Pathways to Overcoming Natural Gas Dependency on Russia—The German Case

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Natural Gas in the German Economy

2.1. Energy Mix and Consumption

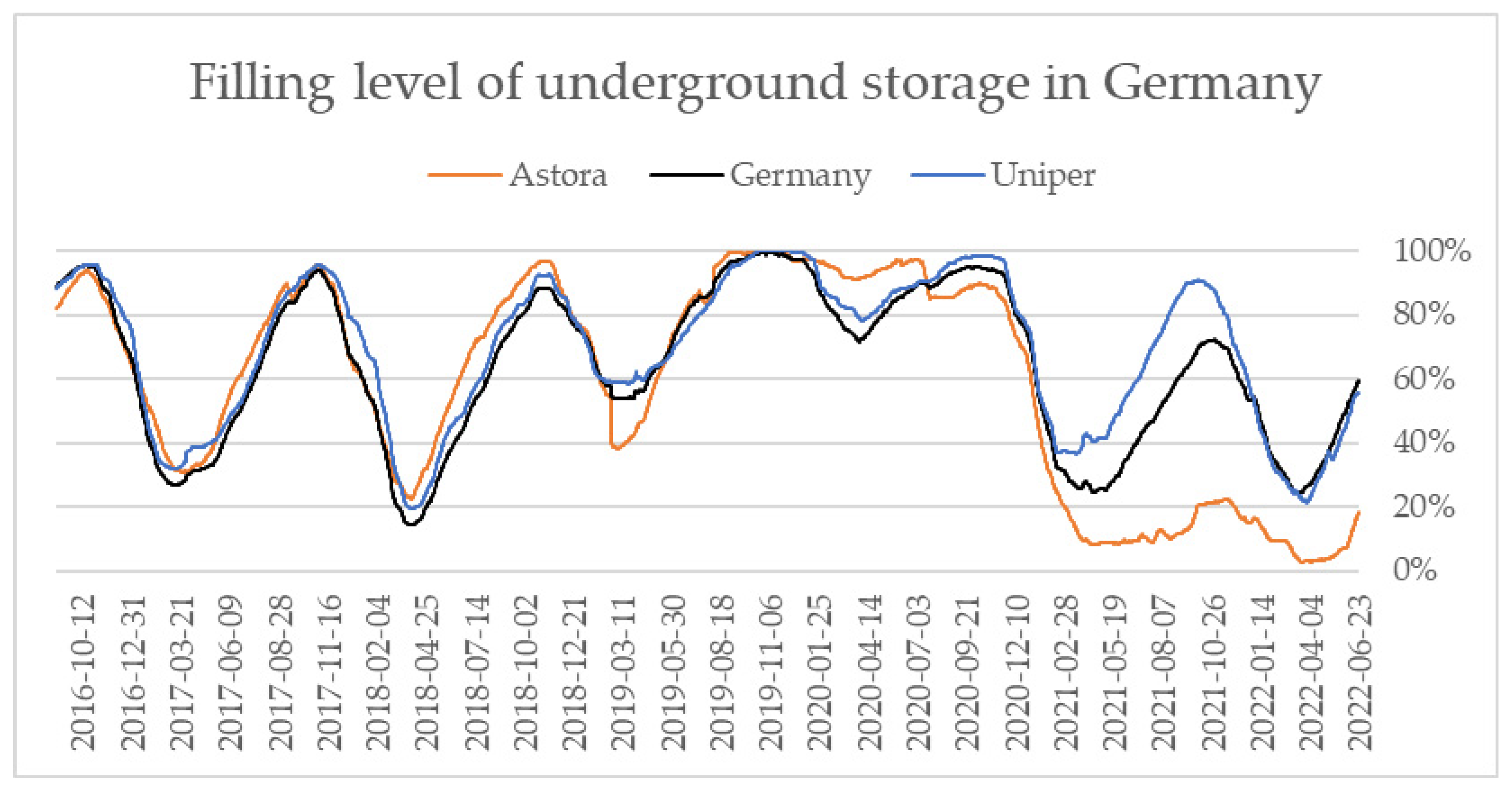

2.2. Import Flows and Storage

3. Developments Surrounding the War in Ukraine

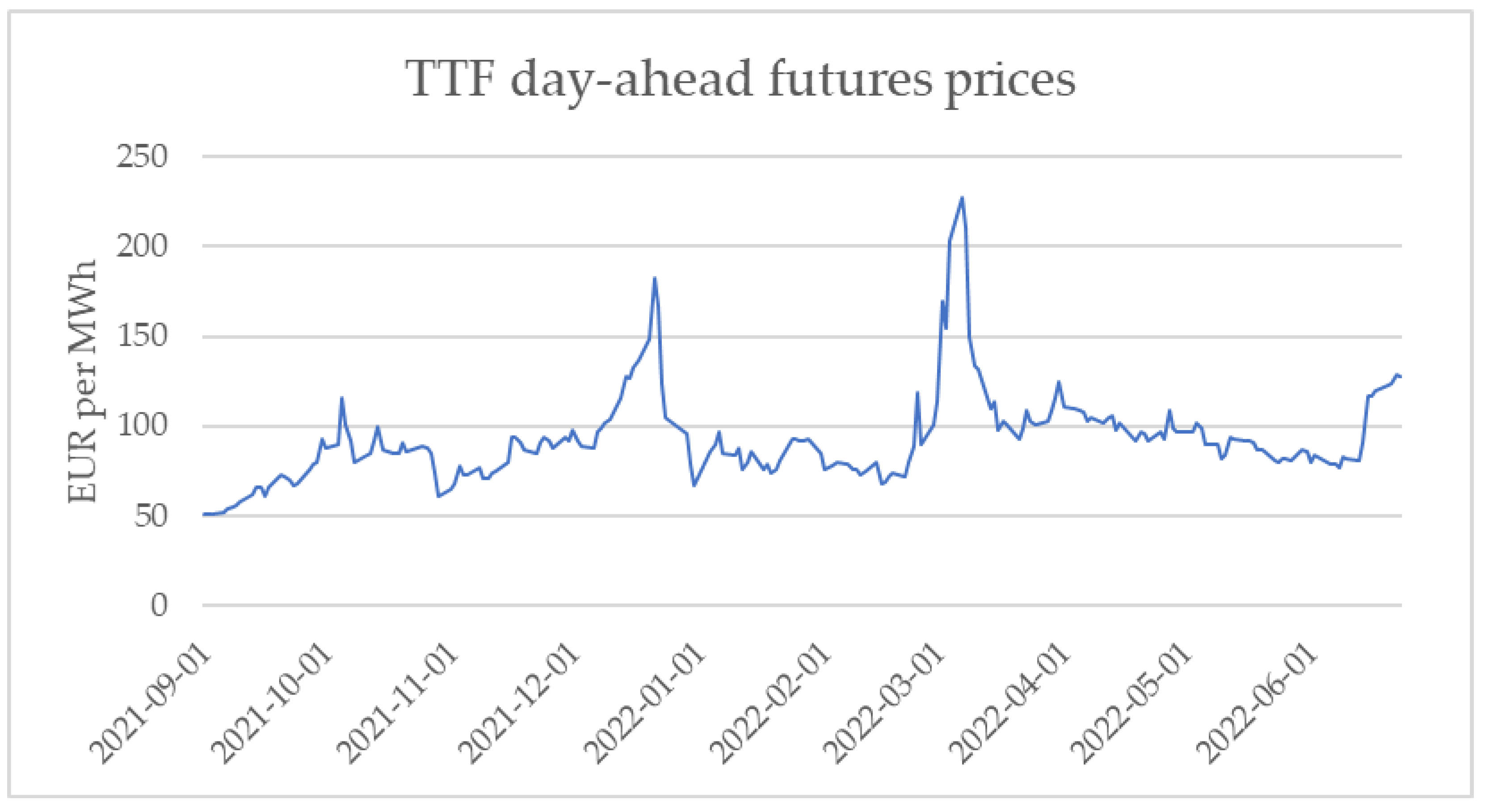

3.1. Market Developments and Gas Flows 2021–2022

3.2. The Regulatory Response of Germany and the EU

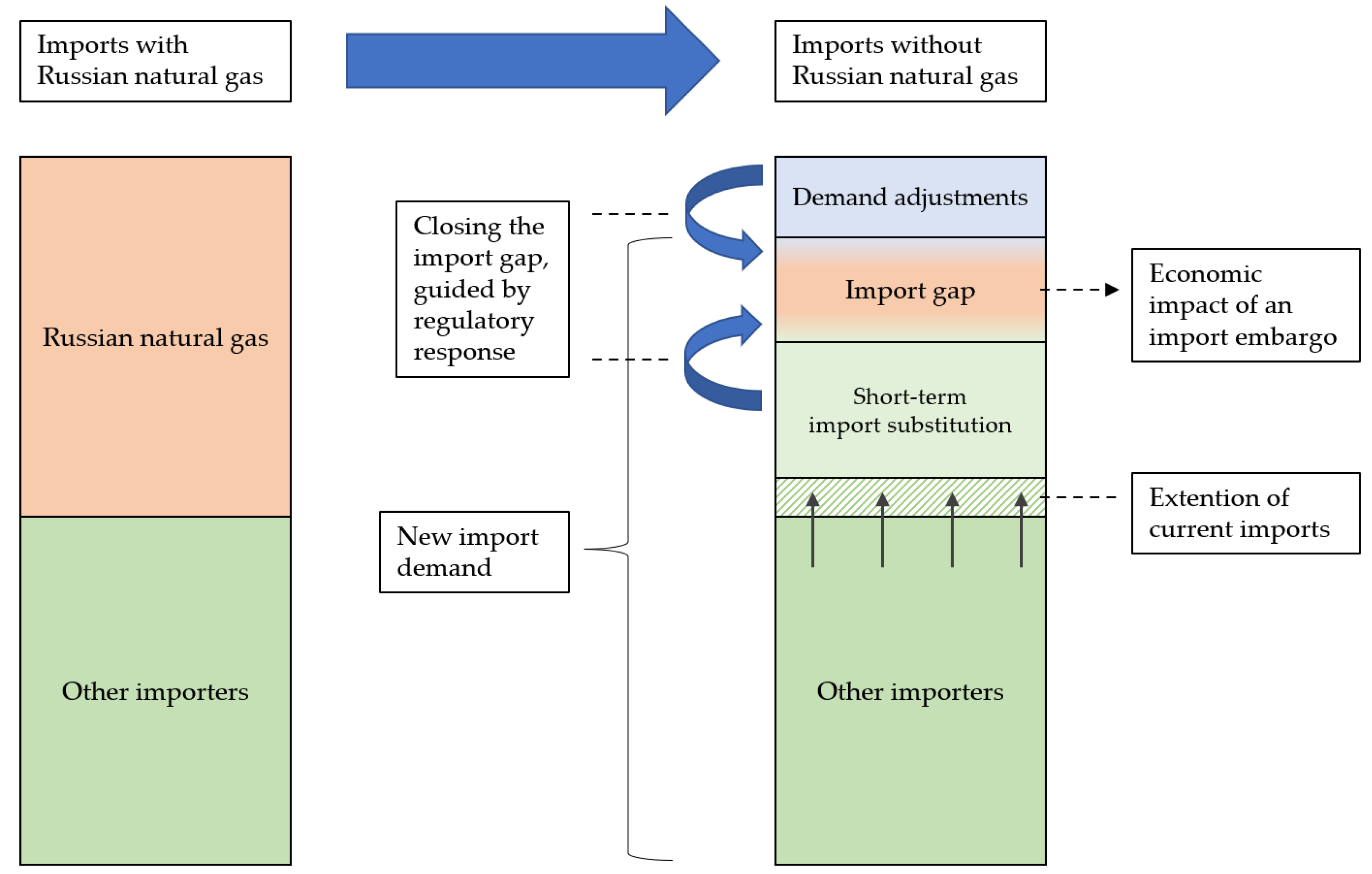

4. Economic Impact of an Import Embargo

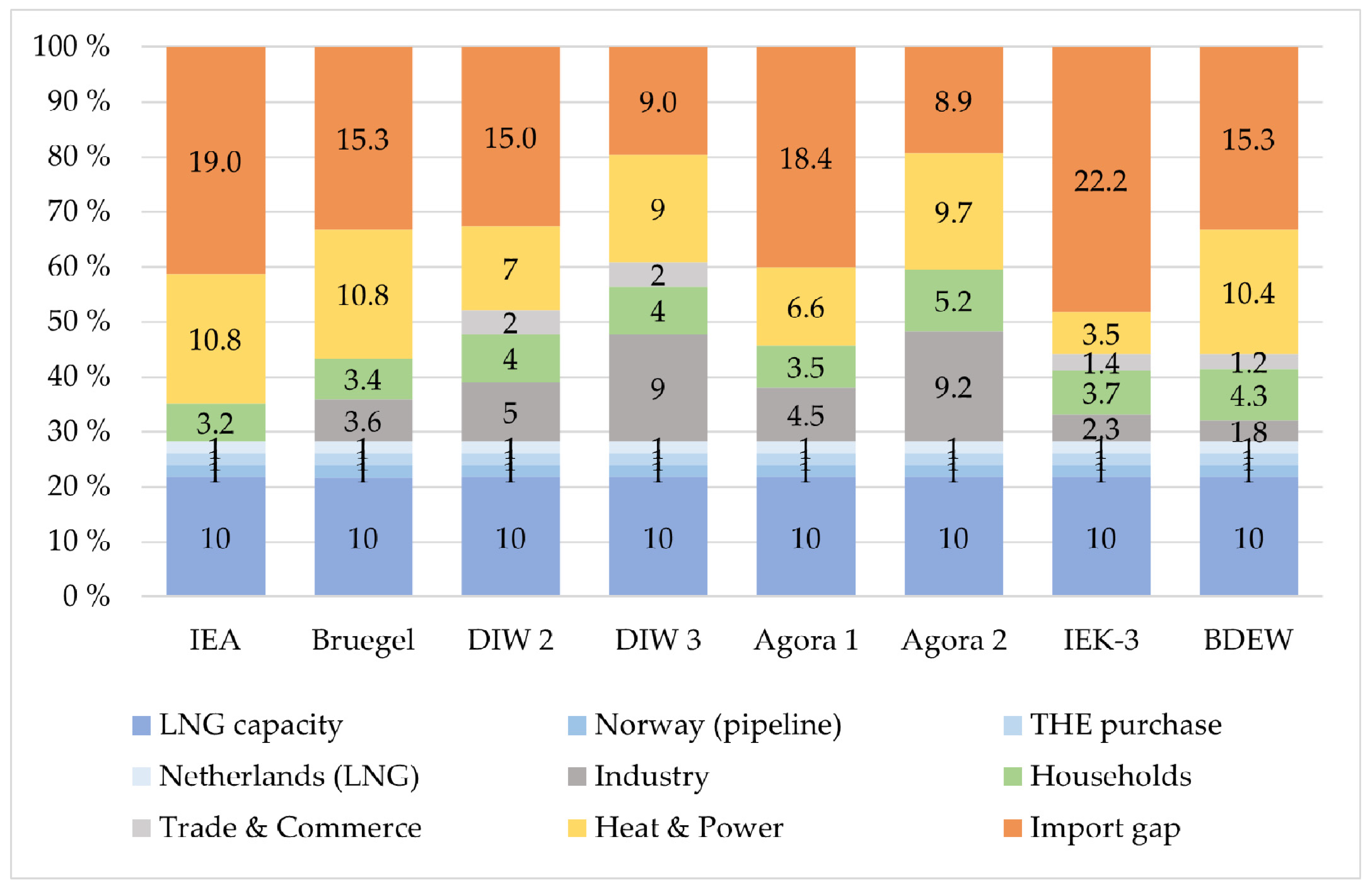

5. Strategies to Replace Natural Gas from Russia

5.1. Short-Term Supply Substitution Potential

5.2. Potential of Short-Term Demand Reductions

6. Lessons for Other European Countries

6.1. Differences in Dependence and Market Structure

6.2. Crisis Responses and Challenges

7. Discussion

8. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- BMWK. Second Energy Security Progress Report; BMWK: Berlin, Germany, 2022. [Google Scholar]

- BP Statistical Review of World Energy 2021 (Internet). BP p.l.c. 2021 (Cited London). Available online: https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2021-full-report.pdf (accessed on 8 May 2022).

- BMWK. Energy Security Progress Report; BMWK: Berlin, Germany, 2021. [Google Scholar]

- EIA. Carbon Dioxide Emissions Coefficients; U.S. Energy Information Agency: Washington, DC, USA, 2022. [Google Scholar]

- Financial Stability, Financial Services and Capital Markets Union. EU Taxonomy: Commission Presents Complementary Climate Delegated Act to Accelerate Decarbonisation (Press Release); Publications Office of the European Union: Luxembourg, 2022. [Google Scholar]

- AGEB. Energieverbrauch in Deutschland. Daten Für Das 1. Bis 4. Quartal 2021: AG Energiebilanzen e.V.; 2022. Available online: https://ag-energiebilanzen.de/wp-content/uploads/2022/01/quartalsbericht_q4_2021.pdf (accessed on 9 May 2022).

- Fraunhofer ISE. Erstellung von Anwendungsbilanzen für die Jahre 2018 Bis 2020 für die Sektoren Industrie und GHD; Fraunhofer ISE Research Institute: Freiburg im Breisgau, Germany, 2021. [Google Scholar]

- BDEW. Kurzfristige Substitutions—und Einsparpotenziale Erdgas in Deutschland; BDEW: Berlin, Germany, 2022. [Google Scholar]

- Weyerstrass, K.; Fortin, I.; Grozea-Helmenstein, D.; Koch, S.P.; Gemeinschaftsdiagnose, P. Von der Pandemie zur Energiekrise—Wirtschaft und Politik im Dauerstress. Gemeinschaftsdiagnose Frühjahr 2022; Institute for Advanced Studies (IHS): Vienna, Austria, 2022. [Google Scholar]

- Bachmann, R.; Baqaee, D.; Bayer, C.; Kuhn, M.; Löschel, A.; Moll, B.; Peichl, A.; Pittel, K.; Schularick, M. What if? The Economic Effects for Germany of a Stop of Energy Imports from Russia; Ifo Institute-Leibniz Institute for Economic Research at the University of Munich: Munich, Germany, 2022. [Google Scholar]

- Refinitiv. TRNLTTFD1; Refinitiv Eikon: New York, NY, USA, 2022. [Google Scholar]

- Winzer, C. Conceptualizing energy security. Energy Policy 2012, 46, 36–48. [Google Scholar] [CrossRef] [Green Version]

- Azzuni, A.; Breyer, C. Definitions and dimensions of energy security: A literature review. Wiley Interdiscip. Rev. Energy Environ. 2018, 7, e268. [Google Scholar] [CrossRef]

- Ang, B.W.; Choong, W.L.; Ng, T.S. Energy security: Definitions, dimensions and indexes. Renew. Sustain. Energy Rev. 2015, 42, 1077–1093. [Google Scholar] [CrossRef]

- Månsson, A.; Johansson, B.; Nilsson, L.J. Assessing energy security: An overview of commonly used methodologies. Energy 2014, 73, 1–14. [Google Scholar] [CrossRef] [Green Version]

- Chalvatzis, K.J.; Ioannidis, A. Energy supply security in the EU: Benchmarking diversity and dependence of primary energy. Appl. Energy 2017, 207, 465–476. [Google Scholar] [CrossRef]

- Blondeel, M.; Bradshaw, M.J.; Bridge, G.; Kuzemko, C. The geopolitics of energy system transformation: A review. Geogr. Compass 2021, 15, e12580. [Google Scholar] [CrossRef]

- IEA. Energy Security and Climate Change—Assessing Interactions; International Energy Agency: Paris, France, 2007. [Google Scholar]

- Scheepers, M.; Seebregts, A.; De Jong, J.; Maters, J. EU Standards for Security of Supply; Energy Research Center (ECN)/Clingendael International Energy Programme: Hague, The Netherlands, 2007. [Google Scholar]

- Jansen, J.C.; Arkel, W.V.; Boots, M.G. Designing Indicators of Long-Term Energy Supply Security; Energy research Centre of the Netherlands ECN Westerduinweg: Sint Maartensvlotbrug, The Netherlands, 2004. [Google Scholar]

- Intharak, N.; Julay, J.H.; Nakanishi, S.; Matsumoto, T.; Sahid, E.J.M.; Aquino, A.G.O.; Aponte, A.A. A Quest for Energy Security in the 21st Century; Asia Pacific Energy Research Centre Report: Tokyo, Japan, 2007. [Google Scholar]

- Kruyt, B.; Van Vuuren, D.P.; de Vries, H.J.; Groenenberg, H. Indicators for energy security. Energy Policy 2009, 37, 2166–2181. [Google Scholar] [CrossRef]

- IEA. Energy Security; International Energy Agency: Paris, France, 2019. [Google Scholar]

- Grigas, A. The New Geopolitics of Natural Gas; Harvard University Press: Cambridge, MA, USA, 2017. [Google Scholar]

- Lilliestam, J.; Ellenbeck, S. Energy security and renewable electricity trade—Will Desertec make Europe vulnerable to the “energy weapon”? Energy Policy 2011, 39, 3380–3391. [Google Scholar] [CrossRef]

- Stegen, K.S. Deconstructing the “energy weapon”: Russia’s threat to Europe as case study. Energy Policy 2011, 39, 6505–6513. [Google Scholar] [CrossRef]

- Ranjan, A.; Hughes, L. Energy security and the diversity of energy flows in an energy system. Energy 2014, 73, 137–144. [Google Scholar] [CrossRef]

- De Rosa, M.; Gainsford, K.; Pallonetto, F.; Finn, D.P. Diversification, concentration and renewability of the energy supply in the European Union. Energy 2022, 253, 124097. [Google Scholar] [CrossRef]

- Jewell, J.; Cherp, A.; Riahi, K. Energy security under de-carbonization scenarios: An assessment framework and evaluation under different technology and policy choices. Energy Policy 2014, 65, 743–760. [Google Scholar] [CrossRef]

- Lesbirel, S.H. Diversification and energy security risks: The Japanese case. Jpn. J. Polit. Sci. 2004, 5, 1–22. [Google Scholar] [CrossRef]

- Martišauskas, L.; Augutis, J.; Krikštolaitis, R. Methodology for energy security assessment considering energy system resilience to disruptions. Energy Strategy Rev. 2018, 22, 106–118. [Google Scholar] [CrossRef]

- Pavlović, D.; Banovac, E.; Vištica, N. Defining a composite index for measuring natural gas supply security—The Croatian gas market case. Energy Policy 2018, 114, 30–38. [Google Scholar] [CrossRef]

- Kong, Z.; Lu, X.; Jiang, Q.; Dong, X.; Liu, G.; Elbot, N.; Zhang, Z.; Chen, S. Assessment of import risks for natural gas and its implication for optimal importing strategies: A case study of China. Energy Policy 2019, 127, 11–18. [Google Scholar] [CrossRef]

- Gong, C.; Gong, N.; Qi, R.; Yu, S. Assessment of natural gas supply security in Asia Pacific: Composite indicators with compromise Benefit-of-the-Doubt weights. Resour. Policy 2020, 67, 101671. [Google Scholar] [CrossRef]

- Gasser, P. A review on energy security indices to compare country performances. Energy Policy 2020, 139, 111339. [Google Scholar] [CrossRef]

- BMWK. Energiedaten: Gesamtausgabe; BMWK: Berlin, Germany, 2022. [Google Scholar]

- Erdgasstatistik (Internet). Federal Office for Economic Affairs and Export Control. 2022. Available online: https://www.bafa.de/DE/Energie/Rohstoffe/Erdgasstatistik/erdgas_node.html (accessed on 6 May 2022).

- EU Natural Gas Import Dependency Down to 83% in 2021 (Internet). Publications Office of the European Union. 2022. Available online: https://ec.europa.eu/eurostat/web/products-eurostat-news/-/ddn-20220419-1 (accessed on 19 April 2022).

- AGEB. Energieverbrauch in Deutschland im Jahr 2021. Energieverbrauch 2021 Wächst Durch Pandemie und Wetter AG Energiebilanzen e.V.; 2022. Available online: https://ag-energiebilanzen.de/wp-content/uploads/2022/04/AGEB_Jahresbericht2021_20220425_dt.pdf (accessed on 10 May 2022).

- BDEW. Monatlicher Erdgasverbrauch in Deutschland 2022—Vorjahresvergleich; BDEW: Berlin, Germany, 2022. [Google Scholar]

- IEK-3 FJ. Wie Sicher Ist Die Energieversorgung Ohne Russisches Erdgas? IEK-3: Jülich, Germany, 2022. [Google Scholar]

- Müller, S.; Peter, F.; Saerbeck, B.; Burmeister, H.; Heilmann, F.; Langenheld, A.; Lenck, T.; Metz, J.; Müller, S.; Peter, F.; et al. Energiesicherheit und Klimaschutz Vereinen—Maßnahmen für den Weg aus der Fossilen Energiekrise. Impuls; Agora Energiewende: Berlin, Germany, 2022. [Google Scholar]

- BMWK. Instrumente zur Sicherung der Gasversorgung; BMWK: Berlin, Germany, 2019. [Google Scholar]

- AGSI. Aggregated Gas Storage Inventory; Gas Infrastructure Europe (GIE): Brussels, Belgium, 2022. [Google Scholar]

- Natural Gas Supply Statistics (Internet). Publications Office of the European Union. 2022. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Natural_gas_supply_statistics#Supply_structure (accessed on 23 May 2022).

- Thompson, G. Asia’s Demand Engine Fires up Global LNG Supply: Wood Mackenzie; 2022. Available online: https://www.woodmac.com/news/opinion/asias-demand-engine-fires-up-global-lng-supply/ (accessed on 2 December 2021).

- Fraunhofer ISE. Annual Total Electricity Generation in Germany; Fraunhofer ISE Research Institute: Freiburg im Breisgau, Germany, 2022. [Google Scholar]

- Taylor, K.; Noyan, O. Stop Financing Putin’s War with Energy Imports, Ukrainian NGO Pleads, Euractiv. 2022. Available online: https://www.euractiv.com/section/energy/news/stop-financing-putins-war-with-energy-imports-ukrainian-ngo-pleads/ (accessed on 3 March 2022).

- Refinitiv. EURRUB=X; Refinitiv Eikon: New York, NY, USA, 2022. [Google Scholar]

- Reuters. Russian Inflation Jumps to 17.83% in April, Highest since Early 2002; Reuters: London, UK, 2022. [Google Scholar]

- Deutsche Welle. Gazprom to Further Cut Gas Supplies to Germany via Nord Stream; DW: Bonn, Germany, 2022. [Google Scholar]

- Zachmann, G.; Sgaravatti, G.M.B. European Natural Gas Imports; Bruegel Datasets: Brussels, Belgium, 2022. [Google Scholar]

- Delfs, A. Germany Says Latest Russian Gas-Flow Cuts Politically Motivated: Bloomberg. 2022. Available online: https://www.bloomberg.com/news/articles/2022-06-15/germany-says-latest-russian-gas-flow-cuts-politically-motivated (accessed on 15 June 2022).

- BMWK. Bundesministerium für Wirtschaft und Klimaschutz ruft Frühwarnstufe des Notfallplans Gas aus—Versorgungssicherheit weiterhin gewährleistet (Press Release); Federal Ministry for Economic Affairs and Climate Action (BMWK): Berlin, Germany, 2022. [Google Scholar]

- BMWK. Bundesministerium für Wirtschaft und Klimaschutz ruft Alarmstufe des Notfallplans Gas aus—Versorgungssicherheit weiterhin gewährleistet (Press Release); Federal Ministry for Economic Affairs and Climate Action (BMWK): Berlin, Germany, 2022. [Google Scholar]

- BMWK. FAQ Liste—Notfallplan Gas; BMWK: Berlin, Germany, 2022. [Google Scholar]

- Publications Office of the European Union. Press Statement by President von der Leyen on the Commission’s Proposals Regarding REPowerEU, Defence Investment Gaps and the Relief and Reconstruction of Ukraine (Press Release); Publications Office of the European Union: Luxembourg, 2022. [Google Scholar]

- European Commission. Factsheet on Gas Storage Proposal. Refilling Gas Storage for Next Winter; European Commission: Brussels, Belgium, 2022. [Google Scholar]

- Deutscher Bundestag. Entwurf eines Gesetzes zur Änderung des Energiewirtschaftsgesetzes zur Einführung von Füllstandsvorgaben für Gasspeicheranlagen. In Gesetzentwurf der Fraktionen SPD, BÜNDNIS 90/DIE GRÜNEN und FDP; Bundestag, D., Ed.; Deutscher Bundestag: Berlin, Germany, 2022. [Google Scholar]

- Handelsblatt. Bundestag Beschließt Mögliche Enteignung. von Energiefirmen; Handelsblatt: Berlin, Germany, 2022. [Google Scholar]

- WirtschaftsWoche. Österreich Droht Gazprom Wegen Nichtbefülltem Gasspeicher; WirtschaftsWoche: Dusseldorf, Germany, 2022. [Google Scholar]

- WirtschaftsWoche. Moskau Verbietet Geschäfte Mit Ehemaligen Gazprom-Töchtern im Ausland; WirtschaftsWoche: Dusseldorf, Germany, 2022. [Google Scholar]

- Krukowska, E.; Nardelli, A. EU Drafts Plan for Buying Russian Gas without Breaking Sanctions: Bloomberg. 2022. Available online: https://www.bloomberg.com/news/articles/2022-05-14/eu-drafts-plan-for-buying-russian-gas-without-breaking-sanctions (accessed on 14 May 2022).

- Tagesschau. Norwegen will Mehr Erdgas Liefern; Tagesschau: Hamburg, Germany, 2022. [Google Scholar]

- Bundesnetzagentur. Aktuelle Lage der Gasversorgung in Deutschland; Bundesnetzagentur: Berlin, Germany, 2022. [Google Scholar]

- Handelsblatt. Finanzminister Lindner Bewilligt drei Milliarden Euro für Schwimmende LNG Terminals; Handelsblatt: Berlin, Germany, 2022. [Google Scholar]

- S&P Global. Germany Sees Russian Gas Share Falling to 10% by Mid-2024 Amid Floating LNG Rush 2022. Available online: https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/electric-power/050322-germany-sees-russian-gas-share-falling-to-10-by-mid-2024-amid-floating-lng-rush (accessed on 3 May 2022).

- Deutscher Bundestag. Beschleunigung des Einsatzes von Flüssiggas Beschlossen; Bundestag, D., Ed.; Deutscher Bundestag: Berlin, Germany, 2022. [Google Scholar]

- Reuters. Factbox: Germany’s LNG Import Project Plans; Reuters: London, UK, 2022. [Google Scholar]

- LNG Database. Gas Infrastructure Europe. 2022. Available online: https://www.gie.eu/transparency/databases/lng-database/ (accessed on 25 April 2022).

- Fabian, J.; Wingrove, J.; Krukowska, E.U.S. EU Reach LNG Supply Deal to Cut Dependence on Russia: Bloomberg. 2022. Available online: https://www.bloomberg.com/news/articles/2022-03-25/u-s-and-eu-reach-energy-supply-deal-to-cut-dependence-on-russia (accessed on 25 March 2022).

- Chapa, S.; Paulsson, L. What LNG Can and Can’t Do to Replace Europe’s Imports of Russian Gas: Bloomberg. 2022. Available online: https://www.bloomberg.com/news/articles/2022-03-11/what-lng-can-and-can-t-do-to-replace-russian-gas-quicktake (accessed on 11 March 2022).

- Krauss, C. Why the U.S. Can’t Quickly Wean Europe from Russian Gas: The New York Times. 2022. Available online: https://www.nytimes.com/2022/03/25/business/energy-environment/biden-europe-lng-natural-gas.html (accessed on 26 March 2022).

- Baqaee, D.; Farhi, E. Networks, Barriers, and Trade; National Bureau of Economic Research: Cambridge, MA, USA, 2019. [Google Scholar]

- Baqaee, D.; Moll, B.; Landais, C.; Martin, P. The Economic Consequences of a Stop of Energy Imports from Russia; CAE Focus No 084-2022; CAE: Paris, France, 2022. [Google Scholar]

- Bayer, C.; Kriwoluzky, A.; Seyrich, F. Stopp Russischer Energieeinfuhren Würde Deutsche Wirtschaft Spürbar Treffen, Fiskalpolitik Wäre in der Verantwortung; Deutsches Institut für Wirtschaftsforschung (DIW): Berlin, Germany, 2022. [Google Scholar]

- Krebs, T. Auswirkungen Eines Erdgasembargos Auf Die Gesamtwirtschaftliche Produktion in Deutschland; Hans-Böckler-Stiftung: Düsseldorf, Germany, 2022. [Google Scholar]

- Acemoglu, D.; Carvalho, V.M.; Ozdaglar, A.; Tahbaz-Salehi, A. The network origins of aggregate fluctuations. Econometrica 2012, 80, 1977–2016. [Google Scholar] [CrossRef] [Green Version]

- Carvalho, V.M.; Tahbaz-Salehi, A. Production networks: A primer. Annu. Rev. Econ. 2019, 11, 635–663. [Google Scholar] [CrossRef] [Green Version]

- Bundesbank. Zu den Möglichen Gesamtwirtschaftlichen Folgen des Ukrainekriegs: Simulationsrechnungen zu Einem Verschärften Risikoszenario. Monatsbericht. 15; Deutsche Bundesbank: Berlin, Germany, 2022. [Google Scholar]

- Behringer, J.; Dullien, S.; Herzog-Stein, A.; Hohlfeld, P.; Rietzler, K.; Stephan, S.; Theobald, T.; Tober, S. Ukraine-Krieg erschwert Erholung nach Pandemie; IMK Report; Institut für Makroökonomie und Konjunkturforschung: Düsseldorf, Germany, 2022; p. 174. [Google Scholar]

- Goldman Sachs. Global Views: Where Russia Matters Most; Global Views: Dallas, TX, USA, 2022. [Google Scholar]

- Giehl, J.; Verwiebe, P.; Evers, M.; Schulz, L.; Joachim, M.-K. Analyse Möglicher Maßnahmen zur Reduktion der Erdgasimporte aus Russland. Berlin: Fachgebiet Energie- und Ressourcenmanagement; Technische Universität Berlin: Berlin, Germany, 2022. [Google Scholar]

- Shiryaevskaya, A. How Germany’s LNG Terminals Will Morph into Green Hydrogen Hubs: Bloomberg. 2022. Available online: https://www.bloomberg.com/news/articles/2022-05-12/how-to-turn-lng-terminals-into-green-hydrogen-hubs (accessed on 12 May 2022).

- BMWK. Habeck Presents Second Energy Security Progress Report—Dependence on Russian Energy Imports down Further. (Press Release); Federal Ministry for Economic Affairs and Climate Action: Berlin, Germany, 2022. [Google Scholar]

- IEA. A 10-Point Plan to Reduce the European Union’s Reliance on Russian Natural Gas; International Energy Agency: Paris, France, 2022. [Google Scholar]

- Zachmann, G.; Sgaravatti, G.M.; Tagliapietra, S.B. Preparing for the First Winter without Russian Gas; Bruegel: Brussels, Belgium, 2022. [Google Scholar]

- Holz, F.; Sogalla, R.; von Hirschhausen, C.R.; Kemfert, C. Energieversorgung in Deutschland Auch Ohne Erdgas aus Russland Gesichert. DIW Aktuell. 83; Deutsches Institut für Wirtschaftsforschung (DIW): Berlin, Germany, 2022. [Google Scholar]

- Pécout, A. How France Is Preparing for a Possible Suspension of Russian Gas Imports; Le Monde: Paris, France, 2022. [Google Scholar]

- Ritchie, H.; Roser, M.; Rosado, P. Energy, Country Profiles: Our World in Data. 2022. Available online: https://ourworldindata.org/energy (accessed on 17 June 2022).

- Stratmann, K. Niederländer Wollen Gasförderung Steigern und Fordern Das Auch von Deutschland; Handelsblatt: Düsseldorf, Germany, 2022. [Google Scholar]

- Der Spiegel. Gaslieferungen Nach Frankreich Kommen zum Erliegen; Der Spiegel: Hamburg, Germany, 2022. [Google Scholar]

- Albanese, C.; Brambilla, A. Italy Signs Gas Deals in Angola, Congo to Cut Russia Ties: Bloomberg. 2022. Available online: https://www.bloomberg.com/news/articles/2022-04-20/italy-snaps-up-angolan-gas-after-deals-for-north-african-supply (accessed on 20 April 2022).

- Kombrink, H. Germany in Favour of Cross-Border Gas Development: Expronews. 2022. Available online: https://expronews.com/developmentandproduction/germany-in-favour-of-cross-border-gas-development/?utm_source=rss&utm_medium=rss&utm_campaign=germany-in-favour-of-cross-border-gas-development (accessed on 21 April 2022).

- Reuters. Spain’s Gas Imports Rise 16% Driven by Seaborne LNG Purchases; Reuters: London, UK, 2022. [Google Scholar]

- Burke, P.J.; Yang, H. The price and income elasticities of natural gas demand: International evidence. Energy Econ. 2016, 59, 466–474. [Google Scholar] [CrossRef] [Green Version]

- Asche, F.; Nilsen, O.B.; Tveteras, R. Natural gas demand in the European household sector. Energy J. 2008, 29, 27–46. [Google Scholar] [CrossRef] [Green Version]

- Bernau, P.; Bollmann, R.; Brankovic, M.; Theurer, M. Abschied von Putins Gas. Frankfurter Allgemeine Zeitung. 1 May 2022. [Google Scholar]

- Blas, J. Biden’s Gas Exports Create Imported Headaches: Bloomberg. 2022. Available online: https://www.bloomberg.com/opinion/articles/2022-04-19/amid-ukraine-war-u-s-gas-exports-deepen-inflation-woes-at-home (accessed on 19 April 2022).

- Buurma, C.; Freitas, G. US Natural Gas Slumps as LNG Plant Shutdown Strands Supplies: Bloomberg. 2022. Available online: https://www.bloomberg.com/news/articles/2022-06-14/us-natural-gas-plunges-as-texas-lng-plant-may-restart-in-90-days (accessed on 14 June 2022).

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Halser, C.; Paraschiv, F. Pathways to Overcoming Natural Gas Dependency on Russia—The German Case. Energies 2022, 15, 4939. https://doi.org/10.3390/en15144939

Halser C, Paraschiv F. Pathways to Overcoming Natural Gas Dependency on Russia—The German Case. Energies. 2022; 15(14):4939. https://doi.org/10.3390/en15144939

Chicago/Turabian StyleHalser, Christoph, and Florentina Paraschiv. 2022. "Pathways to Overcoming Natural Gas Dependency on Russia—The German Case" Energies 15, no. 14: 4939. https://doi.org/10.3390/en15144939

APA StyleHalser, C., & Paraschiv, F. (2022). Pathways to Overcoming Natural Gas Dependency on Russia—The German Case. Energies, 15(14), 4939. https://doi.org/10.3390/en15144939