Effectiveness and Feasibility of Market Makers for P2P Electricity Trading

Abstract

:1. Introduction

2. Motivative Experiment and Market Rules

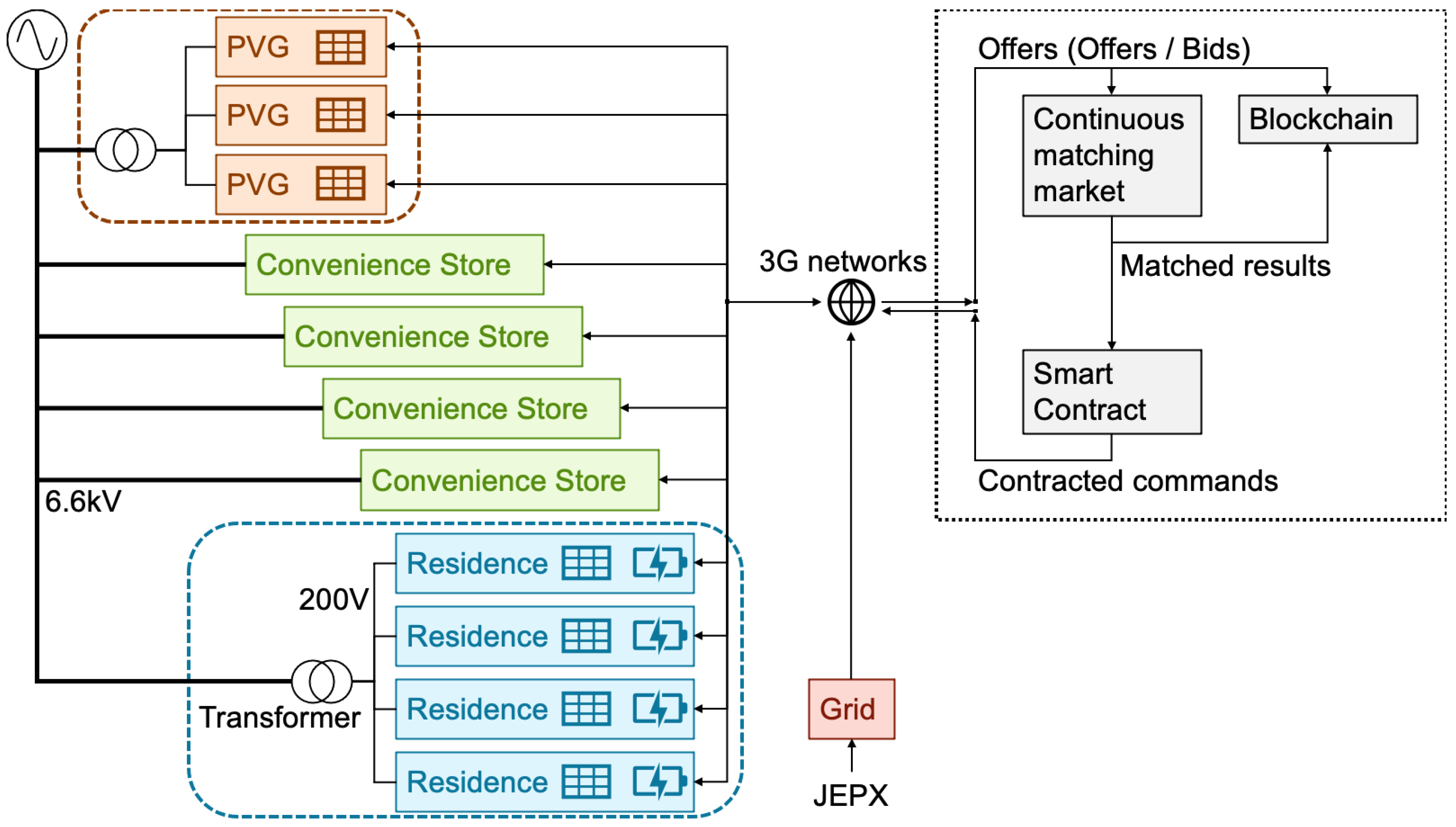

2.1. Motivative Demonstration Project and Potential Problem

2.2. Market Rules

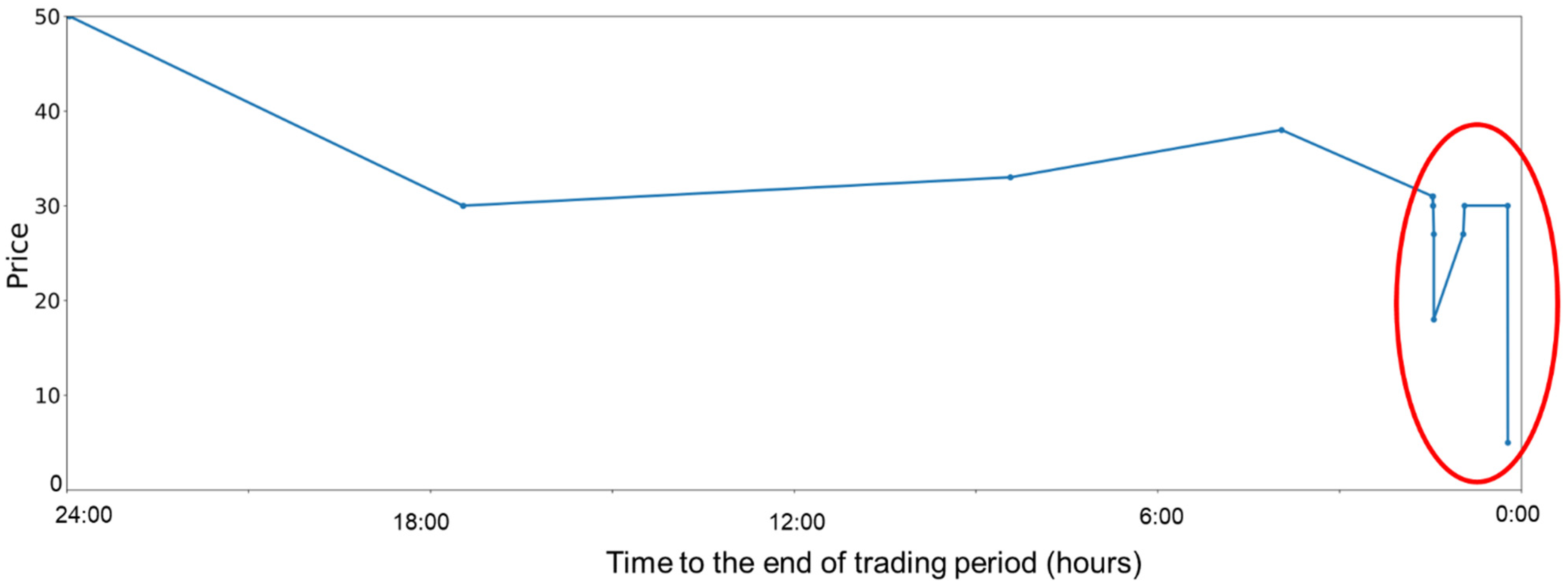

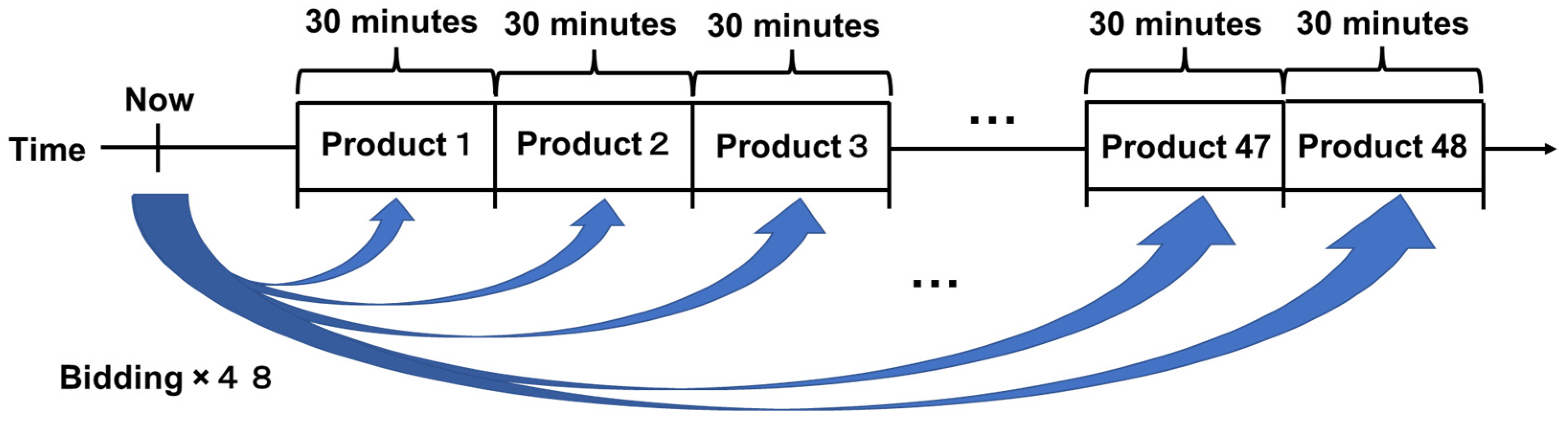

- The market for each product is assumed to open 24 h before the start of the 30-min electricity delivery period and close 10 min before the end of the time interval. In other words, the market accepts orders from participants for 24 h and 20 min.

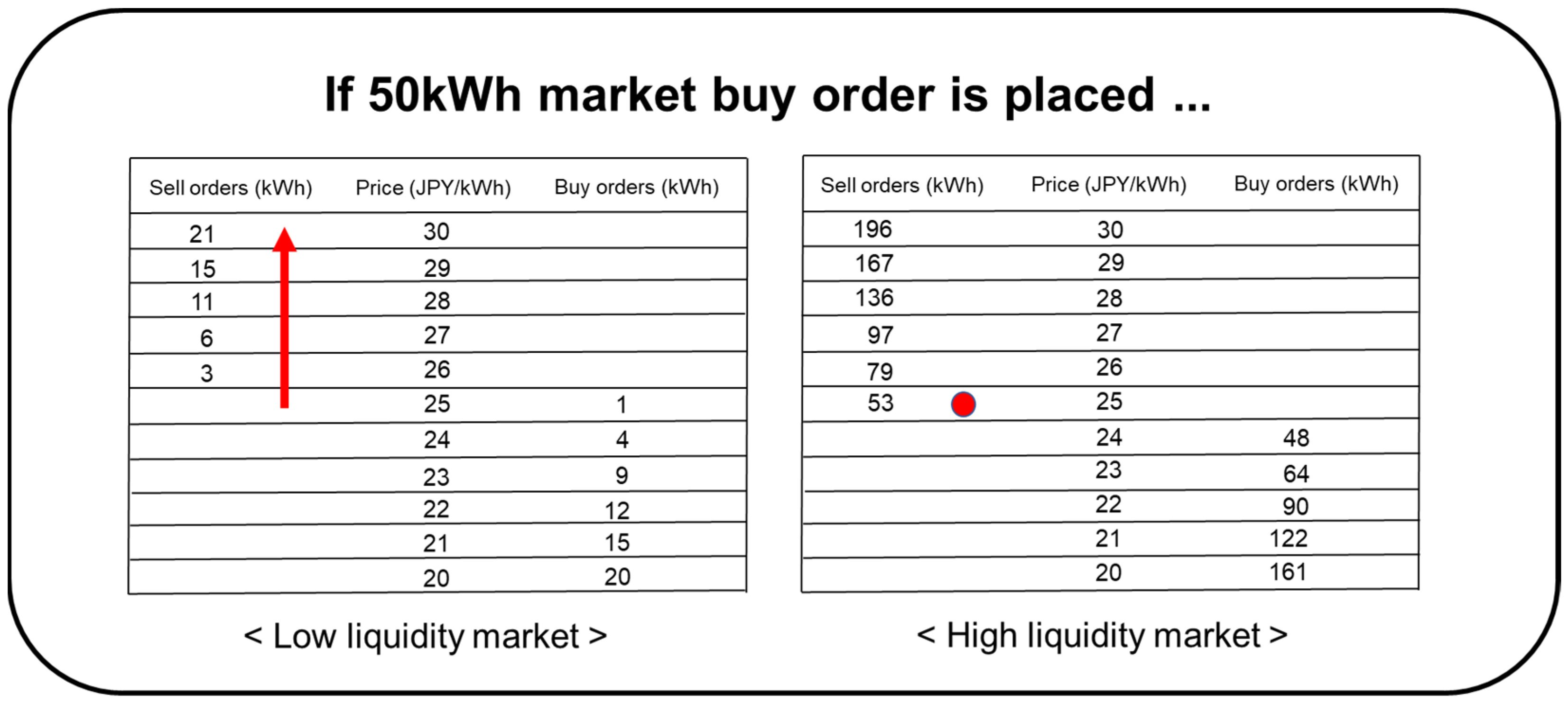

- Orders in the book are executed in continuous sessions or according to the principle of price and time priority. Specifically, offers with prices lower than those of bids and bids with prices higher than those of offers are executed immediately, whereas other orders remain on the board.

- If the matched offer and bid volumes are different, the executed amount is adjusted to a smaller value.

- If multiple orders at the same price exist on the board, the earliest order is prioritized.

3. Development of Artificial Market Simulation System

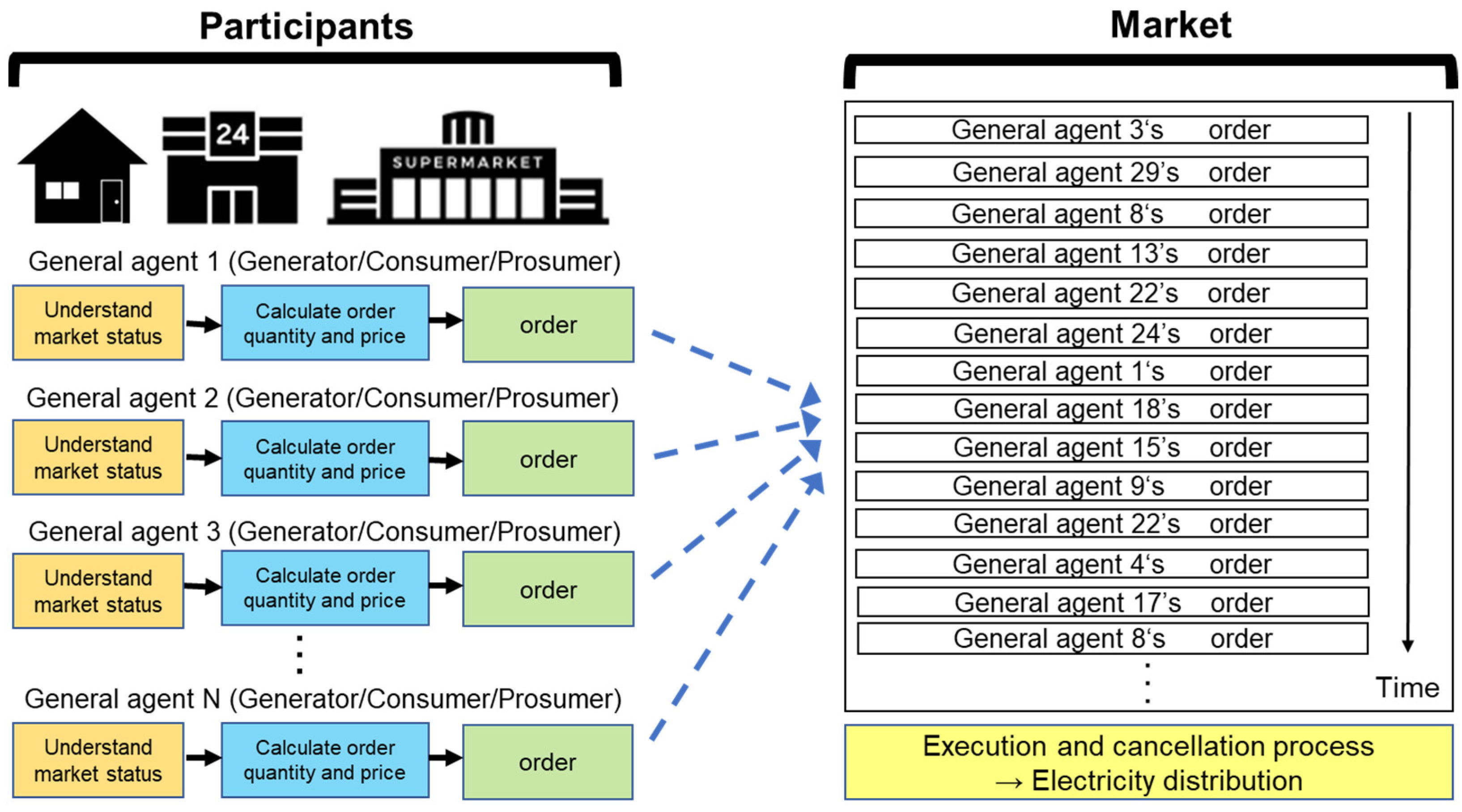

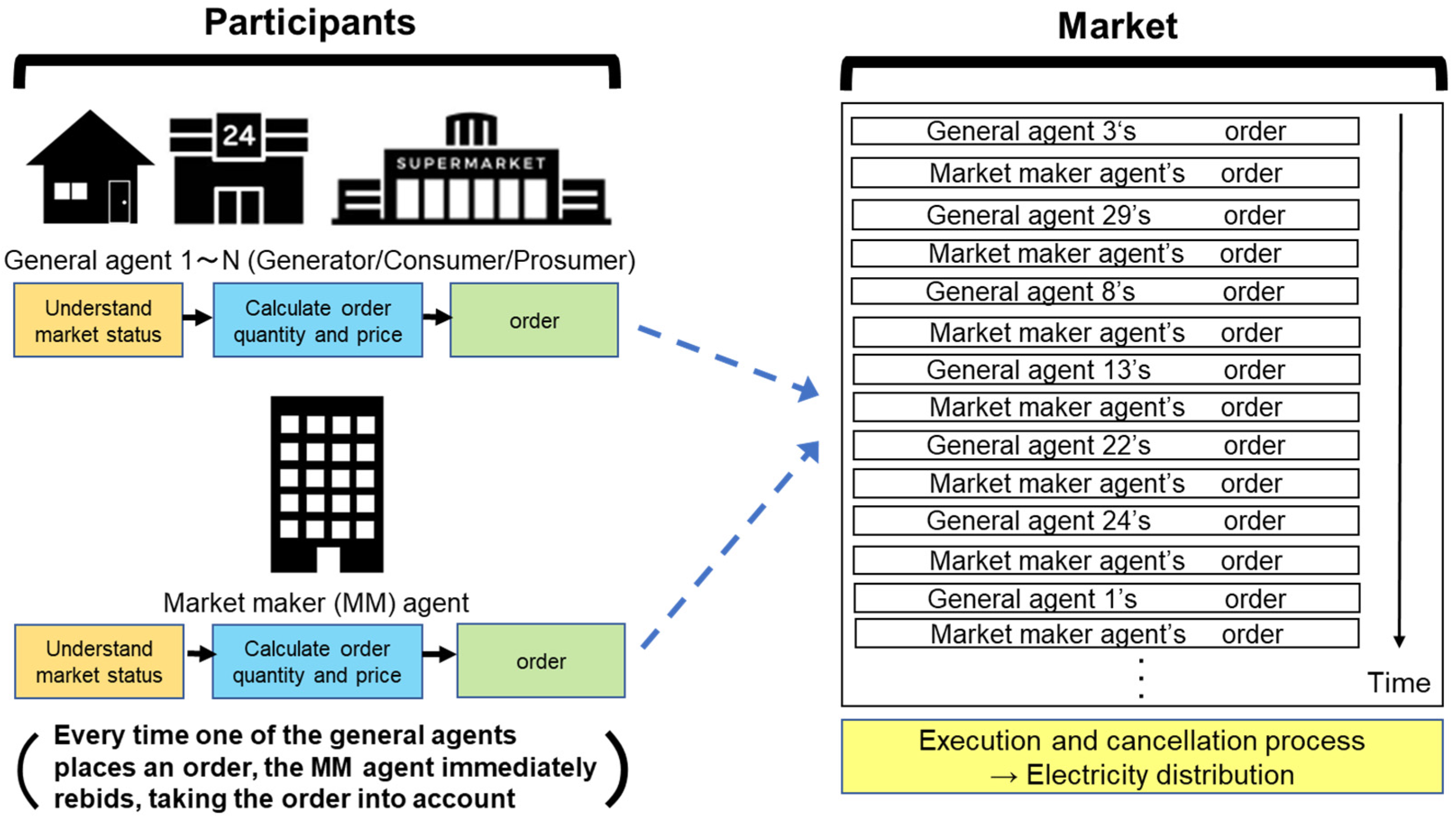

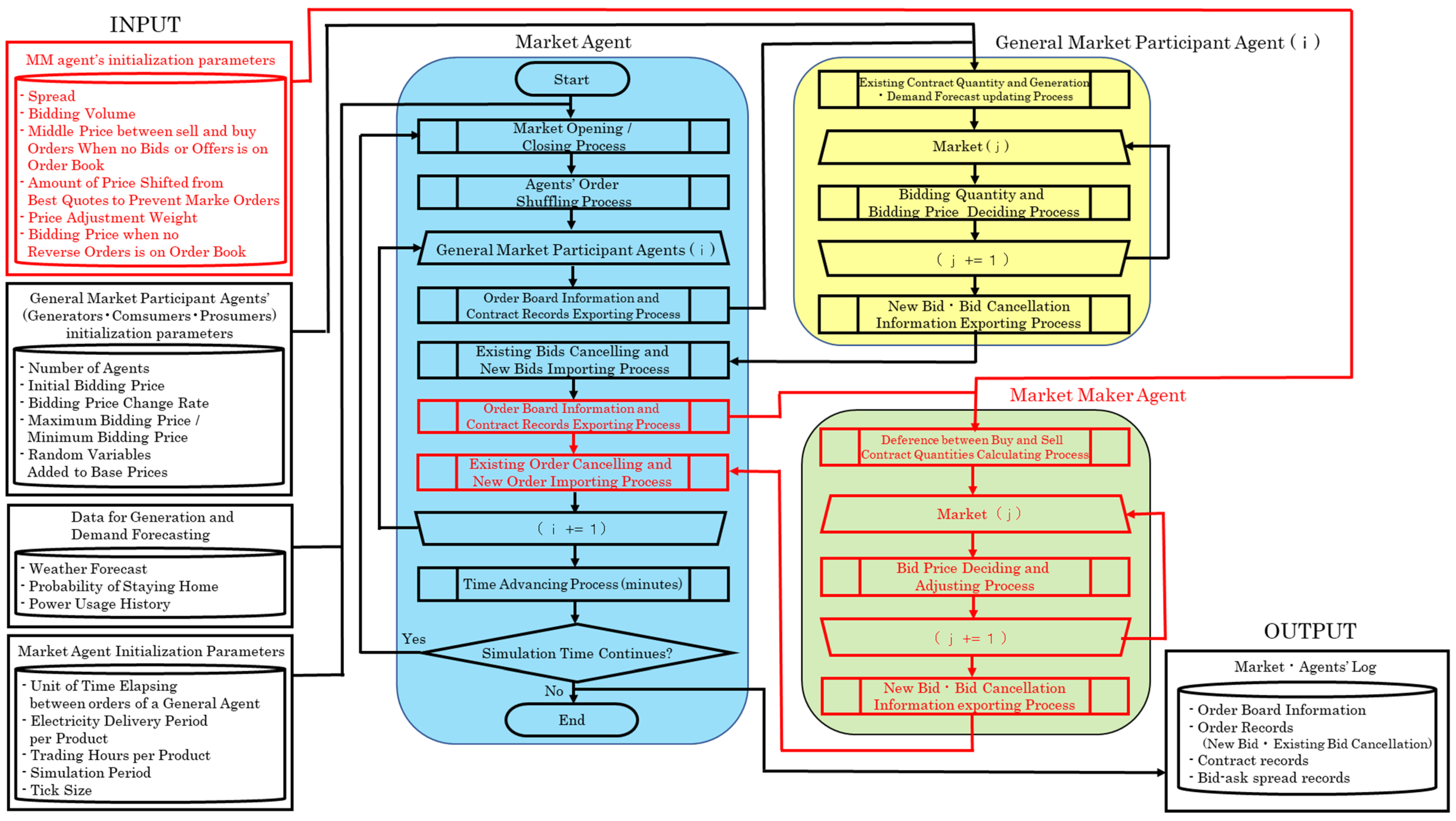

3.1. Basic Configuration and Information Flow

3.2. Market Maker’s Bidding Strategies

3.2.1. Bidding Strategy of the Simple Market Maker

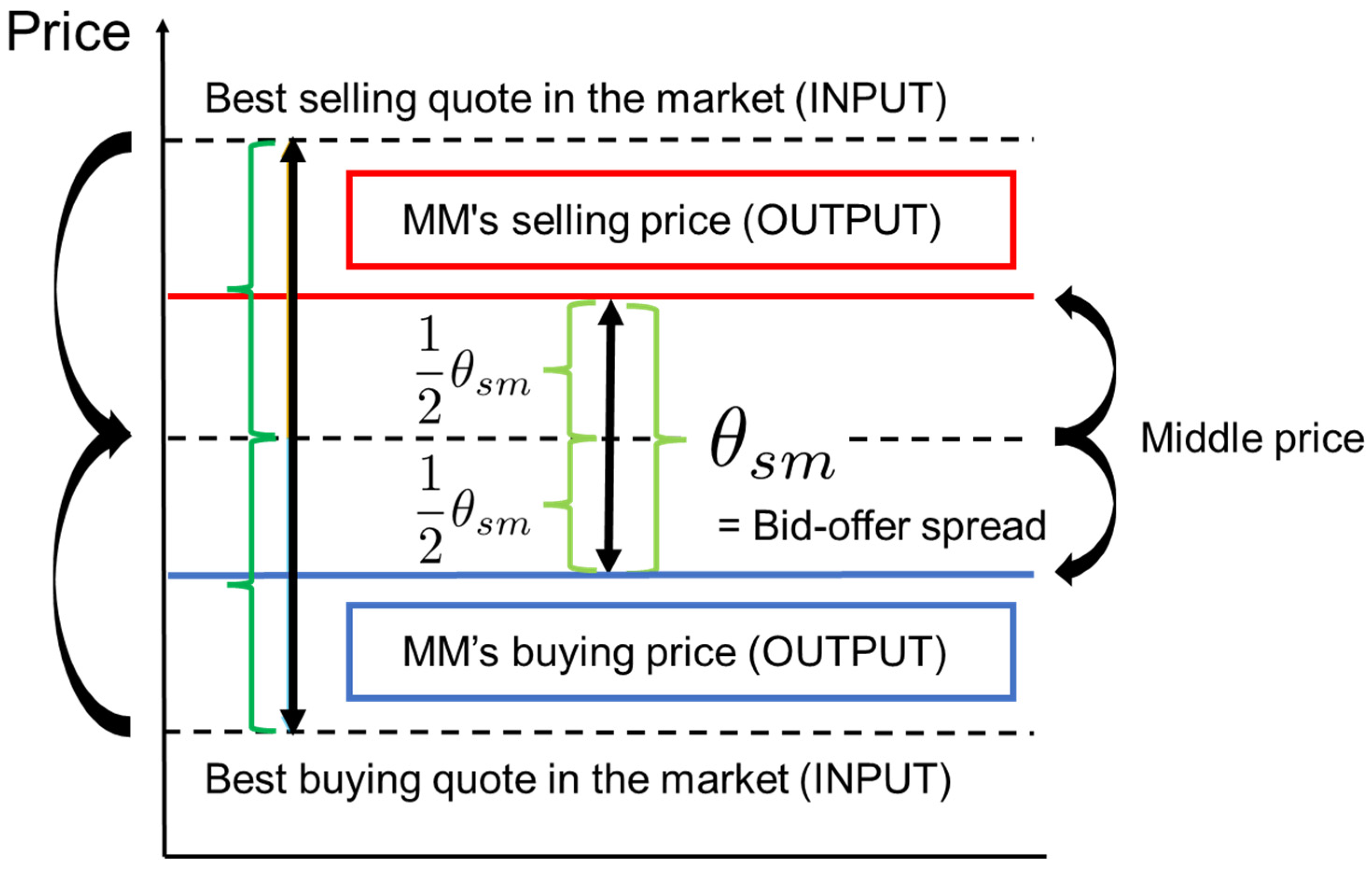

- The market maker derives the best quotes on the order board in each bidding turn, that is, the lowest selling quote and the highest buying quote. The selling and buying prices are then calculated using the middle price between the two best quotes. More exactly, the selling (buying) price is shifted up (down) by half of the specified spread value, from the middle price.

- If either or both sell/buy orders do not exist on the board of the market, the middle price cannot be determined. Therefore, in this case, we assume that the middle price is given a priori as an initial parameter. Specifically, we set the initial setting parameter at 25 JPY/kWh in our simulation, which is the mean value of the upper limit price of 50 JPY/kWh and the lower limit price of 0 JPY/kWh.

- In addition, since market makers are supposed to keep quoting both sell and buy prices, they are programmed to always place a limit order, not a market order, in this simulation. Therefore, in case the bidding price of our strategies may result in a market order, it is shifted up or down such that it becomes a limit order.

- That is, sell and buy prices are adjusted in the same direction by the same amount so that the spread is kept constant at the value of an initial parameter in this case as well.

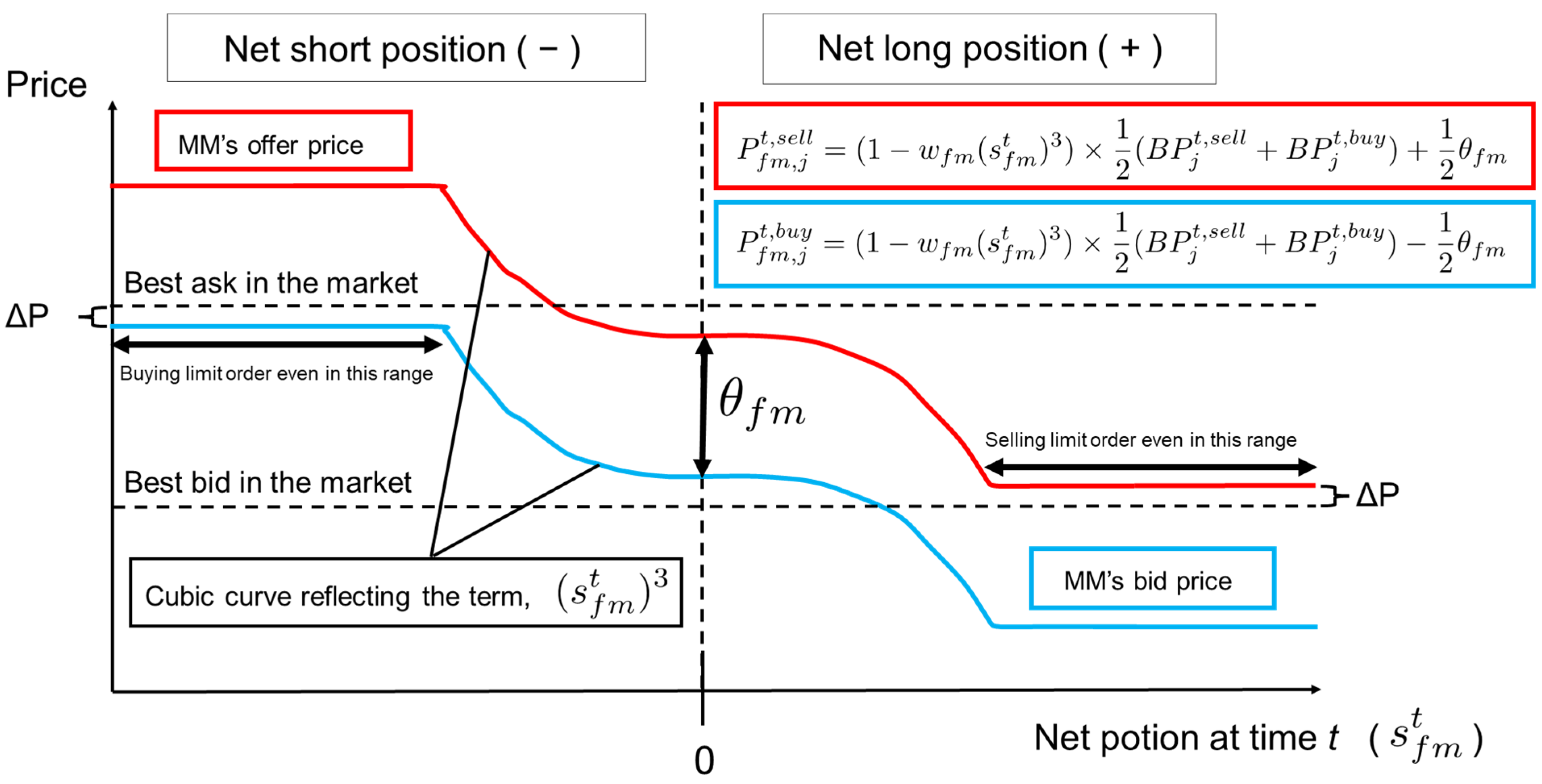

3.2.2. Bidding Strategy of the Flexible Market Maker

- The price adjustment is conducted according to the term where is the market maker’s net position at time (i.e., total executed buying volume minus total executed selling volume for all products up to time ) and is a weighting term. The effect based on the net position is reflected when . For instance, if the selling contract amount is greater than the buying amount, both selling and buying prices are shifted up. When the market maker’s position is net long, both selling and buying prices are shifted down according to the term .

- If the market maker’s bid price (buying order price), given by the blue line in Figure 10, were shifted beyond the best selling quote on the board, shown by the horizontal dotted line on the upper side, the order would be executed as a market order. To avoid this and make the bidding a limit order, the buying order price will be fixed just below the best selling quote by . Similarly, the selling order price will be fixed just above the best buying quote to avoid the selling order becoming a market order.

- To incentivize market makers, we assume that market makers may place an order at a favorable price when there is no other selling or buying order on the board. For example, when no other selling orders exist, which often happens at night or in the early morning with no solar power generation, the market maker can make a sell order at a relatively high price (e.g., 33 JPY/kWh in our simulation) because the market maker is the sole seller in the entire market.

- For the opposite-side order, a buy order in this case, the market maker is assumed to use the same price as the previous bidding, . On the other hand, with no other buying orders, the market maker places a buy order at a relatively low price (e.g., 17 JPY/kWh in our simulation) while using the same selling price as the previous bidding, . In either case, the spread between the selling and buying prices may become wider than .

- When calculating in Figure 10, the executed volume at the above two particular prices, i.e., the selling amount at the price of 33 JPY/kWh and the buying amount at 17 JPY/kWh, is excluded to avoid the effects of the extreme imbalances during these periods.

4. Artificial Market Simulation Using Supply and Demand Data

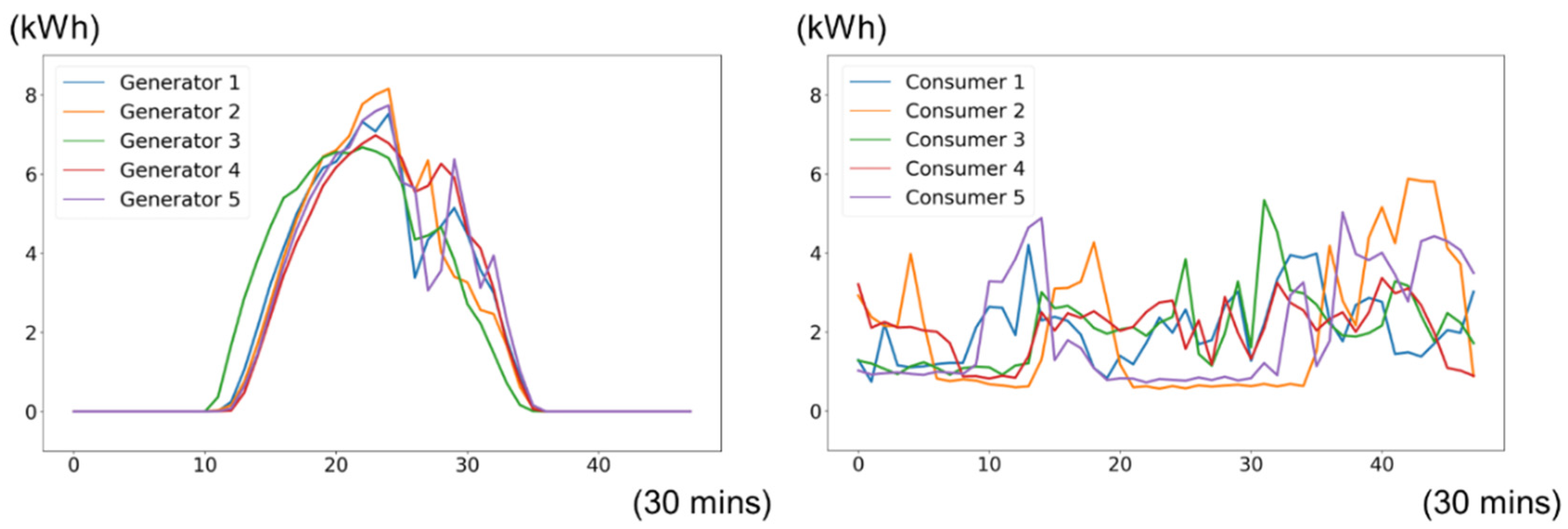

4.1. Supply and Demand Data

- Case 1.

- P2P market simulation without market makers.

- Case 2.

- P2P market simulation with the simple market maker that focuses only on market liquidity and electricity price stability.

- Case 3.

- P2P market simulation with the flexible market maker that considers its profitability, not only market liquidity and electricity price stability.

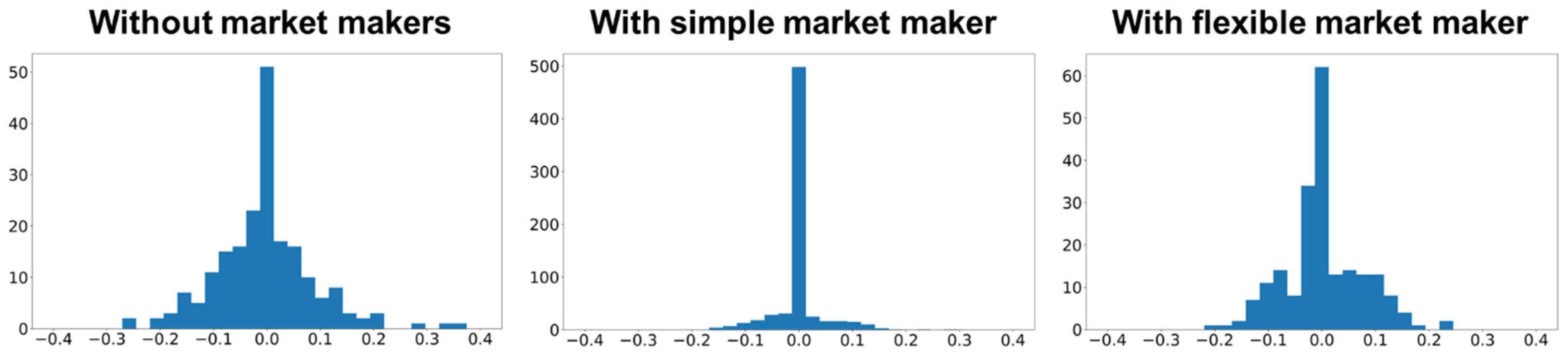

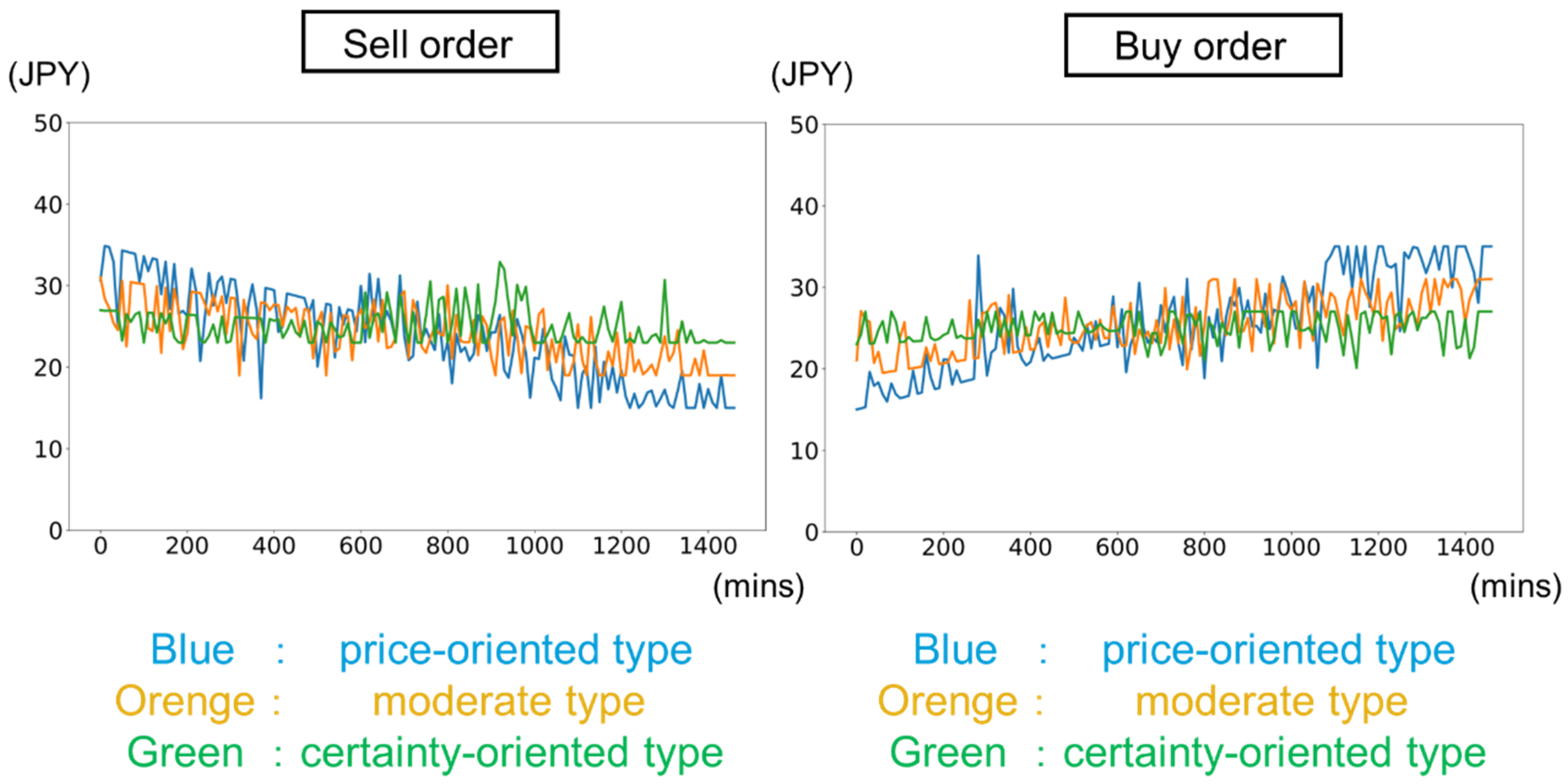

4.2. Case 1: Without Market Makers

4.3. Case 2: Introduction of the Simple Market Maker

4.4. Case 3: Introduction of the Flexible Market Maker

5. Comparative Discussions

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Bidding Strategies of General Agents

Appendix A.1. Generators and Consumers

Appendix A.2. Prosumers

References

- Mengelkamp, E.; Gärttner, J.; Rock, K.; Kessler, S.; Orsini, L.; Weinhardt, C. Designing microgrid energy markets: A case study: The Brooklyn Microgrid. Appl. Energy 2018, 210, 870–880. [Google Scholar] [CrossRef]

- Werth, A.; Kitamura, N.; Tanaka, K. Conceptual study for open energy systems: Distributed energy network using interconnected DC nanogrids. IEEE Trans. Smart Grid 2015, 6, 1621–1630. [Google Scholar] [CrossRef]

- Lezama, F.; Soares, J.; Hernandez-Leal, P.; Kaisers, M.; Pinto, T.; Vale, Z. Local energy markets: Paving the path toward fully transactive energy systems. IEEE Trans. Power Syst. 2018, 34, 4081–4088. [Google Scholar] [CrossRef] [Green Version]

- Matsuda, Y.; Tanaka, K. EV mobility charging service based on blockchain. In Proceedings of the 2020 IEEE International Conference on Environment and Electrical Engineering and 2020 IEEE Industrial and Commercial Power Systems Europe (EEEIC/I&CPS Europe), Madrid, Spain, 9–12 June 2020. [Google Scholar]

- Goranović, A.; Meisel, M.; Fotiadis, L.; Wilker, S.; Treytl, A.; Sauter, T. Blockchain applications in microgrids an overview of current projects and concepts. In Proceedings of the IECON 2017—43rd Annual Conference of the IEEE Industrial Electronics Society, Beijing, China, 29 October–1 November 2017; pp. 6153–6158. [Google Scholar]

- Parka, C.; Yong, T. Comparative review and discussion on P2P electricity trading. Energy Procedia 2017, 128, 3–9. [Google Scholar] [CrossRef]

- Sagawa, D.; Tanaka, K.; Ishida, F.; Saito, H.; Takenaga, N.; Nakamura, S.; Aoki, N.; Nameki, M.; Saegusa, K. Bidding agents for PV and electric vehicle-owning users in the electricity P2P trading market. Energies 2021, 14, 8309. [Google Scholar] [CrossRef]

- Matsuda, Y.; Yamazaki, Y.; Oki, H.; Takeda, Y.; Sagawa, D. Tanaka, K. Demonstration of blockchain based peer to peer energy trading system with real-life used PHEV and HEMS charge control. Energies 2021, 14, 7484. [Google Scholar] [CrossRef]

- Takeda, Y.; Nakai, Y.; Senoo, T.; Tanaka, K. Designing a user-centric P2P energy trading platform: A case study—Higashi-Fuji Demonstration. Energies 2021, 14, 7289. [Google Scholar] [CrossRef]

- Zhang, W.; Wang, X.; Huang, Y.; Qi, S.; Zhao, Z.; Lin, F. A Peer-To-Peer Market Mechanism for Distributed Energy Resourses. In Proceedings of the 2019 IEEE Innovative Smart Grid Technologies—Asia (ISGT Asia), Chengdu, China, 21–24 May 2019; pp. 1375–1380. [Google Scholar]

- Leong, C.H.; Gu, C.; Li, F. Auction Mechanism for P2P Local Energy Trading considering Physical Constraints. Energy Procedia 2019, 158, 6613–6618. [Google Scholar] [CrossRef]

- Lin, J.; Pipattanasomporn, M.; Rahman, S. Comparative analysis of auction mechanisms and bidding strategies for P2P solar transactive energy markets. Appl. Energy 2019, 255, 113687. [Google Scholar] [CrossRef]

- Azim, M.I.; Tushar, W.; Saha, T.K. Cooperative negawatt P2P energy trading for low-voltage distribution networks. Appl. Energy 2021, 299, 117300. [Google Scholar] [CrossRef]

- Azizi, A.; Aminifar, F.; Moeini-Aghtaie, M.; Alizadeh, A. Transactive Energy Market Mechanism With Loss Implication. IEEE Trans. Smart Grid 2021, 12, 1215–1223. [Google Scholar] [CrossRef]

- Andoni, M.; Robu, V.; Flynn, D.; Abram, S.; Geach, D.; Jenkins, D.; McCallum, P.; Peacock, A. Blockchain technology in the energy sector: A systematic review of challenges and opportunities. Renew Sustain. Energy Rev. 2019, 100, 143–174. [Google Scholar] [CrossRef]

- Ahl, A.; Yarime, M.; Tanaka, K.; Sagawa, D. Review of blockchain-based distributed energy: Implications for institutional development. Renew. Sustain. Energy Rev. 2019, 107, 200–211. [Google Scholar] [CrossRef]

- Nemoto, J.; Goto, M. Measurement of Dynamic Efficiency in Production: An Application of Data Envelopment Analysis to Japanese Electric Utilities. J. Product. Anal. 2003, 19, 191–210. [Google Scholar] [CrossRef]

- Kontani, R.; Tanaka, K.; Yamada, Y. Feasibility conditions for demonstrative peer-to-peer energy market. Energies 2021, 14, 7418. [Google Scholar] [CrossRef]

- Japan Exchange Group, Incorporated. Market Maker Program. Available online: https://www.jpx.co.jp/english/derivatives/rules/market-maker/index.html (accessed on 14 April 2022).

- Kardakos, E.G.; Simoglou, C.K.; Bakirtzis, A.G. Optimal bidding strategy in transmission-constrained electricity markets. Electr. Power Syst. Res. 2014, 109, 141–149. [Google Scholar] [CrossRef]

- Maceas Henao, M.; Espinosa Oviedo, J.J. Bidding Strategy for VPP and Economic Feasibility Study of the Optimal Sizing of Storage Systems to Face the Uncertainty of Solar Generation Modelled with IGDT. Energies 2022, 15, 953. [Google Scholar] [CrossRef]

- Singh, S.; Fozdar, M.; Malik, H.; Khan, I.A.; Al Otaibi, S.; Albogamy, F.R. Impacts of Renewable Sources of Energy on Bid Modeling Strategy in an Emerging Electricity Market Using Oppositional Gravitational Search Algorithm. Energies 2021, 14, 5726. [Google Scholar] [CrossRef]

- Qussous, R.; Harder, N.; Weidlich, A. Understanding Power Market Dynamics by Reflecting Market Interrelations and Flexibility-Oriented Bidding Strategies. Energies 2022, 15, 494. [Google Scholar] [CrossRef]

- Khaloie, H.; Abdollahi, A.; Shafie-Khah, M.; Siano, P.; Nojavan, S.; Anvari-Moghaddam, A.; Catalao, J.P.S. Co-optimized bidding strategy of an integrated wind-thermal-photovoltaic system in deregulated electricity market under uncertainties. J. Clean. Prod. 2020, 242, 118434. [Google Scholar] [CrossRef]

- Zheng, Y.; Yu, H.; Shao, Z.; Jian, L. Day-ahead bidding strategy for electric vehicle aggregator enabling multiple agent modes in uncertain electricity markets. Appl. Energy 2020, 280, 115977. [Google Scholar] [CrossRef]

- Sadeghi, S.; Jahangir, H.; Vatandoust, B.; Golkar, M.A.; Ahmadian, A.; Elkamel, A. Optimal bidding strategy of a virtual power plant in day-ahead energy and frequency regulation markets: A deep learning-based approach. Int. J. Electr. Power Energy Syst. 2021, 127, 106646. [Google Scholar] [CrossRef]

- Li, S.; Park, C.S. Wind power bidding strategy in the short-term electricity market. Energy Econ. 2018, 75, 336–344. [Google Scholar] [CrossRef]

- Mahvi, M.; Ardehali, M.M. Optimal bidding strategy in a competitive electricity market based on agent-based approach and numerical sensitivity analysis. Energy 2011, 36, 6367–6374. [Google Scholar] [CrossRef]

- Baltaoglu, S.; Tong, L.; Zhao, Q. Algorithmic bidding for virtual trading in electricity markets. IEEE Trans. Power Syst. 2019, 34, 535–543. [Google Scholar] [CrossRef] [Green Version]

- Deng, S.J.; Oren, S.S. Electricity derivatives and risk management. Energy 2006, 31, 940–953. [Google Scholar] [CrossRef]

- Algieri, B.; Leccadito, A.; Tunaru, D. Risk premia in electricity derivatives markets. Energy Econ. 2021, 100, 105300. [Google Scholar] [CrossRef]

- Bevin-McCrimmon, F.; Diaz-Rainey, I.; McCarten, M.; Sise, G. Liquidity and risk premia in electricity futures. Energy Econ. 2018, 75, 503–517. [Google Scholar] [CrossRef]

- Matsumoto, T.; Bunn, D.W.; Yamada, Y. Pricing electricity day-ahead cap futures with multifactor skew-t densities. Quant. Financ. 2021, 22, 835–860. [Google Scholar] [CrossRef]

- Groll, A.; Cabrera, B.L.; Meyer-Brandis, T. A consistent two-factor model for pricing temperature derivatives. Energy Econ. 2016, 55, 112–126. [Google Scholar] [CrossRef] [Green Version]

- Lee, Y.; Oren, S.S. An equilibrium pricing model for weather derivatives in a multi-commodity setting. Energy Econ. 2009, 31, 702–713. [Google Scholar] [CrossRef] [Green Version]

- Kanamura, T.; Ohashi, K. Pricing summer day options by good-deal bounds. Energy Econ. 2009, 31, 289–297. [Google Scholar] [CrossRef]

- Benth, F.E.; Di Persio, L.; Lavagnini, S. Stochastic Modeling of Wind Derivatives in Energy Markets. Risks 2018, 6, 56. [Google Scholar] [CrossRef] [Green Version]

- Rodríguez, Y.E.; Pérez-Uribe, M.A.; Contreras, J. Wind Put Barrier Options Pricing Based on the Nordix Index. Energies 2021, 14, 1177. [Google Scholar] [CrossRef]

- Boyle, C.F.; Haas, J.; Kern, J.D. Development of an irradiance-based weather derivative to hedge cloud risk for solar energy systems. Renew. Energy 2020, 164, 1230–1243. [Google Scholar] [CrossRef]

- Bhattacharya, S.; Gupta, A.; Kar, K.; Owusu, A. Risk management of renewable power producers from co-dependencies in cashflows. Eur. J. Oper. Res. 2020, 283, 1081–1093. [Google Scholar] [CrossRef]

- Yamada, Y.; Matsumoto, T. Going for derivatives or forwards? Minimizing cashflow fluctuations of electricity transactions on power markets. Energies 2021, 14, 7311. [Google Scholar] [CrossRef]

- Matsumoto, T.; Yamada, Y. Simultaneous hedging strategy for price and volume risks in electricity businesses using energy and weather derivatives. Energy Econ. 2021, 95, 105101. [Google Scholar] [CrossRef]

- Matsumoto, T.; Yamada, Y. Customized yet standardized temperature derivatives: A non-parametric approach with suitable basis selection for ensuring robustness. Energies 2021, 14, 3351. [Google Scholar] [CrossRef]

- Worthmann, K.; Kellett, C.M.; Braun, P.; Grune, L.; Weller, S.R. Distributed and Decentralized Control of Residential Energy Systems Incorporating Battery Storage. IEEE Trans. Smart Grid 2015, 6, 1914–1923. [Google Scholar] [CrossRef] [Green Version]

- Nguyen, V.H.; Tran, Q.T.; Besanger, Y.; Labonne, A. Complementary business models for distribution system operator in a peer-to-peer electricity market. In Proceedings of the 2021 IEEE International Conference on Environment and Electrical Engineering and 2021 IEEE Industrial and Commercial Power Systems Europe, Bari, Italy, 8–11 June 2021; pp. 1–6. [Google Scholar]

- Huang, Q.; Xu, Y.; Courcoubetis, C. Strategic Storage Operation in Wholesale Electricity Markets: A Game Theoretic Analysis. In Proceedings of the 2019 IEEE 58th Conference on Decision and Control (CDC), Nice, France, 11–13 December 2019; pp. 2201–2207. [Google Scholar]

- Bose, S.; Cai, D.W.H.; Low, S.; Wierman, A. The role of a market maker in networked Cournot competition. In Proceedings of the 53rd IEEE Conference on Decision and Control, Los Angeles, CA, USA, 15–17 December 2014; pp. 4479–4484. [Google Scholar]

- Worthmann, K.; Kellett, C.M.; Grüne, L.; Weller, S.R. Distributed control of residential energy systems using a market maker. IFAC Proc. Vol. 2014, 47, 11641–11646. [Google Scholar] [CrossRef] [Green Version]

- Kusada, Y.; Mizuta, T.; Hayakawa, S.; Izumi, K. Impact of Position-Based Market Makers to Shares of Markets’ Volumes—An Artificial Market Approach. Trans. Jpn. Soc. Artif. Intell. 2015, 30, 675–682. (In Japanese) [Google Scholar] [CrossRef] [Green Version]

- Mizuta, T.; Izumi, K. Investigation of Frequent Batch Auctions Using Agent Based Model; JPX Working Paper, 17; Japan Exchange Group, Inc.: Tokyo, Japan, 2016; Available online: https://www.jpx.co.jp/english/corporate/research-study/working-paper/b5b4pj000000i468-att/E_JPX_working_paper_Vol17.pdf (accessed on 13 April 2022).

- Abe, R.; Tanaka, K.; Triet, N.V. Energy Internet: An open energy platform to transform legacy power systems into open innovation and global economic. In The Energy Internet: An Open Energy Platform to Transform Legacy Power Systems into Open Innovation and Global Economic Engines; Su, W., Huang, A., Eds.; Woodhead Publishing: Cambridge, UK, 2018; pp. 241–264. [Google Scholar]

- Tanaka, K.; Abe, R.; Nguyen-Van, T.; Yamazaki, Y.; Kamitamari, T.; Sako, K.; Koide, T. A Proposal on an Electricity Trading Platform Using Blockchain, Volume 7: Transdisciplinary Engineering Methods for Social Innovation of Industry 4.0; IOS Press: Amsterdam, The Netherlands, 2018; pp. 976–983. [Google Scholar]

- Waseda, F.; Tanaka, K. Bidding agent for electric vehicles in peer-to-peer electricity trading market considering uncertainty. In Proceedings of the 2020 IEEE International Conference on Environment and Electrical Engineering and 2020 IEEE Industrial and Commercial Power Systems Europe (EEEIC/I&CPS Europe), Madrid, Spain, 9–12 June 2020. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Items | Content |

|---|---|

| Data category | Generation and demand (kWh) |

| Category of participant | Residencial household |

| Number of households | Five |

| Weather | Sunny |

| Period | One day (24 h; 0:00–24:00) |

| Measurement interval | 5 min |

| Amount of data | 1440 for generation and 1440 for demand |

| Items | Values | |

|---|---|---|

| General agents | Number of agents | 18 agents in total = 6 generators + 6 consumers + 6 prosumers (6 agents for each = 2 price-oriented-type agents + 2 moderate-type agents + 2 certainty-oriented-type agents) |

| Total generation per day and Total demand per day | (Generator) Generation: 100 kWh/day Demand: 0 kWh/day (Consumer) Generation: 0 kWh/day Demand: 100 kWh/day (Prosumer) Generation: 100 kWh/day Demand: 100 kWh/day | |

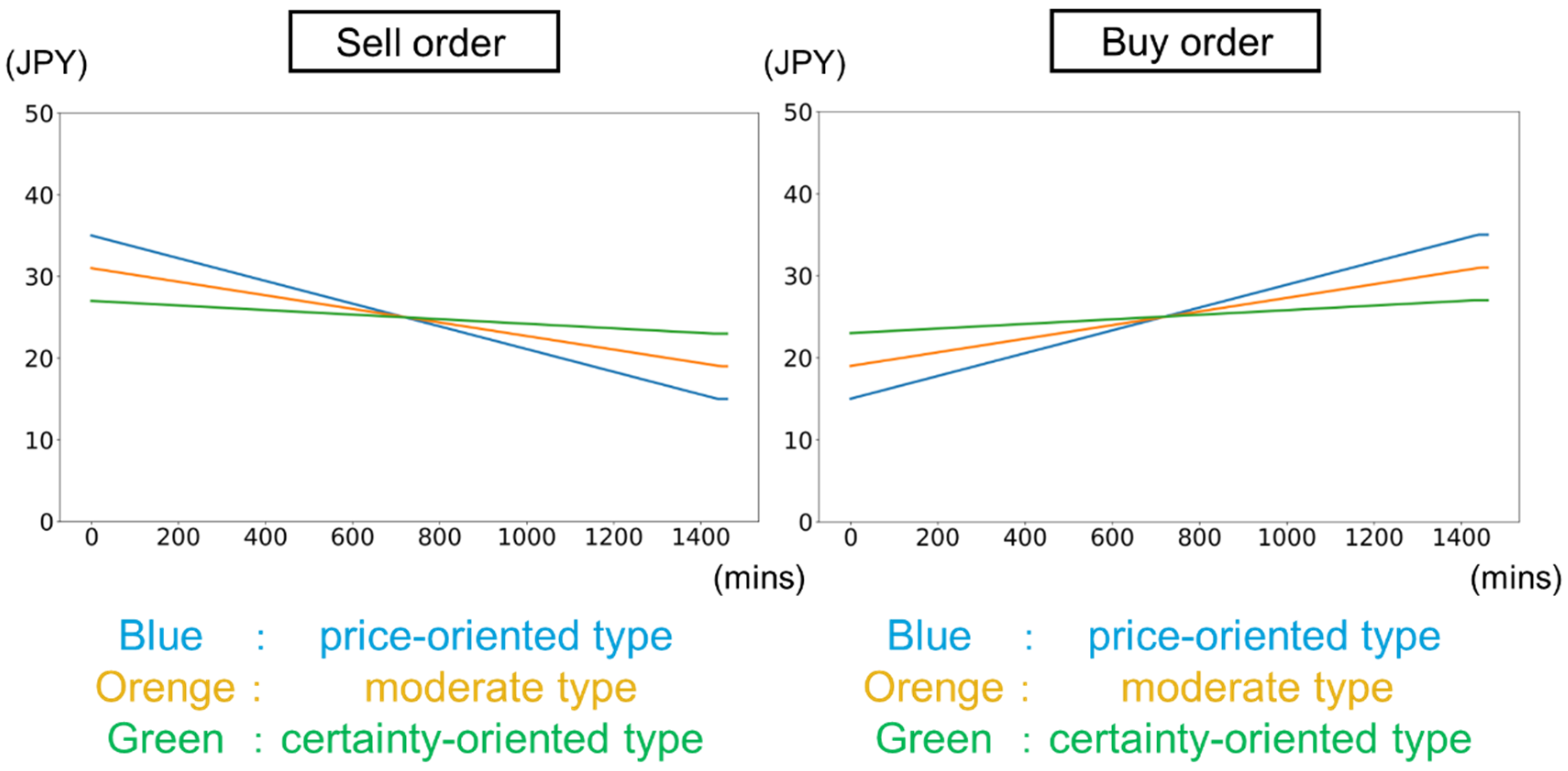

| Initial bidding price | For generators and prosumers’ sell orders Price-oriented type: 35 JPY/kWh Moderate type: 31 JPY/kWh Certainty-oriented type: 27 JPY/kWh For consumers and prosumers’ buy orders Price-oriented type: 15 JPY/kWh Moderate type: 19 JPY/kWh Certainty-oriented type: 23 JPY/kWh | |

| Bidding price change rate | For generators and prosumers’ sell orders Price-oriented type: −0.0139 JPY/kWh/min Moderate type: 0.0083 JPY/kWh/min Certainty-oriented type: −0.0028 JPY/kWh/min For consumers and prosumers’ buy orders Price-oriented type: 0.0139 JPY/kWh/min Moderate type: 0.0083 JPY/kWh/min Certainty-oriented type: 0.0028 JPY/kWh/min | |

| Maximum bidding price/ Minimum bidding price | For generators and prosumers’ sell orders Price-oriented type: 15 JPY/kWh Moderate type: 19 JPY/kWh Certainty-oriented type: 23 JPY/kWh For consumers and prosumers’ buy orders Price-oriented type: 35 JPY/kWh Moderate type: 31 JPY/kWh Certainty-oriented type: 27 JPY/kWh | |

| Random variables added to base prices | Mean: 0.0 Standard deviation: Normal distribution subject to the conditions below (In the case of “price-oriented-type agent” and “within 10 h after the 30-min delivery period starts”) 6.0 (In the case of “moderate-type agent” and “within 10 h after the 30-min delivery period starts”) 4.5 (Others) 3.0 | |

| Market agent | Unit of time elapsing between orders of a general agent | 10 min |

| Electricity delivery period per product | 30 min | |

| Trading hours per product | (Starting time) 24 h before the 30-min delivery period starts (Ending time) 10 min before the 30-min delivery period ends | |

| Simulation period | 2 days (1 day for bidding and 1 day for delivering) | |

| Tick size | 0.01 JPY/kWh | |

| Total Tradable Volume | Total Executed Volume | Execution Rate |

|---|---|---|

| 950.3kWh | 268.7 kWh | 28.3% |

| Mean | Max | Min |

|---|---|---|

| 3.96 JPY/kWh | 16.00 JPY/kWh | 0.01 JPY/kWh |

| Items | Values | |

|---|---|---|

| Simple market maker agent | Spread | 3.00 JPY/kWh |

| Bidding volume | (Sell volume) 10.0Wh (Buy volume) 10.0 kWh | |

| Reference middle price between sell and buy orders when neither bid nor offer is on the order book | 25.00 JPY/kWh | |

| The amount of price shift from the best quotes to prevent market orders | 0.01 JPY/kWh | |

| Total Tradable Volume | Total Executed Volume | Execution Rate |

|---|---|---|

| 950.3 kWh | 134.0 kWh + 1632.6 kWh/2 = 950.3 kWh (Trading volume not involving the simple market maker) 134.0 kWh (Trading volume involving the simple market maker as a seller or buyer) 1632.6 kWh | 100.0% |

| Mean | Max | Min |

|---|---|---|

| 2.90 JPY/kWh | 3.01 JPY/kWh | 0.01 JPY/kWh |

| Items | Values | |

|---|---|---|

| Flexible market maker agent | Price adjustment weight | 0.00005 |

| Bidding price when no reverse order is on the order book | (Sell order price) 33.00 JPY/kWh (Buy order price) 17.00 JPY/kWh | |

| Total Tradable Volume | Total Executed Volume | Execution Rate |

|---|---|---|

| 950.3 kWh | 104.2 kWh + 732.5 kWh/2 = 470.4 kWh (Trading volume not involving the flexible market maker) 104.2 kWh (Trading volume involving the flexible market maker as a seller or buyer) 732.5 kWh | 49.5% |

| Mean | Max | Min |

|---|---|---|

| 8.03 JPY/kWh | 16.00 JPY/kWh | 0.01 JPY/kWh |

| Tradable Volume if All Orders Are Executed | Case 1: without Market Makers | Case 2: with Simple Market Maker | Case 3: with Flexible Market Maker |

|---|---|---|---|

| 950.3 kWh | 268.7 kWh (28.3%) | 950.3 kWh (100.0%) | 470.4 kWh (49.5%) |

| Mean | Variance (Standard Deviation) | Maximum | Minimum | |

|---|---|---|---|---|

| Case 1: Without Market Makers | −0.0043 | 0.0085 (0.0922) | 0.354 (35.4% up) | −0.267 (26.7% down) |

| Case 2: With Simple Market Maker | 0.0001 | 0.0018 (0.0429) | 0.295 (29.5% up) | −0.164 (16.4% down) |

| Case 3: With Flexible Market Maker | 0.0027 | 0.0053 (0.0729) | 0.231 (23.1% up) | −0.196 (19.6% down) |

| Generation/Demand = 100/100 = 1 | Generation/Demand = 130/100 = 1.3 | Generation/Demand = 70/100 = 0.7 | Generation/Demand = 40/100 = 0.4 | |

|---|---|---|---|---|

| Simple Market Maker | 2029.80 JPY | −6281.62 JPY | −7406.00 JPY | −16773.05 JPY |

| Flexible Market Maker | 2900.04 JPY | 520.54 JPY | 453.72 JPY | −3367.36 JPY |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kuno, S.; Tanaka, K.; Yamada, Y. Effectiveness and Feasibility of Market Makers for P2P Electricity Trading. Energies 2022, 15, 4218. https://doi.org/10.3390/en15124218

Kuno S, Tanaka K, Yamada Y. Effectiveness and Feasibility of Market Makers for P2P Electricity Trading. Energies. 2022; 15(12):4218. https://doi.org/10.3390/en15124218

Chicago/Turabian StyleKuno, Shinji, Kenji Tanaka, and Yuji Yamada. 2022. "Effectiveness and Feasibility of Market Makers for P2P Electricity Trading" Energies 15, no. 12: 4218. https://doi.org/10.3390/en15124218

APA StyleKuno, S., Tanaka, K., & Yamada, Y. (2022). Effectiveness and Feasibility of Market Makers for P2P Electricity Trading. Energies, 15(12), 4218. https://doi.org/10.3390/en15124218