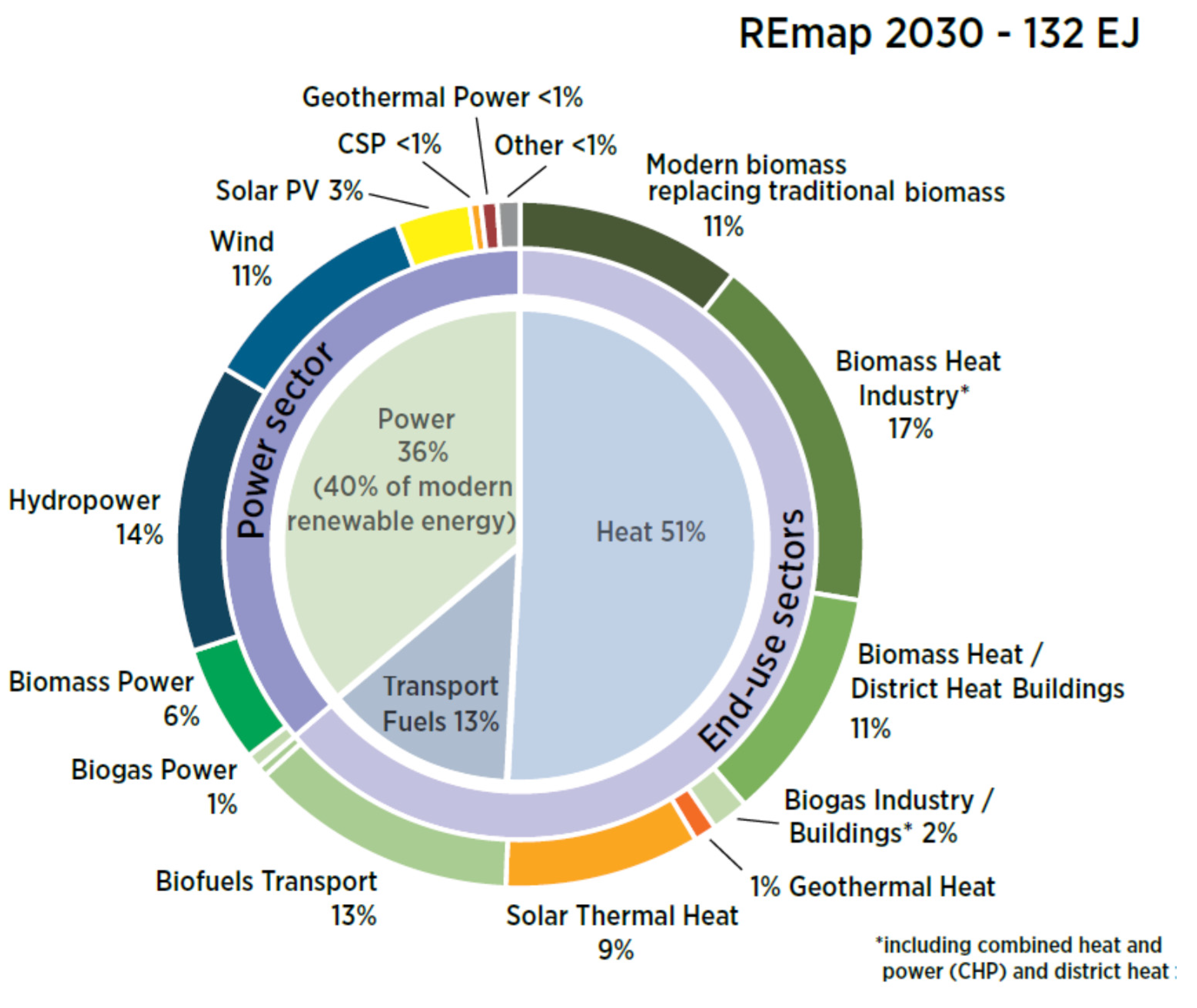

| End-use sectors: | 51.5 | 63.2 | 78.5 | 14.7 | 13.4 | 17.8 |

| Modern biomass replacing traditional biomass | 12.2 | 3.0 | ||||

| Traditional biomass | 31.9 | 28.8 | 0 | 9.1 | 6.5 | 0.0 |

| Biomass heat industry | 7.3 | 12.1 | 20.7 | 2.1 | 2.7 | 4.7 |

| Biomass heat/DH buildings | 7.6 | 8.4 | 13.5 | 2.2 | 1.9 | 3.1 |

| Biogas industry/buildings | 0.4 | 1.9 | 2.1 | 0.1 | 0.4 | 0.5 |

| Geothermal heat | 0.2 | 0.9 | 1.3 | 0.1 | 0.2 | 0.3 |

| Solar thermal heat | 1.4 | 4.7 | 11.2 | 0.4 | 1.1 | 2.5 |

| Biofuels transport | 2.6 | 6.5 | 16.2 | 0.7 | 1.5 | 3.5 |

| Electromobility (using renewable electricity) | 1.3 | 0.3 | ||||

| Power sector: | 11.5 | 29.8 | 53 | 3.3 | 6.7 | 12.0 |

| Biogas power | 0.1 | 0.5 | 1.0 | 0 | 0.1 | 0.2 |

| Biomass power | 0.9 | 3.7 | 7.1 | 0.3 | 0.8 | 1.6 |

| Hydroelectricity | 9.3 | 16.7 | 18.2 | 2.7 | 3.8 | 4.1 |

| Wind | 0.9 | 5.6 | 17.0 | 0.3 | 1.3 | 3.9 |

| Solar PV | 0.1 | 1.9 | 5.8 | 0 | 0.4 | 1.3 |

| CSP | 0 | 0.5 | 0.9 | 0 | 0.1 | 0.2 |

| Geothermal power | 0.1 | 0.9 | 1.7 | 0 | 0.2 | 0.4 |

| Other | 1.3 | 0.3 | ||||

| Total | 62.9 | 93.0 | 131.5 | 18.0 | 21.0 | 29.9 |

3.3. Findings at Sector-Level

| Sector | 2010 | Reference Case 2030 | REmap 2030 | RE use in REmap 2030 | |||||

|---|---|---|---|---|---|---|---|---|---|

| Modern biomass | Other renewables | Total (modern) | |||||||

| Replacing traditional biomass | Other | ||||||||

| (%) | (%) | (%) | (EJ/year) | (EJ/year) | (EJ/year) | (EJ/year) | |||

| Industry | Heat | 8 | 9 | 19 | N/A | 21 | 3 | 24 | |

| Heat, electricity and DH | 11 | 15 | 26 | 26 | 25 | 51 | |||

| Buildings | Heat | 12 | 16 | 35 | 12 | 14 | 9 | 35 | |

| Heat, electricity and DH | 14 | 20 | 38 | 18 | 35 | 65 | |||

| Transport | Fuels | 3 | 5 | 15 | N/A | 16 | 0 | 16 | |

| Fuels and electricity | 3 | 6 | 17 | 16 | 0 | 16 | |||

| Electricity generation | 18 | 26 | 44 | N/A | 10 | 52 | 62 | ||

| DH generation | 4 | 14 | 27 | N/A | 2 | 0.2 | 2.2 | ||

| Total | 18 | 21 | 30 | 12 | 60 | 60 | 132 | ||

3.4. REmap 2030 Costs

| Sector | Substitution costs | REmap Options | Total system costs |

|---|---|---|---|

| (USD/GJ) | (EJ/year) | (USD billion/year) | |

| Industry | 5 | 12.7 | 63.7 |

| Buildings | 1.6 | 10.2 | 16.3 |

| Transport | −4.1 | 12.0 | −49.2 |

| Power generation | 5.7 | 15.5 | 88.4 |

| DH | 5.3 | 2.5 | 13.2 |

| Total 1 | 2.5 | 53.0 | 133.0 |

| Total after accounting for externalities 1 | −13.8–−2.3 | −123.0–−738.0 | |

| With human health only 2 | −2.6–0.6 | 31.2–−137.8 | |

| With CO2 emissions only 3 | −8.7–−0.4 | −21.2–−467.1 |

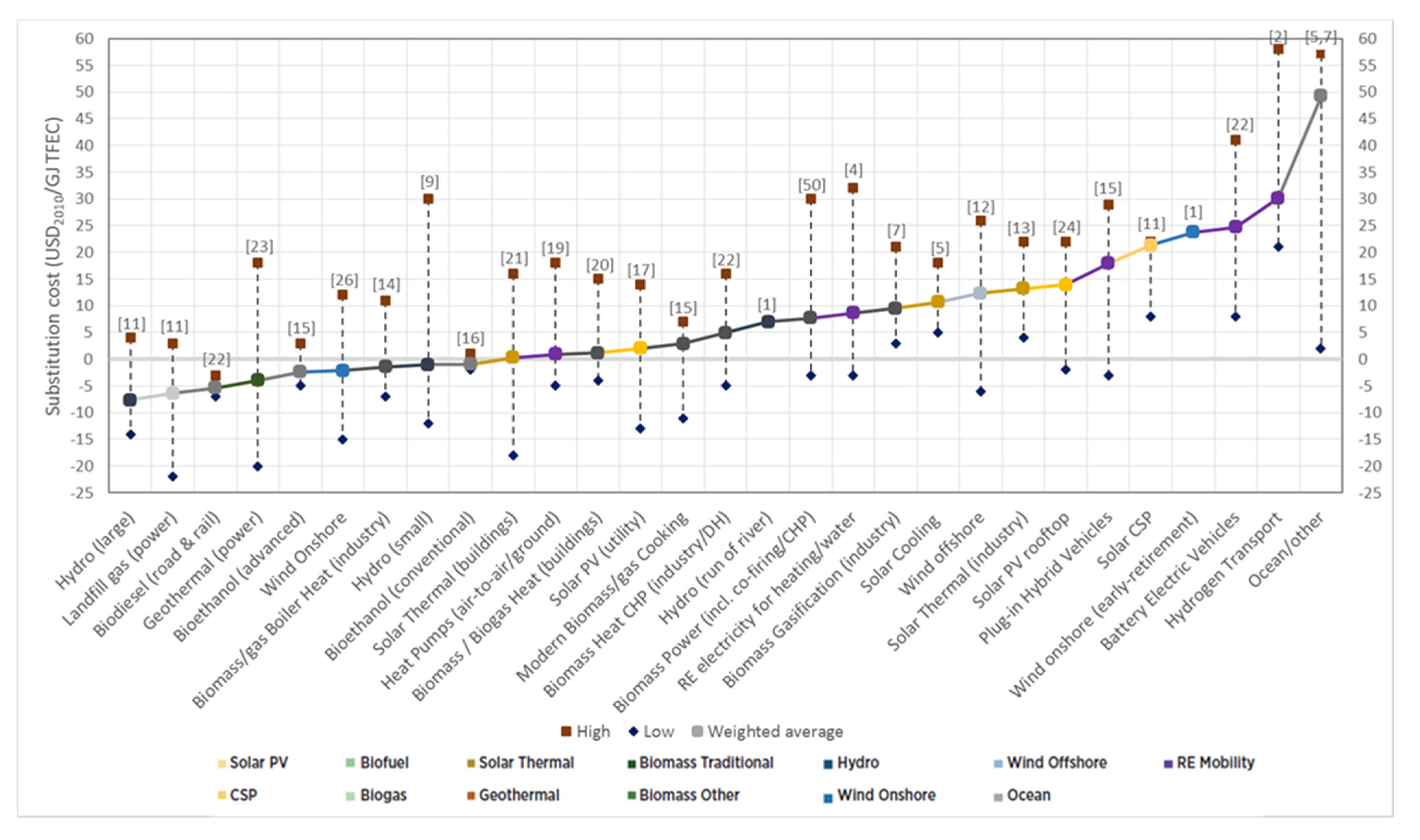

3.5. REmap 2030 Action Areas

| Technology | Units | 2012 | REmap 2030 | CAGR (Indicator 1) | Penetration level (Indicator 2) | Action areas for deployment and system change (for Indicators 1 and 2) | 2030 substitution costs (Indicator 3) | Action areas for cost-competitiveness (for Indicator 3) | ||

|---|---|---|---|---|---|---|---|---|---|---|

| 2000–2012 | 2012-REmap 2030 | 2012 | REmap 2030 | |||||||

| (%/year) | (%/year) | (%) | (%) | (USD/GJ) | ||||||

| Power generation technologies 1: | ||||||||||

| Hydropower (excl. pumped storage) | [GW] | 1004 | 1,601 | 3 | 3 | 18.2 | 17.1 | Retrofitting dams with turbines | −7.6 | - |

| Focus on micro/small hydropower | - | |||||||||

| Pumped hydro | [GW] | 150 | 325 | N/A | 4 | 2.7 | 3.5 | Recognize its role as energy storage technology | N/A | - |

| Wind onshore | [GW] | 283 | 1266 | 26 | 9 | 5.1 | 13.5 | Improved wind forecasting; grid integration | −2.6 | Higher turbine efficiency |

| Wind offshore | [GW] | 6 | 240 | N/A | 23 | 0.1 | 2.6 | Balance between high potential wind resource area and generation costs; shortages of skilled labor force and more learning experiences | 12.3 | Balance between high potential wind resource area and generation costs; minimize material requirements (e.g., copper, steel); increase component recycling |

| Solar PV | [GW] | 100 | 1,180 | 23 | 15 | 1.8 | 12.6 | - | 2 (utility), 13.9 (rooftop) | Higher efficiency with focus on solar cell and material technologies |

| CSP | [GW] | 3 | 83 | 8 | 22 | 0.1 | 0.9 | High temperature steam for advanced turbines; combination with desalination; energy storage | 21.3 | Development of alternative heat transfer fluids; new receivers, reflector and material designs |

| Power generation technologies 1: | ||||||||||

| Biomass power | [GW] | 83 | 383 | 7 | 9 | 1.5 | 4.1 | Utilize CHP potential; convert coal power plants to biomass plants in countries where coal plants are being retired, as well as those with large and/or young coal power plant capacity | 7.7 | - |

| Geothermal | [GW] | 11 | 64 | 3 | 10 | 0.2 | 0.7 | Reach higher maturity level by modularizing/off-site assembly of plant components for high altitudes; novel drilling for high-temperature well operation | −3.9 | Exhausted steam condensation; explore feasible applications of condensation heat |

| Ocean | [GW] | 1 | 9 | - | 17 | 0.0 | 0.1 | Resolve construction issues; assessment of environmental impacts | 13 | Consider combined generation with air-conditioning/fresh water production; hybrid options |

| Biomass: | ||||||||||

| Traditional | [EJ/year] | 27 | 12 | 0 | -5 | 8.0 | 2.7 | Creating a market for affordable and reliable modern cooking equipment; efficient technologies utilizing a range of fuels | N/A | Develop and deploy advanced biofuel technologies; improving quality and energy density of solid biomass products; higher efficiency conversion technologies to final products |

| Advanced cooking | [EJ/year] | 1 | 4 | 10 | 8 | 0.3 | 0.9 | 3 | ||

| Industrial/DH CHP | [EJ/year] | 3 | 14 | 10 | 13 | 0.9 | 3.1 | Consider biomass-fired process heat technologies in new plants; prioritize plants which has better access to biomass | 5–10 | |

| Industry boilers | [EJ/year] | 4 | 7 | 0 | 0 | 1.2 | 1.6 | |||

| Wood pellets | [EJ/year] | 1 | 3 | 49 | 6 | 0.3 | 0.7 | - | 1–2 | |

| Chips, logs | [EJ/year] | 5 | 6 | 6 | 1 | 1.5 | 1.3 | |||

| Liquid biofuels (incl. biogas) | [bln ltrs/year] | 105 | 650 | 16 | 11 | 0.7 | 3.4 | Phase out the use of conventional feedstocks | −5 (conventional)–−1 (advanced) | |

| Total demand 2 | [EJ/year] | 51 | 108 | 1 | 4 | 10.6 | 17.1 | Feedstock collection; sustainability issues; international trade; infrastructure; resource efficiency | N/A | |

| Non-biomass renewable heat: | ||||||||||

| Total solar thermal | [mln m2] | 383 | 4,029 | 9 | 14 | 0.4 | 2.5 | High temperature process heat in industry; modifying existing processes for retrofitting | N/A | Consider when new capacity is being built |

| Share in buildings 3 | [%] | 99 | 67 | - | 11 | 1.2 | 6.2 | 0.3 | ||

| Share in industry 3 | [%] | 1 | 33 | - | 43 | 0.0 | 1.6 | 13.2 | ||

| Geothermal heat | [EJ/year] | 1 | 1 | 10 | 4 | 0.4 | 2.5 | Long term delivery for low/high heat | 2 | Optimization of heat extraction |

| Electrification: | ||||||||||

| Heat Pump | [GW] | 50 | 474 | N/A | 13 | - | - | Utilize high temperature options in industry where technology exists; better information on its benefits | 1 | Improve coefficient of performance |

| Battery storage 4 | [GW] | 2 | 150 | N/A | 27 | 0.5 | 5.6 | Identify key areas it can play a role next to interconnectors, DSM, dispatchable, e.g., islands and off-grid, residential PV, high variable RE shares | N/A | - |

| BEV, PHEV 5 | [mln] | 0 | 160 | N/A | 46 | 0 | 10 | Overcome maximum range and speed limitations; develop enabling infrastructure; fast chargers and higher capacity batteries | 20–25 | - |

4. Discussion of Results and Indicators

5. Strength and Limitations of the REmap Methodology

- (i)

- We compiled the national energy plans originating from countries to develop the Reference Case into comparable format. However, background assumptions on drivers for population growth and economic development as well as the ambition level of target setting within the plans vary across countries, thereby representing different scenario families. For countries where national plans were unavailable or availability was limited to few sectors only, we used data from other studies to fill the gaps. Similarly, this may add uncertainty due to lack of consistency across data sources. Although the aim of this study is not to develop detailed energy scenarios for countries, background assumptions in national energy plans of countries need to be harmonized further and consistency should be improved before aggregation.

- (ii)

- For each country, the Reference Case includes current policies related to energy efficiency and RE. It is straightforward to quantify the extent RE policies contribute to 2030 TFEC at sector level since RE policies often have targets based on generation, capacity or RE share. Given energy consumption is aggregated at sector level, it is not possible to monitor energy efficiency progress in the absence of physical activity indicators (e.g., ton-km freight transported per year) and specific energy consumption data in both 2010 and 2030. To the extent possible, such data also needs to be available at country level in addition to national plans. This is essential to understand the nexus between energy efficiency and RE since as shown in this study the synergies between them should be considered to double the global RE share.

- (iii)

- We developed the Reference Case starting with the 2010 base year of the SE4All objective and looked out to 2030. National plans are often prepared with data from a few years prior (see Annex) and therefore may not take into account the rapid developments in the RE sector. It is therefore likely that the RE share will reach the 2030 Reference Case estimates of 21% before that time. At country level, with the current progress in deployment of renewables, the US will exceed its Reference Case projections according to the Annual Energy Outlook 2014 within the next few years [49]. China is also exceeding its targets [50]. Therefore it is necessary to continuously update the Reference Case of the countries to take into account the latest developments because this determines the gap to a doubling of the global RE share.

- (iv)

- Depending on data availability, we followed different approaches to estimate the REmap Options of each country. If countries provided an accelerated RE projection (e.g., Germany), we took this as a basis to estimate the realizable potential of technologies. Otherwise, literature data and communication with the national experts were the basis of the assessment. Although we defined a number of criteria to determine the realizable potential (e.g., costs, age of capital stock, resource availability), the estimated potentials could differ on how the criteria are prioritized across countries. The link between the realizable potentials and the criteria for each country should be identified further and compared across countries with further analysis of cost-benefits of technologies, utilization of technical resource potentials, and retrofits of existing capacity versus new investments.

- (v)

- The analysis represents an assessment of a point in time and we did not estimate in detail the time period between 2010 and 2030, and any of the interactions, developments and dynamics across technologies and feedbacks in energy prices due to demand and supply changes (e.g., rebound effects). We rather assumed that all REmap Options are implemented in a single step by 2030. Furthermore, the costs of infrastructure were excluded from the analysis, which would raise the costs estimated in this analysis. Most variables in the assessment are exogenous without taking into account the potential effect in demand reduction due to the implementation of the REmap Options. While the cost-supply curve is static, the energy system in general—for instance, the process of meeting electricity or heat demand—is dynamic. For example, there are institutional barriers, or transaction costs along with technology costs. Incorporating these could change the ranking of technologies.

6. Conclusions

Acknowledgments

Conflicts of Interest

Abbreviations

| AD | Anaerobic digestion |

| CHP | Combined heat and power |

| CO2 | Carbon dioxide |

| CSP | Concentrated solar power |

| DH | District heat |

| EU | European Union |

| EV | Electrical vehicle |

| FF | Fossil fuel |

| ICE | Internal combustion engines |

| IRENA | International Renewable Energy Agency |

| LPG | Liquified Petroleum Gas |

| NOx | Mono-nitrogen oxide |

| NREAP | National Renwable Energy Action Plans |

| OECD | Organisation for Economic Co-operation and Development |

| O&M | Operations and Maintenance |

| OTEC | Ocean thermal energy conversion |

| PM2.5 | Particulate Matter (ø 2.5 µm) |

| PT | Parabolic Trough |

| PV | Photovoltaic |

| R&D | Research and development |

| RE | Renewable energy |

| REmap | Renewable Energy Roadmap |

| SE4All | Sustainable Energy for All |

| SO2 | Sulphur dioxide |

| TFEC | Total final energy consumption |

| UAE | United Arab Emirates |

| UK | United Kingdom |

| US | United States |

Annex

| Country | Main source for Reference Case | Time frame | Sectors covered in cited sources |

|---|---|---|---|

| Australia | [51] | 2012–2050 | TFEC |

| Brazil | [52,53] | 2005–2030 | TFEC |

| Canada | [54] | 2010–2035 | TFEC |

| China | [29] | 2010–2035 | TFEC |

| Denmark | [55] | 2012–2025 | TFEC |

| Ecuador | [29] | 2010–2035 | TFEC |

| France | [33,56] | 2010–2030 | TFEC |

| Germany | [33,57] | 2010–2050 | TFEC |

| India | [29] | 2010–2035 | TFEC |

| Indonesia | [58] | 2010–2030 | TFEC |

| Italy | [33,59] | 2010–2050 | TFEC |

| Japan | [29] | 2010–2035 | TFEC |

| Malaysia | [60] | 2010–2035 | TFEC |

| Mexico | [61]; IRENA analysis | 2011–2025 | Power sector |

| Morocco | [62] | 2012–2030 | TFEC |

| Nigeria | IRENA analysis | 2010–2030 | TFEC |

| Russia | [29] | 2010–2035 | TFEC |

| Saudi Arabia | [29,63] | 2010–2035 | TFEC; Power sector |

| South Africa | [64]; IRENA analysis | 2010–2030 | Power sector |

| South Korea | [65] | 2010–2030 | TFEC |

| Tonga | IRENA analysis | 2010–2030 | TFEC |

| Turkey | [66]; IRENA analysis | 2012–2021 | Power sector |

| Ukraine | [67,68] | 2009–2030 | TFEC |

| UAE | [69] | 2010–2030 | TFEC |

| UK | [70,71,72] | 2010–2050 | TFEC |

| US | [73] | 2013–2040 | TFEC |

| Crude oil | (USD/GJ) | 20 | |

|---|---|---|---|

| Coal 1 | (USD/GJ) | 2–5 | |

| Natural gas (household) 1 | (USD/GJ) | 15–22 | |

| Natural gas (industry) 1 | (USD/GJ) | 8–11 | |

| Electricity (household) 2 | (USD/kWh) | 0.02–0.38 | |

| Electricity (industry) 2 | (USD/kWh) | 0.04–0.20 | |

| Petroleum products | (USD/GJ) | 16.4 | |

| Diesel and Gasoline | (USD/GJ) | 30 | |

| Biodiesel | (USD/GJ) | 23 | |

| Conventional ethanol | (USD/GJ) | 27 | |

| Advanced ethanol | (USD/GJ) | 25 | |

| Primary biomass 3 | (USD/GJ) | 8–30 | |

| Biomass residues and waste 3 | (USD/GJ) | 1–15 | |

| Traditional biomass | (USD/GJ) | 3 | |

| Nuclear fuel | (USD/GJ) | 0.2 |

| Renewable energy technologies | ||||||

|---|---|---|---|---|---|---|

| Capacity factor | Lifetime | Reference capacity or annual mileage | Overnight capital cost | O&M costs | Conversion efficiency | |

| INDUSTRY SECTOR | (%) | (years) | (kW) | (USD/kW) | (USD/kW/year) | (%) |

| Solar thermal | 10 | 25 | 500 | 655 | 9.8 | 100 |

| Geothermal | 55 | 42 | 100 | 1500 | 37.5 | 100 |

| Biomass boilers | 85 | 25 | 500 | 580 | 14.5 | 88 |

| BUILDINGS SECTOR | (%) | (years) | (kW) | (USD/kW) | (USD/kW/year) | (%) |

| Space heating: Geothermal heat pumps | 50 | 15 | 12 | 1500 | 37.5 | 350 |

| Space heating: Air-to-Air heat pumps | 50 | 15 | 12 | 780 | 19.5 | 350 |

| Water heating: Biomass | 30 | 15 | 20 | 600 | 15.0 | 80 |

| Water heating: Solar (thermosiphon) | 12 | 20 | 82 | 150 | 3.8 | 100 |

| Space heating: Biogas | 50 | 15 | 50 | 600 | 15.0 | 80 |

| Space heating: Pellet burners | 30 | 15 | 20 | 775 | 19.4 | 85 |

| Space Cooling: Solar | 12 | 20 | 5 | 1350 | 33.8 | 80 |

| Cooking biogas (from AD) | 10 | 25 | 9 | 39 | 1.0 | 48 |

| Cooking biomass (solid) | 10 | 20 | 5 | 15 | 0.4 | 30 |

| Cooking bioethanol | 10 | 20 | 5 | 10 | 0.3 | 50 |

| TRANSPORT SECTOR (passenger road vehicles) | (%) | (years) | (passenger-km/year/vehicle) | (USD/vehicle) | (USD/vehicle/year) | (MJ/passenger-km) |

| Conventional bioethanol | N/A | 12 | 15,000 | 28,000 | 2,800 | 1.06 |

| Conventional bioethanol | N/A | 12 | 15,000 | 28,000 | 2,800 | 1.06 |

| Biodiesel | N/A | 12 | 15,000 | 30,000 | 3,000 | 0.98 |

| Plug-in hybrid | N/A | 12 | 15,000 | 30,000 | 3,000 | 0.98 |

| Battery electric | N/A | 12 | 15,000 | 32,000 | 2,880 | 0.47 |

| POWER SECTOR | (%) | (years) | (kW) | (USD/kW) | (USD/kW/year) | (%) |

| Hydro (Small) | 50 | 40 | 0.05 | 2800 | 56.0 | 100 |

| Hydro (Large) | 50 | 60 | 100 | 1500 | 30.0 | 100 |

| Wind onshore | 38 | 30 | 100 | 1500 | 60.0 | 100 |

| Wind offshore | 48 | 30 | 50 | 2870 | 157.9 | 100 |

| Solar PV (Rooftop) | 16 | 30 | 0.1 | 1400 | 14.0 | 100 |

| Solar PV (Utility) | 18 | 30 | 1 | 1000 | 10.0 | 100 |

| POWER SECTOR | (%) | (years) | (kW) | (USD/kW) | (USD/kW/year) | (%) |

| Solar CSP PT no storage | 35 | 35 | 50 | 3500 | 35.0 | 100 |

| Solar CSP PT storage | 50 | 35 | 50 | 4500 | 135.0 | 100 |

| Biomass power | 80 | 25 | 50 | 2750 | 68.8 | 38 |

| Landfill gas power | 80 | 25 | 0.5 | 1800 | 45.0 | 32 |

| Geothermal | 80 | 50 | 25 | 3100 | 124.0 | 10 |

| Tide, wave, ocean | 50 | 25 | 5 | 3350 | 67.0 | 100 |

| Conventional fuel technologies | ||||||

| Capacity factor | Lifetime | Reference capacity or annual mileage | Overnight capital cost | O&M costs | Conversion efficiency | |

| INDUSTRY SECTOR | (%) | (years) | (kW) | (USD/kW) | (USD/kW/year) | (%) |

| Coal | 85 | 25 | 2000 | 300 | 7.5 | 90 |

| Petroleum products | 85 | 25 | 2000 | 200 | 5.0 | 85 |

| Natural gas | 85 | 25 | 2000 | 100 | 2.5 | 95 |

| BUILDINGS SECTOR | (%) | (years) | (kW) | (USD/kW) | (USD/kW/year) | (%) |

| Space heating: coal | 85 | 15 | 20 | 175 | 6.1 | 90 |

| Space heating: petroleum products | 85 | 15 | 20 | 175 | 6.1 | 85 |

| Space heating: natural gas | 85 | 15 | 20 | 162 | 5.7 | 95 |

| Water heating: natural gas | 80 | 15 | 20 | 150 | 5.3 | 95 |

| Space & Water heating: traditional biomass | 85 | 25 | 2,000 | 100 | 2.5 | 50 |

| Water heating: electricity | 10 | 10 | 5 | 150 | 3.8 | 85 |

| Space cooling: electricity | 10 | 10 | 10 | 150 | 3.8 | 250 |

| Cooking LPG/kerosene | 10 | 20 | 5 | 10 | 0.3 | 50 |

| Cooking natural gas | 10 | 25 | 9 | 39 | 1.0 | 48 |

| Cooking electricity | 10 | 10 | 7 | 24 | 0.6 | 75 |

| Cooking traditional biomass | 10 | 3 | 5 | 10 | 0.25 | 10 |

| TRANSPORT SECTOR (passenger road vehicles) | (%) | (years) | (passenger-km/year/vehicle) | (USD/vehicle) | (USD/vehicle/year) | (MJ/passenger-km) |

| Petroleum products | N/A | 12 | 15,000 | 28,000 | 2,800 | 1.06 |

| POWER SECTOR | (%) | (years) | (kW) | (USD/kW) | (USD/kW/year) | (%) |

| Coal (type 1) | 80 | 60 | 650 | 1300 | 52.0 | 30 |

| Natural gas | 80 | 30 | 650 | 1000 | 40.0 | 55 |

| Oil | 30 | 50 | 400 | 1200 | 18.0 | 40 |

| Nuclear (type 1) | 84 | 60 | 1200 | 5500 | 137.5 | 33 |

| Diesel (gen-set) | 40 | 20 | 0 | 1500 | 37.5 | 42 |

| Coal (type 2) | 80 | 60 | 650 | 3000 | 120.0 | 42 |

| Nuclear (type 2) | 84 | 60 | 1200 | 7500 | 187.5 | 33 |

References

- IEA (International Energy Agency). World Energy Balances; OECD/IEA: Paris, France, 2013. [Google Scholar]

- IPCC (Intergovernmental Panel on Climate Change). Renewable Energy Sources and Climate Change Mitigation; Prepared by Working Group III of the Intergovernmental Panel on Climate Change; Edenhofer, O., Pichs-Madruga, R., Sokona, Y., Seyboth, K., Matschoss, P., Kadner, S., Zwickel, T., Eickemeier, P., Hansen, G., Schlömer, S., et al., Eds.; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2011. [Google Scholar]

- GEA (Global Energy Assessment). Global Energy Assessment—Toward a Sustainable Future; Cambridge University Press: Cambridge, UK; New York, NY, USA; International Institute for Applied Systems Analysis: Laxenburg, Austria, 2012; Available online: http://www.globalenergyassessment.org/ (accessed on 10 September 2014).

- US EIA (United States Energy Information Administration). International Energy Outlook 2013; U.S. Energy Information Administration, U.S. Department of Energy: Washington, DC, USA, 2013. Available online: http://www.eia.gov/forecasts/ieo/ (accessed on 10 September 2014).

- IPCC. Technical Summary; Prepared by Working Group III of the Intergovernmental Panel on Climate Change Assessment Report 5. Final Draft; IPCC: Geneva, Switzerland, 2014; Available online: http://report.mitigation2014.org/drafts/final-draft-postplenary/ipcc_wg3_ar5_final-draft_postplenary_technical-summary.pdf (accessed on 10 September 2014).

- IEA. Technology Roadmap: Bioenergy for Heat and Power; OECD/IEA: Paris, France, 2012; Available online: https://www.iea.org/publications/freepublications/publication/2012_Bioenergy_Roadmap_2nd_Edition_WEB.pdf (accessed on 10 September 2014).

- Lim, S.S.; Vos, T.; Flaxman, A.D.; Danaei, G.; Shibuya, K.; Adair-Rohani, H.; Amann, M.; Anderson, H.R.; Andrews, K.G.; Aryee, M.; et al. A comparative risk assessment of burden of disease and injury attributable to 67 risk factors and risk factor clusters in 21 regions, 1990–2010: A systematic analysis for the Global Burden of Disease Study 2010. Lancet 2013, 380, 2224–2260. [Google Scholar] [CrossRef]

- IEA. World Energy Outlook 2013; OECD/IEA: Paris, France, 2013; Available online: http://www.worldenergyoutlook.org/publications/weo-2013/ (accessed on 10 September 2014).

- SE4All. Sustainable Energy for All; United Nations, Vienna International Centre: Vienna, Austria, 2014; Available online: www.se4all.org (accessed on 10 September 2014).

- UN (United Nations). United Nations General Assembly Declares 2014–2024. Decade of Sustainable Energy for All; United Nations: New York, NY, USA; Geneva, Switzerland, 2012; Available online: http://www.un.org/News/Press/docs/2012/ga11333.doc.htm (accessed on 21 December 2012).

- Banerjee, S.G.; Elizondo Azuela, G.; Bhatia, M.; Bushueva, I.; Inon, J.G.; Jaques Goldenberg, I.; Portale, E.; Sarkar, A. Global Tracking Framework; Volume 3 of Global Tracking Framework, Sustainable Energy for All; The World Bank: Washington, DC, USA, 2013; Available online: http://documents.worldbank.org/curated/en/2013/05/17765643/global-tracking-framework-vol-3-3-main-report (accessed on 10 September 2014).

- IRENA (International Renewable Energy Agency). REmap 2030: A Renewable Energy Roadmap; IRENA: Abu Dhabi, UAE, 2014; Available online: http://www.irena.org/remap/REmap_Report_June_2014.pdf (accessed on 10 September 2014).

- Elliston, B.; MacGill, I.; Diesendorf, M. Least cost 100% renewable electricity scenarios in the Australian National Electricity Market. Energy Policy 2013, 59, 270–282. [Google Scholar] [CrossRef]

- Mileva, A.; Nelson, J.H.; Johnston, J.; Kammen, D.M. SunShot solar power reduces costs and uncertainty in future low carbon electricity systems. Environ. Sci. Technol. 2013, 47, 9053–9060. [Google Scholar] [CrossRef] [PubMed]

- Taliotis, C.; Miketa, A.; Howells, M.; Hermann, S.; Welsch, M.; Broad, O.; Rogner, H.; Bazilian, M.; Gielen, D. An indicative assessment of investment opportunities in the African electricity supply sector. J. Energy South. Afr. 2014, 25, 2–12. [Google Scholar]

- Demirbas, A. Global renewable energy projections. Energy Sources Part B Econ. Plan. Policy 2009, 4, 212–224. [Google Scholar] [CrossRef]

- Foyn, T.H.S.; Karlsson, K.; Balyk, O.; Grohnheit, P.E. A global renewable energy system: A modelling exercise in ETSAP/TIAM. Appl. Energy 2011, 88, 526–534. [Google Scholar] [CrossRef]

- Jacobson, M.Z.; Delucchi, M.A. Providing all global energy with wind, water, and solar power, Part I: Technologies, energy resources, quantities and areas of infrastructure, and materials. Energy Policy 2011, 39, 1154–1169. [Google Scholar] [CrossRef]

- Krey, V.; Clarke, L. Role of renewable energy in climate mitigation: A synthesis of recent scenarios. Clim. Policy 2011, 11, 1131–1158. [Google Scholar] [CrossRef]

- Luderer, G.; Krey, V.; Calvin, K.; Merrick, J.; Mima, S.; Pietzcker, R.; van Vliet, J.; Wada, K. The role of renewable energy in climate stabilization: results from the EMF27 scenarios. Clim. Change 2014, 123, 427–441. [Google Scholar] [CrossRef]

- Deng, Y.Y.; Blok, K.; van der Leun, K. Transition to a fully sustainable global energy system. Energy Strategy Rev. 2012, 1, 109–121. [Google Scholar] [CrossRef]

- Teske, S.; Preffer, T.; Simon, S.; Naegler, T.; Graus, W.; Lins, C. Energy Revolution—A sustainable world energy outlook. Energy Effic. 2011, 4, 409–433. [Google Scholar] [CrossRef]

- Taibi, E.; Gielen, D.; Bazilian, M. The potential for renewable energy in industrial applications. Renew. Sustain. Energy Rev. 2012, 16, 735–744. [Google Scholar] [CrossRef]

- Saygin, D.; Gielen, D.J.; Draeck, M.; Worrell, E.; Patel, M.K. Assessment of the technical and economic potentials of biomass use for the production of steam, chemicals and polymers. Renew. Sustain. Energy Rev. 2014, 40, 1153–1167. [Google Scholar] [CrossRef]

- Liaquat, A.M.; Kalam, M.A.; Masjuki, H.H.; Jayed, M.H. Potential emissions reductions in road transport sector using biofuel in developing countries. Atmos. Environ. 2010, 44, 3869–3877. [Google Scholar] [CrossRef]

- Juul, N.; Meibom, M. Road transport and power system scenarios for Northern Europe in 2030. Appl. Energy 2012, 92, 573–582. [Google Scholar] [CrossRef]

- Connolly, D.; Mathiesen, B.V.; Ridjan, I. A comparsion between renewable transport fuels that can supplement or replace biofuels in a 100% renewable energy system. Energy 2014, 73, 110–125. [Google Scholar] [CrossRef]

- Brown, J.; Hendry, C. Public demonstration projects and field trials: Accelerating commercialisation of sustainable technology in solar photovoltaics. Energy Policy 2009, 37, 2560–2573. [Google Scholar] [CrossRef]

- IEA. World Energy Outlook 2012; OECD/IEA: Paris, France, 2012; Available online: http://www.worldenergyoutlook.org/publications/weo-2012/ (accessed on 10 September 2014).

- IRENA. Global Bioenergy Supply and Demand Projections. A Working Paper for REmap 2030; IRENA: Abu, Dhabi, UAE, 2014; Available online: http://www.irena.org/remap/IRENA_REmap_2030_Biomass_paper_2014.pdf (accessed on 10 September 2014).

- Hirth, L.; Ueckerdt, F.; Edenhofer, O. Integration costs revisited—An economic framework for wind and solar variability. Renew. Energy 2015, 74, 925–939. [Google Scholar] [CrossRef]

- Delucchi, M.A.; Jacobson, M.Z. Providing all global energy with wind, and solar power, Part II: Reliability, system and transmission costs, and policies. Energy Policy 2011, 39, 1170–1190. [Google Scholar] [CrossRef]

- EC (European Commission). National Renewable Energy Action Plans; European Commission: Brussels, Belgium, 2010; Available online: http://ec.europa.eu/energy/renewables/action_plan_en.htm (accessed on 10 September 2014).

- WB (The World Bank). Gross Fixed Capital Formation; The World Bank: Washington, DC, USA, 2014; Available online: http://data.worldbank.org/indicator/NE.GDI.FTOT.CD/countries?display=graph (accessed on 10 September 2014).

- FSFM (Frankfurt School of Finance & Management). Global Trends in Renewable Energy Investment 2013; UNEP Collaborating Centre Frankfurt School of Finance & Management GmbH: Frankfurt, Germany, 2013. [Google Scholar]

- CSIRO (Commonwealth Scientific and Industrial Research Organization). Unlocking Australia’s Energy Potential; Commonwealth Scientific and Industrial Research Organisation: Clayton South, VIC, Australia, 2011; Available online: http://www.csiro.au/~/media/CSIROau/Divisions/CSIRO%20Energy%20Technology/Aust_energy_potential_CET_publcation%20Standard.pdf (accessed on 10 September 2014).

- Jenkins, J.; Mansur, S. Bridging the Clean Energy Valleys of Death; Breakthrough Institute: Oakland, CA, USA, 2011; Available online: http://thebreakthrough.org/blog/Valleys_of_Death.pdf (accessed on 10 September 2014).

- IRENA. Road transport: The cost of renewables solutions; IRENA: Abu Dhabi, UAE, 2013; Available online: http://costing.irena.org/media/2787/Road_Transport.pdf (accessed on 10 September 2014).

- ACORE (American Council on Renewable Energy). Input on Biofuel Pathways for U.S. Department of Energy, Bioenergy Technologies Office; American Council on Renewable Energy: Washington, DC, USA, 2014; Available online: http://www.acore.org/images/uploads/ACOREMemberCommentsDOERFIBiofuelPathways.pdf (accessed on 10 September 2014).

- Auerswald, P.E.; Branscomb, M.L. Valleys of Death and Darwinian Seas: Financing the Invention to Innovation Transition in the United States. J. Technol. Transf. 2003, 28, 227–239. [Google Scholar] [CrossRef]

- Nemet, F.G. Demand-pull, technology-push, and government-led incentives for non-incremental technical change. Res. Policy 2009, 38, 700–709. [Google Scholar] [CrossRef]

- Jacobsson, S.; Johnson, A. The diffusion of renewable energy technology: An analytical framework and key issues for research. Energy Policy 2000, 28, 625–640. [Google Scholar] [CrossRef]

- Anadón, L.D.; Bosetti, V.; Bunn, M.; Catenacci, M.; Lee, A. Expert Judgements about RD&D and the future of nuclear energy. Environ. Sci. Technol. 2012, 46, 11497–11504. [Google Scholar] [PubMed]

- Loftus, P.J.; Cohen, A.M.; Long, J.C.S.; Jenkins, J.D. A critical review of global decarbonization scenarios: What do they really tell us about feasibility? WIREs Clim. Change 2014, 324. [Google Scholar] [CrossRef]

- WWF; Ecofys; OMA. The Energy Report: 100 Percent Renewable Energy by 2050; World Wide Fund for Nature: Gland, Switzerland, 2011; Available online: http://assets.panda.org/downloads/the_energy_report_lowres_111110.pdf (accessed on 10 September 2014).

- Greenpeace; EREC; GWEC. Energy Revolution: A Sustainable World Energy Outlook 2050; Greenpeace International, European Renewable Energy Council, Global Wind Energy Council: Amsterdam/Brussels, the Netherlands/Belgium, 2012; Available online: www.greenpeace.org/international/Global/international/publications/climate/2012/Energy%20Revolution%202012/ER2012.pdf (accessed on 10 September 2014).

- ExxonMobil. The Outlook for Energy: A View to 2040; ExxonMobil: Irving, TX, USA, 2014. [Google Scholar]

- IEA. World Energy Outlook 2014; OECD/IEA: Paris, France, 2014. [Google Scholar]

- US EIA. Annual Energy Outlook 2014; U.S. Energy Information Administration, U.S. Department of Energy: Washington, DC, USA, 2014. Available online: http://www.eia.gov/forecasts/aeo/ (accessed on 10 September 2014).

- IRENA. Renewable Energy Prospects: China, REmap 2030 Analysis; IRENA: Abu, Dhabi, UAE, 2014; Available online: http://www.irena.org/remap/IRENA_REmap_China_report_2014.pdf (accessed on 10 September 2014).

- BREE (Bureau of Resources and Energy Economics). Australian Energy Projections; Bureau of Resources and Energy Economics: Canberra, Australia, 2012. Available online: http://www.bree.gov.au/sites/bree.gov.au/files/files//publications/aep/australian-energy-projections-to-2050.pdf (accessed on 10 September 2014).

- EME (Ministerio de Minas e Energia, Brasilisa). Plano Decenal de Expansao de Energia 2021; Ministerio de Minas e Energia: Brasilisa, Brazil, 2007. Available online: http://www.epe.gov.br/PDEE/20130326_1.pdf (accessed on 10 September 2014).

- EME. Plano Nacional de Energia 2030; Ministerio de Minas e Energia: Brasilisa, Brazil, 2012. Available online: http://www.epe.gov.br/PNE/20080512_2.pdf (accessed on 10 September 2014).

- NEB (National Energy Board). Canada’s Energy Future: Energy Supply and Demand Projections to 2035; National Energy Board: Calgary, AB, Canada, 2011; Available online: http://www.neb-one.gc.ca/clf-nsi/archives/rnrgynfmtn/nrgyrprt/nrgyftr/2011/nrgsppldmndprjctn2035-eng.pdf (accessed on 10 September 2014).

- DEA (Danish Energy Agency). Danish Energy Outlook; Danish Energy Agency: Copenhagen; Available online: http://www.ens.dk/sites/ens.dk/files/dokumenter/publikationer/downloads/danish_energy_outlook_2011.pdf (accessed on 10 September 2014).

- DGEC (Direction Generale de l’energie et de Climat). Synthese. Scenarios prospectifs Energie—Climat—Air a Horizon 2030; Direction Generale de l’energie et de Climat: Paris, France, 2011; Available online: http://www.developpement-durable.gouv.fr/IMG/pdf/11–0362_5A_ET_note_synthese_sc_pros_v3.pdf (accessed on 10 September 2014).

- DLR/Fraunhofer IWES/IFNE. Langfristszenarien und Strategien fuer den Ausbau der erneuerbaren Energien in Deutschland bei Beruecksichtigung der Entwicklung in Europa und global; DLR/Fraunhofer IWES/IFNE: Stuttgart/Kassel/Teltow, Germany, 2012; Available online: http://www.dlr.de/dlr/Portaldata/1/Resources/bilder/portal/portal_2012_1/leitstudie2011_bf.pdf (accessed on 29 March 2012).

- MEMR (Ministry of Energy and Mineral Resources). Indonesia Energy Outlook 2010; Ministry of Energy and Mineral Resources Republic Indonesia: Jakarta, Indonesia, 2012; Available online: http://www.esdm.go.id/publikasi/indonesia-energy-outlook/ringkasan-eksekutif/doc_download/1255-ringkasan-eksekutif-indonesia-energy-outlook-2010.html (accessed on 10 September 2014).

- MSE (Ministry of Economic Development). Strategia Energetica Nazionale: per un’energia pie Competitive e Sosteniblie; Ministry of Economic Development: Rome, Italy, 2013. Available online: http://www.sviluppoeconomico.gov.it/images/stories/normativa/20130314_Strategia_Energetica_Nazionale.pdf (accessed on 10 September 2014).

- APEC. Energy Demand and Supply Outlook, 5th ed.; APEC, IEEJ: Tokyo, Japan, 2013; Available online: http://publications.apec.org/publication-detail.php?pub_id=1389 (accessed on 10 September 2014).

- CFE (Comision Federal de Electricidad). Programa de Obras e Inversiones del Sector Electrico 2011–2025; Comision Federal de Electricidad: Distrito Federal, Mexico, 2013; Available online: http://aplicaciones.cfe.gob.mx/aplicaciones/otros/POISE2011_2025%20WEB.ZIP (accessed on 10 September 2014).

- MEMEE (Ministere de l’Energie, des Mines, de l’Eau et de l’Environment). Etude Prospective de la Demande D’energie a L’horizon 2030; Ministere de l’Energie, des Mines, de l’Eau et de l’Environment: Rabat, Morocco, 2013. Available online: http://www.mem.gov.ma/SitePages/GrandsChantiers/DOPPROSP203008–01–13.pdf (accessed on 10 September 2014).

- K.A. Care (King Abdullah City for Atomic and Renewable Energy). Saudi Arabia’s Renewable Energy Strategy and Solar Energy Deployment Roadmap; King Abdullah City for Atomic and Renewable Energy: Riyadh, Saudi Arabia, 2013; Available online: http://www.irena.org/DocumentDownloads/masdar/Abdulrahman%20Al%20Ghabban%20Presentation.pdf (accessed on 10 September 2014).

- SA DoE (Republic of South Africa, Department of Energy). Integrated Resource Plan for Electricity 2010–2030; Revision 2, Final report; Republic of South Africa, Department of Energy: Pretoria, South Africa, 2011. Available online: http://www.energy.gov.za/IRP/irp%20files/IRP2010_2030_Final_Report_20110325.pdf (accessed on 10 September 2014).

- KPX. Present & Future of NRE: The 3rd National NRE Basic Plan; Ministry of Trade, Industry and Energy: Sejong, Korea, 2011. [Google Scholar]

- TEIAS (Turkish Electric Transmission Company). Turkiye Elektrik Enerjisi 10 Yillik Uretim Kapasite Projeksiyonu (2012–2021); Turkish Electric Transmission Company: Ankara, Turkey, 2012. Available online: http://www.teias.gov.tr/YayinRapor/APK/projeksiyon/KAPASITEPROJEKSIYONU2012.pdf (accessed on 10 September 2014).

- SAEE (State Agency for Energy Efficiency and Energy Saving of Ukraine). National Renewable Energy Action Plan (NREAP) through 2020; Draft. State Agency for Energy Efficiency and Energy Saving of Ukraine: Kiev, Ukraine, 2012. Available online: http://saee.gov.ua/documents/NpdVE_eng.pdf (accessed on 10 September 2014).

- UNAS. vestment Requirements and Benefits Arising from Energy Efficiency and Renewable Energy Policies in Ukraine; UNAS: Kiev, Ukraine, 2013; Available online: http://www.iea-etsap.org/web/Workshop/Paris_Jun2013/1_4%20PodoletsDiachuk_TIMESUA.pdf (accessed on 17 June 2013).

- IRENA/MI. Renewable Energy Prospects: United Arab Emirates, REmap 2030 Analysis; IRENA/Masdar Institute: Abu Dhabi, UAE, 2015. [Google Scholar]

- DECC (Department of Energy & Climate Change). Pathways to 2050: Key Results; Department of Energy & Climate Change: London, UK, 2011. Available online: https://www.gov.uk/government/publications/pathways-to-2050-key-results (accessed on 11 May 2011).

- DECC. UK Renewable Energy Roadmap; Department of Energy & Climate Change: London, UK, 2011. Available online: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/48128/2167-uk-renewable-energy-roadmap.pdf (accessed on 10 September 2014).

- DECC. Updated energy and emissions: 2012; Department of Energy & Climate Change: London, UK, 2012. Available online: https://www.gov.uk/government/publications/2012-energy-and-emissions-projections (accessed on 15 October 2012).

- US EIA. Annual Energy Outlook 2013; U.S. Energy Information Administration, U.S. Department of Energy: Washington, DC, USA, 2013. Available online: http://www.eia.gov/forecasts/aeo/pdf/0383(2013).pdf (accessed on 10 September 2014).

© 2015 by International Renewable Energy Agency (IRENA); licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Saygin, D.; Kempener, R.; Wagner, N.; Ayuso, M.; Gielen, D. The Implications for Renewable Energy Innovation of Doubling the Share of Renewables in the Global Energy Mix between 2010 and 2030. Energies 2015, 8, 5828-5865. https://doi.org/10.3390/en8065828

Saygin D, Kempener R, Wagner N, Ayuso M, Gielen D. The Implications for Renewable Energy Innovation of Doubling the Share of Renewables in the Global Energy Mix between 2010 and 2030. Energies. 2015; 8(6):5828-5865. https://doi.org/10.3390/en8065828

Chicago/Turabian StyleSaygin, Deger, Ruud Kempener, Nicholas Wagner, Maria Ayuso, and Dolf Gielen. 2015. "The Implications for Renewable Energy Innovation of Doubling the Share of Renewables in the Global Energy Mix between 2010 and 2030" Energies 8, no. 6: 5828-5865. https://doi.org/10.3390/en8065828

APA StyleSaygin, D., Kempener, R., Wagner, N., Ayuso, M., & Gielen, D. (2015). The Implications for Renewable Energy Innovation of Doubling the Share of Renewables in the Global Energy Mix between 2010 and 2030. Energies, 8(6), 5828-5865. https://doi.org/10.3390/en8065828