Towards Deep Decarbonisation of Energy-Intensive Industries: A Review of Current Status, Technologies and Policies

Abstract

1. Introduction

1.1. Background

1.2. Overview of Industrial Decarbonisation Worldwide

1.3. The Issues Considered

2. Materials and Methods

3. Characteristics of the Swedish Energy System and Basic Industries

3.1. Energy Portfolio

3.2. Emissions Profile: History, Present and Future Outlook

3.3. Swedish Energy-Intensive Industries (EIIs)

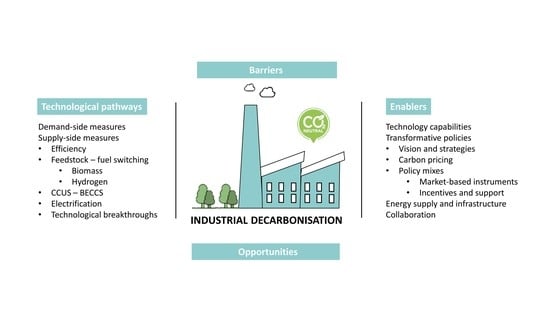

4. Industrial Decarbonisation

4.1. Technological Options

4.2. Decarbonising The Iron and Steel Industry

4.2.1. Current State

4.2.2. Decarbonisation Pathways

4.3. Decarbonising the Mining Industry

4.3.1. Current State

4.3.2. Decarbonisation Pathways

4.4. Decarbonising the Cement Industry

4.4.1. Current State

4.4.2. Decarbonisation Pathways

4.5. Decarbonising the Pulp and Paper Industry

4.5.1. Current State

4.5.2. Decarbonisation Pathways

4.6. Decarbonising the Refinery Sector

4.6.1. Current State

4.6.2. Decarbonisation Pathways

4.7. A Way Forward for Swedish EIIs

5. Drivers of Industrial Decarbonisation

5.1. Proactive Measures to Address the Climate and Energy Challenges

5.2. Policy Support

5.2.1. Relevant Policies at International, European and National Level

- Regulations reducing emissions of industrial gases

- Energy efficiency directive (EED)

- Renewable energy directive (RED)

- Funding for demonstration of innovative low-carbon technology and investment instruments that can provide capital to energy-intensive industries.

5.2.2. Carbon Pricing

5.2.3. Energy Efficiency Measures

5.2.4. RD&D and Technology Support

5.3. Cooperation

5.4. Technological Capabilities

5.5. Public Awareness about the Environment

6. Opportunities and Barriers

6.1. Opportunities

6.2. Barriers

- Technical

- Economic

- Market

- Institutional

7. Concluding Remarks and Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- United Nations/Framework Convention on Climate Change (UNFCCC). The Paris Agreement; United Nations: Paris, France, 2015. [Google Scholar]

- Smil, V. Energy Transitions: History, Requirements, Prospects; Praeger: Santa Barbara, CA, USA, 2010. [Google Scholar]

- Fattouh, B.; Poudineh, R.; West, R. The rise of renewables and energy transition: What adaptation strategy exists for oil companies and oil-exporting countries? Energy Transit. 2019, 3, 45–58. [Google Scholar] [CrossRef]

- Åhman, M.; Nilsson, L.J.; Johansson, B. Global climate policy and deep decarbonization of energy-intensive industries. Clim. Policy 2017, 17, 634–649. [Google Scholar] [CrossRef]

- Rissman, J.; Bataille, C.; Masanet, E.; Aden, N.; Morrow, W.R.; Zhou, N.; Elliott, N.; Dell, R.; Heeren, N.; Huckestein, B.; et al. Technologies and policies to decarbonize global industry: Review and assessment of mitigation drivers through 2070. Appl. Energy 2020, 266, 114848. [Google Scholar] [CrossRef]

- Wesseling, J.H.; Lechtenböhmer, S.; Åhman, M.; Nilsson, L.J.; Worrell, E.; Coenen, L. The transition of energy intensive processing industries towards deep decarbonization: Characteristics and implications for future research. Renew. Sustain. Energy Rev. 2017, 79, 1303–1313. [Google Scholar] [CrossRef]

- World Resources Institute. Climate Watch. Available online: https://www.wri.org/our-work/project/climatewatch/historical-emissions#project-tabs (accessed on 21 August 2020).

- International Energy Agency. Energy Technology Perspectives 2020; IEA: Paris, France, 2020. [Google Scholar]

- Fischedick, M.; Roy, J.; Abdel-Aziz, A.; Acquaye, A.; Allwood, J.M.; Ceron, J.-P.; Geng, Y.; Kheshgi, H.; Lanza, A.; Perczyk, D.; et al. Industry; Cambridge University Press: Cambridge, UK, 2014. [Google Scholar]

- Krausmann, F.; Gingrich, S.; Eisenmenger, N.; Erb, K.H.; Haberl, H.; Fischer-Kowalski, M. Growth in global materials use, GDP and population during the 20th century. Ecol. Econ. 2009, 68, 2696–2705. [Google Scholar] [CrossRef]

- International Energy Agency. Data and Statistics. Available online: https://www.iea.org/data-and-statistics?country=WORLD&fuel=CO2emissions&indicator=CO2BySector (accessed on 26 October 2020).

- European Commission. Final Report of the High-Level Panel of the European Decarbonisation Pathways Initiative; European Commission: Paris, France, 2018. [Google Scholar]

- European Commission. A Roadmap for Moving to a Competitive Low Carbon Economy in 2050; European Commision: Brussel, Belgium, 2011. [Google Scholar]

- Bramstoft, R.; Skytte, K. Decarbonizing Sweden’s energy and transportation system by 2050. Int. J. Sustain. Energy Plan. Manag. 2017, 14, 3–20. [Google Scholar] [CrossRef]

- International Energy Agency. Energy Policies of IEA Countries: Sweden 2019 Review; IEA: Paris, France, 2019. [Google Scholar]

- Energy Transitions Commision. Better Energy, Greater Prosperity: Achievable Pathways to Low-Carbon Energy Systems; ETC: London, UK, 2017. [Google Scholar]

- International Energy Agency. Energy Technology Perspectives 2017; IEA: Paris, France, 2017. [Google Scholar]

- Energy Transition Commission. Mission Possible: Reaching Net-Zero Carbon Emissions from Harder-to Abate Sectors by Mid-Century; ETC: London, UK, 2018. [Google Scholar]

- Energy Transitions Commission. Mission Possible: Reaching Net-Zero Carbon Emissions from Harder-to Abate Sectors by Mid-Century—Steel; ETC: London, UK, 2019. [Google Scholar]

- Energy Transitions Commission. Mission Possible: Reaching Net-Zero Carbon Emissions from Harder-to Abate Sectors by Mid-Century —Cement; ETC: London, UK, 2019. [Google Scholar]

- International Renewable Energy Agency. Reaching Zero with Renewables: Eliminating CO2 Emissions from Industry and Transport in Line with the 1.5 °C Climate Goal; IRENA: Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- Global CCS Institute. Global Status of CCS 2019: Targeting Climate Change; GCCSI: Melbourne, Australia, 2019. [Google Scholar]

- Roussanaly, S.; Berghout, N.; Fout, T.; Garcia, M.; Gardarsdottir, S.; Mohd, S.; Ramirez, A.; Rubin, E.S. Towards improved cost evaluation of Carbon Capture and Storage from industry. Int. J. Greenh. Gas Control. 2021, 106, 103263. [Google Scholar] [CrossRef]

- Global CCS Institute. Global Status of CCS 2020; GCCSI: Melbourne, Australia, 2020. [Google Scholar]

- Bataille, C.; Åhman, M.; Neuhoff, K.; Nilsson, L.J.; Fischedick, M.; Lechtenböhmer, S.; Solano-Rodriquez, B.; Denis-Ryan, A.; Stiebert, S.; Waisman, H.; et al. A review of technology and policy deep decarbonization pathway options for making energy-intensive industry production consistent with the Paris Agreement. J. Clean. Prod. 2018, 187, 960–973. [Google Scholar] [CrossRef]

- Ministry of the Environment and Energy. The Swedish Climate Policy Framework; Ministry of the Environment and Energy: Stockholm, Sweden, 2018.

- Naturvårdsverket. Underlag Till Regeringens Klimatpolitiska Handlingsplan. 2019. Available online: https://www.naturvardsverket.se/Documents/publikationer6400/978-91-620-6879-0.pdf?pid=24382 (accessed on 26 October 2020).

- Gode, J.; Särnholm, E.; Zetterberg, L.; Arnell, J.; Zetterberg, T. Swedish Long-Term Low Carbon Scenario; IVL Swedish Environmental Research Institute: Stockholm, Sweden, 2010. [Google Scholar]

- Johansson, M.T.; Söderström, M. Options for the Swedish steel industry—Energy efficiency measures and fuel conversion. Energy 2011, 36, 191–198. [Google Scholar] [CrossRef]

- Åhman, M.; Olsson, O.; Vogl, V.; Nyqvist, B.; Maltais, A.; Nilsson, L.J.; Hallding, K.; Skånberg, K.; Nilsson, M. Hydrogen Steelmaking for a Low-Carbon Economy: A Joint LU-SEI Working Paper for the HYBRIT Project; EESS report 109; Lunds Universitet: Lund, Sweden, 2018. [Google Scholar]

- Toktarova, A.; Karlsson, I.; Rootzén, J.; Göransson, L.; Odenberger, M.; Johnsson, F. Pathways for low-carbon transition of the steel industry—A Swedish case study. Energies 2020, 13, 3840. [Google Scholar] [CrossRef]

- Ahlström, J.M.; Zetterholm, J.; Pettersson, K.; Harvey, S.; Wetterlund, E. Economic potential for substitution of fossil fuels with liquefied biomethane in Swedish iron and steel industry—Synergy and competition with other sectors. Energy Convers. Manag. 2020, 209, 112641. [Google Scholar] [CrossRef]

- Karlsson, I.; Toktarova, A.; Rootzén, J.; Odenberger, M. Technical Roadmap Cement Industry; Mistra Carbon Exit: Stockholm, Sweden, 2020. [Google Scholar]

- Satti, S. Greenhouse Gas Abatement Strategies for the Chemical Industry in Sweden; KTH Royal Institute of Technology: Stockholm, Sweden, 2018. [Google Scholar]

- Åhman, M.; Nikoleris, A.; Nilsson, L.J. Decarbonising Industry in Sweden—An Assessment Of possibilities and Policy Needs; Lund University: Lund, Sweden, 2012; ISBN 978-91-86961-03-9. [Google Scholar]

- Klugman, S.; Stripple, H.; Lönnqvist, T.; Swedish Environmental Research Institute, I.; Sandberg, E.; Krook-Riekkola, A.; University of Technology, L. A Climate Neutral Swedish Industry—An Inventory of Technologies; IVL Swedish Environmental Research Institute: Stockholm, Sweden, 2019. [Google Scholar]

- Fossil Free Sweden. Roadmap for Fossil Free Competitiveness; Fossil Free Sweden: Stockholm, Sweden, 2018. [Google Scholar]

- Yin, R.K.; Campbell, D.T. Case study Research and Applications: Design and Methods; SAGE Publications: Thousand Oaks, CA, USA, 2018. [Google Scholar]

- Bhattacherjee, A. Social Science Research: Principles, Methods, and Practices; Global Text Project: Athens, GA, USA, 2012. [Google Scholar]

- Swedish Energy Agency. Energy in Sweden 2019; Swedish Energy Agency: Eskilstuna, Sweden, 2019.

- Energimyndigheten. Statistik Database: Annual Energy Balance. Available online: http://www.energimyndigheten.se/en/facts-and-figures/statistics/ (accessed on 24 August 2020).

- Urban, F.; Nordensvärd, J. Low carbon energy transitions in the nordic countries: Evidence from the environmental kuznets curve. Energies 2018, 11, 2209. [Google Scholar] [CrossRef]

- Swedish Climate Policy Council. 2019 Report of the Swedish Climate Policy Council; Swedish Climate Policy Council: Stokcholm, Sweden, 2019; ISBN 978-91-9846712-3.

- Kander, A. Economic Growth, Energy Consumption and CO2 Emissions in Sweden 1800–2000; Almqvist & Wiksell International: Stockholm, Sweden, 2002. [Google Scholar]

- Swedish Environmental Protection Agency. Greenhouse Gas Emissions and Removals. Available online: https://www.scb.se/en/finding-statistics/statistics-by-subject-area/environment/emissions/greenhouse-gas-emissions-and-removals/ (accessed on 24 August 2020).

- Svensson, O.; Khan, J.; Hildingsson, R. Studying industrial decarbonisation: Developing an interdisciplinary understanding of the conditions for transformation in energy-intensive natural resource-based industry. Sustainability 2020, 12, 2129. [Google Scholar] [CrossRef]

- Muhammad, H.A.; Roh, C.; Cho, J.; Rehman, Z.; Sultan, H.; Baik, Y.J.; Lee, B. A comprehensive thermodynamic performance assessment of CO2 liquefaction and pressurization system using a heat pump for carbon capture and storage (CCS) process. Energy Convers. Manag. 2020, 206, 112489. [Google Scholar] [CrossRef]

- Leung, D.Y.C.; Caramanna, G.; Maroto-Valer, M.M. An overview of current status of carbon dioxide capture and storage technologies. Renew. Sustain. Energy Rev. 2014, 39, 426–443. [Google Scholar] [CrossRef]

- European Commission. Horizon 2020 Work Programme 2014-2015: General Annexes; European Commision: Brussels, Belgium, 2014; Available online: https://ec.europa.eu/research/participants/data/ref/h2020/wp/2014_2015/annexes/h2020-wp1415-annex-ga_en.pdf (accessed on 26 October 2020).

- Anameric, B.; Kawatra, S.K. Direct iron smeling reduction processes. Miner. Process. Extr. Metall. Rev. 2009, 30, 1–51. [Google Scholar] [CrossRef]

- Quader, M.A.; Ahmed, S.; Ghazilla, R.A.R.; Ahmed, S.; Dahari, M. A comprehensive review on energy efficient CO2 breakthrough technologies for sustainable green iron and steel manufacturing. Renew. Sustain. Energy Rev. 2015, 50, 594–614. [Google Scholar] [CrossRef]

- Steelonthenet.com. Steel Industry Emissions of CO2. Available online: https://www.steelonthenet.com/kb/CO2-emissions.html (accessed on 10 September 2020).

- The European Steel Association (EUROFER). Low Carbon Roadmap: Pathways to a CO2-Neutral European Steel Industry; EUROFER: Brussels, Belgium, 2019. [Google Scholar]

- IEAGHG. Iron and Steel CCS Study (Techno-Economics Integrated Steel Mill), 2013/04; IEAGHG: Cheltenham, UK, 2013. [Google Scholar]

- Otto, A.; Robinius, M.; Grube, T.; Schiebahn, S.; Praktiknjo, A.; Stolten, D. Power-to-steel: Reducing CO2 through the integration of renewable energy and hydrogen into the German steel industry. Energies 2017, 10, 451. [Google Scholar] [CrossRef]

- Xylia, M.; Silveira, S.; Duerinck, J.; Meinke-Hubeny, F. Weighing regional scrap availability in global pathways for steel production processes. Energy Effic. 2018, 11, 1135–1159. [Google Scholar] [CrossRef]

- Onarheim, K.; Mathisen, A.; Arasto, A. Barriers and opportunities for application of CCS in Nordic industry-A sectorial approach. Int. J. Greenh. Gas Control 2015, 36, 93–105. [Google Scholar] [CrossRef]

- Chan, Y.; Petithuguenin, L.; Fleiter, T.; Herbst, A.; Arens, M.; Stevenson, P. Industrial Innovation: Pathways to Deep Decarbonisation of Industry. Part 1: Technology Analysis; ICF: London, UK, 2019. [Google Scholar]

- Kuramochi, T.; Ramírez, A.; Turkenburg, W.; Faaij, A. Comparative assessment of CO2 capture technologies for carbon-intensive industrial processes. Prog. Energy Combust. Sci. 2012, 38, 87–112. [Google Scholar] [CrossRef]

- Carpenter, A. CO2 Abatement in the Iron and Steel Industry; CCC/193; IEA Clean Coal Centre: London, UK, 2012; ISBN 978-92-9029-513-6. [Google Scholar]

- Kirschen, M.; Badr, K.; Pfeifer, H. Influence of direct reduced iron on the energy balance of the electric arc furnace in steel industry. Energy 2011, 36, 6146–6155. [Google Scholar] [CrossRef]

- HYBRIT. Fossil Free Steel; HYBRIT: Stockholm, Sweden, 2017. [Google Scholar]

- Vogl, V.; Åhman, M.; Nilsson, L.J. Assessment of hydrogen direct reduction for fossil-free steelmaking. J. Clean. Prod. 2018, 203, 736–745. [Google Scholar] [CrossRef]

- Axelson, M.; Robson, I.; Khandekar, G.; Wynys, T. Breaking through Industrial Low-CO2 Technologies on the Horizon; Institute for European Studies, Vrije Universiteit Brussel: Brussels, Belgium, 2018. [Google Scholar]

- Siderwin. Development of New Methodologies for Industrial CO2-Free Steel Production by Electrotwinning. Available online: https://www.siderwin-spire.eu/ (accessed on 10 September 2020).

- Pei, M.; Petäjäniemi, M.; Regnell, A.; Wijk, O. Toward a fossil free future with hybrit: Development of iron and steelmaking technology in Sweden and Finland. Metals 2020, 10, 972. [Google Scholar] [CrossRef]

- Triple Steelix. Nytt Projekt för Fossilfri Uppvärmning i Stålindustrins Ugnar. Available online: https://www.triplesteelix.se/sv-SE/projekt/platis-”plasmateknik-i-stålindustrins-ugnar”-43910363 (accessed on 24 September 2020).

- Jernkontoret. Klimatfärdplan för en Fossilfri och Konkurrenskraftig Stålindustri i Sverige; Jernkontoret: Stockholm, Sweden, 2018. [Google Scholar]

- Höganäs. Sustainability: Unique Plant for Renewable Energy Gas and Bio-Coke. Available online: https://www.hoganas.com/sv/sustainability/renewable-energy-gas-and-bio-coke/ (accessed on 9 September 2020).

- Sveriges Geologiska Undersökning (SGU). Mining Statistics 2016; SGU: Uppsala, Sweden, 2017. [Google Scholar]

- Svemin. Roadmap for Long-Term Competitiveness and a Fossil-Free Mining and Minerals Industry; Svemin: Stockholm, Sweden, 2018. [Google Scholar]

- Boliden Group. A Sustainable Future with Metals: Annual and Sustainability Report 2019; Boliden: Stockholm, Sweden, 2019. [Google Scholar]

- LKAB. Autonomous Vehicles, Electrification and Automation with a Focus on People. Available online: https://www.lkab.com/en/news-room/news/sjalvkorande-fordon-elektrifiering-och-automation-med-manniskan-i-centrum/ (accessed on 10 September 2020).

- LKAB. Leading the Way to Decarbonisation. Available online: https://www.lkab.com/en/news-room/news/leading-the-way-to-decarbonisation/ (accessed on 10 September 2020).

- Wilhelmsson, B.; Kolberg, C.; Larsson, J.; Eriksson, J.; Eriksson, M. CemZero—Feasibility Study; Vattenfall, Cementa: Stockholm, Sweden, 2018. [Google Scholar]

- Cementa. Nollvision för Koldioxid [Zero Vision for Carbon Dioxide]; Cementa: Stockholm, Sweden, 2018. [Google Scholar]

- Cementa. Färdplan Cement för ett Klimatneutralt Betongbyggande; Cementa: Stockholm, Sweden, 2018. [Google Scholar]

- Hasanbeigi, A.; Price, L.; Lin, E. Emerging energy-efficiency and CO2 emission-reduction technologies for cement and concrete production: A technical review. Renew. Sustain. Energy Rev. 2012, 16, 6220–6238. [Google Scholar] [CrossRef]

- Hoenig, M.S.V. CO2 reduction in the cement industry. In Proceedings of the VDZ Congress, Dusseldorf, Germany, 22 September 2002; pp. 489–492. [Google Scholar]

- Cormos, A.-M.; Dragan, S.; Petrescu, L.; Sandu, V.; Cormos, C.-C. Techno-economic and environmental evaluations of decarbonized fossil-intensive industrial processes by reactive absorption & adsorption CO2 capture systems. Energies 2020, 13, 1268. [Google Scholar] [CrossRef]

- Leeson, D.; Mac Dowell, N.; Shah, N.; Petit, C.; Fennell, P.S. A techno-economic analysis and systematic review of carbon capture and storage (CCS) applied to the iron and steel, cement, oil refining and pulp and paper industries, as well as other high purity sources. Int. J. Greenh. Gas Control. 2017, 61, 71–84. [Google Scholar] [CrossRef]

- European Commission. Technological Pathways and Some Examples of Projects in Cement Sector. Available online: https://ec.europa.eu/transparency/regexpert/index.cfm?do=groupDetail.groupDetailDoc&id=39572&no=2 (accessed on 25 September 2020).

- International Energy Agency; Cement Sustainability Initiative. Technology Roadmap for Cement; IEA: Paris, France, 2018. [Google Scholar]

- Lechtenböhmer, S.; Nilsson, L.J.; Åhman, M.; Schneider, C. Decarbonising the energy intensive basic materials industry through electrification—Implications for future EU electricity demand. Energy 2016, 115, 1623–1631. [Google Scholar] [CrossRef]

- European Commission. Deep Decarbonisation of Industry: The Cement Sector; European Commission: Brussels, Belgium, 2020. [Google Scholar]

- Lehne, J.; Preston, F. Making Concrete Change: Innovation in Low-Carbon Cement and Concrete; Chatham House: London, UK, 2018. [Google Scholar]

- Bataille, C. Low and Zero Emissions in the Steel and Cement Industries Barriers, Technologies and Policies; OECD Publishing: Paris, France, 2020; pp. 2–42. [Google Scholar]

- Rootzén, J.; Johnsson, F. Technologies and policies for GHG emission reductions along the supply chains for the Swedish construction industry. In Proceedings of the ECEEE 2017 Summer Study, Belambra Presqu’île de Giens, France, 29 May–3 June 2017. [Google Scholar]

- Nataly Echevarria Huaman, R.; Xiu Jun, T. Energy related CO2 emissions and the progress on CCS projects: A review. Renew. Sustain. Energy Rev. 2014, 31, 368–385. [Google Scholar] [CrossRef]

- Bao, J.; Zhang, L.; Song, C.; Zhang, N.; Guo, M.; Zhang, X. Reduction of efficiency penalty for a natural gas combined cycle power plant with post-combustion CO2 capture: Integration of liquid natural gas cold energy. Energy Convers. Manag. 2019, 198, 111852. [Google Scholar] [CrossRef]

- Johansson, D.; Franck, P.Å.; Berntsson, T. CO2 capture in oil refineries: Assessment of the capture avoidance costs associated with different heat supply options in a future energy market. Energy Convers. Manag. 2013, 66, 127–142. [Google Scholar] [CrossRef]

- Voldsund, M.; Anantharaman, R.; Berstad, D.; De Lena, E.; Fu, C.; Gardarsdottir, S.O.; Jamali, A.; Pérez-Calvo, J.; Romano, M.; Roussanaly, S.; et al. CEMCAP Comparative Techno-Economic Analysis of CO2 Capture in Cement Plants (D4.6); SINTEF: Trondheim, Norway, 2019. [Google Scholar] [CrossRef]

- Skogsindustrierna. Roadmap for Fossil Free Competitiveness: Forest Sector; Fossil Free Sweden: Stockholm, Sweden, 2018. [Google Scholar]

- Moshkelani, M.; Marinova, M.; Perrier, M.; Paris, J. The forest biorefinery and its implementation in the pulp and paper industry: Energy overview. Appl. Therm. Eng. 2013, 50, 1427–1436. [Google Scholar] [CrossRef]

- Rafione, T.; Marinova, M.; Montastruc, L.; Paris, J. The green integrated forest biorefinery: An innovative concept for the pulp and paper mills. Appl. Therm. Eng. 2014, 73, 74–81. [Google Scholar] [CrossRef]

- Ericsson, K.; Nilsson, L.J. Climate Innovations in the Paper Industry: Prospects for Decarbonisation (D2.4); IMES/EESS Report Series, 110, Miljö-och Energisystem; LTH, Lunds Universitet: Lund, Sweden, 2018. [Google Scholar]

- Pettersson, K.; Mahmoudkhani, M.; von Schenck, A. Opportunities for Biorefineries in the Pulping Industry. In Systems Perspectives on Biorefineries; Sandén, B., Pettersson, K., Eds.; Chalmers University of Technology: Göteborg, Sweden, 2014. [Google Scholar]

- Naqvi, M.; Yan, J.; Dahlquist, E. Black liquor gasification integrated in pulp and paper mills: A critical review. Bioresour. Technol. 2010, 101, 8001–8015. [Google Scholar] [CrossRef] [PubMed]

- Larsson, A.; Nordin, A.; Backman, R.; Warnqvist, B.; Eriksson, G. Influence of black liquor variability, combustion, and gasification process variables and inaccuracies in thermochemical data on equilibrium modeling results. Energy Fuels 2006, 20, 359–363. [Google Scholar] [CrossRef]

- Ferreira, A.F.; Dias, A.P.S.; Silva, C.M.; Costa, M. Evaluation of thermochemical properties of raw and extracted microalgae. Energy 2015, 92, 365–372. [Google Scholar] [CrossRef]

- Hrbek, J. Status Report on Thermal Biomass Gasification in Countries Participating in IEA Bioenergy Task 33; IEA Bioenergy: Paris, France, 2016. [Google Scholar]

- Bajpai, P. Chapter 11—Emerging technologies. In Pulp and Paper Industry: Energy Conservation; Bajpai, P., Ed.; Elsevier: Amsterdam, The Netherlands, 2016; ISBN 9780128034118. [Google Scholar]

- IEA Bioenergy. Implementation Agendas: 2018–2019 Update Compare and Contrast Transport Biofuels Policies; IEA Bioenergy: Paris, France, 2019. [Google Scholar]

- Smink, D.; Kersten, S.R.A.; Schuur, B. Process development for biomass delignification using deep eutectic solvents. Conceptual design supported by experiments. Chem. Eng. Res. Des. 2020, 164, 86–101. [Google Scholar] [CrossRef]

- Sherrard, A. Record Third Quarter Sales of HVO in Sweden. Available online: https://www.svebio.se/en/press/pressmeddelanden/record-third-quarter-sales-hvo-sweden/ (accessed on 26 October 2020).

- Preem. Sustainability Report 2019; Preem: Stockholm, Sweden, 2019. [Google Scholar]

- Institute for European Studies. A Bridge towards a Carbon Neutral Europe; IES: Brussels, Belgium, 2018. [Google Scholar]

- Naturvårdsverket. Scenarier över Utsläpp och Upptag av Växthusgaser 2019; Naturvårdsverket: Stockholm, Sweden, 2019. [Google Scholar]

- Jernkontoret. Production. Available online: https://www.jernkontoret.se/en/the-steel-industry/industry-facts-and-statistics/production/ (accessed on 11 September 2020).

- Rootzén, J.; Johnsson, F. CO2 emissions abatement in the Nordic carbon-intensive industry—An end-game in sight? Energy 2015, 80, 715–730. [Google Scholar] [CrossRef]

- Ryhagen, Å. Pulp & paper in Sweden. Available online: http://www.pptgroup.se/index.php/about-2/pulp-paper-in-sweden/#:~:text=Swedentodayproduces6.2million,363000tonsoftissue (accessed on 11 September 2020).

- Rehfeldt, M.; Worrell, E.; Eichhammer, W.; Fleiter, T. A review of the emission reduction potential of fuel switch towards biomass and electricity in European basic materials industry until 2030. Renew. Sustain. Energy Rev. 2020, 120, 109672. [Google Scholar] [CrossRef]

- Sweco. Klimatneutral Konkurrenskraft—Kvantifiering av Åtgärder i Klimatfärdplaner; Sweco: Stockholm, Sweden, 2019. [Google Scholar]

- Svemin. Färdplan för en Konkurrenskraftig och Fossilfri Gruv- och Mineralnäring; Svemin: Stockholm, Sweden, 2018. [Google Scholar]

- Börjesson, M.; Athanassiadis, D.; Lundmark, R.; Ahlgren, E.O. Bioenergy futures in Sweden—system effects of CO2 reduction and fossil fuel phase-out policies. GCB Bioenergy 2015, 7, 1118–1135. [Google Scholar] [CrossRef]

- International Energy Agency and Norden. Nordic Energy Technology Perspectives 2016; OECD/IEA: Paris, France, 2016. [Google Scholar]

- Kan, X.; Hedenus, F.; Reichenberg, L. The cost of a future low-carbon electricity system without nuclear power—the case of Sweden. Energy 2020, 195, 117015. [Google Scholar] [CrossRef]

- Nykvist, B.; Maltais, A.; Olsson, O. Financing the Decarbonisation of Heavy Industry Sectors in Sweden; SEI: Stockholm, Sweden, 2020. [Google Scholar]

- Katofsky, R.; Stanberry, M.; Hagenstad, M.; Frantzis, L. Climate Change Adaptation, Damages and Fossil Fuel Dependence: An RETD Position Paper on the Costs of Inaction; IEA-RTD: Paris, France, 2011. [Google Scholar]

- Calmfors, L.; Hassler, J.; Nasiritousi, N.; Bäckstrand, K.; Silbye, F.; Sørensen, P.B.; Carlén, B.; Kriström, B.; Greaker, M.; Golombek, R.; et al. Climate Policies in the Nordics—Nordic Economic Policy Review 2019; Nordic Council of Ministers: Copenhagen, Denmark, 2019; ISBN 9789289360883. [Google Scholar]

- European Commission. A 2030 Framework for Climate and Energy Policies; COM(2013) 169 Final; European Commission: Brussels, Belgium, 2013. [Google Scholar]

- European Commission. European Commission—Press Release. Available online: https://ec.europa.eu/commission/presscorner/detail/en/ip_20_1599 (accessed on 23 September 2020).

- Ministry of the Environment. Sweden’s Sixth National Communication on Climate Change; Ministry of the Environment: Stockholm, Sweden, 2014.

- Hammar, H.; Åkerfeldt, S. CO2 Taxation in Sweden: 20 years of Experience and Looking Ahead. Available online: https://www.globalutmaning.se/wp-content/uploads/sites/8/2011/10/Swedish_Carbon_Tax_Akerfedlt-Hammar.pdf (accessed on 26 October 2020).

- European Commission. EU ETS Handbook; European Commission: Brussels, Belgium, 2015. [Google Scholar]

- Naturvårdsverket. National Inventory Report Sweden 2019—Greenhouse Gas Emission Inventories 1990–2017; Naturvårdsverket: Stockholm, Sweden, 2014. [Google Scholar]

- Egenhofer, C.; Alessi, M.; Georgiev, A.; Fujiwara, N. The EU Emissions Trading System and Climate Policy Towards 2050 Real Incentives to Reduce Emissions and Drive Innovation; Centre for European Policy Studies: Brussels, Belgium, 2011. [Google Scholar]

- Brown, L.M.; Hanafi, A.; Petsonk, A. The EU Emissions Trading System: Results and Lesson Learned; Environmental Defense Fund: New York, NY, USA, 2012. [Google Scholar]

- Hu, J.; Crijns-Graus, W.; Lam, L.; Gilbert, A. Ex-ante evaluation of EU ETS during 2013–2030: EU-internal abatement. Energy Policy 2015, 77, 152–163. [Google Scholar] [CrossRef]

- Kettner, C.; Kletzan-Slamanig, D.; Köppl, A.; Schinko, T.; Türk, A. Price Volatility in Carbon Markets: Why It Matters and How It Can Be Managed; WIFO: Vienna, Austria, 2011. [Google Scholar]

- Bayer, P.; Aklin, M. The European Union Emissions Trading System reduced CO2 emissions despite low prices. Proc. Natl. Acad. Sci. USA 2020, 117, 8804–8812. [Google Scholar] [CrossRef]

- Wråke, M.; Burtraw, D.; Löfgren, Å.; Zetterberg, L. What have we learnt from the European union’s emissions trading system? Ambio 2012, 41, 12–22. [Google Scholar] [CrossRef] [PubMed]

- Åhman, M. EU Emissions Trading Scheme: Contentious Issues; IVL Swedish Environment Research Institute: Stockholm, Sweden, 2007. [Google Scholar]

- Felbermayr, G.; Peterson, S. Economic Assessment of Carbon Leakage and Carbon Border Adjustment; European Parliament: Brussels, Belgium, 2020; ISBN 978-92-846-6753-6. [Google Scholar]

- Ferguson, S.; Sanctuary, M. Why is carbon leakage for energy-intensive industry hard to find? Environ. Econ. Policy Stud. 2019, 21, 1–24. [Google Scholar] [CrossRef]

- Branger, F.; Quirion, P.; Chevallier, P. Carbon leakage and competitiveness of cement and steel industries under the EU ETS: Much ado about nothing. Energy J. 2017, 37, 3. [Google Scholar] [CrossRef]

- Grubb, M.; Counsell, T. Tackling Carbon Leakage Sector-Specific Solutions for a World of Unequal Carbon Prices; Carbon Trust: Cambridge, UK, 2010. [Google Scholar]

- Vivid Economics; Ecofys. Carbon Leakage Prospects under Phase III of the EU ETS and Beyond. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/318893/carbon_leakage_prospects_under_phase_III_eu_ets_beyond.pdf (accessed on 30 March 2021).

- Arlinghaus, J. Impacts of Carbon Prices on Indicators of Competitiveness: A Review of Empirical Findings; OECD: Paris, France, 2015. [Google Scholar]

- Löfgren, A.; Wråke, M.; Hagberg, T.; Roth, S. The Effect of EU-ETS on Swedish Industry’s Investment in Carbon Mitigating Technologies; University of Gothenburg: Gothenburg, Sweden, 2013; ISSN 1403-2465. [Google Scholar]

- Ministry of the Environment and Energy. Sweden’s Draft Integrated National Energy and Climate Plan; Ministry of the Environment and Energy: Stockholm, Sweden, 2020.

- Fischer, C.; Newell, R.G. Environmental and technology policies for climate mitigation. J. Environ. Econ. Manag. 2008, 55, 142–162. [Google Scholar] [CrossRef]

- Hanemann, M. Cap-and-trade: A sufficient or necessary condition for emission reduction? Oxford Rev. Econ. Policy 2010, 226, 225–252. [Google Scholar] [CrossRef]

- Popp, D. Innovation and climate policy. Annu. Rev. Resour. Econ. 2010, 2, 275–298. [Google Scholar] [CrossRef]

- European Commission. The EU Emissions Trading System (EU ETS). Available online: https://ec.europa.eu/clima/policies/ets_en (accessed on 30 March 2021).

- Karakaya, E.; Nuur, C.; Assbring, L. Potential transitions in the iron and steel industry in Sweden: Towards a hydrogen-based future? J. Clean. Prod. 2018, 195, 651–663. [Google Scholar] [CrossRef]

- Thomassen, G.; Van Passel, S.; Dewulf, J. A review on learning effects in prospective technology assessment. Renew. Sustain. Energy Rev. 2020, 130, 109937. [Google Scholar] [CrossRef]

- Rahman, M.M. Green Products: A Study on Young & Native Swedish Consumers’ Purchase Intentions of Green Products; Umeå University: Umeå, Sweden, 2013. [Google Scholar]

- Fankhauser, S.; Bowen, A.; Calel, R.; Dechezleprêtre, A.; Grover, D.; Rydge, J.; Sato, M. Who will win the green race? In search of environmental competitiveness and innovation. Glob. Environ. Chang. 2013, 23, 902–913. [Google Scholar] [CrossRef]

- Oberthür, S.; Khandekar, G.; Wyns, T. Global governance for the decarbonization of energy-intensive industries: Great potential underexploited. Earth Syst. Gov. 2020, 100072. [Google Scholar] [CrossRef]

- Stern, N. The Economics of Climate Change; Cambridge University Press: Cambridge, UK, 2004; ISBN 0203495780. [Google Scholar]

- Johnsson, F.; Kjärstad, J.; Rootzén, J. The threat to climate change mitigation posed by the abundance of fossil fuels. Clim. Policy 2019, 19, 258–274. [Google Scholar] [CrossRef]

- The Global Commission on the Economy and Climate. Better Growth Better Climate: The New Climate Economy Report; New Climate Economy: Washington, DC, USA, 2014. [Google Scholar]

- European Commission. State of the Union: Q & A on the 2030 Climate Target Plan. Available online: https://ec.europa.eu/commission/presscorner/detail/en/QANDA_20_1598 (accessed on 26 October 2020).

- HYBRIT. SSAB, LKAB and Vattenfall Building Unique Pilot Project in Luleå for Large-Scale Hydrogen Storage Investing a Quarter of a Billion Swedish Kronor. Available online: https://www.hybritdevelopment.se/en/april-7-2021-hybrit-ssab-lkab-and-vattenfall-building-unique-pilot-project-in-lulea-for-large-scale-hydrogen-storage-investing-a-quarter-of-a-billion-swedish-kronor/ (accessed on 12 April 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Technology | Description | Example | CO2 Intensity or Reduction Potential | Technology Readiness Level (TRL) 1 | References |

|---|---|---|---|---|---|

| Reference Steelmaking Technology | |||||

| Blast Furnace | The blast furnace (BF) is fed with iron ore, limestone and coke to produce liquid iron. The liquid iron is then converted into steel in a basic oxygen furnace (BOF). The BF partly re-uses the BF gas as fuel, but send most of the gas for use in other processes. Biochars have the potential to replace metallurgical coke, but only up to 10%. | 1.5–2.2 t CO2/t steel | Commercial (TRL 9) | [52,53,54] | |

| Electric Arc Furnace (EAF) | Steel scrap is heated and melted by heat of electric arcs. More than 40% of energy comes from chemical sources by fossil fuels: natural and coal. The fossil fuels could potentially be replaced by biofuels. | 0.6 t CO2/t steel | Commercial (TRL 9) | [55,56] | |

| Alternative Low-Carbon Technologies | |||||

| Top-gas recycling blast furnace (without CCUS) | The BF gas is conditioned and recycled in the process, thus re-introducing carbon monoxide and hydrogen (H2) in the process, which acts as reducing agents. | ULCOS-BF, IGAR | up to 25%; with CCUS can be up to 60% | TRL 7 | [54,57,58] |

| Smelting reduction (without CCUS) | Ores are partly reduced in the pre-reduction unit by using off gas from the smelting unit. Thereafter, final reduction and melting takes place in the smelting unit. The raw iron is then processed in a BOF to produce steel. Unlike the BF, smelting furnaces operations allows for full utilisation of biomass substitutes. | HIsarna | up to 35%, with CCUS can be up to 80% | Commercial (TRL 9) | [58,59,60] |

| Direct reduction using electrical arc furnaces | In the process, the reducing agents (natural gas) reacts with the iron ore without melting the iron. The product is a solid iron product called as sponge iron which must be melted afterwards for alloying purposes. | Midrex, HYL | 40–60% | Commercial (TRL 9) | [54,60,61] |

| Hydrogen direct reduction | Instead of natural gas, this process utilises H2 as the reducing agent. The produced sponge iron is then heated and melted in EAF. | HYBRIT, GrINHy, H2Future, SuSteel, SALCOS | Up to 95% | TRL 5–7 | [62,63,64] |

| Electrowinning | The electrolysis process transform iron ore into steel plate. With this technology, carbon is replaced by electricity. The BF would be an electric plant, with oxygen being the only gas emitted. | SIDERWIN, ULCOWIN | Up to 95% | TRL 5–6 | [9,64,65] |

| Carbon capture utilisation and storage | CO2 is captured either before or after combustion. The concept of partial capture is being explored to reduce the cost for CO2 capture in the industrial sector. The CO2 can also be used as a feedstock for chemical or material production. | Carbon2Chem, Steelanol | Typical capture rate: 90% | TRL 6–9 | [54] |

| Technology | Brief Description | CO2 Intensity or Reduction Potential | Technology Readiness Level (TRL) 1 | References |

|---|---|---|---|---|

| Cement Manufacturing Process | ||||

| Dry kilns | The raw materials are ground and dried to raw meal, and then fed to the precalciner kiln. This process is more thermally efficient than the conventional wet process. | 0.85 t CO2/t clinker | Commercial (TRL 9) | [75,79] |

| Carbon Capture and Storage (CCS) | ||||

| Chemical absorption | CO2 is captured after being generated in the cement kiln via chemical absorption. | Typical capture rate > 90% | TRL 7 | [75,80,81,82] |

| Oxy-fuel technology | Using pure oxygen instead of air to provide a high CO2 concentration exhaust gas stream for further capture. | Typical capture rate Full oxy-fuel > 90% Partial oxy-fuel~65% | TRL 7 | [59,78,82,83] |

| Calcium looping | Flue gas containing CO2 is reacted with CaO-based sorbent to form CaCO3. The CaCO3 is passed to the calciner to produce CaO that is passed back to the carbonator while leaving a pure CO2 stream behind. | Typical capture rate > 90% | TRL 7 | [59,80,81,82] |

| Electrification + CCS | Electrification of cement production combined with CCS | Potential = 0 t CO2/t clinker (if fossil free electricity is used) | TRL 2–4 | [75,82,84] |

| Fuel Switching | Depend on the fuel mix percentage | [85] | ||

| Biomass | Combusting biomass as a fuel to provide the necessary process heat. | TRL 9 | ||

| Hydrogen | Combusting hydrogen as a fuel to provide the high temperatures required in the cement manufacturing process. | TRL 2 | ||

| Alternative binders | Substitution of clinker with lower GHG cementious materials | Average 20–30% CO2 reduction. | ||

| Fly ash BF slag Limestone and calcined clays | Theoretical potential 60% reduction for substitution levels of over 70%. | TRL 9 TRL 7 TRL 5–7 | [86] [82,86] [82,86] | |

| Alternative cement chemistries Calcium sulfone aluminate, geopolymer, magnesium silicate, etc. | All these chemistries have potential to replace limestone, but require extensive piloting and commercialisation. | Depends on the chemistries | TRL 2–4 | [87] |

| Technology | Description | CO2 Reduction Potential | Technology Readiness Level (TRL) | Reference |

|---|---|---|---|---|

| Waste heat recovery | Optimise heat usage and recover waste heat for new purposes | 10% | TRL 7 | [58] |

| Electrification | Increased use of low-carbon electricity Use of electricity for general operations and some heating processes. Production of hydrogen with electrolysers | 25% | TRL 4–8 | [107] |

| Carbon capture and storage | Partial capture of CO2 emission, for instance at steam reforming plants (SMR) to produce a low-carbon intensity hydrogen. | 25% for partial capture; up to >90% for full capture | TRL 6–7 | [107] |

| Low carbon feedstocks | Integration of bio-based feedstocks, power to-fuels (renewable hydrogen) into the refinery. Negative emissions could potentially be achieved when combined with CCS. | Depending on pathways to produce renewable feedstocks | TRL 3–7 | [107] |

| Industry | Capacity in 2018 | Total GHG Emissions | Historical GHGs Emission Reduction Rate (% Change) | Future Scenario of CO2-Emission Reduction c (% Change) | Ref. | ||

|---|---|---|---|---|---|---|---|

| Value | Unit | MtCO2, 2018 | 1990–2018 | 1990–2030 | 1990–2045 | ||

| Iron and steel | 4.6 | Mt crude steel/year | 5.7 | −1.3% | 6% | 7% | [45,108,109] |

| Mining | 81.4 | Mt ore/year | 0.8 | 49.2% | Not specified | Not specified | [45,70,108] |

| Cement | 3.0 | Mt cement/year | 2.5 | 2.8% | −12% | −15% | [45,75,108] |

| Refinery a | 21.8 | Mt crude oil/year | 3.0 | 33.2% | 46% | 49% | [45,108,110] |

| Pulp and paper b | 6.2 | Mt paper and packaging/year | 0.8 | −58.8% | −64% | −72% | [45,108,111] |

| Total industry d | 16.8 | −17% | −18% | −20% | |||

| Industry | Total CO2 Emission in 2018 (Mt CO2-eq) | Decarbonisation Pathways | Status in Sweden | Example Projects | Potential Reduction of Annual CO2 Emission (Mt CO2-eq/y) | |

|---|---|---|---|---|---|---|

| Steel | 5.7 | Hydrogen | Hydrogen direct reduction of iron ore | Demonstration project | HYBRIT | 4–5 |

| Electrification | Electrification of heat treatment process (<1000 °C) Electrification of heating process (>1000 °C) | Initiated process, R&D | PLATIS | 0.3–0.4 | ||

| Fuel switching | Switching to biomass-based gas Switching to biochar | R&D | Probiostål | 0.5–0.6 0.1–0.2 | ||

| Mining, mineral and metal | 2.2 | Electrification | Electrification of processes Electrification of work machines | R&D Test project | Electrified Mine Truck Operation | 0.2–0.3 0.5–1 |

| Fuel switching | Switching to biofuels | R&D | HYBRIT | 0.5–0.6 | ||

| CCS/CCU | CO2 capture for reuse or storage in geological formation | Demo and test facilities required | 0.4–0.5 | |||

| Cement | 2.5 | Electrification | Electrification of heating processes | R&D, test project | Cemzero | 0.4–0.6 |

| Fuel switching | Switching to biofuels in heating process | Currently, 20% biofuels and 50% waste fuel | 0.4–0.6 | |||

| CCS/CCU | CO2 capture for reuse or storage in geological formation | Pilot project in Norway | 1–1.1 | |||

| New products | CO2 uptake in cement-containing products and new cement varieties | R&D | 0.3–0.4 | |||

| Pulp & paper | 0.8 | Electrification | Electrification of heating process | R&D | Not specified | |

| Fuel switching | Replace fossil oil in the lime kilns with biofuels | Ongoing | Not specified | |||

| Refinery | 2.8 | Hydrogen | Replace fossil-based hydrogen with renewable H2 | Test project | Preem-Vattenfall | Not specified |

| CCS/CCU | CO2 capture for reuse or storage in geological formation | Test project, under development | Preem CCS, CinfraCap | Not specified | ||

| New products | Production of renewable fuels | Ongoing process, R&D | Not specified | |||

| Policy Type | Policy | Short Description | Effective Date/Year |

|---|---|---|---|

| Price-based system | Carbon dioxide (CO2) tax | Most fossil fuel use, as well as low blends of biofuels in gasoline and diesel are subject to CO2 tax. Emitters to pay a fee per ton of CO2 they emit, at a nominal rate of SEK 1190 per tonne of CO2. Industries covered by the EU ETS generally do not pay the CO2 Tax. | 1991 |

| Energy tax | Most fossil fuels as well as a low blends of biofuels in gasoline and diesel used in the industry are subject to the energy tax. The manufacturing industry pays 30% of the general energy tax. | 1924 | |

| EU ETS | Under the ‘cap and trade’ principle, a cap is set on the total emissions that can be emitted by all participants but, within that limit, allows participants in the system to buy and sell allowances as they require. Includes emissions from major industries, incineration plants and civil aviation within EU. | 1 January 2005 | |

| Technology support policies | Climate leap | The program aims to reduce emissions by providing local and regional investments in all sectors, except those included in the EU ETS. | 2015 |

| Industrial leap | The program aims to support the development of technologies and processes to significantly reduce process emissions in Swedish industry. Feasibility studies and full-scale investments can be granted. | 2018 | |

| Investment support for renewables | The program aims to support solar power and initiatives for wind power through investment support, dissemination of knowledge and information. | 2009 | |

| Quota system | Electricity certificate system | The system aims to increase the production of renewable electricity. Producers of electricity are allocated a certificate unit for every MWh of electricity generated, which can then be sold in an open market. The purchasers are mainly electricity suppliers having quota obligations. | 2003 |

| Command and control regulations | Environmental code | The code contains general rules for consideration to be observed in all activities and measures that affect the environment including GHG emissions. | 1 January 1999 |

| Information and voluntary approaches | Energy audit | Large companies are required to conduct an energy audit at least every fourth year except they have implemented an environment or energy management system. | 2010 |

| Energy step | Energy efficiency program where companies can get support for projecting energy efficiency actions or investing in energy efficiency measures identified in the audit. | 2018 | |

| Grants energy audit | Financial support to small and medium-sized enterprises (SME) to conduct an energy audit. | 2010 | |

| Energy and climate coaches | A national initiative that combines coaching and knowledge transfer between participating companies to improve energy efficiency. | 2016 | |

| Energy efficiency network | A network project for SMEs that supporting them to introduce energy management principles. The networks has regional coordinators and energy experts. | 2015 | |

| Information | Provides useful knowledge and tools on how to mitigate climate change and adapt to climate change. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nurdiawati, A.; Urban, F. Towards Deep Decarbonisation of Energy-Intensive Industries: A Review of Current Status, Technologies and Policies. Energies 2021, 14, 2408. https://doi.org/10.3390/en14092408

Nurdiawati A, Urban F. Towards Deep Decarbonisation of Energy-Intensive Industries: A Review of Current Status, Technologies and Policies. Energies. 2021; 14(9):2408. https://doi.org/10.3390/en14092408

Chicago/Turabian StyleNurdiawati, Anissa, and Frauke Urban. 2021. "Towards Deep Decarbonisation of Energy-Intensive Industries: A Review of Current Status, Technologies and Policies" Energies 14, no. 9: 2408. https://doi.org/10.3390/en14092408

APA StyleNurdiawati, A., & Urban, F. (2021). Towards Deep Decarbonisation of Energy-Intensive Industries: A Review of Current Status, Technologies and Policies. Energies, 14(9), 2408. https://doi.org/10.3390/en14092408