1. Introduction

A rational and planned change in priorities in the structure of the fuel and energy balance is the guarantor of the sustainable development of society [

1,

2,

3]. While being a characteristic of the total fuel and energy complex (hereinafter FEC), this balance under the influence of global challenges is highly vulnerable [

4,

5]. Authors refer to the mentioned problems: growth of consumption [

6], market change [

7,

8,

9], depletion/lack of resources [

10,

11,

12], import substitution [

13,

14,

15,

16,

17,

18], scientific and technological progress [

19,

20], global climate change [

21,

22], and growing demand for energy quality and energy efficiency [

23], as well as infrastructure wear and tear [

24,

25,

26,

27].

Countries—participants of the global energy market—should not ignore global changes [

28]. These include the energy crisis, partially provoked by the accelerated development of renewable energy technologies [

29,

30,

31,

32] in countries with an insufficient level of technological development. Under such circumstances, the lack of protection mechanisms in the form of technology might threaten not only energy security [

33,

34], but also the sustainability of the whole country’s economic system [

35,

36,

37].

Counteraction to this cannot occur due to isolation, since the energy sector is not able to exist for a long time in isolation from other spheres and external influence [

38,

39]. As a response to challenges, end-to-end digital technologies and Industry 4.0 technologies are developing [

40,

41,

42,

43,

44], stimulating the restructuring of the energy sector [

45]. Authors have identified seven blocks of technologies, united by common functions or ways of realization: digital and IT, smart grid, renewable and Non-conventional energy sources, storage technologies, and a block of industrial production technologies [

46,

47].

The assessment of the impact of technological implementation should be carried out on the scale of the whole country. In this article, the assessment is considered on the example of Russia, which, in 2021, was ranked third in the world in terms of energy production and consumption [

48]. The main energy resource for primary consumption in the country is natural gas and oil, which account for 41.5% and 35.4%, respectively [

48]. Natural gas is also the main resource for electricity generation, accounting for 41.8%. Due to the diversity of the country in terms of energy supply conditions and levels of regional development, the analysis can only be carried out using a comprehensive approach, which can then be applied to other countries.

Under the pressure of the extent and speed of global changes, it is necessary to track and predict the state of the FEC of countries by system-forming industries (oil, gas and coal, as well as electric and heat power). In many ways, they are the key factors of regional development. In the case of this study, the types of electricity generation were not considered separately from each other, and all of them are included. However, their ratio is indirectly reflected in the electricity cost parameter (shown in

Table A1 in

Appendix A). Thus, in regions with a high share of hydro and nuclear power, this value is lower in comparison with others. However, when applying this methodology to other countries, it is possible to consider the percentage of green generation (nuclear, renewables and hydropower) as another parameter (presented in

Section 2.1.8).

The oil industry is one of the leading sectors of the Russian economy, with oil and gas revenues accounting for almost 30% of the federal budget each year. The export of crude oil and petroleum products accounted for 36% of total Russian exports in 2021 [

9]. The Russian Federation has the world’s sixth-largest proven oil reserves, accounting for about 8.5% of the world’s total [

16]. Oil is included in the list of strategic minerals according to the Strategy for the Development of the Mineral Resource Base up to 2035, approved by an RF Government Decree. As of January 2021, the recoverable oil reserves were 12 billion tons [

9].

Currently, there is also no problem with the depletion of gas resources in Russia. In 2020, the increment of geological reserves of gas in the country was 1.618 trillion m

3 and 54.4 million tons of gas condensate [

25]. At the same time, due to the geopolitical situation, Europe considers it necessary to refuse Russian pipeline gas. It creates a risk of uncertainty not only for the gas market, but also for the energy security and energy supply of consumers in the world in general. Consequently, during 2021, Gazprom delivered less than 145 billion m

3 to Europe, which is the lowest result since 2016 [

26].

In 2021, the volume of coal production in the country reached 439 million tons [

18]. Russia’s subsoil contains one-third of the world’s coal resources and one-fifth of the explored reserves, i.e., 193.3 billion tons [

49]. Over the past two decades, the production and export of this type of fuel in the Russian Federation have grown steadily, on average by 2.9% and 9.6% per year, respectively [

50]. The positions of Russian coal companies are competitive in terms of production costs, which allows them to pass through times of low prices in the market.

According to the Ministry of Energy of Russia and the program of the prospective development of the UESR of Russia for the period from 2021 to 2027, the country is showing an increase in the demand for electricity in the time period up to 2027 [

15]. The main vector of the fight against climate change in this industry is the creation of more environmentally friendly technologies and technological processes that will be accompanied by a reduction in greenhouse gas emissions. The gradual introduction of more nuclear power plants and RES, replacing thermal power plants based on coal and other fossil fuels, will be a reliable course for the decarbonization of the electric power industry in Russia.

About 40% of Russia’s electricity is generated from low-carbon sources, including nuclear power plants and large hydropower plants [

23]. There are a total of 37 power units (including two floating nuclear thermal power plant reactors) in operation at Russian NPPs, with a total installed capacity of over 29.5 GW [

51]. The share of RES is still relatively small, but it is gradually growing. By 2050, it is planned to increase to 12.5% of the total generation [

52].

The Russian heat power industry was developed under extremely harsh climatic conditions, as a result of which it became one of the largest in the world, ranking first by the length of heating networks (183,000 km) and fourth by the volume of thermal energy produced [

53]. The main heat consumers are industrial enterprises and households, accounting for 49% and 39%, respectively [

14]. At the same time, the share of industrial facilities consuming thermal energy is gradually increasing, which evidences the development of the national economy and its industrial complexes.

Understanding the initial conditions in the country helps to determine its division into functional territorial units. In the proposed approach of the assessment, the authors carried out the zoning of the territory in question into seven local fuel and energy complexes (hereinafter LFEC) according to the territorial division into the UESR (unified energy systems of Russia [

54]), as shown in

Figure 1. Energy systems are correlated with their prevailing industries, on the basis of which it is possible to determine the degree of influence of external challenges.

Figure 1 partially reflects the relation mentioned above. Thus, the North-Western LFEC heat power industry is influenced by the growth of consumption and infrastructure wear and tear as a result of external challenges, and in the electric power industry, among others, the need for import substitution is highlighted. It is rational to start from the standout external challenges when choosing the technologies required for development within the 4D trends.

In order to take into account a more local level of sector enterprises and to unite previous trends [

55,

56,

57], the authors expanded the 3D concept with the fourth component [

58,

59,

60,

61,

62]. Hence, 4D trends at the same time included:

Digitalization—the trend towards the change in approaches to business processes based on the introduction of digital technologies;

Decarbonization—the trend towards the transition to “low-carbon” energy due to the rationalization of energy source used;

Decentralization—the trend to increase the number of small economic hubs for the energy supply;

Decrease—the trend to reduce the consumption of all types of resources and materials, as well as the amount of waste produced.

When considering the state of energy systems in the complex of external challenges and subsequent technological development (taking into account its current level), it is possible to assess the prospective state of the LFEC. Thus, in scenario forecasting, the authors started from a whole complex of influencing external factors: from local levels, gradually growing to the scale of the country.

Despite the large number of articles on scenario forecasting of the development of the FEC of the Russian Federation, their authors do not take into account regional peculiarities and their impact on the overall fuel and energy balance [

53,

63]. For instance, in [

64], the methodological foundations of modeling the long-term development of the Far Eastern region are considered, but the targets require updating and are not universal. In addition, scaling of the results is difficult in a number of articles [

65,

66]. In turn, forecasting development based on intelligent algorithms relies on the analysis of previous changes, which makes it difficult to integrate with scenarios [

67,

68,

69].

Reliance on foreign models in forecasting within the Russian Federation is impractical due to the use of statistical data from the EU and a number of countries [

70]. The potential of using models for the USA is low despite the similar zoning of the countries. This is due to the orientation of American models to the specific features of the United States, in connection with which the vectors of development are not just different from each other, but also, in current conditions, are characterized by a higher rate of change.

The authors propose a completely new methodology for assessing the impact of industrial technology implementation in the country, based on its division into smaller entities according to certain criteria. The proposed study is based on taking into account the initial state of the LFEC, predicting the degree of influence of various factors, taking into account expert opinions and conducting a final comprehensive forecast assessment. This process will make it possible to assess the objective functions of the regions in advance. In turn, this leads to better financing in areas with insufficient support in order to develop an FEC within the framework of sustainable development. This subsequent connection to regional development and the comprehensiveness of the consideration of influencing factors make the authors’ approach relevant and effective.

2. Materials and Methods

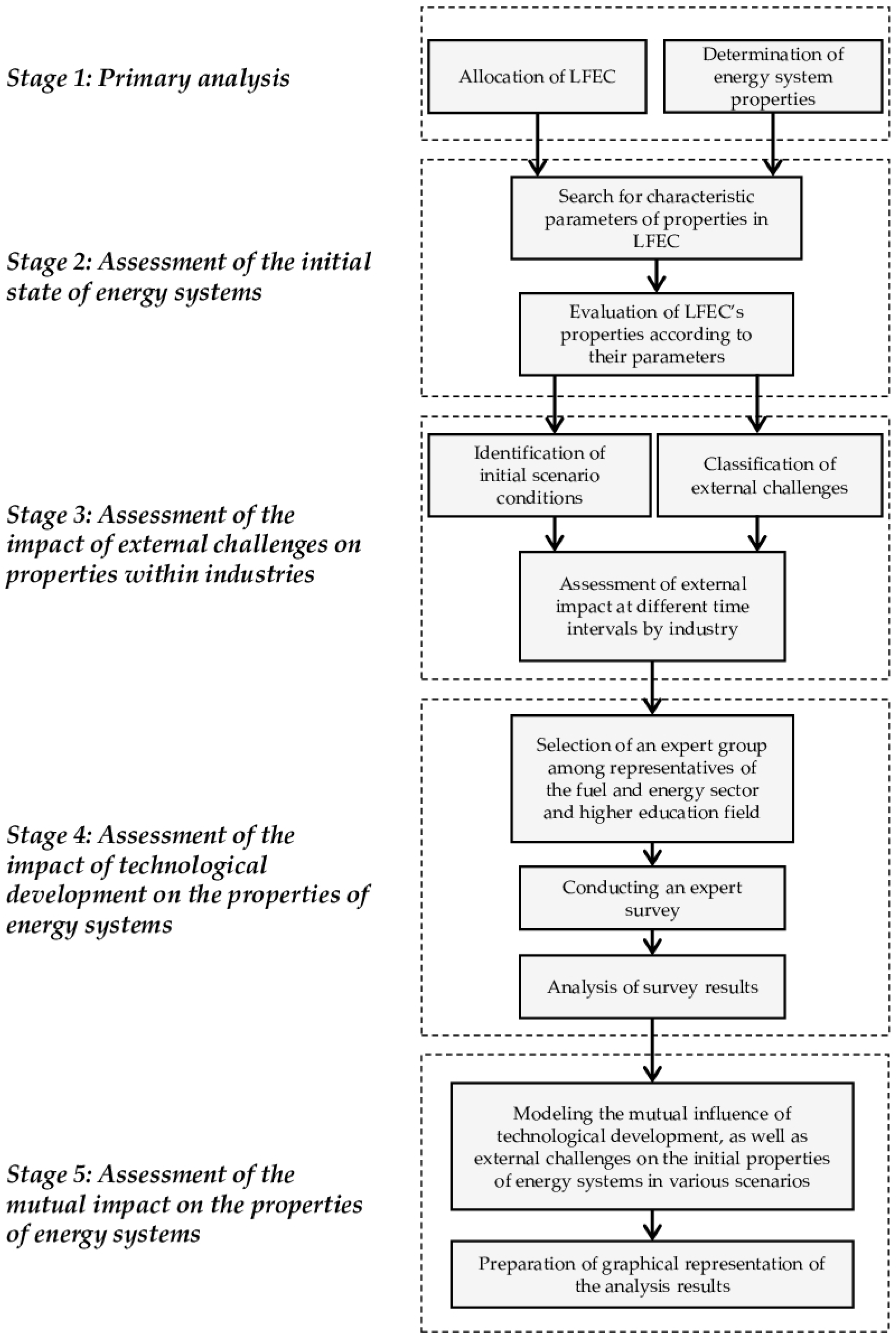

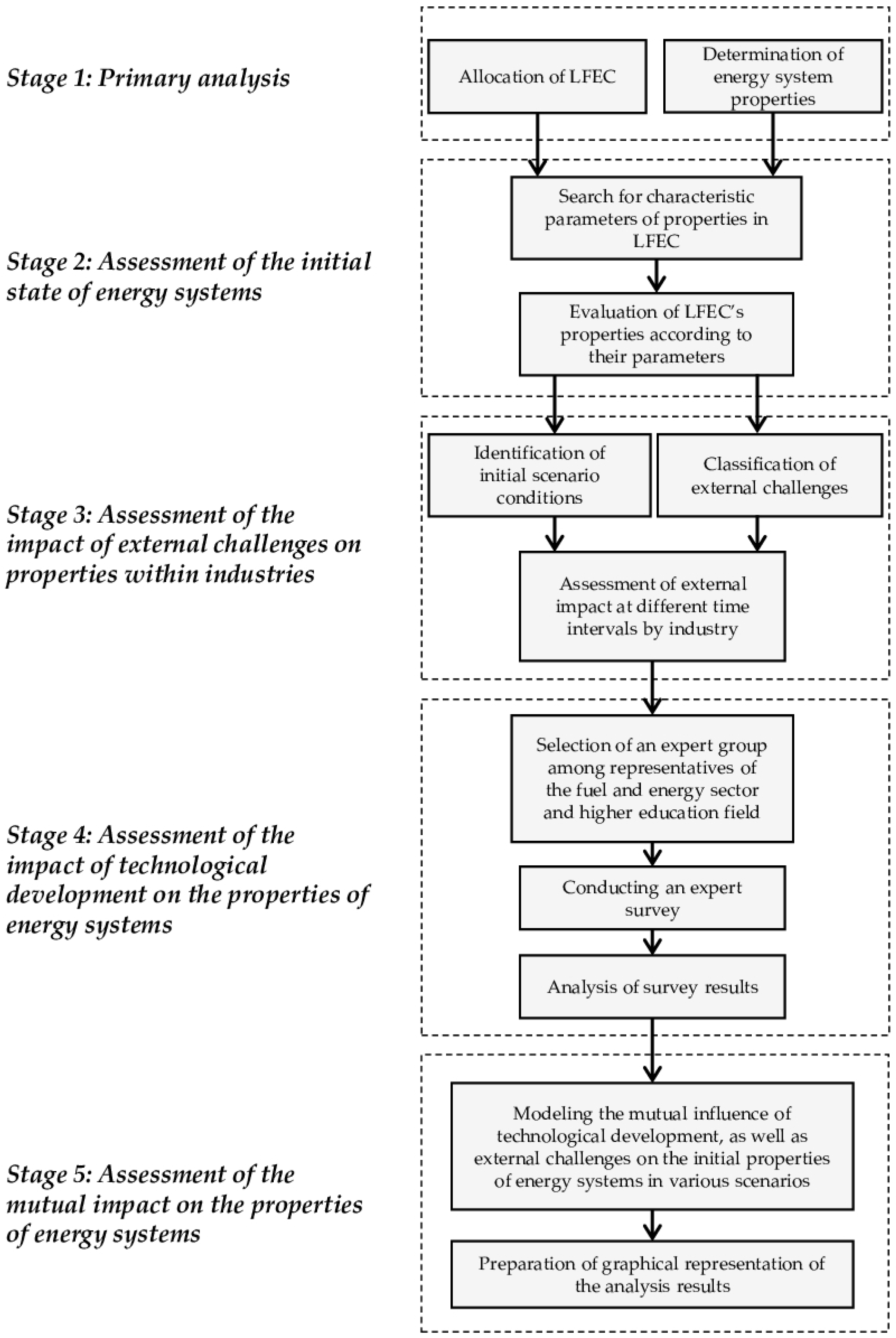

The research was divided into five stages, which are shown in

Figure 2. The research methodology includes the following steps: initially, a review of the LFEC was conducted to determine its current state by selected properties and indicative parameters. Then, the influence of external factors of impact (challenges) was assessed on the basis of an expert opinion for different time intervals according to three scenarios. Further, when conducting a survey of specialists in the field of fuel and energy, the dependence between technological development and changes in the properties of energy systems was identified. The result of these steps was the predicted value of property changes according to scenarios in time intervals. Thus, the impact of both global challenges and the process of technological development was taken into account at the last stage. At the same time, the current state of the FEC and fuel and energy balance within the country was used as the basis [

71], as well as a share of the influence of industries by region. It was allocated based on a normalized assessment of specific industry parameters.

The analysis of expert survey results is based on the Delphi method, which is extremely common in scenario forecasting in the energy sector and allows summarizing individual expert opinions [

72,

73]. A similar method applies to strategic planning. The influence of external factors was taken into account by analogy with articles [

74,

75].

2.1. Analysis of the Initial State of Energy Systems

To carry out a scenario analysis of the development of the fuel and energy complex, it is necessary to set the starting point—the initial state of the energy system. Considering the prospects for development on a national scale at once is difficult: not indicative and neither advisable.

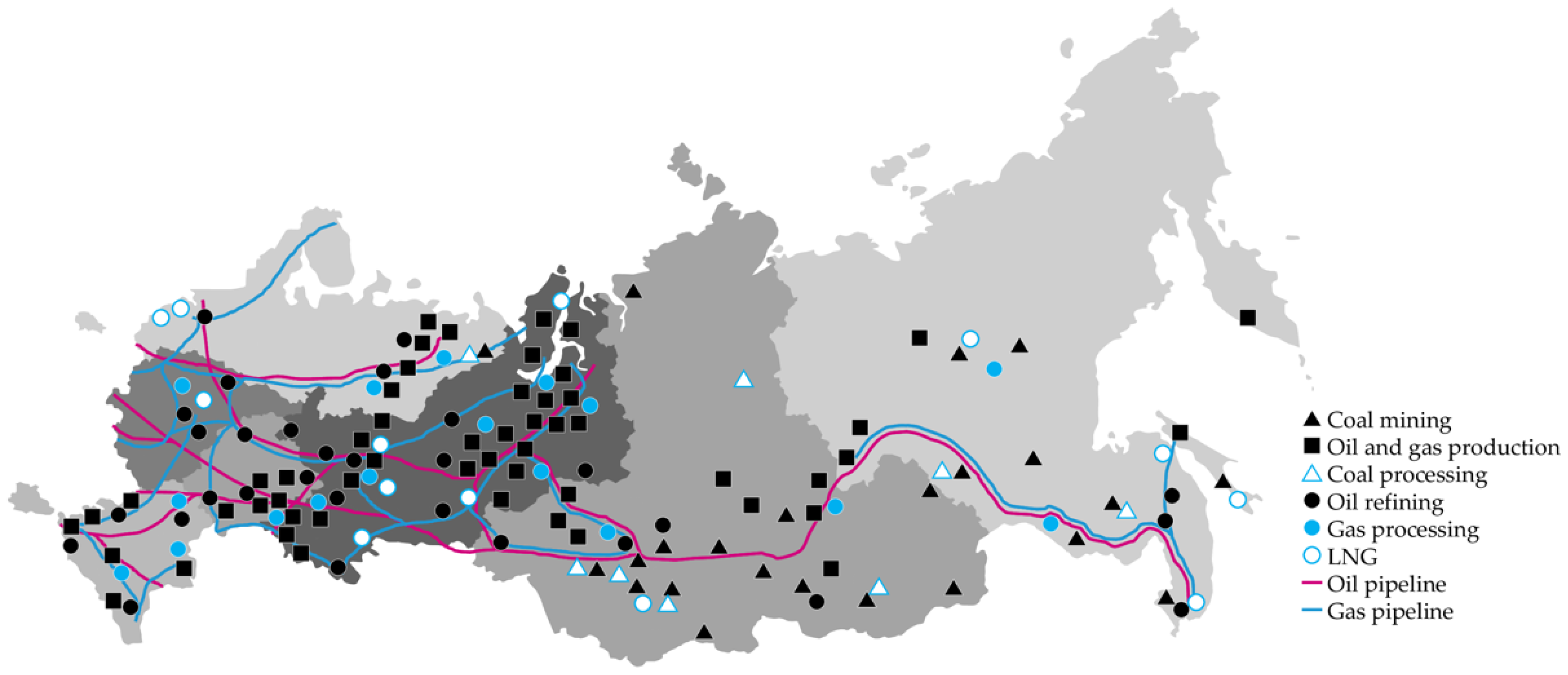

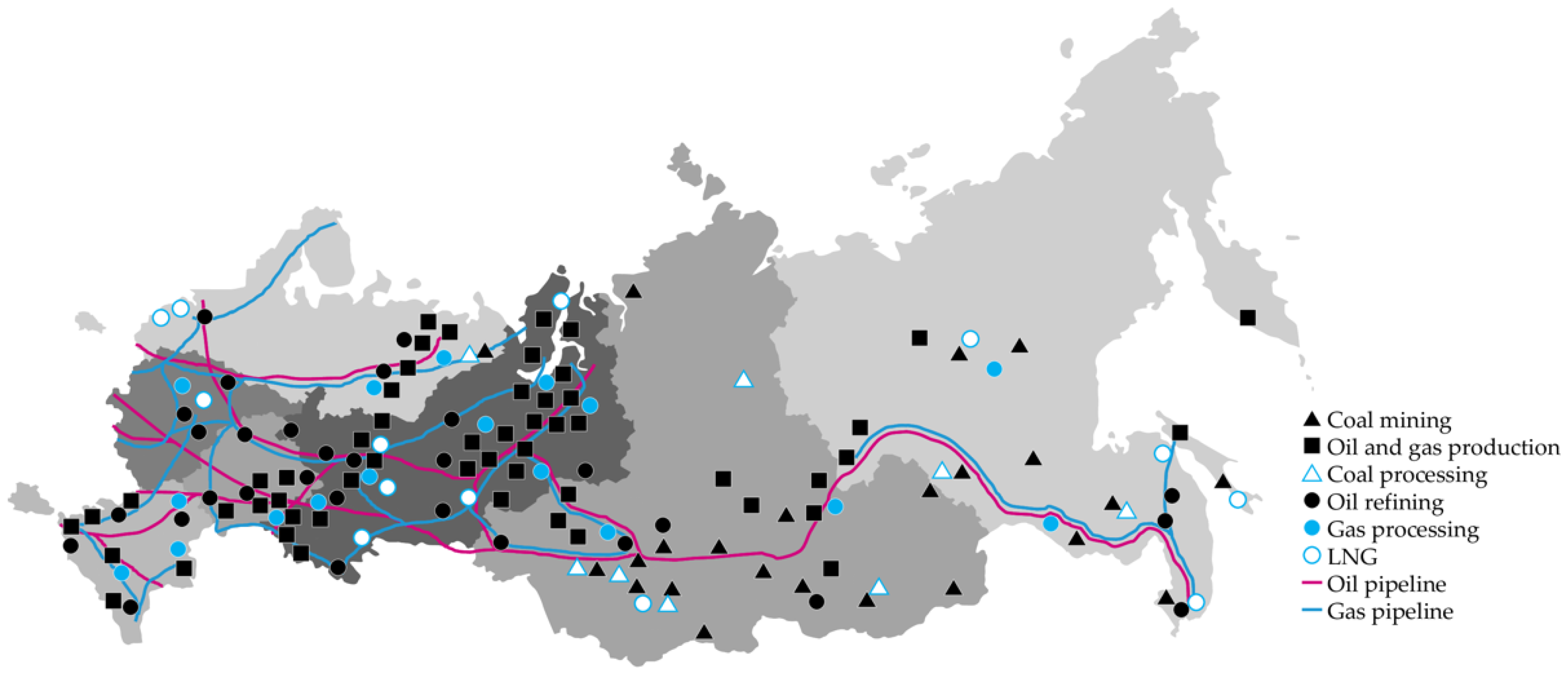

The Russian Federation has vast territories and large deposits of minerals. It also combines several time and climatic zones. For the most accurate forecasting, taking into account zonal specifics, the country’s energy system was divided into 7 LFECs: Central; Southern; North-Western; Middle Volga; Ural; Siberian and Eastern. That division is presented in

Figure 3 along with the main transport routes, hubs of processing and extraction of resources.

The LFEC is a closed territorial circuit that unites the main energy sectors: oil, gas and coal, as well as electric and heat power. At the same time, each energy complex has its own dominant industry or even several of them. Each LFEC is characterized by an objective function that defines the zones of its development and local problems, which further makes it possible to identify the potential for the introduction and use of the technology blocks under consideration.

2.1.1. The Current State of the Central LFEC

There are no significant reserves of traditional resources in this region, but the most important transport routes for the supply of fossil fuels abroad pass through it. The LFEC’s area is a point of concentration of the managerial layer of most spheres of the FEC. The location at the intersection of the main international consumer and the territorial area of resource extraction determines the importance of logistics. Current conditions are forcing managers to reorient supplies, as well as optimize in order to increase efficiency, reliability and environmental friendliness. Energy consumed in the region is mainly spent on domestic needs. Quite a large share of the region’s electricity is generated by nuclear power plants, about 42.8% for 2021 [

52]. Heat supply in winter and autumn months plays an important role in ensuring comfortable living conditions.

2.1.2. The Current State of the Southern LFEC

The Southern LFEC is characterized by the absence of any significant connection with the coal industry in comparison with others. The main focus in the region is on the transportation and processing of oil and gas. Energy and heat consumption is mostly for non-industrial use, but it is lower in comparison with other regions due to different climatic conditions and sizes of areas covered. Establishing trade relations with Kazakhstan and other CIS countries despite large-scale global changes might become a stable driver for the development of the region’s processing capacities. Nuclear power and hydropower play an important role in electricity generation in the region, accounting for 28.8% and 18.2%, respectively [

52]. RES received 4.1% of the total generation, but they continue to grow rapidly in the region.

2.1.3. The Current State of the North-Western LFEC

The theoretical possibility of an increase in resource extraction in this LFEC is very unlikely and is associated with significant costs despite large reserves (for example, in the Pechora coal basin). At the same time, the budget of individual districts, including the Nenets Autonomous Okrug, depends on small production volumes on a national scale. Similar to the Central LFEC, this region can be called a logistics center, where two Nordic gas streams and the Baltic pipeline system for oil transportation originate. It is the second of the most important business centers and central maritime logistics control point. For a while, the main role of the FEC was assigned to the gas industry, but there is also potential for the coal industry. The consumption of energy and heat is quite high due to harsh climatic conditions and the demands of detached large cities. The share of electricity generated in this region from nuclear power plants is 34.9% [

52].

2.1.4. The Current State of the LFEC of Middle Volga

Due to the small reserves, the main emphasis in terms of importance in the FEC of this LFEC is on processing and subsequent transportation by rail, rather than mining. Further development of the region might be carried out taking into account the case of the Orenburg Gas Processing Plant, which is increasing its capacity in the face of sanctions. The coal industry is of great importance for the region due to the active transportation of intermediate and final products. Electricity and heat consumption is kept at the level of the Central and North-Western LFECs because of the concentration of individual industries rather than the need to provide for the population. Nuclear power plants account for 29.9% of electricity generation and hydroelectric power plants for 18.5% [

52].

2.1.5. The Current State of the Ural LFEC

Along with the Siberian LFEC, most of the production capacities are concentrated in this area (except for the coal industry). Location at the intersection of transport routes and between regions with the main reserves and domestic consumers of energy resources leads to regional dependence on the transport infrastructure. The oil industry is of the greatest importance for LFECs. However, the construction of the Power of Siberia 2 might provoke a transition from the oil to the gas industry. Energy and heat consumption is unevenly distributed over the territory, where separate regions with extremely high needs stand out because of the production facilities. The target function of this region is to ensure uninterrupted transportation and production. Even under sanction pressure and during the restructuring of the market, the state of the region is stable.

2.1.6. The Current State of the Siberian LFEC

The Siberian LFEC is the leader in most industries in terms of reserves. Almost the entire chain from extraction to processing of resources is represented in this area in order to provide other regions. The development of the LFEC from the position of a business center is not advisable due to the peculiar climatic conditions and remoteness of the consumption centers of the country. FEC industries are equal in the region. Energy and heat are mostly spent on production in a fairly large amount due to the climate conditions. At the same time, a certain level of energy security must be ensured to supply backbone enterprises. In terms of electricity generation, hydropower plants play a key role in the region, accounting for 59.4% of the total [

52]. Despite the focus of the region on the extraction of resources, within the framework, the target function was to preserve territories as natural reserves due to the degree of forest degradation against the backdrop of climate change.

2.1.7. The Current State of the Eastern LFEC

Against the backdrop of market changes, this region might develop in the strongest way among others. Mainly it is a point of processing (which is highest in the coal industry) and transport routes of resources to Asia. Gas processing is also developed, for example, in the Amur Gas Processing Plant. The basis of the regional FEC is the gas industry and its transportation through the Power of Siberia and the Sakhalin–Khabarovsk–Vladivostok gas pipeline to the Asia-Pacific countries. The LFEC is characterized by the dependence on critical climatic changes and seasonal cataclysms (floods, etc.), which affects the level of target reliability of heat and power supply. Hydropower plants are actively used for power generation, generating 41% of the region’s electricity [

52]. The function of the region is logistical and industrial.

2.1.8. Determination and Evaluation of the LFEC’s Properties

Qualitative expression of the state of the LFEC is not enough for scenario forecasting. Therefore, it was required to identify quantitative parameters by industries. To assess the sustainable development of the energy system, each LFEC is considered through five properties Ti, where:

Sustainability T1—the ability of the FEC to maintain its current state under the influence of external global challenges;

Accessibility T2—the state of the FEC, in which it possesses the necessary amount of resources prepared for use by consumers ubiquitously and anytime;

Efficiency T3—the ability of the FEC to achieve an expected result with the usage of a minimum amount of resources and energy;

Adaptability T4—the ability of the FEC to adapt to external influencing factors;

Reliability T5—the ability of the FEC to maintain its performance under given conditions.

In order to carry out scenario forecasting, the initial state of each LFEC was assessed according to those five properties. Each property was associated with a number of parameters Pn (from 2 to 4, depending on the industry in question and the availability of information).

Parameters differ in their units of measurement, which is the reason for the impropriety of their comparison without further actions. In addition, large values of the parameters in some cases demonstrated the poorness of development of properties, and not vice versa.

Therefore, to correlate those values with each other in properties, they were normalized according to the Formula (1) in the range [0;1], where 0—parameter is poorly developed, 1—parameter is strongly developed in the LFEC.

where

—normalized value;

—initial value;

—maximum value in the median interval;

—minimal value in the median interval.

The sum of normalized parameters by properties is a coefficient, the value of which reflects the initial and further state of power systems after the analysis of the data obtained.

Table 1 shows the summarized values of the parameters for the LFEC (where “EP” is for electric power and “HP” is for heat power). As an example, the authors attach selected parameters for the gas industry in the Central LFEC by the property T

1 (sustainability): the amount of network gas available for the average monthly wage of regional residents in m

3 (the normalized value equals 1) and the length of the constructed gas pipelines in m (normalized value equals 0.98).

A complete list of parameters without division by LFEC is presented in

Appendix A in

Table A1.

The resulting total value for the Central LFEC’s gas industry in terms of property T1 (1.98) exceeds the others. This shows a high degree of sustainability of the gas industry in the central region. Similarly, it is possible to conduct a primary analysis for other regions and industries.

2.2. Analysis of the Influence of External Challenges on LFEC

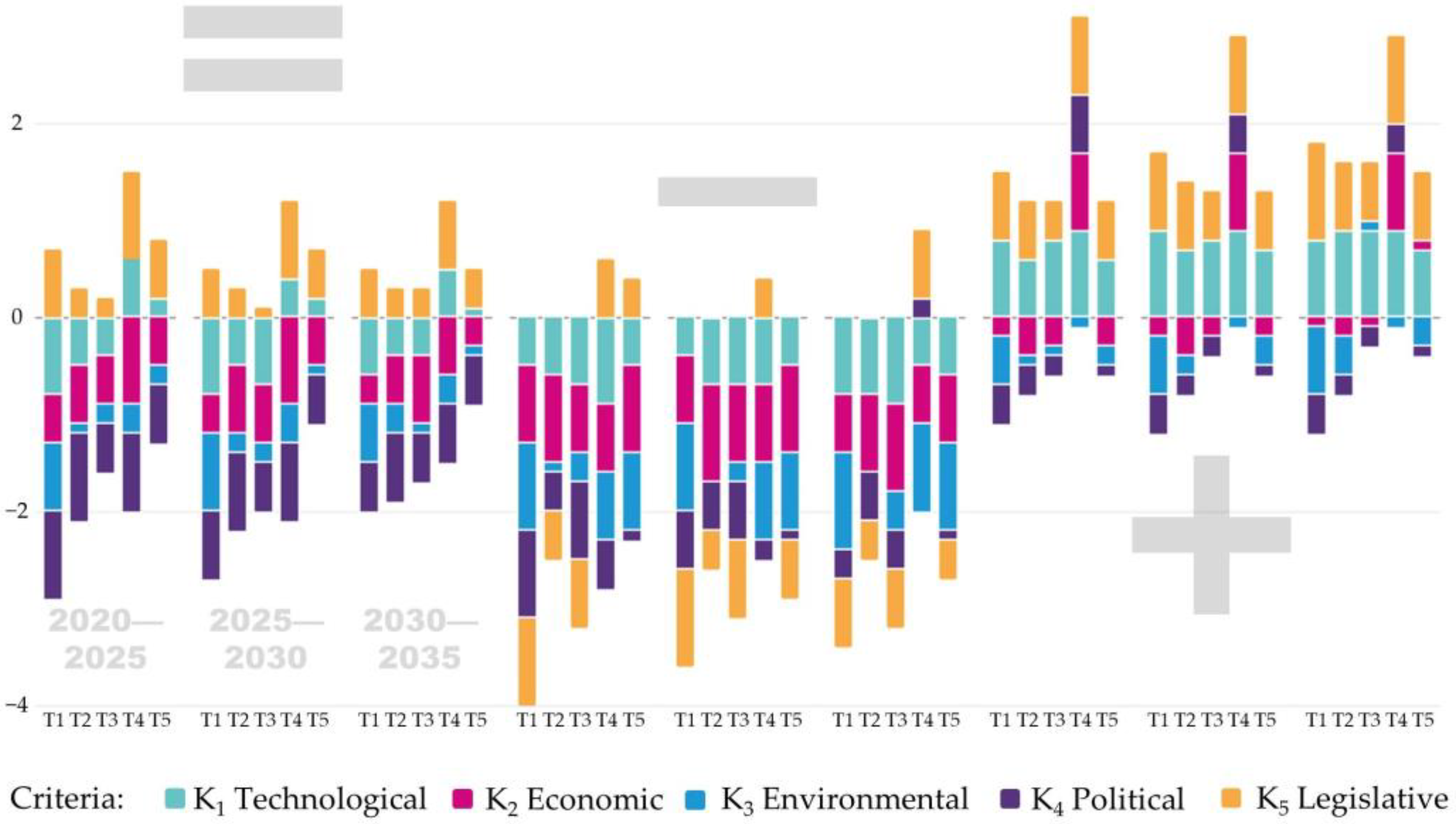

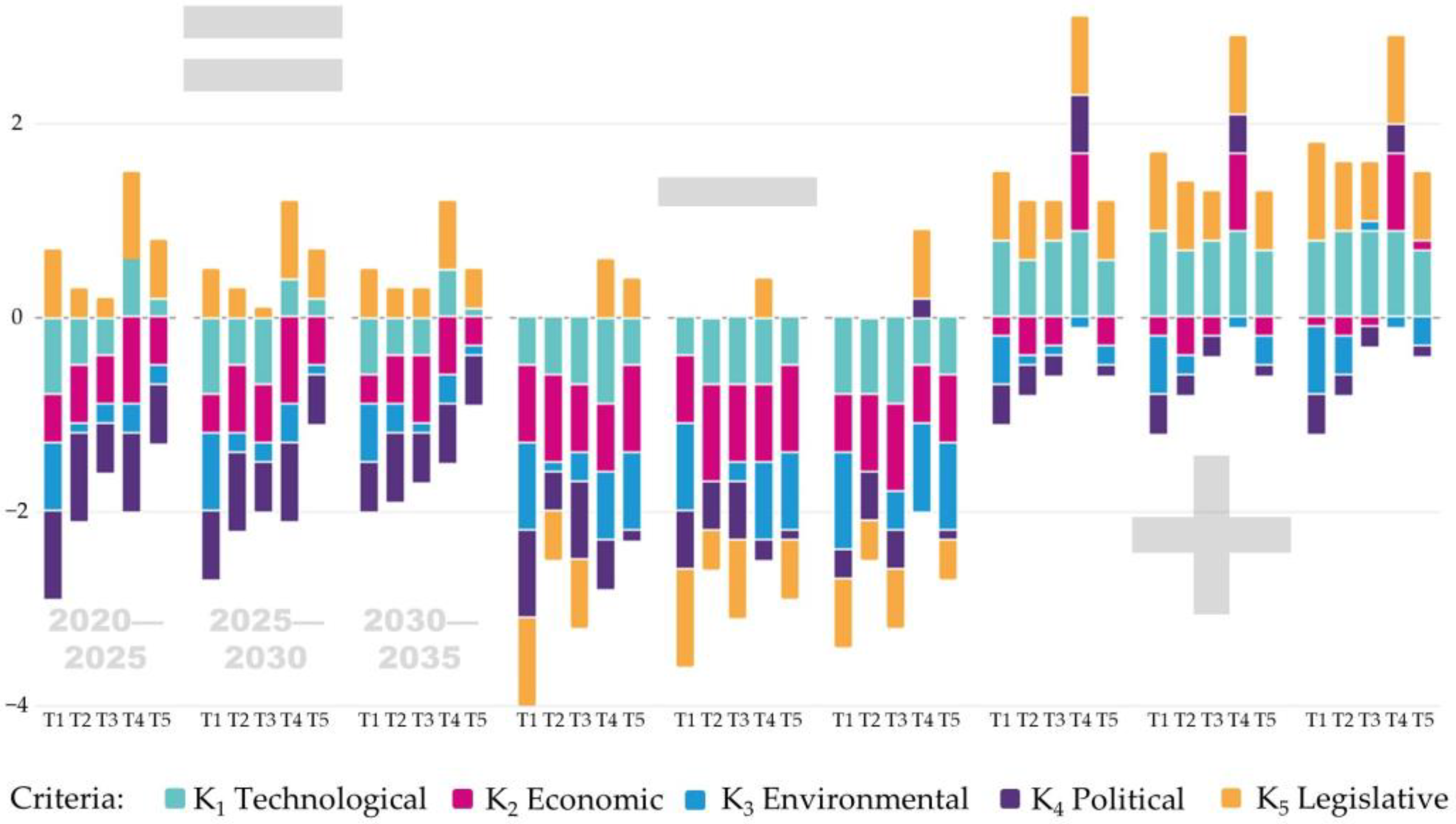

The external impact on the FEC is divided into challenges of five different directions: technological (K1), economic (K2), environmental (K3), political (K4) and legislative (K5). The assessment of the degree of influence of each challenge according to the criteria for three time periods (2020–2025, 2025–2030, 2030–2035+) was carried out in three scenarios: negative, neutral and positive. Impact assessment moves from the values of the criteria for the country as a whole to the values of the criteria for industries.

For example, as the first step, it was assumed that in the period of 2020–2025, according to the negative scenario in terms of the K2 economic criterion, the economic crisis in the Russian Federation would have a serious impact on the sustainability of the FEC. In the neutral scenario for the same time period, there will be a reduction in production capacity and an outflow of personnel. In turn, according to the positive scenario, the crisis will be overcome by reorienting to the domestic market while establishing new foreign trade relations.

Challenges through five criteria have an impact on the properties: it can be both positive and negative, which depends on its degree. For instance, economic instability (criterion K2) for all scenarios and periods of time negatively affects the sustainability (property T1) of the FEC of the Russian Federation in varying degrees. At the same time, legislative changes (K5) have a positive effect on the adaptability of the country’s FEC (T4) in the same conditions and scenario.

The assessment of the influence of the K

z criteria on the properties T

i was initially carried out in range [−1; 1], where −1—there is a strong negative effect, 0—there is no effect, 1—there is a strong positive effect. As an example, the authors in

Table 2 present the results of the initial assessment for the neutral scenario over three time periods.

Normalization was required for the obtained values, since the degree of influence depended, among other things, on the number and weight of the found parameters P

n within the framework of the T

i properties. It was carried out in the range [−n; +n] (where n—the number of parameters P

n of the property T

i) by Formula (2):

where

—normalized value (

Table 3);

—initial value (

Table 2);

—minimum value in median range;

—interval parameter range (2

);

—minimum value in interval parameter range.

The division into the LFEC at this stage was not carried out: instead, this step of analysis was applied to industries. For example, for the gas industry considered in

Section 2.1.8, two parameters P

n were identified for the property T

1 (sustainability). Based on this, in all scenarios the normalization of property T

i according to the K

z criteria was carried out in the range [−2; 2]. The normalization results are presented in

Table 3.

To consider this example, authors conclude that the geopolitical situation has the highest degree of negative impact (criterion K4) on the accessibility (property T2) in the gas industry according to the neutral scenario in the first of three time periods. At the same time, legislative features (K5), on the contrary, have a positive effect on adaptability (property T4). Similar conclusions by analogy can be drawn for other industries, time intervals and scenario conditions.

The values obtained by the authors were averaged for further use in a comprehensive assessment of the impact of external challenges on the FEC. The results are presented in

Figure 4 for all scenarios (where “=” is for the neutral scenario, “−” is for the negative scenario and “+” is for the positive scenario) over three time periods (2020–2025, 2025–2030, 2030–2035+). Grouping by time intervals on the graph for the negative and positive scenarios is similar to the basic one.

2.3. Analysis of the Impact of Technological Development on the Properties in LFEC

To identify the degree of influence of technological development on the change of properties Ti in the energy industries over three time periods (2022–2025, 2025–2030, 2030–2035+), a survey was formed for each LFEC. The degree of this impact, according to the results of the survey, was assessed on a scale from −10 to 10 with a discreteness of 1, where the values reflect:

−10—maximum degradation of technological development and, as a result, deterioration in the values of the properties of the energy industry;

0—no changes in the values of industry properties;

10—maximum technological development and, as a result, the improvement of the values of the properties of the energy industry.

The duration of the survey was 2 weeks. The selection of the expert group was carried out from structures related to research and educational activities, as well as from companies in the fuel and energy sector. During this period, 47 people took part in the survey, including employees of 12 educational institutions and representatives of 10 industry companies. This sample of respondents was formed in order to rely on the opinion of leading experts and professors from educational institutions close to the subject under consideration. According to the results, the degree of transformation of the properties of each LFEC and its direction was revealed.

The final assessment went from the local level to the global one. First, it was carried out for the LFEC by industry at three time intervals and then the median value was obtained. Scenario division was not performed at this stage.

According to Formula (3), median values were identified to characterize the behavior of properties at given time intervals.

where

—median value;

—lower limit of the median interval;

—median interval width;

—number of all values;

—pre-median cumulative frequency;

—number of observations in the median interval.

As an example,

Table 4 shows the obtained values of the impact of technological development in the gas industry on sustainability (property T

1) for the LFEC and the country as a whole (median values).

Based on the data obtained from experts, it can be concluded that the impact of technological development on the sustainability (T1) of the gas industry in the country will gradually increase (even though its initial weight is small at the LFEC levels). The highest final value is predicted for the sustainability of the Ural and Eastern LFEC, while a greater change in property compared to the initial one was revealed for the Central and Southern LFECs and the LFEC of Middle Volga.

When assessing, it is important (as in the previous stages) to correlate obtained results with the number of selected parameters Pn within the framework of the properties Ti. For this purpose, normalization was carried out according to Formula (2), where the median values were recalculated to a range of values quantitatively equal to the number of parameters.

Based on this, primary data were converted to another measurement scale, the result of which is presented in

Table 5 for the example mentioned earlier (sustainability (T

1) property of the gas industry). This normalization was required for further assessment of the total effect of both external challenges and technological development on the LFEC.

2.4. Obtaining Scenario Coefficients for the Development of FEC by Properties

To predict the state of an LFEC, a comprehensive assessment is required. The impact on the energy system is both external challenges and technological progress. These areas have been assessed in the previous sections. The summation result is shown in

Table 6 using an example similar to the previous sections.

The initial values of the properties Ti were taken as the starting point, and in all subsequent iterations, normalization was performed to the number of found parameters Pn. Thus, it became possible to sum the results obtained for each period of time in each scenario in order to obtain property coefficients. Further, the obtained value was divided by the number of found parameters Pn, by means of which the normalization was carried out.

3. Results and Discussion

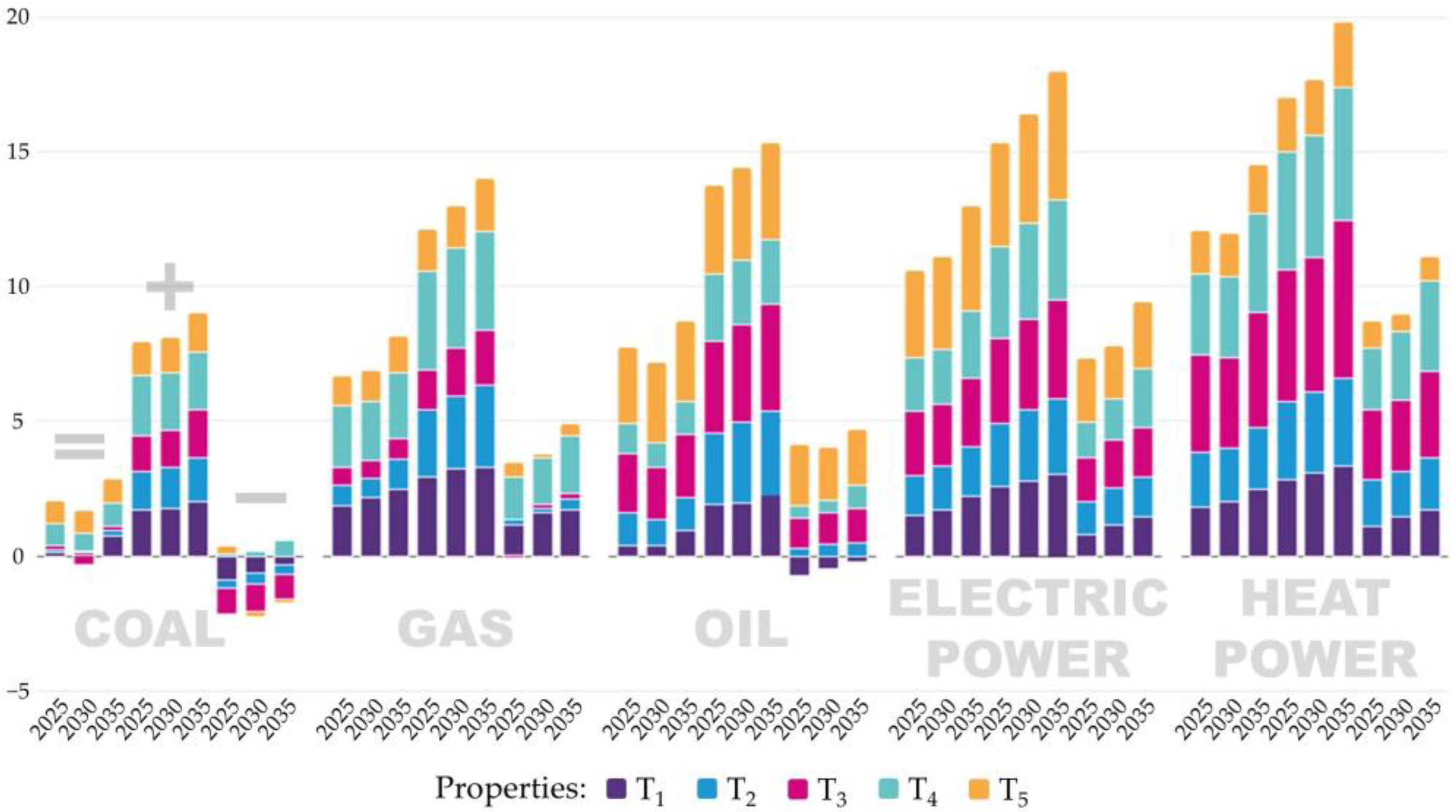

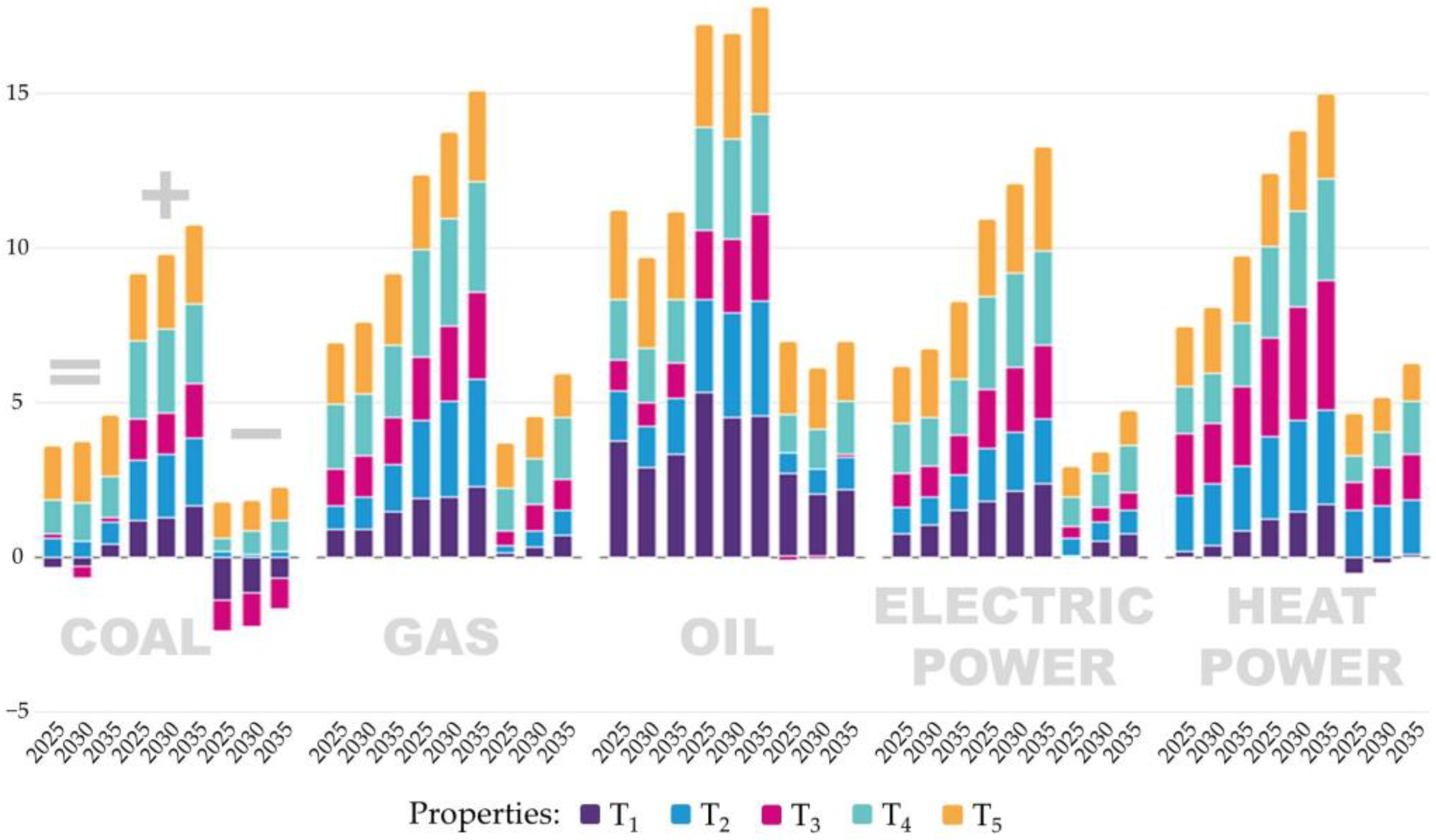

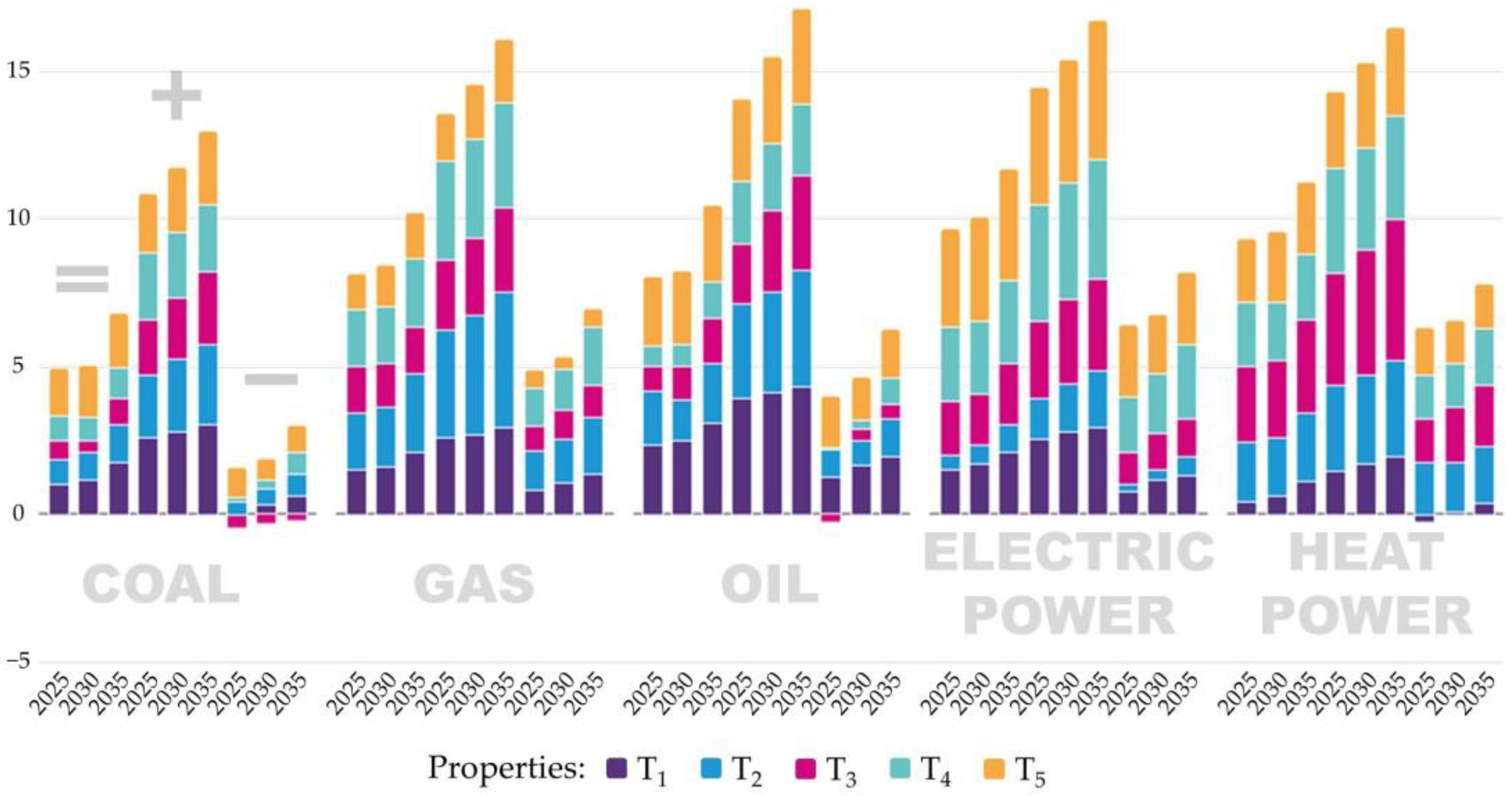

Based on the results of a comprehensive assessment of the prospects of FEC development under the influence of global challenges and technology development, scenario coefficients of FEC development were obtained for each of the seven LFECs. The resulting charts, showing the degree of development of main energy industries for the three scenarios (negative, neutral and positive) for the selected time intervals (2020–2025, 2025–2030, 2030–2035), are presented in

Figure 5,

Figure 6,

Figure 7,

Figure 8,

Figure 9,

Figure 10 and

Figure 11. In these, the division within industries into neutral (“=”), negative (“−”) and positive (“+”) scenarios is similar to the coal industry.

In all charts, the columns representing the sum of the coefficients of Ti properties are divided into five groups by the energy industry. The first nine columns describe the coal industry, and the next nine columns describe the gas industry, followed by oil, electricity and heat energy. In each group, the first three columns describe the obtained coefficients for the neutral scenario, the next three for the positive scenario, and the last 3 columns for the negative scenario.

The significance of the contribution of one of the five properties to the development of a particular energy sector under the chosen scenario at a certain time interval is determined by the proportion of the corresponding color in the column under consideration. For example, the development of the electric power industry of the Central LFEC under neutral and positive scenarios at all time intervals is mostly influenced by reliability (T5).

High values of the obtained property coefficients indicate the potential for growth in the level of development of the industry. On this basis, an almost linear increase in the values of the coefficients of properties in industries, observed in some cases, reflects regions that prevail in the rate of their development. These rates are related to both the external background and the internal level of technological development.

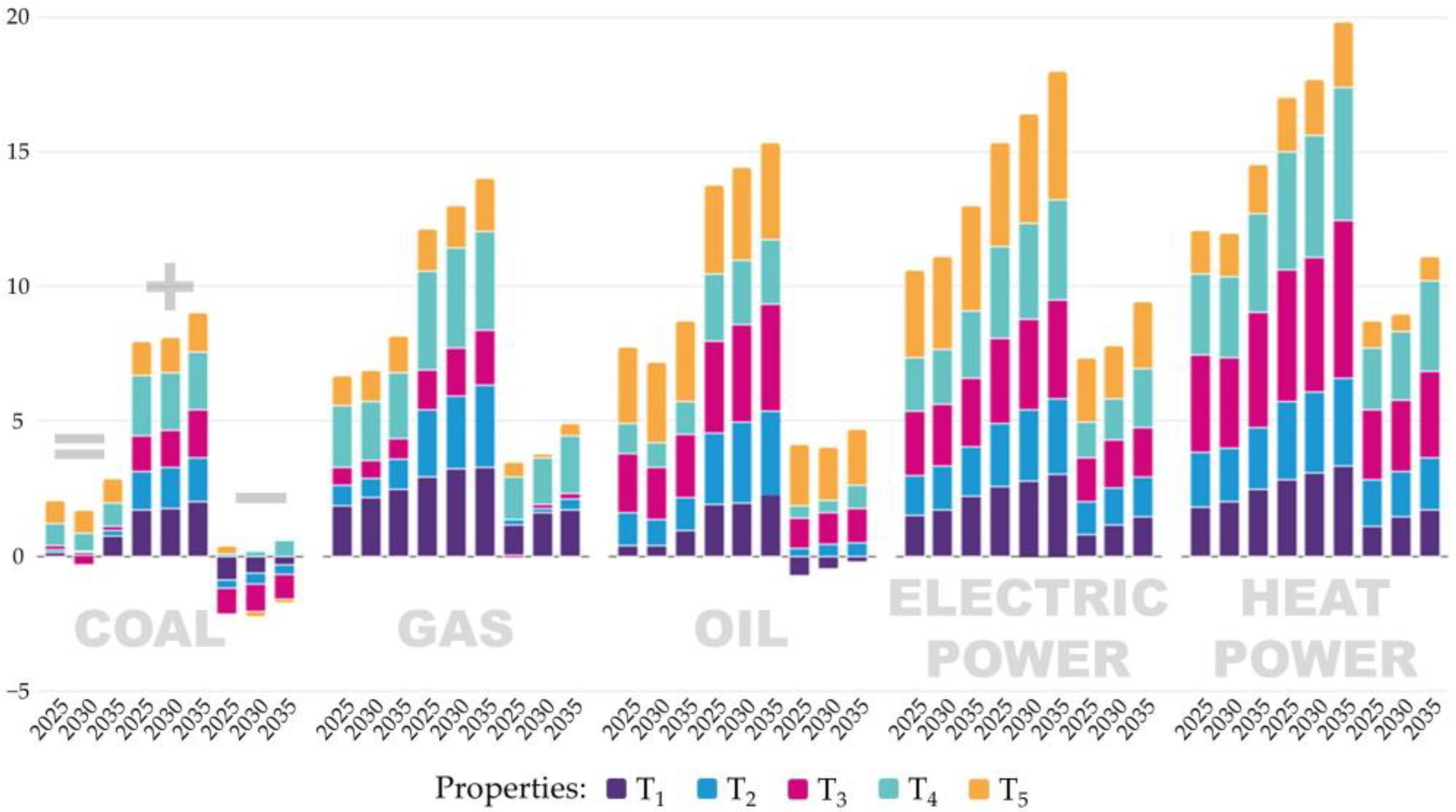

The authors have identified that the greatest development in the Central LFEC in all scenarios is electric and heat power, which is shown in

Figure 5. The greatest contribution to this development in the electric power industry belongs to its reliability T

5, and in the heat power industry to efficiency T

3. In the heat power industry, large losses occur during heat transmission, which is the main problem of the industry in conditions of its relatively high level of development in the central region. Therefore, the main reserve for increasing it is to improve the efficiency of heat transmission and generation. In turn, due to the high performance of other properties, the main development of the electric power industry in the central region might take place precisely because of the increase in reliability.

For the coal and oil industries in the negative scenario, and (in terms of T3 efficiency) even in the neutral scenario, there are negative values of the coefficients of some properties. This indicates a regression in the coal industry and a slowdown in the development of the oil industry, partly due to the lack of large deposits in the central region.

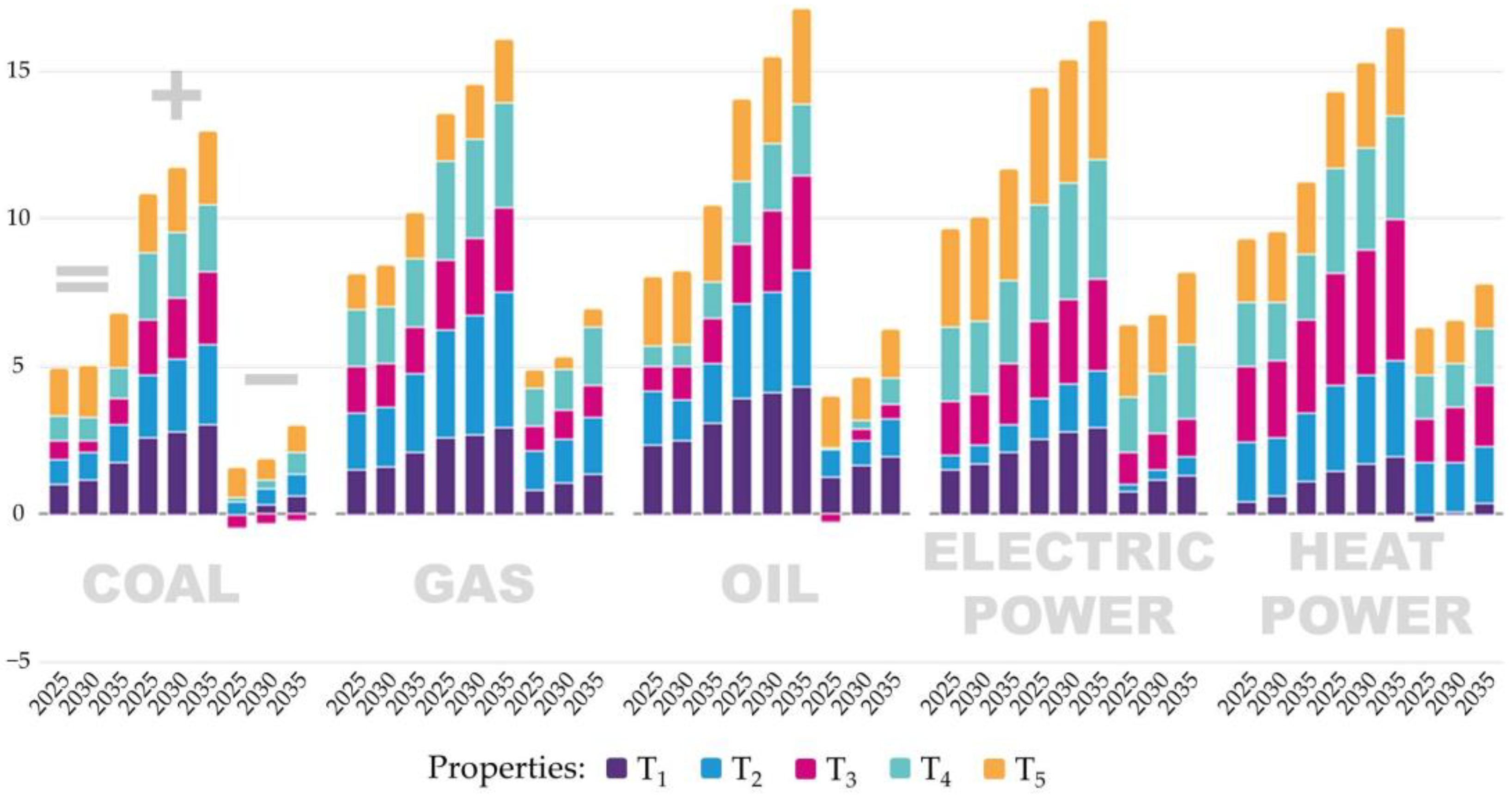

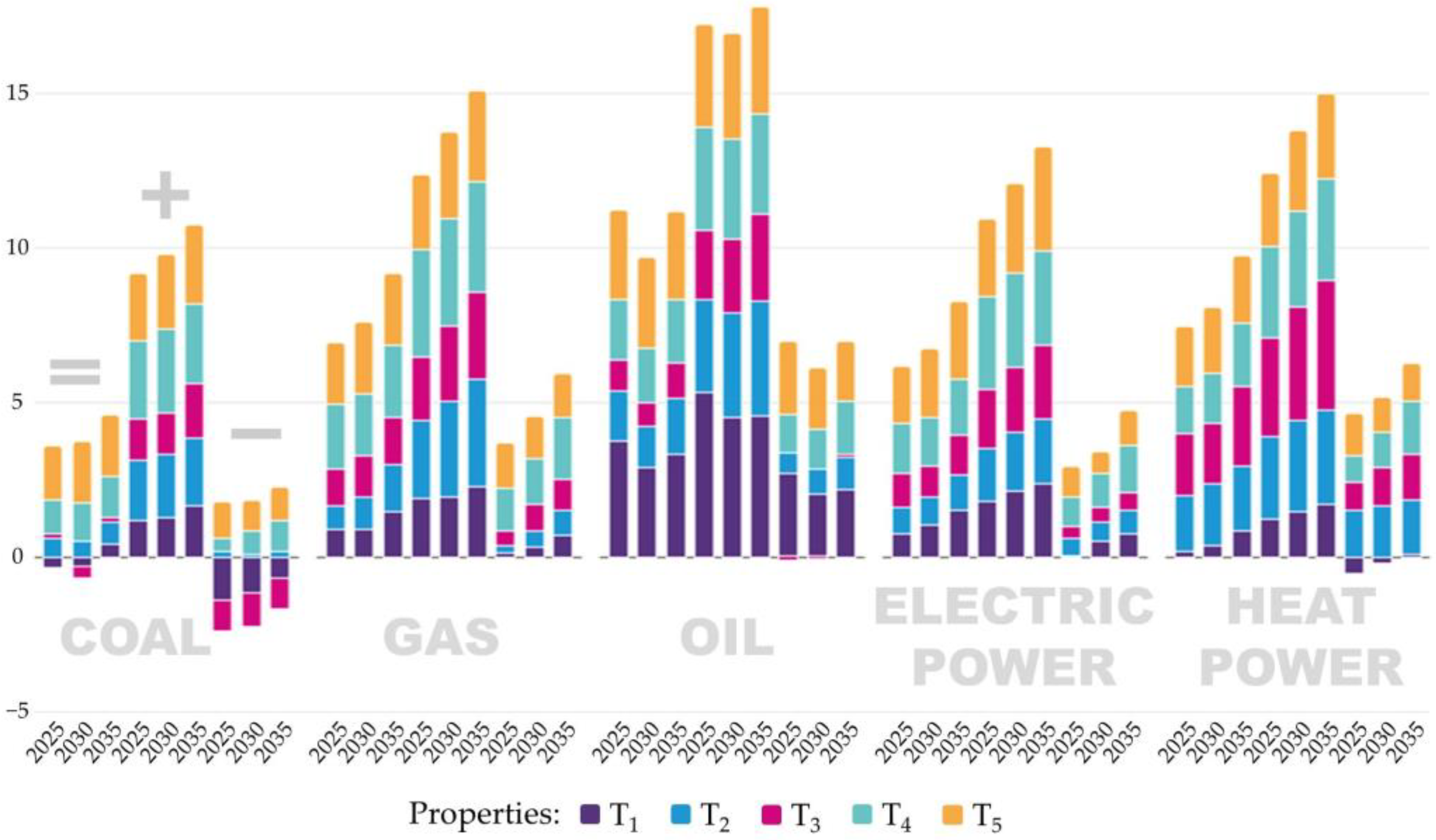

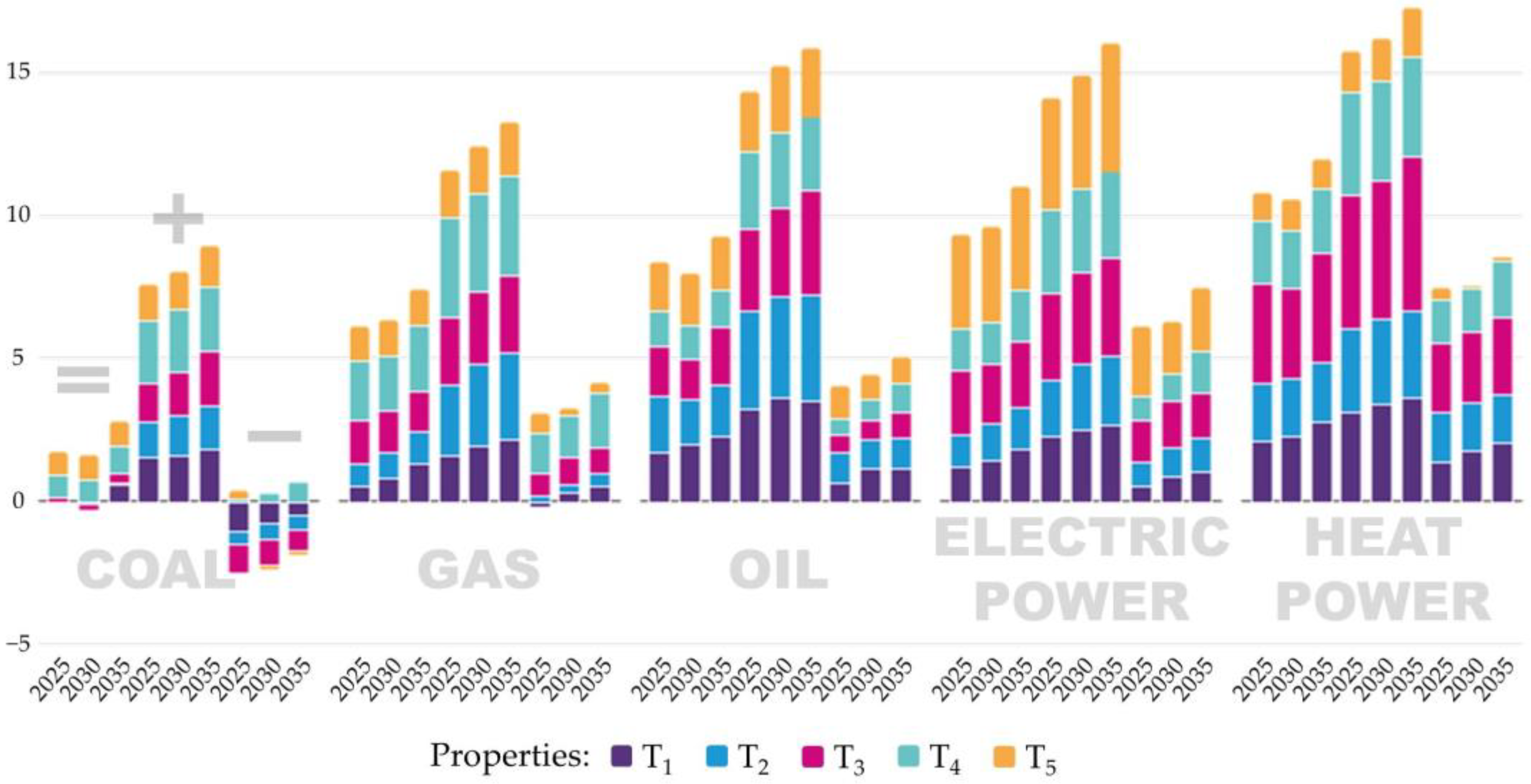

The most developed energy sector of the Southern LFEC in all scenarios is the oil industry, mostly because of its sustainability T

1 influence, which is shown in

Figure 6. However, this case is atypical. First, in the time period 2025–2030, there will be a decrease in the level of industrial development compared to 2020–2025. Then, by 2030–2035, a growth stage will begin, differing between scenarios only in its rate. The decline in development is due to the fact that in this region, the oil and gas industry is represented mainly by refining facilities and transportation. In any of the scenarios at the initial stage, it is expected to change the transport chains and to make the reorientation of markets, which temporarily causes a slowdown in industrial development.

In the negative scenario, the weights of the positive and negative values of the property coefficients are almost equal. This is a logical outcome of the low connection between the Southern LFEC and the coal industry at present. This correlation points to the need for consideration of the sustainability and adaptability of the industry as points of future growth.

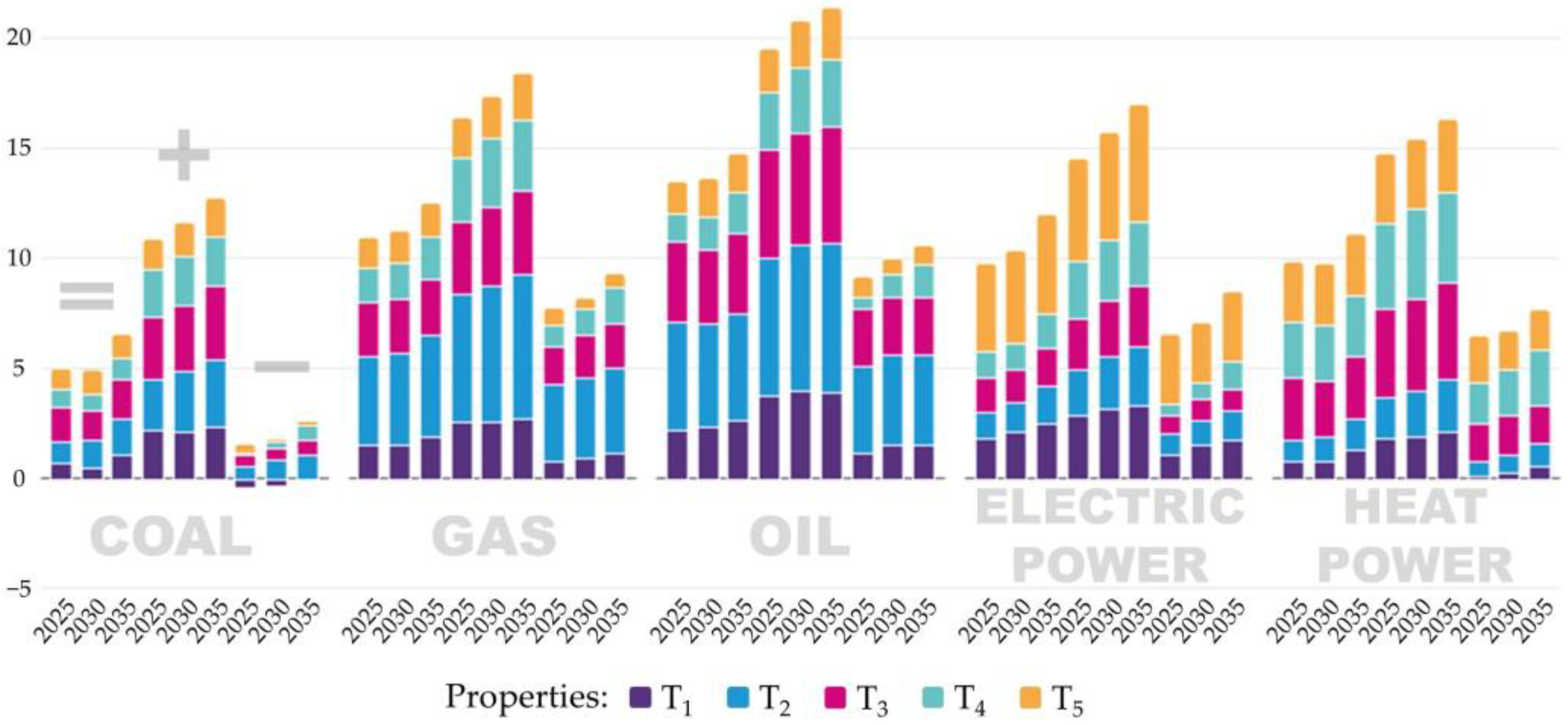

In the case of the North-Western LFEC, all industries might develop harmoniously, and it is not reasonable to single out a leader among them. In each of the industries, the greatest contribution is made by different properties, which is due to their specifics. This correlation is shown in

Figure 7. The coal industry demonstrates a noticeable lag in the case of the negative scenario. Despite the potential for the development of mining in the Pechora coal basin, opportunities for this are not presented in a negative scenario. The main effort goes to the maintenance and development of the more priority industries for the residents of the region—heat and electricity power.

According to the results of the analysis, the North-Western LFEC is characterized by gradual high rates of the development of industries, which is expressed by the linearity of the increase in the contributions of the properties’ coefficients. In the future, this LFEC might be on the same level as the Central LFEC in terms of industrial development.

The LFEC of the Middle Volga is characterized by the absence of a clearly leading industry with approximately the same level of development of heat and electric power, as well as the oil industry. In terms of the oil industry and electric power development, this might occur in equal proportions at the expense of all properties of energy systems (

Figure 8).

This region also lacks large deposits of minerals, but there are many industrial facilities and industries along the Volga River. This stimulates the development of heat and electric power industries to provide production in positive and neutral scenarios while increasing the volume of output. The development of the oil industry in this case is caused by a change in trade relations due to the transport role of the LFEC.

The oil industry is the leading one of the Ural LFEC, the development of which is supported by increasing accessibility T

2, which is proved by

Figure 9. The sustainability T

1 and T

3 efficiency of this industry also contributes greatly to its development in each of the scenarios. The priority of the oil industry is associated with the concentration of most of the oil production capacity in the area. In addition, this region is a transportation route for another oil-producing region, the Siberian LFEC. On this basis, the development of its availability will be conditioned by the development of oil transportation and storage technologies.

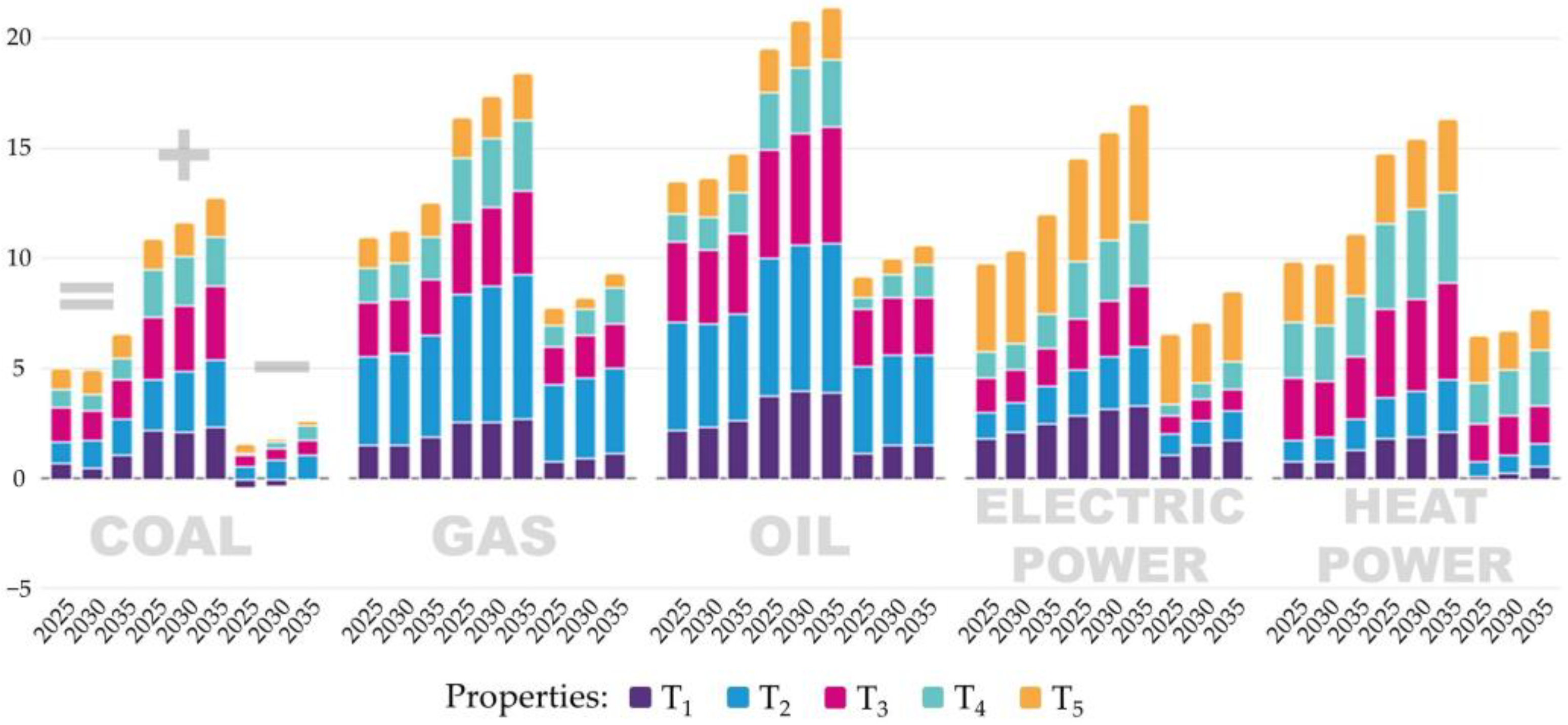

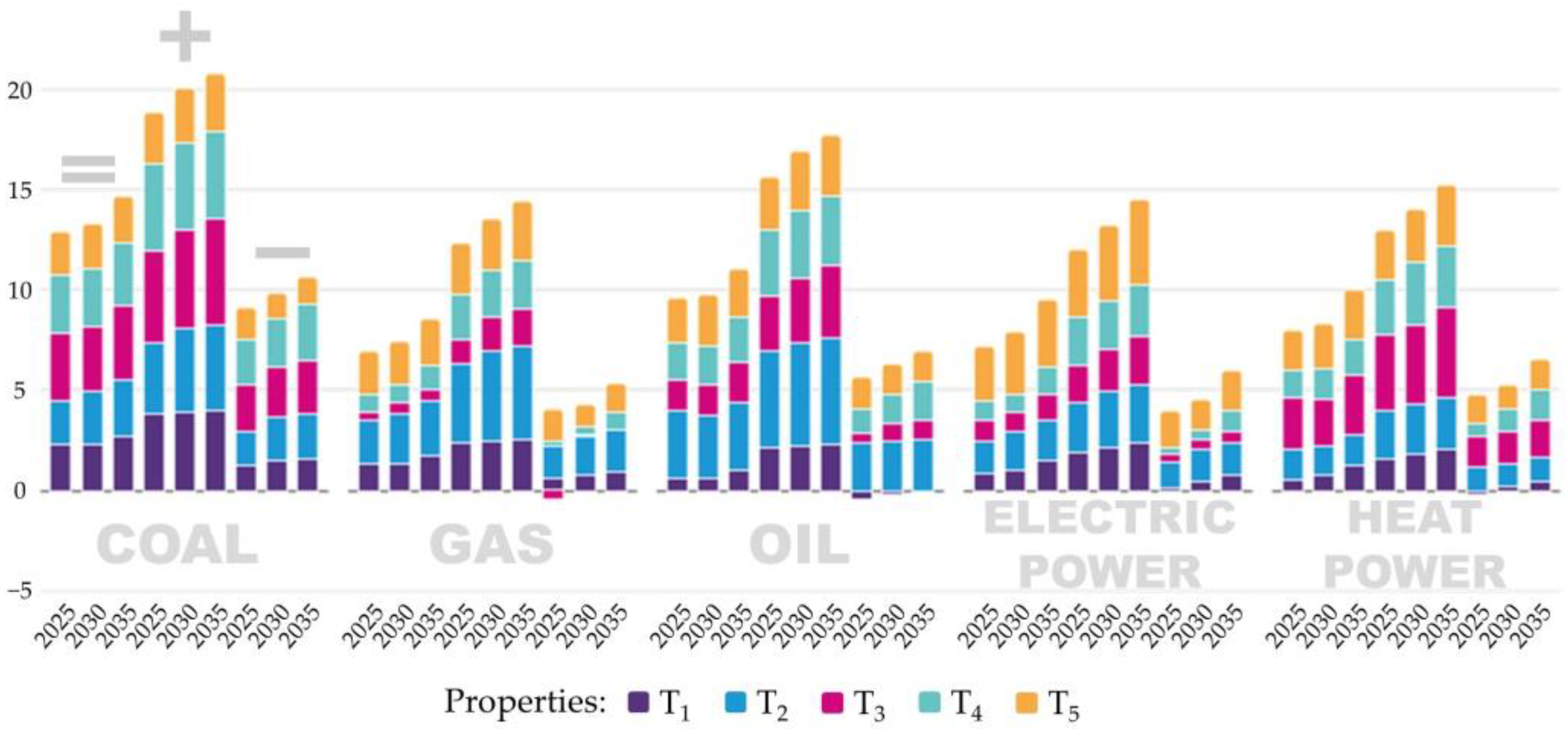

In the territories of the Siberian LFEC, the strongest development might be in the coal industry (shown in

Figure 10). The joint growth of the level of value of all properties leads to the fact that the rate of development of this industry becomes the leader in all scenarios. At the same time, the gas, heat energy and electricity industries develop slower than in other regions (with the exception of the Eastern LFEC).

This region is a leader in terms of reserves and production of minerals in almost all industries, but the coal industry might receive special development because of the predominance of deposit capacity relative to other LFECs. Moreover, unlike the oil and gas industries, where their development can be supported by the LFEC of the Urals, there is no such opportunity for the coal industry. The vastness of Siberia’s territory, uneven population density, and harsh climatic conditions slow down the development of heat and electricity in this LFEC.

The Eastern LFEC is characterized by the low level of development of almost all industries due to its remoteness from the central regions, low population density and isolated infrastructure. The oil and coal industries will develop the most in all scenarios, mostly at the expense of accessibility T

2 and reliability T

5. It is clearly shown in

Figure 11. The development of the coal industry in Eastern LFEC, however, partly depends on the level of production in Siberian LFEC.

Thus, modeling of the impact of scenario criteria due to global challenges in the development of industries through properties and assessing the impact of technological development on their change will allow tracing the mutual influence of challenges and technological progress on the structure of the energy supply. This, in turn, will make it possible to determine the problematic points of development and the areas required for investment in order to maintain the target values of the properties of power systems in the long term.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}