Re-Designing GB’s Electricity Market Design: A Conceptual Framework Which Recognises the Value of Distributed Energy Resources

Abstract

1. Introduction

2. Literature Review

2.1. Market Objectives and Market Design Implementation

2.2. Technological Developments Have Led to Concerns over the Efficacy of the Electricity Market Design

2.2.1. Issues

2.2.2. Potential Benefits to Be Exploited through Electricity Market Design Re-Configuration

- (1)

- Reducing balancing costs through the displacement of more expensive, and carbon-intensive forms of flexibility such as an open-cycle gas turbine [77].

- (2)

- (3)

- Locating flexible services near to, or co-locating with, VRE generation can mitigate the extent of price cannibalisation by absorbing excess VRE and reinjecting at times of increased demand. This reinjection will likely coincide with higher power prices, resulting in a more profitable capture rate [80].

- This has an added benefit of reducing network constraints via the removal of the excess electrons on the network. By storing, and not curtailing this zero-carbon generation, when reinjected this removes the need for carbon-intensive technologies which may have been otherwise required [80].

- (4)

- Regional geographies will become increasingly important under a decentralised electricity system. Local balancing can be facilitated through the deployment of generation and demand in proximity on the network. This removes the distance that electrons would otherwise travel and possibly breach network capacity in doing so, thus leading to a more efficient use of the network [9,20,21,45,78,81].

2.3. The Distribution Gap

2.3.1. COVID-19

2.3.2. Pursuing a Smart Energy System Approach

3. Methodology

3.1. Stage 1: Review of Previously Proposed Market Designs

3.2. Stage 2: Modularisation of GB’s Electricity Market Design

3.3. Stage 3: Construction of a Strawman Design

- (1)

- Augmentation: Introducing a new module to an existing system which embodies new concepts, addressing a specific need currently not catered for.

- (2)

- Layering: The process of new rules being attached to an existing module, to provide an additional function.

- (3)

- Exclusion: Removing a module which is no longer required.

- (1)

- Rectified an issue in line with the objectives of this design,

- (2)

- Had any knock-on impacts on fellow modules or the coordination between them, and

- (3)

- Could be implemented alongside other proposed solutions.

- This created the strawman design which then underwent evaluation (Section 3.4).

3.4. Stage 4: Appraisal and the Validation of the Strawman Design

4. The Market Design

4.1. Objectives

4.2. Overview of the Design

- Module 1: The DSP pool market,

- Module 2: The DSP ancillary market,

- Module 3: The DSP balancing market,

- Module 4: The wholesale market,

- Module 5: The independent integrated system operator (IISO) ancillary market, and

- Module 6: The IISO balancing market.

4.3. The Electricity Market Design

4.3.1. Regulatory Changes

Priority Dispatch for VRE

Network Charges

4.4. The DSP

4.4.1. Module 1: The DSP Pay-As-Clear Pool Module

4.4.2. Operating within Module 1

4.4.3. Module 2: The DSP Ancillary Market

- Associated carbon,

- The distance of the technology from load, and

- Any arising network issues from such a dispatch and the cost of procurement.

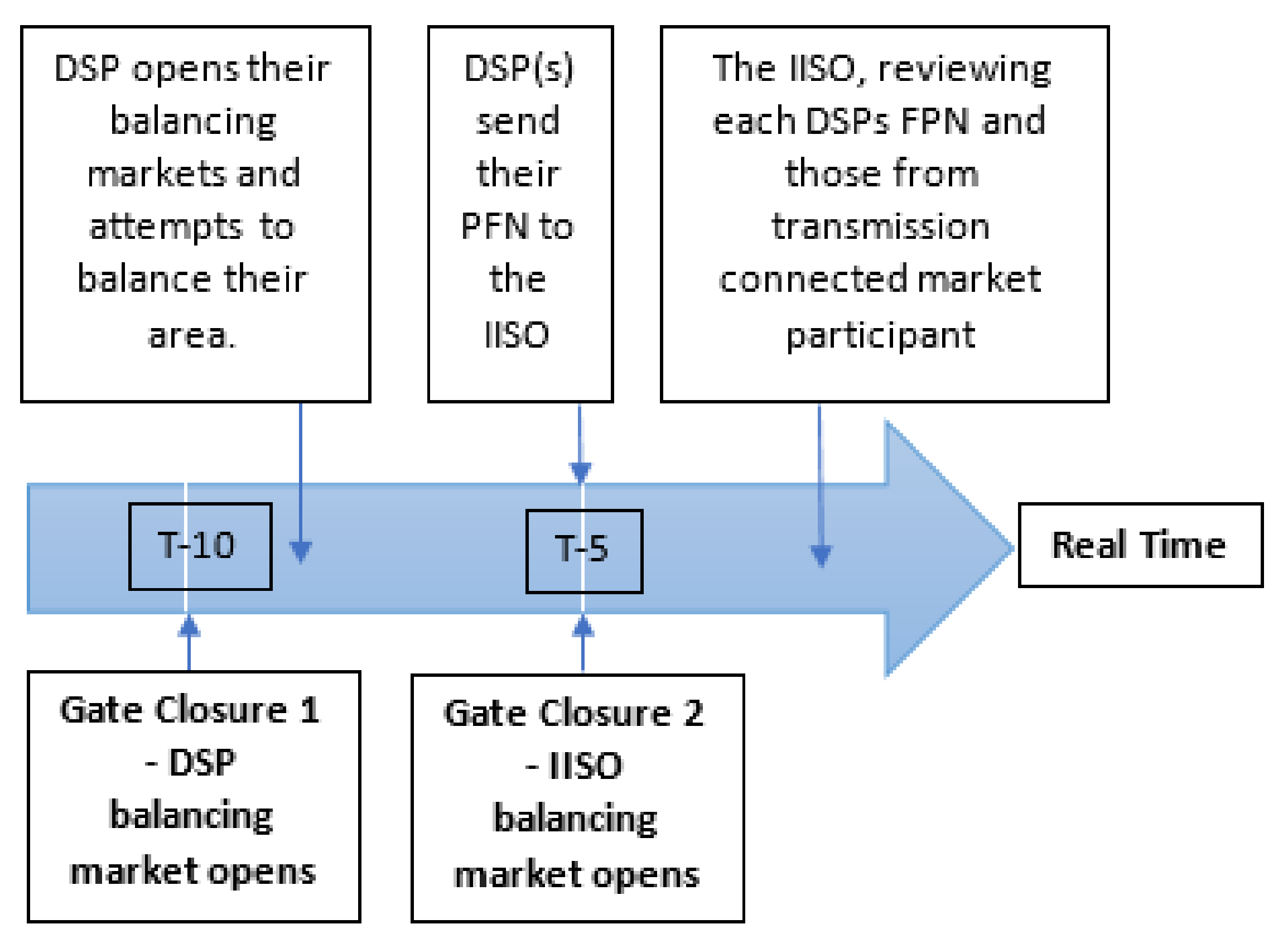

4.4.4. Module 3: The DSP Balancing Market

4.5. Module 4: The Wholesale Market

4.6. The IISO

4.6.1. Module 5: The IISO Ancillary Market

4.6.2. Module 6: The IISO Balancing Market

4.7. Coordination

4.8. Exclusion of the Capacity Market

4.9. Justification Table

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Nomenclature

| CfD | Contract for Difference |

| DAH | Day Ahead |

| DER | Distributed Energy Resources |

| DLMP | Distributed Locational Marginal Price |

| DNO | Distribution Network Operator |

| DSODSP | Distributed System Operator Distributed Service Provider |

| DUoS | Distribution Use of System |

| EVs | Electric Vehicles |

| FES | Future Energy Scenarios |

| FPN | Final Physical Notification |

| GB | Great Britain |

| GSP | Grid Supply Point |

| ID | Intraday |

| IISO | Independent Integrated System Operator |

| IoT | Internet of Things |

| LEM | Local Energy Markets |

| NETA | New Electricity Trading Arrangements |

| ODFM | Operation Downward Frequency Management |

| OPEX | Operational Expenditure |

| P2P | Peer to Peer |

| SES | Smart Energy System |

| TNUoS | Transmission Network Use of System |

| TSO | Transmission System Operator |

| VRE | Variable Renewable Energy |

References

- Mathews, J.A. The renewable energies technology surge: A new techno-economic paradigm in the making? Futures 2013, 46, 10–22. [Google Scholar] [CrossRef]

- BEIS. Electricity Generation Costs. 2020. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/911817/electricity-generation-cost-report-2020.pdf (accessed on 5 September 2020).

- Markard, J. The next phase of the energy transition and its implications for research and policy. Nat. Energy 2018, 3, 628–633. [Google Scholar] [CrossRef]

- Kern, F.; Kuzemco, C.; Mitchell, C. Measuring and Explaining Policy Paradigm Change. Policy Polit. 2014, 42, 513–530. [Google Scholar] [CrossRef]

- HM Government. Powering Our Net Zero Future. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/943807/201214_BEIS_EWP_Command_Paper_LR.pdf (accessed on 21 December 2020).

- National Grid ESO. Future Energy Scenarios. Available online: https://www.nationalgrideso.com/future-energy/future-energy-scenarios/fes-2020-documents (accessed on 29 July 2020).

- Papalexopoulos, A.; Frowd, R.; Birbas, A. On the development of organized nodal local energy markets and a framework for the TSO-DSO coordination. Electr. Power Syst. Res. 2020, 189, 106810. [Google Scholar] [CrossRef]

- NIC. Smart Power. Available online: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/505218/IC_Energy_Report_web.pdf (accessed on 2 November 2017).

- Zhang, C.; Wu, J.; Zhou, Y.; Cheng, M.; Long, C. Peer-to-Peer energy trading in a Microgrid. Appl. Energy 2018, 220, 1–12. [Google Scholar] [CrossRef]

- BEIS, Ofgem. Upgrading Our Energy System, Smart Systems and Flexibility Plan-Call for Evidence Question Summaries and Response from the Government and Ofgem; BEIS, Ofgem: London, UK, 2017. [Google Scholar]

- Gerard, H.; Israel, E.; Puente, R.; Six, D. Coordination between transmission and distribution system operators in the electricity sector: A conceptual framework. Util. Policy 2018, 50, 40–48. [Google Scholar] [CrossRef]

- Koirala, B.P.; Ávila, J.P.C.; Gómez, T.; Hakvoort, R.A.; Herder, P.M. Local alternative for energy supply: Performance assessment of integrated community energy systems. Energies 2016, 9, 981. [Google Scholar] [CrossRef]

- Pérez-Arriaga, I.; Schwenen, S.; Glachant, J. From Distribution Networks to Smart Distribution Systems: Rethinking the Regulation of European Electricity DSOs. Util. Policy 2013. [Google Scholar] [CrossRef]

- Energy Networks Association. Active Network Management Good Practice Guide. Available online: http://www.energynetworks.org/modx/assets/files/news/publications/1500205_ENA_ANM_report_AW_online.pdf (accessed on 14 April 2017).

- Poudineh, R.; Jamasb, T. Distributed generation, storage, demand response and energy efficiency as alternatives to grid capacity enhancement. Energy Policy 2014, 67, 222–231. [Google Scholar] [CrossRef]

- Spiliotis, K.; Ramos Gutierrez, A.I.; Belmans, R. Demand flexibility versus physical network expansions in distribution grids. Appl. Energy 2016, 182, 613–624. [Google Scholar] [CrossRef]

- Strielkowski, W.; Streimikiene, D.; Fomina, A.; Semenova, E. Internet of Energy (IoE) and High-Renewables Electricity System Market Design. Energies 2019, 12, 4790. [Google Scholar] [CrossRef]

- Morstyn, T.; Teytelboym, A.; Mcculloch, M.D.; Member, S. Designing Decentralized Markets for Distribution System Flexibility. IEEE Trans. Power Syst. 2018, 34, 2128–2139. [Google Scholar] [CrossRef]

- Policy Exchange. Impact of Locational Pricing in Great Britain. Working Paper. 2020. Available online: https://policyexchange.org.uk/wp-content/uploads/Appendix-1-Aurora-Energy-Research.pdf (accessed on 9 January 2021).

- Mengelkamp, E.; Gärttner, J.; Rock, K.; Kessler, S.; Orsini, L.; Weinhardt, C. Designing microgrid energy markets. Appl. Energy 2017, 210, 870–880. [Google Scholar] [CrossRef]

- Roques, F.; Finon, D. Adapting electricity markets to decarbonisation and security of supply objectives: Toward a hybrid regime? Energy Policy 2017, 105, 584–596. [Google Scholar] [CrossRef]

- Willis, R.; Mitchell, C.; Hoggett, R.; Britton, J.; Poulter, H.; Pownall, T.; Lowes, R. Getting Energy Governance Right: Lessons from IGov. Working Paper. Available online: http://projects.exeter.ac.uk/igov/wp-content/uploads/2019/08/IGov-Getting-energy-governance-right-Sept2019.pdf (accessed on 20 September 2020).

- Lockwood, M.; Mitchell, C.; Hoggett, R. Energy Governance in the United Kingdom. In Handbook of Energy Governance in Europe, 1st ed.; Springer International Publishing: Berlin/Heidelberg, Germany, 2019. [Google Scholar]

- Mitchell, C. Electricity markets and their regulatory systems for a sustainable future. In Global Energy Issues, Potentials, Policy Implications; Ekins, P., Bradshaw, M., Eds.; Oxford University Press: Oxford, UK, 2015; Volume 6, pp. 45–66. [Google Scholar] [CrossRef]

- Chilvers, J.; Foxon, T.J.; Galloway, S.; Hammond, G.P.; Infield, D.; Leach, M.; Pearson, P.J.G.; Strachan, N.; Strbac, G.; Thomson, M. Realising transition pathways for a more electric, low-carbon energy system in the United Kingdom: Challenges, insights and opportunities. Prock. IMeche Part A J. Power Energy 2017, 231, 1–38. [Google Scholar] [CrossRef]

- Ford, R.; Hardy, J. Are we seeing clearly? The need for aligned vision and supporting strategies to deliver net-zero electricity systems. Energy Policy 2020, 147, 111902. [Google Scholar] [CrossRef]

- Meadowcroft, J. What about the politics? Sustainable development, transition management, and long term energy transitions. Policy Sci. 2009, 42, 323–340. [Google Scholar] [CrossRef]

- Kemp, R.; Rotmans, J.; Loorbach, D. Assessing the Dutch energy transition policy: How does it deal with dilemmas of managing transitions? J. Environ. Policy Plan. 2007, 9, 315–331. [Google Scholar] [CrossRef]

- European Commission. Clean Energy for All New Electricity Market Design. A Fair Deal for Consumers. Available online: https://ec.europa.eu/energy/sites/ener/files/documents/technical_memo_marketsconsumers.pdf (accessed on 20 June 2018).

- Kominers, S.D.; Teytelboym, A.; Crawford, V.P. An invitation to market design. Oxf. Rev. Econ. Policy 2017, 33, 541–571. [Google Scholar] [CrossRef]

- Leslie, G.; Stern, D.I.; Shanker, A.; Hogan, M.T. Designing Electricity Markets for High Penetrations of Zero or Low Marginal Cost Intermittent Energy Sources. SSRN Electron. J. 2020. [Google Scholar] [CrossRef]

- Judson, E.; Fitch-Roy, O.; Pownall, T.; Bray, R.; Poulter, H.; Soutar, I.; Lowes, R.; Connor, P.; Britton, J.; Woodman, B.; et al. The centre cannot (always) hold: Examining pathways towards energy system de-centralisation. Renew. Sustain. Energy Rev. 2020, 118. [Google Scholar] [CrossRef]

- Bray, R.; Woodman, B.; Connor, P. Policy and Regulatory Barriers to Local Energy Markets in Great Britain Working Paper. Available online: http://geography.exeter.ac.uk/media/universityofexeter/schoolofgeography/images/researchgroups/epg/09.05.18_Policy_and_Regulatory_Barriers_to_LEMs_in_GB__BRAY._.pdf (accessed on 20 September 2018).

- Hu, J.; Harmsen, R.; Crijns-Graus, W.; Worrell, E.; van den Broek, M. Identifying barriers to large-scale integration of variable renewable electricity into the electricity market: A literature review of market design. Renew. Sustain. Energy Rev. 2018, 81, 2181–2195. [Google Scholar] [CrossRef]

- Green, R. Draining the Pool: The reform of electricity trading in England and Wales. Energy Policy 1999, 27, 515–525. [Google Scholar] [CrossRef][Green Version]

- Bower, J. Why Did Electricity Prices Fall in England and Wales: Market Mechanism or Market Structure? Oxford Institute Energy Studies: Oxford, UK, 2002; pp. 1–57. [Google Scholar]

- European Commission. GB Implementation Plan. Available online: https://ec.europa.eu/energy/sites/ener/files/gb_implementation_plan-final.pdf (accessed on 21 December 2020).

- Morstyn, T.; Teytelboym, A.; Hepburn, C.; McCulloch, M.D. Integrating P2P Energy Trading with Probabilistic Distribution Locational Marginal Pricing. IEEE Trans. Smart Grid 2020, 11, 3095–3106. [Google Scholar] [CrossRef]

- Ruester, S.; Schwenen, S.; Batlle, C.; Pérez-Arriaga, I. From distribution networks to smart distribution systems: Rethinking the regulation of European electricity DSOs. Util. Policy 2014, 31, 229–237. [Google Scholar] [CrossRef]

- Lin, J.; Magnago, F. ELECTRICITY MARKETS Theories and Applications; Wiley-IEEE Press: Hoboken, NJ, USA, 2017. [Google Scholar]

- EPEX SPOT. Market Integration of Renewables—Mission Accomplished? Available online: https://www.epexspot.com/sites/default/files/download_center_files/202009_Market integration of renewables.pdf (accessed on 11 November 2020).

- Peng, D.; Poudineh, R. Electricity market design under increasing renewable energy penetration: Misalignments observed in the European Union. Util Policy 2019, 61, 100970. [Google Scholar] [CrossRef]

- Sorknæs, P.; Lund, H.; Skov, I.R.; Djørup, S.; Skytte, K.; Morthorst, P.E.; Fausto, F. Smart Energy Markets-Future electricity, gas and heating markets. Renew. Sustain. Energy Rev. 2020, 119. [Google Scholar] [CrossRef]

- Lund, H.; Østergaard, P.A.; Connolly, D.; Ridjan, I.; Mathiesen, B.V.; Hvelplund, F.; Thellufsen, J.Z.; Sorknæs, P. Energy storage and smart energy systems. Int. J. Sustain. Energy Plan. Manag. 2016, 11, 3–14. [Google Scholar] [CrossRef]

- Rodr, J.; Rib, D.; Carlos, Á.; Peñalvo-l, E. Novel Conceptual Architecture for the Next-Generation Electricity Markets to Enhance a Large Penetration of Renewable Energy. Energies 2019, 12, 2605. [Google Scholar] [CrossRef]

- Britton, J.; Marques, A.; Pourmirza, Z. Exploring the potential of Heat as a Service in decarbonisation: Evidence needs and research gaps. Energy Sources Part B Econ. Plan. Policy 2021. [Google Scholar] [CrossRef]

- Newbery, D.M. Electricity liberalisation in Britain: The quest for a satisfactory wholesale market design. Energy J. 2005, 26, 43–70. [Google Scholar] [CrossRef]

- Legislation.gov.uk. The Electricity Act 1989: Part II: Transfers to Successor Companies. Available online: https://www.legislation.gov.uk/ukpga/1989/29/part/II/crossheading/transfers-to-successor-companies (accessed on 22 December 2020).

- OFFER. Review of Electricity Trading Arrangements Background Paper 1 Electricity Trading Arrangements in England and Wales. Available online: https://www.ofgem.gov.uk/ofgem-publications/79088/review-electricity-trading-arrangements-background-england-and-walespdf (accessed on 5 March 2018).

- Cornwall Insight. Challenges of Designing Markets to Bring Forward Low Marginal Cost Resources the Net Zero Paradox Working Paper. Available online: https://www.cornwall-insight.com/insight-papers/the-net-zero-paradox-challenges-of-designing-markets-to-bring-forward-low-marginal-cost-resources (accessed on 17 November 2020).

- Nelson, T.; Orton, F.; Chappel, T. Electricity market design in a decarbonised energy system Electricity market design. Decarbonised Energy Syst. 2017. [Google Scholar] [CrossRef]

- De Vries, L.J.; Verzijlbergh, R.A. How renewable energy is reshaping Europe’s Electricity market design. Econ. Energy Environ. Policy 2018, 7, 31–49. [Google Scholar] [CrossRef]

- COAG Energy Council. Response to Post 2025 Market Design Consultation Paper. Available online: http://www.coagenergycouncil.gov.au/publications/post-2025-market-design-consultation-paper-–-september-2020 (accessed on 2 October 2020).

- IRENA. Renewable Power Generation Costs in 2019; IRENA: Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- BEIS. Dukes 2020 Chapter 5: Electricity. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/904805/DUKES_2020_Chapter_5.pdf (accessed on 12 November 2020).

- BEIS. Contracts for Difference for Low Carbon Electricity Generation Consultation on proposed amendments to the scheme. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/885248/cfd-ar4-proposed-amendments-consultation.pdf (accessed on 27 November 2020).

- Keay, M.; Robinson, D. The Decarbonised Electricity System of the Future: The “Two Market” Approach Part 1 Overall concept Working Paper. Available online: https://www.oxfordenergy.org/wpcms/wp-content/uploads/2017/06/The-Decarbonised-Electricity-Sysytem-of-the-Future-The-Two-Market-Approach-OIES-Energy-Insight.pdf (accessed on 2 June 2018).

- Riesz, J.; Milligan, M. Designing electricity markets for a high penetration of variable renewables. Energy Environ. 2015, 4. [Google Scholar] [CrossRef]

- Bauknecht, D.; Brunekreeft, G.; Meyer, R. From Niche to Mainstream: The Evolution of Renewable Energy in the German Electricity Market. In Evolution of Global Electricity Markets; Elsevier: Amsterdam, The Netherlands, 2013. [Google Scholar] [CrossRef]

- Hogan, W.W. On an “Energy Only” Electricity Market Design for Resource Adequacy. Available online: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.438.4422&rep=rep1&type=pdf (accessed on 3 May 2018).

- Cornwall Insight. Wholesale Power Price Cannibalisation. Available online: https://www.cornwall-insight.com/insight-papers/wholesale-power-price-cannibalisation (accessed on 4 March 2019).

- López, P.J.; Steininger, K.W.; Zilberman, D. The cannibalization effect of wind and solar in the California wholesale electricity market. Energy Econ. 2020, 85, 104552. [Google Scholar] [CrossRef]

- Simshauser, P. On the stability of energy-only markets with government-initiated contracts-for-differences. Energies 2019, 12, 2566. [Google Scholar] [CrossRef]

- Green Alliance. Smart Investment. Valuing Flexibility in the UK Electricity Market Working Paper. Available online: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/568982/An_analysis_of_electricity_flexibility_for_Great_Britain.pdf (accessed on 5 September 2018).

- Shakoor, A.; Davies, G.; Strbac, G. Roadmap for Flexibility Services to 2030. Available online: http://poyry.co.uk/sites/www.poyry.co.uk/files/decentralisedreliabilityoptionspublicreport_v300_0.pdf (accessed on 16 March 2018).

- Energy UK. Contracts for Difference (CfD). Proposed Amendments to the Scheme 2020. Available online: https://www.gov.uk/government/consultations/contracts-for-difference-cfd-proposed-amendments-to-the-scheme-2020 (accessed on 25 September 2020).

- Energy Systems Catapult. Towards a New Framework for Electricity Markets Working Paper. Available online: https://es.catapult.org.uk/reports/towards-a-new-framework-for-electricity-markets/ (accessed on 12 January 2020).

- Ofgem. Wholesale Energy Markets in 2016. Available online: https://www.ofgem.gov.uk/system/files/docs/2016/08/wholesale_energy_markets_in_2016.pdf (accessed on 16 September 2017).

- Elexon. Where Can I Find Details of Wholesale Prices of Electricity in Great Britain? Available online: https://www.elexon.co.uk/knowledgebase/where-can-i-find-details-of-wholesale-prices-of-electricity-in-great-britain/ (accessed on 20 November 2020).

- Ofgem. Decision to Suspend the Secure and Promote Market Making Obligation with Effect. Available online: https://www.ofgem.gov.uk/system/files/docs/2019/11/mmo_suspension_decision_letter_2.pdf (accessed on 13 January 2020).

- Cramton, P. Electricity market design. Oxford Rev. Econ. Policy 2017, 33, 589–612. [Google Scholar] [CrossRef]

- OFGEM. Options for Improving Locational Accuracy of Distribution Charges–Discussion Note. Available online: https://www.ofgem.gov.uk/system/files/docs/2019/09/000_-_working_paper_-_summer_2019_-_locational_charges_note_final.pdf (accessed on 2 August 2020).

- Nieße, A.; Lehnhoff, S.; Tröschel, M.; Uslar, M.; Wissing, C.; Appelrath, H.J.; Sonnenschein, M. Market-Based Self-Organized Provision of Active Power and Ancillary Services: An Agent-Based Approach for Smart Distribution Grids. In Proceedings of the 2012 IEEE Work Complex Eng COMPENG, Aachen, Germany, 11–13 June 2012; pp. 47–51. [Google Scholar] [CrossRef]

- Ofgem. Electricity System Flexibility. Available online: https://www.ofgem.gov.uk/electricity/retail-market/market-review-and-reform/electricity-system-flexibility (accessed on 26 June 2018).

- HM Government, Ofgem. Smart Systems and Flexibility Plan Upgrading Our Energy System Smart Systems and Flexibility Plan. Available online: https://www.ofgem.gov.uk/system/files/docs/2017/07/upgrading_our_energy_system_-_smart_systems_and_flexibility_plan.pdf (accessed on 1 June 2018).

- Olivella-Rosell, P.; Lloret-Gallego, P.; Munné-Collado, Í.; Villafafila-Robles, R.; Sumper, A.; Ottessen, S.Ø.; Rajasekharan, J.; Bremdal, B.A. Local flexibility market design for aggregators providing multiple flexibility services at distribution network level. Energies 2018, 11, 822. [Google Scholar] [CrossRef]

- Sanders, D.; Hart, A.; Ravishankar, M.; Brunert, J. An Analysis of Electricity System Flexibility for Great Britain. Available online: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/568982/An_analysis_of_electricity_flexibility_for_Great_Britain.pdf (accessed on 12 September 2017).

- Stanley, R.; Johnston, J.; Sioshansi, F. Chapter 6: Platforms to Support Non wire Alternatives and DSO Flexibility Trading. In Consumers, Prosumers, Prosumagers: How Service Innovations Will Disrupt the Utility Business Model, 1st ed.; Academic Press: London, UK, 2019; pp. 111–127. [Google Scholar]

- Brinkel, N.B.G.; Schram, W.L.; AlSkaif, T.A.; Lampropoulos, I.; van Sark, W.G.J.H.M. Should we reinforce the grid? Cost and emission optimization of electric vehicle charging under different transformer limits. Appl. Energy 2020, 276, 115285. [Google Scholar] [CrossRef]

- European Commission. METIS Studies Study S14-Wholesale Market Prices, Revenues and Risks for Producers with High Shares of Variable RES in the Power System; European Commission: Brussels, Belgium, 2018. [Google Scholar]

- WPD. Comparison of Price Incentive Models for Locally Matched Electricity Networks. Appendix A: Study on Local Matching. Available online: https://www.westernpower.co.uk/downloads/1907 (accessed on 15 March 2018).

- National Grid ESO. Potential Transmission Charging Arrangements at Exporting Grid Supply Points (GSPs). Available online: https://www.nationalgrid.com/sites/default/files/documents/42344-Exporting GSP consultation final.pdf (accessed on 13 June 2019).

- Edomah, N.; Ndulue, G. Energy transition in a lockdown: An analysis of the impact of COVID-19 on changes in electricity demand in Lagos Nigeria. Glob. Transit. 2020, 2, 127–137. [Google Scholar] [CrossRef] [PubMed]

- Norouzi, N.; Zarazua de Rubens, G.; Choubanpishehzafar, S.; Enevoldsen, P. When pandemics impact economies and climate change: Exploring the impacts of COVID-19 on oil and electricity demand in China. Energy Res. Soc. Sci. 2020, 68, 101654. [Google Scholar] [CrossRef] [PubMed]

- Bahmanyar, A.; Estebsari, A.; Ernst, D. The impact of different COVID-19 containment measures on electricity consumption in Europe. Energy Res. Soc. Sci. 2020, 68, 101683. [Google Scholar] [CrossRef]

- National Grid ESO. GC143: Last Resort Disconnection of Embedded Generation. Available online: https://www.nationalgrideso.com/document/168336/download (accessed on 11 October 2020).

- IEA. Covid-19 Impact on Electricity. Available online: https://www.iea.org/reports/covid-19-impact-on-electricity (accessed on 17 November 2020).

- Zhang, X.; Pellegrino, F.; Shen, J.; Copertaro, B.; Huang, P.; Kumar Saini, P.; Lovati, M. A preliminary simulation study about the impact of COVID-19 crisis on energy demand of a building mix at a district in Sweden. Appl. Energy 2020, 280, 115954. [Google Scholar] [CrossRef]

- National Grid ESO. 2019-20 End of Year Report Evidence Chapters. Available online: https://www.nationalgrideso.com/document/168786/download (accessed on 12 May 2020).

- Drax. Electric Insights Quarterly (Q2 2020). Available online: https://www.drax.com/wp-content/uploads/2020/08/200828_Drax20_Q2_Report_005.pdf (accessed on 19 September 2020).

- Robinson, D.; Keay, M. Glimpses of the Future Electricity System? Demand Flexibility and a Proposal for a Special Auction. Available online: https://www.oxfordenergy.org/wpcms/wp-content/uploads/2020/10/Glimpses-of-the-future-electricity-system.pdf (accessed on 27 October 2020).

- National Grid ESO. CMP 345 ‘Defer the additional Covid BSUoS Costs’. Available online: https://www.nationalgrideso.com/document/170686/download (accessed on 14 July 2020).

- National Grid ESO. GC0147: Mod Title: Last Resort Generation–Enduring Solution. Available online: https://www.nationalgrideso.com/document/173401/download (accessed on 23 September 2020).

- National Grid ESO. Summer Insights: Webinar 9: ODFM and Managing Low Demand. Available online: http://powerresponsive.com/summer-insights-2020-industry-podcasts/ (accessed on 22 September 2020).

- National Grid ESO. Grid Code Development Forum. Available online: https://www.nationalgrideso.com/industry-information/codes/grid-code-old/meetings/grid-code-development-forum-8-july-2020 (accessed on 10 July 2020).

- Unruh, G.C. Understanding carbon lock-in. Energy Policy 2000, 28, 817–830. [Google Scholar] [CrossRef]

- Fligstein, N.; Calder, R. Architecture of Markets. Emerg. Trends Soc. Behav. Sci. 2015, 1–14. [Google Scholar] [CrossRef]

- Electric Nation Project. Summary of the Findings of the Electric Nation Smart Charging Trial. Available online: http://www.electricnation.org.uk/2019/07/17/electric-nation-smart-charged-conference-review/ (accessed on 12 January 2020).

- Oxford City Council. Oxfordshire to trial £40m industry first local energy system project. Available online: https://www.oxford.gov.uk/news/article/1050/oxfordshire_to_trial_40m_industry_first_local_energy_system_project (accessed on 12 January 2020).

- BEIS, OLEV. Innovation in Vehicle-To-Grid (V2G) Systems: Real-World Demonstrators. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/681321/Innovation_in_Vehicle-To-Grid__V2G__Systems_-_Real-World_Demonstrators_-_Competition_Results.pdf (accessed on 12 January 2020).

- Lowes, R.; Rosenow, J.; Qadrdan, M.; Wu, J. Hot stuff: Research and policy principles for heat decarbonisation through smart electrification. Energy Res. Soc. Sci. 2020, 70, 101735. [Google Scholar] [CrossRef] [PubMed]

- ESO NG. Wider Access to the GB Balancing Mechanism and TERRE Review and Update. Available online: https://www.nationalgrideso.com/document/170896/download (accessed on 2 August 2020).

- Flexitricity. Ev.Energy and Flexitricity Partnership Helps Suppliers Unlock Balancing Mechanism with Smart EV Charging. Available online: https://www.flexitricity.com/resources/press-release/evenergy-and-flexitricity-partnership-helps-suppliers-unlock-balancing-mechanism-smart-ev-charging/ (accessed on 7 February 2021).

- BEIS. Capacity Market-Consultation on Future Improvements. 2020. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/862674/capacity-market-consultation-future-improvements.pdf (accessed on 20 January 2021).

- Behl, D.V.; Ferreira, S. Systems thinking: An analysis of key factors and relationships. Procedia Comput. Sci. 2014, 36, 104–109. [Google Scholar] [CrossRef]

- Arnold, R.D.; Wade, J.P. A Definition of Systems Thinking: A Systems Approach. Procedia Comput. Sci. 2015, 44, 669–678. [Google Scholar] [CrossRef]

- Davidz, H.; Nightingale, D. Model Based Systems Engineering with Department of Defense Architectural Framework. Syst. Eng. 2007, 11. [Google Scholar] [CrossRef]

- Gharajedaghi, J. Systems Thinking: Managing Chaos and Complexity: A Platform for Designing Business Architecture, 2nd ed.; Elsevier: Burlington, VT, USA, 2011. [Google Scholar]

- Esmat, A.; Usaola, J.; Moreno, M.Á. Distribution-level flexibility market for congestion management. Energies 2018, 11, 1056. [Google Scholar] [CrossRef]

- Baldwin, C.; Clark, K. Design Rules: The Power of Modularity; The MIT Press: Cambridge, UK, 2000. [Google Scholar]

- Alexander, C. A City Is Not a Tree; Sustasis Press: Portland, OR, USA, 2015; ISBN 978-0-9893469-7-9. [Google Scholar]

- Franco, C.J.; Castaneda, M.; Dyner, I. Simulating the new British Electricity-Market Reform. Eur. J. Oper. Res. 2015. [Google Scholar] [CrossRef]

- Sovacool, B.K. Energy policymaking in Denmark: Implications for global energy security and sustainability. Energy Policy 2013, 61, 829–839. [Google Scholar] [CrossRef]

- Lockwood, M. The Danish System of Electricity Policy-Making and Regulation Working Paper. Available online: http://projects.exeter.ac.uk/igov/wp-content/uploads/2015/06/ML-Danish-model-of-regulation.pdf (accessed on 8 December 2017).

- Policy Exchange. Powering Net Zero. Working Paper. Available online: https://policyexchange.org.uk/wp-content/uploads/Electricity-Market-Design.pdf (accessed on 8 January 2021).

- Bryman, A. Social Research Methods, 5th ed.; Oxford University Press: Oxford, UK, 2016. [Google Scholar]

- National Grid ESO. Final Report Second Balancing Services Charges Task Force. Available online: http://chargingfutures.com/media/1477/second-balancing-services-charges-task-force-final-report.pdf (accessed on 17 September 2020).

- Market4Res. Post-2020 Framework for a Liberalised Electricity Market with a Large share of Renewable Energy Sources. Available online: https://market4res.eu/wp-content/uploads/LR-Market4RES-final-publication.pdf (accessed on 13 June 2017).

- Ofgem. Great Britain and Northern Ireland Regulatory Authorities Reports 2017. Available online: https://www.ofgem.gov.uk/system/files/docs/2017/08/new_donagh_report.pdf (accessed on 2 August 2018).

- CMA. Appendix 5.2: Locational Pricing in the Electricity Market in Great Britain Contents. Available online: https://assets.publishing.service.gov.uk/media/576bcac940f0b652dd0000a8/appendix-5-2-locational-pricing-fr.pdf (accessed on 18 September 2018).

- European Commission. The Future Electricity Intraday Market Design. Available online: https://op.europa.eu/en/publication-detail/-/publication/f85fbc70-4f81-11e9-a8ed-01aa75ed71a1/language-en (accessed on 5 May 2020).

- EPEXSPOT. Basics of the Power Market. Available online: https://www.epexspot.com/en/basicspowermarket#power-exchanges-organise-trading-and-operate-markets (accessed on 8 December 2020).

- Liu, Z.; Wu, Q.; Oren, S.S.; Huang, S.; Li, R.; Cheng, L. Distribution locational marginal pricing for optimal electric vehicle charging through chance constrained mixed-integer programming. IEEE Trans. Smart Grid 2018, 9, 644–654. [Google Scholar] [CrossRef]

- Xu, R.; Liu, Z.; Yu, Z. Exploring the profitability and efficiency of variable renewable energy in spot electricity market: Uncovering the locational price disadvantages. Energies 2019, 12, 2820. [Google Scholar] [CrossRef]

- Kristov, L.; De Martini, P.; Taft, J.D. A Tale of Two Visions: Designing a Decentralized Transactive Electric System. IEEE Power Energy Mag. 2016, 14, 63–69. [Google Scholar] [CrossRef]

- Mihaylov, M.; Jurado, S.; Avellana, N.; Van Moffaert, K.; De Abril, I.M.; Nowé, A. NRGcoin: Virtual currency for trading of renewable energy in smart grids. Int. Conf. Eur. Energy Mark. EEM 2014. [Google Scholar] [CrossRef]

- PicloFlex. Competition Data. Available online: https://docs.google.com/forms/d/e/1FAIpQLSc-lDxZicbDkZy8WAyjdiLwuvSDefnjrmfB5AjMLq2uVsE_OA/viewform (accessed on 18 December 2020).

- Xu, Y.; Ahokangas, P.; Louis, J.N.; Pongrácz, E. Electricity market empowered by artificial intelligence: A platform approach. Energies 2019, 12, 4128. [Google Scholar] [CrossRef]

- Yuan, Z.; Hesamzadeh, M.R. Hierarchical coordination of TSO-DSO economic dispatch considering large-scale integration of distributed energy resources. Appl. Energy 2017, 195, 600–615. [Google Scholar] [CrossRef]

- ENTSOE. TSO-DSO Report an Integrated Approach to Active System Management with the Focus on TSO-DSO Coordination in Congestion Management and Balancing Content. Available online: https://eepublicdownloads.azureedge.net/clean-documents/Publications/Position papers and reports/TSO-DSO_ASM_2019_190416.pdf (accessed on 12 May 2020).

- National Grid ESO. The Power Potential Project A guide to participating. Available online: https://www.nationalgrid.com/sites/default/files/documents/Power Potential guide to participating_0.pdf (accessed on 5 June 2018).

- National Grid ESO. Dynamic Containment 2. Available online: https://www.nationalgrideso.com/document/162381/download (accessed on 3 February 2020).

- National Grid ESO. Frequently Asked Questions: The Power Potential Project V2 December. Available online: https://www.nationalgrideso.com/innovation/projects/power-potential (accessed on 4 March 2020).

- Energy Networks Association. Open Networks Project: Opening Markets for Network Flexibility. Available online: http://www.energynetworks.org/assets/files/electricity/futures/Open_Networks/14574_ENA_Open Networks Report_AW_v9_Web.pdf (accessed on 17 June 2020).

- Willis, R.; Mitchell, C.; Hoggett, R. Enabling the Transformation of the Energy System: Recommendations from IGov. Available online: http://projects.exeter.ac.uk/igov/wp-content/uploads/2019/04/IGov-Enabling-the-transformation-of-the-energy-system-Sept2019.pdf (accessed on 12 September 2019).

- BEIS. Electricity Market Reform: Capacity Market-GOV.UK. Available online: https://www.gov.uk/government/collections/electricity-market-reform-capacity-market (accessed on 19 August 2017).

- Lockwood, M. The Development of the Capacity Market for Electricity in Great Britain. Available online: http://projects.exeter.ac.uk/igov/wp-content/uploads/2017/10/WP-1702-Capacity-Market.pdf (accessed on 23 May 2019).

- Milstein, I.; Tishler, A. On the effects of capacity payments in competitive electricity markets: Capacity adequacy, price cap, and reliability. Energy Policy 2019, 129, 370–385. [Google Scholar] [CrossRef]

- Energy Systems Catapult. Broad model for a capacity remuneration mechanism in an ESP-led market. Available online: https://es.catapult.org.uk/reports/broad-model-for-a-capacity-remuneration-mechanism/ (accessed on 12 March 2020).

- Pöyry. Decentralised Reliability Options-Securing Energy Markets. Available online: http://poyry.co.uk/sites/www.poyry.co.uk/files/decentralisedreliabilityoptionspublicreport_v300_0.pdf (accessed on 12 March 2020).

- IRENA. Electricity Storage Valuation Framework: Assessing System Value and Ensuring Project Viability. Available online: https://www.irena.org/publications/2020/Mar/Electricity-Storage-Valuation-Framework-2020 (accessed on 2 April 2020).

- Kraan, O.; Kramer, G.J.; Nikolic, I.; Chappin, E.; Koning, V. Why fully liberalised electricity markets will fail to meet deep decarbonisation targets even with strong carbon pricing. Energy Policy 2019, 131, 99–110. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Issue | Summary |

|---|---|

| Missing money | The dispatch of generating assets is determined by their Operational Expenditure (OPEX) cost, principally the fuel element [2]. As more efficient thermal assets enter the market with lower OPEX costs, the older units are displaced. This phenomenon is exacerbated by variable generating assets with low OPEX cost due to the removal of the fuel element, displacing the more expensive technologies [42,57,58]. This results in a lower capture rate for those still required to meet demand, decreasing the incentive to invest in technologies reliant upon a sustained clearing price, leading to concerns over long-term capacity adequacy [21,59,60]. |

| Price cannibalisation | High VRE output can displace thermal generators with higher OPEX costs, lowering the clearing price and reducing the VRE capture rate [61,62,63]. This increases the risk for those operating in the market without a form of revenue assurance scheme such as the CfD [57,61]. |

| Lacking flexibility | Despite agreement on the requirement for flexibility by governmental bodies, economic regulators, system operators, academics and industry bodies, to date, only the balancing and ancillary market provide value for flexibility as a service [64,65]. Furthermore, neither the CfD nor the capacity market were designed for the procurement of flexible services. The CfD addressed long-term investment into low-carbon generation, whereas the capacity market was designed to only respond to the system adequacy challenge and not the emergent flexibility adequacy challenge [56,63,64,66]. Additionally, in securing system adequacy, the capacity market has reduced the prevalence of scarcity events in which prices would rise as the margins between supply and demand converge, raising the market clearing price [67]. These events provide the signal for possible revenue stream for flexibility from demand-side assets as they can reduce one’s demand during these high-priced events, or generate an income based on the arbitrage opportunities [31]. |

| Lacking transparency | An estimated 85% of GB electricity is traded bilaterally in which the volumes and prices are not within the public domain, only accessible through a subscription to a price reporting agency [68,69,70]. This opaque structure dampens investment signals as the financial compensation received for a service is not known, which may also result in the cheapest technology not being dispatched [40,71]. |

| Not reflecting changing energy geographies | The increased deployment of DER evidences the need to reflect regional geographies within the electricity market design. However, GB operates under a single price bidding zone, with price formation at the national level [72]. This does not reflect local characteristics such as the scarcity or surplus of electricity within a constrained area of the network [20,73]. Reflecting ‘local’ network conditions would signal where on the network value could be realised by providing a specific service, i.e., flexibility. Solving locational issues with either generating or demand-side assets or services in close proximity via a local market would support their integration, helping to conserve the profits from these services in the local economy, which may also encourage new investment into DER [12,13]. |

| Representative | |||

|---|---|---|---|

| Academics | 9 | LEM representatives | 2 |

| Consultants | 3 | Trade associations | 2 |

| Incumbent energy supplier | 3 | Transmission system operator (TSO) | 1 |

| Think tank | 3 | Distributed system operator (DSO) | 1 |

| BSC implementor | 2 | European energy regulator | 1 |

| Energy economic regulator | 2 | SME energy supplier | 1 |

| Electricity traders | 2 | DER installer and optimiser | 1 |

| Government representatives | 2 | ||

| Module | Re-Configuration | Specifics |

|---|---|---|

| The DSP pool market | Augmented | Procurement method: Auction Timescale of procurement: DAH/ID Clip size: 0.05 Mw Settlement: Pay as clear |

| The DSP ancillary market | Augmented | Procurement method: Auction Timescale of procurement: DAH/ID Settlement: Pay as clear Clip size: Product specific. No higher than 0.1 MW |

| The DSP balancing market | Augmented | Procurement method: Utilising bids/offers Timescale of procurement: 5 min window before the opening of the IISO balancing market (Module 6) Settlement: Pay as clear Clip size: 0.05 Mw |

| The wholesale market | Layered | Procurement method: Auctions Timescale of procurement: DAH/ID Settlement: Pay as clear Clip size: 0.1 MW |

| The IISO ancillary market | Layered | Procurement method: Auctions Timescale of procurement: DAM/ID Settlement: Pay as clear Clip size: Product specific. No higher than 0.1 MW |

| The IISO balancing market | Layered | Procurement method: Utilising bids/offers Timescale of procurement: Real time Settlement: Pay as clear Clip size: 0.1 Mw |

| The capacity market | Excluded | Rationale for exclusion discussed in Section 4.8. |

| Structure | Pool |

|---|---|

| Suitability for VRE | Reduced risk of facing imbalance charges as a result of a central market which pools liquidity. This promotes the ability for VRE generators to procure, or sell, depending upon the environmental conditions which may result in deviations from contracted positions. |

| Due to standardised products, trades can operate on a faster timescale allowing them to occur closer to real time compared to continuous trading. This also allows VRE to react to fluctuations in output due to environmental conditions and mitigate imbalance charges. | |

| Transparency | Uniform price auction provides transparency and ensures that the least expensive and most efficient generating unit or service is dispatched. |

| Market prices are visible to buyers/traders/sellers. | |

| Reducing trading costs | Typically lower transaction costs than continuous trading. |

| Safe counterparty risk, often provided by the central exchange. |

| Issue | Change to Module(s) | Explanation for How This Will Aid in Mitigating the Issues Identified Within Table 1 |

|---|---|---|

| Missing money | Coordinated markets | The introduction of new routes to market(s) can provide additional revenue streams for technologies and services which may otherwise find themselves out of merit. |

| Nodal (regional investment signals) | The clearing price at each GSP nodes shall indicate to investors the potential value streams from the deployment of a technology, or the provision of a service, in one GSP opposed to another [12,13,126]. Furthermore, in reviewing trends over time within the various marketplaces, it may provide investors with insights as to when particular DSP pay-as-clear pool markets may be at risk of being oversupplied, which could result in specific technologies being out of merit. With this information, they can avoid the deployment of a technology or the provision of a service in this marketplace, in favour of another. | |

| Nodal (constrained markets) | The nodal structure represents multiple constrained markets as opposed to the current signal bidding zone in GB. Therefore, a generating or demand-side asset within one GSP will not be competing directly against a GSP in another part of the country. As such, a market participant would be directly competing against those located within their GSP, which may lessen the depression of the market clearing price depending upon the proportion of VRE generation and required load to satisfy. | |

| Scarcity events (transparency and the exclusion of the capacity market) | The formation of power prices at the local level will reflect regional scarcity and thus the market clearing price will allow for transparent scarcity events to emerge [20,73], a solution suggested by [60] to overcome the missing money phenomenon. Furthermore, the capacity market has been excluded to reduce the dampening effects of this out-of-market mechanism on the emergence of scarcity prices [67]. | |

| Price cannibalisation | Nodal (regional investment signals) | Similar to missing money. Transparent clearing prices of the bids being accepted/rejected will provide investors with the data to identify whether a GSP region is close to cannibalising prices at times of high VRE output. |

| Flexibility | The flexibility markets of both Modules 1 and 4 will provide an established route for the procurement of flexible technologies. These technologies, when coupled with VRE, can prevent cannibalisation events through storing excess generation during peaks [141,142]. | |

| Lacking flexibility | Specific markets for flexibility | The flexibility markets of both Modules 1 and 4 will provide a clear reference price for flexible actions within each market module. |

| Smart energy system approach | Allowing flexible load from across the energy system to provide flexibility will unlock large flexible capacity which could be cheaper than sourcing flexibility from the electricity silo [43,44,101]. | |

| Lacking transparency | Freely available bid data | Transparent trade data for bilateral trades alongside the pool market structures shall aid in revealing the value of specific services. |

| Not reflecting regional differences | Nodal (transparency of prices) | Trade data are made transparent to aid in revealing the value of specific services. This may reveal the value for specific services at different nodes on the network. |

| Nodal (geographically constrained) | By excluding transmission-connected technologies from directly competing in the DSP local balancing and coordinating market (Modules 1–3), only technologies within that geographical area will be represented in the clearing and bid/offer prices of these markets. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pownall, T.; Soutar, I.; Mitchell, C. Re-Designing GB’s Electricity Market Design: A Conceptual Framework Which Recognises the Value of Distributed Energy Resources. Energies 2021, 14, 1124. https://doi.org/10.3390/en14041124

Pownall T, Soutar I, Mitchell C. Re-Designing GB’s Electricity Market Design: A Conceptual Framework Which Recognises the Value of Distributed Energy Resources. Energies. 2021; 14(4):1124. https://doi.org/10.3390/en14041124

Chicago/Turabian StylePownall, Thomas, Iain Soutar, and Catherine Mitchell. 2021. "Re-Designing GB’s Electricity Market Design: A Conceptual Framework Which Recognises the Value of Distributed Energy Resources" Energies 14, no. 4: 1124. https://doi.org/10.3390/en14041124

APA StylePownall, T., Soutar, I., & Mitchell, C. (2021). Re-Designing GB’s Electricity Market Design: A Conceptual Framework Which Recognises the Value of Distributed Energy Resources. Energies, 14(4), 1124. https://doi.org/10.3390/en14041124