Does Fossil Fuel Financing Affect Banks’ ESG Ratings?

Abstract

:1. Introduction

2. Literature Review

2.1. Rationale to Shift Financing from Fossil Fuels to the Renewable Energy Sector

2.2. Involvement of the Banking Sector in Energy Transition and Its Determinants

2.3. Coal Pricing in Bank Practices and Greenwashing

2.4. ESG Risk and Its Impact on Bank Activity and Performance

3. Materials and Methods

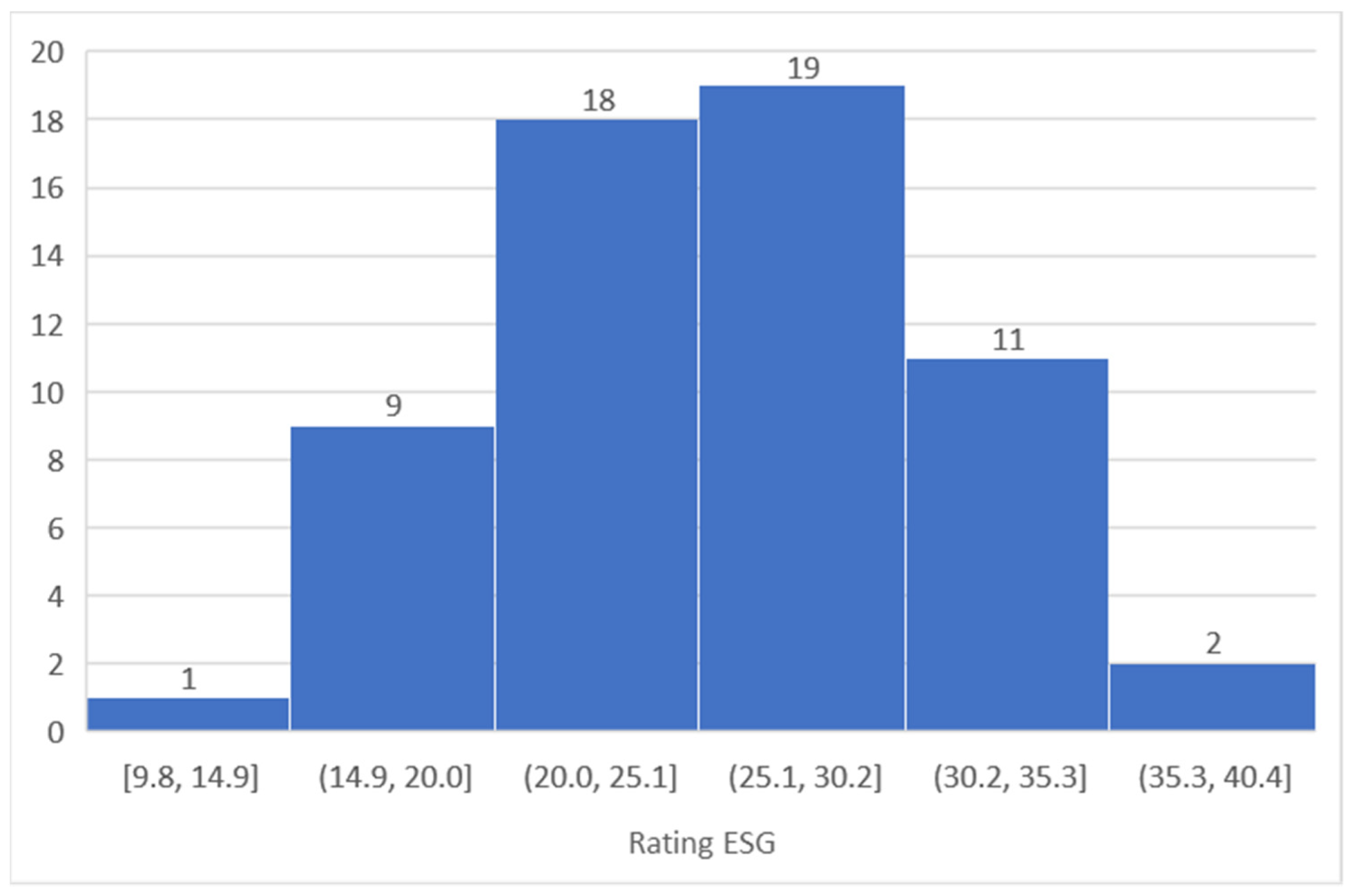

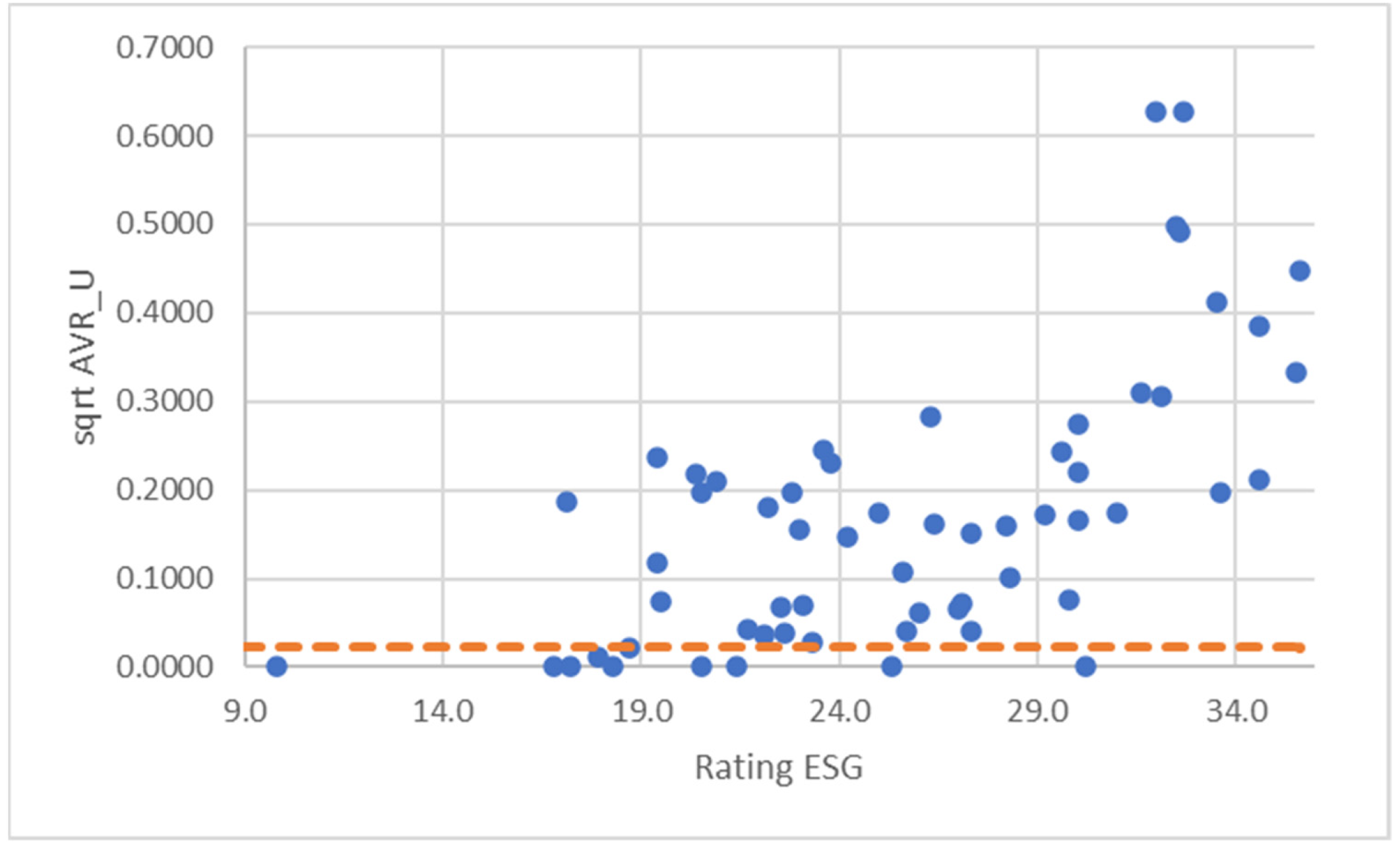

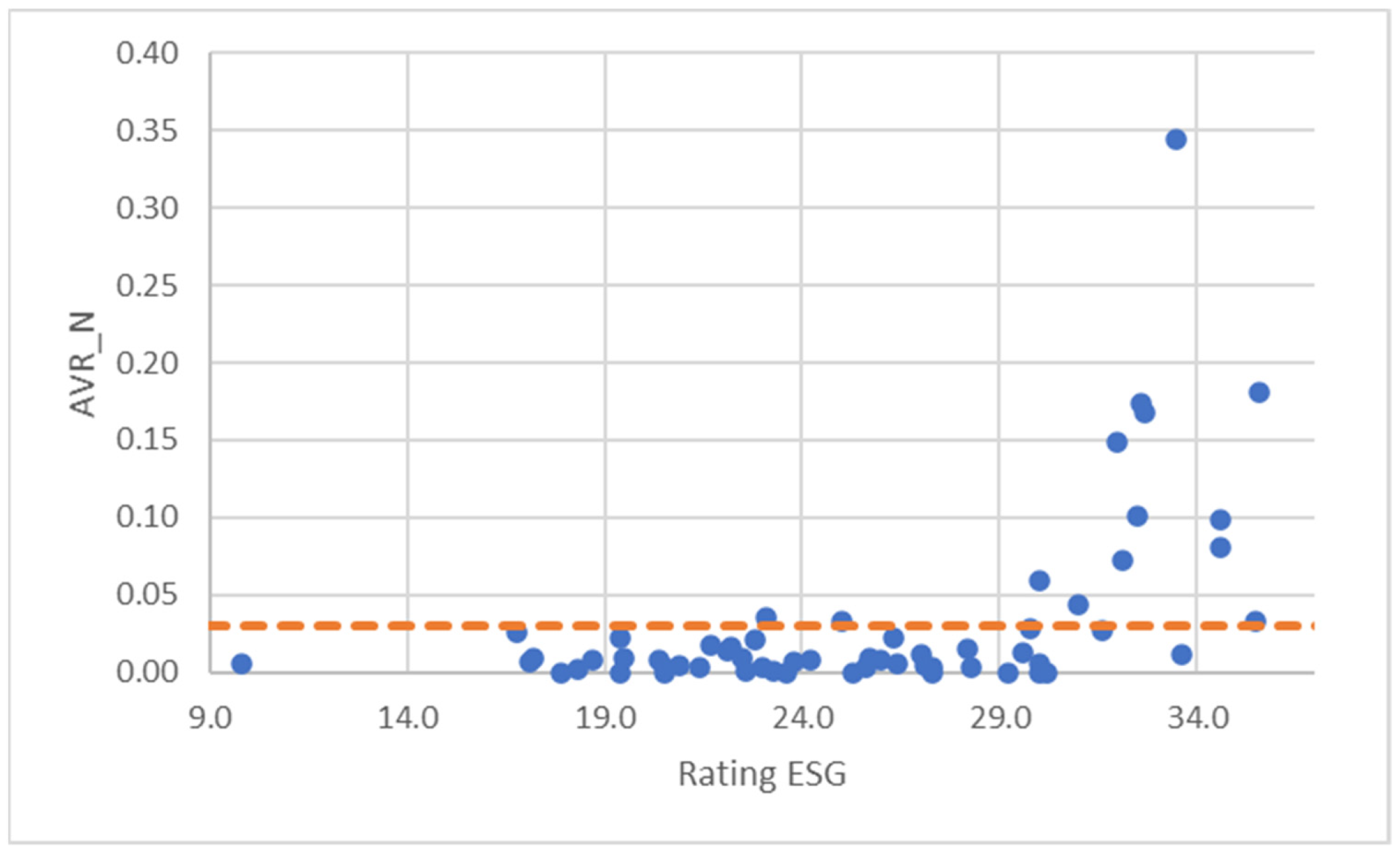

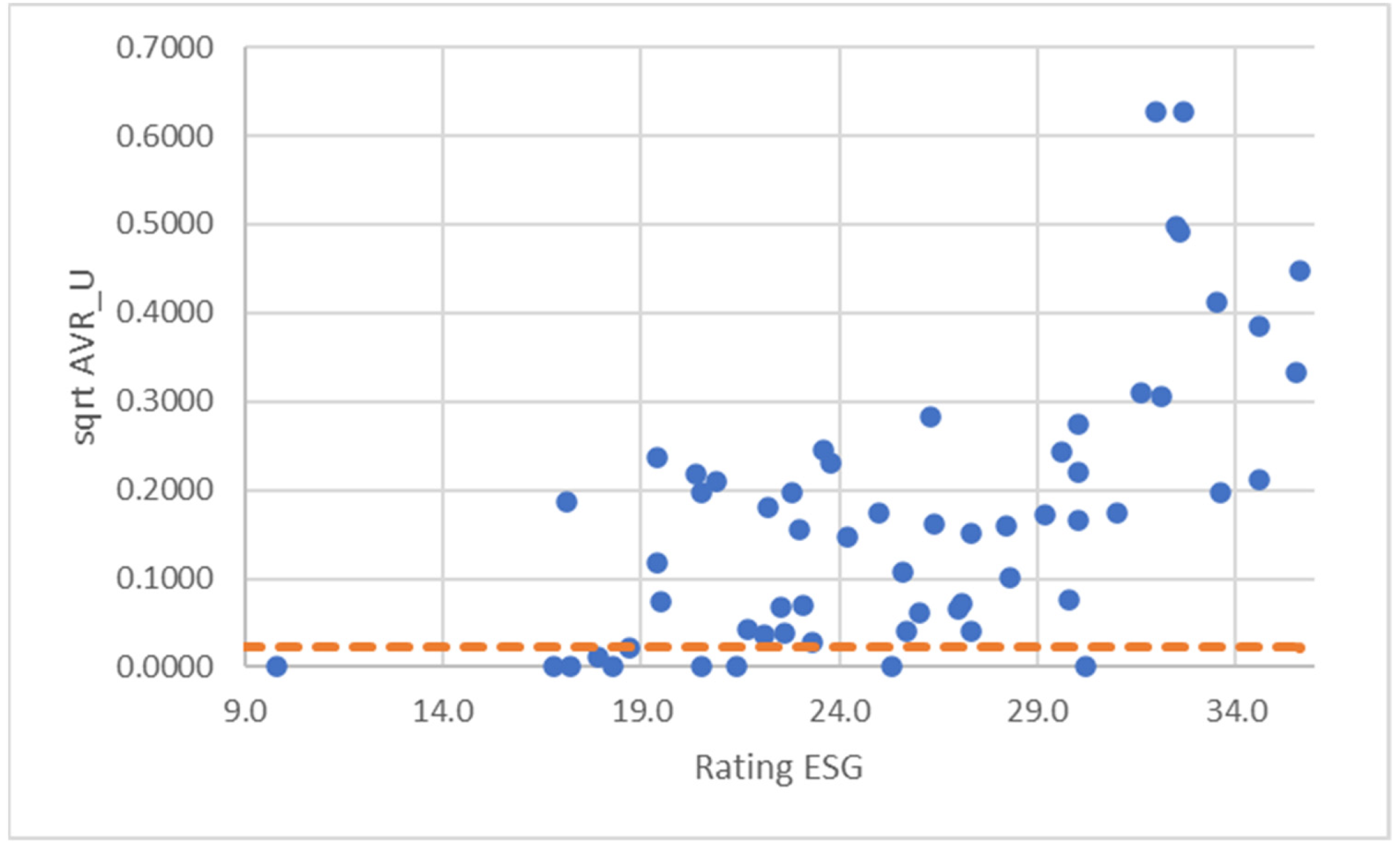

4. Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Jeucken, M. Sustainable Finance and Banking: The Financial Sector and the Future of the Planet; Routledge: London, UK, 2010. [Google Scholar]

- da Silva Inácio, L.; Delai, I. Sustainable banking: A systematic review of concepts and measurements. Environ. Dev. Sustain. 2021, 24, 1–39. [Google Scholar] [CrossRef]

- Danisman, G.O.; Demir, E.; Zaremba, A. Financial Resilience to the COVID-19 Pandemic: The Role of Banking Market Structure. Appl. Econ. 2021, 53, 1–24. [Google Scholar] [CrossRef]

- Başarir, C.; Darici, B. Financial Systems, Central Banking and Monetary Policy During COVID-19 Pandemic and After; Lexington Books: Lanham, MD, USA, 2021. [Google Scholar]

- Foglia, M.; Addi, A.; Angelini, E. The Eurozone banking sector in the time of COVID-19: Measuring volatility connectedness. Glob. Financ. J. 2021, 51, 100677. [Google Scholar] [CrossRef]

- Korzeb, Z.; Niedziółka, P. Resistance of commercial banks to the crisis caused by the COVID-19 pandemic: The case of Poland. Equilib. Q. J. Econ. Econ. Policy 2020, 15, 205–234. [Google Scholar] [CrossRef]

- Demirguc-Kunt, A.; Pedraza, A.; Ruiz, C. Banking sector performance during the COVID-19 Crisis. J. Bank Financ. 2021, 133, 106305. [Google Scholar] [CrossRef]

- Bernardelli, M.; Korzeb, Z.; Niedziółka, P. The banking sector as the absorber of the COVID-19 crisis? economic consequences: Perception of WSE investors. Oecon. Copernic. 2021, 12, 335–374. [Google Scholar] [CrossRef]

- Park, S.R.; Jang, J.Y. The Impact of ESG Management on Investment Decision: Institutional Investors’ Perceptions of Country-Specific ESG Criteria. Int. J. Financ. Stud. 2021, 9, 48. [Google Scholar] [CrossRef]

- KPMG. Purpose and Value Take Center Stage. Available online: https://home.kpmg/xx/en/home/insights/2020/07/banks-put-esg-at-the-heart-of-their-operations.html (accessed on 10 January 2022).

- Kotsantonis, S.; Bufalari, V. Do Sustainable Banks Outperform. Driving Value Creation Through ESG Practices. KKS Advisors, Deloitte, EIB, GABV. Available online: https://www2.deloitte.com/content/dam/Deloitte/lu/Documents/financial-services/Banking/lu-do-sustainable-banks-outperform-driving-value-creation-through-ESG-practices-report-digital.pdf (accessed on 12 January 2022).

- Reclaim Finance. Banking on Climate Chaos: Fossil Fuel Finance Report. 2021. Available online: https://reclaimfinance.org/site/en/2021/03/24/baking-climate-chaos-fossil-fuel-finance-report-2021/ (accessed on 10 January 2022).

- Clifford, C. 60 Largest Banks in the World Have Invested $3.8 Trillion in Fossil Fuels Since the Paris Agreement. Available online: https://www.cnbc.com/2021/03/24/how-much-the-largest-banks-have-invested-in-fossil-fuel-report.html (accessed on 10 January 2022).

- Sustainalytics. Available online: https://www.sustainalytics.com (accessed on 6 December 2021).

- World Bank Group. Bank Regulation and Supervision a Decade After the Global Financial Crisis. Global Financial Development Report 2019/2020. Available online: https://issuu.com/world.bank.publications/docs/9781464814471 (accessed on 10 January 2022).

- Glomsrød, S.; Wei, T. Business as unusual: The implications of fossil divestment and green bonds for financial flows, economic growth and energy market. Energy Sustain. Dev. 2018, 44, 1–10. [Google Scholar] [CrossRef]

- Plantinga, A.; Scholtens, B. The financial impact of fossil fuel divestment. Clim. Policy. 2021, 21, 107–119. [Google Scholar] [CrossRef]

- Ivanov, I.; Kruttli, M.S.; Watugala, S.W. Banking on Carbon: Corporate Lending and Cap-and-Trade Policy. Available online: https://ssrn.com/abstract=3650447 (accessed on 12 January 2022).

- Park, H.; Kim, J.D. Transition towards green banking: Role of financial regulators and financial institutions. Asian J. Sustain. Soc. Responsib. 2020, 5, 5. [Google Scholar] [CrossRef]

- Brutscher, P.-B.; Ravillard, P.; Semeniuk, G. Do Energy Efficient Firms Have Better Access to Finance? Energy J. 2021, 42, 6. [Google Scholar] [CrossRef]

- Sachs, J.D.; Woo, W.T.; Yoshino, N.; Taghizadeh-Hesary, F. Why Is Green Finance Important? ADBI Working Paper 917; Asian Development Bank Institute: Tokyo, Japan, 2019; Available online: https://www.adb.org/publications/why-green-finance-important (accessed on 10 January 2022).

- Best, R. Switching towards coal or renewable energy? The effects of financial capital on energy transitions. . Energy Econ. 2017, 63, 75–83. [Google Scholar] [CrossRef] [Green Version]

- Eckardt, A.; Mazutis, D. Banking for a Low Carbon Future: Explaining Climate Change Responses in a Low-Salience Industry. In Academy of Management Proceedings; Academy of Management: New York, NY, USA, 2020; Volume 2020. [Google Scholar] [CrossRef]

- Bhandary, R.R.; Gallagher, K.S.; Zhang, F. Climate finance policy in practice: A review of the evidence. Clim. Policy 2021, 21, 529–545. [Google Scholar] [CrossRef]

- Marques-Ibanez, D.; Reghezza, A.; Altunbas, Y.; d’Acri, C.R.; Spaggiar, M. Do Banks Fuel Climate Change? ECB Working Papers 2550; European Central Bank: Frankfurt, Germany, 2021. [Google Scholar]

- Kuykendall, T. S&P Global: Banks Provided 11% More Money to Coal-Related Companies Since 2016—Report. Available online: https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/banks-provided-11-more-money-to-coal-related-companies-since-2016-8211-report-62849285 (accessed on 11 January 2022).

- Chen, X.; Li, Z.; Gallagher, K.P.; Mauzerall, D.L. Financing carbon lock-in in developing countries: Bilateral financing for power generation technologies from China, Japan, and the United States. Appl. Energy 2021, 300, 117318. [Google Scholar] [CrossRef]

- Baruya, P. International Finance for Coal-Fired Power Plants; CCC/277; EA Clean Coal Centre: London, UK, 2017; Available online: https://usea.org/sites/default/files/International%20finance%20for%20coal%20fired%20power%20plants%20-%20ccc277.pdf (accessed on 10 January 2022).

- Manych, N.; Steckel, J.C.; Jakob, M. Finance-based accounting of coal emissions. Environ. Res. Lett. 2021, 16, 044028. [Google Scholar] [CrossRef]

- Dvorak, P.; Hua, S.; Yoon, F. Coal Projects in Asia Face Dwindling Financing as Climate Pressure Mounts. The Wall Street Journal. Available online: https://www.wsj.com/articles/coal-projects-in-asia-face-dwindling-financing-as-climate-pressure-mounts-11627896602 (accessed on 4 January 2022).

- Kim, J.W.; Lee, J.-S. Greening Energy Finance of Multilateral Development Banks: Review of the World Bank’s Energy Project Investment (1985–2019). Energies 2021, 14, 2648. [Google Scholar] [CrossRef]

- Heine, D.; Semmler, W.; Mazzucato, M.; Braga, J.P.; Flaherty, M.; Gevorkyan, A.; Hayde, E.; Radpour, S. Financing Low-Carbon Transitions Through Carbon Pricing and Green Bonds; Policy Research Working Paper 8991; World Bank: Washington, DC, USA, 2019; Available online: https://openknowledge.worldbank.org/handle/10986/32316 (accessed on 10 January 2022).

- Delis, M.D.; de Greiff, K.; Ongena, S. Being Stranded with Fossil Fuel Reserves? Climate Policy Risk and the Pricing of Bank Loans; EBRD Working Paper 231; European Central Bank: Frankfurt, Germany, 2019; Available online: https://www.ebrd.com/publications/working-papers/fossil-fuel-reserves (accessed on 10 January 2022).

- Fard, A.; Javadi, S.; Kim, I. Environmental Regulation and the Cost of Bank Loans: International Evidence. J. Financ. Stab. 2020, 51, 956. [Google Scholar] [CrossRef]

- Zhou, X.; Wilson, C.; Caldecott, B. The Energy Transition and Changing Financing Costs. Oxford Sustainable Finance Programme. 2021. Available online: https://www.smithschool.ox.ac.uk/research/sustainable-finance/publications/The-energy-transition-and-changing-financing-costs.pdf (accessed on 11 February 2022).

- Ehlers, T.; Packer, F.; de Greiff, K. The Pricing of Carbon Risk in Syndicated Loans: Which Risks are Priced and Why? BIS Working Papers 946; Bank for International Settlements: Basel, Switzerland, 2021; Available online: https://www.bis.org/publ/work946.htm (accessed on 10 January 2022).

- Chan, H.-Y.; Merdekawati, M.; Suryadi, B. Bank climate actions and their implications for the coal power sector. Energy Strategy Rev. 2022, 39, 100799. [Google Scholar] [CrossRef]

- Kustra, A.; Pawłowski, S.; Kozieł, D. Trendy zmian finansowania górnictwa węgla przez międzynarodowe instytucje finansowe. Przegląd Górniczy 2019, 75, 34–40. Available online: http://yadda.icm.edu.pl/yadda/element/bwmeta1.element.baztech-1ed551a0-181a-49b2-a7c8-192d2310cd62 (accessed on 10 January 2022).

- Zioło, M. Finanse Zrównoważone. Rozwój, Ryzyko, Rynek; Polskie Wydawnictwo Ekonomiczne: Warsaw/Szczecin, Poland, 2020. [Google Scholar]

- Korzeb, Z.; Kulpaka, P.; Niedziółka, P. Deoligopolizacja Rynku Agencji Ratingowych Oraz Inne Inicjatywy na Rzecz Poprawy Jakości Ratingów Zewnętrznych w Kontekście Oddziaływania Agencji Ratingowych na Stabilność Finansową; Materiały i Studia No. 333; Narodowy Bank Polski: Warsaw, Poland, 2019; Available online: https://www.nbp.pl/publikacje/materialy_i_studia/ms333.pdf (accessed on 10 January 2022).

- Niedziółka, P. Expected effects of the opening of the on-shore credit ratings’ market in China for the Big Three and its rationale. Bank Kredyt 2020, 51, 189–210. Available online: https://bankikredyt.nbp.pl/content/2020/02/BIK_02_2020_04.pdf (accessed on 10 January 2022).

- Kosiński, K. Ratingi ESG Wdzierają się do Polskich Spółek. Available online: https://www.pb.pl/ratingi-esg-wdzieraja-sie-do-polskich-spolek-981928 (accessed on 11 January 2022).

- Billio, M.; Costola, M.; Hristova, I.; Latino, C.; Pelizzon, L. Inside the ESG Ratings: (Dis)Agreement and Performance; SAFE Working Paper 284; Ca’ Foscari University of Venice: Venice, Italy, 2020; Available online: https://www.unive.it/pag/fileadmin/user_upload/dipartimenti/economia/doc/Pubblicazioni_scientifiche/working_papers/2020/WP_DSE_billio_costola_histova_latino_pelizzon_17_20.pdf (accessed on 11 January 2022).

- Walter, I. Sense and Nonsense in ESG Scoring. J. Law Financ. Account. 2020, 5, 307–336. [Google Scholar] [CrossRef]

- Norton, L. Market Wants ESG Data. Morningstar. Available online: https://www.morningstar.ca/ca/news/215859/market-wants-esg-data.aspx (accessed on 10 December 2021).

- Drempetic, S.; Klein, C.; Zwergel, B. The Influence of Firm Size on the ESG Score: Corporate Sustainability Ratings Under Review. J. Bus. Ethics 2020, 167, 333–360. [Google Scholar] [CrossRef]

- Chih, H.L.; Chih, H.H.; Chen, T.H. On the determinants of corporate social responsibility: International evidence on the financial industry. J. Bus. Ethics 2010, 93, 115–135. [Google Scholar] [CrossRef]

- Ciciretti, R.; Kobeissi, N.; Zhu, Y. Corporate social responsibility and financial performance: An analysis of bank community responsibility. Int. J. Bank. Account. Financ. 2014, 5, 342–373. [Google Scholar] [CrossRef]

- Cornett, M.M.; Erhemjamts, O.; Tehranian, H. Greed or good greeds: An examination of the relation between corporate social responsibility and the financial performance of U.S. commercial banks around the financial crisis. J. Bank Financ. 2016, 70, 137–159. [Google Scholar] [CrossRef]

- Tang, D.Y.; Yan, J.; Yao, Y. The Determinants of ESG Ratings: Rater Ownership Matters. Available online: https://ssrn.com/abstract=3889395 (accessed on 7 October 2021).

- Crespi, F.; Migliavacca, M. The Determinants of ESG Rating in the Financial Industry: The Same Old Story or a Different Tale? Sustainability 2020, 12, 6398. [Google Scholar] [CrossRef]

- KPMG, ESG Risks in Banks. Available online: https://assets.kpmg/content/dam/kpmg/xx/pdf/2021/05/esg-risks-in-banks.pdf (accessed on 11 October 2021).

- La Torre, M.; Leo, S.; Panetta, I.C. Banks and Environmental, Social and Governance Drivers: Follow the Market or the Authorities? Available online: https://onlinelibrary.wiley.com/doi/epdf/10.1002/csr.2132 (accessed on 23 October 2021).

- Azmi, W.; Hassan, M.K.; Houston, R.; Karim, M.S. ESG activities and banking performance: International evidence from emerging economies. J. Int. Financ. Mark. Inst. Money 2021, 70, 101277. [Google Scholar] [CrossRef]

- Tarmuji, I.; Maelah, R.; Tarmuji, N.H. The Impact of Environmental, Social and Governance Practices (ESG) on Economic Performance: Evidence from ESG Score. Int. J. Trade Econ. Financ. 2016, 7, 67–74. [Google Scholar] [CrossRef] [Green Version]

- Bruder, B.; Cheikh, Y.; Deixonne, F.; Zheng, B. Integration of ESG in Asset Allocation. Available online: https://ssrn.com/abstract=3473874 (accessed on 10 December 2021).

- Shakil, M.H.; Mahmood, N.; Tasnia, M.; Munim, Z.H. Do environmental, social and governance performance affect the financial performance of banks? A cross-country study of emerging market banks. Manag. Environ. Qual. 2019, 30, 1331–1344. [Google Scholar] [CrossRef]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Finance Investig. 2015, 5, 210–233. [Google Scholar] [CrossRef] [Green Version]

- Safarzynska, K.; van den Bergh, J. Financial stability at risk due to investing rapidly in renewable energy. Energy Policy 2017, 108, 12–20. [Google Scholar] [CrossRef]

- Eceiza, J.; Harreis, H.; Härtl, D.; Viscardi, S. Banking Imperatives for Managing Climate Risk. McKinsey & Company. Available online: https://www.mckinsey.com/~/media/mckinsey/business%20functions/risk/our%20insights/banking%20imperatives%20for%20managing%20climate%20risk/banking-imperatives-for-managing-climate-risk.pdf?shouldIndex=false (accessed on 10 December 2021).

- EBA—European Banking Authority. EBA Report on Management and Supervision of ESG Risks for Credit Institutions and Investment Firms. EBA/REP/2021.18. Available online: https://www.eba.europa.eu/sites/default/documents/files/document_library/Publications/Reports/2021/1015656/EBA%20Report%20on%20ESG%20risks%20management%20and%20supervision.pdf (accessed on 10 January 2022).

- Whelan, T.; Atz, U.; van Holt, T.; Clark, C. ESG and Financial Performance. Uncovering the Relationship by Aggregating Evidence from 1,000 Plus Studies Published Between 2015–2020. Studies Published Between 2015–2020. NYU Stern. Available online: https://www.stern.nyu.edu/sites/default/files/assets/documents/NYU-RAM_ESG-Paper_2021%20Rev_0.pdf (accessed on 14 December 2021).

- MSCI. MSCI World ESG Select Impact ex Fossil Fuels Index. 2019. Available online: https://www.msci.com/eqb/methodology/meth_docs/MSCI_World_ESG_Select_Impact_ex_Fossil_Fuels_Index_Aug2019.pdf (accessed on 12 February 2022).

- Haniffa, R.M.; Cooke, T.E. The impact of culture and corporate governance on corporate social reporting. J. Account. Public Policy 2005, 24, 391–430. [Google Scholar] [CrossRef]

- Buallay, A. Is sustainability reporting (ESG) associated with performance? Evidence from the European banking sector. Manag. Environ. Qual. 2019, 30, 98–115. [Google Scholar] [CrossRef]

- Miralles-Quirós, M.M.; Miralles-Quirós, J.L.; Redondo Hernández, J. ESG Performance and shareholder value creation in the banking industry: International differences. Sustainability 2019, 11, 1404. [Google Scholar] [CrossRef] [Green Version]

- Devalle, A.; Fiandrino, S.; Cantino, A. The Linkage between ESG Performance and Credit Ratings: A Firm-Level Perspective Analysis. Int. J. Bus. Manag. Sci. 2017, 12, 53–65. [Google Scholar] [CrossRef] [Green Version]

- Bouyé, E.; Menville, D. The Convergence of Sovereign Environmental, Social and Governance Ratings; Policy Research Working Paper 9583; World Bank: Washington, DC, USA, 2021; Available online: https://openknowledge.worldbank.org/handle/10986/35291 (accessed on 10 January 2022).

- Hickel, J. The sustainable development index: Measuring the ecological efficiency of human development in the Anthropocene. Ecol. Econ. 2020, 167, 106331. [Google Scholar] [CrossRef]

- Zhou, Z. Ensemble Methods. Foundations and Algorithms; Chapman and Hall/CRC: Boca Raton, FL, USA, 2012. [Google Scholar]

- Di Tommaso, C.; Thornton, J. Do ESG scores effect bank risk taking and value? Evidence from European banks. Corp. Soc. Responsib. Environ. 2020, 27, 2286–2298. [Google Scholar] [CrossRef]

- Douglas, E.; Van Holt, T.; Whelan, T. Responsible Investing: Guide to ESG Data Providers and Relevant Trends. J. Environ. Invest. 2017, 8, 92–114. Available online: https://cbey.yale.edu/sites/default/files/Responsible%20Investing%20-%20Guide%20to%20ESG%20Data%20Providers%20and%20Relevant%20Trends.pdf (accessed on 10 January 2022).

- Doyle, T.M. Ratings That Don’t Rate: The Subjective World of ESG Rating Agencies. American Council for Capital Formation. Available online: https://accfcorpgov.org/wp-content/uploads/2018/07/ACCF_RatingsESGReport.pdf (accessed on 12 January 2022).

- Weber, I. Sense and Nonsense in ESG Ratings. Harvard Law School Forum on Corporate Governance. Available online: https://corpgov.law.harvard.edu/2020/12/02/sense-and-nonsense-in-esg-ratings/ (accessed on 12 January 2022).

- Hemingway, C.A.; Maclagan, P.W. Managers’ Personal Values as Drivers of Corporate Social Responsibility. J. Bus. Ethics 2004, 50, 33–44. [Google Scholar] [CrossRef]

- Christensen, D.M.; Serafeim, G.; Sikochi, A. Why is Corporate Virtue in the Eye of the Beholder? The Case of ESG Ratings. Account. Rev. 2021, 97, 147–175. [Google Scholar] [CrossRef]

- Amel-Zadeh, A.; Serafeim, G. Why and How Investors Use ESG Information: Evidence from a Global Survey. Financ. Anal. J. 2018, 74, 87–103. [Google Scholar] [CrossRef] [Green Version]

- Caruso, G.; Gattone, S.A.; Fortuna, F.; Di Battista, T. Cluster Analysis for mixed data: An application to credit risk evaluation. Socio Econ. Plan. Sci. 2021, 73, 100850. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Name of the Bank | Country |

|---|---|

| Agricultural Bank of China | China |

| Bank of China | China |

| Bank of Communications | China |

| China CITIC Bank | China |

| China Construction Bank | China |

| China Everbright Bank | China |

| China Merchants Bank | China |

| China Minsheng Bank | China |

| Industrial & Commercial Bank of China Ltd. | China |

| Industrial Bank | China |

| Ping An | China |

| Postal Savings Bank of China | China |

| Shanghai Pudong Development Bank | China |

| State Bank of India | India |

| Mizuho Financial Group Inc | Japan |

| Mitsubishi UFJ Financial Group Inc | Japan |

| Sumitomo Mitsui Banking Corporation | Japan |

| Sumitomo Mitsui Trust Bank | Japan |

| Shinhan Financial Group | South Korea |

| Commonwealth Bank | Australia |

| National Australia Bank | Australia |

| Westpac Banking Corporation | Australia |

| Australia and New Zealand Banking Group | Australia |

| Danske Bank | Denmark |

| Nordea | Finland |

| BNP Paribas | France |

| Groupe BPCE/Natixis | France |

| Crédit Agricole | France |

| Crédit Mutuel | France |

| Société Générale | France |

| Commerzbank | Germany |

| Deutsche Bank | Germany |

| DZ Bank | Germany |

| Intesa Sanpaolo | Italy |

| UniCredit | Italy |

| ING | Netherlands |

| Rabobank | Netherlands |

| Sberbank | Russia |

| BBVA | Spain |

| Santander | Spain |

| Credit Suisse | Switzerland |

| UBS | Switzerland |

| Barclays | United Kingdom |

| HSBC | United Kingdom |

| Lloyds Banking Group | United Kingdom |

| Standard Chartered | United Kingdom |

| NatWest (formerly The Royal Bank of Scotland Group Plc) | United Kingdom |

| Bank of Montreal | Canada |

| Canadian Imperial Bank of Commerce | Canada |

| Royal Bank of Canada | Canada |

| Scotiabank | Canada |

| Bank of America | United States |

| Citigroup | United States |

| Goldman Sachs | United States |

| JPMorgan Chase | United States |

| Morgan Stanley | United States |

| TD Bank | United States |

| Truist Financial | United States |

| U.S. Bancorp | United States |

| Wells Fargo | United States |

| Variable | Description | Source and Period of Data |

|---|---|---|

| ARB | Average external credit rating of a bank | Standard & Poor’s, Moody’s, Fitch Ratings (September 2021) |

| NPL/Gross_Loans | Non-Performing Loans/Gross Loans | Orbis Bureau van Dijk (Consolidated, 2020) |

| Tier_1 | Tier 1 Capital Ratio | Orbis Bureau van Dijk (Consolidated, 2020) |

| NIM | Net Interest Margin | Orbis Bureau van Dijk (Consolidated, 2020) |

| ROE | Return on Equity | Orbis Bureau van Dijk (Consolidated, 2020) |

| C/I | Cost/Income Ratio | Orbis Bureau van Dijk (Consolidated, 2020) |

| LADSTF | Liquid Assets/(Deposits+ Short Term Funding) Ratio | Orbis Bureau van Dijk (Consolidated, 2020) |

| SPV | 1 Year bank’s share_price_volatility | Orbis Bureau van Dijk (September 2021) |

| CDS5y | Credit Default Swap (5 year average margin) | Orbis Bureau van Dijk (September 2021) |

| CAGR_G | Compound Annual Growth Rate of fossil fuels enterprises financing (2016–2020) | Authors’ elaboration based on [12] |

| CAGR_N | Compound Annual Growth Rate of coal mines’ financing (2016–2020) | Authors’ elaboration based on [12] |

| CAGR_U | Compound Annual Growth Rate of coal power plants’ financing (2016–2020) | Authors’ elaboration based on [12] |

| AVR_G | Fossil fuels enterprises financing’s share in bank’s portfolio (5 year average) | Authors’ elaboration based on [12] |

| AVR_N | Coal mines_financing’s share in bank’s portfolio (5 year average) | Authors’ elaboration based on [12] |

| AVR_U | Coal power plants_financing share in bank’s portfolio (5 year average) | Authors’ elaboration based on [12] |

| SDI | Sustainable Development Index | [69] |

| ARC | Average credit rating of a country of a bank’s registration | Standard & Poor’s, Moody’s, Fitch Ratings (September 2021) |

| Specification | Min. | 1st Qu. | Median | Mean | 3rd Qu. | Max. |

|---|---|---|---|---|---|---|

| ARB | 11.50 | 14.46 | 15.83 | 15.71 | 16.75 | 21.00 |

| NPL/Gross_Loans | 0.39 | 1.04 | 1.56 | 1.97 | 2.84 | 6.31 |

| Tier_1 | 8.51 | 13.20 | 14.20 | 14.75 | 16.13 | 21.40 |

| NIM | 0.48 | 1.04 | 1.66 | 1.74 | 2.33 | 5.43 |

| ROE | −9.68 | 3.44 | 6.12 | 6.29 | 9.75 | 15.95 |

| C/I | 25.19 | 52.25 | 60.52 | 57.01 | 65.81 | 91.99 |

| LADSTF | 5.07 | 23.34 | 41.89 | 44.73 | 54.27 | 161.22 |

| SPV | 0.14 | 0.22 | 0.30 | 0.30 | 0.37 | 0.44 |

| CDS5y | 0.22 | 0.31 | 0.44 | 0.51 | 0.54 | 1.53 |

| CAGR_G | −1.00 | −0.06 | 0.03 | 0.03 | 0.12 | 0.90 |

| CAGR_N | −1.00 | −0.12 | 0.08 | 0.20 | 0.25 | 10.00 |

| CAGR_U | −1.00 | −0.19 | −0.02 | 0.52 | 0.14 | 10.00 |

| AVR_G | 0.00 | 0.14 | 0.28 | 0.47 | 0.46 | 3.64 |

| AVR_N | 0.00 | 0.00 | 0.01 | 0.03 | 0.03 | 0.34 |

| AVR_U | 0.00 | 0.00 | 0.03 | 0.05 | 0.05 | 0.39 |

| SDI | 60.07 | 76.01 | 79.46 | 78.21 | 81.56 | 85.60 |

| ARC | 12.00 | 17.00 | 19.00 | 18.16 | 21.00 | 21.00 |

| Variable | Value | Std. Error | z Value | p Value | Odds Ratio |

|---|---|---|---|---|---|

| (Intercept) | 27.9918 | 11.1954 | 2.500 | 0.0124 | |

| SDI | −0.3914 | 0.1466 | −2.669 | 0.0076 | 0.6761 |

| AVR_N_cut-off | 3.2076 | 1.1082 | 2.894 | 0.0038 | 24.7197 |

| Variable | Value | Std. Error | z Value | p Value | Odds Ratio |

|---|---|---|---|---|---|

| (Intercept) | −3.7165 | 0.8976 | −4.140 | 3.47 × 10−5 | |

| AVR_G | 1.7914 | 0.8684 | 2.063 | 0.039120 | 5.9978 |

| AVR_U_cut-off | 3.5776 | 1.0273 | 3.483 | 0.000496 | 35.7875 |

| Specifications | Anticipated | ||||

|---|---|---|---|---|---|

| Non-High | High | ||||

| Actual | Non-High | 42 | 1 | cut-off point | 0.2988 |

| High | 5 | 12 | count R2 | 90.00% | |

| Specification | Anticipated | ||||

|---|---|---|---|---|---|

| Non-Low | Low | ||||

| Actual | Non-Low | 46 | 4 | cut-off point | 0.5025 |

| Low | 3 | 7 | count R2 | 93.33% | |

| Specification | Anticipated | |||

|---|---|---|---|---|

| Low | Medium | High | ||

| Actual | Low | 7 | 3 | 0 |

| Medium | 1 | 31 | 1 | |

| High | 0 | 2 | 15 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bernardelli, M.; Korzeb, Z.; Niedziółka, P. Does Fossil Fuel Financing Affect Banks’ ESG Ratings? Energies 2022, 15, 1495. https://doi.org/10.3390/en15041495

Bernardelli M, Korzeb Z, Niedziółka P. Does Fossil Fuel Financing Affect Banks’ ESG Ratings? Energies. 2022; 15(4):1495. https://doi.org/10.3390/en15041495

Chicago/Turabian StyleBernardelli, Michał, Zbigniew Korzeb, and Paweł Niedziółka. 2022. "Does Fossil Fuel Financing Affect Banks’ ESG Ratings?" Energies 15, no. 4: 1495. https://doi.org/10.3390/en15041495

APA StyleBernardelli, M., Korzeb, Z., & Niedziółka, P. (2022). Does Fossil Fuel Financing Affect Banks’ ESG Ratings? Energies, 15(4), 1495. https://doi.org/10.3390/en15041495