How CO2-to-Diesel Technology Could Help Reach Net-Zero Emissions Targets: A Canadian Case Study

, ,

, ,

Abstract

:

1. Introduction

2. Methods

2.1. Hybrid Approach to Levelized Cost of Carbon Abatement Projections

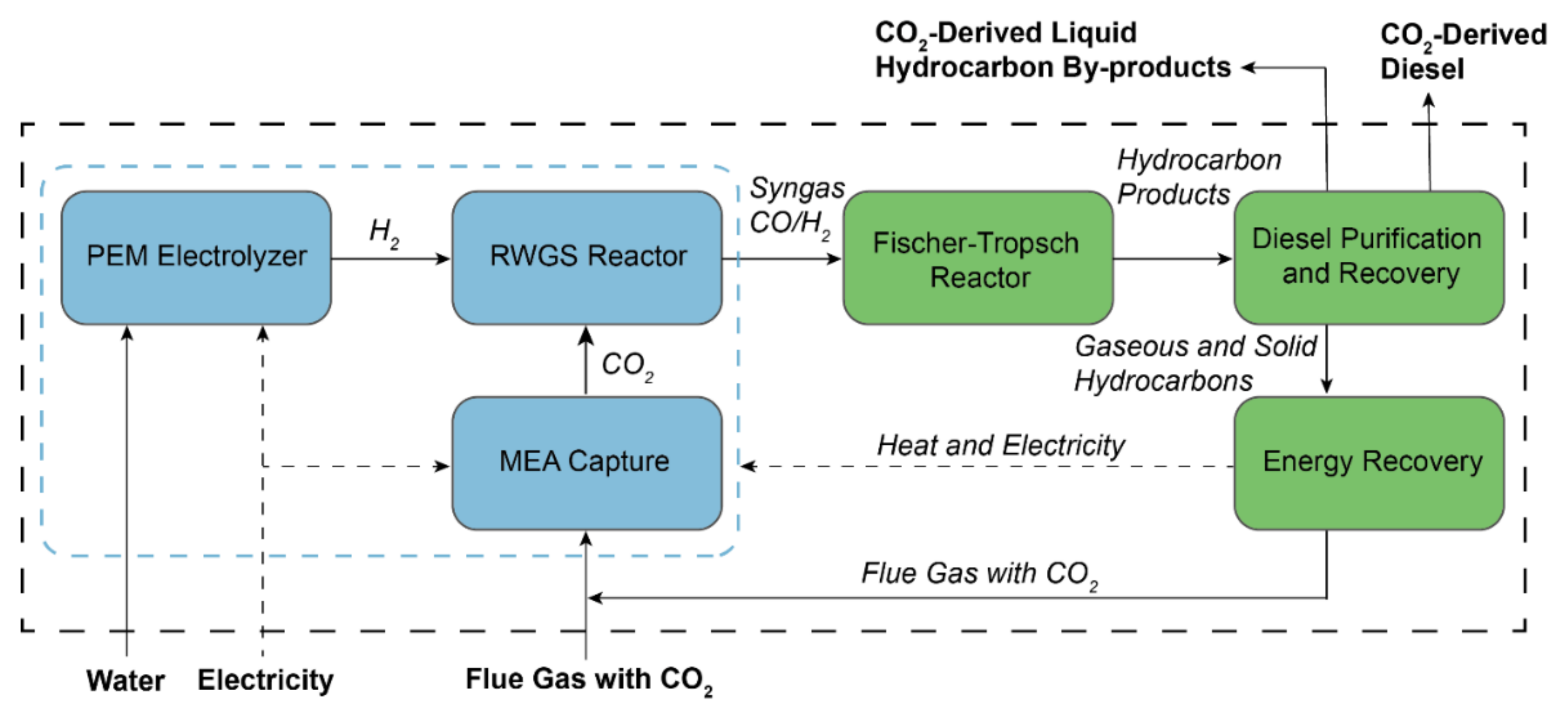

2.2. CO2-to-Diesel Case Study

3. Results & Discussion

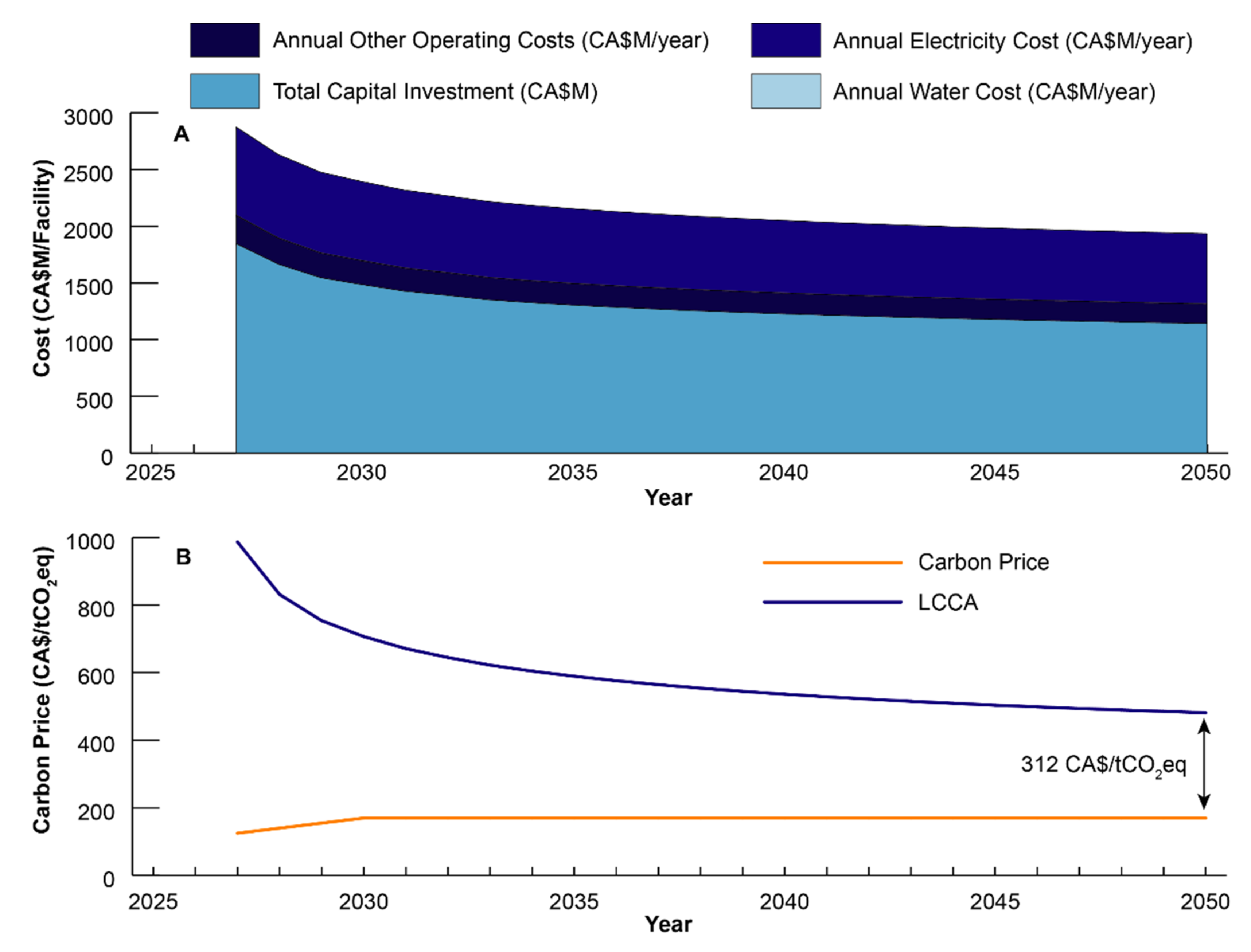

3.1. Learning Curve Effects on LCCA

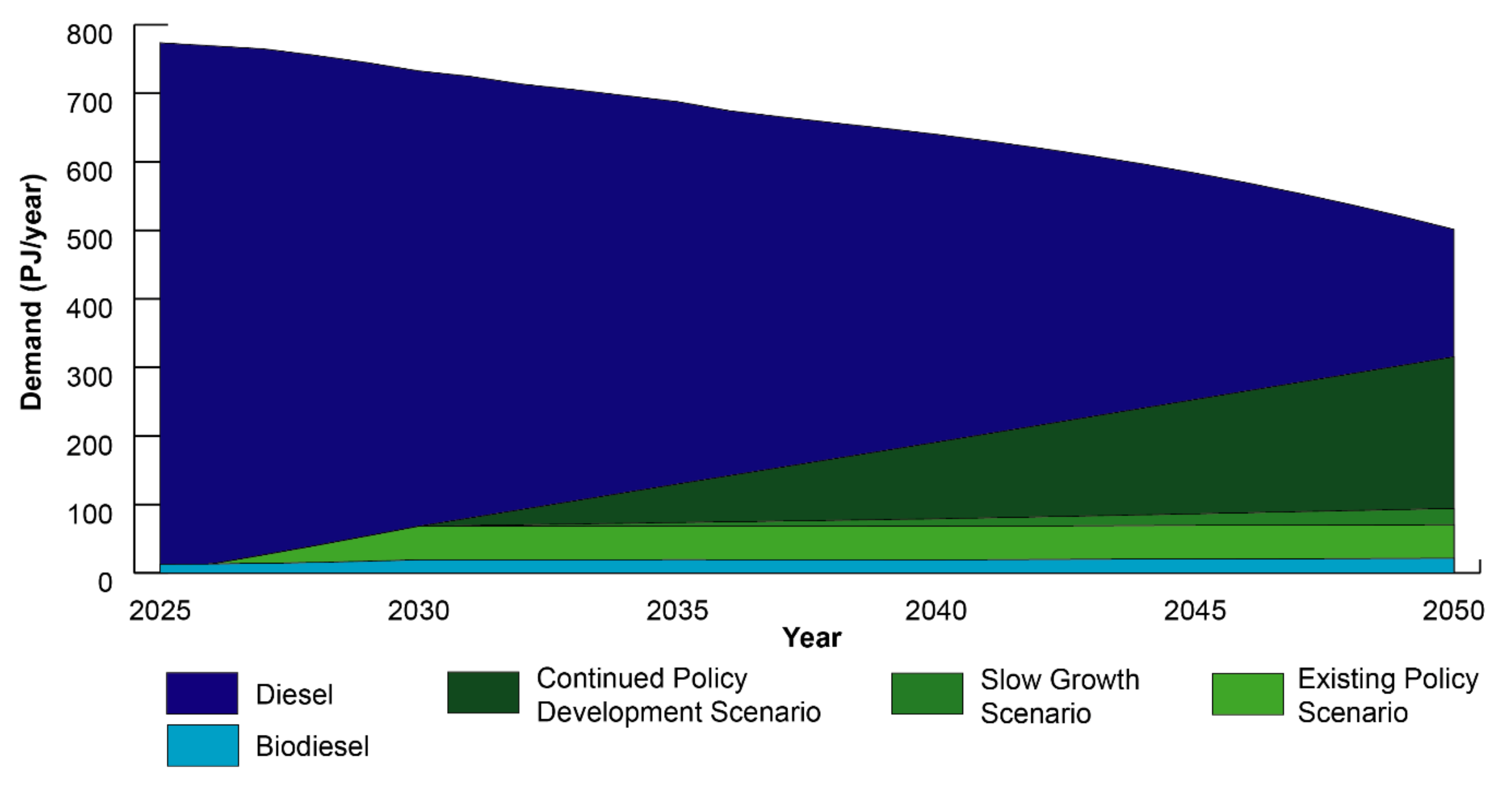

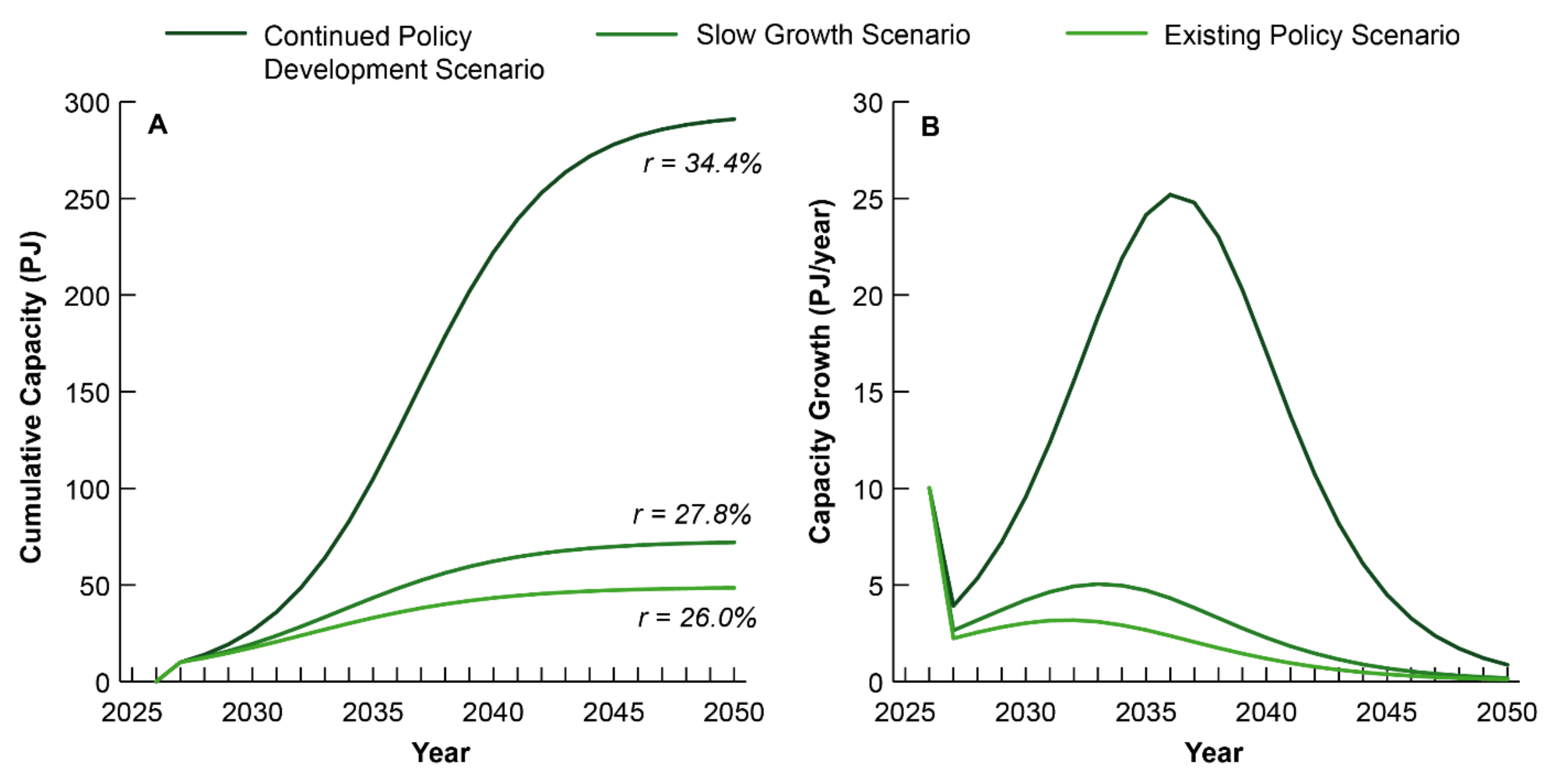

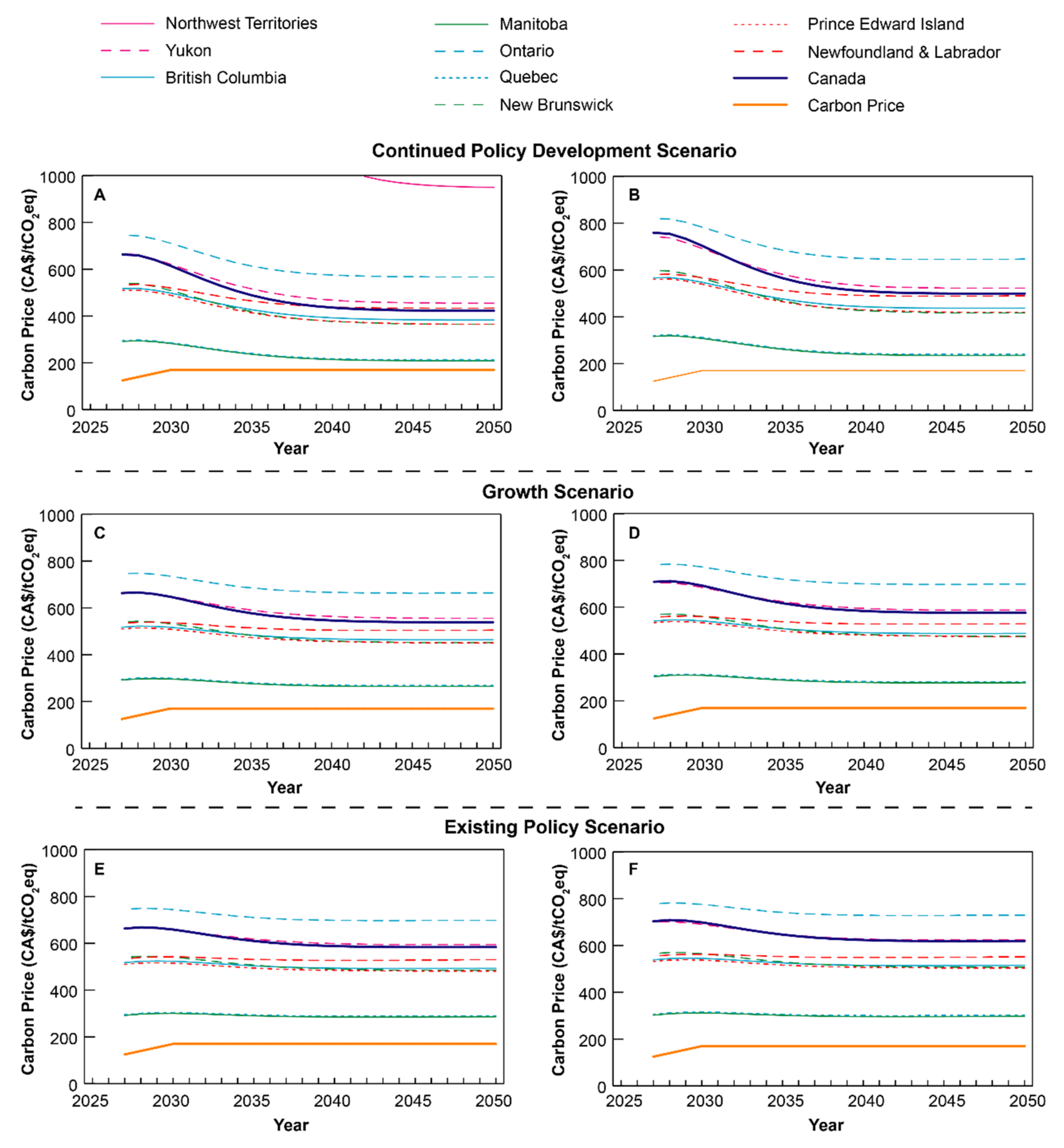

3.2. Adapting Policy Scenarios in Canada to CO2-Derived Diesel Demand

- (1)

- the consumption of diesel is sufficiently regulated to facilitate a one-to-one substitution of fossil fuel-derived diesel with diesel produced from the CO2-to-diesel process and;

- (2)

- no additional higher blending regulations are introduced and CO2-derived diesel competes equally with all sources of diesel. Here, diesel from the CO2-to-diesel process follows a one-to-one substitution with the diesel pool in the year it is substituted.

3.3. Projections for CO2-to-Diesel in Canada

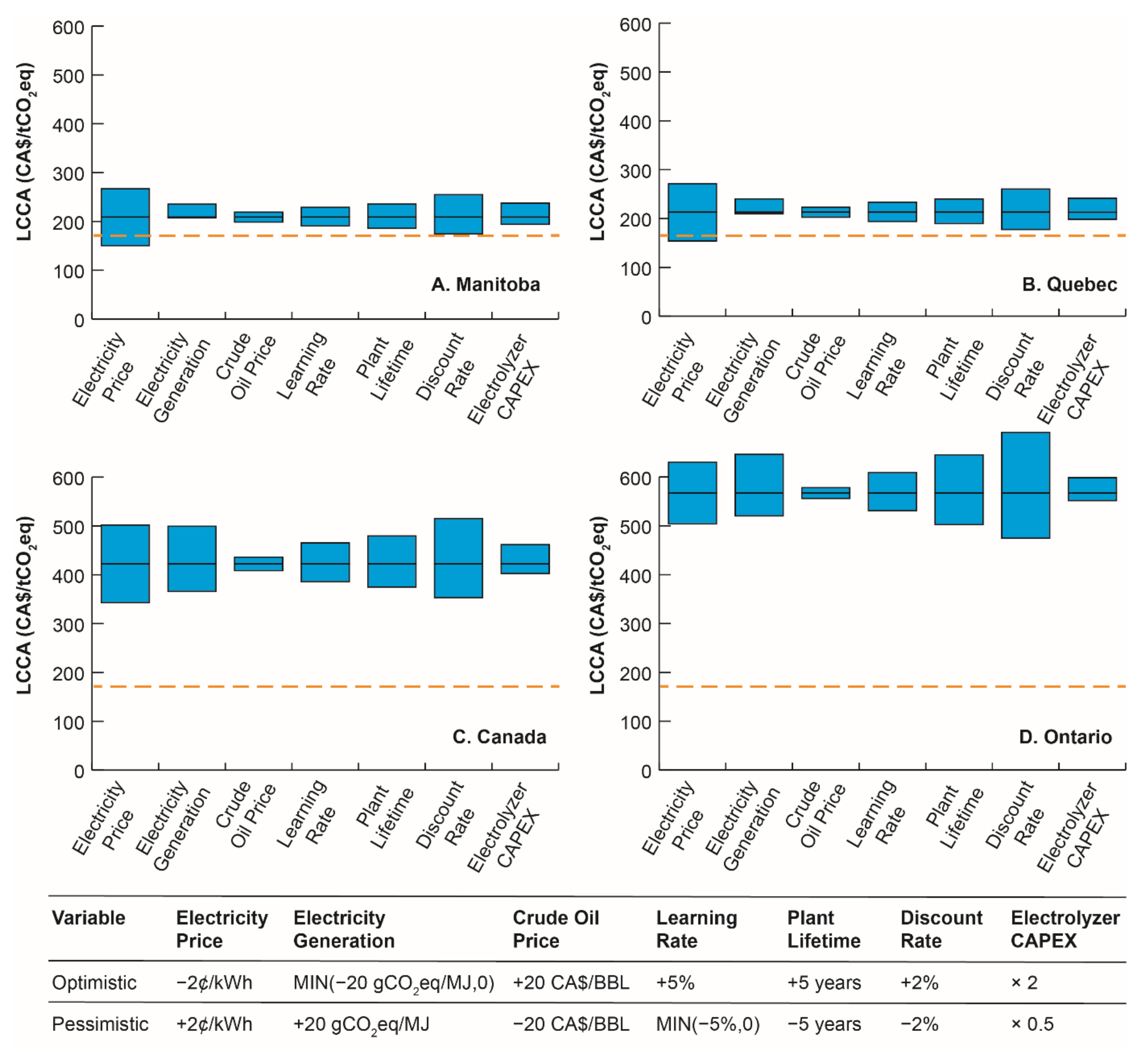

3.4. Sensitivity Analysis

4. Future Work

5. Conclusions and Policy Implications

5.1. Conclusions

5.2. Policy Implications

Supplementary Materials

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| LCCA | Levelized Cost of Carbon Abatement |

| TLC | Technology Learning Curve |

| TRL | Technology Readiness Level |

| MEA | Monoethanolamine |

| RWGS | Reverse Water Gas Shift |

| FT | Fischer Tropsch |

| HDRD | Hydrogenation-Derived Renewable Diesel |

References

- International Energy Agency (IEA). CO2 Emissions from Fuel Combustion Statistics. Available online: https://doi-org/10.1787/co2-data-en (accessed on 18 March 2021).

- International Energy Agency (IEA). CCUS in Clean Energy Transitions; IEA Publications: Paris, France, 2020. [Google Scholar]

- Grim, R.G.; Huang, Z.; Guarnieri, M.T.; Ferrell, J.R., III; Tao, L.; Schaidle, J.A. Transforming the Carbon Economy: Challenges and Opportunities in the Convergence of Low-Cost Electricity and Reductive CO2 Utilization. Energy Environ. Sci. 2020, 13, 472–494. [Google Scholar] [CrossRef]

- MacDowell, N.; Fennell, P.S.; Shah, N.; Maitland, G.C. The Role of CO2 Capture and Utilization in Mitigating Climate Change. Nat. Clim. Chang. 2017, 7, 243–249. [Google Scholar] [CrossRef] [Green Version]

- Hepburn, C.; Adlen, E.; Beddington, J.; Carter, E.A.; Fuss, S.; MacDowell, N.; Minx, J.C.; Smith, P.; Williams, C.K. The Technological and Economic Prospects for CO2 Utilization and Removal. Nature 2019, 575, 87–97. [Google Scholar] [CrossRef] [Green Version]

- Naims, H. Economics of Carbon Dioxide Capture and Utilization—A Supply and Demand Perspective. Environ. Sci. Pollut. Res. 2016, 23, 22226–22241. [Google Scholar] [CrossRef] [Green Version]

- Zimmermann, A.W.; Schomäcker, R. Assessing Early-Stage CO2 Utilization Technologies—Comparing Apples and Oranges? Energy Technol. 2017, 5, 850–860. [Google Scholar] [CrossRef] [Green Version]

- Roh, K.; Bardow, A.; Bongartz, D.; Burre, J.; Chung, W.; Deutz, S.; Han, D.; Heßelmann, M.; Kohlhaas, Y.; König, A.; et al. Early-stage Evaluation of Emerging CO2 Utilization Technologies at Low Technology Readiness Levels. Green Chem. 2020, 22, 3842–3859. [Google Scholar] [CrossRef]

- Otto, A.; Grube, T.; Schiebahn, S.; Stolten, D. Closing the Loop: Captured CO2 as a Feedstock in the Chemical Industry. Energy Environ. Sci. 2015, 8, 3283–3297. [Google Scholar] [CrossRef] [Green Version]

- Schakel, W.; Fernández-Dacosta, C.; Van Der Spek, M.; Ramírez, A. New Indicator for Comparing the Energy Performance of CO2 Utilization Concepts. J. CO2 Util. 2017, 22, 278–288. [Google Scholar] [CrossRef]

- Rubin, E.S. Improving Cost Estimates for Advanced Low-carbon Power Plants. Int. J. Greenh. Gas Control 2019, 88, 1–9. [Google Scholar] [CrossRef]

- Zimmermann, A.; Wunderlich, J.; Buchner, G.; Muller, L.; Armstrong, K.; Michailos, S.; Marxen, A.; Naims, H.; Mason, F.; Stokes, G.; et al. Techno-Economic Assessment & Life-Cycle Assessment Guidelines for CO2 Utilization; Global CO2 Initiative: Ann Arbor, MI, USA, 2018. [Google Scholar]

- Friedmann, S.J.; Fan, Z.; Byrum, Z.; Ochu, E.; Bhardwaj, A.; Sheerazi, H. Levelized Cost of Carbon Abatement: An Improved Cost-Assessment Methodology for a Net-Zero Emissions World; Columbia University Center on Global Energy Policy: New York, NY, USA, 2020. [Google Scholar]

- Global CCS Institute. Is the World Ready for Carbon Capture and Storage? Global CCS Institute: Melbourne, Australia, 2018. [Google Scholar]

- World Bank Group. GDP (Current US$). Available online: https://data.worldbank.org/indicator/NY.GDP.MKTP.CD (accessed on 11 March 2021).

- Environment and Climate Change Canada. National Inventory Report 1990-2018: Greenhouse Gas Sources and Sinks in Canada; Environment and Climate Change Canada: Ottawa, ON, Canada, 2020. [Google Scholar]

- Environment and Climate Change Canada. Progress Towards Canada’s Greenhouse Gas Emissions Reduction Target. Available online: https://www.canada.ca/en/environment-climate-change/services/environmental-indicators/progress-towards-canada-greenhouse-gas-emissions-reduction-target.html (accessed on 11 March 2021).

- Environment and Climate Change Canada. What Is the Clean Fuel Standard? Available online: https://www.canada.ca/en/environment-climate-change/services/managing-pollution/energy-production/fuel-regulations/clean-fuel-standard/about.html (accessed on 11 March 2021).

- International Carbon Action Partnership (ICAP). Canada Proposes Rising Carbon Price to 2030. Available online: https://icapcarbonaction.com/en/news-archive/736-canada-proposes-rising-carbon-price-to-2030 (accessed on 11 March 2021).

- Spurgeon, J.M.; Kumar, B. A Comparative Technoeconomic Analysis of Pathways for Commercial Electrochemical CO2 Reduction to Liquid Products. Energy Environ. Sci. 2018, 11, 1536–1551. [Google Scholar] [CrossRef]

- Dimitriou, I.; García-Gutiérrez, P.; Edler, R.J.; Cuéllar-Franca, R.M.; Azapagic, A.; Allen, R.W.K. Carbon Dioxide Utilisation for Production of Transport Fuels: Process and Economic Analysis. Energy Environ. Sci. 2015, 8, 1775–1789. [Google Scholar] [CrossRef] [Green Version]

- Canada Energy Regulator. Canada’s Energy Future 2020: Energy Supply and Demand Projections to 2050; Canada Energy Regulator: Ottawa, ON, Canada, 2020. [Google Scholar]

- Environment and Climate Change Canada. Clean Fuel Standard: Proposed Regulatory Approach. Available online: https://www.canada.ca/en/environment-climate-change/services/managing-pollution/energy-production/fuel-regulations/clean-fuel-standard/regulatory-approach.html (accessed on 11 March 2021).

- Zauner, A.; Böhm, H.; Rosenfeld, D.C.; Tichler, R. Innovative Large-scale Energy Storage Technologies and Power-to-Gas Concepts after Optimization: Report on Learning Curves and Economies of Scale. Available online: https://www.storeandgo.info/fileadmin/downloads/deliverables_2019/20190801-STOREandGO-D7.5-EIL-Report_on_experience_curves_and_economies_of_scale.pdf (accessed on 4 December 2020).

- Department of the Environment. Clean Fuel Regulations. Can. Gaz. Part I 2020, 154, 3761–4305. [Google Scholar]

- Global CCS Institute. The Global Status of CCS: 2019; Global CCS Institute: Melbourne, Australia, 2019. [Google Scholar]

- Lambert, N. Study of Hydrogenation Derived Renewable Diesel as a Renewable Fuel Option in North America. Available online: https://www.nrcan.gc.ca/sites/www.nrcan.gc.ca/files/oee/files/pdf/transportation/alternative-fuels/resources/pdf/HDRD_Final_Report_eng.pdf (accessed on 11 March 2021).

- Canada Energy Regulator. Canada’s Energy Future; Canada Energy Regulator: Ottawa, ON, Canada, 2020. [Google Scholar]

- Hansen, M.; Bhargava, A.; Nadew, M.; Stogran, M.; Hansen, L.; Hundal, M.; Budgell, P.; Safton, R. Analyzing Uncertainty in Projections of Canadian Energy Use and Production: Results and Insights from EMF 34 Scenarios. Energy Policy 2021, 148, 111915. [Google Scholar] [CrossRef]

- Davis, M.; Moronkeji, A.; Ahiduzzaman, M.; Kumar, A. Assessment of Renewable Energy Transition Pathways for a Fossil Fuel-Dependent Electricity-Producing Jurisdiction. Energy Sustain. Dev. 2020, 59, 243–261. [Google Scholar] [CrossRef]

- Bošković, B.; Leach, A. Leave It in the Ground? Oil Sands Development under Carbon Pricing. Can. J. Econ. 2020, 53, 526–562. [Google Scholar] [CrossRef]

- Institut de L’energie Trottier. Canadian Energy Outlook 2021—Horizon 2060; Institut de L’energie Trottier: Montreal, QC, Canada, 2021. [Google Scholar]

- Canada Energy Regulator. Canada’s Renewable Power Landscape 2017—Energy Market Analysis. Available online: https://www.cer-rec.gc.ca/en/data-analysis/energy-commodities/electricity/report/2017-canadian-renewable-power/canadas-renewable-power-landscape-2017-energy-market-analysis-ghg-emission.html (accessed on 11 March 2021).

- International Energy Agency (IEA). World Energy Balances. Available online: https://doi.org/10.1787/enestats-data-en (accessed on 18 March 2021).

- Thomassen, G.; Van Passel, S.; Dewulf, J. A Review on Learning Effects in Prospective Technology Assessment. Renew. Sust. 2020, 130, 109937. [Google Scholar] [CrossRef]

- Brynolf, S.; Taljegard, M.; Grahn, M.; Hansson, J. Electrofuels for the transport sector: A review of production costs. Renew. Sustain. Energy Rev. 2018, 81, 1887–1905. [Google Scholar] [CrossRef]

- National Energy Technology Laboratory. Technology Learning Curve (FOAK to NOAK). Available online: http://citeseerx.ist.psu.edu/viewdoc/download;jsessionid=2215E76B047081C1EF98E855F731153A?doi=10.1.1.385.8547&rep=rep1&type=pdf (accessed on 18 January 2021).

- Schoots, K.; Ferioli, F.; Kramer, G.J.; Van der Zwaan, B.C.C. Learning Curves for Hydrogen Production Technology: An Assessment of Observed Cost Reductions. Int. J. Hydrog. 2008, 33, 2630–2645. [Google Scholar] [CrossRef]

- Rubin, E.S.; Yeh, S.; Antes, M.; Berkenpas, M.; Davison, J. Use of Experience Curves to Estimate the Future Cost of Power Plants with CO2 Capture. Int. J. Greenh. Control 2007, 1, 188–197. [Google Scholar] [CrossRef] [Green Version]

- Environment and Climate Change Canada. Pan-Canadian Framework on Clean Growth and Climate Change: Canada’s Plan to Address Climate Change and Grow the Economy; Environment and Climate Change Canada: Ottawa, ON, Canada, 2016. [Google Scholar]

- USDA Foreign Agriculture Service. Canada: Biofuels Annual 2019. Available online: https://www.fas.usda.gov/data/canada-biofuels-annual-5 (accessed on 11 March 2021).

- Rogers, E.M. Diffusion of Innovations; Free Press: New York, NY, USA, 1995. [Google Scholar]

- Schmidt, O.; Hawkes, A.; Gambhir, A.; Staffell, I. The Future Cost of Electrical Energy Storage Based on Experience Rates. Nat. Energy 2017, 2, 1–8. [Google Scholar] [CrossRef]

- Competition Bureau Canada. A Guide to Retail Gasoline Pricing in Canada. Available online: https://www.competitionbureau.gc.ca/eic/site/cb-bc.nsf/eng/04429.html (accessed on 11 March 2021).

- Gebremariam, S.N.; Marchetti, J.M. Economics of Biodiesel Production. Energy Convers. Manag. 2018, 168, 74–84. [Google Scholar] [CrossRef]

- Ogunkunle, O.; Ahmed, N.A. A Review of Global Current Scenario of Biodiesel Adoption and Combustion in Vehicular Diesel Engines. Energy Rep. 2019, 5, 1560–1579. [Google Scholar] [CrossRef]

- Naylor, R.L.; Higgins, M.M. The Political Economy of Biodiesel in an Era of Low Oil Prices. Renew. Sust. Energy Rev. 2017, 77, 695–705. [Google Scholar] [CrossRef]

- De Luna, P.; Hahn, C.; Higgins, D.; Jaffer, S.A.; Jaramillo, T.F.; Sargent, E.H. What Would It Take for Renewably Powered Electrosynthesis to Displace Petrochemical Processes? Science 2019, 364, eaav3506. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Jouny, M.; Luc, W.; Jiao, F. General Techno-Economic Analysis of CO2 Electrolysis Systems. Ind. Eng. Chem. Res. 2018, 57, 2165–2177. [Google Scholar] [CrossRef]

- Van der Zwaan, B.; Keppo, I.; Johnsson, F. How to Decarbonize the Transport Sector? Energy Policy 2013, 61, 562–573. [Google Scholar] [CrossRef] [Green Version]

- de Blas, I.; Mediavilla, M.; Capellán-Pérez, I.; Duce, C. The Limits of Transport Decarbonization under the Current Growth Paradigm. Energy Strategy Rev. 2020, 32, 100543. [Google Scholar] [CrossRef]

- International Energy Agency (IEA). Net Zero by 2050: A Roadmap for the Global Energy Sector; IEA Publications: Paris, France, 2021. [Google Scholar]

- National Round Table on the Environment and the Economy. Achieving 2050: A Carbon Pricing Policy for Canada; National Round Table on the Environment and the Economy: Ottawa, ON, Canada, 2009. [Google Scholar]

- British Petroleum Company. Energy Outlook 2020 Edition; British Petroleum Company: London, UK, 2020. [Google Scholar]

- World Bank Group. State and Trends of Carbon Pricing 2020; World Bank Group: Washington, DC, USA, 2020. [Google Scholar]

- Rosenbloom, D.; Markard, J.; Geels, F.W.; Fuenfschilling, L. Opinion: Why Carbon Pricing is not Sufficient to Mitigate Climate Change—And How “Sustainability Transition Policy” Can Help. Proc. Natl. Acad. Sci. USA 2020, 117, 8664–8668. [Google Scholar] [CrossRef] [Green Version]

- Bataille, C.; Guivarch, C.; Hallegatte, S.; Rogelj, J.; Waisman, H. Carbon Prices Across Countries. Nat. Clim. Chang. 2018, 8, 648–650. [Google Scholar] [CrossRef] [Green Version]

- Beck, L. The US Section 45Q Tax Credit for Carbon Oxide Sequestration: An Update; Global CCS Institute: Melbourne, Australia, 2020. [Google Scholar]

- Wolinetz, M. Biofuels in Canada 2020: Tracking Biofuel Consumption, Feedstocks, Avoided Greenhouse Gas Emissions and Fuel Cost Impacts; Navius Research: Vancouver, BC, Canada, 2020. [Google Scholar]

- Ye, J. Canadian Provincial Renewable Energy Standards. Available online: https://www.c2es.org/document/canadian-provincial-renewable-energy-standards/ (accessed on 11 March 2021).

- Jordaan, S.M.; Romo-Rabago, E.; McLeary, R.; Reidy, L.; Nazari, J.; Herremans, I.M. The Role of Energy Technology Innovation in Reducing Greenhouse Gas Emissions: A Case Study of Canada. Renew. Sust. Energ. Rev. 2017, 78, 1397–1409. [Google Scholar] [CrossRef]

- International Energy Agency (IEA). World Energy Outlook 2020; IEA Publications: Paris, France, 2020. [Google Scholar]

- International Renewable Energy Agency (IRENA). Future of Solar Photovoltaic 2019: Deployment, Investment, Technology, Grid Integration, and Socio-economic Aspects (A Global Energy Transformation: Paper); IRENA: Abu Dhabi, United Arab Emirates, 2019. [Google Scholar]

- Wene, C.O. Energy Technology Learning Through Deployment in Competitive Markets. Eng. Econ. 2008, 53, 340–364. [Google Scholar] [CrossRef]

- Lohwasser, R.; Madlener, R. Relating R&D Investment Policies to CCS Market Diffusion through Two-Factor Learning. Energy Policy 2013, 52, 439–452. [Google Scholar]

- Weyant, J.P. Accelerating the Development and Diffusion of New Energy Technologies: Beyond the “Valley of Death”. Energy Econ. 2013, 33, 674–682. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

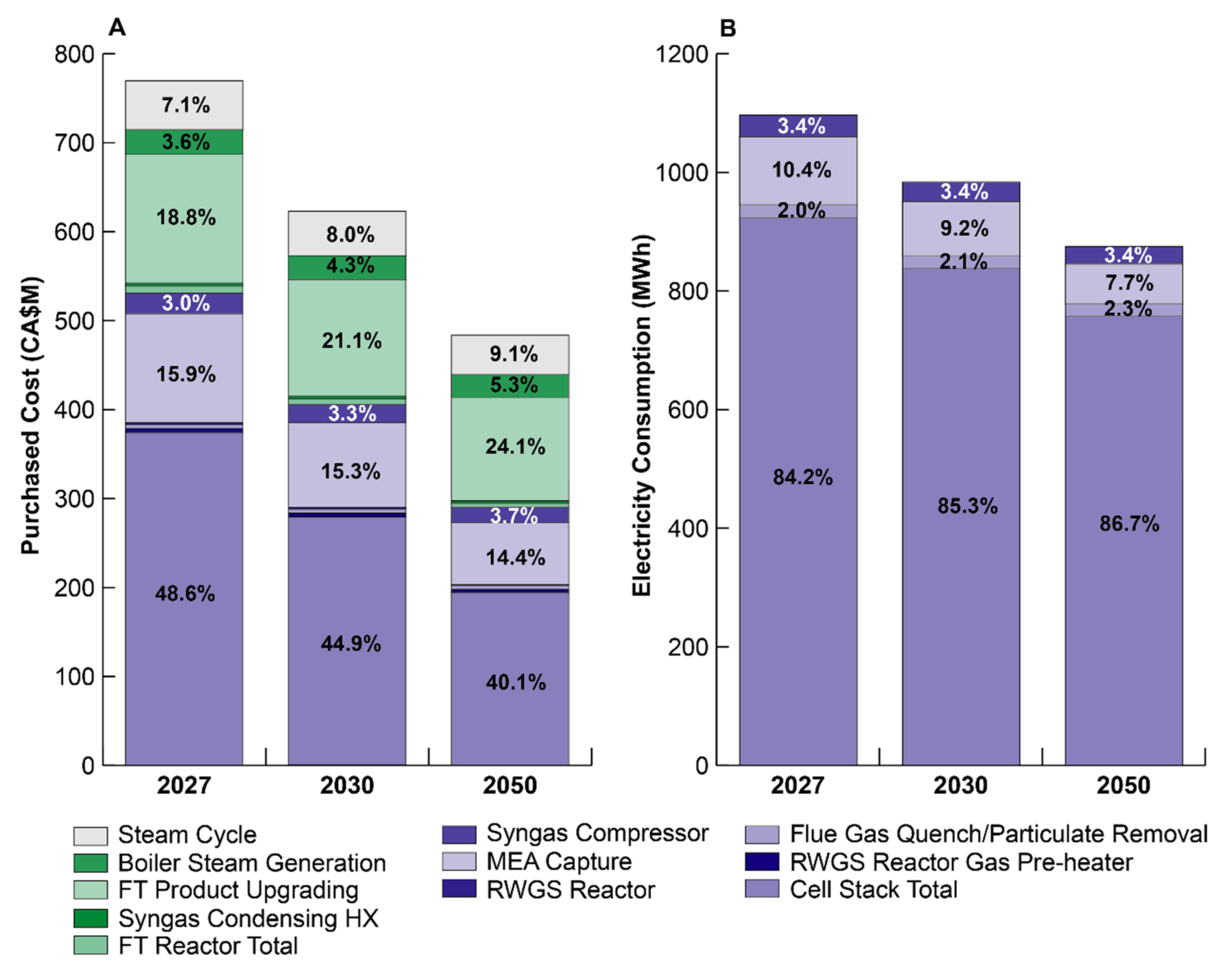

| Component | Capital Expense (CA$M) | Cost Share | Sub-Components | Learning Rate | Sources |

|---|---|---|---|---|---|

| PEM Electrolyzer | 374.06 | 48.6% | Yes | 12.9% | [24] |

| Gas Pre-Heater before RWGS reactor | 4.56 | 0.6% | 4% | [37] | |

| Flue Gas Quench and Particulate Removal | 4.71 | 0.6% | 2% | [37] | |

| RWGS Reactor | 2.19 | 0.3% | 11% | [24,38] | |

| MEA Capture | 112.20 | 15.9% | 11% | [39] | |

| Syngas Feed Compressor | 23.26 | 3.0% | 5% | [35] | |

| FT Reactor | 7.67 | 1.0% | Yes | 12.3% | [24] |

| Syngas Cooler Water Condensing Heat Excharger | 3.35 | 0.4% | 4% | [37] | |

| FT Product Upgrading | 144.57 | 18.8% | 4.0% | [35] | |

| Boiler Steam Generation | 27.82 | 3.6% | 1% | [37] | |

| Steam Cycle | 54.83 | 7.1% | 4% | [37] | |

| Overall | 769.43 | 100.0% | 9.5% |

| Component | Electricity (MW) | Electricity Share | Electricity Minimum (MW) | Learning Rate | Source(s) |

|---|---|---|---|---|---|

| PEM Electrolyzer | 923.5 | 84.2% | 572.6% | 12.9% | [24] |

| Flue Gas Quench and Particulate Removal | 21.9 | 2.0% | 2% | [37] | |

| MEA Capture | 114.2 | 10.4% | 11% | [39] | |

| Syngas Feed Compressor | 37.2 | 3.4% | 5% | [35] | |

| Total Consumption | 1096.8 | 100.0% | |||

| Net Generation | 10.9 | 1.0% | |||

| Net Total | 1085.9 | 99.0% |

| Product | 2026 (PJ) | 2030 (PJ) | 2050 (PJ) |

|---|---|---|---|

| Diesel Demand | 756.1 | 713.5 | 480.1 |

| Biodiesel | 13.2 | 19.3 | 21.4 |

| CO2-Derived Diesel under Existing Policy Scenario (Scenario 1) | 0.0 | 49.0 | 49.0 |

| CO2-Derived Diesel under Growth Scenario (Scenario 2) | 0.0 | 49.0 | 72.8 |

| CO2-Derived Diesel under Continued Policy Development Scenario (Scenario 3) | 0.0 | 49.0 | 294.0 |

| Region | LCCA | Levelized Diesel Price Above Canadian Average | ||

|---|---|---|---|---|

| 2027 (CA$/tCO2eq) | 2050 (CA$/tCO2eq) | 2027 (CA$/L) | 2050 (CA$/L) | |

| Carbon Price | 125.00 | 170.00 | 0.34 | 0.46 |

| Canada | 663.10 | 422.41 | 2.82 | 1.73 |

| Newfoundland & Labrador | 534.03 | 433.60 | 4.07 | 2.99 |

| Prince Edward Island | 509.90 | 364.72 | 3.17 | 1.82 |

| Nova Scotia | No Abatement | No Abatement | 4.53 | 3.06 |

| New Brunswick | 539.95 | 364.72 | 3.11 | 1.99 |

| Quebec | 295.45 | 212.67 | 1.62 | 0.69 |

| Ontario | 745.55 | 567.32 | 5.30 | 4.00 |

| Manitoba | 291.84 | 208.75 | 1.63 | 0.66 |

| Saskatchewan | No Abatement | 1576.49 | 2.11 | 1.11 |

| Alberta | No Abatement | No Abatement | 2.72 | 1.65 |

| British Columbia | 517.39 | 383.09 | 3.44 | 2.18 |

| Yukon | 666.67 | 454.96 | 3.88 | 2.64 |

| Northwest Territories | 5006.75 | 949.59 | 4.20 | 2.71 |

| Nunavut | No Abatement | No Abatement | 4.94 | 3.26 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ruttinger, A.W.; Kannangara, M.; Shadbahr, J.; De Luna, P.; Bensebaa, F. How CO2-to-Diesel Technology Could Help Reach Net-Zero Emissions Targets: A Canadian Case Study. Energies 2021, 14, 6957. https://doi.org/10.3390/en14216957

Ruttinger AW, Kannangara M, Shadbahr J, De Luna P, Bensebaa F. How CO2-to-Diesel Technology Could Help Reach Net-Zero Emissions Targets: A Canadian Case Study. Energies. 2021; 14(21):6957. https://doi.org/10.3390/en14216957

Chicago/Turabian StyleRuttinger, Andrew William, Miyuru Kannangara, Jalil Shadbahr, Phil De Luna, and Farid Bensebaa. 2021. "How CO2-to-Diesel Technology Could Help Reach Net-Zero Emissions Targets: A Canadian Case Study" Energies 14, no. 21: 6957. https://doi.org/10.3390/en14216957

APA StyleRuttinger, A. W., Kannangara, M., Shadbahr, J., De Luna, P., & Bensebaa, F. (2021). How CO2-to-Diesel Technology Could Help Reach Net-Zero Emissions Targets: A Canadian Case Study. Energies, 14(21), 6957. https://doi.org/10.3390/en14216957