1. Introduction

Annually, humans use a large amount of energy to sustain and improve the standard of living around the globe. For example, the world’s consumption of non-renewable fossil fuels such as coal, oil, and gas was over 10,000 million tonnes of oil equivalent (4.19 × 10

14 Joules) in 2007 [

1]. The imbalance between global energy resource availability, demand, and production poses a great challenge to decision-makers in the energy sector. Furthermore, the depletion of oil and gas reserves in developed countries coupled with rapidly increasing demand for energy in developing countries may create new threats to international energy security system in the future. Recent energy surveys reveal that it may take decades before renewable energy sources will be able to play a major part in stabilizing global energy markets [

2,

3,

4]. Although the consumption of renewable energy sources has grown significantly over the past decades, their contribution to meeting global primary energy demand in 2008 was only about 13%, which is far less than fossil fuels’ share of about 81% [

5]. Hence, while research and development initiatives focusing on renewable sources of energy are currently receiving increasing attention and financial support, fossil fuels are still the most essential element of the world energy portfolio [

6]. In particular, petroleum remains to be an important non-renewable energy resource and a key driver of economic systems in both developing and developed countries [

7].

If the historical trends of energy demand and consumption are projected into the future, fossil fuels may continue to dominate the energy market, and even an increase in the consumption of oil may be expected [

8]. However, strong sociopolitical will and economic incentives to implement stringent policies for mitigating the climate change by promoting the consumption of alternative energies can decrease the dominance of oil in the future global energy mix. Nonetheless, it should be recognized that there is no panacea for the global energy crisis as the widely proposed and advocated alternative sources of energy are not without drawbacks [

9]. For example, production of industrial bio-fuels requires allocation of considerable amounts of natural resources such as land and water, and may potentially impact food production and climate change in negative ways [

10,

11,

12,

13]. Likewise, wind energy and hydropower depend upon availability of suitable locations while solar energy is intermittent and, currently, expensive [

14,

15]. Moreover, the need for large capital investments and concerns about proper handling of radioactive waste detracts from the favorability of nuclear energy [

16]. Resolving these concerns is a precursor for a more balanced global energy mix.

Growing energy insecurity and climate change are two key concerns at the heart of the International Energy Agency’s World Energy Outlook report [

17]. It is critical to address reliability and sustainability challenges lying ahead of the world’s energy supply and management systems. Recent incidences of nuclear power plant failure under harsh natural disasters in Japan are creating a new wave of anti-nuclear power movements in Europe, as well as in other parts of the world [

18]. Furthermore, the heightened safety and security concerns are adding to the uncertainty about the role of nuclear power in the future. In addition, the large body of evidence for anthropogenic climate change indicates the need for devising insightful strategies to provide a framework for integrated management of energy sector to facilitate the transition from fossil fuels to cleaner energy sources. In this regard, it is necessary to synthesize the role of non-renewable and renewable energy sources in the future energy landscape.

Of all energy sources, oil has the highest demand, giving it a unique position as the price-setter for global energy markets. Oil markets have occasionally experienced unpredicted price fluctuations, triggering adverse impacts on economic growth at regional and global scales. Ample oil resources of Organization of Petroleum Exporting Countries (OPEC) enable it to affect the supply and price of oil. OPEC oversees supply and pricing of a significant share of the global oil resources by coordinating and unifying the petroleum policies of twelve major oil producing countries that, as of 2010, hold more than 40% of the world’s crude oil production [

19]. The vast production capacity of OPEC, including its active and spare capacities, could thus be utilized as a practical means of impacting the price of oil. Historically, OPEC has played an active part in providing relatively reliable and efficient supply of energy to global markets, while safeguarding the economic interests of its individual member countries and the organization as a whole to a relatively good extent. Meanwhile, the power of a few nationalized oil companies plays a crucial role in the energy market and more specifically in the oil market. Thus, some have blamed the OPEC’s power and impact on the market security [

20,

21] as mismanagement, and internal conflicts of the few oil exporters are deemed to destabilize the world energy market [

22].

The objective of this paper is to investigate different perspectives on the role of OPEC’s future oil production levels in the global energy mix to draw insights for the global energy security. To this end, we have used historical data, as well as projections from such sources as British Petroleum (BP), International Energy Agency (IEA), the United States’ Energy Information Administration (EIA), and OPEC to provide an overview of the global energy portfolio. Furthermore, we provide a synthetic image of the future global energy balance by describing the trends in the evolution of production capacity of different components of the global energy portfolio. We have discussed the global oil outlooks to illustrate the implications of OPEC’s oil production decisions for the global energy security. Finally, the role of OPEC’s oil reserves and production capacity in maintaining stability, balance, and security of the world’s energy markets, as well as the implications of its production strategies for the global energy transition are highlighted.

3. OPEC and World Energy Outlook

Bentley

et al. [

42] provided a review of energy and socio-economic data sources, modeling approaches, and assumptions for several contemporary forecasts of the global oil supply. They identified two main classes of forecasts,

i.e., peak forecasts and quasi-linear forecasts. The peak forecasts anticipate the peak of oil production to occur by 2030 after which point the global production of oil will decline, whereas the quasi-linear forecasts anticipate that global oil production will continue to rise in response to demand or it will plateau around the year 2030 [

42]. The peak oil forecasts are essentially based on the finiteness of oil arising from physical limits on feasible extraction rates. Counterarguments to these forecasts have been made based on the inaccuracy of previous peaking forecasts, adequacy of proven global reserves for sufficient production, and discovery of new reserves [

43]. Although some of these arguments like potential room for expansion of proven reserves appear legitimate despite the uncertainties regarding investment decisions [

43], Jakobsson

et al. [

44] challenge these arguments’ scientific rigor, demonstrating that they are “unconvincing on both theoretical and empirical grounds.” While the outcome of the quasi-linear analyses can be questioned and critiqued on several physical, socio-economic, and political grounds, like any other projection, they nonetheless provide plausible projections for future energy mix, which have important implications for the global energy security.

The quasi-linear and peak oil projections have, respectively, provided high and low oil production forecasts [

45]. These forecasts range from 39.3 Mb/day to 105.2 Mb/day, the majority of which are larger than the median 91.45, and a significant number are in the range of 60–80 Mb/day. The projections of oil production by 2030 from such sources as EIA, IEA, and OPEC are on the higher end of the forecasts whereas other sources including LBST, Campbell, Peak Oil Consulting, and Uppsala University’s Global Energy Systems Group provide peak forecasts in the lower range [

45].

Table 2 summarizes key assumptions and projected attributes for these examples of global oil production reference forecasts for 2030.

Table 2.

Examples of global oil production reference forecasts summarizing the range of key assumptions and projected attributes for 2030 (adapted and updated from Sorrell

et al. [

45]).

Table 2.

Examples of global oil production reference forecasts summarizing the range of key assumptions and projected attributes for 2030 (adapted and updated from Sorrell et al. [45]).

| Forecast | Forecast source | Key assumptions † | Key projected attributes † |

|---|

| High production | IEA, EIA, and OPEC | Ultimate recoverable resource: 3,345–3,577 billion barrels

Average annual economic growth rate: 3.1%–3.5%

Average annual global population growth: 0.9%–1.0% | Average oil price: US $ 106–123

Average Production or supply: 96.5–105.7 Mb/day

Average decline rate: 4%–8.5% |

| Low production | LSBT, Campbell, Peak Oil Consulting, Uppsala Global Energy Systems Group | Ultimate recoverable resource: 1840–3150 billion barrels | Average Production: 39.3–75 Mb/day

Average Post-peak average decline rate: 2%–4.5% |

It is particularly worthwhile to investigate the dynamics of the global energy portfolio under high oil production projections due to high demand for this energy source coupled with crucial dependence of member countries of OPEC on oil production as their primary means of generating revenues. The reinforcing feedback mechanism between the need of both buyers and sellers to trade oil is a difficult challenge to overcome in order to move towards a more balanced global energy mix. For this reason, a number of energy perspectives from the high-oil production forecasts have been discussed in the present synthesis to draw insights for the global energy outlook, as well as the role of OPEC in the future oil production and supply in an oil-dominated future. Understandably, these energy outlooks are not exhaustively representative of what will actually happen in the future. Rather, they represent the probable future energy scenarios based on certain assumptions and conditions. We have discussed the projections from EIA in greater detail as they characterize a wide range of possible global oil outlooks under a variety of price and production scenarios.

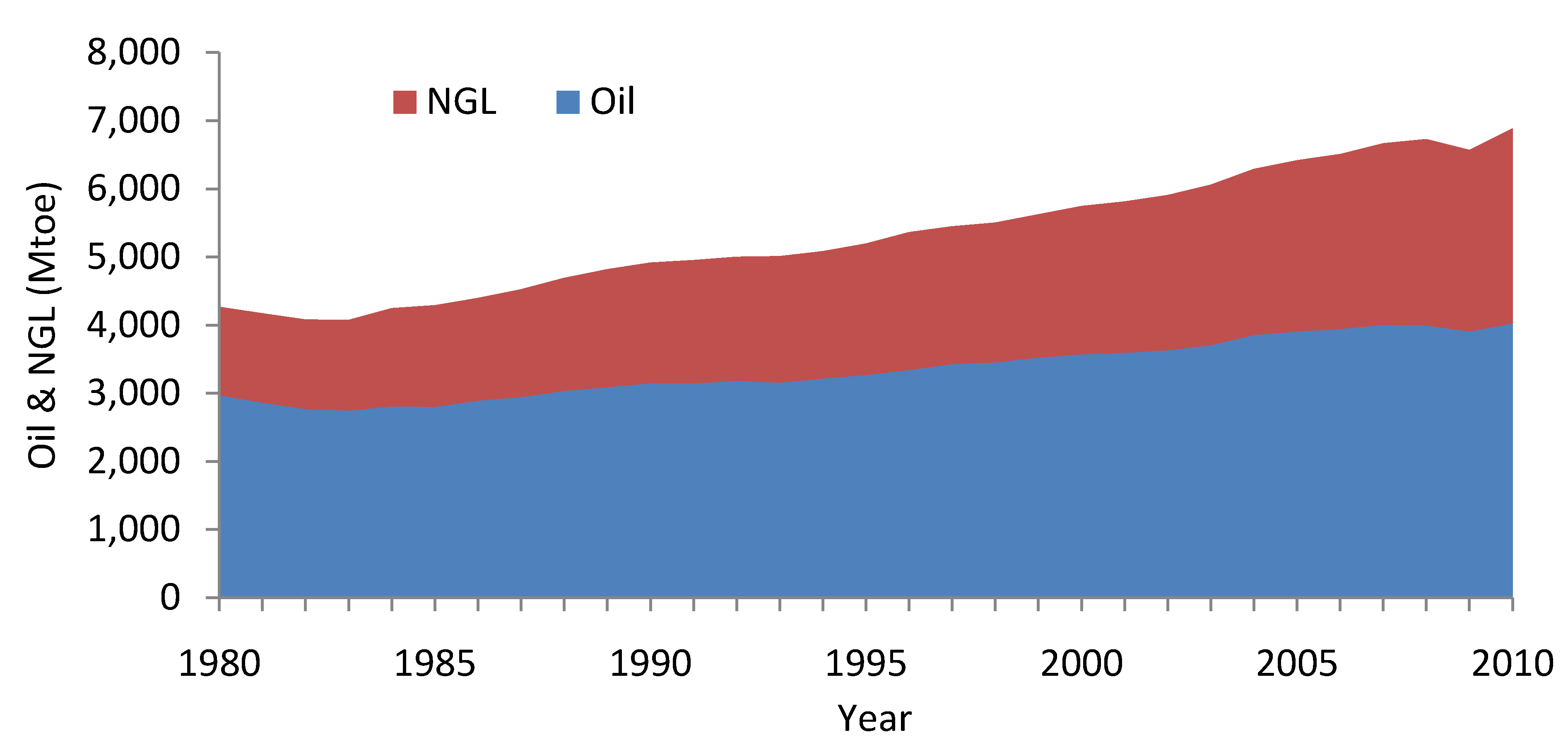

The IEA has estimated that fossil fuels will account for more than three quarters of the overall increase in energy use between 2007 and 2030 [

8]. Based on the reference scenario of IEA’s projection, if the global energy policies remain unchanged, the world will increasingly rely on large-scale supplies of oil and NGL sources and their share in the world energy portfolio will likely increase from 57% in 2002 to approximately 60% in 2030 [

8]. Continued reliance on oil and NGL may potentially translate into an increase of about 70% in the global demand within the next two decades. These projections further reveal that, even if governments decide to adopt low GHG emission policies, the total global demand for oil and NGL may only decrease by about 10% and 11%, respectively [

8]. In order for this reduction to actually take place alternative energy sources should be introduced in an economically and technologically viable fashion while complying with prescribed low GHG emission targets.

The reference case for the OPEC’s own projections assumes that world population will maintain an increasing trend, reaching 8.3 billion by 2030, about 95% of which will be population increase in developing countries [

46]. Notwithstanding the significant variability in regional economic growth (e.g., China and India), the reference case assumes that on average the global economy will grow steadily at 3.5% per year within the timeframe of 2010–2030 [

46]. Furthermore, despite efforts to account for energy policy changes set forth by governments, this factor will likely be responsible for large uncertainties in projected energy demands. In particular, it is difficult to envision a robust global consensus with regard to GHG emission reduction policies. Although it is anticipated that extensive investment on renewables will increase the share of low-emission energies, under OPEC’s reference case scenario fossil fuels will likely comprise over 80% of the world’s energy mix by 2030 [

46].

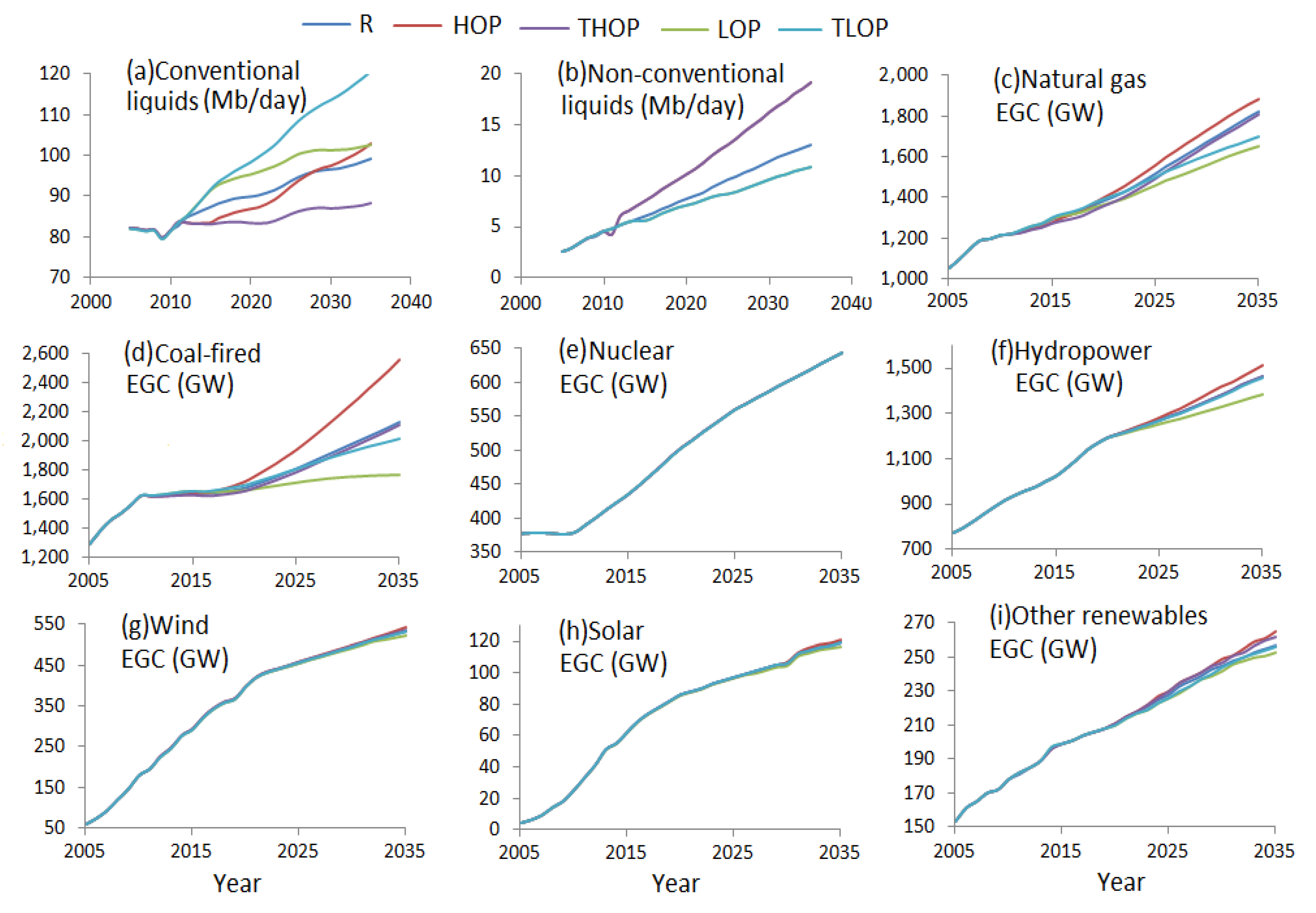

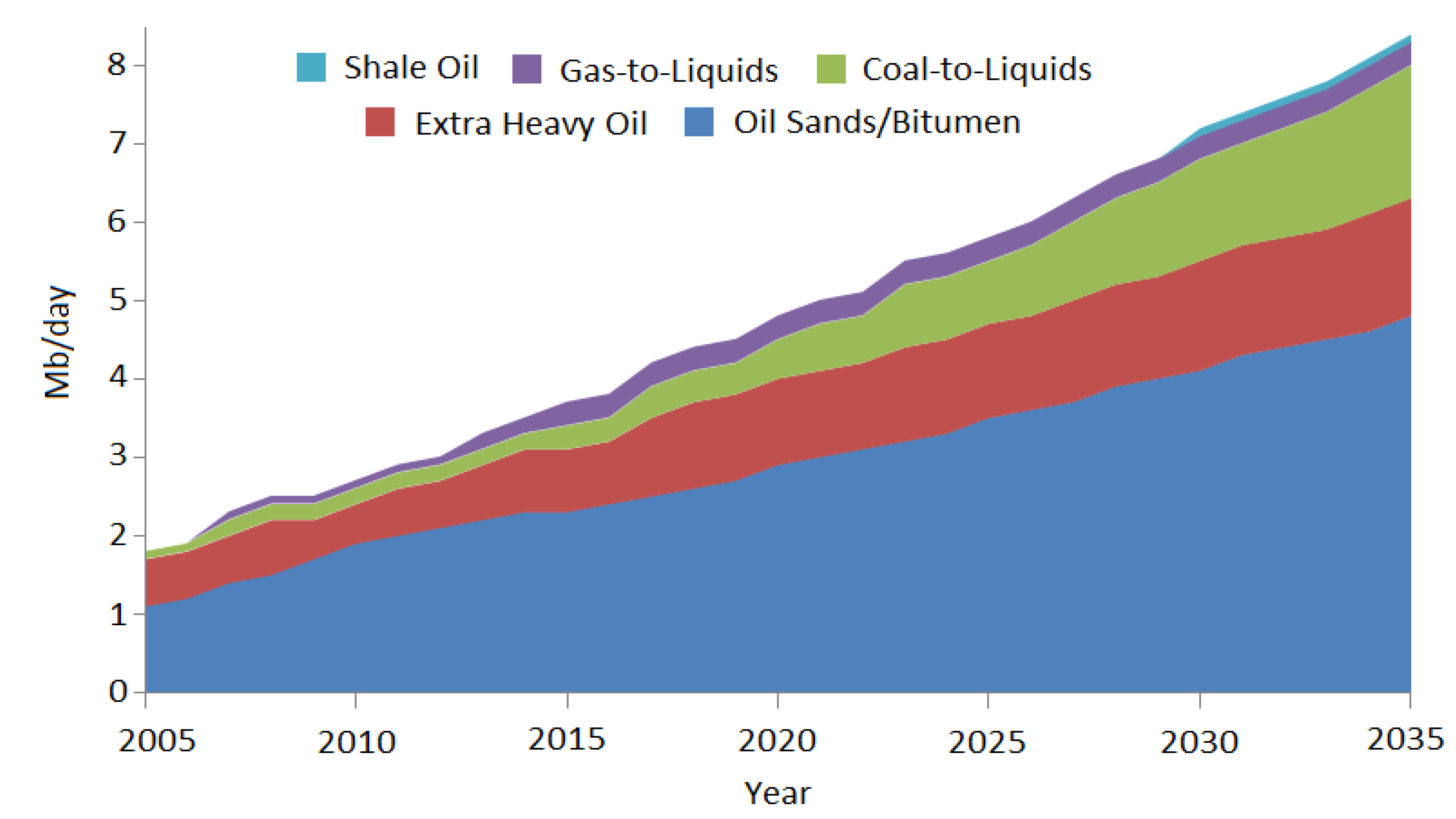

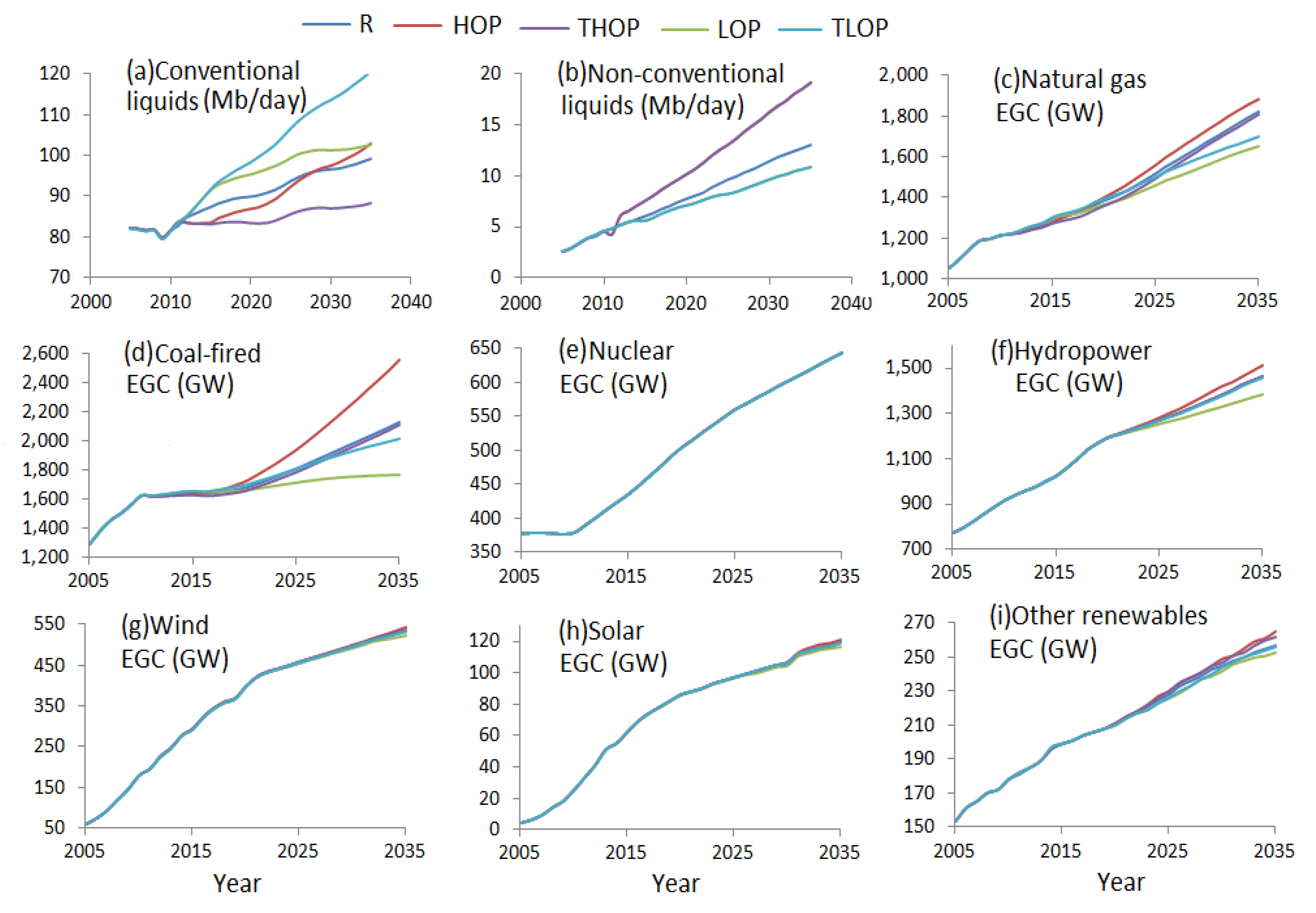

Figure 13 illustrates the EIA’s projected trends in the production of different energy sources. In the reference scenario, which is the business-as-usual trend estimate, projections are developed based on the current technologies and regulations, regardless of the future policies and legislations that affect energy markets. The high oil price scenario characterizes increase in demand driven by higher economic growth of non-OECD countries accompanied by a decrease in oil production. The traditional high oil price scenario associates the high oil price with the decrease in oil supply by OPEC countries. Similarly, low oil price scenario relates the low oil price to the increase in the oil supply accompanied by a decrease in the oil demand. Finally, the traditional low oil price scenario assumes low oil prices will be associated with the increase in oil supply by OPEC countries. While the projected share of different energy sources varies under different scenarios, overall, the energy production from all sources is expected to grow by 2035. Oil is projected to remain the backbone of the global energy mix, especially under low oil price scenarios, which poses a challenge for non-conventional liquid fuels to become economically competitive (

Figure 13a). The economic incentives and energy security concerns are likely to boost the production of non-conventional liquid fuels (

Figure 13b). As shown in

Figure 13c–f similar long-term trends are projected for the electricity generation capacity from natural gas, coal-fired sources, and hydropower, except the electricity generation capacity for coal-fired sources is expected to plateau under the low oil price scenario. The nuclear sources appear to be insensitive to different scenarios (

Figure 13e). Furthermore, the growth trend for wind power, solar energy, and other renewables are similar, and they become more competitive under high oil price scenarios (

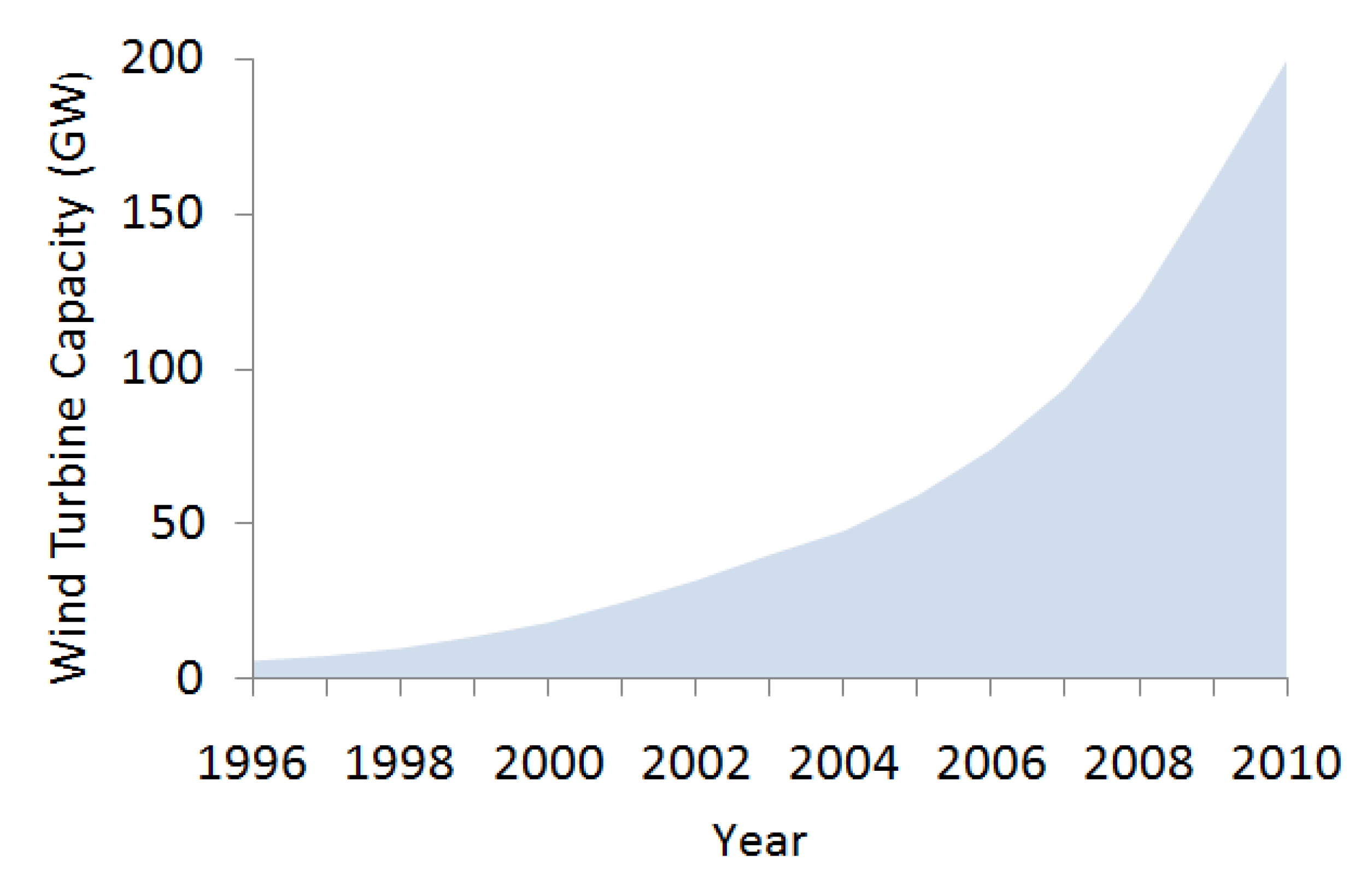

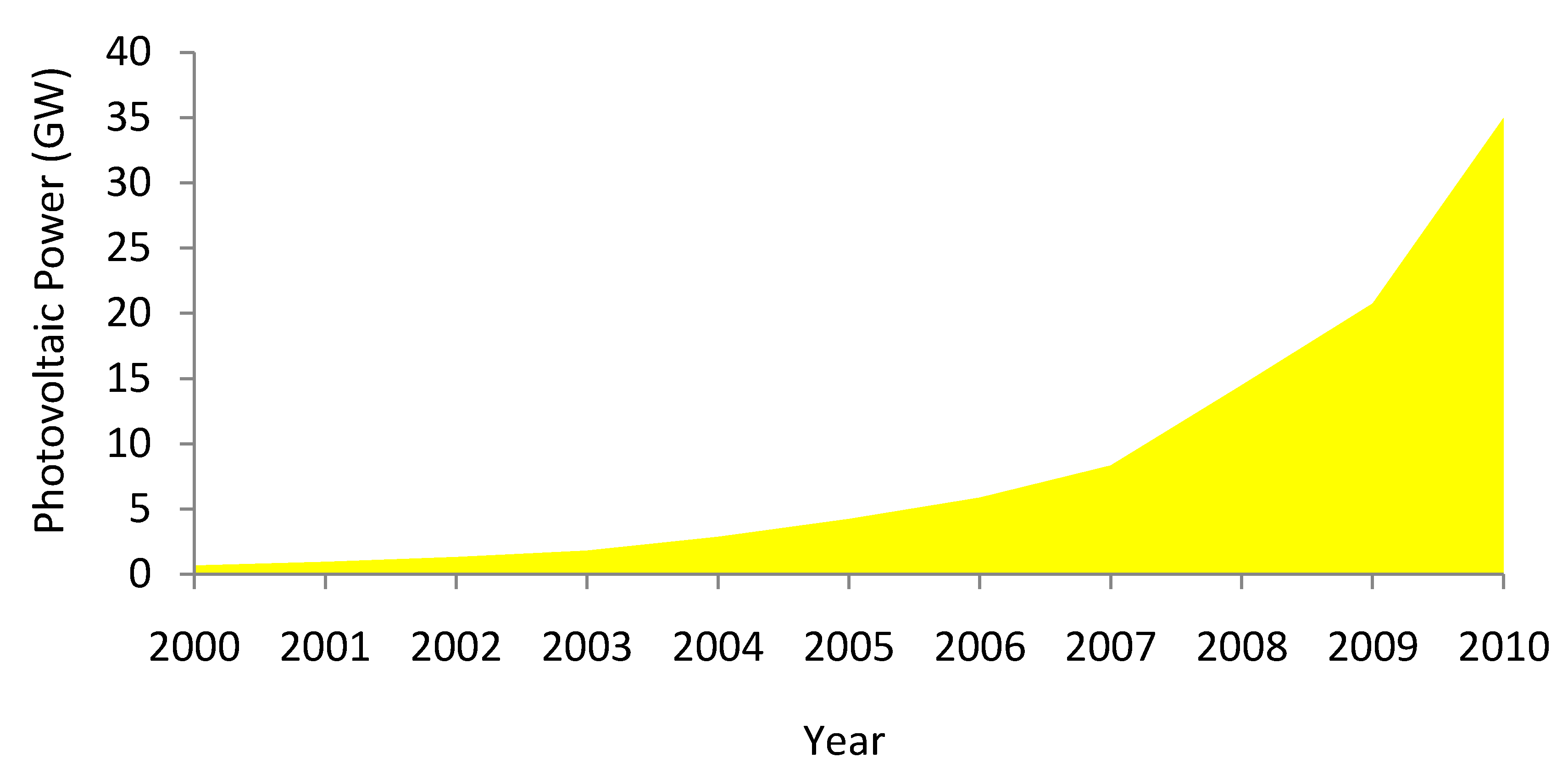

Figure 13g–i).

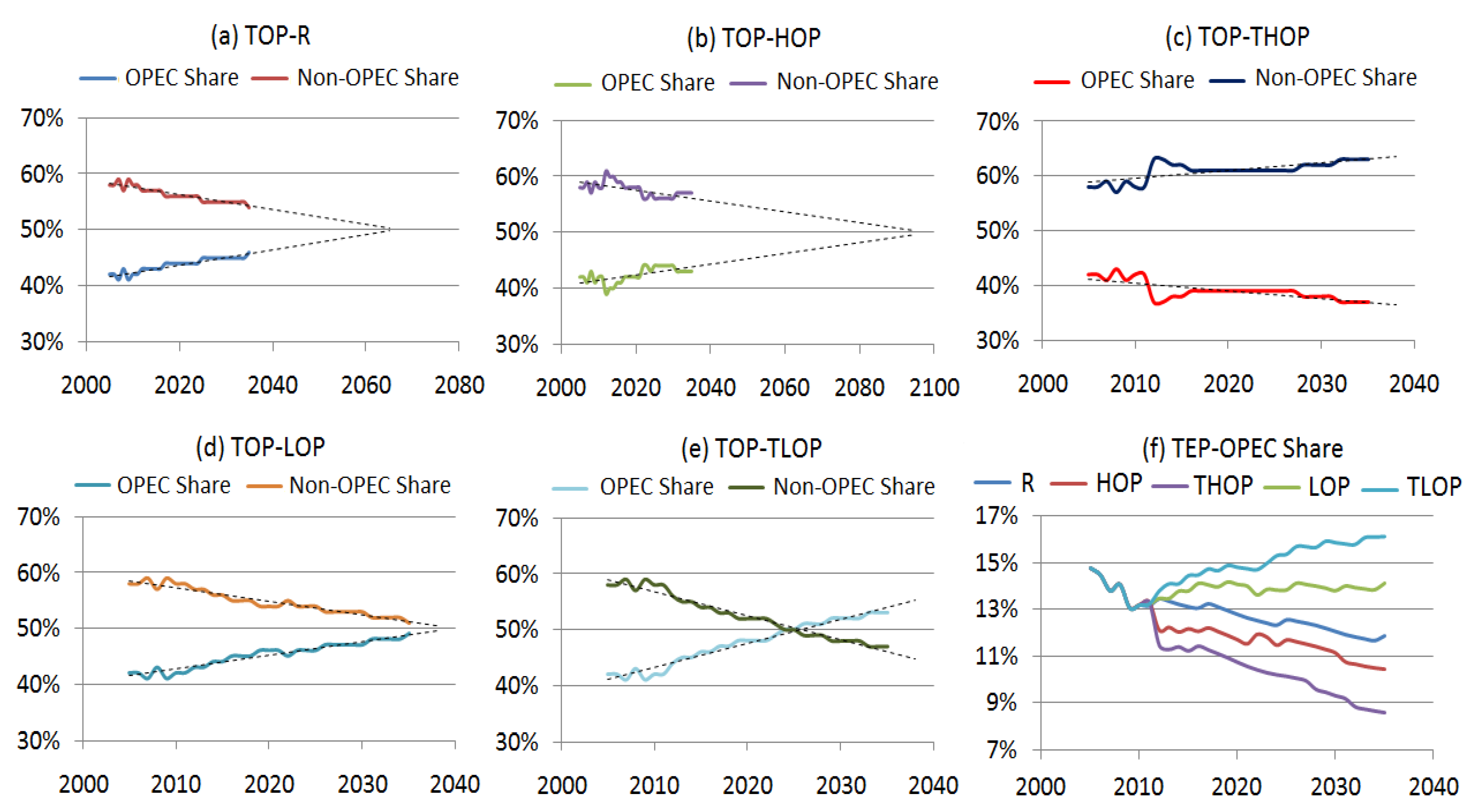

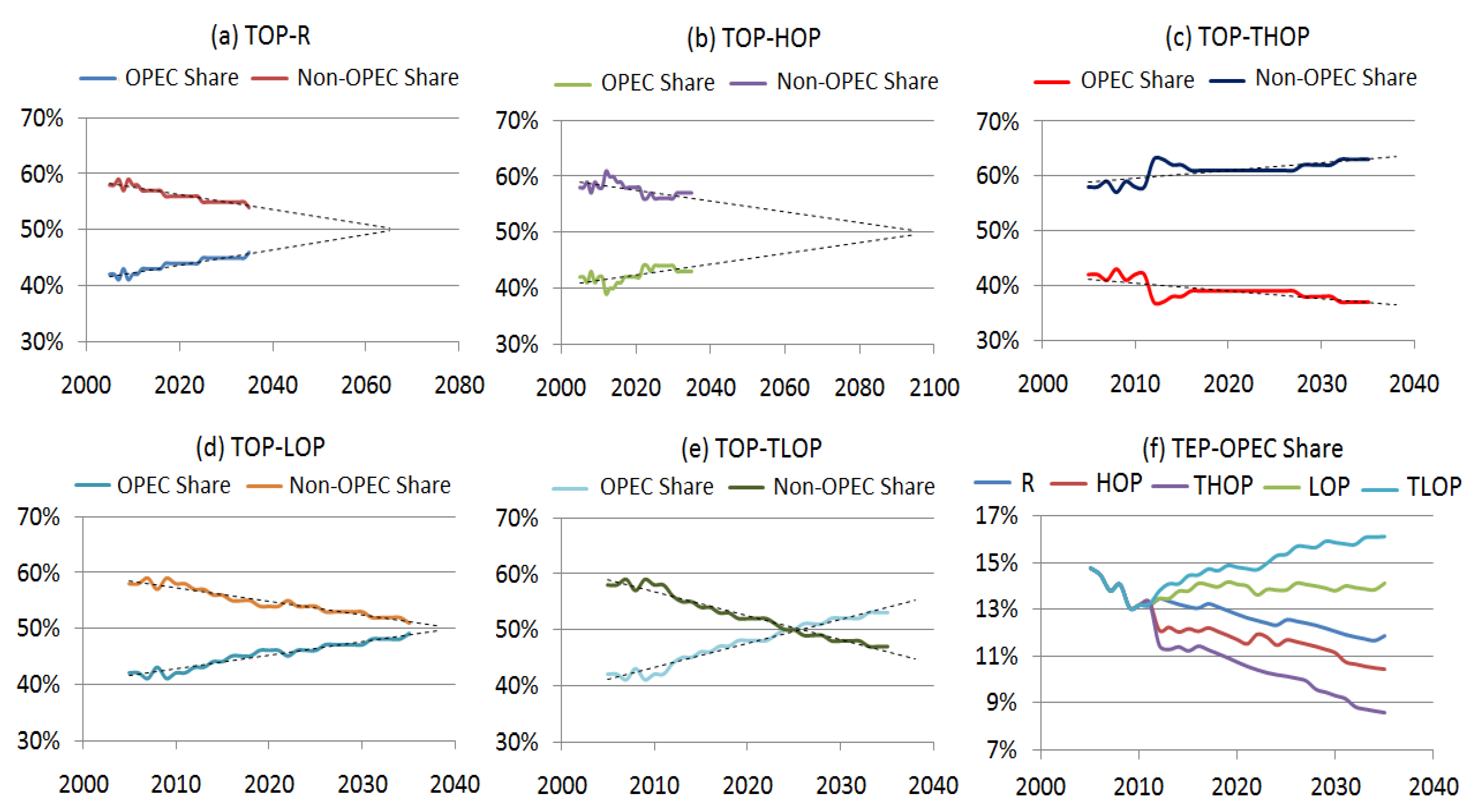

Figure 14 shows the EIA’s projections of OPEC and non-OPEC world’s total oil production. Under the reference scenario, the OPEC’s share of oil production increases by 4% over the period of 2005–2035 (

Figure 14a). If this growth rate holds into the future, OPEC will become the dominant oil producer by 2065.

Figure 14b shows the OPEC and non-OPEC oil production assuming high oil price scenario over the mentioned period. Based on this scenario, the share of OPEC from total oil production increases over time, but the growth rate will be slower than that in the reference case. Under traditional high oil price scenario, OPEC will never dominate the oil market in the future due to a decreasing trend over the study period (

Figure 14c). However, the traditional high oil price scenario is less likely to happen due to the oil dependent economies of the OPEC member countries, as well as the decreased market share of the oil produced by OPEC based on this scenario.

A low oil price scenario, on the other hand, portray a more powerful role for OPEC in the future energy markets. Based on the low oil price scenario, OPEC’s contribution to oil production increases by 7% over the period of 2005–2035 (

Figure 14d). Continuation of this trend can make OPEC the dominant oil supplier by 2038. Likewise, OPEC’s share increases by 11% based on the traditional low oil price scenario and OPEC becomes the dominant oil supplier by 2026 (

Figure 14e). Although the share of oil in the global energy markets is decreasing due to emerging policies addressing climate change and depleting fossil fuel reserves, even under the worst case scenario (traditional high oil price scenario), the oil produced by OPEC appears to be an important component of the global energy mix, contributing to at least 10% of the total energy supply in the next two decades (

Figure 14f).

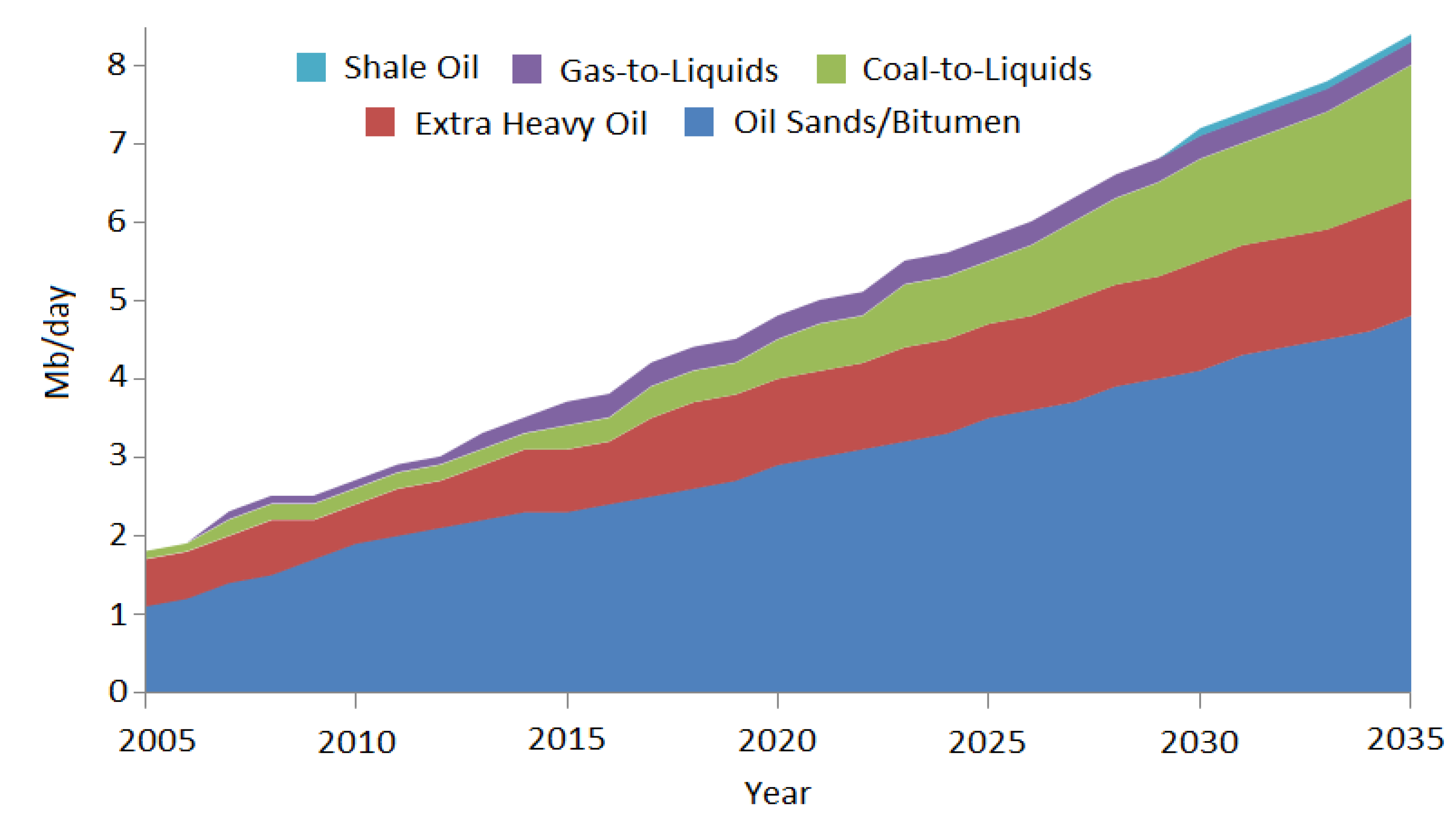

In general, the non-conventional liquid fuels including biofuels become more competitive under the high oil price scenario, which may result in decreasing demand for oil in the long run and eventually, diminishing its share in the global market share. However, the scenarios of rapid expansion of the non-conventional liquid fuel production might not be effective in the short-run as they require extensive institutional and technological change in transportation and industrial sectors [

47,

48]. Under the EIA’s reference scenario, the share of non-conventional liquid resources to the total liquid production will be increasing from 3% to 12% over the period of 2005–2035, implying the significant role of these resources in the global energy mix. However, the environmental impacts of producing energy from non-conventional liquid resources as well as the investment restrictions may become an obstacle to the further development of these sources, especially for the Canada’s oil sands and Venezuela’s extra-heavy oil projects.

Figure 13.

Projected share of different energy sources in terms of liquid fuel production (Mb/day) and electricity generation capacity (EGC) (GW) by 2035 under EIA’s scenarios: (

a) reference (R); (

b) high oil price (HOP); (

c) traditional high oil price (THOP); (

d) low oil price (LOP); and (

e) traditional low oil price (TLOP) (source of data: EIA [

25]).

Figure 13.

Projected share of different energy sources in terms of liquid fuel production (Mb/day) and electricity generation capacity (EGC) (GW) by 2035 under EIA’s scenarios: (

a) reference (R); (

b) high oil price (HOP); (

c) traditional high oil price (THOP); (

d) low oil price (LOP); and (

e) traditional low oil price (TLOP) (source of data: EIA [

25]).

Figure 14.

EIA’s projections of the world’s share of total oil production (TOP) and total energy production (TEP) under different scenarios: (

a) reference (R); (

b) high oil price (HOP); (

c) traditional high oil price (THOP); (

d) low oil price (LOP); and (

e) traditional low oil price (TLOP) (Source of data: EIA [

25]).

Figure 14.

EIA’s projections of the world’s share of total oil production (TOP) and total energy production (TEP) under different scenarios: (

a) reference (R); (

b) high oil price (HOP); (

c) traditional high oil price (THOP); (

d) low oil price (LOP); and (

e) traditional low oil price (TLOP) (Source of data: EIA [

25]).

The dichotomous debate on the global energy outlook is replete with contrasting views to the perspectives of EIA, IEA, and OPEC regarding the global oil outlook [

49,

50,

51]. A recent synthesis of peak oil production by Sorrell

et al. [

52] concludes that the peak of oil production is very likely to occur by 2030. Some researchers, in fact, caution that the world’s peak oil production may already have passed [

53] or the production may be in a plateau state [

48]. A direct link between the peak oil literature and the global energy outlook is the dire need for advancement of alternative energy sources along with institutional and infrastructural reforms in the global energy management. The high oil production scenarios are not compatible with the potential climate change mitigation policies. As was illustrated in

Section 2, non-conventional liquid fuels and renewable energy sources are gaining increasing significance in the global energy mix, and transition from a fossil-fuel-based mix to a more balanced portfolio is only a matter of time. However, the existing interdependencies between an oil-dominated world and socio-economic and geopolitical stability are a critical fact, affecting the timeframe of the energy transition era [

54,

55]. Decisions of major oil producing organizations like OPEC can impact the timing and turbulence of the energy transition.

4. OPEC’s Oil Reserves and Production Capacity: Implications for Oil Security

OPEC’s ample energy resources provide an opportunity for employing stabilizing measures on the oil market. For instance, OPEC’s production restraints coupled with growing demand for oil resulted in a significant increase in oil price toward the end of 2010 [

1].

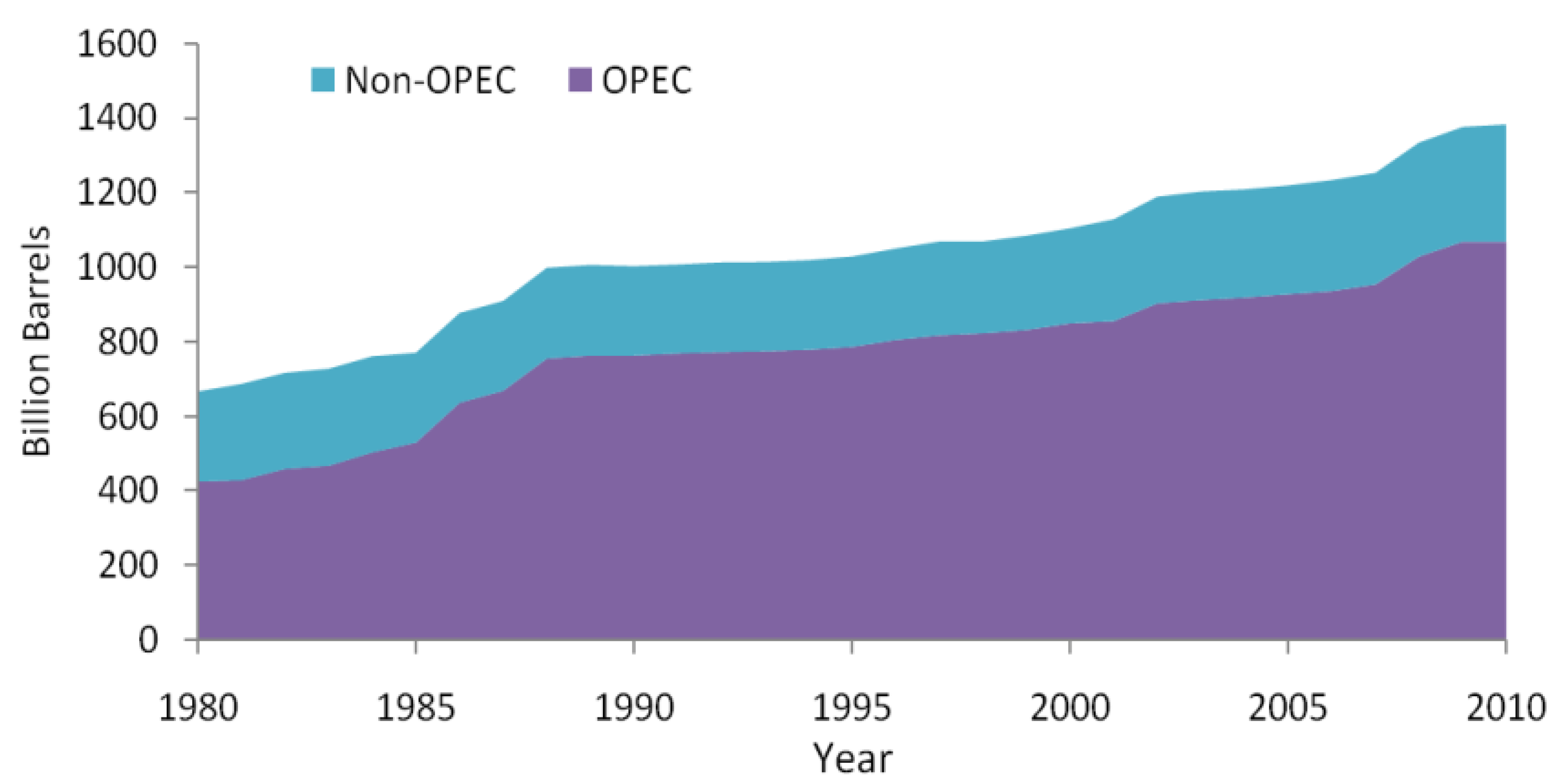

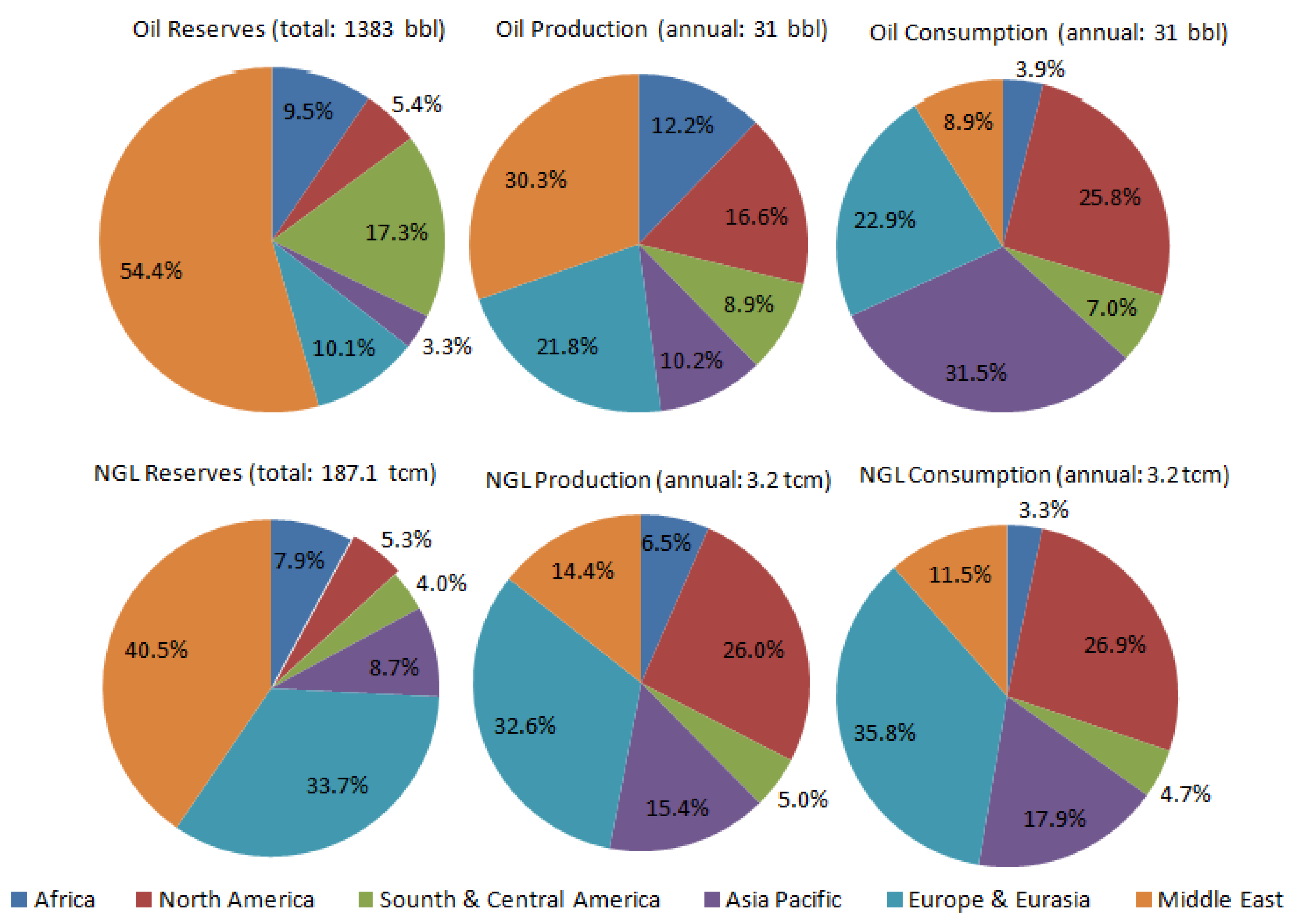

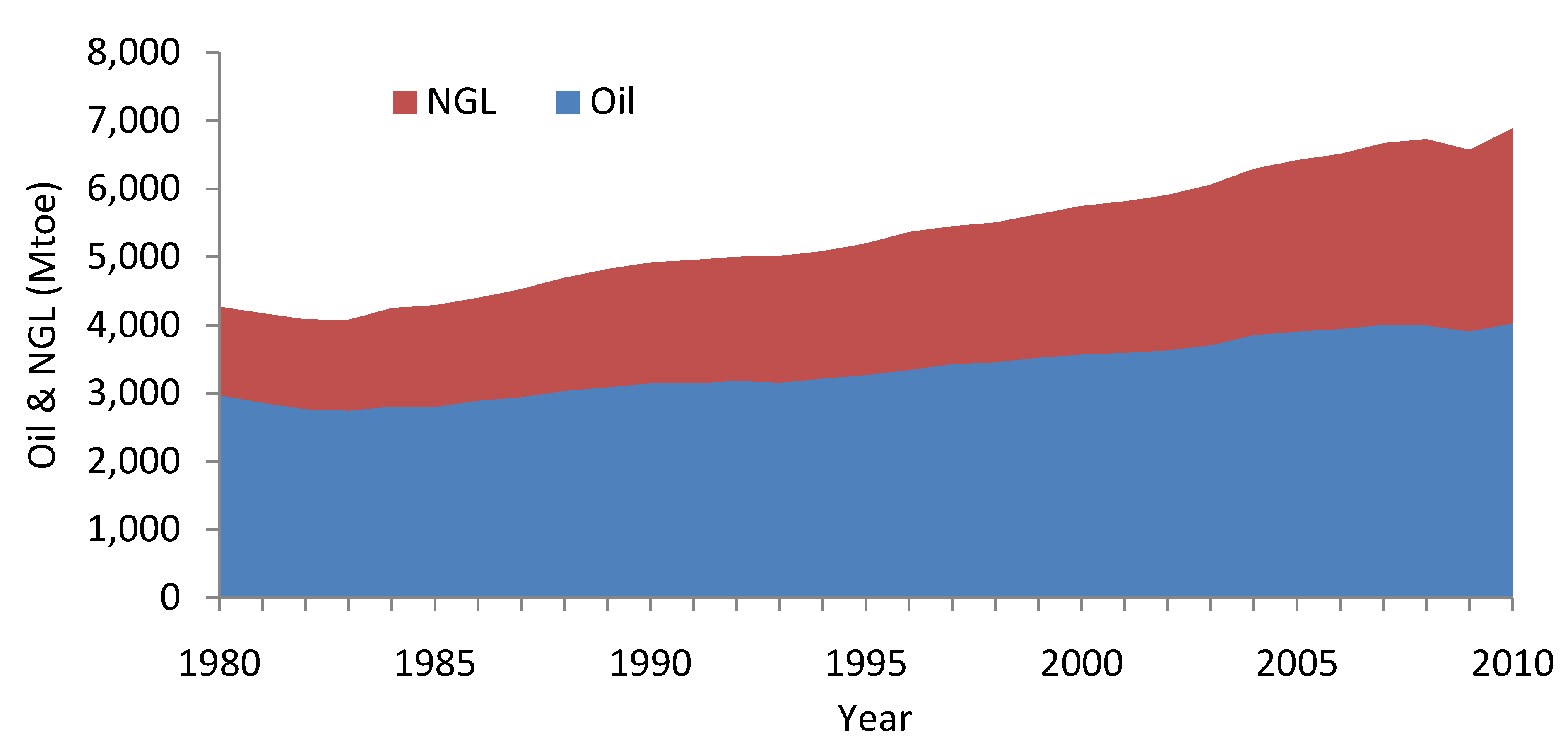

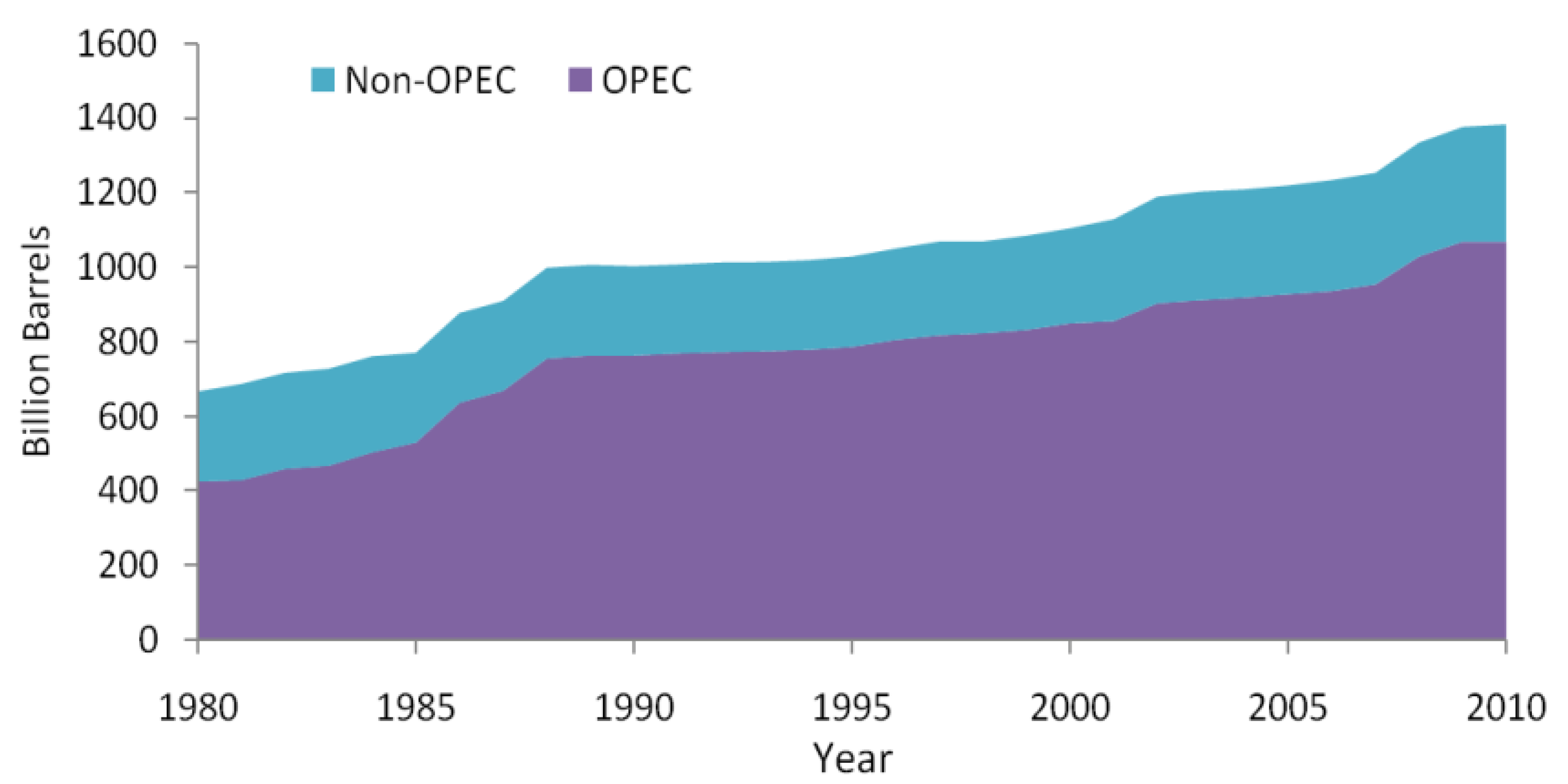

Figure 15 presents historical trend of OPEC and non-OPEC proven oil and NGL reserves using data from BP Statistical Review of World Energy [

1]. This figure illustrates that OPEC member states collectively possess more than 80% of the world’s proven oil and NGL reserves. Also,

Figure 15 shows that nearly all supply shocks are generated by OPEC’s production. Based on EIA’s reference scenario, OPEC’s oil production would need to be increased by about 25% over the current production levels if OPEC were to maintain its share in the global oil markets in 2030 [

25]. In the current synthesis, we treat OPEC as one large energy producing unit, which will have a unified strategy about the global energy decisions. The intra-OPEC dynamics and disputes regarding the logistics of future oil production in response to increasing consumption are thus assumed to have marginal impact on OPEC’s production level as a whole. OPEC members’ investment in maintaining and/or expanding their oil infrastructure will be an indicator of which country will have the potential to act as the marginal supplier of the additional oil, which has important implications for the global energy security given the geopolitical volatility of the Middle East.

Figure 15.

Historical trend of OPEC and non-OPEC proven oil and NGL reserves (Source of data: BP [

1]).

Figure 15.

Historical trend of OPEC and non-OPEC proven oil and NGL reserves (Source of data: BP [

1]).

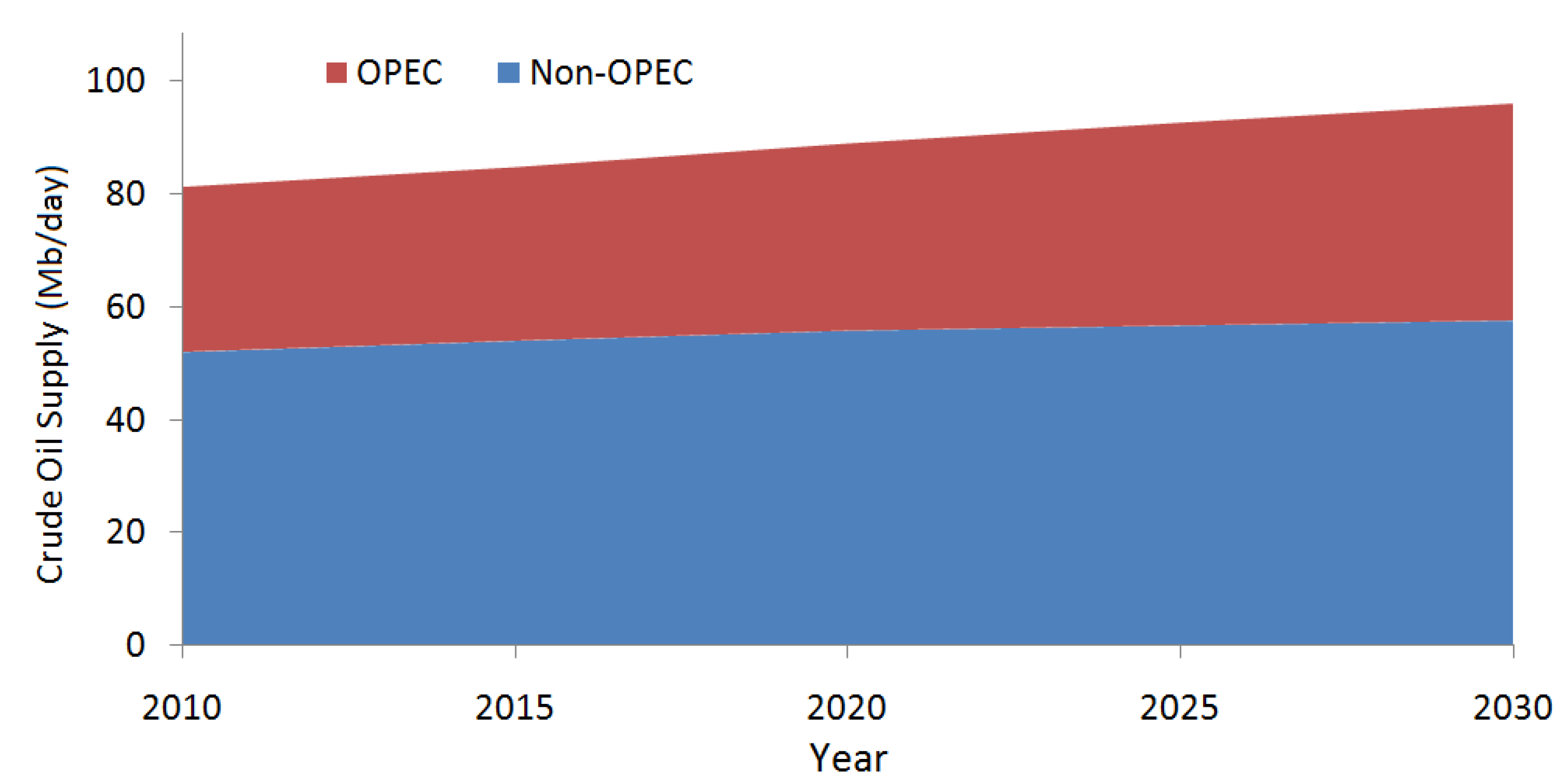

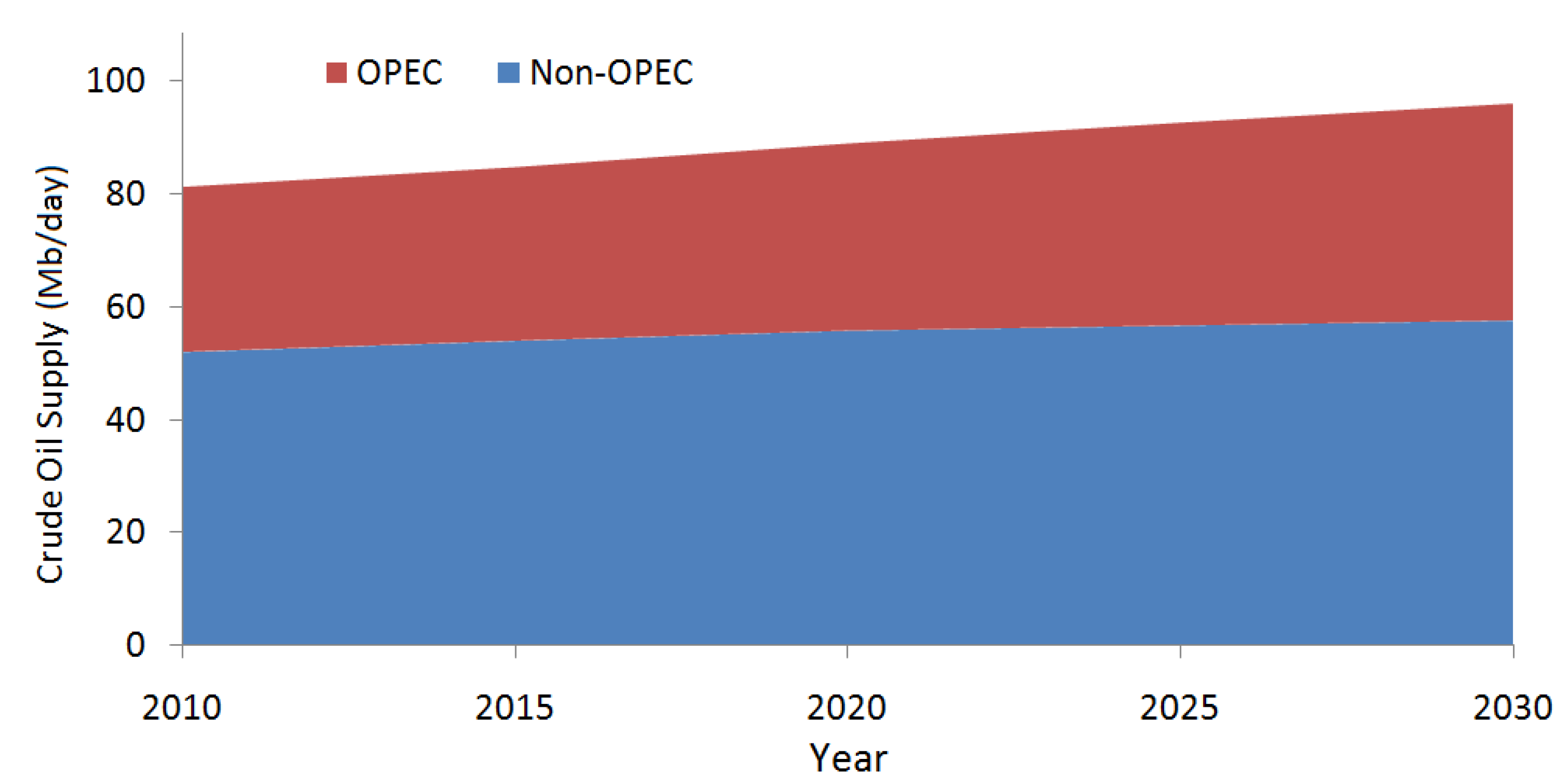

OPEC has extensive potentials to help meet the rising global oil demand by 2030.

Figure 16 shows the OPEC and non-OPEC projected contributions to global oil markets [

19]. The global demand for oil may rise from over 80 Mb/day to approximately 105 Mb/day by 2030. The economic recovery following the recent global economic recession will potentially create a heightened growth in oil demand in the medium-term. In the long-run, throughout the period of 2010–2030, the net average annual oil demand is expected to increase by about 0.9% annually due to significant growth in demand from rapidly expanding economies such as China and India, which will likely compensate for declining oil demand from member countries of OECD.

Projected trends of energy demand provide insights into oil supply management and production capacity expansion, which can guide capital investments in oil and NGL sectors.

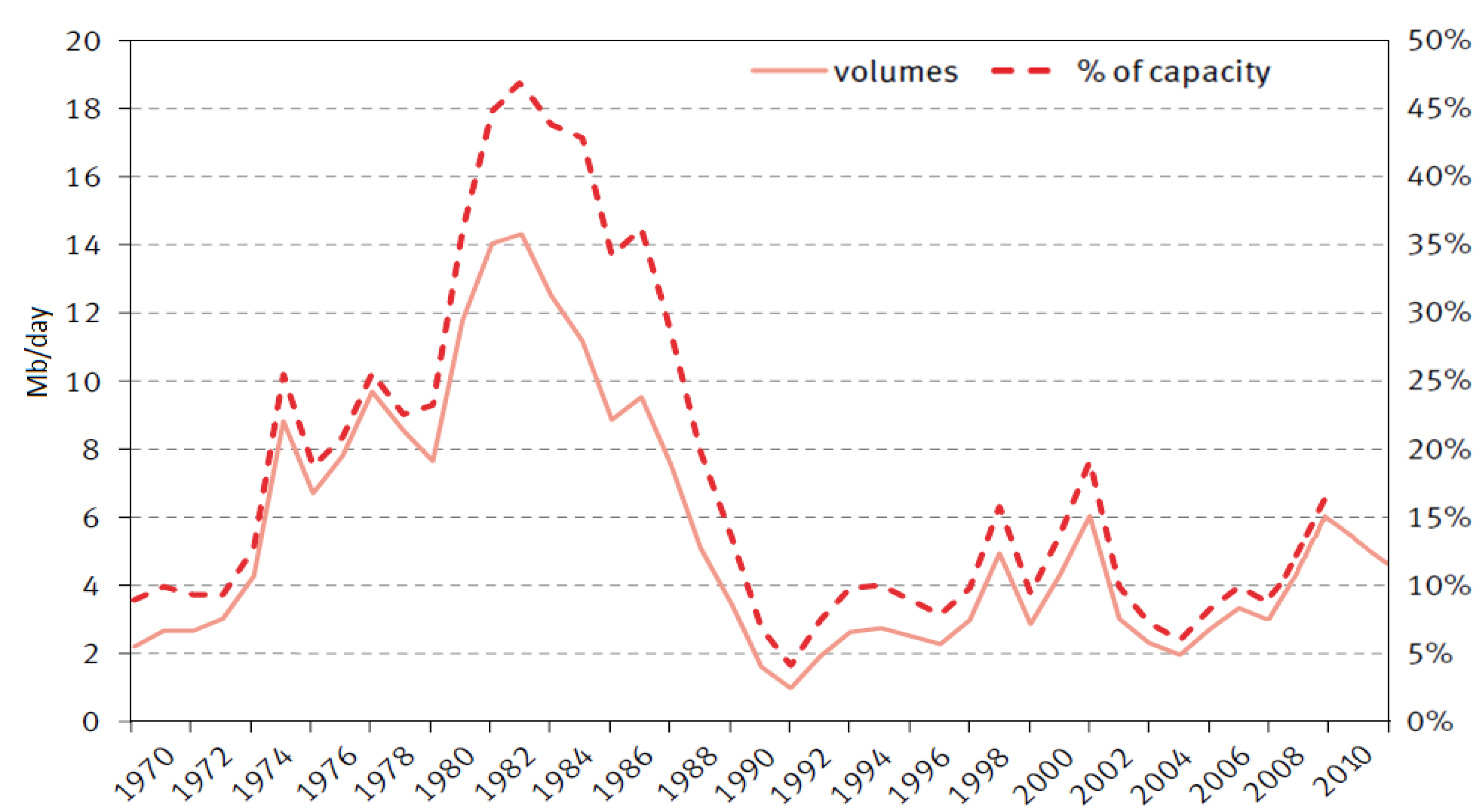

Figure 17 shows OPEC’s spare production capacity over the past four decades. The figure displays historical trends of production and spare production capacity. It is worth noting that the largest discrepancy between OPEC’s oil production and available production capacity occurred in early 1980s, when OPEC was unable to use approximately half of its available production capacity. This was an artifact of over-investment in capacity expansion coupled with declining global oil demand, likely due to the price increase associated with the Iran-Iraq war [

21,

22].

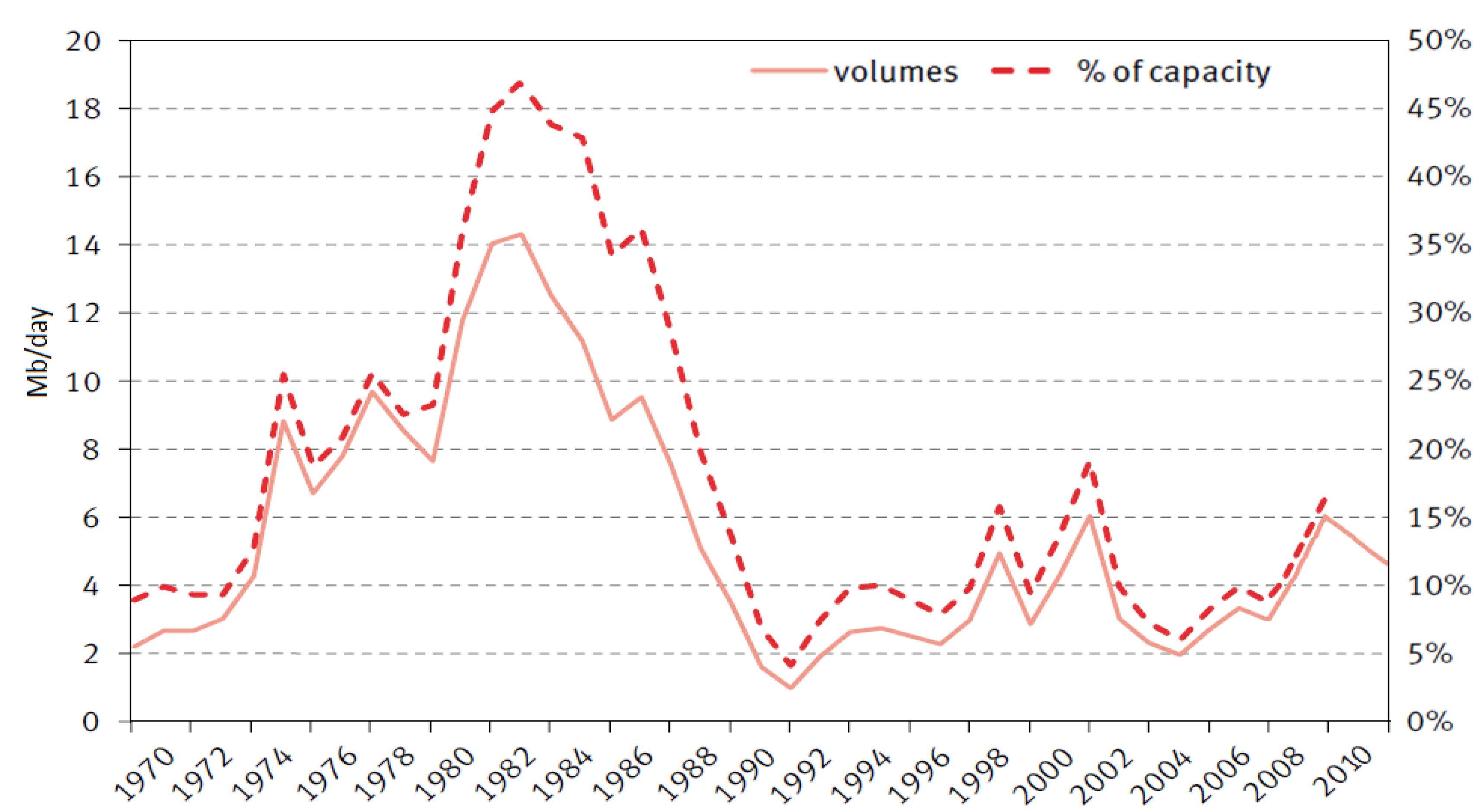

Figure 16.

OPEC and non-OPEC crude oil supply by 2030 (Source of data: OPEC [

19]).

Figure 16.

OPEC and non-OPEC crude oil supply by 2030 (Source of data: OPEC [

19]).

Figure 17.

OPEC’s spare production capacity (Source: OPEC World Oil Outlook

© OPEC Secretariat, 2010, p. 140 [

46], data for 2010 and 2011 from OPEC, 2011 [

56]).

Figure 17.

OPEC’s spare production capacity (Source: OPEC World Oil Outlook

© OPEC Secretariat, 2010, p. 140 [

46], data for 2010 and 2011 from OPEC, 2011 [

56]).

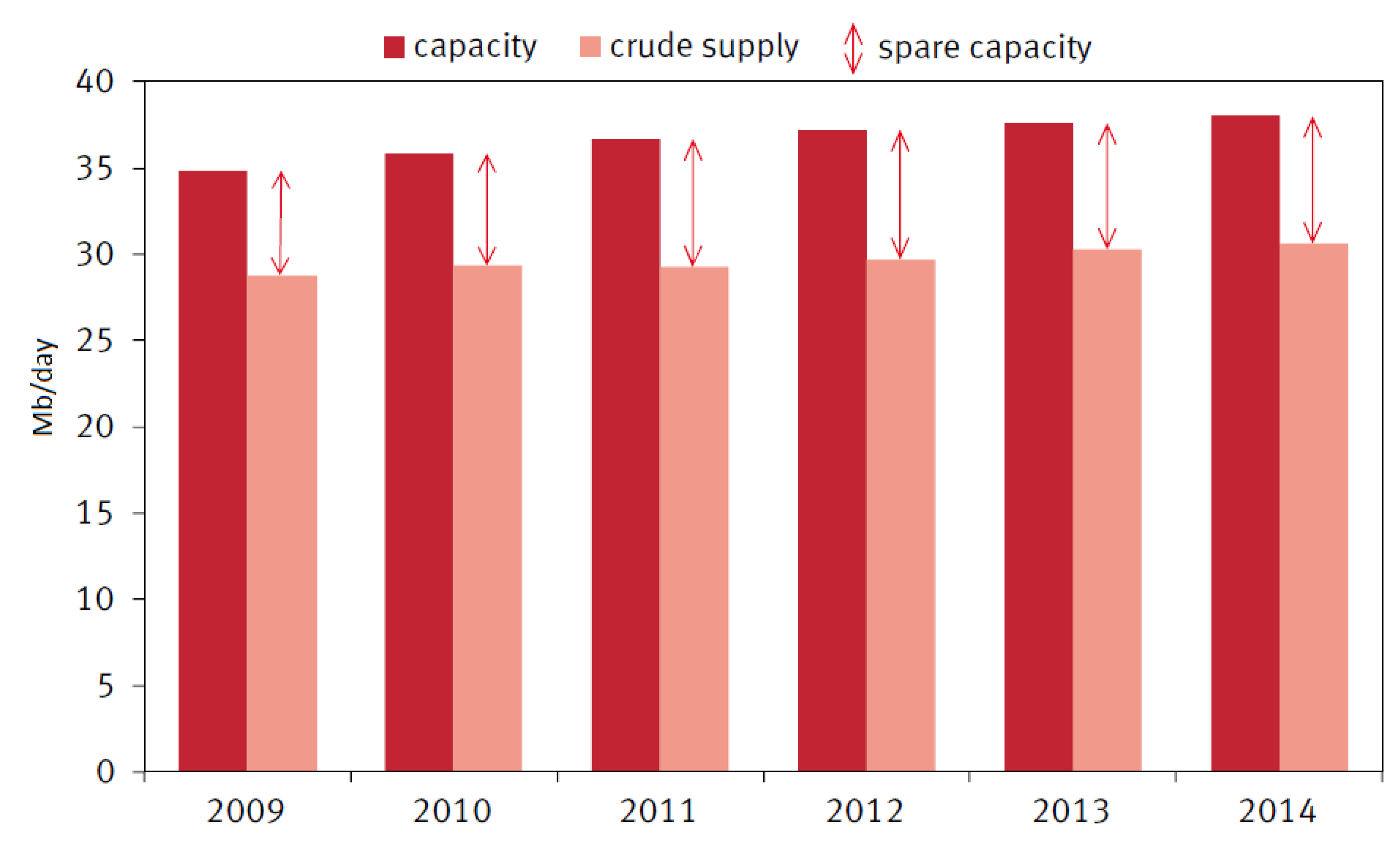

OPEC’s current and projected medium-term crude oil production capacity and supply are shown in

Figure 18. The figure illustrates that in medium-term OPEC can take advantage of spare crude oil production capacity to help meet the rising demand while stabilizing the price. The figure also portrays OPEC’s potential production capacity growth over the period of 2009–2014. The critical importance of retaining reasonable spare capacity was manifested in the 2000’s when economic recovery after the global financial crisis drove an increase in the oil demand by more than 20% between 2002 and 2008 during which time OPEC’s spare capacity fell to about 3 Mb/day. In order for OPEC to maintain its key role in global fossil fuel supply system, as a reliable producer, it is necessary to expand production capacity at rates comparable to increase in global oil and NGL demand–a task that is inherently subject to great uncertainties such as potential geopolitical instabilities, investment risks, and future prices, among others.

Figure 18.

OPEC’s medium-term crude oil capacity and supply (source: OPEC World Oil Outlook

© OPEC Secretariat, 2010, p. 70 [

46]).

Figure 18.

OPEC’s medium-term crude oil capacity and supply (source: OPEC World Oil Outlook

© OPEC Secretariat, 2010, p. 70 [

46]).

As the world approaches the peak of oil production, the energy management sectors and political governments will need to choose between non-cooperative and cooperative management strategies. The global oil market is characterized by interaction of international competition and cooperation that can jeopardize or improve energy security in the face of a terminal decline in oil production. Individual countries will react differently to the problem of the global oil peak.

Friedrichs [

57] synthesized historical evidences to hypothesize that while some countries will adopt socio-economic adaptation to alleviate peak oil crisis, others may practice predatory militarism or totalitarian retrenchment. Overly large price fluctuations in the past have triggered detrimental economic instability affecting nearly all stakeholders, signifying the need for appropriate mechanisms to avoid price swings [

58]. If the future looks like the past, OPEC will not only maintain its importance as a key player in the global energy market, but it may also gain further significance due to increasing demand in the face of limited resources. It follows from this argument that if a serious and practical action plan to facilitate the energy transition is not employed in the lead time before the pinnacle of the energy crisis, the transition era will be a long and tortuous path, and the realization of a unified front to mitigate climate change will only be pushed further into the future.

OPEC’s future production and supply strategies will depend on which global energy outlook scenario unfolds. From a historical standpoint, OPEC has used two main strategies to influence global energy prices,

i.e., “shutting in” available production capacity, and growth restriction by limiting capacity development in terms of infrastructure and resource exploration [

59]. The noted strategies have been aimed mostly at maintaining high prices to the extent that OPEC has been described by some as a bureaucratic oil cartel [

60]. If the EIA’s low oil price and traditional low oil price scenarios happen, OPEC will become the dominant oil supplier to the global markets by 2035 (

Figure 14f). However, the accuracy of the reported OPEC reserves has been questioned as these reserves have been increasing significantly over time without reflecting changes due to continuous production [

61].

Whether OPEC’s reserves are indeed overstated or not cannot be corroborated externally. That being said, our current synthesis of world energy outlook suggests that, in the long-run, OPEC may shift its strategies towards intensifying the development of infrastructural capacity. This strategy shift will occur either willingly and deliberately due to increased demand, or it will happen unwillingly and mandatorily to avoid potential loss of market share to alternative energies. It has been estimated that a sustained annual growth of about 10% would be needed for the non-conventional liquid fuels to attenuate the peak oil [

62]. The additional capacity will allow OPEC to increase the oil supply in order to push the oil prices to lower equilibrium prices to make the non-conventional liquid fuels and alternative renewables less competitive. The low oil price strategy may pose physical risks to the global energy supply as rapid post-peak decline rates may make it difficult for non-conventional sources to come on-stream in significant capacity in a timely fashion.

On the other hand, OPEC can contribute to market stability and energy security by promoting constructive communication with major oil consumers, as well as by collaboration with producers of renewable energies to identify the least turbulent paths for global energy transition while finding opportunities to minimize global socio-economic consequences [

46,

63]. As global demand for oil increases in medium- and long-terms, the world’s reliance on OPEC’s proven reserves and production capacity is expected to increase [

7]. In the absence of strategic reasons (e.g., competition with non-conventional liquid fuels and renewables), it would be plausible to envision that OPEC’s crude oil supply will grow moderately, decreasing the effectiveness of the GHG reduction efforts. In fact, OPEC estimates upstream investment requirements, excluding additional infrastructure, to be approximately $575 billion in 2009 U.S. dollars [

46]. The profitability of oil investments will depend largely on timing of investments and security of demand, as well as dynamics of market share for other sources of energy.

While climate change mitigation policies such as carbon tax and/or pricing, and R&D investment in renewable energy development can increase the long-term energy security for oil-importing countries, these policies can dramatically reduce the demand for fossil fuels which will reduce the vital revenues for oil-exporting countries. Furthermore, the dependency of the existing economies in the developed world on fossil fuels is a barrier to an abrupt shift to renewable energy sources as the renewables mostly contribute to the energy production in the form of electricity, while transportation and industrial sectors are highly dependent on the fossil fuels, especially on oil. As such, the global energy policy to mitigate climate change can significantly impact the industry and stability of energy markets [

64,

65], which may be part of the reason why the political powers are seemingly lethargic in reaching a global consensus to facilitate the energy transition and adoption of aggressive climate warming mitigation policies.

6. Conclusions

The global energy portfolio comprises a mix of well-established non-renewable fossil fuels, nuclear energy, and rapidly growing renewable energies. The primary energy consumption is currently dominated by fossil fuels, especially by oil. The present synthesis of the world energy balance outlook suggests that, under current policies and legislations, i.e., if historical energy production and consumption trends hold into the future, the world will continue to rely on fossil fuels as the main source of meeting its primary energy needs by 2030. The world should be increasingly concerned about the implications and consequences of an oil-dominated future for the global energy security and efforts to mitigate climate warming. The decisions as to timing and extent of capacity expansion, as well as profitability of future oil production and trade are subject to substantial uncertainty. The transition to alternative energy sources is ultimately inevitable due to physical resource limits coupled with the need for enforcement of stringent low GHG energy policies, as well as potential geopolitical instabilities, constraining the global supply and competitiveness of oil.

OPEC has the potential to dominate the global oil market in the next a few decades, enabling this organization to facilitate or hinder the energy transition policies. This will also allow OPEC to play a key role in the global energy security through cooperative or non-cooperative strategies. OPEC’s supply strategies and production levels can impact the price of oil, which can affect the timing and manner in which the transition will occur. OPEC can utilize its spare crude oil production capacity to help meet the rising demand while stabilizing the price in medium-term. In the long-run, sufficient capital-investment to expand oil production capacity can temporarily improve the global energy security at the expense of exacerbating the global warming. In order to maintain its share in the global energy markets, OPEC may adopt a non-cooperative strategy by driving market prices to lower levels to make the energy production from other sources less competitive. Alternatively, OPEC can contribute to market stability and energy security through a cooperative portfolio management approach that takes advantage of constructive communication with major oil consumers and producers of renewable energies. This approach can help identify opportunities for stabilizing the oil market and contributing to a less turbulent energy transition path, which can benefit all parties through facilitating adaptation to the impending energy crisis within the available lead time.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}