A Stochastic Decision-Making Tool Suite for Distributed Energy Resources Integration in Energy Markets

Abstract

1. Introduction

1.1. Background and Motivation

1.2. Literature Review and Research Gap

1.3. Contributions and Study Layout

- Development of a suite of computational tools encompassing forecasting, uncertainty management, and decision-making capabilities that will be used in a framework for optimal bidding of different types of DER assets (PV, ESS, and DR). These tools will be based on a commercial VPP and will be used for participation in short and medium-term energy market modalities, such as day-ahead markets and bilateral contracting. This suite considers the assumed risk profile in uncertainty management through elements such as stochastic programming [80] and the conditional value-at-risk (CVaR) [81] method.

- A hybrid method for time series forecasting, scenario generation, and reduction has been established. This method is based on the Time2Vec Transformer Encoder, Monte Carlo simulations, and the Fast-Forward reduction methods. It is designed to manage uncertainties in variables such as electricity prices and PV power production.

- Investigation of the effect of mandatory participation policies and risk profiles on optimal bidding decisions for profit maximization with DER assets, specifically ESS. The study proposes a planning support tool in the form of an energy policy sandbox for testing under uncertain regulatory conditions.

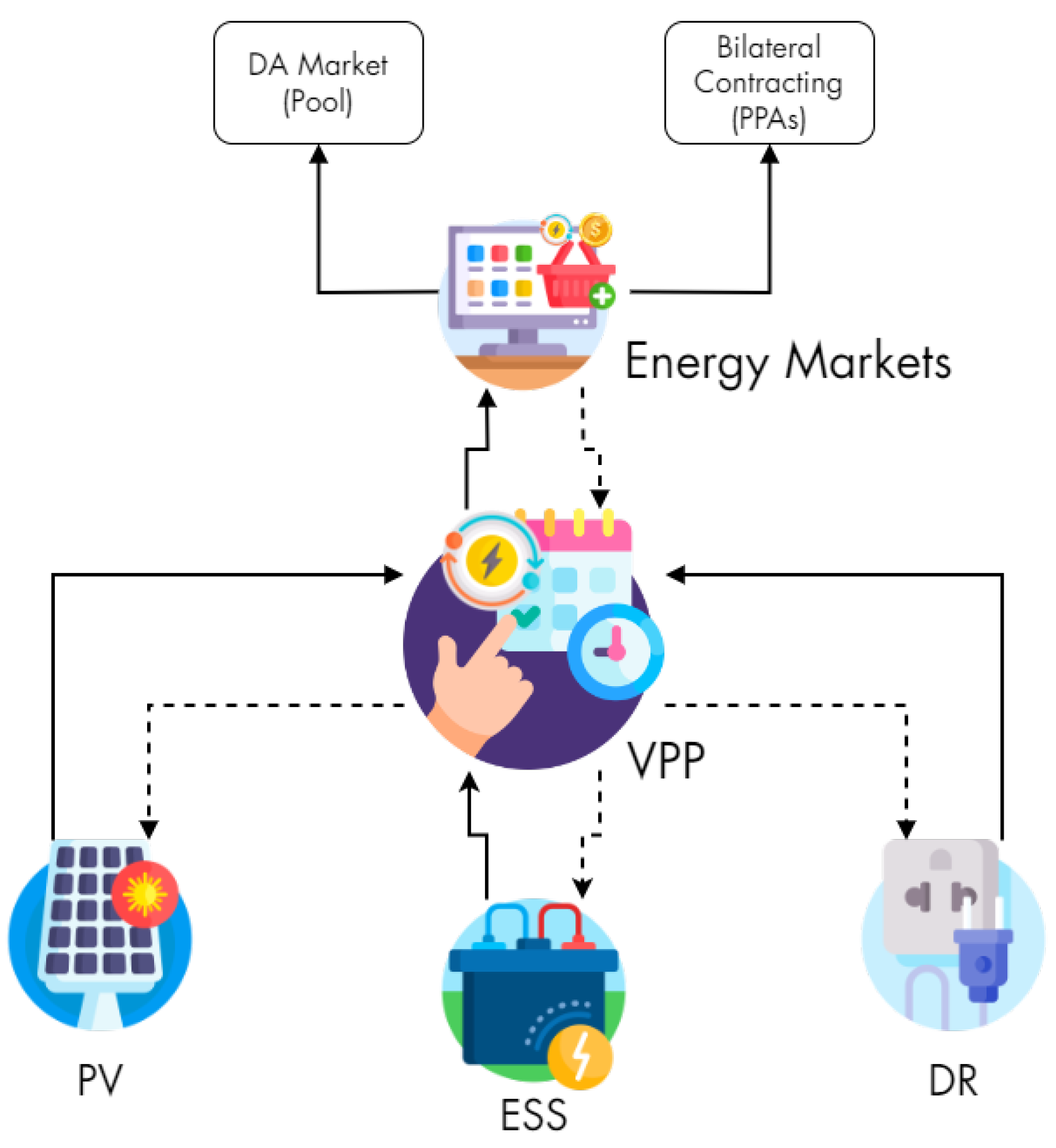

2. Framework of the Decision-Making Tool Suite

2.1. Scenario-Based Uncertainty Representation

2.2. Optimal Bidding Decision-Making Module

3. Results and Discussion

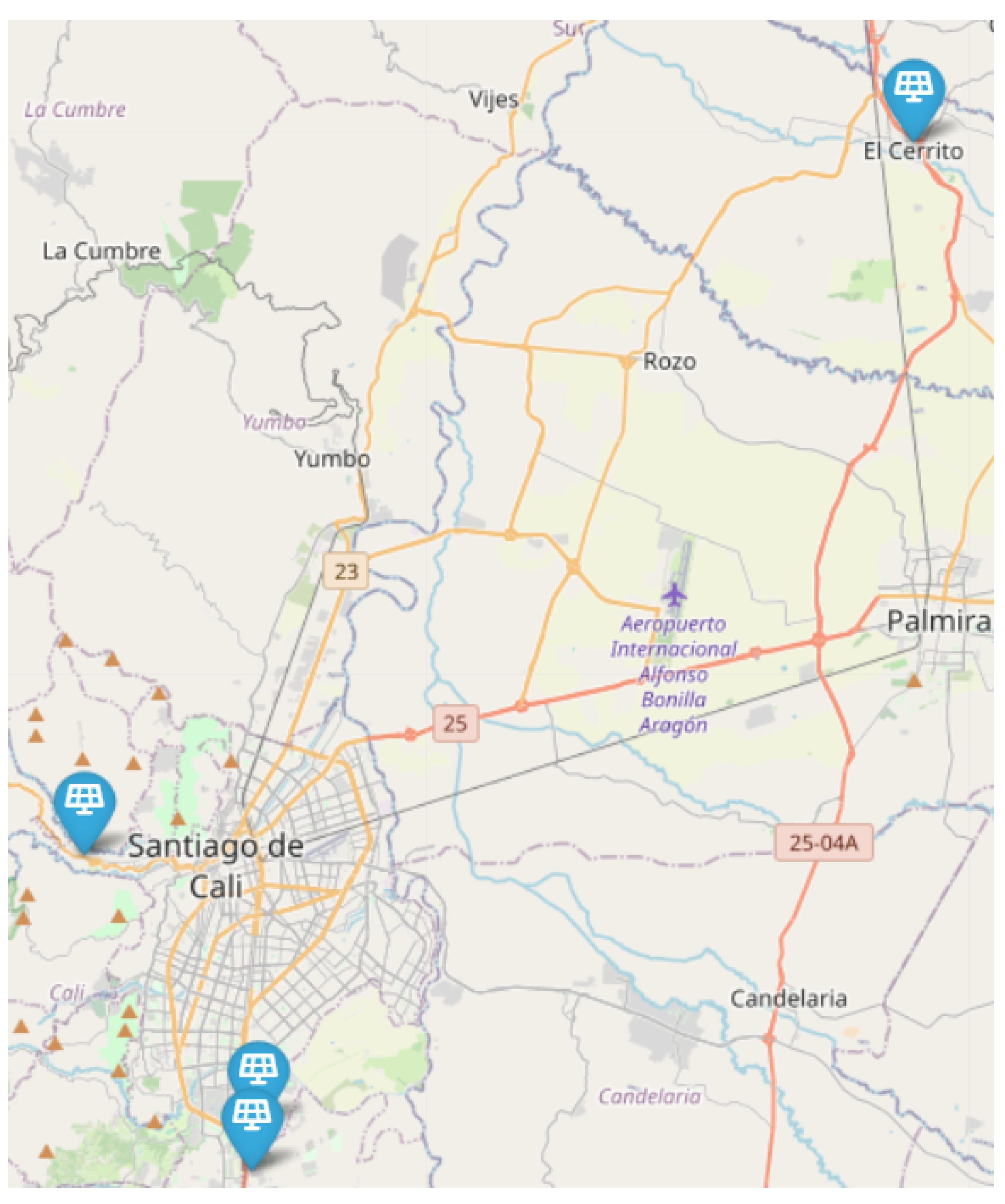

3.1. Input Data

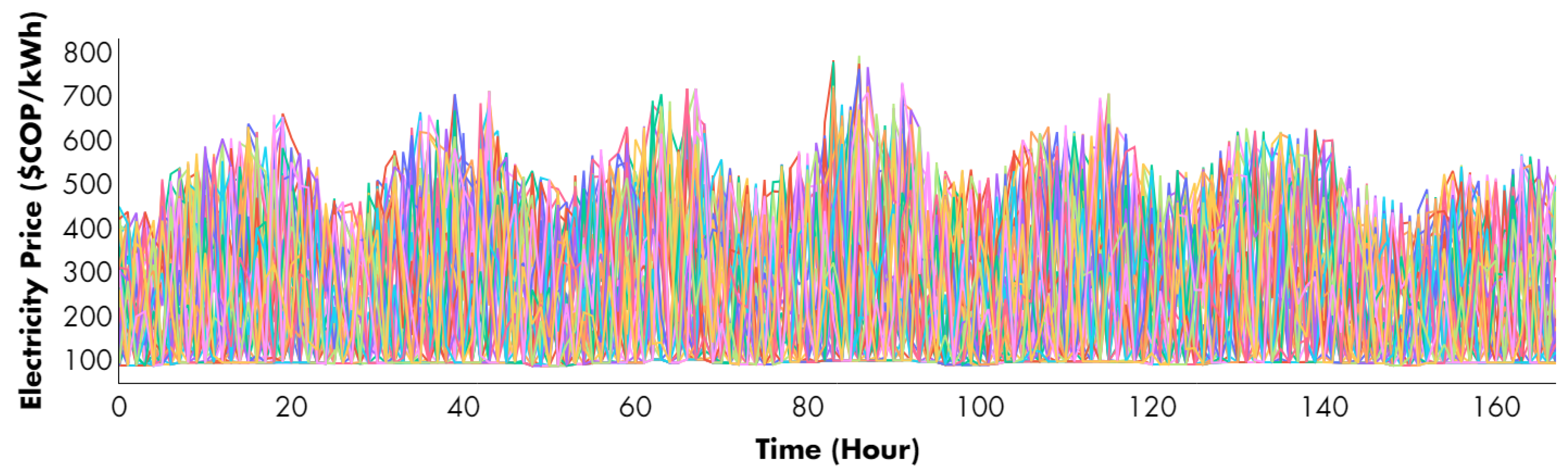

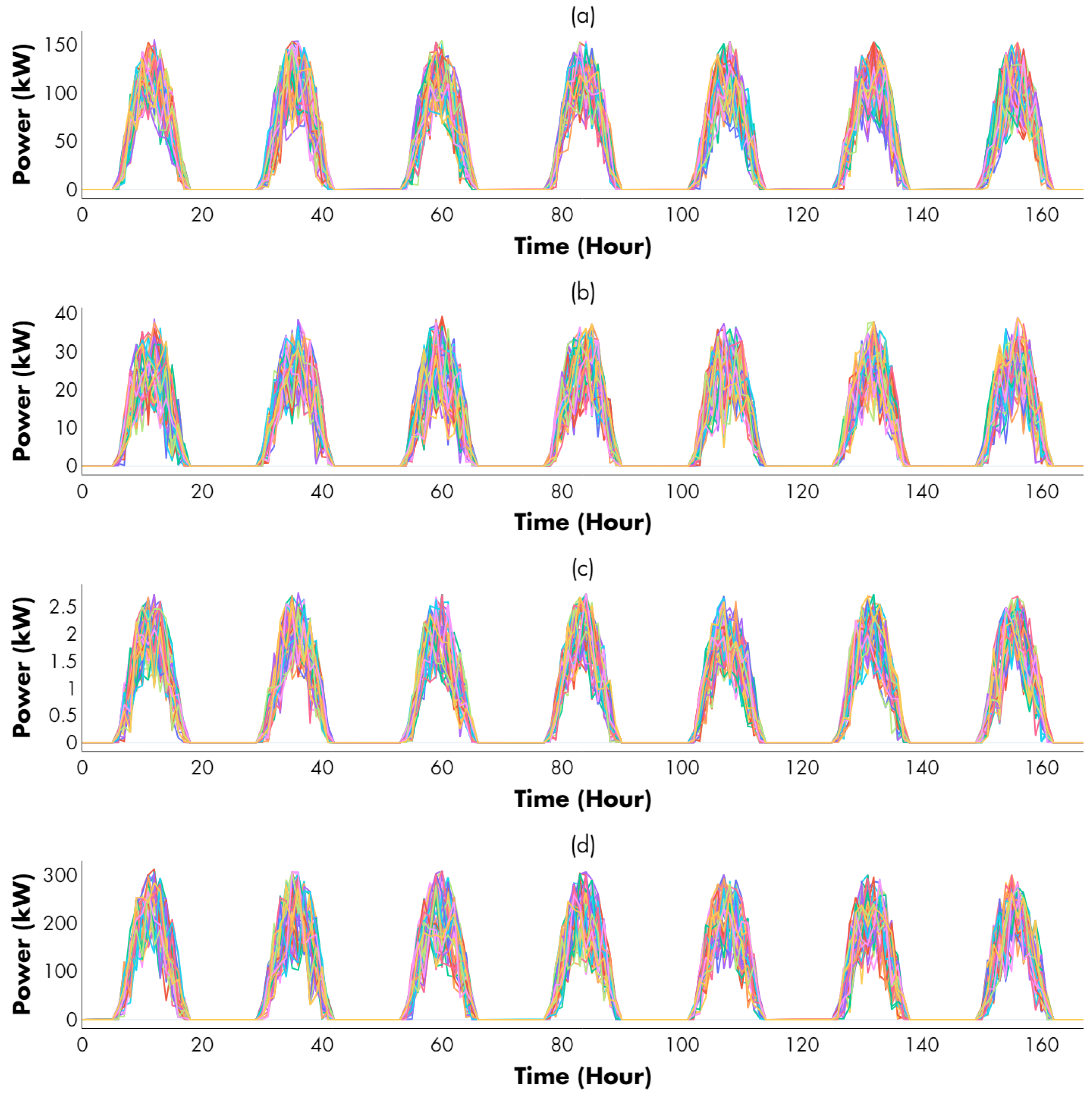

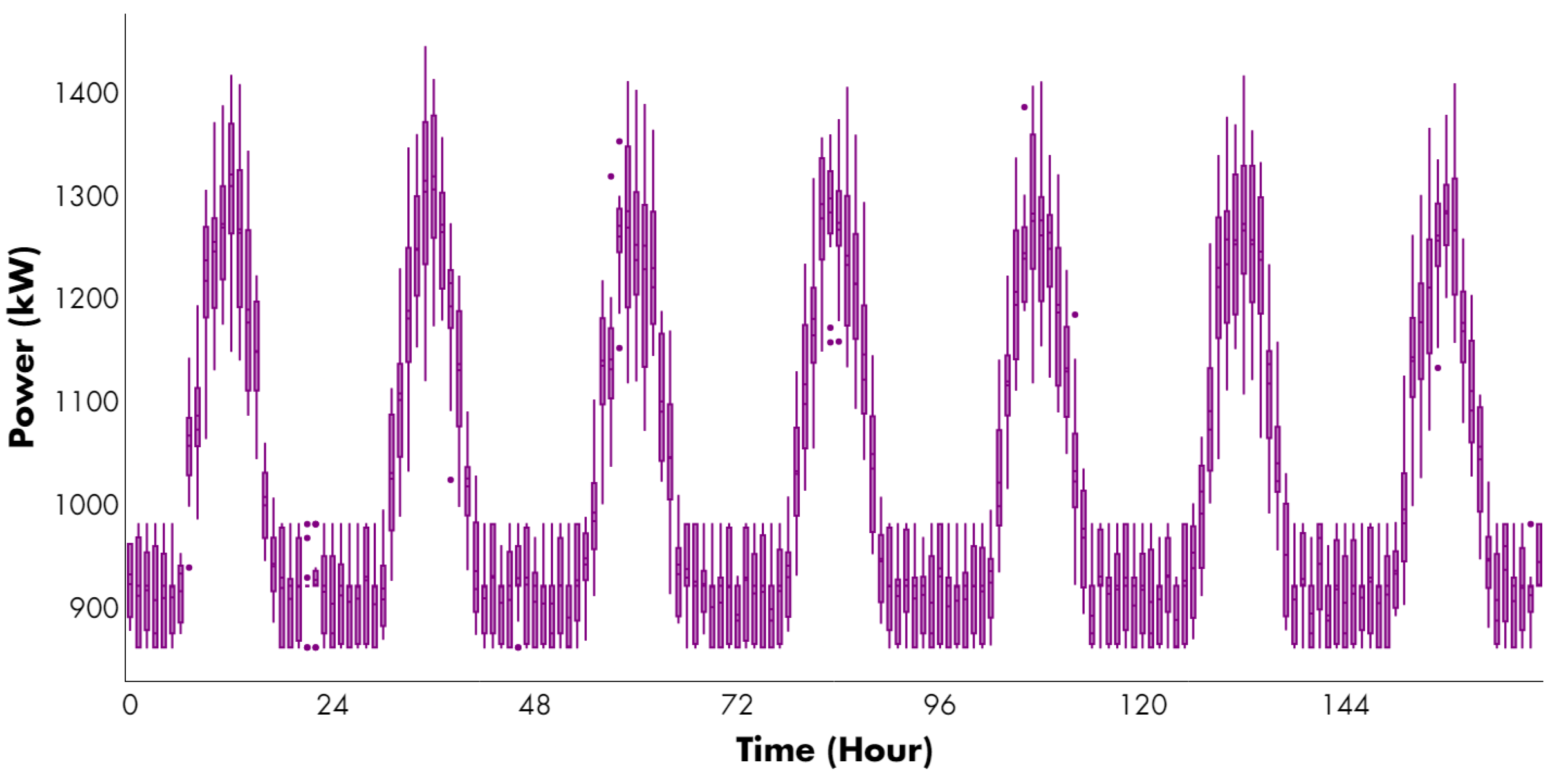

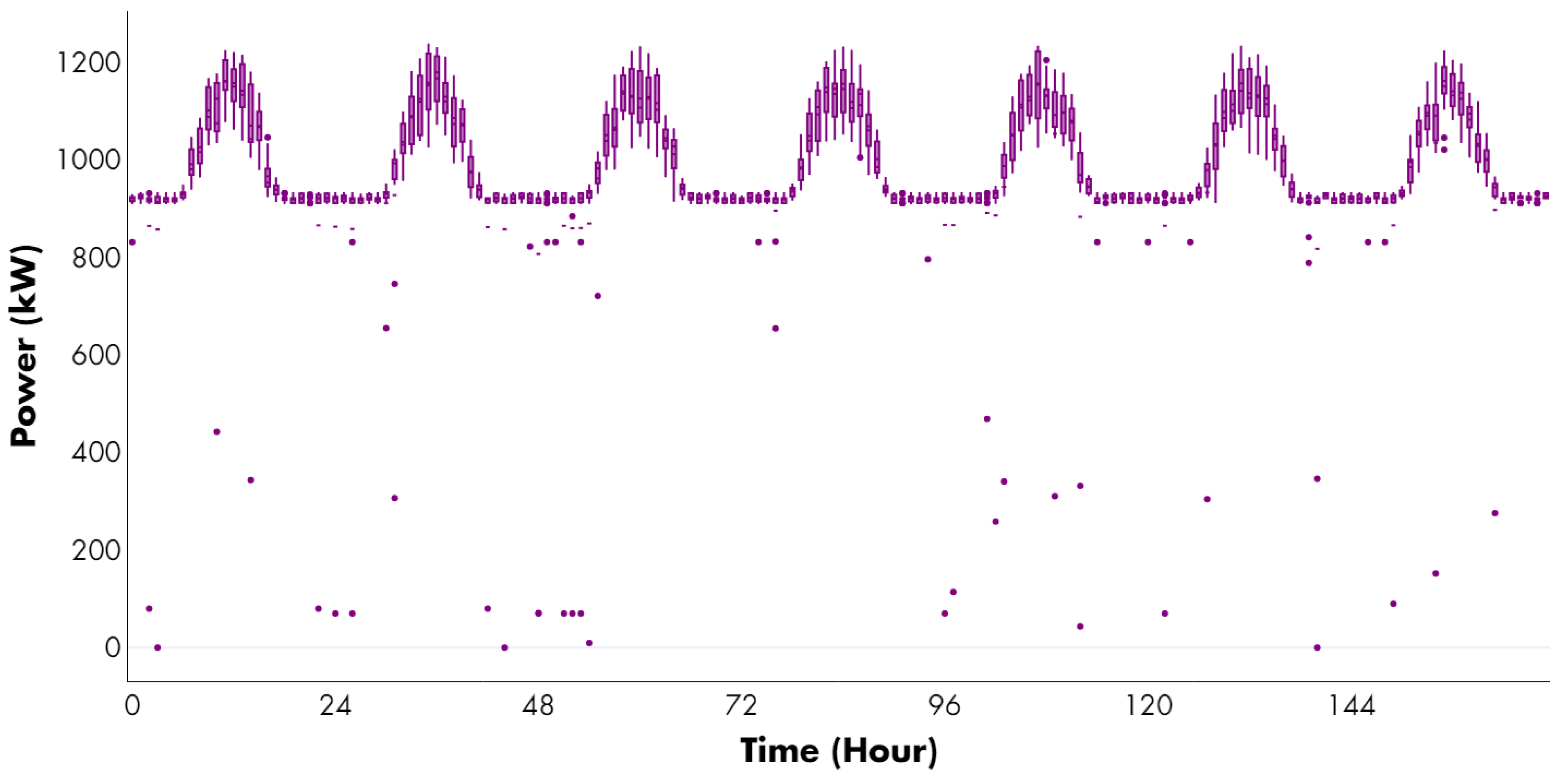

3.1.1. Variables with Uncertainty

3.1.2. Decision-Making Inputs

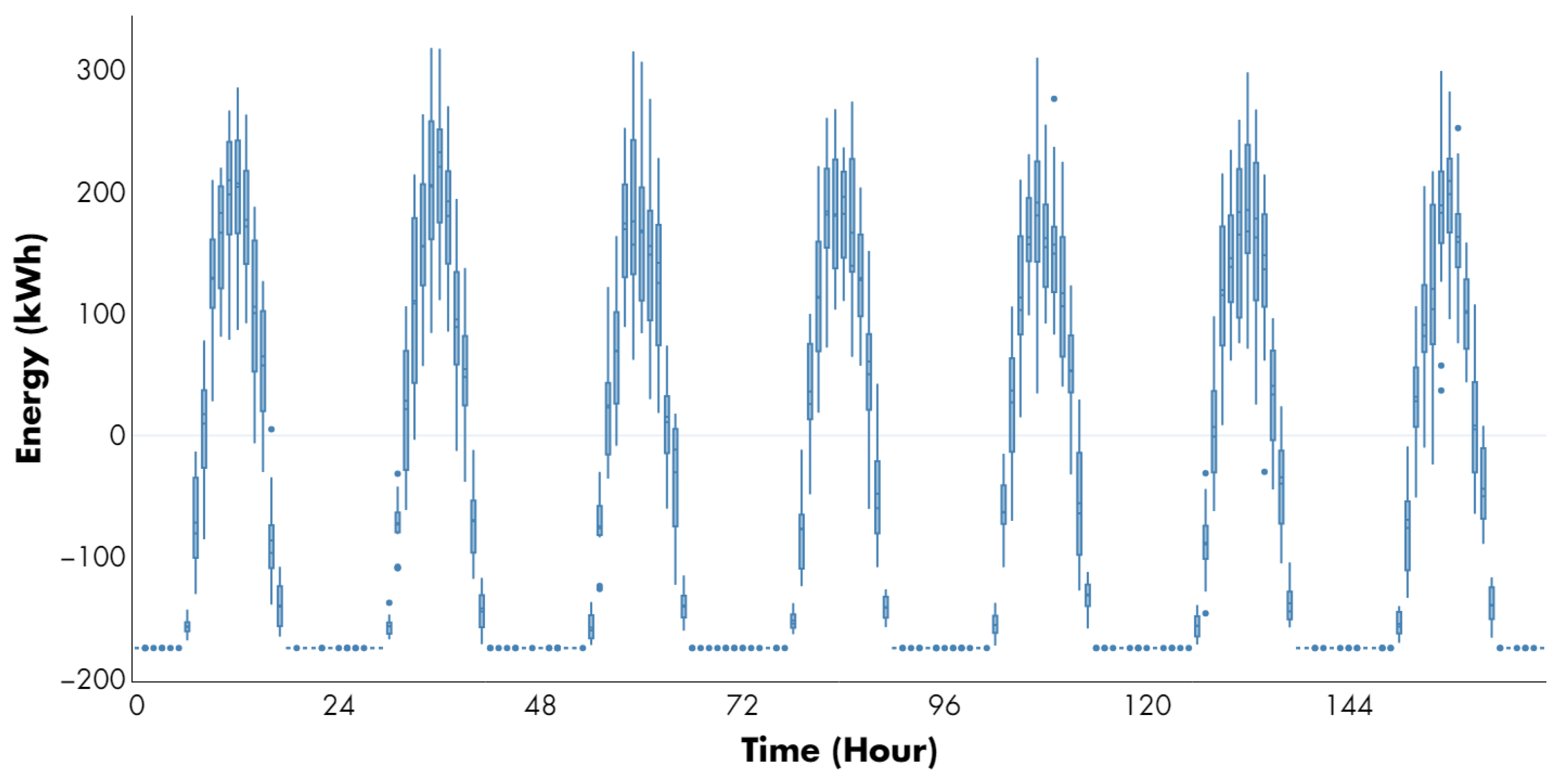

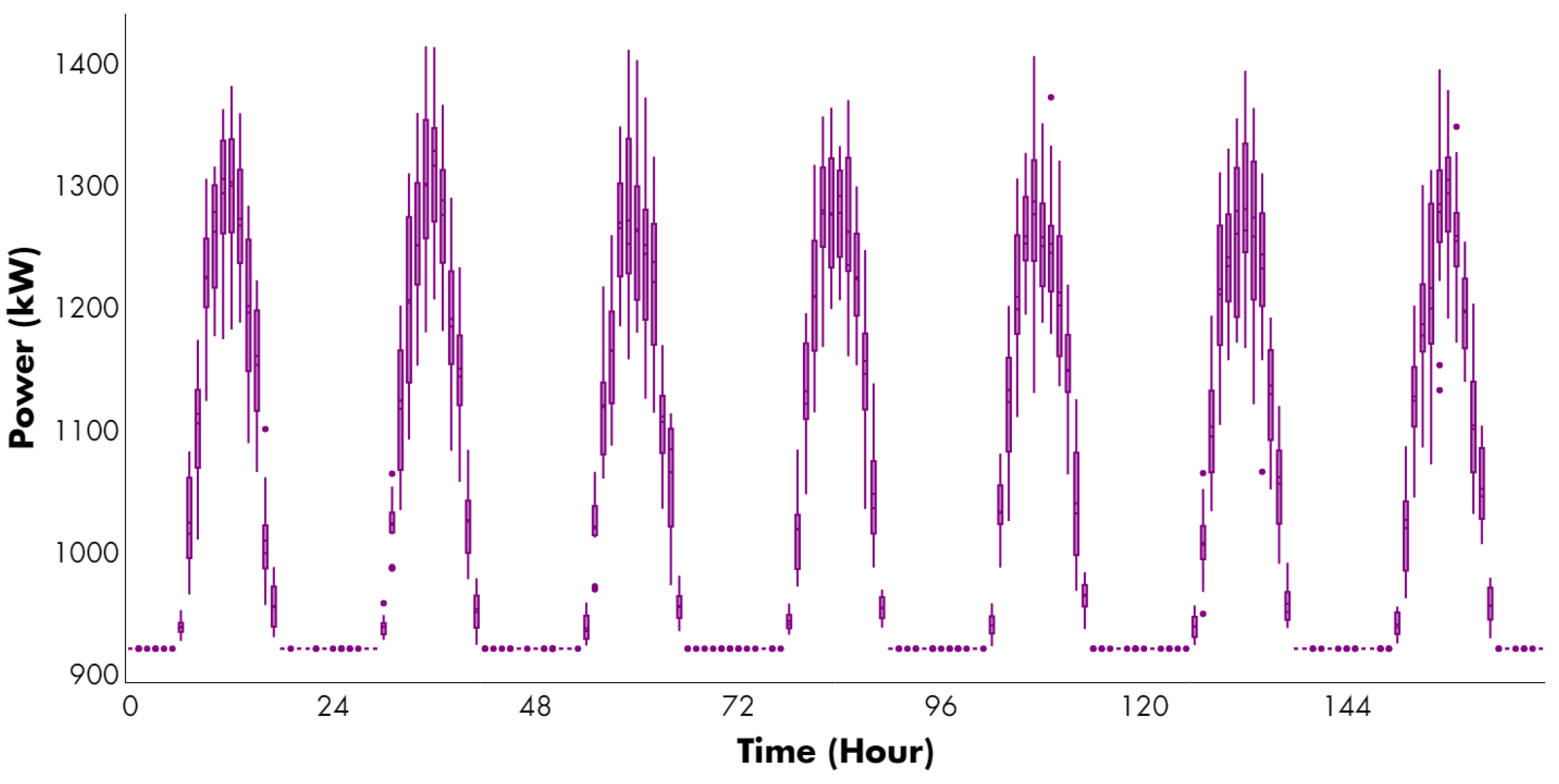

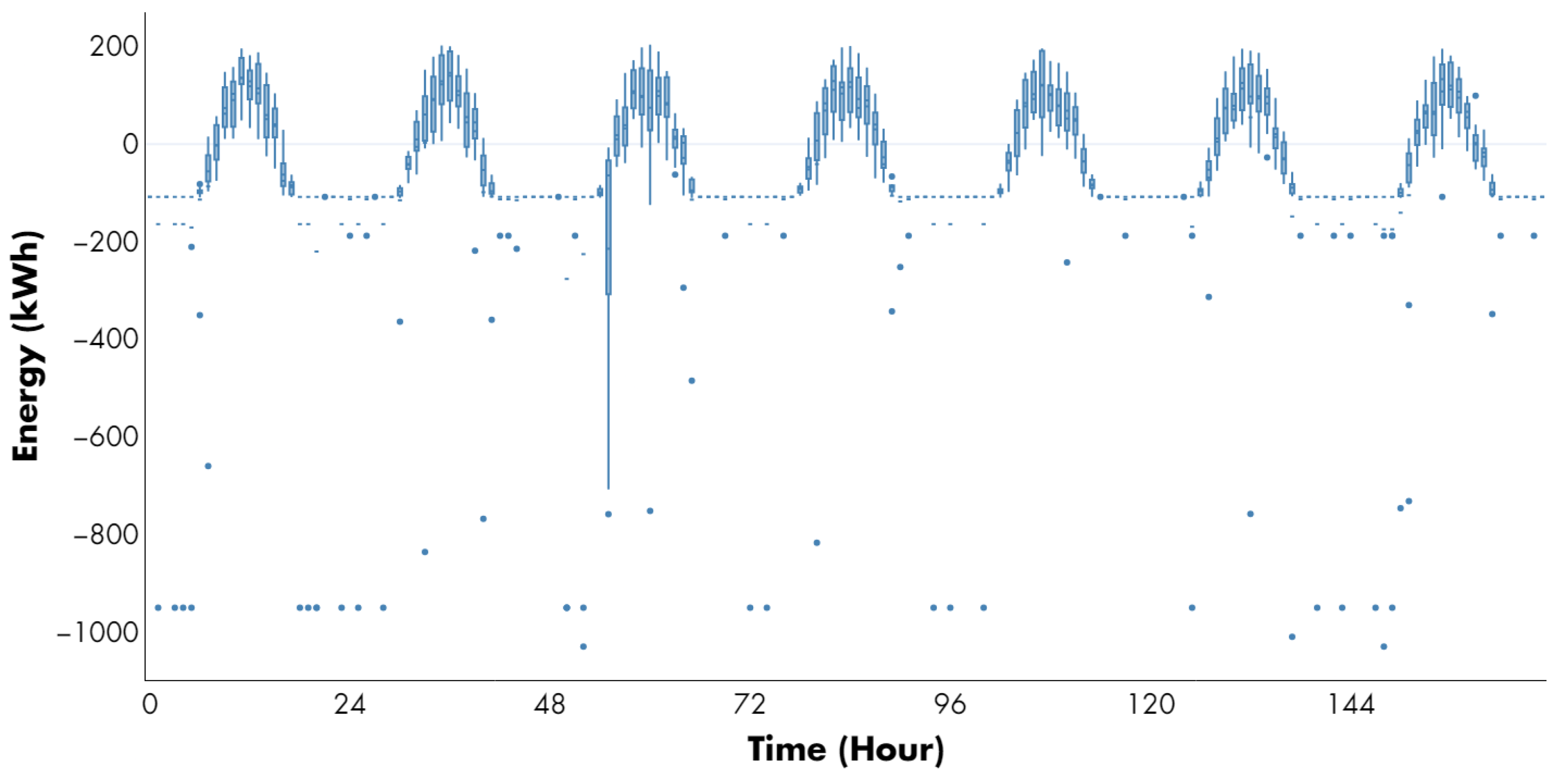

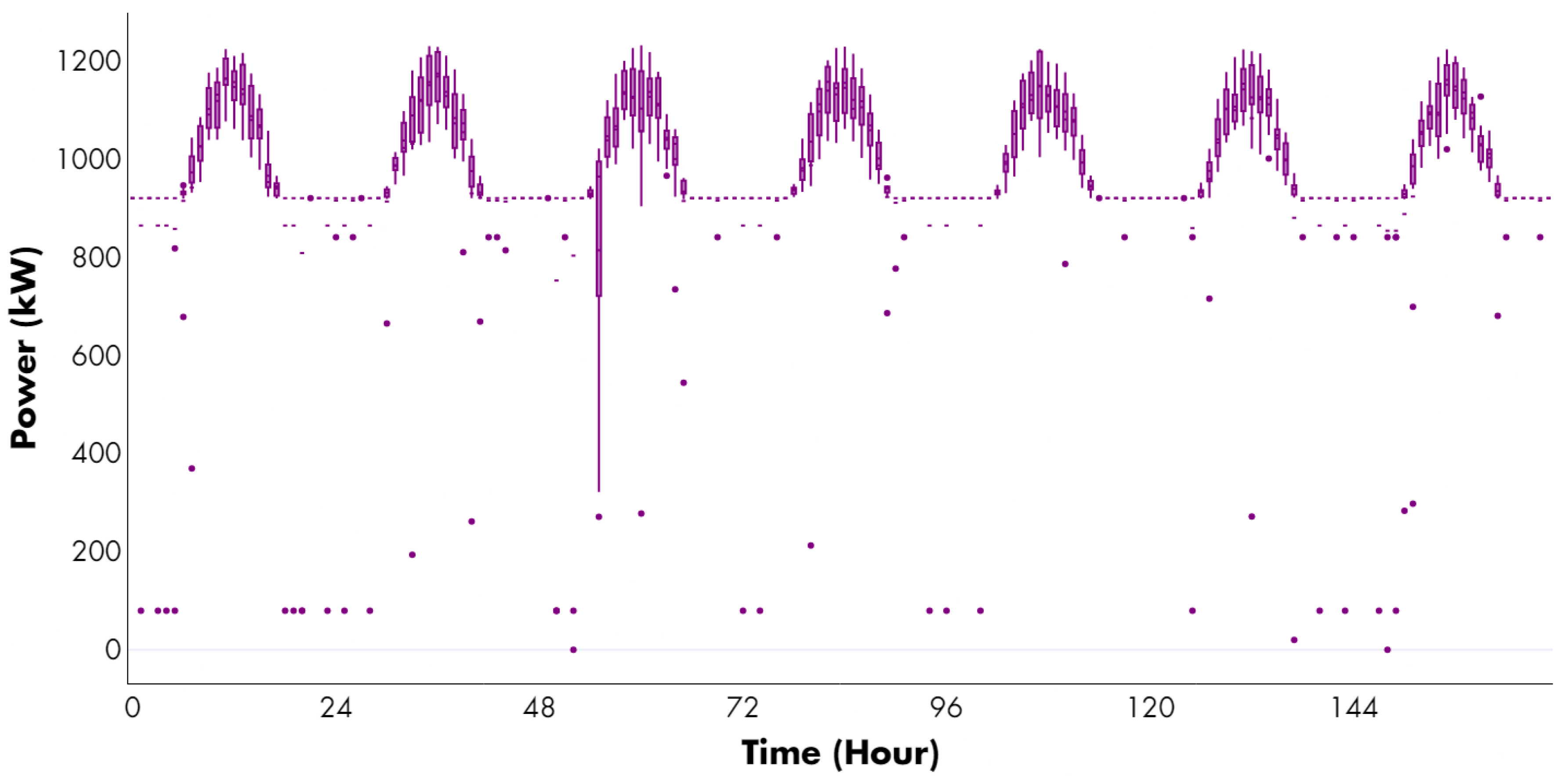

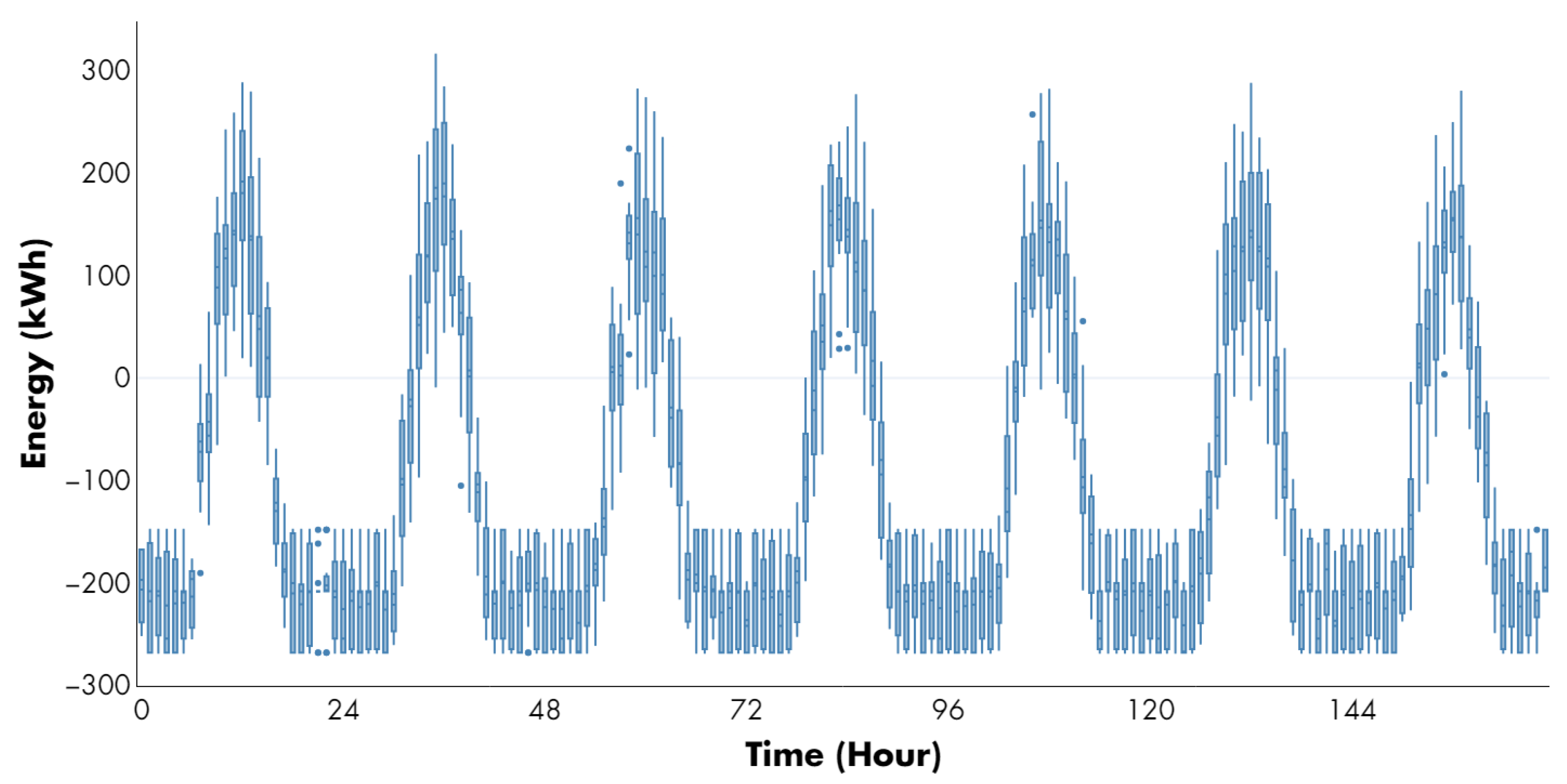

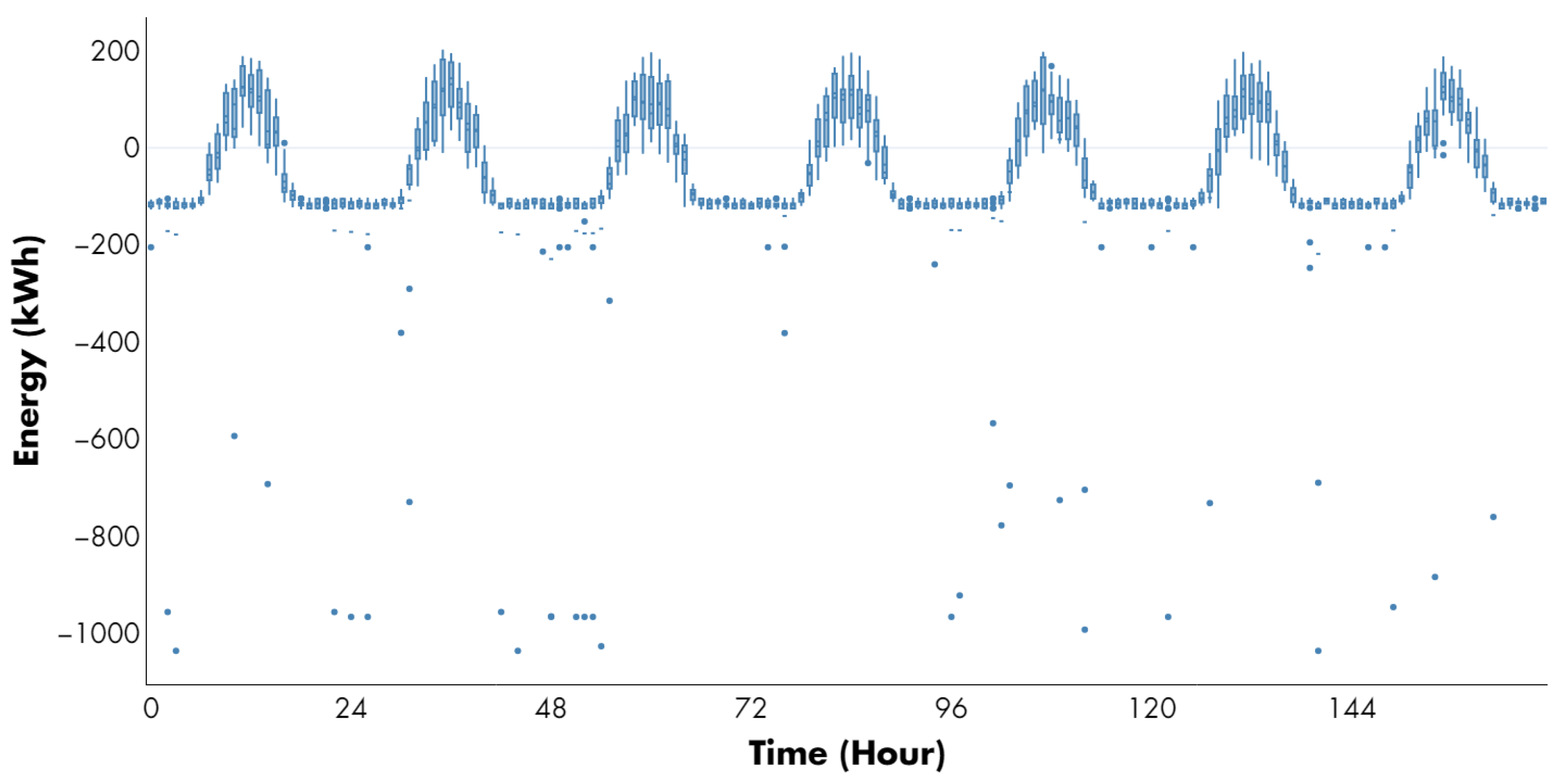

3.2. Simulation Results

- Case 1: Risk-neutral DERs participation in bilateral contracts and day-ahead markets.

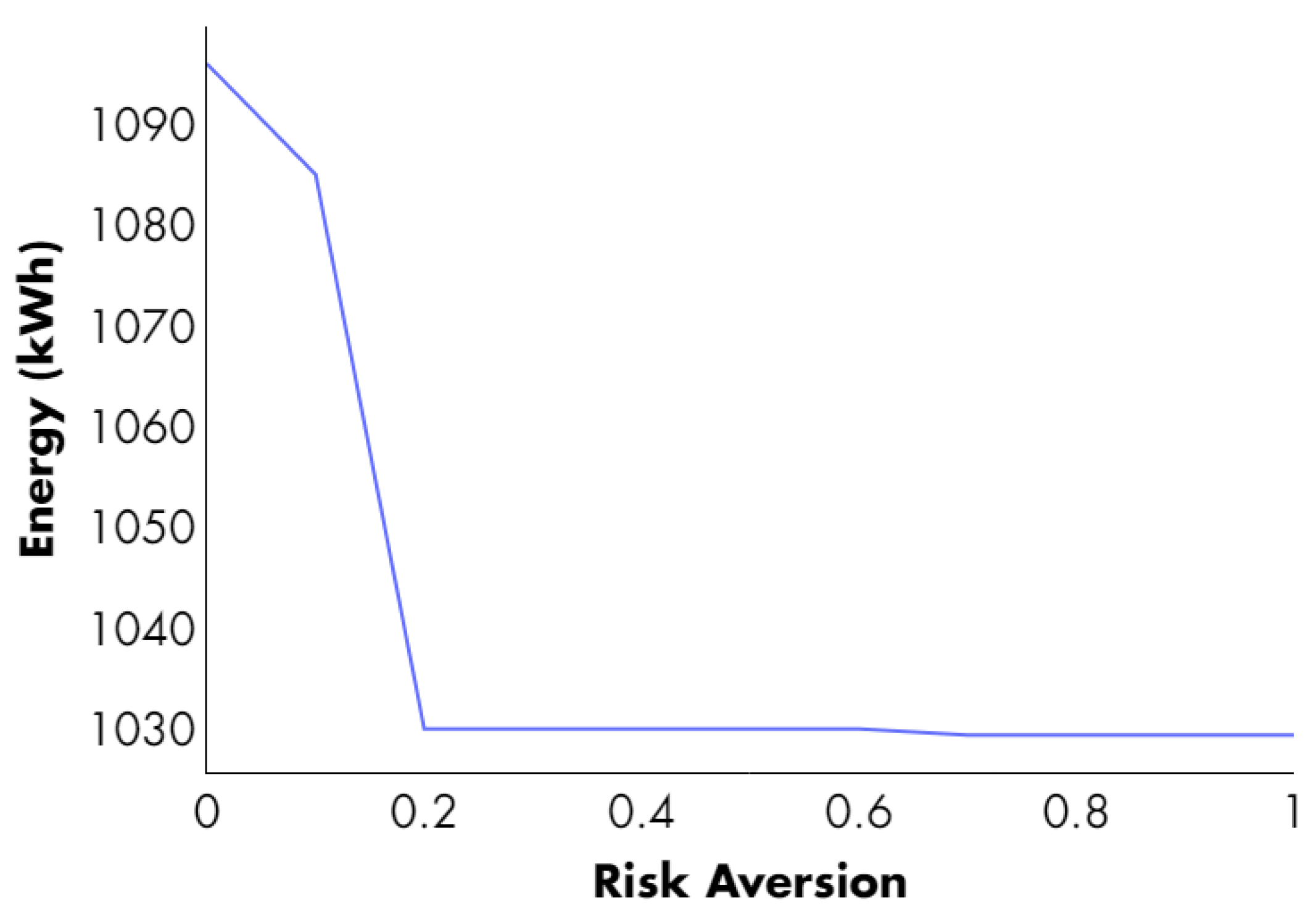

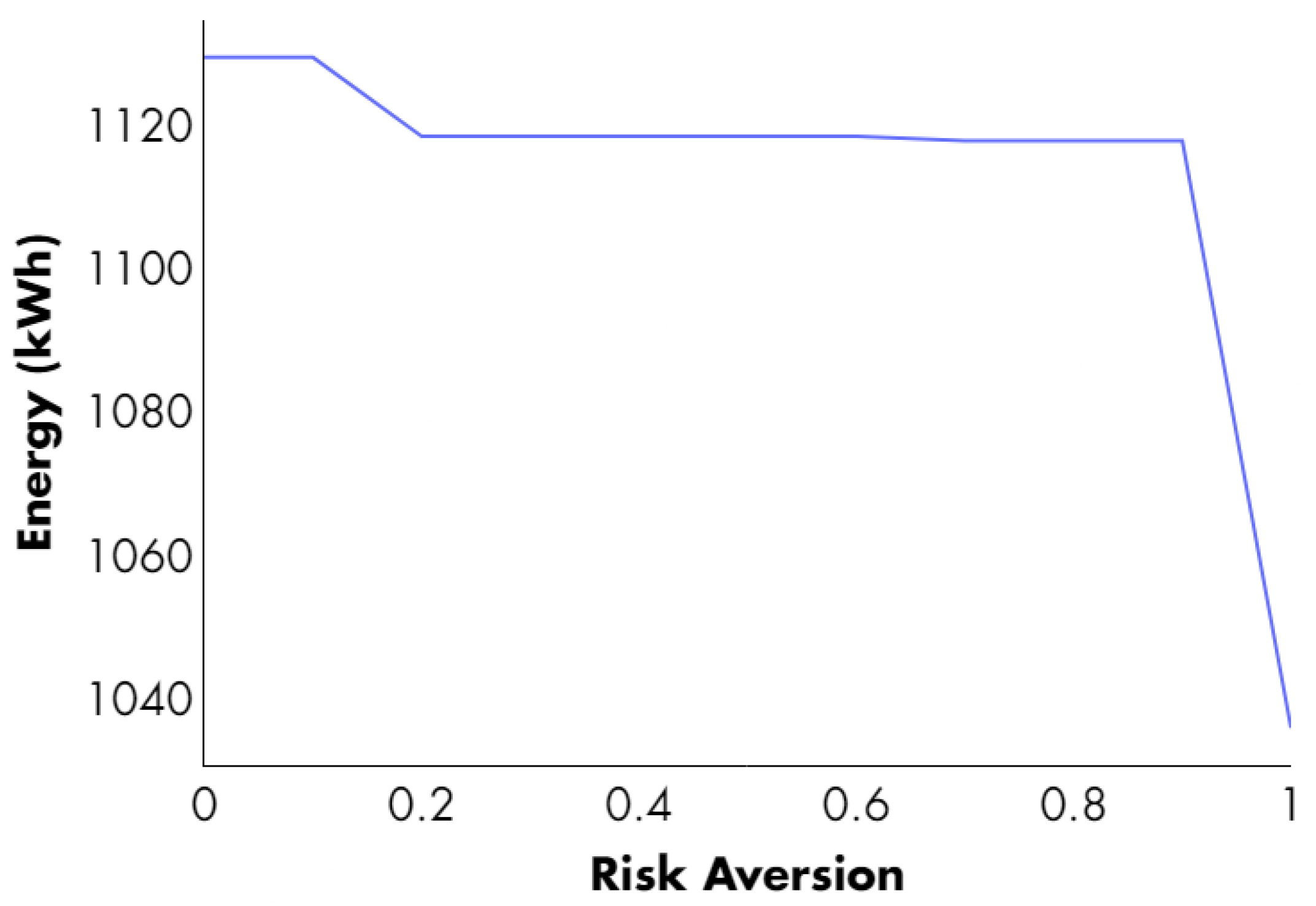

- Case 2: Risk profile incidence on DERs participation in bilateral contracts and day-ahead markets.

- Case 3: Incidence of mandatory participation of certain types of DER (ESS) in the CVPP for bilateral contracts and day-ahead markets.

3.2.1. Case 1

3.2.2. Case 2

3.2.3. Case 3

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| BC | Bilateral Contracting |

| CVPP | Commercial Virtual Power Plant |

| DR | Demand Response |

| DER | Distributed Energy Resources |

| ESS | Energy Storage System |

| ICT | Information and Communication Technologies |

| PV | Photovoltaic units |

| QCQP | Quadratically Constrained Quadratic Programming |

| PPA | Power Purchase Agreement |

| VPP | Virtual Power Plant |

| Sets | |

| H | Set of time periods (time horizon) |

| Set of electricity price and PV production scenarios | |

| Set of PV candidates for bilateral contract signing/day-ahead market agreement | |

| Set of ESS candidates for bilateral contract signing/day-ahead market agreement | |

| Set of DR scheme candidates for bilateral signing/day-ahead market agreement | |

| Indexes | |

| t | Index of time periods (hours) ranging from 1 to H |

| j | Index of PV units ranging from 1 to |

| e | Index of ESS units ranging from 1 to |

| d | Index of DR schemes ranging from 1 to |

| s | Index of electricity price and PV production scenarios ranging from 1 to |

| Constants | |

| Sale price of bilateral contract ($ COP/kWh) | |

| Maximum amount that can be sold in bilateral contracting (kWh) | |

| CVaR Confidence level | |

| Weighting factor to balance expected profit and CVaR (risk profile). | |

| Parameters | |

| Probability of occurrence of operating scenario s | |

| Pool market price in period t and scenario s ($ COP/kWh) | |

| Power production of PV unit j in time t and scenario s (kW) | |

| Capacity offer price declared by the owner of PV unit j ($ COP/kWh) | |

| Capacity offer price declared by the owner of ESS unit e ($ COP/kWh) | |

| Capacity offer price declared by the provider of DR scheme d ($ COP/kWh) | |

| Capacity of PV unit j during a medium-term period declared by its owner (kW) | |

| Capacity of ESS unit e declared by its owner (kW) | |

| Upper limit of curtailing power of DR scheme d declared by its provider (kW) | |

| Depth of discharge window width of ESS unit e declared by its owner | |

| Maximum charging rate of ESS unit e declared by its owner (kW) | |

| Maximum discharging rate of ESS unit e declared by its owner(kW) | |

| Initial energy of ESS unit e declared by its owner for all scenarios (kWh) | |

| Charging/discharging efficiency of ESS unit e | |

| Discharge contribution factor (over 24 h) of ESS unit e | |

| Variables | |

| VPP available power of for the period t and operative scenario s (kW) | |

| Percentage of max power of the VPP that is willing to be supplied via PPAs | |

| Fraction of the maximum power that can be contracted by the CVPP via PPAs (kW) | |

| Binary variable set to 1 if PV unit j is contracted. | |

| Binary variable set to 1 if ESS unit e is contracted | |

| Binary variable set to 1 if DR scheme d is contracted | |

| Binary variable set to 1 if ESS unit e is charged/discharged in time t and scenario s | |

| Power charged to ESS unit e for time t and scenario s (kW) | |

| Power discharged to ESS unit e for time t and scenario s (kW) | |

| Power of ESS unit e in period t and scenario s (kW) | |

| Power curtailed by demand response d for time t and scenario s (kW) | |

| Amount of VPP power curtailed for period t and scenario s (kW). | |

| Power sold (+)/purchased (−) in the pool market for period t and scenario s (kW). | |

| Energy level of ESS unit e in time t and scenario s (kWh) | |

| Value-at-Risk (VaR) | |

References

- Asif, M. Introduction to the Four-Dimensional Energy Transition. In The 4Ds of Energy Transition: Decarbonization, Decentralization, Decreasing Use and Digitalization; King Fahd University of Petroleum and Minerals: Dhahran, Saudi Arabia, 2022; pp. 1–10. [Google Scholar]

- Rajendran, K.; Ezhil Prabhu, M. Energy Transition Landscape: Landscape Approach for Pollution-Generating Large-Scale Industries. In Handbook of Research on Issues, Challenges, and Opportunities in Sustainable Architecture; IGI Global: Hershey, PA, USA, 2022; pp. 248–282. [Google Scholar]

- Bellizio, F.; Xu, W.; Qiu, D.; Ye, Y.; Papadaskalopoulos, D.; Cremer, J.L.; Teng, F.; Strbac, G. Transition to Digitalized Paradigms for Security Control and Decentralized Electricity Market. Proc. IEEE 2022, 111, 744–761. [Google Scholar] [CrossRef]

- Borowski, P.F. Digital Transformation and Prosumers Activities in the Energy Sector. In Intelligent Systems in Digital Transformation: Theory and Applications; Springer: Berlin/Heidelberg, Germany, 2022; pp. 129–150. [Google Scholar]

- Çelık, D.; Meral, M.E.; Waseem, M. A new area towards to digitalization of energy systems: Enables, challenges and solutions. In Proceedings of the 2022 14th International Conference on Electronics, Computers and Artificial Intelligence (ECAI), Ploiesti, Romania, 30 June–1 July 2022; IEEE: Piscataway, NJ, USA, 2022; pp. 1–6. [Google Scholar]

- Hargroves, K.; James, B.; Lane, J.; Newman, P. The Role of Distributed Energy Resources and Associated Business Models in the Decentralised Energy Transition: A Review. Energies 2023, 16, 4231. [Google Scholar] [CrossRef]

- Christakou, K. A unified control strategy for active distribution networks via demand response and distributed energy storage systems. Sustain. Energy Grids Netw. 2016, 6, 1–6. [Google Scholar] [CrossRef]

- Ghasemi, A.; Shojaeighadikolaei, A.; Hashemi, M. Combating Uncertainties in Wind and Distributed PV Energy Sources Using Integrated Reinforcement Learning and Time-Series Forecasting. arXiv 2023, arXiv:2302.14094. [Google Scholar]

- Valova, R.; Brown, G. Distributed Energy Resource Interconnection: An Overview of Challenges and Opportunities in the United States. Sol. Compass 2022, 2, 100021. [Google Scholar] [CrossRef]

- Asif, M. Decentralization in Energy Sector. In The 4Ds of Energy Transition: Decarbonization, Decentralization, Decreasing Use and Digitalization; King Fahd University of Petroleum and Minerals: Dhahran, Saudi Arabia, 2022; pp. 287–297. [Google Scholar]

- Soshinskaya, M.; Crijns-Graus, W.H.; Guerrero, J.M.; Vasquez, J.C. Microgrids: Experiences, barriers and success factors. Renew. Sustain. Energy Rev. 2014, 40, 659–672. [Google Scholar] [CrossRef]

- Asmus, P. Microgrids, virtual power plants and our distributed energy future. Electr. J. 2010, 23, 72–82. [Google Scholar] [CrossRef]

- Merino, J.; Gómez, I.; Fraile-Ardanuy, J.; Santos, M.; Cortés, A.; Jimeno, J.; Madina, C. Fostering DER integration in the electricity markets. In Distributed Energy Resources in Local Integrated Energy Systems; Elsevier: Amsterdam, The Netherlands, 2021; pp. 175–205. [Google Scholar]

- Zahraoui, Y.; Korõtko, T.; Rosin, A.; Agabus, H. Market Mechanisms and Trading in Microgrid Local Electricity Markets: A Comprehensive Review. Energies 2023, 16, 2145. [Google Scholar] [CrossRef]

- Dinther, C.v.; Flath, C.M.; Gaerttner, J.; Huber, J.; Mengelkamp, E.; Schuller, A.; Staudt, P.; Weidlich, A. Engineering energy markets: The past, the present, and the future. In Market Engineering: Insights from Two Decades of Research on Markets and Information; Springer: Berlin/Heidelberg, Germany, 2021; pp. 113–134. [Google Scholar]

- González, D.M.L.; Rendon, J.G. Opportunities and challenges of mainstreaming distributed energy resources towards the transition to more efficient and resilient energy markets. Renew. Sustain. Energy Rev. 2022, 157, 112018. [Google Scholar] [CrossRef]

- Guzman, C.P.; Bañol Arias, N.; Franco, J.F.; Rider, M.J.; Romero, R. Enhanced coordination strategy for an aggregator of distributed energy resources participating in the day-ahead reserve market. Energies 2020, 13, 1965. [Google Scholar] [CrossRef]

- Pudjianto, D.; Ramsay, C.; Strbac, G. Virtual power plant and system integration of distributed energy resources. IET Renew. Power Gener. 2007, 1, 10–16. [Google Scholar] [CrossRef]

- Ekanayake, J.B.; Jenkins, N.; Liyanage, K.M.; Wu, J.; Yokoyama, A. Smart Grid: Technology and Applications; John Wiley & Sons: Hoboken, NJ, USA, 2012. [Google Scholar]

- Nosratabadi, S.M.; Hooshmand, R.A.; Gholipour, E. A comprehensive review on microgrid and virtual power plant concepts employed for distributed energy resources scheduling in power systems. Renew. Sustain. Energy Rev. 2017, 67, 341–363. [Google Scholar] [CrossRef]

- Khajeh, H.; Akbari Foroud, A.; Firoozi, H. Robust bidding strategies and scheduling of a price-maker microgrid aggregator participating in a pool-based electricity market. IET Gener. Transm. Distrib. 2019, 13, 468–477. [Google Scholar] [CrossRef]

- Dabbagh, S.R.; Sheikh-El-Eslami, M.K. Risk assessment of virtual power plants offering in energy and reserve markets. IEEE Trans. Power Syst. 2015, 31, 3572–3582. [Google Scholar] [CrossRef]

- Zhang, G.; Jiang, C.; Wang, X. Comprehensive review on structure and operation of virtual power plant in electrical system. IET Gener. Transm. Distrib. 2019, 13, 145–156. [Google Scholar] [CrossRef]

- Naval, N.; Yusta, J.M. Virtual power plant models and electricity markets-A review. Renew. Sustain. Energy Rev. 2021, 149, 111393. [Google Scholar] [CrossRef]

- Gómez San Román, T. Integration of DERs on Power Systems: Challenges and Opportunities; SSRN: Barcelona, Spain, 2017. [Google Scholar]

- Gough, M.; Santos, S.F.; Lotfi, M.; Javadi, M.S.; Osório, G.J.; Ashraf, P.; Castro, R.; Catalão, J.P. Operation of a technical virtual power plant considering diverse distributed energy resources. IEEE Trans. Ind. Appl. 2022, 58, 2547–2558. [Google Scholar] [CrossRef]

- Essakiappan, S.; Shoubaki, E.; Koerner, M.; Rees, J.F.; Enslin, J. Dispatchable Virtual Power Plants with forecasting and decentralized control, for high levels of distributed energy resources grid penetration. In Proceedings of the 2017 IEEE 8th International Symposium on Power Electronics for Distributed Generation Systems (PEDG), Florianópolis, Brazil, 17–20 April 2017; IEEE: Piscataway, NJ, USA, 2017; pp. 1–8. [Google Scholar]

- Wang, X.; Liu, Z.; Zhang, H.; Zhao, Y.; Shi, J.; Ding, H. A review on virtual power plant concept, application and challenges. In Proceedings of the 2019 IEEE Innovative Smart Grid Technologies-Asia (ISGT Asia), Chengdu, China, 21–24 May 2019; pp. 4328–4333. [Google Scholar]

- Pal, P.; Parvathy, A.; Devabalaji, K. A broad review on optimal operation of Virtual power plant. In Proceedings of the 2019 2nd International Conference on Power and Embedded Drive Control (ICPEDC), Chennai, India, 21–23 August 2019; IEEE: Piscataway, NJ, USA, 2019; pp. 400–405. [Google Scholar]

- Hadayeghparast, S.; Farsangi, A.S.; Shayanfar, H. Day-ahead stochastic multi-objective economic/emission operational scheduling of a large scale virtual power plant. Energy 2019, 172, 630–646. [Google Scholar] [CrossRef]

- Cheng, L.; Zhou, X.; Yun, Q.; Tian, L.; Wang, X.; Liu, Z. A review on virtual power plants interactive resource characteristics and scheduling optimization. In Proceedings of the 2019 IEEE 3rd Conference on Energy Internet and Energy System Integration (EI2), Changsha, China, 8–10 November 2019; IEEE: Piscataway, NJ, USA, 2019; pp. 514–519. [Google Scholar]

- Lehmbruck, L.; Kretz, J.; Aengenvoort, J.; Sioshansi, F. Aggregation of front-and behind-the-meter: The evolving VPP business model. In Behind and Beyond the Meter; Elsevier: Amsterdam, The Netherlands, 2020; pp. 211–232. [Google Scholar]

- Naughton, J.; Wang, H.; Riaz, S.; Cantoni, M.; Mancarella, P. Optimization of multi-energy virtual power plants for providing multiple market and local network services. Electr. Power Syst. Res. 2020, 189, 106775. [Google Scholar] [CrossRef]

- Dehghanniri, M.F.; Golkar, M.A.; Olanlari, F.G. Power exchanging of a VPP with its neighboring VPPs and participating in Day-ahead and spinning reserve markets. In Proceedings of the 2022 30th International Conference on Electrical Engineering (ICEE), Tehran, Iran, 17–19 May 2022; IEEE: Piscataway, NJ, USA, 2022; pp. 336–340. [Google Scholar]

- Nezamabadi, H.; Setayesh Nazar, M. Arbitrage strategy of virtual power plants in energy, spinning reserve and reactive power markets. IET Gener. Transm. Distrib. 2016, 10, 750–763. [Google Scholar] [CrossRef]

- Liu, J.; Hu, H.; Yu, S.S.; Trinh, H. Virtual Power Plant with Renewable Energy Sources and Energy Storage Systems for Sustainable Power Grid-Formation, Control Techniques and Demand Response. Energies 2023, 16, 3705. [Google Scholar] [CrossRef]

- Hua, H.; Chen, X.; Gan, L.; Sun, J.; Dong, N.; Liu, D.; Qin, Z.; Li, K.; Hu, S. Demand-side Joint Electricity and Carbon Trading Mechanism. IEEE Trans. Ind. Cyber-Phys. Syst. 2023, 2, 14–25. [Google Scholar] [CrossRef]

- Yang, Q.; Wang, H.; Wang, T.; Zhang, S.; Wu, X.; Wang, H. Blockchain-based decentralized energy management platform for residential distributed energy resources in a virtual power plant. Appl. Energy 2021, 294, 117026. [Google Scholar] [CrossRef]

- Cioara, T.; Antal, M.; Mihailescu, V.T.; Antal, C.D.; Anghel, I.M.; Mitrea, D. Blockchain-based decentralized virtual power plants of small prosumers. IEEE Access 2021, 9, 29490–29504. [Google Scholar] [CrossRef]

- Gough, M.; Santos, S.F.; Almeida, A.; Lotfi, M.; Javadi, M.S.; Fitiwi, D.Z.; Osório, G.J.; Castro, R.; Catalão, J.P. Blockchain-based transactive energy framework for connected virtual power plants. IEEE Trans. Ind. Appl. 2021, 58, 986–995. [Google Scholar] [CrossRef]

- Sarmiento-Vintimilla, J.C.; Torres, E.; Larruskain, D.M.; Pérez-Molina, M.J. Applications, operational architectures and development of virtual power plants as a strategy to facilitate the integration of distributed energy resources. Energies 2022, 15, 775. [Google Scholar] [CrossRef]

- Nguyen-Duc, H.; Nguyen-Hong, N. A study on the bidding strategy of the Virtual Power Plant in energy and reserve market. Energy Rep. 2020, 6, 622–626. [Google Scholar] [CrossRef]

- Wang, H.; Cheng, Y.; Liu, C.; Gao, H.; Liu, J. Robust Optimization Day-ahead Trading Strategy for Virtual Power Plant in Energy Market. In Proceedings of the 2023 Panda Forum on Power and Energy (PandaFPE), Chengdu, China, 27–30 April 2023; IEEE: Piscataway, NJ, USA, 2023; pp. 2346–2350. [Google Scholar]

- Ghasemi-Olanlari, F.; Moradi-Sepahvand, M.; Amraee, T. Two-stage risk-constrained stochastic optimal bidding strategy of virtual power plant considering distributed generation outage. IET Gener. Transm. Distrib. 2023, 17, 1884–1901. [Google Scholar] [CrossRef]

- Shabanzadeh, M.; Sheikh-El-Eslami, M.K.; Haghifam, M.R. A medium-term coalition-forming model of heterogeneous DERs for a commercial virtual power plant. Appl. Energy 2016, 169, 663–681. [Google Scholar] [CrossRef]

- Jafari, M.; Foroud, A.A. A medium/long-term auction-based coalition-forming model for a virtual power plant based on stochastic programming. Int. J. Electr. Power Energy Syst. 2020, 118, 105784. [Google Scholar] [CrossRef]

- Khorasany, M.; Raoofat, M. Bidding strategy for participation of virtual power plant in energy market considering uncertainty of generation and market price. In Proceedings of the 2017 Smart Grid Conference (SGC), Tehran, Iran, 20–21 December 2017; IEEE: Piscataway, NJ, USA, 2017; pp. 1–6. [Google Scholar]

- Rahimi, M.; Ardakani, F.J.; Ardakani, A.J. Optimal stochastic scheduling of electrical and thermal renewable and non-renewable resources in virtual power plant. Int. J. Electr. Power Energy Syst. 2021, 127, 106658. [Google Scholar] [CrossRef]

- Oladimeji, O.; Ortega, Á.; Sigrist, L.; Rouco, L.; Sánchez-Martín, P.; Lobato, E. Optimal Participation of Heterogeneous, RES-Based Virtual Power Plants in Energy Markets. Energies 2022, 15, 3207. [Google Scholar] [CrossRef]

- Jordehi, A.R. A stochastic model for participation of virtual power plants in futures markets, pool markets and contracts with withdrawal penalty. J. Energy Storage 2022, 50, 104334. [Google Scholar] [CrossRef]

- Tan, Z.; Fan, W.; Li, H.; De, G.; Ma, J.; Yang, S.; Ju, L.; Tan, Q. Dispatching optimization model of gas-electricity virtual power plant considering uncertainty based on robust stochastic optimization theory. J. Clean. Prod. 2020, 247, 119106. [Google Scholar] [CrossRef]

- Shabanzadeh, M.; Sheikh-El-Eslami, M.K.; Haghifam, M.R. The design of a risk-hedging tool for virtual power plants via robust optimization approach. Appl. Energy 2015, 155, 766–777. [Google Scholar] [CrossRef]

- Zhang, Y.; Liu, F.; Wang, Z.; Su, Y.; Wang, W.; Feng, S. Robust scheduling of virtual power plant under exogenous and endogenous uncertainties. IEEE Trans. Power Syst. 2021, 37, 1311–1325. [Google Scholar] [CrossRef]

- Naughton, J.; Wang, H.; Cantoni, M.; Mancarella, P. Co-optimizing virtual power plant services under uncertainty: A robust scheduling and receding horizon dispatch approach. IEEE Trans. Power Syst. 2021, 36, 3960–3972. [Google Scholar] [CrossRef]

- Rabiee, A.; Sadeghi, M.; Aghaeic, J.; Heidari, A. Optimal operation of microgrids through simultaneous scheduling of electrical vehicles and responsive loads considering wind and PV units uncertainties. Renew. Sustain. Energy Rev. 2016, 57, 721–739. [Google Scholar] [CrossRef]

- Amini, M.; Almassalkhi, M. Trading off robustness and performance in receding horizon control with uncertain energy resources. In Proceedings of the 2018 Power Systems Computation Conference (PSCC), Dublin, Ireland, 11–15 June 2018; IEEE: Piscataway, NJ, USA, 2018; pp. 1–7. [Google Scholar]

- Nguyen, H.T.; Le, L.B.; Wang, Z. A bidding strategy for virtual power plants with the intraday demand response exchange market using the stochastic programming. IEEE Trans. Ind. Appl. 2018, 54, 3044–3055. [Google Scholar] [CrossRef]

- Wang, J.; Dai, H.; Yang, M.; Liu, H. Optimal dispatching of virtual power plant considering the uncertainty of PV. In Proceedings of the 2019 IEEE Sustainable Power and Energy Conference (iSPEC), Beijing, China, 21–23 November 2019; IEEE: Piscataway, NJ, USA, 2019; pp. 1381–1385. [Google Scholar]

- Zuluaga, J.; Murillo-Sanchez, C.E.; Moreno-Chuquen, R.; Chamorro, H.R.; Sood, V.K. Day-ahead unit commitment for hydro-thermal coordination with high participation of wind power. IET Energy Syst. Integr. 2023, 5, 119–127. [Google Scholar] [CrossRef]

- Sheidaei, F.; Ahmarinejad, A. Multi-stage stochastic framework for energy management of virtual power plants considering electric vehicles and demand response programs. Int. J. Electr. Power Energy Syst. 2020, 120, 106047. [Google Scholar] [CrossRef]

- Ullah, Z.; Arshad.; Hassanin, H. Modeling, optimization, and analysis of a virtual power plant demand response mechanism for the internal electricity market considering the uncertainty of renewable energy sources. Energies 2022, 15, 5296. [Google Scholar] [CrossRef]

- Falabretti, D.; Gulotta, F.; Siface, D. Scheduling and operation of RES-based virtual power plants with e-mobility: A novel integrated stochastic model. Int. J. Electr. Power Energy Syst. 2023, 144, 108604. [Google Scholar] [CrossRef]

- Ying, L.; Ma, F.; Cui, X.; Shusheng, T. Research on Bidding Strategy of Virtual Power Plant Considering Risk Preference. In Proceedings of the 2023 3rd Power System and Green Energy Conference (PSGEC), Shanghai, China, 24–26 August 2023; IEEE: Piscataway, NJ, USA, 2023; pp. 311–317. [Google Scholar]

- Alahyari, A.; Ehsan, M.; Moghimi, M. Managing distributed energy resources (DERs) through virtual power plant technology (VPP): A stochastic information-gap decision theory (IGDT) approach. Iran. J. Sci. Technol. Trans. Electr. Eng. 2020, 44, 279–291. [Google Scholar] [CrossRef]

- Kim, H.J.; Kang, H.J.; Kim, M.K. Data-driven bidding strategy for DER aggregator based on gated recurrent unit–enhanced learning particle swarm optimization. IEEE Access 2021, 9, 66420–66435. [Google Scholar] [CrossRef]

- Yan, X.; Gao, C.; Song, M.; Chen, T.; Ding, J.; Guo, M.; Wang, X.; Abbes, D. An IGDT-based day-ahead co-optimization of energy and reserve in a VPP considering multiple uncertainties. IEEE Trans. Ind. Appl. 2022, 58, 4037–4049. [Google Scholar] [CrossRef]

- Shafiekhani, M.; Ahmadi, A.; Homaee, O.; Shafie-khah, M.; Catalao, J.P. Optimal bidding strategy of a renewable-based virtual power plant including wind and solar units and dispatchable loads. Energy 2022, 239, 122379. [Google Scholar] [CrossRef]

- Fang, F.; Yu, S.; Xin, X. Data-driven-based stochastic robust optimization for a virtual power plant with multiple uncertainties. IEEE Trans. Power Syst. 2021, 37, 456–466. [Google Scholar] [CrossRef]

- Zhu, J.; Duan, P.; Liu, M.; Xia, Y.; Guo, Y.; Mo, X. Bi-Level real-time economic dispatch of VPP considering uncertainty. IEEE Access 2019, 7, 15282–15291. [Google Scholar] [CrossRef]

- Liu, Y.; Li, M.; Lian, H.; Tang, X.; Liu, C.; Jiang, C. Optimal dispatch of virtual power plant using interval and deterministic combined optimization. Int. J. Electr. Power Energy Syst. 2018, 102, 235–244. [Google Scholar] [CrossRef]

- Ju, L.; Tan, Q.; Lu, Y.; Tan, Z.; Zhang, Y.; Tan, Q. A CVaR-robust-based multi-objective optimization model and three-stage solution algorithm for a virtual power plant considering uncertainties and carbon emission allowances. Int. J. Electr. Power Energy Syst. 2019, 107, 628–643. [Google Scholar] [CrossRef]

- Wu, M.; Xu, J.; Zeng, L.; Li, C.; Liu, Y.; Yi, Y.; Wen, M.; Jiang, Z. Two-stage robust optimization model for park integrated energy system based on dynamic programming. Appl. Energy 2022, 308, 118249. [Google Scholar] [CrossRef]

- Abbasi, M.; Asadi, A.; BenElghali, S.; Zerrougui, M. Short-Term Forecasting of Uncertain Parameters for Virtual Power Plants. In Proceedings of the 2021 IEEE 26th International Workshop on Computer Aided Modeling and Design of Communication Links and Networks (CAMAD), Virtual, 25–27 October 2021; IEEE: Piscataway, NJ, USA, 2021; pp. 1–6. [Google Scholar]

- Jasinski, M.; Najafi, A.; Homaee, O.; Kermani, M.; Tsaousoglou, G.; Leonowicz, Z.; Novak, T. Operation and planning of energy hubs under uncertainty—a review of mathematical optimization approaches. IEEE Access 2023, 11, 7208–7228. [Google Scholar] [CrossRef]

- Dogan, A.; Cidem Dogan, D. A review on machine learning models in forecasting of virtual power plant uncertainties. Arch. Comput. Methods Eng. 2023, 30, 2081–2103. [Google Scholar] [CrossRef]

- Cantillo-Luna, S.; Moreno-Chuquen, R.; Lopez-Sotelo, J.; Celeita, D. An Intra-Day Electricity Price Forecasting Based on a Probabilistic Transformer Neural Network Architecture. Energies 2023, 16, 6767. [Google Scholar] [CrossRef]

- Ye, J.; Zhao, B.; Liu, D.; Wei, Q.; Wang, Y. TADNet: Temporal Attention Decomposition Networks for Probabilistic Energy Forecasting. IEEE Trans. Power Syst. 2024. [Google Scholar] [CrossRef]

- Xu, C.; Sun, Y.; Du, A.; Gao, D.c. Quantile regression based probabilistic forecasting of renewable energy generation and building electrical load: A state of the art review. J. Build. Eng. 2023, 79, 107772. [Google Scholar] [CrossRef]

- Doelle, O.; Klinkenberg, N.; Amthor, A.; Ament, C. Probabilistic intraday PV power forecast using ensembles of deep Gaussian mixture density networks. Energies 2023, 16, 646. [Google Scholar] [CrossRef]

- Birge, J.R.; Louveaux, F. Introduction to Stochastic Programming; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2011. [Google Scholar]

- Rockafellar, R.T.; Uryasev, S. Optimization of conditional value-at-risk. J. Risk 2000, 2, 21–42. [Google Scholar] [CrossRef]

- Kazemi, S.M.; Goel, R.; Eghbali, S.; Ramanan, J.; Sahota, J.; Thakur, S.; Wu, S.; Smyth, C.; Poupart, P.; Brubaker, M. Time2vec: Learning a vector representation of time. arXiv 2019, arXiv:1907.05321. [Google Scholar]

- Cantillo-Luna, S.; Moreno-Chuquen, R.; Lopez-Sotelo, J. Intra-day Electricity Price Forecasting Based on a Time2Vec-LSTM Model. In Proceedings of the IEEE Colombian Conference on Applications of Computational Intelligence, Cali, Colombia, 27–29 July 2022; Springer: Berlin/Heidelberg, Germany, 2023; pp. 107–121. [Google Scholar]

- Zobaa, A.F.; Aleem, S.A. Uncertainties in Modern Power Systems; Academic Press: Cambridge, MA, USA, 2020. [Google Scholar] [CrossRef]

- Narvaez, G.; Giraldo, L.F.; Bressan, M.; Guillen, C.A.; Pabón, M.A.; Díaz, N.; Porras, M.F.; Medina, B.H.; Jiménez, F.; Jiménez-Estévez, G.; et al. An interactive tool for visualization and prediction of solar radiation and photovoltaic generation in Colombia. Big Earth Data 2023, 7, 904–929. [Google Scholar] [CrossRef]

- Hemmati, M.; Mohammadi-Ivatloo, B.; Soroudi, A. Uncertainty management in decision-making in power system operation. In Decision Making Applications in Modern Power Systems; Elsevier: Amsterdam, The Netherlands, 2020; pp. 41–62. [Google Scholar]

- Cantillo-Luna, S.; Moreno-Chuquen, R.; Celeita, D.; Anders, G. Deep and Machine Learning Models to Forecast Photovoltaic Power Generation. Energies 2023, 16, 4097. [Google Scholar] [CrossRef]

- Rodriguez-Leguizamon, C.K.; López-Sotelo, J.A.; Cantillo-Luna, S.; López-Castrillón, Y.U. PV Power Generation Forecasting Based on XGBoost and LSTM Models. In Proceedings of the 2023 IEEE Workshop on Power Electronics and Power Quality Applications (PEPQA), Cali, Colombia, 5–6 October 2023; IEEE: Piscataway, NJ, USA, 2023; pp. 1–6. [Google Scholar]

- Heitsch, H.; Römisch, W. Scenario reduction algorithms in stochastic programming. Comput. Optim. Appl. 2003, 24, 187–206. [Google Scholar] [CrossRef]

- Li, Q.; Gao, D.W. Fast scenario reduction for power systems by deep learning. arXiv 2019, arXiv:1908.11486. [Google Scholar]

- Shabanzadeh, M.; Sheikh-El-Eslami, M.K.; Haghifam, M.R. Decision making tool for virtual power plants considering midterm bilateral contracts. In Proceedings of the Iranian Regulation CIRED Conference and Exhibition on Electricity Distribution, Lyon, France, 15–18 June 2015; pp. 1–6. [Google Scholar]

- Zakariazadeh, A.; Jadid, S.; Siano, P. Smart microgrid energy and reserve scheduling with demand response using stochastic optimization. Int. J. Electr. Power Energy Syst. 2014, 63, 523–533. [Google Scholar] [CrossRef]

- Ayón, X.; Moreno, M.Á.; Usaola, J. Aggregators’ optimal bidding strategy in sequential day-ahead and intraday electricity spot markets. Energies 2017, 10, 450. [Google Scholar] [CrossRef]

- Cantillo, S.; Moreno, R. Power system operation considering detailed modelling of energy storage systems. Int. J. Electr. Comput. Eng. 2021, 11, 182. [Google Scholar] [CrossRef]

- Conejo, A.J.; Garcia-Bertrand, R.; Carrion, M.; Caballero, Á.; de Andres, A. Optimal involvement in futures markets of a power producer. IEEE Trans. Power Syst. 2008, 23, 703–711. [Google Scholar] [CrossRef]

- Nguyen, D.T.; Le, L.B. Risk-constrained profit maximization for microgrid aggregators with demand response. IEEE Trans. Smart Grid 2014, 6, 135–146. [Google Scholar] [CrossRef]

- Seabold, S.; Perktold, J. Statsmodels: Econometric and statistical modeling with python. In Proceedings of the 9th Python in Science Conference, Austin, TX, USA, 28–30 June 2010. [Google Scholar]

- Chollet, F.; Nguyen, L.; Baihan, L.; Chu, J.; Feng, Y.; Finzi, D.; Watson, J.; Laszlo, S.; Crosse, M.; Honke, G.; et al. Keras. 2015. Available online: https://github.com/fchollet/keras (accessed on 3 March 2024).

- Kingma, D.P.; Ba, J. Adam: A method for stochastic optimization. arXiv 2014, arXiv:1412.6980. [Google Scholar]

- Bynum, M.L.; Hackebeil, G.A.; Hart, W.E.; Laird, C.D.; Nicholson, B.L.; Siirola, J.D.; Watson, J.P.; Woodruff, D.L. Pyomo-Optimization Modeling in Python; Springer: Berlin/Heidelberg, Germany, 2021; Volume 67. [Google Scholar]

- Hart, W.E.; Watson, J.P.; Woodruff, D.L. Pyomo: Modeling and solving mathematical programs in Python. Math. Program. Comput. 2011, 3, 219–260. [Google Scholar] [CrossRef]

- Czyzyk, J.; Mesnier, M.P.; Moré, J.J. The NEOS Server. IEEE J. Comput. Sci. Eng. 1998, 5, 68–75. [Google Scholar] [CrossRef]

- MOSEK ApS. The MOSEK Optimization Toolbox for Python Manual. Version 10.1. 2022. Available online: https://docs.mosek.com/latest/pythonfusion/index.html (accessed on 8 March 2024).

- Sengupta, M.; Xie, Y.; Lopez, A.; Habte, A.; Maclaurin, G.; Shelby, J. The National Solar Radiation Data Base (NSRDB). Renew. Sustain. Energy Rev. 2018, 89, 51–60. [Google Scholar] [CrossRef]

- National Renewable Energy Laboratory (NREL). National Solar Radiation Database. Available online: https://registry.opendata.aws/nrel-pds-nsrdb (accessed on 14 December 2023).

- Luque, A.; Hegedus, S. Handbook of Photovoltaic Science and Engineering; John Wiley & Sons: Hoboken, NJ, USA, 2011. [Google Scholar]

- Molina, A.; Martínez, F. Modelo de Generación Fotovoltaica; Explorador Solar: Santiago, Chile, 2017; p. 13. [Google Scholar]

- XM Colombia. Portal de Variables del Mercado Eléctrico Colombiano SINERGOX. Available online: https://sinergox.xm.com.co/trpr/Paginas/Historicos/Historicos.aspx (accessed on 14 December 2023).

- Journois, M.; Story, R.; Gardiner, J.; Rump, H.; Bird, A.; Lima, A.; Cano, J.; Leonel, J.; Sampson, T.; Baker, J.; et al. Python-Visualization/Folium: v0.15.0; Zenodo: Geneve, Switzerland, 2022. [Google Scholar]

- XM. Sistema de Información para el Mercado de Energía Mayorista (SIMEM). Available online: https://www.simem.co (accessed on 10 December 2023).

- Comisión de Regulación de Energía y Gas (CREG). Resolución 096 de 2019. Available online: https://gestornormativo.creg.gov.co/gestor/entorno/docs/resolucion_creg_0096_2019.htm#INICIO (accessed on 27 December 2023).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| MAE () | RMSE () | MAPE (%) | PICP (%) |

|---|---|---|---|

| 12.38 | 27.63 | 5.81 | 95.23 |

| PV No. | Location (Lat-Lon) | Rated Capacity (kW) | Firm Energy (kW) | Price Offer () |

|---|---|---|---|---|

| PV1 | 3.368783, −76.519726 | 200 | 55 | 190 |

| PV2 | 3.455787, −76.575902 | 50 | 11 | 220 |

| PV3 | 3.686235, −76.307398 | 3.5 | 0.6 | 285 |

| PV4 | 3.353617 −76.521868 | 400 | 108 | 164 |

| ESS No. | Capacity (kWh) | DoD (%) | Chg/Dchg Limit (kW) | Chg/Dchg Efficiency (%) | Dchg Cycle Duration (h) | Initial Energy (kWh) | Price Offer () |

|---|---|---|---|---|---|---|---|

| ESS1 | 19.8 | 80 | 10.0 | 85 | 8 | 11.2 | 460 |

| ESS2 | 100.0 | 85 | 60.0 | 80 | 8 | 65.7 | 370 |

| DR Scheme No. | Maximum Load Reduction (kW) | Price Offer () |

|---|---|---|

| DR1 | 80.0 | 210 |

| DR2 | 580.0 | 150 |

| DR3 | 1.5 | 265 |

| DR4 | 260.0 | 160 |

| Risk Profile () | Expected Revenues (Million $COP) | CVaR (Million $COP) |

|---|---|---|

| 0.0 | 20.20 | 19.82 |

| 0.1 | 20.16 | 19.83 |

| 0.2 | 20.13 | 19.92 |

| 0.3 | 20.11 | 19.92 |

| 0.4 | 20.08 | 19.92 |

| 0.5 | 20.05 | 19.92 |

| 0.6 | 20.03 | 19.92 |

| 0.7 | 20.00 | 19.92 |

| 0.8 | 19.97 | 19.92 |

| 0.9 | 19.94 | 19.92 |

| 1.0 | 19.93 | 19.93 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cantillo-Luna, S.; Moreno-Chuquen, R.; Celeita, D.; Anders, G.J. A Stochastic Decision-Making Tool Suite for Distributed Energy Resources Integration in Energy Markets. Energies 2024, 17, 2419. https://doi.org/10.3390/en17102419

Cantillo-Luna S, Moreno-Chuquen R, Celeita D, Anders GJ. A Stochastic Decision-Making Tool Suite for Distributed Energy Resources Integration in Energy Markets. Energies. 2024; 17(10):2419. https://doi.org/10.3390/en17102419

Chicago/Turabian StyleCantillo-Luna, Sergio, Ricardo Moreno-Chuquen, David Celeita, and George J. Anders. 2024. "A Stochastic Decision-Making Tool Suite for Distributed Energy Resources Integration in Energy Markets" Energies 17, no. 10: 2419. https://doi.org/10.3390/en17102419

APA StyleCantillo-Luna, S., Moreno-Chuquen, R., Celeita, D., & Anders, G. J. (2024). A Stochastic Decision-Making Tool Suite for Distributed Energy Resources Integration in Energy Markets. Energies, 17(10), 2419. https://doi.org/10.3390/en17102419