Decarbonization Pathways, Strategies, and Use Cases to Achieve Net-Zero CO2 Emissions in the Steelmaking Industry

, ,

, ,

Abstract

:1. Introduction

2. Decarbonization Pathways

- The consumption of electrical energy from renewable sources.

- The use and generation of green hydrogen (H2).

- The consumption of NG.

- The transition to alternative carbon sources.

- The consumption of iron ore and pellets.

- The increased use of scrap.

- The development and implementation of CO2 storage technologies.

- The production and use of CCU products.

- The optimized blast furnace–basic oxygen furnace (BF-BOF) route (Route 1).

- A route based on direct reduction (DR) (Route 2).

- Reduction by smelting (Route 3).

- The electrolysis of iron ore (Route 4).

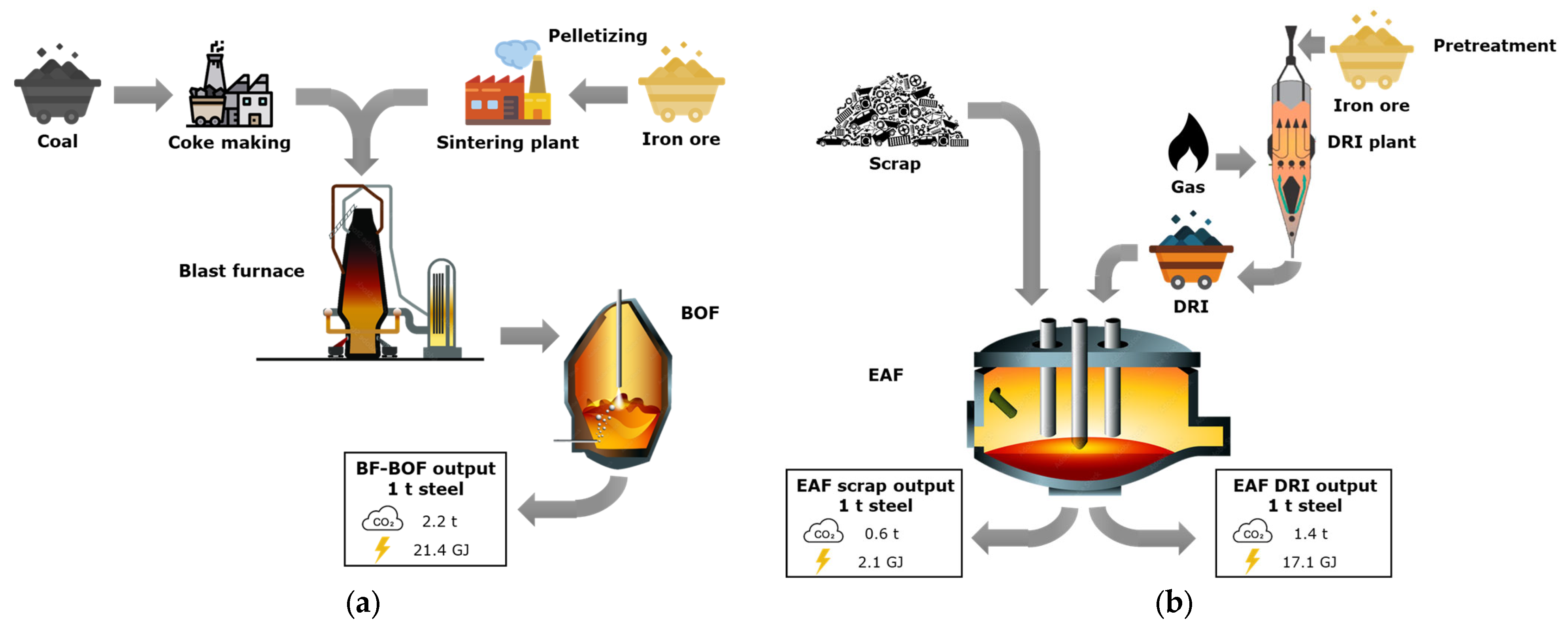

2.1. Energy, Raw Materials, and Carbon Capture Overview

2.2. Hydrogen

2.3. Electricity

2.4. Policy and Decarbonization Barriers

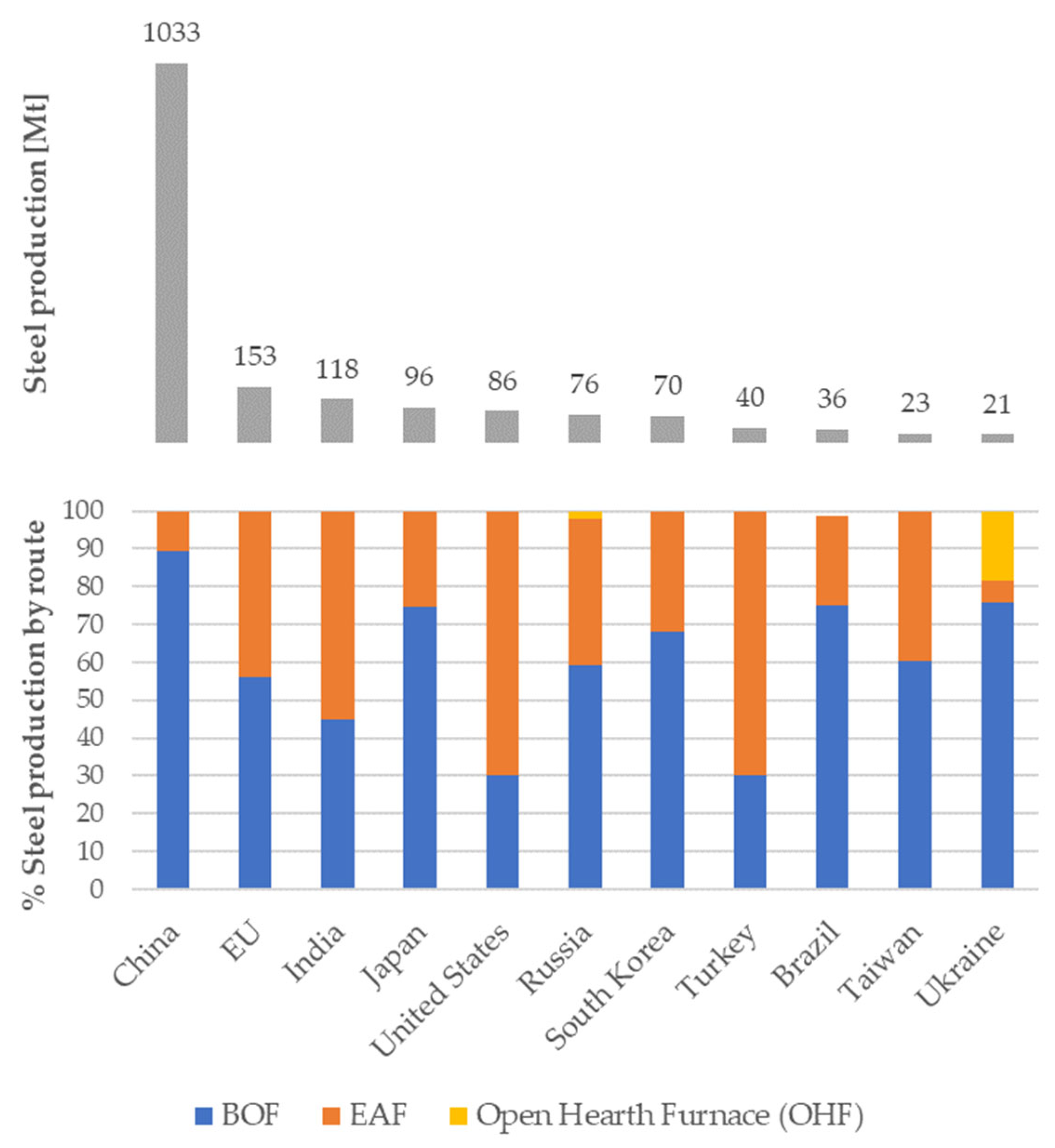

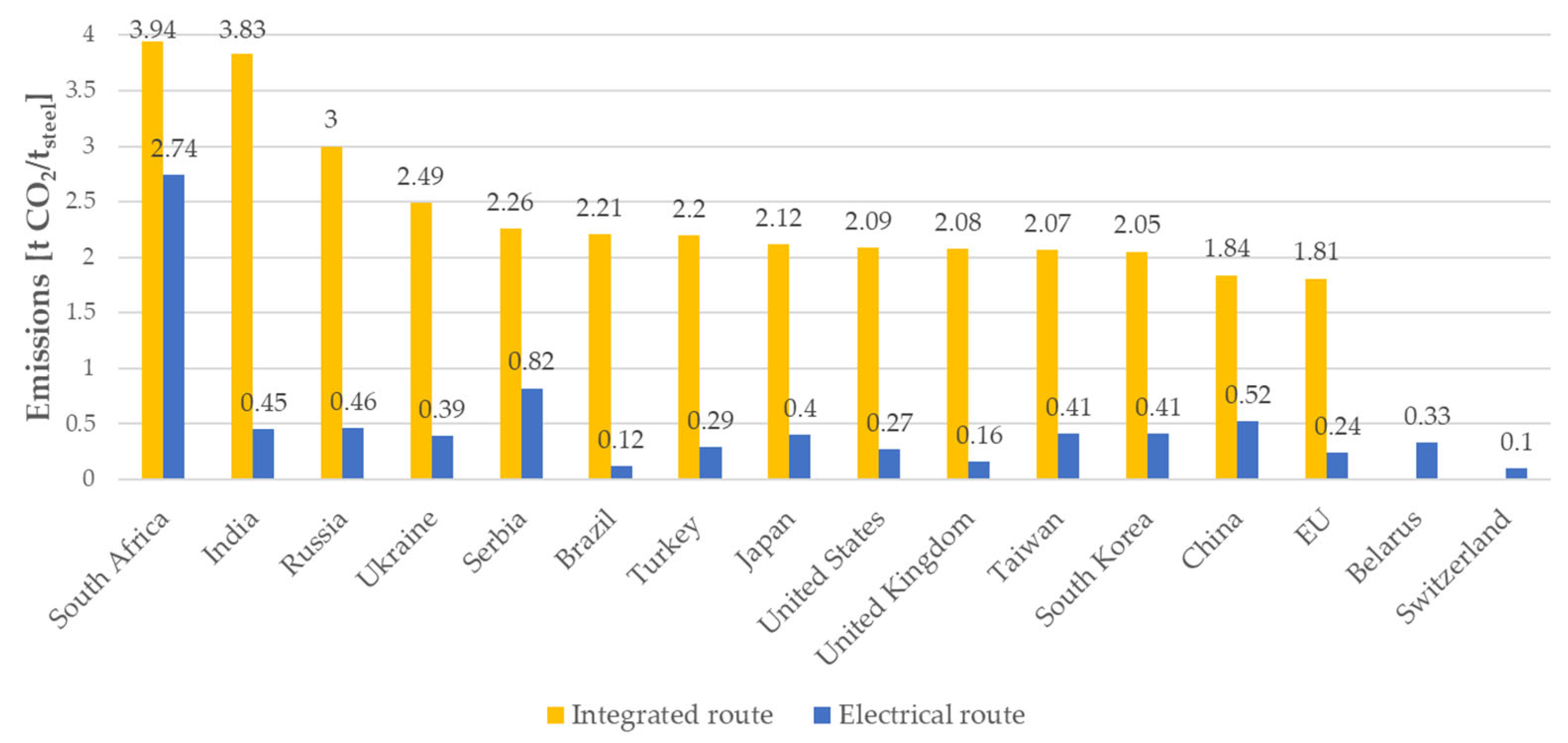

3. Decarbonization Strategies by Top Steel Producers

- Short term: sinter replacement by pellets, ferrous scrap usage’s increase, increase the energy efficiency of the processes, and start replacing NG with H2.

- Midterm: include CCS and start using pure H2 as a reductant.

- Long term: full deployment of H2 technologies to produce steel and use renewable energy sources.

- Identify and characterize new opportunities to use and reuse lower-quality scrap by having a better understanding of the scrap market and the opportunities.

- Select and integrate the best available technologies to upgrade, sort, and characterize lower-quality scrap to enhance the scrap quality.

- Create industrial demonstrators of scrap sorting/cleaning based on innovative combinations of BATs.

- Define valorization routes of the waste generated by the upgrading schemas.

4. Use Cases

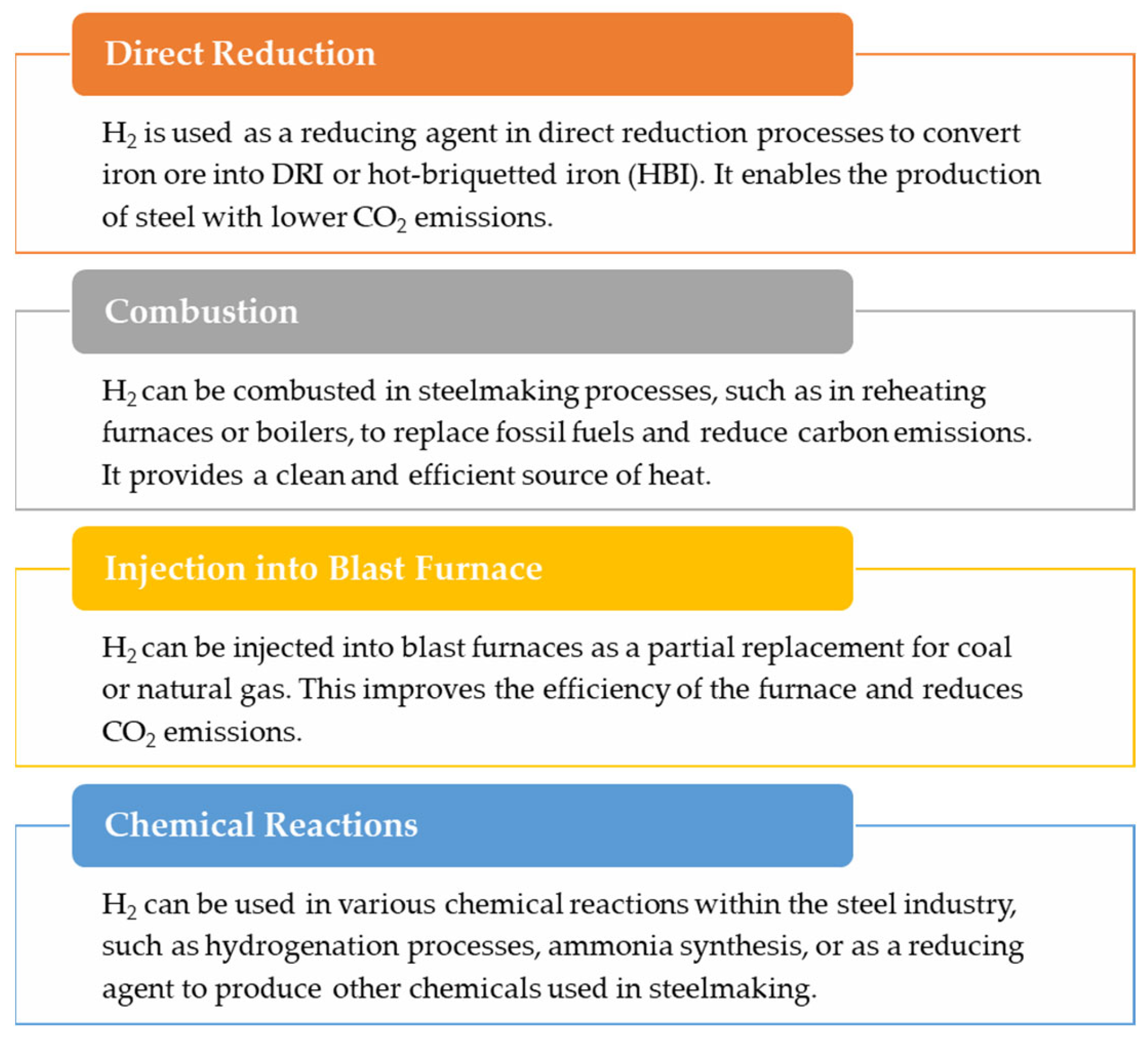

4.1. Hydrogen in the Steel Sector

- Utilize renewable energy for the EAF operation.

- If fossil fuels such as NG are still being used:

- Gradually increase the H2 content.

- Capture CO2 emissions from the DRI process.

- Reuse the captured CO2 within the process.

- Incorporate H2 in the DRI process:

- Use blue hydrogen.

- Transition to 100% green hydrogen.

- Achieve the goal of complete decarbonization.

- Injecting H2-rich streams or biogas to replace coke consumption.

- Fix CO2 into a chemical compound by using additional H2.

4.2. Use Case 1: Hot Rolling Mill

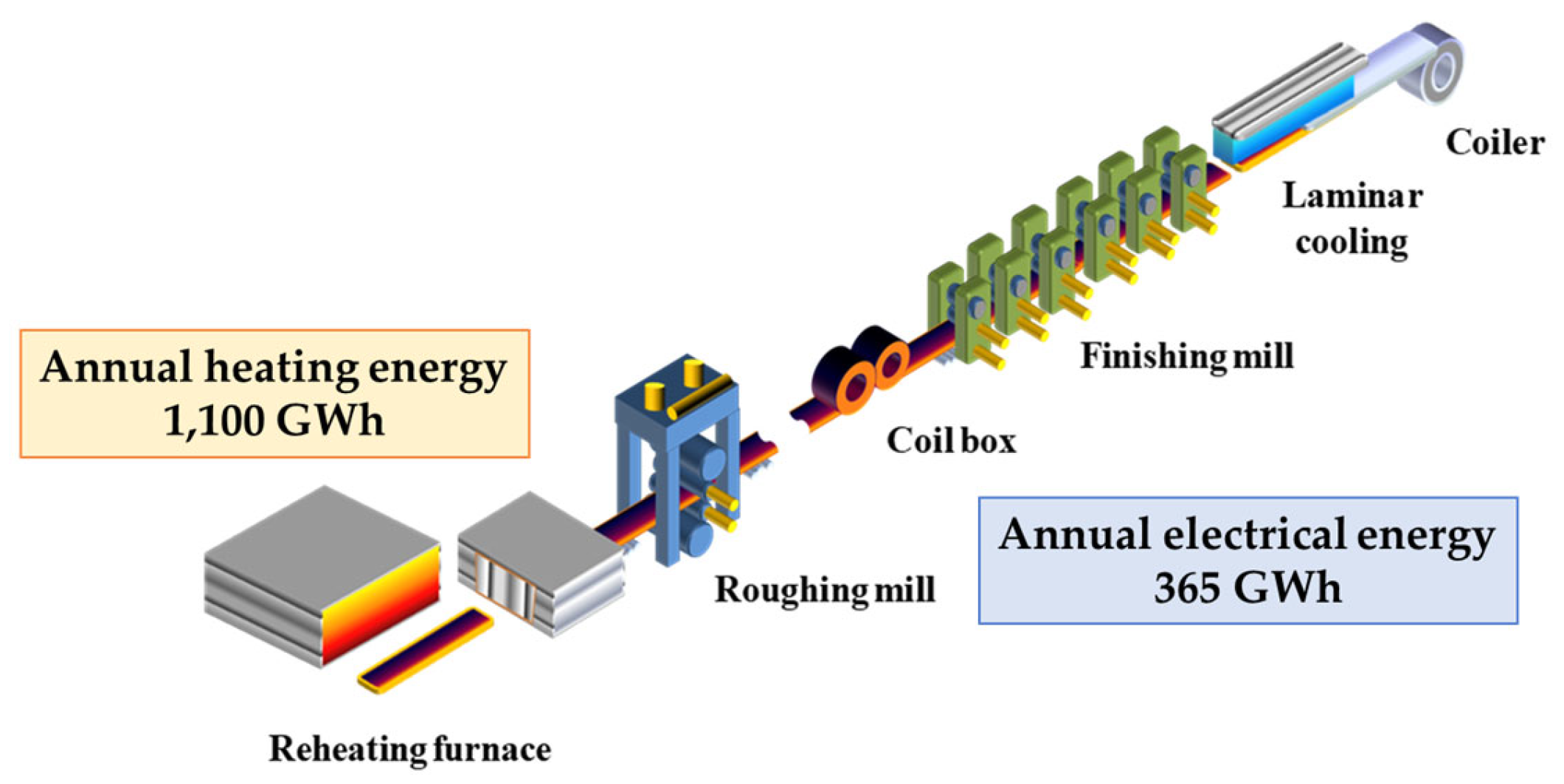

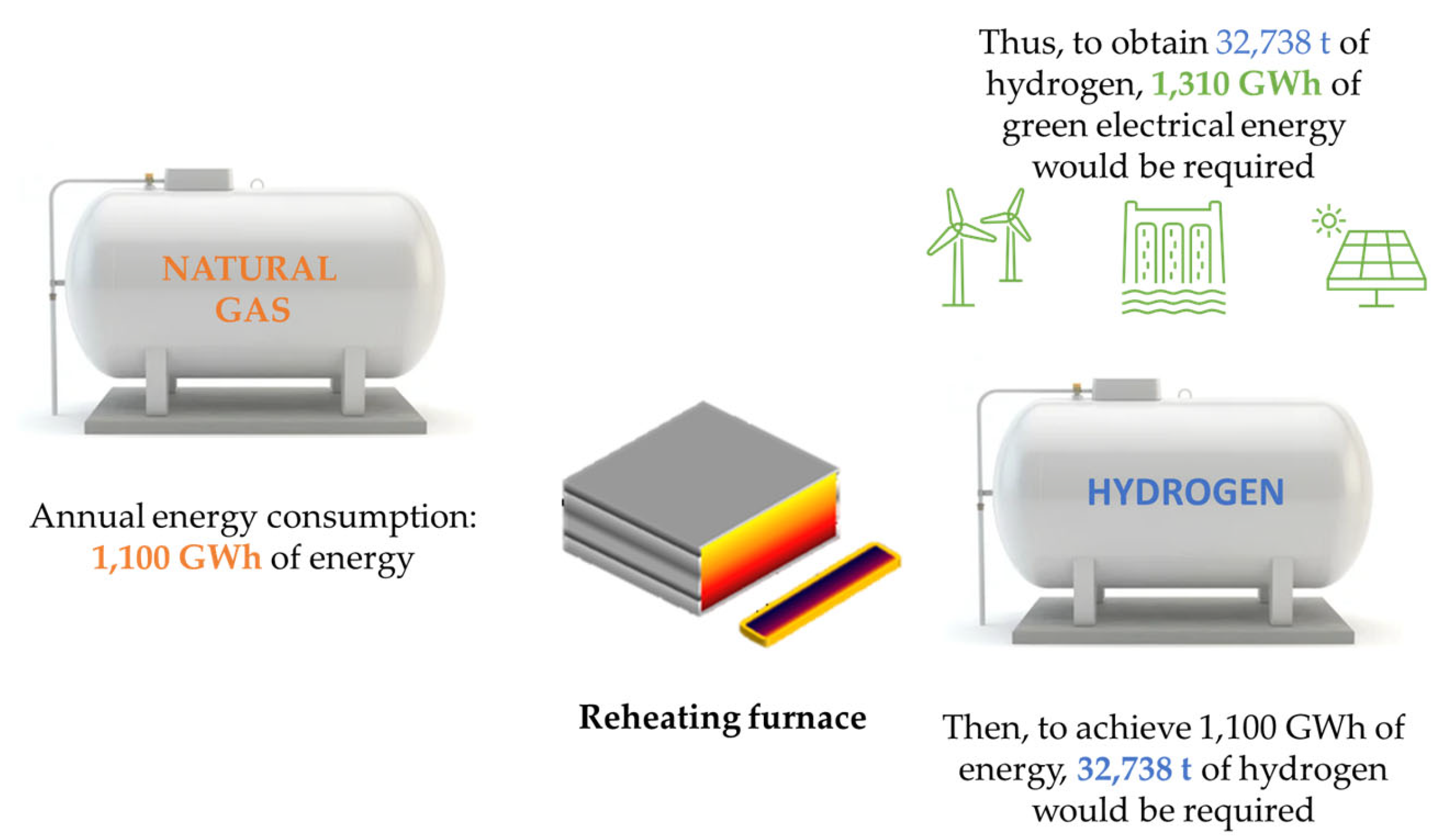

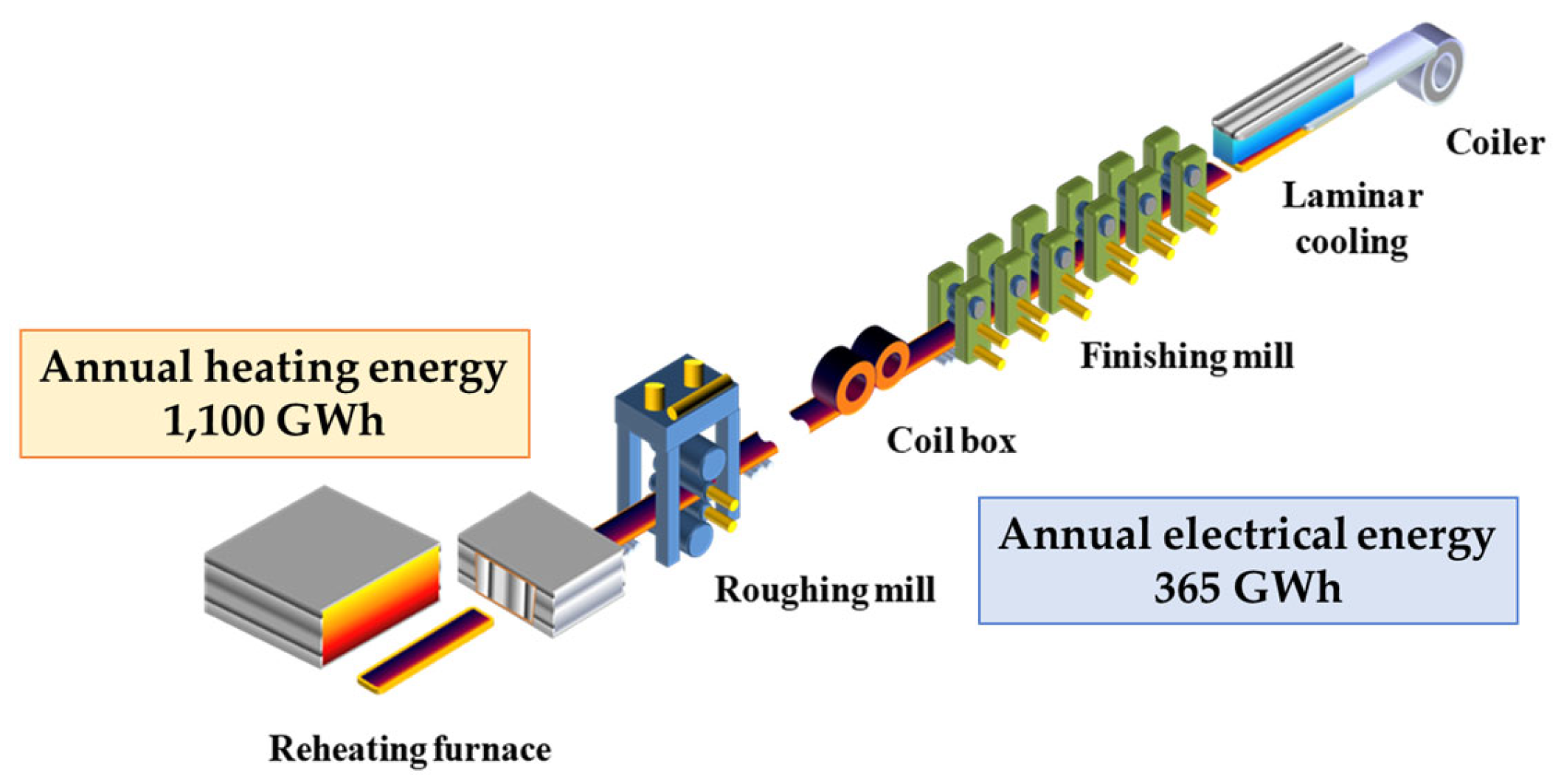

4.2.1. Average Values of Electrical Energy Demand in a Hot Rolling Mill

4.2.2. Hydrogen as a Reheating Furnace Fuel

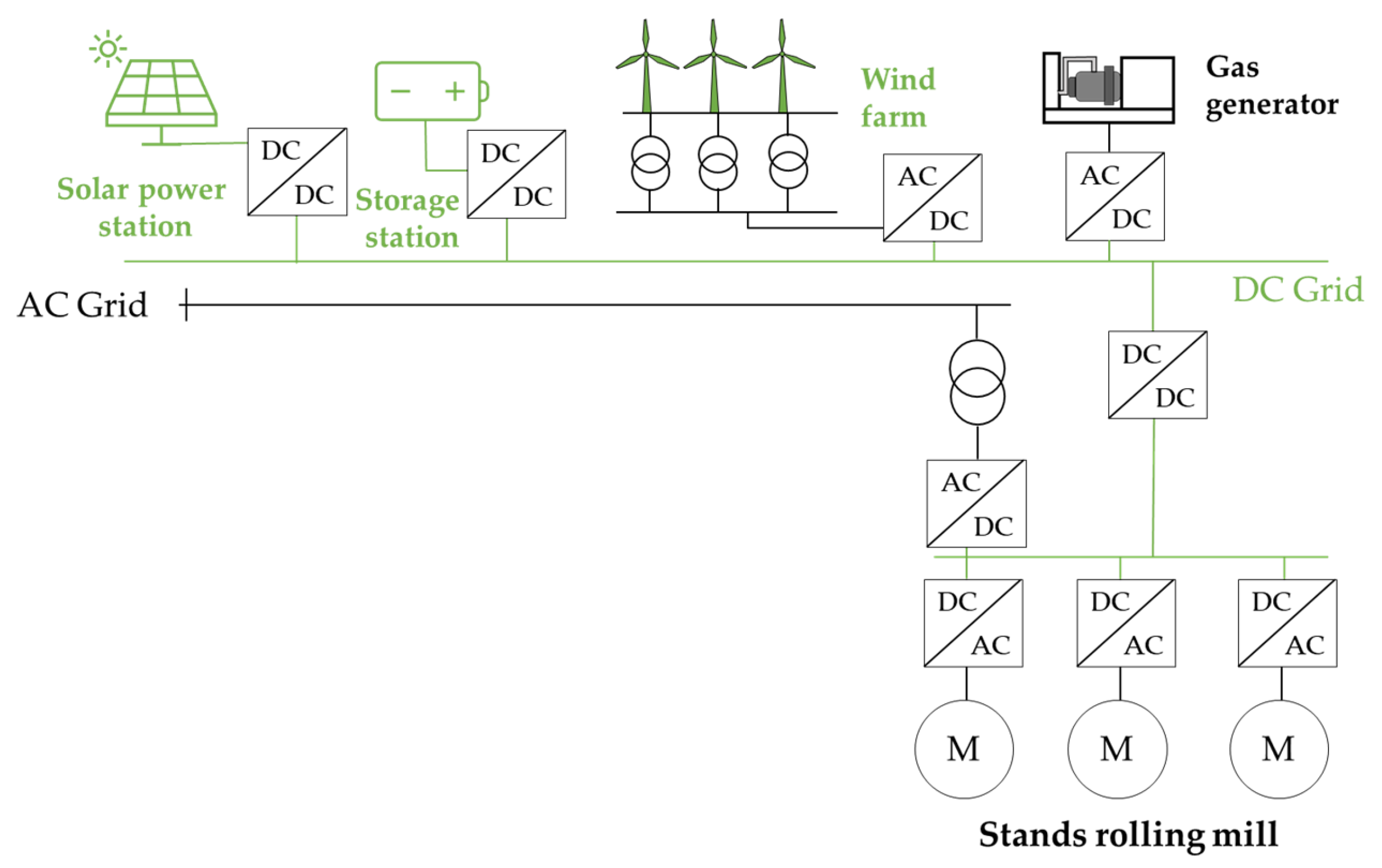

4.2.3. New Electrification Approaches

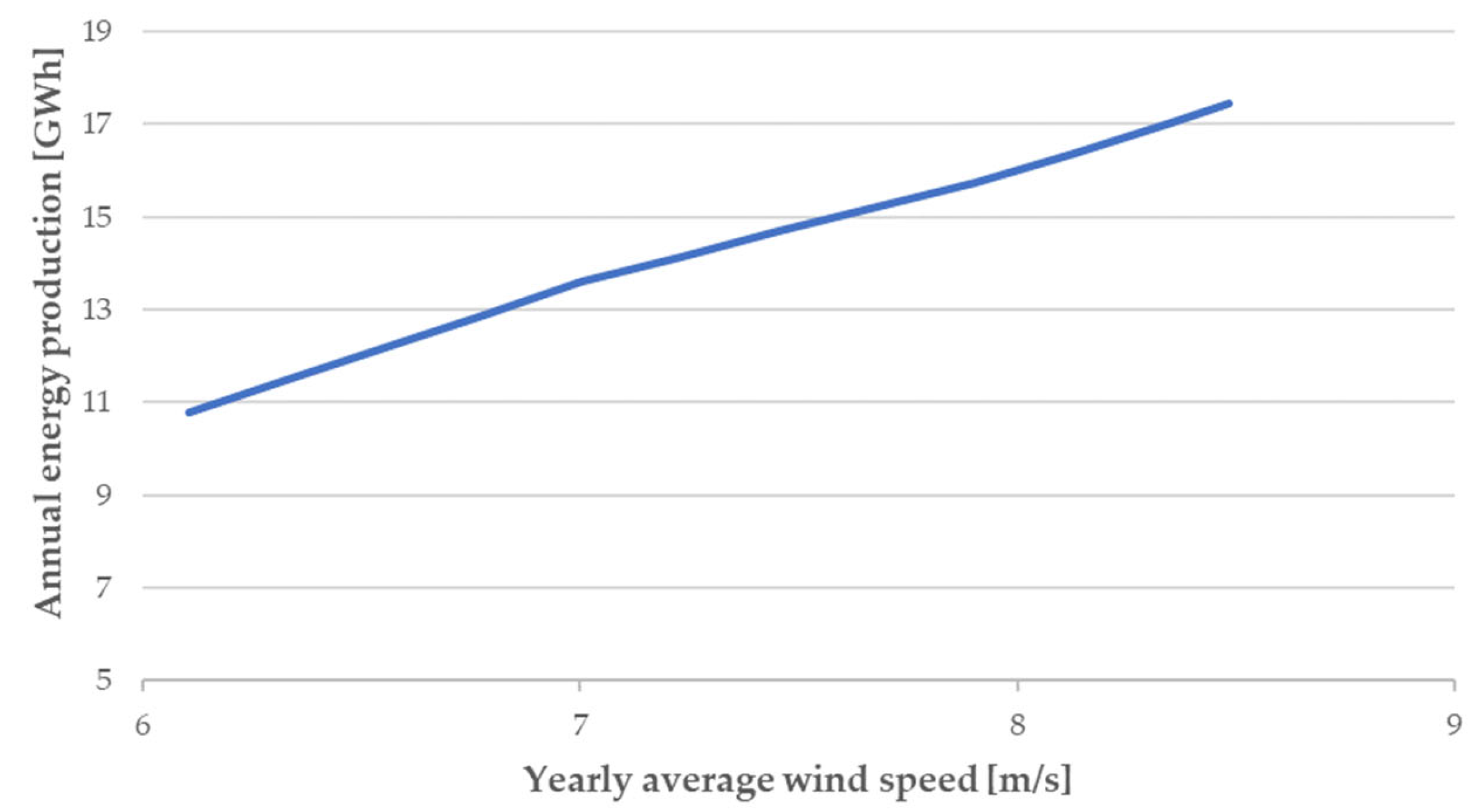

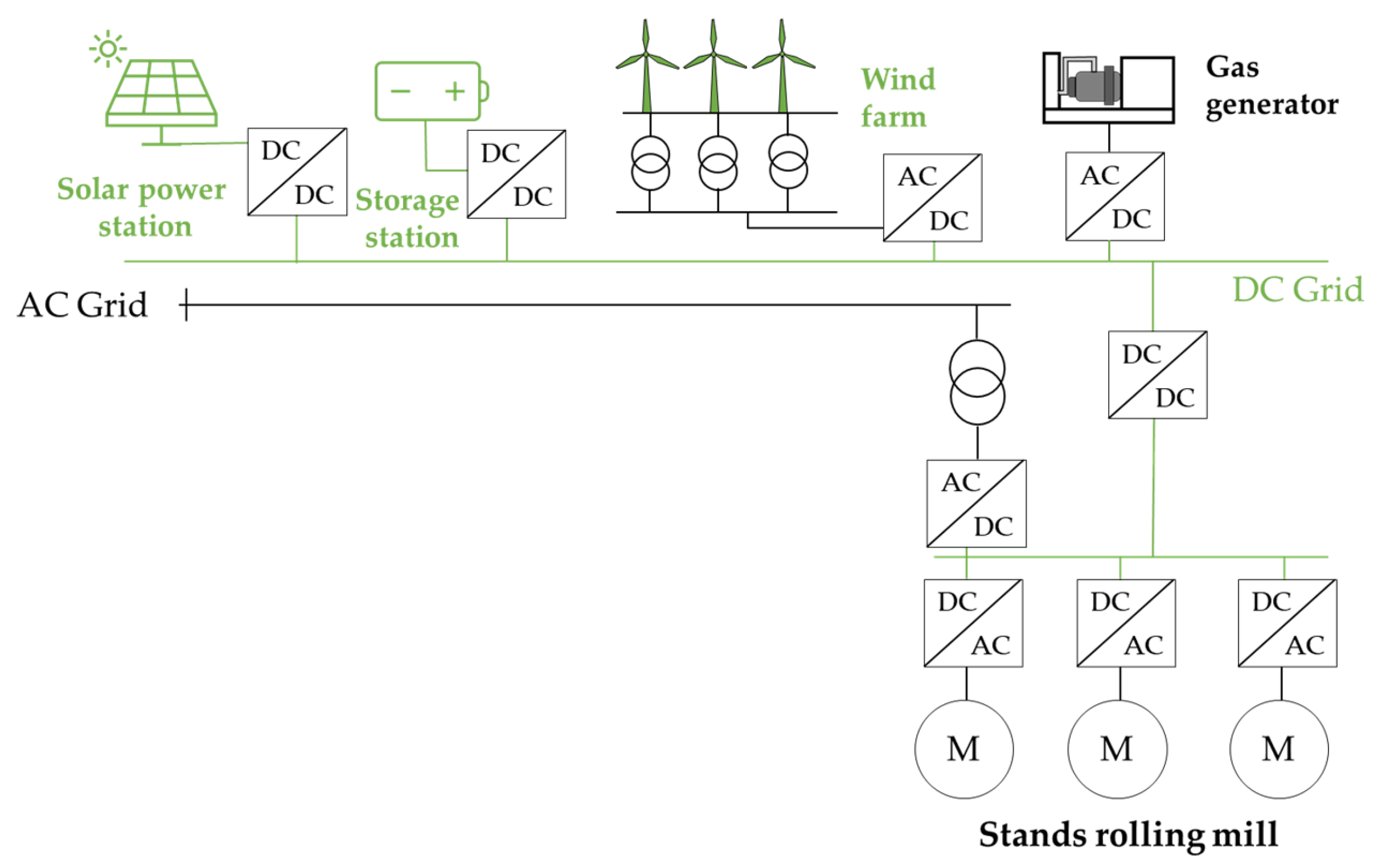

Renewable-Energy-Production Systems

Battery Storage Systems

Upgrading of the Rolling Mill Drives

Integration of Renewable Energy Sources into the Distribution Network

Energy-Management Optimization

4.2.4. CO2 Emissions

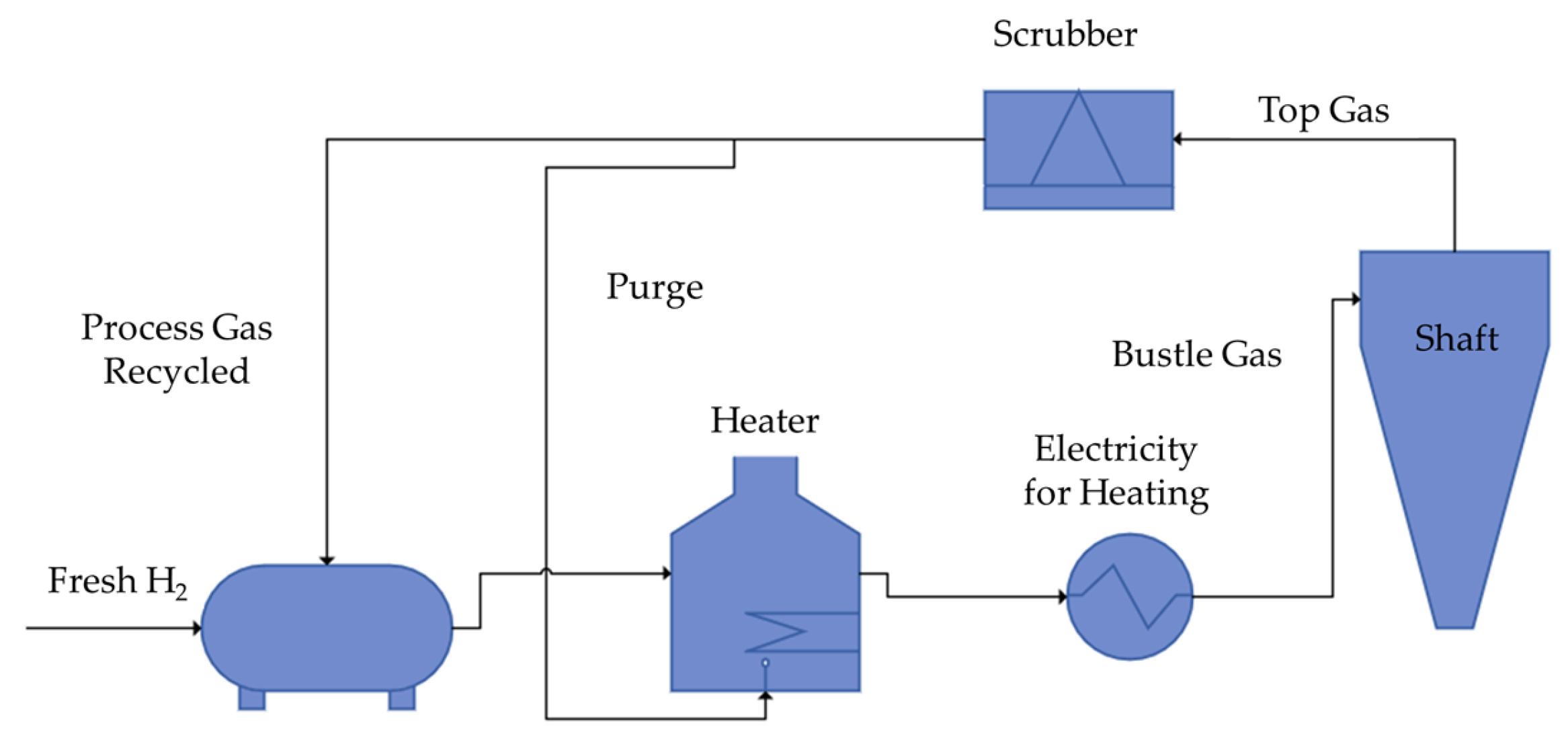

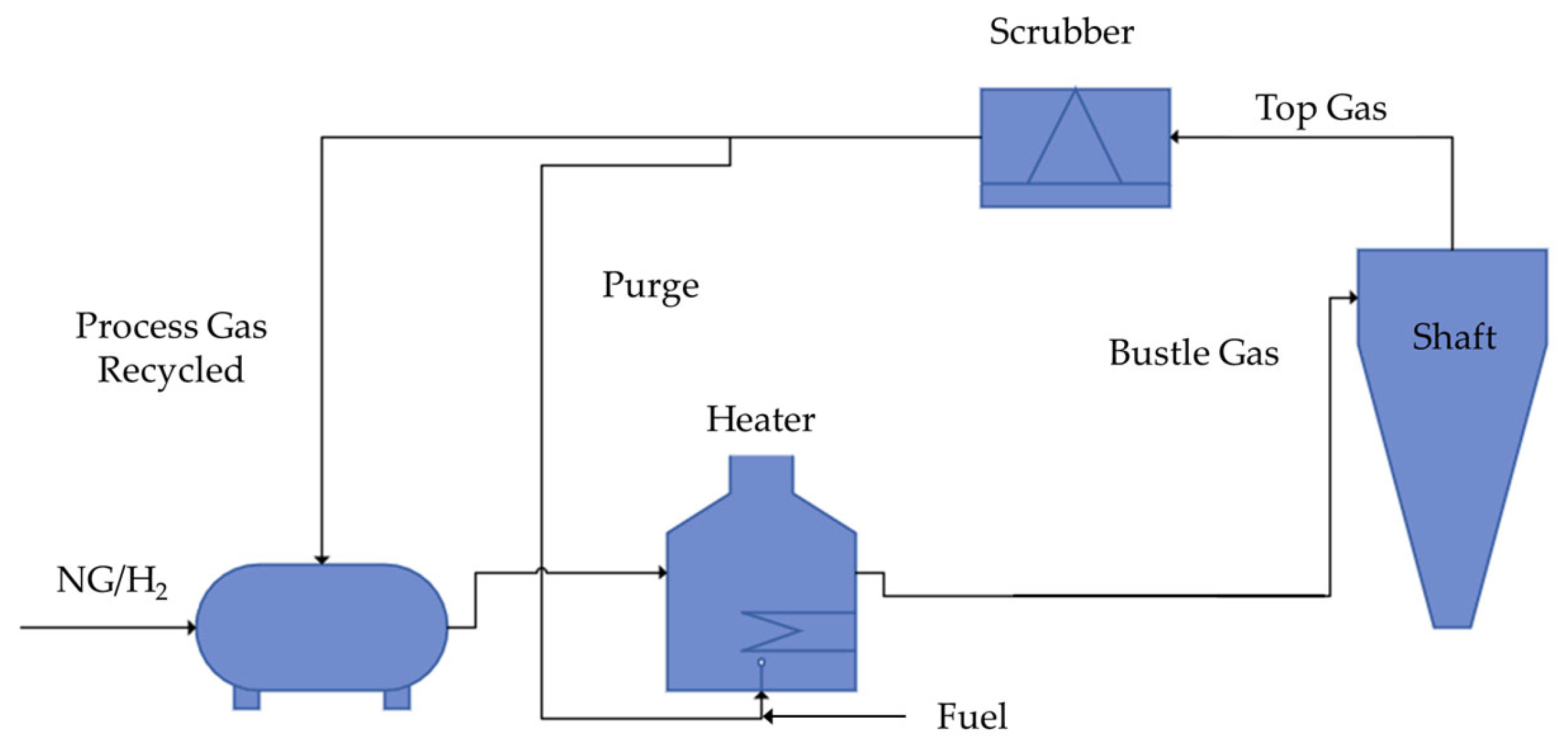

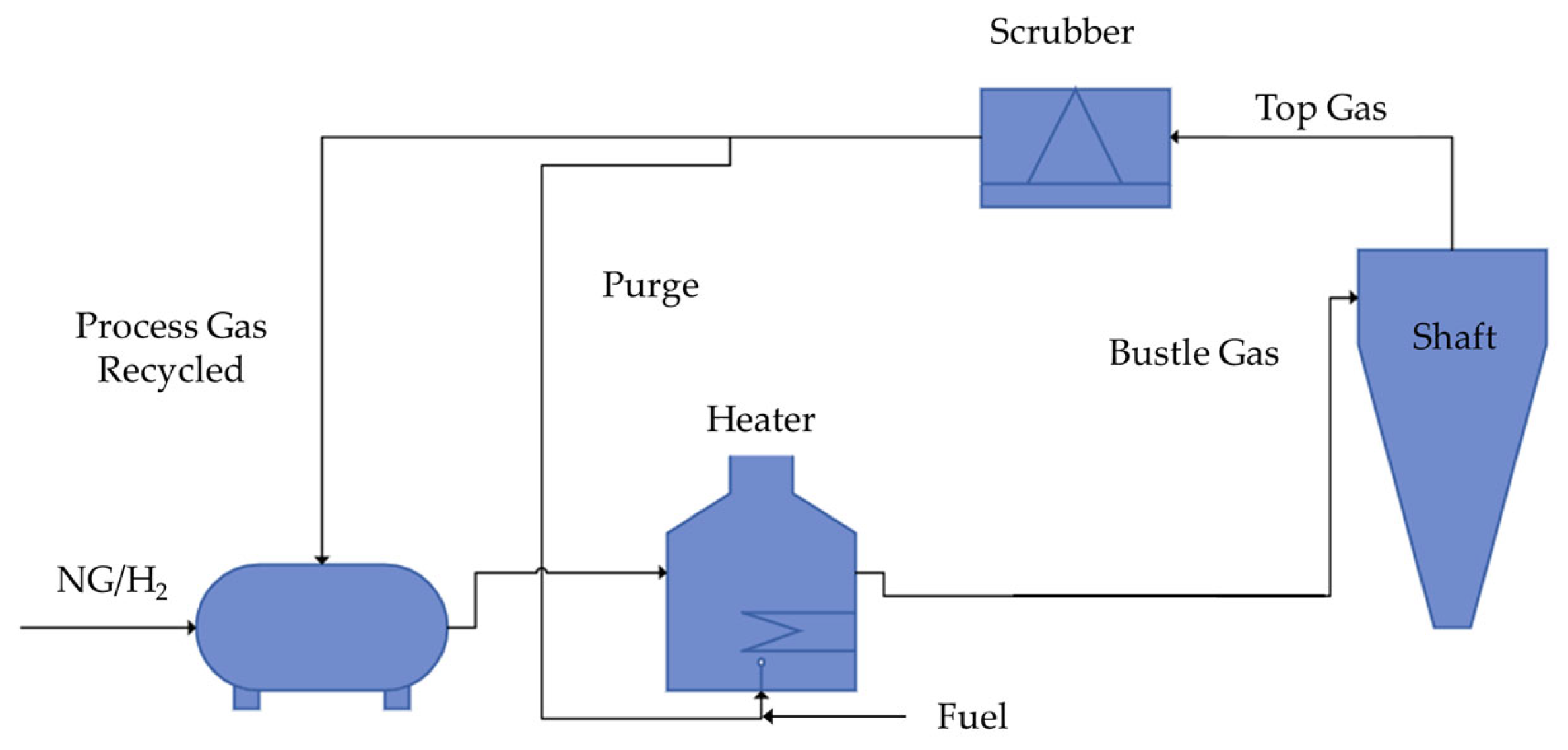

4.3. Use Case 2: DRI Production—CO2 Emissions and H2 Break-Even Price for H2-DRI

- Around 10 GJ of NG is needed per ton of DRI.

- Data coming from Table 4:

- The NG LHV is 38,979.32 MJ/Nm3.

- The NG density is 0.79 kg/Nm3.

- 75.94% is the NG carbon mass in %.

- In total, 1 mol of C is equal to 1 mol of CO2.

- The ratio of kmol of CO2 to kg of CO2 is 44.

- H2 harnesses and electricity are green.

- Around 10 GJ of NG is needed per each DRI ton. NG prices usually oscillate between 1 and 12 EUR/GJ [169].

- CO2 prices oscillate between 0 and 100 EUR/tCO2 [93], and per GJ of NG, 56 kg of CO2 is associated, considering 257 Nm3 NG/tDRI, 1 mol C = 1 mol CO2, and around 500 kg of CO2/tDRI.

- A total of 550 Nm3 H2/tDRI is fixed. Additionally, up to 250 Nm3 H2/tDRI or other heat sources, e.g., NG or electricity, are required as fuel for the reduction gas heater.

- H2 harnesses and electricity for heating is green; therefore, no CO2 emissions are associated.

- The theoretical energy required for H2 heating is set to 450 kWh/tDRI (considering that the electrical heating efficiency is 85%, 530 kWh/tDRI, using gas and with an efficiency of 60%, 750 kWh/tDRI is needed).

- The cost of electricity is set at 100 EUR/MWh.

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Abbreviations

| AFOLU | Agriculture, forestry, and land use |

| BAT | Best Available Technique |

| BF | Blast furnace |

| BFG | Blast furnace gas |

| BM | Biomass |

| BOF | Basic oxygen furnace |

| C | Carbon |

| CBAM | Carbon Border Adjustment Mechanism |

| CCS | Carbon capture and storage |

| CCU | Carbon capture and usage |

| CCUS | Carbon capture, utilization, and storage |

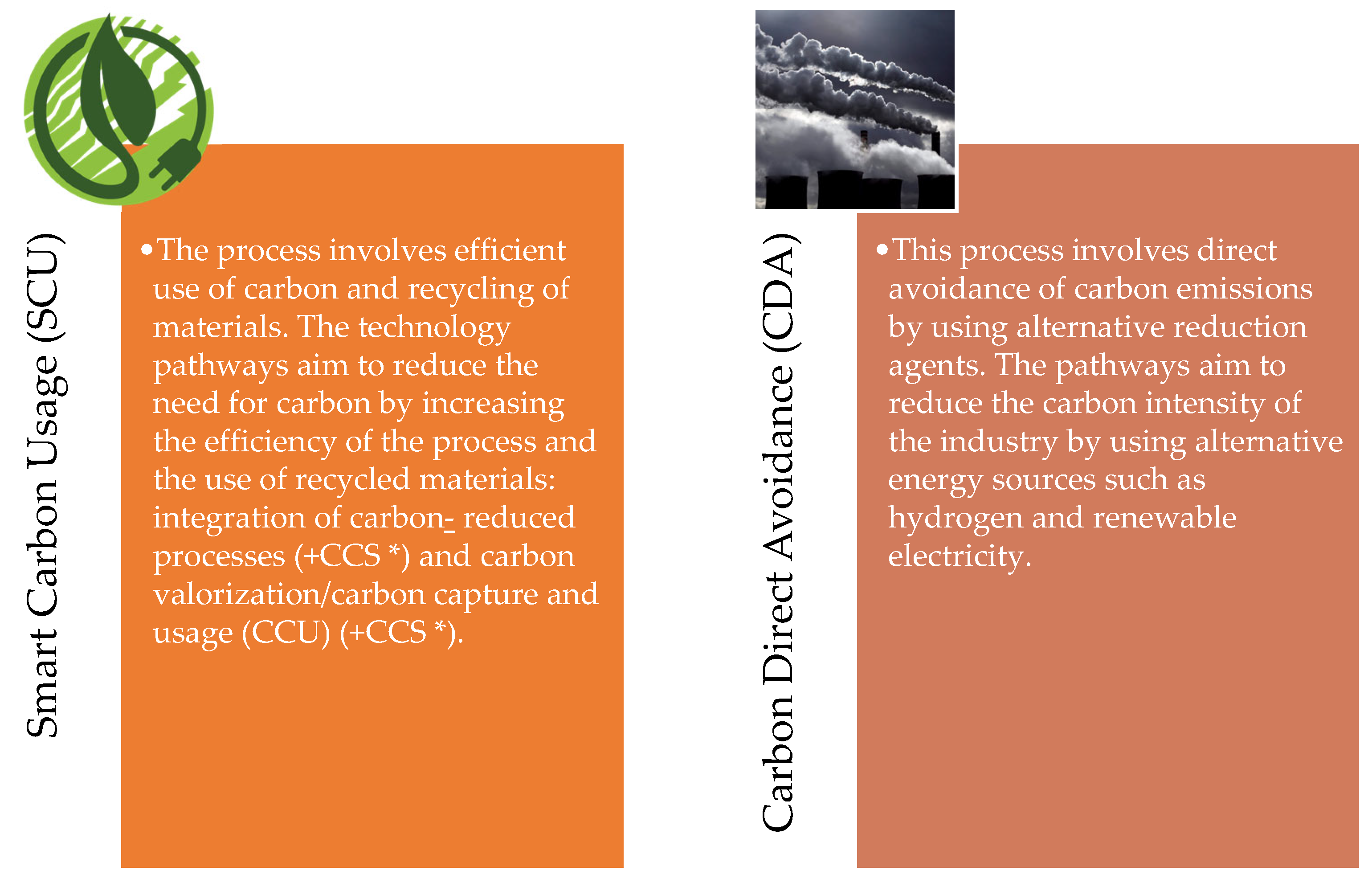

| CDA | Carbon direct avoidance |

| COG | Coke oven gas |

| DC | Direct current |

| DR | Direct reduction |

| DRI | Direct reduced iron |

| EAF | Electric arc furnace |

| ETS | Emissions Trading Scheme |

| EU | European Union |

| EU ETS | European Union Emissions Trading System |

| GHG | Greenhouse gases |

| H2 | Hydrogen |

| HBI | Hot Briquetted Iron |

| IEA | International Energy Agency |

| IPCC | Intergovernmental Panel on Climate Change |

| LCFFES | Low-carbon fuels, feedstocks, and energy sources |

| LHV | Lower heating value |

| LTS | US Long-Term Strategy |

| NG | Natural gas |

| PSH | Peak sun hours |

| PSO | Particle Swarm Optimization |

| PV | Solar generator |

| SCU | Smart carbon utilization |

| SMR | Steam methane reforming |

| SRF | Solid recovered fuel |

| TBD | To Be Defined |

| TRL | Technology Readiness Level |

| UK | United Kingdom |

| USA | United States of America |

| WF | Wind energy |

| WG | Waste gases |

References

- Beck, A.; Unterluggauer, J.; Helminger, F.; Solís-Gallego, I. Decarbonisation Pathways for the Finishing Line in a Steel Plant and Their Implications for Heat Recovery Measures. Energies 2023, 16, 852. [Google Scholar] [CrossRef]

- International Energy Agency. Iron and Steel Technology Roadmap—Towards a More Sustainable Steelmaking; IEA: Paris, France, 2020. [Google Scholar]

- Draxler, M.; Sormann, A.; Kempken, T.; Hauck, T.; Pierret, J.-C.; Borlee, J.; Di Donato, A.; De Santis, M.; Wang, C. Technology Assesment and Roadmapping (Deliverable 1.2); Green Steel for Europe Consortium: Brussels, Belgium, 2021. [Google Scholar]

- Mandova, H.; Patrizio, P.; Leduc, S.; Kjärstad, J.; Wang, C.; Wetterlund, E.; Kraxner, F.; Gale, W. Achieving Carbon-Neutral Iron and Steelmaking in Europe through the Deployment of Bioenergy with Carbon Capture and Storage. J. Clean. Prod. 2019, 218, 118–129. [Google Scholar] [CrossRef]

- Kim, Y.; Worrell, E. International Comparison of CO2 Emission Trends in the Iron and Steel Industry. Energy Policy 2002, 30, 827–838. [Google Scholar] [CrossRef]

- Worlsteel Association. 2022 World Steel in Figures; World Steel Association: Brussels, Belgium, 2022. [Google Scholar]

- European Commission; European Research Executive Agency; Vu, H.; Cecchin, F.; Iacob, N.; Stroia, C. Climate-Neutral Steelmaking in Europe: Decarbonisation Pathways, Investment Needs, Policy Conditions, Recommendations; Stroia, C., Iacob, N., Eds.; Publications Office of the European Union: Luxembourg, 2022.

- Somers, J. Technologies to Decarbonise the EU Steel Industry; Publications Office of the European Union: Luxemburg, 2022.

- U.S. Energy Information Administration. Annual Energy Outlook 2022 with Projections to 2050; U.S. Energy Information Administration: Washington, DC, USA, 2022.

- U.S. Department of Energy. Industrial Decarbonization Roadmap; U.S. Department of Energy: Washington, DC, USA, 2022.

- Intergovernmental Panel on Climate Change (IPCC). Climate Change 2007—Mitigation of Climate Change; Contribution of Working Group III to the Fourth Assessment Report of the Intergovernmental Panel on Climate Change; Cambridge University Press: New York, NY, USA, 2007. [Google Scholar]

- Direct CO2 Emissions from Industry in the Net Zero Scenario, 2000–2030—Charts—Data & Statistics. Available online: https://www.iea.org/data-and-statistics/charts/direct-co2-emissions-from-industry-in-the-net-zero-scenario-2000-2030 (accessed on 21 October 2023).

- Campbell-Davis, R.; Graham, A.; Witteveen, M.; Gamage, C.; Hutchinson, L. Net-Zero Steel. Sector Transition Strategy; Mission Possible Partnership: 2021. Available online: https://missionpossiblepartnership.org/wp-content/uploads/2021/10/MPP-Steel-Transition-Strategy-2021.pdf (accessed on 21 October 2023).

- Ritchie, H.; Rosado, P.; Roser, M. Emissions by Sector; Our World in Data: Oxford, UK, 2023. [Google Scholar]

- Sun, Y.; Tian, S.; Ciais, P.; Zeng, Z.; Meng, J.; Zhang, Z. Decarbonising the Iron and Steel Sector for a 2 °C Target Using Inherent Waste Streams. Nat. Commun. 2022, 13, 297. [Google Scholar] [CrossRef]

- The European Steel Association (EUROFER). Low Carbon Roadmap Pathways to a CO2-Neutral European Steel Industry; The European Steel Association: Brussels, Belgium, 2019. [Google Scholar]

- Bazo, M. Nuevas Rutas Comerciales y Aranceles al Acero: La UE le Planta Cara a China. Available online: https://logistica.cdecomunicacion.es/sector-logistico/134636/nuevo-corredor-aranceles-acero-ue-china (accessed on 21 October 2023).

- Aplauden la Imposición de Arancel de 25% al Acero Asiático. Available online: https://www.elfinanciero.com.mx/empresas/2023/08/17/aplauden-la-imposicion-de-arancel-de-25-al-acero-asiatico/ (accessed on 21 October 2023).

- European Union. EU Climate Target Plan 2030—Building a Modern, Sustainable and Resilient Europe; European Union: Brussels, Belgium, 2020. [Google Scholar]

- Koolen, D.; Vidovik, D. Greenhouse Gas Intensities of the EU Steel Industry and Its Trading Partners; Publications Office of the European Union: Luxembourg, 2022.

- ArcelorMittal. Climate Action Report 1; ArcelorMittal: Luxembourg, 2019. [Google Scholar]

- Making Net-Zero Steel Possible. An Industry-Backed, 1.5 °C—Aligned Transition Strategy; Mission Possible Partnership: 2022. Available online: https://missionpossiblepartnership.org/wp-content/uploads/2023/01/Making-Net-Zero-Aviation-possible.pdf (accessed on 21 October 2023).

- Hölling, M. Decarbonising the Energy Intensive Steel Industry by Usage of Hydrogen—Technological and Economical Aspects. In Proceedings of the Hydrogen & Fuel Cells Energy Summit 2019, Madrid, Spain, 6–7 February 2019. [Google Scholar]

- Hasanbeigi, A.; Springer, C. How Clean Is the U.S. Steel Industry? An International Benchmarking of Energy and CO2 Intensities; Global Efficiency Intelligence: São Francisco, CA, USA, 2019. [Google Scholar]

- Ministry of Steel. Government of India Annual Report 2020–2021. Available online: https://steel.gov.in/sites/default/files/Annual%20Report-Ministry%20of%20Steel%202020-21.pdf (accessed on 21 October 2023).

- Toktarova, A.; Karlsson, I.; Rootzén, J.; Göransson, L.; Odenberger, M.; Johnsson, F. Pathways for Low-Carbon Transition of the Steel Industry—A Swedish Case Study. Energies 2020, 13, 3840. [Google Scholar] [CrossRef]

- Vercoulen, P.; Lee, S.; Han, X.; Zhang, W.; Cho, Y.; Pang, J. Carbon-Neutral Steel Production and Its Impact on the Economies of China, Japan, and Korea: A Simulation with E3ME-FTT:Steel. Energies 2023, 16, 4498. [Google Scholar] [CrossRef]

- Kim, J.; Sovacool, B.K.; Bazilian, M.; Griffiths, S.; Lee, J.; Yang, M.; Lee, J. Decarbonizing the Iron and Steel Industry: A Systematic Review of Sociotechnical Systems, Technological Innovations, and Policy Options. Energy Res. Soc. Sci. 2022, 89, 102565. [Google Scholar] [CrossRef]

- Gajdzik, B.; Wolniak, R.; Grebski, W. Process of Transformation to Net Zero Steelmaking: Decarbonisation Scenarios Based on the Analysis of the Polish Steel Industry. Energies 2023, 16, 3384. [Google Scholar] [CrossRef]

- Harpprecht, C.; Naegler, T.; Steubing, B.; Tukker, A.; Simon, S. Decarbonization Scenarios for the Iron and Steel Industry in Context of a Sectoral Carbon Budget: Germany as a Case Study. J. Clean. Prod. 2022, 380, 134846. [Google Scholar] [CrossRef]

- Suer, J.; Traverso, M.; Jäger, N. Carbon Footprint Assessment of Hydrogen and Steel. Energies 2022, 15, 9468. [Google Scholar] [CrossRef]

- Digiesi, S.; Mummolo, G.; Vitti, M. Minimum Emissions Configuration of a Green Energy–Steel System: An Analytical Model. Energies 2022, 15, 3324. [Google Scholar] [CrossRef]

- Arens, M.; Worrell, E.; Eichhammer, W.; Hasanbeigi, A.; Zhang, Q. Pathways to a Low-Carbon Iron and Steel Industry in the Medium-Term—the Case of Germany. J. Clean. Prod. 2017, 163, 84–98. [Google Scholar] [CrossRef]

- Bataille, C.; Åhman, M.; Neuhoff, K.; Nilsson, L.J.; Fischedick, M.; Lechtenböhmer, S.; Solano-Rodriquez, B.; Denis-Ryan, A.; Stiebert, S.; Waisman, H.; et al. A Review of Technology and Policy Deep Decarbonization Pathway Options for Making Energy-Intensive Industry Production Consistent with the Paris Agreement. J. Clean. Prod. 2018, 187, 960–973. [Google Scholar] [CrossRef]

- Fischedick, M.; Marzinkowski, J.; Winzer, P.; Weigel, M. Techno-Economic Evaluation of Innovative Steel Production Technologies. J. Clean. Prod. 2014, 84, 563–580. [Google Scholar] [CrossRef]

- Energiewende, A.; Institute, W. Breakthrough Strategies for Climate-Neutral Industry in Europe: Policy and Technology; Smart Energy for Europe Platform (SEFEP) gGmbH: Berlin, Germany, 2021. [Google Scholar]

- Bloomberg NEF. Decarbonizing Steel: Technologies and Costs; Bloomberg NEF: New York, NY, USA, 2021. [Google Scholar]

- Mission Possible: Reaching Net-Zero Carbon Emissions from Harder-to-Abate Sectors. 2018. Available online: https://www.energy-transitions.org/publications/mission-possible/ (accessed on 11 June 2023).

- Fleiter, T.; Arens, M.; Herbst, A.; Rehfeldt, M. Industrial Innovation: Pathways to Deep Decarbonisation of Industry. Part 2: Scenario Analysis and Pathways to Deep Decarbonisation; ICF: Lexington, KY, USA, 2019. [Google Scholar]

- Agency, I.E.; Kueppers, M.; Hodgson, D.; Levi, P.; Vass, T.; Lechtenbohmer, T. IEA 2022, Iron and Steel; IEA: Paris, France, 2022. [Google Scholar]

- Material Economics. Industrial Transformation 2050 Industrial Transformation 2050. 2019. Available online: https://materialeconomics.com/material-economics-industrial-transformation-2050.pdf?cms_fileid=303ee49891120acc9ea3d13bbd498d13 (accessed on 11 June 2023).

- McKinsey. Decarbonization of Industrial Sectors: The Next Frontier; McKinsey: London, UK, 2018. [Google Scholar]

- European Commission. Updating the 2020 New Industrial Strategy: Building a Stronger Single Market for Europe’s Recovery; European Commission: Brussels, Belgium, 2021. [Google Scholar]

- ArcelorMittal. Climate Action Report 2; ArcelorMittal: Luxembourg, 2021. [Google Scholar]

- Tata Steel. Carbon Neutral Steelmaking Is a Major Challenge for the Steel Industry Worldwide; Tata Steel: London, UK, 2022. [Google Scholar]

- Tata Steel. Tata Steel Opts for Hydrogen Route at Its IJmuiden Steelworks; Tata Steel Group: London, UK, 2021. [Google Scholar]

- Tata Steel. Transformation of the Steel Industry Can Become a Successful Model for the Transition to Climate Neutrality. Available online: https://www.tatasteeleurope.com/corporate/news/tata-steel-opts-for-hydrogen-route-at-its-ijmuiden-steelworks (accessed on 11 June 2023).

- Thyssenkrupp. Transformation of the Steel Industry Can Become a Successful Model for the Transition to Climate Neutrality. Available online: https://www.thyssenkrupp.com/en/newsroom/press-releases/pressdetailpage/transformation-of-the-steel-industry-can-become-a-successful-model-for-the-transition-to-climate-neutrality-113235 (accessed on 11 June 2023).

- Register, U.S.A.F. Executive Order 14008 of January 27, 2021, Tackling the Climate Crisis at Home and Abroad; Executive Office of the President: Washington, DC, USA, 2021.

- United States Department of State and the United States Executive Office of the President. The Long-Term Strategy of the United States: Pathways to Net-Zero Greenhouse Gas Emissions by 2050; Executive Office of the President: Washington, DC, USA, 2021.

- Kempken, T.; Hauck, T.; Wang, C.; Santis, M.; Szulc, W.; Draxler, M.; Sormann, A.; Queipo, P.; Miranda, M.; Croon, D.; et al. Decarbonisation Pathways 2030 and 2050 (Deliverable D1.7); Green Steel for Europe Consortium: Brussels, Belgium, 2021. [Google Scholar]

- Green Steel Tracker. Available online: https://www.industrytransition.org/green-steel-tracker/ (accessed on 11 June 2023).

- Toktarova, A.; Göransson, L.; Johnsson, F. Design of Clean Steel Production with Hydrogen: Impact of Electricity System Composition. Energies 2021, 14, 8349. [Google Scholar] [CrossRef]

- United States Energy Information Administration. Manufacturing Energy Consumption Survey (MECS): 2018 MECS Survey Data; United States Energy Information Administration: Washington, DC, USA, 2021.

- Vicente, A. Ferrous Scrap—A Key Factor in Steel Decarbonization; Steel Times International: Guildford, UK, 2022. [Google Scholar]

- Improve the EAF Scrap Route for a Sustainable Value Chain in the EU Circular Economy Scenario. Roadmap. An Evolution Document for a Strategic Look to the Future of European EAF Steelmaking; ESTEP: Brussels, Belgium, 2021.

- CirculArity Enhancements by Low Quality Scrap Analysis and Refinement; Horizon Europe: Brussels, Belgium, 2022.

- de la Peña, B.; Iriondo, A.; Galletebeitia, A.; Gutierrez, A.; Rodriguez, J.; Lluvia, I.; Vicente, A. Toward the Decarbonization of the Steel Sector: Development of an Artificial Intelligence Model Based on Hyperspectral Imaging at Fully Automated Scrap Characterization for Material Upgrading Operations. Steel Res. Int. 2023. [Google Scholar] [CrossRef]

- ArcelorMittal. ALTXOR. Proceso Robotizado Optimizado Para Mejorar La Calidad de Chatarras de Acero; ArcelorMittal: Luxembourg, 2023. [Google Scholar]

- Nogueira, C.A.; Trancoso, M.A.; Pedrosa, F.; Crujeira, A.T.; Oliveira, P.C.; Gonçalves, A.M.; Margarido, F.; Santos, R.N.; Durão, F.; Guimarães, C. The Role of Automated Sorting in the Recovery of Aluminium Alloys Waste. In Wastes: Solutions, Treatments and Opportunities; CRC Press: Boca Raton, FL, USA, 2015. [Google Scholar] [CrossRef]

- Margarido, F.; Santos, R.N.; Durão, F.; Guimarães, C.; Nogueira, C.; Oliveira, P.; Pedrosa, F.; Gonçalves, A.M. Separation of Non-Ferrous Frations of Shredded End-of-Life Vehicles for Valorising Its Alloys. In Proceedings of the Proceedings of the International Conference on Mining, Material and Metallurgical Engineering, Prague, Czech Republic, 11–12 August 2014. [Google Scholar]

- Vicente Rojo, A. New Methods for Ferrous Raw Materials Characterization in Electric Steelmaking; Universidad del País Vasco: Bilbao, Spain, 2020. [Google Scholar]

- Vicente, A.; Picon, A.; Barco, E. New Method for Estimating the Economic Penalties of Ferrous Scraps in the Steelmaking Industry Due to Material Degradation during Its Storage in Scrap Yards. Ironmak. Steelmak. 2020, 47, 473–481. [Google Scholar] [CrossRef]

- Rodríguez, D.J.; Vicente, A.; Jaras, R.; Sorrosal, G.; Arteche, J.A.; Lago, R.A. Digital Solution for Optimazing Scrap Yard Management. 2023. Available online: https://imis.aist.org/store/detail.aspx?id=PR-387-082 (accessed on 11 June 2023).

- ArcelorMittal HYPER-DEEPSCRAP. Clasificador Avanzado de Residuos Procedente Del Tratamiento de Chatarra Férrica de Acería; ArcelorMittal: Luxembourg, 2021. [Google Scholar]

- Le Coq, X.; Russo, P. Birat Quality of Heavy Market Scrap—Development of New and Simple Methods for Quality Assessment and Quality Improvement: Final Report; European Commission, Directorate-General for Research and Innovation; European Commission: Brussels, Belgium, 2002. [Google Scholar]

- Trancoso, M.A.; Nogueira, C.; Calisto, S. Validation and Setting up Quality Control for Characterization of Aluminum Alloys in Non-Ferrous Fraction of Auto-Shredders. SN Appl. Sci. 2020, 2, 1762. [Google Scholar] [CrossRef]

- European Commission; Directorate-General for Research and Innovation; Grieco, R.; Zani, M.; Bengtson, A.; Brunk, M.; Noll, R.; Appell, A.; Gurell, J.; Chiarotti, U.; et al. Inline Elemental Characterisation of Scrap Charging for Improved EAF Charging Control and Internal Scrap Recycling (IPRO); Publications Office: Luxembourg, 2015. [Google Scholar]

- Nuñez, E.; Priyadarshi, H.; Picco, A.; Vicente, A. New Methodology for Estimating the Influence of Cu Content of Ferrous Scrap Materials in the Total Cost of Operation (TCO) of Scrap Mix in Electric Arc Furnace Steelmaking. In Proceedings of the EASES (European Academic Symposium on EAF Steelmaking), Oulu, Finland, 5 June 2023. [Google Scholar]

- Armellini, D.; Ometto, M.; Ponton, C. 2022 International Joint Conference on Neural Networks (IJCNN); IEEE: Piscataway, NJ, USA, 2022. [Google Scholar]

- Bavestrelli, G. AISTech 2023. In Proceedings of the Iron & Steel Technology Conference, Detroit, MI, USA, 8–11 May 2023. [Google Scholar]

- European Commission; Directorate-General for Research and Innovation; Pierre, R.; Ansseau, O.; Pierret, J.; Gutierrez, J.; Frittella, P.; Unamuno, I.; Milling, O. Optimization of Scrap Charge Management and Related Process Adaptation for Performances Improvement and Cost Reduction (OPTISCRAPMANAGE): Final Report; Publications Office: Luxembourg, 2021. [Google Scholar]

- AUTOMATIA—Soluciones de Inteligencia Artificial Para La Automatización y Control de Sistemas y Procesos Productivos (ZE-2020/00032) 2022. Available online: https://www.hinegroup.com/es/innovacion/proyectos-hazitek/ (accessed on 11 June 2023).

- Romagnoli, S.; Tarabu, C.; Maleki Vishkaei, B.; De Giovanni, P. The Impact of Digital Technologies and Sustainable Practices on Circular Supply Chain Management. Logistics 2023, 7, 1. [Google Scholar] [CrossRef]

- SCHROTT24 GMBH Scrap Dealing in the Digital Age: A Transparent and Efficient Platform for Price and Supply Chain Management. Available online: https://cordis.europa.eu/project/id/816314 (accessed on 25 June 2023).

- Miletic, I.; Garbaty, R.; Waterfall, S.; Mathewson, M. Model-based optimization of scrap steel purchasing. IFAC Proc. Vol. 2007, 40, 263–266. [Google Scholar] [CrossRef]

- Dock, J.; Wallner, S.; Traupmann, A.; Kienberger, T. Provision of Demand-Side Flexibility through the Integration of Power-to-Gas Technologies in an Electric Steel Mill. Energies 2022, 15, 5815. [Google Scholar] [CrossRef]

- Bampaou, M.; Panopoulos, K.; Seferlis, P.; Sasiain, A.; Haag, S.; Wolf-Zoellner, P.; Lehner, M.; Rog, L.; Rompalski, P.; Kolb, S.; et al. Economic Evaluation of Renewable Hydrogen Integration into Steelworks for the Production of Methanol and Methane. Energies 2022, 15, 4650. [Google Scholar] [CrossRef]

- International Energy Agency (IEA). The Future of Hydrogen; IEA: Paris, France, 2019. [Google Scholar]

- International Renewable Energy (IRENA). Green Hydrogen Cost Reduction: Scaling up Electrolysers to Meet the 1.5 °C Climate Goal; IRENA: Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- IEA. Global Hydrogen Review 2022; IEA: Paris, France, 2022. [Google Scholar]

- Turner, L.A.; Delasalle, F.; Kettleborough, I.; Wagner, A.; Hall, A.; Atreya, M.; Graham, A.; Mazzanti, T.; Meldrum, M.; Morrison, H.; et al. Making the Hydrogen Economy Possible: Accelerating Clean Hydrogen in an Electrified Economy; Mission Possible Partnership, Energy Transitions Commission: Leusden, The Netherlands, 2021. [Google Scholar]

- IEA—International Energy Agency. Available online: https://www.iea.org (accessed on 25 June 2023).

- Hölling, M.; Gellert, S. Direct Reduction: Transition from Natural Gas to Hydrogen? ASMET: Viena, Austria, 2018. [Google Scholar]

- Cheng, W.; Lee, S. How Green Are the National Hydrogen Strategies? Sustainability 2022, 14, 1930. [Google Scholar] [CrossRef]

- World Energy Council, in Collaboration with EPRI and PwC World Energy Council. National Hydrogen Strategies 2021; World Energy Council: London, UK, 2021. [Google Scholar]

- Pawelec, G.; Muron, M.; Bracht, J.; Boonet-Cantalloube, B.; Floristean, A.; Brahy, N. Hydrogen Europe. Clean Hydrogen Monitor 2020; Hydrogen Europe Intelligence Department: Brussels, Belgium, 2020. [Google Scholar]

- European Commission. A Hydrogen Strategy for a Climate-Neutral Europe; European Commission: Brussels, Belgium, 2020. [Google Scholar]

- Ministry for Ecological Transition and the Demographic Challenge (MITERD). Hoja de Ruta Del Hidrógeno: Una Apuesta Por El Hidrógeno Renovable; Ministry for Ecological Transition and Demographic Challenge (MITERD): Madrid, Spain, 2020.

- The European Hydrogen Backbone (EHB) Initiative|EHB European Hydrogen Backbone. Available online: https://www.ehb.eu/ (accessed on 11 June 2023).

- National Academies of Sciences, Engineering, and Medicine. Accelerating Decarbonization in the United States Energy Sector; National Academies of Sciences, Engineering, and Medicine: Washington, DC, USA, 2021. [Google Scholar]

- European Network of Transmission System Operators for Electriciy (ENTSO-E). Electricity in Europe 2017: Synthetic Overview of Electric System Consumption, Generation and Exchanges in 34 European Countries; ENTSO-E: Brussels, Belgium, 2017. [Google Scholar]

- Quarterly Report on European Electricity Markets 2022; European Commission: Brussels, Belgium, 2022.

- European Commission. European Green Deal: Delivering on Our Targets; European Commission: Brussels, Belgium, 2021. [Google Scholar]

- Kempken, T.; Hauck, T.; Santis, M.D.; Rodriguez, P.Q.; Miranda, M.; Gonzalez, D.; Simonelli, F.; Vu, H.; Szulc, W.; Croon, D.; et al. Collection of Possible Decarbonisation Barriers; Green Steel for Europe Consortium: Brussels, Belgium, 2021. [Google Scholar]

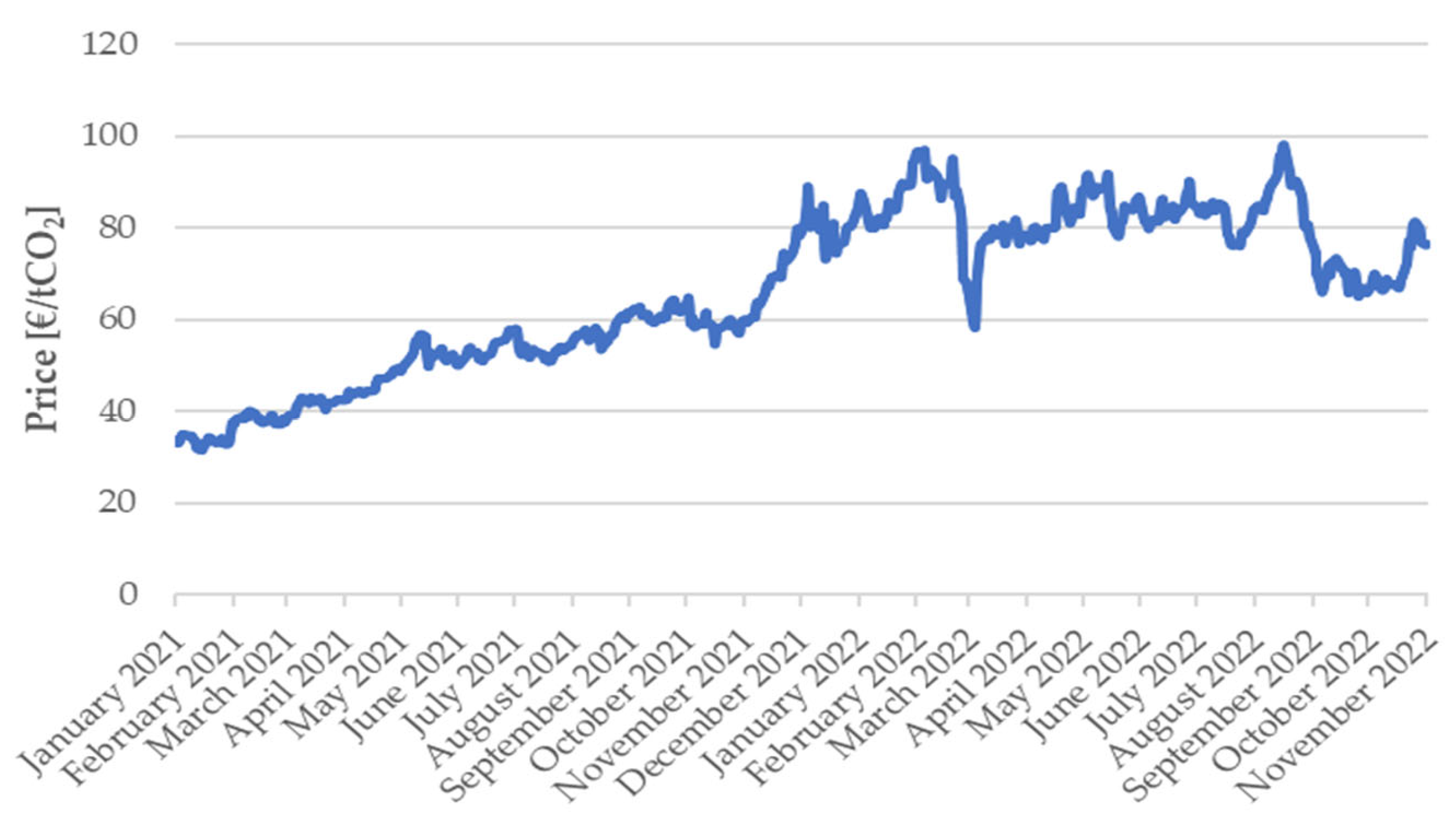

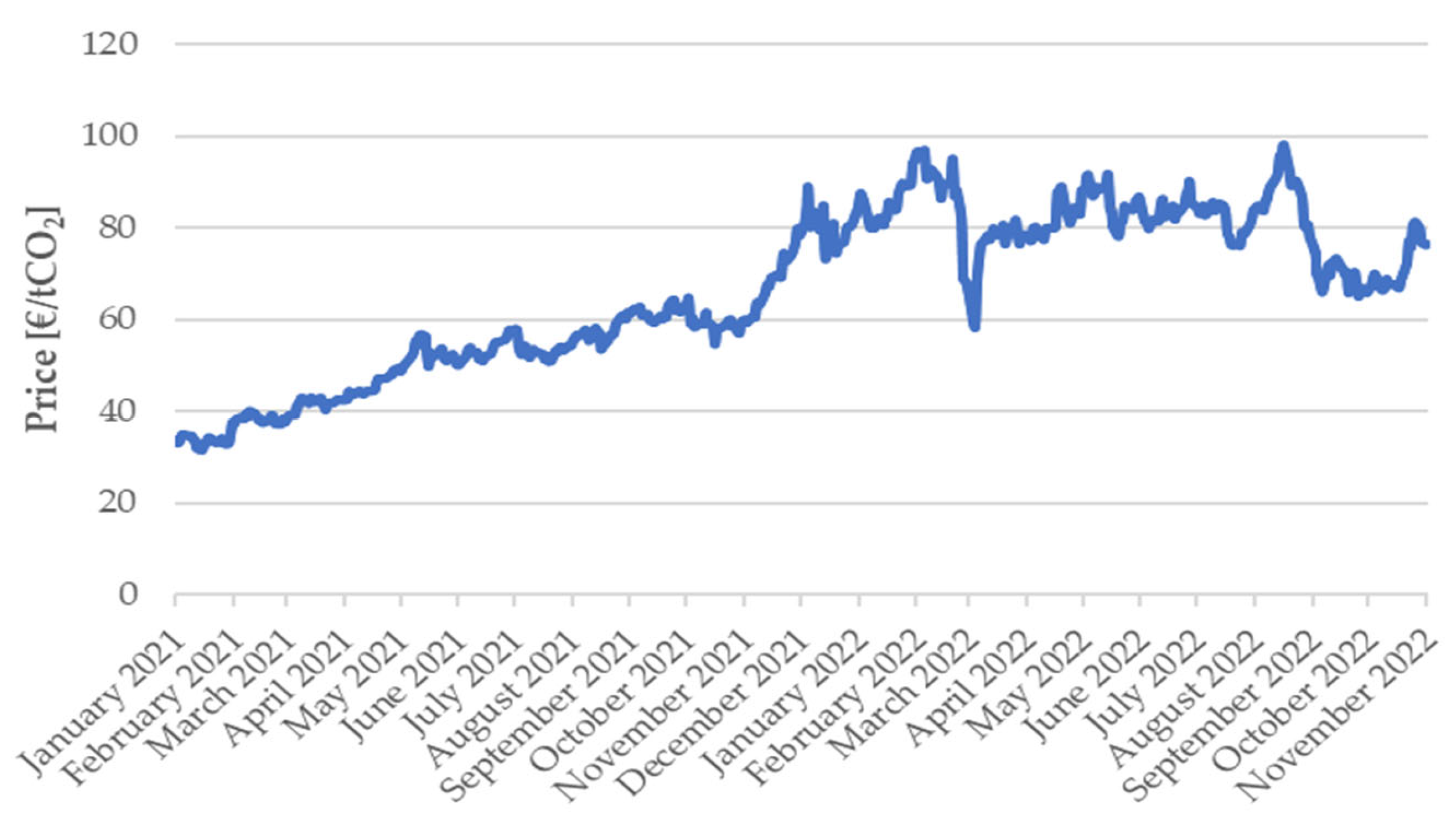

- EU Emissions Trading System (EU ETS) 2022; European Commission: Brussels, Belgium, 2022.

- Stede, J.; Pauliuk, S.; Hardadi, G.; Neuhoff, K. Carbon Pricing of Basic Materials: Incentives and Risks for the Value Chain and Consumers. Ecol. Econ. 2021, 189, 107168. [Google Scholar] [CrossRef]

- Establishing a Carbon Border Adjustment Mechanism 2021. Available online: https://eur-lex.europa.eu/legal-content/en/TXT/?uri=CELEX%3A52021PC0564 (accessed on 25 June 2023).

- Ember. EU Carbon Price Tracker; Ember: Galston, UK, 2022. [Google Scholar]

- World Steel Association. Climate Change and the Production of Iron and Steel; World Steel Association: Brussels, Belgium, 2021. [Google Scholar]

- European Commission 2050 Long-Term Strategy. Available online: https://climate.ec.europa.eu/eu-action/climate-strategies-targets/2050-long-term-strategy_en (accessed on 25 June 2023).

- Mallapaty, S. How China Could Be Carbon Neutral by Mid-Century. Nature 2020, 586, 482–483. [Google Scholar] [CrossRef] [PubMed]

- China Baowu Steel Group Corporation Limited. Corporate Social Responsibility Report; China Baowu Steel Group Corporation Limited: Shanghai, China, 2020. [Google Scholar]

- ArcelorMittal. ArcelorMittal Integrated Annual Review 2021; ArcelorMittal: Luxembourg, 2021. [Google Scholar]

- Nippon Steel. Nippon Steel Sustainability Report 2021; Nippon Steel Corporation: Tokyo, Japan, 2021. [Google Scholar]

- POSCO Corporate. Citizenship Report 2020; POSCO: Seoul, Republic of Korea, 2020. [Google Scholar]

- SALCOS Saltziger. Available online: https://salcos.salzgitter-ag.com/en/index.html?no_cache=1 (accessed on 25 June 2023).

- Tata Steel. Tata Steel in Europe Sustainability Report 2019/2020; Tata Steel Europe Limited: Ijmuiden, The Netherlands, 2020. [Google Scholar]

- Voestalpine Corporate. Responsability Report 2020; Voestalpine AG: Linz, Austria, 2020. [Google Scholar]

- García Higuera, A.; Van Woensel, L. Carbon-Free Steel Production: Cost Reduction Options and Usage of Existing Gas Infrastructure; European Parliamentary Research Service: Brussels, Belgium, 2021. [Google Scholar]

- Chan, Y.; Petithuguenin, L.; Fleiter, T.; Herbst, A.; Arens, M.; Stevenson, P. Industrial Innovation: Pathways to Deep Decarbonisation of Industry. Part 1: Technology Analysis; ICF Consulting Services Limited and Fraunhofer ISI: London, UK, 2019. [Google Scholar]

- U.S. Department of Energy Advanced Manufacturing Office. Manufacturing Energy and Carbon Footprint: All Manufacturing (2018 MECS); U.S. Department of Energy Advanced Manufacturing Office: Washington, DC, USA, 2021.

- Otto, A.; Robinius, M.; Grube, T.; Schiebahn, S.; Praktiknjo, A.; Stolten, D. Power-to-Steel: Reducing CO2 through the Integration of Renewable Energy and Hydrogen into the German Steel Industry. Energies 2017, 10, 451. [Google Scholar] [CrossRef]

- Orcajo, G.A.; Pedrayes, F.; Cano, J.M.; Norniella, J.G.; Rojas, C.H.; Rodríguez, J. Voltage Sag Ride-Through in a Joint Installation of a Hot Rolling Mill Plant and a Wind Farm. IEEE Trans. Ind. Appl. 2023, 59, 5190–5200. [Google Scholar] [CrossRef]

- Orcajo, G.A.; Diez, J.R.; Cano, J.M.; Norniella, J.G.; Pedrayes González, J.F.; Rojas, C.H. Coordinated Management of Electrical Energy in a Steelworks and a Wind Farm. IEEE Trans. Ind. Appl. 2022, 58, 5488–5502. [Google Scholar] [CrossRef]

- Rodríguez, D.J.; Alonso Orcajo, G.; Cano, J.M.; GNorniella, J.; Vicente, A. Thermal Analysis of Dry-Type Air-Core Coils for the Optimization of Passive Filtering Systems. Energies 2020, 13, 4540. [Google Scholar] [CrossRef]

- Alonso Orcajo, G.A.; Rodríguez Diez, J.; Cano, J.M.; Norniella, J.G.; Pedrayes González, J.F.; Rojas, C.H.; Ardura, G.P.; Cifrián, R.D. Enhancement of Power Quality in an Actual Hot Rolling Mill Plant Through a STATCOM. IEEE Trans. Ind. Appl. 2020, 56, 3238–3249. [Google Scholar] [CrossRef]

- Orcajo, G.A.; Rodríguez, J.; Cano, J.M.; Norniella, J.G.; Ardura, P.; Llera, R.; Cifrián, D. Retrofit of a Hot Rolling Mill Plant with Three-Level Active Front End Drives. IEEE Trans. Ind. Appl. 2018, 54, 2964–2974. [Google Scholar] [CrossRef]

- Orcajo, G.A.; Ardura, P.; Rodríguez, J.; Cano, J.M.; Norniella, J.G.; Llera, R.; Cifrián, D. Overcurrent Protection Response of a Hot Rolling Mill Filtering System: Analysis of the Process Conditions. IEEE Trans. Ind. Appl. 2017, 53, 2596–2607. [Google Scholar] [CrossRef]

- Dudin, M.N.; Reshetov, K.Y.; Mysachenko, V.I.; Mironova, N.N.; Divnenko, O.V. “Green Technology” and Renewable Energy in the System of the Steel Industry in Europe. IJEEP 2017, 7, 310–315. [Google Scholar]

- de Beer, J.; Worrell, E.; Blok, K. Future Technologies for Energy-Efficient Iron and Steel Making. Annu. Rev. Energy Environ. 1998, 23, 123–205. [Google Scholar] [CrossRef]

- Xu, Z.; Zheng, Z.; Gao, X. Energy-Efficient Steelmaking-Continuous Casting Scheduling Problem with Temperature Constraints and Its Solution Using a Multi-Objective Hybrid Genetic Algorithm with Local Search. Appl. Soft Comput. 2020, 95, 106554. [Google Scholar] [CrossRef]

- Lian, X.; Zheng, Z.; Wang, C.; Gao, X. An Energy-Efficient Hybrid Flow Shop Scheduling Problem in Steelmaking Plants. Comput. Ind. Eng. 2021, 162, 107683. [Google Scholar] [CrossRef]

- Energy Efficient Solutions for EAF Steelmaking|Journal of Achievements in Materials and Manufacturing Engineering. Available online: https://journalamme.org/resources/html/article/details?id=180436&language=en (accessed on 11 June 2023).

- Full Article: News of 50 Hertz. Available online: https://www.50hertz.com/en/News/FullarticleNewsof50Hertz/13545/using-renewables-to-ensure-grid-stability-50hertz-and-enertrag-launch-voltage-stability-pilot-project (accessed on 6 August 2023).

- Alvarez, M. Gobierno Vasco y Sidenor se Asocian para Comprar Ocho Parques Solares en Cataluña. Available online: https://www.elcorreo.com/Economia/gobierno-vasco-sidenor-asocian-comprar-ocho-parques-cataluna-20230728115254-nt.html (accessed on 6 August 2023).

- Storm Builds Belgium’s First Subsidy-Free Wind Farm at the ArcelorMittal Site in Ghent|Storm Be. Available online: https://www.storm.be/en/windfarm/haven-gent-phase-3b-0/news/storm-builds-belgiums-first-subsidy-free-wind-farm-arcelormittal-site-ghent (accessed on 6 August 2023).

- Fontenoy, E. Eneco and ArcelorMittal Unveil Belgium’s Largest Solar Roof. Available online: https://belgium.arcelormittal.com/en/eneco-and-arcelormittal-unveil-belgiums-largest-solar-roof/ (accessed on 6 August 2023).

- Wei, M.; McMillan, C.A.; de la Rue du Can, S. Electrification of Industry: Potential, Challenges and Outlook. Curr. Sustain. Renew. Energy Rep. 2019, 6, 140–148. [Google Scholar] [CrossRef]

- Hasanbeigi, A.; Kirshbaum, L.A. Industrial Electrification in U.S. States; Global Efficiency Intelligence: St. Petersburg, FL, USA.

- Lechtenböhmer, S.; Nilsson, L.J.; Åhman, M.; Schneider, C. Decarbonising the Energy Intensive Basic Materials Industry through Electrification—Implications for Future EU Electricity Demand. Energy 2016, 115, 1623–1631. [Google Scholar] [CrossRef]

- Barberouss, M.; Apostolou, M.; Debregeas, A.; Bono, C. Electrification of Primary Steel Production Based on ΣIDERWIN Process: Simulation the European Power System in 2050; European Council for an Energy Efficient Economy: Stockholm, Sweden, 2020. [Google Scholar]

- ArcelorMittal. ArcelorMittal and John Cockerill Announce Plans to Develop World’s First Industrial Scale Low Temperature, Iron Electrolysis Plant. Available online: https://corporate.arcelormittal.com/media/press-releases/arcelormittal-and-john-cockerill-announce-plans-to-develop-world-s-first-industrial-scale-low-temperature-iron-electrolysis-plant/ (accessed on 6 August 2023).

- Ren, L.; Zhou, S.; Peng, T.; Ou, X. A Review of CO2 Emissions Reduction Technologies and Low-Carbon Development in the Iron and Steel Industry Focusing on China. Renew. Sustain. Energy Rev. 2021, 143, 110846. [Google Scholar] [CrossRef]

- Fan, Z.; Friedmann, S.J. Low-Carbon Production of Iron and Steel: Technology Options, Economic Assessment, and Policy. Joule 2021, 5, 829–862. [Google Scholar] [CrossRef]

- Elsheikh, H.; Eveloy, V. Assessment of Variable Solar- and Grid Electricity-Driven Power-to-Hydrogen Integration with Direct Iron Ore Reduction for Low-Carbon Steel Making. Fuel 2022, 324, 124758. [Google Scholar] [CrossRef]

- Birat, J.-P. 16—Carbon Dioxide (CO2) Capture and Storage Technology in the Iron and Steel Industry. In Developments and Innovation in Carbon Dioxide (CO2) Capture and Storage Technology; Maroto-Valer, M.M., Ed.; Woodhead Publishing Series in Energy; Woodhead Publishing: Sawston, UK, 2010; Volume 1, pp. 492–521. ISBN 978-1-84569-533-0. [Google Scholar]

- Rosa, L.; Mazzotti, M. Potential for Hydrogen Production from Sustainable Biomass with Carbon Capture and Storage. Renew. Sustain. Energy Rev. 2022, 157, 112123. [Google Scholar] [CrossRef]

- Koukouzas, N.; Christopoulou, M.; Giannakopoulou, P.P.; Rogkala, A.; Gianni, E.; Karkalis, C.; Pyrgaki, K.; Krassakis, P.; Koutsovitis, P.; Panagiotaras, D.; et al. Current CO2 Capture and Storage Trends in Europe in a View of Social Knowledge and Acceptance. A Short Review. Energies 2022, 15, 5716. [Google Scholar] [CrossRef]

- Leeson, D.; Mac Dowell, N.; Shah, N.; Petit, C.; Fennell, P.S. A Techno-Economic Analysis and Systematic Review of Carbon Capture and Storage (CCS) Applied to the Iron and Steel, Cement, Oil Refining and Pulp and Paper Industries, as Well as Other High Purity Sources. Int. J. Greenh. Gas Control. 2017, 61, 71–84. [Google Scholar] [CrossRef]

- D’Amore, F.; Romano, M.C.; Bezzo, F. Carbon Capture and Storage from Energy and Industrial Emission Sources: A Europe-Wide Supply Chain Optimisation. J. Clean. Prod. 2021, 290, 125202. [Google Scholar] [CrossRef]

- Swennenhuis, F.; de Gooyert, V.; de Coninck, H. Towards a CO2-Neutral Steel Industry: Justice Aspects of CO2 Capture and Storage, Biomass- and Green Hydrogen-Based Emission Reductions. Energy Res. Soc. Sci. 2022, 88, 102598. [Google Scholar] [CrossRef]

- ArcelorMittal. ArcelorMittal Inaugurates Flagship Carbon Capture and Utilisation Project at Its Steel Plant in Ghent, Belgium. Available online: https://corporate.arcelormittal.com/media/press-releases/arcelormittal-inaugurates-flagship-carbon-capture-and-utilisation-project-at-its-steel-plant-in-ghent-belgium/ (accessed on 6 August 2023).

- ET EnergyWorld. Tata Steel Commissions India’s First Plant for CO2 Capture from Blast Furnace Gas. Available online: https://energy.economictimes.indiatimes.com/news/power/tata-steel-commissions-indias-first-plant-for-co2-capture-from-blast-furnace-gas/86219103 (accessed on 6 August 2023).

- Khalid, Y.; Wu, M.; Silaen, A.; Martinez, F.; Okosun, T.; Worl, B.; Low, J.; Zhou, C.; Johnson, K.; White, D. Oxygen Enrichment Combustion to Reduce Fossil Energy Consumption and Emissions in Hot Rolling Steel Production. J. Clean. Prod. 2021, 320, 128714. [Google Scholar] [CrossRef]

- Lu, B.; Chen, D.; Chen, G.; Yu, W. An Energy Apportionment Model for a Reheating Furnace in a Hot Rolling Mill—A Case Study. Appl. Therm. Eng. 2017, 112, 174–183. [Google Scholar] [CrossRef]

- Von Scheele, J. Decarbonisation and Use of Hydrogen in Reheat Furnaces. In Proceedings of the Aachener Ofenbau- und Thermprocess-Kolloquium, Aachen, Germany, 7–8 October 2021. [Google Scholar]

- Tenova. TSX SmartBurner Burning up to 100% Hydrogen. Available online: https://tenova.com/newsroom/latest-tenova/tsx-smartburner-burning-100-hydrogen (accessed on 22 October 2023).

- Reheating Furnaces for Steel. Available online: https://www.sms-group.com/es-es/plants/reheating-furnaces (accessed on 22 October 2023).

- Danieli. HYDRO MAB to Take a Step Ahead in Green Steel. Available online: https://www.danieli.com/en/news-media/news/danieli-hydro-mab-take-step-ahead-green-steel_37_596.htm (accessed on 22 October 2023).

- OVAKO. Ovako First in the World to Heat Steel Using Hydrogen. Available online: https://mb.cision.com/Main/1471/3098033/1236951.pdf (accessed on 22 October 2023).

- SMS. Green Power Supply with X-Pact® Eco Grid. Available online: https://www.sms-group.com/services/x-pact-eco-grid (accessed on 15 July 2023).

- Shuli, J.; Collini, V. The Revolutionary MIDA Hybrid Minimill for a competitive green steel production. La Metall. Ital. Int. J. Ital. Assoc. Metall. 2023, 75–80. Available online: https://www.aimnet.it/la_metallurgia_italiana/2023/gennaio/10.pdf (accessed on 22 October 2023).

- VESTAS. 4 MW Platform Brochure V136-4.5 MW. Available online: https://www.vestas.com/en/products/4-mw-platform/v136-4-5-mw (accessed on 15 July 2023).

- Intergovernmental Panel On Climate Change (IPCC). Climate Change 2022—Impacts, Adaptation and Vulnerability: Working Group II Contribution to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change, 1st ed.; Cambridge University Press: Cambridge, UK, 2023; ISBN 978-1-00932-584-4. [Google Scholar]

- MIDREX® Process. Available online: https://www.midrex.com/technology/midrex-process/ (accessed on 6 August 2023).

- Energy Transition in the European Steel Industry—Reality Not Exception. Available online: https://www.midrex.com/tech-article/energy-transition-in-the-european-steel-industry-reality-not-exception/ (accessed on 6 August 2023).

- Atsushi, M.; Uemura, H.; Sakaguchi, T. MIDREX Processes. Kobelco Technol. Rev. 2010, 29, 50–57. [Google Scholar]

- Metius, G.; Gaines, H.; Riley, M.F.; Iii, L.E.B.; Damstedt, B. DRI Production Using Coke Oven Gas (COG): Results of the MIDREX® Thermal Reactor SystemTM (TRS®) Testing and Future Commercial Application; AIST: Warrendale, PA, USA, 2015. [Google Scholar]

- Rechberger, K.; Conde, A.S.; Spanlang, A.; Kofler, I.; Rechberger, K. Green Hydrogen for Low-Carbon Steelmaking; Primetals Technologies: London, UK, 2021. [Google Scholar]

- voestalpine Steel Division. Comparison of Process Technology: MIDREX vs. ENERGIRON; Voestalpine Steel Division: Linz, Austria, 2013. [Google Scholar]

- Midrex Technologies, Inc. 2021 World Direct Reduction Statistics; Midrex Technologies, Inc.: Charlotte, NC, USA, 2021. [Google Scholar]

- Cavaliere, P. Direct Reduced Iron: Most Efficient Technologies for Greenhouse Emissions Abatement. In Clean Ironmaking and Steelmaking Processes: Efficient Technologies for Greenhouse Emissions Abatement; Cavaliere, P., Ed.; Springer International Publishing: Cham, Switzerland, 2019; pp. 419–484. ISBN 978-3-03021-209-4. [Google Scholar]

- Duarte, P. Hydrogen-Based Steelmaking; Millennium Steel: Botany, Australia, 2019. [Google Scholar]

- ISO 6976:2016; Calculation of Calorific Values, Density, Relative Density and Wobbe Indices from Composition. ISO: Geneva, Switzerland, 2016. Available online: https://www.iso.org/standard/55842.html (accessed on 12 August 2023).

- Kidnay, A.J.; Parrish, W.R.; McCartney, D.G. Fundamentals of Natural Gas Processing; CRC Press: Boca Raton, FL, USA, 2006; ISBN 978-0-42913-564-4. [Google Scholar]

- Información Básica de Los Sectores de La Energía En España; Comisión Nacional de Energía (CNE): Madrid, Spain, 1999.

- MIDREX NGTM with H2 Addition: Moving from Natural Gas to Hydrogen in Decarbonizing Ironmaking. Available online: https://www.midrex.com/tech-article/moving-from-natural-gas-to-hydrogen-in-decarbonizing-ironmaking/ (accessed on 5 August 2023).

- EU Natural Gas. 2023 Data—2010–2022 Historical—2024 Forecast—Price—Quote. Available online: https://tradingeconomics.com/commodity/eu-natural-gas (accessed on 6 August 2023).

- Thomas, G. Overview of Storage Development DOE Hydrogen Program; Natural Gas: Livermore, CA, USA, 2000. [Google Scholar]

- ArcelorMittal en España. HyDeal España: Hub de Hidrógeno. Available online: https://spain.arcelormittal.com/comunicados/hydeal-espana-hub-hidrogeno/ (accessed on 18 September 2023).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Development | Description | Literature |

|---|---|---|

| Scrap Recycling Technologies | Advancements in the scrap recycling technologies, such as shredding, sorting, and separation techniques, have improved the efficiency and effectiveness of scrap processing. These technologies help maximize the recovery of valuable materials from scrap, reducing the reliance on virgin resources. | [57,58,59,60,61,62] |

| Scrap Sorting and Classification | Innovations in scrap sorting and classification systems enable more precise identification and segregation of different types of scrap. This allows for better material utilization and enhances the quality of the recycled steel. Automated sorting technologies, including sensors and artificial intelligence, are being employed to optimize the scrap sorting process. | [57,58,62,63,64,65] |

| Scrap Quality Assessment | Quality assessment techniques for scrap, such as spectroscopic analysis, enable the determination of the chemical composition and the impurity levels. Accurate assessment of the scrap quality helps optimize steelmaking processes, maintain product quality, and reduce rejections and waste. | [58,62,63,66,67,68,69] |

| Scrap Management and Traceability Systems | Digital solutions and software platforms are being developed to facilitate scrap management and traceability. These systems enable better tracking of scrap from the collection to processing, ensuring transparency, compliance with regulations, and verification of sustainability claims. They also enhance supply chain efficiency and ease the selection of the most suitable scrap that meets specific steelmaking requirements. | [64,70,71,72,73] |

| Scrap Supply Chain Optimization | Optimization tools and algorithms are being employed to optimize the entire scrap supply chain, including collection, transportation, and processing. These tools help minimize logistical costs, reduce carbon emissions, and improve overall operational efficiency. They consider factors such as scrap availability, transportation routes, and processing capabilities to streamline the supply chain and maximize the resource utilization. | [64,69,73,74,75,76] |

| Energy Source | Steel Technology | Horizon | Challenges | Incremental Cost |

|---|---|---|---|---|

| Renewable Energy | Iron electrolysis | Long-term 2050 | High energy requirements and cost. Transition to electrolysis. | High |

| Green hydrogen | DRI with green hydrogen | Medium-term 2040 | Scalability of production and cost. Integration of DRI with green hydrogen. | Moderate |

| Smart Carbon | Utilizing circular carbon and hydrogen (green or blue), carbon-based products manufactured from waste gases | Medium-term 2040 | Scaling up and commercial viability. Transition to Smart Carbon. | High |

| Blue Hydrogen | DRI with blue hydrogen (from reformed NG) | Near-term | Carbon capture and storage infrastructure and cost. Integration of DRI with blue hydrogen. | Moderate |

| DRI and Carbon Capture | DRI current technology with CCS | Near-term 2030 | CCS infrastructure, integration, and cost. | High |

| Blast Furnace and Carbon Capture | BF current technology and incorporate CCS | Near-term 2030 | High |

| Pillar | Description | Literature |

|---|---|---|

| Energy efficiency | Improve system efficiency, process performance, and thermal energy recovery. Expand energy management practices. Increase application of smart manufacturing strategies to reduce energy consumption. Transition from high-carbon process heat technologies to low-carbon energy sources. | [113,114,115,116,117,118,119,120,121,122,123,124,125,126,127,128] |

| Industrial electrification | Electrify thermal processes to reduce emissions from fossil fuel combustion. | [113,129,130,131,132,133] |

| LCFFES | Adopt clean energy technologies that do not release GHGs. Develop low-carbon or carbon-free energy sources, including clean hydrogen and synthetic fuels. | [32,53,77,113,114,115,134,135,136] |

| CCU | Implement CCUS as a primary source of long-term emission reductions. Utilize carbon utilization and storage to achieve additional carbon reductions. | [4,137,138,139,140,141,142,143,144] |

| GJ/tDRI | Nm3 NG/tDRI | kg NG/tDRI | kg C/tDRI | Scenario | kg C in DRI | Total C out | kg CO2/tDRI |

|---|---|---|---|---|---|---|---|

| 10 | 257 | 203 | 154.1 | 1 | −15 | 139.1 | 510 |

| 2 | −35 | 119.1 | 437 | ||||

| 3 | 0 | 154.1 | 565 | ||||

| 50 | 40 | 30 | 4 | −15 | 15 | 55 |

| Energy | 100% NG | H2 with NG as Fuel (1.5% C in DRI) | 100% H2 with Only H2 as Fuel | 100% H2 with Only Electrical Heating |

|---|---|---|---|---|

| NG process (GJ/tDRI) | 7.5–7.9 | - | - | |

| NG fuel (GJ/tDRI) 1 | 2.1–2.9 | 2–2.5 | - | |

| H2 process (GJ/tDRI) | - | 6.1–7 | 5.9 | 5.9 |

| H2 fuel (GJ/tDRI) 1 | - | - | 2.7 | - |

| Electricity (kWh/tDRI) 2 | 90–135 | 80–125 | 80–125 | 530–620 |

| tCO2/GJ NG | 0.0565 | 0.0565 | - | |

| The gas flow required (Nm3/tDRI) | 255–300 | 60 (NG)/600 (H2) | 800 | 550 |

| Energy | 100% NG | H2 with NG as Fuel (1.5% C in DRI) | Comparison |

|---|---|---|---|

| NG process (GJ/tDRI) | 7.7 | - | - |

| NG fuel (GJ/tDRI) | 2.5 | 2.1 | 0.4 |

| H2 process (GJ/tDRI) | - | 6.5 | - |

| H2 fuel (GJ/tDRI) | - | - | - |

| Total NG (GJ/tDRI) | 10.2 | 2.1 | 8.1 |

| Total H2 (kg/tDRI) 1 | - | 54.2 | - |

| Electricity (kWh/tDRI) | 120 | 90 | 30 |

| NG Price (EUR/GJ) | CO2 Price (EUR/tCO2) | |||||

|---|---|---|---|---|---|---|

| 0 | 20 | 40 | 60 | 80 | 100 | |

| 1 | 0.20 | 0.37 | 0.54 | 0.71 | 0.87 | 1.04 |

| 2 | 0.35 | 0.52 | 0.69 | 0.86 | 1.02 | 1.19 |

| 3 | 0.50 | 0.67 | 0.84 | 1.01 | 1.17 | 1.34 |

| 4 | 0.65 | 0.82 | 0.99 | 1.16 | 1.32 | 1.49 |

| 5 | 0.80 | 0.97 | 1.14 | 1.30 | 1.47 | 1.64 |

| 6 | 0.95 | 1.12 | 1.29 | 1.45 | 1.62 | 1.79 |

| 7 | 1.10 | 1.27 | 1.44 | 1.60 | 1.77 | 1.94 |

| 8 | 1.25 | 1.42 | 1.59 | 1.75 | 1.92 | 2.09 |

| 9 | 1.40 | 1.57 | 1.74 | 1.90 | 2.07 | 2.24 |

| 10 | 1.55 | 1.72 | 1.88 | 2.05 | 2.22 | 2.39 |

| 11 | 1.70 | 1.87 | 2.03 | 2.20 | 2.37 | 2.54 |

| 12 | 1.85 | 2.02 | 2.18 | 2.35 | 2.52 | 2.69 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rodríguez Diez, J.; Tomé-Torquemada, S.; Vicente, A.; Reyes, J.; Orcajo, G.A. Decarbonization Pathways, Strategies, and Use Cases to Achieve Net-Zero CO2 Emissions in the Steelmaking Industry. Energies 2023, 16, 7360. https://doi.org/10.3390/en16217360

Rodríguez Diez J, Tomé-Torquemada S, Vicente A, Reyes J, Orcajo GA. Decarbonization Pathways, Strategies, and Use Cases to Achieve Net-Zero CO2 Emissions in the Steelmaking Industry. Energies. 2023; 16(21):7360. https://doi.org/10.3390/en16217360

Chicago/Turabian StyleRodríguez Diez, Josué, Silvia Tomé-Torquemada, Asier Vicente, Jon Reyes, and G. Alonso Orcajo. 2023. "Decarbonization Pathways, Strategies, and Use Cases to Achieve Net-Zero CO2 Emissions in the Steelmaking Industry" Energies 16, no. 21: 7360. https://doi.org/10.3390/en16217360

APA StyleRodríguez Diez, J., Tomé-Torquemada, S., Vicente, A., Reyes, J., & Orcajo, G. A. (2023). Decarbonization Pathways, Strategies, and Use Cases to Achieve Net-Zero CO2 Emissions in the Steelmaking Industry. Energies, 16(21), 7360. https://doi.org/10.3390/en16217360