The Role of Crypto Trading in the Economy, Renewable Energy Consumption and Ecological Degradation

Abstract

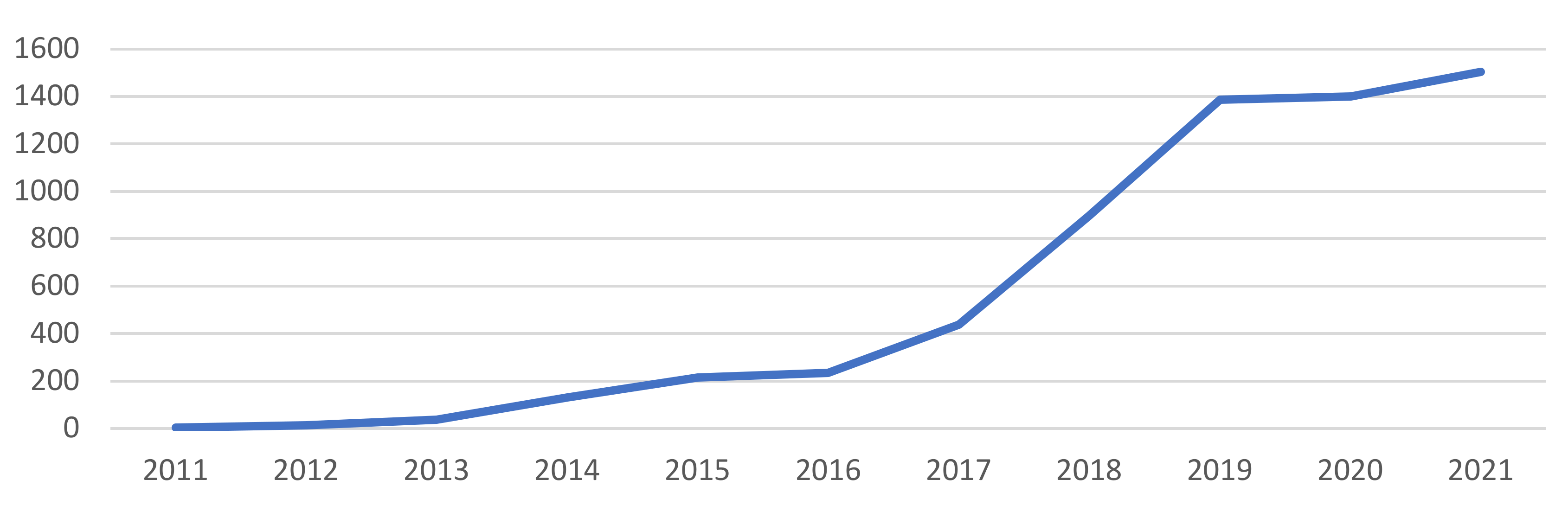

1. Introduction

- Electricity consumption is 204.50 TWh (Terawatt-hour) which is comparable to the power consumption of Thailand;

- The carbon footprint is 114.06 Mt of CO2, which is comparable to the carbon footprint of the Czech Republic;

- The electronic waste is 34.36 kt which is comparable to the small IT equipment waste of the Netherlands [5].

2. Literature Review

- Keywords: cryptocurrency, bitcoin*;

- Boolean operators: OR;

- Subject areas: Business, Management, Accounting, Economics, Econometrics and Finance;

- Year: 2011–2021;

- Language: English.

2.1. Economic Growth and Cryptocurrency

2.2. Cryptocurrency and Energy Consumption

2.3. Cryptocurrency and Environment Degradation

3. Materials and Methods

4. Results

5. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Soni, A.; Maheshwari, S. A survey of attacks on the bitcoin system. In Proceedings of the 2018 IEEE International Students’ Conference on Electrical, Electronics and Computer Science (SCEECS), Bhopal, India, 24–25 February 2018. [Google Scholar] [CrossRef]

- Li, J.-P.; Naqvi, B.; Rizvi, S.K.A.; Chang, H.-L. Bitcoin: The biggest financial innovation of the fourth industrial revolution and a portfolio’s efficiency booster. Technol. Forecast. Soc. Chang. 2021, 162, 120383. [Google Scholar] [CrossRef]

- Web Site of the Company “Triple A”. Cryptocurrency across the World. Available online: https://triple-a.io/crypto-ownership/ (accessed on 16 April 2022).

- Chiriac, I. The influence of intangible assets on the new economy at European level. In Proceedings of the 32nd International Business Information Management Association Conference, IBIMA 2018—Vision 2020: Sustainable Economic Development and Application of Innovation Management from Regional Expansion to Global Growth, Seville, Spain, 15–16 November 2018; pp. 506–514. [Google Scholar]

- Bitcoin Energy Consumption Index. Available online: https://digiconomist.net/bitcoin-energy-consumption (accessed on 1 April 2022).

- Dzwigol, H.; Dzwigol-Barosz, M.; Kwilinski, A. Formation of global competitive enterprise environment based on industry 4.0 concept. Int. J. Entrep. 2020, 24, 1–6. [Google Scholar]

- Kwilinski, A.; Dielini, M.; Mazuryk, O.; Filippov, V.; Kitseliuk, V. System Constructs for the Investment Security of a Country. J. Secur. Sustain. Issues 2020, 10, 345–358. [Google Scholar] [CrossRef]

- Kwilinski, A.; Volynets, R.; Berdnik, I.; Holovko, M.; Berzin, P. E-Commerce: Concept and legal regulation in modern economic conditions. J. Leg. Ethical Regul. Issues 2019, 22, 1–7. [Google Scholar]

- Kwilinski, A.; Dalevska, N.; Kravchenko, S.; Hroznyi, I.; Kovalenko, O. Formation of the entrepreneurship model of e-business in the context of the introduction of information and communication technologies. J. Entrep. Educ. 2019, 22, 1–7. [Google Scholar]

- Tkachenko, V.; Kwilinski, A.; Klymchuk, M.; Tkachenko, I. The Economic-Mathematical Development of Buildings Construction Model Optimization on the Basis of Digital Economy. Manag. Syst. Prod. Eng. 2019, 27, 119–123. [Google Scholar] [CrossRef]

- Trzeciak, M.; Kopec, T.P.; Kwilinski, A. Constructs of Project Programme Management Supporting Open Innovation at the Strategic Level of the Organisation. J. Open Innov. Technol. Mark. Complex. 2022, 8, 58. [Google Scholar] [CrossRef]

- Kwilinski, A.; Dalevska, N.; Dementyev, V.V. Metatheoretical Issues of the Evolution of the International Political Economy. J. Risk Financ. Manag. 2022, 15, 124. [Google Scholar] [CrossRef]

- Kwilinski, A.; Vyshnevskyi, O.; Dzwigol, H. Digitalization of the EU Economies and People at Risk of Poverty or Social Exclusion. J. Risk Financ. Manag. 2020, 13, 142. [Google Scholar] [CrossRef]

- Melnychenko, O. Is Artificial Intelligence Ready to Assess an Enterprise’s Financial Security? J. Risk Financ. Manag. 2020, 13, 191. [Google Scholar] [CrossRef]

- Ciężki, D.; Drożdż, W. Using multicurrency cash pooling in the liquidity management of a capital group. Polityka Energetyczna 2019, 22, 137–150. [Google Scholar] [CrossRef]

- Petroye, O.; Lyulyov, O.; Lytvynchuk, I.; Paida, Y.; Pakhomov, V. Effects of information security and innovations on country’s image: Governance aspect. Int. J. Saf. Secur. Eng. 2020, 10, 459–466. [Google Scholar] [CrossRef]

- Yang, C.; Kwilinski, A.; Chygryn, O.; Lyulyov, O.; Pimonenko, T. The green competitiveness of enterprises: Justifying the quality criteria of digital marketing communication channels. Sustainability 2021, 13, 13679. [Google Scholar] [CrossRef]

- Kuzior, A.; Lyulyov, O.; Pimonenko, T.; Kwilinski, A.; Krawczyk, D. Post-industrial tourism as a driver of sustainable development. Sustainability 2021, 13, 8145. [Google Scholar] [CrossRef]

- Kwilinski, A.; Litvin, V.; Kamchatova, E.; Polusmiak, J.; Mironova, D. Information support of the entrepreneurship model complex with the application of cloud technologies. Int. J. Entrep. 2021, 25, 1–8. [Google Scholar]

- Bogachov, S.; Kwilinski, A.; Miethlich, B.; Bartosova, V.; Gurnak, A. Artificial intelligence components and fuzzy regulators in entrepreneurship development. Entrep. Sustain. Issues 2020, 8, 487–499. [Google Scholar] [CrossRef]

- Kwilinski, A.; Dzwigol, H.; Dementyev, V. Model of entrepreneurship financial activity of the transnational company based on intellectual technology. Int. J. Entrep. 2020, 24, 1–5. [Google Scholar]

- Kwilinski, A.; Kuzior, A. Cognitive Technologies in the Management and Formation of Directions of the Priority Development of Industrial Enterprises. Manag. Syst. Prod. Eng. 2020, 28, 133–138. [Google Scholar] [CrossRef]

- Kwilinski, A.; Tkachenko, V.; Kuzior, A. Transparent cognitive technologies to ensure sustainable society development. J. Secur. Sustain. Issues 2019, 9, 561–570. [Google Scholar] [CrossRef]

- Melnychenko, O. Application of artificial intelligence in control systems of economic activity. Virtual Econ. 2019, 2, 30–40. [Google Scholar] [CrossRef]

- Bilan, Y.; Pimonenko, T.; Starchenko, L. Sustainable business models for innovation and success: Bibliometric analysis. E3S Web Conf. 2020, 159, 04037. [Google Scholar] [CrossRef]

- Rahmanov, F.; Mursalov, M.; Rosokhata, A. Consumer Behavior in Digital Era: Impact of COVID-19. Mark. Manag. Innov. 2021, 2, 243–251. [Google Scholar] [CrossRef]

- Cosmulese, C.G.; Grosu, V.; Hlaciuc, E.; Zhavoronok, A. The Influences of the Digital Revolution on the Educational System of the EU Countries. Mark. Manag. Innov. 2019, 3, 242–254. [Google Scholar] [CrossRef]

- Shkarlet, S.; Kholiavko, N.; Dubyna, M.; Zhuk, O. Innovation, Education, Research Components of the Evaluation of Information Economy Development (as Exemplified by Eastern Partnership Countries). Mark. Manag. Innov. 2019, 1, 70–83. [Google Scholar] [CrossRef]

- Ahmed, A.A.A.; Paruchuri, H.; Vadlamudi, S.; Ganapathy, A. Cryptography in financial markets: Potential channels for future financial stability. Acad. Account. Financ. Stud. J. 2021, 25, 1–9. [Google Scholar]

- Kwilinski, A. Implementation of Blockchain Technology in Accounting Sphere. Acad. Account. Financ. Stud. J. 2019, 23, 1–6. [Google Scholar]

- Semenova, K.D.; Tarasova, K.I. Establishment of the new digital world and issues of cyber-risks management. Mark. Manag. Innov. 2017, 3, 236–244. [Google Scholar] [CrossRef]

- Hazard, J.; Sclavounis, O.; Stieber, H. Are transaction costs drivers of financial institutions? contracts made in heaven, hell, and the cloud in between. In Banking Beyond Banks and Money. New Economic Windows; Springer International Publishing: Cham, Switzerland, 2016; pp. 213–237. [Google Scholar] [CrossRef]

- Masharsky, A.; Skvortsov, I. Problems and prospects of cryptocurrency development. In Grabchenko’s International Conference on Advanced Manufacturing Processes; Springer International Publishing: Cham, Switzerland, 2022; pp. 435–444. [Google Scholar] [CrossRef]

- Bojaj, M.M.; Muhadinovic, M.; Bracanovic, A.; Mihailovic, A.; Radulovic, M.; Jolicic, I.; Milosevic, I.; Milacic, V. Forecasting macroeconomic effects of stablecoin adoption: A Bayesian approach. Econ. Model. 2022, 109, 105792. [Google Scholar] [CrossRef]

- Sadraoui, T.; Nasr, A.; Mgadmi, N. Studding relationship between bitcoin, exchange rate and financial development: A panel data analysis. Int. J. Manag. Financ. Account. 2021, 13, 232–252. [Google Scholar] [CrossRef]

- Hunter, G.W.; Kerr, C. Virtual money illusion and the fundamental value of non-fiat anonymous digital payment methods: Coining a (bit of) theory to describe and measure the bitcoin phenomenon. Int. Adv. Econ. Res. 2019, 25, 151–164. [Google Scholar] [CrossRef]

- De Vries, A. Bitcoin boom: What rising prices mean for the network’s energy consumption. Joule 2021, 5, 509–513. [Google Scholar] [CrossRef]

- Truby, J. Decarbonizing Bitcoin: Law and policy choices for reducing the energy consumption of Blockchain technologies and digital currencies. Energy Res. Soc. Sci. 2018, 44, 399–410. [Google Scholar] [CrossRef]

- Us, Y.; Pimonenko, T.; Lyulyov, O. Energy efficiency profiles in developing the free-carbon economy: On the example of Ukraine and the V4 countries. Polityka Energetyczna 2021, 23, 49–66. [Google Scholar] [CrossRef]

- Kharazishvili, Y.; Kwilinski, A.; Sukhodolia, O.; Dzwigol, H.; Bobro, D.; Kotowicz, J. The Systemic Approach for Estimating and Strategizing Energy Security: The Case of Ukraine. Energies 2021, 14, 2126. [Google Scholar] [CrossRef]

- Kotowicz, J.; Węcel, D.; Kwilinski, A.; Brzęczek, M. Efficiency of the power-to-gas-to-liquid-to-power system based on green methanol. Appl. Energy 2022, 314, 118933. [Google Scholar] [CrossRef]

- Kyrylov, Y.; Hranovska, V.; Boiko, V.; Kwilinski, A.; Boiko, L. International Tourism Development in the Context of Increasing Globalization Risks: On the Example of Ukraine’s Integration into the Global Tourism Industry. J. Risk Financ. Manag. 2020, 13, 303. [Google Scholar] [CrossRef]

- Drożdż, W.; Kinelski, G.; Czarnecka, M.; Wójcik-Jurkiewicz, M.; Maroušková, A.; Zych, G. Determinants of Decarbonization—How to Realize Sustainable and Low Carbon Cities? Energies 2021, 14, 2640. [Google Scholar] [CrossRef]

- Drożdż, W. The development of electromobility in Poland. Virtual Econ. 2019, 2, 61–69. [Google Scholar] [CrossRef]

- Saługa, P.W.; Szczepańska-Woszczyna, K.; Miśkiewicz, R.; Chłąd, M. Cost of Equity of Coal-Fired Power Generation Projects in Poland: Its Importance for the Management of Decision-Making Process. Energies 2020, 13, 4833. [Google Scholar] [CrossRef]

- Hussain, H.I.; Haseeb, M.; Kamarudin, F.; Dacko-Pikiewicz, Z.; Szczepańska-Woszczyna, K. The Role of Globalization, Economic Growth and Natural Resources on the Ecological Footprint in Thailand: Evidence from Nonlinear Causal Estimations. Processes 2021, 9, 1103. [Google Scholar] [CrossRef]

- Drab-Kurowska, A.; Drożdż, W. Digital Postal Operator as an Important Element of the National Energy Security System. Energies 2021, 15, 231. [Google Scholar] [CrossRef]

- Drożdż, W.; Mróz-Malik, O.J. Challenges for the Polish energy policy in the field of offshore wind energy development. Polityka Energetyczna-Energy Policy J. 2020, 23, 5–18. [Google Scholar] [CrossRef]

- Lyulyov, O.; Chortok, Y.; Pimonenko, T.; Borovik, O. Ecological and economic evaluation of transport system functioning according to the territory sustainable development. Int. J. Ecol. Dev. 2015, 30, 1–10. [Google Scholar]

- Pimonenko, T.; Prokopenko, O.; Dado, J. Net zero house: EU experience in Ukrainian conditions. Int. J. Ecol. Econ. Stat. 2017, 38, 46–57. [Google Scholar]

- Cebula, J.; Pimonenko, T. Comparison financing conditions of the development biogas sector in Poland and Ukraine. Int. J. Ecol. Dev. 2015, 30, 20–30. [Google Scholar]

- Prokopenko, O.; Cebula, J.; Chayen, S.; Pimonenko, T. Wind energy in Israel, Poland and Ukraine: Features and opportunities. Int. J. Ecol. Dev. 2017, 32, 98–107. [Google Scholar]

- Us, Y.; Pimonenko, T.; Lyulyov, O. The impact of energy efficiency policy on Ukraine’s green brand: A bibliometrics analysis. Polityka Energetyczna 2021, 24, 5–18. [Google Scholar] [CrossRef]

- Kharazishvili, Y.; Kwilinski, A.; Grishnova, O.; Dzwigol, H. Social Safety of Society for Developing Countries to Meet Sustainable Development Standards: Indicators, Level, Strategic Benchmarks (with Calculations Based on the Case Study of Ukraine). Sustainability 2020, 12, 8953. [Google Scholar] [CrossRef]

- Miśkiewicz, R. The Impact of Innovation and Information Technology on Greenhouse Gas Emissions: A Case of the Visegrád Countries. J. Risk Financ. Manag. 2021, 14, 59. [Google Scholar] [CrossRef]

- Miśkiewicz, R. Challenges facing management practice in the light of Industry 4.0: The example of Poland. Virtual Econ. 2019, 2, 37–47. [Google Scholar] [CrossRef]

- Drożdż, W.; Mróz-Malik, O.; Kopiczko, M. The Future of the Polish Energy Mix in the Context of Social Expectations. Energies 2021, 14, 5341. [Google Scholar] [CrossRef]

- Letunovska, N.; Lyuolyov, O.; Pimonenko, T.; Aleksandrov, V. Environmental management and social marketing: A bibliometric analysis. E3S Web Conf. 2021, 234, 00008. [Google Scholar] [CrossRef]

- Pimonenko, T.; Us, Y.; Lyulyova, L.; Kotenko, N. The impact of the macroeconomic stability on the energy-efficiency of the European countries: A bibliometric analysis. E3S Web Conf. 2021, 234, 00013. [Google Scholar] [CrossRef]

- Starchenko, L.; Lyeonov, S.; Vasylieva, T.; Pimonenko, T.; Lyulyov, O. Environmental management and green brand for sustainable entrepreneurship. E3S Web Conf. 2021, 234, 00015. [Google Scholar] [CrossRef]

- Sotnyk, I.; Shvets, I.; Momotiuk, L.; Chortok, Y. Management of Renewable Energy Innovative Development in Ukrainian Households: Problems of Financial Support. Mark. Manag. Innov. 2018, 4, 150–160. [Google Scholar] [CrossRef]

- Vakulenko, I.; Saher, L.; Lyulyov, O.; Pimonenko, T. A systematic literature review of smart grids. E3S Web Conf. 2021, 250, 08006. [Google Scholar] [CrossRef]

- Lyulyov, O.; Vakulenko, I.; Pimonenko, T.; Kwilinski, A.; Dzwigol, H.; Dzwigol-Barosz, M. Comprehensive assessment of smart grids: Is there a universal approach? Energies 2021, 14, 3497. [Google Scholar] [CrossRef]

- Cebula, J.; Chygryn, O.; Chayen, S.V.; Pimonenko, T. Biogas as an alternative energy source in Ukraine and Israel: Current issues and benefits. Int. J. Environ. Technol. Manag. 2018, 21, 421–438. [Google Scholar] [CrossRef]

- Lyulyov, O.; Paliienko, M.; Prasol, L.; Vasylieva, T.; Kubatko, O.; Kubatko, V. Determinants of shadow economy in transition countries: Economic and environmental aspects. Int. J. Glob. Energy Issues 2021, 43, 166–182. [Google Scholar] [CrossRef]

- O’Dwyer, K.J.; Malone, D. Bitcoin Mining and its Energy Footprint. In Proceedings of the 5th IET Irish Signals & Systems Conference 2014 and 2014 China-Ireland International Conference on Information and Communities Technologies (ISSC 2014/CIICT 2014), Limerick, Ireland, 26–27 June 2014. [Google Scholar] [CrossRef]

- Küfeoğlu, S.; Özkuran, M. Bitcoin mining: A global review of energy and power demand. Energy Res. Soc. Sci. 2019, 58, 101273. [Google Scholar] [CrossRef]

- Vranken, H. Sustainability of bitcoin and blockchains. Curr. Opin. Environ. Sustain. 2017, 28, 1–9. [Google Scholar] [CrossRef]

- Sedlmeir, J.; Buhl, H.U.; Fridgen, G.; Keller, R. The energy consumption of blockchain technology: Beyond myth. Bus. Inf. Syst. Eng. 2020, 62, 599–608. [Google Scholar] [CrossRef]

- Huynh, A.N.Q.; Duong, D.; Burggraf, T.; Luong, H.T.T.; Bui, N.H. Energy Consumption and Bitcoin Market. Asia-Pac. Financ. Mark. 2021, 29, 79–93. [Google Scholar] [CrossRef]

- Howson, P. Tackling climate change with blockchain. Nat. Clim. Chang. 2019, 9, 644–645. [Google Scholar] [CrossRef]

- Mora, C.; Rollins, R.L.; Taladay, K.; Kantar, M.B.; Chock, M.K.; Shimada, M.; Franklin, E.C. Bitcoin emissions alone could push global warming above 2 c. Nat. Clim. Chang. 2018, 8, 931. [Google Scholar] [CrossRef]

- Erdogan, S.; Ahmed, M.Y.; Sarkodie, S.A. Analysing asymmetric effects of cryptocurrency demand on environmental sustainability. Environ. Sci. Pollut. Res. 2022, 29, 31723–31733. [Google Scholar] [CrossRef]

- Wang, Y.; Lucey, B.; Vigne, S.A.; Yarovaya, L. An index of cryptocurrency environmental attention (ICEA). China Financ. Rev. Int. 2022. [Google Scholar] [CrossRef]

- Jiang, S.; Li, Y.; Lu, Q.; Hong, Y.; Guan, D.; Xiong, Y.; Wang, S. Policy assessments for the carbon emission flows and sustainability of bitcoin blockchain operation in China. Nat. Commun. 2021, 12, 1–10. [Google Scholar] [CrossRef]

- Goodkind, A.L.; Jones, B.A.; Berrens, R.P. Cryptodamages: Monetary value estimates of the air pollution and human health impacts of cryptocurrency mining. Energy Res. Soc. Sci. 2020, 59, 101281. [Google Scholar] [CrossRef]

- Di Febo, E.; Ortolano, A.; Foglia, M.; Leone, M.; Angelini, E. From bitcoin to carbon allowances: An asymmetric extreme risk spillover. J. Environ. Manag. 2021, 298, 113384. [Google Scholar] [CrossRef]

- De Vries, A.; Stoll, C. Bitcoin’s growing e-waste problem. Resour. Conserv. Recycl. 2021, 175, 105901. [Google Scholar] [CrossRef]

- Kwilinski, A.; Lyulyov, O.; Dzwigol, H.; Vakulenko, I.; Pimonenko, T. Integrative smart grids’ assessment system. Energies 2022, 15, 545. [Google Scholar] [CrossRef]

- Pimonenko, T.; Lyulyov, O.; Us, Y. Cointegration between economic, ecological and tourism development. J. Tour. Serv. 2021, 12, 169–180. [Google Scholar] [CrossRef]

- Polcyn, J.; Us, Y.; Lyulyov, O.; Pimonenko, T.; Kwilinski, A. Factors influencing the renewable energy consumption in selected European countries. Energies 2022, 15, 108. [Google Scholar] [CrossRef]

- Chygryn, O.; Lyulyov, O.; Pimonenko, T.; Mlaabdal, S. Efficiency of oil-production: The role of institutional factors. Eng. Manag. Prod. Serv. 2020, 12, 92–104. [Google Scholar] [CrossRef]

- Chygryn, O.; Pimonenko, T.; Luylyov, O.; Goncharova, A. Green bonds like the incentive instrument for cleaner production at the government and corporate levels: Experience from EU to Ukraine. J. Environ. Manag. Tour. 2018, 9, 1443–1456. [Google Scholar] [CrossRef]

- Cocco, L.; Pinna, A.; Marchesi, M. Banking on blockchain: Costs savings thanks to the blockchain technology. Future Internet 2017, 9, 25. [Google Scholar] [CrossRef]

- Sokolovska, A.; Zatonatska, T.; Stavytskyy, A.; Lyulyov, O.; Giedraitis, V. The impact of globalisation and international tax competition on tax policies. Res. World Econ. 2020, 11, 1–15. [Google Scholar] [CrossRef]

- Tambovceva, T.; Ivanov, I.H.; Lyulyov, O.; Pimonenko, T.; Stoyanets, N.; Yanishevska, K. Food security and green economy: Impact of institutional drivers. Int. J. Glob. Environ. Issues 2020, 19, 158–176. [Google Scholar] [CrossRef]

- Melnyk, L.; Sineviciene, L.; Lyulyov, O.; Pimonenko, T.; Dehtyarova, I. Fiscal decentralisation and macroeconomic stability: The experience of Ukraine’s economy. Probl. Perspect. Manag. 2018, 16, 105–114. [Google Scholar] [CrossRef][Green Version]

- Lyulyov, O.; Pimonenko, T.; Kwilinski, A.; Us, Y. The heterogeneous effect of democracy, economic and political globalisation on renewable energy. E3S Web Conf. 2021, 250, 03006. [Google Scholar] [CrossRef]

- Lyulyov, O.; Lyeonov, S.; Tiutiunyk, I.; fzPodgórska, J. The impact of tax gap on macroeconomic stability: Assessment using panel VEC approach. J. Int. Stud. 2021, 14, 139–152. [Google Scholar] [CrossRef]

- Our World in Data. Available online: https://ourworldindata.org/co2-emissions (accessed on 17 April 2022).

- Shahbaz, M.; Lean, H.H.; Shabbir, M.S. Environmental Kuznets curve hypothesis in Pakistan: Cointegration and Granger causality. Renew. Sustain. Energy Rev. 2012, 16, 2947–2953. [Google Scholar] [CrossRef]

- World Data Bank. Available online: https://databank.worldbank.org/reports.aspx?source=2&series=NY.GDP.PCAP.CD&country= (accessed on 17 April 2022).

- Eurostat. Available online: https://ec.europa.eu/eurostat/databrowser/view/sdg_07_40/default/table?lang=en (accessed on 17 April 2022).

- Ukrstat. Available online: http://www.ukrstat.gov.ua (accessed on 17 April 2022).

- Crystal Blockchain. Available online: https://crystalblockchain.com/geography-of-international-blockchain-transactions/ (accessed on 17 April 2022).

- Gygli, S.; Haelg, F.; Potrafke, N.; Sturm, J.E. The KOF globalisation index–revisited. Rev. Int. Organ. 2019, 14, 543–574. [Google Scholar] [CrossRef]

- Porter, M.; Kramer, M. Creating Shared Value. Harv. Bus. Rev. 2011, 89, 62–77. [Google Scholar]

- Truby, J.; Brown, R.D.; Dahdal, A.; Ibrahim, I. Blockchain, climate damage, and death: Policy interventions to reduce the carbon emissions, mortality, and net-zero implications of non-fungible tokens and Bitcoin. Energy Res. Soc. Sci. 2022, 88, 102499. [Google Scholar] [CrossRef]

- Benetton, M.; Compiani, G.; Morse, A. Crypto Mining: Pollution, Government Incentives, and Energy Crowding-Out. 2019. Available online: https://www.nber.org/system/files/chapters/c14530/c14530.pdf (accessed on 17 April 2022).

- Putranti, I.R. Crypto Mining: Indonesia Carbon Tax Challenges and Safeguarding International Commitment on Human Security. Int. J. Bus. Econ. Soc. Dev. 2022, 3, 10–18. [Google Scholar] [CrossRef]

- Jakob, M. Globalization and climate change: State of knowledge, emerging issues, and policy implications. Wiley Interdiscip. Rev. Clim. Chang. 2022, 85, e771. [Google Scholar] [CrossRef]

{kind=link}

| Variables | Symbol | Sources |

|---|---|---|

| Carbon dioxide emissions | CO2 | Our World in Data [90] |

| Gross domestic product per capita | GDP | World Data Bank [92] |

| A share of renewable energy in final energy consumption | RE | Eurostat [93]; Ukrstat [94] |

| International blockchain transactions received | CT | Crystal Blockchain [95] |

| Real gross fixed capital formation | GFCF | World Data Bank [92] |

| Labour force | LF | World Data Bank [92] |

| Globalisation | GI | KOF Globalisation Index [96] |

| Economic openness (Trade (% of GDP)) | EO | World Data Bank [92] |

| Variables | Mean | Median | Maximum | Minimum | Std. Dev. | Skewness | Kurtosis | Jarque–Bera |

|---|---|---|---|---|---|---|---|---|

| CO2 | 3.74 × 108 | 3.37 × 108 | 8.31 × 108 | 1.54 × 108 | 1.90 × 108 | 1.275 | 3.715 | 13.734 |

| GDP | 33,152.39 | 40,578.64 | 53,018.63 | 2124.662 | 16,392.180 | −0.773 | 2.172 | 6.023 |

| RE | 11.421 | 11.495 | 18.267 | 2.6 | 5.036 | −0.288 | 1.692 | 4.004 |

| CT | 117,665.5 | 10.199 | 4,681,000 | 0.006 | 691,092.7 | 6.347 | 42.252 | 3332.823 |

| GFCF | 3.66 × 1011 | 3.62 × 1011 | 8.71 × 1011 | 1.45 × 1011 | 2.62 × 1011 | 0.261 | 1.799 | 3.357 |

| LF | 26,034,725 | 25,875,327 | 44,351,163 | 9,019,570 | 10,632,838 | 0.045 | 2.175 | 1.348 |

| GI | 84.501 | 87.185 | 92.838 | 70.241 | 5.744 | −0.802 | 2.869 | 5.072 |

| EO | 88.954 | 86.246 | 158.823 | 54.868 | 32.627 | 0.916 | 2.787 | 6.657 |

| Variables | Statistical Values | Levin, Lin and Chu | Im, Pesaran and Shin W-Stat | ADF-Fisher Chi-Square | Hadri |

|---|---|---|---|---|---|

| CO2 | statistics | −1.334 | 1.248 | 14.034 | 2.216 |

| probability | 0.091 | 0.089 | 0.059 | 0.000 | |

| GDP | statistics | −14.937 | −3.870 | 47.044 | 2.437 |

| probability | 0.000 | 0.000 | 0.000 | 0.007 | |

| RE | statistics | −9.527 | −2.248 | 38.056 | 2.991 |

| probability | 0.000 | 0.012 | 0.001 | 0.001 | |

| CT | statistics | −3.629 | −0.952 | 41.061 | 5.916 |

| probability | 0.000 | 0.017 | 0.000 | 0.000 | |

| GFCF | statistics | −8.942 | −1.866 | 31.092 | 6.091 |

| probability | 0.000 | 0.031 | 0.013 | 0.000 | |

| LF | statistics | −1.825 | 1.929 | 6.060 | 3.589 |

| probability | 0.034 | 0.073 | 0.087 | 0.000 | |

| GI | statistics | −8.190 | −4.337 | 68.398 | 4.622 |

| probability | 0.000 | 0.003 | 0.000 | 0.000 | |

| OE | statistics | −1.789 | 1.327 | 23.990 | 3.789 |

| probability | 0.036 | 0.009 | 0.089 | 0.000 |

| Statistical Values | Panel v-Statistic | Panel Rho-Statistic | Panel PP-Statistic | Panel ADF-Statistic | Statistic Values | Group Rho-Statistic | Group PP-Statistic | Group ADF-Statistic |

|---|---|---|---|---|---|---|---|---|

| Series: GDP, LF, GFCF, RE, CT, GI, EO | ||||||||

| Within-dimension | Between-dimension | |||||||

| statistics | −0.797 | 1.905 | −4.372 | −2.409 | statistics | 2.552 | −8.918 | −0.504 |

| probability | 0.787 | 0.972 | 0.000 | 0.008 | probability | 0.995 | 0.000 | 0.007 |

| Weighted | ||||||||

| statistics | −1.416 | 1.352 | −6.527 | −1.979 | ||||

| probability | 0.922 | 0.912 | 0.000 | 0.024 | ||||

| Series: CO2, GDP, RE, CT, GI, EO | ||||||||

| statistics | 2.922 | 0.518 | 1.117 | 1.493 | statistics | 1.805 | 1.627 | 1.582 |

| probability | 0.002 | 0.008 | 0.068 | 0.932 | probability | 0.065 | 0.948 | 0.943 |

| Weighted | ||||||||

| statistics | 3.461 | 0.426 | 1.122 | 0.777 | ||||

| probability | 0.000 | 0.065 | 0.869 | 0.781 | ||||

| Series: GDP, LF, GFCF, RE, CT, GI, EO Model Specification: No Deterministic Trend | t-Statistic | Prob. |

|---|---|---|

| ADF | −2.111216 | 0.0174 |

| Residual variance | 0.001322 | |

| HAC variance | 0.000894 | |

| Series: CO2, GDP, RE, CT, GI, EO Model specification: No deterministic trend | ||

| ADF | −3.49021 | 0.0002 |

| Residual variance | 0.008482 | |

| HAC variance | 0.007344 | |

| Dependent Variables | Independent Variables | Coefficient | Probability | Dependent Variables | Independent Variables | Coefficient | Probability |

|---|---|---|---|---|---|---|---|

| GDP | GFCF | 0.802 | 0.002 | RE | GDP | 2.214 | 0.042 |

| LF | −1.598 | 0.498 | GFCF | 2.558 | 0.024 | ||

| RE | 0.064 | 0.027 | LF | −2.094 | 0.075 | ||

| CT | 0.017 | 0.081 | CT | −0.024 | 0.271 | ||

| GI | −0.126 | 0.937 | GI | −1.290 | 0.303 | ||

| OE | 0.519 | 0.348 | OE | −0.177 | 0.593 | ||

| GFCF | GDP | 0.840 | 0.001 | CT | GDP | 7.533 | 0.423 |

| LF | 1.845 | 0.378 | GFCF | −5.842 | 0.552 | ||

| RE | 0.034 | 0.846 | LF | 6.742 | 0.461 | ||

| CT | 0.010 | 0.268 | RE | −1.492 | 0.623 | ||

| GI | −0.688 | 0.621 | GI | −3.732 | 0.800 | ||

| OE | −0.298 | 0.569 | OE | −3.428 | 0.369 | ||

| LF | GDP | −1.026 | 0.000 | CO2 | GDP | −5.722 | 0.316 |

| GFCF | 1.079 | 0.000 | GDP2 | 0.235 | 0.359 | ||

| RE | −0.207 | 0.129 | RE | 1.043 | 0.026 | ||

| CT | 0.005 | 0.580 | CT | 0.019 | 0.071 | ||

| GI | −0.057 | 0.915 | GI | 11.939 | 0.106 | ||

| OE | −0.033 | 0.803 | EO | −0.451 | 0.366 |

| Dependent Variables | Independent Variables | Coefficient | Probability | Dependent Variables | Independent Variables | Coefficient | Probability |

|---|---|---|---|---|---|---|---|

| GDP | GFCF | 1.018 | 0.000 | RE | GDP | 1.479 | 0.006 |

| LF | 0.941 | 0.000 | GFCF | 1.864 | 0.000 | ||

| RE | 0.208 | 0.002 | LF | −1.409 | 0.007 | ||

| CT | 0.006 | 0.078 | CT | −0.003 | 0.870 | ||

| GI | 0.005 | 0.990 | GI | −1.662 | 0.155 | ||

| OE | −0.021 | 0.838 | OE | −0.045 | 0.885 | ||

| GFCF | GDP | 0.932 | 0.000 | CT | GDP | 7.529 | 0.268 |

| LF | 0.873 | 0.000 | GFCF | −6.314 | 0.377 | ||

| RE | 0.240 | 0.000 | LF | 6.482 | 0.325 | ||

| CT | 0.005 | 0.085 | RE | −0.484 | 0.852 | ||

| GI | 0.347 | 0.367 | GI | −1.896 | 0.890 | ||

| OE | −0.037 | 0.709 | OE | −1.964 | 0.575 | ||

| LF | GDP | 1.010 | 0.000 | CO2 | GDP | 1.239 | 0.026 |

| GFCF | 1.024 | 0.000 | GDP2 | −0.081 | 0.502 | ||

| RE | 0.213 | 0.003 | RE | 0.382 | 0.239 | ||

| CT | 0.006 | 0.334 | CT | 0.013 | 0.043 | ||

| GI | 0.277 | 0.510 | GI | 3.814 | 0.197 | ||

| OE | −0.078 | 0.467 | EO | −0.520 | 0.142 |

| Variables | Characteristics | Short-Term | Long-Term | ||||||

|---|---|---|---|---|---|---|---|---|---|

| D(GDP) | D(GFCF) | D(LF) | D(RE) | D(CT) | D(GI) | D(OE) | |||

| D(GDP) | statistics | - | 0.636 | 0.985 | 0.113 | 0.000 | −0.726 | −0.732 | −0.426 |

| probability | 0.000 | 0.556 | 0.073 | 0.070 | 0.349 | 0.055 | 0.010 | ||

| D(GFCF) | statistics | 0.771 | - | 0.723 | 0.185 | 0.009 | 0.360 | 0.506 | −0.176 |

| probability | 0.000 | 0.695 | 0.286 | 0.096 | 0.675 | 0.238 | 0.354 | ||

| D(LF) | statistics | 0.012 | 0.007 | - | 0.007 | −0.001 | 0.072 | 0.007 | −0.040 |

| probability | 0.556 | 0.695 | 0.699 | 0.267 | 0.407 | 0.874 | 0.030 | ||

| D(RE) | statistics | 0.158 | 0.212 | 0.764 | - | 0.002 | −0.257 | −0.811 | −0.297 |

| probability | 0.073 | 0.086 | 0.699 | 0.720 | 0.780 | 0.073 | 0.042 | ||

| D(CT) | statistics | 0.259 | 10.105 | −67.307 | 2.076 | - | 56.250 | 11.184 | −12.373 |

| probability | 0.070 | 0.096 | 0.267 | 0.720 | 0.041 | 0.435 | 0.044 | ||

| D(GI) | statistics | −0.042 | 0.017 | 0.332 | −0.011 | 0.002 | - | −0.065 | −0.043 |

| probability | 0.349 | 0.675 | 0.407 | 0.780 | 0.041 | 0.490 | 0.305 | ||

| D(OE) | statistics | 0.166 | 0.094 | 0.127 | −0.132 | 0.002 | -0.256 | - | 0.018 |

| probability | 0.055 | 0.238 | 0.874 | 0.073 | 0.435 | 0.490 | 0.829 | ||

| H0 | F-Stat. | Prob. | H0 | F-Stat. | Prob. | H0 | F-Stat. | Prob. | H0 | F-Stat. | Prob. |

|---|---|---|---|---|---|---|---|---|---|---|---|

| GFCF → GDP | 4.470 | 0.018 | GFCF → LF | 1.383 | 0.264 | GI → LF | 6.631 | 0.004 | CT → OE | 1.935 | 0.161 |

| GDP → GFCF | 5.808 | 0.006 | RE → GFCF | 1.706 | 0.196 | LF → GI | 1.527 | 0.234 | OE → GI | 0.240 | 0.788 |

| LF → GDP | 0.288 | 0.751 | GFCF → RE | 5.608 | 0.008 | OE → LF | 1.987 | 0.152 | GI → OE | 1.393 | 0.264 |

| GDP → LF | 2.419 | 0.003 | CT → GFCF | 1.824 | 0.178 | LF → OE | 1.058 | 0.358 | GDP → CO2 | 0.239 | 0.789 |

| RE → GDP | 2.527 | 0.094 | GFCF → CT | 4.286 | 0.022 | CT → RE | 0.676 | 0.516 | CO2 → GDP | 14.476 | 0.000 |

| GDP → RE | 2.672 | 0.083 | GI → GFCF | 1.405 | 0.261 | RE → CT | 1.328 | 0.279 | RE → CO2 | 4.436 | 0.019 |

| CT → GDP | 2.714 | 0.082 | GFCF → GI | 2.629 | 0.089 | GI → RE | 0.687 | 0.511 | CO2 → RE | 0.669 | 0.518 |

| GDP → CT | 4.119 | 0.026 | OE → GFCF | 6.857 | 0.003 | RE → GI | 0.607 | 0.552 | CT → CO2 | 3.492 | 0.043 |

| GI → GDP | 3.285 | 0.051 | GFCF → OE | 0.305 | 0.739 | OE → RE | 2.430 | 0.102 | CO2 → CT | 2.656 | 0.086 |

| GDP → GI | 6.649 | 0.004 | RE → LF | 0.497 | 0.613 | RE → OE | 0.044 | 0.957 | GI → CO2 | 0.280 | 0.757 |

| OE → GDP | 0.259 | 0.773 | LF → RE | 2.133 | 0.133 | GI → CT | 0.361 | 0.701 | CO2 → GI | 1.971 | 0.157 |

| GDP → OE | 0.349 | 0.708 | CT → LF | 0.524 | 0.597 | CT → GI | 0.165 | 0.849 | OE → CO2 | 0.784 | 0.464 |

| LF → GFCF | 0.367 | 0.695 | LF → CT | 1.183 | 0.320 | OE → CT | 1.250 | 0.300 | CO2 → OE | 0.157 | 0.855 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Miśkiewicz, R.; Matan, K.; Karnowski, J. The Role of Crypto Trading in the Economy, Renewable Energy Consumption and Ecological Degradation. Energies 2022, 15, 3805. https://doi.org/10.3390/en15103805

Miśkiewicz R, Matan K, Karnowski J. The Role of Crypto Trading in the Economy, Renewable Energy Consumption and Ecological Degradation. Energies. 2022; 15(10):3805. https://doi.org/10.3390/en15103805

Chicago/Turabian StyleMiśkiewicz, Radosław, Krzysztof Matan, and Jakub Karnowski. 2022. "The Role of Crypto Trading in the Economy, Renewable Energy Consumption and Ecological Degradation" Energies 15, no. 10: 3805. https://doi.org/10.3390/en15103805

APA StyleMiśkiewicz, R., Matan, K., & Karnowski, J. (2022). The Role of Crypto Trading in the Economy, Renewable Energy Consumption and Ecological Degradation. Energies, 15(10), 3805. https://doi.org/10.3390/en15103805