The Thermoeconomic Environment Cost Indicator (iex-TEE) as a One-Dimensional Measure of Resource Sustainability

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

An Outlook to Some Sustainability Indices in the Literature

- It must be expressed by a—possibly simple—numeric expression and produce results that can be unambiguously ranked within two opposite limits.

- It must be calculated based on intrinsic properties of both the process (the system that it refers to) and of the (local or global) environment.

- It must be normalized in some sense, so that it may be used to compare different systems, different environmental conditions, different scenarios and/or different time series for the same community.

- It must be calculated based on an unambiguous, reproducible method under a well-defined set of fundamental assumptions.

- It must comply with the accepted laws of physics.

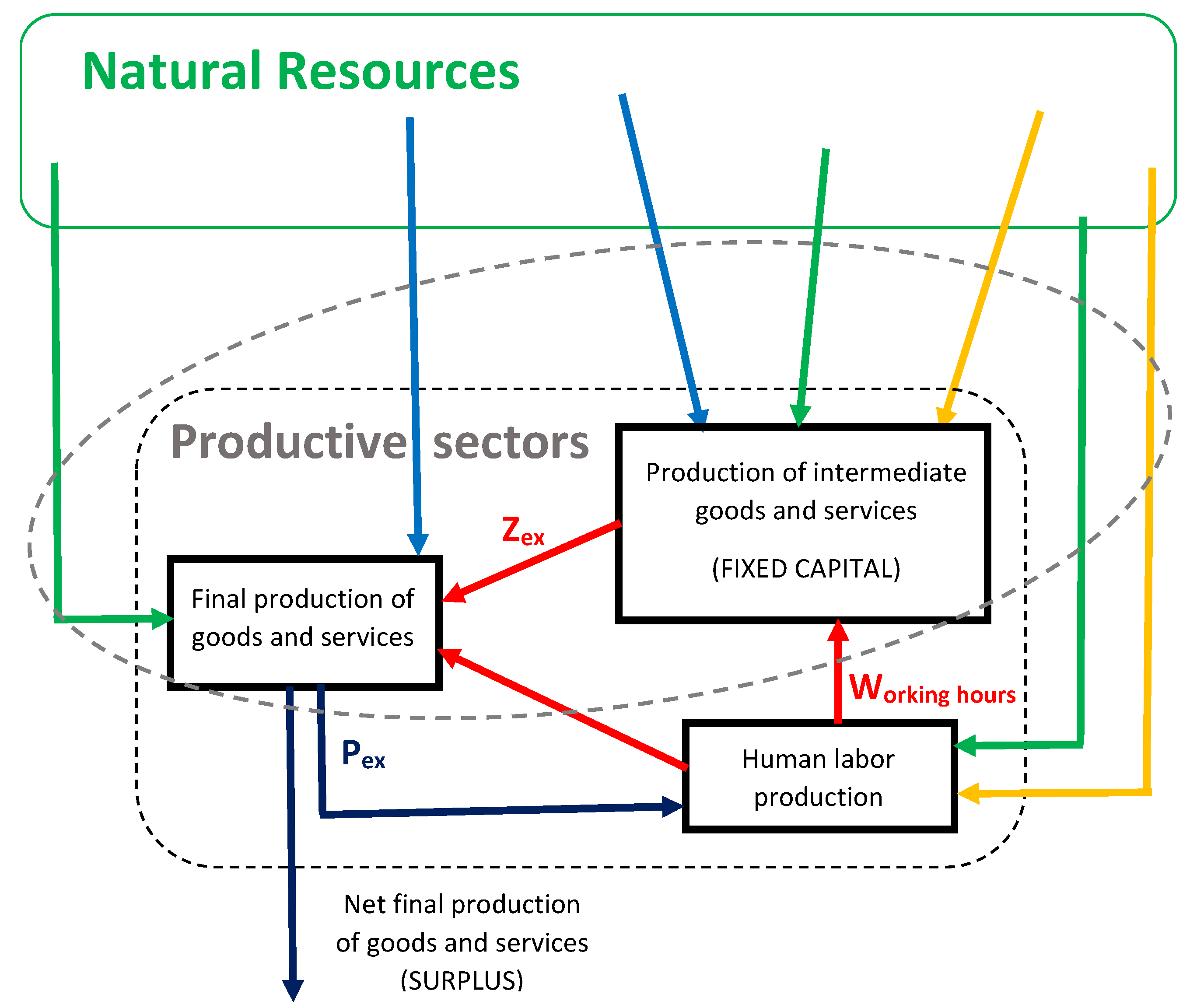

2. Exergy Cost Accounting for Assessing Sustainability

- clear limits for the control volume, where the start of the exergy supply chains of the system is located, and where the unit exergy costs of all inputs crossing the limits must be known [35].

- The actual primary exergy resources must be identified, considering both renewable and non-renewable resources.

- The impact affecting the resources available at the present moment, not that in a distant past time, must be assessed.

- All exergy costs related to polluting emissions must be evaluated, besides the exergy costs of the inputs.

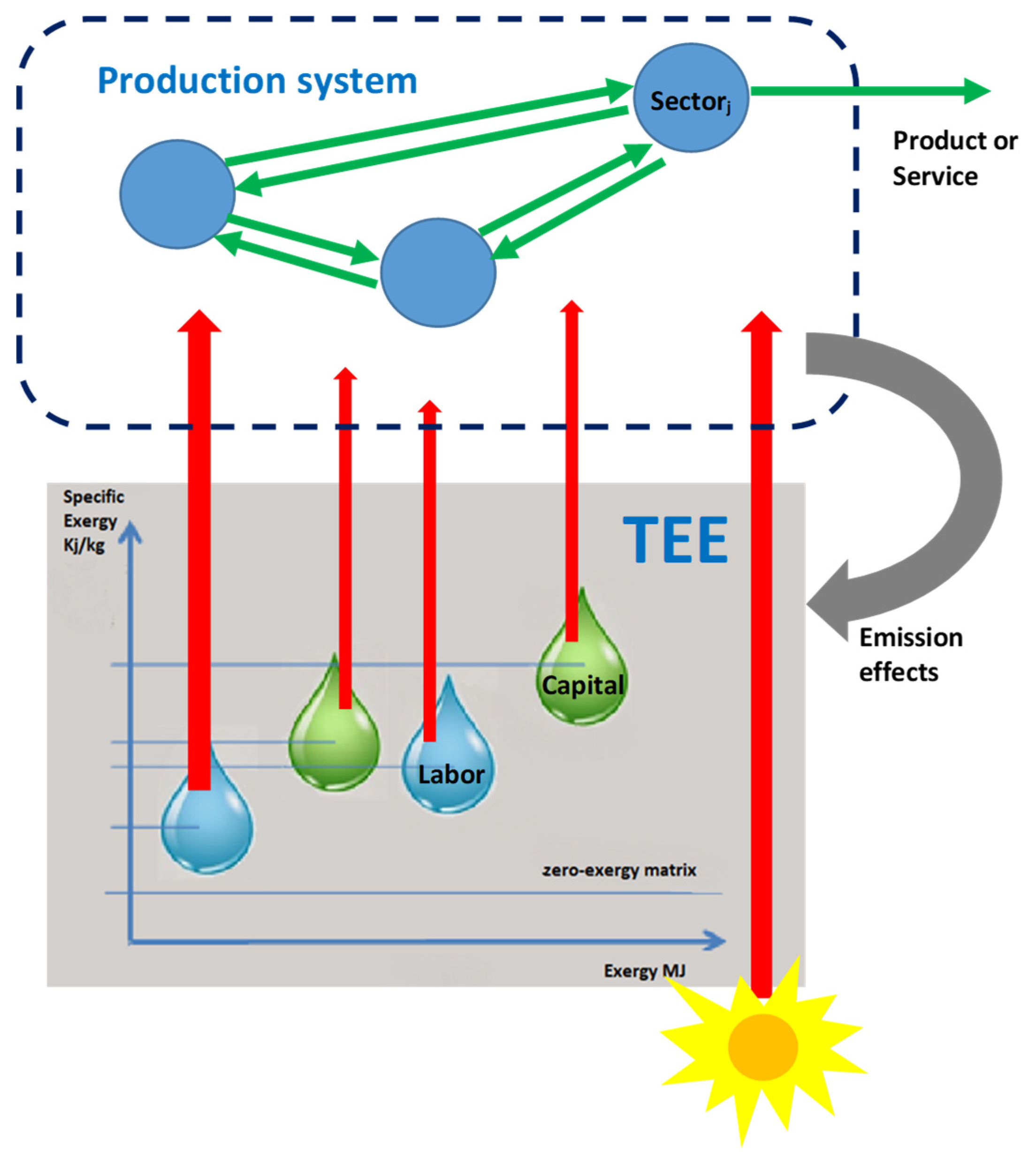

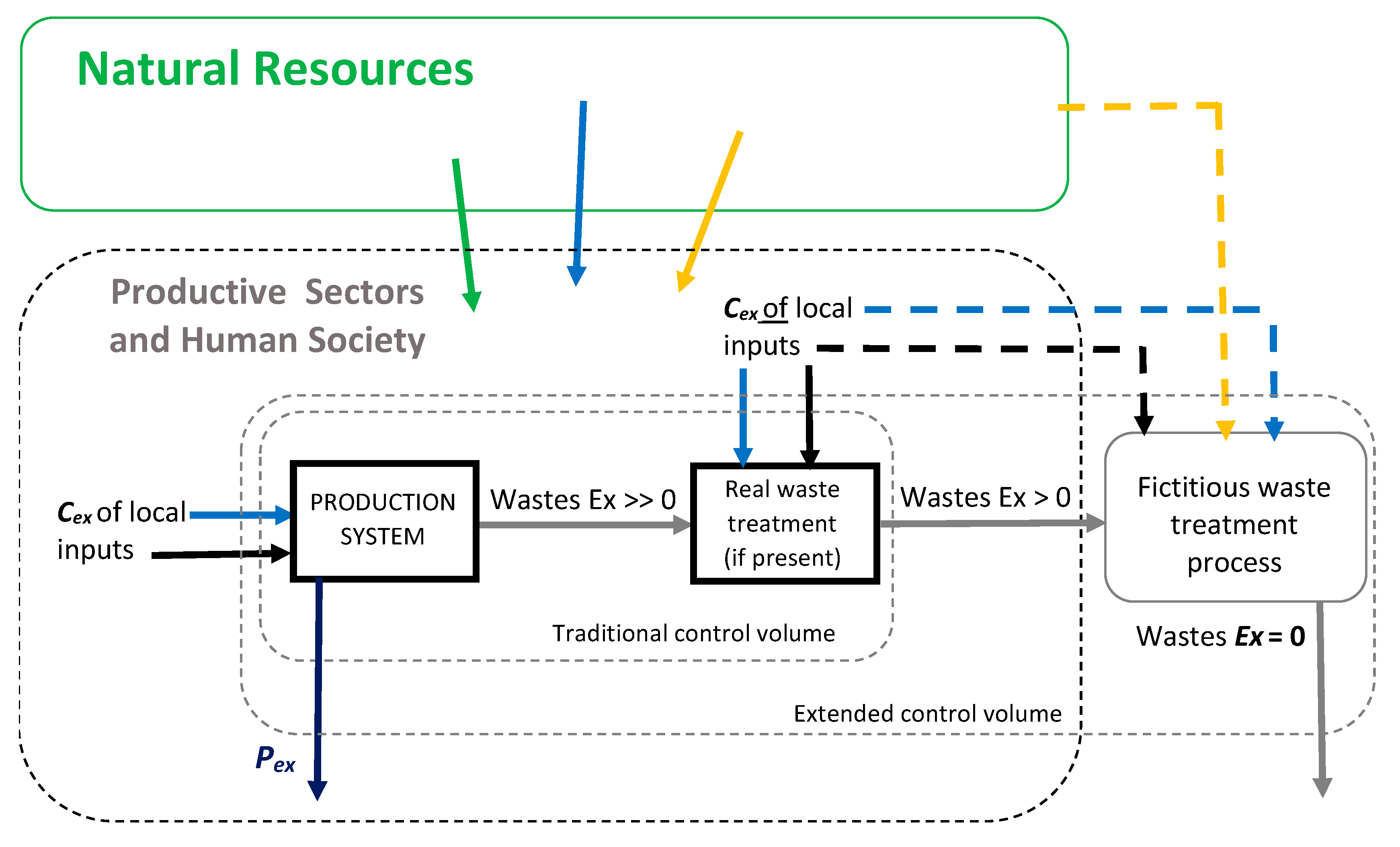

2.1. Definition of the Thermoeconomic Environment (TEE)

- Overcoming the drawbacks of the reference environment used in basic exergy analysis. Some of these drawbacks are that the reference environment has no resources of energy or raw materials that are required to be consumed to obtain a specific process or product. The reference temperature cannot be modified, which means that some phenomena, like global warming [41], cannot be accounted-for. In addition, the reference environment is not affected by any polluting emissions from the production system.

- Defining a framework consistent with the formulations of CExC [42] and EEA.

- CExC and EEA are milestones of the effort of including in the exergy accounting analysis a progressively more complete picture of the indirect effects and externalities of the production process. Some of the ideas developed in those approaches will be used in the following to define the proposed sustainability indicator.

- Suggesting new options for a consistent exergy cost definition of all resources. As will be evident in the following, the framework of the TEE may help the definition of a proper exergy cost for the effect of polluting emissions from the production process, or for the indirect destruction of resources, including living biomass.

2.2. Chemical Exergy Calculation

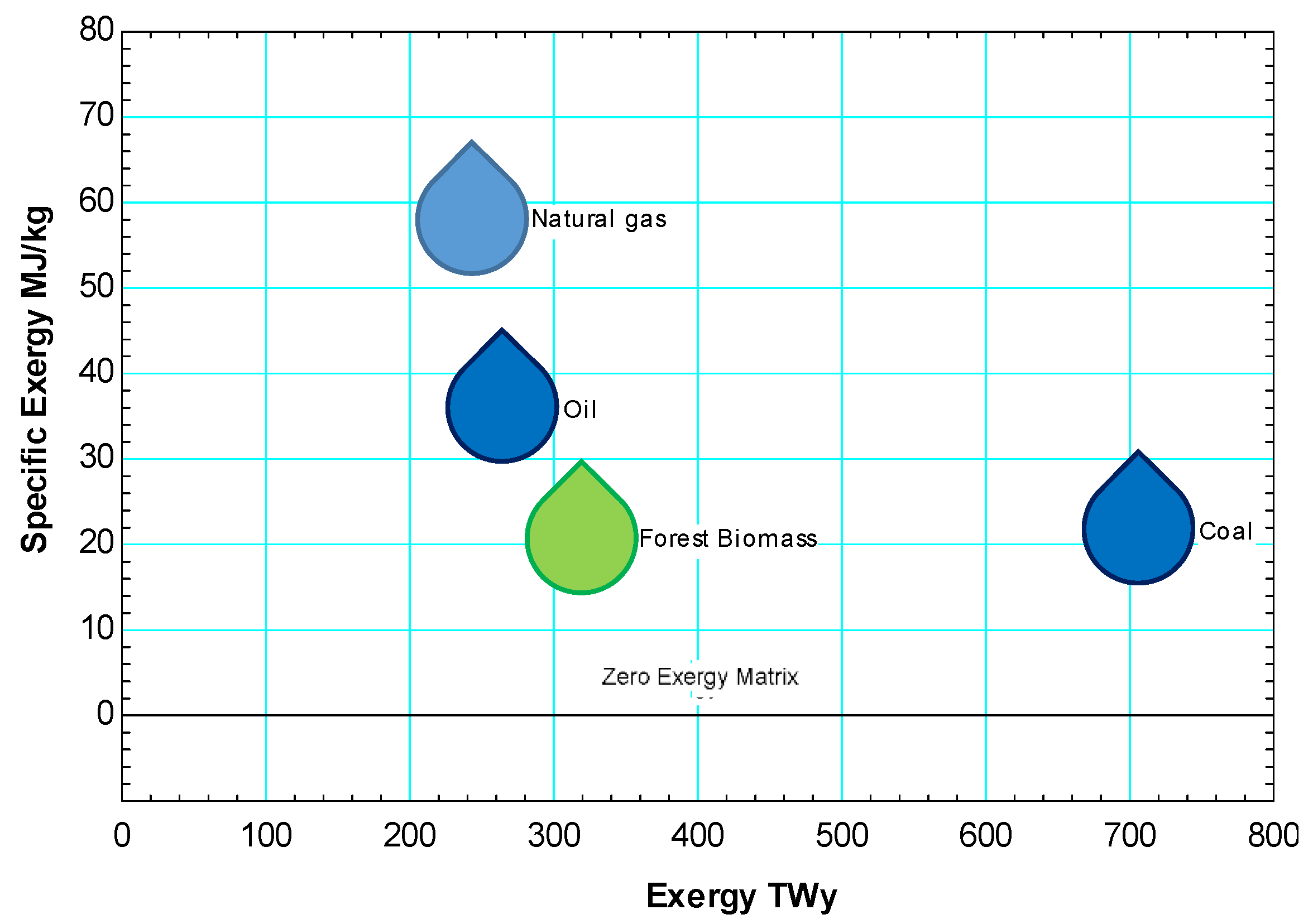

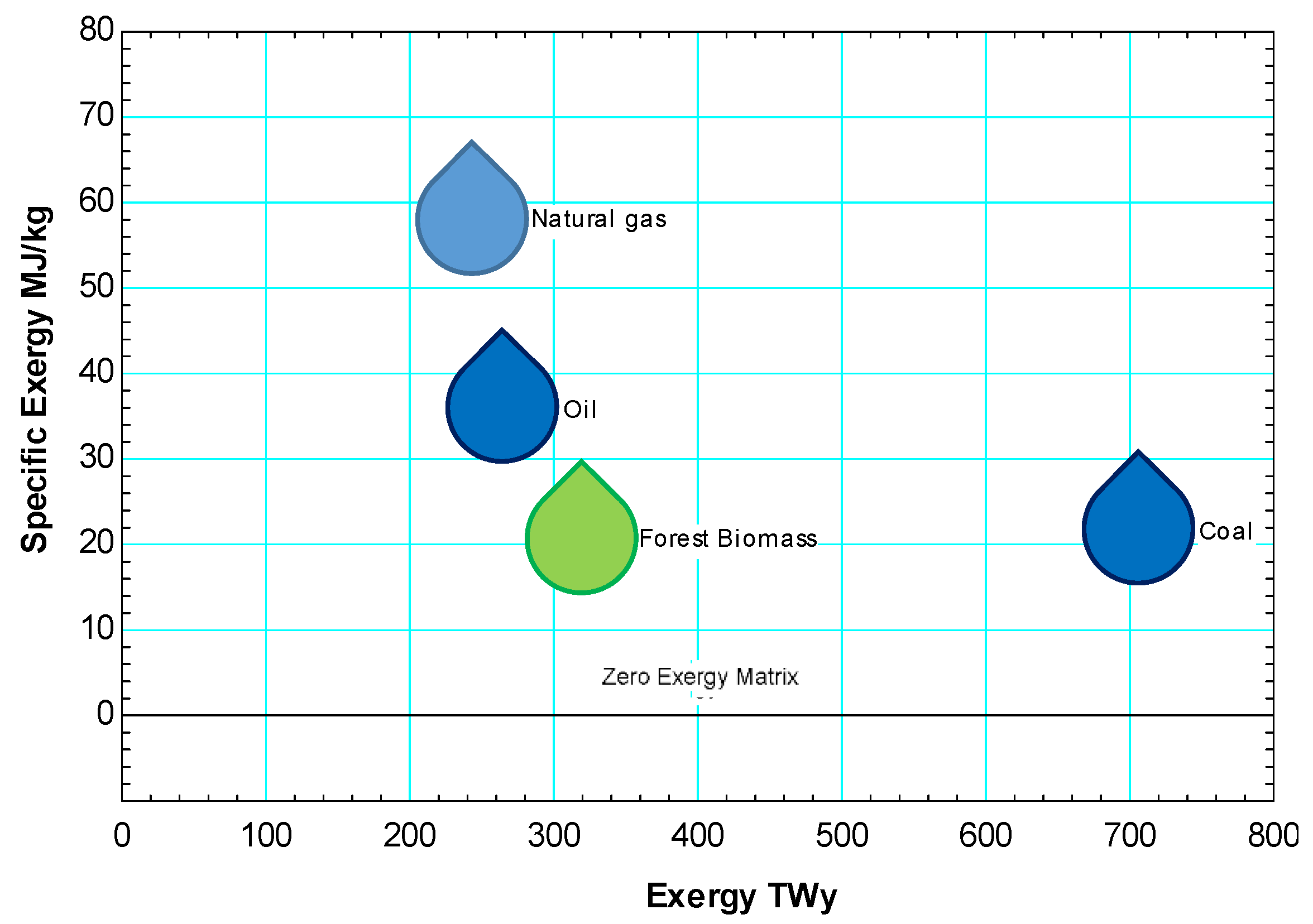

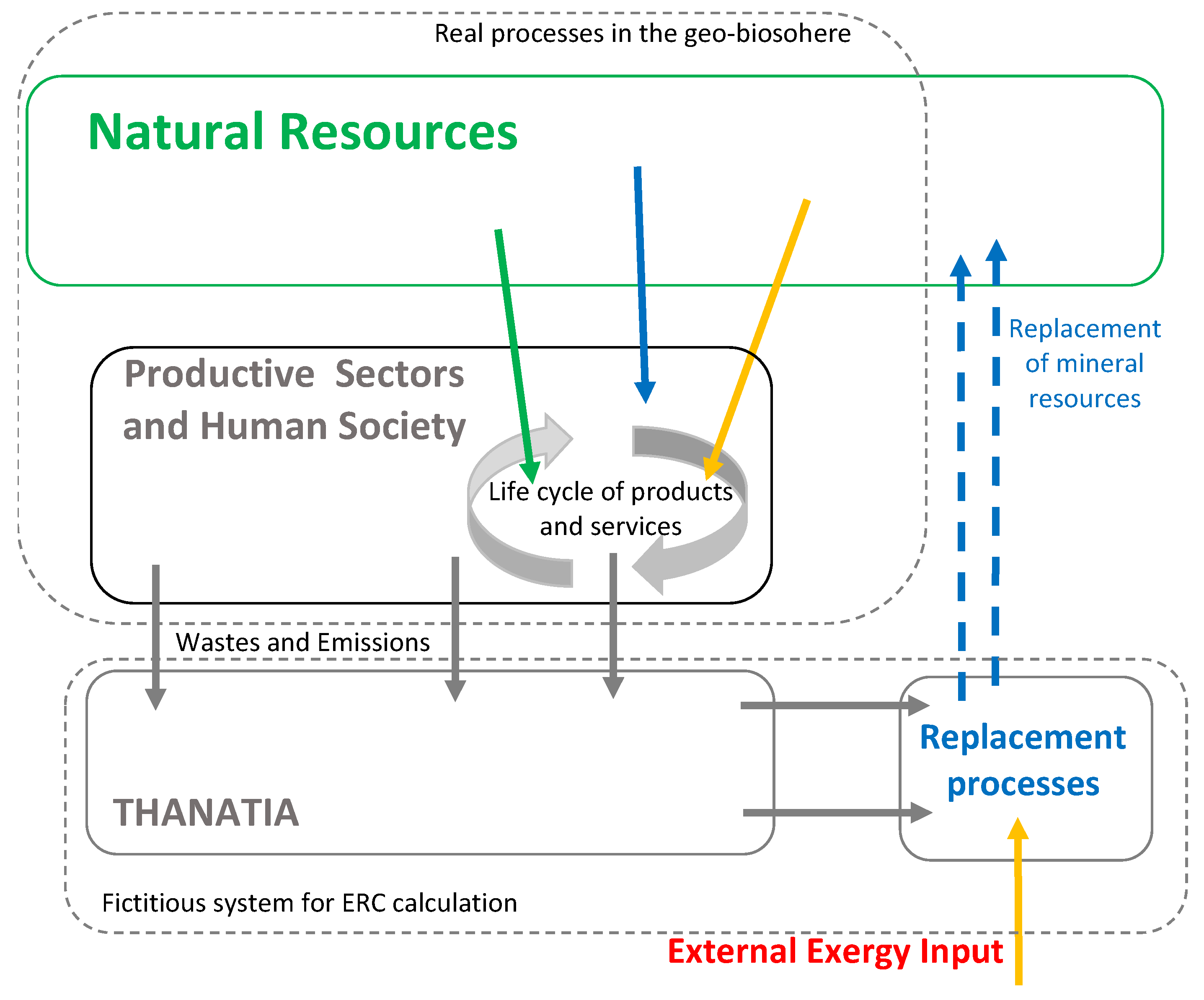

2.3. The Exergy Cost of Mineral Resources

- To extend the supply chain describing the indirect consumption of resources.

- To define a set of unit exergy costs, not equal to one, which is regarded as equivalent to the mechanism of additional exergy resource destruction.

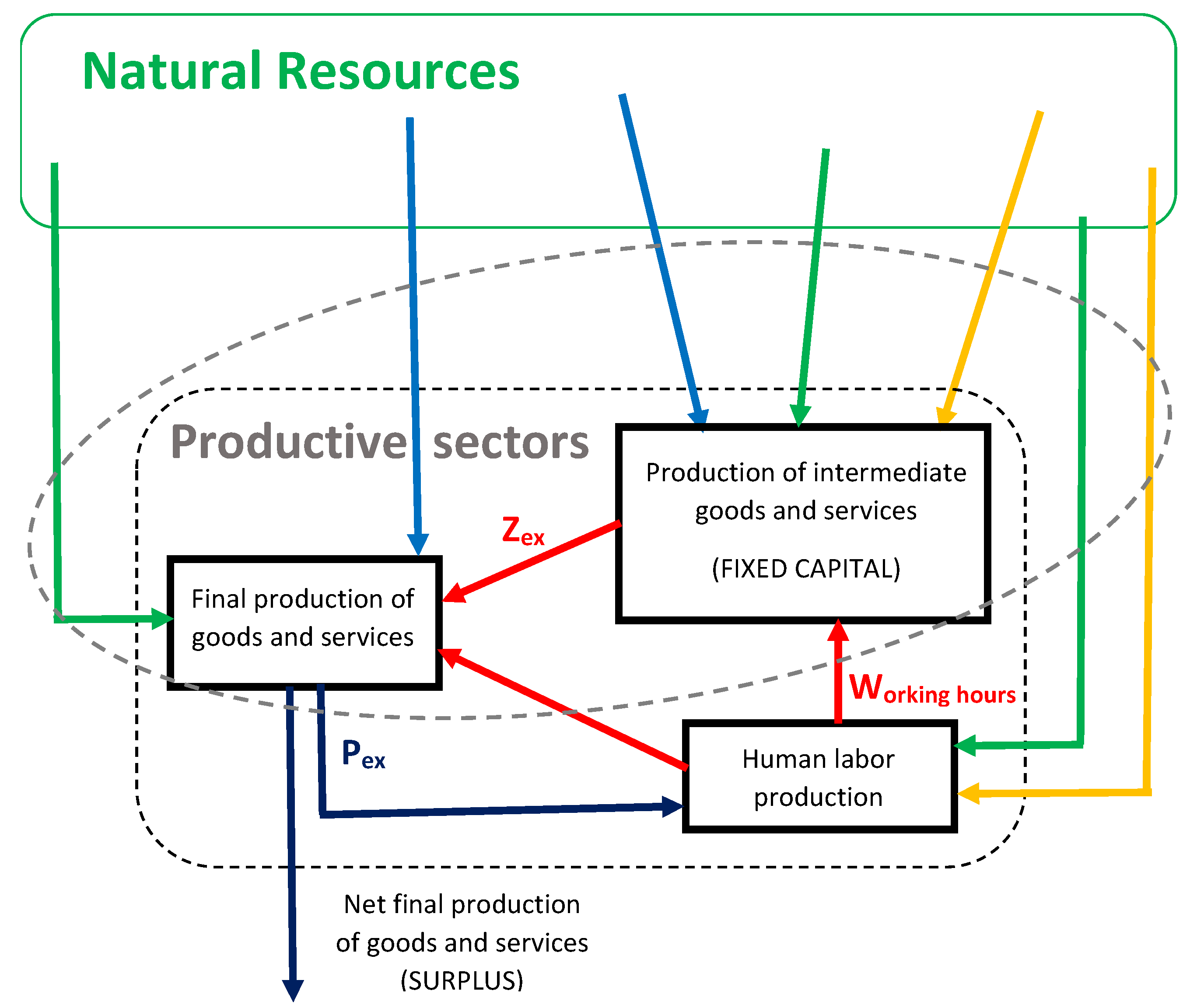

2.4. The Exergy Equivalent of Capital and Human Work

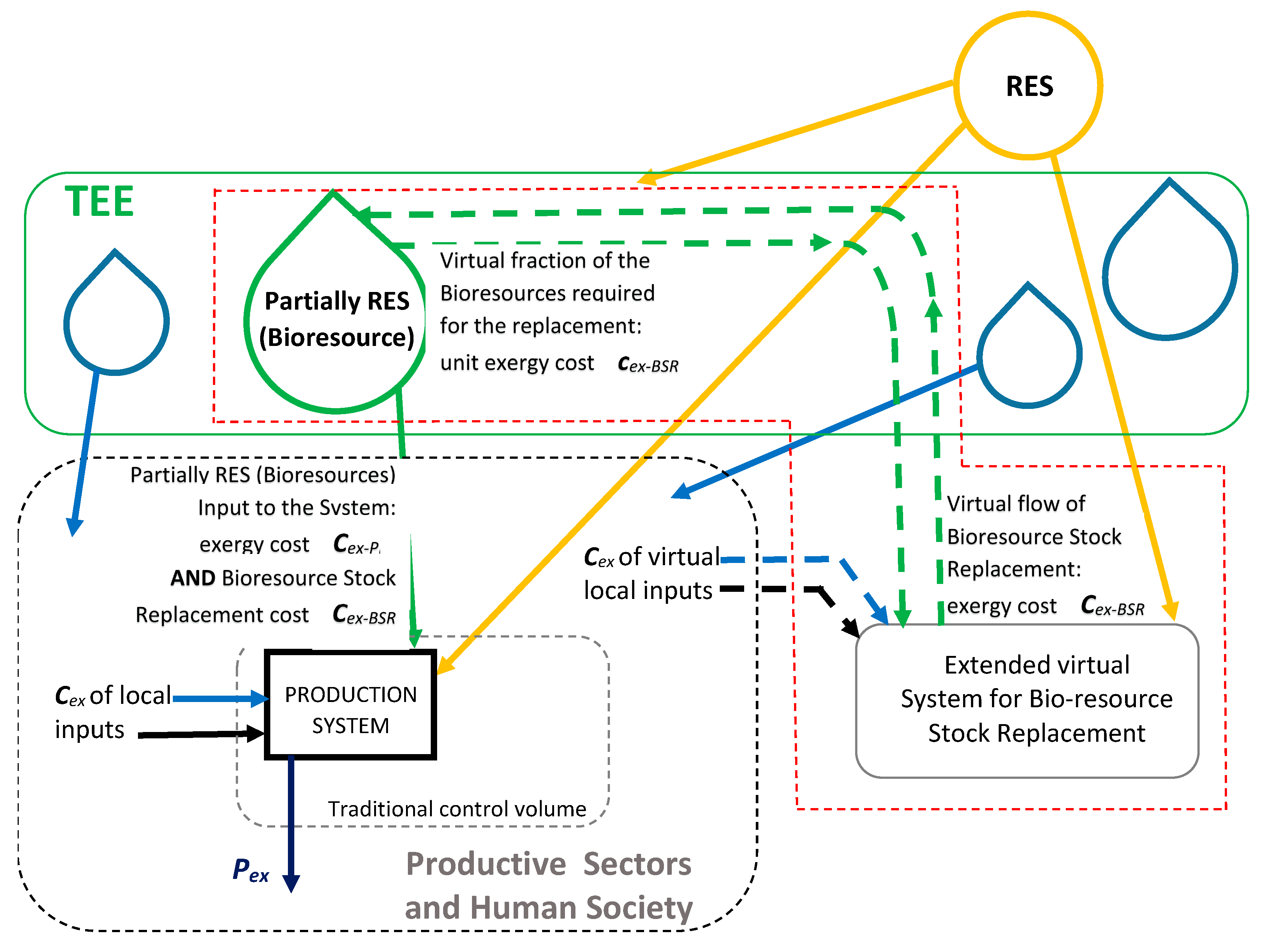

2.5. The Exergy Cost of Products of Biological Systems

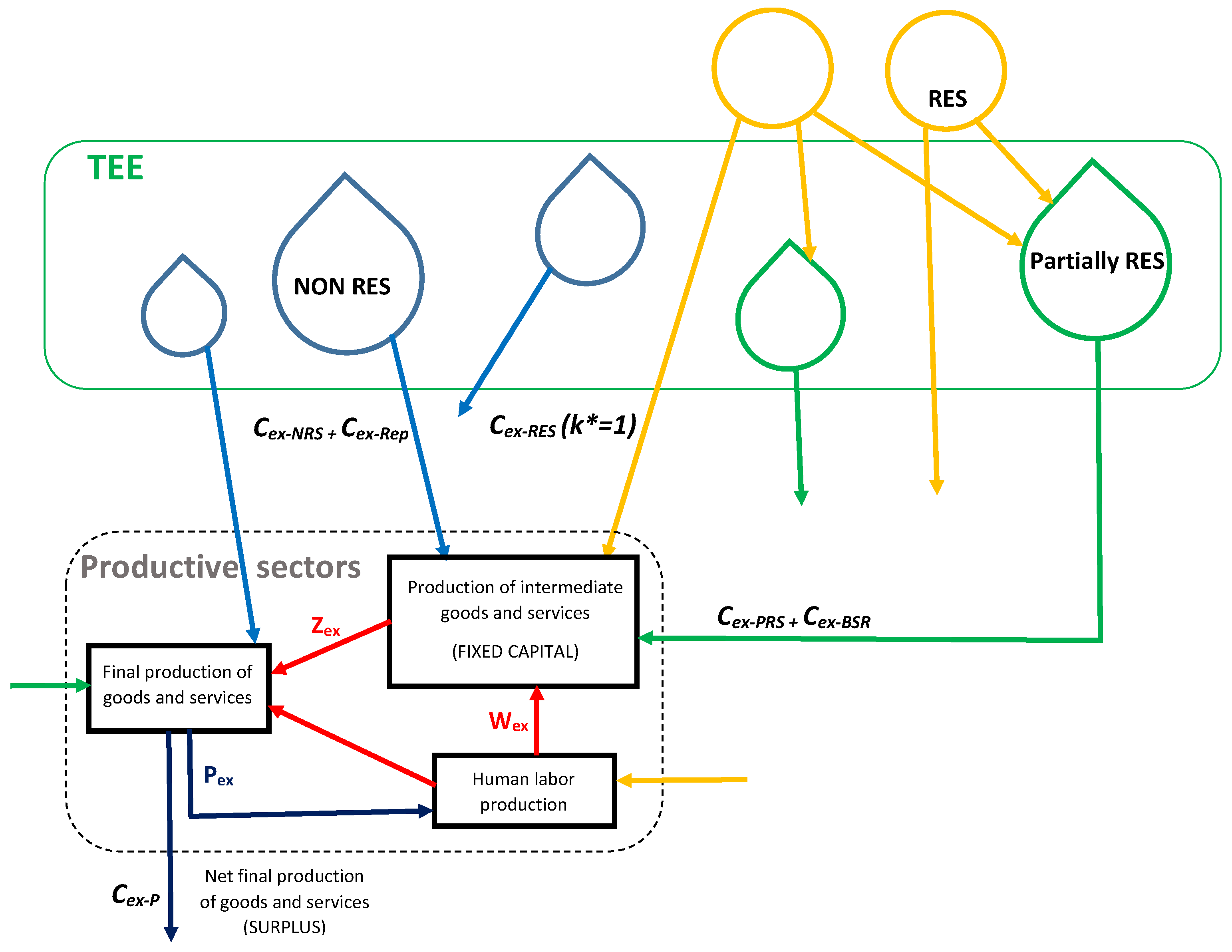

- Solar energy and other renewable resources have a unit exergy cost equal to one.

- All non-renewable resources can be evaluated at their exergy cost, including indirect consumption and the ERC of the mineral resources.

- The capital and human work can be evaluated at their exergy equivalent, via one of the methodologies previously outlined.

2.6. The Exergy Evaluation of Polluting Emissions

- The destruction of the confine restrictions of reservoirs.

- The variation in the zero-exergy matrix temperature or composition.

- The dilution of substances inside the reservoirs, reducing their concentration.

- The indirect destruction of the (living) biomass stock inside the reservoirs.

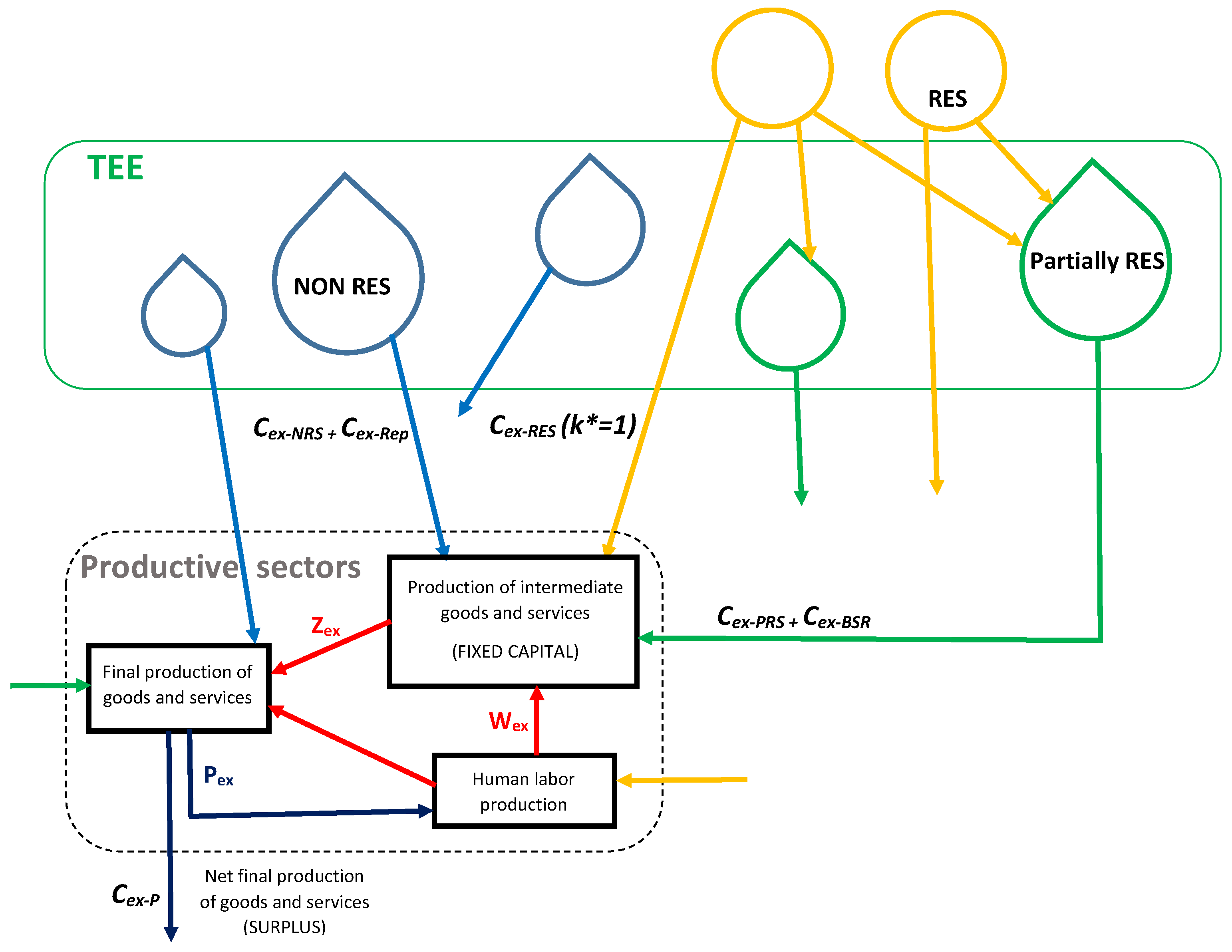

3. The Thermoeconomic Environment Cost and the Exergy Resource Sustainability

- is the TEEC of the product P.

- is the exergy cost of the product P, taking into account only RES.

- and are the exergy costs of the product P, taking into account only partially RES, or non-RES, respectively,

- and are the exergy costs of the product P, taking into account only the exergy BSR cost of partially RES, or the ERC of mineral non-RES, respectively.

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Nomenclature

| α | natural growth rate of the bioresource in a reservoir |

| β | extraction rate of the bioresource from a reservoir |

| ρ | fraction of the bioresource required for the replacement (Figure 5) |

| k | growth rate in the extended system required for the replacement (Figure 5) |

| TEEC of the product P | |

| TEEC of the product P, taking into account only RES | |

| TEEC of the product P, taking into account only partially RES | |

| TEEC of the product P, taking into account only non-RES | |

| TEEC of the product P, taking into account only the exergy BSR cost of partially RES | |

| TEEC of the product P, taking into account only the ERC of mineral non-RES | |

| k* | unit exergy cost of a flow |

| exergy-based resource sustainability indicator | |

| M | amount of bioresource in a reservoir |

| M0 | bioresource stock at instant t = 0 |

| Pex | exergy of the product |

| dR/dt | flow of bioresource required for stock replacement |

| t | time |

| Zex | exergy of the fixed capital |

Acronyms

| BSR | bioresource stock replacement |

| CExC | cumulative exergy consumption |

| EEA | extended exergy accounting |

| ERC | exergy replacement cost |

| RES | renewable energy source |

| TEE | thermoeconomic environment |

| TEEC | thermoeconomic environment cost |

References

- Reini, M.; Casisi, M. Exergy Analysis with Variable Ambient Conditions, ECOS 2016. In Proceedings of the 29th International Conference on Efficiency, Cost, Optimization, Simulation and Environmental Impact of Energy Systems, Portoros, Slovenia, 19–23 July 2016. [Google Scholar]

- Bejan, A.; Tsatsaronis, G.; Moran, M. Thermal Design and Optimization; John Wiley & Sons: New York, NY, USA, 1996. [Google Scholar]

- Bejan, A. Advanced Engineering Thermodynamics, 3rd ed.; John Wiley & Sons Inc.: Hoboken, NJ, USA, 2006. [Google Scholar]

- Reini, M.; Casisi, M. The Gouy-Stodola Theorem and the derivation of exergy revised. Energy 2020, 210, 118486. [Google Scholar] [CrossRef]

- Gaggioli, R.A.; Petit, P.J. Use The Second Law First. Chemtech 1977, 7, 496–506. [Google Scholar]

- Rosen, M. A Concise Review of Exergy-Based Economic Methods. In Proceedings of the 3rd IASME/WSEAS Int. Conf. on Energy & Environment, University of Cambridge, Cambridge, UK, 23–25 February 2008. [Google Scholar]

- Tiruta-Barna, L.; Benetto, E. A conceptual framework and interpretation of Emergy algebra. Ecol. Eng. 2013, 53, 290–298. [Google Scholar] [CrossRef]

- Gaggioli, R.A. The concept of available energy. Chem. Eng. Sci. 1961, 16, 87–96. [Google Scholar] [CrossRef]

- Dincer, I.; Rosen, M.A. EXERGY: Energy, Environment and Sustainable Development, 1st ed.; Elsevier: Burlington, VT, USA, 2007. [Google Scholar]

- Gaggioli, R.A.; Paulus, D.M. Available energy—Part II: Gibbs extended. J. Energy Res. Technol. 2002, 124, 110–115. [Google Scholar] [CrossRef]

- Gaggioli, R.A.; Richardson, D.H.; Bowman, A.J. Available energy—Part I: Gibbs revisited. J. Energy Resour. Technol.–Trans. ASME 2002, 124, 105–109. [Google Scholar] [CrossRef]

- Sciubba, E.; Wall, G. A brief commented history of exergy from the beginnings to 2004. Int. J. Thermodyn. 2010, 10, 1–26. [Google Scholar]

- Gaggioli, R.; Reini, M. Panel I: Connecting 2nd Law Analysis with Economics, Ecology and Energy Policy. Entropy 2014, 16, 3903–3938. [Google Scholar] [CrossRef] [Green Version]

- Reini, M.; Daniotti, S. Energy/Exergy Based Cost Accounting in Large Ecological-Technological Energy Systems. In Proceedings of the 12th Joint European Thermodynamics Conference, Brescia, Italy, 1–5 July 2013. [Google Scholar]

- Szargut, J. Exergy Method: Technical and Ecological Applications; Gateshead (GB), WIT Press: Southampton, UK, 2005. [Google Scholar]

- Leontief, W.W. The Structure of the American Economy, 1919–1939, 2nd ed.; Oxford University Press: New York, NY, USA, 1951. [Google Scholar]

- Valero, A.C.; Valero, A.D. Thanatia—The Destiny of the Earth’s Mineral Resources—A Thermodynamic Cradle-to-Cradle Assessment; World Scientific Publishing Company: Toh Tuck Link, Singapore, 2014; p. 670. [Google Scholar]

- Szargut, J.; Morris, D.R.; Steward, F.R. Exergy Analysis of Thermal, Chemical, and Metallurgical Processes; Hemisphere: London, UK, 1987. [Google Scholar]

- Kharrazi, A.; Kraines, S.; Hoang, L.; Yarime, M. Advancing quantification methods of sustainability: A critical examination Emergy, exergy, ecological footprint, and ecological information-based approaches. Ecol. Indic. 2014, 37, 81–89. [Google Scholar] [CrossRef]

- Odum, H.T. Environmental Accounting: Emergy and Environmental Decision Making, 1st ed.; John Wiley & Sons: New York, NY, USA, 1996. [Google Scholar]

- Brown, M.T.; Ulgiati, S. Emergy-based indices and ratios to evaluate sustainability: Monitoring economies and technology toward environmentally sound innovation. Ecol. Eng. 1997, 9, 51–69. [Google Scholar] [CrossRef]

- Sciubba, E. Exergy as a Direct Measure of Environmental Impact. Adv. Energy Syst. 1999, 39, 573–581. [Google Scholar] [CrossRef]

- Sciubba, E. Beyond thermoeconomics? The concept of extended exergy accounting and its application to the analysis and design of thermal systems. Exergy Int. J. 2001, 1, 68–84. [Google Scholar] [CrossRef]

- Sciubba, E. Extended exergy accounting applied to energy recovery from waste: The concept of total recycling. Energy 2003, 28, 1315–1334. [Google Scholar] [CrossRef]

- Sciubba, E.; Bastianoni, S.; Tiezzi, E. Exergy and extended exergy accounting of very large complex systems with an application to the province of Siena, Italy. J. Environ. Manag. 2008, 86, 372–382. [Google Scholar] [CrossRef]

- Koroneos, C.J.; Nanaki, E.A.; Xydis, G.A. Sustainability Indicators for the Use of Resources—The Exergy Approach. Sustainability 2012, 4, 1867–1878. [Google Scholar] [CrossRef] [Green Version]

- Rosen, M.A.; Dincer, I.; Kanoglu, M. Role of exergy in increasing efficiency and sustainability and reducing environmental impact. Energy Policy 2008, 36, 128–137. [Google Scholar] [CrossRef]

- Aydin, H.; Turan, O.; Karakoc, T.H.; Midilli, A. Exergetic Sustainability Indicators as a Tool in Commercial Aircraft: A Case Study for a Turbofan Engine. Int. J. Green Energy 2015, 12, 28–40. [Google Scholar] [CrossRef]

- Dewulf, J.; Van Langenhove, H.; Mulder, J.; Van Den Berg, M.M.D.; van der Kooi, H.J.; de Swaan Arons, J. Illustrations towards quantifying the sustainability of technology. Green Chem. 2000, 2, 108–114. [Google Scholar] [CrossRef]

- Dale, V.H.; Beyeler, S.C. Challenges in the development and use of ecological indicators. Ecol. Indicat. 2001, 1, 3–10. [Google Scholar] [CrossRef] [Green Version]

- Paul, B.D. A history of the concept of Sustainable Development: Literature review. Available online: https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.532.7232&rep=rep1&type=pdf (accessed on 1 October 2013).

- Sciubba, E. Can an Environmental Indicator valid both at the local and global scales be derived on a thermodynamic basis? Ecol. Indicat. 2013, 29, 125–137. [Google Scholar] [CrossRef]

- Kehdr, S.; Reini, M.; Casisi, M. A critical review of exergy based cost accounting approaches. In Proceedings of the 6th International Conference on Contemporary Problems of Thermal Engineering CPOTE 2020, Krakow, Poland, 21–24 September 2020. [Google Scholar]

- Hau, J.L.; Bakshi, B.R. Expanding exergy analysis to account for ecosystem products and service. Environ. Sci. Technol. 2004, 38, 3768–3777. [Google Scholar] [CrossRef] [PubMed]

- Valero, A.; Serra, L.; Uche, J. Fundamentals of Exergy Cost Accounting and Thermoeconomics. Part I Theory J. Energy Resour. Technol. 2006, 128, 1–8. [Google Scholar] [CrossRef]

- Gaudreau, K.; Fraser, R.A.; Murphy, S. The Tenuous Use of Exergy as a Measure of Resource Value or Waste Impact. Sustainability 2009, 1, 1444–1463. [Google Scholar] [CrossRef] [Green Version]

- Sciubba, E. From Engineering Economics to Extended Exergy Accounting: A Possible Path from Monetary to Resource-Based Costing. J. Ind. Ecol. 2004, 8, 19–40. [Google Scholar] [CrossRef]

- Yang, J.; Chen, B. Extended exergy-based sustainability accounting of a household biogas project in rural China. Energy Policy 2014, 68, 264–272. [Google Scholar] [CrossRef]

- Romero, J.C.; Linares, P. Exergy as a global energy sustainability indicator. A review of the state of the art. Renew. Sustain. Energy Rev. 2014, 33, 427–442. [Google Scholar] [CrossRef]

- Kehdr, S.; Casisi, M.; Reini, M. The role of the Thermoeconomic Environment in the exergy based cost accounting of technological and biological systems, submitted to Energy, previously. In Proceedings of the ECOS 2021—The 34th International Conference on Efficiency, Cost, Optimization, Simulation and Environmental Impact of Energy Systems, Taormina, Italy, 28 June–2 July 2021. [Google Scholar]

- Giorgi, F.; Coppola, E.; Raffaele, F. A consistent picture of the hydroclimatic response to global warming from multiple indices: Models and observations. J. Geophys. Res. Atmos. 2014, 119, 11–695. [Google Scholar] [CrossRef]

- Szargut, J.; Stanek, W. Thermo-ecological optimization of a solar collector. Energy 2007, 32, 584–590. [Google Scholar] [CrossRef]

- Szargut, J.; Ziębik, A.; Stanek, W. Depletion of the non-renewable natural exergy resources as a measure of the ecological cost. Energy Convers. Manag. 2002, 43, 1149–1163. [Google Scholar] [CrossRef]

- Valero, A.; Valero, A.; Stanek, W. Assessing the exergy degradation of the natural capital: From Szargut’s updated reference environment to the new thermoecological-cost methodology. Energy 2018, 163, 1140–1149. [Google Scholar] [CrossRef]

- Valero, A.D.; Agudelo, A.; Valero, A.D. The crepuscular planet. A model for the exhausted atmosphere and hydrosphere. Energy 2011, 36, 3745–3753. [Google Scholar] [CrossRef]

- Valero, A.; Valero, A.; Gómez, J.B. The crepuscular planet. A model for the exhausted continental crust. Energy 2011, 36, 694–707. [Google Scholar] [CrossRef]

- Rocco, M.V.; Colombo, A.; Sciubba, E. Advances in exergy analysis: A novel assessment of the Extended Exergy Accounting method. Appl. Energy 2014, 113, 1405–1420. [Google Scholar] [CrossRef]

- Rocco, M.; Colombo, E. Internalization of human labor in embodied energy analysis: Definition and application of a novel approach based on environmentally extended Input-Output analysis. Appl. Energy 2016, 182, 590–601. [Google Scholar] [CrossRef]

- Lozano, M.; Valero, A. Theory of the exergetic cost. Energy 1993, 18, 939–960. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Khedr, S.; Casisi, M.; Reini, M. The Thermoeconomic Environment Cost Indicator (iex-TEE) as a One-Dimensional Measure of Resource Sustainability. Energies 2022, 15, 2260. https://doi.org/10.3390/en15062260

Khedr S, Casisi M, Reini M. The Thermoeconomic Environment Cost Indicator (iex-TEE) as a One-Dimensional Measure of Resource Sustainability. Energies. 2022; 15(6):2260. https://doi.org/10.3390/en15062260

Chicago/Turabian StyleKhedr, Sobhy, Melchiorre Casisi, and Mauro Reini. 2022. "The Thermoeconomic Environment Cost Indicator (iex-TEE) as a One-Dimensional Measure of Resource Sustainability" Energies 15, no. 6: 2260. https://doi.org/10.3390/en15062260

APA StyleKhedr, S., Casisi, M., & Reini, M. (2022). The Thermoeconomic Environment Cost Indicator (iex-TEE) as a One-Dimensional Measure of Resource Sustainability. Energies, 15(6), 2260. https://doi.org/10.3390/en15062260