Potential Solutions for the Short to Medium-Term Natural Gas Shortage Issues of Europe: What Can Qatar Do?

Abstract

1. Introduction

2. Materials and Methods

3. Results and Discussion

3.1. Problem 1—Limited LNG Quantities to Export

3.2. Problem 2—Long-Term Fixed Contracting Strategy

3.3. Problem 3—European LNG Terminals Have Limited Space for More Gas

3.4. Solutions for Problem 1

3.5. Solutions for Problem 2

3.6. Solutions for Problem 3

4. Conclusions

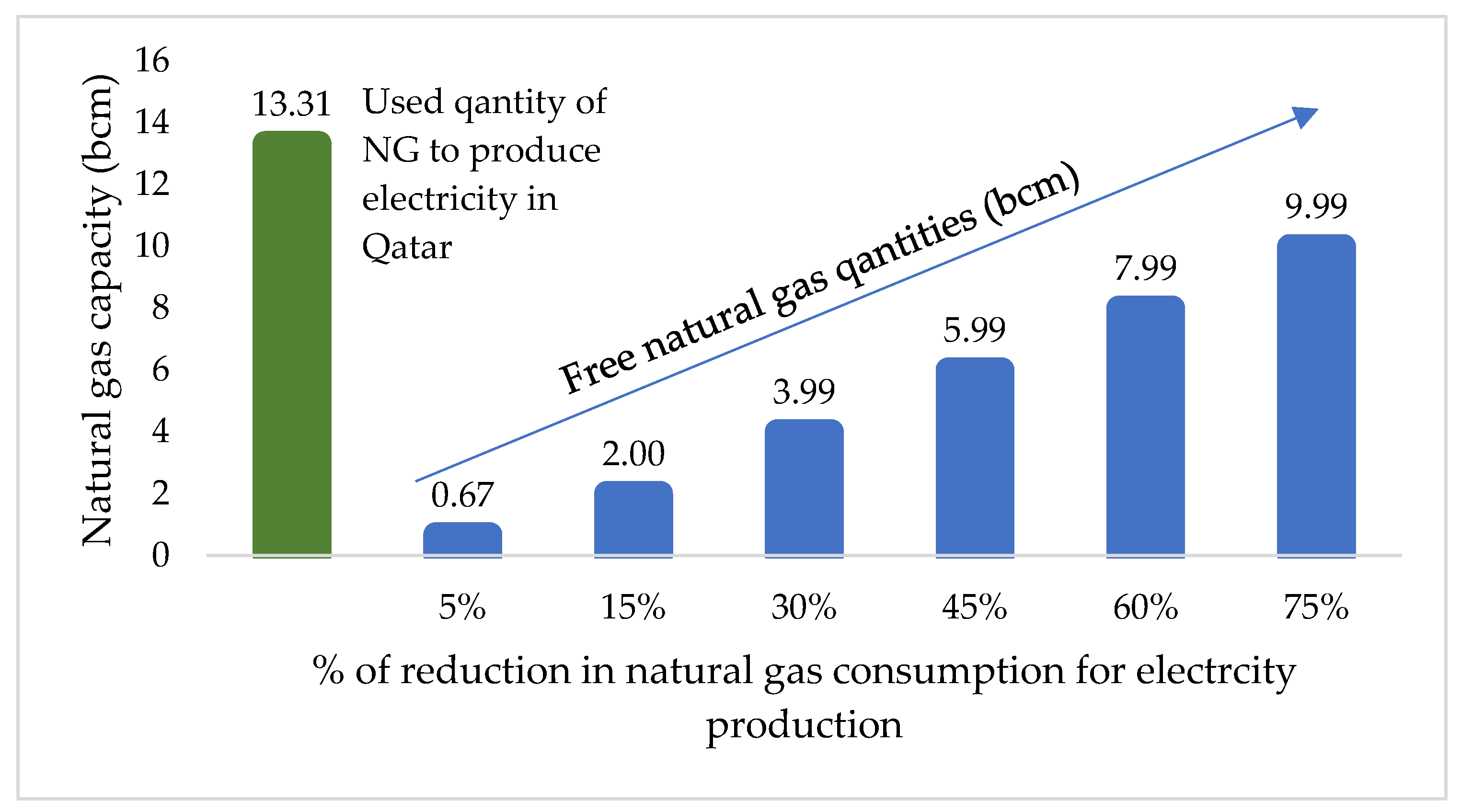

- Reducing local natural gas consumption for power production by relying on renewable energy resources can free some quantities of natural gas. If 15% of locally generated electricity is produced from renewables in Qatar, around 2 BCM of natural gas can be saved and used for exportation purposes. More free natural gas can be obtained if more local electricity is produced from renewables.

- Producing RNG from green hydrogen and captured carbon dioxide results in increasing natural gas quantities which can be exported to Europe. Use of renewable resources (wind and solar) in Qatar to produce 5000 MW of renewable power can lead to the production of 0.45 BCM of RNG, which can be exported to Europe.

- Regarding the other problem that limits Qatar from exporting more gas to Europe, moving the contracts due to end to Europe and increasing dependence on spot markets can reduce the effect of the problem of a long-term fixed contracting strategy. Based on calculations, redirecting all contracts due to end in 2023, 2024, 2025, and 2026 between Qatar and other buyers to Europe will increase the export capacity of LNG to reach 44.8 BCM (an increase of export capacity of about 48% compared to the year 2020). Finally, LNG terminals in Europe have the capacity to import around 207 BCM of LNG, and the total yearly imported capacity is 110.4. Therefore, there is free space for 96.6 BCM of LNG to be imported to Europe. However, this space is not enough to cover the gas shortage if Russia cuts off all gas supplies. Therefore, using floating import terminals can resolve the issue of the limited space available for receiving more gas in European LNG terminals.

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Anderson, B.; Salem, M.; Adam, P. Qatar Will Stand “in Solidarity” with European Countries during Energy Crisis; CNN Bus: Atlanta, GA, USA, 2022. [Google Scholar]

- Filimonova, I.V.; Komarova, A.V.; Sharma, R.; Novikov, A.Y. Transformation of international liquefied natural gas markets: New trade routes. Energy Rep. 2022, 8, 675–682. [Google Scholar] [CrossRef]

- BP Statistical Review. BP Statistical Review of World Energy; Pureprint Group Limited: Uckfield, UK, 2019. [Google Scholar]

- CBS News. What’s behind Russia Cutting off Natural Gas to Bulgaria and Poland? CBS News: Atlanta, GA, USA, 2022. [Google Scholar]

- Scott, D. Explainer: Could more LNG Supplies Get to Europe in the Event of a Crisis? Reuters: London, UK, 2022. [Google Scholar]

- Kochanek, E. The Energy Transition in the Visegrad Group Countries. Energies 2021, 14, 2212. [Google Scholar] [CrossRef]

- Rokicki, T.; Perkowska, A. Diversity and Changes in the Energy Balance in EU Countries. Energies 2021, 14, 1098. [Google Scholar] [CrossRef]

- Romanova, T. Russia’s political discourse on the EU’s energy transition (2014–2019) and its effect on EU-Russia energy relations. Energy Policy 2021, 154, 112309. [Google Scholar] [CrossRef]

- Sutrisno, A.; Alkemade, F. EU gas infrastructure resilience: Competition, internal changes, and renewable energy pressure. Energy Rep. 2020, 6, 24–30. [Google Scholar] [CrossRef]

- Guerrero-Mestre, V.; Poncela, M.; Fulli, G.; Contreras, J. A probabilistic analysis of power generation adequacy towards a climate-neutral Europe. Energy Rep. 2020, 6, 3316–3333. [Google Scholar] [CrossRef]

- Fetisov, V.; Tcvetkov, P.; Müller, J. Tariff approach to regulation of the European gas transportation system: Case of Nord Stream. Energy Rep. 2021, 7, 413–425. [Google Scholar] [CrossRef]

- Halser, C.; Paraschiv, F. Pathways to Overcoming Natural Gas Dependency on Russia—The German Case. Energies 2022, 15, 4939. [Google Scholar] [CrossRef]

- Halkos, G.E.; Gkampoura, E.C. Evaluating the effect of economic crisis on energy poverty in Europe. Renew Sustain. Energy Rev. 2021, 144, 110981. [Google Scholar] [CrossRef]

- EU Commission. The European Green Deal; EU Commission: Brussels, Belgium, 2019; Volume 53. [Google Scholar]

- Maris, G.; Flouros, F. The Green Deal, National Energy and Climate Plans in Europe: Member States’ Compliance and Strategies. Adm. Sci. 2021, 11, 75. [Google Scholar] [CrossRef]

- IEA. A 10-Point Plan to Reduce the European Union’ s Reliance on Russian Natural Gas; IEA: Paris, France, 2022. [Google Scholar]

- EC. REPowerEU: Joint European action for more affordable, secure and sustainable energy. Eur. Comm. 2022, 3. [Google Scholar]

- Mišík, M. The EU needs to improve its external energy security. Energy Policy 2022, 165, 112930. [Google Scholar] [CrossRef]

- Herranz-Surrallés, A. Energy diplomacy under scrutiny: Parliamentary control of intergovernmental agreements with third-country suppliers. West. Eur. Politics 2017, 40, 183–201. [Google Scholar] [CrossRef]

- Thaler, P.; Pakalkaite, V. Governance through real-time compliance: The supranationalisation of European external energy policy. J. Eur. Public Policy 2021, 28, 208–228. [Google Scholar] [CrossRef]

- Psaki, J. Press Briefing by Press Secretary Jen Psaki. White House Brief Room. 2022. Available online: https://www.whitehouse.gov/briefing-room/press-briefings/2022/01/25/press-briefing-by-press-secretary-jen-psaki-january-25-2022/ (accessed on 4 September 2022).

- Lambert, L.A.; Tayah, J.; Lee-Schmid, C.; Abdalla, M.; Abdallah, I.; Ali, A.H.; Esmail, S.; Ahmed, W. The EU’s natural gas Cold War and diversification challenges. Energy Strateg. Rev. 2022, 43, 100934. [Google Scholar] [CrossRef]

- Aljazeera. US, Qatar Leaders to Meet Amid Europe Energy Concerns; Aljazeera: London, UK, 2022. [Google Scholar]

- Antitrust: Commission opens investigation into restrictions to the free flow of gas sold by Qatar Petroleum in Europe. Eur. Comm. 2018. Available online: https://ec.europa.eu/commission/presscorner/detail/en/IP_18_4239 (accessed on 29 October 2022).

- Sönnichsen, N. Global Operational LNG Export Capacity by Country; Global Energy Monitor: Munich, Germany, 2021. [Google Scholar]

- GIIGNL. The LNG Industry—GIIGNL Annual Report. Neuilly-Sur-Seine, France. 2021. Available online: https://giignl.org/resources2/ (accessed on 29 October 2022).

- Elliott, S. UK Government Denies Report It Asked Qatar for Additional LNG Supplies; S&P Global: New York, NY, USA, 2021. [Google Scholar]

- Qatar to Raise LNG Production by 64% to 126 Mtpa by 2027. Available online: https://thepeninsulaqatar.com/article/25/11/2019/Qatar-to-raise-LNG-production-by-64-to-126-mtpa-by-2027 (accessed on 29 October 2022).

- Zarzecki, D. Development of the LNG Terminal in Świnoujście, Poland. Futur. Energy Consum. Secur. Nat. Gas 2022, 30, 191–220. [Google Scholar] [CrossRef]

- Zaretskaya, V.; Peterson, W.W.C. Three countries provided almost 70% of liquefied natural gas received in Europe in 2021. Today Energy 2022, 2, 1–62. [Google Scholar]

- Miller, R. Qatar, Energy Security, and Strategic Vision in a Small State. J. Arab. Stud. 2020, 10, 122–138. [Google Scholar] [CrossRef]

- Wright, S. Qatar’s LNG: Impact of the changing east-asian market. Middle East. Policy 2017, 24, 154–165. [Google Scholar] [CrossRef]

- North Field. QatarGas. 2022. Available online: https://www.qatargas.com/english/aboutus/north-field (accessed on 4 September 2022).

- QatarGas. The Trains. 2022. Available online: https://www.qatargas.com/english/operations/lng-trains (accessed on 4 September 2022).

- EU Gas Diversification Could Bring Longer-Term Benefits For Qatar. Energy Connect 2022. Available online: https://www.energyconnects.com/opinion/thought-leadership/2022/march/eu-gas-diversification-could-bring-longer-term-benefits-for-qatar/ (accessed on 4 September 2022).

- Nikolay, K. Qatar is no short-term savior, but it may still play a role in strengthening EU energy security. Middle East. Inst. 2022. Available online: https://www.mei.edu/publications/qatar-no-short-term-savior-it-may-still-play-role-strengthening-eu-energy-security (accessed on 7 February 2022).

- IGU. World LNG Report; IGU: Barcelona, Spain, 2021. [Google Scholar]

- King & Spalding. An Overview of LNG Import Terminals in Europe; King & Spalding: Atlanta, GA, USA, 2018. [Google Scholar]

- Kahramaa. Statistic Report 2019; Kahramaa: Doha, Qatar, 2021. [Google Scholar]

- Worldometer. Qatar Electricity. 2022. Available online: https://www.worldometers.info/electricity/qatar-electricity/ (accessed on 29 October 2022).

- IGU. Natural Gas Conversion Pocketbook; IGU: Oslo, Norway, 2012. [Google Scholar]

- Zafar, S. Solar Energy in Qatar; EcoMENA: Riyadh, Saudi Arabia, 2021. [Google Scholar]

- Méndez, C.; Bicer, Y. Assessment of wind energy potential and characteristics in Qatar for clean electricity generation. Wind. Eng. 2022, 46, 598–614. [Google Scholar] [CrossRef]

- Knoema. Qatar—CO2 Emissions. 2018. Available online: https://knoema.com/atlas/Qatar/CO2-emissions (accessed on 8 September 2022).

- National Academies Press. The Hydrogen Economy; National Academies Press: Washington, DC, USA, 2004. [Google Scholar] [CrossRef]

- Zeal, T. Are LNG liquefaction projects taking longer to construct? IGT Int. Liq. Nat. Gas Conf. Proc. 2019, 1, 331–343. [Google Scholar]

- Elliott, S. Croatia Eyes Expansion of Floating LNG Import Terminal, Slovenia Supply Option; S&P Global: New York, NY, USA, 2022. [Google Scholar]

- Al-Haidous, S.; Govindan, R.; Elomri, A.; Al-Ansari, T. An optimization approach to increasing sustainability and enhancing resilience against environmental constraints in LNG supply chains: A Qatar case study. Energy Rep. 2022, 8, 9742–9756. [Google Scholar] [CrossRef]

- Vivoda, V. LNG export diversification and demand security: A comparative study of major exporters. Energy Policy 2022, 170, 113218. [Google Scholar] [CrossRef]

- Babonneau, F.; Benlahrech, M.; Haurie, A. Transition to zero-net emissions for Qatar: A policy based on Hydrogen and CO2 capture & storage development. Energy Policy 2022, 170, 113256. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Problems | Source |

|---|---|

| The volume of gas supply by Russia to Europe is large, and the gas transfer via pipelines is stopped | [30] |

| Qatar’s commitments to supply gas to customers | [31] |

| Qatari gas is mostly marketed to Asian purchasers under long-term contracts, leaving little room for quota increases. Qatar has no intention of jeopardizing its position as a dependable supplier by breaching or renegotiating its long-term contracts, which Qatar regards as essential. | [22] |

| Qatari contracts are extremely restrictive, prohibiting LNG shipments from being diverted to foreign countries or resold. | [32] |

| Limited available capacity by European terminals to absorb the extra supply of LNG | [29] |

| Asset | Number of Trains Per Asset | Train Capacity (Mtpa) | LNG Capacity Per Asset (Mtpa) | Major Equity Owners |

|---|---|---|---|---|

| RL1 | 2 | 3.3 | 6.6 | QP (63%), XOM (25%) |

| RL2 | 3 | 4.7 | 14.1 | QP (67%), XOM (31%) |

| RL3 | 2 | 7.8 | 15.6 | QP (70%), XOM (30%) |

| QG1 | 3 | 3.3 | 10.0 | QP (65%), XOM (10%), TOT (10%) |

| QG2 | 2 | 7.8 | 15.6 | QP (70%), XOM (30%) QP (65%), XOM (16.7%), TOT (16.7%) |

| QG3 | 1 | 7.8 | 7.8 | QP (68.5%), COP (30%) |

| QG4 | 1 | 7.8 | 7.8 | QP (70%), RDS (30%) |

| RL1 | 2 | 3.3 | 6.6 | QP (63%), XOM (25%) |

| From | To | LNG Quantities Sold on a Long-Term Contract (BCM) | LNG Quantities Sold on a Spot and on a Short-Term Contract (BCM) |

|---|---|---|---|

| Qatar | Asia | 72.2 | 10.1 |

| Europe | 30.2 | 3.8 | |

| Americas | 0.86 | 0.001 | |

| The Middle East and Africa | 3.23 | 0.004 |

| Country | Terminal | Send-Out Capacity (BCM/year) |

|---|---|---|

| Belgium | Zeebrugge | 12 |

| France | Dunkerque | 13 |

| Fos Cavaou | 16.5 | |

| Fos Tonkin | 3.4 | |

| Montoir-De-Bretagne | 10 | |

| Greece | Revithoussa | 8.25 |

| Italy | La Spezia | 8 |

| Olt Offshore LNG Toscana | 3.75 | |

| Porto Levante | 8 | |

| Lithuania | Klaipėdos | 4 |

| The Netherlands | Gate | 16 |

| Poland | Świnoujście LNG | 7.5 |

| Malta | Delimara | 0.7 |

| Portugal | Sines—Ren Atlântico | 7.6 |

| Spain | Barcelona | 17.1 |

| Cartagena | 11.8 | |

| Huelva | 11.8 | |

| Bilbao Bahía De Bizkaia | 8.8 | |

| Sagunto | 8.8 | |

| Mugardos El Ferrol | 7.2 | |

| El Musel—Gijon | 8.8 | |

| Turkey | Aliaga | 6.2 |

| Marmara Ereglisi | 6.2 | |

| Aliaga | 5.3 | |

| Dörtyol | 11 | |

| United Kingdom | Grain Lng | 27.5 |

| South Hook LNG | 21 | |

| Dragon LNG | 7.6 | |

| Total | 28 terminals | 277.8 |

| Export Country | Seller | Buyer | Amount (BCM) | Duration |

|---|---|---|---|---|

| Qatar | QG 1 | Naturgy Energy Group | 1 | 2005/2024 |

| QG 1 | Naturgy Energy Group | 1 | 2006/2025 | |

| QG 3 | RWE Supply & Trading | 1.5 | 2016/2023 | |

| QG 5 | Centrica | 4.2 | 2014/2023 | |

| QG 5 | Petronas | 1.6 | 2014/2023 | |

| QG 5 | Shell | 1.5 | 2019/2023 | |

| QG 1 | Endesa | 1 | 2005/2025 | |

| RL 3 | KOGAS | 2.8 | 2007/2026 | |

| Total | 14.6 |

| Country | Terminal | Initial Capacity (BCM/year) |

|---|---|---|

| Albania | Eagle LNG FSRU | 8 |

| Croatia | Krk Island FSRU | 2 |

| Estonia | Padalski LNG | 2.5 |

| Estonia | Muuga (Tallinn) LNG | 4 |

| Germany | Brunsbüttel LNG | 5 |

| Ireland | Shannon LNG | 2.7 |

| Latvia | Riga LNG Terminal | 5 |

| Romania | Constanta LNG | 8 |

| Ukraine | Odessa LNG | 5 |

| Greece | Gastrade | 6.1 |

| Italy | Porto Empedocle | 8 |

| Total | 13 | 56.3 |

| This Study | Other Studies |

|---|---|

Problems:

Solutions:

| Study 1 [48] Problems:

Solutions:

|

| Study 2 [49] Problems:

Solutions:

| |

| Study 3 [50] Problems:

Solutions:

|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Al-Breiki, M.; Bicer, Y. Potential Solutions for the Short to Medium-Term Natural Gas Shortage Issues of Europe: What Can Qatar Do? Energies 2022, 15, 8306. https://doi.org/10.3390/en15218306

Al-Breiki M, Bicer Y. Potential Solutions for the Short to Medium-Term Natural Gas Shortage Issues of Europe: What Can Qatar Do? Energies. 2022; 15(21):8306. https://doi.org/10.3390/en15218306

Chicago/Turabian StyleAl-Breiki, Mohammed, and Yusuf Bicer. 2022. "Potential Solutions for the Short to Medium-Term Natural Gas Shortage Issues of Europe: What Can Qatar Do?" Energies 15, no. 21: 8306. https://doi.org/10.3390/en15218306

APA StyleAl-Breiki, M., & Bicer, Y. (2022). Potential Solutions for the Short to Medium-Term Natural Gas Shortage Issues of Europe: What Can Qatar Do? Energies, 15(21), 8306. https://doi.org/10.3390/en15218306